Сontents. Introduction. Chapter 1. Economic and financial situation in the Republic of Belarus

|

|

|

- Lorraine Bell

- 6 years ago

- Views:

Transcription

1 APPROVED Edict of the President of the Republic of Belarus No. 182, dated May 25, 2017 REPORT of the National Bank of the Republic of Belarus for 2016 Minsk

2 2 Introduction Сontents Chapter 1. Economic and financial situation in the Republic of Belarus 1.1. Macroeconomic conditions of monetary policy implementation and banking sector development 1.2. The balance of payments and gross external debt 1.3. Financial sector Banking sector Institutional characteristics Structure of banks assets/liabilities Effectiveness and sustainability of the banking sector Financial market Foreign exchange market Interbank credit market Deposit and credit markets interest rates Government securities market National Bank s securities market Corporate securities market Bank management funds Leasing organizations Microfinance organizations Forex companies Chapter 2. National Bank s activities 2.1. Monetary policy Monetary policy target Exchange rate policy Interest rate policy and bank liquidity regulation Key monetary indicators 2.2. Supervision of banks activities Streamlining regulatory legal framework for banking supervision Off-site supervision Audits of banks 2.3. Regulation of banking operations Participation in the development of regulatory legal acts and banks local documents on credit and deposit markets Development of the system for non-cash settlements of retail payments Streamlining regulation of non-cash settlements

3 Formation of credit histories and provision of credit reports 2.4. Regulation of non-bank operations Regulation of leasing activities Regulation of microfinance organizations activities Regulation of operations involving over-the-counter financial instruments Monitoring the compliance with legislation on leasing activities, as well as the observance of legislation on providing and attracting microloans by microfinance institutions 2.5. Foreign exchange regulation and foreign exchange control 2.6. Financial stability monitoring 2.7. Accounting and reporting 2.8. Cash circulation 2.9. Payment system Information technologies Financial literacy Research activities International cooperation Staffing and staff training Internal audit Chapter 3. Financial statements Forms of annual financial statements of the National Bank for 2016 Notes to the annual financial statements of the National Bank for 2016 Conclusion Attachments Tables, figures, and schedules to Chapter Tables, figures, and schedules to Chapter 2

4 4 Introduction The Report of the National Bank for 2016 was prepared in accordance with Article 46 of the Banking Code of the Republic of Belarus (hereinafter the Banking Code ). In 2016, the monetary policy of the Republic of Belarus as part of the unified economic policy was implemented in line with the Monetary Policy Guidelines of the Republic of Belarus for 2016 approved by Edict of the President of the Republic of Belarus No. 505 dated December 18, 2015, having regard to the current macroeconomic situation. The National Bank s activities in 2016 were aimed at attaining the main monetary policy targets and performing the functions of the central bank assigned thereto by legislation of the Republic of Belarus.

5 5 Chapter 1 Economic and financial situation in the Republic of Belarus 1.1. Macroeconomic conditions of monetary policy implementation and banking sector development * Despite the fact that the economy of the Republic of Belarus was functioning under the unfavourable external economic conditions at the beginning of the year, the downturn in the economic activities in 2016, as a whole, was slowing down. Since 2016 H2, the key economic indicators have been improved and the rates of recession decreased. In the year under review, the volume of Gross Domestic Product (hereinafter GDP ) amounted to BYN94.3 billion, having decreased (in comparable prices) by 2.6% on the 2015 level (in 2015, by 3.8%). GDP energy intensity grew over 2016 by 1.2% (in 2015, went down by 4.9%) (Attachment 1.1). Retail turnover (in comparable prices) dropped in 2016 by 4.1% compared with 2015 (in 2015, by 1.3% on a year earlier). Households real wages dropped in 2016 by 4% compared with 2015 (in 2015, by 3.1%); real disposable money income went down by 7.3% (in 2015, by 5.9%). Investment in fixed capital decreased (in comparable prices) by 17.9% on a year earlier (in 2015, by 17.5%). The annual volume of investments in fixed capital totaled BYN18.1 billion; their share in GDP 19.2% (24.2% in 2015). In the technological structure of investment in fixed capital the expenditures for construction and installation works (52.9%) were dominating, while investments in assets (machinery, equipment, and vehicles) amounted to 35.1% and other works and costs 12% of the total volume of capital investments. Industrial output dropped in 2016 (in comparable prices) versus 2015 by 0.4% (in 2015, by 6.6%). Finished industrial stock at the enterprises warehouses amounted as at January 1, 2017 to BYN3.7 billion, having risen by 9.3% since the beginning of the year. With respect to the monthly average volume of production it amounted as at January 1, 2017 to 66.9% compared with 68.7% as at January 1, * This section was prepared based on the National Statistical Committee s data.

6 6 Agricultural output went up in 2016 (in comparable prices) by 3.4% compared with 2015 (in 2015, dropped by 2.5%). Transportation of cargo (excluding pipeline industry) dropped by 3.2% (in 2015, by 6.6%). Cargo turnover (excluding pipeline industry) went up by 1% (in 2015, declined by 8.8%). Passenger turnover went down in 2016 by 3.6% compared with 2015 (in 2015, by 4.2%). Financial situation of non-financial organizations in 2016 compared with 2015 (Attachment 1.2) was as follows: - revenues from the sale of products, goods, works, and services amounted in 2016 to BYN171.8 billion, having grown in nominal terms by 9% compared with 2015; and - profit from the sale of products totaled BYN12.6 billion, a 5.8% growth (in nominal terms) compared with At the same time, profit before tax went up by 38.9%; net profit by 54.8%. The real values of revenues from the sale of products went down, with an insignificant growth in proceeds from the sale of products, goods, works, services, as well as other profit indicators. Due to the outstripping growth of proceeds and cost of sold products over that of revenues from the sale of products the return on sales went down from 7.6% in 2015 to 7.3% in 2016; return on sold products from 9.4% to 9.2% respectively. According to the National Bank s calculations, in 2016 the share of lossmaking and low-return enterprises (in terms of return on sales) totaled 58.3%. In 2016, 1,434 organizations (19%) were in the red compared with 1,644 organizations (21.7%) in In 2016, the amount of net loss per one organization in the red in the republic on average totaled BYN1.8 million (in 2015, BYN2.5 million). Budgetary policy in 2016 remained well-balanced. In 2016, the Government ran a consolidated budget surplus of 1.3% of GDP (compared with 1.8% of GDP in 2015). In 2016, consolidated budget revenues grew by 7.1%, amounting to BYN28.5 billion (30.2% of GDP compared with 29.6% of GDP in 2015) (Attachment 1.3). Consolidated budget expenses amounted to BYN27.3 billion (29% of GDP versus 27.8% of GDP in 2015). According to the Ministry of Finance s data, in 2016 the republican budget ran a surplus as well in the amount of BYN1 billion, or 1.1% of GDP (in 2015, 1.7% of GDP). Republican budget revenues grew in 2016 compared with 2015 by 6.2% and totaled BYN17.8 billion (18.8% of GDP versus 18.6% of GDP in 2015). Republican budget expenses totaled BYN16.8 billion (17.8% of GDP compared with 16.9% of GDP in 2015).

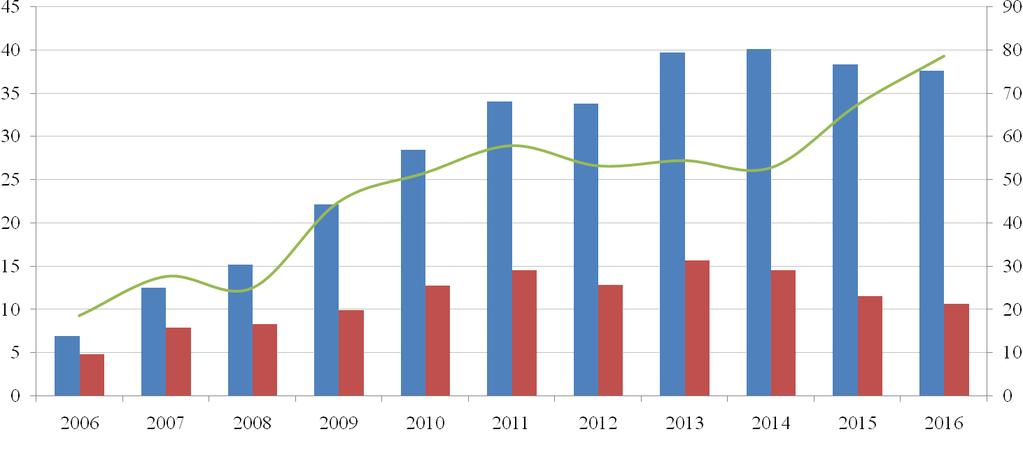

7 7 According to the Ministry of Finance s data, as at January 1, 2017, the Government debt of the Republic of Belarus amounted to BYN37 billion, growing by BYN4.1 billion (or by 12.5%) compared with early As at January 1, 2017, the Government domestic debt totaled BYN10.2 billion (10.9% of GDP), having grown over 2016 by BYN0.5 billion, or by 5% (adjusted for the currency translation differences). In 2016, domestic government bonds for legal and natural persons denominated in foreign exchange and in Belarusian rubles worth USD1,642.5 million and BYN543.7 million were placed. In the year under review, government bonds for legal and natural persons denominated in foreign exchange and in Belarusian rubles worth USD1,502.6 million and BYN599.5 million were retired. The Government external debt amounted as at January 1, 2017 to USD13.6 billion (28.5% of GDP), having increased over 2016 by USD1,198.8 million, adjusted for the currency translation differences, or by 9.6%. In 2016, the Government attracted external loans in the amount of USD1,934.9 million; repaid USD892,4 million The balance of payments and gross external debt In 2016, the balance of payments of the Republic of Belarus ran a surplus. The current account deficit reduced due to the improvement in the results of foreign trade in services and decline in payments under the investment income item. The deficit of the current account of the balance of payments totaled USD1.7 billion, or 3.6% of GDP, having dropped by USD0.1 billion compared with 2015 (Attachment 1.4). In 2016, the deficit of foreign trade in goods and services totaled USD27.3 million (in 2015, the surplus of foreign trade worth USD121.2 million was observed). According to the balance of payments, in 2016 the balance of foreign trade in goods was characterized by the deficit in the amount of USD2.6 billion (in 2015, USD2.1 billion). At that, the balance of foreign trade in energy goods worsened by USD1.1 billion due to the low global prices for oil and oil products and shortfall in delivery of oil from the Russian Federation, amounting to minus USD2.7 billion. The balance of foreign trade in non-energy goods totaled USD0.1 billion, compared with minus USD0.5 billion in In 2016, exports of goods dropped by 12.2%, or by USD3.2 billion, amounting to USD23 billion. Reduction in the delivery of oil and oil products, milk foods, fertilizers, and black metals made the major impact on the dynamics of exports.

8 8 Imports of goods dropped in 2016 by 9.7%, or by USD2.7 billion, amounting to USD25.6 billion. Declining investments in fixed capital accounted for the decrease in the investment imports by USD0.6 billion due to the decline in the households real income. The imports of intermediate goods dropped by USD1.6 billion, including that of energy goods by USD1.8 billion. In 2016, the turnover of foreign trade in services remained at the level of 2015, amounting to USD11.1 billion, with the exports of services growing by 2.7% and totaling USD6.8 billion. The imports of services dropped by 2.8%, amounting to USD4.2 billion. The surplus of foreign trade in services totaled USD2.6 billion (up by 13.3% compared with 2015) and compensated the deficit in the trade in goods. The balance of primary income improved by USD0.2 billion and stood at minus USD2.2 billion, that was caused by a decrease in income payments to foreign investors. The balance of secondary income totaled USD0.6 billion against USD0.5 billion in According to the financial account (excluding reserve assets), in 2016 net borrowing from other countries totaled USD1.3 billion versus USD0.7 billion in Attraction of financial resources to the Republic of Belarus at the expense of foreign direct investments amounted to USD1.2 billion (in 2015, USD1.5 billion). At the same time, the inflow of foreign direct investments (excluding reinvested incomes) was still insufficient USD0.5 billion compared with USD0.4 billion in The Government and the National Bank of the Republic of Belarus attracted on net basis USD0.8 billion, including at the expense of credits to the Government of the Republic of Belarus USD1 billion and due to placement of securities by the National Bank USD0.5 billion. In 2016, net borrowing of foreign investments by the banking sector totaled USD0.1 billion; by the other sectors USD0.4 billion. In 2016, the balance of payments ran a surplus of USD0.5 billion compared with a deficit of USD0.6 billion in As at January 1, 2017, gross external debt of the Republic of Belarus amounted to USD37.6 billion, or 78.6% of GDP, decreasing over 2016 by USD0.7 billion (Attachment 1.5). As at January 1, 2017, the external debt of the government agencies sector of the Republic of Belarus totaled USD14.2 billion, having grown since the beginning of the year by USD1.2 billion, or by 9.1%.

9 9 The National Bank s external debt dropped over 2016 by USD0.3 billion, or by 15.4%, amounting as at January 1, 2017 to USD1.5 billion. Long-term borrowings accounted for the major part (94.5%) of the debt. The banking sector s liabilities (excluding intercompany financing) went down over 2016 by USD0.5 billion, or by 8.2%, amounting to USD5.9 billion as at January 1, At that, repayment of the long-term debt worth USD0.4 billion was accompanied by reduction in the short-term liabilities by USD0.1 billion. External debt of the other sectors (excluding intercompany financing) went down over 2016 by USD1.2 billion, amounting to USD14.1 billion as at January 1, At that, a decline in both the long-term liabilities (by USD1 billion, or by 14.4%) and short-term liabilities (by USD0.3 billion, or by 3.1%) was observed. Over the recent years, a stable trend towards switching from the shortterm to the long-term borrowing has been observed in the Republic of Belarus. As at January 1, 2017, long-term borrowings accounted for 71.7% of the total volume of borrowings Financial sector Banking sector Institutional characteristics As at January 1, 2017, the banking activities in the Republic of Belarus were carried out by 24 banks and three non-bank financial institutions. Five banks underwent liquidation (JSC Delta Bank, InterPayBank JSC, CJSC BIT-Bank, JSC Eurobank, and CJSC N.E.B. Bank ). The total number of banks organizational units (branches, banking services centers, settlement and cash centers, and exchange offices) in the territory of the country dropped over 2016 by 12.7%, amounting as at January 1, 2017 to 3,682. As at January 1, 2017, there were five representative offices of foreign banks in the Republic of Belarus, including those of the Russian Federation (representative offices of two banks), Latvia, and Germany, as well as a representative office of the Interstate Bank. Belarusian Banks had nine representative offices abroad. Foreign capital participated in the authorized capital of 19 banks. In 14 banks the share of foreign investors in the authorized capital exceeded 50% (of which four banks were wholly-foreign owned). Capital from Russia, Austria, Iran, Switzerland, Cyprus, Poland, Kazakhstan, United Arab Emirates,

10 10 Lebanon, Georgia, the USA, Great Britain, Germany, and other countries participates in the authorized capital of Belarusian banks. As at January 1, 2017, the banks aggregate registered authorized capital amounted to BYN4.7 billion, having increased over 2016 by 5.2%. Institutional development of banks in 2016 was characterized by: - the decreased share of banks controlled by the Government in the banking sector s aggregate authorized capital from 82% to 80.2%, with their share in the banking sector s regulatory capital declining from 63.7% to 61.4% and the share in the banking sector s assets growing from 65.4% to 66.8%; - the increased share of foreign banks * in the banking sector s aggregate authorized capital from 15.3% to 17.1%. The share of such banks in the aggregate authorized capital went up from 32.9% to 35%. In the banking sector s assets the share of such banks dropped from 32.5% to 30.7%; and - the remaining share of banks of private form of ownership in the aggregate authorized capital of the banking sector at the level of 2.7%, with the share of these banks in the banks assets growing by 0.5 percentage point and amounting to 2.6% and in the aggregate regulatory capital from 3.5% to 3.6% Structure of banks assets/liabilities In 2016, banks assets (liabilities) grew by BYN1,420.7 million, or by 2.3%, amounting as at January 1, 2017 to BYN64,467 million (Attachments ). As at January 1, 2017, assets (liabilities)/gdp ratio totaled 68.3% (as at January 1, 2016, 70.1%). As at January 1, 2017, the share of banks claims on the economy in the banks assets amounted to 62.5% (as at January 1, 2016, 66%). The share of the long-term credits in the total debt under credits amounted as at January 1, 2017 to 74.8%, having increased over 2016 by 1.7 percentage points. Banks claims on the economy ** went down over 2016 by BYN1,355.7 million, or by 3.3% (in 2015, grew by 20%), amounting as at January 1, 2017 to BYN40,276.5 million. Banks claims on the economy in the national currency dropped by BYN519.7 million, or by 3% (went up by 5.5% in 2015), in foreign exchange (in dollar terms) by USD1,099.5 million, or by 8.5% (in 2015, by 14.9%). In 2016, banks claims on the economy (at the exchange rate of the Belarusian ruble versus the US dollar as at January 1, 2016) dropped by 2016 by 2.8%. * Foreign banks are banks in which the share of foreign investors in the authorized capital exceeds 50%. ** Claims of banks and JSC Development Bank of the Republic of Belarus on the economy dropped over

11 11 BYN2,561.4 million, or by 6.2%, amounting as at January 1, 2017 to BYN39,070.8 million. Implementation of the bad assets repayment schemes, provided for by Edict of the President of the Republic of Belarus No. 320 On Developing Agricultural Production in the Vitebsk Region dated August 25, 2016, Edict of the President of the Republic of Belarus No. 496 On the Measures on Financial Sanation of the Legal Persons Participants of the Holding Company Myasomolprom ; and Resolution of the Council of Ministers and the National Bank of the Republic of Belarus No. 923/28 On Measures Designed to Implement Edict of the President of the Republic of Belarus No. 268 dated July 14, 2016 dated November 15, 2016 made a significant impact on the decline of the banks claims on the economy. As at January 1, 2017, the share of debt under credits granted by banks and JSC Development Bank of the Republic of Belarus within government programs and measures in line with decisions of the President and the Council of Ministers of the Republic of Belarus totaled BYN17, million as at January 1, 2017, having dropped since the beginning of the year by BYN million, or by 3.4%, including debt under credits granted by banks BYN14, million (a drop by BYN, million, or by 7.3%), under credits granted by JSC Development Bank of the Republic of Belarus BYN3, million (an increase by BYN503.1 million, or by 16.6%). As at January 1, 2017, the share of debt under credits granted by banks within government programs and measures totaled 35.3%, having dropped in 2016 by 1.6 percentage point. In 2016, banks granted credits worth BYN502.1 million, including soft credits worth BYN473.8 million and on banks terms BYN28.3 million, for house construction within implementation of Resolution of the Council of Ministers of the Republic of Belarus No On the Measures Designed to Execute Tasks for 2016 on Housing Construction, Volumes of Putting into Operation and Financing Housing Construction and Objects of Engineering and Transport Infrastructure in 2017 dated December 29, 2015, including soft credits worth BYN473.8 million, and on banks terms BYN28.3 million. Soft credits were granted at the expense of funds of the Ministry of Finance in the amount of BYN299.9 million, and at the expense of bank s reimbursable resources BYN147.6 million. Funds attracted from residents of the Republic of Belarus dominated the banks liabilities (in %; in %). As at January 1, 2017, the share of the natural persons funds totaled 32.2% (as at January 1, %); economic entities funds 19.5% (as at January 1, %). In 2016, funds attracted from natural persons (including bank deposits, bank deposits in precious metals and stones, saving certificates and bonds) rose

12 12 by BYN387.4 million, or by 1.9%, amounting as at January 1, 2017 to BYN20,750.5 million. Foreign exchange component dominated the structure of funds attracted from the natural persons. In 2016, the share of funds attracted from households in foreign exchange in the total volume of attracted funds dropped from 80.1% to 78.1%. The share of funds attracted from households in the national currency went up from 19.9% to 21.9%. In 2016, funds attracted in foreign exchange went down by BYN105.1 million, or by 0.6%, amounting as at January 1, 2017 to BYN16,208.9 million. Funds attracted in the national currency grew by BYN492.5 million, or by 12.2%, amounting as at January 1, 2017 to BYN4,541.6 million. Bonds were the most popular banking products with households for placement of temporary free funds. They grew over the year under review by BYN583.8 million, or by 58.2%, amounting as at January 1, 2017 to BYN1,586.5 million (7.7% of the total volume of attracted natural persons funds). Natural persons bank deposits * in the national currency grew over 2016 by BYN499.6 million, or by 12.4%, amounting as at January 1, 2017 to BYN4,520.1 million, of which bank time deposits and deposits in escrow went up by BYN336,2 million, or by 12.9%, amounting to BYN2,950.7 million. Natural persons deposits in foreign exchange (in ruble terms) dropped over 2016 by BYN697.4 million, or by 4.6%, amounting as at January 1, 2017 to BYN14,552.9 million. Time deposits and deposits in escrow dropped by BYN574.9 million, or by 4%, amounting to BYN13,707.4 million as at January 1, Natural persons deposits in foreign exchange (in dollar terms) decreased over 2016 by USD782.1 million, or by 9.5%, amounting as at January 1, 2017 to USD7,430.7 billion. At that, time deposits and deposits in escrow dropped by USD692.6 million, or by 9%, amounting as at January 1, 2017 to USD6,998.9 million. The bulk of bank deposits was placed with JSC JSSB Belarusbank, JSC Belagroprombank, Belinvestbank JSC, Priorbank JSC, BPS-Sberbank, and Bank BelVEB OJSC, the share of which in the natural persons deposit market amounted as at January 1, 2017 to 85.2% of the total volume of deposits with banks, or BYN16,239.8 million. As at January 1, 2017, the savings deposited with banks averaged BYN2,182.4 per citizen of the Republic of Belarus, compared with BYN2,144.8 as at January 1, This indicator decreased in dollar terms from USD1,155.1 to USD1,114.3 or by 3.5%. * Here and hereinafter in subparagraph the information on the natural persons bank deposits is given based on the methodology of calculation of broad money supply.

13 13 In 2016, legal persons bank deposits * grew by BYN520.5 million, or by 5.2%, amounting to BYN10,618.5 million as at January 1, Legal persons bank deposits in the national currency grew over 2016 by BYN859.5 million, or by 24.8%, amounting as at January 1, 2017 to BYN4,329 million. Legal persons deposits in foreign exchange (in ruble terms) dropped over 2016 by BYN339 million, or by 5.1%, amounting as at January 1, 2017 to BYN6,289.5 million. Legal persons deposits in foreign exchange (in dollar terms) dropped over 2016 by USD358.3 million, or by 10%, amounting as at January 1, 2017 to USD3,211.4 million. Legal persons time deposits and deposits in escrow in the national currency and foreign exchange (in ruble terms) amounted as at January 1, 2017 to BYN6,224.9 million, or 58.6% of the legal persons total deposits Effectiveness and sustainability of the banking sector In 2016, the National Bank took measures aimed at ensuring stability of the banking sector and improving efficiency of its functioning and interaction with the real sector of the economy. As at January 1, 2017, banks regulatory capital totaled BYN8.7 billion, having increased over 2016 by 11.4% in nominal terms. In 2016, the main sources of the regulatory capital growth in the banking sector as a whole were: increase in the registered authorized capital, growth in funds established at the expense of banks profit, and provision of resources to owners in the form of subsidized credits (loans). As at January 1, 2017, the regulatory capital/gdp ratio was 9.3%. In 2016, the banking sector s income had the following structure: interest income 75.3%, commission income 13.4%, other banking income 9.2%, other operational income 2%, and receipts under written-off debts 0.1%. In the structure of expenditures * the interest expenses totaled 45.8%, other operational expenditures 24.5%, other banking expenditures 6.3%, and commission expenses 4.5%. Net allocations to reserves in 2016 totaled 17%. Profit obtained by banks in 2016 totaled BYN884.9 million (in 2015 BYN585.9 million). Increase in net interest income due to decline in interest expenses was the key factor of profit increase. The profit obtained by banks made it possible for them to preserve capital and insure sustainability to potential shocks. * Here and hereinafter in subparagraph the information on the legal persons bank deposits is given based on the methodology of calculation of broad money supply. * The amount of expenses for allocations to reserves is given less the amount of expenses from reduction of reserves.

14 14 At the end of 2016, the banking sector s return on assets was 1.3% (1% in 2015) and return on regulatory capital 10.8% (in 2015, 8.4%). Credit risk remained the most significant one for the banking sector. As at January 1, 2017, bad assets of the functioning banks (assets classified under risk Groups III, IV, and V) totaled BYN5.1 billion. Assets classified under Group III grew over the year by 75.8%, amounting as at January 1, 2017 to BYN3.5 billion (68.4% of the total volume of bad assets), assets classified under Group IV 62.1% (16.9%), and assets classified under Group V 227.6% (14.7%). The share of bad assets in the assets exposed to credit risk grew over 2016 from 6.8% to 12.8%. Worsening of the financial indicators of the real sector enterprises activities (primarily, the state-owned ones) on the background of continuing decline in economic activity, as well as their high debt load, was the key reason of the credit risk potential growth. With a view to ensuring stable functioning and preventing creation of conditions threatening depositors and other creditors, the banks incurred considerable expenses when establishing special provisions to cover possible losses under assets exposed to credit risk and transactions which are not reported on the balance sheet. Over 2016, net allocations to reserves totaled BYN1.4 billion. In 2016, the most authoritative international audit companies carried out special audits in 9 core banks, which made it possible to assess the level of credit risk accepted by banks and the possibility of its compensation at the expense of available capital. The quality of assets of remaining banks will be assessed in the course of the annual audit of accounting (financial) statements for With a view to leveling out the situation, the Government and the National Bank of the Republic of Belarus took a number of measures designed to reduce the bad debt, including by means of transferring a part of bad assets to the JSC Asset Management Agency, and implementing the Edicts of the President of the Republic of Belarus on the restructuring of the agricultural enterprises debt. As a result, the share of bad assets in the assets exposed to credit risk dropped from the maximum value of 14.9% as at November 1, 2016 to 12.8% as at January 1, Despite the worsening of situation in the real sector of the economy, in 2016, banks met the major secure functioning requirements: - adequacy of banks regulatory capital (the ratio of the regulatory capital and risks assumed by banks) 18.6% (the prescribed minimum prudential requirement for an individual bank being 10%); - ratio of liquid assets to total assets 30.8% (the prescribed requirement being at least 20%); - short-term liquidity (the ratio of actual liquidity to required

15 15 liquidity) 2.1% (the requirement being at least 1); - instant liquidity (the ratio of assets on demand to liabilities on demand) 142.3% (the requirement being at least 20%); and - current liquidity (the ratio of current assets to current liabilities) 131.8% (the requirement being at least 70%). Thus, the banking sector s stability as at year-end 2016 was characterized as adequate Financial market Foreign exchange market In 2016, domestic foreign exchange market volume totaled USD70.1 billion, by 5.9% below the level of The stock market volume amounted to USD9.3 billion, having dropped by 46.2%; the over-the-counter market volume stood at USD49.7 billion, having grown over 2016 by 15.3%. Lifting of the previously imposed restrictions on carrying out foreign exchange transactions in the over-the-counter market, as well as lowering for the Belarusian exporting organizations, since September 1, 2016, of the amount of the obligatory sale of foreign exchange from 30% to 20% of the amount of receipts in foreign exchange, were conducive to reallocation of the volume of foreign exchange transactions in favour of the over-the-counter segment. Cash market turnover stood at USD11.1 billion, having decreased over 2016 by 10%. In the year under review, resident economic entities: - sold foreign exchange in the amount of USD16.1 billion, a drop by 10.1% (by USD1.8 billion) compared with 2015; and - purchased foreign exchange in the amount of USD16.3 billion, a decline by 11% (by USD2 billion) compared with 2015 (Attachment 1.10). In 2016, foreign exchange purchased by resident economic entities in the domestic foreign exchange market was, mainly, used to repay credits (USD6.1 billion or 37.3% of the total volume purchased over the year), procure raw products and materials (USD2.3 billion or 14.3%), purchase equipment and components (USD1.7 billion or 10.7%), and foods and agricultural products (USD1.2 billion or 7.2%). A total of 69.5% of the foreign exchange purchased by resident economic entities was used for the above-mentioned purposes. As a result, net demand for foreign exchange by resident economic entities in 2016 stood at USD0.2 billion (in 2015, USD0.4 billion). At that, the bulk of sales felt on January and December 2016 (USD0.5 billion), while in February - November 2016 net sale of foreign exchange totaled USD0.2 billion. In January 2016, households were net buyers of foreign exchange (USD0.2 billion); in February - December 2016 net sellers (USD2.1 billion).

16 16 Households sold over 2016 USD1.9 billion on a net basis (in 2015, USD0.1 billion). At that, net supply under operations involving foreign exchange in cash totaled USD2.4 billion; net demand under operations involving non-cash foreign exchange amounted to USD0.6 billion (Attachment 1.11). The operations involving the US dollars dominated the Belarusian foreign exchange market (56.9%). The share of this currency in foreign exchange operations fell by 3.7 percentage points compared with 2015, with the shares of euro increasing from 22.8% to 23.9% and the Russian ruble from 16.3% to 18.8%. The volume of operations involving other foreign currencies remained insignificant (less than 1%) Interbank credit market In 2016, interbank credits in the national currency continued to be one of the main instruments regulating banks liquidity. Resident banks of the Republic of Belarus and non-resident banks were involved in the activities in this segment of the money market. In the year under review the interbank credit market was characterized by a transfer from the structural deficit to the structural surplus of liquidity. The volume of operations carried out by banks in the interbank market was lower in 2016 than in 2015 totaling BYN23 billion (in 2015, BYN28 billion), that was due to the structural surplus of ruble liquidity formed in April 2016, which had been accruing till the year-end. The structure of the interbank market changed compared with 2015 as to reduction in the terms of lending. Intraday interbank credits accounted in 2015 for 66%, while in 2016 such credits totaled 73% of the aggregate market. At that, the share of transactions concluded for the term of 2-7 days dropped to 26% of the total market volume (in 2015, 32%). At the same time, the banks continued in 2016 to attract/place resources in the national currency in the interbank market through repo transactions. In the year under review, the share of such operations in the total volume of the interbank market averaged 29% of the balance of amounts owed (in 2015, 40%). The interest rates in the intraday ruble interbank market had been, mainly, within the interest rate band formed by the standing facilities designed to regulate banks liquidity (Attachment 1.12). The average weighted interest rate in the intraday interbank market dropped from 29.4% per annum in January 2016 to 10.5% per annum in December Deposit and credit markets interest rates

17 17 The situation with liquidity in the banking sector, as well as the foreign exchange and money markets, determined the dynamics of interest rates in the deposit and credit markets in 2016 (Attachment 1.13). At that, the fundamental principles of the interest rate policy ensuring of the excess of the return on savings in the national currency over the return on savings in foreign exchange were preserved, as well as ensuring of positive interest rates in the economy in real terms. The National Bank focused special attention on the improvement of the structure and well-balancing of the deposit market by means of increasing the share of long-term deposits in the national currency and expansion of the yield-gap on long-term and short-term deposits. Implementation of the measures taken in 2016 resulted in a more significant decline (compared to the forecasted one) in the level of interest rates on fresh credits and fresh natural and legal persons deposits, which had been gradually declining over the whole period. Interest rates on the natural persons fresh time bank deposits in the national currency reached maximum in March 2016, amounting to 25.5% per annum. In December 2016 they declined up to 14.3% per annum (a drop since December 2015 by 10.3 percentage points). Interest rates on the natural persons fresh time bank deposits in foreign exchange totaled 2.3% in December 2016, a drop by 1.5 percentage points compared with December Interest rates on the legal persons fresh time bank deposits in the national currency reached maximum in February 2016 and averaged 26.8% per annum, having decreased in December 2016 to 8.6% per annum (a drop since December 2015 by 15.9 percentage points). Interest rates on the legal persons fresh time bank deposits in foreign exchange averaged 2.5% per annum in December 2016, having dropped by 2.3 percentage points compared with December At that, in December 2016, the return on fresh long-term irrevocable bank deposits in the national currency exceeded the return on the fresh short-term irrevocable bank deposits by 7.3 percentage points (the short-term interest rates averaged 12.5% per annum; the long-term interest rates averaged 19.8% per annum), in January 2016 by 4.7 percentage points (the short-term interest rates averaged 24.3% per annum; the long-term interest rates averaged 29% per annum). The interest rate on aggregate bank credits in the national currency amounted to 12% per annum in December 2016, having dropped by 5.3 percentage points versus December The interest rate on fresh bank credits * to legal persons in the national currency amounted to 20.8% per annum in December 2016, having dropped by 13.5 percentage points versus December * Excluding soft credits granted pursuant to decisions of the President and the Government of the Republic of Belarus at the expense of the republican and local government agencies.

18 18 The interest rates on fresh bank credits * in foreign exchange issued to legal persons averaged 8.3% per annum in December 2016, having dropped by 1.7 percentage points compared with December Government securities market According to the data of the Ministry of Finance, the volume of government securities placed in the domestic market grew over 2016 by BYN489.8 million, or by 5%, totaling BYN10,234.2 million as at January 1, 2017, including: - government long-term bonds denominated in the national currency BYN1,594.2 million (15.6%); - government long-term bonds denominated in foreign exchange BYN8,639.3 million (84.4%); and - other government securities BYN0.7 million (0.01%). As at January 1, 2017, government long-term bonds accounted for 100% of the government securities portfolio. In the structure of government securities, bonds with variable yield accounted for 34.5% and bonds with fixed interest yield 65.5% (as at January 1, 2016, the share of government bonds with variable yield totaled 42.9%, with fixed yield 57.1%). In 2016, the volume of primary trade in government bonds in the organized market totaled BYN1,089.9 million, a 4.2 times increase versus 2015; the number of deals totaled 1,433 (in 2015, the volume of trade amounted to BYN257.3 million; number of deals 866). The volume of secondary trade in government bonds totaled BYN4,851.1 million, a 1.2 times drop versus 2015; the number of deals totaled 952 (in 2015, the volume of trade amounted to BYN5,646.2 million; number of deals 489) National Bank s securities market In 2016, the National Bank placed bonds denominated in Belarusian rubles worth BYN28,712.4 million at placement value, or worth BYN28,850.5 million at face value, with BYN27,033.8 being repaid at face value. As at January 1, 2017, the volume of the circulating National Bank s bonds denominated in Belarusian rubles totaled BYN1,816.7 million at face value. As at January 1, 2016, the National Bank s bonds denominated in Belarusian rubles were not circulating. In 2016, the National Bank also placed bonds denominated in hard currency: - in the US dollars worth USD2,330.3 million at actual value, or worth USD2,327.7 million at face value, with USD2,130.8 million being repaid at face value. As at January 1, 2017, the volume of circulating bonds

19 19 denominated in the USD dollars totaled USD1,701.3 million, exceeding by 13.1% the level of January 1, 2016 (USD1,504.3 million); and - in euro worth EUR1,022.2 million at placement value, or worth EUR1,021.4 million at face value, with EUR680.7 million being repaid at face value. As at January 1, 2017, the volume of circulating bonds denominated in euro totaled EUR779.9 million, exceeding by 77.5% the level of January 1, 2016 (EUR439.3 million). The volume of banks investments in debt and equity instruments of the securities market totaled BYN16,217.5 million *, of which the National Bank s securities accounted for BYN5,556.6 million, or 34.3%, including bonds denominated in hard currency worth BYN3,749.5 million, or 67.5%. In 2016, 474 deals worth BYN974.7 million were entered into with the National Bank s bonds in the secondary stock market on the floor of the JSC Belarusian Currency and Stock Exchange, an increase by BYN811.9 million (five times) versus 2015 (16 deals worth BYN162.8 million). The share of repo deals in the total volume of the secondary stock exchange market of the National Bank s bonds totaled 21.6%, or 248 deals worth BYN210.1 million. 439 transactions worth million in equivalent were carried out with the National Bank s bonds denominated in the hard currency, an increase by BYN799.5 million (12 deals worth BYN142.3 million) compared with transactions worth 32.9 million were carried out with the National Bank s bonds denominated in Belarusian rubles, an increase by BYN12.4 million (4 deals worth BYN20.5 million) compared with In 2016, the volume of registered purchase/sale deals involving transactions with the National Bank s bonds denominated in hard currency totaled BYN160.1 million in equivalent in the over-the-counter market (in 2015, no deals involving these bonds were registered). ** Corporate securities market In 2016, the share of the corporate segment of the securities market continued to reduce. The volume of issue of shares and corporate securities dropped almost twice, amounting to BYN4,965.4 (in 2015, BYN8,283.3 million). The share of this segment in the total volume of the shares and bonds issue in 2016 reached 50.1% (in 2015, 59.5%) (Attachment 1.14). The share of the corporate bonds market dropped from 32.7% to 20.4%. Reduction of the corporate segment of the market was caused by an increase in the share of the government segment (the share of issue of government securities and local executive and administrative authorities bonds * According to the data of banks balance-sheets, excluding the incomes planned to be received in the form of interest. ** Deals involving the National Bank s bonds denominated in the national currency are allowed on the floor of the JSC Belarusian Currency and Stock Exchange only.

20 20 and the National Bank s bonds), that caused reduction in resources available for borrowing by the corporate issuers under the limited volume of the market. In 2016, the volume of the issues of shares registered in the Government Securities Register totaled BYN2,939.3 million, dropping by 21.3% compared with 2015 (BYN3,733.6 million). As at January 1, 2017, the volume of listed issues of the operating issuers shares amounted to BYN29,168 million, increasing by 11.2% compared with January 1, 2016 (BYN26,228.7 million), with the ratio of the volume of shares in circulation to GDP totaling 30.9% (as at January 1, 2016, 29.2%). In the reporting period, 133 issues of corporate bonds of 60 issuers worth BYN2,026.1, including the banks bonds worth BYN520.3 million, were registered. This volume of issue is lower than in 2015 (BYN4,549.7 million). The volume of bonds issued by banks in 2016 went down 4 times versus 2015 (BYN2,232.3 million). The share of banks bonds in the total volume of issued corporate bonds continued to reduce from 49.1% in 2015 to 25.7% in In 2016, the share of corporate bonds issued in foreign exchange totaled 65.8% of the total volume of issue (in 2015, 58%). Thus, as at the beginning of 2017, 554 issues of corporate bonds of 221 issuers worth BYN13,072.1 million, or 13.9% of GDP, were in circulation (as at January 1, 2016, BYN12,712.9 million, or 14.1% of GDP). As a result, the volume of corporate bonds in circulation grew over the year by 2.8%. The volume of corporate bonds issued in foreign exchange amounted as at January 1, 2017 to 50.1% of the total volume of corporate bonds in circulation (as at January 1, 2016, 43.6%). The expanding share of corporate bonds denominated in foreign exchange points to the continuing trend of growing foreign exchange risk and the degree of the securities market vulnerability, due to the fact that the risks related to the currencies conversion in the course of the securities repayment and payment of income increased. The stock market of the derivatives, which are one of the instruments of foreign exchange risk management, is represented by non-deliverable future contracts for the exchange rate of the US dollar, euro, and the Russian ruble versus the Belarusian ruble; euro versus the US dollar. But, no deals were entered into in the stock exchange market in At the same time, with a view to hedging foreign exchange risks the banks proposed forward contracts for foreign exchange purchase, sale, or conversion, as well as swap deals with foreign exchange. There is no derivatives market in the Republic of Belarus. In 2016, the volume of registered issues of housing bonds, which certify the contribution by their owners of definite amounts of funds for construction of

21 21 a certain size of a total area of a housing accommodation, totaled BYN191.3 million, a 1.2 times decline versus 2015 (BYN235.9 million). According to Edict of the President of the Republic of Belarus No. 537 On Issuance of Bonds by Banks dated August 28, 2006, banks were granted the right to issue bonds secured by the right to claim the repayment of the principal amount of debt and payment of interest under the credits issued thereby for construction, reconstruction, or acquisition of housing against security of real estate (mortgage bonds). In 2016, mortgage bonds were not registered. The total volume of mortgage bonds circulating as at January 1, 2017 amounted to BYN210 million. In the year under review, 14 issues of bonds of local executive and administrative authorities of 11 issuers worth BYN1,124 million were registered, exceeding 4 times the volume of issue in 2015 (BYN229.4 million). At that, bonds denominated in foreign exchange accounted for 83.7% of issue. As at January 1, 2017, bonds of local executive and administrative authorities worth BYN1,899.8 million were in circulation, a 99.2% increase compared with January 1, 2016 (BYN953.7 million). The market value/gdp ratio totaled 2%. As at January 1, 2017, 60 professional participants were acting in the securities market (including 24 banks), of which there were 57 brokers, 57 dealers, 32 participants involved in depository activities, 19 participants in securities trust management, one participant in the activities on organizing securities trading, and one in clearing activities. In 2015, initial public offering of corporate bonds worth BYN201.4 million was carried out on the floor of the JSC Belarusian Currency and Stock Exchange, a 2 times drop compared with 2015 (BYN543.9 million). In 2016, banks bonds worth BYN36.4 million (in 2015, BYN309.2) and other legal persons bonds worth BYN165 million were placed. The volume of placed exchange-traded bonds dropped over 2016 up to BYN148.3 million (from BYN239.7 million in 2015). In addition to the sharp decline in the volume of initial public offering of corporate securities, their share in the total volume of primary offering dropped up to 15.6% as well (in 2015, 67.9%). This reduction was due to an increase by more than 4 times in the volume of placed government securities. The limited capacity of the market resulted in the decline in the volume of resources available to the corporate sector. The share of corporate bonds denominated in foreign exchange in the total volume of corporate bonds issued for the first time totaled 12.4% (in 2015, 42.3%). In 2016, open joint-stock companies didn t place their shares in the primary market. In 2016, the total volume of the secondary trading in corporate securities in the

22 22 stock market totaled BYN2,359.4 million, declining by 30% compared with 2015 (BYN3,345.9 million), including in shares BYN50.3 million (2.2% of the aggregate volume of secondary trades); in 2015, BYN20.2 million (0.6%). In the secondary market the repo transactions with the government bonds and the National Bank s bonds totaled 44% (in 2015, 47.6%). The weighted average yield in the secondary market of corporate bonds denominated in Belarusian rubles stood at: - on banks bonds 21.2% per annum (in 2015, 24.4% per annum), and - on other legal persons bonds 33.3% per annum (in 2015, 42.3% per annum). The shares market capitalization totaled: - as at January 1, 2015, BYN684 million (0.8% of GDP); - as at January 1, 2016, BYN991.6 million (1.1% of GDP); and - as at January 1, 2017, BYN2,426.1 million (2.6% of GDP). The level of capitalization grew as at January 1, 2017 due to the increase in the number of shares in circulation, based on which the market price is calculated. In 2016, purchase/sale transactions involving securities worth BYN7,768.4 million (in 2015, BYN9,187 million), of which transactions involving bonds amounted to 96.7%, were entered into in the OTC securities market Bank management funds As at January 1, 2017, two bank management funds of the trust manager Priorbank JSC ( Raiffeisen - Assets Portfolio - USD and Raiffeisen - Assets Portfolio - EUR ) were in operation. The value of the funds net assets totaled USD902.6 thousand and EUR817.3 thousand (as at January 1, 2016 USD1,804.2 thousand and EUR1,211.1 thousand). 201 natural persons, including three non-residents, were obligees of the above-mentioned funds. In 2016, the value of the bank management funds nominal share, reflecting the return on investment in bank management fund, had differently directed dynamics. After a sharp decline at the beginning of the year, the return on investment went up in March According to the information of the trust manager Priorbank JSC, the funds assets were placed into the shares of equities, the price of which was lower, on the average, than the market price, that led to the formation of losses. The strategy of assets management was revised over the year, that led to a positive result a growth in the value of the nominal share of both funds in July 2016 and its stabilization by the end of the year.

23 23 In 2016, the level of yield of the bank management funds was negative ( Raiffeisen - Assets Portfolio - USD minus 4.2% and Raiffeisen - Assets Portfolio - EUR minus 3.1%), leading to a decline in the net assets value of both bank management funds Leasing organizations As at January 1, 2017, 95 leasing institutions, of which 27 were established with foreign capital participation, were in the Register of Leasing Organizations. The leasing organizations aggregate authorized capital totaled BYN385.5 million as at January 1, The amount of the aggregate net profit of the leasing organizations which presented their reports for 2016 stood at BYN171.7 million. The share of the lessors fees (income) in the volume of leasing payments accrued over 2016 totaled 17.5%. As at January 1, 2017 the volume of the leasing portfolio * totaled BYN2,302.9 million, or USD1.2 billion (at the BYN1/USD1 exchange rate as at January 1, 2017), having dropped since early 2016 by BYN150.6 million, or by 6.1%. Slowing down of the economic entities business activity and inflow of investments to the core capital were conducive to the decline in the leasing portfolio in the year under review. The share of overdue debt in the volume of leasing payments accrued in 2016 amounted as at January 1, 2017 to 3.2% (as at January 1, 2016, 4.1%). Financial leasing operations with the condition of repurchase of the leasing item accounted for 97.4% of the leasing organizations leasing portfolio. Liabilities under agreements entered into in the national currency amounted to 66.1% of the leasing portfolio. Five leasing organizations established with participation of banks capital ( АSB Leasing LLC, OJSC Promagroleasing, VTB Leasing JLLC, Raiffeisen - Leasing JLLC, and OJSC Agroleasing ) accounted for about 70% (BYN1,610.0 million) of the aggregate leasing portfolio. As at January 1, 2017, the export leasing operations ** accounted for 3.1% of the total leasing portfolio. The majority of export operations (88.8%) was carried out by OJSC Promagroleasing. The volume of new business (the aggregate value of the agreements entered into by the leasing companies from January 1 to December 31, 2016) stood at BYN1,111.5 million, having grown over the year by BYN57.8 million, or by 5.5%, compared with * An amount of the lessees debt to lessors under leasing payments as at the reporting date. ** International leasing, where a lessor and a seller (deliverer) of an item of leasing are entities of the Republic of Belarus, while a lessee is an entity of other state.

24 24 As at January 1, 2017, the volume of the leasing companies new business totaled 11.7% of the volume of the long-term credits issued by banks to the economic entities, with the share of new business in the GDP being 1.2%. Over 2016, the leasing companies brisked up the work with lessees being natural persons, that resulted in the 4 times increase in the number of financial lease (leasing) agreements entered into with the natural persons. The number of the leasing companies which signed the financial lease (leasing) agreements with the natural persons grew up. As at January 1, 2016, 29 leasing companies worked in this segment of the leasing market (as at January 1, 2017, 43 leasing companies). Over 2016, more than 167 thousand items of leasing were passed to lessees (of which 153 thousand to natural persons), an increase by 110 thousand items versus The items of leasing were acquired by the leasing organizations at the expense of both their own and attracted funds. More than 50% of the items of leasing worth BYN378.9 million were acquired in 2016 at the expense of own funds (in 2015, 38.2% worth BYN248.2 million). 49.9% of the items of leasing worth BYN377.4 million were acquired at the expense of the attracted special purpose banks credits (in 2015, 61.8% worth BYN401.1 million). At that, the share of advances obtained from lessees accounted for 36.4% of the volume of own funds (in 2015, 42.2%). As at January 1, 2017, leasing organizations attracted credits and loans from non-residents worth BYN435.3 million, or USD222.2 million (at the BYN1/USD1 exchange rate as at January 1, 2017), that amounted to 24.4% of the total volume of credits and loans attracted by leasing institutions Microfinance organizations As at January 1, 2017, 115 microfinance organizations (four consumer cooperatives, four funds, and 107 lombards) were on the Register of Microfinance Organizations. In 2016, the number of microfinance organizations went up by nine, with 23 new organizations being included in the abovementioned register and 14 organizations being excluded therefrom. According to the reports as at January 1, 2017, the microfinance organizations assets totaled BYN23.5 million, own capital BYN15 million, liabilities BYN8.5 million, and net profit obtained over the year BYN3.7 million. The microfinance organizations assets grew by BYN4.1 million (21.1%), own capital by BYN1.8 million (13.6%), and liabilities by BYN2.3 million (37.1%). Net profit of the microfinance organizations in 2016 went up by BYN0.5 million (11.9%), being less than net profit in In 2016, the total amount of attracted monetary funds stood at BYN7.3 million, growing by BYN1.6 million (28.1%) compared with 2015, including:

25 25 - consumer cooperatives attracted BYN0.3 million, the same amount as in 2015, including, from the natural persons being founders BYN0.2 million, or 66.7% (in 2015, BYN0.1 million, or 48%); - funds attracted BYN0.2 million (an increase by BYN0.1 million, or twice as much as in 2015), including from the natural persons being founders BYN0.1 million (50%) (in 2015, BYN0.1 million, or 53.8%); and - lombards attracted BYN6.8 million (an increase by BYN1.5 million, or by 28.3% compared with 2015), including from property owners, founders (participants) BYN4.4 million, or 64.7% (in 2015, BYN3.6 million, or 68.3%). The amount of microloans granted in 2016 totaled BYN100.9 million, an increase by BYN29.6 million, or by 41.5%, compared with 2015, including: - by consumer cooperatives BYN0.9 million (the same amount as in 2015). The whole amount was granted to natural persons for the purposes of developing business and entrepreneurial activities; - by funds BYN4 million (an increase by BYN3.4 million, or 6.7 times, compared with 2015). The microloans to natural persons for the purposes related to business and entrepreneurial initiative accounted for the largest share BYN3.6 million, or 90% (in 2015, BYN0.5 million, or 78.7%); and - by lombards BYN96 million (an increase by BYN26.2 million, or 37.5%, compared with 2015). Microloans versus pledged items from precious metals and stones BYN82.1 million, or 85.5%, versus other pledged movables BYN9.2 million, or 9.6%, and versus pledged vehicles BYN4.7 billion, or 4.9%, accounted for the largest share (in 2015, 81.1%, 10.1%, and 8.8% respectively) Forex companies As at January 1, 2017, six organizations, five of which were 100% - foreign owned, were included in the Register of Forex Companies. According to the reports as at January 1, 2017, the forex companies assets totaled BYN2.7 million, own capital BYN1.2 million, and liabilities BYN1.5 million. The forex companies authorized capital totaled BYN1.6 million as at January 1, 2017, including BYN1.4 million (87.5%) placed by nonresidents. The activities on conducting operations involving non-deliverable OTC financial instruments initiated by natural and legal persons (activities in the OTC forex market) in 2016 were carried out by four forex companies, as well as the first banking forex platform (MTBankFX), which is a joint project of the Joint - Stock Company Minsk Transit Bank and the Suisse bank DukascopyBankSA, was established.

26 26 The amount of funds in foreign exchange invested by the clients of forex companies for the purpose of opening or maintaining their open position (the amount of marginal security) totaled USD0.6 million as at January 1, With a view to meeting their liabilities on repaying marginal security the forex companies, in line with legislation, build up and place secured capital, the amount of which totaled USD0.3 million as at January 1, 2017, on current (settlement) bank accounts with a special functioning regime, which were opened with no less than two banks or non-bank financial institutions of the Republic of Belarus. In 2016, the clients of forex companies and Joint - Stock Company Minsk Transit Bank totaled 974, of which 84 clients were non-residents (8.6%). In 2016, the clients of forex companies and Joint - Stock Company Minsk Transit Bank initiated 176,986 transactions worth USD3,864.8 million (having regard to the leverage), including by non-residents 8,909 transactions (5%) worth USD71.6 million (1.9%). In 2016, the amount of transactions initiated by one client averaged 182, the average amount of the open position under which totaled USD21.8 thousand (having regard to the leverage). In line with Edict of the President of the Republic of Belarus No. 231 On Carrying Out Activities in the Over-the-counter Forex Market dated June 4, 2015, the National Forex Center, the functions of which are assigned to the JSC Belarusian Currency and Stock Exchange, establishes a guarantee fund at the expense of forex companies, banks, and non-bank financial institutions contributions, for the purpose of discharging their obligations to clients involving repayment of marginal security. As at January 1, 2017, the guarantee fund amounted to USD0.5 million.

27 27 Chapter 2 National Bank s activities In 2016, the monetary policy was aimed at curbing inflation and facilitating the stable and well-balanced development of the country s economy. In the year under review, the National Bank continued to implement the monetary policy in the monetary targeting regime, with a key instrument of attaining the ultimate inflation target being control over money supply. The growth of broad money supply, as the indicator having stable interrelation with dynamics of prices, was determined as the intermediate target, while the level of ruble money supply was defined as the operational target Monetary policy Monetary policy target In 2016, curbing of inflation, measured by the Consumer Price Index, up to 12% was the major monetary policy target in In the year under review the level of inflation was below the forecasted indicator. According to the National Statistical Committee s data, the consumer prices grew in 2016 by 10.6% (December-on- December), in 2015 by 12% (Attachment 2.1). Consumer prices and tariffs grew to the utmost in the sphere of services (by 17.6%) (in 2015, by 15.7%) compared with the growth of prices for food products and non-foods (by 10.4% and 6.8% respectively) (in 2015, by 11% and 11.5% respectively). The core inflation went down from 11.3% in 2015 to 10% in 2016 and, according to the National Bank s estimates, led to the increase in the consumer prices by 7.7 percentage points (the share of this indicator totaled 72.4% in 2016 against 68.7% in 2015). Regulated prices and tariffs, including the prices for fruit and vegetable products, grew over 2016 by 12.6% compared with 13.9% in 2015, contributing to the growth in the consolidated consumer prices index by 2.9 percentage points (the share of this indicator was 27.6%, having dropped by 3.7 percentage points compared with 2015). The inflationary processes slowed down in 2016 due to the following factors: - dynamics of money supply, which was formed in line with the macroeconomic situation in the country; - contraction of domestic demand; - decline in import prices by certain positions; and

28 28 - restrained pricing policy of organizations, which manifested itself in the decrease in the rates of profit on the background of declining households incomes. The following factors made the upward pressure on the consumer prices growth: - administrative measures, which made direct as well as indirect impact on the prices and tariffs level; - depreciation of the Belarusian ruble exchange rate versus foreign currencies at the beginning of the year; and - high inflationary expectations of the economic entities. Industrial producers prices rose in 2016 by 8.9% compared with 17% in 2015, with prices for investment goods increasing by 11.9%, for intermediate goods by 7.2%, and for consumer goods by 11.6% Exchange rate policy The exchange rate policy was carried out in 2016 in the managed floating regime. Since November 1, 2016, the weights of foreign currencies included in the currency basket were changed: the share of the Russian ruble was increased from 40% to 50%, of the US dollar retained at the level of 30%, of the euro decreased from 30% to 20%. This decision was taken with a view to converging the weight of the Russian ruble in the currency basket with the share of the Russian Federation in the foreign trade turnover of the Republic of Belarus. In 2016, the Belarusian ruble depreciated by 5.5% against the US dollar (to BYN1,9585/USD1), by 0.7% (to BYN2,0450/EUR1) against the euro, and by 27.1% against the Russian ruble (to BYN3,2440/RUB100). The official exchange rate of the Belarusian ruble dropped by 14.7% against the currency basket. The most drastic decline occurred at the beginning of the year due to the heightened households and economic entities demand for foreign exchange under the influence of the devaluation expectations formed due to depreciation of the Russian ruble exchange rate. The cost of the currency basket amounted to BYN0,2542 at the beginning of December 2016 saw a 10.8% decrease in the real effective exchange rate index of the Belarusian ruble, as measured by the producer price index, from December 2015 (Attachment 2.2) Interest rate policy and bank liquidity regulation The changes in the exchange rate and the currency basket value were calculated as at the last working day of the year with a use of the weights ratios of the currency basket being in effect since November 1, 2016.

29 29 In 2016, the National Bank s interest rate policy was implemented having regard to the need to comply with the inflation target and attain macroeconomic well-balancing. After its increase on January 9, 2015, the refinance rate was gradually decreased from 25% to 18% per annum, the rate on standing operations designed to provide liquidity (overnight credit; swap transactions) from 30% to 23% per annum, the rate on standing operations designed to withdraw liquidity from 16% to 11% per annum. The average weighted interest rate in the intraday interbank market was decreased from 29.4% per annum in January 2016 to 10.5% per annum in December The National Bank s transactions designed to maintain liquidity dominated the structure of monetary transactions in 2016 Q1, that was due to the deficit of the banking system s liquidity (the share of auctions designed to provide liquidity totaled 40.5%). Under the impact of the National Bank s transactions in the domestic market the level of the banking system s liquidity in Belarusian rubles started to grow. In addition, with a view to reducing the liquidity deficit, the required reserves ratios in respect of total attracted funds were reduced by 0.5 percentage point up to 7.5%. As a result, since 2016 Q2, the banking system s liquidity has been characterized by a stable surplus. Therefore, the National Bank used, mainly, liquidity withdrawal transactions, in which the auctions designed to place the National Bank s bonds were dominating (86.6%). In 2016, the average daily balance of debt on operations designed to maintain current liquidity of the banking system amounted to BYN134.1 million. In the reporting year, banks average daily balance of operations designed to withdraw liquidity stood at BYN962.5 million Key monetary indicators An increase in the broad money supply (M3) in 2016 accounted for 3.8%, or BYN1.2 billion, of which the ruble money supply (M2*) 19.4%, or BYN1.8 billion (Attachment 2.3). In 2016, the increase in M2* was mainly due to an inflow in term deposits and deposits in escrow of the natural persons (by BYN336.2 million, or by 12.9%) and legal persons (by BYN338.7 million, or by 16.7%), transferable deposits of natural persons (by BYN163.4 million, or by 11.6%) and legal persons (by BYN520,8 million, or by 36.1%), and growth in cash in circulation (by BYN367 million, or by 25.8%) (Attachment 2.4).

30 30 In 2016, the share of natural persons term deposits and deposits in escrow in the structure of the ruble money supply dropped by 1.6 percentage points, the share of legal persons term deposits decreased by 0.5 percentage points. The share of cash in circulation went up by 0.9 percentage point, the share of natural persons transferable deposits increased by 1 percentage point, the share of legal persons transferable deposits went up by 2.2 percentage points, and the share of securities issued by banks in the national currency (outside bank circulation) grew by 0.1 percentage point. In 2016, the share of the ruble constituent of the broad money supply increased from 27.7% to 31.8 %. As of January 1, 2017, foreign currency deposits amounted to USD10.6 billion in dollar terms, a USD1.1 billion, or a 9.7% decrease in In 2016, the velocity of the broad money supply circulation fell, on an annualized basis, to 2.8 circulations, or by 6.3% (to 3 circulations, or by 17.3%, in 2015). The velocity of the ruble money supply circulation increased, on an annualized basis, to 10.1 circulations, or by 8.5% (to 9.3 circulations, or by 6.1%, in 2015). In 2016, the ruble money base decreased by BYN58 million. The main factors, which led to the decrease in the ruble money supply, were the decrease in the National Bank s net ruble claims on banks in Belarusian rubles by BYN3 billion, and the decrease in the National Bank s net ruble claims on the Government of the Republic of Belarus by BYN0.4 trillion. Foreign exchange operations carried out by the National Bank and the Government of the Republic of Belarus increased the ruble money base by BYN3.2 billion. As of January 1, 2017, international reserve assets of the Republic of Belarus amounted to: - USD4.9 billion under the IMF s methodology, a USD0.8 billion decrease in the year under review; and - USD5.2 billion on the national definition, a USD0.7 billion increase in the year under review. As of January 1, 2017, the amount of gold and foreign exchange reserves covered 2 months of goods and services imports. The growth in gold and forex reserves was mainly due to the attracted funds from the sale of bonds in foreign exchange by the National Bank and the Ministry of Finance, net purchase by the National Bank of foreign exchange in the domestic foreign exchange market, which was generated as a result of excess of the foreign exchange supply over the demand therefor, revenues from export duties for oil and oil products, two trenches of the financial credit of the Eurasian Fund for Stabilization and Development, and increase in the price of gold in the international precious metals market. Scheduled repayment of the external and internal obligations in foreign exchange by the Government and

31 31 the National Bank of the Republic of Belarus had a curbing impact on the dynamics of reserves Supervision of banks activities Streamlining regulatory legal framework for banking supervision In 2016, the work was going on to streamline regulatory legal framework governing banking supervision and bring it into line with international standards and experience of practical application (Attachment 2.5). In April 2016, within the framework of the Financial Sector Assessment Program (FSAP) in the Republic of Belarus the IMF and the World Bank mission conducted assessment of the National Bank s compliance with the Core Principles for Effective Banking Supervision, developed by the Basel Committee on Banking Supervision (BCBS), as the banking supervision authority. Based on the result of the assessment, the experts noted the achievement of significant progress in the sphere of development of the banking supervision system of the Republic of Belarus. Recommendations were received under 11 principles, which, in accordance with the updated assessment methodology, focus more on the practical implementation of the principles than on the availability of legal and regulatory frameworks. A plan of actions designed to implement the recommendations was developed. With a view to determining the banks readiness to implement the liquidity ratios Basel III as secure functioning requirements, the meeting by banks of the Net Stable Funding Ratio (NSFR) and the Liquidity Coverage Ratio (LCR) continued to be monitored over In order to improve the foreign exchange liquidity management, the liquidity coverage ratio in foreign exchange was calculated not only with respect to core foreign currencies, but also in aggregate for all types of foreign exchange. As part of the countercyclical regulation measures taken by the National Bank, which are aimed at ensuring stable functioning of banks under current macroeconomic conditions, the amount of provisions made under assets and contingent liabilities classified under Risk Group II was reduced from 10% to 5%, making it possible to reallocate the released special provisions under assets not related to the bad ones in favour of increasing the volumes of special provisions under the bad debt. In 2016, the National Bank continued to limit credit risk under loans issued to legal and natural persons in Belarusian rubles at excessively high interest rates by means of gradual reduction of the ratio used to determine the

32 32 upper limit of the annual interest rate, at which the banks are required to include the loan granted to a legal person into the special portfolio of homogeneous loans, with special provisioning under such portfolios worth 30% of the balance owed under loan. With a view to maintaining the level of yield of the Belarusian banks along with lowering the credit risk by means of creating more attractive conditions for placing foreign exchange resources in the government securities in foreign exchange characterized by a limited risk and a high degree of liquidity, the degree of risk under securities of the Government and the National Bank denominated in foreign exchange was changed when calculating the credit risk value, liquidity indicators and risk concentration. As a result of granting the powers to supervise the activities of the JSC Development Bank of the Republic of Belarus to the National Bank, since August 5, 2016 the National Bank s requirements in the sphere of banking supervision established for banks and non-bank finance institutions has been applied to this bank. The special aspects of application of the secure functioning requirements to the Development Bank, as well as the specific procedure for making special provisions and calculating regulatory capital having regard to the specific nature of its activities, were established. In the year under review, the right not to reduce the regulatory capital by certain intangible assets purchased in , which was granted to the banks in 2015, was extended to include the non-bank financial institutions and the Development Bank. This right was also applied to the intangible assets upgraded in The given changes were aimed at reducing the pressure on the regulatory capital from the intangible assets in the future, which could make it possible for banks, non-bank finance institutions and the Development Bank to continue active implementation of innovative banking technologies and building the technical capacity up to the level complying with the best standards of financial services provision. Having regard to the need to improve the efficiency of corporate governance at banks with account of the IMF s and the World Bank s recommendations, as well as to further implement the updated international standards in the sphere of corporate governance and organization of the risk management and internal control systems, additional requirements were set with regard to the composition, procedures and functions of the supervisory boards (boards of directors) and committees established under them, as well as the requirements to the activities of external auditors and information disclosure in this sphere. In order to improve the effectiveness of interaction of the National Bank s units participating in the inspections and the level of control over compliance with the requirements of the legislation regulating the procedures for organizing and conducting inspections, the inspection procedure is established, the stages

33 33 of this process related to the planning and preparation of inspections, their conduct and preparation of materials and consideration of results are detailed. For each stage, deadlines and responsible units are defined. With the aim of regulating certain matters of procedure with account of the current practice of applying the legislation norms, the resolutions of the Board of the National Bank related to the issues of external auditors activities, registration of banks and non-bank financial institutions and their licensing, assessment of compliance with qualification requirements and (or) requirements to the business reputation for managers, chef accountant, their deputies, members of the bank s management authorities, the Development Bank, nonbank financial institution, attestation for the right of acquiring a certificate of professional accountant of a bank, and attestation for compliance with professional requirements to a crisis manager in case of a bankruptcy of a bank or non-bank financial institution were amended Off-site supervision In 2016, taking the timely measures, including those of supervision response, aimed at ensuring safe and liquid functioning of banks and non-bank finance institutions (hereinafter for the purpose of this section the banks ), protecting the interests of their depositors and creditors, minimizing the risks accepted by banks, streamlining their operational costs, as well as preventing bankruptcy of the banking sector s participants, were the main tasks of the offsite supervision. An ongoing work to increase banks capitalization (in the first place to remedy failure to comply with minimum regulatory capital requirement), to improve corporate governance and to prevent performance of non-core activities thereby from happening, and tackling other issues stemming from their activities, was carried out with management and owners of banks. Banks measures to prevent decrease of the regulatory capital in real terms (taking into account inflation) and maintain regulatory capital adequacy at the level of at least 12% were controlled on an ongoing basis. In 2016, the National Bank executed control over the banks compliance with secure functioning requirements and other prudential norms and restrictions. The work was continued to provide equal conditions for functioning of banks and ensure fair competition. Particular emphasis was placed on the financial standing of banks which bear the main burden of lending to the real sector of the Belarusian economy (first and foremost the state-owned banks). Measures to ensure banks sustainable and safe functioning were regularly addressed at the meetings of the Board of the National Bank.

34 34 Within the framework of the off-site supervision, the National Bank was constantly assessing financial sustainability of banks and effectiveness of their activities, paid attention to the efficiency of risks management, primarily of the credit risk, prospects for further functioning of banks, as well as revealing problems at banks at early stages of their occurrence. Considerable attention was paid to the exercise of control over the state of liquidity and management of liquidity at banks, as well as to the issues of foreign exchange risk management. The work was continued to improve the National Bank s information and analytical system for the purpose of strengthening and expanding possibilities of the off-site supervision. Based on the results of the analysis of reports and other information, the National Bank, on the basis of a motivated judgment, took appropriate supervisory response measures with respect to banks to halt negative trends and avoid (prevent) situations threatening the depositors and other creditors interests. In 2016, the special permission (license) to carry out banking activities was revoked from the CJSC N.E.B. Bank in line with the decision on the liquidation of this bank taken at the shareholders general meeting. The National Bank continued to constructively cooperate with international financial institutions, audit organizations, the Association of Belarusian Banks, and supervisory bodies of other countries Audits of banks In 2016, the National Bank conducted three full-scope and 16 limitedscope audits of the Belarusian banks, including six audits under orders from law enforcement authorities and courts. The following banks were audited: JSC Belagroprombank, JSC JSSB Belarusbank, Belinvestbank JSC, Open Joint Stock Company "BPS-Sberbank", JSC MTBank, Zepter Bank CJSC, TC BANK JSC, JSC Eurotorginvestbank, Bank Moscow-Minsk JSC, Reshenie Bank Joint-Stock Company, CJSC Alfa-Bank, OJSC Belarusky Narodny Bank, CJSC VTB Bank (Belarus), JSC Absolutbank, JSC Delta Bank, and CJSC BTA Bank. In the course of audit, particular emphasis was placed on the quality of banks assets and level of credit risk, quality of corporate management of banks, development of risk management and internal control systems, and their compliance with the level of risks being taken. Based on the results of the audit, the instructions to remedy identified violations and prevent them from happening in the future, as well as to remedy