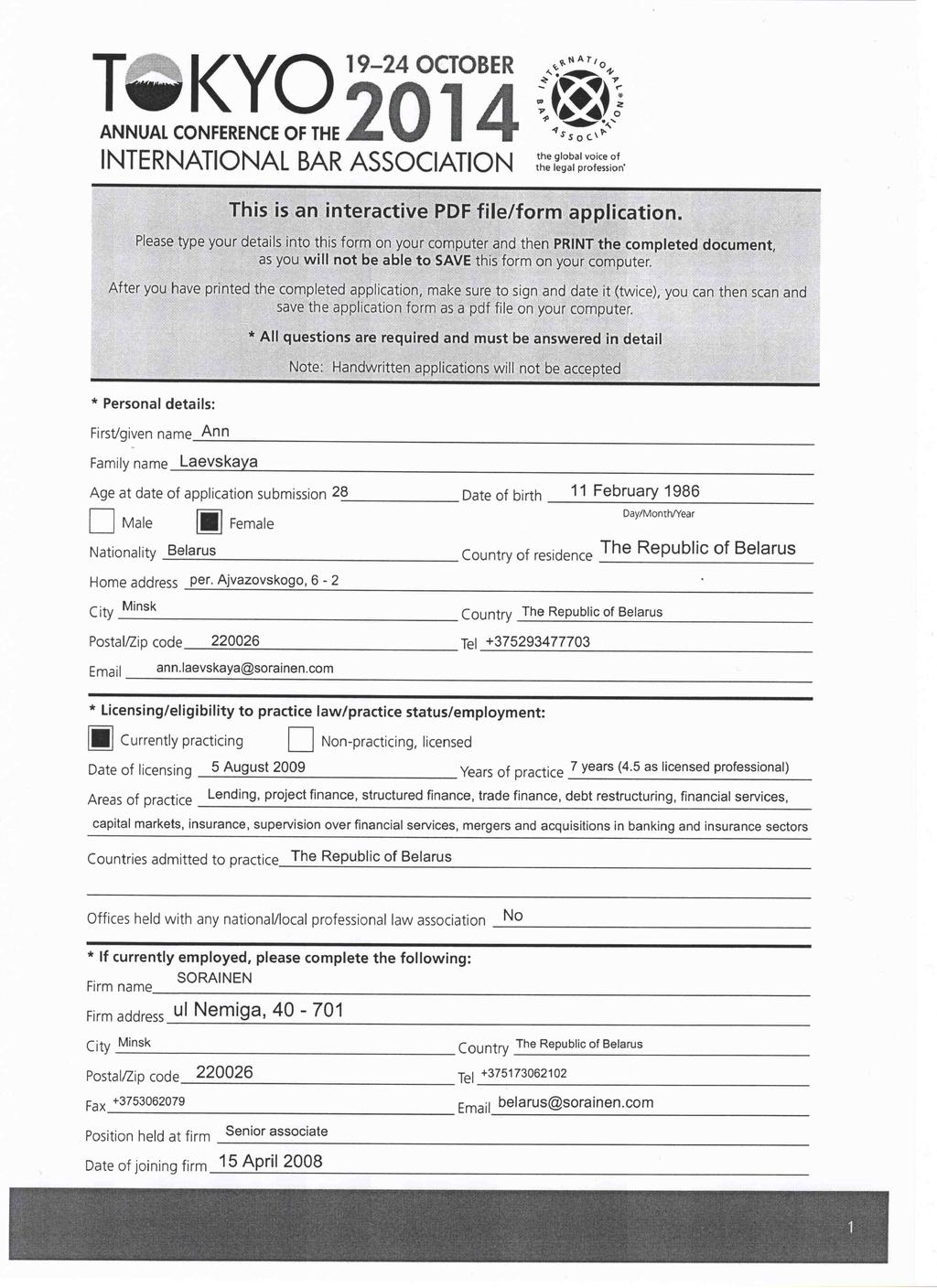

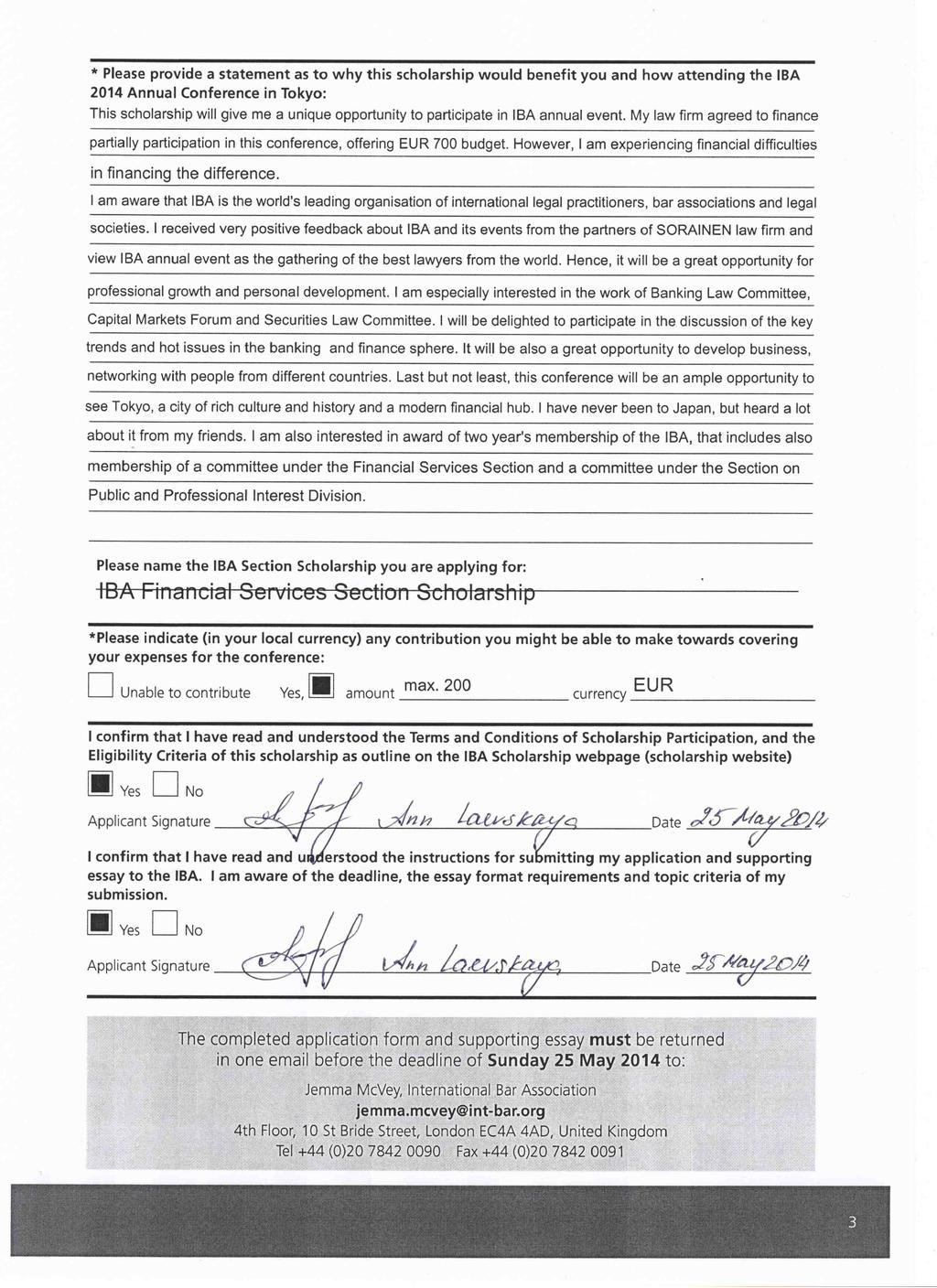

Ann Laevskaya, IBA Financial Services Section Scholarship

|

|

|

- Abigayle Gray

- 6 years ago

- Views:

Transcription

1

2

3

4 Ann Laevskaya, IBA Financial Services Section Scholarship

5 Liabilities in the financial sector; are the regulatory and contractual obligations placed on intermediaries in the financial sector set at the right level to promote a thriving market and avoid the next crisis? The classic example of a financial intermediary is a bank that consolidates deposits and uses the funds to transform them into loans. The term financial intermediaries also typically refers to private equity and venture capital funds, private pension funds, leasing companies, insurance companies, and microloans providers. Out of mentioned types of the financial intermediaries, Belarusian financial market is dominated by banks and insurance companies, which are subject to most detailed and comprehensive regulation and will be the primary focus of this essay. The leasing market emerged in 1991 and has been rapidly developing since then. In 2014 supervision over leasing companies was transferred from the Ministry of Economy to the National Bank and new regulation was introduced. The number of microloans providers is actively growing. So far activity of such companies has not been subject to keen attention of the state, resulting in exorbitant interest rates and outrageous fines for defaulting borrowers. Microloans providers are expected to be put under the supervision of the National Bank shortly and their activity will be heavily regulated. Collective investment institutions are almost non-existent. Few pension funds are functioning on the basis of insurance companies and several collective investment funds are managed by Belarusian banks. The legal framework for joint stock investment funds has been in place since 1992; however, no such funds are functioning at the moment. It is expected that the concept of a new law on investment funds will be developed by the end of 2014, while drafting and adoption of the law may take additionally two or three years. The law will provide the legal framework for joint stock investment funds and unit investment funds. Recently few companies emerged in Belarus, positioning themselves as private equity and venture capital funds. Those do not represent the collective investment institutions, but instead consolidate the

6 money of business angels, foreign private funds and international financial institutions. No specific regulatory framework for the activity of such companies exists. This essay considers the regulatory framework for the banks and insurance companies, as the biggest, most actively developing and most heavily regulated financial intermediaries in Belarus. The essay seeks connections between the level of liabilities placed on the financial intermediaries and promotion of successful, healthy and strong market on the one hand and prevention of the crisis on the other hand. Before proceeding with the review of the particular requirement in the finance sector, it is due mentioning that in Belarus the level of regulation of the financial markets per se does not have a direct connection with prevention of crisis. This is explained by peculiarities of Belarusian economy structure that per se may provoke or contribute to, the financial disorder and economic crisis. 70% of Belarusian GDP is produced by state-controlled companies. State-controlled companies often enjoy substantial benefits and subsidies from the state to keep them on the market, including cheap financial resources. Such structure of Belarusian economy is also associated with extra burden for budget in terms of salary increase and salary-related social payments for employees. In 2011 Belarus was hit by crisis that was accompanied by almost 180% devaluation of Belarusian national currency and hyperinflation breaking the 109% level. Though it was preceded by world financial crisis, the situation in Belarus in 2011 was determined to the large extent by internal reasons. The roots of the crisis are commonly attributed to excessive state spending and heavy government dominance in the country s economy. Prior to the crisis the government announced a number of government-directed lending programs to ensure modernisation of the Belarusian economy. This modernisation contributed to the current account deficit and heightened pressure on the exchange rate and foreign exchange reserves. The crisis was fuelled by generous administrative growth in salaries, pensions, minimum wage and other social benefits shortly before the Presidential elections in 2010, which lead to significant rise of demand for foreign currency and imported goods. The right level of regulation of the financial intermediaries activity is a precondition for a thriving market. It also influences the possibility of crisis and its consequences. However, such regulation alone, irrespective of its level and adequacy, is not able to prevent the crisis in Belarus due to specifics of Belarusian economy structure.

7 Banks Out of 31 banks functioning in Belarus, four of them are state-owned, holding the largest value of assets around 64% of the whole banking system. The National Bank performs supervision over the Belarusian banking system and acts as the registration authority for the newly established banks. Banks may be established by local and foreign shareholders, be it individuals or legal entities. There is a quota set up on the foreign capital participation in the Belarusian banking system. It amounts to 50% of the total volume of authorised fund of the banking system and is set by the National Bank upon approval of the President. Banks with foreign investments should obtain prior authorisation from the National Bank to increase the authorised fund of a bank using non-residents funds and to sell shares to non-residents. National Bank may establish restrictions on banking operations for foreign banks if similar restrictions on activities of banks with Belarusian investments have been imposed in the relevant foreign countries. Banking activity is licensed in Belarus. In order to obtain and maintain the license, the bank should ensure, inter alia, that: - it maintains the regulatory capital above the required threshold; - it is compliant with safe functioning requirements; and - adequate risk management and internal control system are established. The basic requirements ensuring safety of the banking system include the requirements to the authorised fund of the newly established bank and safe functioning requirements. The minimum amount of the authorised fund of a new bank, including a bank formed as a result of reorganisation, constitutes EUR 25 million. This requirement was introduced in June 2011, however, the operating banks have not been forced to adjust their authorised funds in accordance with the new requirement (previous minimum was EUR 5 million). The authorised fund may be formed with cash and certain other types of property. The minimum amount of the authorised fund should be paid in cash. Non-monetary contributions are allowed to the extent relevant property constitutes the fixed assets and is necessary for carrying out banking activity.

8 For the formation of the authorised fund of a bank, only own means of its founders may be used. I.e. the shareholders are not allowed to form or increase the authorised fund with the borrowed funds. Monetary contributions to the authorised fund of a bank may be made both in Belarusian roubles and in foreign currency. However, the entire authorised fund is declared and accounted in Belarusian roubles. In June 2012 in view of anticipated integration of the financial markets of Belarus, Russia and Kazakhstan, the requirements as to the minimum size of regulatory capital of banks that do not attract monetary funds of individuals to accounts or deposits and do not open and operate individuals bank accounts were revised. These banks should have increased their regulatory capital to EUR 15 million no later than 1 January 2014 (previous threshold was EUR 5 million). The requirement as to the minimum amount of regulatory capital will be unified for all banks in Belarus as of 1 January 2015 and will constitute EUR 25 million. Regulatory capital consists, inter alia, of the authorised fund. The regulatory capital requirement should be complied in Euro, while the authorised fund is declared and accounted in Belarusian roubles. Hence, upon devaluation of Belarusian rouble the regulatory capital substantially decreases and the banks and their shareholders need to take measure for increasing the regulatory capital through injections in the authorised fund, provision of subordinated loans or increase of the authorised fund at the expense of the bank s profit. Subordinated loans are usually a preferred choice, especially among banks established by foreign shareholders. However, the amount of the subordinated loan that may be considered for the purpose of regulatory capital calculation is limited. Other safe functioning requirements include regulatory capital adequacy requirements, liquidity ratios, risk concentration restrictions, foreign exchange risk restrictions, and requirements to the banks participation in the authorised capital of other profit-making organisations. The requirements are generally adequate, both from the perspective of promotion of thriving market and prevention of banks failure. However, the banks are far from being fully compliant with the requirements. As of 1 May 2014, almost half of Belarusian privately-owned banks do not comply with regulatory capital requirements or regulatory capital adequacy ratios. Partially, this is caused by reluctance of private shareholders to make injections in the authorised capital of the banks in view of potential

9 devaluation of respective contributions. In 2011 the devaluation swallowed up around 65% of the authorised funds recorded within the regulatory capital; in 2014 devaluation expectations are high again. In spite of this incompliance, during the past two years the National Bank took comparatively mild measures, including loosening foreign exchange risk restrictions for those increasing the authorised capital with contributions in foreign currency, introducing limitations imposed on the amount of attracted retail deposits from the individuals or, in the worst case scenario, prohibiting declaration of profit and payment of dividends to the shareholders. No banking licenses were recalled or suspended due to incompliance with regulatory capital requirements. In order to promote stability of the banking system, requirements to establishment of reserve funds and making mandatory reservations with the National Bank exist. On the date of approval of their annual reports banks are required to create a reserve fund not less than 5 per cent of the registered authorised fund. Standards for mandatory reservation deposited in the National Bank are as follows: - for retail deposits in Belarusian rubles 0 per cent; - for corporate deposits in Belarusian rubles 9 per cent; and - for the funds raised in foreign currency 13 per cent. Activity on acceptance of retails deposits and providing loans to individuals and corporate customers is subject to limitations. All banks accepting retail deposits are required to register with the Agency for Guaranteed Reimbursement of Bank Deposits, pay one-time registration fee and make quarterly contributions. Registration fee constitutes 0.5 per cent of the registered authorised fund. Quarterly contributions constitute 0.3 per cent of the remainder of the retail deposits attracted by the bank as of the beginning of the month following respective quarter. In view of pre-crisis situation in Belarusian economy and financial system the National Bank recently took certain measures to restrict lending pace, reduce loan rates, primarily on consumer loans, as well as to limit foreign currency lending.

10 Since 1 January 2014, the approach to assessing credit exposure risk in respect of loans to individuals, when calculating regulatory capital adequacy was changed. A risk weight of 200 per cent was set for loans at an interest rate exceeding the refinancing rate increased by 150 per cent but below or equal to three times that amount. For loans at an interest rate exceeding three times the amount of the refinancing rate a risk weight of 500 per cent was set. Thus, loans with annual interest rates exceeding per cent and up to 64.5 per cent belong to the VIII risk group with a risk weight of 200 per cent, while loans with an annual interest rate exceeding 64.5% belong to the IX risk group with a risk weight of 500 per cent. In addition, since 12 December 2013, for consumer loans at annual interest rates exceeding twice the amount of the refinancing rate (ie 43 per cent as of 19 May 2014) the banks are required to form a special reserve for potential losses on assets subject to credit risk of 100% of the total amount of those loans. The above mentioned measures are aimed at limiting the economic feasibility for banks to provide consumer loans at high interest rates. Since 15 January 2014, banks are prohibited from providing loans to Belarusian enterprises in foreign currency for settlement with residents of the country. The prohibition does not apply to attracting foreign currency loans by residents from non-residents. It also does not affect loans provided by banks from non-residents resources, connected with these loans in terms, amounts and currencies. Since 8 May 2014 the limitations on the maximum interest rates for loans to the legal entities were established. The decision was made in order to increase availability of loan facilities for the real economy. Under the new legislation, the interest rates for loans to the legal entities must not exceed average interest rate for new loans extended by the legal entities in Belarusian roubles, calculated and notified by the National Bank on monthly basis. In April such average interest rate constituted 39.4 per cent. The ceiling on interest rates will be in force until 1 January It is expected that during this period the interest rates in the economy will go down to adequate level and the financial situation will be generally more stable (ie interest rates on interbank loans and retail deposits go down as well). Insurance companies

11 The Belarusian insurance market is heavily controlled by the state. The Ministry of Finance performs supervision over the insurance market and acts as the registration authority for the newly established insurers. Foreign insurers, except for some cases, are not allowed to conduct insurance activity in Belarus, other than through establishment of a subsidiary and obtaining a licence for such subsidiary. There is also an obligation on the Belarusian legal entities, foreign legal entities that carry out their activities in Belarus, Belarusian citizens and persons with no citizenship that permanently reside in Belarus to insure their valuable interests in Belarus only with insurers authorised to run an insurance business in Belarus. Foreign investments in the Belarusian insurance sector are limited by 30 per cent quota. For the purpose of quota calculation, the total value of all contributions of foreign investors and their subsidiaries in authorised funds of insurers registered in Belarus is divided by the aggregate authorised funds of insurers registered in Belarus, multiplied by 100. Belarusian law provides for two types of insurance voluntary and mandatory, the latter making a substantial share in overall insurance. In 2013 payments under mandatory types of insurance constituted about 45.5 per cent of all insurance fees collected in Belarus. Unlike in the banking sector, where different players act in relatively uniform legal environment, the state and private insurance companies (especially those with foreign investments) clearly act under different rules of play. Mandatory insurance can be arranged only by state-owned and state-controlled insurance companies 1. Additionally, the insurance companies with the share of private (local or foreign) investors of at least 50% are prevented from insuring the interests of the Republic of Belarus, its territorial administrative units, state authorities, state legal entities, the legal entities in which the Republic of Belarus or its territorial administrative units own the controlling stake. Considering that 70% of Belarusian GDP is 1 State-controlled insurance company means insurance company with a state share of over 50 per cent in their authorised fund.

12 produced by state-owned and state-controlled enterprises, private insurance companies are allowed to act in a quite narrow niche. Insurance companies of foreign parent companies may not engage in the life insurance, property insurance related to delivery of goods, supplying services or performing contractor work for state needs, and insurance of the valuable interests of Belarus and its territorial administrative units. Since 1 July 2014 foreign subsidiaries will be able to engage in life insurance of the individuals. However, this is only a tiny step of long-expected liberalisation of the insurance market. Belarus is still far from introduction of fair rules of play for private and state-owned insurers and promotion of healthy and strong insurance market. Currently the insurance market is dominated by the state company Belgosstrakh, which share in the total volume of insurance fees collected by Belarusian insurers accounts for around 48.5 per cent. The requirements to the minimum amount of authorised fund of insurers are as follows: - EUR 1 million equivalent for insurers not engaged in life insurance; - EUR 2 million equivalent for insurers engaged in life insurance. - EUR 5 million equivalent for insurers exclusively involved in the reinsurance activity. The contribution of each founder to the authorised fund and respectively the share of each shareholder may not exceed 35 per cent of the company's authorised fund. An insurer must at all times have funds in its bank accounts with Belarus banking institutions in an amount equal to the minimum amount of the insurer's authorised capital. Since 1 July the requirements to the authorised fund of all insurers will be unified and will constitute EUR 5 million. Limitations on the maximum amount of share will be lifted. The existing insurers will have to increase their authorised funds gradually by 1 May Respective changes were adopted in anticipation of integration of the financial markets of Belarus, Russia and Kazakhstan. The insurers are required to form reserves out of the collected insurance fees and comply with the requirements to the investment of such reserves. The investment must be performed on the basis of recurrence, profitability, liquidity and diversity. State-owned and state-controlled insurance companies place funds with the state-owned banks and may invest funds of their reserves in the securities of the Republic of Belarus, the National Bank and

13 local executive authorities. Such investments may be performed only on the basis of agreements concluded with Belarusian state-owned banks. Additionally, state-owned and state-controlled insurance companies may invest their reserves in the securities of state-owned Belarusian banks (except for the shares) and precious metals, subject to their placement with Belarusian state-owned banks. Other insurance companies may invest funds of their reserves only in the following instruments: - securities of the Republic of Belarus, - securities of the National Bank, - securities of local executive authorities, - securities of Belarusian banks (except for shares), - securities of Belarusian legal entities (except for shares and promissory notes), - real estate (except for residential premises), - precious metals (except for waste) subject to their placement with Belarusian banks. The law also establishes the minimum or maximum amounts (in percentage) that must be invested in various instruments. The objects for investment of funds of insurance companies are limited and restrain flow of funds in the Belarusian economy and role of insurance companies as financial intermediaries. Belarusian law limits purposes of use of funds created by the insurance companies, including insurance reserve funds, guarantee funds, and prevention measures funds and assets, acquired out of such resources. In particular, insurance companies are prohibited: - to pledge securities, acquired out of the insurance reserve fund resources; and - to use otherwise insurance reserve fund resources and assets, acquired out of such resources in order to secure performance of obligations which are not connected with insurance activity. The Ministry of Finance carefully monitors compliance with requirements to investing the funds of the reserves. In 2014 licences of two private insurers were suspended, inter alia, for failure to comply with the requirements on formation of reserve funds and their proper investment. * * *

14 The right level of regulation of the financial intermediaries activity is a precondition for a thriving market. It also influences the possibility of crisis and its consequences. However, such regulation alone, irrespective of its level and adequacy, is not able to prevent the crisis in Belarus due to specifics of Belarusian economy structure. Belarusian banking legislation sets generally adequate requirements to the banks as financial intermediaries, both from the perspective of promotion of a thriving market and prevention of banks failure. At the moment, banks lending operations are heavily restricted; however, these measures are justified considering high interest rates in the economy. Legislation on insurance activity sets substantial preferences for state-owned and state-controlled insurance companies, restricting development of strong and healthy market. As the result, the insurance market is dominated by one state company, collecting almost half of the insurance fees. The objects for investment of funds of insurance companies are limited and restrain flow of funds in the Belarusian economy and role of insurance companies as financial intermediaries. Recently, Belarus increased the requirements to the regulatory capital of banks and authorised funds of the insurance company in view of anticipated integration of financial markets of Belarus, Russia and Kazakhstan. However, there are many challenges on the way of integration, associated with liberalisation of Belarusian financial market, on the one hand, and support of the national players, provision of Belarusian financial stability and prevention of future crises, on the other hand.

Banking and Credit Organizations in the Russian Market

20. Banking 20.1 Introduction As of 1 February 2016 there were 676 banks registered in Russia. The Central Bank of the Russian Federation (the Bank of Russia ) is the key regulatory authority for banking

20. Banking 20.1 Introduction As of 1 February 2016 there were 676 banks registered in Russia. The Central Bank of the Russian Federation (the Bank of Russia ) is the key regulatory authority for banking

Money market. Alexander Mukha

Currency Market and Banking System: Pressure of adverse factors Alexander Mukha 219 Summary In 2013, Belarus faced a marked deterioration of external terms of trade, which brought about export cuts, drops

Currency Market and Banking System: Pressure of adverse factors Alexander Mukha 219 Summary In 2013, Belarus faced a marked deterioration of external terms of trade, which brought about export cuts, drops

FINANCIAL STABILITY IN THE REPUBLIC OF BELARUS

NATIONAL BANK OF 1 THE REPUBLIC OF BELARUS FINANCIAL STABILITY IN THE REPUBLIC OF BELARUS 2010 MINSK, 2011 2 This publication has been prepared by the Banking Supervision Directorate in concert with the

NATIONAL BANK OF 1 THE REPUBLIC OF BELARUS FINANCIAL STABILITY IN THE REPUBLIC OF BELARUS 2010 MINSK, 2011 2 This publication has been prepared by the Banking Supervision Directorate in concert with the

International Monetary Fund Washington, D.C.

2006 International Monetary Fund May 2006 IMF Country Report No. 06/179 Republic of Belarus: Financial Sector Assessment Program Technical Note Deposit Insurance This Technical Note on Deposit Insurance

2006 International Monetary Fund May 2006 IMF Country Report No. 06/179 Republic of Belarus: Financial Sector Assessment Program Technical Note Deposit Insurance This Technical Note on Deposit Insurance

Article 56 of the Bank of Russia Law.

As of January 1, 2017 No. Commentary Relevant laws and regulations 1. Duties and powers of banking supervision 1.1 Banking supervisory The Bank of Russia Articles 4 and 56 of authority Federal Law No.

As of January 1, 2017 No. Commentary Relevant laws and regulations 1. Duties and powers of banking supervision 1.1 Banking supervisory The Bank of Russia Articles 4 and 56 of authority Federal Law No.

REPORT MONETARY POLICY INSTRUMENTS OF THE NATIONAL BANK OF POLAND IN 2007 BANKING SECTOR LIQUIDITY

REPORT MONETARY POLICY INSTRUMENTS OF THE NATIONAL BANK OF POLAND IN 2007 BANKING SECTOR LIQUIDITY Warsaw 2008 2 Banking sector liquidity Executive summary Pursuant to Article 227 para. 1 of the Constitution

REPORT MONETARY POLICY INSTRUMENTS OF THE NATIONAL BANK OF POLAND IN 2007 BANKING SECTOR LIQUIDITY Warsaw 2008 2 Banking sector liquidity Executive summary Pursuant to Article 227 para. 1 of the Constitution

On the Approval of the Statute of the National Bank of the Republic of Belarus

On the Approval of the Statute of the National Bank of the Republic of Belarus Edict of the President of the Republic of Belarus No. 320 dated June 13, 2001 1. To approve the attached Statute of the National

On the Approval of the Statute of the National Bank of the Republic of Belarus Edict of the President of the Republic of Belarus No. 320 dated June 13, 2001 1. To approve the attached Statute of the National

Approved by the State Duma on September 18, Approved by the Federation Council on October 14, 1998

FEDERAL LAW NO. 40-FZ OF FEBRUARY 25, 1999 ON INSOLVENCY (BANKRUPTCY) OF CREDIT INSTITUTIONS (with the Amendments and Additions of January 2, 2000, June 19, August 7, 2001, March 21, 2002, December 8,

FEDERAL LAW NO. 40-FZ OF FEBRUARY 25, 1999 ON INSOLVENCY (BANKRUPTCY) OF CREDIT INSTITUTIONS (with the Amendments and Additions of January 2, 2000, June 19, August 7, 2001, March 21, 2002, December 8,

Сontents. Introduction. Chapter 1. Economic and financial situation in the Republic of Belarus

APPROVED Edict of the President of the Republic of Belarus No. 182, dated May 25, 2017 REPORT of the National Bank of the Republic of Belarus for 2016 Minsk 2 Introduction Сontents Chapter 1. Economic

APPROVED Edict of the President of the Republic of Belarus No. 182, dated May 25, 2017 REPORT of the National Bank of the Republic of Belarus for 2016 Minsk 2 Introduction Сontents Chapter 1. Economic

NATIONAL BANK OF THE REPUBLIC OF MACEDONIA

NATIONAL BANK OF THE REPUBLIC OF MACEDONIA Pursuant to Article 64 paragraph 1 item 22 of the Law on the National Bank of the Republic of Macedonia ( Official Gazette of the Republic of Macedonia No. 3/2002,

NATIONAL BANK OF THE REPUBLIC OF MACEDONIA Pursuant to Article 64 paragraph 1 item 22 of the Law on the National Bank of the Republic of Macedonia ( Official Gazette of the Republic of Macedonia No. 3/2002,

Creation of the System of Contractual Savings for Housing in Belarus

GERMAN ECONOMIC TEAM IN BELARUS 76 Zakharova Str., 220088 Minsk, Belarus. Tel./fax: +375 (17) 236 1147, 236 4395 E-mail: bmer@ipm.by. Internet: http://research.by/ PP/04/05 Creation of the System of Contractual

GERMAN ECONOMIC TEAM IN BELARUS 76 Zakharova Str., 220088 Minsk, Belarus. Tel./fax: +375 (17) 236 1147, 236 4395 E-mail: bmer@ipm.by. Internet: http://research.by/ PP/04/05 Creation of the System of Contractual

FINANCIAL STABILITY IN THE REPUBLIC OF BELARUS

NATIONAL BANK OF THE REPUBLIC OF BELARUS FINANCIAL STABILITY IN THE REPUBLIC OF BELARUS 2009 MINSK, 2010 2 This publication has been prepared by the Banking Supervision Directorate in concert with the

NATIONAL BANK OF THE REPUBLIC OF BELARUS FINANCIAL STABILITY IN THE REPUBLIC OF BELARUS 2009 MINSK, 2010 2 This publication has been prepared by the Banking Supervision Directorate in concert with the

ABLV High Yield CIS Bond Fund Prospectus

ABLV High Yield CIS Bond Fund Prospectus Open-end mutual fund Registered in Latvia, with the Financial and Capital Market Commission: Fund registration date: 15.06.2007 Fund registration No.: 06.03.05.263/34

ABLV High Yield CIS Bond Fund Prospectus Open-end mutual fund Registered in Latvia, with the Financial and Capital Market Commission: Fund registration date: 15.06.2007 Fund registration No.: 06.03.05.263/34

LAW OF THE REPUBLIC OF ARMENIA ON BANKRUPTCY OF BANKS, CREDIT ORGANISATIONS, INVESTMENT COMPANIES, INVESTMENT FUND MANAGERS AND INSURANCE COMPANIES

LAW OF THE REPUBLIC OF ARMENIA Adopted on 6 November 2001 ON BANKRUPTCY OF BANKS, CREDIT ORGANISATIONS, INVESTMENT COMPANIES, INVESTMENT FUND MANAGERS AND INSURANCE COMPANIES (Title supplemented by HO-368-N

LAW OF THE REPUBLIC OF ARMENIA Adopted on 6 November 2001 ON BANKRUPTCY OF BANKS, CREDIT ORGANISATIONS, INVESTMENT COMPANIES, INVESTMENT FUND MANAGERS AND INSURANCE COMPANIES (Title supplemented by HO-368-N

BUDGET SYSTEM LAW. / Official Gazette of the Republic of Serbia No. 9, 26 February 2002/ I. GENERAL PROVISIONS. Article 1

BUDGET SYSTEM LAW / Official Gazette of the Republic of Serbia No. 9, 26 February 2002/ I. GENERAL PROVISIONS Content and Scope of the Law Article 1 This Law shall regulate the planning, preparation and

BUDGET SYSTEM LAW / Official Gazette of the Republic of Serbia No. 9, 26 February 2002/ I. GENERAL PROVISIONS Content and Scope of the Law Article 1 This Law shall regulate the planning, preparation and

ON BANK FOR DEVELOPMENT

RUSSIAN FEDERATION FEDERAL LAW ON BANK FOR DEVELOPMENT as of May 17, 2007. No. 82-FZ Passed by the State Duma April 20, 2007 Approved by the Federation Council May 4, 2007 (as amended by Federal Laws Nos.

RUSSIAN FEDERATION FEDERAL LAW ON BANK FOR DEVELOPMENT as of May 17, 2007. No. 82-FZ Passed by the State Duma April 20, 2007 Approved by the Federation Council May 4, 2007 (as amended by Federal Laws Nos.

Adopted by the State Duma on July 7, 1995 Endorsed by the Council of the Federation on July 21, Federal Law on Banks and Banking Activities

FEDERAL LAW NO. 17-FZ OF FEBRUARY 3, 1996 ON INTRODUCING THE AMENDMENTS AND ADDENDA TO THE LAW OF THE RSFSR ON BANKS AND BANKING ACTIVITIES IN THE RSFSR (with the Amendments and Additions of July 31, 1998,

FEDERAL LAW NO. 17-FZ OF FEBRUARY 3, 1996 ON INTRODUCING THE AMENDMENTS AND ADDENDA TO THE LAW OF THE RSFSR ON BANKS AND BANKING ACTIVITIES IN THE RSFSR (with the Amendments and Additions of July 31, 1998,

Russia Takeover Guide

Russia Takeover Guide Contact Vassily Rudomino VRudomino@alrud.com Contents Page INTRODUCTION 1 THE REGULATION OF TAKEOVERS 1 ORDINARY AND PRIVELLEGED SHARES, CONVERTIBLE SECURITIES 1 ACQUISITION OF MORE

Russia Takeover Guide Contact Vassily Rudomino VRudomino@alrud.com Contents Page INTRODUCTION 1 THE REGULATION OF TAKEOVERS 1 ORDINARY AND PRIVELLEGED SHARES, CONVERTIBLE SECURITIES 1 ACQUISITION OF MORE

Budget and tax problems and central banks: Russia s experiences

Budget and tax problems and central banks: Russia s experiences Oleg Vyugin 1 1. Medium-term budget and tax positions of emerging market economies The most widely used indicator of the position of the

Budget and tax problems and central banks: Russia s experiences Oleg Vyugin 1 1. Medium-term budget and tax positions of emerging market economies The most widely used indicator of the position of the

Belarus: Brief review of the key amendments to the Tax Code 2019 August 2018

Belarus: Brief review of the key amendments to the Tax Code 2019 EY started its activities in Belarus in 1994 and we opened our Minsk office in 2000. Ernst & Young Legal Services LLC provides legal services

Belarus: Brief review of the key amendments to the Tax Code 2019 EY started its activities in Belarus in 1994 and we opened our Minsk office in 2000. Ernst & Young Legal Services LLC provides legal services

ANNEX I. Law of the Republic of Kazakhstan No. 57, June 13, 2005 On Currency Regulating and Currency Control

ANNEX I Law of the Republic of Kazakhstan No. 57, June 13, 2005 On Currency Regulating and Currency Control This Law shall regulate social relations arising when exercising the rights for currency values

ANNEX I Law of the Republic of Kazakhstan No. 57, June 13, 2005 On Currency Regulating and Currency Control This Law shall regulate social relations arising when exercising the rights for currency values

THE LAW OF THE KYRGYZ REPUBLIC. On the National Bank of the Kyrgyz Republic

Bishkek July 29, 1997, # 59 THE LAW OF THE KYRGYZ REPUBLIC On the National Bank of the Kyrgyz Republic Chapter I. General provisions Chapter II. Reporting by the Bank of Kyrgyzstan Chapter III. Capital

Bishkek July 29, 1997, # 59 THE LAW OF THE KYRGYZ REPUBLIC On the National Bank of the Kyrgyz Republic Chapter I. General provisions Chapter II. Reporting by the Bank of Kyrgyzstan Chapter III. Capital

NOTE: THIS TRANSLATION IS INFORMATIVE, I.E. NOT LEGALLY BINDING! 189/2004 Coll. ACT

NOTE: THIS TRANSLATION IS INFORMATIVE, I.E. NOT LEGALLY BINDING! 189/2004 Coll. ACT of 1 April 2004 on collective investment Amendment: 377/2005 Coll. Amendment: 57/2006 Coll., 70/2006 Coll. Amendment:

NOTE: THIS TRANSLATION IS INFORMATIVE, I.E. NOT LEGALLY BINDING! 189/2004 Coll. ACT of 1 April 2004 on collective investment Amendment: 377/2005 Coll. Amendment: 57/2006 Coll., 70/2006 Coll. Amendment:

General Information on the Russian Banking Sector. Banking sector in the economy of Russia

Summary Methodology to "Review of the Banking Sector of the Russian Federation" * (18 th Issue ) (Internet - version) Comments refer to the data of Review of the Banking Sector of the Russian Federation

Summary Methodology to "Review of the Banking Sector of the Russian Federation" * (18 th Issue ) (Internet - version) Comments refer to the data of Review of the Banking Sector of the Russian Federation

Federal Law No. 65-FZ of April 26, 1995 reworded the present Law

Federal Law No. 65-FZ of April 26, 1995 reworded the present Law FEDERAL LAW NO. 394-1 OF DECEMBER 2, 1990 ON THE CENTRAL BANK OF THE RUSSIAN FEDERATION (THE BANK OF RUSSIA) (with the Amendments of December

Federal Law No. 65-FZ of April 26, 1995 reworded the present Law FEDERAL LAW NO. 394-1 OF DECEMBER 2, 1990 ON THE CENTRAL BANK OF THE RUSSIAN FEDERATION (THE BANK OF RUSSIA) (with the Amendments of December

CHARTER OF ING BANK ŚLĄSKI SPÓŁKA AKCYJNA. 1. The business name of the Bank shall be: ING Bank Śląski Spółka Akcyjna.

CHARTER OF ING BANK ŚLĄSKI SPÓŁKA AKCYJNA Consolidated Text As adopted by way of the ING Bank Śląski S.A. Supervisory Board Resolution No. 58/XII/2015 of 17 September 2015, recorded under Rep. A No. 1023/2015,

CHARTER OF ING BANK ŚLĄSKI SPÓŁKA AKCYJNA Consolidated Text As adopted by way of the ING Bank Śląski S.A. Supervisory Board Resolution No. 58/XII/2015 of 17 September 2015, recorded under Rep. A No. 1023/2015,

NEW STATE PROGRAM ON PROJECT FINANCING IN RUSSIA

NEW STATE PROGRAM ON PROJECT FINANCING IN RUSSIA www.gratanet.com The Government of the Russian Federation by its resolution No. 158 of 15 February 2018 approved: the Project Finance Factory program which

NEW STATE PROGRAM ON PROJECT FINANCING IN RUSSIA www.gratanet.com The Government of the Russian Federation by its resolution No. 158 of 15 February 2018 approved: the Project Finance Factory program which

Ukraine Annual Report 2 Annual Report

Ukraine Annual Report 2012 2 ANNUAL REPORT 2012 FINANCIAL STATEMENTS 3 Financial Statements Public Joint Stock Company ProCredit Bank Financial Statements Year ended 31 December 2012 Together with Independent

Ukraine Annual Report 2012 2 ANNUAL REPORT 2012 FINANCIAL STATEMENTS 3 Financial Statements Public Joint Stock Company ProCredit Bank Financial Statements Year ended 31 December 2012 Together with Independent

Summary Methodology to "Review of the Banking Sector of the Russian Federation" * (16 th Issue ) (Internet - version)

(Internet - version)") Summary Methodology to "Review of the Banking Sector of the Russian Federation" * (16 th Issue ) (Internet - version) Comments refer to the data of Review of the Banking Sector of the Russian Federation

Summary Methodology to "Review of the Banking Sector of the Russian Federation" * (16 th Issue ) (Internet - version) Comments refer to the data of Review of the Banking Sector of the Russian Federation

Bank of Moscow (Open Joint Stock Company) Consolidated financial statements. for the year ended 31 December 2011 and Independent auditors report

Consolidated financial statements. for the year ended 31 December 2011 and Independent auditors report") Bank of Moscow (Open Joint Stock Company) Consolidated financial statements for the year ended 31 December 2011 and Independent auditors report Consolidated financial statements for the year ended 31 December

Bank of Moscow (Open Joint Stock Company) Consolidated financial statements for the year ended 31 December 2011 and Independent auditors report Consolidated financial statements for the year ended 31 December

THE LAW ON BUDGET AND FINANCE MANAGEMENT

Passed 24.03.1994 In force Published in Vestnesis 06.04.94 22.07.99.M.G. THE LAW ON BUDGET AND FINANCE MANAGEMENT =================================================== Published in Zinotajs N0.6, 28.04.94

Passed 24.03.1994 In force Published in Vestnesis 06.04.94 22.07.99.M.G. THE LAW ON BUDGET AND FINANCE MANAGEMENT =================================================== Published in Zinotajs N0.6, 28.04.94

FEDERAL LAW On the Central Bank of the Russian Federation (Bank of Russia)

") RUSSIAN FEDERATION FEDERAL LAW On the Central Bank of the Russian Federation (Bank of Russia) (as amended by Federal Laws No. 5-FZ, dated 10 January 2003; No. 180-FZ, dated 23 December 2003; No. 58-FZ,

RUSSIAN FEDERATION FEDERAL LAW On the Central Bank of the Russian Federation (Bank of Russia) (as amended by Federal Laws No. 5-FZ, dated 10 January 2003; No. 180-FZ, dated 23 December 2003; No. 58-FZ,

JESSICA JOINT EUROPEAN SUPPORT FOR SUSTAINABLE INVESTMENT IN CITY AREAS JESSICA INSTRUMENTS FOR ENERGY EFFICIENCY IN LITHUANIA FINAL REPORT

JESSICA JOINT EUROPEAN SUPPORT FOR SUSTAINABLE INVESTMENT IN CITY AREAS JESSICA INSTRUMENTS FOR ENERGY EFFICIENCY IN LITHUANIA FINAL REPORT 17 April 2009 This document has been produced with the financial

JESSICA JOINT EUROPEAN SUPPORT FOR SUSTAINABLE INVESTMENT IN CITY AREAS JESSICA INSTRUMENTS FOR ENERGY EFFICIENCY IN LITHUANIA FINAL REPORT 17 April 2009 This document has been produced with the financial

REPUBLIC OF SLOVENIA PUBLIC FINANCE ACT

REPUBLIC OF SLOVENIA PUBLIC FINANCE ACT - Official Gazette of RS No. 79/1999 LJUBLJANA, 30. SEPTEMBER 1999 1. GENERAL PROVISIONS - 1- Article 1 (Contents and Scope of the Act) (1) This Act shall regulate

REPUBLIC OF SLOVENIA PUBLIC FINANCE ACT - Official Gazette of RS No. 79/1999 LJUBLJANA, 30. SEPTEMBER 1999 1. GENERAL PROVISIONS - 1- Article 1 (Contents and Scope of the Act) (1) This Act shall regulate

LITHUANIA THE LAW ON COLLECTIVE INVESTMENT UNDERTAKINGS

LITHUANIA THE LAW ON COLLECTIVE INVESTMENT UNDERTAKINGS Important Disclaimer This translation has been generously provided by the Securities Commission of the Republic of Lithuania. This does not constitute

LITHUANIA THE LAW ON COLLECTIVE INVESTMENT UNDERTAKINGS Important Disclaimer This translation has been generously provided by the Securities Commission of the Republic of Lithuania. This does not constitute

IOPS Member country or territory pension system profile: ARMENIA. Report issued on April 2012, validated by the Central Bank of Armenia

IOPS Member country or territory pension system profile: ARMENIA Report issued on April 2012, validated by the Central Bank of Armenia ARMENIA DEMOGRAPHICS AND MACROECONOMICS Total Population (000s) 3.1

IOPS Member country or territory pension system profile: ARMENIA Report issued on April 2012, validated by the Central Bank of Armenia ARMENIA DEMOGRAPHICS AND MACROECONOMICS Total Population (000s) 3.1

THE LAW OF THE REPUBLIC OF TAJIKISTAN ON BANKS AND BANKING ACTIVITIES CHAPTER 1. GENERAL REGULATIONS

THE LAW OF THE REPUBLIC OF TAJIKISTAN ON BANKS AND BANKING ACTIVITIES Article 1. Concepts of a Bank CHAPTER 1. GENERAL REGULATIONS A bank in the Republic of Tajikistan is an institution, created for attracting

THE LAW OF THE REPUBLIC OF TAJIKISTAN ON BANKS AND BANKING ACTIVITIES Article 1. Concepts of a Bank CHAPTER 1. GENERAL REGULATIONS A bank in the Republic of Tajikistan is an institution, created for attracting

Deposit Guarantee Schemes Frequently Asked Questions

EUROPEAN COMMISSION MEMO Brussels, 15 April 2014 Deposit Guarantee Schemes Frequently Asked Questions Why was the revision of the Directive on Deposit Guarantee Schemes necessary? The original Directive

EUROPEAN COMMISSION MEMO Brussels, 15 April 2014 Deposit Guarantee Schemes Frequently Asked Questions Why was the revision of the Directive on Deposit Guarantee Schemes necessary? The original Directive

amended from time to time concerning the definition of micro, small and medium-sized enterprises

Financial Instrument Envisaged state aid regime Investment focus Investment range Eligible Investees Venture Capital Fund(s) Envisaged to be Article 21 of the General Block Exemption Regulation 1 (GBER)

Financial Instrument Envisaged state aid regime Investment focus Investment range Eligible Investees Venture Capital Fund(s) Envisaged to be Article 21 of the General Block Exemption Regulation 1 (GBER)

OF HOUSEHOLDS COUNTERCYCLICAL CAPITAL BUFFER. June BACKGROUND MATERIAL FOR DECISION

REVIEW OF THE SURVEY OF THE FINANCIAL BEHAVIOUR COUNTERCYCLICAL CAPITAL BUFFER BACKGROUND MATERIAL FOR DECISION 13 17 OF HOUSEHOLDS Q1 June 13 Abbreviations ISSN 2424-371 CCB ECB EEA ESRB GDP MFI RE countercyclical

REVIEW OF THE SURVEY OF THE FINANCIAL BEHAVIOUR COUNTERCYCLICAL CAPITAL BUFFER BACKGROUND MATERIAL FOR DECISION 13 17 OF HOUSEHOLDS Q1 June 13 Abbreviations ISSN 2424-371 CCB ECB EEA ESRB GDP MFI RE countercyclical

FEDERAL LAW On the Central Bank of the Russian Federation (Bank of Russia)

") RUSSIAN FEDERATION FEDERAL LAW On the Central Bank of the Russian Federation (Bank of Russia) (as amended by Federal Laws No. 5-FZ of January 10, 2003; No. 180-FZ of December 23, 2003; No. 58-FZ of June

RUSSIAN FEDERATION FEDERAL LAW On the Central Bank of the Russian Federation (Bank of Russia) (as amended by Federal Laws No. 5-FZ of January 10, 2003; No. 180-FZ of December 23, 2003; No. 58-FZ of June

Bank finance and regulation. Multi-jurisdictional survey. Belarus. Enforcement of security interests in banking transactions

Bank finance and regulation Multi-jurisdictional survey Belarus Enforcement of security interests in banking transactions Anna Rusetskaya and Natallia Kaliuta Magisters, Minsk arusetskaya@magisters.com/nkaliuta@magisters.com

Bank finance and regulation Multi-jurisdictional survey Belarus Enforcement of security interests in banking transactions Anna Rusetskaya and Natallia Kaliuta Magisters, Minsk arusetskaya@magisters.com/nkaliuta@magisters.com

ACBA CREDIT-AGRICOLE BANK CJSC OPERATIONAL TARIFFS (LENDING OPERATIONS)

") ACBA CREDIT-AGRICOLE BANK CJSC OPERATIONAL TARIFFS (LENDING OPERATIONS) Valid from August 16, 2018 1. This document shall establish the interest s of the loans provided to the clients by ACBA-CREDIT AGRICOLE

ACBA CREDIT-AGRICOLE BANK CJSC OPERATIONAL TARIFFS (LENDING OPERATIONS) Valid from August 16, 2018 1. This document shall establish the interest s of the loans provided to the clients by ACBA-CREDIT AGRICOLE

ON CURRENCY REGULATION AND CURRENCY CONTROL Law of the Republic of Kazakhstan No. 57, June 13, 2005

ON CURRENCY REGULATION AND CURRENCY CONTROL Law of the Republic of Kazakhstan No. 57, June 13, 2005 This Law regulates social relations arising upon exercise the rights to currency valuables by residents

ON CURRENCY REGULATION AND CURRENCY CONTROL Law of the Republic of Kazakhstan No. 57, June 13, 2005 This Law regulates social relations arising upon exercise the rights to currency valuables by residents

Chapter I. General Provisions

Federal Law No. 76-FZ of June 23, 2003 amended the present Federal Law. The amendments shall enter into force from January 1, 2004 See text of the Federal Law in the previous wording FEDERAL LAW ON THE

Federal Law No. 76-FZ of June 23, 2003 amended the present Federal Law. The amendments shall enter into force from January 1, 2004 See text of the Federal Law in the previous wording FEDERAL LAW ON THE

Capital split between compartments

Financial Instrument Capital split between compartments Accelerator & Seed Capital Fund(s) The Acceleration compartment (or window ) provides initial financing to emerging entrepreneurs to research, assess

Financial Instrument Capital split between compartments Accelerator & Seed Capital Fund(s) The Acceleration compartment (or window ) provides initial financing to emerging entrepreneurs to research, assess

RESPONSIBLE LENDING REGULATIONS CHAPTER I GENERAL PROVISIONS

APPROVED by Resolution No 03-144 of the Board of the Bank of Lithuania of 1 September 2011 (as amended by Resolution No 03-90 of the Board of the Bank of Lithuania of 28 May 2015) In case of inconsistencies

APPROVED by Resolution No 03-144 of the Board of the Bank of Lithuania of 1 September 2011 (as amended by Resolution No 03-90 of the Board of the Bank of Lithuania of 28 May 2015) In case of inconsistencies

Covered Bond Act (688/2010) In accordance with the decision of the Parliament the following is enacted:

In accordance with the decision of the Parliament the following is enacted:") UNOFFICIAL TRANSLATION Covered Bond Act (688/2010) In accordance with the decision of the Parliament the following is enacted: Chapter 1 Section 1 General provisions Scope of application This Act provides

UNOFFICIAL TRANSLATION Covered Bond Act (688/2010) In accordance with the decision of the Parliament the following is enacted: Chapter 1 Section 1 General provisions Scope of application This Act provides

Consolidated Condensed Interim Financial Statements and Report on Review

Consolidated Condensed Interim Financial Statements and Report on Review CONTENTS Report on Review Consolidated Condensed Interim Financial Statements Consolidated Condensed Interim Statement of Financial

Consolidated Condensed Interim Financial Statements and Report on Review CONTENTS Report on Review Consolidated Condensed Interim Financial Statements Consolidated Condensed Interim Statement of Financial

THE CENTRAL BANK OF THE REPUBLIC OF ARMENIA BOARD RESOLUTION No. 39

THE CENTRAL BANK OF THE REPUBLIC OF ARMENIA BOARD RESOLUTION No. 39 Adopted on February 9, 2007 ON APPROVAL OF REGULATION 2 ON REGULATION OF BANKING, PRUDENTIAL STANDARDS FOR BANKING This Regulation includes

THE CENTRAL BANK OF THE REPUBLIC OF ARMENIA BOARD RESOLUTION No. 39 Adopted on February 9, 2007 ON APPROVAL OF REGULATION 2 ON REGULATION OF BANKING, PRUDENTIAL STANDARDS FOR BANKING This Regulation includes

UZBEKISTAN LAW ON SECURITIES AND STOCK EXCHANGE

UZBEKISTAN LAW ON SECURITIES AND STOCK EXCHANGE Important Disclaimer This does not constitute an official translation and the translator and the EBRD cannot be held responsible for any inaccuracy or omission

UZBEKISTAN LAW ON SECURITIES AND STOCK EXCHANGE Important Disclaimer This does not constitute an official translation and the translator and the EBRD cannot be held responsible for any inaccuracy or omission

CORPORATE CHARTER POWSZECHNA KASA OSZCZĘDNOŚCI BANK POLSKI SPÓŁKA AKCYJNA

CORPORATE CHARTER POWSZECHNA KASA OSZCZĘDNOŚCI BANK POLSKI SPÓŁKA AKCYJNA I. General provisions 1 1. Powszechna Kasa Oszczędności Bank Polski Spółka Akcyjna, hereinafter referred to as the Bank, is a bank

CORPORATE CHARTER POWSZECHNA KASA OSZCZĘDNOŚCI BANK POLSKI SPÓŁKA AKCYJNA I. General provisions 1 1. Powszechna Kasa Oszczędności Bank Polski Spółka Akcyjna, hereinafter referred to as the Bank, is a bank

ABLV Bank, AS in Liquidation

ABLV Bank, AS in Liquidation Registration No.: 50003149401 Legal address: Website: 23 Elizabetes Street, Riga, Latvia www.ablv.com Phone: + 371 6777 5222 Final Terms of Offer of the Third Bond Issue Series

ABLV Bank, AS in Liquidation Registration No.: 50003149401 Legal address: Website: 23 Elizabetes Street, Riga, Latvia www.ablv.com Phone: + 371 6777 5222 Final Terms of Offer of the Third Bond Issue Series

Below we provide a comparative outline of the principal changes related to: 5

THIRD ANTIMONOPOLY PACKAGE IN RUSSIA March 19, 2012 To Our Clients and Friends: In January, Federal Law No. 401-FZ on Amendments to the Federal Law on Protection of Competition 1 and Certain Legislative

THIRD ANTIMONOPOLY PACKAGE IN RUSSIA March 19, 2012 To Our Clients and Friends: In January, Federal Law No. 401-FZ on Amendments to the Federal Law on Protection of Competition 1 and Certain Legislative

Guidelines May Banking & Finance Kyiv. General provisions on lending. Parties to the loan agreement. Applicable law and jurisdiction

Banking & Finance Kyiv Guidelines May 2017 In This Issue: Cross-border financing in Ukraine - General provisions on lending - Loan registration - Licensing requirements and approvals - Payment restrictions

Banking & Finance Kyiv Guidelines May 2017 In This Issue: Cross-border financing in Ukraine - General provisions on lending - Loan registration - Licensing requirements and approvals - Payment restrictions

THE BANKING ACT 1) of August 29, A unified text CHAPTER 1 GENERAL PROVISIONS

of August 29, A unified text CHAPTER 1 GENERAL PROVISIONS") THE BANKING ACT 1) of August 29, 1997 A unified text drawn up on the basis of Journal of Laws (Dziennik Ustaw Dz.U.) 2002 No. 72, item 665; No. 126, item 1070; No. 141, item 1178; No. 144, item 1208; No.

THE BANKING ACT 1) of August 29, 1997 A unified text drawn up on the basis of Journal of Laws (Dziennik Ustaw Dz.U.) 2002 No. 72, item 665; No. 126, item 1070; No. 141, item 1178; No. 144, item 1208; No.

BERMUDA MONETARY AUTHORITY

BERMUDA MONETARY AUTHORITY CONSULTATION PAPER SECURING ENHANCED PROTECTION FOR DEPOSITORS PROPOSALS FOR INTRODUCING DEPOSIT INSURANCE IN BERMUDA SEPTEMBER 2010 Table of Contents 0. INTRODUCTION... 3 1.

BERMUDA MONETARY AUTHORITY CONSULTATION PAPER SECURING ENHANCED PROTECTION FOR DEPOSITORS PROPOSALS FOR INTRODUCING DEPOSIT INSURANCE IN BERMUDA SEPTEMBER 2010 Table of Contents 0. INTRODUCTION... 3 1.

Insurance services in Sweden

Insurance services in UTLÄNDSKA FÖRSÄKRINGSBOLAGS FÖRENING Insurance services in June 2010 Vinge is one of the leading law firms in Scandinavia, offering a full range of commercial legal services. Our

Insurance services in UTLÄNDSKA FÖRSÄKRINGSBOLAGS FÖRENING Insurance services in June 2010 Vinge is one of the leading law firms in Scandinavia, offering a full range of commercial legal services. Our

1 DIRECTIVE 2013/36/EU OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 26 June 2013 on access to the

Methodology underlying the determination of the benchmark countercyclical capital buffer rate and supplementary indicators signalling the build-up of cyclical systemic financial risk The application of

Methodology underlying the determination of the benchmark countercyclical capital buffer rate and supplementary indicators signalling the build-up of cyclical systemic financial risk The application of

Official Journal of the European Union

L 63/22 28.2.2004 COMMISSION REGULATION (EC) No 364/2004 of 25 February 2004 amending Regulation (EC) No 70/2001 as regards the extension of its scope to include aid for research and development THE COMMISSION

L 63/22 28.2.2004 COMMISSION REGULATION (EC) No 364/2004 of 25 February 2004 amending Regulation (EC) No 70/2001 as regards the extension of its scope to include aid for research and development THE COMMISSION

ACT ON BANKS. The National Council of the Slovak Republic has adopted this Act: SECTION I PART ONE BASIC PROVISIONS. Article 1

ACT ON BANKS The full wording of Act No. 483/2001 Coll. dated 5 October 2001 on banks and on changes and the amendment of certain acts, as amended by Act No. 430/2002 Coll., Act No. 510/2002 Coll., Act

ACT ON BANKS The full wording of Act No. 483/2001 Coll. dated 5 October 2001 on banks and on changes and the amendment of certain acts, as amended by Act No. 430/2002 Coll., Act No. 510/2002 Coll., Act

Cyprus Financial Assistance Programme Memoranda signed with the EU and the International Monetary Fund: Q&A regarding the financial sector

Cyprus Financial Assistance Programme Memoranda signed with the EU and the International Monetary Fund: Q&A regarding the financial sector Part A: Key policy questions Q1: What were the reasons that Cyprus

Cyprus Financial Assistance Programme Memoranda signed with the EU and the International Monetary Fund: Q&A regarding the financial sector Part A: Key policy questions Q1: What were the reasons that Cyprus

SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness. General Provisions

GOVERNMENT No. -2006-ND-CP Draft 1653 SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness Hanoi, [ ] 2006 DECREE PROVIDING GUIDELINES FOR IMPLEMENTATION OF LAW ON INVESTMENT Pursuant to the

GOVERNMENT No. -2006-ND-CP Draft 1653 SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness Hanoi, [ ] 2006 DECREE PROVIDING GUIDELINES FOR IMPLEMENTATION OF LAW ON INVESTMENT Pursuant to the

RIETUMU BANKA AS. Condensed Interim Bank Separate and Group Consolidated Financial Statements For the six month period ended 30 June 2016

RIETUMU BANKA AS Condensed Interim Bank Separate and Group Consolidated Financial Statements For the six month period ended Contents Report of Council and Board of Directors 3 Independent auditors Report

RIETUMU BANKA AS Condensed Interim Bank Separate and Group Consolidated Financial Statements For the six month period ended Contents Report of Council and Board of Directors 3 Independent auditors Report

ARTICLES OF ASSOCIATION OF GETIN HOLDING SPÓŁKA AKCYJNA

ARTICLES OF ASSOCIATION OF GETIN HOLDING SPÓŁKA AKCYJNA Uniform text of Articles of Association of Getin Holding Spółka Akcyjna, drawn up on 14.02.1996, including amendments adopted by Company s General

ARTICLES OF ASSOCIATION OF GETIN HOLDING SPÓŁKA AKCYJNA Uniform text of Articles of Association of Getin Holding Spółka Akcyjna, drawn up on 14.02.1996, including amendments adopted by Company s General

THE REPUBLIC OF ARMENIA LAW ON INVESTMENT FUNDS. Adopted on 22 December 2010 SECTION 1 GENERAL PROVISIONS CHAPTER 1 GENERAL PROVISIONS

THE REPUBLIC OF ARMENIA LAW ON INVESTMENT FUNDS Adopted on 22 December 2010 The purpose of this law is the protection of investors rights, the development of a pooled investments system, the adoption of

THE REPUBLIC OF ARMENIA LAW ON INVESTMENT FUNDS Adopted on 22 December 2010 The purpose of this law is the protection of investors rights, the development of a pooled investments system, the adoption of

Adopted by the State Duma on June 25, 1999 Approved by the Federation Council on July 2, 1999

FEDERAL LAW NO. 160-FZ OF JULY 9, 1999 ON FOREIGN INVESTMENT IN THE RUSSIAN FEDERATION (with the Amendments and Additions of July 25, 2002, December 8, 2003, July 22, 2005, June 3, 2006, June 26, 2007,

FEDERAL LAW NO. 160-FZ OF JULY 9, 1999 ON FOREIGN INVESTMENT IN THE RUSSIAN FEDERATION (with the Amendments and Additions of July 25, 2002, December 8, 2003, July 22, 2005, June 3, 2006, June 26, 2007,

Ukraine Economic Growth and Financial Infrastructure. Michael Bleyzer March 2005 v10

Ukraine Economic Growth and Financial Infrastructure Michael Bleyzer March 2005 v10 1 UKRAINE: Economic Highlights Few non-oil producing countries in the world can show the following combination of economic

Ukraine Economic Growth and Financial Infrastructure Michael Bleyzer March 2005 v10 1 UKRAINE: Economic Highlights Few non-oil producing countries in the world can show the following combination of economic

7. Monetary Trends and Policy

Quarterly Monitor No. 36 January March 214 47 7. Monetary and Policy Inflation has been stable for the past two quarters at about the lower level of the target corridor but the National Bank of Serbia

Quarterly Monitor No. 36 January March 214 47 7. Monetary and Policy Inflation has been stable for the past two quarters at about the lower level of the target corridor but the National Bank of Serbia

89 Government of the Kyrgyz Republic (2007) National. 90 International Finance Corporation (IFC) (2006), Central

National. 90 International Finance Corporation (IFC) (2006), Central") A. HOUSING DEMAND AND AVAILABILITY OF HOUSING FINANCE Private investment in housing production has been constantly increasing over recent years with a 5.1 billion soms (98% of total investment) peak in

A. HOUSING DEMAND AND AVAILABILITY OF HOUSING FINANCE Private investment in housing production has been constantly increasing over recent years with a 5.1 billion soms (98% of total investment) peak in

T H E D E P O S I T G U A R A N T E E S C H E M E A C T ( T H E Z S J V ) 1. GENERAL PROVISIONS. Article 1 (Subject matter of the Act)

1. GENERAL PROVISIONS. Article 1 (Subject matter of the Act)") LEGAL NOTICE All effort has been made to ensure the accuracy of the translation, which is based on the original Slovenian texts. All translations of this kind may, nevertheless, be subject to a certain

LEGAL NOTICE All effort has been made to ensure the accuracy of the translation, which is based on the original Slovenian texts. All translations of this kind may, nevertheless, be subject to a certain

Bank finance and regulation. Multi-jurisdictional survey. Latvia. Enforcement of security interests in banking transactions

Bank finance and regulation Multi-jurisdictional survey Latvia Enforcement of security interests in banking transactions Part I types of security Edgars Lodzins and Liene Krumina Borenius, Riga Edgars.Lodzins@borenius.lv/Liene.Krumina@borenius.lv

Bank finance and regulation Multi-jurisdictional survey Latvia Enforcement of security interests in banking transactions Part I types of security Edgars Lodzins and Liene Krumina Borenius, Riga Edgars.Lodzins@borenius.lv/Liene.Krumina@borenius.lv

Official Journal of the European Union DECISIONS

6.7.2018 L 171/11 DECISIONS DECISION (EU) 2018/947 OF THE EUROPEAN PARLIAMT AND OF THE COUNCIL of 4 July 2018 providing further macro-financial assistance to Ukraine THE EUROPEAN PARLIAMT AND THE COUNCIL

6.7.2018 L 171/11 DECISIONS DECISION (EU) 2018/947 OF THE EUROPEAN PARLIAMT AND OF THE COUNCIL of 4 July 2018 providing further macro-financial assistance to Ukraine THE EUROPEAN PARLIAMT AND THE COUNCIL

ASIFMA and SIFMA believe that the high-level concerns of financial services firms, including their own members, with the Draft Measures include:

6 April 2018 Institutional Department China Securities Regulatory Commission Fukai Building 19 Jinrong Avenue, Xicheng District Beijing, China 100033 On behalf of its members, the Asia Securities Industry

6 April 2018 Institutional Department China Securities Regulatory Commission Fukai Building 19 Jinrong Avenue, Xicheng District Beijing, China 100033 On behalf of its members, the Asia Securities Industry

Monetary policy operating procedures: the Peruvian case

Monetary policy operating procedures: the Peruvian case Marylin Choy Chong 1. Background (i) Reforms At the end of 1990 Peru initiated a financial reform process as part of a broad set of structural reforms

Monetary policy operating procedures: the Peruvian case Marylin Choy Chong 1. Background (i) Reforms At the end of 1990 Peru initiated a financial reform process as part of a broad set of structural reforms

Citadele Eastern European Fixed Income Funds FUND RULES

2A Republikas laukums, Riga, LV-1010, Latvia Open-end Investment Fund FUND RULES The Fund is registered in the Republic of Latvia Registered with the Financial and Capital Market Commission: The Fund was

2A Republikas laukums, Riga, LV-1010, Latvia Open-end Investment Fund FUND RULES The Fund is registered in the Republic of Latvia Registered with the Financial and Capital Market Commission: The Fund was

Bank Finance and Regulation Survey. CYPRUS Dr. K. Chrysostomides & Co LLC

Bank Finance and Regulation Survey CYPRUS Dr. K. Chrysostomides & Co LLC CONTACT INFORMATION Chryso Dekatris and Pavlos Symeonides Dr. K. Chrysostomides & Co LLC 1, Lampousas Street 1095, Nicosia, Cyprus

Bank Finance and Regulation Survey CYPRUS Dr. K. Chrysostomides & Co LLC CONTACT INFORMATION Chryso Dekatris and Pavlos Symeonides Dr. K. Chrysostomides & Co LLC 1, Lampousas Street 1095, Nicosia, Cyprus

ARTICLES OF ASSOCIATION OF GETIN HOLDING Spółka Akcyjna

ARTICLES OF ASSOCIATION OF GETIN HOLDING Spółka Akcyjna Uniform text of Articles of Association of Getin Holding Spółka Akcyjna drawn up on 14.02.1996, including amendments adopted by the Company s General

ARTICLES OF ASSOCIATION OF GETIN HOLDING Spółka Akcyjna Uniform text of Articles of Association of Getin Holding Spółka Akcyjna drawn up on 14.02.1996, including amendments adopted by the Company s General

Chapter 3 BASEL III IMPLEMENTATION: CHALLENGES AND OPPORTUNITIES IN CAMBODIA. By Ban Lim 1

Chapter 3 BASEL III IMPLEMENTATION: CHALLENGES AND OPPORTUNITIES IN CAMBODIA By Ban Lim 1 1. Introduction 1.1 Objective and Scope of Study The Basel Agreement of 1993 explicitly incorporated the different

Chapter 3 BASEL III IMPLEMENTATION: CHALLENGES AND OPPORTUNITIES IN CAMBODIA By Ban Lim 1 1. Introduction 1.1 Objective and Scope of Study The Basel Agreement of 1993 explicitly incorporated the different

Business Environment: Russia

Business Environment: Russia Euromonitor International 13 April 2010 Despite the economic recession of 2009, a recovery is expected in 2010. The business environment remains challenging due to over-regulation,

Business Environment: Russia Euromonitor International 13 April 2010 Despite the economic recession of 2009, a recovery is expected in 2010. The business environment remains challenging due to over-regulation,

The Financial System and Banking Sector in Turkey

The Financial System and Banking Sector in Turkey October 2009, Istanbul Contents 1. Impacts of Recent Developments on the Turkish Economy and the Sector 1.1. Economic Performance 1.2. Measures adopted

The Financial System and Banking Sector in Turkey October 2009, Istanbul Contents 1. Impacts of Recent Developments on the Turkish Economy and the Sector 1.1. Economic Performance 1.2. Measures adopted

CHARTER OF THE EASTERN AND SOUTHERN AFRICAN TRADE AND DEVELOPMENT BANK

CHARTER OF THE EASTERN AND SOUTHERN AFRICAN TRADE AND DEVELOPMENT BANK CONTENTS ARTICLE PAGE Preamble 1 1. Definition 2 2. Establishment of the Bank 3 3. Membership of the Bank 4 4. Objectives of the Bank

CHARTER OF THE EASTERN AND SOUTHERN AFRICAN TRADE AND DEVELOPMENT BANK CONTENTS ARTICLE PAGE Preamble 1 1. Definition 2 2. Establishment of the Bank 3 3. Membership of the Bank 4 4. Objectives of the Bank

DIRECTIVES. DIRECTIVE 2014/49/EU OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 16 April 2014 on deposit guarantee schemes.

12.6.2014 Official Journal of the European Union L 173/149 DIRECTIVES DIRECTIVE 2014/49/EU OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 16 April 2014 on deposit guarantee schemes (recast) (Text with

12.6.2014 Official Journal of the European Union L 173/149 DIRECTIVES DIRECTIVE 2014/49/EU OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 16 April 2014 on deposit guarantee schemes (recast) (Text with

ABN AMRO Group reports second quarter and half year 2009 financial results

Amsterdam, 26 August ABN AMRO Group reports second quarter and half year financial results Second quarter update ABN AMRO Group has recorded a loss after tax of EUR 1,761 million for the second quarter

Amsterdam, 26 August ABN AMRO Group reports second quarter and half year financial results Second quarter update ABN AMRO Group has recorded a loss after tax of EUR 1,761 million for the second quarter

GRATA FINANCE & SECURITIES GROUP

GRATA FINANCE & SECURITIES GROUP LEGAL ALERT 1 (JANUARY MARCH 2012) In keeping with GRATA s practice of informing clients regarding important legal developments that might influence their business, we

GRATA FINANCE & SECURITIES GROUP LEGAL ALERT 1 (JANUARY MARCH 2012) In keeping with GRATA s practice of informing clients regarding important legal developments that might influence their business, we

ARTICLES. of the Joint-Stock Company STATE SAVINGS BANK OF UKRAINE

REGISTERED with the National Bank of Ukraine on February 28, 2003 Registration Number 4 Deputy Chairman of the National Bank of Ukraine [Signature] O.V. Shlapak [Impression of the official seal with inscription:

REGISTERED with the National Bank of Ukraine on February 28, 2003 Registration Number 4 Deputy Chairman of the National Bank of Ukraine [Signature] O.V. Shlapak [Impression of the official seal with inscription:

ARTICLES OF ASSOCIATION OF THE BANK HANDLOWY W WARSZAWIE S.A.

Uniform text of the Articles of Association of the Bank Handlowy w Warszawie S.A. edited by the Resolution of the Supervisory Board of November 14, 2015 with the amendments adopted by the Resolution No

Uniform text of the Articles of Association of the Bank Handlowy w Warszawie S.A. edited by the Resolution of the Supervisory Board of November 14, 2015 with the amendments adopted by the Resolution No

COMMISSION DELEGATED REGULATION (EU) /... of

/... of") EUROPEAN COMMISSION Brussels, 18.5.2016 C(2016) 2860 final COMMISSION DELEGATED REGULATION (EU) /... of 18.5.2016 supplementing Regulation (EU) No 600/2014 of the European Parliament and of the Council

EUROPEAN COMMISSION Brussels, 18.5.2016 C(2016) 2860 final COMMISSION DELEGATED REGULATION (EU) /... of 18.5.2016 supplementing Regulation (EU) No 600/2014 of the European Parliament and of the Council

CURRENT STATE OF THE BANKING SECTOR OF KAZAKHSTAN

1 The National Bank of the Republic of Kazakhstan CURRENT STATE OF THE BANKING SECTOR OF KAZAKHSTAN AS OF 1 JANUARY 2018 Almaty 2018 2 THE PURPOSE OF REVIEW CURRENT STATE OF THE BANKING SECTOR OF KAZAKHSTAN

1 The National Bank of the Republic of Kazakhstan CURRENT STATE OF THE BANKING SECTOR OF KAZAKHSTAN AS OF 1 JANUARY 2018 Almaty 2018 2 THE PURPOSE OF REVIEW CURRENT STATE OF THE BANKING SECTOR OF KAZAKHSTAN

Law of Georgia. On Insurance

The Consulting Firm Ltd. Law of Georgia On Insurance 19, Lermontov Str., Tbilisi, 380007 Phone: + 995 8832 93 20 76, 93 59 65 Fax: +995 (32) 001127 or +995 (32) 001077 E-mail: dikke@dikke.com.ge Law of

The Consulting Firm Ltd. Law of Georgia On Insurance 19, Lermontov Str., Tbilisi, 380007 Phone: + 995 8832 93 20 76, 93 59 65 Fax: +995 (32) 001127 or +995 (32) 001077 E-mail: dikke@dikke.com.ge Law of

ARTICLES OF ASSOCIATION OF SPECIAL CLOSED-END TYPE REAL ESTATE INVESTMENT COMPANY INVL BALTIC REAL ESTATE

ARTICLES OF ASSOCIATION OF SPECIAL CLOSED-END TYPE REAL ESTATE INVESTMENT COMPANY INVL BALTIC REAL ESTATE The Articles of Association were signed in Vilnius on [ ] [ ] [ ] Authorised person: [ ] [ ] 1

ARTICLES OF ASSOCIATION OF SPECIAL CLOSED-END TYPE REAL ESTATE INVESTMENT COMPANY INVL BALTIC REAL ESTATE The Articles of Association were signed in Vilnius on [ ] [ ] [ ] Authorised person: [ ] [ ] 1

Quarterly report containing the interim financial statements of the Group for Q3 of the financial year of

Quarterly report containing the interim financial statements of the Group for Q3 of the financial year of 2016-2017 covering the period from 01-07-2016 to 31-03-2017 Publication date: 16 May 2017 TABLE

Quarterly report containing the interim financial statements of the Group for Q3 of the financial year of 2016-2017 covering the period from 01-07-2016 to 31-03-2017 Publication date: 16 May 2017 TABLE

Guide to Islamic Finance in Russia

in Russia Part I: Infrastructure 2009 About the Guide 2 This Islamic Finance Guide in Russia is the result of research work by specialists of IFC Linova, corroborated in practice and expressed for the

in Russia Part I: Infrastructure 2009 About the Guide 2 This Islamic Finance Guide in Russia is the result of research work by specialists of IFC Linova, corroborated in practice and expressed for the

ANNUAL REPORT FOR 2009

K O M E R C I J A L N A B A N K A A D B U D VA ANNUAL REPORT 2009 Budva, April 2010 Budva, 30 April 2010 ANNUAL REPORT FOR 2009 In accordance with the Law on Banks, the Statute, the Bank s business policies,

K O M E R C I J A L N A B A N K A A D B U D VA ANNUAL REPORT 2009 Budva, April 2010 Budva, 30 April 2010 ANNUAL REPORT FOR 2009 In accordance with the Law on Banks, the Statute, the Bank s business policies,

LAW ON LOCAL PUBLIC FINANCE. The Parliament shall pass this organic law. CHAPTER I General Provisions

LAW ON LOCAL PUBLIC FINANCE The Parliament shall pass this organic law CHAPTER I General Provisions Article 1. Terms The following terms shall be used under this law: Local public finances - a component

LAW ON LOCAL PUBLIC FINANCE The Parliament shall pass this organic law CHAPTER I General Provisions Article 1. Terms The following terms shall be used under this law: Local public finances - a component

C. ENABLING REGULATION AND GENERAL BLOCK EXEMPTION REGULATION

C. ENABLING REGULATION AND GENERAL BLOCK EXEMPTION REGULATION 14. 5. 98 EN Official Journal of the European Communities L 142/1 I (Acts whose publication is obligatory) COUNCIL REGULATION (EC) No 994/98

C. ENABLING REGULATION AND GENERAL BLOCK EXEMPTION REGULATION 14. 5. 98 EN Official Journal of the European Communities L 142/1 I (Acts whose publication is obligatory) COUNCIL REGULATION (EC) No 994/98

AGE Platform Europe contribution to the Draft Report on an Adequate, Safe and Sustainable pensions (2012/2234(INI)) Rapporteur: Ria OOMEN-RUIJTEN

) Rapporteur: Ria OOMEN-RUIJTEN") 18 December 2012 AGE Platform Europe contribution to the Draft Report on an Adequate, Safe and Sustainable pensions (2012/2234(INI)) Rapporteur: Ria OOMEN-RUIJTEN AGE Platform Europe, a European network

18 December 2012 AGE Platform Europe contribution to the Draft Report on an Adequate, Safe and Sustainable pensions (2012/2234(INI)) Rapporteur: Ria OOMEN-RUIJTEN AGE Platform Europe, a European network

Devaluation as a Reason for Economical Growth or Crisis

International Journal of Economics and Finance; Vol. 9, No. 2; 2017 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education Devaluation as a Reason for Economical Growth or

International Journal of Economics and Finance; Vol. 9, No. 2; 2017 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education Devaluation as a Reason for Economical Growth or

BALANCE OF PAYMENTS, INTERNATIONAL INVESTMENT POSITION, AND EXTERNAL DEBT OF THE RUSSIAN FEDERATION. Moscow

2017 BALANCE OF PAYMENTS, INTERNATIONAL INVESTMENT POSITION, AND EXTERNAL DEBT OF THE RUSSIAN FEDERATION Moscow This publication has been prepared by the Statistics and Data Management Department of the

2017 BALANCE OF PAYMENTS, INTERNATIONAL INVESTMENT POSITION, AND EXTERNAL DEBT OF THE RUSSIAN FEDERATION Moscow This publication has been prepared by the Statistics and Data Management Department of the

CHARTER OF JOINT STOCK COMPANY «First Tower Company»

APPROVED by the General Meeting of Shareholders of PJSC MegaFon September, 2016 CHARTER OF JOINT STOCK COMPANY «First Tower Company» Moscow CONTENTS Article 1. General Information... 3 Article 2. Trade

APPROVED by the General Meeting of Shareholders of PJSC MegaFon September, 2016 CHARTER OF JOINT STOCK COMPANY «First Tower Company» Moscow CONTENTS Article 1. General Information... 3 Article 2. Trade