Presentation to m Cubed Asset Solutions

|

|

|

- Bertina Dixon

- 5 years ago

- Views:

Transcription

1 Presentation to m Cubed Asset Solutions Mike Adsetts, Eugene Botha, Willem Gaymans, Evan Gilbert 20 October

2 Contents Overview MMI Investments Our investment philosophy The current investment environment Performance analysis 2

3 Overview MMI Investments 3 Momentum Outcome-based Solutions

4 MMI investment team in a nutshell 80 investment professionals Managing in excess of R315 bn 528 supporting staff 808 years total investment experience 560 years investment experience within MMI More than 160 academic qualifications 1 shared objective Note: as at 30 June Momentum Outcome-based Solutions

5 MMI investment capabilities OBI portfolio solutions portfolio construction & management Systematic strategies and structuring passives, smart beta, structuring, hedging Growth through rates fixed income, credit, LDI Growth through capital listed property, SP Reid Alternatives hedge funds, private equity, infrastructure Research and insight macro and economic OBI themes & strategy Global investment management global portfolio construction & management 5 Momentum Outcome-based Solutions

6 CIO office Capabilities Investment philosophy Investment management Stakeholder management Consulting Role: To refine, own and champion the MMI Investment philosophy. To formulate principles, guide and approve frameworks, assess needs and prioritise investment initiatives that facilitate the creation of responsible investment portfolios that are consistent with and take into account the specific client needs as identified in ongoing engagement with respective segments and stakeholders Name Surname Role Experience Qualifications Sonja Saunderson Chief Investment Officer 16 BSc,BCom(Hons), MCom (Cum Laude) Michael Adsetts Investment strategist & Deputy in CIO office 12 BSc(Hons),CFA, MBA 6 Momentum Outcome-based Solutions

,MSc")

7 Portfolio Solutions Capabilities Portfolio construction & management Performance and risk insights Role: Create and manage OBI portfolios aligned to the investment philosophy through the construction, selection, identification & where necessary co-creation of investment capabilities Name Surname Role Experience Qualifications Eugene Botha Head: Portfolio Solutions 10 BSc (Hons),MSc Jako De Jager Senior PM: Upper Retail 15 BCom(Hons) Investment Management Jana Van Rooijen Portfolio Manager 10 BCom Bcom(Hons), MCom, PhD (Management Evan Gilbert Senior PM: Lower Retail 7 Studies) Reinier Erasmus Investment Analyst 3 BCom, BBusSci, CAIA Yameka Stofile Investment Analyst 3 BCom Neill Maree Investment Analyst 25 Bcom(Hons) Accounting, CIS Hamza Moosa Quantative Research Analyst 7 BSc (Mathematical Sciences) Barend Crous MIC Portfolio Manager 17 B Com, CFA 7 Momentum Outcome-based Solutions

8 Portfolio Solutions (Risk & Performance insight) Name Surname Role Experience Qualifications Joseph Pearson Head: Investment Performance & Risk Insight 9 Phd(Economics), Executive MSc Risk and Investment Management (Edhec) MSc Business Mathematics and Informatics, BComQuantitative Risk Management Yanna Fourtounas Manager: Investment Performance Insight 10 BSc Actuarial and Financial Mathematics Fehmida Sheik Investment Performance Insight Analyst 13 Matric, Certificate NQF Level 1 Joan Tshivinda Investment Performance Insight Analyst 6 BSc Hons Computational and Applied Mathematics Tyron Pillay Investment Performance Insight Analyst 1 Lerato Sibanyoni Investment Performance Insight Analyst 6 BBusScBachelor of Business Science (Finance Honours), Certificate in Investment Performance Measurement (CIPM) BCompt(Accounting Sciences), Post Graduate Diploma in Accounting Sciences, Post Graduate Certificate in Advanced Taxation Clinton Reddy Manager: System Integration and Optimization 14 PC A+, MDP, BCom 3rd Yr (Incomplete) Bernice Smith Investment Performance Insight Analyst 7.5 BComAccounting (cum laude); B Com (Hons) Accounting; Certificate in the Theory of Accounting; Chartered Accountant (SA); CFA level 2 Clinton Reddy Performance & Attribution Specialist 14 PC A+, MDP, BCom 3rd Yr(Incomplete) BComAccounting; B Com (Hons) Accounting; Certificate in the Theory of Accounting; Chartered Louri Van der Merwe Investment Performance Insight Analyst 9.5 Accountant (SA); CFA level 1 8 Momentum Outcome-based Solutions

9 Portfolio Solutions (Risk & Performance insight) Name Surname Role Experience Qualifications Alexandros Voyiatzakis Collateral Analyst 15 Bcom Acc, Bcompt Honours Wynand Van der Walt Middle Office Analyst 7 CFA Level 1, B.com.honsFinancial management (UP), B.com Accounting Science(UP) Lerato Ramagaga Collateral Analyst 7 Bcome (Economics), Bcom(Hons) Business Financial Management Itumeleng Thlapane Investment Accountant 5 BCom Accounting; Certificate in the Theory of Accounting; Chartered Accountant (SA); Mcom Development Finance student Shushil Makan Middle Office Analyst 6 BComAccounting; Certificate in the Theory of Accounting; Chartered Accountant (SA) 9 Momentum Outcome-based Solutions

10 MMI Responsible Investing Supporting the Code for Responsible Investing in South Africa (CRISA). ESG integration Report Progress Regulation and Codes Active voting on managed assets ESG research integrations on fund managers Signatories of the United Nations-supported Principles for Responsible Investment Initiative (UNPRI) 2006 On the UNPRI working committees since 2009 Active Owners Responsible Investment Advocacy RI themed balanced portfolio with a 14 year track record, inception date May Research survey on the code for responsible investing in South Africa (CRISA) Part of the Sustainability Steering committee of MMI from November 2012 to June 2014 (committee dissolved) Seek Disclosure Member of the Carbon Disclosure Project (CDP). Member of International Corporate Governance Network (ICGN). 10 Momentum Outcome-based Solutions

11 MMI Investment Philosophy 11 Momentum Outcome-based Solutions

Goal (Liability)")

Time")

12 What is Outcome Based Investing? Investment objective (how to achieve it) Goal (Liability) Results Outcome-based investing plans for the end goal as well as the journey that leads to the outcome Start (Assets) Time 12 Momentum Outcome-based Solutions

13 Outcome-based investment philosophy Time frame Risk appetite (capital losses, market relevant, minimum returns, etc.) Investment goal (nominal amount, required level of growth, cash flow matching, etc.) 13 Momentum Outcome-based Solutions

14 Outcomes-based investing principles Start by defining an end-state / outcome: A nominal rand amount A required level of growth (e.g. CPI+x%) A series of pre-defined cash flows A notional asset which is interest rate sensitive A market related / investable index Assess the length of time to reach the outcome What risks are you prepared to take Capital loss Minimum return (no more than -20% in any one year) Not less than the market return Is the outcome reasonably possible based on investment fundamentals Construct a portfolio that best matches the desired outcome 14 Momentum Outcome-based Solutions

15 Outcome-based Investment process We believe in stress-free investing asset class strategy manager Multi-asset class For risk management at total portfolio level Multi-strategy For consistent returns in dynamic market conditions Multi-manager For specialist expertise in each style 15 Momentum Outcome-based Solutions

16 1 Risk appetite calibrated CPI+ 6% Time horizon Minimising probability of capital loss Minimising extent of capital loss Probability of achieving the objective (CPI plus) Minimising drawdown against the objective Six years 15% 15% 35% 35% 16 Momentum Outcome-based Solutions

17 40% 30% 20% 10% 0% -10% -20% -30% 2 Strategy level enhancements Local equity example Size 60% 50% 40% 30% 20% 10% 0% Value -40% 60% 50% 40% 30% 20% 10% 0% -10% Source: Momentum Outcome-based Solutions Momentum -10% 15% 10% 5% 0% -5% -10% -15% -20% -25% -30% -35% Growth 17 Momentum Outcome-based Solutions

18 3 Selecting the best provider Selection and construction principles to follow: Identify investment managers suiting identified strategies Only use active management where there is skill Where no potential for value add or consistent skill, liquidity, market depth, high cost of trading or for risk control, passive investing may be preferable Co-create strategies with investment managers where needed There should be a value add net of fees Most active investment managers are not strategy pure strategy mix should be accounted for in the process of portfolio construction Investment manager risk should not destroy the certainty in the outcome but add to it Investment manager contribution to active risk should relate to value add expectations A well-diversified investment manager blend is crucial to protect against concentrated risk and volatility in outcomes 18 Momentum Outcome-based Solutions

19 Probabilities of delivering on the objectives Build up Long term forward looking 80.00% Probabilities - Beta + Alpha+ Strategy levers 70.00% 60.00% 50.00% 40.00% 30.00% 20.00% 10.00% 0.00% Factor 3 Factor 4 Factor 5 Factor 6 Factor 7 Beta Beta + Alpha Beta + Alpha + Strategy levers *Probabilities based on consistent generation of alpha over the longer term 1964 to Momentum Outcome-based Solutions

20 Factor Series TM Stress-free investing Optimising the risk-return profile based investment to help you achieve your Factor Series TM Portfolio ranges Target Portfolio Range Passive beta Classic Portfolio Range Traditional active asset classes Enhanced Portfolio Range Traditional and new asset classes Flexible Portfolio Range Balanced asset allocation Fund of Funds Range Collective investments 20 Momentum Outcome-based Solutions

21 Factor Series TM Stress-free investing Optimising the risk-return profile based investment to help you achieve your Increasing return Increasing risk 21 Momentum Outcome-based Solutions

22 Factor Series TM Stress-free investing Optimising the risk-return profile based investment to help you achieve your Potential to achieve Increasing cost Increasing return Increasing risk 22 Momentum Outcome-based Solutions

23 Economic overview 23 Momentum Outcome-based Solutions

24 Global economic overview Global US Eurozone UK Japan EM China Growth downgrades accelerated in DM but stabilising in EM Slower growth path than historically sluggish productivity gains + unfavourable demographics + limited policy room Firm consumption + services growth drag from oil + exports should fade Gradual strengthening in inflation Delayed tightening cycle in response to rising external risks Mild growth accommodative fiscal + monetary policy partly eroded by weak external demand + geopolitical risks Expected to avoid annual recession weaker sterling-induced boost to tourism + exports to partly counter blow to private sector confidence Slow reform momentum curtailing growth despite massive stimulus efforts Growth differential with DM expected to widen anaemic global trade + muted commodity prices + financial vulnerabilities limits extent of rebound Cyclical slowdown expected as policy turns more neutral trend growth supported by reforms 24 Momentum Outcome-based Solutions

25 Local economic overview Growth Expect a gradual improvement towards trend by 2018 driven in outer years by firmer commodity prices + increase in energy supply + higher global growth Consumer Facing tepid jobs growth + lower real wage growth + stringent credit criteria Investment Dampened by policy uncertainty + weak demand + profitability strain Current account Fiscal Currency Currency benefit partly offset by high input costs + fragile global demand + structural drag from dividend payments Debt stabilisation threatened by slower revenue growth + political pressure to spend in lacklustre growth environment credit worthiness under scrutiny Positive real carry trade overshadowed by domestic political tensions Modest revival in commodity prices over medium term is rand positive Inflation Profile likely to improve in 2017 on lower food inflation risks: rand + wages Interest rates Real rates still viewed as accommodative rates could rise another 25bps in 2016 (limited space for unfavourable shocks) without unduly affecting growth 25 Momentum Outcome-based Solutions

26 Source: Deutsche Bank Momentum")

26 GDP: SA consumers are vulnerable Culprits include deteriorating (nominal + real) income growth + rising ST debt pressure + deteriorating wealth effects + job losses but 4Q16 could be a turning point Vulnerability index measures wealth (house + equity prices, debt to asset growth) + purchasing power (employment, inflation, consumer confidence, wages) + debt affordability (debt instalments, ST debt share, debt services costs, insolvencies, savings) 26 Source: Deutsche Bank Momentum Outcome-based Solutions

27 GDP: SA corporates are under pressure Growth in (real) corporate profitability under strain Avg. since 1994 Q (latest) Business confidence remains in the doldrums Q09 1Q16 3Q Agriculture Mining Manufacturing Utilities Construction Trade Transport Finance Government Personal services Total Building contractors Manufacturing Retailers Wholesalers New vehicle dealers Composite Index level (above 50 = satisfactory) Source: SARB, Global Insight, Stats SA, Momentum Investments Source: BER, Momentum Investments 27 Momentum Outcome-based Solutions

28 GDP: Marginal improvement expected in 2017 Global growth expected to increase BBG: 2.9% (2016) to 3.1% (2017), IMF: 3.1% (2016) to 3.4% (2017) Mild commodity price uptick Commodity prices up 8% from recent trough Energy supply constraint dissipating 4 th Unit of Ingula pumped storage connected + 2 nd unit of Medupi synchronised ahead of latest schedule Reversal of drought impact International Grains Council estimates 2016/17 maize production to be 68% higher than last year (12.9m tonnes) Early growth indicators showing a slight improvement lead indicator and business confidence 28 Momentum Outcome-based Solutions

29 Impact of sub-ig status on the SA economy Immediate currency impact Sustained currency depreciation higher expected inflation interest rate response dampens domestic demand Tighter fiscal policy in an attempt to improve debt metrics + offset revenue slippage higher taxes + lower government expenditure Consumer hit negatively by rising interest rates + higher personal taxes + VAT + lower employment prospects + negative wealth effect Do not necessarily expect a negative feedback loop from poor economic growth + unfavourable political climate deteriorating fiscal position further downgrades (i.e. Brazil) 29 Momentum Outcome-based Solutions

30 Rand: Key drivers UPSIDE RISKS DOWNSIDE RISKS GLOBAL LOCAL GLOBAL LOCAL Massive China stimulus package spurring an earlier acceleration in commodity prices SA avoids downgrade Global growth recession Further material growth downgrades Fed holds off/delays interest rate hikes SA growth surprises positively Increasingly fragile European Union Lingering ratings pressure China hard-landing Labour and sociopolitical instability Rise in geopolitical risks Further widening in twin deficits 30 Momentum Outcome-based Solutions

31 Rand: Recently impacted by negative investor confidence Recent political turmoil has likely left investors concerned about SA s credit rating once again Structural drag on current account (dividend payments) requires foreign capital funding 100 Total net portfolio inflows (USD billion) 100 Current account breakdown (R'bn) Jul - Dec 2015 Jan - Aug Invisibles (income and current transfers) Trade and services USDZAR SA EM Q Q Q Q Q Q Source: Bloomberg, INET BFA, Momentum Investments Source: Global Insight, Momentum Investments (data up to 3Q16 for rand) 31 Momentum Outcome-based Solutions

32 Rand: Expected profile Political tussles eroding relative real carry trade benefit, while a mild commodity price recovery is expected to bid rand firmer in late-2017/ USDZAR F avg (16% depreciation) 2017F avg (2% appreciation) 2018F avg (8% appreciation) Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17 May-17 Sep-17 Jan-18 May-18 Sep-18 Source: INET BFA, Momentum Investments 32 Momentum Outcome-based Solutions

33 Inflation: Food inflation should fall meaningfully in 2017 Maize prices have started to reverse favourably International food prices stable from a year ago 100 Yellow maize (% y/y, lead 12 m) Food (USD) 80 PPI crops (% y/y) Food (ZAR) 60 Food inflation (% y/y) Oil (USD) Oil (ZAR) Index level Dec-08 Feb-11 Apr-13 Jun-15 Aug-17 Aug-15 Nov-15 Feb-16 May-16 Aug-16 Source: INET BFA, Momentum Investments Source: INET BFA, Momentum Investments 33 International Grains Council estimates country s 2016/17 maize production will improve to 12.9 million tons Momentum Outcome-based Solutions (68% from their 2015/16 estimate of 7.7 million tons)

34 Interest rates: Expecting peak in repo at 7.25% We expect a further 25 basis points hike this year: Prolonged breach of inflation target vulnerable to further currency shocks Sticky longer-dated inflation expectations threat to second-round inflation Sizeable current account deficit requires real interest rates to shift higher SARB sees real rates as accommodative % Nominal repo rate Real repo rate % Jan-06 Aug-07 Apr-09 Nov-10 Jun-12 Feb-14 Sep-15 May-17 Dec Source: INET BFA, Momentum Investments Momentum Outcome-based Solutions

35 The current investment environment 35 Momentum Outcome-based Solutions

36 Local asset classes One year to September % 8.4% 7.6% 7.1% 5.9% 3.8% Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep-16 SWIX ALBI STeFI SA Listed Property ILB CPI Source: INET BFA and Momentum Investments *CPI is lagged by one month due to availability of inflation data All returns in rand terms 36 investments

37 120 FTSE/JSE sectors One year to September One year to September 2016 Resources = 9.77% Financials = -0.91% Industrials = 4.49% Three months to September 2016 Resources = 8.07% Financials = 0.85% Industrials = -2.05% Oct Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep-16 Resources Financials Industrials FTSE/JSE Resources was the only sector to have positive returns for the three-month and oneyear periods Source: INET BFA and Momentum Investments 37 investments

38 Global asset classes One year to September % 9.1% 8.2% 6.5% % Oct Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Sep-16 Global Bonds Global Property Global ILB Global Equity USD/ZAR Source: INET BFA and Momentum Investments All returns in rand terms 38 investments

39 MSCI developed and emerging markets One year to September One year to September 2016 Developed markets = 9.18% Emerging markets = 14.21% SWIX = 9.91% Three months to September 2016 Developed markets = 4.42% Emerging markets = 8.39% SWIX = 7.51% Sep 30, 2015 Nov 11, 2015 Dec 23, 2015 Feb 03, 2016 Mar 16, 2016 Apr 27, 2016 Jun 08, 2016 Jul 20, 2016 Aug 31, 2016 Source: INET BFA, MSCI and Momentum Investments MSCI Developed Markets (USD) MSCI Emerging Markets (USD) SWIX (USD) 39 investments

40 Asset class return ranges Expected returns (% over 1 year, in ZAR terms) Gold ETF Platinum ETF Global bonds Global cash ILBs Cash DM equity EM equity Equity Bonds Property Rand-sensitive returns would be 3.4% higher using spot (13.60) rather than Sep avg. (14.10) 40 Source: Momentum Investments investments

41 Investment returns 41 Momentum Outcome-based Solutions

42 Momentum MoM Enhanced Factor Portfolio Range TM Portfolio returns to September 2016 Portfolio One year Three years Four years Five years Six years Seven years Momentum MoM Enhanced Factor % 11.5% 15.2% 16.5% 15.0% 15.2% CPI+7% 13.0% 12.7% 12.8% 12.7% 12.6% 12.3% Strategic benchmark 9.8% 12.3% 15.1% 16.8% 15.1% 15.3% Momentum MoM Enhanced Factor % 11.1% 14.1% 15.3% 14.0% 14.2% CPI+6% 12.0% 11.7% 11.8% 11.7% 11.6% 11.3% Strategic benchmark 9.7% 11.8% 14.2% 15.8% 14.3% 14.3% Momentum MoM Enhanced Factor % 10.6% 11.9% 12.8% 12.2% CPI+5% 10.9% 10.7% 10.8% 10.7% 10.6% Strategic benchmark 9.3% 10.7% 11.8% 13.3% 12.6% Momentum MoM Enhanced Factor 4 9.9% 9.8% 10.5% 11.3% 10.9% 11.3% CPI+4% 9.9% 9.7% 9.8% 9.7% 9.8% 9.3% Strategic benchmark 8.9% 9.8% 10.5% 11.9% 11.3% 11.5% Momentum MoM Enhanced Factor 3 9.3% 9.1% 9.4% 10.2% 10.0% 9.8% CPI+3% 8.9% 8.7% 8.8% 8.7% 8.6% 8.3% Strategic benchmark 8.3% 9.2% 9.7% 10.9% 10.6% 10.2% Important notes 1. Returns for periods exceeding one year are annualised. 2. All returns quoted are before deduction of fees, except where a portfolio includes underlying investments where fees are deducted from the return, but after the deduction of performance-based fees. 3. The inception date of the combined, local and global portfolios is 1 July 2011 and actual portfolio and benchmark returns have been used since then. Portfolio and benchmark returns for longer periods are based on mappings from certain old portfolios to the new portfolios and details of these old portfolios are on the individual fund fact sheets.. 42 Momentum Outcome-based Solutions

43 Enhanced Factor 7 Portfolio relative to the CPI-related benchmark over seven-year rolling periods 25% 20% 15% 10% 5% 0% Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 CPI+7% Enhanced Factor 7 Enhanced Factor 7 BM Important notes The inception date of the Momentum MoM Enhanced Factor 7 portfolio is July For periods before then, the portfolio and benchmark returns for the Momentum High Equity Portfolio have been used from April Momentum Outcome-based Solutions

44 25% Enhanced Factor 6 Portfolio relative to the CPI-benchmark over six-year rolling periods 20% 15% 10% 5% 0% Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 CPI +6% Enhanced Factor 6 Enhanced Factor 6 BM Important notes The inception date of the Momentum MoM Enhanced 6 portfolio is July For periods before then, the portfolio and benchmark returns for the Momentum Balanced Portfolio have been used from April Momentum Outcome-based Solutions

45 16% Enhanced Factor 5 Portfolio relative to the CPI-benchmark over five-year rolling periods 14% 12% 10% 8% 6% 4% 2% 0% Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16 CPI+5% Enhanced Factor 5 Enhanced Factor 5 BM Important notes The returns for Enhanced Factor 5 are actual returns from July 2011, for periods before then, the actual building block returns are used in the new Enhanced allocations. 45 Momentum Outcome-based Solutions

46 Enhanced Factor 4 Portfolio relative to the CPI-benchmark over four-year rolling periods 25% 20% 15% 10% 5% 0% Jun-03 Jun-04 Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16 CPI +4% Enhanced Factor 4 Enhanced Factor 4 BM Important notes The returns for Enhanced Factor 4 are actual returns from July 2011, for periods before then, the actual building block returns are used in the new Enhanced allocations. 46 Momentum Outcome-based Solutions

47 Enhanced Factor 3 Portfolio relative to the CPI-benchmark over three-year rolling periods 18% 16% 14% 12% 10% 8% 6% 4% 2% 0% CPI+3% Enhanced Factor 3 Enhanced Factor 3 BM Important notes The inception date of the Momentum MoM Enhanced 3 portfolio is July For periods before then, the portfolio and benchmark returns for the Momentum MoM Absolute Strategies Portfolio have been used from January Momentum Outcome-based Solutions

48 Did we create certainty in outcomes? Actual realised probabilities (Measured to September 2016) Portfolio Enhanced Factor 7 Enhanced Factor 6 Enhanced Factor 5 Enhanced Factor 4 Enhanced Factor 3 Number of observations Periods outperforming Realised probability of outperforming 85.8% 82.0% 100.0% 80.0% 76.3% Predicted probability of outperforming 55.6% 68.2% 73.4% 75.9% 70.8% Observations from 1 December Momentum Outcome-based Solutions

49 Overview of building blocks 49 Momentum Outcome-based Solutions

50 Momentum MoM Enhanced Factor Portfolio Range TM Building block returns to September 2016 Portfolio Three months One year Three years Five years Portfolio Three months One year Three years Five years Classic Equity 0.5% 9.0% 9.6% 16.3% Commodity -3.6% 10.3% 5.5% 4.1% SWIX 0.3% 9.0% 10.9% 16.8% STeFI 1.9% 7.2% 6.4% 6.0% Property -0.2% 7.7% 18.1% 20.2% Flexible Bond 4.0% 10.8% 8.8% 9.5% SAPY -0.7% 3.8% 14.5% 17.9% ALBI 3.4% 7.6% 6.8% 8.0% ILB 0.4% 8.6% 8.5% 9.4% Stable Hedge 1.0% 6.8% 6.6% 6.5% ILBI 0.4% 8.4% 8.4% 9.2% STeFI 1.9% 7.2% 6.4% 6.0% TAA 1.1% 7.6% 7.3% 8.8% Moderate Hedge 1.2% 8.3% 8.2% 8.1% ILBI 0.4% 8.4% 8.4% 9.2% ALBI 3.4% 7.6% 6.8% 8.0% Global Equity 1.7% 16.2% 15.9% 23.2% Aggressive Hedge 1.8% 9.6% 8.5% 10.6% MSCI AC 0.9% 12.7% 16.1% 22.5% 50 SWIX: 50 STeFI 1.1% 8.3% 8.8% 11.4% Global Bonds -5.3% 8.6% 13.0% 12.4% Absolute Strategies 2.2% 9.5% 7.8% 8.2% Citigroup WGBI -5.6% 8.8% 12.9% 12.5% CPI+4% 2.3% 9.9% 9.7% 9.7% Strategic BM 1.5% 8.2% 8.5% 10.5% Important notes 1. Returns for periods exceeding one year are annualised. 2. All returns quoted are before deduction of fees, except where a portfolio includes underlying investments where fees are deducted from the return, but after the deduction of performance-based fees. 50 Momentum Outcome-based Solutions

51 Equity manager Returns 51 Momentum Outcome-based Solutions

52 Momentum MoM Classic Equity Portfolio Allocations Strategy Allocation Manager Allocation Momentum 23% Core Value 25% Coronation 0.0% SIM 12.1% Dibanisa 9.8% Foord 14.8% Prudential 15.6% Deep Value 7% Blue Alpha 10.2% Fairtree 12.5% Value 45% Perpetua 11.9% Truffle 13.1% Optimization done using constructed peer averages per strategy to Maximize probability of delivering SWIX + 2% over rolling 3 year periods Ensure that maximum relative drawdown is less than -5% over rolling 12 months 52 Momentum Outcome-based Solutions

53 ` Momentum MoM Classic Equity Portfolio Underlying investment manager returns to 30 September 2016 Three month One year Two years Three years Five years Weightings 30 September 2016 SWIX 0.3% 9.0% 7.5% 10.9% 16.8% Classic Equity 0.5% 9.0% 6.6% 9.6% 16.3% Dibanisa 0.2% 9.0% 7.6% 10.9% 16.5% 9.9% Prudential 1.0% 8.9% 7.7% 11.4% 18.0% 15.4% Foord 0.4% 5.7% 6.3% 10.2% 18.7% 14.8% Blue Alpha/ Coronation 0.2% 7.6% 5.2% 7.8% 16.6% 9.7% Satrix Momentum -3.5% 5.8% 9.2% 13.2% 21.0% 11.7% Fairtree 3.1% 18.6% 14.4% 15.6% N/A 12.9% Truffle -0.5% 5.3% 10.3% 13.3% N/A 13.2% Perpetua 3.0% 12.7% 1.0% N/A N/A 12.0% 53 Momentum Outcome-based Solutions

54 Market returns concentration One-year returns ending: September-16 August-16 July-16 NASPERS NASPERS NASPERS SIBANYE GOLD LTD SIBANYE GOLD LTD ANGLOGOLD ASHANTI LTD HARMONY Market-cap weighted returns: 10 shares contributed 116% to the return of the SWIX, while 20 shares contributed 134% Source: Barra, Deutsche Securities and Momentum Investments BRITISH AMERICAN TOBACCO SIBANYE GOLD LTD ANGLO SABMILLER PLC HARMONY Top 5 ANGLOGOLD ASHANTI LTD 90% Top 5 ANGLOGOLD ASHANTI LTD 92% Top 5 GFIELDS 81% Top 6 BRITISH AMERICAN TOBACCO 96% Top 6 HARMONY 97% Top 6 BRITISH AMERICAN TOBACCO LONMIN GFIELDS SABMILLER PLC IMPALA PLATINUM HOLDINGS STEINHOFF INTL HLD NV STEINHOFF INTL HLD NV GFIELDS SAPPI SAPPI Top 10 SAPPI 116% Top 10 LONMIN 110% Top 10 TIGBRANDS 103% SHOPRIT TIGBRANDS SHOPRIT NORTHAM SHOPRIT ANGLO AMERICAN PLATINUM TIGBRANDS CLICKS GROUP LTD LONMIN ANGLO AMERICAN PLATINUM LIMITED REINET INVESTMENTS RESILIENT REIT LTD CLICKS GROUP LTD CAPITEC IMPALA PLATINUM HOLDINGS VODACOM NEW EUROPE PROPERTY INVESTMENTS PLC 54 Momentum Outcome-based Solutions PAN-AF ASPEN ASPEN CAPITEC PAN-AF PAN-AF CLICKS GROUP LTD CAPITEC BLUETEL NORTHAM Top 20 EXXARO 134% Top 20 ANGLO 121% Top 20 VODACOM 119% Remaining (Positive) 15% Remaining (Positive) 12% Remaining (Positive) 14% Negative (75 Shares) -49% Negative (74 Shares) -33% Negative (72 Shares) -32% 87%

55 The All Share index return; and return ex SAB, NPN SAB Miller and Naspers have been significant contributors to performance 55 Momentum Outcome-based Solutions

56 Equity Portfolio positioning 56 Momentum Outcome-based Solutions

57 Momentum MoM Classic Equity Portfolio Top 10 Holdings at 30 September 2016 Absolute Weight Active Weight NASPERS 13.8% -5.0% BRITISH AMERICAN TOBACCO 6.1% 1.5% STEINHOFF INTL HLD NV 3.9% 0.1% FIRSTRAND 3.7% 1.1% SASOL 3.5% -0.3% STANDARD BANK GP 3.3% 0.2% OLDMUTUAL 2.7% 0.6% MTN GROUP 2.2% -1.6% BHPBILL 2.0% 0.6% ANGLO 2.0% 0.2% 57 Momentum Outcome-based Solutions

58 Momentum MoM Classic Equity Portfolio Investment manager positioning at 30 September 2016 SIM Mom Prudential Perpetua Foord High Growth Truffle Fairtree Classic INDUSTRIALS Automobiles & Parts Construction & Materials Food & Beverage Health Care Industrial Goods & Services Media Personal & Household Goods Retail Technology Telecommunications Travel & Leisure Utilities Active Overweight: > 2.5% Active Underweight: -2.5%- 0% Active Overweight: 0% - 2.5% Active Underweight > -2.5% 58 Momentum Outcome-based Solutions

59 Momentum MoM Classic Equity Portfolio Investment manager positioning at 30 September 2016 SIM Prudential Perpetua Foord High Growth Truffle Fairtree Classic RESOURCES Chemicals Basic Resources Oil & Gas FINANCIALS Banks Financial Services Insurance Real Estate Active Overweight: > 2.5% Active Underweight: -2.5%- 0% Active Overweight: 0% - 2.5% Active Underweight > -2.5% CASH Momentum Outcome-based Solutions

60 Summary 60 Momentum Outcome-based Solutions

61 Summary point on products delivery Products continue to deliver on their CPI Objectives/goals over the longer time periods Portfolios performing in line with strategic benchmark Portfolios remain defensively positioned TAA contributed over the short term Naspers weight in SWIX made it difficult for domestic equity managers to outperform their benchmarks 61 Momentum Outcome-based Solutions

62 Active vs. Passive investing? Evan Gilbert 62

63 The Active vs. Passive Investing Debate Key questions : What is a benchmark? What are the key differences between Active and Passive investment approaches? What are the pros and cons of each approach? When is it best to use which approach? How do we use Active and Passive investments in the MOBS portfolios? Outcomes Based Investing Application to the Enhanced Range Classic Equity 63 Momentum Outcome-based Solutions

64 What is a benchmark vs. an objective? This is a proxy for/represents the underlying investment universe in the portfolio Usually set at the asset class level e.g. JSE All Share Index Can be multi-asset class Any investment mandate has a benchmark Serves as a basis for performance assessment A good benchmark must be: Appropriate (match the investment environment) Investable (can be replicated) Properly weighted (aim to avoid concentration) Transparent and easy to understand Broad market indices based on market capitalisation are the most common/popular benchmarks at the asset class level, but there are others: Style-specific indices (e.g. value in equities or fixed income can be used for certain investment styles) Peer relative e.g. top quartile (useful for assessing how well your manager is doing compared to the competition) Can also have objectives (different to benchmarks): Absolute returns (normally defined in terms of returns above inflation) Custom (usually a combination of different asset classes e.g. 60% equity, 30% bonds, 10% cash) 64 Momentum Outcome-based Solutions

65 Active vs. Passive What are the key differences? Active Managers Goal: benchmark outperformance An active manager tries to outperform a benchmark in a specific asset class (e.g. SA Equity - ALSI) Active positioning The portfolio composition is different to the index by design Investment Philosophy Differences to the index based on an investment philosophy e.g. value Performance: Alpha Evaluated on ability to produce alpha (outperformance relative to the benchmark on a risk adjusted basis) Cost experience Normally higher for the client Higher management fees More trading/transaction costs Passive Managers Goal: benchmark replication A passive manager tries to replicate the returns a benchmark in an asset class (e.g. ALSI) Passive positioning The portfolio is constructed the same as the benchmark (or as close to it as is possible) by design Investment philosophy None Performance Tracking error Tracking error how closely does its returns match those of the benchmark? Cost experience Lower cost experience for the client Very low manager fees JDJ1 Lower turnover, depending on strategy 65 Momentum Outcome-based Solutions

66 Types of Passive Investing Strategies/Products Full replication Index tracking notes Benchmark Returns Partial replication Access via: Segregated mandates (if big enough) Unit Trusts Exchange Traded Funds (ETFs) 66 Momentum Outcome-based Solutions

67 Active vs. Passive investing The pros and cons Pros Cons Active Investing Offers the potential to outperform the index (if the manager s investment strategy works) Depending on the strategy, should deliver less volatile returns than traditional market cap indices Costs more than passive approaches It always needs to produce alpha on average to counteract the cost drag The alpha stream is lumpy and the strategy generally requires a long term investment horizon deliver benchmark beating returns Lots of active portfolios resemble the benchmark so you can end up paying a lot for a closet index tracker Passive Investing Accurate replication of asset class returns Relatively cheap Gives you the bulk of the returns you need to reach your investment objective Can only ever (at best) match the benchmark Will usually lag the benchmark because of fees Depending on a client s risk profile, passive investments may introduce more volatility/risk 67 Momentum Outcome-based Solutions

68 Active vs. Passive When do you use which? You can come up with very good investment solutions built only from passive investment that are: Cheap Diversified Offer a reasonable chance of success But there are some very good reasons to at the very least complement this with active managers: Not all asset classes and investment strategies are represented in the passive world (Smart Beta is changing this) Some clients don t want average returns they want to back an active manager that seems to know what they are doing. 68 Momentum Outcome-based Solutions

69 New developments in the Passive Space Smart Beta the best of both worlds? Systematic investment strategies that have elements of both passive and active investing There is a rule book that is followed there is no manager discretion like passive investing (other than setting the rules) Portfolio will be different to market-capitalisation benchmark possibility of outperformance like Active investments Smart Beta portfolios are usually based on a Factor RAFI stocks weighted by their fundamental performance (profits, sales, growth) not their prices (market capitalisation approach) Value consistent exposure to cheap assets Momentum consistent exposure to assets with both positive recent price changes and positive earning revisions Offers cheap access to active-type investment strategies Provides a cheaper alternative to active managers focussing on a style/factor Devil in the detail : definitions of factors and risk management in portfolio construction No rules works perfectly all the time an active manager could still perform better 69 Momentum Outcome-based Solutions

70 Active and Passive Investments how do we choose between (or combine) them? OBI selection and building block construction principles : Identify investment managers that match the identified strategies Only use active management where there is demonstrable skill Passive investing may be preferable where No potential for value add or consistent skill; Liquidity, market depth, high cost of trading; or Risk control. There should always be a value add net of fees Risk management: Investment manager contribution to active risk should relate to value add expectations Investment manager risk should not destroy the certainty in the outcome but add to it A well-diversified investment manager blend is crucial to protect against concentrated risk and volatility in outcomes 70 Momentum Outcome-based Solutions

71 Active versus passive : Cash (lagged by one month) One-year rolling average to August* % 155% 135% Active outperforms 115% 10% 95% 5% 75% 55% 35% 0% 15% Active underperforms -5% -5% -25% Aug-05 Nov-05 Feb-06 May-06 Aug-06 Nov-06 Feb-07 May-07 Aug-07 Nov-07 Feb-08 May-08 Aug-08 Nov-08 Feb-09 May-09 Aug-09 Nov-09 Feb-10 May-10 Aug-10 Nov-10 Feb-11 May-11 Aug-11 Nov-11 Feb-12 May-12 Aug-12 Nov-12 Feb-13 May-13 Aug-13 Nov-13 Feb-14 May-14 Aug-14 Nov-14 Feb-15 May-15 Aug-15 Nov-15 Feb-16 May-16 Aug-16 Active Cash managers - STeFI (12m rolling) Active Cash Managers Cumulative STeFI Cumulative Source: Alexander Forbes S.A. Money Market Manager Watch Survey, INET BFA and Momentum Investments * Lagged by one month due to availability of data 71 Momentum Outcome-based Solutions

72 Active versus passive: Bonds (lagged by one month) One-year rolling average to August* % 200% 10% Active outperforms 150% 5% 100% 0% 50% -5% -10% Active underperforms 0% -15% -50% Sep-05 Dec-05 Mar-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07 Dec-07 Mar-08 Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Active Bond managers - ALBI (12m rolling) Active Bond Managers Cumulative ALBI Cumulative Source: Alexander Forbes S.A Bond Manager Watch Survey, INET BFA and Momentum Investments * Lagged by one month due to availability of data 72 Momentum Outcome-based Solutions

73 Active versus passive: Property (lagged by one month) One-year rolling average to August* % 1350% 10% Active outperforms 1150% 5% 950% 750% 0% 550% -5% 350% -10% Active underperforms 150% -15% -50% Dec-03 Apr-04 Aug-04 Dec-04 Apr-05 Aug-05 Dec-05 Apr-06 Aug-06 Dec-06 Apr-07 Aug-07 Dec-07 Apr-08 Aug-08 Dec-08 Apr-09 Aug-09 Dec-09 Apr-10 Aug-10 Dec-10 Apr-11 Aug-11 Dec-11 Apr-12 Aug-12 Dec-12 Apr-13 Aug-13 Dec-13 Apr-14 Aug-14 Dec-14 Apr-15 Aug-15 Dec-15 Apr-16 Aug-16 Active Property managers - SAPY (12m rolling) Active Property Managers Cumulative SAPY Cumulative Source: Alexander Forbes S.A. Property Manager Watch, INET BFA and Momentum Investments * Lagged by one month due to availability of data 73 Momentum Outcome-based Solutions

74 Active vs. Passive: Equity (lagged by one month) One-year rolling active to August* % 850% 10% Active outperforms 750% 650% 5% 550% 0% 450% 350% -5% 250% -10% Active underperforms 150% 50% -15% Feb-05 Feb-06 Feb-07 Feb-08 Feb-09 Feb-10 Feb-11 Feb-12 Feb-13 Feb-14 Feb-15 Feb-16 Active Equity managers - SWIX (12m rolling) Active Equity Managers Cumulative SWIX Cumulative -50% The average of the active equity managers underperformed the SWIX for the year ended August 2016 Source: Alexander Forbes S.A. Equity Manager Watch Survey, INET BFA and Momentum Investments * Lagged by one month due to availability of data 74 Momentum Outcome-based Solutions

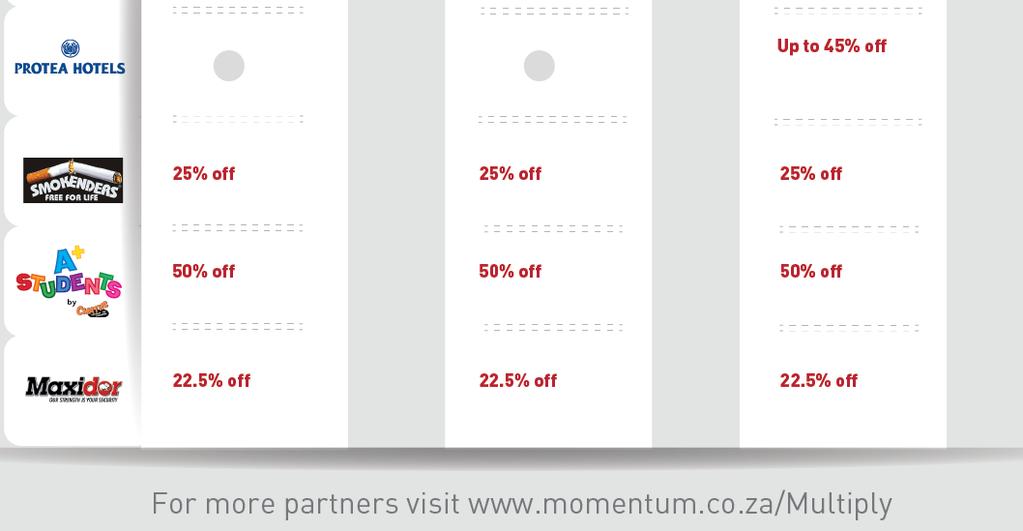

75 Enhanced Factor Range Classic Equity Portfolio Strategy and Manager Allocations Strategy Allocation Manager Allocation Momentum 23% Core Value 25% Coronation 0.0% SIM 12.1% Dibanisa 9.8% Foord 14.8% Prudential 15.6% Deep Value 7% Blue Alpha 10.2% Fairtree 12.5% Value 45% Perpetua 11.9% Truffle 13.1% Optimization done using constructed peer averages per strategy to Maximize probability of delivering SWIX + 2% over rolling 3 year periods Ensure that maximum relative drawdown is less than -5% over rolling 12 months 75 Momentum Outcome-based Solutions

76 Enhanced Factor Range Classic Equity Strategy performance relative to SWIX 30% 20% 10% 0% -10% -20% -30% -40% Jul-04 May-05 Mar-06 Jan-07 Nov-07 Sep-08 Jul-09 May-10 Mar-11 Jan-12 Nov-12 Sep-13 Jul-14 May-15 Mar-16 Value Core Momentum Deep Value 76 Momentum Outcome-based Solutions

77 Performance of Classic Equity vs. SWIX 15% 850% 10% Active outperforms 750% 650% 5% 550% 0% 450% 350% -5% 250% -10% Active underperforms 150% 50% -15% -50% May-04 Jun-05 Jul-06 Aug-07 Sep-08 Oct-09 Nov-10 Dec-11 Jan-13 Feb-14 Mar-15 Apr-16 Classic equity - SWIX (12m rolling) SWIX Cumulative Classic Equity Cumulative 77 Momentum Outcome-based Solutions

78 Enhanced Equity vs. Average Active Managers Performance relative to SWIX (36m rolling) 30% 20% Active outperforms 10% 0% -10% -20% Active underperforms -30% Dec-06 Jan-08 Feb-09 Mar-10 Apr-11 May-12 Jun-13 Jul-14 Aug-15 Active equity - SWIX (36m rolling) Classic equity - SWIX (36m rolling) 78 Momentum Outcome-based Solutions

79 Summary Active vs. Passive is not really the question! We should rather ask: When is it best to use Active or Passive? What is the best combination of Active and Passive investments? Each have their pros and cons: Passive investments are cheap and gets you most of the way there (via Beta) But it can t always give you access to the investment strategies that you want Active investments can give you the extra performance (via Alpha) But it s more expensive and Alpha is not always consistently delivered Smart Beta offers the potential of the best of both approaches but is still very new We use a combination of active and passive investments in the Enhanced Factor Range Classic Equity building block: Passive core (SWIX tracker in Local Equity Building Block) Active managers Various specialised strategies We believe that this gives us the right combination of expected level of outperformance and cost for our clients 79 Momentum Outcome-based Solutions

80 Thank you 80 momentum asset management

81 Multiply Overview Gretel Wundram 81

82 Multiply CVP Combines new technologies With a deep understanding of human behaviour To help customers become more financially well Using compelling rewards to drive the change Financial Wellness 82

83 Multiply plans Free plan that starts the wellness journey and gives base level rewards Incentivises wellness by providing access to wellness facilities and offers deep discounts on relevant lifestyle benefits AND financial products Incentivises wellness by providing access to wellness facilities and family discounts on necessities such as funeral, education, food and clothing 83

84 Points structure Multiply Provider has 3 levels Multiply Premier has 5 statuses 84

85 Pricing structure Multiply Provider Multiply Premier 85

86 Starter partners Health and fitness Travel Food and clothing Lifestyle Education Financial wellness and many more 86

87 Pricing structure 87

88 Pricing structure 88

89 Thank you 89 Momentum Outcome-based Solutions

Key market performance drivers

Key market performance drivers Monthly charts September 2016 1 Market returns concentration One-year returns ending: September-16 August-16 July-16 NASPERS NASPERS NASPERS SIBANYE GOLD LTD SIBANYE GOLD

Key market performance drivers Monthly charts September 2016 1 Market returns concentration One-year returns ending: September-16 August-16 July-16 NASPERS NASPERS NASPERS SIBANYE GOLD LTD SIBANYE GOLD

Key market performance drivers

Key market performance drivers Monthly charts September 2017 1 Market returns concentration One-year returns ending: September-17 August-17 July-17 NASPERS NASPERS NASPERS ANGLO ANGLO ANGLO STANDARD BANK

Key market performance drivers Monthly charts September 2017 1 Market returns concentration One-year returns ending: September-17 August-17 July-17 NASPERS NASPERS NASPERS ANGLO ANGLO ANGLO STANDARD BANK

Key market performance drivers. Monthly charts to 31 March 2018

Key market performance drivers Monthly charts to 31 March 2018 Market concentration One-year returns ending: March-18 February-18 January-18 NASPERS NASPERS NASPERS STANDARD BANK GROUP LTD STANDARD BANK

Key market performance drivers Monthly charts to 31 March 2018 Market concentration One-year returns ending: March-18 February-18 January-18 NASPERS NASPERS NASPERS STANDARD BANK GROUP LTD STANDARD BANK

Key market performance drivers. Monthly charts to 30 September 2018

Key market performance drivers Monthly charts to 30 September 2018 Market concentration One-year Capped SWIX contributions ending September 2018 Source: StatPro, Power BI and Momentum Investments Active

Key market performance drivers Monthly charts to 30 September 2018 Market concentration One-year Capped SWIX contributions ending September 2018 Source: StatPro, Power BI and Momentum Investments Active

QUARTERLY REPORT TO MEMBERS 2nd Quarter 2011

QUARTERLY REPORT TO MEMBERS 2nd Quarter 211 This is your first-quarter report for the year 211 on the Media24 Retirement Fund and its performance. We have shown the performance of the Media24 portfolios

QUARTERLY REPORT TO MEMBERS 2nd Quarter 211 This is your first-quarter report for the year 211 on the Media24 Retirement Fund and its performance. We have shown the performance of the Media24 portfolios

Sanlam Employee Benefits

Sanlam Employee Benefits Sanlam Plus Pension & Provident Preservation monthly investment fact sheets March 2017 Sanlam Plus Pension & Provident Preservation March 2017 Member Investment Selection Menu

Sanlam Employee Benefits Sanlam Plus Pension & Provident Preservation monthly investment fact sheets March 2017 Sanlam Plus Pension & Provident Preservation March 2017 Member Investment Selection Menu

MEET THE TEAM FOORD ASSET MANAGEMENT

MEET THE TEAM FOORD ASSET MANAGEMENT November 2015 MEET THE TEAM SPEAKERS Welcome Paul Cluer Managing Director Share focus Michael Townshend Portfolio Manager and Resources Analyst Returns and macro environment

MEET THE TEAM FOORD ASSET MANAGEMENT November 2015 MEET THE TEAM SPEAKERS Welcome Paul Cluer Managing Director Share focus Michael Townshend Portfolio Manager and Resources Analyst Returns and macro environment

Economic and market snapshot for January 2016

From left to right: Herman van Papendorp (Head of Macro Research and Asset Allocation), Sanisha Packirisamy (Economist) Economic and market snapshot for January 2016 Global economic developments United

From left to right: Herman van Papendorp (Head of Macro Research and Asset Allocation), Sanisha Packirisamy (Economist) Economic and market snapshot for January 2016 Global economic developments United

BATSETA Durban Mark Davids Head of Pre-retirement Investments

BATSETA Durban 2016 Mark Davids Head of Pre-retirement Investments Liberty Corporate VALUE Dividend yield Earning yield Key considerations in utilising PASSIVE and Smart Beta solutions in retirement fund

BATSETA Durban 2016 Mark Davids Head of Pre-retirement Investments Liberty Corporate VALUE Dividend yield Earning yield Key considerations in utilising PASSIVE and Smart Beta solutions in retirement fund

Joint Forum. 4th Quarter Investment report to the. Sanlam Umbrella Fund. Create STRENGTH in numbers

Investment report to the Joint Forum 4th Quarter 2014 Sanlam Umbrella Fund Create STRENGTH in numbers Sanlam Umbrella Fund Section Page number Background & Overview of the Fund 2 Default Strategies 3 Short

Investment report to the Joint Forum 4th Quarter 2014 Sanlam Umbrella Fund Create STRENGTH in numbers Sanlam Umbrella Fund Section Page number Background & Overview of the Fund 2 Default Strategies 3 Short

In thousands Actual (113) 6m MA (198) 12m MA (191) Dec-07 Dec-09 Dec-11 Dec-13 Dec-15 Dec-17

6m MA (198) 12m MA (191) Dec-07 Dec-09 Dec-11 Dec-13 Dec-15 Dec-17") may 2018 400 200 In thousands 0-200 -400-600 Actual (113) 6m MA (198) 12m MA (191) -800 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15 Dec-17 40 30 Eurozone France Italy Portugal Germany Spain Greece Ireland 20 10

may 2018 400 200 In thousands 0-200 -400-600 Actual (113) 6m MA (198) 12m MA (191) -800 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15 Dec-17 40 30 Eurozone France Italy Portugal Germany Spain Greece Ireland 20 10

OUTLOOK 2014/2015. BMO Asset Management Inc.

OUTLOOK 2014/2015 BMO Asset Management Inc. We would like to take this opportunity to provide our capital markets outlook for the remainder of 2014 and the first half of 2015 and our recommended asset

OUTLOOK 2014/2015 BMO Asset Management Inc. We would like to take this opportunity to provide our capital markets outlook for the remainder of 2014 and the first half of 2015 and our recommended asset

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Gill Marcus, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 27 March 2014 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Gill Marcus, Governor of the South African Reserve Bank Since the previous

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 27 March 2014 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Gill Marcus, Governor of the South African Reserve Bank Since the previous

Companies we invest in

Companies we invest in Top holdings 31 December 2017 Company Weight Alphabet 5.90 Mastercard 5.18 Wells Fargo 4.36 Morgan Stanley 3.95 Home Depot 3.94 Unilever 3.93 Siemens 3.83 Throughout 2017, we have

Companies we invest in Top holdings 31 December 2017 Company Weight Alphabet 5.90 Mastercard 5.18 Wells Fargo 4.36 Morgan Stanley 3.95 Home Depot 3.94 Unilever 3.93 Siemens 3.83 Throughout 2017, we have

MARKET & FUND COMMENTARY

MARKET & FUND COMMENTARY 10.2014 Global economics and geopolitical tension dominated in October. Policy and growth divergence amongst developed markets widened during the month, with the USA on the way

MARKET & FUND COMMENTARY 10.2014 Global economics and geopolitical tension dominated in October. Policy and growth divergence amongst developed markets widened during the month, with the USA on the way

General Investor Report as at 31/03/2018

STANLIB TOP40 ETF A 49,24 0,27 13 788 601 The investment objective of the STANLIB TOP40 Exchange Traded Fund is to provide returns that replicate the performance of the FTSE/JSE TOP40 Index ( the index

STANLIB TOP40 ETF A 49,24 0,27 13 788 601 The investment objective of the STANLIB TOP40 Exchange Traded Fund is to provide returns that replicate the performance of the FTSE/JSE TOP40 Index ( the index

Snapshot of SA Economy

Snapshot of SA Economy Kgotso Radira 1 September 29 Economic Outlook Global share indices 2 Indices 18 16 14 12 1 8 6 4 25 26 27 28 29 S&P 5 FTSE 1 DAX Nikkei 3 Global interest rates 7 % 6 5 4 3 2 1 1999

Snapshot of SA Economy Kgotso Radira 1 September 29 Economic Outlook Global share indices 2 Indices 18 16 14 12 1 8 6 4 25 26 27 28 29 S&P 5 FTSE 1 DAX Nikkei 3 Global interest rates 7 % 6 5 4 3 2 1 1999

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 30 March 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 30 March 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

SOLUTIONS RANGE. Authorised Financial Services Provider (FSP 612)

") SOLUTIONS RANGE Authorised Financial Services Provider (FSP 612) MONEY MARKET AND ENHANCED YIELD FUNDS Money Market The fund aims to achieve returns above the STefI Call Index, while minimising the risk

SOLUTIONS RANGE Authorised Financial Services Provider (FSP 612) MONEY MARKET AND ENHANCED YIELD FUNDS Money Market The fund aims to achieve returns above the STefI Call Index, while minimising the risk

monthly fund fact sheets

investments monthly fund fact sheets month ended 31 may 2013 collective investments International Funds Multi-Asset Funds Factor Series Funds Income Funds Best Blend Funds Property Funds Equity Funds Please

investments monthly fund fact sheets month ended 31 may 2013 collective investments International Funds Multi-Asset Funds Factor Series Funds Income Funds Best Blend Funds Property Funds Equity Funds Please

Batseta Seminar. Understanding risk April 2016

Batseta Seminar Understanding risk April 2016 $350bn Global ETP cumulative flow The global ETP inflow 2015 Source: BlackRock ETP Landscape The global ETP inflow by asset class & exposure 2015 The SATRIX

Batseta Seminar Understanding risk April 2016 $350bn Global ETP cumulative flow The global ETP inflow 2015 Source: BlackRock ETP Landscape The global ETP inflow by asset class & exposure 2015 The SATRIX

Total

The following report provides in-depth analysis into the successes and challenges of the Northcoast Tactical Growth managed ETF strategy throughout 2017, important research into the mechanics of the strategy,

The following report provides in-depth analysis into the successes and challenges of the Northcoast Tactical Growth managed ETF strategy throughout 2017, important research into the mechanics of the strategy,

Investment Platform Portfolio List as at 1 December 2016

Investment Platform Portfolio List as at 1 December 2016 GENERAL INFORMATION OVERVIEW FEES (Excl. VAT) Name Hollard Prime Money Market Maximise interest income, preserve the fund s capital and provide

Investment Platform Portfolio List as at 1 December 2016 GENERAL INFORMATION OVERVIEW FEES (Excl. VAT) Name Hollard Prime Money Market Maximise interest income, preserve the fund s capital and provide

Monthly Feedback 31 March 2016 Ampersand Asset Management. CIS Minimum Disclosure Documents (MDDs) Ampersand Momentum CPI Plus 2 Fund of Funds

Ampersand Momentum CPI Plus 2 Fund of Funds") Monthly Feedback 31 March 2016 Ampersand Asset Management CIS Minimum Disclosure Documents (MDDs) Ampersand Momentum CPI Plus 2 Fund of Funds Ampersand Momentum CPI Plus 4 Fund of Funds Ampersand Momentum

Monthly Feedback 31 March 2016 Ampersand Asset Management CIS Minimum Disclosure Documents (MDDs) Ampersand Momentum CPI Plus 2 Fund of Funds Ampersand Momentum CPI Plus 4 Fund of Funds Ampersand Momentum

PIMCO: The New Neutral

PIMCO: The New Neutral Philanthropy Summit 2015 Investing in the New Neutral world April 2015 PIMCO Australia Pty Ltd ABN 54 084 280 508 AFS Licence 246862 Level 19, 363 George St. Sydney, NSW 2000 telephone:

PIMCO: The New Neutral Philanthropy Summit 2015 Investing in the New Neutral world April 2015 PIMCO Australia Pty Ltd ABN 54 084 280 508 AFS Licence 246862 Level 19, 363 George St. Sydney, NSW 2000 telephone:

Financial Market Outlook: Stock Rally Continues with Faster & Stronger GDP Rebound, Earnings Recovery & Liquidity

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

HSBC Fund Update. HSBC GIF Global Emerging Markets Bond. April Market overview. Portfolio strategy

HSBC Fund Update April 2016 HSBC GIF Global Emerging Markets Bond Market overview The rally in Emerging Market (EM) assets continued in March given the improvement in global risk sentiment on the back

HSBC Fund Update April 2016 HSBC GIF Global Emerging Markets Bond Market overview The rally in Emerging Market (EM) assets continued in March given the improvement in global risk sentiment on the back

MonitorING Turkey ING BANK A.Ş. Further fiscal support in the Medium Term Plan. Emerging Markets 4 October 2017

q ING BANK A.Ş. ECONOMIC RESEARCH GROUP MonitorING Turkey October 17 Emerging Markets October 17 USD/TRY MonitorING Turkey Further fiscal support in the Medium Term Plan In 17, accelerated spending and

q ING BANK A.Ş. ECONOMIC RESEARCH GROUP MonitorING Turkey October 17 Emerging Markets October 17 USD/TRY MonitorING Turkey Further fiscal support in the Medium Term Plan In 17, accelerated spending and

Absolute Return Manager Watch TM Survey for the month ending July 2018

JULY 2018 2018/07/31 2018/05/01 2018/01/01 2017/08/01 2015/08/01 2013/08/01 2011/08/01 2008/08/01 Month Ending JULY 2018 2018/04/01 2018/01/01 2017/09/01 2017/05/01 2015/05/01 2011/05/01 2008/05/01 CPI

JULY 2018 2018/07/31 2018/05/01 2018/01/01 2017/08/01 2015/08/01 2013/08/01 2011/08/01 2008/08/01 Month Ending JULY 2018 2018/04/01 2018/01/01 2017/09/01 2017/05/01 2015/05/01 2011/05/01 2008/05/01 CPI

This document is intended for use by intermediaries.

ECONOMIC REPORT b y G l a c i e r R e s e a r c h 2 2 S e p t e m b e r 2 0 1 6 REVIEW PERIOD: AUGUST 2016 S U M M A R Y August saw continued refinement of reactions by investors to Brexit, as many sought

ECONOMIC REPORT b y G l a c i e r R e s e a r c h 2 2 S e p t e m b e r 2 0 1 6 REVIEW PERIOD: AUGUST 2016 S U M M A R Y August saw continued refinement of reactions by investors to Brexit, as many sought

The New World of Investing in Exchange Traded Products (ETPs)

") The New World of Investing in Exchange Traded Products (ETPs) Presentation at: JSE / Investec / etfsa.co.za ETP Seminar 26 th February 2013 Mike Brown Managing Director etfsa.co.za Agenda What are Exchange

The New World of Investing in Exchange Traded Products (ETPs) Presentation at: JSE / Investec / etfsa.co.za ETP Seminar 26 th February 2013 Mike Brown Managing Director etfsa.co.za Agenda What are Exchange

Prudential International Investments Advisers, LLC. Global Investment Strategy May 2008

Prudential International Investments Advisers, LLC. Global Investment Strategy May 2008 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy May 2008 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

CHALLENGING BELIEFS THE SOUTH AFRICAN EXPERIENCE MANAGED VOLATILITY

CHALLENGING BELIEFS THE SOUTH AFRICAN EXPERIENCE MANAGED VOLATILITY Grant Watson Saliegh Salaam HIGH RISK = HIGH RETURN? Falling Risk Rising Risk 2 Source: Quantitative Investments, INET Negative returns

CHALLENGING BELIEFS THE SOUTH AFRICAN EXPERIENCE MANAGED VOLATILITY Grant Watson Saliegh Salaam HIGH RISK = HIGH RETURN? Falling Risk Rising Risk 2 Source: Quantitative Investments, INET Negative returns

MONTHLY PORTFOLIO REPORT May 2015

Funds MONTHLY PORTFOLIO REPORT May 2015 5 th Floor, Protea Place, 40 Dreyer Street, Claremont. Postnet Suite 64, Private Bag X1005, Claremont, 7735. T +27 (0)21 492 0200 DIRECTORS: DP du Plessis (Chairman)

Funds MONTHLY PORTFOLIO REPORT May 2015 5 th Floor, Protea Place, 40 Dreyer Street, Claremont. Postnet Suite 64, Private Bag X1005, Claremont, 7735. T +27 (0)21 492 0200 DIRECTORS: DP du Plessis (Chairman)

Q QUARTERLY PERSPECTIVES

Q2-219 QUARTERLY PERSPECTIVES Tavistock Wealth - Investment Team Outlook Christopher Peel - John Leiper - Andrew Pottie - Sekar Indran - Alex Livingstone India Turnbull - Jonah Levy - James Peel Welcome

Q2-219 QUARTERLY PERSPECTIVES Tavistock Wealth - Investment Team Outlook Christopher Peel - John Leiper - Andrew Pottie - Sekar Indran - Alex Livingstone India Turnbull - Jonah Levy - James Peel Welcome

Absolute Return Manager Watch TM Survey for the month ending April 2018

APRIL 201 2018/04/30 2018/02/01 2018/01/01 2017/05/01 2015/05/01 2013/05/01 2011/05/01 2008/05/01 Month Ending APRIL 2018 2018/01/01 2017/10/01 2017/09/01 2017/02/01 2015/02/01 2011/02/01 2008/02/01 CPI

APRIL 201 2018/04/30 2018/02/01 2018/01/01 2017/05/01 2015/05/01 2013/05/01 2011/05/01 2008/05/01 Month Ending APRIL 2018 2018/01/01 2017/10/01 2017/09/01 2017/02/01 2015/02/01 2011/02/01 2008/02/01 CPI

Eurozone Economic Watch. July 2018

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

MARKET & FUND COMMENTARY

MARKET & FUND COMMENTARY 04.2014 Over the course of a strong quarter ending April 2014, the JSE All Share Index rose by 9.6%, with large caps marginally outperforming small caps. Resources (RESI20) rose

MARKET & FUND COMMENTARY 04.2014 Over the course of a strong quarter ending April 2014, the JSE All Share Index rose by 9.6%, with large caps marginally outperforming small caps. Resources (RESI20) rose

Year to Date (%) 10 Years. Month (%)

10 Years. Month (%)") FLEXIPORTFOLIO Performance report 1 December 215 South African economic review Local economic news flow remains depressing. Following the 1.3 annualised contraction in GDP in the second quarter, the economy

FLEXIPORTFOLIO Performance report 1 December 215 South African economic review Local economic news flow remains depressing. Following the 1.3 annualised contraction in GDP in the second quarter, the economy

General Investor Report as at 30/09/2017

STANLIB TOP40 ETF - A A 49,91 0,27 14 089 053 The investment objective of the STANLIB TOP40 Exchange Traded Fund is to provide returns that replicate the performance of the FTSE/JSE TOP40 Index ( the index

STANLIB TOP40 ETF - A A 49,91 0,27 14 089 053 The investment objective of the STANLIB TOP40 Exchange Traded Fund is to provide returns that replicate the performance of the FTSE/JSE TOP40 Index ( the index

Multi-Manager Watch TM Survey for the month ending November 2016

NOVEMBER 20 2016/11/30 2016/09/01 2016/01/01 2015/12/01 2014/12/01 2013/12/01 2011/12/01 2009/12/01 2006/12/01 Multi-Manager Watch Survey Multi-Manager Watch TM Survey for the month ending November 2016

NOVEMBER 20 2016/11/30 2016/09/01 2016/01/01 2015/12/01 2014/12/01 2013/12/01 2011/12/01 2009/12/01 2006/12/01 Multi-Manager Watch Survey Multi-Manager Watch TM Survey for the month ending November 2016

Short Extension (130/30) Fund Strategy

Fund Strategy") Short Extension (130/30) Fund Strategy Richard Hasson Neil Brown Russell Bodill September 2009 Performance through Focus Why Select Equity Investments? Select Equity investment approach High conviction,

Short Extension (130/30) Fund Strategy Richard Hasson Neil Brown Russell Bodill September 2009 Performance through Focus Why Select Equity Investments? Select Equity investment approach High conviction,

Annual Report. year ended 30 june Momentum Collective Investments Scheme

Annual Report year ended 30 june Momentum Collective Investments Scheme contents Momentum Collective Investments Scheme Annual report for the year ended 30 June Chief executive officer s report 3 Report

Annual Report year ended 30 june Momentum Collective Investments Scheme contents Momentum Collective Investments Scheme Annual report for the year ended 30 June Chief executive officer s report 3 Report

Nedgroup Investments NPW Fund of Funds

Nedgroup Investments NPW Fund of Funds 2018 The Nedbank Private Wealth Fund of Funds A range of three actively managed multi-asset solutions, which mainly follow a specialist building blockapproach. Nedgroup

Nedgroup Investments NPW Fund of Funds 2018 The Nedbank Private Wealth Fund of Funds A range of three actively managed multi-asset solutions, which mainly follow a specialist building blockapproach. Nedgroup

RECM MONEY MARKET FUND (Class A) Minimum Disclosure Document - Period ended 30 April 2015

Minimum Disclosure Document - Period ended 30 April 2015") RECM MONEY MARKET FUND (Class A) The RECM Money Market Fund is a money market unit trust that provides a sensible cash portfolio with very competitive fees. The Fund aims to maximise interest income, preserve

RECM MONEY MARKET FUND (Class A) The RECM Money Market Fund is a money market unit trust that provides a sensible cash portfolio with very competitive fees. The Fund aims to maximise interest income, preserve

Sanlam Lifestage LIFESTAGE PROGRAMME LIFESTAGE PROGRAMME. How Sanlam Lifestage works. Sanlam Umbrella Fund Monthly Fact Sheet April 2018

Accumulator phase Preserver phase Sanlam Umbrella Monthly Fact Sheet April 2018 Sanlam Lifestage Mandate description Sanlam Lifestage is the s trustee approved default investment strategy and aims to meet

Accumulator phase Preserver phase Sanlam Umbrella Monthly Fact Sheet April 2018 Sanlam Lifestage Mandate description Sanlam Lifestage is the s trustee approved default investment strategy and aims to meet

The Matrix Review. December 2018

The Matrix Review December 2018 Why Matrix Fund Managers Diversified Business Long funds AUM = R5.9 billion Hedge funds AUM = R3.1 billion Robust investment process across asset classes Evolution Hedge

The Matrix Review December 2018 Why Matrix Fund Managers Diversified Business Long funds AUM = R5.9 billion Hedge funds AUM = R3.1 billion Robust investment process across asset classes Evolution Hedge

AMP MySuper. A lifecycle investment solution 31 DECEMBER 2017 QUARTERLY REPORT FOR EMPLOYERS AND ADVISERS

31 DECEMBER 2017 QUARTERLY REPORT FOR EMPLOYERS AND ADVISERS AMP MySuper A lifecycle investment solution All fund returns are quoted post fees and taxes AMP MYSUPER 1 Contents Message from your fund manager

31 DECEMBER 2017 QUARTERLY REPORT FOR EMPLOYERS AND ADVISERS AMP MySuper A lifecycle investment solution All fund returns are quoted post fees and taxes AMP MYSUPER 1 Contents Message from your fund manager

Market volatility to continue

How much more? Renewed speculation that financial institutions may report increased US subprime-related losses has sent equity markets tumbling. How much more bad news can investors expect going forward?

How much more? Renewed speculation that financial institutions may report increased US subprime-related losses has sent equity markets tumbling. How much more bad news can investors expect going forward?

South African Reserve Bank STATEMENT OF THE MONETARY POLICY COMMITTEE. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT 24 January 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous meeting of

South African Reserve Bank PRESS STATEMENT 24 January 2017 STATEMENT OF THE MONETARY POLICY COMMITTEE Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous meeting of

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Concentrated equity markets and ETF investing

Concentrated equity markets and ETF investing Towards more efficient portfolios Daniel R Wessels August 2011 1 Unfair situation For the skilful manager Market Concentrated market Sector weights Diversified

Concentrated equity markets and ETF investing Towards more efficient portfolios Daniel R Wessels August 2011 1 Unfair situation For the skilful manager Market Concentrated market Sector weights Diversified

Allan Gray Balanced Portfolio

Fund managers: Andrew Lapping, Duncan Artus, Jacques Plaut, Ruan Stander (Most foreign assets are invested in Orbis funds). Inception date: 5 April 2017 30 September 2018 Portfolio description and summary

Fund managers: Andrew Lapping, Duncan Artus, Jacques Plaut, Ruan Stander (Most foreign assets are invested in Orbis funds). Inception date: 5 April 2017 30 September 2018 Portfolio description and summary

Indexation at the Core

Indexation at the Core Behind the name change: Core and Satellite Approach to Portfolio Construction Active approach Core-Satellite approach Index approach Combines best of both worlds Seeks to outperform

Indexation at the Core Behind the name change: Core and Satellite Approach to Portfolio Construction Active approach Core-Satellite approach Index approach Combines best of both worlds Seeks to outperform

Foord Conservative Fund

Cash Value 2 (R 000s) ZA Reg 28 Foord Conservative Fund INVESTMENT OBJECTIVE The fund aims to provide investors with a net-of-fee return of 4% per annum above the annual change in the South African Consumer

Cash Value 2 (R 000s) ZA Reg 28 Foord Conservative Fund INVESTMENT OBJECTIVE The fund aims to provide investors with a net-of-fee return of 4% per annum above the annual change in the South African Consumer

November PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy November 2015 John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Theresa Miller Phone:

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy November 2015 John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Theresa Miller Phone:

Russia: Macro Outlook for 2019

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

MULTI MANAGER TARGET RETURN FUND

PENSIONS INVESTMENTS LIFE INSURANCE MULTI MANAGER TARGET RETURN FUND QUARTER 3 (Q3) 2016: JULY TO SEPTEMBER Welcome to the third edition of the Multi Manager Target Return Fund quarterly updates. In this

PENSIONS INVESTMENTS LIFE INSURANCE MULTI MANAGER TARGET RETURN FUND QUARTER 3 (Q3) 2016: JULY TO SEPTEMBER Welcome to the third edition of the Multi Manager Target Return Fund quarterly updates. In this

february 2019

february 2019 Momentum multi-managed life stage portfolios returns for february 2019 Lifestages progression The portfolio range has a lifestage model which allows a member of a retirement fund

february 2019 Momentum multi-managed life stage portfolios returns for february 2019 Lifestages progression The portfolio range has a lifestage model which allows a member of a retirement fund

Investec Global Gold I Acc GBP

Fund Summary Quick Stats Citi Code AEE1 FE Crown Rating Price Date 13/07/2018 ISIN Code SEDOL Code GB00B1XFGM25 B1XFGM2 Morningstar Analyst Rating Mid Price 123.63p (+0.60p) S&P Capital IQ Grading Bid

Fund Summary Quick Stats Citi Code AEE1 FE Crown Rating Price Date 13/07/2018 ISIN Code SEDOL Code GB00B1XFGM25 B1XFGM2 Morningstar Analyst Rating Mid Price 123.63p (+0.60p) S&P Capital IQ Grading Bid

DIVERSIFIED ALTERNATIVES

DIVERSIFIED ALTERNATIVES Contents Introduction Investment philosophy Economic themes Investment process Key characteristics Key risks and how they are mitigated Diversified s STANLIB Multi-Manager Diversified

DIVERSIFIED ALTERNATIVES Contents Introduction Investment philosophy Economic themes Investment process Key characteristics Key risks and how they are mitigated Diversified s STANLIB Multi-Manager Diversified

BROAD COMMODITY INDEX

BROAD COMMODITY INDEX COMMENTARY + STRATEGY FACTS JUNE 2017 80.00% CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) 60.00% 40.00% 20.00% 0.00% -20.00% -40.00% -60.00% -80.00% ABCERI S&P GSCI ER BCOMM ER

BROAD COMMODITY INDEX COMMENTARY + STRATEGY FACTS JUNE 2017 80.00% CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) 60.00% 40.00% 20.00% 0.00% -20.00% -40.00% -60.00% -80.00% ABCERI S&P GSCI ER BCOMM ER

The active ingredient in markets and passive s growth

The Allocator September 1, 2017 The active ingredient in markets and passive s growth David Bianco Chief Investment Strategist, Americas Deutsche Asset Management Active and Passive asset management will

The Allocator September 1, 2017 The active ingredient in markets and passive s growth David Bianco Chief Investment Strategist, Americas Deutsche Asset Management Active and Passive asset management will

ISCF ishares Edge MSCI Multifactor Intl Small-Cap ETF

ishares Edge MSCI Multifactor Intl Small-Cap ETF ETF.com segment: Equity: Developed Markets Ex-U.S. - Small Cap Competing ETFs: FDTS, SCZ, SCHC, GWX, FNDC Related ETF Channels: Developed Markets Ex-U.S.,

ishares Edge MSCI Multifactor Intl Small-Cap ETF ETF.com segment: Equity: Developed Markets Ex-U.S. - Small Cap Competing ETFs: FDTS, SCZ, SCHC, GWX, FNDC Related ETF Channels: Developed Markets Ex-U.S.,

The World of ETFs: Diversification, Transparency, Low Cost and Access to All Asset Classes

The World of ETFs: Diversification, Transparency, Low Cost and Access to All Asset Classes FSP Invest Protect & Prosper Symposium 20 th October 2012 Mike Brown Managing Director etfsa.co.za Agenda What

The World of ETFs: Diversification, Transparency, Low Cost and Access to All Asset Classes FSP Invest Protect & Prosper Symposium 20 th October 2012 Mike Brown Managing Director etfsa.co.za Agenda What

FNB PROPERTY MARKET ANALYTICS

1 June 21 FNB MAY HOUSE PRICE INDEX AND PROPERTY ECONOMIC REVIEW - Price growth acceleration continues, with expected peak believed to be nearing MARKET ANALYTICS JOHN LOOS: FNB HOME LOANS STRATEGIST 11-64912

1 June 21 FNB MAY HOUSE PRICE INDEX AND PROPERTY ECONOMIC REVIEW - Price growth acceleration continues, with expected peak believed to be nearing MARKET ANALYTICS JOHN LOOS: FNB HOME LOANS STRATEGIST 11-64912

Market Perspectives The Year Ahead 2019

Market Perspectives The Year Ahead 2019 TD Wealth Asset Allocation Committee (WAAC) Overview Overweight equities and underweight fixed income as equity valuations now discount global earnings slowdown

Market Perspectives The Year Ahead 2019 TD Wealth Asset Allocation Committee (WAAC) Overview Overweight equities and underweight fixed income as equity valuations now discount global earnings slowdown

PRUDENTIAL PORTFOLIO MANAGERS UNIT TRUSTS LIMITED ANNUAL REPORT

PRUDENTIAL PORTFOLIO MANAGERS UNIT TRUSTS LIMITED ANNUAL REPORT MANAGING DIRECTOR S REPORT 31 DECEMBER 2017 Dear Investor, 2017: A surprisingly good year for SA investors In the face of poor economic conditions

PRUDENTIAL PORTFOLIO MANAGERS UNIT TRUSTS LIMITED ANNUAL REPORT MANAGING DIRECTOR S REPORT 31 DECEMBER 2017 Dear Investor, 2017: A surprisingly good year for SA investors In the face of poor economic conditions

Prudential International Investments Advisers, LLC. Global Investment Strategy June 2009

Prudential International Investments Advisers, LLC. Global Investment Strategy June 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy June 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

DBEM Xtrackers MSCI Emerging Markets Hedged Equity ETF

Xtrackers MSCI Emerging Markets Hedged Equity ETF ETF.com segment: Equity: Emerging Markets - Total Market Competing ETFs: HEEM, RFEM, TLEH, HEMV, LVHE Related ETF Channels: Total Market, Emerging Markets,

Xtrackers MSCI Emerging Markets Hedged Equity ETF ETF.com segment: Equity: Emerging Markets - Total Market Competing ETFs: HEEM, RFEM, TLEH, HEMV, LVHE Related ETF Channels: Total Market, Emerging Markets,

Monthly Client Investment Report: Kruger Ci Global Fund of Funds

Monthly Client Investment Report: Kruger Ci Global Fund of Funds April 2018 Kruger International Market Commentary International: Equity markets rebounded in April amid the easing of geopolitical tension

Monthly Client Investment Report: Kruger Ci Global Fund of Funds April 2018 Kruger International Market Commentary International: Equity markets rebounded in April amid the easing of geopolitical tension

1 February 2016 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT. JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST

1 February 2016 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST 087-328 0157

1 February 2016 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za THEO SWANEPOEL: PROPERTY MARKET ANALYST 087-328 0157

GRAYSWAN SCORECARDS 01 DECEMBER 2017

GRAYSWAN SCORECARDS 01 DECEMBER 2017 Gray Swan Financial Services (Pty) Ltd (Reg No: 2010/009813/07) is an authorised Financial Services Provider (FSP No: 42290). we keep the score, you secure the win

GRAYSWAN SCORECARDS 01 DECEMBER 2017 Gray Swan Financial Services (Pty) Ltd (Reg No: 2010/009813/07) is an authorised Financial Services Provider (FSP No: 42290). we keep the score, you secure the win

RECM MONEY MARKET FUND (Class A) Minimum Disclosure Document - Period ended 30 September 2018

Minimum Disclosure Document - Period ended 30 September 2018") RECM MONEY MARKET FUND (Class A) FUND FACTS Portfolio Manager ASISA Sector Fund Launch Date Inception Date (Class A) Total Fund Size Fund Size (Class A) Min. Investment (Lump Sum) Min. Investment (Monthly)

RECM MONEY MARKET FUND (Class A) FUND FACTS Portfolio Manager ASISA Sector Fund Launch Date Inception Date (Class A) Total Fund Size Fund Size (Class A) Min. Investment (Lump Sum) Min. Investment (Monthly)