Chapter 10. Basic financial. Basic Financial Concepts

|

|

|

- Melina Webb

- 5 years ago

- Views:

Transcription

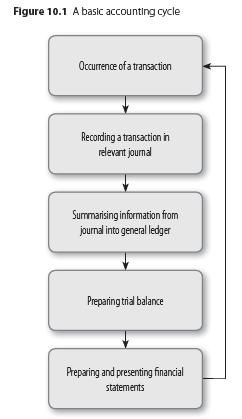

1 Chapter 10 Basic financial conceptschapter 10 Basic Financial Concepts

2 Learning outcomes Describe the purpose of accounting Explain the basic accounting cycle Define entity and explain the concept Explain the purpose of financial statements Define and classify income, expenses, assets, equity, and liabilities Prepare an elementary statement of comprehensive income (income statement) and statement of financial position (balance sheet) Discuss the duality concept

3 Learning outcomes (cont.) Describe who uses financial statements and their information needs Discuss the management of assets, equity and liabilities Discuss the use of financial ratios and how it can help to manage your finances Conduct a financial-ratio analysis Discuss the use of the Balanced Scorecard as a financial performance management tool Name and discuss the various sources of finance and circumstances in which they can be used

4 Accounting defined A continuous scientific process that involves bookkeeping and reporting. It can be divided into two domains: Financial accounting: reporting of financial activities to external users of financial information Management accounting: reporting of financial activities to internal users of financial information

5

6 Entity An economic unit Operates separately from other units Financial statements are recorded separately from any other unit Can be a person, partnership, CC, company or charitable organisation

7 Purpose of financial statements To provide information about the entity s: Financial position, financial performance and cash flow situation, that is useful for economic decision-making

8 Purpose of financial statements (cont.) Three primary financial statements used for reporting: o Statement of profit or loss and other comprehensive income (income statement) o Statement of financial position (balance sheet) o Statement of cash flows (cash-flow statement)

9 Elements of financial statements Income: Increases in economic benefits During an accounting period In the form of an increase or inflow of assets, or otherwise the decrease in liabilities which leads to an increase in equity This excludes increases because of owners contributions

10 Elements of financial statements (cont.) Expenses: Decreases in economic benefits During an accounting period In the form of an outflow or decrease in assets, or otherwise the increase in liabilities which leads to a decrease in equity This excludes decreases because of distributions to owners Any money that was spent or due to be spent in the operation of an entity during a specific accounting period

11 Assets: Elements of financial statements (cont.) Resources Controlled by an entity As a result of past events From which future economic benefits will flow to the entity Non-current assets: assets that will not be converted into cash within the following 12 months Current assets: assets that will be converted into cash within the following 12 months

12 Elements of financial statements Equity: The remaining interest in assets after liabilities (obligations) have been deducted from assets Thus, An owner s interest in assets against which creditors have no claim

13 Elements of financial statements Liabilities: A present obligation That arose from a past event The settlement will cause an outflow of future economic resources

14 Duality concept

15

16 Types of financial information Financial information: information expressed in numeric format of financial nature. Divided into: o Monetary information: financial information expressed in terms of a currency e.g. Rands o Non-monetary information: financial information not expressed in terms of a currency, but rather in financial ratios, quantities and percentages

17 Types of financial information (cont.) Non-financial information: information expressed in numeric format, but not of financial nature

18 Financial management Management: planning, organising, leading and controlling activities Management of assets o Non-current: land, buildings, equipment etc. o Current: debtors, inventory, cash and equivalents Management of equity Management of liabilities

19 Financial ratio analysis Liquidity ratios Current ratio: Current assets Current liabilities Acid-test ratio: (Current assets Inventory) Current liabilities

20 Activity ratios Inventory turnover rate: Cost of inventory sold Inventory Debtors collection period: Debtors (trade) Average sales per day = Debtors (trade) Annual sales 365

21 Activity ratios (cont.) Creditors payment period: Creditors (trade) Average purchases per day = Creditors (trade) (Average purchases 365) Non-current asset turnover: Sales Non-current assets (at carrying amount) Total asset turnover: Sales Total assets

22 Debt ratio: Debt ratios Total liabilities Total assets Debt-equity ratio: Non-current liabilities Equity Times interest earned: Earnings before interest and taxes Interest

23 Profitability ratios Gross profit margin: [(Sales Cost of sales) Sales] x 100 Operating profit margin: (Earnings before interest and taxes Sales) x 100 Net profit margin: (Profit for the year Sales) x 100 Return on investment: (Profit for the year Total assets) x 100

24 Return on equity: (Profit for the year Equity) x 100 Earnings per share: Profit available for ordinary shareholders Number of ordinary shares in issue P/E ratio: Profitability ratios (cont.) Market price per ordinary share Earnings per share

25 Financing capital requirements Financing strategies: o Aggressive financing strategy o Conservative financing strategy o Mid-way strategy Choice of strategy depends on: o Combination of non-current and current external capital o Combination of ordinary share capital plus reserves together with external non-current capital o Financing through own internal funds

26 Sources of finance Internal sources: o Own equity o Profit or earnings o Speeding up collections from customers o Credit from suppliers External sources: Long-term finance o Long-term loan o Debentures

27 Sources of finance (cont.) Intermediate (mid-term) finance: o Leases o Operating lease o Financial lease Short-term financing: o Trade credit o Bank credit o Banker s acceptance Factoring

28 Sources of start-up finance for entrepreneurs Business Partners Limited:. web: Commercial Banks: ABSA Bank: First National Bank: Nedbank: Standard Bank: Khula Enterprise Finance: web:

29 Sources of start-up finance for entrepreneurs (cont.) Industrial Development Corporation (IDC): web: Other useful websites include:

Name of business Statement of cash flows for the financial year end 31 December 20X1 (DIRECT METHOD) Inflow /(outflow)

Inflow /(outflow)") Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

MNB102-E. Tel: (012)

") MNB102-E LECTURER : Mr ABRAM PHENYA Email: Phenyam@unisa.ac.za Tel: (012) 429-4493 Financial management function (Page 408) Cash inflow Inflow of funds BUSINESS Cash outflow Outflow of funds Financial

MNB102-E LECTURER : Mr ABRAM PHENYA Email: Phenyam@unisa.ac.za Tel: (012) 429-4493 Financial management function (Page 408) Cash inflow Inflow of funds BUSINESS Cash outflow Outflow of funds Financial

Cranswick Plc is a food supplier company listed on the London Stock Exchange. The following

Financial Ratio Analysis Cranswick Plc is a food supplier company listed on the London Stock Exchange. The following represent ratios for the company for the year ended 31 st March 2012. Investors ratios

Financial Ratio Analysis Cranswick Plc is a food supplier company listed on the London Stock Exchange. The following represent ratios for the company for the year ended 31 st March 2012. Investors ratios

Analysis and Interpretation of Financial Statements

Analysis and Interpretation of Financial Statements Prof Pieter Pelle INTRODUCTION Objective of financial reporting provide information for decision making Primary statements income statement, balance

Analysis and Interpretation of Financial Statements Prof Pieter Pelle INTRODUCTION Objective of financial reporting provide information for decision making Primary statements income statement, balance

LIQUIDITY MANAGEMENT Presentation by: CPA Richard Kamami Secretary, PSB,Murang a PSB 23rd November 2017

LIQUIDITY MANAGEMENT Presentation by: CPA Richard Kamami Secretary, PSB,Murang a PSB 23rd November 2017 Uphold public interest Outline Definitions Assessment of Liquidity Criticism Liquidity Management

LIQUIDITY MANAGEMENT Presentation by: CPA Richard Kamami Secretary, PSB,Murang a PSB 23rd November 2017 Uphold public interest Outline Definitions Assessment of Liquidity Criticism Liquidity Management

ACCOUNTANCY. Part B. Q17. State the significance of Analysis of Financial Statements to the Lenders. (1 mark)

") ACCOUNTANCY [Time allowed: 3 hours] [Maximum marks:80] General Instructions: (i) This question paper contains three parts A, B and C. (ii) Part A is compulsory for all candidates. (iii) Candidates can

ACCOUNTANCY [Time allowed: 3 hours] [Maximum marks:80] General Instructions: (i) This question paper contains three parts A, B and C. (ii) Part A is compulsory for all candidates. (iii) Candidates can

Financial and Management Accounting Concepts

Financial and Management Accounting Concepts Editorial This month's newsletter focuses on the way in which you can interpret fully the information you present in the form of financial statements to either

Financial and Management Accounting Concepts Editorial This month's newsletter focuses on the way in which you can interpret fully the information you present in the form of financial statements to either

> > > > > > > > Chapter 16. Understanding Accounting and Financial Statements

> > > > > > > > Chapter 16 Understanding Accounting and Financial Statements 1 2 3 Explain the functions and importance of accounting, and identify the three basic activities involving accounting. Describe

> > > > > > > > Chapter 16 Understanding Accounting and Financial Statements 1 2 3 Explain the functions and importance of accounting, and identify the three basic activities involving accounting. Describe

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

CHAPTER 14 FINANCIAL MANAGEMENT

CHAPTER 14 FINANCIAL MANAGEMENT Chapter content Introduction The financial function and financial management Concepts in financial management Objective and fundamental principles of financial management

CHAPTER 14 FINANCIAL MANAGEMENT Chapter content Introduction The financial function and financial management Concepts in financial management Objective and fundamental principles of financial management

MULTIPLE CHOICE QUESTIONS CHAPTERS 6 10

MULTIPLE CHOICE QUESTIONS CHAPTERS 6 10 CHAPTER 6 1. Each T account contains the exact amount owing to a supplier (A) Sales ledger (B) Purchases ledger (C) General ledger (D) Cash book 2. The Trial balance

MULTIPLE CHOICE QUESTIONS CHAPTERS 6 10 CHAPTER 6 1. Each T account contains the exact amount owing to a supplier (A) Sales ledger (B) Purchases ledger (C) General ledger (D) Cash book 2. The Trial balance

2/2/2009. Financial statement EARNING POWER AND IRREGULAR ITEMS. EARNING POWER AND IRREGULAR ITEMS continued. Chapter 14

Chapter 14 Financial statement analysis PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd EARNING POWER AND IRREGULAR ITEMS Earning power refers to

Chapter 14 Financial statement analysis PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd EARNING POWER AND IRREGULAR ITEMS Earning power refers to

Consolidated Cash Flow Statement for the year ended 30th June, 2002

Consolidated Cash Flow Statement for the year ended 30th June, 2002 Notes Net cash inflow from operating activities (a) 4,916,217 6,797,641 Returns on investments and servicing of finance Interest received

Consolidated Cash Flow Statement for the year ended 30th June, 2002 Notes Net cash inflow from operating activities (a) 4,916,217 6,797,641 Returns on investments and servicing of finance Interest received

GRADE 11 TEST ON ADJUSTMENTS FOR MORE TESTS AND TASKS REFER TO THE GRADE 11 STUDY GUIDE

GRADE 11 TEST ON ADJUSTMENTS FOR MORE TESTS AND TASKS REFER TO THE GRADE 11 STUDY GUIDE FINANCIAL STATEMENTS (80 marks; 48 minutes) You are provided with information relating to BB Spaza, which is owned

GRADE 11 TEST ON ADJUSTMENTS FOR MORE TESTS AND TASKS REFER TO THE GRADE 11 STUDY GUIDE FINANCIAL STATEMENTS (80 marks; 48 minutes) You are provided with information relating to BB Spaza, which is owned

COMPANIES INTERPRETATION OF FINANCIAL STATEMENTS 13 MARCH 2014

COMPANIES INTERPRETATION OF FINANCIAL STATEMENTS 13 MARCH 2014 In this lesson we: Introduction Lesson Description Look at analysing financial statements and its purpose Consider users of financial statements

COMPANIES INTERPRETATION OF FINANCIAL STATEMENTS 13 MARCH 2014 In this lesson we: Introduction Lesson Description Look at analysing financial statements and its purpose Consider users of financial statements

ACCOUNTING RATIOS ACTIVITY / TURNOVER RATIOS BY- ANUJ JINDAL

ACCOUNTING RATIOS ACTIVITY / TURNOVER RATIOS BY- ANUJ JINDAL ACTIVITY/ TURNOVER/ EFFICIENCY RATIOS Rapidity with which the resources available to the concern are being used to produce revenue from operations

ACCOUNTING RATIOS ACTIVITY / TURNOVER RATIOS BY- ANUJ JINDAL ACTIVITY/ TURNOVER/ EFFICIENCY RATIOS Rapidity with which the resources available to the concern are being used to produce revenue from operations

Chapter 13 Financial management

Chapter 13 Financial management 1. Concept in financial management... 3 1.1. Balance sheet, asset and financing structure... 3 1.2. Capital... 3 1.3. Income... 3 1.4. Costs... 4 1.4.1. Fixed costs... 4

Chapter 13 Financial management 1. Concept in financial management... 3 1.1. Balance sheet, asset and financing structure... 3 1.2. Capital... 3 1.3. Income... 3 1.4. Costs... 4 1.4.1. Fixed costs... 4

[Prepared by ~~~ Hina Saleem Butt~~~ ms ]

![[Prepared by ~~~ Hina Saleem Butt~~~ ms ]](/thumbs/94/122314826.jpg "[Prepared by ~~~ Hina Saleem Butt~~~ ms ]") Practice question from different books Short term financial planning Solution/:- Average = (Opening + Ending) / 2 Operating Cycle = Inventory Period + A/R period = 64.15 + 28.61 = 92.76 Cash Cycle= Operating

Practice question from different books Short term financial planning Solution/:- Average = (Opening + Ending) / 2 Operating Cycle = Inventory Period + A/R period = 64.15 + 28.61 = 92.76 Cash Cycle= Operating

REVISING CASH FLOW AND RATIO ANALYSIS 21 AUGUST 2014

REVISING CASH FLOW AND RATIO ANALYSIS 21 AUGUST 2014 Lesson Description In this lesson we: Focus on Cash Flow Statements and calculations Look at ratio calculations and comments. Test Yourself The information

REVISING CASH FLOW AND RATIO ANALYSIS 21 AUGUST 2014 Lesson Description In this lesson we: Focus on Cash Flow Statements and calculations Look at ratio calculations and comments. Test Yourself The information

New Horizon School Assignment No.-1 ( ) Sub:- Accountancy Class -XII

Sub:- Accountancy Class -XII") New Horizon School Assignment No.-1 (2018-19) Sub:- Accountancy Class -XII TOPIC FINANCIAL STATEMENTS OF A COMPANY Q1) State the conditions under which shares are disclosed in the Balance Sheet of the

New Horizon School Assignment No.-1 (2018-19) Sub:- Accountancy Class -XII TOPIC FINANCIAL STATEMENTS OF A COMPANY Q1) State the conditions under which shares are disclosed in the Balance Sheet of the

The statement of cash flows reports cash flows, cash receipts, and cash payments, to show where cash came from and how it was spent.

Accounting Fundamentals Lesson 10 10.0 Cash Flow Statement The balance sheet reports financial position, and balance sheets from two periods show whether cash increased or decreased. But that doesn t tell

Accounting Fundamentals Lesson 10 10.0 Cash Flow Statement The balance sheet reports financial position, and balance sheets from two periods show whether cash increased or decreased. But that doesn t tell

(DHHM/DBM/DMM/DHRM/ DFM/DIB/DIM/DBFM 01)

") (DHHM/DBM/DMM/DHRM/ DFM/DIB/DIM/DBFM 01) COMMON PAPER Paper - I : Perspectives of Management Answer any Five questions from the following 1) Explain the nature and scope of management. 2) What are the

(DHHM/DBM/DMM/DHRM/ DFM/DIB/DIM/DBFM 01) COMMON PAPER Paper - I : Perspectives of Management Answer any Five questions from the following 1) Explain the nature and scope of management. 2) What are the

MANAGEMENT PROGRAMME

No. of Printed Pages 5 MS-4 MANAGEMENT PROGRAMME Term-End Examination ) 1 4 0 June, 2014 MS-4 : ACCOUNTING AND FINANCE FOR MANAGERS Time : 3 hours Maximum Marks : 100 Note : Attempt any five questions.

No. of Printed Pages 5 MS-4 MANAGEMENT PROGRAMME Term-End Examination ) 1 4 0 June, 2014 MS-4 : ACCOUNTING AND FINANCE FOR MANAGERS Time : 3 hours Maximum Marks : 100 Note : Attempt any five questions.

Cash flow from financing activities. Cash flow from investing activities; Cash flow from operating activities;

COMPONENTS OF CASH FLOW STATEMENT The cash flow statement should report cash flows during the period classified by operating, investing and financing activities. Cash flow statement explains the reasons

COMPONENTS OF CASH FLOW STATEMENT The cash flow statement should report cash flows during the period classified by operating, investing and financing activities. Cash flow statement explains the reasons

Use the data provided to answer the questions that follow relating to Newtech Ltd for 2014: Abbreviated Balance Sheet:

POST GRAD DIPLOMA IN MANAGEMENT FINANCIAL MANAGEMENT REVISION QUESTIONS QUESTION 1 Use the data provided to answer the questions that follow relating to Newtech Ltd for 2014: Abbreviated Balance Sheet:

POST GRAD DIPLOMA IN MANAGEMENT FINANCIAL MANAGEMENT REVISION QUESTIONS QUESTION 1 Use the data provided to answer the questions that follow relating to Newtech Ltd for 2014: Abbreviated Balance Sheet:

GROUP PROFIT AND LOSS ACCOUNT

GROUP PROFIT AND LOSS ACCOUNT Continuing Continuing activities Goodwill activities before goodwill Amortisation before Operating Unaudited amortisation & operating Audited operating exceptional Total &

GROUP PROFIT AND LOSS ACCOUNT Continuing Continuing activities Goodwill activities before goodwill Amortisation before Operating Unaudited amortisation & operating Audited operating exceptional Total &

Chapter 18 Extra review questions

Accounting for Non-Accountants 10th Online Material 1 Chapter 18 Extra review questions 1 From the data presented below, calculate the following ratios for 2020 and 2021: Gross profit margin Current ratio

Accounting for Non-Accountants 10th Online Material 1 Chapter 18 Extra review questions 1 From the data presented below, calculate the following ratios for 2020 and 2021: Gross profit margin Current ratio

SUGGESTED SOLUTION INTERMEDIATE N 18 EXAM

SUGGESTED SOLUTION INTERMEDIATE N 18 EXAM SUBJECT- F.M. Test Code CIN 5021 (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e ANSWER-1

SUGGESTED SOLUTION INTERMEDIATE N 18 EXAM SUBJECT- F.M. Test Code CIN 5021 (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e ANSWER-1

Management of working capital

Management of working capital Gross Working Capital = Total of Current Assets. Net Working Capital (Working Capital Gap) = Current Assets - Current Liabilities Net Working Capital is also called Working

Management of working capital Gross Working Capital = Total of Current Assets. Net Working Capital (Working Capital Gap) = Current Assets - Current Liabilities Net Working Capital is also called Working

GRADE 12 CLASS TEST COMPANY 70 minutes; 120 marks

GRADE 12 CLASS TEST COMPANY 70 minutes; 120 marks QUESTION 1: BALANCE SHEET, NOTES AND RATIOS (90 marks) You are provided with information of Chuba Ltd, a public company, for the financial year ended 31

GRADE 12 CLASS TEST COMPANY 70 minutes; 120 marks QUESTION 1: BALANCE SHEET, NOTES AND RATIOS (90 marks) You are provided with information of Chuba Ltd, a public company, for the financial year ended 31

FINANCIAL MANAGEMENT

FINANCIAL MANAGEMENT Question 1: What is financial management? Explain the functions of financial management. (May 13, Nov 11) (Mark 7) Answer: Financial management is that specialized activity which is

FINANCIAL MANAGEMENT Question 1: What is financial management? Explain the functions of financial management. (May 13, Nov 11) (Mark 7) Answer: Financial management is that specialized activity which is

CASH FLOWS FROM OPERATING ACTIVITIES

1 CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers (calc a) Cash paid to suppliers and employees (calc b) Cash generated from / (used in) operations Dividends received Interest received

1 CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers (calc a) Cash paid to suppliers and employees (calc b) Cash generated from / (used in) operations Dividends received Interest received

Resource Sheet Accounting

Resource Sheet Accounting Interpretation of Accounts Student Activity Answers (Q1) In the earlier Boyle plc question, calculate the following (use 2 decimal places where appropriate): (a) Return on Capital

Resource Sheet Accounting Interpretation of Accounts Student Activity Answers (Q1) In the earlier Boyle plc question, calculate the following (use 2 decimal places where appropriate): (a) Return on Capital

0079/ /en Annual Financial Report PETROLINA (HOLDINGS) PUBLIC LTD PHL

PUBLIC LTD PHL") 0079/00015500/en Annual Financial Report PETROLINA (HOLDINGS) PUBLIC LTD Annual Report 19 April 2016 ANNOUNCEMENT We wish to inform you that the Board of Directors of Petrolina (Holdings) Public Ltd met

0079/00015500/en Annual Financial Report PETROLINA (HOLDINGS) PUBLIC LTD Annual Report 19 April 2016 ANNOUNCEMENT We wish to inform you that the Board of Directors of Petrolina (Holdings) Public Ltd met

Understanding Financial Statements. Elizabeth Rankin

Understanding Financial Statements Elizabeth Rankin Overview Accounting Concepts Principles Financial Statements Evaluating Performance Horizontal Analysis Vertical Analysis Ratio Analysis Entity Concept

Understanding Financial Statements Elizabeth Rankin Overview Accounting Concepts Principles Financial Statements Evaluating Performance Horizontal Analysis Vertical Analysis Ratio Analysis Entity Concept

NATIONAL SENIOR CERTIFICATE ACCOUNTING GRADE 12 NOVEMBER 2015 SPECIAL ANSWER BOOK

CENTRE NUMBER EXAMINATION NUMBER NATIONAL SENIOR CERTIFICATE ACCOUNTING GRADE 12 NOVEMBER 2015 SPECIAL ANSWER BOOK QUESTION MARKS INITIAL MOD. 1 2 3 4 5 TOTAL This answer book consists of 15 pages. Accounting

CENTRE NUMBER EXAMINATION NUMBER NATIONAL SENIOR CERTIFICATE ACCOUNTING GRADE 12 NOVEMBER 2015 SPECIAL ANSWER BOOK QUESTION MARKS INITIAL MOD. 1 2 3 4 5 TOTAL This answer book consists of 15 pages. Accounting

CHAPTERS COVERED : CHAPTERS 1-8, 10 & LEARNER GUIDE : STUDY UNITS 1-4 & 8. DUE DATE : 3:00 p.m. 21 AUGUST 2012

Page 1 of 6 ASSIGNMENT 2 ND SEMESTER : FINANCIAL MANAGEMENT () CHAPTERS COVERED : CHAPTERS 1-8, 10 & 21-24 LEARNER GUIDE : STUDY UNITS 1-4 & 8 DUE DATE : 3:00 p.m. 21 AUGUST 2012 TOTAL MARKS : 100 INSTRUCTIONS

Page 1 of 6 ASSIGNMENT 2 ND SEMESTER : FINANCIAL MANAGEMENT () CHAPTERS COVERED : CHAPTERS 1-8, 10 & 21-24 LEARNER GUIDE : STUDY UNITS 1-4 & 8 DUE DATE : 3:00 p.m. 21 AUGUST 2012 TOTAL MARKS : 100 INSTRUCTIONS

TOTAL TRAINING SOLUTIONS

TOTAL TRAINING SOLUTIONS Global Cash Flow Analysis Get Global by Understanding Global Cash Flow Jeffery W. Johnson Bankers Insight Group jeffery.johnson@bankers-insight.com 770-846-4511 September 2015

TOTAL TRAINING SOLUTIONS Global Cash Flow Analysis Get Global by Understanding Global Cash Flow Jeffery W. Johnson Bankers Insight Group jeffery.johnson@bankers-insight.com 770-846-4511 September 2015

MARK SCHEME for the November 2004 question paper 9706 ACCOUNTING

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Advanced Level MARK SCHEME for the November 2004 question paper 9706 ACCOUNTING 9706/04 Paper 4 Problem Solving (Supplementary Topics), maximum raw

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Advanced Level MARK SCHEME for the November 2004 question paper 9706 ACCOUNTING 9706/04 Paper 4 Problem Solving (Supplementary Topics), maximum raw

Rate = 1 n RV / C Where: RV = Residual Value C = Cost n = Life of Asset Calculate the rate if: Cost = 100,000

Solved by ABr & Chanda Rehman Final MCQs It is supposed that on 31st December, 2007, the sundry debtors are amounted to Rs. 40,000. On the basis of past experience, it is estimated that 10% of the sundry

Solved by ABr & Chanda Rehman Final MCQs It is supposed that on 31st December, 2007, the sundry debtors are amounted to Rs. 40,000. On the basis of past experience, it is estimated that 10% of the sundry

Part 5: GLOSSARY OF TERMS

Part 5: GLOSSARY OF TERMS ABN Withholding Tax Account Levels Accounts Accounting Equation Accounts List Accounts Payable Accounts Receivable Accounting Period The amount withheld from a supplier who provides

Part 5: GLOSSARY OF TERMS ABN Withholding Tax Account Levels Accounts Accounting Equation Accounts List Accounts Payable Accounts Receivable Accounting Period The amount withheld from a supplier who provides

WEEK 10 Analysis of Financial Statements

WEEK 10 Analysis of Financial Statements Learning Objectives 1. Organize a systematic financial statements analysis using common-size financial statements and ratio analysis. 2. Recognize the potential

WEEK 10 Analysis of Financial Statements Learning Objectives 1. Organize a systematic financial statements analysis using common-size financial statements and ratio analysis. 2. Recognize the potential

Duration of online examination will be of 1 Hour 20 minutes (80 minutes).

.") Program Name: PGDBA Subject: Financial Management Assessment Name: FM - Exam Weightage: 70 Total Marks: 70 Duration: 80 mins Online Examination: Online examination is a Computer based examination. Online

Program Name: PGDBA Subject: Financial Management Assessment Name: FM - Exam Weightage: 70 Total Marks: 70 Duration: 80 mins Online Examination: Online examination is a Computer based examination. Online

CHAPTER - VI RATIO ANALYSIS 6.3 UTILITY OF RATIO ANALYSIS 6.4 LIMITATIONS OF RATIO ANALYSIS 6.5 RATIO TABLES, CHARTS, ANALYSIS AND

CHAPTER - VI RATIO ANALYSIS 6.1 INTRODUCTION 6.2 NATURE OF RATIO 6.3 UTILITY OF RATIO ANALYSIS 6.4 LIMITATIONS OF RATIO ANALYSIS 6.5 RATIO TABLES, CHARTS, ANALYSIS AND INTERPRETATION OF DIFFERENT RATIOS

CHAPTER - VI RATIO ANALYSIS 6.1 INTRODUCTION 6.2 NATURE OF RATIO 6.3 UTILITY OF RATIO ANALYSIS 6.4 LIMITATIONS OF RATIO ANALYSIS 6.5 RATIO TABLES, CHARTS, ANALYSIS AND INTERPRETATION OF DIFFERENT RATIOS

SOLUTION: ADVANCED FINANCIAL REPORTING, MAY 2014

SOLUTION 1(a) Goodwill is only calculated when control is gained. In substance, it is like the previously held investment is disposed of and a 70% controlled investment acquired. The previously held investment

SOLUTION 1(a) Goodwill is only calculated when control is gained. In substance, it is like the previously held investment is disposed of and a 70% controlled investment acquired. The previously held investment

Part A of examination paper

Prof Johan Burger 2017 Managing Institutional Capacity 1 Diploma Programme in Public Accountability Module code 13 206 171; twenty credits Preparation for November examination June examination MEMORANDUM

Prof Johan Burger 2017 Managing Institutional Capacity 1 Diploma Programme in Public Accountability Module code 13 206 171; twenty credits Preparation for November examination June examination MEMORANDUM

Cash Flow Statements. Chapter 15. Luby & O Donoghue (2005)

") Cash Flow Statements Chapter 15 Luby & O Donoghue (2005) Cash is king profits can be manufactured by creative accounting but creating cash is impossible. Terry Smith, Accounting for Growth Typical cash

Cash Flow Statements Chapter 15 Luby & O Donoghue (2005) Cash is king profits can be manufactured by creative accounting but creating cash is impossible. Terry Smith, Accounting for Growth Typical cash

Quantitative skills Ratios

gross profit margin Method To calculate gross profit margin, two figures from the income statement are needed: sales revenue and gross profit. The formula for calculating the gross profit margin is: Gross

gross profit margin Method To calculate gross profit margin, two figures from the income statement are needed: sales revenue and gross profit. The formula for calculating the gross profit margin is: Gross

HOW TO IMPROVE CASH FLOW

HOW TO IMPROVE CASH FLOW What causes cash flow problems? Allowing customers too much credit Overtrading How can cash flow be improved? Review trade credit with suppliers Review credit offered to customers

HOW TO IMPROVE CASH FLOW What causes cash flow problems? Allowing customers too much credit Overtrading How can cash flow be improved? Review trade credit with suppliers Review credit offered to customers

+44 (0) International Accounting Standards (IAS) Guidance: Terminology and Presentation

International Accounting Standards (IAS) Guidance: Terminology and Presentation") internationalenquiries@ediplc.com +44 (0) 2476 518951 www.lcci.org.uk International Accounting Standards (IAS) Guidance: Terminology and Presentation Contents Introduction 3 1 First Level 4 1.1 Terminology

internationalenquiries@ediplc.com +44 (0) 2476 518951 www.lcci.org.uk International Accounting Standards (IAS) Guidance: Terminology and Presentation Contents Introduction 3 1 First Level 4 1.1 Terminology

Interim Statement 2004/2005

Interim Statement 2004/2005 Financial Summary 2004/2005 2003/2004 m m Turnover 95.3 94.9 Operating profit before goodwill amortisation and exceptional items 3.5 3.6 Profit before tax, goodwill amortisation

Interim Statement 2004/2005 Financial Summary 2004/2005 2003/2004 m m Turnover 95.3 94.9 Operating profit before goodwill amortisation and exceptional items 3.5 3.6 Profit before tax, goodwill amortisation

IAS 7 : STATEMENT OF CASH FLOWS COMPILED BY: MR. YAGNESH DESAI.

IAS 7 : STATEMENT OF CASH FLOWS CASH FLOWS : TERMINOLOGY Inflows and outflows of cash and cash equivalents. CASH : Comprises cash on hand and demand deposits. CASH EQUIVALENTS : Short-term, highly liquid

IAS 7 : STATEMENT OF CASH FLOWS CASH FLOWS : TERMINOLOGY Inflows and outflows of cash and cash equivalents. CASH : Comprises cash on hand and demand deposits. CASH EQUIVALENTS : Short-term, highly liquid

Accounting Functions. The various financial statements are- Income Statement Balance Sheet

Accounting Functions The accounting system provides a structure of maintaining details of business transactions that represent the finances of the organization. The various financial statements are- Income

Accounting Functions The accounting system provides a structure of maintaining details of business transactions that represent the finances of the organization. The various financial statements are- Income

Class 12 Accountancy NCERT Solutions Cash Flow Statement

Class 12 Accountancy NCERT Solutions Cash Flow Statement TEST YOUR UNDERSTANDING I DO IT YOUR SELF I Question 1. The profit and loss account of Roy Limited is given here under Question 2. From the following

Class 12 Accountancy NCERT Solutions Cash Flow Statement TEST YOUR UNDERSTANDING I DO IT YOUR SELF I Question 1. The profit and loss account of Roy Limited is given here under Question 2. From the following

You are provided with the following transactions that took place during a recent fis-

Chapter 17 PROBLEMS: SET C You are provided with the following transactions that took place during a recent fis- P17-1C cal year. (a) (b) (c) (d) (e) (f) (g) (h) (i) (j) Cash Inflow, Where Reported Outflow,

Chapter 17 PROBLEMS: SET C You are provided with the following transactions that took place during a recent fis- P17-1C cal year. (a) (b) (c) (d) (e) (f) (g) (h) (i) (j) Cash Inflow, Where Reported Outflow,

- A resource - Controlled by the entity - As a result of a past event - From economic benefits are expected to flow to the entity.

Elements and recognition criteria 1. Identify the definition for each of these elements: a. Assets b. Liabilities c. Equity d. Income e. Expenses - A resource - Controlled by the entity - As a result of

Elements and recognition criteria 1. Identify the definition for each of these elements: a. Assets b. Liabilities c. Equity d. Income e. Expenses - A resource - Controlled by the entity - As a result of

Week 5, Chap3 Accounting 1A, Financial Accounting. Instructor: Michael Booth

Week 5, Chap3 Accounting 1A, Financial Accounting Instructor: Michael Booth Business Background How do business activities affect the income statement? How are these activities recognized and measured?

Week 5, Chap3 Accounting 1A, Financial Accounting Instructor: Michael Booth Business Background How do business activities affect the income statement? How are these activities recognized and measured?

ANALYSIS OF COMPANY FINANCIAL STATEMENTS 09 MAY 2013

ANALYSIS OF COMPANY FINANCIAL STATEMENTS 09 MAY 2013 Lesson Description In this lesson we: Focus on ratios affection liquidity, solvency, risk & returns Discuss ratio calculations & relevant comments Key

ANALYSIS OF COMPANY FINANCIAL STATEMENTS 09 MAY 2013 Lesson Description In this lesson we: Focus on ratios affection liquidity, solvency, risk & returns Discuss ratio calculations & relevant comments Key

FINANCIAL STATEMENT REVIEW TOOLKIT NOVEMBER 2018

FINANCIAL STATEMENT REVIEW TOOLKIT NOVEMBER 2018 Issued NOVEMBER 2018 VERSION 1 1 COPYRIGHT 2018 THE SOUTH AFRICAN INSTITUTE OF CHARTERED ACCOUNTANTS Copyright in all publications originated by The South

FINANCIAL STATEMENT REVIEW TOOLKIT NOVEMBER 2018 Issued NOVEMBER 2018 VERSION 1 1 COPYRIGHT 2018 THE SOUTH AFRICAN INSTITUTE OF CHARTERED ACCOUNTANTS Copyright in all publications originated by The South

Week 14, Chap14 Accounting 1A, Financial Accounting

Week 14, Chap14 Accounting 1A, Financial Accounting Analyzing Financial Statements Instructor: Michael Booth Understanding The Business Return on an equity security investment Dividends Increase in share

Week 14, Chap14 Accounting 1A, Financial Accounting Analyzing Financial Statements Instructor: Michael Booth Understanding The Business Return on an equity security investment Dividends Increase in share

INTRODUCTION FORMAT OF THE INCOME STATEMENT:

INTRODUCTION What is the Income Statement ( Earning Statement)? Income statement is the report that measures the success of a company operations for a given period of time. What is the Usefulness of income

INTRODUCTION What is the Income Statement ( Earning Statement)? Income statement is the report that measures the success of a company operations for a given period of time. What is the Usefulness of income

Performance Indicators for 6 years

Performance Indicators for 6 years FINANCIAL POSITION Balance sheet (Rupees in Thousand) Other noncurrent assets Total assets 2,084,856 6,544 2,436,65 2,040,33 11,386 2,257,568 4,417,23 1,803,2 101,268

Performance Indicators for 6 years FINANCIAL POSITION Balance sheet (Rupees in Thousand) Other noncurrent assets Total assets 2,084,856 6,544 2,436,65 2,040,33 11,386 2,257,568 4,417,23 1,803,2 101,268

BROAD-BASED BLACK ECONOMIC EMPOWERMENT TRANSACTION 18 December 2018

KHULA SIZWE BROAD-BASED BLACK ECONOMIC EMPOWERMENT TRANSACTION 18 December 2018 The Circular published on 18 December 2018 is the main source of detailed information on the proposed B-BBEE transaction,

KHULA SIZWE BROAD-BASED BLACK ECONOMIC EMPOWERMENT TRANSACTION 18 December 2018 The Circular published on 18 December 2018 is the main source of detailed information on the proposed B-BBEE transaction,

ASSIGNMENT MEMORANDUM

Page 1 of 6 ASSIGNMENT MEMORANDUM SUBJECT : FINANCIAL ACCOUNTING (FA) ASSIGNMENT : 1 st SEMESTER 2010 Markers: Any question found to be copied should only be given 40% of the initial mark awarded. QUESTION

Page 1 of 6 ASSIGNMENT MEMORANDUM SUBJECT : FINANCIAL ACCOUNTING (FA) ASSIGNMENT : 1 st SEMESTER 2010 Markers: Any question found to be copied should only be given 40% of the initial mark awarded. QUESTION

REVIEW PROBLEM Rockford Company s comparative balance sheet for 2012 and the company s income statement for the year follow:

REVIEW PROBLEM Rockford Company s comparative balance sheet for 2012 and the company s income statement for the year follow: Additional data: 1. Rockford paid a cash dividend in 2012. 2. The $4 million

REVIEW PROBLEM Rockford Company s comparative balance sheet for 2012 and the company s income statement for the year follow: Additional data: 1. Rockford paid a cash dividend in 2012. 2. The $4 million

IAB Level 4 Certificate in International Accounting Standards and IFRS 603/3017/X. Qualification Specification

IAB Level 4 Certificate in International Accounting Standards and IFRS 603/3017/X Qualification Specification Contents 1 Introduction to the qualification... 2 2 Statement of level... 2 3 Aims... 2 4 Target

IAB Level 4 Certificate in International Accounting Standards and IFRS 603/3017/X Qualification Specification Contents 1 Introduction to the qualification... 2 2 Statement of level... 2 3 Aims... 2 4 Target

BENEFITS OF CASH FLOW INFORMATION

16 Accounting Standard (AS) 3 Cash Flow Statements Contents OBJECTIVE SCOPE Paragraphs 1-2 BENEFITS OF CASH FLOW INFORMATION 3-4 DEFINITIONS 5-7 Cash and Cash Equivalents 6-7 PRESENTATION OF A CASH FLOW

16 Accounting Standard (AS) 3 Cash Flow Statements Contents OBJECTIVE SCOPE Paragraphs 1-2 BENEFITS OF CASH FLOW INFORMATION 3-4 DEFINITIONS 5-7 Cash and Cash Equivalents 6-7 PRESENTATION OF A CASH FLOW

MANAGEMENT PROGRAMME

MANAGEMENT PROGRAMME Kzt Term-End Examination (:)) December, 2009 : ACCOUNTING AND FINANCE FOR MANAGERS Time : 3 hours Maximum Marks : 100 (Weightage 70%) Note : Attempt any five questions. All questions

MANAGEMENT PROGRAMME Kzt Term-End Examination (:)) December, 2009 : ACCOUNTING AND FINANCE FOR MANAGERS Time : 3 hours Maximum Marks : 100 (Weightage 70%) Note : Attempt any five questions. All questions

Accounting Sample Questions and Answers

Accounting Sample Questions and Answers 1-Accounting provides information on (A) Cost and income for managers (B) Company s tax liability for a particular year (C) Financial conditions of an institution

Accounting Sample Questions and Answers 1-Accounting provides information on (A) Cost and income for managers (B) Company s tax liability for a particular year (C) Financial conditions of an institution

Time allowed : 3 hours Maximum marks : 100. Total number of questions : 8 Total number of printed pages : 12

: 1 : 222 Roll No... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 12 NOTE : All working notes should be shown distinctly. PART A (Answer Question

: 1 : 222 Roll No... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 12 NOTE : All working notes should be shown distinctly. PART A (Answer Question

NATIONAL SENIOR CERTIFICATE GRADE 12

NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING NOVEMBER 2009(1) MEMORANDUM MARKS: 300 This memorandum consists of 21 pages. Accounting 2 DoE/November 2009(1) QUESTION 1 1.1 Briefly explain why it is important

NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING NOVEMBER 2009(1) MEMORANDUM MARKS: 300 This memorandum consists of 21 pages. Accounting 2 DoE/November 2009(1) QUESTION 1 1.1 Briefly explain why it is important

MOCK TEST PAPER 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING. Suggested Answers/ Hints

: GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING. Suggested Answers/ Hints") MOCK TEST PAPER 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING Suggested Answers/ Hints 1. (a) (i) Standard input (kg.) of Material SW: Test Series:

MOCK TEST PAPER 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING Suggested Answers/ Hints 1. (a) (i) Standard input (kg.) of Material SW: Test Series:

STUDY UNITS COVERED : STUDY UNITS 1-5 & 7 CHAPTERS COVERED : CHAPTERS 1-5, 7, 8, 9 & 18. DUE DATE : 3:00 p.m. 18 March 2014

Page 1 of 7 ASSIGNMENT 1 ST SEMESTE : FINANCIAL MANAGEMENT STUDY UNITS COVEED : STUDY UNITS 1-5 & 7 CHAPTES COVEED : CHAPTES 1-5, 7, 8, 9 & 18 DUE DATE : 3:00 p.m. 18 March 2014 TOTAL MAKS : 100 INSTUCTIONS

Page 1 of 7 ASSIGNMENT 1 ST SEMESTE : FINANCIAL MANAGEMENT STUDY UNITS COVEED : STUDY UNITS 1-5 & 7 CHAPTES COVEED : CHAPTES 1-5, 7, 8, 9 & 18 DUE DATE : 3:00 p.m. 18 March 2014 TOTAL MAKS : 100 INSTUCTIONS

BSc.(Hons) Banking and International Finance, BSc.(Hons) Tourism and Hospitality Management, Diploma in Public Administration and Management

Banking and International Finance, BSc.(Hons) Tourism and Hospitality Management, Diploma in Public Administration and Management") BSc.(Hons) Banking and International Finance, BSc.(Hons) Tourism and Hospitality Management, Diploma in Public Administration and Management & BSc.(Hons) Public Administration and Management Cohort: BBIF/04/FT/PT

BSc.(Hons) Banking and International Finance, BSc.(Hons) Tourism and Hospitality Management, Diploma in Public Administration and Management & BSc.(Hons) Public Administration and Management Cohort: BBIF/04/FT/PT

Topic 8 Ratio Analysis. Higher Business Management

Topic 8 Ratio Analysis Higher Business Management 1 Learning Intentions / Success Criteria Learning Intentions Ratio analysis Success Criteria Learners should be able to describe and explain: the purpose

Topic 8 Ratio Analysis Higher Business Management 1 Learning Intentions / Success Criteria Learning Intentions Ratio analysis Success Criteria Learners should be able to describe and explain: the purpose

SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME

GENERAL / SPECIAL DEGREE PROGRAMME") All Rights Reserved No. of Pages - 15 No of Questions - 06 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR I SEMESTER II (Intake IV Group A) END SEMESTER

All Rights Reserved No. of Pages - 15 No of Questions - 06 SCHOOL OF ACCOUNTING AND BUSINESS BSc. (APPLIED ACCOUNTING) GENERAL / SPECIAL DEGREE PROGRAMME YEAR I SEMESTER II (Intake IV Group A) END SEMESTER

ANALYSIS OF THE FINANCIAL STATEMENTS

5 ANALYSIS OF THE FINANCIAL STATEMENTS CONTENTS PAGE STUDY OBJECTIVES 166 INTRODUCTION 167 METHODS OF STATEMENT ANALYSIS 167 A. ANALYSIS WITH THE AID OF FINANCIAL RATIOS 168 GROUPS OF FINANCIAL RATIOS

5 ANALYSIS OF THE FINANCIAL STATEMENTS CONTENTS PAGE STUDY OBJECTIVES 166 INTRODUCTION 167 METHODS OF STATEMENT ANALYSIS 167 A. ANALYSIS WITH THE AID OF FINANCIAL RATIOS 168 GROUPS OF FINANCIAL RATIOS

CHAPTER 12 STATEMENT OF CASH FLOWS

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS Material 1. The following information has been extracted from the records of a cotton merchant, for the month of March,

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS Material 1. The following information has been extracted from the records of a cotton merchant, for the month of March,

INSTITUTE OF ACTUARIES OF INDIA

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 14 th November 2011 Subject CT2 Finance and Financial Reporting Time allowed: Three Hours (10.00 13.00 Hrs) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 14 th November 2011 Subject CT2 Finance and Financial Reporting Time allowed: Three Hours (10.00 13.00 Hrs) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES

Chapter 4 The Income Statement, Comprehensive Income, and the Statement of Cash Flows

Chapter 4 The Income Statement, Comprehensive Income, and the Statement of Cash Flows QUESTIONS FOR REVIEW OF KEY TOPICS Question 4 1 The income statement is a change statement that reports transactions

Chapter 4 The Income Statement, Comprehensive Income, and the Statement of Cash Flows QUESTIONS FOR REVIEW OF KEY TOPICS Question 4 1 The income statement is a change statement that reports transactions

CHAPTER 17 PROBLEMS: SET B

CHAPTER 17 PROBLEMS: SET B P17-1B You are provided with the following transactions that took place during a recent fiscal year. Statement of Cash Inflow, Cash Flow Outflow, or Transaction Activity Affected

CHAPTER 17 PROBLEMS: SET B P17-1B You are provided with the following transactions that took place during a recent fiscal year. Statement of Cash Inflow, Cash Flow Outflow, or Transaction Activity Affected

Analysis and Interpretation of Financial Statements

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

Unit II. Module III. Ratio Analysis. Assignments

Unit II Module III Ratio Analysis Assignments Exercise Q.1. State the purpose and mode of determining the following ratios: (i) Inventory ratios (ii) Debtors Ratios (iii) Operating Ratios Q. 2. State the

Unit II Module III Ratio Analysis Assignments Exercise Q.1. State the purpose and mode of determining the following ratios: (i) Inventory ratios (ii) Debtors Ratios (iii) Operating Ratios Q. 2. State the

Rebeccas Coffee 2018 Prepared for Rebeccas Coffee 05 December 2018

Prepared for 5 December 218 Page 1/22 Data Reporting Period Period End 3-6-215 3-6-216 3-6-217 3-6-218 Period Length (months) 12 12 12 12 Profit & Loss Revenue 3,4, 5,, 5,8, 6,612, Gross Margin ($) 865,

Prepared for 5 December 218 Page 1/22 Data Reporting Period Period End 3-6-215 3-6-216 3-6-217 3-6-218 Period Length (months) 12 12 12 12 Profit & Loss Revenue 3,4, 5,, 5,8, 6,612, Gross Margin ($) 865,

Q U E S T I O N S B A S E D O N F I N A N C I A L M A N A G E M E N T

Q U E S T I O N S B A S E D O N F I N A N C I A L M A N A G E M E N T 1) The Yield to Maturity of a bond is the same as: a) The present value of the bond b) The bonds internal rate of return c) The future

Q U E S T I O N S B A S E D O N F I N A N C I A L M A N A G E M E N T 1) The Yield to Maturity of a bond is the same as: a) The present value of the bond b) The bonds internal rate of return c) The future

Williams Plumbing 2018 Prepared for Williams Plumbing 05 December 2018

Prepared for 5 December 218 Page 1/22 Data Reporting Period Period End 3-6-215 3-6-216 3-6-217 3-6-218 Period Length (months) 12 12 12 12 Profit & Loss Revenue 18,, 31,5, 35,, 42,, Gross Margin ($) 4,8,

Prepared for 5 December 218 Page 1/22 Data Reporting Period Period End 3-6-215 3-6-216 3-6-217 3-6-218 Period Length (months) 12 12 12 12 Profit & Loss Revenue 18,, 31,5, 35,, 42,, Gross Margin ($) 4,8,

Topic 1! The Accounting Equation and The effect of Economic Transactions!

Topic 1 The Accounting Equation and The effect of Economic Transactions Accounting in Action : Knowing the Numbers : In business, accounting and financial statement are the means for communicating the

Topic 1 The Accounting Equation and The effect of Economic Transactions Accounting in Action : Knowing the Numbers : In business, accounting and financial statement are the means for communicating the

FM101 CHAPTERS COVERED : CHAPTERS 1, 5, 7 AND 8. DUE DATE : 3:00 p.m. 21 AUGUST 2012

Page 1 of 11 ASSIGNMENT 2 ND SEMESTER : FINANCIAL MANAGEMENT 1 () CHAPTERS COVERED : CHAPTERS 1, 5, 7 AND 8 DUE DATE : 3:00 p.m. 21 AUGUST 2012 TOTAL MARKS : 100 INSTRUCTIONS TO CANDIDATES FOR COMPLETING

Page 1 of 11 ASSIGNMENT 2 ND SEMESTER : FINANCIAL MANAGEMENT 1 () CHAPTERS COVERED : CHAPTERS 1, 5, 7 AND 8 DUE DATE : 3:00 p.m. 21 AUGUST 2012 TOTAL MARKS : 100 INSTRUCTIONS TO CANDIDATES FOR COMPLETING

Accounting Fundamentals

Subject no. 50A Certificate in Offshore Finance and Administration Accounting Fundamentals July 2012 Tuesday morning 10 July 2012 Time allowed: 2 hours Do not open this examination paper until the presiding

Subject no. 50A Certificate in Offshore Finance and Administration Accounting Fundamentals July 2012 Tuesday morning 10 July 2012 Time allowed: 2 hours Do not open this examination paper until the presiding

Bank Financial Management

1) The Yield to Maturity of a bond is the same as: a) The present value of the bond b) The bonds internal rate of return c) The future value of the bond QUESTIONS BASED ON FINANCIAL MANAGEMENT 2) Choose

1) The Yield to Maturity of a bond is the same as: a) The present value of the bond b) The bonds internal rate of return c) The future value of the bond QUESTIONS BASED ON FINANCIAL MANAGEMENT 2) Choose

FINANCIAL RATIOS. LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1. Current Liabilities SAMPLE BALANCE SHEET ASSETS

You want current and quick ratios to be > 1. Current Liabilities SAMPLE BALANCE SHEET ASSETS") FINANCIAL RATIOS ROUND ALL ANSWERS TO TWO DECIMALS UNLESS REQUESTED OTHERWISE IN THE PROBLEM LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1 Current Ratio Quick Ratio

FINANCIAL RATIOS ROUND ALL ANSWERS TO TWO DECIMALS UNLESS REQUESTED OTHERWISE IN THE PROBLEM LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1 Current Ratio Quick Ratio

Statement of Accounts Summary 2012/13

Introduction Statement of Accounts Summary 2012/13 Doncaster Council is required to produce an annual Statement of Accounts to provide assurance to the public that the Council has used public money legally

Introduction Statement of Accounts Summary 2012/13 Doncaster Council is required to produce an annual Statement of Accounts to provide assurance to the public that the Council has used public money legally

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By http://vustudents.ning.com 1- What is Financial Management? The procedure of managing the financial resources, as well as accounting and financial

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By http://vustudents.ning.com 1- What is Financial Management? The procedure of managing the financial resources, as well as accounting and financial

BATCH All Batches. DATE: MAXIMUM MARKS: 100 TIMING: 3 Hours. PAPER 3 : Cost Accounting

BATCH All Batches DATE: 25.09.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 3 : Cost Accounting Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made by the candidates. Working

BATCH All Batches DATE: 25.09.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 3 : Cost Accounting Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made by the candidates. Working

B.COM II ADVANCED AND COST ACCOUNTING

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

Learning Outcomes. The Statement of Cash Flows. Chapter 4: The Income Statement, Comprehensive Income and The Statement of Cash Flows: Part 2

Chapter 4: The Income Statement, Comprehensive Income and The Statement of Cash Flows: Part 2 The Statement of Cash Flows Dr. Chula King Intermediate Accounting 1 Learning Outcomes After completing this

Chapter 4: The Income Statement, Comprehensive Income and The Statement of Cash Flows: Part 2 The Statement of Cash Flows Dr. Chula King Intermediate Accounting 1 Learning Outcomes After completing this

5. Risk in capital budgeting implies that the decision maker knows of the cash flows. A. Probability B. Variability C. Certainity D.

1. The assets of a business can be classified as A. Only fixed assets B. Only current assets C. Fixed and current assets D. None of the above 2. What is customer value? A. Post purchase dissonance B. Excess

1. The assets of a business can be classified as A. Only fixed assets B. Only current assets C. Fixed and current assets D. None of the above 2. What is customer value? A. Post purchase dissonance B. Excess

Understanding Accounting & Financial Statements

This image cannot currently be displayed. Accounting Principles INDE-Engineering Economy Understanding Accounting & Financial Statements Presented By: Magdy Akladios, PhD, PE, CSP, CPE, CSHM ACCOUNTING

This image cannot currently be displayed. Accounting Principles INDE-Engineering Economy Understanding Accounting & Financial Statements Presented By: Magdy Akladios, PhD, PE, CSP, CPE, CSHM ACCOUNTING

Do not open this examination paper until the presiding officer or an invigilator tells you to.

Please complete this box: Candidate number: as indicated on your admission slip Desk number: If you are using a calculator, please enter the make and model number: Make (company name): Model number: Subject

Please complete this box: Candidate number: as indicated on your admission slip Desk number: If you are using a calculator, please enter the make and model number: Make (company name): Model number: Subject