Cash Flow Statements. Chapter 15. Luby & O Donoghue (2005)

|

|

|

- Lydia Morgan

- 5 years ago

- Views:

Transcription

1 Cash Flow Statements Chapter 15 Luby & O Donoghue (2005)

2 Cash is king profits can be manufactured by creative accounting but creating cash is impossible. Terry Smith, Accounting for Growth

3 Typical cash flows CASH FLOWS IN OUT 1. Customer payments X X 1. Suppliers payments 2. Capital grants X X 2. Staff payments 3. Owners buy shares X X 3. Dividends 4. Sale of fixed assets X X 4. Purchase of fixed assets 5. Bank Loans X X 5. Repayment of loans 6. Tax refunds X X 6. Tax 7. Interest received X X 7. Interest paid 8. Sale of Business X X 8. Business acquisitions 9. Dividends received X X 9. Overheads/expenses

4 Cash Cash in hand and deposits repayable on demand with any qualifying financial institution less overdrafts from any qualifying financial institution repayable on demand. Cash includes cash in hand and deposits denominated in foreign currencies. (FRS 1) Deposits are repayable on demand if they can be withdrawn at any time without penalty, and notice of not more than 24 hours.

5 Financial Reporting Standard 1 (FRS 1) Financial Reporting Standard 1 (FRS 1) is an attempt to ensure that all companies report a summary of their cash flows. FRS 1 applies to all medium and large companies as defined by the Companies Act 1986 and relates to accounting periods ending on or after 23 March 1997.

6 Purpose of FRS 1 To show the cash inflows and outflows for the financial year and the consequent increase or decrease in cash. The cash flows are reported in various categories to enable the reader to identify key developments. To convert the operating profit or loss into the equivalent amount of cash released or consumed in the day to day running of the business. To show how the increase or decrease in cash for the reporting period links the net funds (where cash and bank balances are greater than loans/debt) or net debt (where loans/ debt are greater than bank cash balances) at the start and end of the reporting period.

7 Categories of cash flow 1. Operating activities 2. Return on investment/serving of debt 3. Taxation 4. Capital expenditure 5. Acquisitions and disposals 6. Equity dividends paid 7. Management of liquid resources 8. Financing

8 Cash flow statement 2 steps Step One Calculate overall cash flow Total cash movement (000) Total movement in cash in the reporting period Cash at 1 Jan 300 Cash at 31 Dec 470 Cash Movement +170 Cash increased by 170,000 over the year. Step Two Prepare Cash Flow Statement Categories of cash ( 000) 1. Operating activities Return on investment/serving of debt (10) 3. Taxation (20) 4. Capital expenditure (200) 5. Acquisitions and disposals (100) 6. Equity dividends paid (50) 7. Management of liquid resources (50) 8. Financing

9 Category 1: Net cash flow from operating activities Cash flows from operating activities are in general the cash effects of transactions relating to the operating or trading activities of the business (the normal trading activities of the business, not capital activities). Operating cash flows will be concerned with: cash collected from customers cash paid to trade creditors for purchases cash paid to staff /PAYE/PRSI cash paid for services (overheads) In calculating the net cash flow from operating activities two formats are permitted by FRS 1 called The Direct Method The Indirect Method

10 Category 2: Returns on investments and servicing of debt Interest received: from loans given to other businesses. Interest paid: on loans from financial institutions, debentures, interest element on finance lease repayments, dividends paid to non equity shareholders (preference shareholders). Dividends received: from investment in subsidiaries, related companies and fixed asset investments.

11 Category 3: Taxation Only corporation tax payments and refunds during the year are reported in this section.

12 Category 4: Capital expenditure and financial investment This category of activity includes divesting activities such as cash flow from the sale of tangible, intangible and financial fixed assets as well purchases of tangible, intangible and financial fixed assets.

13 Category 5: Acquisitions and disposals This category includes receipts and payments in respect of disposals or acquisitions of interests in subsidiaries, associated or joint venture companies. The cost of buying a business is reported net of any cash included in the purchase price.

14 Category 6: Equity dividends paid Part of the cash generated by a successful business is paid to the owners as a dividend. This important outflow is reported as a separate item in the cash flow statement.

15 Category 7: Management of liquid resources This section deals with receipts and payments in respect of current asset investments, which are considered to be liquid (readily marketable). Under the definitions section in FRS 1, liquid resources are those that can be realised (turned into cash) without disruption to the business of the entity or which can be traded in an active market. Examples include commercial paper and short-term investments readily convertible into cash at their carrying value or close to it.

16 Category 8: Financing This category covers the receipts and payments, which arise from issues or repayments of finance, from or to, the providers of external finance. Cash inflows from this category would include the issue of shares, debentures/bonds or just simply getting a bank loan. The repayments of the capital elements of loans/debentures would be considered a cash outflow.

17 Reconciliation of net cash flow to net debt The first two objectives or purposes of FRS 1 are achieved by preparing the cash flow statement. The third objective of FRS1 is to show how the increase or decrease in cash for the reporting period links the net funds or net debt at the start and end of the reporting period. Net debt is as per the definitions in FRS 1 the borrowings of the entity less cash and liquid resources. If cash and liquid resources exceed debt then the term used becomes Net Funds. The revised FRS 1 requires an additional statement Reconciliation of net cash flow to movements in net debt to be shown in the notes to the accounts. A further note is required to further analyse the changes in net debt/funds breaking debt into periods of less than one year and greater than one year.

18 Reconciliation of net cash flow to net debt

19 Comprehensive example Trading P&L a/c for the year ended (,000) (,000) Turnover 4,210 3,694 Cost of goods sold 1, Gross profit 3,157 2,771 Administration expenses 1,200 1,012 Selling and distribution 921 2, ,868 Operating profit 1, Interest Net profit before tax Corporation tax Net Profit after tax Transfer to reserve Dividends - interim Dividends - final Retained profits for the year (174) (467) Retained profits b/f Retained profits c/f Additional information 1. Authorised share capital is 20,000, cent ordinary shares 2. Administration expenses for the year ended 31/3/04 are the following: Depreciation on assets in existence at the year-end 560,000. Loss on the sale of fixed assets for 80,000. The assets had a net book value of 150,000 when sold Balance sheet as at Fixed Assets At N.B.V. 13,120 10,456 Current Assets Stock Debtors Short-term investments Prepayments and accrued Income 8 10 Bank Creditors < 12 months Trade creditors Taxation Dividends Bank overdraft Creditors >12 months Debentures 4,000 3,500 Bank loans 600 4, ,000 Capital and Reserves Called up Share Capital 8,090 6,391 Ordinary shares nominal value 0.50 per share 6,000 5,000 Reserves Share premium 623 General reserve 1,423 1,173 Retained profits ,090 6,391

20 Calculate the overall cash flow

21 Prepare the cash flow statement

22 Prepare the reconciliation of net debt to net cash flow

23 Interpreting cash flow statements Is the overall cash movement positive or negative, and is the cash movement significant? Is the company heavily in overdraft? What is the net debt/funds situation and is it getting better or worse? Compare the operating net profit to operating cash flow. Is the company generating sufficient cash from its operating activities? If the company is not generating sufficient cash from its operating activities is this due to large increases in stocks and debtors which can signal poor control over working capital. Identify the main cash inflows to the business. The biggest cash inflow for a business should be its operating activities but other major ones would be issues of shares/debentures. Identify the major cash outflows of a business. These in general would be in the whole area of capital expenditure (investing in new fixed assets or investments). Try and assess how this capital expenditure was financed. Was it through a new issue of shares, debentures or from the cash flows generated from operating activities. Come to an overall conclusion about the cash position of the business in terms of the business s ability to generate cash and how it spends it. Also link this to the profitability performance of the business.

24 Sample Arnotts Group Cash Flow from Operating Activities 30,420 23,719 Returns on Investments and Servicing of Finance Interest received Interest paid (1,042) (1,442) Interest element of finance lease rental payments (23) (23) Premium paid on redemption of debenture stock - (3) Preference dividends paid (6) (6) Net Cash Outflow from Returns on Investments and Servicing of Finance (1,007) (1,350) Taxation Corporation tax paid (4,315) (3,129) Capital Expenditure and Financial Investment Purchase of tangible fixed assets (6,253) (9,136) Repayment of loan by associated undertaking - 64 Net Cash Outflow from Capital Expenditure and Financial Investment (6,253) (9,072) Equity Dividends Paid (5,955) (5,107) Cash Inflow Before Financing 12,890 5,061 Financing (11,840) (8,961) Increase/(Decrease) in Cash in the Year 1,050 (3,900)

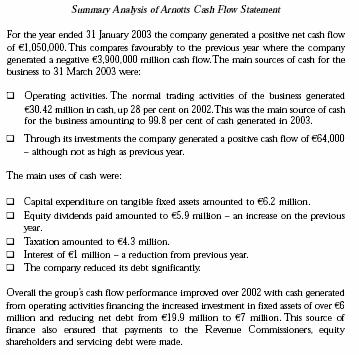

25 Commentary

Commercial(&( Retail(

Commercial(&( Retail( !! ANNUAL! REPORT!&! ACCOUNTS! Avent Limited (Formerly Cannon Rubber Ltd) Annual report and financial statements for the 52 week period ended 1 January 2006 Registered number: 00313835

Commercial(&( Retail( !! ANNUAL! REPORT!&! ACCOUNTS! Avent Limited (Formerly Cannon Rubber Ltd) Annual report and financial statements for the 52 week period ended 1 January 2006 Registered number: 00313835

Consolidated Cash Flow Statement for the year ended 30th June, 2002

Consolidated Cash Flow Statement for the year ended 30th June, 2002 Notes Net cash inflow from operating activities (a) 4,916,217 6,797,641 Returns on investments and servicing of finance Interest received

Consolidated Cash Flow Statement for the year ended 30th June, 2002 Notes Net cash inflow from operating activities (a) 4,916,217 6,797,641 Returns on investments and servicing of finance Interest received

Statement of cash flows PURPOSE & SCOPE

IAS 7 Statement of cash flows PURPOSE & SCOPE Purpose Users needs Scope The fundamental purpose of being in business is to generate profit, as this will increase the owners' wealth. Profitability relates

IAS 7 Statement of cash flows PURPOSE & SCOPE Purpose Users needs Scope The fundamental purpose of being in business is to generate profit, as this will increase the owners' wealth. Profitability relates

GROUP PROFIT AND LOSS ACCOUNT

GROUP PROFIT AND LOSS ACCOUNT Continuing Continuing activities Goodwill activities before goodwill Amortisation before Operating Unaudited amortisation & operating Audited operating exceptional Total &

GROUP PROFIT AND LOSS ACCOUNT Continuing Continuing activities Goodwill activities before goodwill Amortisation before Operating Unaudited amortisation & operating Audited operating exceptional Total &

Williams Grand Prix Holdings PLC

Registration number: 07475805 Williams Grand Prix Holdings PLC Consolidated Financial Statements for the 6 month period ended 30 June Consolidated Profit and Loss Account for the 6 Months Ended 30 June

Registration number: 07475805 Williams Grand Prix Holdings PLC Consolidated Financial Statements for the 6 month period ended 30 June Consolidated Profit and Loss Account for the 6 Months Ended 30 June

35 Manchester United PLC Annual Report 2002 Financial statements

35 Manchester United PLC Annual Report 2002 Contents 36 Consolidated profit and loss account 36 Statement of total recognised gains and losses 37 Consolidated balance sheet 38 balance sheet 39 Consolidated

35 Manchester United PLC Annual Report 2002 Contents 36 Consolidated profit and loss account 36 Statement of total recognised gains and losses 37 Consolidated balance sheet 38 balance sheet 39 Consolidated

Name of business Statement of cash flows for the financial year end 31 December 20X1 (DIRECT METHOD) Inflow /(outflow)

Inflow /(outflow)") Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

IOLKOS DEVELOPMENT ENTERTAINMENT S.A. 85 MESOGEION AVE., Athens, Greece General Commerce Reg. No SA Reg. No.

85 MESOGEION AVE., 11526 Athens, Greece General Commerce Reg. No. 59231 SA Reg. No. 57343/1/Β/4/47 TRANSLATED ABSTRACT OF ANNUAL FINANCIAL STATEMENTS 1 ST JANUARY TO 31 ST DECEMBER 217 STATEMENT OF FINANCIAL

85 MESOGEION AVE., 11526 Athens, Greece General Commerce Reg. No. 59231 SA Reg. No. 57343/1/Β/4/47 TRANSLATED ABSTRACT OF ANNUAL FINANCIAL STATEMENTS 1 ST JANUARY TO 31 ST DECEMBER 217 STATEMENT OF FINANCIAL

Reference. PwC Holdings Ltd and Its Subsidiaries Consolidated Income Statement for the financial year ended 31 December 2003

Consolidated Income Statement (Alternative 1: Illustrating the classification of expenses by function) 2 The Group FRS 1(77,82) SGX 1207(5)(a) Sales Cost of sales Gross profit 5,15 (24,512) 28,80 42,5

Consolidated Income Statement (Alternative 1: Illustrating the classification of expenses by function) 2 The Group FRS 1(77,82) SGX 1207(5)(a) Sales Cost of sales Gross profit 5,15 (24,512) 28,80 42,5

SLAS 9. Sri Lanka Accounting Standard 9. Cash Flow Statements

Sri Lanka Accounting Standard 9 Cash Flow Statements 107 Contents Sri Lanka Accounting Standard 9 Cash Flow Statements Objective Scope Paragraphs 1-2 Benefits of Cash Flow Information 3-4 Definitions 5

Sri Lanka Accounting Standard 9 Cash Flow Statements 107 Contents Sri Lanka Accounting Standard 9 Cash Flow Statements Objective Scope Paragraphs 1-2 Benefits of Cash Flow Information 3-4 Definitions 5

Accounting Title 2014/3/ /12/ /3/31 Balance Sheet

Financial Statement Balance Sheet Accounting Title 2014/3/31 2013/12/31 2013/3/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 7,974,989 6,997,862 6,433,466

Financial Statement Balance Sheet Accounting Title 2014/3/31 2013/12/31 2013/3/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 7,974,989 6,997,862 6,433,466

ACCOUNTANCY. Part B. Q17. State the significance of Analysis of Financial Statements to the Lenders. (1 mark)

") ACCOUNTANCY [Time allowed: 3 hours] [Maximum marks:80] General Instructions: (i) This question paper contains three parts A, B and C. (ii) Part A is compulsory for all candidates. (iii) Candidates can

ACCOUNTANCY [Time allowed: 3 hours] [Maximum marks:80] General Instructions: (i) This question paper contains three parts A, B and C. (ii) Part A is compulsory for all candidates. (iii) Candidates can

Statement of Cash Flows

Sri Lanka Accounting Standard - LKAS 7 Statement of Cash Flows LKAS 7 CONTENTS SRI LANKA ACCOUNTING STANDARD - LKAS 7 STATEMENT OF CASH FLOWS OBJECTIVE paragraphs SCOPE 1 BENEFITS OF CASH FLOW INFORMATION

Sri Lanka Accounting Standard - LKAS 7 Statement of Cash Flows LKAS 7 CONTENTS SRI LANKA ACCOUNTING STANDARD - LKAS 7 STATEMENT OF CASH FLOWS OBJECTIVE paragraphs SCOPE 1 BENEFITS OF CASH FLOW INFORMATION

Statement of Cash Flows

International Accounting Standard 7 Statement of Cash Flows This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 7 Cash Flow Statements was issued by the International

International Accounting Standard 7 Statement of Cash Flows This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 7 Cash Flow Statements was issued by the International

Statement of Cash Flows

Statement of Cash Flows Statement of cash flows General Principles Mandatory for most of the entities Direct and Indirect method Generally starts with PAT (Profit after tax) 2 Overview of AS 3 Requires

Statement of Cash Flows Statement of cash flows General Principles Mandatory for most of the entities Direct and Indirect method Generally starts with PAT (Profit after tax) 2 Overview of AS 3 Requires

Ind AS 7 Statement of Cash Flows. EIRC, Kolkata. Mohit Jain 16 February For discussion purposes only

Ind AS 7 Statement of Cash Flows EIRC, Kolkata Mohit Jain 16 February 2018 For discussion purposes only Overview of Ind AS 7 Requires presentation of a statement of cash flows as an integral part of financial

Ind AS 7 Statement of Cash Flows EIRC, Kolkata Mohit Jain 16 February 2018 For discussion purposes only Overview of Ind AS 7 Requires presentation of a statement of cash flows as an integral part of financial

6 The following terms are used in this Standard with the meanings specified: Cash comprises cash on hand and demand deposits.

International Accounting Standard 7 Statement of Cash Flows 1 Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

International Accounting Standard 7 Statement of Cash Flows 1 Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows

7 Statement of Cash Flows") Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate

Fundamentals Level Skills Module, Paper F7 (IRL) 1 Consolidated balance sheet of Pacemaker as at 31 March 2009: million

1 Consolidated balance sheet of Pacemaker as at 31 March 2009: million") Answers Fundamentals Level Skills Module, Paper F7 (IRL) Financial Reporting (Irish) June 2009 Answers 1 Consolidated balance sheet of Pacemaker as at 31 March 2009: million million Fixed assets Intangible

Answers Fundamentals Level Skills Module, Paper F7 (IRL) Financial Reporting (Irish) June 2009 Answers 1 Consolidated balance sheet of Pacemaker as at 31 March 2009: million million Fixed assets Intangible

SOLUTIONS TO END-OF-CHAPTER QUESTIONS CHAPTER 6

SOLUTIONS TO END-OF-CHAPTER QUESTIONS CHAPTER 6 DEVELOP YOUR UNDERSTANDING Question 6.1 Abi: statement of cash flows for the year ended 31 August 2018 using the direct method Cash flows from operating

SOLUTIONS TO END-OF-CHAPTER QUESTIONS CHAPTER 6 DEVELOP YOUR UNDERSTANDING Question 6.1 Abi: statement of cash flows for the year ended 31 August 2018 using the direct method Cash flows from operating

VDM GROUP LIMITED. and its Controlled Entities ABN

and its Controlled Entities ABN 95 109 829 334 APPENDIX 4E PRELIMINARY FINAL REPORT APPENDIX 4E PRELIMINARY FINAL REPORT CONTENTS LODGED WITH ASX UNDER LISTING RULE 4.3A Page Appendix 4E Results for announcement

and its Controlled Entities ABN 95 109 829 334 APPENDIX 4E PRELIMINARY FINAL REPORT APPENDIX 4E PRELIMINARY FINAL REPORT CONTENTS LODGED WITH ASX UNDER LISTING RULE 4.3A Page Appendix 4E Results for announcement

Appendix 5B. Mining exploration entity quarterly report

Introduced 1/7/96. Origin: Appendix 8. Amended 1/7/97, 1/7/98, 30/9/2001, 1/6/10, 17/12/10 Rule 5.3 SOUTHERN CROSS EXPLORATION N.L. QUARTER ENDED ("Current Quarter") : 31st MARCH 2016 Consolidated Statement

Introduced 1/7/96. Origin: Appendix 8. Amended 1/7/97, 1/7/98, 30/9/2001, 1/6/10, 17/12/10 Rule 5.3 SOUTHERN CROSS EXPLORATION N.L. QUARTER ENDED ("Current Quarter") : 31st MARCH 2016 Consolidated Statement

Drafting Financial Statements (Accounting Practice, Industry and Commerce) (DFS) (2003 standards) Suggested Answers

(DFS) (2003 standards) Suggested Answers") Drafting Financial Statements (Accounting Practice, Industry and Commerce) (DFS) (2003 standards) Suggested Answers SECTION 1 PART A Task 1.1 Loittede plc Consolidated balance sheet as at 30 September,

Drafting Financial Statements (Accounting Practice, Industry and Commerce) (DFS) (2003 standards) Suggested Answers SECTION 1 PART A Task 1.1 Loittede plc Consolidated balance sheet as at 30 September,

Statement of Cash Flows

IAS Standard 7 Statement of Cash Flows In April 2001 the International Accounting Standards Board adopted IAS 7 Cash Flow Statements, which had originally been issued by the International Accounting Standards

IAS Standard 7 Statement of Cash Flows In April 2001 the International Accounting Standards Board adopted IAS 7 Cash Flow Statements, which had originally been issued by the International Accounting Standards

New Zealand Equivalent to International Accounting Standard 7 Statement of Cash Flows (NZ IAS 7)

") New Zealand Equivalent to International Accounting Standard 7 Statement of Cash Flows (NZ IAS 7) Issued November 2004 and incorporates amendments up to and including 31 December 2012 This Standard was

New Zealand Equivalent to International Accounting Standard 7 Statement of Cash Flows (NZ IAS 7) Issued November 2004 and incorporates amendments up to and including 31 December 2012 This Standard was

BENEFITS OF CASH FLOW INFORMATION

16 Accounting Standard (AS) 3 Cash Flow Statements Contents OBJECTIVE SCOPE Paragraphs 1-2 BENEFITS OF CASH FLOW INFORMATION 3-4 DEFINITIONS 5-7 Cash and Cash Equivalents 6-7 PRESENTATION OF A CASH FLOW

16 Accounting Standard (AS) 3 Cash Flow Statements Contents OBJECTIVE SCOPE Paragraphs 1-2 BENEFITS OF CASH FLOW INFORMATION 3-4 DEFINITIONS 5-7 Cash and Cash Equivalents 6-7 PRESENTATION OF A CASH FLOW

Group profit and loss account

Group profit and loss account FOR THE YEAR ENDED 31 MARCH 1999 Before After exceptional Exceptional exceptional items items items 1999 1999 Notes m m m m m ))))))%!!!!!!!0111!!!0111!!!0111!!!01111110051111

Group profit and loss account FOR THE YEAR ENDED 31 MARCH 1999 Before After exceptional Exceptional exceptional items items items 1999 1999 Notes m m m m m ))))))%!!!!!!!0111!!!0111!!!0111!!!01111110051111

ODEON & UCI CINEMAS GROUP. Odeon & UCI Finco plc Financial Results 2013 Q1

ODEON & UCI CINEMAS GROUP Odeon & UCI Finco plc Financial Results 2013 Q1 Contents Page Operating and Financial Review 3 Unaudited Condensed Consolidated Financial Statements: Profit & Loss Account 7 Cashflow

ODEON & UCI CINEMAS GROUP Odeon & UCI Finco plc Financial Results 2013 Q1 Contents Page Operating and Financial Review 3 Unaudited Condensed Consolidated Financial Statements: Profit & Loss Account 7 Cashflow

14. Statement of cash flows

14. Statement of cash flows Accounting and reporting by charities EPOSURE DRAFT Introduction 14.1. Charities preparing their accounts under FRS 102 must provide a statement of cash flows and should refer

14. Statement of cash flows Accounting and reporting by charities EPOSURE DRAFT Introduction 14.1. Charities preparing their accounts under FRS 102 must provide a statement of cash flows and should refer

Consolidated Profit and Loss account for the year ended 31 December 2003

Consolidated Profit and Loss account for the year ended 31 December Before exceptional items and of intangibles Exceptional Before Exceptional items and exceptional items and items and of intangibles of

Consolidated Profit and Loss account for the year ended 31 December Before exceptional items and of intangibles Exceptional Before Exceptional items and exceptional items and items and of intangibles of

MANAGEMENT ACCOUNTING - CASH FLOW

MANAGEMENT ACCOUNTING - CASH FLOW http://www.tutorialspoint.com/accounting_basics/management_accounting_cash_flow.htm Copyright tutorialspoint.com It is very important for a business to keep adequate cash

MANAGEMENT ACCOUNTING - CASH FLOW http://www.tutorialspoint.com/accounting_basics/management_accounting_cash_flow.htm Copyright tutorialspoint.com It is very important for a business to keep adequate cash

Group statements of cash flows

Group statements of cash flows Topic list Syllabus reference 1 Cash flows D1 2 IAS 7 Statement of cash flows: Single company D1 3 Consolidated statements of cash flows D1 Introduction A statement of cash

Group statements of cash flows Topic list Syllabus reference 1 Cash flows D1 2 IAS 7 Statement of cash flows: Single company D1 3 Consolidated statements of cash flows D1 Introduction A statement of cash

The Interpretation of Financial Statements

The Interpretation of Financial Statements Chapter 16 Luby & O Donoghue (2005) Why use ratio analysis Provides framework Comparison to previous years Trends identified Identify areas of concern Targets

The Interpretation of Financial Statements Chapter 16 Luby & O Donoghue (2005) Why use ratio analysis Provides framework Comparison to previous years Trends identified Identify areas of concern Targets

Touchstone Group plc

Date 14 November Contacts Keith Birch, Managing Director Touchstone Group plc 020 8441 7755 David Bick/Trevor Phillips Holborn 020 7929 5599 Touchstone Group plc Further Profit Growth at Half Year Touchstone

Date 14 November Contacts Keith Birch, Managing Director Touchstone Group plc 020 8441 7755 David Bick/Trevor Phillips Holborn 020 7929 5599 Touchstone Group plc Further Profit Growth at Half Year Touchstone

BSc.(Hons) Banking and International Finance, BSc.(Hons) Tourism and Hospitality Management, Diploma in Public Administration and Management

Banking and International Finance, BSc.(Hons) Tourism and Hospitality Management, Diploma in Public Administration and Management") BSc.(Hons) Banking and International Finance, BSc.(Hons) Tourism and Hospitality Management, Diploma in Public Administration and Management & BSc.(Hons) Public Administration and Management Cohort: BBIF/04/FT/PT

BSc.(Hons) Banking and International Finance, BSc.(Hons) Tourism and Hospitality Management, Diploma in Public Administration and Management & BSc.(Hons) Public Administration and Management Cohort: BBIF/04/FT/PT

Financial and Management Accounting Concepts

Financial and Management Accounting Concepts Editorial This month's newsletter focuses on the way in which you can interpret fully the information you present in the form of financial statements to either

Financial and Management Accounting Concepts Editorial This month's newsletter focuses on the way in which you can interpret fully the information you present in the form of financial statements to either

Fund = Working capital = Current assets Current liability

CHAPTER 11 Fund flow statement also referred to as statement of source and application of funds presents the movement of funds and helps to understand the changes in the structure of assets, liabilities

CHAPTER 11 Fund flow statement also referred to as statement of source and application of funds presents the movement of funds and helps to understand the changes in the structure of assets, liabilities

Tiill now you have learnt about the financial

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,

1 July 1999 to 31 Dec 1999 *

SINGAPORE EXCHANGE LIMITED Unaudited Half Year Financial Statement And Dividend Announcement Half-year financial statement on consolidated results for the six months ended 31 December 2000. These figures

SINGAPORE EXCHANGE LIMITED Unaudited Half Year Financial Statement And Dividend Announcement Half-year financial statement on consolidated results for the six months ended 31 December 2000. These figures

Appendix 5B. Mining exploration entity quarterly report

Introduced 1/7/96. Origin: Appendix 8. Amended 1/7/97, 1/7/98, 30/9/2001, 1/6/10, 17/12/10 Rule 5.3 SOUTHERN CROSS EXPLORATION N.L. QUARTER ENDED ("Current Quarter") : 30th September 2015 Consolidated

Introduced 1/7/96. Origin: Appendix 8. Amended 1/7/97, 1/7/98, 30/9/2001, 1/6/10, 17/12/10 Rule 5.3 SOUTHERN CROSS EXPLORATION N.L. QUARTER ENDED ("Current Quarter") : 30th September 2015 Consolidated

Mining exploration entity quarterly report

Appendix 5B Mining exploration entity quarterly report Introduced 01/07/96 Origin Appendix 8 Amended 01/07/97, 01/07/98, 30/09/01, 01/06/10, 17/12/10 Name of entity Predictive Discovery Ltd ABN 11 127

Appendix 5B Mining exploration entity quarterly report Introduced 01/07/96 Origin Appendix 8 Amended 01/07/97, 01/07/98, 30/09/01, 01/06/10, 17/12/10 Name of entity Predictive Discovery Ltd ABN 11 127

2. This Standard supersedes IAS 7 Statement of Changes in Financial Position, approved in July 1977.

COMPARISON OF GRAP 2 WITH IAS 7 GRAP 2 IAS 7 DIFFERENCES Objective Objective.01 The cash flow statement identifies the sources of cash inflows, the items on which cash was expended during the reporting

COMPARISON OF GRAP 2 WITH IAS 7 GRAP 2 IAS 7 DIFFERENCES Objective Objective.01 The cash flow statement identifies the sources of cash inflows, the items on which cash was expended during the reporting

The Siam Cement Public Company Limited and its Subsidiaries

1 The Siam Cement Public Company Limited and its Subsidiaries Consolidated financial statements Consolidated statement of financial position As at 31 December 2017 Assets 2 Current assets Cash and cash

1 The Siam Cement Public Company Limited and its Subsidiaries Consolidated financial statements Consolidated statement of financial position As at 31 December 2017 Assets 2 Current assets Cash and cash

Turnover (see note 2) 8, , , , Operating profit (see note 3) (26.5) (72.0) 471.0

8, , , , Operating profit (see note 3) (26.5) (72.0) 471.0") Consolidated profit and loss account 52 weeks ended 53 weeks ended 1 April 2000 Before After Before After exceptional Exceptional exceptional exceptional Exceptional exceptional items items items items

Consolidated profit and loss account 52 weeks ended 53 weeks ended 1 April 2000 Before After Before After exceptional Exceptional exceptional exceptional Exceptional exceptional items items items items

Unappropriated retained earnings (accumulated deficit) Total unappropriated retained earnings (accumulated deficit) 676, ,797 Total retained ear

Total unappropriated retained earnings (accumulated deficit) 676, ,797 Total retained ear") Financial Statement Balance Sheet Accounting Title 2014/12/31 2013/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 1,183,185 1,177,682 Current bond investment

Financial Statement Balance Sheet Accounting Title 2014/12/31 2013/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 1,183,185 1,177,682 Current bond investment

AFH FINANCIAL GROUP PLC ANNUAL REPORT FOR THE YEAR ENDED 31 OCTOBER 2012

Company Registration No. 07638831 (England and Wales) AFH FINANCIAL GROUP PLC ANNUAL REPORT DIRECTORS AND ADVISERS Directors Secretary Mr A Hudson Mr J Wheatley Mr T Denne Mrs A-M Brown Company number

Company Registration No. 07638831 (England and Wales) AFH FINANCIAL GROUP PLC ANNUAL REPORT DIRECTORS AND ADVISERS Directors Secretary Mr A Hudson Mr J Wheatley Mr T Denne Mrs A-M Brown Company number

Revenue 45,073 39,339 78,966 77,117. Operating expenses (40,169) (37,224) (73,838) (73,151) Other operating income 2, ,834 3,817

(37,224) (73,838) (73,151) Other operating income 2, ,834 3,817") (The figures have not been audited) CONDENSED CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME Individual Quarter Cumulative Quarter Current Corresponding 6 Months 6 Months Quarter

(The figures have not been audited) CONDENSED CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME Individual Quarter Cumulative Quarter Current Corresponding 6 Months 6 Months Quarter

Revenue 67,472 56, ,631 Other income ,935 Share of joint ventures net surplus/(deficit) 115 (31) 220

115 (31) 220") STATEMENT OF COMPREHENSIVE INCOME Revenue 67,472 56,670 132,631 Other income 840 126 1,935 Share of joint ventures net surplus/(deficit) 115 (31) 220 Raw materials, consumables used and other expenses

STATEMENT OF COMPREHENSIVE INCOME Revenue 67,472 56,670 132,631 Other income 840 126 1,935 Share of joint ventures net surplus/(deficit) 115 (31) 220 Raw materials, consumables used and other expenses

ELECTRICAL CONTRACTING LIMITED (AUDIT EXEMPT COMPANY*) DIRECTORS REPORT & FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER Registered No.

DIRECTORS REPORT & FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER Registered No.") (AUDIT EXEMPT COMPANY*) DIRECTORS REPORT & FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2014 Registered No. xxxx * Electrical Contracting Limited is a small company as defined by the Companies Act 2014

(AUDIT EXEMPT COMPANY*) DIRECTORS REPORT & FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2014 Registered No. xxxx * Electrical Contracting Limited is a small company as defined by the Companies Act 2014

CONSOLIDATED BALANCE SHEET (Financial report as of the end of period)

") STOMIL SANOK S.A. Capital Group CONSOLIDATED BALANCE SHEET (Financial report as of the end of period) ASSETS March 31, December 31, March 31, 2 013 2 012 2 012 Fixed assets Tangible fixed assets 183 769

STOMIL SANOK S.A. Capital Group CONSOLIDATED BALANCE SHEET (Financial report as of the end of period) ASSETS March 31, December 31, March 31, 2 013 2 012 2 012 Fixed assets Tangible fixed assets 183 769

CONSOLIDATED PROFIT AND LOSS ACCOUNT For The Six Months Ended June 30, 2003

CONSOLIDATED PROFIT AND LOSS ACCOUNT For The Six Months Ended June 30, 2003 Unaudited Unaudited Note (Restated) Turnover 2 5,463 5,576 Other net loss 3 (5) (1) 5,458 5,575 Direct costs and operating expenses

CONSOLIDATED PROFIT AND LOSS ACCOUNT For The Six Months Ended June 30, 2003 Unaudited Unaudited Note (Restated) Turnover 2 5,463 5,576 Other net loss 3 (5) (1) 5,458 5,575 Direct costs and operating expenses

For personal use only

Mining exploration entity and oil and gas exploration entity ly report Rule 5.5 Mining exploration entity and oil and gas exploration entity ly report Introduced 01/07/96 Origin Appendix 8 Amended 01/07/97,

Mining exploration entity and oil and gas exploration entity ly report Rule 5.5 Mining exploration entity and oil and gas exploration entity ly report Introduced 01/07/96 Origin Appendix 8 Amended 01/07/97,

Smith Soletrader UNAUDITED ACCOUNTS for the year ended 31 December 2014

UNAUDITED ACCOUNTS for the year ended 31 December 2014 Unaudited accounts CONTENTS PAGE Proprietor and Professional Advisers 1 Proprietor s Approval Statement 2 Accountant s Report 3 Profit and Loss Account

UNAUDITED ACCOUNTS for the year ended 31 December 2014 Unaudited accounts CONTENTS PAGE Proprietor and Professional Advisers 1 Proprietor s Approval Statement 2 Accountant s Report 3 Profit and Loss Account

Cash-Flow Statement. According to. Revised Schedule VI Part I of Companies Act, Cash-Flow Statement

Cash-Flow Statement According to Revised Schedule VI Part I of Companies Act, 1956 Cash-Flow Statement QUESTION Prepare a Cash Flow Statement from the following Balance Sheets of Gokaldas Exports Ltd.

Cash-Flow Statement According to Revised Schedule VI Part I of Companies Act, 1956 Cash-Flow Statement QUESTION Prepare a Cash Flow Statement from the following Balance Sheets of Gokaldas Exports Ltd.

Notes to the financial statements

Note 1 UK GAAP accounting policies The separate financial statements of the Company are presented as required by the Companies Act 1985. As permitted by that Act, the separate financial statements have

Note 1 UK GAAP accounting policies The separate financial statements of the Company are presented as required by the Companies Act 1985. As permitted by that Act, the separate financial statements have

1. PRINCIPAL ACCOUNTING POLICIES

1. PRINCIPAL ACCOUNTING POLICIES The accounts have been prepared in accordance with all applicable Hong Kong Financial Reporting Standards (which includes all applicable Statements of Standard Accounting

1. PRINCIPAL ACCOUNTING POLICIES The accounts have been prepared in accordance with all applicable Hong Kong Financial Reporting Standards (which includes all applicable Statements of Standard Accounting

IFRS Interim Results. 25 weeks to 24 July November 2005

IFRS Interim Results 25 weeks to 24 July 2005 17 November 2005 Overview 2 UK GAAP trading update of 20 October remains unchanged Operating profit before exceptionals unchanged at 50.7m Conversion to IFRS

IFRS Interim Results 25 weeks to 24 July 2005 17 November 2005 Overview 2 UK GAAP trading update of 20 October remains unchanged Operating profit before exceptionals unchanged at 50.7m Conversion to IFRS

FRS 102 LIMITED. Example Financial Statements For the year ended 31 December 2015

Example Financial Statements Introduction These illustrative financial statements are an example of a group and parent company financial statements prepared for the first time in accordance with FRS 102

Example Financial Statements Introduction These illustrative financial statements are an example of a group and parent company financial statements prepared for the first time in accordance with FRS 102

Financial Statements of Companies

2 Financial Statements of Companies BASIC CONCEPTS UNIT 1: PREPARATION OF FINANCIAL STATEMENTS While preparing the final accounts of a company the following should be kept in mind: Requirements of Schedule

2 Financial Statements of Companies BASIC CONCEPTS UNIT 1: PREPARATION OF FINANCIAL STATEMENTS While preparing the final accounts of a company the following should be kept in mind: Requirements of Schedule

IIFL WEALTH {UK) LTD ANNUAL REPORT AND FINANCIAL STATEMENTS

LTD ANNUAL REPORT AND FINANCIAL STATEMENTS") Company Registration No. 06506067 (England and Wales) IIFL WEALTH {UK) LTD ANNUAL REPORT AND FINANCIAL STATEMENTS COMPANY INFORMATION Directors Company number Registered office Auditor AN Shah S Vakil

Company Registration No. 06506067 (England and Wales) IIFL WEALTH {UK) LTD ANNUAL REPORT AND FINANCIAL STATEMENTS COMPANY INFORMATION Directors Company number Registered office Auditor AN Shah S Vakil

JAPAUL OIL AND MARITIME SERVICES PLC

JAPAUL OIL AND MARITIME SERVICES PLC UNAUDITED MANAGEMENT ACCOUNT 30TH JUNE, 2016 JAPAUL GROUP STATEMENT OF COMPREHENSIVE INCOME FOR THE PERIOD ENDED JUNE 2016 2016 2015 NOTE Turnover 2 1,167,721 5,816,855

JAPAUL OIL AND MARITIME SERVICES PLC UNAUDITED MANAGEMENT ACCOUNT 30TH JUNE, 2016 JAPAUL GROUP STATEMENT OF COMPREHENSIVE INCOME FOR THE PERIOD ENDED JUNE 2016 2016 2015 NOTE Turnover 2 1,167,721 5,816,855

CONSOLIDATED PROFIT AND LOSS ACCOUNT For the year ended 31 March 2005

CONSOLIDATED PROFIT AND LOSS ACCOUNT For the year ended 31 March 2005 Note Turnover 3 4,461.1 7,115.9 Other net income 4 213.5 17.3 4,674.6 7,133.2 Direct costs and operating expenses (3,113.9) (5,427.0)

CONSOLIDATED PROFIT AND LOSS ACCOUNT For the year ended 31 March 2005 Note Turnover 3 4,461.1 7,115.9 Other net income 4 213.5 17.3 4,674.6 7,133.2 Direct costs and operating expenses (3,113.9) (5,427.0)

Illustrative Financial Statements

Illustrative financial statements Illustrative Financial Statements This document represents information that is used during the presentation of the seminar: Implementing FRS 102 How to convert your financial

Illustrative financial statements Illustrative Financial Statements This document represents information that is used during the presentation of the seminar: Implementing FRS 102 How to convert your financial

Fleetwood Corporation Limited. Preliminary Final Report Year ended 30 June 2012

ABN 69 009 205 261 Preliminary Final Report Results for Announcement to the Market Change Amount $ 000 Revenue from ordinary activities Down 13% to 407,443 Profit from ordinary activities after tax attributable

ABN 69 009 205 261 Preliminary Final Report Results for Announcement to the Market Change Amount $ 000 Revenue from ordinary activities Down 13% to 407,443 Profit from ordinary activities after tax attributable

LASACO ASSURANCE PLC FINANCIAL STATEMENTS THIRD QUARTER ENDED 30TH SEPTEMBER 2014

FINANCIAL STATEMENTS THIRD QUARTER ENDED 30TH SEPTEMBER 2014 2014 Q3 FINANCIAL HIGHLIGHTS MAJOR STATEMENT OF FINANCIAL POSITION ITEMS Group Group Company Company Group Company 2014 2013 2014 2013 Growth

FINANCIAL STATEMENTS THIRD QUARTER ENDED 30TH SEPTEMBER 2014 2014 Q3 FINANCIAL HIGHLIGHTS MAJOR STATEMENT OF FINANCIAL POSITION ITEMS Group Group Company Company Group Company 2014 2013 2014 2013 Growth

New Zealand Equivalent to International Accounting Standard 7 Statement of Cash Flows (NZ IAS 7)

") New Zealand Equivalent to International Accounting Standard 7 Statement of Cash Flows (NZ IAS 7) Issued November 2004 and incorporates amendments to 31 December 2016 other than consequential amendments

New Zealand Equivalent to International Accounting Standard 7 Statement of Cash Flows (NZ IAS 7) Issued November 2004 and incorporates amendments to 31 December 2016 other than consequential amendments

Revenue 42,182 40, , ,230. Operating expenses (38,933) (37,680) (152,250) (151,790) Other operating income 217 1,472 4,354 6,400

(37,680) (152,250) (151,790) Other operating income 217 1,472 4,354 6,400") (The figures have not been audited) CONDENSED CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME Individual Quarter Cumulative Quarter Current Corresponding 12 Months 12 Months Quarter

(The figures have not been audited) CONDENSED CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME Individual Quarter Cumulative Quarter Current Corresponding 12 Months 12 Months Quarter

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 2 CASH FLOW STATEMENTS (PBE IPSAS 2)

") PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 2 (PBE IPSAS 2) Issued September 2014 and incorporates amendments to 31 January 2017 other than consequential amendments resulting

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 2 (PBE IPSAS 2) Issued September 2014 and incorporates amendments to 31 January 2017 other than consequential amendments resulting

UNIT 2 PRIMARY FINANCIAL STATEMENTS IAS 1,7,8,14,18 & IFRS5:

UNIT 2 PRIMARY FINANCIAL STATEMENTS IAS 1,7,8,14,18 & IFRS5: 1 IAS 1 PRESENTATION OF FINANCIAL STATEMENTS OVERVIEW IAS 1 Presentation of Financial Statements sets out the overall requirements for financial

UNIT 2 PRIMARY FINANCIAL STATEMENTS IAS 1,7,8,14,18 & IFRS5: 1 IAS 1 PRESENTATION OF FINANCIAL STATEMENTS OVERVIEW IAS 1 Presentation of Financial Statements sets out the overall requirements for financial

For personal use only

Company Announcement Office ASX Limited ANNOUNCEMENT TO THE MARKET APPENDIX 4E - PRELIMINARY FINAL REPORT (UNAUDITED) FOR THE YEAR ENDED 2016 A.B.N.: 52 054 161 821 Lot 50, Goldmine Road, Helidon, Queensland

Company Announcement Office ASX Limited ANNOUNCEMENT TO THE MARKET APPENDIX 4E - PRELIMINARY FINAL REPORT (UNAUDITED) FOR THE YEAR ENDED 2016 A.B.N.: 52 054 161 821 Lot 50, Goldmine Road, Helidon, Queensland

Appendix 5B. Mining exploration entity and oil and gas exploration entity

Mining exploration entity and oil and gas exploration entity ly report Appendix 5B Rule 5.5 Mining exploration entity and oil and gas exploration entity ly report Introduced 01/07/96 Origin Appendix 8

Mining exploration entity and oil and gas exploration entity ly report Appendix 5B Rule 5.5 Mining exploration entity and oil and gas exploration entity ly report Introduced 01/07/96 Origin Appendix 8

International Equities Corporation Ltd

International Equities Corporation Ltd and Controlled Entities ABN 97 009 089 696 PRELIMINARY FINAL REPORT FOR YEAR ENDED 30 JUNE 2009 APPENDIX 4E APPENDIX 4E PRELIMINARY FINAL REPORT FOR YEAR ENDED 30

International Equities Corporation Ltd and Controlled Entities ABN 97 009 089 696 PRELIMINARY FINAL REPORT FOR YEAR ENDED 30 JUNE 2009 APPENDIX 4E APPENDIX 4E PRELIMINARY FINAL REPORT FOR YEAR ENDED 30

KCE Electronics Public Company Limited and its subsidiaries

Statements of financial position Consolidated Separate financial financial 31 December 31 December Assets Note 2012 2011 2012 2011 Current assets Cash and cash equivalents 7 397,177,878 535,535,464 94,974,827

Statements of financial position Consolidated Separate financial financial 31 December 31 December Assets Note 2012 2011 2012 2011 Current assets Cash and cash equivalents 7 397,177,878 535,535,464 94,974,827

Exposure Draft. Accounting Standard (AS) 7. Statement of Cash Flows

7. Statement of Cash Flows") Exposure Draft Accounting Standard (AS) 7 Statement of Cash Flows Last date for the comments: January 21, 2016 Issued by Accounting Standards Board The Institute of Chartered Accountants of India 1 Exposure

Exposure Draft Accounting Standard (AS) 7 Statement of Cash Flows Last date for the comments: January 21, 2016 Issued by Accounting Standards Board The Institute of Chartered Accountants of India 1 Exposure

CPA Summary Notes. Statement of Cash Flow. Objective of IAS 7

CPA Summary Notes Statement of Cash Flow Objective of IAS 7 The objective of IAS 7 is to require the presentation of information about the historical changes in cash and cash equivalents of an entity by

CPA Summary Notes Statement of Cash Flow Objective of IAS 7 The objective of IAS 7 is to require the presentation of information about the historical changes in cash and cash equivalents of an entity by

SLI Systems Limited and its Subsidiaries Interim Report For the six months ended 31 December 2017

SLI Systems Limited and its Subsidiaries Interim Report For the six months 31 December 2017 Contents Page Consolidated Statement of Comprehensive Income 3 Consolidated Statement of Changes in Equity 4

SLI Systems Limited and its Subsidiaries Interim Report For the six months 31 December 2017 Contents Page Consolidated Statement of Comprehensive Income 3 Consolidated Statement of Changes in Equity 4

Unit 4: Cash Flow Statement(Marks=8) Contents mapping:-

Contents mapping:-") Unit 4: Cash Flow Statement(Marks=8) Contents mapping:- Meaning, objectives and preparation (as per AS 3 (Revised) (Indirect Method only) Scope: (i)adjustments relating to depreciation and amortization,

Unit 4: Cash Flow Statement(Marks=8) Contents mapping:- Meaning, objectives and preparation (as per AS 3 (Revised) (Indirect Method only) Scope: (i)adjustments relating to depreciation and amortization,

IAS 7 : STATEMENT OF CASH FLOWS COMPILED BY: MR. YAGNESH DESAI.

IAS 7 : STATEMENT OF CASH FLOWS CASH FLOWS : TERMINOLOGY Inflows and outflows of cash and cash equivalents. CASH : Comprises cash on hand and demand deposits. CASH EQUIVALENTS : Short-term, highly liquid

IAS 7 : STATEMENT OF CASH FLOWS CASH FLOWS : TERMINOLOGY Inflows and outflows of cash and cash equivalents. CASH : Comprises cash on hand and demand deposits. CASH EQUIVALENTS : Short-term, highly liquid

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35, 36, Sector VI, Pushp Vihar, New Delhi NEW DELHI ISC ACCOUNTS

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35, 36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Companies Act 2013 Applicable for the Eamination

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35, 36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Companies Act 2013 Applicable for the Eamination

Unaudited Condensed Consolidated Statement of Profit or Loss and Other Comprehensive Income For the 4th financial quarter ended 31 December 2015

PRESTAR RESOURCES BHD ( 123066-A ) Unaudited Condensed Consolidated Statement of Profit or Loss and Other Comprehensive Income Individual Quarter Cumulative Quarter Current Year Preceding Year Current

PRESTAR RESOURCES BHD ( 123066-A ) Unaudited Condensed Consolidated Statement of Profit or Loss and Other Comprehensive Income Individual Quarter Cumulative Quarter Current Year Preceding Year Current

Regus plc. Interim Report. Six months ended June 2003

18069_E21932_BRO_V2.qxd 15/9/2003 Regus plc Interim Report Six months June 2003 9:44 am Page a2 2 Interim Report 2003 Chairman s Statement The Regus Group continued to make steady progress during the first

18069_E21932_BRO_V2.qxd 15/9/2003 Regus plc Interim Report Six months June 2003 9:44 am Page a2 2 Interim Report 2003 Chairman s Statement The Regus Group continued to make steady progress during the first

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi NEW DELHI ISC ACCOUNTS

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Revised Schedule VI of Part I & II of Companies

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Revised Schedule VI of Part I & II of Companies

MARKETINGFILE LIMITED

Registered number: 03244074 MARKETINGFILE LIMITED UNAUDITED DIRECTORS' REPORT AND FINANCIAL STATEMENTS COMPANY INFORMATION Directors Alexander Catto Timothy Wise John F Dennehy Kieron Karue Paul R Lo Company

Registered number: 03244074 MARKETINGFILE LIMITED UNAUDITED DIRECTORS' REPORT AND FINANCIAL STATEMENTS COMPANY INFORMATION Directors Alexander Catto Timothy Wise John F Dennehy Kieron Karue Paul R Lo Company

Group profit and loss account Year ended 3 April 1999

Group profit and loss account Year ended 3 April 1999 Notes and page numbers Sales 1 (p44) 8,071.2 7,493.6 Value added tax (560.5) (514.9) Turnover, excluding value added tax 1 (p44) 7,510.7 6,978.7 Cost

Group profit and loss account Year ended 3 April 1999 Notes and page numbers Sales 1 (p44) 8,071.2 7,493.6 Value added tax (560.5) (514.9) Turnover, excluding value added tax 1 (p44) 7,510.7 6,978.7 Cost

Preliminary Results Announcement. Year ended December 2002

Preliminary Results Announcement Year ended December 2002 Financial Highlights Turnover up 9.8m to 133.5m, a 7.9% increase, 12.4% at constant currency Operating margin on continuing operations up from

Preliminary Results Announcement Year ended December 2002 Financial Highlights Turnover up 9.8m to 133.5m, a 7.9% increase, 12.4% at constant currency Operating margin on continuing operations up from

Index to the financial statements

Index to the financial statements Accounting policies 67 68 Acquisitions 96 Adjusted earnings per share 76 Associates 71 84 85 Auditors Remuneration 73 Report to members 65 Balance sheet Company 100 Group

Index to the financial statements Accounting policies 67 68 Acquisitions 96 Adjusted earnings per share 76 Associates 71 84 85 Auditors Remuneration 73 Report to members 65 Balance sheet Company 100 Group

Financial Statements & Report of the Auditors

Financial Statements & Report of the Auditors 45 Significant Accounting Policies a Statement of compliance These financial statements have been prepared in accordance with all applicable Statements of

Financial Statements & Report of the Auditors 45 Significant Accounting Policies a Statement of compliance These financial statements have been prepared in accordance with all applicable Statements of

Appendix 5B. Quarter ended ( current quarter ) December Receipts from product sales and related debtors - -

December Receipts from product sales and related debtors - -") Mining exploration entity ly report Appendix 5B Rule 5.3 Mining exploration entity ly report Introduced 1/7/96. Origin: Appendix 8. Amended 1/7/97, 1/7/98, 30/9/2001, 01/06/10, 17/12/10. Name of entity

Mining exploration entity ly report Appendix 5B Rule 5.3 Mining exploration entity ly report Introduced 1/7/96. Origin: Appendix 8. Amended 1/7/97, 1/7/98, 30/9/2001, 01/06/10, 17/12/10. Name of entity

Statement of Cash Flows

HKAS 7 Revised June 2016August 2017 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2017 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

HKAS 7 Revised June 2016August 2017 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2017 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

Hello Telecom (UK) Plc. Report and Financial Statements. 30 September 2009

Plc. Report and Financial Statements. 30 September 2009") Registered number 4489059 Hello Telecom (UK) Plc Report and Financial Statements 30 September 2009 Report and financial statements Contents Page Company information 1 Chairman's Report 2 Chief Executive's

Registered number 4489059 Hello Telecom (UK) Plc Report and Financial Statements 30 September 2009 Report and financial statements Contents Page Company information 1 Chairman's Report 2 Chief Executive's

Appendix 5B. Brazilian Metals Group Limited. Quarter ended ( current quarter ) March 2011

March 2011") Mining exploration entity ly report Appendix 5B Rule 5.3 Mining exploration entity ly report Introduced 1/7/96. Origin: Appendix 8. Amended 1/7/97, 1/7/98, 30/9/2001, 01/06/10. Name of entity Brazilian

Mining exploration entity ly report Appendix 5B Rule 5.3 Mining exploration entity ly report Introduced 1/7/96. Origin: Appendix 8. Amended 1/7/97, 1/7/98, 30/9/2001, 01/06/10. Name of entity Brazilian

Company accounting policies

Company accounting policies A. Basis of preparation of individual financial statements under UK GAAP These individual financial statements of the Company have been prepared in accordance with applicable

Company accounting policies A. Basis of preparation of individual financial statements under UK GAAP These individual financial statements of the Company have been prepared in accordance with applicable

For personal use only

Introduced 01/07/96 Origin Appendix 8 Amended 01/07/97, 01/07/98, 30/09/01, 01/06/10, 17/12/10, 01/05/2013 Name of entity Tiger Resources Limited Rule 5.3 ABN Quarter ended ( current ) 52 077 110 304 31

Introduced 01/07/96 Origin Appendix 8 Amended 01/07/97, 01/07/98, 30/09/01, 01/06/10, 17/12/10, 01/05/2013 Name of entity Tiger Resources Limited Rule 5.3 ABN Quarter ended ( current ) 52 077 110 304 31

For personal use only

Rule 5.3 Introduced 01/07/96 Origin Appendix 8 Amended 01/07/97, 01/07/98, 30/09/01, 01/06/10, 17/12/10 Name of entity International Coal Limited ABN Quarter ended ( current ) 65 149 197 651 31 March 2015

Rule 5.3 Introduced 01/07/96 Origin Appendix 8 Amended 01/07/97, 01/07/98, 30/09/01, 01/06/10, 17/12/10 Name of entity International Coal Limited ABN Quarter ended ( current ) 65 149 197 651 31 March 2015

Appendix 5B. Quarter ended ( current quarter ) September Receipts from product sales and related debtors - -

September Receipts from product sales and related debtors - -") Mining exploration entity ly report Appendix 5B Rule 5.3 Mining exploration entity ly report Introduced 1/7/96. Origin: Appendix 8. Amended 1/7/97, 1/7/98, 30/9/2001, 01/06/10. Name of entity REGALPOINT

Mining exploration entity ly report Appendix 5B Rule 5.3 Mining exploration entity ly report Introduced 1/7/96. Origin: Appendix 8. Amended 1/7/97, 1/7/98, 30/9/2001, 01/06/10. Name of entity REGALPOINT

LEAVING CERTIFICATE 2010 MARKING SCHEME ACCOUNTING HIGHER LEVEL

Coimisiún na Scrúduithe Stáit State Examinations Commission LEAVING CERTIFICATE 2010 MARKING SCHEME ACCOUNTING HIGHER LEVEL LEAVING CERTIFICATE 2010 MARKING SCHEME ACCOUNTING HIGHER LEVEL 2 LEAVING CERTIFICATE

Coimisiún na Scrúduithe Stáit State Examinations Commission LEAVING CERTIFICATE 2010 MARKING SCHEME ACCOUNTING HIGHER LEVEL LEAVING CERTIFICATE 2010 MARKING SCHEME ACCOUNTING HIGHER LEVEL 2 LEAVING CERTIFICATE

Isles of Scilly Steamship Company Limited

Isles of Scilly Steamship Company Limited Summary financial statements For the period ended Contents Page Director s Report 1 Consolidated Profit and Loss Account 2 Consolidated Balance Sheet 3 Consolidated

Isles of Scilly Steamship Company Limited Summary financial statements For the period ended Contents Page Director s Report 1 Consolidated Profit and Loss Account 2 Consolidated Balance Sheet 3 Consolidated

2016/2/25 Financial Statement Balance Sheet

2016/2/25 Financial Statement Balance Sheet Financial Statement Balance Sheet Accounting Title 2015/12/31 2014/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents

2016/2/25 Financial Statement Balance Sheet Financial Statement Balance Sheet Accounting Title 2015/12/31 2014/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents

MILLENNIUM & COPTHORNE HOTELS PLC TRADING UPDATE AND RESULTS FOR THE THREE MONTHS ENDED 31 MARCH 2004

6 May 2004 MILLENNIUM & COPTHORNE HOTELS PLC TRADING UPDATE AND RESULTS FOR THE THREE MONTHS ENDED 31 MARCH 2004 Millennium & Copthorne Hotels plc today provides a trading update and results for the three

6 May 2004 MILLENNIUM & COPTHORNE HOTELS PLC TRADING UPDATE AND RESULTS FOR THE THREE MONTHS ENDED 31 MARCH 2004 Millennium & Copthorne Hotels plc today provides a trading update and results for the three

Accounting Title 2016/3/ /12/ /3/31 Balance Sheet

Financial Statement Balance Sheet Accounting Title 2016/3/31 2015/12/31 2015/3/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 626,334 624,357 540,732 Current

Financial Statement Balance Sheet Accounting Title 2016/3/31 2015/12/31 2015/3/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 626,334 624,357 540,732 Current