The Interpretation of Financial Statements

|

|

|

- David Stokes

- 5 years ago

- Views:

Transcription

1 The Interpretation of Financial Statements Chapter 16 Luby & O Donoghue (2005)

2 Why use ratio analysis Provides framework Comparison to previous years Trends identified Identify areas of concern Targets can be set Comparison to other similar organisations

3 Limitations Accounting statements present a limited picture Accounting policies can distort any inter-firm comparisons and trend analysis Historical Ratios can be misleading if used in isolation Effects of inflation ignored Year end figures in statements may not be representative of whole year

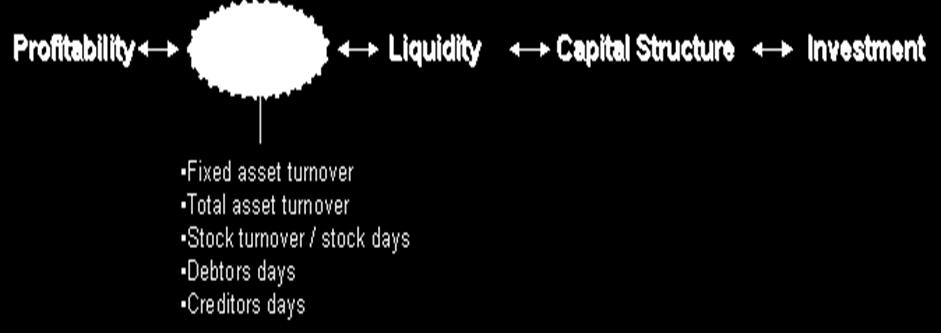

4 Ratio analysis Profitability Efficiency Liquidity Capital Structure Investment

5 Data for ratio illustrations Profit Statements for year ended 31 December Balance sheet as at 31 December Turnover 9,885 Fixed assets 8,595 Less cost of sales Opening stock 500 Current assets Net purchases 6,800 Stock 850 Closing stock (850) (6,450) Debtors 780 Gross profit 3,435 Bank 120 1,750 less expenses (1,200) Net operating profit (PBIT) 2,235 Current liabilities Less interest payable (162) Creditors 585 Net profit before tax 2,073 Bank/ short term loans 500 (1,085) 665 Less taxation (413) Profit after interest and tax 1,660 Long term liabilities less dividends preference (100) Debentures (1,800) less dividends ordinary (800) 7,460 Retained profit for the year 760 Retained profit b/f 1,200 Capital and reserves Retained profit c/f 1,960 Ordinary shares 8,000 4,000 Preference shares 1,000 Market price of shares 1.21 Retained profit 1,960 8 million ordinary shares issued Reserves 500 7,460

6 Profitability Efficiency Liquidity Capital Structure Investment against against sales sales Measured against against capital capital employed employed Gross profit margin Net profit margin Expenses to sales Return on capital employed Return on owners equity

7 Gross profit margin Gross Profit x 100 Sales This indicates the margin of profit between sales and cost of sales. 3,435 x 100= 34.7% 9,885

8 PROFITABILITY Net profit margin Net Profit x 100 Sales This shows the amount of profit after all expenses are deducted. 2,235 x 100 = 22.6% 9,885

9 PROFITABILITY Expenses to sales Expenses x 100 Sales This shows the percentage of sales needing to cover expenses. This ratio assesses the ability of management in controlling expenses of the business. 1,200 x 100 = 12.1% 9,885

10 PROFITABILITY Return on Capital Employed (ROCE) Net Profit x 100 Capital employed Usually net profit before interest and tax share capital + reserves + Loans This shows the ratio of net profit to the investment in the business. 2,235 x 100 = 24.1% 9,260

11 PROFITABILITY Return on Owners Equity (ROOE) Can be before or after interest and tax Net Profit x 100 Shareholders funds Should only relate to ordinary shareholders This ratio assesses the return (profit) for the ordinary (equity) shareholders alone. 1,660 x 100 = 22.3% 7,460

12

13 EFFICIENCY Fixed asset turnover Sales _ Fixed Assets This shows the number of times that the fixed assets are turned over in the period. A high rate of return indicates that a business is operating efficiently and is making the best possible use of assets. A low rate suggests inefficient use of assets. 9,885 = 1.2 : 1 8,595

14 EFFICIENCY Total asset turnover Sales _ Total assets This shows the number of times that the total net assets are turned over in the period. A high rate of return indicates that a business is operating efficiently and is making the best possible use of assets. A low rate suggests inefficient use of assets. 9,885 = : 1 9,260

15 EFFICIENCY Stock turnover Cost of sales Average stock Stock turnover is the average number of times per year that the whole value of stock is purchased and resold. The quicker stock is told the quicker profit will be made on that item. A low rate of turnover shows that old stock is being left on the shelves. 6,450 = 9.6 times 675

16 EFFICIENCY Stock days Stock can also be measured by examining the number of days on average that stock is held. Average stock x 365 Cost of sales 675 x 365 = 38.2 days 6,450

17 EFFICIENCY Debtors days Trade Debtors x 365 Credit Sales Indicates how quickly debtors pay. This ratio can be expressed as the number of days credit taken by debtors. 780 x 365 = 28.8 days 9,885

18 EFFICIENCY Creditors days Trade Creditors x 365 Credit Purchases Indicates how long before creditors are paid. This ratio can be expressed as the number of days credit taken before payment. 585 x 365 = 31.4 days 6,800

19 Return on Capital Employed (ROCE ) Note: the combination of net profit margin and the asset turnover gives the return on capital employed. Profit Margin x Asset Turnover Sales x Net Profit x 100 = Net Profit x100 Capital Employed Sales Capital Employed

20

21 LIQUIDITY Current ratio Current Assets Current Liabilities This is a measure of the short term solvency of a business. 1,750 = 1.6 : 1 1,085

22 Current ratios sector norms Industry Type Current Ratio Manufacturing : 1 Wholesalers 2 : 1 Retail/Supermarkets 0.8 : 1 Hotels, restaurants, fast foods 0.4 : 1

23 LIQUIDITY Acid-test ratio Current Assets - Stock Current Liabilities Also know as quick ratio. Indicates the ability of a business to pay off short term liabilities without resorting to the liquidation of stock or the sale of fixed assets. 900 = 0.8 : 1 1,085

24

25 Capital structure Capital structure measures the funding mix of a business.

26 CAPITAL STRUCTURE Financing Through debt Through equity Interest must be paid on the debt Dividends will be paid to shareholders Interest is tax deductible Dividends are not tax deductible Debt generally cheaper Equity requires higher returns to compensate for risk Debt is risky because interest must be paid Dividends are at discretion of management and may be deferred Loan must be repaid Equity does not require repayment

27 CAPITAL STRUCTURE Gearing Preference shares and long term loans All shareholders funds and long term loans This is the ratio of fixed interest debt and capital to ordinary share capital. 2,800 = 0.38 : 1 7,460 38%

28 CAPITAL STRUCTURE Gearing The higher the ratio of debt to equity, the more dependent the organisation is upon borrowed funds, and the greater the risk that it will be unable to meet interest payments on these funds as they fall due. Low gearing = where debt is less than capital & reserves. Neutral gearing = debt = capital & reserves. High gearing = debt is greater than capital & reserves. < 100% = 100% > 100%

29 CAPITAL STRUCTURE Interest cover Profit before interest Interest payable The ability of a company to meets its interest commitments, measured by expressing the profit before interest as a multiple of the interest paid and payable. 2,235 = 13.8 : 1 162

30

31 INVESTMENT Earnings per share (EPS) Profit available for ordinary dividend Number of equity shares issued Earnings is measured in pence / cents and is concerned with the profits available to ordinary shareholders from which a dividend can be paid. 1,560 = ie 19.5 cent 8,000

32 INVESTMENT Price/earnings ratio (PE) Market Price Earnings per share Market price as a multiple of the latest earnings per share. Used as a relative measure of stock market performance. Relates the EPS to the price the shares sell at in the market. The greater the PE the greater the demand for shares = 6.2 times 0.195

33 Price/earnings ratio (PE) The P/E ratio depends mainly on four things: The overall level of the stock market (e.g. bull or bear). The industry in which the company operates. The company s record. The markets view on the company s prospects. INVESTMENT P/E ratio Commentary <8 The market feels that these companies have poor future prospects and/or are trading in unfashionable business sectors The market feels that these companies have reasonable prospects but are unsure regarding if and when these companies will shine The market feels these companies have very good prospects and that these prospects are beginning to be reflected in the share price as demand for the share increases. Companies with P/Es of 15 are considered good safe blue chip investments >20 These are the boom stocks or high flyers. Their potential is generally reflected already in their share price and the demand for the share is on the increase. These type of companies tend to be young high flyers who retain all their profits for future growth.

34 INVESTMENT Dividend cover Profit available to pay dividend Dividends paid and proposed This ratio indicates the proportion of available profits, which is distributed to shareholders, and the amount which is retained by the organisation. 1,560 = 2 times 800

35 INVESTMENT Dividend yield Dividend per share Price per share The real rate of return on investment in shares x 100 = 8.3% 1.21

36 Dividend yield The average dividend yield for the major world markets over the last twenty years UK Ireland Eurobloc (ex UK) USA Japan Asia pacific (ex Japan) Dividend Yield % 2.7% 1.8% 2.4% 1.5% 0.9% 3.1% (Source: Irish Times Business Supplement)

37 Setting the context The age of the business The size of the business The economic and political environment Industry Trends

38 Company performance number of years Have sales increased or decreased and by what percentage? Has operating profit increased or decreased and by what percentage? Has loan interest increased or decreased and by what percentage? Check the long-term loans in the balance sheet to see if they have increased/decreased. Compare profit after tax to see if it has increased or decreased. Calculate percentage increase/decrease in fixed assets. If assets have been increased, has this been financed through increased loans or issued share capital? Check to see if the business has cash or an overdraft, and is this increasing or decreasing? Check current assets and liabilities for any major increases. Check the percentage increase/ decrease in long-term loans.

39 Company comparison Check both businesses are in the same industry/sector Compare the size of each business. This is normally done, by comparing the total asset levels in the balance sheet (fixed assets + current assets- current liabilities). Compare sales and profit levels. Compare financing. For example is one company highly geared and the other low geared? Compare cash balances/overdraft levels.

40 Sector overviews Hospitality and tourism performance is commented on throughout chapter 16 and should be read and studied carefully. For a retail overview the performance of Arnotts is analysis in a case study from page 339 of the text book.

41 Hospitality ratios Ratio Formula Occupancy ratios Rooms occupied x 100 Rooms available Number of guests x 100 Guest capacity Actual room revenue x100 Potential room revenue Average room rate Average rate per guest Room revenue Rooms occupied Room revenue Number of guests Average spend Sales Number of covers Sales mix Rooms revenue x 100 Total hotel revenue Food revenue x 100 Total hotel revenue Bar revenue x 100 Total hotel revenue

2. Changes in a company s accounting policies and estimates can significantly distort any inter-firm comparisons and trend analysis.

Chapter 17 Solution 17.1 The limitations of ratio analysis are: 1. Accounting statements present a limited picture only of a business. The information included in the accounts does not cover all aspects

Chapter 17 Solution 17.1 The limitations of ratio analysis are: 1. Accounting statements present a limited picture only of a business. The information included in the accounts does not cover all aspects

Cash Flow Statements. Chapter 15. Luby & O Donoghue (2005)

") Cash Flow Statements Chapter 15 Luby & O Donoghue (2005) Cash is king profits can be manufactured by creative accounting but creating cash is impossible. Terry Smith, Accounting for Growth Typical cash

Cash Flow Statements Chapter 15 Luby & O Donoghue (2005) Cash is king profits can be manufactured by creative accounting but creating cash is impossible. Terry Smith, Accounting for Growth Typical cash

Cranswick Plc is a food supplier company listed on the London Stock Exchange. The following

Financial Ratio Analysis Cranswick Plc is a food supplier company listed on the London Stock Exchange. The following represent ratios for the company for the year ended 31 st March 2012. Investors ratios

Financial Ratio Analysis Cranswick Plc is a food supplier company listed on the London Stock Exchange. The following represent ratios for the company for the year ended 31 st March 2012. Investors ratios

Quantitative skills Ratios

gross profit margin Method To calculate gross profit margin, two figures from the income statement are needed: sales revenue and gross profit. The formula for calculating the gross profit margin is: Gross

gross profit margin Method To calculate gross profit margin, two figures from the income statement are needed: sales revenue and gross profit. The formula for calculating the gross profit margin is: Gross

Resource Sheet Accounting

Resource Sheet Accounting Interpretation of Accounts Student Activity Answers (Q1) In the earlier Boyle plc question, calculate the following (use 2 decimal places where appropriate): (a) Return on Capital

Resource Sheet Accounting Interpretation of Accounts Student Activity Answers (Q1) In the earlier Boyle plc question, calculate the following (use 2 decimal places where appropriate): (a) Return on Capital

Understanding Financial Statements. Elizabeth Rankin

Understanding Financial Statements Elizabeth Rankin Overview Accounting Concepts Principles Financial Statements Evaluating Performance Horizontal Analysis Vertical Analysis Ratio Analysis Entity Concept

Understanding Financial Statements Elizabeth Rankin Overview Accounting Concepts Principles Financial Statements Evaluating Performance Horizontal Analysis Vertical Analysis Ratio Analysis Entity Concept

Chapter 19. Financial Statement Analysis. Learning Objectives. The Annual Report Usually Contains...

PowerPoint to accompany Chapter 19 Financial Statement Analysis Learning Objectives 1. Perform a horizontal analysis of comparative financial statements 2. Perform a vertical analysis of financial statements

PowerPoint to accompany Chapter 19 Financial Statement Analysis Learning Objectives 1. Perform a horizontal analysis of comparative financial statements 2. Perform a vertical analysis of financial statements

Drafting Financial Statements (Accounting Practice, Industry and Commerce) (DFS) (2003 standards) Suggested Answers

(DFS) (2003 standards) Suggested Answers") Drafting Financial Statements (Accounting Practice, Industry and Commerce) (DFS) (2003 standards) Suggested Answers SECTION 1 PART A Task 1.1 Loittede plc Consolidated balance sheet as at 30 September,

Drafting Financial Statements (Accounting Practice, Industry and Commerce) (DFS) (2003 standards) Suggested Answers SECTION 1 PART A Task 1.1 Loittede plc Consolidated balance sheet as at 30 September,

ACCOUNTING RATIOS ACTIVITY / TURNOVER RATIOS BY- ANUJ JINDAL

ACCOUNTING RATIOS ACTIVITY / TURNOVER RATIOS BY- ANUJ JINDAL ACTIVITY/ TURNOVER/ EFFICIENCY RATIOS Rapidity with which the resources available to the concern are being used to produce revenue from operations

ACCOUNTING RATIOS ACTIVITY / TURNOVER RATIOS BY- ANUJ JINDAL ACTIVITY/ TURNOVER/ EFFICIENCY RATIOS Rapidity with which the resources available to the concern are being used to produce revenue from operations

myepathshala.com (For Crash Course & Revision)

") 14.1 Introduction of Chapter 14.2 Liquidity Ratios (Formulas) Chapter 14 Accounting Ratios 14.3 Liquidity Ratios (Questions) [Ill. 1, 4, 11, 20, 22] Ill. 1 From the following, compute the Current Ratio

14.1 Introduction of Chapter 14.2 Liquidity Ratios (Formulas) Chapter 14 Accounting Ratios 14.3 Liquidity Ratios (Questions) [Ill. 1, 4, 11, 20, 22] Ill. 1 From the following, compute the Current Ratio

ACCA F3. Provided by Academy of Professional Accounting (APA) Financial Accounting (FA) 财务会计第二十九讲. ACCA Lecturer: Rachel XU

Financial Accounting (FA) 财务会计第二十九讲. ACCA Lecturer: Rachel XU") Professional Accounting Education Provided by Academy of Professional Accounting (APA) ACCA F3 Financial Accounting (FA) 财务会计第二十九讲 ACCA Lecturer: Rachel XU ACCAspace 中国 ACCA 特许公认会计师教育平台 Copyright ACCAspace.com

Professional Accounting Education Provided by Academy of Professional Accounting (APA) ACCA F3 Financial Accounting (FA) 财务会计第二十九讲 ACCA Lecturer: Rachel XU ACCAspace 中国 ACCA 特许公认会计师教育平台 Copyright ACCAspace.com

General Certificate of Education June 2007 Advanced Level Examination. Unit 6 Published Accounts of Limited Companies and Accounting Standards

General Certificate of Education June 2007 Advanced Level Examination ACCOUNTING Unit 6 Published Accounts of Limited Companies and Accounting Standards ACC6 Friday 15 June 2007 9.00 am to 10.15 am For

General Certificate of Education June 2007 Advanced Level Examination ACCOUNTING Unit 6 Published Accounts of Limited Companies and Accounting Standards ACC6 Friday 15 June 2007 9.00 am to 10.15 am For

EXCEL PROFESSIONAL INSTITUTE FINANCIAL STATEMENT INTERPRETATION

EXCEL PROFESSIONAL INSTITUTE FINANCIAL STATEMENT INTERPRETATION Elikem Vulley Most of the marks in an examination question will be available for sensible, well explained and accurate comments on the key

EXCEL PROFESSIONAL INSTITUTE FINANCIAL STATEMENT INTERPRETATION Elikem Vulley Most of the marks in an examination question will be available for sensible, well explained and accurate comments on the key

RATIO ANALYSIS. Inventories + Debtors + Cash & Bank + Receivables / Accruals + Short terms Loans + Marketable Investments

A. LIQUIDITY RATIOS - Short Term Solvency RATIO ANALYSIS Ratio Formula Numerator Denominator Significance/Indicator 1. Current Ratio Current Assets Current Liabilities Inventories + Debtors + Cash & Bank

A. LIQUIDITY RATIOS - Short Term Solvency RATIO ANALYSIS Ratio Formula Numerator Denominator Significance/Indicator 1. Current Ratio Current Assets Current Liabilities Inventories + Debtors + Cash & Bank

An Introduction to Understanding Financial Ratios

An Introduction to Understanding Financial Ratios Business Information Factsheet BIF009 September 2015 Introduction The financial position of any business can be determined from three key financial statements:

An Introduction to Understanding Financial Ratios Business Information Factsheet BIF009 September 2015 Introduction The financial position of any business can be determined from three key financial statements:

ACCOUNTANCY. Part B. Q17. State the significance of Analysis of Financial Statements to the Lenders. (1 mark)

") ACCOUNTANCY [Time allowed: 3 hours] [Maximum marks:80] General Instructions: (i) This question paper contains three parts A, B and C. (ii) Part A is compulsory for all candidates. (iii) Candidates can

ACCOUNTANCY [Time allowed: 3 hours] [Maximum marks:80] General Instructions: (i) This question paper contains three parts A, B and C. (ii) Part A is compulsory for all candidates. (iii) Candidates can

Interpretation of consolidated financial statements

Interpretation of consolidated financial statements F7 for exams in September 2016, December 2016, March 2017 and June 2017 There are additional issues to be considered when calculating and analysing ratios

Interpretation of consolidated financial statements F7 for exams in September 2016, December 2016, March 2017 and June 2017 There are additional issues to be considered when calculating and analysing ratios

Bought to you by AS- Level Accounting Unit 2 Revision Notes

A-PDF Watermark DEMO: Purchase from www.a-pdf.com to remove the watermark for more notes visit Bought to you by AS- Level Accounting Unit 2 Revision Notes Types of Business Organisation: Sole Traders:

A-PDF Watermark DEMO: Purchase from www.a-pdf.com to remove the watermark for more notes visit Bought to you by AS- Level Accounting Unit 2 Revision Notes Types of Business Organisation: Sole Traders:

WEEK 10 Analysis of Financial Statements

WEEK 10 Analysis of Financial Statements Learning Objectives 1. Organize a systematic financial statements analysis using common-size financial statements and ratio analysis. 2. Recognize the potential

WEEK 10 Analysis of Financial Statements Learning Objectives 1. Organize a systematic financial statements analysis using common-size financial statements and ratio analysis. 2. Recognize the potential

Agilent Technologies, Inc.

Agilent Technologies, Inc. Fast Facts Financial Snapshot Operating Performance The company reported revenue of US$XX million during the fiscal year 2011 (2011). The company's revenue grew at a CAGR of

Agilent Technologies, Inc. Fast Facts Financial Snapshot Operating Performance The company reported revenue of US$XX million during the fiscal year 2011 (2011). The company's revenue grew at a CAGR of

Chapter 18 Extra review questions

Accounting for Non-Accountants 10th Online Material 1 Chapter 18 Extra review questions 1 From the data presented below, calculate the following ratios for 2020 and 2021: Gross profit margin Current ratio

Accounting for Non-Accountants 10th Online Material 1 Chapter 18 Extra review questions 1 From the data presented below, calculate the following ratios for 2020 and 2021: Gross profit margin Current ratio

ANALYSIS OF COMPANY FINANCIAL STATEMENTS 09 MAY 2013

ANALYSIS OF COMPANY FINANCIAL STATEMENTS 09 MAY 2013 Lesson Description In this lesson we: Focus on ratios affection liquidity, solvency, risk & returns Discuss ratio calculations & relevant comments Key

ANALYSIS OF COMPANY FINANCIAL STATEMENTS 09 MAY 2013 Lesson Description In this lesson we: Focus on ratios affection liquidity, solvency, risk & returns Discuss ratio calculations & relevant comments Key

New Standards Restaurant

7.1 Using this selection of some of the financial ratios of the New Standards Restaurant, write a short commentary on their liquidity position during the years analyzed. New Standards Restaurant 2008 2009

7.1 Using this selection of some of the financial ratios of the New Standards Restaurant, write a short commentary on their liquidity position during the years analyzed. New Standards Restaurant 2008 2009

Gaiam, Inc. Gaiam, Inc. Financial Snapshot. Operating Performance. Fast Facts. SWOT Analysis. [Figure] Gaiam, Inc. - SWOT Profile Page 1

![Gaiam, Inc. Gaiam, Inc. Financial Snapshot. Operating Performance. Fast Facts. SWOT Analysis. [Figure] Gaiam, Inc. - SWOT Profile Page 1](/thumbs/86/94009915.jpg "Gaiam, Inc. Gaiam, Inc. Financial Snapshot. Operating Performance. Fast Facts. SWOT Analysis. [Figure] Gaiam, Inc. - SWOT Profile Page 1") Gaiam, Inc. Fast Facts Headquarters Address Telephone Fax Website Ticker Symbol, Stock Exchange Financial Snapshot Operating Performance The company reported revenue of US$XX million during the fiscal

Gaiam, Inc. Fast Facts Headquarters Address Telephone Fax Website Ticker Symbol, Stock Exchange Financial Snapshot Operating Performance The company reported revenue of US$XX million during the fiscal

Paper Reference(s) 6002/01 London Examinations GCE. Accounting (Modular Syllabus) Advanced Subsidiary/Advanced Level

6002/01 London Examinations GCE. Accounting (Modular Syllabus) Advanced Subsidiary/Advanced Level") Paper Reference(s) 6002/01 London Examinations GCE Accounting (Modular Syllabus) Advanced Subsidiary/Advanced Level Unit 2 Corporate and Management Accounting Thursday 16 June 2011 Morning Source booklet

Paper Reference(s) 6002/01 London Examinations GCE Accounting (Modular Syllabus) Advanced Subsidiary/Advanced Level Unit 2 Corporate and Management Accounting Thursday 16 June 2011 Morning Source booklet

PAPER 20: FINANCIAL ANALYSIS & BUSINESS VALUATION

PAPER 20: FINANCIAL ANALYSIS & BUSINESS VALUATION Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL C Answer to PTP_Final_Syllabus

PAPER 20: FINANCIAL ANALYSIS & BUSINESS VALUATION Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL C Answer to PTP_Final_Syllabus

Financial Decision Making

Subject no. C16J Chartered Secretaries Qualifying Scheme Level Two Financial Decision Making November 2012 Tuesday afternoon 27 November 2012 Time allowed: 3 hours and 15 minutes (including reading time)

Subject no. C16J Chartered Secretaries Qualifying Scheme Level Two Financial Decision Making November 2012 Tuesday afternoon 27 November 2012 Time allowed: 3 hours and 15 minutes (including reading time)

Chapter 4 Analyzing and Interpreting Financial Statements

Analyzing and Interpreting Financial Statements Solutions to Even-Numbered Problems and Cases 4.2 Northern Electric Corporation (a) (b) (c) Price Earnings 60 Earnings 20 20 60 Earnings 20 3.00 Earnings

Analyzing and Interpreting Financial Statements Solutions to Even-Numbered Problems and Cases 4.2 Northern Electric Corporation (a) (b) (c) Price Earnings 60 Earnings 20 20 60 Earnings 20 3.00 Earnings

INTER CA NOVEMBER 2018

INTER CA NOVEMBER 2018 Sub: FINANCIAL MANAGEMENT Topics Estimation of Working Capital, Receivables Management, Accounting Ratio, Leverages, Capital Structure. Test Code N16 Branch: Multiple Date: (50 Marks)

INTER CA NOVEMBER 2018 Sub: FINANCIAL MANAGEMENT Topics Estimation of Working Capital, Receivables Management, Accounting Ratio, Leverages, Capital Structure. Test Code N16 Branch: Multiple Date: (50 Marks)

CHAPTER Time Value of Money

CHAPTER 6 6.1 Time Value of Money Money has time value. A rupee is less valuable in the future than it is today. Time value of money could be studied under the following heads: Future value of a single

CHAPTER 6 6.1 Time Value of Money Money has time value. A rupee is less valuable in the future than it is today. Time value of money could be studied under the following heads: Future value of a single

Analysis and Interpretation of Financial Statements

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

Nike, Inc. Financial Statement Analysis CHAPTER 17

CHAPTER 17 AP Photo/Matt York Financial Statement Analysis Nike, Inc. J ust do it. These three words identify one of the most recognizable brands in the world, Nike. While this phrase inspires athletes

CHAPTER 17 AP Photo/Matt York Financial Statement Analysis Nike, Inc. J ust do it. These three words identify one of the most recognizable brands in the world, Nike. While this phrase inspires athletes

Proposed Dividend minus Preference Dividend

Interpretation of accounts Definitions 1 Capital Employed Everyone s money Total of Financed by 2 Equity Funds Owners money Equity Capital + Reserves 3 Fixed Interest Capital Borrowed money Debenture Loan

Interpretation of accounts Definitions 1 Capital Employed Everyone s money Total of Financed by 2 Equity Funds Owners money Equity Capital + Reserves 3 Fixed Interest Capital Borrowed money Debenture Loan

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay. Lecture - 14 Ratio Analysis

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay Lecture - 14 Ratio Analysis Dear students, in our last session we are started the

Managerial Accounting Prof. Dr. Varadraj Bapat Department of School of Management Indian Institute of Technology, Bombay Lecture - 14 Ratio Analysis Dear students, in our last session we are started the

AF4 Asset Classes Part 3: Shares

AF4 Asset Classes Part 3: Shares The milestones for this part are to understand: The main types of share. The difference between technical and fundamental analysis How to calculate and interpret Price/Earnings

AF4 Asset Classes Part 3: Shares The milestones for this part are to understand: The main types of share. The difference between technical and fundamental analysis How to calculate and interpret Price/Earnings

LESSON Trend Analysis and Component Percentages. CENTURY 21 ACCOUNTING 2009 South-Western, Cengage Learning

Trend Analysis and Component Percentages Trend Analysis and Component Percentage 2 Financial statements report the financial condition and progress of a business for a fiscal period. Accounting concepts

Trend Analysis and Component Percentages Trend Analysis and Component Percentage 2 Financial statements report the financial condition and progress of a business for a fiscal period. Accounting concepts

Fundamentals Level Skills Module, F7 (IRL)

") Answers Fundamentals Level Skills Module, F7 (IRL) Financial Reporting (Irish) December 2007 Answers 1 (a) Consolidated balance sheet of Plateau as at 30 September 2007 000 000 Fixed assets Goodwill (w

Answers Fundamentals Level Skills Module, F7 (IRL) Financial Reporting (Irish) December 2007 Answers 1 (a) Consolidated balance sheet of Plateau as at 30 September 2007 000 000 Fixed assets Goodwill (w

CPA P1 Managerial Finance. Syllabus 2 Sources of Finance

CPA P1 Managerial Finance Syllabus 2 Sources of Finance Sources of business finance can include: - Share capital - Loan stock - Convertibles and warrants - Government assistance We will evaluate each one

CPA P1 Managerial Finance Syllabus 2 Sources of Finance Sources of business finance can include: - Share capital - Loan stock - Convertibles and warrants - Government assistance We will evaluate each one

Foundation Access Course for Undergraduate Programmes. Examinations for 2010 / Semester 2

Foundation Access Course for Undergraduate Programmes Cohort: FACUP/10A/FT Examinations for 2010 / Semester 2 MODULE: FOUNDATION OF ACCOUNTING 2 MODULE CODE: ACCF 0118 Duration: 2 Hours Reading time: 15

Foundation Access Course for Undergraduate Programmes Cohort: FACUP/10A/FT Examinations for 2010 / Semester 2 MODULE: FOUNDATION OF ACCOUNTING 2 MODULE CODE: ACCF 0118 Duration: 2 Hours Reading time: 15

LESSON 6 RATIO ANALYSIS CONTENTS

LESSON 6 RATIO ANALYSIS CONTENTS 6.0 Aims and Objectives 6.1 Introduction 6.2 Definition 6.3 How the Accounting Ratios are Expressed? 6.4 Purpose, Utility & Limitations of Ratio Analysis 6.5 Classification

LESSON 6 RATIO ANALYSIS CONTENTS 6.0 Aims and Objectives 6.1 Introduction 6.2 Definition 6.3 How the Accounting Ratios are Expressed? 6.4 Purpose, Utility & Limitations of Ratio Analysis 6.5 Classification

ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA. Examiner's Report AA3 EXAMINATION - JULY 2018 (AA31) FINANCIAL ACCOUNTING AND REPORTING

FINANCIAL ACCOUNTING AND REPORTING") ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA Examiner's Report AA3 EXAMINATION - JULY 2018 (AA31) FINANCIAL ACCOUNTING AND REPORTING Most of the common mistakes made by candidates have been identified

ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA Examiner's Report AA3 EXAMINATION - JULY 2018 (AA31) FINANCIAL ACCOUNTING AND REPORTING Most of the common mistakes made by candidates have been identified

Certificate in Accounting

Certificate in Accounting ASE3012 Level 3 Thursday 4 April 2013 Time allowed: 3 hours Information There are 5 questions in this question paper. Total marks available: 100 All questions carry equal marks.

Certificate in Accounting ASE3012 Level 3 Thursday 4 April 2013 Time allowed: 3 hours Information There are 5 questions in this question paper. Total marks available: 100 All questions carry equal marks.

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2 UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION Financial Statements: Structure 6.0 Introduction 6.1 Unit Objectives 6.2 Relationship

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2 UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION Financial Statements: Structure 6.0 Introduction 6.1 Unit Objectives 6.2 Relationship

GAP - Annual Financial Report 2017 Please see attached.

GAP - Annual Financial Report Please see attached. 0090/00023548/en Annual Financial Report G.A.P. VASSILOPOULOS PUBLIC LTD GAP Attachment: 1. GAP VASSILOPOULOS - Annual Results Regulated Publication Date:

GAP - Annual Financial Report Please see attached. 0090/00023548/en Annual Financial Report G.A.P. VASSILOPOULOS PUBLIC LTD GAP Attachment: 1. GAP VASSILOPOULOS - Annual Results Regulated Publication Date:

Week 14, Chap14 Accounting 1A, Financial Accounting

Week 14, Chap14 Accounting 1A, Financial Accounting Analyzing Financial Statements Instructor: Michael Booth Understanding The Business Return on an equity security investment Dividends Increase in share

Week 14, Chap14 Accounting 1A, Financial Accounting Analyzing Financial Statements Instructor: Michael Booth Understanding The Business Return on an equity security investment Dividends Increase in share

INDIAN SCHOOL MUSCAT Senior Section Department of Commerce and Humanities

INDIAN SCHOOL MUSCAT Senior Section Department of Commerce and Humanities Class : 12 Worksheet-No 10 B Ratio Analysis Reference: T.S.Grewal Date of issue --------------2017 ACCOUNTANCY (055) Date of submission

INDIAN SCHOOL MUSCAT Senior Section Department of Commerce and Humanities Class : 12 Worksheet-No 10 B Ratio Analysis Reference: T.S.Grewal Date of issue --------------2017 ACCOUNTANCY (055) Date of submission

FINANCIAL MANAGEMENT

FINANCIAL MANAGEMENT PROFESSIONAL 2 EXAMINATION - APRIL 2010 NOTES: Section A - Answer all three questions. Section B - Answer two questions only. (If you provide answers to more questions than required

FINANCIAL MANAGEMENT PROFESSIONAL 2 EXAMINATION - APRIL 2010 NOTES: Section A - Answer all three questions. Section B - Answer two questions only. (If you provide answers to more questions than required

UNIT IV CAPITAL BUDGETING

UNIT IV CAPITAL BUDGETING Capital Budgeting: Capital budgeting is the process of making investment decision in long-term assets or courses of action. Capital expenditure incurred today is expected to bring

UNIT IV CAPITAL BUDGETING Capital Budgeting: Capital budgeting is the process of making investment decision in long-term assets or courses of action. Capital expenditure incurred today is expected to bring

Ratio Analysis. Assets = Liabilities + Shareholder s Equity

Ratio Analysis The purpose of a financial statement is to disclose information about the financial position of an entity to interested parties. By reporting the finances, shareholders are able to make

Ratio Analysis The purpose of a financial statement is to disclose information about the financial position of an entity to interested parties. By reporting the finances, shareholders are able to make

Profit attributable to: Owners of the parent 112,700 Non-controlling interest (w (ii)) 15, ,900

) 15, ,900") Answers Fundamentals Level Skills Module, Paper F7 (IRL) Financial Reporting (Irish) June 2014 Answers 1 (a) Penketh Consolidated goodwill as at 1 October 2013 Controlling interest Share exchange (90,000

Answers Fundamentals Level Skills Module, Paper F7 (IRL) Financial Reporting (Irish) June 2014 Answers 1 (a) Penketh Consolidated goodwill as at 1 October 2013 Controlling interest Share exchange (90,000

WORKING CAPITAL ANALYSIS OF SELECT CEMENT COMPANIES IN INDIA

CHAPTER - IV WORKING CAPITAL ANALYSIS OF SELECT CEMENT COMPANIES IN INDIA CHAPTER IV WORKING CAPITAL ANALYSIS OF SELECT CEMENT COMPANIES IN INDIA In this chapter an attempt has been made to analyse the

CHAPTER - IV WORKING CAPITAL ANALYSIS OF SELECT CEMENT COMPANIES IN INDIA CHAPTER IV WORKING CAPITAL ANALYSIS OF SELECT CEMENT COMPANIES IN INDIA In this chapter an attempt has been made to analyse the

MILLENNIUM & COPTHORNE HOTELS PLC TRADING UPDATE AND RESULTS FOR THE THREE MONTHS ENDED 31 MARCH 2004

6 May 2004 MILLENNIUM & COPTHORNE HOTELS PLC TRADING UPDATE AND RESULTS FOR THE THREE MONTHS ENDED 31 MARCH 2004 Millennium & Copthorne Hotels plc today provides a trading update and results for the three

6 May 2004 MILLENNIUM & COPTHORNE HOTELS PLC TRADING UPDATE AND RESULTS FOR THE THREE MONTHS ENDED 31 MARCH 2004 Millennium & Copthorne Hotels plc today provides a trading update and results for the three

SOLUTION: ADVANCED FINANCIAL REPORTING, MAY 2014

SOLUTION 1(a) Goodwill is only calculated when control is gained. In substance, it is like the previously held investment is disposed of and a 70% controlled investment acquired. The previously held investment

SOLUTION 1(a) Goodwill is only calculated when control is gained. In substance, it is like the previously held investment is disposed of and a 70% controlled investment acquired. The previously held investment

Goodwill arising on acquisition 98,800

Answers Fundamentals Level Skills Module, Paper F7 (UK) Financial Reporting (United Kingdom) December 2009 Answers 1 (a) (i) Goodwill in Salva at 1 April 2009 000 000 Shares issued (120 million x 80% x

Answers Fundamentals Level Skills Module, Paper F7 (UK) Financial Reporting (United Kingdom) December 2009 Answers 1 (a) (i) Goodwill in Salva at 1 April 2009 000 000 Shares issued (120 million x 80% x

UNIT 3 RATIO ANALYSIS

Understanding and Analysis of Financial Statements UNIT 3 RATIO ANALYSIS Structure Page Nos. 3.0 Introduction 52 3.1 Objectives 54 3.2 Categories of Ratios 54 3.2.1 Long-term Solvency Ratios 3.2.2 Liquidity

Understanding and Analysis of Financial Statements UNIT 3 RATIO ANALYSIS Structure Page Nos. 3.0 Introduction 52 3.1 Objectives 54 3.2 Categories of Ratios 54 3.2.1 Long-term Solvency Ratios 3.2.2 Liquidity

BSc.(Hons) Banking and International Finance, BSc.(Hons) Tourism and Hospitality Management, Diploma in Public Administration and Management

Banking and International Finance, BSc.(Hons) Tourism and Hospitality Management, Diploma in Public Administration and Management") BSc.(Hons) Banking and International Finance, BSc.(Hons) Tourism and Hospitality Management, Diploma in Public Administration and Management & BSc.(Hons) Public Administration and Management Cohort: BBIF/04/FT/PT

BSc.(Hons) Banking and International Finance, BSc.(Hons) Tourism and Hospitality Management, Diploma in Public Administration and Management & BSc.(Hons) Public Administration and Management Cohort: BBIF/04/FT/PT

CASH FLOW STATEMENT & RATIO ANALYSIS 25 APRIL 2013

CASH FLOW STATEMENT & RATIO ANALYSIS 25 APRIL 2013 Lesson Description In this lesson we: Look at a question relating to Cash Flow Statement & Ratio Analysis. Questions Question 1 (Adapted from November

CASH FLOW STATEMENT & RATIO ANALYSIS 25 APRIL 2013 Lesson Description In this lesson we: Look at a question relating to Cash Flow Statement & Ratio Analysis. Questions Question 1 (Adapted from November

Z I C A ZAMBIA INSTITUTE OF CHARTERED ACCOUNTANTS CHARTERED ACCOUNTANTS EXAMINATIONS LICENTIATE LEVEL L6: CORPORATE FINANCIAL MANAGEMENT

Z I C A ZAMBIA INSTITUTE OF CHARTERED ACCOUNTANTS CHARTERED ACCOUNTANTS EXAMINATIONS LICENTIATE LEVEL L6: CORPORATE FINANCIAL MANAGEMENT SERIES: DECEMBER 2011 TOTAL MARKS 100 TIME ALLOWED: THREE (3) HOURS

Z I C A ZAMBIA INSTITUTE OF CHARTERED ACCOUNTANTS CHARTERED ACCOUNTANTS EXAMINATIONS LICENTIATE LEVEL L6: CORPORATE FINANCIAL MANAGEMENT SERIES: DECEMBER 2011 TOTAL MARKS 100 TIME ALLOWED: THREE (3) HOURS

condition & operating results in a condensed form. Financial statements are used as a

2.1 FINANCIAL ANALYSIS Financial statements are formal records of the financial activities of a business, person or other entity and provide an overview of a business or person s financial condition in

2.1 FINANCIAL ANALYSIS Financial statements are formal records of the financial activities of a business, person or other entity and provide an overview of a business or person s financial condition in

ESSENTIALLY, a balance sheet is a historic statement showing

INTERPRETATION OF BALANCE SHEETS AND OTHER FINANCIAL STATEMENTS: PRELIMINARY REFLECTIONS Emmanuel Fava ESSENTIALLY, a balance sheet is a historic statement showing the financial position of a business

INTERPRETATION OF BALANCE SHEETS AND OTHER FINANCIAL STATEMENTS: PRELIMINARY REFLECTIONS Emmanuel Fava ESSENTIALLY, a balance sheet is a historic statement showing the financial position of a business

Article The importance of linking profitability and cash flow when analysing financial statements.

Article The importance of linking profitability and cash flow when analysing financial statements. By: Martin Kelly, BSc (Econ) Hons, DIP.Acc, FCA, MBA, MCMI. Teaching Fellow in Accounting Queens University

Article The importance of linking profitability and cash flow when analysing financial statements. By: Martin Kelly, BSc (Econ) Hons, DIP.Acc, FCA, MBA, MCMI. Teaching Fellow in Accounting Queens University

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By http://vustudents.ning.com 1- What is Financial Management? The procedure of managing the financial resources, as well as accounting and financial

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By http://vustudents.ning.com 1- What is Financial Management? The procedure of managing the financial resources, as well as accounting and financial

KODA LTD Quarterly and Half-Year Financial Statement and Dividend Announcement

KODA LTD Quarterly and Half-Year Financial Statement and Dividend Announcement PART I 1(a) INFORMATION REQUIRED FOR ANNOUNCEMENTS OF QUARTERLY (Q1, Q2 & Q3), HALF-YEAR AND FULL YEAR RESULTS An income statement

KODA LTD Quarterly and Half-Year Financial Statement and Dividend Announcement PART I 1(a) INFORMATION REQUIRED FOR ANNOUNCEMENTS OF QUARTERLY (Q1, Q2 & Q3), HALF-YEAR AND FULL YEAR RESULTS An income statement

PAPER 20: FINANCIAL ANALYSIS & BUSINESS VALUATION

PAPER 20: FINANCIAL ANALYSIS & BUSINESS VALUATION Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL C PTP_Final_Syllabus 2012_Dec2015_Set

PAPER 20: FINANCIAL ANALYSIS & BUSINESS VALUATION Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 LEVEL C PTP_Final_Syllabus 2012_Dec2015_Set

Financial statements aim at providing financial

Accounting Ratios 5 LEARNING OBJECTIVES After studying this chapter, you will be able to : Explain the meaning, objectives and limitations of analysis using accounting ratios; Identify the various types

Accounting Ratios 5 LEARNING OBJECTIVES After studying this chapter, you will be able to : Explain the meaning, objectives and limitations of analysis using accounting ratios; Identify the various types

Parent Company Financial Statements

IHG Annual Report and Form 20-F Parent Company Financial Statements 156 Parent company balance sheet 157 Notes to the Parent Company Financial Statements Stay Guest Journey Step four The Stay phase of

IHG Annual Report and Form 20-F Parent Company Financial Statements 156 Parent company balance sheet 157 Notes to the Parent Company Financial Statements Stay Guest Journey Step four The Stay phase of

Name of Document PURCHASE ORDER DELIVERY NOTE. Shows a list of transactions and the amount owed at the end of the month The Customer

Topic Area : Flow & Purpose of Financial Documents Purchase Order Delivery Note Name of Document PURCHASE ORDER DELIVERY NOTE GRN INVOICE Purpose of Document Used by the purchaser to order goods from a

Topic Area : Flow & Purpose of Financial Documents Purchase Order Delivery Note Name of Document PURCHASE ORDER DELIVERY NOTE GRN INVOICE Purpose of Document Used by the purchaser to order goods from a

TIME: 1 HOUR 30 MINUTES. Forenames

SPECIMEN OXFORD CAMBRIDGE AND RSA EXAMINATIONS LEVEL 4 CERTIFICATE IN MANAGEMENT CONSULTING 10331 UNIT 2 ANALYSING FINANCIAL STATEMENTS AND REPORTS SPECIMEN TIME: 1 HOUR 30 MINUTES INSTRUCTIONS TO CANDIDATES

SPECIMEN OXFORD CAMBRIDGE AND RSA EXAMINATIONS LEVEL 4 CERTIFICATE IN MANAGEMENT CONSULTING 10331 UNIT 2 ANALYSING FINANCIAL STATEMENTS AND REPORTS SPECIMEN TIME: 1 HOUR 30 MINUTES INSTRUCTIONS TO CANDIDATES

Financial and Management Accounting Concepts

Financial and Management Accounting Concepts Editorial This month's newsletter focuses on the way in which you can interpret fully the information you present in the form of financial statements to either

Financial and Management Accounting Concepts Editorial This month's newsletter focuses on the way in which you can interpret fully the information you present in the form of financial statements to either

REPORT ON THE FINANCIAL EVALUATION:

REPORT ON THE FINANCIAL EVALUATION: McDONALD'S CORPORATION AND YUM! BRANDS TAMARA AYRAPETOVA The aim of this paper is to perform financial analysis by using financial ratios and to comment, evaluate, and

REPORT ON THE FINANCIAL EVALUATION: McDONALD'S CORPORATION AND YUM! BRANDS TAMARA AYRAPETOVA The aim of this paper is to perform financial analysis by using financial ratios and to comment, evaluate, and

Statement of cash flows PURPOSE & SCOPE

IAS 7 Statement of cash flows PURPOSE & SCOPE Purpose Users needs Scope The fundamental purpose of being in business is to generate profit, as this will increase the owners' wealth. Profitability relates

IAS 7 Statement of cash flows PURPOSE & SCOPE Purpose Users needs Scope The fundamental purpose of being in business is to generate profit, as this will increase the owners' wealth. Profitability relates

Ratio Analysis. CA Past Years Exam Question

Ratio Analysis CA Past Years Exam Question Question : 1 Nov, 2009 From the Following Information, Calculate the Amount of Fixed Assets & Proprietors Funds. 1. Ratio of Fixed Assets to Proprietors Funds

Ratio Analysis CA Past Years Exam Question Question : 1 Nov, 2009 From the Following Information, Calculate the Amount of Fixed Assets & Proprietors Funds. 1. Ratio of Fixed Assets to Proprietors Funds

COMPANIES INTERPRETATION OF FINANCIAL STATEMENTS 13 MARCH 2014

COMPANIES INTERPRETATION OF FINANCIAL STATEMENTS 13 MARCH 2014 In this lesson we: Introduction Lesson Description Look at analysing financial statements and its purpose Consider users of financial statements

COMPANIES INTERPRETATION OF FINANCIAL STATEMENTS 13 MARCH 2014 In this lesson we: Introduction Lesson Description Look at analysing financial statements and its purpose Consider users of financial statements

Prepared by D. El-Hoss. Business Ratios. All questions are the copyright of Cambridge International Examination Board.

Business Ratios 14 5 (a) Explain the meaning of the following accounting terms. Examiner s (i) Margin......... Mark-up.........[4] (b) Zakari is a trader. He provides the following information for the

Business Ratios 14 5 (a) Explain the meaning of the following accounting terms. Examiner s (i) Margin......... Mark-up.........[4] (b) Zakari is a trader. He provides the following information for the

RATIO ANALYSIS OF PUBLICLY TRADED HOTEL COMPANIES LISTED ON THE STOCK EXCHANGE OF THAILAND (SET)

") RATIO ANALYSIS OF PUBLICLY TRADED HOTEL COMPANIES LISTED ON THE STOCK EXCHANGE OF THAILAND (SET) Bhamorasathit, Slisa Chulalongkorn University Katawandee, Punthumadee Chulalongkorn University ABSTRACT

RATIO ANALYSIS OF PUBLICLY TRADED HOTEL COMPANIES LISTED ON THE STOCK EXCHANGE OF THAILAND (SET) Bhamorasathit, Slisa Chulalongkorn University Katawandee, Punthumadee Chulalongkorn University ABSTRACT

Annual Qualification Review 2010

LCCI International Qualifications Level 2 Book-keeping & Accounts Annual Qualification Review 2010 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Level 2 Book-keeping & Accounts Annual Qualification Review 2010 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

Cardinal Health, Inc. - Financial and Strategic SWOT Analysis Review

Publication Date: FEB 2013 7000 Cardinal Place Phone Revenue Dublin, OH Fax Net Profit 43017 Website Employees United States Exchange Industry Company Overview Cardinal Health, Inc. (Cardinal Health) is

Publication Date: FEB 2013 7000 Cardinal Place Phone Revenue Dublin, OH Fax Net Profit 43017 Website Employees United States Exchange Industry Company Overview Cardinal Health, Inc. (Cardinal Health) is

FINANCIAL ACCOUNTING 3

FINBUS4 NOVEMBER 2013 EXAMINATION DATE: 7 NOVEMBER 2013 TIME: 09H00 13H00 TOTAL: 100 MARKS DURATION: 4 HOURS PASS MARK: 40% (BUS-AC3) FINANCIAL ACCOUNTING 3 THIS EXAMINATION PAPER CONSISTS OF 4 QUESTIONS:

FINBUS4 NOVEMBER 2013 EXAMINATION DATE: 7 NOVEMBER 2013 TIME: 09H00 13H00 TOTAL: 100 MARKS DURATION: 4 HOURS PASS MARK: 40% (BUS-AC3) FINANCIAL ACCOUNTING 3 THIS EXAMINATION PAPER CONSISTS OF 4 QUESTIONS:

CHAPTER 20. Analysis and interpretation of financial statements CONTENTS

CHAPTER 20 Analysis and interpretation of financial statements CONTENTS 20.1 Horizontal and vertical analysis 20.2 Trend analysis 20.3 Effect of transactions on ratios 20.4 Ratio analysis 20.5 Ratio analysis

CHAPTER 20 Analysis and interpretation of financial statements CONTENTS 20.1 Horizontal and vertical analysis 20.2 Trend analysis 20.3 Effect of transactions on ratios 20.4 Ratio analysis 20.5 Ratio analysis

Hello Telecom (UK) Plc. Report and Financial Statements. 30 September 2009

Plc. Report and Financial Statements. 30 September 2009") Registered number 4489059 Hello Telecom (UK) Plc Report and Financial Statements 30 September 2009 Report and financial statements Contents Page Company information 1 Chairman's Report 2 Chief Executive's

Registered number 4489059 Hello Telecom (UK) Plc Report and Financial Statements 30 September 2009 Report and financial statements Contents Page Company information 1 Chairman's Report 2 Chief Executive's

Topic 8 Ratio Analysis. Higher Business Management

Topic 8 Ratio Analysis Higher Business Management 1 Learning Intentions / Success Criteria Learning Intentions Ratio analysis Success Criteria Learners should be able to describe and explain: the purpose

Topic 8 Ratio Analysis Higher Business Management 1 Learning Intentions / Success Criteria Learning Intentions Ratio analysis Success Criteria Learners should be able to describe and explain: the purpose

CASH MANAGEMENT. After studying this chapter, the reader should be able to

C H A P T E R 1 1 CASH MANAGEMENT I N T R O D U C T I O N This chapter continues the discussion of cash flows. It illustrates the fact that net income shown on an income statement does not imply that there

C H A P T E R 1 1 CASH MANAGEMENT I N T R O D U C T I O N This chapter continues the discussion of cash flows. It illustrates the fact that net income shown on an income statement does not imply that there

INFORMATION REQUIRED FOR ANNOUNCEMENTS OF QUARTERLY (Q1, Q2 & Q3), HALF-YEAR AND FULL YEAR RESULTS

, HALF-YEAR AND FULL YEAR RESULTS") INFORMATION REQUIRED FOR ANNOUNCEMENTS OF QUARTERLY (Q1, Q2 & Q3), HALF-YEAR AND FULL YEAR RESULTS 1(a) An income statement (for the group) together with a comparative statement for the corresponding period

INFORMATION REQUIRED FOR ANNOUNCEMENTS OF QUARTERLY (Q1, Q2 & Q3), HALF-YEAR AND FULL YEAR RESULTS 1(a) An income statement (for the group) together with a comparative statement for the corresponding period

Profit attributable to: Owners of the parent 116,500 Non-controlling interest (w (ii)) 15, ,700

) 15, ,700") Answers Fundamentals Level Skills Module, Paper F7 (SGP) Financial Reporting (Singapore) June 2014 Answers 1 (a) Penketh Consolidated goodwill as at 1 October 2013 Controlling interest Share exchange (90,000

Answers Fundamentals Level Skills Module, Paper F7 (SGP) Financial Reporting (Singapore) June 2014 Answers 1 (a) Penketh Consolidated goodwill as at 1 October 2013 Controlling interest Share exchange (90,000

FM202. CHAPTERS COVERED : CHAPTERS 1-4 and 16 LEARNER GUIDE : STUDY UNITS 1-3 DUE DATE : 3:00 p.m. 21 AUGUST 2012 TOTAL MARKS : 100

Page 1 of 11 ASSIGNMENT 2 ND SEMESTER : FINANCIAL MANAGEMENT 2 () CHAPTERS COVERED : CHAPTERS 1-4 and 16 LEARNER GUIDE : STUDY UNITS 1-3 DUE DATE : 3:00 p.m. 21 AUGUST 2012 TOTAL MARKS : 100 INSTRUCTIONS

Page 1 of 11 ASSIGNMENT 2 ND SEMESTER : FINANCIAL MANAGEMENT 2 () CHAPTERS COVERED : CHAPTERS 1-4 and 16 LEARNER GUIDE : STUDY UNITS 1-3 DUE DATE : 3:00 p.m. 21 AUGUST 2012 TOTAL MARKS : 100 INSTRUCTIONS

Glossary of Accounting Terms

Glossary of Accounting Terms asset An item of value. audit Examination of an organisation's affairs, mainly through its accounting records. authorised share capital The total number and value of shares

Glossary of Accounting Terms asset An item of value. audit Examination of an organisation's affairs, mainly through its accounting records. authorised share capital The total number and value of shares

ACCA Paper F9 Financial Management. Mock Exam. Commentary, Marking scheme and Suggested solutions

ACCA Paper F9 Financial Management Mock Exam Commentary, Marking scheme and Suggested solutions 2 Suggested solutions Section A D Statement A is incorrect: Matching (not smoothing) is where liabilities

ACCA Paper F9 Financial Management Mock Exam Commentary, Marking scheme and Suggested solutions 2 Suggested solutions Section A D Statement A is incorrect: Matching (not smoothing) is where liabilities

MILLENNIUM & COPTHORNE HOTELS PLC TRADING UPDATE AND RESULTS FOR THE NINE MONTHS ENDED 30 SEPTEMBER 2004

4 November 2004 MILLENNIUM & COPTHORNE HOTELS PLC TRADING UPDATE AND RESULTS FOR THE NINE MONTHS ENDED 30 SEPTEMBER 2004 Millennium & Copthorne Hotels plc today provides a trading update and results for

4 November 2004 MILLENNIUM & COPTHORNE HOTELS PLC TRADING UPDATE AND RESULTS FOR THE NINE MONTHS ENDED 30 SEPTEMBER 2004 Millennium & Copthorne Hotels plc today provides a trading update and results for

EXERCISES E14 1. E14 2.

EXERCISES E14 1. 1. Car manufacturer (high inventory; high property & equipment; lower inventory turnover) 2. Wholesale candy company (high inventory turnover) 3. Retail fur store (high gross profit; high

EXERCISES E14 1. 1. Car manufacturer (high inventory; high property & equipment; lower inventory turnover) 2. Wholesale candy company (high inventory turnover) 3. Retail fur store (high gross profit; high

Financial statements provide a common format for. cash management RATIO ANALYSIS. Figure 1: Income statement of ABC group (management accounts format)

") How to illuminate your business IN THE FIRST PART OF THIS FEATURE, WILL SPINNEY SETS OUT SOME ELEMENTS OF RATIO ANALYSIS THAT CASH MANAGERS SHOULD BE AWARE OF, BOTH IN THEIR DAY-TO-DAY JOB AND ALSO TO

How to illuminate your business IN THE FIRST PART OF THIS FEATURE, WILL SPINNEY SETS OUT SOME ELEMENTS OF RATIO ANALYSIS THAT CASH MANAGERS SHOULD BE AWARE OF, BOTH IN THEIR DAY-TO-DAY JOB AND ALSO TO

LCD Global Investments Ltd Company Registration No N (Incorporated in the Republic of Singapore)

") LCD Global Investments Ltd Company Registration No.197301118N (Incorporated in the Republic of Singapore) UNAUDITED FIFTH QUARTER FINANCIAL STATEMENT AND DIVIDEND ANNOUNCEMENT FOR THE PERIOD ENDED 30 SEPTEMBER

LCD Global Investments Ltd Company Registration No.197301118N (Incorporated in the Republic of Singapore) UNAUDITED FIFTH QUARTER FINANCIAL STATEMENT AND DIVIDEND ANNOUNCEMENT FOR THE PERIOD ENDED 30 SEPTEMBER

Accounting For Managers

Accounting For Managers Professor ZHOU Ning SCHOOL OF ECONOMICS AND MANAGEMENT BEIHANG UNIVERSITY zning80@buaa.edu.cn Chapter 13 Financial Statement Analysis The objectives of Chapter 13 Business objectives

Accounting For Managers Professor ZHOU Ning SCHOOL OF ECONOMICS AND MANAGEMENT BEIHANG UNIVERSITY zning80@buaa.edu.cn Chapter 13 Financial Statement Analysis The objectives of Chapter 13 Business objectives

J B GUPTA CLASSES , Copyright: Dr JB Gupta. Chapter 11. Fundamental analysis.

J B GUPTA CLASSES 98184931932, drjaibhagwan@gmail.com, www.jbguptaclasses.com Copyright: Dr JB Gupta Chapter 11 Fundamental analysis Chapter Index The Concept of Fundamental Analysis Valuation of Goodwill

J B GUPTA CLASSES 98184931932, drjaibhagwan@gmail.com, www.jbguptaclasses.com Copyright: Dr JB Gupta Chapter 11 Fundamental analysis Chapter Index The Concept of Fundamental Analysis Valuation of Goodwill

2010 Annual Results. Analysts Presentation. 22 March 2011

2010 Annual Results Analysts Presentation 22 March 2011 FORWARD-LOOKING STATEMENTS The presentation may contain certain forward-looking statements with respect to the financial condition, results of operations

2010 Annual Results Analysts Presentation 22 March 2011 FORWARD-LOOKING STATEMENTS The presentation may contain certain forward-looking statements with respect to the financial condition, results of operations

For personal use only

PRELIMINARY FULL YEAR REPORT ANNOUNCEMENT The a2 Milk Company Limited For the year ended 30 June 2016 Preliminary full year (12 month) report on consolidated results (including the results for the previous

PRELIMINARY FULL YEAR REPORT ANNOUNCEMENT The a2 Milk Company Limited For the year ended 30 June 2016 Preliminary full year (12 month) report on consolidated results (including the results for the previous

FINANCIAL ANALYSIS AND PLANNING-RATIO ANALYSIS

CHAPTER 3 FINANCIAL ANALYSIS AND PLANNING-RATIO ANALYSIS LEARNING OUTCOMES r r r r r r r Discuss Sources of financial data for Analysis. Discuss financial ratios and its Types. Discuss use of financial

CHAPTER 3 FINANCIAL ANALYSIS AND PLANNING-RATIO ANALYSIS LEARNING OUTCOMES r r r r r r r Discuss Sources of financial data for Analysis. Discuss financial ratios and its Types. Discuss use of financial

Governance and Reporting

Subject no. 56A Diploma in Offshore Finance and Administration Governance and Reporting July 2011 Friday morning 15 July 2011 Time allowed: 3 hours Do not open this examination paper until the presiding

Subject no. 56A Diploma in Offshore Finance and Administration Governance and Reporting July 2011 Friday morning 15 July 2011 Time allowed: 3 hours Do not open this examination paper until the presiding

Insert Cover Image using Slide Master View Do not distort. Hotel Industry India

Insert Cover Image using Slide Master View Do not distort Hotel Industry India September 2014 Executive Summary Market Tourism is slated to grow at 7% CAGR over 2013-18e India has emerged as a favorite

Insert Cover Image using Slide Master View Do not distort Hotel Industry India September 2014 Executive Summary Market Tourism is slated to grow at 7% CAGR over 2013-18e India has emerged as a favorite

CONSOLIDATED PROFIT AND LOSS ACCOUNT CONSTANT EXCHANGE RATES (unaudited)

") 15 CONSOLIDATED PROFIT AND LOSS ACCOUNT CONSTANT EXCHANGE RATES (unaudited) Note: A description of the exchange rate conventions used is given on page 12. US $ Millions constant rates TURNOVER 10,458 10,859

15 CONSOLIDATED PROFIT AND LOSS ACCOUNT CONSTANT EXCHANGE RATES (unaudited) Note: A description of the exchange rate conventions used is given on page 12. US $ Millions constant rates TURNOVER 10,458 10,859

Chapter 10 International finance: theory and practice

Slide 10.1 Chapter 10 International finance: theory and practice Slide 10.2 International financial and equity markets Foreign Exchange Market Money Markets Structured Investment Vehicles (SIVs) and Derivatives

Slide 10.1 Chapter 10 International finance: theory and practice Slide 10.2 International financial and equity markets Foreign Exchange Market Money Markets Structured Investment Vehicles (SIVs) and Derivatives