Class 12 Accountancy NCERT Solutions Cash Flow Statement

|

|

|

- Rosaline Johns

- 5 years ago

- Views:

Transcription

1 Class 12 Accountancy NCERT Solutions Cash Flow Statement TEST YOUR UNDERSTANDING I DO IT YOUR SELF I Question 1. The profit and loss account of Roy Limited is given here under

2

3 Question 2. From the following information calculate net cash from operations

4 TEST YOUR UNDERSTANDING II Question 1. Choose one of the two alternatives given below and fill in the blanks in the following statements (a) If the net profits earned during the year is Rs. 50,000 and the amount of debtors in the beginning and the end of the year is Rs. 10,000 and Rs.20,000 respectively, then the cash from operating activities will be equal to Rs..(Rs. 40,000/ Rs.60,000). Answer Rs. 40,000 (b) If the net profits made during the year are Rs. 50,000 and the bills receivables have decreased by Rs. 10,000 during the year then the cash flow from operating activities will be equal to Rs..(Rs. 40,000/Rs. 60,000). Answer Rs. 60,000 (c) Expenses paid in advance at the end of the year are the profit made during the year (added to/deducted from). Answer Deducted from (d) An increase in accrued income during the particular year is..for calculating the cash flow from operating activities (added to/deducted from). Answer Added to (f) For calculating cash flow from operating activities, provision for doubtful debts is..the profit made during the year (added to/deducted from). Answer Added to Question 2. While computing cash from operating activities, indicate whether the foltowing items witl be added or subtracted from the net profit, if not to be considered write NC.

5 DO IT YOURSELF II Question 1. From the following particulars, calculate cash flows form investing activities Interest received on debentures held as investment Rs.60,000 Dividend received on shares held as investment Rs.10,000 A plot of land had been purchased for investment purposes and was let out for commercial use

6 and rent received Rs. 30,000. Question 2. From the following Information, calculate cash flow from investing and financing activities In year 2011, machine costing Rs. 2,00,000 was sold at a profit of Rs. 1,50,000, depreciation charged on machine during the year 2011 amounted to Rs. 2,50,000.

7 SHORT ANSWER TYPE QUESTIONS Question 1. What is a cash flow statement? Answer A cash flow statement shows inflow and outflow of cash and cash equivalents from various activities of a company during a specific period. The primary objective of cash flow statement is to provide useful information about cash flows (inflows and outflows) of an enterprise during a particular period under various heads, i.e., operating activities, investing activities and financing activities. It explains the reasons of receipts and payments in cash and change in cash balances during an accounting year in a company. Question 2. How the various activities are classified (as per AS-3 revised) while preparing cash flow statement? Answer As per Accounting Standard-3 various activities of cash flow statement are classified into three categories as follows (i) Cash Flow from Operating Activities : These are the principal revenue producing activities of the enterprise and other activities. The cash flow statement begins with the operating activities section. Operating activities generally reflect cash generated and/or paid as a result of the firm s core business functions. Under US GAAP, this category incorporates the cash received from customers, paid to suppliers, paid for operating costs, paid for income taxes, received from interest or dividends, and paid for periodic interest costs.

8 (ii) Investing Activities: These are the acquisition and disposal of long-term assets, other investments not included in cash equivalents. Cash flows from investing activities are those involving non-current capital assets used in the firm s operations, such as Property, Plant, Equipment (PP&E) and intangible assets. When a company invests in new long-term capacity by acquiring either PP&E or another company, the investment is a cash outflow from investing activities. Disposals of these types of assets for cash generate inflows. (iii) Financing Activities : These are the activities that result in changes in the size and composition of the owner s capital and borrowings of the enterprise. Cash flows from financing activities are those that take place between a firm and its investors. These include both the equity investments of stockholders (owners) and the loans from bondholders and other creditors. When the company issues new shares, it records a cash inflow from financing, and when it repurchases shares, pays dividends or pays off debt, it records a cash outflow. Question 3. State the uses of cash flow statement Answer The various uses of cash flow statement are as follows (i) First of all a cash flow statement along with other financial statements provides information that enables users to evaluate changes in net assets of an enterprise, its financial structure (including its liquidity and solvency) and its ability to affect the amounts and timings of cash flows in order to adapt to changing circumstances and opportunities. (ii) Cash flow information is useful in assessing the ability of the enterprise to generate cash and cash equivalents and enables users to develop models to assess and compare the present value of the future cash flows of different enterprises. (iii) It also enhances the comparability of the reporting of operating performance by different enterprises because it eliminates the effects of using different accounting treatments for the same transactions and events. (iv)historical cash flow information is often used as an indicator of the amount, timing and certainty of future cash flows. It is also helpful in checking the accuracy of past assessments of future cash flows and in examining the relationship between profitability and net cash flow and impact of changing prices. Question 4. What are the objectives of preparing cash flow statement? Answer The various objectives of preparing cash flow statement are as follows (i) The first and most important objective of cash flow statement is that helps to ascertain the gross

9 inflows and out flows of cash and cash equivalents from operating, investing and financial activities. (ii) A cash flow statement helps in determining the various causes for change in the cash balances during an accounting period. (iii) A cash flow statement is also prepared to determine the liquidity position of the organisation. (iv) Moreover a cash flow statement is prepared to know about the requirement of cash in future. Question 5. Explain the terms: Cash equivalents, Cash flows. Answer A cash flow statement shows inflows and outflows of cash and cash equivalents from various activities of an enterprise during a particular period. As per AS-3, Cash equivalents means short term highly liquid investments that are readily convertible into known amounts of cash and which are subject to an insignificant risk of changes in value. Thus, cash equivalents refer to such investments that are held for the purpose of meeting short term cash commitments rather than for investments or other purposes. An investment normally qualifies as cash equivalent only when it has a short maturity, of say, three months or less from the date of acquisition. Investments in shares are excluded from cash equivalents unless they are in substantial cash equivalents, e.g., preference shares of a company acquired shortly before their specific redemption date provided there is only insignificant risk of. Failure of the company to repay the amount at maturity. Similarly, short term marketable securities which can be readily converted into cash are treated as cash equivalents. Question 6. Prepare a format of cash flow from operating activities under direct method and indirect method. Answer Format of cash flow from operating activities under direct method is as follows Format of cash flow from operating activities under indirect method is as follows

10 Question 7. Now that you know the meaning of operating activities, state clearly what would constitute the operating activities for the following types of enterprises (i) Hotel (ii) Film production house (iii) Financial enterprise (iv) Media enterprise (v) Steel manufacturing unit (vi) Software business unit Answer Operating Activities: As we know that these are the principal revenue producing activities of the enterprise and other activities. Operating activities generally reflect cash generated and/or paid as a result of the firm s core business functions. Hence, the following will be the operating activities in the above mentioned enterprises respectively (i) In Case of a Hotel :Receipts from sale of goods and services to the customer will be operating activity related to revenue generation. And payment of wages and salaries, electricity, food items and other items used in accommodation and stay of customer will be an operating activity related to expenditure. (ii) Film Production House: In case of film production house revenue generating operating activity would be its receipts from selling film rights of a film to the distributors and its operating activity related to expenditure would be payment made to the staff member, unit, actors, actresses,

11 directors, location rent and air fare etc. (iii) Financial Enterprise: In case of a financial enterprise like bank the receipts from repayment of loans, interest incomes from investments, etc. will be considered as revenue generating operating activity and repayment of loans, recovery expenditure for recover of loans, etc. Salaries of employees will be considered as operating activity related to the expenditure. (iv) Media Enterprise: A media enterprise is involved in service industry and its revenue generating operating activity would be receipts from advertisements. And expenditure related operating activity would be payments to staff, reporters, photographers, etc. (v) Steel Manufacturing Unit :The main source for revenue for a steel manufacturing unit would be its receipts from sale of steel sheets, steel castings, steel rods, etc. And the expenditure related operating activity would be payment for raw material (iron, coal), salaries to staff, etc. (vi) Software Business Unit: A software business unit is basically a service providing unit which get its revenue through receipts from sale of software and renewal of licenses as an operating activity and various payment made by it in the form of salaries to its employees, etc. It is the part of operating activity as expenditure. Question 8. The nature/type of enterprise can change altogether the category into which a particular activity may be classified. Do you agree? Illustrate your answer. Answer Yes, the nature or type of an enterprise can change altogether the category into which a particular activity may be classified. This can be better understood with the help of an example of two firms. One engaged in real estate and the other engaged in general business. For the firm that is engaged in real estate business purchase and sales of building will be part of the operating activity on the other hand firm that is engaged in general business purchase and sales of building will be part of the investing activity. Hence, it can be said that the classification of activities depends on the nature and type of enterprise. LONG ANSWER TYPE QUESTIONS Question 1. Describe the procedure to prepare cash flow statement. Answer The procedure for preparing cash flow statement is as follows Step 1 First of all cash flows from operating activities is ascertain. Step 2 After that cash flows from investing activities is ascertain. Step 3 The third step is to ascertain the cash flows from financing activities.

12 Step 4 Sum up the total of all the three steps and ascertain net increase or decrease. Step 5 Write the opening balance of cash and cash equivalents and deduct it from the amount ascertained in Step 4. The resulting figure arrived is the closing balance of cash and cash equivalents. There are two methods viz Direct Method and Indirect Method for the preparation of cash flow statement. The main difference in direct and indirect method is to calculate the cash flow from operating activities. Computation of rest of the two activities will remain same. Here are the Performance of cash flow statement from both the methods.

13

14

15 Question 2. Describe Direct and Indirect method of ascertaining cash flow from operating activities. Answer Computation of Cash Flow From Operating Activities The first section of cash flow statement, known as cash flow from operating activities, can be prepared by two methods known as direct method and indirect method. (i) Direct Method: In the direct method format, each line of the operating activities section represents a sum of all cheques or deposits in a particular category, e.g., the operating activities section would include such items as cash received from customers; cash paid to suppliers; cash paid for interest; cash paid for wages; cash paid for research and development; cash paid for selling, general, and administrative costs; and any other relevant summary lines. Direct Method Format: Cash flow from operating activities is calculated by direct method as follows

16 (ii) Indirect Method: In indirect method, the net income figure from the income statement is used to calculate the amount of net cash flow from operating activities. Since income statement is prepared on accrual basis in which revenue is recognised when earned and not when received therefore net income does not represent the net cash flow from operating activities and is necessary to adjust EBIT for those items which effect net income although no actual cash has been paid or received against them. Indirect Method: Following is the indirect method formula which is used to calculate cash flow from operating activities Question 3. Explain the major cash inflows and outflows from investing activities. Answer Cash Flows from Investing Activities: The next step in building cash flow statement is to look at money a company spent on new capital investments. If a company capitalizes an investment, then that outflow of money does not show up on the income statement. That s because accounting rules allow the company to depreciate (expense) the cost of the investment over time. From a practical standpoint, if a company purchase an asset such as new plant equipment or

17 machinery, then they most likely paid for that asset in cash. When money leaves a company, we have an outflow of cash that we need to show in our statement. Example In this example, let s say X Company purchased a new computer system for Rs. 15,00,000 along with an assembly line machine for Rs. 20,00,000. These were the only two capital investments made by X Company for the year. In this example, the company was also required to buy a new Machinery worth Rs. 5,00,000 into a special decommissioning fund. Normally, a company might show one line item for the capital investments and label that line item as additions to plant. In this example, we are going to show these items separately In the above example, we saw that the company made investment in fixed assets and used Rs.40,00,000. Question 4. Explain the major Cash inflows and outflows from financing activities. Answer Cash Flows from Financing Activities :The final category of adjustments we need to address on a statement of cash flows is money raised by financing activities. As was the case with cash from operations, we can have both positive and negative adjustments to cash flow depending on the financing activities the company is engaged during the year. Typical adjustments appearing here include changes in long and short term debt (issuing and redemption), issuing of preferred stock, issuing of common stock, retirement of stock, and stock dividends paid in cash. Example In our example, X Company decided to raise Rs. 2,50,000 by issuing common stock. They also issued around Rs.5,00,000 in preference share, and redeemed around Rs. 3,00,000 in long term debt. Finally, they paid a cash

18 In this example, X Company used less money in their financing activities than they generated during the year. NUMERICAL QUESTIONS Question 1. Anand Ltd arrived at a net income of Rs. 5,00,000 for the year ended March 31, Depreciation for the year was Rs. 2,00,000. There was a gain of Rs. 50,000 on assets sold which was credited to profit and loss account. Bills receivable increased during the year by Rs. 40,000 and bills payable also increased by Rs. 60,000. Compute the cash flow from operating activities by the indirect approach. Question 2. From the information given below, you are required to prepare the cash paid for the inventory Cash paid for inventory amounts to Rs. 1,59,500 Note :Purchase is considered to be credit purchase. Inventory in beginning and end has no effect.

19 Question 3. For each of the following transactions, calculate the resulting cash flow and state the nature of cash flow viz, operating, investing and financing. (a) Acquired machinery for Rs. 2,50,000 paying 20% drawn and executing a bond for the balance payable. (b) Paid Rs. 2,50,000 to acquire shares in Informa Tech and received a dividend of Rs.50,000 after acquisition. (c) Sold machinery of original cost Rs. 2,00,000 with an accumulated depreciation of Rs. 1,60,000 for Rs. 60,000. (b) Related to investing activity. Acquiring shares in Informa Tech is an investment and dividend received on it is also part of same (Rs. 2,50,000-50,000= Rs. 2,00,000 outflow). (c) Related to investing activity. It is treated as sale of investment. Rs. 60,000 inflow and Rs. 20,000 as profit on sale of investment as operating activity. Question 4. The following is the profit and loss account of Yamuna Limited Additional Information s (i) Trade debtors decrease by Rs. 30,000 during the year. (ii) Prepaid expenses increase by Rs. 5,000 during the year. (iii) Trade creditors decrease by Rs. 15,000 during the year. (iv)outstanding expenses increased by Rs. 3,000 during the year. (v) Operating expenses included depreciation of Rs. 25,000. Compute net cash provided by operations for the year ended March 31, 2007 by the indirect

20 method Question 5. Compute cash from operations from (i) Profit for the year is a sum of Rs. 10,000 after providing for depreciation of Rs. 2,000. (ii) The current assets of the business for the year ended March 31, 2010 and 2011 are as follows

21 Prepare of cash flow statement from summary cash account. Question 6. From the following Particulars of Bharat Gas Limited, calculate cash flows from investing activities. Also show the workings clearly preparing the ledger accounts. Additional Information (a) Patents were written-off to the extent of Rs. 40,000 and some patents were sold at a profit of Rs.20,000. (b) A machine costing Rs. 1,40,000 (depreciation provided thereon Rs. 60,000) was sold for Rs. 50,000. Depreciation charged during the year was Rs. 1,40,000. (c) On March 31, 2007, 10% investments were purchased for Rs. 1,80,000 and some investments

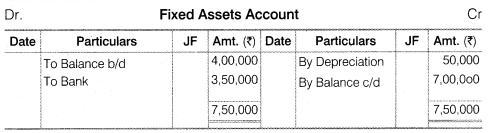

22 were sold at a profit of Rs.20,000. Interest on investment was received on March 31, (d) Amartax Ltd paid 10% on its shares. (e) A plot of land had been purchased for investment purposes and let out for commercial use and rent received Rs.30,000. Working Note Machine costing Rs. 1,40,000 less depreciation Rs. 60,000, present value Rs. 80,000 sold for Rs. 50,000 i.e., loss on sale Rs. 30,000.

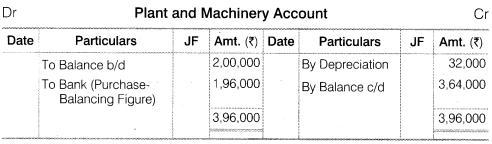

23 Note: Any income received on investment is a part of investments like dividend, interest or rent received. Additional Information Machine costing Rs.80,000 on which accumulated depreciation was Rs.50,000 was sold for Rs. 20,000.

24 Question 8. From the following Balance Sheet of Tiger Super Steel Ltd, prepare Cash flow statement.

25 Additional Information Depreciation Charged on Land and building Rs. 20,000 and plant Rs. 10,000 during the year.

26 Question 9. Prepare cash flow statement from the following information Additional Information Depreciation charged on plant amount to Rs. 80,000.

27

28 Question 10. From the following information, prepare cash flow statement for Yogeta Ltd. Additional Information Net profit for the year after charging Rs. 50,000 as depreciation was Rs. 1,50,000, dividend paid on share was Rs. 50,000, tax provision created during the year amounted to Rs. 60,000.

29

30 Question 11. Following is the Financial Statement of Garima Ltd. Prepare cash flow statement.

31

32

33 Note Debtors and creditors account can also be prepared to calculate cash receipt or cash paid. Question 12. Following is the Balance Sheet of Computer India Ltd

34 Additional Information Interest paid on debenture? 600.

Tiill now you have learnt about the financial

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,

BENEFITS OF CASH FLOW INFORMATION

16 Accounting Standard (AS) 3 Cash Flow Statements Contents OBJECTIVE SCOPE Paragraphs 1-2 BENEFITS OF CASH FLOW INFORMATION 3-4 DEFINITIONS 5-7 Cash and Cash Equivalents 6-7 PRESENTATION OF A CASH FLOW

16 Accounting Standard (AS) 3 Cash Flow Statements Contents OBJECTIVE SCOPE Paragraphs 1-2 BENEFITS OF CASH FLOW INFORMATION 3-4 DEFINITIONS 5-7 Cash and Cash Equivalents 6-7 PRESENTATION OF A CASH FLOW

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Name of business Statement of cash flows for the financial year end 31 December 20X1 (DIRECT METHOD) Inflow /(outflow)

Inflow /(outflow)") Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

6.2 Need for Changes in Financial Position. 6.3 Statement of Changes in Financial Position--- Meaning

Analysis Overview of Financial Statements UNIT 6 STATEMENT OF CHANGES IN FINANCIAL POSITION Structure 6.0 Objectives 6.1 Introduction 6.2 Need for Changes in Financial Position 6.3 Statement of Changes

Analysis Overview of Financial Statements UNIT 6 STATEMENT OF CHANGES IN FINANCIAL POSITION Structure 6.0 Objectives 6.1 Introduction 6.2 Need for Changes in Financial Position 6.3 Statement of Changes

Statement of Cash Flows

Statement of Cash Flows Statement of cash flows General Principles Mandatory for most of the entities Direct and Indirect method Generally starts with PAT (Profit after tax) 2 Overview of AS 3 Requires

Statement of Cash Flows Statement of cash flows General Principles Mandatory for most of the entities Direct and Indirect method Generally starts with PAT (Profit after tax) 2 Overview of AS 3 Requires

6 The following terms are used in this Standard with the meanings specified: Cash comprises cash on hand and demand deposits.

International Accounting Standard 7 Statement of Cash Flows 1 Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

International Accounting Standard 7 Statement of Cash Flows 1 Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows

7 Statement of Cash Flows") Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate

Statement of Cash Flows

IAS Standard 7 Statement of Cash Flows In April 2001 the International Accounting Standards Board adopted IAS 7 Cash Flow Statements, which had originally been issued by the International Accounting Standards

IAS Standard 7 Statement of Cash Flows In April 2001 the International Accounting Standards Board adopted IAS 7 Cash Flow Statements, which had originally been issued by the International Accounting Standards

SLAS 9. Sri Lanka Accounting Standard 9. Cash Flow Statements

Sri Lanka Accounting Standard 9 Cash Flow Statements 107 Contents Sri Lanka Accounting Standard 9 Cash Flow Statements Objective Scope Paragraphs 1-2 Benefits of Cash Flow Information 3-4 Definitions 5

Sri Lanka Accounting Standard 9 Cash Flow Statements 107 Contents Sri Lanka Accounting Standard 9 Cash Flow Statements Objective Scope Paragraphs 1-2 Benefits of Cash Flow Information 3-4 Definitions 5

Statement of Cash Flows

Sri Lanka Accounting Standard - LKAS 7 Statement of Cash Flows LKAS 7 CONTENTS SRI LANKA ACCOUNTING STANDARD - LKAS 7 STATEMENT OF CASH FLOWS OBJECTIVE paragraphs SCOPE 1 BENEFITS OF CASH FLOW INFORMATION

Sri Lanka Accounting Standard - LKAS 7 Statement of Cash Flows LKAS 7 CONTENTS SRI LANKA ACCOUNTING STANDARD - LKAS 7 STATEMENT OF CASH FLOWS OBJECTIVE paragraphs SCOPE 1 BENEFITS OF CASH FLOW INFORMATION

Statement of Cash Flows

International Accounting Standard 7 Statement of Cash Flows This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 7 Cash Flow Statements was issued by the International

International Accounting Standard 7 Statement of Cash Flows This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 7 Cash Flow Statements was issued by the International

FINAL ACCOUNTS vis-à-vis Financial Statements. Samir K Mahajan

FINAL ACCOUNTS vis-à-vis Financial Statements Samir K Mahajan CLASSIFICATION OF FINAL ACCOUNT Trial balance proves the arithmetical accuracy of the business transactions, but it is not the end. The businessman

FINAL ACCOUNTS vis-à-vis Financial Statements Samir K Mahajan CLASSIFICATION OF FINAL ACCOUNT Trial balance proves the arithmetical accuracy of the business transactions, but it is not the end. The businessman

16 Statement of Cash Flows

Chapter 16 Statement of Cash Flows Learning Objectives: Learn about the purpose of the statement of cash flows Learn about the various sections of the statement of cash flows Learn how to prepare a statement

Chapter 16 Statement of Cash Flows Learning Objectives: Learn about the purpose of the statement of cash flows Learn about the various sections of the statement of cash flows Learn how to prepare a statement

Chapter 12 - Reporting and Analyzing Cash Flows. Chapter Outline

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

Financial statements. Chapter One-A. A- Statements of cash flows. 1 IAS 7 Statement of cash flows F5(a)-(h)

-(h)") Chapter One-A Financial statements A- Statements of cash flows Topic list Syllabus reference 1 IAS 7 Statement of cash flows F5(a)-(h) 2 Preparing a statement of cash flows F5(g) Introduction In the long

Chapter One-A Financial statements A- Statements of cash flows Topic list Syllabus reference 1 IAS 7 Statement of cash flows F5(a)-(h) 2 Preparing a statement of cash flows F5(g) Introduction In the long

CHAPTER 12 STATEMENT OF CASH FLOWS

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

Statement of cash flows PURPOSE & SCOPE

IAS 7 Statement of cash flows PURPOSE & SCOPE Purpose Users needs Scope The fundamental purpose of being in business is to generate profit, as this will increase the owners' wealth. Profitability relates

IAS 7 Statement of cash flows PURPOSE & SCOPE Purpose Users needs Scope The fundamental purpose of being in business is to generate profit, as this will increase the owners' wealth. Profitability relates

Cash flow from financing activities. Cash flow from investing activities; Cash flow from operating activities;

COMPONENTS OF CASH FLOW STATEMENT The cash flow statement should report cash flows during the period classified by operating, investing and financing activities. Cash flow statement explains the reasons

COMPONENTS OF CASH FLOW STATEMENT The cash flow statement should report cash flows during the period classified by operating, investing and financing activities. Cash flow statement explains the reasons

Some deferred items for which adjusting entries would be made include: Prepaid insurance Prepaid rent Office supplies Depreciation Unearned revenue

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

Book-III:- Analysis of Financial Statement of a company. Financial Statements of a Company

SUPPORT MATERIAL ACCOUNTANCY CLASS-XII Book-III:- Analysis of Financial Statement of a company Financial Statements of a Company Financial Statements: Financial statements are the end products of accounting

SUPPORT MATERIAL ACCOUNTANCY CLASS-XII Book-III:- Analysis of Financial Statement of a company Financial Statements of a Company Financial Statements: Financial statements are the end products of accounting

HANDOUT FOR WEEK 3 UNDERSTANDING THE INCOME STATEMENT. (Profit and loss statement)

") HANDOUT FOR WEEK 3 UNDERSTANDING THE INCOME STATEMENT Introduction (Profit and loss statement) The financial account system generates and important report that captures the financial performance of the

HANDOUT FOR WEEK 3 UNDERSTANDING THE INCOME STATEMENT Introduction (Profit and loss statement) The financial account system generates and important report that captures the financial performance of the

Project Cost Management

PDHonline Course P104 (8 PDH) Project Cost Management Instructor: William J. Scott, P.E. 2012 PDH Online PDH Center 5272 Meadow Estates Drive Fairfax, VA 22030-6658 Phone & Fax: 703-988-0088 www.pdhonline.org

PDHonline Course P104 (8 PDH) Project Cost Management Instructor: William J. Scott, P.E. 2012 PDH Online PDH Center 5272 Meadow Estates Drive Fairfax, VA 22030-6658 Phone & Fax: 703-988-0088 www.pdhonline.org

Statement of Cash Flows

CHAPTER 14 Statement of Cash Flows LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Prepare the operating activities section of a statement of cash flows

CHAPTER 14 Statement of Cash Flows LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Prepare the operating activities section of a statement of cash flows

Statement of Cash Flows. Statement of Cash Flows. Classification of Business Activities. Learning Objectives

Statement of Cash Flows Learning Objectives 1. Understand the different activities of a business and how this influences the cash flow statement 2. Understand the direct and indirect methods for preparation

Statement of Cash Flows Learning Objectives 1. Understand the different activities of a business and how this influences the cash flow statement 2. Understand the direct and indirect methods for preparation

FINANCIAL STATEMENTS ANALYSIS - AN INTRODUCTION

Financial Statements Analysis - An Introduction 27 FINANCIAL STATEMENTS ANALYSIS - AN INTRODUCTION You have already learnt about the preparation of financial statements i.e. Balance Sheet and Trading and

Financial Statements Analysis - An Introduction 27 FINANCIAL STATEMENTS ANALYSIS - AN INTRODUCTION You have already learnt about the preparation of financial statements i.e. Balance Sheet and Trading and

Rate = 1 n RV / C Where: RV = Residual Value C = Cost n = Life of Asset Calculate the rate if: Cost = 100,000

Solved by ABr & Chanda Rehman Final MCQs It is supposed that on 31st December, 2007, the sundry debtors are amounted to Rs. 40,000. On the basis of past experience, it is estimated that 10% of the sundry

Solved by ABr & Chanda Rehman Final MCQs It is supposed that on 31st December, 2007, the sundry debtors are amounted to Rs. 40,000. On the basis of past experience, it is estimated that 10% of the sundry

Exposure Draft. Accounting Standard (AS) 7. Statement of Cash Flows

7. Statement of Cash Flows") Exposure Draft Accounting Standard (AS) 7 Statement of Cash Flows Last date for the comments: January 21, 2016 Issued by Accounting Standards Board The Institute of Chartered Accountants of India 1 Exposure

Exposure Draft Accounting Standard (AS) 7 Statement of Cash Flows Last date for the comments: January 21, 2016 Issued by Accounting Standards Board The Institute of Chartered Accountants of India 1 Exposure

2. This Standard supersedes IAS 7 Statement of Changes in Financial Position, approved in July 1977.

COMPARISON OF GRAP 2 WITH IAS 7 GRAP 2 IAS 7 DIFFERENCES Objective Objective.01 The cash flow statement identifies the sources of cash inflows, the items on which cash was expended during the reporting

COMPARISON OF GRAP 2 WITH IAS 7 GRAP 2 IAS 7 DIFFERENCES Objective Objective.01 The cash flow statement identifies the sources of cash inflows, the items on which cash was expended during the reporting

STATEMENT OF CASH FLOWS

Chapter 16 STATEMENT OF CASH FLOWS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

Chapter 16 STATEMENT OF CASH FLOWS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

Accounting Functions. The various financial statements are- Income Statement Balance Sheet

Accounting Functions The accounting system provides a structure of maintaining details of business transactions that represent the finances of the organization. The various financial statements are- Income

Accounting Functions The accounting system provides a structure of maintaining details of business transactions that represent the finances of the organization. The various financial statements are- Income

Financial Statements of Companies

2 Financial Statements of Companies BASIC CONCEPTS UNIT 1: PREPARATION OF FINANCIAL STATEMENTS While preparing the final accounts of a company the following should be kept in mind: Requirements of Schedule

2 Financial Statements of Companies BASIC CONCEPTS UNIT 1: PREPARATION OF FINANCIAL STATEMENTS While preparing the final accounts of a company the following should be kept in mind: Requirements of Schedule

CHAPTER: - 8. Analysis of Cash flow

CHAPTER: - 8 Analysis of Cash flow Particular Page No. Introduction 231 Meaning of Certain terms 231 Classification of cash flow 231 Information required for cash flow Statement 233 Utility of Cash Flow

CHAPTER: - 8 Analysis of Cash flow Particular Page No. Introduction 231 Meaning of Certain terms 231 Classification of cash flow 231 Information required for cash flow Statement 233 Utility of Cash Flow

FINANCIAL MANAGEMENT

FINANCIAL MANAGEMENT Question 1: What is financial management? Explain the functions of financial management. (May 13, Nov 11) (Mark 7) Answer: Financial management is that specialized activity which is

FINANCIAL MANAGEMENT Question 1: What is financial management? Explain the functions of financial management. (May 13, Nov 11) (Mark 7) Answer: Financial management is that specialized activity which is

Chapter 13 Statement of Cash Flows Study Guide Solutions Fill-in-the-Blank Equations. Exercises

Chapter 13 Statement of Cash Flows Study Guide Solutions Fill-in-the-Blank Equations 1. Net cash flow from operating activities 2. Change in Cash 3. Cash used to purchase property, plant, and equipment

Chapter 13 Statement of Cash Flows Study Guide Solutions Fill-in-the-Blank Equations 1. Net cash flow from operating activities 2. Change in Cash 3. Cash used to purchase property, plant, and equipment

Learning Outcomes. The Statement of Cash Flows. Chapter 4: The Income Statement, Comprehensive Income and The Statement of Cash Flows: Part 2

Chapter 4: The Income Statement, Comprehensive Income and The Statement of Cash Flows: Part 2 The Statement of Cash Flows Dr. Chula King Intermediate Accounting 1 Learning Outcomes After completing this

Chapter 4: The Income Statement, Comprehensive Income and The Statement of Cash Flows: Part 2 The Statement of Cash Flows Dr. Chula King Intermediate Accounting 1 Learning Outcomes After completing this

Ind AS 7 Statement of Cash Flows. EIRC, Kolkata. Mohit Jain 16 February For discussion purposes only

Ind AS 7 Statement of Cash Flows EIRC, Kolkata Mohit Jain 16 February 2018 For discussion purposes only Overview of Ind AS 7 Requires presentation of a statement of cash flows as an integral part of financial

Ind AS 7 Statement of Cash Flows EIRC, Kolkata Mohit Jain 16 February 2018 For discussion purposes only Overview of Ind AS 7 Requires presentation of a statement of cash flows as an integral part of financial

Statement of Cash Flows

HKAS 7 Revised June 2016August 2017 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2017 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

HKAS 7 Revised June 2016August 2017 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2017 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

Paper-12 : COMPANY ACCOUNTS & AUDIT

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

How to Read Financial Statements 2015

CORPORATE LAW AND PRACTICE Course Handbook Series Number B-2157 How to Read Financial Statements 2015 Chair Chad Rucker To order this book, call (800) 260-4PLI or fax us at (800) 321-0093. Ask our Customer

CORPORATE LAW AND PRACTICE Course Handbook Series Number B-2157 How to Read Financial Statements 2015 Chair Chad Rucker To order this book, call (800) 260-4PLI or fax us at (800) 321-0093. Ask our Customer

A CLEAR UNDERSTANDING OF THE INDUSTRY

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

SET - I Paper 2-Fundamentals of Accounting

SET - I Paper 2-Fundamentals of Accounting Full Marks: 100 Time allowed: 3 Hours PART A I. Choose the correct answer from the given four alternatives: [6 1=6] 1. Accounting function does not include (a)

SET - I Paper 2-Fundamentals of Accounting Full Marks: 100 Time allowed: 3 Hours PART A I. Choose the correct answer from the given four alternatives: [6 1=6] 1. Accounting function does not include (a)

MANAGEMENT ACCOUNTING - CASH FLOW

MANAGEMENT ACCOUNTING - CASH FLOW http://www.tutorialspoint.com/accounting_basics/management_accounting_cash_flow.htm Copyright tutorialspoint.com It is very important for a business to keep adequate cash

MANAGEMENT ACCOUNTING - CASH FLOW http://www.tutorialspoint.com/accounting_basics/management_accounting_cash_flow.htm Copyright tutorialspoint.com It is very important for a business to keep adequate cash

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

The statement of cash flows reports cash flows, cash receipts, and cash payments, to show where cash came from and how it was spent.

Accounting Fundamentals Lesson 10 10.0 Cash Flow Statement The balance sheet reports financial position, and balance sheets from two periods show whether cash increased or decreased. But that doesn t tell

Accounting Fundamentals Lesson 10 10.0 Cash Flow Statement The balance sheet reports financial position, and balance sheets from two periods show whether cash increased or decreased. But that doesn t tell

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2 UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION Financial Statements: Structure 6.0 Introduction 6.1 Unit Objectives 6.2 Relationship

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2 UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION Financial Statements: Structure 6.0 Introduction 6.1 Unit Objectives 6.2 Relationship

ACCOUNTANCY PROBLEMS

ACCOUNTANCY PROBLEMS 1. Calculate the CR of VGC.Ltd from the following particulars. Machinery 27,000 Trade Receivables 1,10,000 Current investments 30,000 Debentures (to be redeemed after 2 years) 2,10,000

ACCOUNTANCY PROBLEMS 1. Calculate the CR of VGC.Ltd from the following particulars. Machinery 27,000 Trade Receivables 1,10,000 Current investments 30,000 Debentures (to be redeemed after 2 years) 2,10,000

IAS 7 : STATEMENT OF CASH FLOWS COMPILED BY: MR. YAGNESH DESAI.

IAS 7 : STATEMENT OF CASH FLOWS CASH FLOWS : TERMINOLOGY Inflows and outflows of cash and cash equivalents. CASH : Comprises cash on hand and demand deposits. CASH EQUIVALENTS : Short-term, highly liquid

IAS 7 : STATEMENT OF CASH FLOWS CASH FLOWS : TERMINOLOGY Inflows and outflows of cash and cash equivalents. CASH : Comprises cash on hand and demand deposits. CASH EQUIVALENTS : Short-term, highly liquid

Financial Statements, Taxes and Cash Flow

Financial Statements, Taxes and Cash Flow Faculty of Business Administration Lakehead University Spring 2003 May 5, 2003 2.1 The Balance Sheet 2.2 The Income Statement 2.3 Cash Flow 2.4 Taxes 2.5 Capital

Financial Statements, Taxes and Cash Flow Faculty of Business Administration Lakehead University Spring 2003 May 5, 2003 2.1 The Balance Sheet 2.2 The Income Statement 2.3 Cash Flow 2.4 Taxes 2.5 Capital

IAS 7: Statement of Cash Flows

IAS 7: Statement of Cash Flows The Statement of Cash Flows is one of the primary statements that comprise a complete set of IFRS-compliant financial statements, as required by IAS 1: Presentation of Financial

IAS 7: Statement of Cash Flows The Statement of Cash Flows is one of the primary statements that comprise a complete set of IFRS-compliant financial statements, as required by IAS 1: Presentation of Financial

ACCOUNTING RATIOS MCQs LIQUIDITY RATIOS BY- ANUJ JINDAL

ACCOUNTING RATIOS MCQs LIQUIDITY RATIOS BY- ANUJ JINDAL LIQUIDITY RATIOS CURRENT RATIO / WORKING CAPITAL RATIO: Current Ratio= current assets/ current liabilities LIQUIDITY RATIOS QUICK/ACID TEST/ LIQUID

ACCOUNTING RATIOS MCQs LIQUIDITY RATIOS BY- ANUJ JINDAL LIQUIDITY RATIOS CURRENT RATIO / WORKING CAPITAL RATIO: Current Ratio= current assets/ current liabilities LIQUIDITY RATIOS QUICK/ACID TEST/ LIQUID

Paper No:34 Solved by Chanda Rehman & ABr

Paper No:34 Solved by Chanda Rehman & ABr FINALTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Time: 120 min Marks: 87 Question No: 1 ( Marks: 1 ) - Please choose one We can say that

Paper No:34 Solved by Chanda Rehman & ABr FINALTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Time: 120 min Marks: 87 Question No: 1 ( Marks: 1 ) - Please choose one We can say that

Reading & Understanding Financial Statements

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

Reading & Understanding Financial Statements. A Guide to Financial Reporting

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi NEW DELHI ISC ACCOUNTS

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Revised Schedule VI of Part I & II of Companies

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Revised Schedule VI of Part I & II of Companies

Group statements of cash flows

Group statements of cash flows Topic list Syllabus reference 1 Cash flows D1 2 IAS 7 Statement of cash flows: Single company D1 3 Consolidated statements of cash flows D1 Introduction A statement of cash

Group statements of cash flows Topic list Syllabus reference 1 Cash flows D1 2 IAS 7 Statement of cash flows: Single company D1 3 Consolidated statements of cash flows D1 Introduction A statement of cash

NC 824. First Year B. C. A. Examination. April / May Financial Accounting & Management. Time : 3 Hours] [Total Marks : 50

![NC 824. First Year B. C. A. Examination. April / May Financial Accounting & Management. Time : 3 Hours] [Total Marks : 50](/thumbs/95/123010063.jpg "NC 824. First Year B. C. A. Examination. April / May Financial Accounting & Management. Time : 3 Hours] [Total Marks : 50") NC 824 First Year B. C. A. Examination April / May 2003 Financial Accounting & Management Seat No. Time : 3 Hours] [Total Marks : 50 Instructions : (1) Figures to the right indicate marks. (2) Show calculations

NC 824 First Year B. C. A. Examination April / May 2003 Financial Accounting & Management Seat No. Time : 3 Hours] [Total Marks : 50 Instructions : (1) Figures to the right indicate marks. (2) Show calculations

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 2 CASH FLOW STATEMENTS (PBE IPSAS 2)

") PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 2 (PBE IPSAS 2) Issued September 2014 and incorporates amendments to 31 January 2017 other than consequential amendments resulting

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 2 (PBE IPSAS 2) Issued September 2014 and incorporates amendments to 31 January 2017 other than consequential amendments resulting

Visit Free Slides and Ebooks : CHAPTER 23. Statement of Cash Flows

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

As at March 31, 2017 Balance Sheet as at March 31, 2018 Note No. Rs. Lakhs Rs. Lakhs Rs. Lakhs

As at March 31, 2018 As at March 31, 2017 Balance Sheet as at March 31, 2018 Note No. Rs. Lakhs Rs. Lakhs Rs. Lakhs Particulars ASSETS Non-current assets Property, plant and equipment 1.1 162.81 42.76

As at March 31, 2018 As at March 31, 2017 Balance Sheet as at March 31, 2018 Note No. Rs. Lakhs Rs. Lakhs Rs. Lakhs Particulars ASSETS Non-current assets Property, plant and equipment 1.1 162.81 42.76

ACCOUNTANCY. Part B. Q17. State the significance of Analysis of Financial Statements to the Lenders. (1 mark)

") ACCOUNTANCY [Time allowed: 3 hours] [Maximum marks:80] General Instructions: (i) This question paper contains three parts A, B and C. (ii) Part A is compulsory for all candidates. (iii) Candidates can

ACCOUNTANCY [Time allowed: 3 hours] [Maximum marks:80] General Instructions: (i) This question paper contains three parts A, B and C. (ii) Part A is compulsory for all candidates. (iii) Candidates can

myepathshala.com (For Crash Course & Revision)

") 14.1 Introduction of Chapter 14.2 Liquidity Ratios (Formulas) Chapter 14 Accounting Ratios 14.3 Liquidity Ratios (Questions) [Ill. 1, 4, 11, 20, 22] Ill. 1 From the following, compute the Current Ratio

14.1 Introduction of Chapter 14.2 Liquidity Ratios (Formulas) Chapter 14 Accounting Ratios 14.3 Liquidity Ratios (Questions) [Ill. 1, 4, 11, 20, 22] Ill. 1 From the following, compute the Current Ratio

Module 7 Statement of Cash Flows

IFRS for SMEs Standard (2015) + Q&As IFRS Foundation Supporting Material for the IFRS for SMEs Standard Module 7 Statement of Cash Flows IFRS Foundation Supporting Material for the IFRS for SMEs Standard

IFRS for SMEs Standard (2015) + Q&As IFRS Foundation Supporting Material for the IFRS for SMEs Standard Module 7 Statement of Cash Flows IFRS Foundation Supporting Material for the IFRS for SMEs Standard

Statement of Cash Flows

CA BUSINESS SCHOOL EXECUTIVE DIPLOMA IN BUSINESS AND ACCOUNTING STRATEGY SEMESTER 1 LKAS 07 Statement of Cash Flows M B G Wimalarathna (FCA, FCMA, MCIM, FMAAT, MCPM)(MBA PIM/USJ) Objective Information

CA BUSINESS SCHOOL EXECUTIVE DIPLOMA IN BUSINESS AND ACCOUNTING STRATEGY SEMESTER 1 LKAS 07 Statement of Cash Flows M B G Wimalarathna (FCA, FCMA, MCIM, FMAAT, MCPM)(MBA PIM/USJ) Objective Information

CHAPTER 17. The Cash Flow Statement. Brief Questions Exercises 12, 13 3, 4, 5, 11 6, 7, 8, 9, 10, 11

CHAPTER 17 The Cash Flow Statement ASSIGNMENT CLASSIFICATION TABLE Study Objectives Brief Questions Exercises Exercises Problems Set A Problems Set B 1. Describe the purpose and content of the cash flow

CHAPTER 17 The Cash Flow Statement ASSIGNMENT CLASSIFICATION TABLE Study Objectives Brief Questions Exercises Exercises Problems Set A Problems Set B 1. Describe the purpose and content of the cash flow

CASH FLOWS FROM OPERATING ACTIVITIES

1 CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers (calc a) Cash paid to suppliers and employees (calc b) Cash generated from / (used in) operations Dividends received Interest received

1 CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers (calc a) Cash paid to suppliers and employees (calc b) Cash generated from / (used in) operations Dividends received Interest received

Analysis of Financial Statement Chapter VI. Answers to the very short answers questions.

Analysis of Financial Statement Chapter VI Answers to the very short answers questions. Ans.1 Ans.2 Analysis of Financial statement is the systematic process of identifying the financial strength and weaknesses

Analysis of Financial Statement Chapter VI Answers to the very short answers questions. Ans.1 Ans.2 Analysis of Financial statement is the systematic process of identifying the financial strength and weaknesses

2.1 MEANING AND BUSINESS ENTITY CONCEPT

Accounting Concepts 2 ACCOUNTING CONCEPTS In the previous lesson, you have studied the meaning and nature of business transactions and objectives of financial accounting. In order to maintain uniformity

Accounting Concepts 2 ACCOUNTING CONCEPTS In the previous lesson, you have studied the meaning and nature of business transactions and objectives of financial accounting. In order to maintain uniformity

14. Statement of cash flows

14. Statement of cash flows Accounting and reporting by charities EPOSURE DRAFT Introduction 14.1. Charities preparing their accounts under FRS 102 must provide a statement of cash flows and should refer

14. Statement of cash flows Accounting and reporting by charities EPOSURE DRAFT Introduction 14.1. Charities preparing their accounts under FRS 102 must provide a statement of cash flows and should refer

CS101 Introduction of computing

FINAL TERM EXAMINATION MGT101- Financial Accounting (PAPER 1). Question No: 1 (Marks: 1 ) basic accounting principle/concept according to which Business is independent from its owner(s) is known as: Separate

FINAL TERM EXAMINATION MGT101- Financial Accounting (PAPER 1). Question No: 1 (Marks: 1 ) basic accounting principle/concept according to which Business is independent from its owner(s) is known as: Separate

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES INVESTING ACTIVITIES FINANCING ACTIVITIES

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson. The statement of cash flows is a required component of financial statements.

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson The statement of cash flows is a required component of financial statements. BASICS OF CASH FLOW REPORTING Purpose of the Statement

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson The statement of cash flows is a required component of financial statements. BASICS OF CASH FLOW REPORTING Purpose of the Statement

New Zealand Equivalent to International Accounting Standard 7 Statement of Cash Flows (NZ IAS 7)

") New Zealand Equivalent to International Accounting Standard 7 Statement of Cash Flows (NZ IAS 7) Issued November 2004 and incorporates amendments up to and including 31 December 2012 This Standard was

New Zealand Equivalent to International Accounting Standard 7 Statement of Cash Flows (NZ IAS 7) Issued November 2004 and incorporates amendments up to and including 31 December 2012 This Standard was

REVISED OUTLINE GUIDANCE NOTES

REVISED OUTLINE GUIDANCE NOTES regarding adoption of Schedule VI to the Companies Act 1956 in the subject of ACCOUNTANCY Class XII For the Board Examination, March 2014 1 CONTENT Chapter 1: GENERAL INTRODUCTION

REVISED OUTLINE GUIDANCE NOTES regarding adoption of Schedule VI to the Companies Act 1956 in the subject of ACCOUNTANCY Class XII For the Board Examination, March 2014 1 CONTENT Chapter 1: GENERAL INTRODUCTION

Learning Objectives. Chapter 5. Balance Sheet. Learning Objective 1, 2, 3. Liquidity. Chapter Overview. Balance Sheet and Statement of Cash Flows

Chapter 5 Balance Sheet and Statement of Cash Flows Campbell, Coca-Cola, American Airlines, Borders Learning Objectives 1. Explain uses, limitations of a balance sheet 2. Identify major classifications

Chapter 5 Balance Sheet and Statement of Cash Flows Campbell, Coca-Cola, American Airlines, Borders Learning Objectives 1. Explain uses, limitations of a balance sheet 2. Identify major classifications

You are provided with the following transactions that took place during a recent fis-

Chapter 17 PROBLEMS: SET C You are provided with the following transactions that took place during a recent fis- P17-1C cal year. (a) (b) (c) (d) (e) (f) (g) (h) (i) (j) Cash Inflow, Where Reported Outflow,

Chapter 17 PROBLEMS: SET C You are provided with the following transactions that took place during a recent fis- P17-1C cal year. (a) (b) (c) (d) (e) (f) (g) (h) (i) (j) Cash Inflow, Where Reported Outflow,

Using Financial Statements in the Credit Review Process. Wendi Rosenblatt, Hearst Television

Using Financial Statements in the Credit Review Process Wendi Rosenblatt, Hearst Television Agenda What is Available Financial Statement Overview DineEquity, Inc. Annual Report/Form 10K Review Availability

Using Financial Statements in the Credit Review Process Wendi Rosenblatt, Hearst Television Agenda What is Available Financial Statement Overview DineEquity, Inc. Annual Report/Form 10K Review Availability

MGT101 FINANCIAL ACCOUNTING SOLVED QUIZZES 3 LESSON 1 30

MGT101 FINANCIAL ACCOUNTING SOLVED QUIZZES 3 LESSON 1 30 Wages paid to laborers working in the manufacturing department is treated as an expense of: Cost of goods sold Administrative expense Selling expense

MGT101 FINANCIAL ACCOUNTING SOLVED QUIZZES 3 LESSON 1 30 Wages paid to laborers working in the manufacturing department is treated as an expense of: Cost of goods sold Administrative expense Selling expense

MIDTERM EXAMINATION Spring 2010 MGT101- Financial Accounting (Session - 6)

") MIDTERM EXAMINATION Spring 2010 MGT101- Financial Accounting (Session - 6) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Double entry accounting system includes: Accrual accounting

MIDTERM EXAMINATION Spring 2010 MGT101- Financial Accounting (Session - 6) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Double entry accounting system includes: Accrual accounting

Capsule on Accounting Standards

Capsule on Accounting Standards Conducted by Young Members Empowerment Committee jointly with Accounting Standards Board Presented by CA Manish C. Iyer, Deputy Director, Technical Directorate, ICAI 1 Standards

Capsule on Accounting Standards Conducted by Young Members Empowerment Committee jointly with Accounting Standards Board Presented by CA Manish C. Iyer, Deputy Director, Technical Directorate, ICAI 1 Standards

US Financial Reporting - Primary Terms (Definition Report)

") 1 String usfr-gc General Concepts (usfr-gc:generalconcepts) This is a category for storing general concepts. General concepts are high-level business reporting concepts such as "assets" and "liabilities"

1 String usfr-gc General Concepts (usfr-gc:generalconcepts) This is a category for storing general concepts. General concepts are high-level business reporting concepts such as "assets" and "liabilities"

Unappropriated retained earnings (accumulated deficit) Total unappropriated retained earnings (accumulated deficit) 676, ,797 Total retained ear

Total unappropriated retained earnings (accumulated deficit) 676, ,797 Total retained ear") Financial Statement Balance Sheet Accounting Title 2014/12/31 2013/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 1,183,185 1,177,682 Current bond investment

Financial Statement Balance Sheet Accounting Title 2014/12/31 2013/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 1,183,185 1,177,682 Current bond investment

Engineering Economics and Financial Accounting

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

Unit 4: Cash Flow Statement(Marks=8) Contents mapping:-

Contents mapping:-") Unit 4: Cash Flow Statement(Marks=8) Contents mapping:- Meaning, objectives and preparation (as per AS 3 (Revised) (Indirect Method only) Scope: (i)adjustments relating to depreciation and amortization,

Unit 4: Cash Flow Statement(Marks=8) Contents mapping:- Meaning, objectives and preparation (as per AS 3 (Revised) (Indirect Method only) Scope: (i)adjustments relating to depreciation and amortization,

Statement of Cash Flows

13-1 13 Statement of Cash Flows Learning Objectives 1 2 Discuss the usefulness and format of the statement of cash flows. Prepare a statement of cash flows using the indirect method. 3 Analyze the statement

13-1 13 Statement of Cash Flows Learning Objectives 1 2 Discuss the usefulness and format of the statement of cash flows. Prepare a statement of cash flows using the indirect method. 3 Analyze the statement

Analysis of Financial Statement & Cash Flow Statements

Analysis of Financial Statement & Cash Flow Statements Q.1 ow are the various activities classified according to AS-3 (Revised) while preparing the Cash Flow Statement? While preparing the cash flow statement

Analysis of Financial Statement & Cash Flow Statements Q.1 ow are the various activities classified according to AS-3 (Revised) while preparing the Cash Flow Statement? While preparing the cash flow statement

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4)

") MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

CHAPTER 7. Cash Flow AnAlysis. of Sample Real. EstatE CompaniEs

CHAPTER 7 Cash Flow AnAlysis of Sample Real EstatE CompaniEs 226 INTRODUCTION CASH FLOW A cash flow statement is one of the most important financial statements for a project or business. A type of financial

CHAPTER 7 Cash Flow AnAlysis of Sample Real EstatE CompaniEs 226 INTRODUCTION CASH FLOW A cash flow statement is one of the most important financial statements for a project or business. A type of financial

ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA. Examiner's Report AA3 EXAMINATION - JANUARY 2016 (AA31) FINANCIAL ACCOUNTING AND REPORTING

FINANCIAL ACCOUNTING AND REPORTING") ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA Examiner's Report AA3 EXAMINATION - JANUARY 2016 (AA31) FINANCIAL ACCOUNTING AND REPORTING The following common mistakes, deficiencies were identified

ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA Examiner's Report AA3 EXAMINATION - JANUARY 2016 (AA31) FINANCIAL ACCOUNTING AND REPORTING The following common mistakes, deficiencies were identified

condition & operating results in a condensed form. Financial statements are used as a

2.1 FINANCIAL ANALYSIS Financial statements are formal records of the financial activities of a business, person or other entity and provide an overview of a business or person s financial condition in

2.1 FINANCIAL ANALYSIS Financial statements are formal records of the financial activities of a business, person or other entity and provide an overview of a business or person s financial condition in

UNIT 2 PRIMARY FINANCIAL STATEMENTS IAS 1,7,8,14,18 & IFRS5:

UNIT 2 PRIMARY FINANCIAL STATEMENTS IAS 1,7,8,14,18 & IFRS5: 1 IAS 1 PRESENTATION OF FINANCIAL STATEMENTS OVERVIEW IAS 1 Presentation of Financial Statements sets out the overall requirements for financial

UNIT 2 PRIMARY FINANCIAL STATEMENTS IAS 1,7,8,14,18 & IFRS5: 1 IAS 1 PRESENTATION OF FINANCIAL STATEMENTS OVERVIEW IAS 1 Presentation of Financial Statements sets out the overall requirements for financial

AS 1 DISCLOSURE OF ACCOUNTING POLICIES

AS 1 DISCLOSURE OF ACCOUNTING POLICIES Summary Need for disclosure of Accounting policies Fundamental Accounting Assumptions 1. Going concern 2. Consistency 3. Accrual Principles regarding the accounting

AS 1 DISCLOSURE OF ACCOUNTING POLICIES Summary Need for disclosure of Accounting policies Fundamental Accounting Assumptions 1. Going concern 2. Consistency 3. Accrual Principles regarding the accounting

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

Financial Statement Analysis. Cash Flow Statement

Financial Statement Analysis Cash Flow Statement 1 The Articulation of the Financial Statements Beginning stocks Flows Ending stocks Cash Flow Statement Beginning Balance Sheet Cash Cash from operations

Financial Statement Analysis Cash Flow Statement 1 The Articulation of the Financial Statements Beginning stocks Flows Ending stocks Cash Flow Statement Beginning Balance Sheet Cash Cash from operations

pt (Definition Report)

") 1 String usfr-gc General Concepts (usfr-gc:generalconcepts) This is a category for storing general concepts. General concepts are high-level business reporting concepts such as "assets" and "liabilities"

1 String usfr-gc General Concepts (usfr-gc:generalconcepts) This is a category for storing general concepts. General concepts are high-level business reporting concepts such as "assets" and "liabilities"

BUSINESS FINANCE. Financial Statement Analysis. 1. Introduction to Financial Analysis. Copyright 2004 by Larry C. Holland

BUSINESS FINANCE Financial Statement Analysis 1. Introduction to Financial Analysis Slide 1 Welcome to the study of business finance. The major topic in this module is Financial Statement Analysis. And

BUSINESS FINANCE Financial Statement Analysis 1. Introduction to Financial Analysis Slide 1 Welcome to the study of business finance. The major topic in this module is Financial Statement Analysis. And

Reading Understanding. Financial Statements. A Layman s Guide to Financial Reporting

Reading Understanding & Financial Statements A Layman s Guide to Financial Reporting 1 Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted,

Reading Understanding & Financial Statements A Layman s Guide to Financial Reporting 1 Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted,

MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3)

") MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following statement shows the revenues and expenses of the

MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following statement shows the revenues and expenses of the

Financial Statement Analysis-FIN621 ACCOUNTING & ACCOUNTING PRINCIPLES

ACCOUNTING & ACCOUNTING PRINCIPLES Lesson-1 Accounting Almost every organization and individual maintains accounts and deals with accounting. In simple terms, it can be described as a record of Income

ACCOUNTING & ACCOUNTING PRINCIPLES Lesson-1 Accounting Almost every organization and individual maintains accounts and deals with accounting. In simple terms, it can be described as a record of Income

BPC6C Cost and Management Accounting. Unit : I to V

BPC6C Cost and Management Accounting Unit : I to V UNIT -1 FUNDAMENTALS OF COST ACCOUNTING Nature and scope of Cost Accounting, Distinction between cost and financial accounting, Cost sheet, tenders Characteristics

BPC6C Cost and Management Accounting Unit : I to V UNIT -1 FUNDAMENTALS OF COST ACCOUNTING Nature and scope of Cost Accounting, Distinction between cost and financial accounting, Cost sheet, tenders Characteristics