to T5? dollar. T4 T1 to T2 but T4 to T5. rate needed to market model) 1 Problem

|

|

|

- Shonda Watkins

- 5 years ago

- Views:

Transcription

1.")

")

Identify a currency that")

In going from Table 1 to Table 5,")

Calculate the level of the exchange")

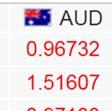

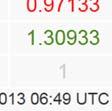

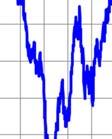

1 Problem Set 4 Determining thee exchange rate (currency market model) 1. Nominal exchange rate. Consider the following tables (T1 to T5) taken from the web site rates.com/ /. In tabless T1, T2, T3, and T4, 1 dollar cann purchase 0.74, 0.71, 0.72, and 0.76 euros, respectively; in T5, 1 dollarr can purchase 0.73 euros. In tables T1, T2,, T3, and T4, 1 euro can purchase 1.35, 1.39, 1.37, and 1.30 dollars, respectively; in T5, 1 euro can c purchase 1.35 dollars. T1 (i) Is the euro appreciating or depreciating with respect to the dollar from T1 to T2? And from T2 to T3? And from T3 to T4? And from T4 to T5? T2 (ii) Is there any currency with respect to which the t euro appre ciates from f T1 to T2, from T22 to T3, fromm T3 to T4, and from T4 to T5? T3 (iii) Identify a currency that, in passing from T11 to T2 appreciated with respect to the dollar but, in passing from T3 to T4, depreciated with respect to the dollar. T4 (iv) Identify a currency that depreciated with respect to thee euro from T1 to T2 but appreciated with respect to the t euro from T4 to T5. T5 (v) In going from Table 1 to Table 5, which currencies appreciate with respect to the euro? Which ones depreciate? 2. Appreciation. Let the dollar euroo exchange rate be e = 2 $/. (i) Calculate the level of the exchange rate that makes the dollar appreciate a 50% with respect to the euro. (ii) Compute the level off the exchange rate needed to induce a 20% appreciation of thee euro with respect to the dollar. 3. Appreciation. In Figures 1 2 (source: / hist.zip), indicate a period in which the euro appreciates (depreciate) with respect to the other displayed currency. 1 Problem set 4: Determining the exchange rate (currency market model) 7 & 28 February & 3 March 2013

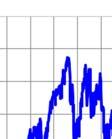

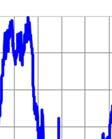

2 Fig. 1. Dollar euro exchange rate (USD/EUR), 4 January February 2013 Fig. 2. Yen euro exchange rate (JPY/EUR), 4 January February Problem set 4: Determining the exchange rate (currency market model) 7 & 28 February & 3 March 2013

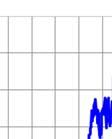

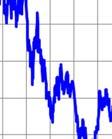

3 4. Three currencies. (i) Is it possible for the yen to depreciate with respect to the euro and, simultaneously, to appreciate with respect to the dollar? (ii) If so, would the euro appreciate or depreciate with respect to the dollar? 5. Commercial arbitrage. Reus and Tarragona are independent countries with their own currencies, the reuro and the tarragollar, respectively. The exchange rate between reuro and tarragollar is 2 reuros per tarragollar. The price of French bread is 3 reuros a piece in Reus and 1 tarragollar a piece in Tarragona. Assuming that there is no significant transportation cost, what changes would cause the commercial arbitrage of French bread in the exchange rate and the price of French bread in Reus and Tarragona? 6. Currency market. (i) Explain if the euro appreciates or depreciates with respect to the dollar if the US real GDP rises. Illustrate your explanation by means of a graphical representation of the currency market. (ii) Address the same two questions (explain and illustrate) if the European Central Bank executes an expansionary open market operation. (iii) Address the same two questions if the events in (i) and (ii) occur simultaneously. 7. Central banks. (i) Explain, and represent graphically, what kind of currency market intervention by the Federal Reserve would cause an appreciation of the euro against the dollar. (ii) Would that intervention also cause an appreciation of the euro if it were carried out by the European Central Bank? 8. Peseta dollar exchange rate. Fig. 3 shows the peseta dollar exchange rate from 1956 to The graph indicates how many pesetas could be purchased with one dollar. (i) Select an interval during which the peseta depreciated with respect to the dollar. (ii) Select any two years between which the peseta appreciated with respect to the dollar. (iii) Conjecture how the graph showing the dollar peseta exchange rate should look like , , , , , , , , ,9592 Fig. 3. Peseta dollar exchange rate, , , , Problem set 4: Determining the exchange rate (currency market model) 7 & 28 February & 3 March 2013

4 9. Currency arbitrage. Explain how triangular arbitrage alters the exchange rates 1 $/, 1 $/, and 2 /. 10. PPP. (i) Suppose a currency is overvalued according to its PPP value. What can be said about the associated real exchange rate? [Hint: is greater, smaller, or equal to 1?] (ii) Assume that P* is twice P. What is the value of the nominal exchange rate consistent with (implied by) PPP? 11. Over/undervaluation. Fill out the following table, where P is the Eurozone CPI, P* is the US CPI, e PPP is the exchange rate $/ ensuring purchasing power parity, e is the equilibrium exchange rate $/ in the currency market, and the last column is the one where it must be specified in which percentage the euro is overvalued or undervalued with respect to the dollar according to e PPP. P P* e PPP e Overvalued/undervalued (%) ½ PPP. Find the purchasing power parity exchange rate (when the euro is the home currency and indirect quotation is adopted) if the nominal exchange rate is 2 /$, the Eurozone CPI is 200, and the US CPI is 600 (assuming that both CPIs are based on the same basket of goods). 13. PPP. Reus and Tarragona are independent countries with their own currency, the reuro and the tarragollar, respectively. The exchange rate between reuro and tarragollar is 2 reuros per tarragollar. The price of a bottle of vermut de Reus is 2 reuros in Reus and 2 tarragollars in Tarragona. (i) Is the reuro overvalued or undervalued with respect to its PPP value? If so, by how much? (ii) Assuming that there is no significant transportation cost, what changes would cause the commercial arbitrage of vermut de Reus in the exchange rate and the prices of the vermut de Reus in Reus and Tarragona? 14. Currency market. (i) Identify 5 events shifting the market supply function of euros to the right. (ii) Identify 5 events shifting the market demand function for euros to the right. 15. Three currencies. (i) If the dollar euro exchange rate is 20 $/ and the yen euro exchange rate is 10 /, what should presumably be the yen dollar exchange rate? (ii) Let the dollar appreciate versus the euro and the yen depreciate versus the euro. Must the dollar appreciate or depreciate versus the yen? 16. Real exchange rate. What is to be expected to happen to the real exchange rate between the dollar and the euro if the euro depreciates with respect to the dollar and the inflation rate in the US is higher than the inflation rate in the Eurozone? 17. Currency market. Determine the effect on the equilibrium exchange rate of the following events. (1) The arrival of a significant number of immigrants from the US (2) The Federal Reserve buys government bonds (3) Both the Federal Reserve and the European Central Bank purchase government bonds (4) The Federal Reserve buys government bonds and the European Central Bank sells them (5) The reduction of the number of tourist coming from the US (6) An increase in the US GDP (7) An increase in the US GDP combined with a decrease in the Eurozone GDP (8) An increase in the Eurozone CPI (9) An increase in both the Eurozone CPI and US CPI (10) Germany leaves the Eurozone (11) The eurozone sets capital controls (restrictions to the sale and purchase of euros) 4 Problem set 4: Determining the exchange rate (currency market model) 7 & 28 February & 3 March 2013

5 18. Real exchange rate. (i) Compute the real exchange rate and the purchasing power parity exchange rate if the nominal exchange rate in the currency market is e = 1/4 /$, the US CPI is P* = 800, and the Eurozone CPI is P = 400 (specify the units of the two rates computed). (ii) If the purchasing power parity exchange rate differs from the nominal exchange rate in the currency market, explain if the euro is overvalued or undervalued with respect to the dollar and calculate the over/undervaluation percentage. 19. Big Mac Index ( mac index). [Slightly hard] Consider the table below. (i) Explain whether the Argentinean peso was overvalued or undervalued with respect to the dollar according to purchasing power parity. Specifically, explain what the numbers in each column mean and how they are obtained. (ii) Do the same for the euro. (iii) As regards Sweden, e PPP = crowns (Swedish kronor) per $ and e from the currency market is 6.35 crowns per $. The deviation of e from e PPP is 42.68%, but the table contends that the crown is overvalued a 74%. Explain the discrepancy. Country BM price in local currency Actual exchange rate (Jan 2013) Local price in $ BM price in $ PPP exchange rate 5 Problem set 4: Determining the exchange rate (currency market model) 7 & 28 February & 3 March 2013 Over/undervaluation against $ (%) Argentina 19,00 4,98 3,82 4,35 12,58 Australia 4,70 0,96 4,90 1,08 12,21 Brazil 11,25 1,99 5,64 2,58 29,22 Britain 2,69 0,63 4,25 0,62 2,73 Canada 5,41 1,00 5,39 1,24 23,51 Chile 2050,00 471,75 4,35 469,39 0,50 China 16,00 6,22 2,57 3,66 41,10 Colombia 8600, ,18 4, ,14 11,05 Denmark 28,50 5,50 5,18 6,53 18,69 Egypt 16,00 6,69 2,39 3,66 45,20 Euro area 3,59 0,74 /$ 4,88 $ 0,82 /$ 11,69 % Hong Kong 17,00 7,76 2,19 3,89 49,83 India 89,00 53,40 1,67 20,38 61,83 Indonesia 27939, ,50 2, ,18 34,51 Israel 14,90 3,72 4,00 3,41 8,40 Japan 320,00 91,07 3,51 73,27 19,54 Lithuania 7,80 2,54 3,07 1,79 29,81 Malaysia 7,95 3,08 2,58 1,82 40,96 Mexico 37,00 12,74 2,90 8,47 33,49 New Zealand 5,20 1,20 4,32 1,19 0,98 Norway 43,00 5,48 7,84 9,85 79,56 Peru 10,00 2,56 3,91 2,29 10,54 Philippines 118,00 40,60 2,91 27,02 33,45 Poland 9,10 3,09 2,94 2,08 32,61 Russia 72,88 30,05 2,43 16,69 44,46 Saudi Arabia 11,00 3,75 2,93 2,52 32,84 South Africa 18,33 9,05 2,03 4,20 53,61 South Korea 3700, ,48 3,41 847,19 21,95 Sweden 48,40 6,35 7,62 11,08 74,54 Switzerland 6,50 0,91 7,12 1,49 63,14 Thailand 87,00 29,76 2,92 19,92 33,05 Turkey 8,45 1,77 4,78 1,93 9,39 United States 4,37 1,00 4,37 1,00 0,00 Venezuela 39,00 4,29 9,08 8,93 107,93 Spain 3,50 0,74 4,75 0,80 8,75

6 Multiple choice questions 1. Arbitrage and speculation differ from each other in that (a) arbitrage only takes place in the currency market, whereas speculation only takes place in the loan market. (b) there is absolutely no difference between them. (c) the outcome of speculation is always a sure event for the speculator, while the outcome of arbitrage is always uncertain for the arbitrageur. 2. Depreciation and devaluation differ from each other in (a) absolutely nothing. (b) that depreciation is a government decision, whereas devaluation is determined by the (c) that depreciation is a reduction of the exchange rate, while devaluation is an increase of the exchange rate. 3. In which case could triangular arbitrage be carried out? (a) 1 $/ 1 $/ 1 / (b) 2 $/ 4 $/ 2 / (c) 2 $/ 2 $/ 1 / (d) 2 $/ 2 $/ 2 / 4. The open economy trilemma refers to (a) interest rates, monetary policy, and capital mobility. (b) exchange rates, monetary policy, and monetary base. (c) discount factors, open market operations, and speculation. (d) exchange rates, monetary policy, and capital mobility. 5. The denial of which sentence is not true? (a) The real interest rate may be smaller than the real exchange rate. (b) The real interest rate is always higher than the real exchange rate. (c) The real interest rate is always equal to the real exchange rate. (d) The real interest rate is always smaller than the real exchange rate. 6. Reus is an independent country with the reuro as home currency. What action by the Central Bank of Reus would not cause an appreciation of the reuro versus the euro? (a) A contractionary open market operation (b) An increase in the reserve ratio (c) The purchase of euros (paid with reuros) (d) The purchase of reuros (paid with euros) 7. What is the foreseeable effect on the exchange rate $/ of the purchase by the European Central Bank of financial assets? (a) Appreciation of the with respect to the $ (b) Depreciation of the $ with respect to the (c) There is absolutely no connection between the loan market and the currency market 8. From which value to which value the dollar depreciates with respect to the euro? (a) From 4 $/ to 2 /$ (b) From 2 $/ to 2 /$ (c) From 2 /$ to 0 5 $/ (d) From 2 /$ to 4 $/ 9. What could explain the depreciation of the euro with respect to the dollar? (a) A fall in the Eurozone prices (b) An increase in the Eurozone interest rate (c) A decrease in the US interest rate (d) A fall in the prices of the US 10. What could not explain the depreciation of the euro with respect to the dollar? (a) A fall in the Eurozone prices (b) An increase in the Eurozone interest rate (c) A decrease in the US interest rate 11. The Federal Reserve has decided to intervene in the currency market to make the dollar appreciate with respect to the euro. Which measure is appropriate to reach that goal? (a) According to the impossible trinity, no such measure exists. (b) The Federal Reserve buys euros in the (c) The Federal Reserve buys dollars in the (d) The Federal Reserve sells dollars in the 6 Problem set 4: Determining the exchange rate (currency market model) 7 & 28 February & 3 March 2013

7 12. Let the real exchange rate be expressed as foreign baskets/domestic basket. How does an increase in the foreign CPI affect the real exchange rate, with the rest of variables determining the real exchange rate held fixed? (a) Causes a rise in the real exchange rate (b) Causes a reduction in the real exchange rate (c) Does not affect the real exchange rate 13. If P = 100, P* = 50, and e = 1 $/, then, according to PPP, the euro is (a) overvalued. (b) undervalued. (c) at parity level. 14. Using proper technical terms, the euro appreciates against the dollar if (a) the US government time ago set a fixed exchange rate at 2 /$ and now changes that fixed rate to 2 $/. (b) there is a floating exchange rate regime between the two currencies and the equilibrium exchange rate in the currency market goes from 2 /$ to 2 $/. (c) there is a floating exchange rate regime between the two currencies and the equilibrium exchange rate in the currency market goes from 2 $/ to 2 /$. (d) the US government time ago set a fixed exchange rate at 2 $/ and now changes that fixed rate to 2 /$. 15. The euro is likely to depreciate against the dollar in the currency market if (a) the US real GDP increases. (b) the US nominal interest rate falls. (c) the Eurozone inflation rate goes up. 16. Which sentence is not true? (a) Triangular arbitrage is not possible when exchange rates are 0.5 $/, 3 $/, and 6 /. (b) There is a tendency for the euro to appreciate against the dollar if the interest rate in the Eurozone goes up. (c) If the real exchange rate differs from 1, then the nominal exchange is not at its purchasing power parity level. (d) Revaluation in a fixed exchange regime is equivalent to depreciation in a floating exchange regime. 17. The competitiveness of the eurozone improves when, other things being equal, (a) the euro depreciates with respect to the dollar. (b) the eurozone CPI rises. (c) the US CPI falls. 18. The nominal exchange rate is 2 $/, the eurozone CPI is 200, and the US CPI is 100. In this case, the euro is (a) overvalued with respect to its purchasing power parity value. (b) undervalued with respect to its purchasing power parity value. (c) at its purchasing power parity level. 19. The impossible trinity (a) says that triangular arbitrage causes currency crises. (b) relates the competitiveness of an economy to the purchasing power parity exchange rate. (c) says that spatial arbitrage causes the real appreciation of the exchange rate. (d) implies that a country with an independent monetary policy and no capital control cannot adopt a fixed exchange regime. 20. What is not false about triangular arbitrage? (a) It can occur under exchange rates 2 $/, 2 $/, and 1 /. (b) It is a way of unfolding a speculative attack. (c) It can occur under exchange rates 1 $/, 2 $/, and 1 /. (d) It is made impossible by the impossible trinity. 21. The European Central Bank executes a contractionary monetary policy. As a result, it is likely that, in the currency market, (a) the euro will appreciate against the dollar. (b) the dollar will appreciate against the euro. (c) the supply of euros will shift to the right. 22. According to the impossible trinity, it is not possible to simultaneously have (a) a fixed exchange rate, a sovereign monetary policy, and free capital flows. (b) high unemployment, low inflation, and a revaluation. (c) a currency crisis, spatial arbitrage, and a speculative attack. (d) commercial arbitrage, an undervalued currency, and Okun s law. 7 Problem set 4: Determining the exchange rate (currency market model) 7 & 28 February & 3 March 2013

8 23. What cannot explain a depreciation of the euro against the dollar? (a) A raise in the US interest rate. (b) A raise in the eurozone inflation rate. (c) A fall in the eurozone GDP. 24. The competitiveness of an economy improves when (a) the Eurocoin rises. (b) its central bank buys the domestic currency in the (c) the real exchange rate falls (a real depreciation occurs). 25. In which case does the dollar appreciate against the euro? (a) In passing from 2 $/ to 4 $/ (b) In passing from 2 $/ to 2 /$ (c) In passing from 2 $/ to ½ /$ 26. Letting the real exchange rate represent a measure of the competitiveness of an economy, the eurozone becomes less competitive if (a) the eurozone general price level falls. (b) the US general price level raises. (c) the dollar appreciates against the euro. 27. In passing from 2 $/ to 2 /$, (a) the euro appreciates with respect to the dollar. (b) the dollar appreciates with respect to the euro. (c) the dollar depreciates with respect to the euro. 28. The euro has depreciated against the dollar. A possible explanation is (a) that the US interest rate went down. (b) that the eurozone inflation rate went up. (c) that the US real GDP has grown. 29. The ECB adopts a fixed exchange rate regime in which the value of the euro is held fixed against the dollar. When a shift to the right in the supply of euros function moves the exchange rate away from its fixed rate, the ECB (a) should necessarily increase its demand for dollars. (b) will sell dollars thereby increasing its dollar reserves. (c) will sell dollars thereby diminishing its dollar reserves. (d) will never carry out any action in the 30. Under a floating exchange rate regime (a) an increase in the value of the home currency against foreign currencies is called appreciation. (b) the government buys the home currency to sustain the exchange rate. (c) an increase in the value of the home currency against foreign currencies is called devaluation. (d) an increase in the value of the home currency against foreign currencies is called revaluation. 31. The US CPI is P* = 800. The eurozone CPI is P = 400. Then the purchasing power parity exchange rate is (a) 2 /$. (b) 1 /$. (c) ½ /$. (d) 1 $/. 8 Problem set 4: Determining the exchange rate (currency market model) 7 & 28 February & 3 March 2013

Problem Set 4 The currency market

Problem Set 4 The currency market 1. Consider the following tables taken from the web site http://www.x-rates.com/. To interpret the data, the exchange rates on February 2, 2011, mean that 1 dollar can

Problem Set 4 The currency market 1. Consider the following tables taken from the web site http://www.x-rates.com/. To interpret the data, the exchange rates on February 2, 2011, mean that 1 dollar can

Introduction to Macroeconomics M Problem set 4

T1 T2 Introduction to Macroeconomics M5 2015-16 Problem set 4 dollar appreciate from T1 to T2? 1. Nominal rate. Consider tables T1 and T2, taken from http://www.x-rates.com/. In T1, for instance, 1 can

T1 T2 Introduction to Macroeconomics M5 2015-16 Problem set 4 dollar appreciate from T1 to T2? 1. Nominal rate. Consider tables T1 and T2, taken from http://www.x-rates.com/. In T1, for instance, 1 can

Introduction to Macroeconomics M

Introduction to Macroeconomics M5 2015-16 Problem Set 4 Multiple choice questions 1. Arbitrage and speculation differ from each other (a) in that arbitrage only takes place in the currency market, whereas

Introduction to Macroeconomics M5 2015-16 Problem Set 4 Multiple choice questions 1. Arbitrage and speculation differ from each other (a) in that arbitrage only takes place in the currency market, whereas

Quoting an exchange rate. The exchange rate. Examples of appreciation. Currency appreciation. Currency depreciation. Examples of depreciation

The exchange rate The nominal exchange rate (or, for short, exchange rate) between two currencies is the price of one currency in terms of the other. It allows domestic purchasing power to be spent abroad.

The exchange rate The nominal exchange rate (or, for short, exchange rate) between two currencies is the price of one currency in terms of the other. It allows domestic purchasing power to be spent abroad.

Governments and Exchange Rates

Governments and Exchange Rates Exchange Rate Behavior Existing spot exchange rate covered interest arbitrage locational arbitrage triangular arbitrage Existing spot exchange rates at other locations Existing

Governments and Exchange Rates Exchange Rate Behavior Existing spot exchange rate covered interest arbitrage locational arbitrage triangular arbitrage Existing spot exchange rates at other locations Existing

Nominal exchange rate

Nominal exchange rate The nominal exchange rate between two currencies is the price of one currency in terms of the other. The nominal exchange rate (or, for short, exchange rate) will be denoted by the

Nominal exchange rate The nominal exchange rate between two currencies is the price of one currency in terms of the other. The nominal exchange rate (or, for short, exchange rate) will be denoted by the

Fiscal Policy and the Global Crisis

Fiscal Policy and the Global Crisis Presentation at Koҫ University, Istanbul Carlo Cottarelli Director IMF Fiscal Affairs Department June 9, 2009 1 Two fiscal questions What is the appropriate fiscal policy

Fiscal Policy and the Global Crisis Presentation at Koҫ University, Istanbul Carlo Cottarelli Director IMF Fiscal Affairs Department June 9, 2009 1 Two fiscal questions What is the appropriate fiscal policy

Reporting practices for domestic and total debt securities

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

GLOBAL MARKET OUTLOOK

GLOBAL MARKET OUTLOOK Max Darnell, Managing Partner, Chief Investment Officer All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. performance is no

GLOBAL MARKET OUTLOOK Max Darnell, Managing Partner, Chief Investment Officer All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. performance is no

Introduction to Exchange Rates and the Foreign Exchange Market

Introduction to Exchange Rates and the Foreign Exchange Market 2 1. Refer to the exchange rates given in the following table. Today One Year Ago June 25, 2010 June 25, 2009 Country Per $ Per Per Per $

Introduction to Exchange Rates and the Foreign Exchange Market 2 1. Refer to the exchange rates given in the following table. Today One Year Ago June 25, 2010 June 25, 2009 Country Per $ Per Per Per $

Introduction to macroeconomics 23 May 2017 M4

Introduction to macroeconomics 23 May 2017 M4 1. Simpson s paradox (a) says that the Laffer curve is a particular case of Okun s law. (b) holds that the fallacy of composition becomes the post hoc ergo

Introduction to macroeconomics 23 May 2017 M4 1. Simpson s paradox (a) says that the Laffer curve is a particular case of Okun s law. (b) holds that the fallacy of composition becomes the post hoc ergo

EQUITY REPORTING & WITHHOLDING. Updated May 2016

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

Quarterly Investment Update First Quarter 2017

Quarterly Investment Update First Quarter 2017 Market Update: A Quarter in Review March 31, 2017 CANADIAN STOCKS INTERNATIONAL STOCKS Large Cap Small Cap Growth Value Large Cap Small Cap Growth Value Emerging

Quarterly Investment Update First Quarter 2017 Market Update: A Quarter in Review March 31, 2017 CANADIAN STOCKS INTERNATIONAL STOCKS Large Cap Small Cap Growth Value Large Cap Small Cap Growth Value Emerging

US Economic Indicators: Import Prices, PPI, & CPI

US Economic Indicators: Import Prices, PPI, & CPI December 1, 17 Dr. Edward Yardeni 51-97-73 eyardeni@ Debbie Johnson --1333 djohnson@ Please visit our sites at blog. thinking outside the box Table Of

US Economic Indicators: Import Prices, PPI, & CPI December 1, 17 Dr. Edward Yardeni 51-97-73 eyardeni@ Debbie Johnson --1333 djohnson@ Please visit our sites at blog. thinking outside the box Table Of

Actuarial Supply & Demand. By i.e. muhanna. i.e. muhanna Page 1 of

By i.e. muhanna i.e. muhanna Page 1 of 8 040506 Additional Perspectives Measuring actuarial supply and demand in terms of GDP is indeed a valid basis for setting the actuarial density of a country and

By i.e. muhanna i.e. muhanna Page 1 of 8 040506 Additional Perspectives Measuring actuarial supply and demand in terms of GDP is indeed a valid basis for setting the actuarial density of a country and

San Francisco Retiree Health Care Trust Fund Education Materials on Public Equity

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

Market Briefing: US MSCI Stock Price Index vs Rest of the World

Market Briefing: US MSCI Stock Price Index vs Rest of the World January 29, 1 Dr. Edward Yardeni 51-972-73 eyardeni@ Joe Abbott 732-97-530 jabbott@ Mali Quintana 0--1333 aquintana@ Please visit our sites

Market Briefing: US MSCI Stock Price Index vs Rest of the World January 29, 1 Dr. Edward Yardeni 51-972-73 eyardeni@ Joe Abbott 732-97-530 jabbott@ Mali Quintana 0--1333 aquintana@ Please visit our sites

DIVERSIFICATION. Diversification

Diversification Helps you capture what global markets offer Reduces risks that have no expected return May prevent you from missing opportunity Smooths out some of the bumps Helps take the guesswork out

Diversification Helps you capture what global markets offer Reduces risks that have no expected return May prevent you from missing opportunity Smooths out some of the bumps Helps take the guesswork out

Session 16. Review Session

Session 16. Review Session The long run [Fundamentals] Output, saving, and investment Money and inflation Economic growth Labor markets The short run [Business cycles] What are the causes business cycles?

Session 16. Review Session The long run [Fundamentals] Output, saving, and investment Money and inflation Economic growth Labor markets The short run [Business cycles] What are the causes business cycles?

DFA Global Equity Portfolio (Class F) Quarterly Performance Report Q2 2014

Quarterly Performance Report Q2 2014") DFA Global Equity Portfolio (Class F) Quarterly Performance Report Q2 2014 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds.

DFA Global Equity Portfolio (Class F) Quarterly Performance Report Q2 2014 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds.

A short history of debt

A short history of debt In the words of the late Charles Kindleberger, debt/financial crises are a hardy perennial we have been here many times before. Over the past decade and a half the ratio of global

A short history of debt In the words of the late Charles Kindleberger, debt/financial crises are a hardy perennial we have been here many times before. Over the past decade and a half the ratio of global

Financial wealth of private households worldwide

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Quarterly Investment Update First Quarter 2018

Quarterly Investment Update First Quarter 2018 Dimensional Fund Advisors Canada ULC ( DFA Canada ) is not affiliated with [insert name of Advisor]. DFA Canada is a separate and distinct company. Market

Quarterly Investment Update First Quarter 2018 Dimensional Fund Advisors Canada ULC ( DFA Canada ) is not affiliated with [insert name of Advisor]. DFA Canada is a separate and distinct company. Market

DFA Global Equity Portfolio (Class F) Performance Report Q3 2018

Performance Report Q3 2018") DFA Global Equity Portfolio (Class F) Performance Report Q3 2018 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q3 2018 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q4 2017

Performance Report Q4 2017") DFA Global Equity Portfolio (Class F) Performance Report Q4 2017 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q4 2017 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q2 2017

Performance Report Q2 2017") DFA Global Equity Portfolio (Class F) Performance Report Q2 2017 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q2 2017 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q3 2015

Performance Report Q3 2015") DFA Global Equity Portfolio (Class F) Performance Report Q3 2015 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DFA Global Equity Portfolio (Class F) Performance Report Q3 2015 This presentation has been prepared by Dimensional Fund Advisors Canada ULC ( DFA Canada ), manager of the Dimensional Funds. This presentation

DOMESTIC CUSTODY & TRADING SERVICES

Pricing Structure DOMESTIC CUSTODY & TRADING SERVICES A flat custody fee of 20bps per account type per year is applicable to all holdings and cash, the custody fee is collected each month but will be capped

Pricing Structure DOMESTIC CUSTODY & TRADING SERVICES A flat custody fee of 20bps per account type per year is applicable to all holdings and cash, the custody fee is collected each month but will be capped

Market Briefing: Currencies

Market Briefing: Currencies December 6, 217 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box Table Of Contents

Market Briefing: Currencies December 6, 217 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box Table Of Contents

Progress towards Strong, Sustainable and Balanced Growth. Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction)

") Progress towards Strong, Sustainable and Balanced Growth Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction) Source: OECD May 2014 Forecast, Haver Analytics, Rogoff and

Progress towards Strong, Sustainable and Balanced Growth Figure 1: Recovery from Financial Crisis (100 = First Quarter of Real GDP Contraction) Source: OECD May 2014 Forecast, Haver Analytics, Rogoff and

Corporate Governance and Investment Performance: An International Comparison. B. Burçin Yurtoglu University of Vienna Department of Economics

Corporate Governance and Investment Performance: An International Comparison B. Burçin Yurtoglu University of Vienna Department of Economics 1 Joint Research with Klaus Gugler and Dennis Mueller http://homepage.univie.ac.at/besim.yurtoglu/unece/unece.htm

Corporate Governance and Investment Performance: An International Comparison B. Burçin Yurtoglu University of Vienna Department of Economics 1 Joint Research with Klaus Gugler and Dennis Mueller http://homepage.univie.ac.at/besim.yurtoglu/unece/unece.htm

Guide to Treatment of Withholding Tax Rates. January 2018

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Internet Appendix: Government Debt and Corporate Leverage: International Evidence

Internet Appendix: Government Debt and Corporate Leverage: International Evidence Irem Demirci, Jennifer Huang, and Clemens Sialm September 3, 2018 1 Table A1: Variable Definitions This table details the

Internet Appendix: Government Debt and Corporate Leverage: International Evidence Irem Demirci, Jennifer Huang, and Clemens Sialm September 3, 2018 1 Table A1: Variable Definitions This table details the

Final exam Non-detailed correction 3 hours

International Finance Master PEI Spring 2013 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours Documents not allowed. Basic calculator allowed. For the Multiple Choice Questions, use the answer

International Finance Master PEI Spring 2013 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours Documents not allowed. Basic calculator allowed. For the Multiple Choice Questions, use the answer

Investment Newsletter

INVESTMENT NEWSLETTER September 2016 Investment Newsletter September 2016 CLIENT INVESTMENT UPDATE NEWSLETTER Relative Price and Expected Stock Returns in International Markets A recent paper by O Reilly

INVESTMENT NEWSLETTER September 2016 Investment Newsletter September 2016 CLIENT INVESTMENT UPDATE NEWSLETTER Relative Price and Expected Stock Returns in International Markets A recent paper by O Reilly

COUNTRY COST INDEX JUNE 2013

COUNTRY COST INDEX JUNE 2013 June 2013 Kissell Research Group, LLC 1010 Northern Blvd., Suite 208 Great Neck, NY 11021 www.kissellresearch.com Kissell Research Group Country Cost Index - June 2013 2 Executive

COUNTRY COST INDEX JUNE 2013 June 2013 Kissell Research Group, LLC 1010 Northern Blvd., Suite 208 Great Neck, NY 11021 www.kissellresearch.com Kissell Research Group Country Cost Index - June 2013 2 Executive

Global Business Economics. Mark Crosby SEMBA International Economics

Global Business Economics Mark Crosby SEMBA International Economics The balance of payments and exchange rates Understand the structure of a country s balance of payments. Understand the difference between

Global Business Economics Mark Crosby SEMBA International Economics The balance of payments and exchange rates Understand the structure of a country s balance of payments. Understand the difference between

Public Pension Spending Trends and Outlook in Emerging Europe. Benedict Clements Fiscal Affairs Department International Monetary Fund March 2013

Public Pension Spending Trends and Outlook in Emerging Europe Benedict Clements Fiscal Affairs Department International Monetary Fund March 13 Plan of Presentation I. Trends and drivers of public pension

Public Pension Spending Trends and Outlook in Emerging Europe Benedict Clements Fiscal Affairs Department International Monetary Fund March 13 Plan of Presentation I. Trends and drivers of public pension

Exchange Rates in the Long Run

Exchange Rates in the Long Run What determines exchange rates? Supply + Demand!» Flow models: Demand & supply of FX to purchase goods and services» Stock models, or asset models Demand & supply of available

Exchange Rates in the Long Run What determines exchange rates? Supply + Demand!» Flow models: Demand & supply of FX to purchase goods and services» Stock models, or asset models Demand & supply of available

Market Briefing: News Events & Key Markets

Market Briefing: News Events & Key Markets August 5, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at

Market Briefing: News Events & Key Markets August 5, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at

Global Economic Indictors: CRB Raw Industrials & Global Economy

Global Economic Indictors: & Global Economy December 14, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box

Global Economic Indictors: & Global Economy December 14, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box

PREDICTING VEHICLE SALES FROM GDP

UMTRI--6 FEBRUARY PREDICTING VEHICLE SALES FROM GDP IN 8 COUNTRIES: - MICHAEL SIVAK PREDICTING VEHICLE SALES FROM GDP IN 8 COUNTRIES: - Michael Sivak The University of Michigan Transportation Research

UMTRI--6 FEBRUARY PREDICTING VEHICLE SALES FROM GDP IN 8 COUNTRIES: - MICHAEL SIVAK PREDICTING VEHICLE SALES FROM GDP IN 8 COUNTRIES: - Michael Sivak The University of Michigan Transportation Research

Market liquidity and emerging market local currency sovereign bonds

Market liquidity and emerging market local currency sovereign bonds Hyun Song Shin* Bank for International Settlements NBB-ECB conference on Managing financial crises: the state of play Brussels, 6 November

Market liquidity and emerging market local currency sovereign bonds Hyun Song Shin* Bank for International Settlements NBB-ECB conference on Managing financial crises: the state of play Brussels, 6 November

World Consumer Income and Expenditure Patterns

World Consumer Income and Expenditure Patterns 2011 www.euromonitor.com iii Summary of Contents Contents Summary of Contents Section 1 Introduction 1 Section 2 Socio-economic parameters 21 Section 3 Annual

World Consumer Income and Expenditure Patterns 2011 www.euromonitor.com iii Summary of Contents Contents Summary of Contents Section 1 Introduction 1 Section 2 Socio-economic parameters 21 Section 3 Annual

Market Correlations: CRB Raw Industrials Spot Price Index

Market Correlations: Spot Price Index December 15, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at www.

Market Correlations: Spot Price Index December 15, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at www.

The Bank of America Merrill Lynch Global Bond Index Rules. PIMCO Global Advantage Government Bond Index Fine Specifications

PIMCO Global Advantage Government Bond Index Fine Specifications July 2017 1 Index Overview The PIMCO Global Advantage Government Bond Index history starts on December 31, 2003. The index has a level of

PIMCO Global Advantage Government Bond Index Fine Specifications July 2017 1 Index Overview The PIMCO Global Advantage Government Bond Index history starts on December 31, 2003. The index has a level of

Market Correlations: Expected Inflation in TIPS

Market Correlations: in TIPS April, 8 Dr. Edward Yardeni 56-97-768 eyardeni@ Joe Abbott 7-497-56 jabbott@ Mali Quintana 48-664- aquintana@ Please visit our sites at www. blog. thinking outside the box

Market Correlations: in TIPS April, 8 Dr. Edward Yardeni 56-97-768 eyardeni@ Joe Abbott 7-497-56 jabbott@ Mali Quintana 48-664- aquintana@ Please visit our sites at www. blog. thinking outside the box

Chart Collection for Morning Briefing

Chart Collection for Morning Briefing February 7, 1 Dr. Edward Yardeni 1-97-73 eyardeni@ Mali Quintana --1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 3 3 Figure 1. S&P

Chart Collection for Morning Briefing February 7, 1 Dr. Edward Yardeni 1-97-73 eyardeni@ Mali Quintana --1333 aquintana@ Please visit our sites at www. blog. thinking outside the box 3 3 Figure 1. S&P

STOXX EMERGING MARKETS INDICES. UNDERSTANDA RULES-BA EMERGING MARK TRANSPARENT SIMPLE

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

Summary 715 SUMMARY. Minimum Legal Fee Schedule. Loser Pays Statute. Prohibition Against Legal Advertising / Soliciting of Pro bono

Summary Country Fee Aid Angola No No No Argentina No, with No No No Armenia, with No No No No, however the foreign Attorneys need to be registered at the Chamber of Advocates to be able to practice attorney

Summary Country Fee Aid Angola No No No Argentina No, with No No No Armenia, with No No No No, however the foreign Attorneys need to be registered at the Chamber of Advocates to be able to practice attorney

Market Correlation: Emerging Markets MSCI

Market Correlation: MSCI March 2, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-536 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside

Market Correlation: MSCI March 2, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Joe Abbott 732-497-536 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside

A Stable International Monetary System Emerges: Inflation Targeting as Bretton Woods, Reversed

A Stable International Monetary System Emerges: Inflation Targeting as Bretton Woods, Reversed Andrew K. Rose UC Berkeley, CEPR and NBER September, 2007 Motivation Many Currency Crises through end of 20

A Stable International Monetary System Emerges: Inflation Targeting as Bretton Woods, Reversed Andrew K. Rose UC Berkeley, CEPR and NBER September, 2007 Motivation Many Currency Crises through end of 20

IMPORTANT TAX INFORMATION

00126803 IMPORTANT TAX INFORMATION Dear Hartford Funds Shareholder: The following information about your enclosed 1099-DIV from Hartford Funds should be used when preparing your 2014 tax return. The information

00126803 IMPORTANT TAX INFORMATION Dear Hartford Funds Shareholder: The following information about your enclosed 1099-DIV from Hartford Funds should be used when preparing your 2014 tax return. The information

KPMG s Individual Income Tax and Social Security Rate Survey 2009 TAX

KPMG s Individual Income Tax and Social Security Rate Survey 2009 TAX B KPMG s Individual Income Tax and Social Security Rate Survey 2009 KPMG s Individual Income Tax and Social Security Rate Survey 2009

KPMG s Individual Income Tax and Social Security Rate Survey 2009 TAX B KPMG s Individual Income Tax and Social Security Rate Survey 2009 KPMG s Individual Income Tax and Social Security Rate Survey 2009

Chapter 17. Exchange Rates and International Economic Policy

Chapter 17 Exchange Rates and International Economic Policy Preview To examine the financial market that determines exchange rates in the long and short runs To understand the role of exchange rates in

Chapter 17 Exchange Rates and International Economic Policy Preview To examine the financial market that determines exchange rates in the long and short runs To understand the role of exchange rates in

2013 Global Survey of Accounting Assumptions. for Defined Benefit Plans. Executive Summary

2013 Global Survey of Accounting Assumptions for Defined Benefit Plans Executive Summary Executive Summary In broad terms, accounting standards aim to enable employers to approximate the cost of an employee

2013 Global Survey of Accounting Assumptions for Defined Benefit Plans Executive Summary Executive Summary In broad terms, accounting standards aim to enable employers to approximate the cost of an employee

EconS 327 Review for Test 2

Test 2 is on Friday, April 24 Test 2 has 30 multiple choice questions. Test 2 will cover the material assigned during weeks 1-14. This includes o Material covered on Test 1 o Material from weeks 8-14 o

Test 2 is on Friday, April 24 Test 2 has 30 multiple choice questions. Test 2 will cover the material assigned during weeks 1-14. This includes o Material covered on Test 1 o Material from weeks 8-14 o

All-Country Equity Allocator February 2018

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Charles Waters cwaters@dcmadvisors.com 917-386-6264 All-Country Equity Allocator February

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Charles Waters cwaters@dcmadvisors.com 917-386-6264 All-Country Equity Allocator February

EconS 327 Test 2 Spring 2010

1. Credit (+) items in the balance of payments correspond to anything that: a. Involves payments to foreigners b. Decreases the domestic money supply c. Involves receipts from foreigners d. Reduces international

1. Credit (+) items in the balance of payments correspond to anything that: a. Involves payments to foreigners b. Decreases the domestic money supply c. Involves receipts from foreigners d. Reduces international

Market Correlations: S&P 500

Market Correlations: S&P 500 September 25, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at www. blog.

Market Correlations: S&P 500 September 25, 2017 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at www. blog.

Chart Collection for Morning Briefing

Chart Collection for Morning Briefing February 12, 219 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at blog. thinking outside the box 25 Figure

Chart Collection for Morning Briefing February 12, 219 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at blog. thinking outside the box 25 Figure

Chapter 2 Foreign Exchange Parity Relations

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

Corrigendum. OECD Pensions Outlook 2012 DOI: ISBN (print) ISBN (PDF) OECD 2012

ISBN (PDF) OECD 2012") OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

The Mundell-Fleming model

The Mundell-Fleming model 2013 General short run macroeconomic equilibrium Income influences demand for money Goods Market Money Market Interest rates affect aggregate demand in the open the economy Income

The Mundell-Fleming model 2013 General short run macroeconomic equilibrium Income influences demand for money Goods Market Money Market Interest rates affect aggregate demand in the open the economy Income

New in 2013: Greater emphasis on capital flows Refinements to EBA methodology Individual country assessments

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

Does One Law Fit All? Cross-Country Evidence on Okun s Law

Does One Law Fit All? Cross-Country Evidence on Okun s Law Laurence Ball Johns Hopkins University Global Labor Markets Workshop Paris, September 1-2, 2016 1 What the paper does and why Provides estimates

Does One Law Fit All? Cross-Country Evidence on Okun s Law Laurence Ball Johns Hopkins University Global Labor Markets Workshop Paris, September 1-2, 2016 1 What the paper does and why Provides estimates

foreign, and hence it is where the prices of many currencies are set. The price of foreign money is

Chapter 2: The BOP and the Foreign Exchange Market The foreign exchange market is the market where domestic money can be exchanged for foreign, and hence it is where the prices of many currencies are set.

Chapter 2: The BOP and the Foreign Exchange Market The foreign exchange market is the market where domestic money can be exchanged for foreign, and hence it is where the prices of many currencies are set.

All-Country Equity Allocator July 2018

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Allison Hay ahay@dcmadvisors.com 917-386-6264 All-Country Equity Allocator July 2018 A

Leila Heckman, Ph.D. lheckman@dcmadvisors.com 917-386-6261 John Mullin, Ph.D. jmullin@dcmadvisors.com 917-386-6262 Allison Hay ahay@dcmadvisors.com 917-386-6264 All-Country Equity Allocator July 2018 A

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile. 4-6 October 2017

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile 4-6 October 2017 Graham Robinson Global Construction Perspectives Global Construction 2030 is the fourth in a series of global studies of the construction

Global Construction 2030 Expo EDIFICA 2017 Santiago Chile 4-6 October 2017 Graham Robinson Global Construction Perspectives Global Construction 2030 is the fourth in a series of global studies of the construction

Figure: EUR-USD Exchange Rate

Figure: EUR-USD Exchange Rate SuSe 2013 1 Monetary Policy and EMU: Open Economy Setting Figure: EUR-USD Exchange Rate SuSe 2013 2 Monetary Policy and EMU: Open Economy Setting Figure: Indirect Quotation

Figure: EUR-USD Exchange Rate SuSe 2013 1 Monetary Policy and EMU: Open Economy Setting Figure: EUR-USD Exchange Rate SuSe 2013 2 Monetary Policy and EMU: Open Economy Setting Figure: Indirect Quotation

Total Imports by Volume (Gallons per Country)

") 3/7/2018 Imports by Volume (Gallons per Country) YTD YTD Country 01/2017 01/2018 % Change 2017 2018 % Change MEXICO 54,235,419 58,937,856 8.7 % 54,235,419 58,937,856 8.7 % NETHERLANDS 12,265,935 10,356,183

3/7/2018 Imports by Volume (Gallons per Country) YTD YTD Country 01/2017 01/2018 % Change 2017 2018 % Change MEXICO 54,235,419 58,937,856 8.7 % 54,235,419 58,937,856 8.7 % NETHERLANDS 12,265,935 10,356,183

Challenges for financial institutions today. Summary

7 February 6 Challenges for financial institutions today Notes for remarks by Malcolm D Knight, General Manager of the BIS, at a European Financial Services Roundtable meeting, Zurich, 7 February 6 Summary

7 February 6 Challenges for financial institutions today Notes for remarks by Malcolm D Knight, General Manager of the BIS, at a European Financial Services Roundtable meeting, Zurich, 7 February 6 Summary

Burgernomics and Purchasing Power Parity

1 Burgernomics and Purchasing Power Parity (Submitted to Economics Review published by Peoples Bank of Sri Lanka January 2015) Ms. H.M.S. Amanda Herath Lecturer, Department of Business Economics, Faculty

1 Burgernomics and Purchasing Power Parity (Submitted to Economics Review published by Peoples Bank of Sri Lanka January 2015) Ms. H.M.S. Amanda Herath Lecturer, Department of Business Economics, Faculty

Challenges faced by Advanced Inflation Targeters: The Case of Israel

Challenges faced by Advanced Inflation Targeters: The Case of Israel Karnit Flug Bank of Israel Prepared for a Conference at the Czech National Bank, April 8 28 Economic Performance of the Israeli Economy

Challenges faced by Advanced Inflation Targeters: The Case of Israel Karnit Flug Bank of Israel Prepared for a Conference at the Czech National Bank, April 8 28 Economic Performance of the Israeli Economy

This paper updates the weights for effective exchange rate calculations, using. New Rates from New Weights

IMF Staff Papers Vol. 53, No. 2 2006 International Monetary Fund New Rates from New Weights TAMIM BAYOUMI, JAEWOO LEE, AND SARMA JAYANTHI* This paper describes the result and the methodology of updating

IMF Staff Papers Vol. 53, No. 2 2006 International Monetary Fund New Rates from New Weights TAMIM BAYOUMI, JAEWOO LEE, AND SARMA JAYANTHI* This paper describes the result and the methodology of updating

Global Consumer Confidence

Global Consumer Confidence The Conference Board Global Consumer Confidence Survey is conducted in collaboration with Nielsen 4TH QUARTER 2017 RESULTS CONTENTS Global Highlights Asia-Pacific Africa and

Global Consumer Confidence The Conference Board Global Consumer Confidence Survey is conducted in collaboration with Nielsen 4TH QUARTER 2017 RESULTS CONTENTS Global Highlights Asia-Pacific Africa and

FOREIGN ACTIVITY REPORT

FOREIGN ACTIVITY REPORT SECOND QUARTER 2012 TABLE OF CONTENTS Table of Contents... i All Securities Transactions... 2 Highlights... 2 U.S. Transactions in Foreign Securities... 2 Foreign Transactions in

FOREIGN ACTIVITY REPORT SECOND QUARTER 2012 TABLE OF CONTENTS Table of Contents... i All Securities Transactions... 2 Highlights... 2 U.S. Transactions in Foreign Securities... 2 Foreign Transactions in

Market Correlations: Brent Crude Oil

Market Correlations: Brent Crude Oil March 6, 2018 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at blog.

Market Correlations: Brent Crude Oil March 6, 2018 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 480-664-1333 djohnson@ Mali Quintana 480-664-1333 aquintana@ Please visit our sites at blog.

Travel Insurance and Assistance

Travel Insurance and Assistance Worldwide research covering over 40 countries Series Prospectus Finaccord 1 Prospectus contents Page What is the research? Which countries are covered What methodology has

Travel Insurance and Assistance Worldwide research covering over 40 countries Series Prospectus Finaccord 1 Prospectus contents Page What is the research? Which countries are covered What methodology has

Rutgers University Spring Econ 336 International Balance of Payments Professor Roberto Chang. Problem Set 2. Deadline: March 1st.

Rutgers University Spring 2012 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 2. Deadline: March 1st Name: 1. The law of one price works under some assumptions. Which of

Rutgers University Spring 2012 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 2. Deadline: March 1st Name: 1. The law of one price works under some assumptions. Which of

Travel Insurance and Assistance

Travel Insurance and Assistance Worldwide research covering over 40 countries Series Prospectus Finaccord Web: www.finaccord.com. E-mail: info@finaccord.com 1 Prospectus contents Page What is the research?

Travel Insurance and Assistance Worldwide research covering over 40 countries Series Prospectus Finaccord Web: www.finaccord.com. E-mail: info@finaccord.com 1 Prospectus contents Page What is the research?

Total Imports by Volume (Gallons per Country)

") 5/4/2016 Imports by Volume (Gallons per Country) YTD YTD Country 03/2015 03/2016 % Change 2015 2016 % Change MEXICO 53,821,885 60,813,992 13.0 % 143,313,133 167,568,280 16.9 % NETHERLANDS 11,031,990 12,362,256

5/4/2016 Imports by Volume (Gallons per Country) YTD YTD Country 03/2015 03/2016 % Change 2015 2016 % Change MEXICO 53,821,885 60,813,992 13.0 % 143,313,133 167,568,280 16.9 % NETHERLANDS 11,031,990 12,362,256

Market Briefing: Gold

Market Briefing: Gold January 3, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box Table Of Contents Table

Market Briefing: Gold January 3, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog. thinking outside the box Table Of Contents Table

International Travel & Tourism Study (Published March 2005)

") International Travel & Tourism Study (Published March 2005) Roy Morgan International conducts surveys in the US,, Australia, New Zealand and Indonesia on a continuous basis. Respondents are asked about

International Travel & Tourism Study (Published March 2005) Roy Morgan International conducts surveys in the US,, Australia, New Zealand and Indonesia on a continuous basis. Respondents are asked about

(Re)Inventing Israeli Capital Markets: Infrastructure for Growth

Inventing Israeli Capital Markets: Infrastructure for Growth") (Re)Inventing Israeli Capital Markets: Infrastructure for Growth Globes Israel Business Conference December 8, 2014 From Scarcity to Innovation Paradox of Israeli Competitive Advantage From Vegetarian

(Re)Inventing Israeli Capital Markets: Infrastructure for Growth Globes Israel Business Conference December 8, 2014 From Scarcity to Innovation Paradox of Israeli Competitive Advantage From Vegetarian

Market Briefing: Global Markets

Market Briefing: Global Markets July 6, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at blog. thinking outside the box Table Of Contents Table

Market Briefing: Global Markets July 6, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at blog. thinking outside the box Table Of Contents Table

Internet Appendix to accompany Currency Momentum Strategies. by Lukas Menkhoff Lucio Sarno Maik Schmeling Andreas Schrimpf

Internet Appendix to accompany Currency Momentum Strategies by Lukas Menkhoff Lucio Sarno Maik Schmeling Andreas Schrimpf 1 Table A.1 Descriptive statistics: Individual currencies. This table shows descriptive

Internet Appendix to accompany Currency Momentum Strategies by Lukas Menkhoff Lucio Sarno Maik Schmeling Andreas Schrimpf 1 Table A.1 Descriptive statistics: Individual currencies. This table shows descriptive

These figures are to be attached to Polterovich and Popov's paper.

These figures are to be attached to Polterovich and Popov's paper. Fig. 3.1. Foreign Exchange Reserves as a % of GDP, Average Ratios for 19-99 Congo, Rep. US Mexico Russia (1993-99) India Brazil UK Pakistan

These figures are to be attached to Polterovich and Popov's paper. Fig. 3.1. Foreign Exchange Reserves as a % of GDP, Average Ratios for 19-99 Congo, Rep. US Mexico Russia (1993-99) India Brazil UK Pakistan

I pledge my honor that I have not violated the Honor Code during this examination.

The University of Chicago Booth School of Business Business Statistics, 41000-81/82, Spring 2011 Instructor: Hedibert F. Lopes Midterm Exam Name You may use a calculator. You may use a one-page-front-back

The University of Chicago Booth School of Business Business Statistics, 41000-81/82, Spring 2011 Instructor: Hedibert F. Lopes Midterm Exam Name You may use a calculator. You may use a one-page-front-back

Total Imports by Volume (Gallons per Country)

") 4/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 02/2017 02/2018 % Change 2017 2018 % Change MEXICO 53,961,589 55,268,981 2.4 % 108,197,008 114,206,836 5.6 % NETHERLANDS 12,804,152 11,235,029

4/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 02/2017 02/2018 % Change 2017 2018 % Change MEXICO 53,961,589 55,268,981 2.4 % 108,197,008 114,206,836 5.6 % NETHERLANDS 12,804,152 11,235,029

Progress Towards Strong, Sustainable, and Balanced Growth. Figure 1: Recovery From Financial Crisis (100 = First Quarter of Real GDP contraction)

") Progress Towards Strong, Sustainable, and Balanced Growth Figure 1: Recovery From Financial Crisis ( = First Quarter of Real GDP contraction) 13 125 196-26 AE Recessions' Range*** 196-26 AE Recessions**

Progress Towards Strong, Sustainable, and Balanced Growth Figure 1: Recovery From Financial Crisis ( = First Quarter of Real GDP contraction) 13 125 196-26 AE Recessions' Range*** 196-26 AE Recessions**

Study Questions (with Answers) Lecture 13. Exchange Rates

Lecture 13. Exchange Rates") Study Questions (with Answers) Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions (with Answers) Lecture 13 1. The statement the yen rose today from 121 to 117 makes

Study Questions (with Answers) Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions (with Answers) Lecture 13 1. The statement the yen rose today from 121 to 117 makes

HEALTH WEALTH CAREER 2016 CA MTCS: MERCER TOTAL COMPENSATION SURVEY FOR THE ENERGY SECTOR OVERVIEW AND SURVEY DEFINITIONS

HEALTH WEALTH CAREER 2016 CA MTCS: MERCER TOTAL COMPENSATION SURVEY FOR THE ENERGY SECTOR OVERVIEW AND SURVEY DEFINITIONS The analysis of the compensation and related information collected is displayed

HEALTH WEALTH CAREER 2016 CA MTCS: MERCER TOTAL COMPENSATION SURVEY FOR THE ENERGY SECTOR OVERVIEW AND SURVEY DEFINITIONS The analysis of the compensation and related information collected is displayed

Macroeonomics. 18 this chapter, Open-Economy Macroeconomics: look for the answers to these questions: Introduction. N.

C H A P T E R In 18 this chapter, look for the answers to these questions: Open-Economy Macroeconomics: How are international flows of goods and assets Basic Concepts related? P R I N C I P L E S O F Macroeonomics

C H A P T E R In 18 this chapter, look for the answers to these questions: Open-Economy Macroeconomics: How are international flows of goods and assets Basic Concepts related? P R I N C I P L E S O F Macroeonomics

Travel Insurance and Assistance

Travel Insurance and Assistance Worldwide research covering over 40 countries Series Prospectus Finaccord Ltd., 2016 Web: www.finaccord.com. E-mail: info@finaccord.com 1 Prospectus contents Page What is

Travel Insurance and Assistance Worldwide research covering over 40 countries Series Prospectus Finaccord Ltd., 2016 Web: www.finaccord.com. E-mail: info@finaccord.com 1 Prospectus contents Page What is

National Income & Business Cycles

National Income & Business Cycles accounting identities for the open economy the small open economy model what makes it small how the trade balance and exchange rate are determined how policies affect

National Income & Business Cycles accounting identities for the open economy the small open economy model what makes it small how the trade balance and exchange rate are determined how policies affect

Planning Global Compensation Budgets for 2018 November 2017 Update

Planning Global Compensation Budgets for 2018 November 2017 Update Planning Global Compensation Budgets for 2018 The year is rapidly coming to a close, and we are now in the midst of 2018 global compensation

Planning Global Compensation Budgets for 2018 November 2017 Update Planning Global Compensation Budgets for 2018 The year is rapidly coming to a close, and we are now in the midst of 2018 global compensation

Developing Housing Finance Systems

Developing Housing Finance Systems Veronica Cacdac Warnock IIMB-IMF Conference on Housing Markets, Financial Stability and Growth December 11, 2014 Based on Warnock V and Warnock F (2012). Developing Housing

Developing Housing Finance Systems Veronica Cacdac Warnock IIMB-IMF Conference on Housing Markets, Financial Stability and Growth December 11, 2014 Based on Warnock V and Warnock F (2012). Developing Housing

Performance Derby: MSCI Regions & Countries STRG, STEG, & LTEG

Performance Derby: MSCI Regions & Countries STRG, STEG, & LTEG February 7, 2018 Dr. Ed Yardeni 516-972-7683 eyardeni@yardeni.com Joe Abbott 732-497-5306 jabbott@yardeni.com Please visit our sites at blog.yardeni.com

Performance Derby: MSCI Regions & Countries STRG, STEG, & LTEG February 7, 2018 Dr. Ed Yardeni 516-972-7683 eyardeni@yardeni.com Joe Abbott 732-497-5306 jabbott@yardeni.com Please visit our sites at blog.yardeni.com

The construction of long time series on credit to the private and public sector

29 August 2014 The construction of long time series on credit to the private and public sector Christian Dembiermont 1 Data on credit aggregates have been at the centre of BIS financial stability analysis

29 August 2014 The construction of long time series on credit to the private and public sector Christian Dembiermont 1 Data on credit aggregates have been at the centre of BIS financial stability analysis