Due Diligence, Legal and Regulatory Valuation aspects

|

|

|

- Alexia O’Brien’

- 5 years ago

- Views:

Transcription

Vice President, Corporate")

1 Due Diligence, Legal and Regulatory Valuation aspects ICSI Certificate Course of Valuation Oct 2013 Chander Sawhney FCA, ACS, Certified Valuer (ICAI) Vice President, Corporate Professionals

2 Contents Particulars Pg. No. What and Why 3 How 10 When and Who 22 Tricky Issues 54

3 WHAT & WHY

4 Value & Valuation Value is* An Economic concept; An Estimate of likely prices to be concluded by the buyer and seller of a good or service that is available for purchase; Not a fact. Valuation is the process of determining the Economic Worth of an Asset or Company under certain assumptions and limiting conditions and subject to the data available on the valuation date. * Source -International Valuation Standard Council

5 Key Facts PRICE IS NOT THE SAME AS VALUE VALUE VARIES WITH PERSON, PURPOSE AND TIME TRANSACTION CONCLUDES AT NEGOTIATED PRICES VALUATION IS HYBRID OF ART & SCIENCE

6 S Standard of Valuation T Thesis of Valuation E Economics of Valuation M Methodologies of Valuation

7 Standard of Valuation Thesis of Valuation Economics of Valuation Methodologies of Valuation Standard of Value is the hypothetical conditions under which a business is valued. While selecting the Standard of Value following points is to be taken care of Subject matter of Valuation; Purpose of Valuation; Statute; Case Laws; Circumstances. Types of Standard of Value: FAIR MARKET VALUE INTRINSIC VALUE INVESTMENT VALUE FAIR VALUE

8 Standard of Valuation Thesis of Valuation Economics of Valuation Methodologies of Valuation Thesis of Value is Premise of value which relates to the assumptions upon which the valuation is based. Premise of Value Going Concern Value as an ongoing operating business enterprise. Liquidation Value when business is terminated. It could be forced or orderly. Value-in-use Value-in-exchange

9 Standard of Valuation Turnover / Profits Thesis of Valuation Economics of Valuation Methodologies of Valuation Valuation across business cycle follow the law of economics Declining Cos. ` Turnover/Profits: Drops Proven Track Record: Substantial Operating History Method of Valuation: Entirely from Existing Assets Cost of Capital: N.A. Mature Cos. Turnover/Profits: Saturated Proven Track Record: Widely Available Method of Valuation: More from Existing Assets Cost of Capital: May be High High Growth Cos. Turnover/Profits : Good Proven Track Record: Available Valuation Methodology: Business Model with Asset Base Cost of Capital: Reasonable Growing Cos. Turnover/Profits: Increasing still Low Proven Track Record: Limited Valuation Methodology: Substantially on Business Model Cost of Capital: Quite High Start Up Cos. Turnover/Profits: Negligible Proven Track Record: None Valuation Methodology: Entirely on Business Model Cost of Capital: Very High Time

10 HOW

11 Enterprise Value Enterprise / Business Value Value of Business Intangibles Equity # Net Current Assets Net Debt # Fixed Assets Stakeholders Assets # Based on Market Values

Comparable Companies Market Multiples Method (Listed Peers) Book Value Method Contingent Claim Valuation (Option Pricing) Discounted Cash Flow Method")

12 Standard of Valuation Thesis of Valuation Economics of Valuation Methodologies of Valuation Valuation Approaches Income Based Method Market Based Method Asset Based Method Other Methods Capitalization of Earning Method (Historical) Comparable Companies Market Multiples Method (Listed Peers) Book Value Method Contingent Claim Valuation (Option Pricing) Discounted Cash Flow Method (Projected Time Value) Comparable Transaction Multiples Method (Unlisted Peers) Liquidation Value Method Price of Recent Investment Method Market Value Method (For Quoted Securities) Replacement Value Method Rule of Thumb (Multiples: Customers, Rooms, Seats, No. of visitors etc.) - Depends upon Industry

13 Need of several valuation methods? Each has strengths and weaknesses Different methods useful in different situations Each gives a different take on the value of the company s stock Provides a range of valuations instead of point estimates Helps in Sanity Check While concluding Value, all the methodologies must be considered and then weights applied as per the facts of the case. In other words, Value conclusion should be based on the Professional Judgement and Simple Average should best be avoided while concluding Value.

14 Sources of Information for Valuation Sources of Information Historical financial results Income Statement, Balance Sheets and Cash Flows Data available in Public Domain Stock Exchange / MCA/SEBI/Independent Report Data on comparable companies SALES/EV- EBITDA/ PAT/BV Promoters and Management background Discussion and Representation with/by the management of the Company Data on projects planned/under implementation including future projection Industry and Regulatory trends

15 Key drivers of valuation CASH FLOW Investor assign value based on the cash flow they expect to receive in the future - Dividends / distributions That s why DCF is most - Sale of liquidation proceeds Value of a cash flow stream is a function of - Timing of cash Receipt - Risk associated with the cashflow prominent method valuation ASSETS Operating Assets - Assets used in the operation of the business including working capital, Property, Plant & Equipment & Intangible assets - Valuing of operating assets is generally reflected in the cash flow generated by the business Non - Operating Assets - Assets not used in the operations including excess cash balances, and assets held for investment purposes, such as vacant land & Securities - Investors generally do not give much value to such assets and Structure modification may be necessary Need for Restructuring

16 Valuation depends upon Purpose Regulatory Accounting Mergers IPO Acquisitions / Investment Voluntary Assessment RBI Income Tax SEBI Stock Exchange Companies Act ESOP Purchase Price Allocation Impairment / Diminution Dispute Resolution Company Law Board/ Courts Arbitration Mediation Value Creation Equity Research Credit Rating Corporate Planning

17 Choice of Valuation Approaches Value in Valuation is a question, and Your choice of Method is the first step towards answer Applicability of a particular approach depends upon: On whose behalf? one buyer vs another buyer, buyer vs seller; For what purpose? independent strategic acquisition, group company consolidation, cross border transaction; When? distress situation, industry downturn, boom etc;

18 Choice of Valuation Approaches In General, Income Approach is preferred; The dominance of profits for valuation of share was emphasised in McCathies case (Taxation, 69 CLR 1) where it was said that the real value of shares in a company will depend more on the profits which the company has been making and should be capable of making, having regard to the nature of its business, than upon the amount which the shares would realise on liquidation. This was also re-iterated by the Indian Courts in Commissioner of Wealth Tax v. Mahadeo Jalan s case (S.C.) (86 ITR 621) and Additional Commissioner of Gift Tax v. Kusumben D. Mahadevia (S.C.) (122 ITR 38). However, Asset Approach is preferred in case of Asset heavy companies and on liquidation; Market Approach is preferred in case of listed entity and to evaluate the value of unlisted company by comparing it with its listed peers;

19 Company Specific Factors Management, Promoter Group Operating, Capital and Corporate Finance Strategies Competitive advantages and cost position Product / Service offering / differentiation / pricing power Scale & Diversification Customer / Supplier concentration Corporate Governance Future prospects / Growth potential Industry peer group Regulatory environment It is the alignment of Company s value via-avis to its external environment

Industry cyclicality (earnings quality) Leading indicators Competition (ROIC) Pricing dynamics; Demand vs.")

20 Industry Risk Analysis Following factors are required to be considered: Good vs. Difficult industry Porter s 5 forces Industry life cycle (growth) Industry cyclicality (earnings quality) Leading indicators Competition (ROIC) Pricing dynamics; Demand vs. Supply (ROIC) Changing business environments Regulation (ROIC) Product characteristics (earnings quality) Capital intensity and cost base (ROIC) Event risk

21 Rule of Thumb A rule of thumb or benchmark indicator is used as a reasonableness check against the values determined by the use of other valuation approaches. Industry Hospital Engineering Mutual Fund OIL Print Media Power Entertainment & Media Metals Textiles Pharma Bulk Drugs Airlines Shipping Cement Banks Valuation Parameters EV/Room Mcap/Order Book Asset under management EV/ Barrel of equivalent EV/Subscriber EV/MW, EBITDA/Per Unit EV/Per screen EBITDA/Ton, EV/Metric ton EBITDA depend upon capacity utilization Percentage & per spindle value New Drug Approvals, Patents EV/Plane or EV/passenger EV/Order Book, Mcap/Order Book EV/Per ton & EBITDA/Per ton Non performing Assets, Current Account & Saving Account per Branch However, Exclusive use of Rule of Thumb is not recommended

22 WHEN & WHO

23 Valuation in Indian Regulatory Environment

NAV - Income Tax Gift of Unquoted Equity Shares")

24 SNAPSHOT OF REGULATORY VALUATIONS IN INDIA Transactions Prescribed Methodologies Mandate to be done by Reserve Bank of India Inbound Investment DFCF CA / MB Outbound Investment Valuer Discretion >5Mn$ - MB, otherwise CA/MB Gift of Unquoted Equity Shares (Min) NAV - Income Tax Gift of Unquoted Equity Shares from Resident (Max) Gift of Unquoted Shares other than Equity Shares DCF (Valuation Based on Assets, Business & Intangibles is also acceptable) Price it would fetch if sold in open market FCA / MB MB ESOP Tax Valuer Discretion MB ESOP Accounting Option Pricing Model - SEBI Takeover Code/ Delisting - Infrequently Traded Only Parameters Prescribed Return on Net Worth, EPS, NAV vis-a vis Industry Average CA/MB Takeover Code/ Delisting - Frequently Traded Based on Market Price - Stock Exchanges Preferential Allotment to Others Preferential Allotment to promoters / their relatives for consideration other than cash Based on 26 weeks / 2 weeks Market Price Valuer Discretion Companies Act, 1956 Sweat Equity Valuer Discretion - CA / MB - Companies Act, 2013 any property, stock, shares, debentures, securities or goodwill or any other assets or the net worth of the Company or its liabilities To be prescribed REGISTERED VALUER

25 RBI Valuation Guidelines

Regulations, 2000.")

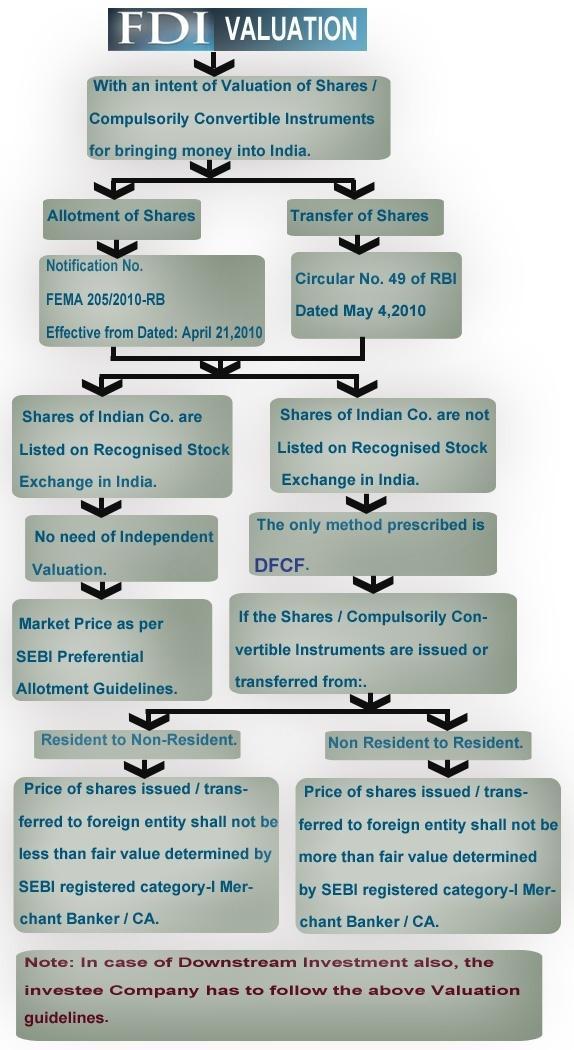

26 FDI VALUATION Notification No. FEMA 20/2000-RB dated May 3, 2000, as amended from time to time deals with Foreign Exchange Management (Transfer or Issue of Security by a Person Resident Outside India) Regulations, In terms of Schedule 1 of the Notification, an Indian company may issue equity shares/compulsorily convertible preference shares and compulsorily convertible debentures (equity instruments) to a person resident outside India under the FDI policy, subject to inter alia, compliance with the pricing guidelines. The price/ conversion formula of convertible capital instruments should be determined upfront at the time of issue of the instruments.

27 Particulars Valuation before April 21, 2010 Valuation after April 21, 2010 Guidelines in Force CCI Guidelines In case of FDI Transactions: Listed Company: Market Value Methods Prescribed Net Assets Value (NAV) as per SEBI Preferential Profit Earning Capacity Allotment Guidelines Value(PECV) Market Value (in case of Listed Company) Unlisted Company: DFCF Discount FEMA Guidelines to Valuation 15% Discount has been prescribed on account of Lack of Marketability In case of ODI Transactions: No method has been prescribed No such Discount has been prescribed Historical / Futuristic It is based on Historical Values It is based on Future Projections Possibility of variation in Value Conclusion As valuation is more Formulae based, final values came standardized As valuation is more dependent on Assumptions and choice of factors like Growth Rate, Cost of Capital etc, value conclusion may vary significantly. Note: Valuation guidelines do not apply to SEBI registered venture capital

28

may not yield Fair Value in line with the Commercial understanding. However Law being such, suitable Logical adjustments may be necessary on a case to case basis.")

29 Approaches to FDI Valuation Discounted Free Cash Flow Method (DFCF) RBI has prescribed DFCF as the only valuation method in case of FDI (excluding for initial subscription); but has not provided any guidance on its technical aspects. Though DFCF is one of the most acceptable Valuation methods used by Business valuers worldwide; however DFCF for all FDI transactions-excluding for initial subscription (like minority stake/start up valuation etc) may not yield Fair Value in line with the Commercial understanding. However Law being such, suitable Logical adjustments may be necessary on a case to case basis. DFCF expresses the present value of the business as a function of its future cash earnings capacity. In this method, the appraiser estimates the cash flows of any business after all operating expenses, taxes, and necessary investments in working capital and capital expenditure is being met. Valuing equity using the free cash flow to stockholders requires estimating only free cash flow to equity holders, after debt holders have been paid off.

30 Major Characteristics of DFCF Valuation Forward Looking and focuses on cash generation Recognizes Time value of Money Allows operating strategy to be built into a model Incorporates value of Tangible and Intangible assets Only as accurate as assumptions and projections used Works best in producing a range of likely values It Represents the Control Value

31 DFCF Valuation Process Understand Business Model Identify Business Cycle Analyze Historical Financial Performance Review Industry and Regulatory Trends Understand Future Growth Plans (including Capex needs) Segregate Business and Other Cash Generating Assets Identify Surplus Assets (assets not utilized for Business say Land/Investments) Create Business Projections (Profitability statement and Balance Sheets) Discount Business Projections to Present (Explicit Period and Perpetuity) Add Value of Surplus Assets and Subtract Value of Contingent Liabilities

32 Free Cash Flows- Value Trend Terminal Value is calculated for the Perpetuity period based on the Adjusted last year cash flows of the Projected period.

method in which the value of Equity is directly valued in lieu of the value of Firm.")

33 Free Cash Flow calculation FREE CASH FLOWS Free cash flows to firm (FCFF) is calculated as EBITDA Taxes Change in Non Cash Working capital Capital Expenditure Free Cash Flow to Firm Note that an alternate to above is following (FCFE) method in which the value of Equity is directly valued in lieu of the value of Firm. Under this approach, the Interest and Finance charges is also deducted to arrive at the Free Cash Flows. Adjustment is also made for Debt (Inflows and Outflows) over the definite period of Cash Flows and also in Perpetuity workings. Theoretically, the value conclusion should remain same irrespective of the method followed (FCFF or FCFE), (Provided, assumptions are consistent).

34 Cost of Capital calculation DISCOUNT RATE WEIGHTED AVERAGE COST OF CAPITAL WACC (K d x D) + (K e x E) (D + E) Where: D = Debt part of capital structure E = Equity part of capital structure K d = Cost of Debt (Post tax) K e = Cost of Equity In case of following FCFE, Discount Rate is Ke and Not WACC

35 Cost of Equity calculation DISCOUNT RATE - COST OF EQUITY The Cost of Equity (Ke) is computed by using Modified Capital Asset Pricing Model (Mod. CAPM) Mod. CAPM Model ke = Rf + B ( Rm-Rf) + SCRP + CSRP Where: Rf = Risk free rate of return (Generally taken as 10-year Government Bond Yield) B = Beta Value (Sensitivity of the stock returns to market returns) K e = Cost of Equity Rm= Market Rate of Return (Generally taken as Long Term average return of Stock Market) SCRP = Small Company Risk Premium CSRP= Company specific Risk premium

36 PERPETUITY FORMULA Terminal value calculation Usually comprises a Large part of Total Value and is sensitive to small changes Capitalizes FCF after definite forecast period as a growing perpetuity; Estimate Terminal Value using Terminal Value Multiplier applied on last year cash flows Gordon Formula is often used to derive the Terminal Cash Flows by applying the last year cash flows as a multiple of the growth rate and discounting factor (1 + g) (WACC g) Estimated Terminal Value is then discounted to present day at company s cost of capital based on the discounting factor of last year projected cash flows IMPORTANT TIP- It is advised to do Sanity check by applying Relative Valuation Multiples to the Terminal Year Financials and also doing Scenario Analysis.

37 An Insight of Valuationwww.CorporateValuations.in

38 SEBI / Stock Exchange Valuation Guidelines

39 Takeover Regulations APPLICABLE LAW: SEBI (Substantial Acquisition of Shares & Takeovers) Regulations, 2011 FREQUENTLY TRADED SHARES Traded Turnover of Shares 10% [In the Last Twelve Calendar Months preceding the Month of Public Announcement (P.A.)] Method of Valuation 1. Highest Negotiated Price Per Share under agreement attracting the obligation to make P.A. 2. The volume weighted avg. price paid or payable by acquirer or PAC during the 52 Weeks; 3. The Highest Price paid or payable by acquirer or PAC in last 26 Weeks; 4. Volume weighted average Market Price of Shares for a period of 60 trading days HIGHEST PRICE AMONG ALL IS THE VALUE PER SHARE FOR P.A. INFREQUENTLY TRADED SHARES Traded Turnover of Shares < 10% [In the Last Twelve Calendar Months preceding the Month of Public Announcement (P.A.)] 1. Book value, 2. Comparable Trading Multiples; Method of Valuation Such other Parameters as are customary for valuation of shares of such companies

40 Preferential Issue (1 of 3) APPLICABLE LAW: SEBI (ICDR) Regulations, 2009 Equity shares of issuer have been listed on recognized stock exchange for a period of 26 weeks or more as on relevant date Method of Valuation 1. The average of the weekly high and low of the closing prices of the related equity shares quoted on the recognised stock exchange during 26 weeks preceding the relevant date, or 2. The average of the weekly high and low of the closing prices of the related equity shares quoted on the recognised stock exchange during 26 weeks preceding the relevant date. HIGHEST PRICE AMONG ALL IS THE VALUE PER SHARE

41 Preferential Issue ( 2 of 3) APPLICABLE LAW: SEBI (ICDR) Regulations, 2009 Equity shares of issuer have been listed on recognized stock exchange for a period of less than 26 weeks as on relevant date Method of Valuation 1. The price at which equity shares were issued by the issuer in its IPO or value per share arrived at in a scheme of arrangement under section 391 to 394 of the Companies Act, 1956, pursuant to which the equity shares of the issuer were listed, as the case may be, or 2. The average of the weekly high and low of the closing prices of the related equity shares quoted on the recognised stock exchange during the period shares have been listed preceding the relevant date, or 3. The average of the weekly high and low of the closing prices of the related equity shares quoted on the recognised stock exchange during 2 weeks preceding the relevant date. HIGHEST PRICE AMONG ALL IS THE VALUE PER SHARE

42 Preferential Issue ( 3 of 3) APPLICABLE LAW: SEBI (ICDR) Regulations, 2009 Equity shares have been issued to promoters / their relatives for consideration other than cash, The VALUATION OF ASSETS in consideration for which the equity shares are issued shall be done by an independent valuer No Method for Valuation has been prescribed. Method of Valuation Chartered Accountant or a Merchant Banker Valuer

43 ESOP Accounting Valuation APPLICABLE LAW: SEBI (ESOS and ESPS) Guidelines, 1999 If a Company listed on recognised stock exchange in India and issued shares under an ESOS / ESPS, the fair value of stock option shall be estimated using an option pricing model (Black-Scholes or a binomial model) which shall be treated as employee compensation cost for the Company. Black-Scholes Model Method of Valuation Not Prescribed Valuer

44 Income Tax Act-1961

45 Equity Shares Valuation APPLICABLE LAW: Income Tax Act 1961 and Rule 11UA If Individual, HUF, Firm or *closely held Company receives Equity shares of a closely held Company Valuation norms shall apply. Minimum Valuation- Net Asset Value Method of Valuation Maximum Valuation- DCF and other methods factoring Tangible and Intangibles Valuer No specific Valuer prescribed for undertaking Minimum Value FCA / Merchant Banker for determining Maximum Value *If a Public Listed Company receives any shares or anyone receives shares of a Public listed Company, valuation norms are not applicable if transaction takes at market price.

46 APPLICABLE LAW: Valuation of shares other than Equity Shares Income Tax Act 1961 and Rule 11UA If Individual, HUF, Firm or *closely held Company receives shares other than Equity shares of a closely held Company Valuation norms shall apply. Method of Valuation Price at which such shares will fetch in the open market. Valuer Valuation report to be issued by Merchant Banker

47 ESOP Tax Valuation APPLICABLE LAW: Income Tax Act 1961 and Notification no. 94/2009 dated issued by CBDT To determine the value of perquisite taxable in hands of employees No method has been prescribed Method of Valuation SEBI registered category I Merchant Banker Valuer

48 Companies Act- 2013

49 Registered Valuer Sec 247 Stock, Shares, Debentures, Securities, Goodwill Financial Valuer Registered Valuer Technical Valuer Property Shall have 5 Years of Continues Experience A Chartered Accountant, Company Secretary or Cost Member of the Institute of Engineers or Member of the Shall have 5 Years of Continues Experience Accountant Institute of Architects having in employment under it, either a chartered accountant or company secretary or cost accountant and either of whom shall have continuous experience of five years A Merchant Banker registered with the Securities and Exchange Board of India A Merchant Banker registered with the Securities and Exchange Board of India having in employment under it, either a member of Institute of Engineers / Architects and either of whom shall have continuous experience of five years

50 Registered Valuer Sec 247 Further Issue of Shares Corporate Debt Restructuring Compromise and Arrangements Registered Valuer (Financial Valuation) Values Exit to Minority Shareholders Registered Valuer Winding up / Liquidation Valuer not to be interested Valuer to exercise due diligence Valuation to be done as per rules Valuer liable for damages on default Non Cash Transactions with Directors

51 Accounting Valuation

52 Purchase Price Allocation What is a Purchase Price Allocation? - an acquiring entity must allocate the purchase price to the assets acquired and liabilities assumed based on estimated fair values at the date of acquisition; - The excess of the cost of an acquired entity (including tangible and intangible assets) over the net of the amounts assigned to assets acquired and liabilities assumed is recorded as Goodwill ; Consideration paid for acquisition Allocated to Tangible Assets Intangible Assets In Proportion to Fair Value Goodwill Balancing Figure

53 Purchase Price Allocation Why Purchase Price Allocation? - Intangible assets recognized separately from goodwill must be valued and amortized for financial reporting purposes, if appropriate - This may result in better Tax planning for undertaking the transactions of acquisition of assets and liabilities; Under Slump sale transaction, specifically the Intangible Assets can be separately accounted for by the Acquirer and Depreciation also claimed under the provisions of Indian Income Tax Law. - PPA is used to allocate the Business Value between Tangible and Intangible Assets.

54 Tricky Issues

55 Discounts Discounts & Premiums come into picture when there exist difference between the subject being valued and the Methodologies applied. As this can translate control value to non-control and vise versa, so these should be judiciously applied. Discount for Entity Level Impact on entity as a whole Key Person Discount Discount for Contingent Liability Discount for diversified company Discount for Holding Company Global Studies over the years on diversified companies and holding companies has shown that companies trade at a discount in the range of 20%. to 40% each. Tax Payout Discount for Shareholders Level Impact on specific ownership interest Discount Lack of Control (DLOC) Discount Lack of Marketability (DLOM) DLOM: As per CCI Guidelines, 15% % stake & special rights discount has been prescribed; however practically DLOM and DLOC depends upon following factors: Size of distribution or dividends Dispute Revenue / Earning Growth / Stability Private Company Shareholders Agreement caveats

56 Premium Control Premium - An investor seeking to acquire control of a company is typically willing to pay more than the current market price of the company. Control premium is an amount that a buyer is usually willing to pay over the fair market value of a publicly traded company to acquire controlling stake in a company Research has shown that the control premium in India has ranged from 20% to 37% in the past few years.

57 Excess Cash and Non Operating Assets Excess cash is defined as total cash (in balance sheet) operating cash (i.e. minimum required cash) to sustain operations (working capital) and manage contingencies Key Issue: Estimation of Excess Cash? One of the solutions is to estimate average cash/sales or total balance sheet size of the company s relevant Industry and then estimate if the company being valued has cash in excess of the industry s average. Non operating Assets are the Surplus assets which are not used in operations of the business and does not reflect its value in the operating earnings of the company. Therefore the fair market value of such Assets should be separately added to the value derived through valuation methodologies to arrive at the value of the company. What is an asset is not yielding adequate returns?

By way of Shareholders Agreement even less % holding may command")

58 Cross Holding and Investments Holdings in other firms can be categorized into: Types of Cross Holding Minority, Passive Investments Minority, Active Investments Majority, Active Investments Meaning If the securities or assets owned in another firm represent less than 20% of the overall ownership of that firm If the securities or assets owned in another firm represent between 20% and 50% of the overall ownership of that firm If the securities or assets owned in another firm represent more than 50% of the overall ownership of that firm Ways to value Cross Holding and Investments: Investment Value Dividend Yield Capitalization or DCF based on expected dividends Seperate Valuation (Preferred) By way of Shareholders Agreement even less % holding may command control value

59 Accounting Practices and Tax issues Most of the information that is used in valuation comes from financial statements. which in turn are made on certain Accounting practices considered appropriate. Cash Accounting v/s Accrual Accounting Operating Lease v/s Financial Lease Capitalization of Expenses Notional Tax vs. Actual Tax Treatment of Intangible Assets Companies Paying MAT Treatment of Tax benefits and Losses

60 Valuation Methodologies and Value Impact Major Valuation Methodologies Ideal for Result Net Asset Value Net Asset Value (Book Value) Net Asset Value (Fair Value) Minority Value Control Value Equity Value Comparable Companies Multiples (CCM) Method Price to Earning, Book Value Multiple Minority Value Equity Value EBIT, EBITDA Multiple Enterprise Value Comparable Transaction Multiples (CTM) Method Price to Earning, Book Value Multiple EBIT, EBITDA Multiple Control Value Equity Value Enterprise Value Equity Firm Discounted Cash Flow (DCF) Control Value Equity Value Enterprise Value

61 IRS Revenue Ruling ( ),USA Revenue Ruling (RR) is one of the oldest guidance available on Valuation in the world but still most relevant for Tax Valuations specifically for Valuing closely held common stock. It is the most widely referenced revenue ruling, also often referenced for Non Tax Valuations. While Valuing, it gives primary guidance on eight basic factors to consider- Nature of the Business and the History of the Enterprise from its inception Economic outlook in general and outlook of the specific industry in particular Book Value of the stock and the Financial condition of the business Earning Capacity of the company Dividend-Paying Capacity of the company. Goodwill or other Intangible value Sales of the stock and the Size of the block of stock to be valued Market prices of stock of corporations engaged in the same or a similar line of business

62 Chander Sawhney, Vice President Corporate Professionals Capital Pvt. Ltd. SEBI registered merchant banker chander@indiacp.com Mobile: ; Direct: D-28, South Extention, Part-I, New Delhi Disclaimer: This presentation contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither corporatevaluations.in nor any other member of the Corporate Professionals organization accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this presentation. On any specific matter, reference should be made to the appropriate advisor. 2013, Corporate Professionals. All rights reserved

Relative Valuation. 31 st August 2016 Business Valuation Master class, New Delhi

Relative Valuation 31 st August 2016 Business Valuation Master class, New Delhi Agenda - Overview of Valuation - Principles of Relative Valuation - Why Relative Valuation is more favoured in Application

Relative Valuation 31 st August 2016 Business Valuation Master class, New Delhi Agenda - Overview of Valuation - Principles of Relative Valuation - Why Relative Valuation is more favoured in Application

Due Diligence, Legal and Regulatory Valuation aspects

In the business world, the rearview mirror is always clearer than the windshield Warren Buffett Due Diligence, Legal and Regulatory Valuation aspects 01/07/2015 FEMA Valuation Aspect (FDI & ODI) Particulars

In the business world, the rearview mirror is always clearer than the windshield Warren Buffett Due Diligence, Legal and Regulatory Valuation aspects 01/07/2015 FEMA Valuation Aspect (FDI & ODI) Particulars

An Insight of Valuation

An Insight of Valuation by- www.corporatevaluations.in a venture of SEBI REGISTERED (CAT -I) MERCHANT BANKER Contents Particulars TABLE OF CONTENT Pg. No. Valuation Overview 1 Approaches to Valuation -

An Insight of Valuation by- www.corporatevaluations.in a venture of SEBI REGISTERED (CAT -I) MERCHANT BANKER Contents Particulars TABLE OF CONTENT Pg. No. Valuation Overview 1 Approaches to Valuation -

RBI guidelines for valuation of shares. FDI Valuation Guidelines

RBI guidelines for valuation of shares For Foreign Direct Investment (FDI) transactions, Notification No. FEMA 20/2000-RB dated May 3, 2000, as amended from time to time deals with Foreign Exchange Management

RBI guidelines for valuation of shares For Foreign Direct Investment (FDI) transactions, Notification No. FEMA 20/2000-RB dated May 3, 2000, as amended from time to time deals with Foreign Exchange Management

The Price is Right. Calculation of Price - Investments

The Price is Right This article attempts to set out the rules for valuation, as prescribed in various regulations, which have an impact on M&A transactions in India. Calculation of Price - Investments

The Price is Right This article attempts to set out the rules for valuation, as prescribed in various regulations, which have an impact on M&A transactions in India. Calculation of Price - Investments

Introduction to Valuation

Introduction to Valuation Romesh Vijay CA, ICAI Certified Valuer Contents Introduction Overview of Methods Used Case Studies Relative Method of Valuation Introduction Valuer A valuer is a fellow who lends

Introduction to Valuation Romesh Vijay CA, ICAI Certified Valuer Contents Introduction Overview of Methods Used Case Studies Relative Method of Valuation Introduction Valuer A valuer is a fellow who lends

Valuation of Shares / Business An Overview. CA Shivaprakash Viraktamath 20 th January 2017

Valuation of Shares / Business An Overview CA Shivaprakash Viraktamath 20 th January 2017 1 Contents 1. Why Valuation? 2. Key Factors Influencing Valuation 3. Sources of Information 4. Valuation for Regulatory

Valuation of Shares / Business An Overview CA Shivaprakash Viraktamath 20 th January 2017 1 Contents 1. Why Valuation? 2. Key Factors Influencing Valuation 3. Sources of Information 4. Valuation for Regulatory

ISSUES IN VALUATION UNDER FEMA

ISSUES IN VALUATION UNDER FEMA REGIONAL CONFERENCE OF WIRC CA. SUJAL SHAH AUGUST 31, 2012 1 VALUATION - INTRODUCTION What is Valuation? Valuation means assigning a value to underlying assets The value

ISSUES IN VALUATION UNDER FEMA REGIONAL CONFERENCE OF WIRC CA. SUJAL SHAH AUGUST 31, 2012 1 VALUATION - INTRODUCTION What is Valuation? Valuation means assigning a value to underlying assets The value

Valuation Techniques BANSI S. MEHTA & CO.

Valuation Techniques USHMA SHAH BANSI S. MEHTA & CO. PRICE is what you pay. VALUE is what you get. They are not the I can make a whole lot more money skilfully managing intangible assets than managing

Valuation Techniques USHMA SHAH BANSI S. MEHTA & CO. PRICE is what you pay. VALUE is what you get. They are not the I can make a whole lot more money skilfully managing intangible assets than managing

One of the major applications of Equity Valuation is the Private companies valuation. Private companies valuation can be applied:

One of the major applications of Equity Valuation is the Private companies valuation. Private companies valuation can be applied: To value a Start up operations of Public companies. To estimate a value

One of the major applications of Equity Valuation is the Private companies valuation. Private companies valuation can be applied: To value a Start up operations of Public companies. To estimate a value

CA SUJAL SHAH. 22 nd June 2013

CA SUJAL SHAH 22 nd June 2013 Value Price Valuation-not an exact science, more an art Value varies with situations Date specific Purchase / Sale of Business Merger/ Demerger Private Equity Buyback of Shares

CA SUJAL SHAH 22 nd June 2013 Value Price Valuation-not an exact science, more an art Value varies with situations Date specific Purchase / Sale of Business Merger/ Demerger Private Equity Buyback of Shares

Valuation Overview & Methodologies

Valuation Overview & Methodologies CA Sujal Shah & CA Bhakti Shah 18th November 2017 ICAI Mumbai Seminar on Valuation VALUATION CONCEPTS Value Price Not an Exact science Value varies with Situation Valuation

Valuation Overview & Methodologies CA Sujal Shah & CA Bhakti Shah 18th November 2017 ICAI Mumbai Seminar on Valuation VALUATION CONCEPTS Value Price Not an Exact science Value varies with Situation Valuation

VALUATION & BIZ MODELLING PROFILE

VALUATION & BIZ MODELLING PROFILE CONTENTS Why Valuation Our process flow Key deliverables of our Valuation Report Our Valuation Credentials Our Valuation Offerings Appendix 1: Valuation Approaches and

VALUATION & BIZ MODELLING PROFILE CONTENTS Why Valuation Our process flow Key deliverables of our Valuation Report Our Valuation Credentials Our Valuation Offerings Appendix 1: Valuation Approaches and

Contents. Topics to discuss

Contents Key Facets of Valuation Premises of Valuation Different Purposes of Valuation Sources of Information Approach for Valuation Types of Values Topics to discuss Fair Value Concept under IFRS Ind

Contents Key Facets of Valuation Premises of Valuation Different Purposes of Valuation Sources of Information Approach for Valuation Types of Values Topics to discuss Fair Value Concept under IFRS Ind

Steps in Business Valuation

Steps in Business Valuation Professor Grant W. Newton, Executive Director Association of Insolvency & Restructuring Advisors Suggested Inquiries and Challenges in Current Environment When the company being

Steps in Business Valuation Professor Grant W. Newton, Executive Director Association of Insolvency & Restructuring Advisors Suggested Inquiries and Challenges in Current Environment When the company being

19 NOVEMBER 2011 DRUSHTI DESAI

19 NOVEMBER 2011 DRUSHTI DESAI PRESENTATION OVERVIEW Purpose of Valuation Steps in Valuation Analysis of Company Principal Methods of Valuation Fair Value Other Value Drivers Issues Purchase / Sale of

19 NOVEMBER 2011 DRUSHTI DESAI PRESENTATION OVERVIEW Purpose of Valuation Steps in Valuation Analysis of Company Principal Methods of Valuation Fair Value Other Value Drivers Issues Purchase / Sale of

Valuation of Equity Shares. CA Sujal Shah 30th December 2016 WIRC Seminar on Valuation

Valuation of Equity Shares CA Sujal Shah 30th December 2016 WIRC Seminar on Valuation 2 Presentation Overview Valuation Concept Valuation Approaches Selection of Methods Requirements under various laws

Valuation of Equity Shares CA Sujal Shah 30th December 2016 WIRC Seminar on Valuation 2 Presentation Overview Valuation Concept Valuation Approaches Selection of Methods Requirements under various laws

Valuation Principles

Valuation Principles The ACG Cup January 20, 2016 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.327.2171 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

Valuation Principles The ACG Cup January 20, 2016 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.327.2171 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

CHAPTER XVII REGISTERED VALUERS Registered Valuer means a person registered as a Valuer under Chapter XVII of the Act.

DRAFT RULES UNDER COMPANIES ACT, 2013 CHAPTER XVII REGISTERED VALUERS Definition 17.1 Registered Valuer means a person registered as a Valuer under Chapter XVII of the Act. Registration as Valuers. 17.2

DRAFT RULES UNDER COMPANIES ACT, 2013 CHAPTER XVII REGISTERED VALUERS Definition 17.1 Registered Valuer means a person registered as a Valuer under Chapter XVII of the Act. Registration as Valuers. 17.2

Valuation Principles

Valuation Principles The ACG Cup January 16, 2018 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.813.4101 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

Valuation Principles The ACG Cup January 16, 2018 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.813.4101 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

The Institute of Chartered Accountants of India

CONCERNS OF ICAI ON AMENDED RULE 11U AND RULE 11UA VIDE NOTIFICATION N0. 23/2018, Dated 24 th MAY, 2018 ISSUED BY THE CBDT Rule 11UA provides for the manner of determining the fair market value of various

CONCERNS OF ICAI ON AMENDED RULE 11U AND RULE 11UA VIDE NOTIFICATION N0. 23/2018, Dated 24 th MAY, 2018 ISSUED BY THE CBDT Rule 11UA provides for the manner of determining the fair market value of various

Business Valuation Report

Certified Business Appraisals, LLC Business Valuation Report Prepared for: John Doe Client Business, Inc. 1 Market Way Your Town, CA December 3, 2017 1 Market Street Suite 100 Anytown, CA 95401 Web: www.yourdomain.com

Certified Business Appraisals, LLC Business Valuation Report Prepared for: John Doe Client Business, Inc. 1 Market Way Your Town, CA December 3, 2017 1 Market Street Suite 100 Anytown, CA 95401 Web: www.yourdomain.com

WIRC 28 th May 2016 Pinkesh Billimoria. Case Studies

WIRC 28 th May 2016 Pinkesh Billimoria Case Studies Valuation A Perspective Valuation is relative to a specific point in time What is being valued Why it is being valued Secure definition of value Going

WIRC 28 th May 2016 Pinkesh Billimoria Case Studies Valuation A Perspective Valuation is relative to a specific point in time What is being valued Why it is being valued Secure definition of value Going

Valuation Principles

Valuation Principles The ACG Cup January 15, 2019 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.813.4101 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

Valuation Principles The ACG Cup January 15, 2019 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.813.4101 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

VALUATION UNDER COMPANIES ACT CA MANDAR GADKARI AUGUST 10, 2017

VALUATION UNDER COMPANIES ACT CA MANDAR GADKARI AUGUST 10, 2017 VALUATION Introduction What is Valuation : The process of determining the current worth of an asset or a company Various techniques to determine

VALUATION UNDER COMPANIES ACT CA MANDAR GADKARI AUGUST 10, 2017 VALUATION Introduction What is Valuation : The process of determining the current worth of an asset or a company Various techniques to determine

Basics of Business Valuation. Presented by: Alon Wexler, CPA, CA, CBV Richter Advisory Group Inc.

Basics of Business Valuation Presented by: Alon Wexler, CPA, CA, CBV Richter Advisory Group Inc. 2017 Objective Brief overview of the Basics of Business Valuation There is more to it than 5x EBITDA! 2

Basics of Business Valuation Presented by: Alon Wexler, CPA, CA, CBV Richter Advisory Group Inc. 2017 Objective Brief overview of the Basics of Business Valuation There is more to it than 5x EBITDA! 2

Fall ESOP Forum

Valuation Basics Presented by: Michael Yi, ASA, CPA Newport Valuations, Inc. 23 Corporate Plaza, Ste 150 Newport Beach, CA 92660 949-706-1313 Myi@newportvaluations.com Your logo here 1 Overview Introductions

Valuation Basics Presented by: Michael Yi, ASA, CPA Newport Valuations, Inc. 23 Corporate Plaza, Ste 150 Newport Beach, CA 92660 949-706-1313 Myi@newportvaluations.com Your logo here 1 Overview Introductions

Advanced Company Analysis Valuation & Financial Modelling. 5-9 March 2017 Manama, Bahrain. euromoneylearningsolutions.

Advanced Company Analysis Valuation & Financial Modelling 5-9 March 2017 Manama, Bahrain euromoneylearningsolutions.com/learnmore Advanced Company Analysis Valuation & Financial Modelling Accelerate your

Advanced Company Analysis Valuation & Financial Modelling 5-9 March 2017 Manama, Bahrain euromoneylearningsolutions.com/learnmore Advanced Company Analysis Valuation & Financial Modelling Accelerate your

Valuation Importance and Issues. Chamber of Tax Consultants, Seminar on Corporate Restructuring 20 January 2017 Pinkesh Billimoria

Valuation Importance and Issues Chamber of Tax Consultants, Seminar on Corporate Restructuring 20 January 2017 Pinkesh Billimoria Investing in India An Easy Difficulty Valuation expectations / Mismatch

Valuation Importance and Issues Chamber of Tax Consultants, Seminar on Corporate Restructuring 20 January 2017 Pinkesh Billimoria Investing in India An Easy Difficulty Valuation expectations / Mismatch

Reporting Aspects Discounted Cash Flow (DCF) Valuation. CA Shirish S. Rahalkar

Valuation. CA Shirish S. Rahalkar") 1 Reporting Aspects Discounted Cash Flow (DCF) Valuation CA Shirish S. Rahalkar The Chartered Accountant Act says, 2 Clause (3) Part I Second Schedule of The Chartered Accountant Act, 1949 states Practising

1 Reporting Aspects Discounted Cash Flow (DCF) Valuation CA Shirish S. Rahalkar The Chartered Accountant Act says, 2 Clause (3) Part I Second Schedule of The Chartered Accountant Act, 1949 states Practising

Introduction. PEs: the invesment process and the Value Creation

Introduction PEs: the invesment process and the Value Creation 1 Contents - Introduction - PE Stages and Investment Process - Initial Strategic Definition: Types of deal and PEs - Deal Sourcing - Initial

Introduction PEs: the invesment process and the Value Creation 1 Contents - Introduction - PE Stages and Investment Process - Initial Strategic Definition: Types of deal and PEs - Deal Sourcing - Initial

The ESOP Association California Western States Annual Conference October 3-5, 2018

The ESOP Association California Western States Annual Conference October 3-5, 2018 Valuation Basics Presented By Josh Edwards Managing Director Eureka Valuation Advisors (949) 719-2270 josh.edwards@eurekacap.com

The ESOP Association California Western States Annual Conference October 3-5, 2018 Valuation Basics Presented By Josh Edwards Managing Director Eureka Valuation Advisors (949) 719-2270 josh.edwards@eurekacap.com

Buying and selling companies: what Corporate Counsel should understand

Asset Valuations: Buying and selling companies: what Corporate Counsel should understand Yves Heijmans, Lead European Counsel, Chevron Phillips Chemicals Int NV Alessandro Macri, Legal Counsel, GMAC Financial

Asset Valuations: Buying and selling companies: what Corporate Counsel should understand Yves Heijmans, Lead European Counsel, Chevron Phillips Chemicals Int NV Alessandro Macri, Legal Counsel, GMAC Financial

IMPORTANT INFORMATION: This study guide contains important information about your module.

217 University of South Africa All rights reserved Printed and published by the University of South Africa Muckleneuk, Pretoria INV371/1/218 758224 IMPORTANT INFORMATION: This study guide contains important

217 University of South Africa All rights reserved Printed and published by the University of South Africa Muckleneuk, Pretoria INV371/1/218 758224 IMPORTANT INFORMATION: This study guide contains important

Rev. Rul , C.B. 237

Rev. Rul. 59-60, 1959-1 C.B. 237 Amplified by Rev. Rul. 83-120. Amplified by Rev. Rul. 80-213. Amplified by Rev. Rul. 77-287. 26 CFR 20.2031-2: Valuation of stocks and bonds. (Also Section 2512.) (Also

Rev. Rul. 59-60, 1959-1 C.B. 237 Amplified by Rev. Rul. 83-120. Amplified by Rev. Rul. 80-213. Amplified by Rev. Rul. 77-287. 26 CFR 20.2031-2: Valuation of stocks and bonds. (Also Section 2512.) (Also

ABV Examination Content Specification Outline

ABV Examination Content Specification Outline AICPA ABV Examination Content Specification Outline 1 2017 American Institute of Certified Public Accountants. All rights reserved. AICPA and American Institute

ABV Examination Content Specification Outline AICPA ABV Examination Content Specification Outline 1 2017 American Institute of Certified Public Accountants. All rights reserved. AICPA and American Institute

Introduction This note gives an introduction to the concept of relative valuation using market comparables. Relative valuation is the predominate meth

Saïd Business School teaching notes APRIL 2009 Note on Valuation and Mechanics of LBOs This Note was prepared by Tim Jenkinson and Ruediger Stucke. Tim Jenkinson is Professor of Finance at the Saïd Business

Saïd Business School teaching notes APRIL 2009 Note on Valuation and Mechanics of LBOs This Note was prepared by Tim Jenkinson and Ruediger Stucke. Tim Jenkinson is Professor of Finance at the Saïd Business

ICAI - WIRC. Case Study on Merger / Amalgamation - Taxation, Accounting and Company law. Speaker Amrish Shah, Partner, Transaction Tax

ICAI - WIRC Case Study on Merger / Amalgamation - Taxation, Accounting and Company law Speaker Amrish Shah, Partner, Transaction Tax 19 November 2011 Contents Modes of M&A in India Legislative framework

ICAI - WIRC Case Study on Merger / Amalgamation - Taxation, Accounting and Company law Speaker Amrish Shah, Partner, Transaction Tax 19 November 2011 Contents Modes of M&A in India Legislative framework

THE ABC's OF VALUATION

THE ABC's OF VALUATION VALUATION OF COMPANIES AND THEIR SECURITIES FOR ESOP PURPOSES: METHODS OF VALUATION Prepared for the Annual Conference of the Ohio Employee Ownership Center April 20, 2007 BUSINESS

THE ABC's OF VALUATION VALUATION OF COMPANIES AND THEIR SECURITIES FOR ESOP PURPOSES: METHODS OF VALUATION Prepared for the Annual Conference of the Ohio Employee Ownership Center April 20, 2007 BUSINESS

Bombay Chartered Accountants Society

Bombay Chartered Accountants Society Recent developments in taxation of capital gains Pinakin Desai Index Notional taxation w.r.t. FMV of unlisted equity shares (Section 50CA) Valuation of shares under

Bombay Chartered Accountants Society Recent developments in taxation of capital gains Pinakin Desai Index Notional taxation w.r.t. FMV of unlisted equity shares (Section 50CA) Valuation of shares under

FEMA Key aspect under FEMA Outbound investment. CA. M. Jagannathan WIRC presentation 22 nd September, 2018

FEMA Key aspect under FEMA Outbound investment CA. M. Jagannathan WIRC presentation 22 nd September, 2018 Why Outbound Investment? Promoting Global Business by Indian entrepreneurs Joint Ventures are medium

FEMA Key aspect under FEMA Outbound investment CA. M. Jagannathan WIRC presentation 22 nd September, 2018 Why Outbound Investment? Promoting Global Business by Indian entrepreneurs Joint Ventures are medium

Checklist 8.28: Revenue Ruling 59-60

Financial Valuation Workbook: Step-by-Step Exercises and Tests to Help You Master Financial Valuation, Third Edition By James R. Hitchner and Michael J. Mard Copyright 2011 by James R. Hitchner and Michael

Financial Valuation Workbook: Step-by-Step Exercises and Tests to Help You Master Financial Valuation, Third Edition By James R. Hitchner and Michael J. Mard Copyright 2011 by James R. Hitchner and Michael

Valuation of Businesses

Convenience translation from German into English Professional Guidelines of the Expert Committee on Business Administration of the Institute for Business Economics, Tax Law and Organization of the Austrian

Convenience translation from German into English Professional Guidelines of the Expert Committee on Business Administration of the Institute for Business Economics, Tax Law and Organization of the Austrian

OFFICE OF CAREER SERVICES INTERVIEWS FINANCIAL MODELING

OFFICE OF CAREER SERVICES INTERVIEWS FINANCIAL MODELING Basic valuation concepts are among the most popular technical tasks you will be asked to discuss in investment banking and other finance interviews.

OFFICE OF CAREER SERVICES INTERVIEWS FINANCIAL MODELING Basic valuation concepts are among the most popular technical tasks you will be asked to discuss in investment banking and other finance interviews.

ESOPS 16.1 Meaning Grant Vesting Period Option Trust

16.1 Meaning Employee Stock Option Plans or ESOPs are increasingly being accepted as a reward for Employee Productivity. Earlier, the use of ESOPs was restricted to knowledge-based companies only but now

16.1 Meaning Employee Stock Option Plans or ESOPs are increasingly being accepted as a reward for Employee Productivity. Earlier, the use of ESOPs was restricted to knowledge-based companies only but now

CTC New Delhi. Outbound Investments. FEMA Overview. CA. Amithraj AN. June 7,

Outbound Investments FEMA Overview + 91 98861 20086 amithraj123@gmail.com June 7, 2014 Contents FEMA Regulations Round Tripping Overview of Indian Tax Concepts Options for Investing 2 Section 1 FEMA Regulations

Outbound Investments FEMA Overview + 91 98861 20086 amithraj123@gmail.com June 7, 2014 Contents FEMA Regulations Round Tripping Overview of Indian Tax Concepts Options for Investing 2 Section 1 FEMA Regulations

Methods and procedures for company valuations in practice

Methods and procedures for company valuations in practice Methods and procedures for company valuation in practice The valuation of a company is an extremely challenging task. The following article gives

Methods and procedures for company valuations in practice Methods and procedures for company valuation in practice The valuation of a company is an extremely challenging task. The following article gives

Global ABV Examination

Accredited in Business Valuation Global ABV Examination content specification outline Effective Aug. 1, 2018 i Valuation Principles Examination This document is nonauthoritative and is included for informational

Accredited in Business Valuation Global ABV Examination content specification outline Effective Aug. 1, 2018 i Valuation Principles Examination This document is nonauthoritative and is included for informational

Valuation Methodologies An overview of the four most commonly used business valuation methodologies

An overview of the four most commonly used business valuation methodologies A complete business valuation often provides an objective starting point for both buyers and sellers of businesses. Without a

An overview of the four most commonly used business valuation methodologies A complete business valuation often provides an objective starting point for both buyers and sellers of businesses. Without a

Financial Analyst Training Programme 10 Days

Financial Analyst Training Programme 10 Days Delegate Profile: This course is targeted at delegates who are new to banking and finance and provides a comprehensive overview of financial reporting, financial

Financial Analyst Training Programme 10 Days Delegate Profile: This course is targeted at delegates who are new to banking and finance and provides a comprehensive overview of financial reporting, financial

WHITE PAPER: ALTERNATIVE INVESTMENT FUNDS

WHITE PAPER: ALTERNATIVE INVESTMENT FUNDS BIRD S EYE VIEW As on March 31, 2016, 209 Alternative s (AIF) have been registered with SEBI 1 with many more in the pipeline. The cumulative investments by the

WHITE PAPER: ALTERNATIVE INVESTMENT FUNDS BIRD S EYE VIEW As on March 31, 2016, 209 Alternative s (AIF) have been registered with SEBI 1 with many more in the pipeline. The cumulative investments by the

CHAPTER VII PREFERENTIAL ISSUE

CHAPTER VII PREFERENTIAL ISSUE Chapter VII not to apply in certain cases. 70. (1) The provisions of this Chapter shall not apply where the preferential issue of equity shares is made: (a) pursuant to conversion

CHAPTER VII PREFERENTIAL ISSUE Chapter VII not to apply in certain cases. 70. (1) The provisions of this Chapter shall not apply where the preferential issue of equity shares is made: (a) pursuant to conversion

Business/Share Valuation Methodologies, Tools & Techniques

Business/Share Valuation Methodologies, Tools & Techniques CA. Ashish Makhija B.Com (Hons.), LLB, MICA, AICWA, FCA Corporate Lawyer, Advisor & Strategist E-mail: ashish@amclawfirm.com Everything that can

Business/Share Valuation Methodologies, Tools & Techniques CA. Ashish Makhija B.Com (Hons.), LLB, MICA, AICWA, FCA Corporate Lawyer, Advisor & Strategist E-mail: ashish@amclawfirm.com Everything that can

Motives and Innovative ways of Structuring and Accounting for Business combination

Motives and Innovative ways of Structuring and Accounting for Business combination Presenter: Amrish Shah January 20, 2017 *Intended for general guidance only Content Modes of M&A in India Indian laws

Motives and Innovative ways of Structuring and Accounting for Business combination Presenter: Amrish Shah January 20, 2017 *Intended for general guidance only Content Modes of M&A in India Indian laws

Regulatory Provisions for ESOPs. -CA Jalaj Sinha. Copyright K P Corporate Solutions Ltd.

Regulatory Provisions for ESOPs -CA Jalaj Sinha Synopsis Provisions of Companies Act,1956 SEBI ESOP Guidelines,1999 Provisions in FEMA Provisions relating to Sweat Equity Shares Provisions of Companies

Regulatory Provisions for ESOPs -CA Jalaj Sinha Synopsis Provisions of Companies Act,1956 SEBI ESOP Guidelines,1999 Provisions in FEMA Provisions relating to Sweat Equity Shares Provisions of Companies

Case studies - Valuations

Case studies - Valuations CA Kushagra Ladha 18 November 2017 Disclaimer: The discussion in this document is purely for academic purposes and hence the table/text/figures represent only illustrative examples.

Case studies - Valuations CA Kushagra Ladha 18 November 2017 Disclaimer: The discussion in this document is purely for academic purposes and hence the table/text/figures represent only illustrative examples.

January 20, for. Acme Distribution. Prepared for: Tim Mills. Prepared by: Tom MacPherson

CALCULATION OF VALUE January 20, 2016 for Acme Distribution 182 First Avenue, Charlotte, NC Prepared for: Tim Mills Prepared by: Tom MacPherson Summit Acquisitions Group, LLC 4200 Settler Heights Drive,

CALCULATION OF VALUE January 20, 2016 for Acme Distribution 182 First Avenue, Charlotte, NC Prepared for: Tim Mills Prepared by: Tom MacPherson Summit Acquisitions Group, LLC 4200 Settler Heights Drive,

Quarterly technical updates. April 2017

Agenda 1 Opening Remarks 2 Regulatory updates 3 Ind AS 4 Q & A 2 1. Opening Remarks 3 2. Regulatory updates 4 Integrated reporting in India SEBI reporting requirement for top 500 companies (by market cap.)

Agenda 1 Opening Remarks 2 Regulatory updates 3 Ind AS 4 Q & A 2 1. Opening Remarks 3 2. Regulatory updates 4 Integrated reporting in India SEBI reporting requirement for top 500 companies (by market cap.)

CTC New Delhi. Corporate Restructuring M&A. Tax & Regulatory Aspects. CA. Amithraj AN. September 17,

New Delhi Corporate Restructuring M&A Tax & Regulatory Aspects + 91 98861 20086 amithraj123@gmail.com September 17, 2016 Contents Overview Business vs. Share Acquisition Transfer of Shares Slump Sale &

New Delhi Corporate Restructuring M&A Tax & Regulatory Aspects + 91 98861 20086 amithraj123@gmail.com September 17, 2016 Contents Overview Business vs. Share Acquisition Transfer of Shares Slump Sale &

Business Reorganisation and Issues

Business Reorganisation and Issues Arun Saripalli Rachesh Kotak Presentation Outline Introduction and Relevance Rationale for restructuring and concerns Expanded definition of international transactions

Business Reorganisation and Issues Arun Saripalli Rachesh Kotak Presentation Outline Introduction and Relevance Rationale for restructuring and concerns Expanded definition of international transactions

NACVA National Association of Certified Valuation Analysts. Professional Standards

NACVA National Association of Certified Valuation Analysts Professional Standards These Professional Standards are effective for engagements accepted on or after January 1, 2008 NACVA PROFESSIONAL STANDARDS

NACVA National Association of Certified Valuation Analysts Professional Standards These Professional Standards are effective for engagements accepted on or after January 1, 2008 NACVA PROFESSIONAL STANDARDS

Questions for Respondents

Questions for Respondents The International Valuation Professional Board invites responses to the following questions. Not all questions need to be answered but to assist analysis of responses received

Questions for Respondents The International Valuation Professional Board invites responses to the following questions. Not all questions need to be answered but to assist analysis of responses received

STRIVE FOR BALANCE BETWEEN GROWTH AND STABILITY.

MAGNUM BALANCED FUND An Open-ended Balanced Scheme STRIVE FOR BALANCE BETWEEN GROWTH AND STABILITY. Invest in a mix of equity and debt with SBI Magnum Balanced. BALANCED FUNDS A Balanced aims to balance

MAGNUM BALANCED FUND An Open-ended Balanced Scheme STRIVE FOR BALANCE BETWEEN GROWTH AND STABILITY. Invest in a mix of equity and debt with SBI Magnum Balanced. BALANCED FUNDS A Balanced aims to balance

M&A IN INDIA LEGAL CHALLENGES. Somasekhar Sundaresan. Mumbai June 28, J. Sagar Associates. New Delhi Mumbai Bangalore Hyderabad

M&A IN INDIA LEGAL CHALLENGES Somasekhar Sundaresan Mumbai June 28, 2007 J. Sagar Associates New Delhi Mumbai Bangalore Hyderabad 1 INDIAN M&A ENVIRONMENT Cross-border deals outsize domestic M&A Foreign

M&A IN INDIA LEGAL CHALLENGES Somasekhar Sundaresan Mumbai June 28, 2007 J. Sagar Associates New Delhi Mumbai Bangalore Hyderabad 1 INDIAN M&A ENVIRONMENT Cross-border deals outsize domestic M&A Foreign

An Introduction to Business Valuation. By Garth M. Tebay, CPA, CVA, CM&AA

An Introduction to Business Valuation By Garth M. Tebay, CPA, CVA, CM&AA Welcome to the challenging world of business valuation. The key to success in this arena is knowledge. When valuing a closely held

An Introduction to Business Valuation By Garth M. Tebay, CPA, CVA, CM&AA Welcome to the challenging world of business valuation. The key to success in this arena is knowledge. When valuing a closely held

Guide to Financial Management Course Number: 6431

Guide to Financial Management Course Number: 6431 Test Questions: 1. Objectives of managerial finance do not include: A. Employee profits. B. Stockholders wealth maximization. C. Profit maximization. D.

Guide to Financial Management Course Number: 6431 Test Questions: 1. Objectives of managerial finance do not include: A. Employee profits. B. Stockholders wealth maximization. C. Profit maximization. D.

Answer to MTP_ Final _Syllabus 2012_ December 2016_Set 1. Paper 20 - Financial Analysis and Business Valuation

Paper 20 - Financial Analysis and Business Valuation Page 1 Paper 20 - Financial Analysis and Business Valuation Time Allowed: 3 Hours Full Marks: 100 Question No. 1 which is compulsory and carries 20

Paper 20 - Financial Analysis and Business Valuation Page 1 Paper 20 - Financial Analysis and Business Valuation Time Allowed: 3 Hours Full Marks: 100 Question No. 1 which is compulsory and carries 20

Glossary of Business Valuation Terms

Adjusted Net Assets Method Asset-Based Approach Beta Blockage Discount Business Business Risk Business Valuation Capital Asset Pricing Model (CAPM) Capitalization Capitalization of Earnings Method Capital

Adjusted Net Assets Method Asset-Based Approach Beta Blockage Discount Business Business Risk Business Valuation Capital Asset Pricing Model (CAPM) Capitalization Capitalization of Earnings Method Capital

PRESENTATION BY: April 10, Wadia Ghandy & Co., Mumbai 1

PRESENTATION BY: April 10, 2014 Wadia Ghandy & Co., Mumbai 1 Legal Overview Legislations et al Foreign Exchange Management Act, 2000 and Notifications issued thereunder. Securities Contract Regulation

PRESENTATION BY: April 10, 2014 Wadia Ghandy & Co., Mumbai 1 Legal Overview Legislations et al Foreign Exchange Management Act, 2000 and Notifications issued thereunder. Securities Contract Regulation

Transactional Valuation - M&A / Private Equity August 2011

www.pwc.com Transactional Valuation - M&A / Private Equity Agenda Valuation for Mergers and Acquisition Valuation for PE Valuation for Demergers Slide 2 Valuation for Mergers and Acquisitions Understanding

www.pwc.com Transactional Valuation - M&A / Private Equity Agenda Valuation for Mergers and Acquisition Valuation for PE Valuation for Demergers Slide 2 Valuation for Mergers and Acquisitions Understanding

Market vs Intrinsic Value

Market vs Intrinsic Value Market Value Determined by the consensus of market participants Observed in the market Intrinsic value Present value of expected future cash flows Not observed Estimated using

Market vs Intrinsic Value Market Value Determined by the consensus of market participants Observed in the market Intrinsic value Present value of expected future cash flows Not observed Estimated using

Business Reorganisation and Issues

Business Reorganisation and Issues 1 Sanjay Tolia Presentation Outline Introduction and Relevance Expanded definition of international transactions Rationale for restructuring and concerns Subscription

Business Reorganisation and Issues 1 Sanjay Tolia Presentation Outline Introduction and Relevance Expanded definition of international transactions Rationale for restructuring and concerns Subscription

Math for Lawyers: Valuation Theory and Practice 101. December 8, 2011

Math for Lawyers: Valuation Theory and Practice 101 December 8, 2011 Agenda Introduction Presentation Questions and Answers (anonymous) Slides now available on front page of Securities Docket www.securitiesdocket.com

Math for Lawyers: Valuation Theory and Practice 101 December 8, 2011 Agenda Introduction Presentation Questions and Answers (anonymous) Slides now available on front page of Securities Docket www.securitiesdocket.com

Ind AS impact. Financial statements to undergo changes, but no major rating or criteria changes foreseen since fundamentals remain the same

Ind AS impact Financial statements to undergo changes, but no major rating or criteria changes foreseen since fundamentals remain the same August 2016 Table of contents Executive summary... 3 Background...

Ind AS impact Financial statements to undergo changes, but no major rating or criteria changes foreseen since fundamentals remain the same August 2016 Table of contents Executive summary... 3 Background...

Growth Finance Expertise. Transfer of Family Business. Business Banking

Growth Finance Expertise Transfer of Family Business Business Banking 1 Business Banking Family businesses are the keystone of the Irish economy, notable family firms include the Musgrave Group, in family

Growth Finance Expertise Transfer of Family Business Business Banking 1 Business Banking Family businesses are the keystone of the Irish economy, notable family firms include the Musgrave Group, in family

Business Valuation Methodology Survey 2017

Business Valuation Methodology Survey 2017 September 2017 Privileged For limited circulation Contents Foreword 03 Executive summary 04 Detailed survey results 05 The survey report focuses on business valuation

Business Valuation Methodology Survey 2017 September 2017 Privileged For limited circulation Contents Foreword 03 Executive summary 04 Detailed survey results 05 The survey report focuses on business valuation

Value Enhancement: Back to Basics. Aswath Damodaran

Value Enhancement: Back to Basics 86 Price Enhancement versus Value Enhancement 87 The Paths to Value Creation Using the DCF framework, there are four basic ways in which the value of a firm can be enhanced:

Value Enhancement: Back to Basics 86 Price Enhancement versus Value Enhancement 87 The Paths to Value Creation Using the DCF framework, there are four basic ways in which the value of a firm can be enhanced:

CIS March 2012 Exam Diet

CIS March 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Level 2 Corporate Finance (1 13) 1. Which of the following statements

CIS March 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Level 2 Corporate Finance (1 13) 1. Which of the following statements

New Platform for SMEs in India to Provide a Tax Efficient Exit for Investors

Real Estate Laws Foreign entities cannot engage in real estate business in India. The only permissible transaction involving real estate is where the non-resident party carries out development of a minimum

Real Estate Laws Foreign entities cannot engage in real estate business in India. The only permissible transaction involving real estate is where the non-resident party carries out development of a minimum

VALUING YOUR BUSINESS

VALUING YOUR BUSINESS Valuing Your Business There are many reasons why you may need to calculate the value of your business. Here we consider the range of methods available as well as some of the factors

VALUING YOUR BUSINESS Valuing Your Business There are many reasons why you may need to calculate the value of your business. Here we consider the range of methods available as well as some of the factors

TVG Business Valuation

T V G The Vant Group Mergers & Acquisitions TVG Business Valuation ABC Company 17766 Preston Rd Dallas, TX 75252 Tel 972.458.8989 Fax 972.458.7342 email: info@thevantgroup.com website: www.thevantgroup.com

T V G The Vant Group Mergers & Acquisitions TVG Business Valuation ABC Company 17766 Preston Rd Dallas, TX 75252 Tel 972.458.8989 Fax 972.458.7342 email: info@thevantgroup.com website: www.thevantgroup.com

Accountant s Guide to Financial Management - Final Exam 100 Questions 1. Objectives of managerial finance do not include:

Accountant s Guide to Financial Management - Final Exam 100 Questions 1. Objectives of managerial finance do not include: Employee profits B. Stockholders wealth maximization Profit maximization Social

Accountant s Guide to Financial Management - Final Exam 100 Questions 1. Objectives of managerial finance do not include: Employee profits B. Stockholders wealth maximization Profit maximization Social

Jubilant First Trust Healthcare Limited Balance Sheet as at 31 March 2016

Balance Sheet as at 31 March 2016 (Rs. '000) Note As at 31 March 2016 As at 31 March 2015 EQUITY AND LIABILITIES Shareholder's funds Share capital 2 20,500 156,132 Reserves and surplus 3 46,622 581,899

Balance Sheet as at 31 March 2016 (Rs. '000) Note As at 31 March 2016 As at 31 March 2015 EQUITY AND LIABILITIES Shareholder's funds Share capital 2 20,500 156,132 Reserves and surplus 3 46,622 581,899

DIPLOMA COURSE IN BUSINESS VALUATION

DIPLOMA COURSE IN BUSINESS VALUATION Course Objective: Valuation, particularly financial valuation, is emerging as an important profession, with the growth in the profession of financial analysts, increased

DIPLOMA COURSE IN BUSINESS VALUATION Course Objective: Valuation, particularly financial valuation, is emerging as an important profession, with the growth in the profession of financial analysts, increased

Deloitte s recommendations on Income Computation & Disclosure Standards In response to CBDT press release dated 26th November, 2015

Deloitte s recommendations on Income Computation & Disclosure Standards In response to CBDT press release dated 26th November, 2015 December 2015 Contents 1. Background... Error! Bookmark not defined.

Deloitte s recommendations on Income Computation & Disclosure Standards In response to CBDT press release dated 26th November, 2015 December 2015 Contents 1. Background... Error! Bookmark not defined.

Working notes should form part of the answer.

PAPER 2 : STRATEGIC FINANCIAL MANAGEMENT Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Wherever necessary suitable assumptions

PAPER 2 : STRATEGIC FINANCIAL MANAGEMENT Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Wherever necessary suitable assumptions

CA - FINAL SECURITY VALUATION. FCA, CFA L3 Candidate

CA - FINAL SECURITY VALUATION FCA, CFA L3 Candidate 2.1 Security Valuation Study Session 2 LOS 1 : Introduction Note: Total Earnings mean Earnings available to equity share holders Income Statement

CA - FINAL SECURITY VALUATION FCA, CFA L3 Candidate 2.1 Security Valuation Study Session 2 LOS 1 : Introduction Note: Total Earnings mean Earnings available to equity share holders Income Statement

Comments on exposure draft technical information paper 1: The Discounted Cashflow Method with Property and Business Valuations

29 April 2011 International Valuations Standards Council Moorgate London DC2R 6PP United Kingdom Email: ivsc@ivsc.org Dear Sirs, Comments on exposure draft technical information paper 1: The Discounted

29 April 2011 International Valuations Standards Council Moorgate London DC2R 6PP United Kingdom Email: ivsc@ivsc.org Dear Sirs, Comments on exposure draft technical information paper 1: The Discounted

Valuation of Intangible Assets including. Purchase Price Allocation :74. Purchase Price Allocation

CA Ravishu Shah Valuation of Intangible Assets including Purchase Price Allocation Investment in knowledge based/intangible assets is one of the key characteristics of modern economies. Every goods including

CA Ravishu Shah Valuation of Intangible Assets including Purchase Price Allocation Investment in knowledge based/intangible assets is one of the key characteristics of modern economies. Every goods including

STAY-IN-INDIA CHECKLIST MCA

STAY-IN-INDIA CHECKLIST MCA 1. Grant of ESOPs to Promoters and Independen t Directors The provisions of the Companies Act do not permit to grant ESOPs to promoters or members of the promoter group or independent

STAY-IN-INDIA CHECKLIST MCA 1. Grant of ESOPs to Promoters and Independen t Directors The provisions of the Companies Act do not permit to grant ESOPs to promoters or members of the promoter group or independent

Understanding Financial Statements and Their Effects on Enhancing Value

Understanding Financial Statements and Their Effects on Enhancing Value 2017 California/Western States Chapter Conference Todd Poling, Vantage Point Advisors Josh Edwards, Eureka Valuation Advisors Main

Understanding Financial Statements and Their Effects on Enhancing Value 2017 California/Western States Chapter Conference Todd Poling, Vantage Point Advisors Josh Edwards, Eureka Valuation Advisors Main

Finance and Accounting for Interviews

This document was developed and written by Ian Lee. All information is meant for public use and purposed for the free transfer of knowledge to interested parties. Send questions and comments to ianlee@uclalumni.net

This document was developed and written by Ian Lee. All information is meant for public use and purposed for the free transfer of knowledge to interested parties. Send questions and comments to ianlee@uclalumni.net

Growth Finance Expertise. Mergers & Acquisitions. Business Banking

Growth Finance Expertise Mergers & Acquisitions 1 Introduction Irish businesses, such as Version 1 in technology and Glanbia in agrifoods, have shown that a well-executed Mergers and Acquisitions (M&A)

Growth Finance Expertise Mergers & Acquisitions 1 Introduction Irish businesses, such as Version 1 in technology and Glanbia in agrifoods, have shown that a well-executed Mergers and Acquisitions (M&A)

CORPORATE VALUATION METHODOLOGIES

CORPORATE VALUATION METHODOLOGIES What is the business worth? Although a simple question, determining the value of any business in today s economy requires a sophisticated understanding of financial analysis

CORPORATE VALUATION METHODOLOGIES What is the business worth? Although a simple question, determining the value of any business in today s economy requires a sophisticated understanding of financial analysis

ACCOUNTING & TAXATION ISSUES RELATING TO CAPITAL MARKET TRANSACTIONS CAPITAL MARKET TRANSACTIONS

ACCOUNTING & TAXATION ISSUES RELATING TO CAPITAL MARKET TRANSACTIONS CAPITAL MARKET TRANSACTIONS CASH MARKET DERIVATIVE MARKET DELIVERY DAILY JOBBING FUTURE OPTIONS BASED (NO DELIVERY) INDEX STOCKS INDEX

ACCOUNTING & TAXATION ISSUES RELATING TO CAPITAL MARKET TRANSACTIONS CAPITAL MARKET TRANSACTIONS CASH MARKET DERIVATIVE MARKET DELIVERY DAILY JOBBING FUTURE OPTIONS BASED (NO DELIVERY) INDEX STOCKS INDEX

TD Bank Financial Group Delivers Very Strong Second Quarter 2007 Earnings

TD B A NK FINANCIAL G ROUP SECOND QUART ER 2007 R EPORT TO SHAR EHOLD ERS Page 1 2 nd Quarter 2007 Report to Shareholders Three and six months ended April 30, 2007 TD Bank Financial Group Delivers Very

TD B A NK FINANCIAL G ROUP SECOND QUART ER 2007 R EPORT TO SHAR EHOLD ERS Page 1 2 nd Quarter 2007 Report to Shareholders Three and six months ended April 30, 2007 TD Bank Financial Group Delivers Very

Financial Reporting for Financial Institutions

CHAPTER 8 Financial Reporting for Financial Institutions BASIC CONCEPTS MUTUAL FUNDS In India, mutual funds are regulated by SEBI (Mutual Funds) Regulations, 1996. According to the SEBI (Mutual Funds)

CHAPTER 8 Financial Reporting for Financial Institutions BASIC CONCEPTS MUTUAL FUNDS In India, mutual funds are regulated by SEBI (Mutual Funds) Regulations, 1996. According to the SEBI (Mutual Funds)

CERTIFICATE COURSE ON FOREIGN EXCHANGE & TREASURY MANAGEMENT

CERTIFICATE COURSE ON FOREIGN EXCHANGE & TREASURY MANAGEMENT The Certificate Course is an advanced course on Treasury Management (including Forex Treasury) for Chartered Accountants organized by Committee

CERTIFICATE COURSE ON FOREIGN EXCHANGE & TREASURY MANAGEMENT The Certificate Course is an advanced course on Treasury Management (including Forex Treasury) for Chartered Accountants organized by Committee

A Primer on Valuation

A Primer on Valuation Introduction Ambitious companies which have plenty of cash look at acquisitions as a way to accelerate growth. What makes a deal attractive to the acquiring company? We do not need

A Primer on Valuation Introduction Ambitious companies which have plenty of cash look at acquisitions as a way to accelerate growth. What makes a deal attractive to the acquiring company? We do not need

COPYRIGHTED MATERIAL. Chapter 1 Comparable Companies Analysis. Chapter 1 Comparable Companies Analysis 1.

Chapter 1 Comparable Companies Analysis Chapter 1 Comparable Companies Analysis 1 COPYRIGHTED MATERIAL Comparable Companies Analysis Steps Step I. Select the Universe of Comparable Companies Step II. Locate

Chapter 1 Comparable Companies Analysis Chapter 1 Comparable Companies Analysis 1 COPYRIGHTED MATERIAL Comparable Companies Analysis Steps Step I. Select the Universe of Comparable Companies Step II. Locate