Due Diligence, Legal and Regulatory Valuation aspects

|

|

|

- Mabel Cobb

- 6 years ago

- Views:

Transcription

1 In the business world, the rearview mirror is always clearer than the windshield Warren Buffett Due Diligence, Legal and Regulatory Valuation aspects 01/07/2015 FEMA Valuation Aspect (FDI & ODI)

2 Particulars FEMA Valuation Guidelines Tricky Issues

3 FEMA Valuation Guidelines

Regulations, 2000.")

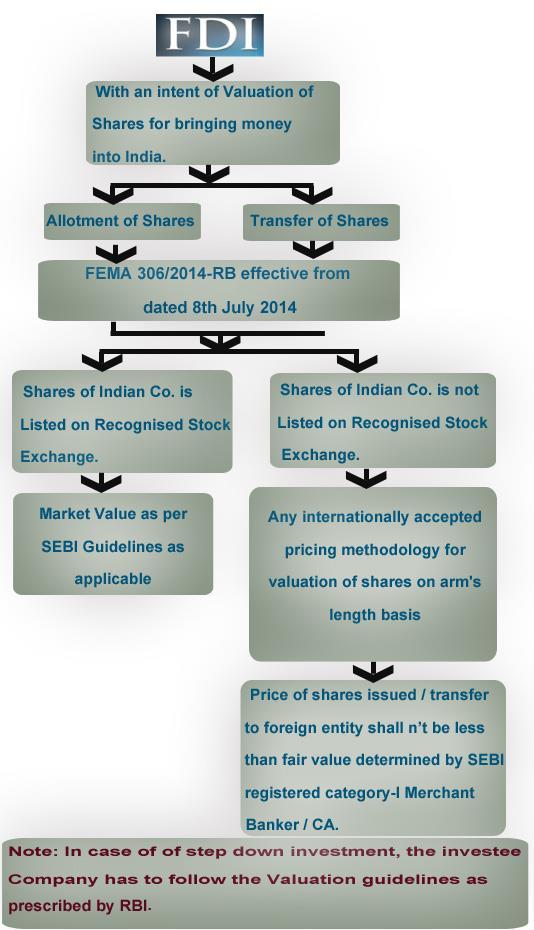

4 FDI VALUATION Notification No. FEMA 20/2000-RB dated May 3, 2000, as amended from time to time deals with Foreign Exchange Management (Transfer or Issue of Security by a Person Resident Outside India) Regulations, In terms of Schedule 1 of the Notification, an Indian company may issue equity shares/compulsorily convertible preference shares and compulsorily convertible debentures (equity instruments) to a person resident outside India under the FDI policy, subject to inter alia, compliance with the pricing guidelines. The price/ conversion formula of convertible capital instruments should be determined upfront at the time of issue of the instruments.

5

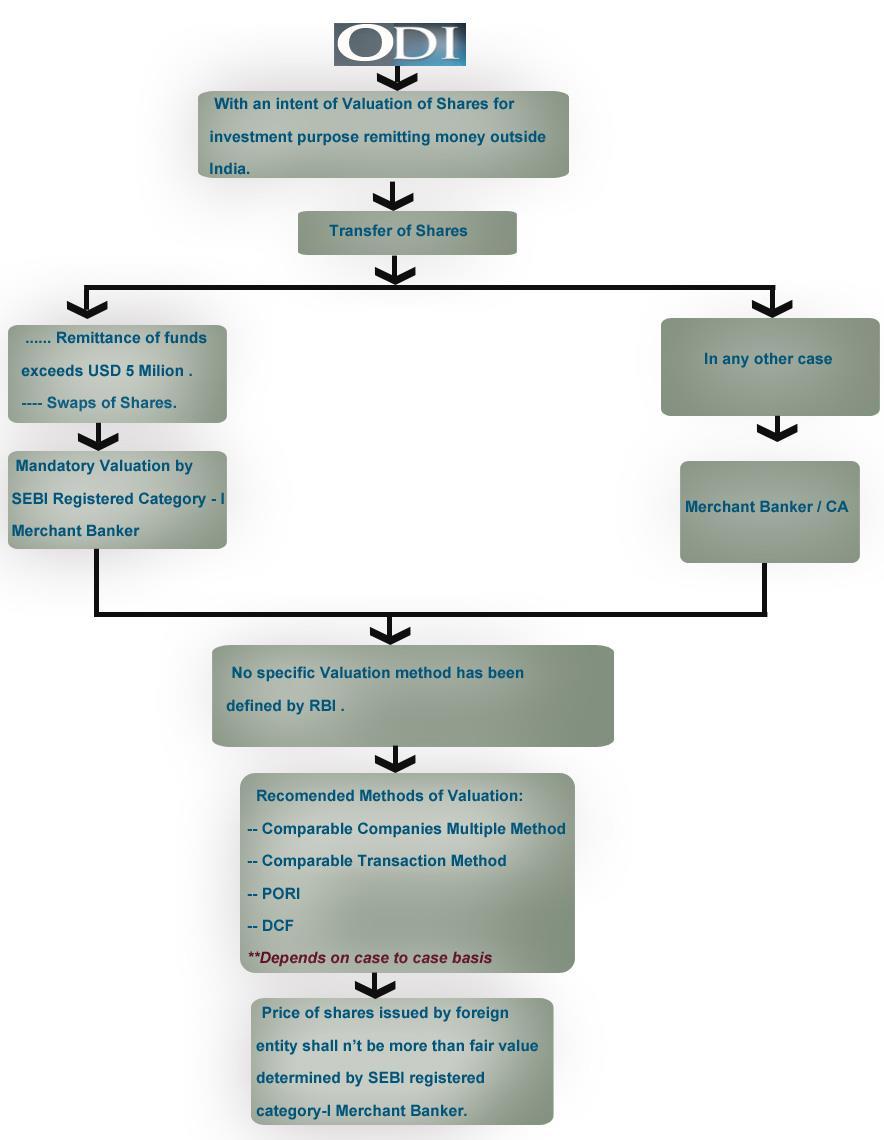

6 FEMA Guidelines to Valuation Particulars Guidelines in Force Methods Prescribed Valuation before April 21, 2010 CCI Guidelines Net Assets Value (NAV) Profit Earning Capacity Value(PECV) Market Value (in case of Listed Company) Valuation before April 1, 2014 In case of FDI Transactions: Listed Company: Market Value as per SEBI Preferential Allotment Guidelines Unlisted Company: DFCF In case of ODI Transactions: No method has been prescribed Valuation after 8 th July 2014 * In case of FDI Transactions: Listed Company: Market Value as per SEBI Guidelines as applicable Unlisted Company: Any international accepted pricing methodology for valuation of shares on arm's length basis In case of ODI Transactions: No method has been prescribed Discount 15% Discount has been prescribed on account of Lack of Marketability No such Discount has been prescribed No such Discount has been prescribed Historical / Futuristic It is based on Historical Values It is based on Future Projections Depends upon method being used Possibility of variation in Value Conclusion As valuation is more Formulae based, final values came standardized As valuation is more dependent on Assumptions and choice of factors like Growth Rate, Cost of Capital etc, value conclusion may vary significantly. In the absence of specified method to follow, any preconception or bias of the valuer gets reflected in the value.

7 FEMA Guidelines to Valuation * Now, RBI vide Notification No. FEMA 306/2014-RB effective from dated 8 th July 2014 has notified the pricing guidelines in case of Transfer or Issue of Security by a Person Resident Outside India as regards Foreign Direct Investment (FDI), which until a few months back RBI through its monitory policy dated 1 st April, 2014 has decided to withdraw all the existing FDI Valuation guidelines relating to valuation in case of any acquisition / sale of shares, accordingly, such transactions since then based on acceptable market practices. Further non-resident investor is not guaranteed any assured exit price at the time of making such investment/agreements and shall exit at the fair price computed as any internationally accepted pricing methodology for valuation of shares on arm's length basis, duly certified by a Chartered Accountant or a SEBI registered Merchant Banker.

8 Discounted Free Cash Flow Method (DFCF) DFCF expresses the present value of the business as a function of its future cash earnings capacity. In this method, the appraiser estimates the cash flows of any business after all operating expenses, taxes, and necessary investments in working capital and capital expenditure is being met. Valuing equity using the free cash flow to stockholders requires estimating only free cash flow to equity holders, after debt holders have been paid off.

9 Major Characteristics of DFCF Valuation Forward Looking and focuses on cash generation Recognizes Time value of Money Allows operating strategy to be built into a model Incorporates value of Tangible and Intangible assets Only as accurate as assumptions and projections used Works best in producing a range of likely values It Represents the Control Value

10 DFCF Valuation Process Understand Business Model Identify Business Cycle Analyze Historical Financial Performance Review Industry and Regulatory Trends Understand Future Growth Plans (including Capex needs) Segregate Business and Other Cash Generating Assets Identify Surplus Assets (assets not utilized for Business say Land/Investments) Create Business Projections (Profitability statement and Balance Sheets) Discount Business Projections to Present (Explicit Period and Perpetuity) Add Value of Surplus Assets and Subtract Value of Contingent Liabilities

11 Free Cash Flows- Value Trend Terminal Value is calculated for the Perpetuity period based on the Adjusted last year cash flows of the Projected period.

12 Free Cash Flow calculation FREE CASH FLOWS Free cash flows to firm (FCFF) is calculated as EBITDA Taxes Change in Non Cash Working capital Capital Expenditure Free Cash Flow to Firm Note that an alternate to above is following (FCFE) method in which the value of Equity is directly valued in lieu of the value of Firm. Under this approach, the Interest and Finance charges is also deducted to arrive at the Free Cash Flows. Adjustment is also made for Debt (Inflows and Outflows) over the definite period of Cash Flows and also in Perpetuity workings. Theoretically, the value conclusion should remain same irrespective of the method followed (FCFF or FCFE), (Provided, assumptions are consistent).

13 Cost of Capital calculation DISCOUNT RATE WEIGHTED AVERAGE COST OF CAPITAL WACC (K d x D) + (K e x E) (D + E) Where: D = Debt part of capital structure E = Equity part of capital structure K d = Cost of Debt (Post tax) K e = Cost of Equity In case of following FCFE, Discount Rate is Ke and Not WACC 01/07/2015 EOK Study Circle - ICAI

14 Cost of Equity calculation DISCOUNT RATE - COST OF EQUITY The Cost of Equity (Ke) is computed by using Modified Capital Asset Pricing Model (Mod. CAPM) Mod. CAPM Model ke = Rf + B ( Rm-Rf) + SCRP + CSRP Where: Rf = Risk free rate of return (Generally taken as 10-year Government Bond Yield) B = Beta Value (Sensitivity of the stock returns to market returns) K e = Cost of Equity Rm= Market Rate of Return (Generally taken as Long Term average return of Stock Market) SCRP = Small Company Risk Premium CSRP= Company specific Risk premium

15 PERPETUITY FORMULA Terminal value calculation Usually comprises a Large part of Total Value and is sensitive to small changes Capitalizes FCF after definite forecast period as a growing perpetuity; Estimate Terminal Value using Terminal Value Multiplier applied on last year cash flows Gordon Formula is often used to derive the Terminal Cash Flows by applying the last year cash flows as a multiple of the growth rate and discounting factor (1 + g) (WACC g) Estimated Terminal Value is then discounted to present day at company s cost of capital based on the discounting factor of last year projected cash flows IMPORTANT TIP- It is advised to do Sanity check by applying Relative Valuation Multiples to the Terminal Year Financials and also doing Scenario Analysis.

16 Tricky issues in DFCF Pre Money or Post Money: If the effect of the money coming in Company is taken in Projections, the Expanded capital base should be considered or else the Equity Value should be reduced by the inflow amount to reconcile with the existing capital base. Terminal growth rate: Since it is tough to estimate the perpetual growth rate of a company, it is preferred to take the perpetuity growth rate factoring in long term estimated GDP of the Country and Historical/Projection Inflation of the Country. Projection Validation via-a-vis Industry: Need to have Sanity check of the projections with the trend of the industry. Beta of Unlisted Company: It is calculated on relative basis by adjusting the average beta of its comparable companies for differences in Capital Structure of the unlisted company with the listed peers. Risk Free Rate: Yield of a Zero Coupon Bond or Long Term government Bond yield should be taken as the risk free rate since it does not have any reinvestment risk.

17 Tricky issues in DFCF (Cont.) Adjustment of Company Specific Risk Premium or Small Company Risk Premium: Small Companies are generally more risky than big companies. CAPM model does not take into consideration the size risk and specific company risk as Beta measures only systematic risk and Market Risk Premium (generally pertaining to Sensex Companies). These risks should also be taken into account while computing the cost of equity. Length of Projections: The Projected Cash Flows should factor in the entire Business Cycle of a Company. Notional/Actual Tax: Actual Tax Liability may be worked out and replaced for the Notional Tax Liability Investments: Investments should be valued separately based on their Independent Cash Flows Surplus Assets: The Value of Surplus Assets (not being utilized for Business purposes) should be added separately and their cash flows should be ignored while computing the Free Cash Flows.

18

19 Some Specific Tricky Issues

20 Discounts Discounts & Premiums come into picture when there exist difference between the subject being valued and the Methodologies applied. As this can translate control value to non-control and vise versa, so these should be judiciously applied. Discount for Entity Level Impact on entity as a whole Key Person Discount Discount for Contingent Liability Discount for diversified company Discount for Holding Company Global Studies over the years on diversified companies and holding companies has shown that companies trade at a discount in the range of 20%. to 40% each. Tax Payout Discount for Shareholders Level Impact on specific ownership interest Discount Lack of Control (DLOC) Discount Lack of Marketability (DLOM) DLOM: As per CCI Guidelines, 15% % stake & special rights discount has been prescribed; however practically DLOM and DLOC depends upon following factors: Size of distribution or dividends Dispute Revenue / Earning Growth / Stability Private Company Shareholders Agreement caveats

21 Premium Control Premium - An investor seeking to acquire control of a company is typically willing to pay more than the current market price of the company. Control premium is an amount that a buyer is usually willing to pay over the fair market value of a publicly traded company to acquire controlling stake in a company Research has shown that the control premium in India has ranged from 20% to 37% in the past few years.

22 Excess Cash and Non Operating Assets Excess cash is defined as total cash (in balance sheet) operating cash (i.e. minimum required cash) to sustain operations (working capital) and manage contingencies Key Issue: Estimation of Excess Cash? One of the solutions is to estimate average cash/sales or total balance sheet size of the company s relevant Industry and then estimate if the company being valued has cash in excess of the industry s average. Non operating Assets are the Surplus assets which are not used in operations of the business and does not reflect its value in the operating earnings of the company. Therefore the fair market value of such Assets should be separately added to the value derived through valuation methodologies to arrive at the value of the company. What is an asset is not yielding adequate returns?

By way of Shareholders Agreement even less % holding may command")

23 Cross Holding and Investments Holdings in other firms can be categorized into: Types of Cross Holding Minority, Passive Investments Minority, Active Investments Majority, Active Investments Meaning If the securities or assets owned in another firm represent less than 20% of the overall ownership of that firm If the securities or assets owned in another firm represent between 20% and 50% of the overall ownership of that firm If the securities or assets owned in another firm represent more than 50% of the overall ownership of that firm Ways to value Cross Holding and Investments: Investment Value Dividend Yield Capitalization or DCF based on expected dividends Separate Valuation (Preferred) By way of Shareholders Agreement even less % holding may command control value

24 Accounting Practices and Tax issues Most of the information that is used in valuation comes from financial statements. which in turn are made on certain Accounting practices considered appropriate. Cash Accounting v/s Accrual Accounting Operating Lease v/s Financial Lease Capitalization of Expenses Notional Tax vs. Actual Tax Treatment of Intangible Assets Companies Paying MAT Treatment of Tax benefits and Losses

25 Valuation Methodologies and Value Impact Major Valuation Methodologies Ideal for Result Net Asset Value Net Asset Value (Book Value) Net Asset Value (Fair Value) Minority Value Control Value Equity Value Comparable Companies Multiples (CCM) Method Price to Earning, Book Value Multiple Minority Value Equity Value EBIT, EBITDA Multiple Enterprise Value Comparable Transaction Multiples (CTM) Method Price to Earning, Book Value Multiple EBIT, EBITDA Multiple Control Value Equity Value Enterprise Value Equity Firm Discounted Cash Flow (DCF) Control Value Equity Value Enterprise Value

26 What we need to do We must Analyze the whole Structure and Systems of the organization and take necessary Actions to Align them with new Legal Environment...

27 Our Valuation Team Mr. Chander Sawhney Partner & Head Valuation & Deals M: D: E: Mr. Maneesh Srivastava AVP Valuation & Biz Modelling M: D: E: Mr. Gaurav Kumar Barick Manager Valuation & Biz Modelling M: D: E: Mr. Sameer Verma Deputy Manager Valuation and Biz Modelling M: D: E:

Due Diligence, Legal and Regulatory Valuation aspects

Due Diligence, Legal and Regulatory Valuation aspects ICSI Certificate Course of Valuation Oct 2013 Chander Sawhney FCA, ACS, Certified Valuer (ICAI) Vice President, Corporate Professionals Contents Particulars

Due Diligence, Legal and Regulatory Valuation aspects ICSI Certificate Course of Valuation Oct 2013 Chander Sawhney FCA, ACS, Certified Valuer (ICAI) Vice President, Corporate Professionals Contents Particulars

RBI guidelines for valuation of shares. FDI Valuation Guidelines

RBI guidelines for valuation of shares For Foreign Direct Investment (FDI) transactions, Notification No. FEMA 20/2000-RB dated May 3, 2000, as amended from time to time deals with Foreign Exchange Management

RBI guidelines for valuation of shares For Foreign Direct Investment (FDI) transactions, Notification No. FEMA 20/2000-RB dated May 3, 2000, as amended from time to time deals with Foreign Exchange Management

An Insight of Valuation

An Insight of Valuation by- www.corporatevaluations.in a venture of SEBI REGISTERED (CAT -I) MERCHANT BANKER Contents Particulars TABLE OF CONTENT Pg. No. Valuation Overview 1 Approaches to Valuation -

An Insight of Valuation by- www.corporatevaluations.in a venture of SEBI REGISTERED (CAT -I) MERCHANT BANKER Contents Particulars TABLE OF CONTENT Pg. No. Valuation Overview 1 Approaches to Valuation -

Relative Valuation. 31 st August 2016 Business Valuation Master class, New Delhi

Relative Valuation 31 st August 2016 Business Valuation Master class, New Delhi Agenda - Overview of Valuation - Principles of Relative Valuation - Why Relative Valuation is more favoured in Application

Relative Valuation 31 st August 2016 Business Valuation Master class, New Delhi Agenda - Overview of Valuation - Principles of Relative Valuation - Why Relative Valuation is more favoured in Application

Valuation of Shares / Business An Overview. CA Shivaprakash Viraktamath 20 th January 2017

Valuation of Shares / Business An Overview CA Shivaprakash Viraktamath 20 th January 2017 1 Contents 1. Why Valuation? 2. Key Factors Influencing Valuation 3. Sources of Information 4. Valuation for Regulatory

Valuation of Shares / Business An Overview CA Shivaprakash Viraktamath 20 th January 2017 1 Contents 1. Why Valuation? 2. Key Factors Influencing Valuation 3. Sources of Information 4. Valuation for Regulatory

ISSUES IN VALUATION UNDER FEMA

ISSUES IN VALUATION UNDER FEMA REGIONAL CONFERENCE OF WIRC CA. SUJAL SHAH AUGUST 31, 2012 1 VALUATION - INTRODUCTION What is Valuation? Valuation means assigning a value to underlying assets The value

ISSUES IN VALUATION UNDER FEMA REGIONAL CONFERENCE OF WIRC CA. SUJAL SHAH AUGUST 31, 2012 1 VALUATION - INTRODUCTION What is Valuation? Valuation means assigning a value to underlying assets The value

The Price is Right. Calculation of Price - Investments

The Price is Right This article attempts to set out the rules for valuation, as prescribed in various regulations, which have an impact on M&A transactions in India. Calculation of Price - Investments

The Price is Right This article attempts to set out the rules for valuation, as prescribed in various regulations, which have an impact on M&A transactions in India. Calculation of Price - Investments

Valuation Techniques BANSI S. MEHTA & CO.

Valuation Techniques USHMA SHAH BANSI S. MEHTA & CO. PRICE is what you pay. VALUE is what you get. They are not the I can make a whole lot more money skilfully managing intangible assets than managing

Valuation Techniques USHMA SHAH BANSI S. MEHTA & CO. PRICE is what you pay. VALUE is what you get. They are not the I can make a whole lot more money skilfully managing intangible assets than managing

One of the major applications of Equity Valuation is the Private companies valuation. Private companies valuation can be applied:

One of the major applications of Equity Valuation is the Private companies valuation. Private companies valuation can be applied: To value a Start up operations of Public companies. To estimate a value

One of the major applications of Equity Valuation is the Private companies valuation. Private companies valuation can be applied: To value a Start up operations of Public companies. To estimate a value

Valuation Overview & Methodologies

Valuation Overview & Methodologies CA Sujal Shah & CA Bhakti Shah 18th November 2017 ICAI Mumbai Seminar on Valuation VALUATION CONCEPTS Value Price Not an Exact science Value varies with Situation Valuation

Valuation Overview & Methodologies CA Sujal Shah & CA Bhakti Shah 18th November 2017 ICAI Mumbai Seminar on Valuation VALUATION CONCEPTS Value Price Not an Exact science Value varies with Situation Valuation

Reporting Aspects Discounted Cash Flow (DCF) Valuation. CA Shirish S. Rahalkar

Valuation. CA Shirish S. Rahalkar") 1 Reporting Aspects Discounted Cash Flow (DCF) Valuation CA Shirish S. Rahalkar The Chartered Accountant Act says, 2 Clause (3) Part I Second Schedule of The Chartered Accountant Act, 1949 states Practising

1 Reporting Aspects Discounted Cash Flow (DCF) Valuation CA Shirish S. Rahalkar The Chartered Accountant Act says, 2 Clause (3) Part I Second Schedule of The Chartered Accountant Act, 1949 states Practising

Valuation of Businesses

Convenience translation from German into English Professional Guidelines of the Expert Committee on Business Administration of the Institute for Business Economics, Tax Law and Organization of the Austrian

Convenience translation from German into English Professional Guidelines of the Expert Committee on Business Administration of the Institute for Business Economics, Tax Law and Organization of the Austrian

CA SUJAL SHAH. 22 nd June 2013

CA SUJAL SHAH 22 nd June 2013 Value Price Valuation-not an exact science, more an art Value varies with situations Date specific Purchase / Sale of Business Merger/ Demerger Private Equity Buyback of Shares

CA SUJAL SHAH 22 nd June 2013 Value Price Valuation-not an exact science, more an art Value varies with situations Date specific Purchase / Sale of Business Merger/ Demerger Private Equity Buyback of Shares

VALUATION UNDER COMPANIES ACT CA MANDAR GADKARI AUGUST 10, 2017

VALUATION UNDER COMPANIES ACT CA MANDAR GADKARI AUGUST 10, 2017 VALUATION Introduction What is Valuation : The process of determining the current worth of an asset or a company Various techniques to determine

VALUATION UNDER COMPANIES ACT CA MANDAR GADKARI AUGUST 10, 2017 VALUATION Introduction What is Valuation : The process of determining the current worth of an asset or a company Various techniques to determine

VALUATION & BIZ MODELLING PROFILE

VALUATION & BIZ MODELLING PROFILE CONTENTS Why Valuation Our process flow Key deliverables of our Valuation Report Our Valuation Credentials Our Valuation Offerings Appendix 1: Valuation Approaches and

VALUATION & BIZ MODELLING PROFILE CONTENTS Why Valuation Our process flow Key deliverables of our Valuation Report Our Valuation Credentials Our Valuation Offerings Appendix 1: Valuation Approaches and

Week 6 Equity Valuation 1

Week 6 Equity Valuation 1 Overview of Valuation The basic assumption of all these valuation models is that the future value of all returns can be discounted back to today s present value. Where t = time

Week 6 Equity Valuation 1 Overview of Valuation The basic assumption of all these valuation models is that the future value of all returns can be discounted back to today s present value. Where t = time

CHAPTER XVII REGISTERED VALUERS Registered Valuer means a person registered as a Valuer under Chapter XVII of the Act.

DRAFT RULES UNDER COMPANIES ACT, 2013 CHAPTER XVII REGISTERED VALUERS Definition 17.1 Registered Valuer means a person registered as a Valuer under Chapter XVII of the Act. Registration as Valuers. 17.2

DRAFT RULES UNDER COMPANIES ACT, 2013 CHAPTER XVII REGISTERED VALUERS Definition 17.1 Registered Valuer means a person registered as a Valuer under Chapter XVII of the Act. Registration as Valuers. 17.2

Valuation. Valuation Methodologies. Agenda. Why Valuation? CA Pratik K. Singhi 02 June 2012 National Workshop on Media & Entertainment. Why Valuation?

Agenda Valuation Why Valuation? Valuation Techniques Intro DCF Methodology: Detail DCF Valuation Finer Points CA Pratik K. Singhi 02 June 2012 National Workshop on Media & Entertainment 1 / June 21, 2007

Agenda Valuation Why Valuation? Valuation Techniques Intro DCF Methodology: Detail DCF Valuation Finer Points CA Pratik K. Singhi 02 June 2012 National Workshop on Media & Entertainment 1 / June 21, 2007

Valuation of Equity Shares. CA Sujal Shah 30th December 2016 WIRC Seminar on Valuation

Valuation of Equity Shares CA Sujal Shah 30th December 2016 WIRC Seminar on Valuation 2 Presentation Overview Valuation Concept Valuation Approaches Selection of Methods Requirements under various laws

Valuation of Equity Shares CA Sujal Shah 30th December 2016 WIRC Seminar on Valuation 2 Presentation Overview Valuation Concept Valuation Approaches Selection of Methods Requirements under various laws

19 NOVEMBER 2011 DRUSHTI DESAI

19 NOVEMBER 2011 DRUSHTI DESAI PRESENTATION OVERVIEW Purpose of Valuation Steps in Valuation Analysis of Company Principal Methods of Valuation Fair Value Other Value Drivers Issues Purchase / Sale of

19 NOVEMBER 2011 DRUSHTI DESAI PRESENTATION OVERVIEW Purpose of Valuation Steps in Valuation Analysis of Company Principal Methods of Valuation Fair Value Other Value Drivers Issues Purchase / Sale of

Introduction to Valuation

Introduction to Valuation Romesh Vijay CA, ICAI Certified Valuer Contents Introduction Overview of Methods Used Case Studies Relative Method of Valuation Introduction Valuer A valuer is a fellow who lends

Introduction to Valuation Romesh Vijay CA, ICAI Certified Valuer Contents Introduction Overview of Methods Used Case Studies Relative Method of Valuation Introduction Valuer A valuer is a fellow who lends

Questions for Respondents

Questions for Respondents The International Valuation Professional Board invites responses to the following questions. Not all questions need to be answered but to assist analysis of responses received

Questions for Respondents The International Valuation Professional Board invites responses to the following questions. Not all questions need to be answered but to assist analysis of responses received

More Corrections and Perpetual Growth Valuation

More Corrections and Perpetual Growth Valuation Valuation and Financial Statement Analysis Peking University Guanghua School of Management April 1, 2019 Lecture 2 Pre-Reading Read McKinsey Valuation pg

More Corrections and Perpetual Growth Valuation Valuation and Financial Statement Analysis Peking University Guanghua School of Management April 1, 2019 Lecture 2 Pre-Reading Read McKinsey Valuation pg

PROFESSIONAL PROGRAMME

1 PROFESSIONAL PROGRAMME UPDATES FOR STRATEGIC MANAGEMENT, ALLIANCES AND INTERNATIONAL TRADE MODULE 3 (Relevant for Students Appearing in June, 2016 Examination) Disclaimer- This document has been prepared

1 PROFESSIONAL PROGRAMME UPDATES FOR STRATEGIC MANAGEMENT, ALLIANCES AND INTERNATIONAL TRADE MODULE 3 (Relevant for Students Appearing in June, 2016 Examination) Disclaimer- This document has been prepared

IMPORTANT INFORMATION: This study guide contains important information about your module.

217 University of South Africa All rights reserved Printed and published by the University of South Africa Muckleneuk, Pretoria INV371/1/218 758224 IMPORTANT INFORMATION: This study guide contains important

217 University of South Africa All rights reserved Printed and published by the University of South Africa Muckleneuk, Pretoria INV371/1/218 758224 IMPORTANT INFORMATION: This study guide contains important

Valuation Methodologies An overview of the four most commonly used business valuation methodologies

An overview of the four most commonly used business valuation methodologies A complete business valuation often provides an objective starting point for both buyers and sellers of businesses. Without a

An overview of the four most commonly used business valuation methodologies A complete business valuation often provides an objective starting point for both buyers and sellers of businesses. Without a

Investment Knowledge Series. Valuation

Investment Knowledge Series Valuation INVESTMENT KNOWLEDGE SERIES Valuation capital city training & consulting www.capitalcitytraining.com i Published 2011 by Capital City Training Ltd ISBN: 978-0-9569238-1-3

Investment Knowledge Series Valuation INVESTMENT KNOWLEDGE SERIES Valuation capital city training & consulting www.capitalcitytraining.com i Published 2011 by Capital City Training Ltd ISBN: 978-0-9569238-1-3

Fundamental Analysis, B7021, Spring 2016

Fundamental Analysis, B7021, Spring 2016 Course Syllabus This draft: October 21, 2015 I. CONTACT DETAILS Prof. Doron Nissim Email: dn75@columbia.edu Office hours (604 Uris): by appointment II. COURSE DESCRIPTION

Fundamental Analysis, B7021, Spring 2016 Course Syllabus This draft: October 21, 2015 I. CONTACT DETAILS Prof. Doron Nissim Email: dn75@columbia.edu Office hours (604 Uris): by appointment II. COURSE DESCRIPTION

Homework and Suggested Example Problems Investment Valuation Damodaran. Lecture 1 Introduction to Valuation

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 1 Introduction to Valuation Lecture 1 is an introduction to valuation. This lecture is intended to give you an overview of

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 1 Introduction to Valuation Lecture 1 is an introduction to valuation. This lecture is intended to give you an overview of

Guide to Financial Management Course Number: 6431

Guide to Financial Management Course Number: 6431 Test Questions: 1. Objectives of managerial finance do not include: A. Employee profits. B. Stockholders wealth maximization. C. Profit maximization. D.

Guide to Financial Management Course Number: 6431 Test Questions: 1. Objectives of managerial finance do not include: A. Employee profits. B. Stockholders wealth maximization. C. Profit maximization. D.

VALUATION IN BUSINESS DIVORCE DISCOUNTED CASH FLOW METHOD AND ITS COMPONENTS

VALUATION IN BUSINESS DIVORCE DISCOUNTED CASH FLOW METHOD AND ITS COMPONENTS ABA BUSINESS DIVORCE COMMITTEE SEPTEMBER 15, 2017 2017 HURON CONSULTING GROUP INC. DISCLAIMER These materials are presented

VALUATION IN BUSINESS DIVORCE DISCOUNTED CASH FLOW METHOD AND ITS COMPONENTS ABA BUSINESS DIVORCE COMMITTEE SEPTEMBER 15, 2017 2017 HURON CONSULTING GROUP INC. DISCLAIMER These materials are presented

ACCRETIVE SDU MONTHLY COMMUNIQUÉ AUGUST Income Tax FEMA India Budget 2014 INCOME TAX

INCOME TAX Taxation of Alternate Investment Funds: The Securities and Exchange Board of India (Alternate Investment Funds) Regulation, 2012 (AIF Regulations) forms the regulatory framework for private

INCOME TAX Taxation of Alternate Investment Funds: The Securities and Exchange Board of India (Alternate Investment Funds) Regulation, 2012 (AIF Regulations) forms the regulatory framework for private

Valuation. Nick Palmer

Valuation Nick Palmer Outline for Today The Misconceptions of Valuation What is Value? How is it created? How do we measure it? Misconceptions on Valuation Myth 1: A valuation is an objective search for

Valuation Nick Palmer Outline for Today The Misconceptions of Valuation What is Value? How is it created? How do we measure it? Misconceptions on Valuation Myth 1: A valuation is an objective search for

CA - FINAL SECURITY VALUATION. FCA, CFA L3 Candidate

CA - FINAL SECURITY VALUATION FCA, CFA L3 Candidate 2.1 Security Valuation Study Session 2 LOS 1 : Introduction Note: Total Earnings mean Earnings available to equity share holders Income Statement

CA - FINAL SECURITY VALUATION FCA, CFA L3 Candidate 2.1 Security Valuation Study Session 2 LOS 1 : Introduction Note: Total Earnings mean Earnings available to equity share holders Income Statement

Lecture 6 Cost of Capital

Lecture 6 Cost of Capital What Types of Long-term Capital do Firms Use? 2 Long-term debt Preferred stock Common equity What Types of Long-term Capital do Firms Use? Capital components are sources of funding

Lecture 6 Cost of Capital What Types of Long-term Capital do Firms Use? 2 Long-term debt Preferred stock Common equity What Types of Long-term Capital do Firms Use? Capital components are sources of funding

ACTY 7292 Financial Statement Analysis Final Exam Semester 1, 2015

Faculty of Creative Industries & Business Department of Accounting and Finance Bachelor of Business ACTY 7292 Financial Statement Analysis Final Exam Date: Wednesday 1 st July 2015 Start time: 8.30AM 11.40AM

Faculty of Creative Industries & Business Department of Accounting and Finance Bachelor of Business ACTY 7292 Financial Statement Analysis Final Exam Date: Wednesday 1 st July 2015 Start time: 8.30AM 11.40AM

Put and call options: Recent Legal and Regulatory Developments

January 2014 Put and call options: Recent Legal and Regulatory Developments 1. Background: Significance of option contracts 1.1 Put and call options on Indian securities (issued by both public and private

January 2014 Put and call options: Recent Legal and Regulatory Developments 1. Background: Significance of option contracts 1.1 Put and call options on Indian securities (issued by both public and private

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By http://vustudents.ning.com 1- What is Financial Management? The procedure of managing the financial resources, as well as accounting and financial

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By http://vustudents.ning.com 1- What is Financial Management? The procedure of managing the financial resources, as well as accounting and financial

Glossary of Business Valuation Terms

Adjusted Net Assets Method Asset-Based Approach Beta Blockage Discount Business Business Risk Business Valuation Capital Asset Pricing Model (CAPM) Capitalization Capitalization of Earnings Method Capital

Adjusted Net Assets Method Asset-Based Approach Beta Blockage Discount Business Business Risk Business Valuation Capital Asset Pricing Model (CAPM) Capitalization Capitalization of Earnings Method Capital

Valuation Importance and Issues. Chamber of Tax Consultants, Seminar on Corporate Restructuring 20 January 2017 Pinkesh Billimoria

Valuation Importance and Issues Chamber of Tax Consultants, Seminar on Corporate Restructuring 20 January 2017 Pinkesh Billimoria Investing in India An Easy Difficulty Valuation expectations / Mismatch

Valuation Importance and Issues Chamber of Tax Consultants, Seminar on Corporate Restructuring 20 January 2017 Pinkesh Billimoria Investing in India An Easy Difficulty Valuation expectations / Mismatch

CIS March 2012 Exam Diet

CIS March 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Level 2 Corporate Finance (1 13) 1. Which of the following statements

CIS March 2012 Exam Diet Examination Paper 2.2: Corporate Finance Equity Valuation and Analysis Fixed Income Valuation and Analysis Level 2 Corporate Finance (1 13) 1. Which of the following statements

Accountant s Guide to Financial Management - Final Exam 100 Questions 1. Objectives of managerial finance do not include:

Accountant s Guide to Financial Management - Final Exam 100 Questions 1. Objectives of managerial finance do not include: Employee profits B. Stockholders wealth maximization Profit maximization Social

Accountant s Guide to Financial Management - Final Exam 100 Questions 1. Objectives of managerial finance do not include: Employee profits B. Stockholders wealth maximization Profit maximization Social

Issue or Transfer of Shares under Exchange Control Regulation

Issue or Transfer of Shares under Exchange Control Regulation - Varatharaj Kumar April 21, 2017 Content Overview Issue of Shares / Compulsory Convertible Preference Shares / Compulsory Convertible Debentures/

Issue or Transfer of Shares under Exchange Control Regulation - Varatharaj Kumar April 21, 2017 Content Overview Issue of Shares / Compulsory Convertible Preference Shares / Compulsory Convertible Debentures/

Comments on exposure draft technical information paper 1: The Discounted Cashflow Method with Property and Business Valuations

29 April 2011 International Valuations Standards Council Moorgate London DC2R 6PP United Kingdom Email: ivsc@ivsc.org Dear Sirs, Comments on exposure draft technical information paper 1: The Discounted

29 April 2011 International Valuations Standards Council Moorgate London DC2R 6PP United Kingdom Email: ivsc@ivsc.org Dear Sirs, Comments on exposure draft technical information paper 1: The Discounted

Provisions Relating to Issue/ Transfer of Shares

Annexure-3 Provisions Relating to Issue/ Transfer of Shares 1. The capital instruments should be issued within 180 days from the date of receipt of the inward remittance received through normal banking

Annexure-3 Provisions Relating to Issue/ Transfer of Shares 1. The capital instruments should be issued within 180 days from the date of receipt of the inward remittance received through normal banking

Foreign Investment FEMA provisions

Foreign Investment FEMA provisions Institute of Chartered Accountants of India Beginner s Study course on FEMA 11 th May 2013 Naresh Ajwani Chartered Accountant Inbound Investment Inbound investment refers

Foreign Investment FEMA provisions Institute of Chartered Accountants of India Beginner s Study course on FEMA 11 th May 2013 Naresh Ajwani Chartered Accountant Inbound Investment Inbound investment refers

Fahmi Ben Abdelkader 5/1/ :34 PM 1. Walking Through From Earnings to Cash Flows. Accrual-based Versus Cash-Flow-based performance measures

Financial Statement Analysis Section 5. The analytical Cash Flow Statement Accrual-based Versus Cash-Flow Flow-based performance measures Students version Fahmi Ben Abdelkader 5/1/2017 10:34 PM 1 Cash-flow

Financial Statement Analysis Section 5. The analytical Cash Flow Statement Accrual-based Versus Cash-Flow Flow-based performance measures Students version Fahmi Ben Abdelkader 5/1/2017 10:34 PM 1 Cash-flow

Answer to MTP_ Final _Syllabus 2012_ December 2016_Set 1. Paper 20 - Financial Analysis and Business Valuation

Paper 20 - Financial Analysis and Business Valuation Page 1 Paper 20 - Financial Analysis and Business Valuation Time Allowed: 3 Hours Full Marks: 100 Question No. 1 which is compulsory and carries 20

Paper 20 - Financial Analysis and Business Valuation Page 1 Paper 20 - Financial Analysis and Business Valuation Time Allowed: 3 Hours Full Marks: 100 Question No. 1 which is compulsory and carries 20

Finance and Accounting for Interviews

This document was developed and written by Ian Lee. All information is meant for public use and purposed for the free transfer of knowledge to interested parties. Send questions and comments to ianlee@uclalumni.net

This document was developed and written by Ian Lee. All information is meant for public use and purposed for the free transfer of knowledge to interested parties. Send questions and comments to ianlee@uclalumni.net

Business Valuation Methodology Survey 2017

Business Valuation Methodology Survey 2017 September 2017 Privileged For limited circulation Contents Foreword 03 Executive summary 04 Detailed survey results 05 The survey report focuses on business valuation

Business Valuation Methodology Survey 2017 September 2017 Privileged For limited circulation Contents Foreword 03 Executive summary 04 Detailed survey results 05 The survey report focuses on business valuation

DCF Choices: Equity Valuation versus Firm Valuation

5 DCF Choices: Equity Valuation versus Firm Valuation Firm Valuation: Value the entire business Assets Liabilities Existing Investments Generate cashflows today Includes long lived (fixed) and short-lived(working

5 DCF Choices: Equity Valuation versus Firm Valuation Firm Valuation: Value the entire business Assets Liabilities Existing Investments Generate cashflows today Includes long lived (fixed) and short-lived(working

Methods and procedures for company valuations in practice

Methods and procedures for company valuations in practice Methods and procedures for company valuation in practice The valuation of a company is an extremely challenging task. The following article gives

Methods and procedures for company valuations in practice Methods and procedures for company valuation in practice The valuation of a company is an extremely challenging task. The following article gives

***************************** SAMPLE PAGES FROM TUTORIAL GUIDE *****************************

DCF Modeling Copyright 2008 by Wall Street Prep, Inc. Table of contents SECTION 1: OVERVIEW DCF in theory and in practice Unlevered vs. levered DCF SECTION 2: MODELING THE DCF Modeling unlevered free cash

DCF Modeling Copyright 2008 by Wall Street Prep, Inc. Table of contents SECTION 1: OVERVIEW DCF in theory and in practice Unlevered vs. levered DCF SECTION 2: MODELING THE DCF Modeling unlevered free cash

The Institute of Chartered Accountants of India

CONCERNS OF ICAI ON AMENDED RULE 11U AND RULE 11UA VIDE NOTIFICATION N0. 23/2018, Dated 24 th MAY, 2018 ISSUED BY THE CBDT Rule 11UA provides for the manner of determining the fair market value of various

CONCERNS OF ICAI ON AMENDED RULE 11U AND RULE 11UA VIDE NOTIFICATION N0. 23/2018, Dated 24 th MAY, 2018 ISSUED BY THE CBDT Rule 11UA provides for the manner of determining the fair market value of various

Homework and Suggested Example Problems Investment Valuation Damodaran. Lecture 2 Estimating the Cost of Capital

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 2 Estimating the Cost of Capital Lecture 2 begins with a discussion of alternative discounted cash flow models, including

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 2 Estimating the Cost of Capital Lecture 2 begins with a discussion of alternative discounted cash flow models, including

OFFICE OF CAREER SERVICES INTERVIEWS FINANCIAL MODELING

OFFICE OF CAREER SERVICES INTERVIEWS FINANCIAL MODELING Basic valuation concepts are among the most popular technical tasks you will be asked to discuss in investment banking and other finance interviews.

OFFICE OF CAREER SERVICES INTERVIEWS FINANCIAL MODELING Basic valuation concepts are among the most popular technical tasks you will be asked to discuss in investment banking and other finance interviews.

WIRC 28 th May 2016 Pinkesh Billimoria. Case Studies

WIRC 28 th May 2016 Pinkesh Billimoria Case Studies Valuation A Perspective Valuation is relative to a specific point in time What is being valued Why it is being valued Secure definition of value Going

WIRC 28 th May 2016 Pinkesh Billimoria Case Studies Valuation A Perspective Valuation is relative to a specific point in time What is being valued Why it is being valued Secure definition of value Going

The Cost of Capital. Principles Applied in This Chapter. The Cost of Capital: An Overview

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital. Chapter 14

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

Course 7804: Financial Analysis and Corporate Valuation - Comprehensive Workshop (5 days) Course introduction. Topics

Course introduction. Topics") Course 7804: Financial Analysis and Corporate Valuation - Comprehensive Workshop (5 days) Course introduction The Financial Analysis section of the course will help participants understand and analyze

Course 7804: Financial Analysis and Corporate Valuation - Comprehensive Workshop (5 days) Course introduction The Financial Analysis section of the course will help participants understand and analyze

Common details. Form FC-GPR - issue of capital instruments by an Indian company to a person

Common details 1.Reporting for 1.1 Form FC-GPR - issue of capital instruments by an Indian company to a person resident outside India Form FC-TRS - transfer of capital instruments between a person resident

Common details 1.Reporting for 1.1 Form FC-GPR - issue of capital instruments by an Indian company to a person resident outside India Form FC-TRS - transfer of capital instruments between a person resident

ABV Examination Content Specification Outline

ABV Examination Content Specification Outline AICPA ABV Examination Content Specification Outline 1 2017 American Institute of Certified Public Accountants. All rights reserved. AICPA and American Institute

ABV Examination Content Specification Outline AICPA ABV Examination Content Specification Outline 1 2017 American Institute of Certified Public Accountants. All rights reserved. AICPA and American Institute

International Glossary of Business Valuation Terms

International Glossary of Business Valuation Terms To enhance and sustain the quality of business valuations for the benefit of the profession and its clientele, the below identified societies and organizations

International Glossary of Business Valuation Terms To enhance and sustain the quality of business valuations for the benefit of the profession and its clientele, the below identified societies and organizations

Why is valuation important?

Valuation in M&A Why is valuation important? The keys to successful M&A Right reasons Right information Right price Right implementation Strategy Due diligence Valuation Integration Valuation elements

Valuation in M&A Why is valuation important? The keys to successful M&A Right reasons Right information Right price Right implementation Strategy Due diligence Valuation Integration Valuation elements

CHAPTER 4 SHOW ME THE MONEY: THE BASICS OF VALUATION

1 CHAPTER 4 SHOW ME THE MOEY: THE BASICS OF VALUATIO To invest wisely, you need to understand the principles of valuation. In this chapter, we examine those fundamental principles. In general, you can

1 CHAPTER 4 SHOW ME THE MOEY: THE BASICS OF VALUATIO To invest wisely, you need to understand the principles of valuation. In this chapter, we examine those fundamental principles. In general, you can

Corporate Finance & Risk Management 06 Financial Valuation

Corporate Finance & Risk Management 06 Financial Valuation Christoph Schneider University of Mannheim http://cf.bwl.uni-mannheim.de schneider@uni-mannheim.de Tel: +49 (621) 181-1949 Topics covered After-tax

Corporate Finance & Risk Management 06 Financial Valuation Christoph Schneider University of Mannheim http://cf.bwl.uni-mannheim.de schneider@uni-mannheim.de Tel: +49 (621) 181-1949 Topics covered After-tax

Discounted Cash Flow Analysis Deliverable #6 Sales Gross Profit / Margin

Discounted Cash Flow Analysis Deliverable #6 The discounted cash flow methodology derives the value of a company by calculating the present value of all future projected cash flows. Unlike comparable companies

Discounted Cash Flow Analysis Deliverable #6 The discounted cash flow methodology derives the value of a company by calculating the present value of all future projected cash flows. Unlike comparable companies

Steps in Business Valuation

Steps in Business Valuation Professor Grant W. Newton, Executive Director Association of Insolvency & Restructuring Advisors Suggested Inquiries and Challenges in Current Environment When the company being

Steps in Business Valuation Professor Grant W. Newton, Executive Director Association of Insolvency & Restructuring Advisors Suggested Inquiries and Challenges in Current Environment When the company being

OVERSEAS DIRECT INVESTMENT

OVERSEAS DIRECT INVESTMENT 29 th December 2018 WIRC of ICAI By: CA Manoj Shah Overseas Direct Investments (ODI) Significance of ODI Promoting global business by Indian entrepreneurs. Promote economic and

OVERSEAS DIRECT INVESTMENT 29 th December 2018 WIRC of ICAI By: CA Manoj Shah Overseas Direct Investments (ODI) Significance of ODI Promoting global business by Indian entrepreneurs. Promote economic and

F3 Financial Strategy

Strategic Level Paper F3 Financial Strategy Senior Examiner s Answers SECTION A Answer to Question One (a)(i) Valuation of Company NN (excluding potential synergistic benefits and integration costs) NN:

Strategic Level Paper F3 Financial Strategy Senior Examiner s Answers SECTION A Answer to Question One (a)(i) Valuation of Company NN (excluding potential synergistic benefits and integration costs) NN:

Basics of Business Valuation. Presented by: Alon Wexler, CPA, CA, CBV Richter Advisory Group Inc.

Basics of Business Valuation Presented by: Alon Wexler, CPA, CA, CBV Richter Advisory Group Inc. 2017 Objective Brief overview of the Basics of Business Valuation There is more to it than 5x EBITDA! 2

Basics of Business Valuation Presented by: Alon Wexler, CPA, CA, CBV Richter Advisory Group Inc. 2017 Objective Brief overview of the Basics of Business Valuation There is more to it than 5x EBITDA! 2

- Kay Grace (author of several books on fundraising and business consultant)

") INTRODUCTION: Capital infusion refers to the process whereby funds are injected into startup companies or large companies by an investor with a financial interest in the company. Capital infusion also

INTRODUCTION: Capital infusion refers to the process whereby funds are injected into startup companies or large companies by an investor with a financial interest in the company. Capital infusion also

Global ABV Examination

Accredited in Business Valuation Global ABV Examination content specification outline Effective Aug. 1, 2018 i Valuation Principles Examination This document is nonauthoritative and is included for informational

Accredited in Business Valuation Global ABV Examination content specification outline Effective Aug. 1, 2018 i Valuation Principles Examination This document is nonauthoritative and is included for informational

RESERVE BANK OF INDIA Foreign Exchange Department Central Office Mumbai RBI/ /613 June 20, 2012

RESERVE BANK OF INDIA Foreign Exchange Department Central Office Mumbai - 400 001 RBI/2011-12/613 June 20, 2012 A.P. (DIR Series) Circular No.133 To All Category - I Authorised Dealer Banks Madam / Sir,

RESERVE BANK OF INDIA Foreign Exchange Department Central Office Mumbai - 400 001 RBI/2011-12/613 June 20, 2012 A.P. (DIR Series) Circular No.133 To All Category - I Authorised Dealer Banks Madam / Sir,

Valuation Inferno: Dante meets

Valuation Inferno: Dante meets DCF Abandon every hope, ye who enter here Aswath Damodaran www.damodaran.com Aswath Damodaran 1 DCF Choices: Equity versus Firm Firm Valuation: Value the entire business

Valuation Inferno: Dante meets DCF Abandon every hope, ye who enter here Aswath Damodaran www.damodaran.com Aswath Damodaran 1 DCF Choices: Equity versus Firm Firm Valuation: Value the entire business

CROSS BORDER MERGER & ACQUISITION By Mr Himanshu Srivastava and Mr Nitin Arora

CROSS BORDER MERGER & ACQUISITION By Mr Himanshu Srivastava and Mr Nitin Arora Merger & Acquisitions ( M&A ) are increasingly been recognized as a business tool. The most widely practiced business strategy

CROSS BORDER MERGER & ACQUISITION By Mr Himanshu Srivastava and Mr Nitin Arora Merger & Acquisitions ( M&A ) are increasingly been recognized as a business tool. The most widely practiced business strategy

Annex - 8 [PART I, Section V, para 1 (iii) ] FC-GPR

![Annex - 8 [PART I, Section V, para 1 (iii) ] FC-GPR](/thumbs/94/119163492.jpg "Annex - 8 [PART I, Section V, para 1 (iii) ] FC-GPR") FC-GPR Annex - 8 [PART I, Section V, para 1 (iii) ] (To be filed by the company through its Authorised Dealer Category I bank with the Regional Office of the RBI under whose jurisdiction the Registered

FC-GPR Annex - 8 [PART I, Section V, para 1 (iii) ] (To be filed by the company through its Authorised Dealer Category I bank with the Regional Office of the RBI under whose jurisdiction the Registered

Foreign Exchange Investment Department Bangladesh Bank Head Office Dhaka FEID Circular No.- 1 Date: May 06, 2018

Foreign Exchange Investment Department Bangladesh Bank Head Office Dhaka www.bb.org.bd FEID Circular No.- 1 Date: May 06, 2018 All Authorized Dealers in Foreign Exchange in Bangladesh Dear Sirs, Transfer

Foreign Exchange Investment Department Bangladesh Bank Head Office Dhaka www.bb.org.bd FEID Circular No.- 1 Date: May 06, 2018 All Authorized Dealers in Foreign Exchange in Bangladesh Dear Sirs, Transfer

1. Sweat equity shares ( ) 2. Stock Option Scheme ( ) 3. Shares issued against exercise of option ( ) Please provide the details of the security

2. Stock Option Scheme ( ) 3. Shares issued against exercise of option ( ) Please provide the details of the security") Form ESOP Annex-13 Return to be filed by Indian company who has issued shares under Employees Stock Options (ESOP) Scheme and/or sweat equity shares. (To be filed by the company through its Authorised

Form ESOP Annex-13 Return to be filed by Indian company who has issued shares under Employees Stock Options (ESOP) Scheme and/or sweat equity shares. (To be filed by the company through its Authorised

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

CHAPTER 13 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

Answer to MTP_Final_Syllabus 2016_Jun2017_Set 2 Paper 14 - Strategic Financial Management

Paper 14 - Strategic Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 14 - Strategic Financial Management Full

Paper 14 - Strategic Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 14 - Strategic Financial Management Full

CHAPTER 2 SHOW ME THE MONEY: THE FUNDAMENTALS OF DISCOUNTED CASH FLOW VALUATION

1 CHAPTER 2 SHOW ME THE MONEY: THE FUNDAMENTALS OF DISCOUNTED CASH FLOW VALUATION In the last chapter, you were introduced to the notion that the value of an asset is determined by its expected cash flows

1 CHAPTER 2 SHOW ME THE MONEY: THE FUNDAMENTALS OF DISCOUNTED CASH FLOW VALUATION In the last chapter, you were introduced to the notion that the value of an asset is determined by its expected cash flows

RESERVE BANK OF INDIA Foreign Exchange Department Central Office Mumbai

RESERVE BANK OF INDIA Foreign Exchange Department Central Office Mumbai - 400 001 RBI/2013-14/490 A.P. (DIR Series) Circular No. 102 February 11, 2014 To All Category - I Authorised Dealer banks Madam

RESERVE BANK OF INDIA Foreign Exchange Department Central Office Mumbai - 400 001 RBI/2013-14/490 A.P. (DIR Series) Circular No. 102 February 11, 2014 To All Category - I Authorised Dealer banks Madam

Chapter 13. Risk, Cost of Capital, and Valuation 13-0

Chapter 13 Risk, Cost of Capital, and Valuation 13-0 Key Concepts and Skills Know how to determine a firm s cost of equity capital Understand the impact of beta in determining the firm s cost of equity

Chapter 13 Risk, Cost of Capital, and Valuation 13-0 Key Concepts and Skills Know how to determine a firm s cost of equity capital Understand the impact of beta in determining the firm s cost of equity

CORPORATE VALUATION METHODOLOGIES

CORPORATE VALUATION METHODOLOGIES What is the business worth? Although a simple question, determining the value of any business in today s economy requires a sophisticated understanding of financial analysis

CORPORATE VALUATION METHODOLOGIES What is the business worth? Although a simple question, determining the value of any business in today s economy requires a sophisticated understanding of financial analysis

Deloitte s recommendations on Income Computation & Disclosure Standards In response to CBDT press release dated 26th November, 2015

Deloitte s recommendations on Income Computation & Disclosure Standards In response to CBDT press release dated 26th November, 2015 December 2015 Contents 1. Background... Error! Bookmark not defined.

Deloitte s recommendations on Income Computation & Disclosure Standards In response to CBDT press release dated 26th November, 2015 December 2015 Contents 1. Background... Error! Bookmark not defined.

After mastering the material in this chapter, you will be able to:

After mastering the material in this chapter, you will be able to: 1. Explain the different concepts of value (1.1 1.2) 2. Understand the principles underpinning the valuation methods (1.3) 3. Explain

After mastering the material in this chapter, you will be able to: 1. Explain the different concepts of value (1.1 1.2) 2. Understand the principles underpinning the valuation methods (1.3) 3. Explain

PPFAS Mutual Fund. Valuation Policy. Investment Valuation for Securities and Other assets

PPFAS Mutual Fund. Investment Valuation for Securities and Other assets SEBI vide Gazette Notification no. LAD-NRO/GN/2011-12/38/4290, dated February 21, 2012 amended Regulation 25, 47 and the Eighth Schedule

PPFAS Mutual Fund. Investment Valuation for Securities and Other assets SEBI vide Gazette Notification no. LAD-NRO/GN/2011-12/38/4290, dated February 21, 2012 amended Regulation 25, 47 and the Eighth Schedule

Inbound FDI and FEMA Policy

Inbound FDI and FEMA Policy WIRC ICAI 27 th Regional Conference 31 August 2012, Mumbai CA. Shabbir Motorwala Agenda An Overview - FDI Policy and FEMA 20 FDI Structural Framework FDI Key reporting / compliance

Inbound FDI and FEMA Policy WIRC ICAI 27 th Regional Conference 31 August 2012, Mumbai CA. Shabbir Motorwala Agenda An Overview - FDI Policy and FEMA 20 FDI Structural Framework FDI Key reporting / compliance

May 19, Issue 136. Annual Return on Foreign liabilities and assets.

May 19, 2017 - Issue 136 RBI updates reporting under FEMA RBI ( Reserve Bank of India ) has vide notification dated May 15,2017 updated Master Direction Reporting under Foreign Exchange Management Act,

May 19, 2017 - Issue 136 RBI updates reporting under FEMA RBI ( Reserve Bank of India ) has vide notification dated May 15,2017 updated Master Direction Reporting under Foreign Exchange Management Act,

I m going to cover 6 key points about FCF here:

Free Cash Flow Overview When you re valuing a company with a DCF analysis, you need to calculate their Free Cash Flow (FCF) to figure out what they re worth. While Free Cash Flow is simple in theory, in

Free Cash Flow Overview When you re valuing a company with a DCF analysis, you need to calculate their Free Cash Flow (FCF) to figure out what they re worth. While Free Cash Flow is simple in theory, in

Disclaimer: This resource package is for studying purposes only EDUCATION

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

Financial Aspects. March 3, ECO 4934: Public Utilities Economics: International Infrastructure

Financial Aspects March 3, 2008 ECO 4934: Public Utilities Economics: International Infrastructure The importance of Financial data Regulators gather and study financial data to partially overcome the

Financial Aspects March 3, 2008 ECO 4934: Public Utilities Economics: International Infrastructure The importance of Financial data Regulators gather and study financial data to partially overcome the

CHAPTER 9 The Cost of Capital

9-1 9-2 CHAPTER 9 The Cost of Capital Cost of Capital Components Debt Preferred Common Equity WACC What types of long-term capital do firms use? Long-term debt Preferred stock Common equity Capital components

9-1 9-2 CHAPTER 9 The Cost of Capital Cost of Capital Components Debt Preferred Common Equity WACC What types of long-term capital do firms use? Long-term debt Preferred stock Common equity Capital components

Paper 3A: Cost Accounting Chapter 4 Unit-I. By: CA Kapileshwar Bhalla

Paper 3A: Cost Accounting Chapter 4 Unit-I By: CA Kapileshwar Bhalla Understand the concept of Cost of Capital that impacts the capital investments decisions for a business. Understand what are the different

Paper 3A: Cost Accounting Chapter 4 Unit-I By: CA Kapileshwar Bhalla Understand the concept of Cost of Capital that impacts the capital investments decisions for a business. Understand what are the different

FOREIGN EXCHANGE RISK MANAGEMENT

FOREIGN EXCHANGE RISK MANAGEMENT 1 RISKS BEING COVERED Foreign Exchange Risk Management primarily tries to mitigate the Exchange rate risk arising out on the risk of an investment's value changing due

FOREIGN EXCHANGE RISK MANAGEMENT 1 RISKS BEING COVERED Foreign Exchange Risk Management primarily tries to mitigate the Exchange rate risk arising out on the risk of an investment's value changing due

CHAPTER 18: EQUITY VALUATION MODELS

CHAPTER 18: EQUITY VALUATION MODELS PROBLEM SETS 1. Theoretically, dividend discount models can be used to value the stock of rapidly growing companies that do not currently pay dividends; in this scenario,

CHAPTER 18: EQUITY VALUATION MODELS PROBLEM SETS 1. Theoretically, dividend discount models can be used to value the stock of rapidly growing companies that do not currently pay dividends; in this scenario,

Improved Decision Making Under Uncertainty: Incorporating a Monte Carlo Simulation into a Discounted Cash Flow Valuation for Equities.

Improved Decision Making Under Uncertainty: Incorporating a Monte Carlo Simulation into a Discounted Cash Flow Valuation for Equities Jack Nurminen Bachelor s Thesis Degree Programme in Finance and Economics

Improved Decision Making Under Uncertainty: Incorporating a Monte Carlo Simulation into a Discounted Cash Flow Valuation for Equities Jack Nurminen Bachelor s Thesis Degree Programme in Finance and Economics

Structuring Inbound Investments

Structuring Inbound Investments Interplay with Companies Act, 2013 & FEMA/FDI Policy January 16, 2016 Lalit Kumar, Partner J. Sagar Associates advocates & solicitors Ahmedabad Bengaluru Chennai Gurgaon

Structuring Inbound Investments Interplay with Companies Act, 2013 & FEMA/FDI Policy January 16, 2016 Lalit Kumar, Partner J. Sagar Associates advocates & solicitors Ahmedabad Bengaluru Chennai Gurgaon

Corporate Finance Primer

Chartered Professional Accountants of Canada, CPA Canada, CPA are trademarks and/or certification marks of the Chartered Professional Accountants of Canada. 2018, Chartered Professional Accountants of

Chartered Professional Accountants of Canada, CPA Canada, CPA are trademarks and/or certification marks of the Chartered Professional Accountants of Canada. 2018, Chartered Professional Accountants of