NIRAJ THAPA FOREX. Foreign exchange constitutes the largest financial market in the world.

|

|

|

- Chad Day

- 5 years ago

- Views:

Transcription

1 NIRAJ THAPA ON FOREX Foreign exchange constitutes the largest financial market in the world. TIM Weithers : Foreign Exchange:-It s not difficult; It s just confusing

2 Contents Topic Some Discussions 2 Slide No Exchanges Rates [Detailed] 6 A/c For Fund Settlement 14 Cross Rates & Currency Pairs 16 International Finance Theory [Detailed] 18 1

3 I N T R O D U C T I O N D A T A Some Discussions FOREX market has no central marketplace Business conducted electronically & globally Principal dealers -larger commercial banks & investment banks A company buys/sells foreign currencies via commercial banks Participants- individuals, firms, and banks Simply stated, exchange of currencies of different countries takes place in FX mkt. Using trends to forecast exchange rates is not productive In London in 2007 $1,359 billion of currency changed hands each day. (Annually, it will be $340 Trillion). New York accounted for $664 billion of turnover per day. 2

4 The Major Currencies I think, the issues in major currencies in FX market could be: Which are the most important currencies for the FX market? Does every country have its own currency? How many currencies are out there? 4 Do the prices of currencies move freely or are exchange rates pegged or fixed? For those floating exchange rates, how much do their prices fluctuate? 5 6 Can you actually trade every currency? 3

5 The United States Dollar The Euro The Japanese Yen The Great Britain Pound The Swiss Franc 1 No, because of lack of confidence & faith in a currency. 2 3 There are around 200 currencies. Some countries have decided to fix or peg the exchange rate between their currency and that of another country. Eg: Argentina 4 Most exchange rates today are determined by market forces, intervention by central banks No, Some countries limit or restrict trade in their money

6 3 6 5

7 Forex Quote Style and Types of Quotes Exchange Rates Exchange Rate It is the rate at which one currency can be exchanged in another. It describes how much one currency can buy another currency. Direct Uses the domestic currency as the price currency and the foreign currency as the base currency. Home currency varies against per unit of a foreign currency. 1 USD = INR 65 Direct Quote for India Indirect Quote for USA European quote Indirect Uses the domestic currency as the base currency and the foreign currency as the price currency. Foreign currency varies against per unit of a home currency. 1 INR = USD Direct Quote for USA Indirect Quote for India 6 American quote

8 Quote Style Convention FX rates are quoted TWO-way USD/INR = Generally, the quote is given up to 4 decimal points except for JPY Market maker always buys at low and sells at high Always talk w.r.t. to currency which is being bought or sold (base currency). Quoted exchange rates are nominal exchange rates Practically, we do follow ACI* Convention in quoting FX rates First currency before oblique is the base and the second currency is the price [Ref. above example] Here: 1) USD is the base currency 2) INR is the price currency 3) is bid rate 4) is ask rate 5) Market is ready to buy 1 INR and sell 1 INR ) Difference of.1010 INR represents spread/bidoffer margin. 7) Spread represents the risk of pricing the exchange of two currencies at a given time *(Association Cambiste Internationale) 7

9 Inflation Political & Economic factors Factors affecting FX rates Expectation of future exchange rate (Balance of Payments) 8

10 Exchange Change In Exchange Rate * Approach Condition Assuming Mobile Capital Result Depreciation Appreciation Balance of payments Persistent deficit Persistent surplus Mundell Fleming Expansionary monetary policy Restrictive monetary policy Expansionary fiscal policy Restrictive fiscal policy Monetary approach Monetary expansion Monetary contraction Asset market approach Persistent deficit Persistent surplus * 9 CFA Institute

11 Currency Crisis An economic downturn as a result of a depreciation of a country s currency and instability in exchange rates. Currency crises do not appear to be anticipated, although there are warning signs. - Deterioration of trade balance - Decline in foreign exchange reserves - Higher rates of inflation - Increase in money supply - Private credit growth - Boom bust cycle in financial markets 10

12 Why 2 way? Price is available for buyer & sellers Limits the profits margin of the quoting bank Quoting bank cannot take advantage by manipulating prices Comparison can be done instantly Lends depth & liquidity 11

13 Appreciation or Depreciation in Currency Rule: Always talk appreciation/depreciation with respect to BASE Currency In case the result is positive, then base currency has appreciated Appreciation It is the gain in value of one currency relative to another currency. % change = New value minus Old value Old value Depreciation It is the loss in value of one currency relative to another currency. In case the result is negative, then base currency has depreciated We do have an error called Sigel s Paradox which states that - The appreciation in one currency is not exactly equal to depreciation in another currency. 12

14 Fixed vs. Flexible Exchange Rates Q. Countries prefer fixed or flexible exchange rates? Countries prefer fixed exchange rates because Stability in international prices for the conduct of trade Anti-inflationary, requires country to follow restrictive monetary & fiscal policies Credibility, if central banks maintain large international reserves to defend fixed rate Fixed rates may be rates inconsistent with economic fundamentals. For example, Asia these days 13

15 A/c For Fund Settlement Vostro A/C Nostro A/C Loro A/C Mirror A/C Your A/c with Us My A/c with U Their A/c With U or Us A/C maintained in local currency by an overseas bank A/C maintained by the bank with its overseas branch for settlement of foreign currency A third bank s Nostro account with you Reflection of the Nostro account maintained in the local currency as well as in foreign currency BOB India opens a current a/c in $ with Citi bank NY Bank of Japan opens a current a/c in INR with HDFC India BOB will say $ A/c as Nostro A/c NEW YORK BOJ will say it as Vostro A/C 14

16 Cash or Today Transaction The settlement that takes place on same date of transaction TOM Transactions The settlement that takes place on one working day after the date of transaction Spot Transaction The settlement that takes place on two working day after the date of transaction Forward Transaction The settlement that takes place after the Spot date 15

17 Cross Rates For cross rates please visit my write up on my blog WSJ World Key Currency Cross Rates Disclaimer: The contributor has not obtained any permission for incorporating the above currency rates table, the contributor expresses his sincere respect to the author TIM WEITHERS from where the content has been incorporated & this has been presented only for knowledge purpose and not for any copy right violation and commercial activities, hence readers are requested to consider for this. 16

18 Currency Pair Source: eknowledgeocean.com. The contributor expresses his since respect to Amit Sir from whose site the content has been incorporated & this has been presented only for knowledge purpose and not for any copy right violation and commercial activities, hence readers are requested to consider for this. 17

19 International Finance Theory DETAILED DISCUSSION ON: 1) INTEREST RATE PARITY 2) PURCHASING POWER PARITY 3) FISHER EFFECT 4) INTERNATIONAL FISHER EFFECT 5) EXPECTATION THEORY 18

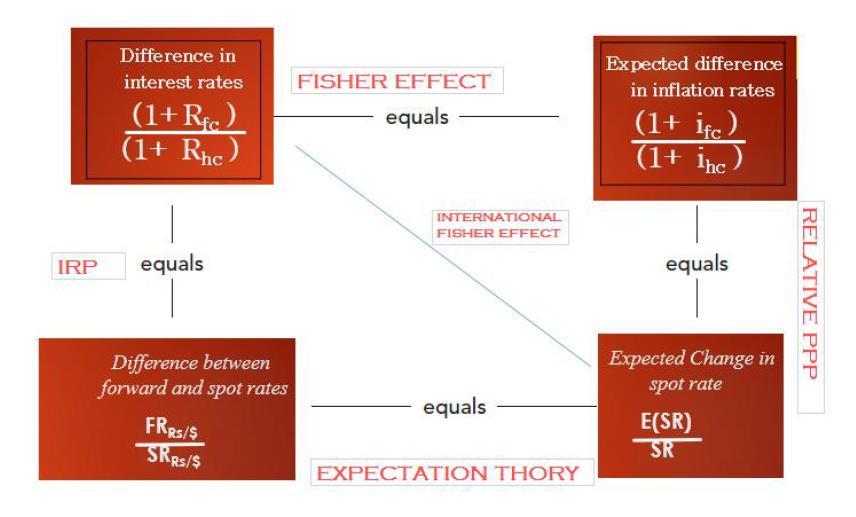

20 Interest Rate Parity IRP An interest rate is the price of money. Simply, it is the cost of borrowing money or the return from investing/depositing money. The interest rate differential between two countries (say $ interest and interest) should be same for exchange risk should be equal to the percentage difference between forward exchange rate and spot exchange rate. This theory holds till there is no restriction on moving money from one economy to another. Practically, dealers set the forward prices by comparing the differences between $ interest and interest. 19

21 To be precise, when money market and currency are in equilibrium then any interest rates differential should be equal to the % difference in forward exchange rates and spot exchange rate, i.e., there won t be any question of earning riskless profit otherwise arbitrageurs will earn riskless profit. IRP Theory relates to a condition of equality of returns on comparable money market instruments. IRP relates Spot Rate and Forward Rate using two countries risk free rates. 20

22 For clarity we may take an example Suppose an investor has $ at the beginning of the year to be invested for a period of 1 year. Let us say $ interest rates on deposits equals 2% p.a. on the other hand Indian deposits offer attractive interest rate of 10% and exchange rate is Rs.50 per $. Now it is to be decided where the amount should be invested. [Assuming that the investor is free to invest in any country] Case I: If the investor invests in US: Amount at the end of the period will be as *102%= $ ( as principal plus 2000 as interest) Case II: If he wishes to invest in India: -First he has to convert the $ amount into Rupee amount, i.e. he has to buy corresponding rupees, hence he can buy *50=Rs.50,00,000. -Now he will invest the 10%, finally at the year end he will have Rs. 50,00,000*110%=55,00,000 (50,00,000-principal + 5,00,000-interest) in his hand. 21

23 Finally, what the theory tells us is that two investments should offer almost exactly same rate of return. Hence at last the investor has to convert the amount generated into $, and we do not know what will be the exchange rate at the year end. Now see how this theory helps us. As per this theory we can fix today the price at which the amount to be sold. Such rate(price) fixed today is the forward rate. The one year forward rate is *. Therefore, by selling Rupees generated at the year end, the investor will be sure to earn / =$ Now see how is computed as forward rate between $ and. For every $ invested you will get (1 + R $ ) and investing in India you will get SR x (1+ R )/FR and these have to be equal so as to prevent arbitrage. 22

24 23

25 Purchasing Power Parity PPP Basically, we have seen that IRP theory is used in obtaining Forward Rate. But we have not discussed how spot rate is determined. Thus, this theory helps in this issue. There are two forms of PPP-(i) Absolute Form of PPP & (ii) Relative Form of PPP Absolute Form of PPP The basic idea behind this theory is that a commodity costs the same regardless of what currency is used to purchase it or where it is selling. This is a straight forward concept. Loosely, speaking as per this theory 1$ will buy same number of say, burger anywhere in the world. Assumptions required to hold absolute PPP true o The transaction cost of trading shipping, insurance, spoilage & so on must be zero. o There must be no barrier on trading-no tariffs, taxes or other political barriers. o The goods traded (burgers) in one place (economy) must be identical to the burger traded in another economy. 24

26 Basket of goods in India As per PPP cost of these goods in India and USA should be same, subject to some assumptions Basket of goods in USA Hamburger in India Hamburger in USA Practically, Absolute PPP will not hold true (ignoring some exceptions) because the assumptions of this theory are rarely met. 25

27 Let s be clear with some cases: If the burger in India costs Rs. 100 in India and exchange rate is Rs.50 per $, then the same burger should cost Rs.100/50=$2 in America. Formally discussing: Let S0 be the spot exchange rate between Rs. & $ [exchange rate is quoted as Rs./$] P$ be the current price in US P be the current price in India Then absolute PPP says that If in case the actual exchange rate is Rs.40/$ then with$2 a trader in America would buy a burger in America and ship it to India and sell the same in Rs.100 per burger and convert the Rs.100 into $, as a result of which he will get 100/40 =$2.5, hence he is gaining $0.5 in this transaction. Since, the trader is making riskless profit and the burgers start moving from US Market to India as a result of which there will be reduced supply of burgers in US and the prices will start rising in US economy at the same time India will lower the price of burger due to increased supply, this will continue till equilibrium is maintained in these two economies. At last the exchange rate quoted will be expected to rise form Rs.40 26

28 Relative Form of PPP This theory does not tell us about what determines the absolute level of exchange rate, moreover, it tells what determines the change in the exchange rate over the given period. Strictly speaking, this theory implies that the differential inflation* rate is always identical to the change in spot rate. Hence change in exchange rates is determined by the difference in the inflation rates of two countries, i.e. any difference in the rates of inflation will be offset by a change in exchange rate. If so then let, S 0 be the current spot exchange rate at t 0 [ /$] E(St ) be the expected exchange rate in t periods i q be the inflation in quote currency [i ] & i b be the inflation rate in base currency[i $ ] 27 *Inflation is the general increase in the average level of prices in the economy; it is typically reported, like interest rates, on an annual or annualized basis.

29 Note: For validity of Relative PPP, validity of Absolute PPP is not mandatory. It is already discussed that Absolute PPP will hold true for rare goods, we shall be focusing more on relative PPP. For example, if prices are rising by 1.0% in the United States and by 6.0% in Mexico, the number of pesos that you can buy for $1 must rise by 1.06/1.01-1, or about 5.0%. Therefore purchasing power parity says that to estimate changes in the spot rate of exchange, you need to estimate differences in inflation rates. Note: If inflation and interest differential are equal then PPP and IRP would give same result. 28

30 Fisher Effect A change in the expected inflation rate causes the same proportionate change in the nominal interest rate; it has no effect on the required real interest rate. This theory tells us the relationship between nominal rates, real rates and inflation. Thus with the help of this theory we can review more carefully the relation between inflation and interests. It is obvious that the investors are ultimately concerned with what they can buy with their money, they need compensation for inflation. Nominal/Money Return :It indicates the rate which money is growing. Nominal rates are called nominal because they have not been adjusted for inflation. It includes inflation. Transactions can be done in the market taking the basis of this return. Real Return: This return is without inflation. It indicates the rate at which the purchasing power is growing. These are the rates which have been adjusted for inflation. 29

Now the question arises here about the impact of inflation.")

31 Clarity Example: You have Rs today and if you invest the same amount you will be with Rs at the year end. And with the same Rs you can buy 20 hamburgers at the beginning of the year. Assume the inflation rate to be 5%. (i.e. the price is expected to go up by 5% during the year.) Now the question arises here about the impact of inflation. See the calculation here: Investment at t 0 =1000 At year end you will get 1155 Then we can say that nominal interest rate (money return) is ( )/1000=15.5% At the beginning you can buy 20 hamburgers [cost per hamburgers is 1000/20=50] Due to rise in price you have to pay 50*1.05=52.50 for 1 hamburgers at year end. If you want to buy the hamburgers at the end with your invested amount then you can buy 1155/52.50=22 hamburgers only. 30

32 What I would like to concentrate is that despite of 15.50% increase in my investment my purchasing power have gone up by 10% only because of inflation. Frankly speaking I am really 10% rich only. It can also be stated that with 5% inflation, each of the Rs nominal dollars we get is worth 5% less in real terms. Hence the real Rs. Value of our investment is 1155/1.05=1100 only. The nominal rate on an investment is the % change in number of rupees you have. The real rate of the investment is the % change in how much you can buy with your rupees-ie, the % change in your buying power. 31

33 Now I would like to make relationship using these 3 terms (real rate, nominal rate & inflation) and the credit for this goes to the great economist Irving Fisher. Fisher effect tells, (1+R)=(1+r)*(1+i) [This is the domestic Fisher effect] Where, R=Nominal Risk Free Rate r= Real Risk Free Rate [Fisher assumed this rate to be constant across the countries] i=inflation Rate Finally solving above equation we will get, r=(r-i)/(1+i) {(1+i) is the discounting factor, r is constant, if we ignore (1+i) in the denominator because the denominator will be slightly more than one, if done as said, then result of (R-i)/(1+i) will be approximately equal to (R-i), then we will get R~r+i, means R is directly proportional to i since r is constant} 32

34 Some Important Noting Fisher on arriving to the conclusion says that investors are not foolish. They do care about the impact of inflation &know that inflation reduces purchasing power and, therefore, they will demand an increase in the nominal rate before lending money. A rise in the rate of inflation causes the nominal rate to rise just enough so that the real rate of interest is unaffected. In other words, the real rate is invariant to the rate of inflation. Fisher is of the view that r will remain constant irrespective of inflation but not all economists would agree with Fisher that the real rate of interest is unaffected by the inflation rate. Practically r differs as per economic conditions of the country. 33

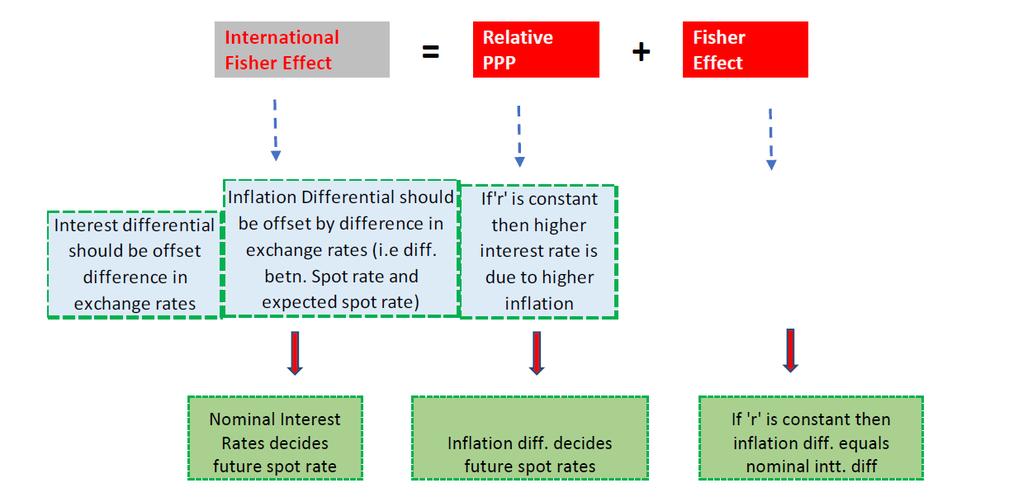

35 This theory is based on the idea that a country with a higher interest rate will have a higher rate of inflation ultimately it causes its currency to depreciate. In theoretical terms, this relationship is expressed as an equality between the expected % change in exchange rate and the difference between the two countries interest rates, divided by one plus the second country s interest rate. This tells us that the difference in returns between the home country and a foreign country is just equal to the difference in inflation rates. Mathematically, International Fisher Effect [also called common real interest rates] Because the divisor approximates 1, the expected percent exchange rate change roughly equals the interest rate differential. 34

36 35

Economists and scholars based on their experience and research over the period have seen that forward rates moreover exaggerate the likely change in the spot rate.")

37 Expectation Theory This theory tells that today s forward rate is going to be the future spot rate. If this theory, holds then FR=E(S) Economists and scholars based on their experience and research over the period have seen that forward rates moreover exaggerate the likely change in the spot rate. When FR predicts that the SR will rise in future, then the FR is over estimating the Future SR and vice versa then SR will change as per the prediction, however many researchers have found that, when the forward rate predicts a rise, the spot rate is more likely to fall, and vice versa. You may refer K. A. Froot and R. H. Thaler, Anomalies: Foreign Exchange, Journal of Economic Perspectives 4 (1990), pp So, this finding is not consistent with the expectations theory. Because of this we say forward rate is an unbiased predictor of future spot rate. 36

38 At A Glance 37

39 Contributor/write up may be Submitted to for publishing on Search for Disclaimer: The above article is contributed by a CA Final student of the Institute and is meant for learning purpose. Due care have been taken into consideration that the content presented above do not violate the opinion of any writers and copyright issues and wherever necessary acknowledgement has been given. For any suggestions, queries and corrections write at: niraj_thapa@hotmail.com

100% Coverage with Practice Manual and last 12 attempts Exam Papers solved in CLASS

1 2 3 4 5 6 FOREIGN EXCHANGE RISK MANAGEMENT (FOREX) + OTC Derivative Concept No. 1: Introduction Three types of transactions in FOREX market which associates two types of risks: 1. Loans(ECB) 2. Investments

1 2 3 4 5 6 FOREIGN EXCHANGE RISK MANAGEMENT (FOREX) + OTC Derivative Concept No. 1: Introduction Three types of transactions in FOREX market which associates two types of risks: 1. Loans(ECB) 2. Investments

MCQ on International Finance

MCQ on International Finance 1. If portable disk players made in China are imported into the United States, the Chinese manufacturer is paid with a) international monetary credits. b) dollars. c) yuan,

MCQ on International Finance 1. If portable disk players made in China are imported into the United States, the Chinese manufacturer is paid with a) international monetary credits. b) dollars. c) yuan,

FOREIGN EXCHANGE MARKET. Luigi Vena 05/08/2015 Liuc Carlo Cattaneo

FOREIGN EXCHANGE MARKET Luigi Vena 05/08/2015 Liuc Carlo Cattaneo TABLE OF CONTENTS The FX market Exchange rates Exchange rates regimes Financial balances International Financial Markets 05/08/2015 Coopeland

FOREIGN EXCHANGE MARKET Luigi Vena 05/08/2015 Liuc Carlo Cattaneo TABLE OF CONTENTS The FX market Exchange rates Exchange rates regimes Financial balances International Financial Markets 05/08/2015 Coopeland

2. Discuss the implications of the interest rate parity for the exchange rate determination.

CHAPTER 5 INTERNATIONAL PARITY RELATIONSHIPS AND FORECASTING FOREIGN EXCHANGE RELATIONSHIPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Give a full definition

CHAPTER 5 INTERNATIONAL PARITY RELATIONSHIPS AND FORECASTING FOREIGN EXCHANGE RELATIONSHIPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Give a full definition

Agenda. Learning Objectives. Chapter 19. International Business Finance. Learning Objectives Principles Used in This Chapter

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

HOMEWORK 8 (CHAPTER 16 PRICE LEVELS AND THE EXCHANGE RATE IN THE LONG RUN) ECO41 FALL 2015 UDAYAN ROY

ECO41 FALL 2015 UDAYAN ROY") HOMEWORK 8 (CHAPTER 16 PRICE LEVELS AND THE EXCHANGE RATE IN THE LONG RUN) ECO41 FALL 2015 UDAYAN ROY Each correct answer is worth 1 point. The maximum score is 20 points. This homework is due in class

HOMEWORK 8 (CHAPTER 16 PRICE LEVELS AND THE EXCHANGE RATE IN THE LONG RUN) ECO41 FALL 2015 UDAYAN ROY Each correct answer is worth 1 point. The maximum score is 20 points. This homework is due in class

STRATEGIC FINANCIAL MANAGEMENT FOREX & OTC Derivatives Summary By CA. Gaurav Jain

1 SFM STRATEGIC FINANCIAL MANAGEMENT FOREX & OTC Derivatives Summary By CA. Gaurav Jain 100% Conceptual Coverage With Live Trading Session Complete Coverage of Study Material, Practice Manual & Previous

1 SFM STRATEGIC FINANCIAL MANAGEMENT FOREX & OTC Derivatives Summary By CA. Gaurav Jain 100% Conceptual Coverage With Live Trading Session Complete Coverage of Study Material, Practice Manual & Previous

Rutgers University Spring Econ 336 International Balance of Payments Professor Roberto Chang. Problem Set 2. Deadline: March 1st.

Rutgers University Spring 2012 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 2. Deadline: March 1st Name: 1. The law of one price works under some assumptions. Which of

Rutgers University Spring 2012 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 2. Deadline: March 1st Name: 1. The law of one price works under some assumptions. Which of

Less Reliable International Parity Conditions

The International Parity Conditions The Law of One Price Interest Rate Parity Less Reliable International Parity Conditions The Real Exchange Rate 1 The International Parity Conditions Though this be madness,

The International Parity Conditions The Law of One Price Interest Rate Parity Less Reliable International Parity Conditions The Real Exchange Rate 1 The International Parity Conditions Though this be madness,

Introduction to Exchange Rates and the Foreign Exchange Market

Introduction to Exchange Rates and the Foreign Exchange Market 2 1. Refer to the exchange rates given in the following table. Today One Year Ago June 25, 2010 June 25, 2009 Country Per $ Per Per Per $

Introduction to Exchange Rates and the Foreign Exchange Market 2 1. Refer to the exchange rates given in the following table. Today One Year Ago June 25, 2010 June 25, 2009 Country Per $ Per Per Per $

INTERNATIONAL FINANCE TOPIC

INTERNATIONAL FINANCE 11 TOPIC The Foreign Exchange Market The dollar ($), the euro ( ), and the yen ( ) are three of the world s monies and most international payments are made using one of them. But

INTERNATIONAL FINANCE 11 TOPIC The Foreign Exchange Market The dollar ($), the euro ( ), and the yen ( ) are three of the world s monies and most international payments are made using one of them. But

Replies to one minute memos, 9/21/03

Replies to one minute memos, 9/21/03 Dear Students, Thank you for asking these great questions. The answer to my question (what is the difference b/n the covered & uncovered interest rate arbitrage? If

Replies to one minute memos, 9/21/03 Dear Students, Thank you for asking these great questions. The answer to my question (what is the difference b/n the covered & uncovered interest rate arbitrage? If

Chapter 6. International Parity Conditions. International Parity Conditions: Learning Objectives. Prices and Exchange Rates

Chapter 6 International arity Conditions International arity Conditions: Learning Objectives Examine how price levels and price level changes (inflation) in countries determine the exchange rate at which

Chapter 6 International arity Conditions International arity Conditions: Learning Objectives Examine how price levels and price level changes (inflation) in countries determine the exchange rate at which

Chapter 10. The Foreign Exchange Market

Chapter 10 The Foreign Exchange Market Why Is The Foreign Exchange Market Important? The foreign exchange market 1. is used to convert the currency of one country into the currency of another 2. provides

Chapter 10 The Foreign Exchange Market Why Is The Foreign Exchange Market Important? The foreign exchange market 1. is used to convert the currency of one country into the currency of another 2. provides

Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences.

5. ARBITRAGE AND SPOT EXCHANGE RATES 5 Arbitrage and Spot Exchange Rates Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences. Arbitrage is the most basic

5. ARBITRAGE AND SPOT EXCHANGE RATES 5 Arbitrage and Spot Exchange Rates Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences. Arbitrage is the most basic

Open Economy. Sherif Khalifa. Sherif Khalifa () Open Economy 1 / 70

Open Economy 1 / 70") Sherif Khalifa Sherif Khalifa () Open Economy 1 / 70 Definition A closed economy is an economy that does not interact with other economies. Definition An open economy is an economy that interacts freely

Sherif Khalifa Sherif Khalifa () Open Economy 1 / 70 Definition A closed economy is an economy that does not interact with other economies. Definition An open economy is an economy that interacts freely

Parity Conditions in International Finance and Currency Forecasting. Chapter 4

Parity Conditions in International Finance and Currency Forecasting Chapter 4 ١ ARBITRAGE AND THE LAW OF ONE PRICE Five Parity Conditions Result From Arbitrage Activities 1. Purchasing Power Parity (PPP)

Parity Conditions in International Finance and Currency Forecasting Chapter 4 ١ ARBITRAGE AND THE LAW OF ONE PRICE Five Parity Conditions Result From Arbitrage Activities 1. Purchasing Power Parity (PPP)

Fx Derivatives- Simplified CA NAVEEN JAIN AUGUST 1, 2015

1 Fx Derivatives- Simplified CA NAVEEN JAIN AUGUST 1, 2015 Agenda 2 History of Fx Overview of Forex Markets Understanding Forex Concepts Hedging Instruments RBI Guidelines Current Forex Markets History

1 Fx Derivatives- Simplified CA NAVEEN JAIN AUGUST 1, 2015 Agenda 2 History of Fx Overview of Forex Markets Understanding Forex Concepts Hedging Instruments RBI Guidelines Current Forex Markets History

INTERNATIONAL FINANCE

INTERNATIONAL FINANCE Ing. Zuzana STRÁPEKOVÁ, PhD. 1 10. 2017/2018 SUA-FEM Nitra The FOREX market is a two-tiered market: Interbank Market (Wholesale) FUNCTION AND STRUCTURE OF THE FOREX MARKET - about

INTERNATIONAL FINANCE Ing. Zuzana STRÁPEKOVÁ, PhD. 1 10. 2017/2018 SUA-FEM Nitra The FOREX market is a two-tiered market: Interbank Market (Wholesale) FUNCTION AND STRUCTURE OF THE FOREX MARKET - about

Chapter 15. The Foreign Exchange Market. Chapter Preview

Chapter 15 The Foreign Exchange Market Chapter Preview In the mid-1980s, American businesses became less competitive relative to their foreign counterparts. By the 2000s, though, competitiveness increased.

Chapter 15 The Foreign Exchange Market Chapter Preview In the mid-1980s, American businesses became less competitive relative to their foreign counterparts. By the 2000s, though, competitiveness increased.

Econ 340. Forms of Exchange Rates. Forms of Exchange Rates. Forms of Exchange Rates. Forms of Exchange Rates. Outline: Exchange Rates

Econ 34 Lecture 13 In What Forms Are Reported? What Determines? Theories of 2 Forms of Forms of What Is an Exchange Rate? The price of one currency in terms of another Examples Recent rates for the US

Econ 34 Lecture 13 In What Forms Are Reported? What Determines? Theories of 2 Forms of Forms of What Is an Exchange Rate? The price of one currency in terms of another Examples Recent rates for the US

Basics of Foreign Exchange Market in India

Basics of Foreign Exchange Market in India Foreign Exchange: Basics What is Foreign Exchange (Forex) How are currency prices determined What is foreign exchange rate policy in India Operation of Forex

Basics of Foreign Exchange Market in India Foreign Exchange: Basics What is Foreign Exchange (Forex) How are currency prices determined What is foreign exchange rate policy in India Operation of Forex

FOREIGN EXCHANGE EXPOSURE AND RISK MANAGEMENT

10 FOREIGN EXCHANGE EXPOSURE AND RISK MANAGEMENT LEARNING OUTCOMES After going through the chapter student shall be able to understand Exchange rate determination Foreign currency market Management of

10 FOREIGN EXCHANGE EXPOSURE AND RISK MANAGEMENT LEARNING OUTCOMES After going through the chapter student shall be able to understand Exchange rate determination Foreign currency market Management of

in equilibrium, are supposed to hold across international markets. Covered Interest Rate Parity Purchasing Power Parity y( (also called the Law of

Week 4 The Parities The Parities There are three fundamental parity conditions that, in equilibrium, are supposed to hold across international markets. Covered Interest Rate Parity Purchasing Power Parity

Week 4 The Parities The Parities There are three fundamental parity conditions that, in equilibrium, are supposed to hold across international markets. Covered Interest Rate Parity Purchasing Power Parity

The Open Economy. (c) Copyright 1998 by Douglas H. Joines 1

Copyright 1998 by Douglas H. Joines 1") The Open Economy (c) Copyright 1998 by Douglas H. Joines 1 Module Objectives Know the major items in the Balance of Payments Accounts Know the determinants of the trade balance Know the major determinants

The Open Economy (c) Copyright 1998 by Douglas H. Joines 1 Module Objectives Know the major items in the Balance of Payments Accounts Know the determinants of the trade balance Know the major determinants

Foreign Exchange Markets: Key Institutional Features (cont)

") Foreign Exchange Markets FOREIGN EXCHANGE MARKETS Professor Anant Sundaram AGENDA Basic characteristics of FX markets: Institutional features Spot markets Forward markets Appreciation, depreciation, premium,

Foreign Exchange Markets FOREIGN EXCHANGE MARKETS Professor Anant Sundaram AGENDA Basic characteristics of FX markets: Institutional features Spot markets Forward markets Appreciation, depreciation, premium,

Midterm - Economics 160B, Spring 2012 Version A

Name Student ID Section (or TA) Midterm - Economics 160B, Spring 2012 Version A You will have 75 minutes to complete this exam. There are 6 pages and 111 points total. Good luck. Multiple choice: Mark

Name Student ID Section (or TA) Midterm - Economics 160B, Spring 2012 Version A You will have 75 minutes to complete this exam. There are 6 pages and 111 points total. Good luck. Multiple choice: Mark

NISM-Series-I: Currency Derivatives Certification Examination

SAMPLE QUESTIONS 1) The market where currencies are traded is known as the. (a) Equity Market (b) Bond Market (c) Fixed Income Market (d) Foreign Exchange Market 2) The USD/CAD (US Canadian Dollars) currency

SAMPLE QUESTIONS 1) The market where currencies are traded is known as the. (a) Equity Market (b) Bond Market (c) Fixed Income Market (d) Foreign Exchange Market 2) The USD/CAD (US Canadian Dollars) currency

In frictionless markets, freely tradable goods should have the same price anywhere: S = P P $

Prices and Exchange Rates In frictionless markets, freely tradable goods should have the same price anywhere: P $ S = P P $ price in US$ S Exchange rate in yen per dollar P Price in Japanese yen Purchasing

Prices and Exchange Rates In frictionless markets, freely tradable goods should have the same price anywhere: P $ S = P P $ price in US$ S Exchange rate in yen per dollar P Price in Japanese yen Purchasing

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET 13 1 Exchange Rate Essentials 2 Exchange Rates in Practice 3 The Market for Foreign Exchange 4 Arbitrage and Spot Exchange Rates 5 Arbitrage

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET 13 1 Exchange Rate Essentials 2 Exchange Rates in Practice 3 The Market for Foreign Exchange 4 Arbitrage and Spot Exchange Rates 5 Arbitrage

International Parity Conditions

International Parity Conditions Eiteman et al., Chapter 6 Winter 2004 Outline of the Chapter How are exchange rates determined? Can we predict them? Prices and Exchange Rates Prices Indices Inflation Rates

International Parity Conditions Eiteman et al., Chapter 6 Winter 2004 Outline of the Chapter How are exchange rates determined? Can we predict them? Prices and Exchange Rates Prices Indices Inflation Rates

Governments and Exchange Rates

Governments and Exchange Rates Exchange Rate Behavior Existing spot exchange rate covered interest arbitrage locational arbitrage triangular arbitrage Existing spot exchange rates at other locations Existing

Governments and Exchange Rates Exchange Rate Behavior Existing spot exchange rate covered interest arbitrage locational arbitrage triangular arbitrage Existing spot exchange rates at other locations Existing

Open Economy. Sherif Khalifa. Sherif Khalifa () Open Economy 1 / 66

Open Economy 1 / 66") Sherif Khalifa Sherif Khalifa () Open Economy 1 / 66 International Flows Definition A closed economy is an economy that does not interact with other economies. Definition An open economy is an economy

Sherif Khalifa Sherif Khalifa () Open Economy 1 / 66 International Flows Definition A closed economy is an economy that does not interact with other economies. Definition An open economy is an economy

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar L8: The Foreign Exchange Market www. notes638.wordpress.com Copyright 2015 Pearson Education, Ltd. All rights reserved. 8-1 Chapter

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar L8: The Foreign Exchange Market www. notes638.wordpress.com Copyright 2015 Pearson Education, Ltd. All rights reserved. 8-1 Chapter

International Parity Conditions. 1. The Law of One Price. 2. Absolute Purchasing Power Parity

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

Capital & Money Markets

Πανεπιστήμιο Πειραιώς, Τμήμα Τραπεζικής και Χρηματοοικονομικής Διοικητικής Μεταπτυχιακό Πρόγραμμα «Χρηματοοικονομική και Τραπεζική Διοικητική» Capital & Money Markets Section 1 Foreign Exchange Markets

Πανεπιστήμιο Πειραιώς, Τμήμα Τραπεζικής και Χρηματοοικονομικής Διοικητικής Μεταπτυχιακό Πρόγραμμα «Χρηματοοικονομική και Τραπεζική Διοικητική» Capital & Money Markets Section 1 Foreign Exchange Markets

Closed vs. Open Economies

Closed vs. Open Economies! A closed economy does not interact with other economies in the world.! An open economy interacts freely with other economies around the world. 1 Percent of GDP The U.S. Economy

Closed vs. Open Economies! A closed economy does not interact with other economies in the world.! An open economy interacts freely with other economies around the world. 1 Percent of GDP The U.S. Economy

ECO 328 SUMMER Sample Questions Topics I.1-3. I.1 National Income Accounting and the Balance of Payments

ECO 328 SUMMER 2004--Sample Questions Topics I.1-3 I.1 National Income Accounting and the Balance of Payments 1. National income equals GNP A. less depreciation, less net unilateral transfers, less indirect

ECO 328 SUMMER 2004--Sample Questions Topics I.1-3 I.1 National Income Accounting and the Balance of Payments 1. National income equals GNP A. less depreciation, less net unilateral transfers, less indirect

27 th Year of Publication. A monthly publication from South Indian Bank. To kindle interest in economic affairs... To empower the student community...

Experience Next Generation Banking A monthly publication from South Indian Bank To kindle interest in economic affairs... To empower the student community... www.southindianbank.com Student s corner ho2099@sib.co.in

Experience Next Generation Banking A monthly publication from South Indian Bank To kindle interest in economic affairs... To empower the student community... www.southindianbank.com Student s corner ho2099@sib.co.in

Chapter 2 Foreign Exchange Parity Relations

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

05/07/55. International Parity Conditions. 1. The Law of One Price

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

International Parity Conditions

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

3. If the price of a British pound increases from $1.50 per pound to $1.80 per pound, we say that:

STUDY GUIDE FINAL ECO41 FALL 2013 UDAYAN ROY Ch 13 National Income Accounting See the questions in Homework 7 and Homework 8. CHAPTER 14 Exchange Rates and Interest Parity 1. How many dollars would it

STUDY GUIDE FINAL ECO41 FALL 2013 UDAYAN ROY Ch 13 National Income Accounting See the questions in Homework 7 and Homework 8. CHAPTER 14 Exchange Rates and Interest Parity 1. How many dollars would it

Chapter 31 Open Economy Macroeconomics Basic Concepts

Chapter 31 Open Economy Macroeconomics Basic Concepts 0 In this chapter, look for the answers to these questions: How are international flows of goods and assets related? What s the difference between

Chapter 31 Open Economy Macroeconomics Basic Concepts 0 In this chapter, look for the answers to these questions: How are international flows of goods and assets related? What s the difference between

6 The Open Economy. This chapter:

6 The Open Economy This chapter: Balance of Payments Accounting Savings and Investment in the Open Economy Determination of the Trade Balance and the Exchange Rate Mundell Fleming model Exchange Rate Regimes

6 The Open Economy This chapter: Balance of Payments Accounting Savings and Investment in the Open Economy Determination of the Trade Balance and the Exchange Rate Mundell Fleming model Exchange Rate Regimes

Nominal exchange rate

Nominal exchange rate The nominal exchange rate between two currencies is the price of one currency in terms of the other. The nominal exchange rate (or, for short, exchange rate) will be denoted by the

Nominal exchange rate The nominal exchange rate between two currencies is the price of one currency in terms of the other. The nominal exchange rate (or, for short, exchange rate) will be denoted by the

Chapter 25 The Exchange Rate and the Balance of Payments The Foreign Exchange Market

Chapter 25 The Exchange Rate and the Balance of Payments 25.1 The Foreign Exchange Market 1) Foreign currency is A) the market for foreign exchange. B) the price at which one currency exchanges for another

Chapter 25 The Exchange Rate and the Balance of Payments 25.1 The Foreign Exchange Market 1) Foreign currency is A) the market for foreign exchange. B) the price at which one currency exchanges for another

Global Business Economics. Mark Crosby SEMBA International Economics

Global Business Economics Mark Crosby SEMBA International Economics The balance of payments and exchange rates Understand the structure of a country s balance of payments. Understand the difference between

Global Business Economics Mark Crosby SEMBA International Economics The balance of payments and exchange rates Understand the structure of a country s balance of payments. Understand the difference between

Chapter 5. The Foreign Exchange Market. Foreign Exchange Markets: Learning Objectives. Foreign Exchange Markets. Foreign Exchange Markets

Chapter 5 The Foreign Exchange Market Foreign Exchange Markets: Learning Objectives Examine the functions performed by the foreign exchange (FOREX) market, its participants, size, geographic and currency

Chapter 5 The Foreign Exchange Market Foreign Exchange Markets: Learning Objectives Examine the functions performed by the foreign exchange (FOREX) market, its participants, size, geographic and currency

Economics. Open-Economy Macroeconomics: Basic Concepts CHAPTER. N. Gregory Mankiw. Principles of. Seventh Edition. Wojciech Gerson ( )

") Seventh Edition Principles of Economics N. Gregory Mankiw Wojciech Gerson (1831-1901) CHAPTER 31 Open-Economy Macroeconomics: Basic Concepts In this chapter, look for the answers to these questions How

Seventh Edition Principles of Economics N. Gregory Mankiw Wojciech Gerson (1831-1901) CHAPTER 31 Open-Economy Macroeconomics: Basic Concepts In this chapter, look for the answers to these questions How

Name Student ID Summer Session II Midterm ECON160B There are 7 pages and 100 points. You have 100 minutes to complete the exam.

Name Student ID Summer Session II 2013 Midterm ECON160B There are 7 pages and 100 points. You have 100 minutes to complete the exam. Multiple Choice Choose the best answer. (2.5 points each, 30 points

Name Student ID Summer Session II 2013 Midterm ECON160B There are 7 pages and 100 points. You have 100 minutes to complete the exam. Multiple Choice Choose the best answer. (2.5 points each, 30 points

Macroeonomics. 18 this chapter, Open-Economy Macroeconomics: look for the answers to these questions: Introduction. N.

C H A P T E R In 18 this chapter, look for the answers to these questions: Open-Economy Macroeconomics: How are international flows of goods and assets Basic Concepts related? P R I N C I P L E S O F Macroeonomics

C H A P T E R In 18 this chapter, look for the answers to these questions: Open-Economy Macroeconomics: How are international flows of goods and assets Basic Concepts related? P R I N C I P L E S O F Macroeonomics

Use the following to answer questions 19-20: Scenario: Exchange Rates The value of a euro goes from US$1.25 to US$1.50.

Name: Date: 1. Open-economy macroeconomics is the branch of economics that deals with: A) reducing regulations on business. B) the relationships between economies of different nations. C) reducing employment

Name: Date: 1. Open-economy macroeconomics is the branch of economics that deals with: A) reducing regulations on business. B) the relationships between economies of different nations. C) reducing employment

Arabian Group of Journals (AGJ) Accounting Research. International Journal of Accounting Research (IJAR) Webpage:

Accounting Research. International Journal of Accounting Research (IJAR) Webpage:") Arabian Group of Journals (AGJ) Accounting Research International Journal of Accounting Research (IJAR) Webpage: www.arabianjbmr.com/ijar_index.php ISSN: 2311-326X EXCHANGE RATE FLUCTUATIONS MAJOR FACTOR

Arabian Group of Journals (AGJ) Accounting Research International Journal of Accounting Research (IJAR) Webpage: www.arabianjbmr.com/ijar_index.php ISSN: 2311-326X EXCHANGE RATE FLUCTUATIONS MAJOR FACTOR

Week-7. Dr. Ahmed. Domestic Firms International Firms Multinational Firms Global Firms

FINC 5880 Dr. Ahmed Week-7 Name Domestic Firms International Firms Multinational Firms Global Firms Factors that make multinational financial management different Exchange rates and trading International

FINC 5880 Dr. Ahmed Week-7 Name Domestic Firms International Firms Multinational Firms Global Firms Factors that make multinational financial management different Exchange rates and trading International

University of Siegen

University of Siegen Faculty of Economic Disciplines, Department of economics Univ. Prof. Dr. Jan Franke-Viebach Seminar Risk and Finance Summer Semester 2008 Topic 4: Hedging with currency futures Name

University of Siegen Faculty of Economic Disciplines, Department of economics Univ. Prof. Dr. Jan Franke-Viebach Seminar Risk and Finance Summer Semester 2008 Topic 4: Hedging with currency futures Name

Quoting an exchange rate. The exchange rate. Examples of appreciation. Currency appreciation. Currency depreciation. Examples of depreciation

The exchange rate The nominal exchange rate (or, for short, exchange rate) between two currencies is the price of one currency in terms of the other. It allows domestic purchasing power to be spent abroad.

The exchange rate The nominal exchange rate (or, for short, exchange rate) between two currencies is the price of one currency in terms of the other. It allows domestic purchasing power to be spent abroad.

CHAPTER 2 THE DOMESTIC AND INTERNATIONAL FINANCIAL MARKETPLACE

CHAPTER 2 THE DOMESTIC AND INTERNATIONAL FINANCIAL MARKETPLACE ANSWERS TO QUESTIONS: 1. The saving-investment cycle consists of net savers (surplus spending units) transferring funds to net investors (deficit

CHAPTER 2 THE DOMESTIC AND INTERNATIONAL FINANCIAL MARKETPLACE ANSWERS TO QUESTIONS: 1. The saving-investment cycle consists of net savers (surplus spending units) transferring funds to net investors (deficit

Study Questions (with Answers) Lecture 13. Exchange Rates

Lecture 13. Exchange Rates") Study Questions (with Answers) Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions (with Answers) Lecture 13 1. The statement the yen rose today from 121 to 117 makes

Study Questions (with Answers) Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions (with Answers) Lecture 13 1. The statement the yen rose today from 121 to 117 makes

Open-Economy Macroeconomics: Basic Concepts

N. Gregory Mankiw Principles of Macroeconomics Sixth Edition 18 Open-Economy Macroeconomics: Basic Concepts Premium PowerPoint Slides by Ron Cronovich 2012 UPDATE In this chapter, look for the answers

N. Gregory Mankiw Principles of Macroeconomics Sixth Edition 18 Open-Economy Macroeconomics: Basic Concepts Premium PowerPoint Slides by Ron Cronovich 2012 UPDATE In this chapter, look for the answers

Chapter 17 Appendix A

Chapter 17 Appendix A The Interest Parity Condition We can derive all the results in the text with a concept that is widely used in international finance. The interest parity condition shows the relationship

Chapter 17 Appendix A The Interest Parity Condition We can derive all the results in the text with a concept that is widely used in international finance. The interest parity condition shows the relationship

Open-Economy Macroeconomics: Basic Concepts

Wojciech Gerson (1831-1901) Seventh Edition Principles of Macroeconomics N. Gregory Mankiw CHAPTER 18 Open-Economy Macroeconomics: Basic Concepts Closed vs. Open Economies A closed economy does not interact

Wojciech Gerson (1831-1901) Seventh Edition Principles of Macroeconomics N. Gregory Mankiw CHAPTER 18 Open-Economy Macroeconomics: Basic Concepts Closed vs. Open Economies A closed economy does not interact

Chapter 17. Exchange Rates and International Economic Policy

Chapter 17 Exchange Rates and International Economic Policy Preview To examine the financial market that determines exchange rates in the long and short runs To understand the role of exchange rates in

Chapter 17 Exchange Rates and International Economic Policy Preview To examine the financial market that determines exchange rates in the long and short runs To understand the role of exchange rates in

Open-Economy Macroeconomics: Basic Concepts

Lesson 10 Open-Economy Macroeconomics: Basic Concepts Henan University of Technology Sino-British College Transfer Abroad Undergraduate Programme 0 In this lesson, look for the answers to these questions:

Lesson 10 Open-Economy Macroeconomics: Basic Concepts Henan University of Technology Sino-British College Transfer Abroad Undergraduate Programme 0 In this lesson, look for the answers to these questions:

Part I: Forwards. Derivatives & Risk Management. Last Week: Weeks 1-3: Part I Forwards. Introduction Forward fundamentals

Derivatives & Risk Management Last Week: Introduction Forward fundamentals Weeks 1-3: Part I Forwards Forward fundamentals Fwd price, spot price & expected future spot Part I: Forwards 1 Forwards: Fundamentals

Derivatives & Risk Management Last Week: Introduction Forward fundamentals Weeks 1-3: Part I Forwards Forward fundamentals Fwd price, spot price & expected future spot Part I: Forwards 1 Forwards: Fundamentals

INTRODUCTION TO FOREX

PRESENTS INTRODUCTION TO FOREX ALL TRADING INFORMATION REVEALED 1 INTRODUCTION The word FOREX is derived from the term Foreign Exchange and is the largest financial market in the world. Unlike many other

PRESENTS INTRODUCTION TO FOREX ALL TRADING INFORMATION REVEALED 1 INTRODUCTION The word FOREX is derived from the term Foreign Exchange and is the largest financial market in the world. Unlike many other

Foreign Exchange Risk Management

C H A P T E R 2 Foreign Exchange Risk Management Coverage of FOREX in Past Examinations: Year May-2012 Nov-2011 May- 2011 SFM (New) MAFA (Old) 8+10(Theory) =18 11+8(With derivative)=19 Nov- 2010 NA NA

C H A P T E R 2 Foreign Exchange Risk Management Coverage of FOREX in Past Examinations: Year May-2012 Nov-2011 May- 2011 SFM (New) MAFA (Old) 8+10(Theory) =18 11+8(With derivative)=19 Nov- 2010 NA NA

Lower prices. Lower costs, esp. wages. Higher productivity. Higher quality/more desirable exports. Greater natural resources. Higher interest rates

1 Goods market Reason to Hold Currency To acquire goods and services from that country Important in... Long run (years to decades) Currency Will Appreciate If... Lower prices Lower costs, esp. wages Higher

1 Goods market Reason to Hold Currency To acquire goods and services from that country Important in... Long run (years to decades) Currency Will Appreciate If... Lower prices Lower costs, esp. wages Higher

Exchange rate and interest rates. Rodolfo Helg, February 2018 (adapted from Feenstra Taylor)

") Exchange rate and interest rates Rodolfo Helg, February 2018 (adapted from Feenstra Taylor) Defining the Exchange Rate Exchange rate (E domestic/foreign ) The price of a unit of foreign currency in terms

Exchange rate and interest rates Rodolfo Helg, February 2018 (adapted from Feenstra Taylor) Defining the Exchange Rate Exchange rate (E domestic/foreign ) The price of a unit of foreign currency in terms

Full file at CHAPTER 2 THE DOMESTIC AND INTERNATIONAL FINANCIAL MARKETPLACE

CHAPTER 2 THE DOMESTIC AND INTERNATIONAL FINANCIAL MARKETPLACE ANSWERS TO QUESTIONS: 1. The saving-investment cycle consists of net savers (surplus spending units) transferring funds to net investors (deficit

CHAPTER 2 THE DOMESTIC AND INTERNATIONAL FINANCIAL MARKETPLACE ANSWERS TO QUESTIONS: 1. The saving-investment cycle consists of net savers (surplus spending units) transferring funds to net investors (deficit

CHAPTER 2 THE DOMESTIC AND INTERNATIONAL FINANCIAL MARKETPLACE

CHAPTER 2 THE DOMESTIC AND INTERNATIONAL FINANCIAL MARKETPLACE ANSWERS TO QUESTIONS: 1. a. A multinational corporation is a firm that has investments in manufacturing and/or distribution facilities in

CHAPTER 2 THE DOMESTIC AND INTERNATIONAL FINANCIAL MARKETPLACE ANSWERS TO QUESTIONS: 1. a. A multinational corporation is a firm that has investments in manufacturing and/or distribution facilities in

International Finance multiple-choice questions

International Finance multiple-choice questions 1. Spears Co. will receive SF1,000,000 in 30 days. Use the following information to determine the total dollar amount received (after accounting for the

International Finance multiple-choice questions 1. Spears Co. will receive SF1,000,000 in 30 days. Use the following information to determine the total dollar amount received (after accounting for the

Macroeconomics in an Open Economy

Chapter 17 (29) Macroeconomics in an Open Economy Chapter Summary Nearly all economies are open economies that trade with and invest in other economies. A closed economy has no interactions in trade or

Chapter 17 (29) Macroeconomics in an Open Economy Chapter Summary Nearly all economies are open economies that trade with and invest in other economies. A closed economy has no interactions in trade or

CHAPTER 2. EXCHANGE RATE DETERMINATION: Exchange Rate Quotations, Balance of Payments, Prices, Parities and Interest Rates

CHAPTER 2. EXCHANGE RATE DETERMINATION: Exchange Rate Quotations, Balance of Payments, Prices, Parities and Interest Rates 1. Foreign Exchange Rates and Quotations A foreign exchange rate is the price

CHAPTER 2. EXCHANGE RATE DETERMINATION: Exchange Rate Quotations, Balance of Payments, Prices, Parities and Interest Rates 1. Foreign Exchange Rates and Quotations A foreign exchange rate is the price

S-18 Solutions Chapter 3 Exchange Rates I: The Monetary Approach in the Long Run

S-18 Solutions Chapter 3 Exchange Rates I: The Monetary Approach in the Long Run e. Suppose the ank of Korea wants to maintain an exchange rate peg with the Japanese yen. What money growth rate would the

S-18 Solutions Chapter 3 Exchange Rates I: The Monetary Approach in the Long Run e. Suppose the ank of Korea wants to maintain an exchange rate peg with the Japanese yen. What money growth rate would the

PRODUCT DISCLOSURE STATEMENT 1 APRIL 2014

PRODUCT DISCLOSURE STATEMENT 1 APRIL 2014 Table of Contents 1. General information 01 2. Significant features of CFDs 01 3. Product Costs and Other Considerations 07 4. Significant Risks associated with

PRODUCT DISCLOSURE STATEMENT 1 APRIL 2014 Table of Contents 1. General information 01 2. Significant features of CFDs 01 3. Product Costs and Other Considerations 07 4. Significant Risks associated with

Midterm - Economics 160B, Fall 2011 Version A

Name Student ID Section (or TA) Midterm - Economics 160B, Fall 2011 Version A You will have 75 minutes to complete this exam. There are 5 pages and 108 points total. Good luck. Multiple choice: Mark best

Name Student ID Section (or TA) Midterm - Economics 160B, Fall 2011 Version A You will have 75 minutes to complete this exam. There are 5 pages and 108 points total. Good luck. Multiple choice: Mark best

Financial markets in the open economy - the interest rate parity. Exchange rates in the short run.

Financial markets in the open economy - the interest rate parity. Exchange rates in the short run. Dr hab. Joanna Siwińska-Gorzelak Foreign Exchange Markets The set of markets where foreign currencies

Financial markets in the open economy - the interest rate parity. Exchange rates in the short run. Dr hab. Joanna Siwińska-Gorzelak Foreign Exchange Markets The set of markets where foreign currencies

Macroeconomics. Open-Economy Macroeconomics: Basic Concepts. Introduction. In this chapter, look for the answers to these questions: N.

C H A P T E R 18 Open-Economy Macroeconomics: Basic Concepts P R I N C I P L E S O F Macroeconomics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2010 South-Western, a part of Cengage Learning,

C H A P T E R 18 Open-Economy Macroeconomics: Basic Concepts P R I N C I P L E S O F Macroeconomics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2010 South-Western, a part of Cengage Learning,

Chapter 2 The Domestic and International Financial Marketplace

Download Solution Manual for Contemporary Financial Management 13th Edition by Moyer Link full: https://testbankservice.com/download/solutionmanual-for-contemporary-financial-management-13th-editionby-moyer/

Download Solution Manual for Contemporary Financial Management 13th Edition by Moyer Link full: https://testbankservice.com/download/solutionmanual-for-contemporary-financial-management-13th-editionby-moyer/

Final exam Non-detailed correction 3 hours. This are indicative directions on how structure the essay questions and what was expected.

International Finance Master PEI Fall 2011 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours This are indicative directions on how structure the essay questions and what was expected. 1. Multiple

International Finance Master PEI Fall 2011 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours This are indicative directions on how structure the essay questions and what was expected. 1. Multiple

Chapter 3 Foreign Exchange Determination and Forecasting

Chapter 3 oreign Exchange Determination and orecasting 1. Applying expansionary macroeconomic policy, which results in higher goods prices and lower real interest rates, will not reduce the balance of

Chapter 3 oreign Exchange Determination and orecasting 1. Applying expansionary macroeconomic policy, which results in higher goods prices and lower real interest rates, will not reduce the balance of

BBK3273 International Finance

BBK3273 International Finance Prepared by Dr Khairul Anuar L1: Foreign Exchange Market www.lecturenotes638.wordpress.com Contents 1. Foreign Exchange Market 2. History of Foreign Exchange 3. Size of the

BBK3273 International Finance Prepared by Dr Khairul Anuar L1: Foreign Exchange Market www.lecturenotes638.wordpress.com Contents 1. Foreign Exchange Market 2. History of Foreign Exchange 3. Size of the

Christiano 362, Winter 2006 Lecture #3: More on Exchange Rates More on the idea that exchange rates move around a lot.

Christiano 362, Winter 2006 Lecture #3: More on Exchange Rates More on the idea that exchange rates move around a lot. 1.Theexampleattheendoflecture#2discussedalargemovementin the US-Japanese exchange

Christiano 362, Winter 2006 Lecture #3: More on Exchange Rates More on the idea that exchange rates move around a lot. 1.Theexampleattheendoflecture#2discussedalargemovementin the US-Japanese exchange

Midterm Exam I: Answer Sheet

Economics 434 Spring 1999 Dr. Ickes Midterm Exam I: Answer Sheet Read the entire exam over carefully before beginning. The value of each question is given. Allocate your time efficiently given the price

Economics 434 Spring 1999 Dr. Ickes Midterm Exam I: Answer Sheet Read the entire exam over carefully before beginning. The value of each question is given. Allocate your time efficiently given the price

AN INTRODUCTION TO TRADING CURRENCIES

The ins and outs of trading currencies AN INTRODUCTION TO TRADING CURRENCIES A FOREX.com educational guide K$ $ kr HK$ $ FOREX.com is a trading name of GAIN Capital - FOREX.com Canada Limited is a member

The ins and outs of trading currencies AN INTRODUCTION TO TRADING CURRENCIES A FOREX.com educational guide K$ $ kr HK$ $ FOREX.com is a trading name of GAIN Capital - FOREX.com Canada Limited is a member

Money and Exchange rates

Macroeconomic policy Class Notes Money and Exchange rates Revised: December 13, 2011 Latest version available at www.fperri.net/teaching/macropolicyf11.htm So far we have learned that monetary policy can

Macroeconomic policy Class Notes Money and Exchange rates Revised: December 13, 2011 Latest version available at www.fperri.net/teaching/macropolicyf11.htm So far we have learned that monetary policy can

Exchange rate: the price of one currency in terms of another. We will be using the notation E t = euro

Econ 330: Money and Banking Fall 2014, Handout 8 Chapter 17 : Foreign Exchange Market 1. Foreign Exchange Market Exchange rate: the price of one currency in terms of another. We will be using the notation

Econ 330: Money and Banking Fall 2014, Handout 8 Chapter 17 : Foreign Exchange Market 1. Foreign Exchange Market Exchange rate: the price of one currency in terms of another. We will be using the notation

Exchange Rates. Exchange Rates. ECO 3704 International Macroeconomics. Chapter Exchange Rates

Exchange Rates CHAPTER 13 1 Exchange Rates What are they? How does one describe their movements? 2 Exchange Rates The nominal exchange rate is the price of one currency in terms of another. The spot rate

Exchange Rates CHAPTER 13 1 Exchange Rates What are they? How does one describe their movements? 2 Exchange Rates The nominal exchange rate is the price of one currency in terms of another. The spot rate

Efficacy of Interest Rate Futures for Corporate

Efficacy of Interest Rate Futures for Corporate The financial sector, corporate and even households are affected by interest rate risk. Interest rate fluctuations impact portfolios of banks, insurance

Efficacy of Interest Rate Futures for Corporate The financial sector, corporate and even households are affected by interest rate risk. Interest rate fluctuations impact portfolios of banks, insurance

AN INTRODUCTION TO TRADING CURRENCIES

The ins and outs of trading currencies AN INTRODUCTION TO TRADING CURRENCIES A FOREX.com educational guide K$ $ kr HK$ $ FOREX.com is a trading name of GAIN Capital UK Limited, FCA No. 113942. Our services

The ins and outs of trading currencies AN INTRODUCTION TO TRADING CURRENCIES A FOREX.com educational guide K$ $ kr HK$ $ FOREX.com is a trading name of GAIN Capital UK Limited, FCA No. 113942. Our services

Chapter 4 Research Methodology

Chapter 4 Research Methodology 4.1 Introduction An exchange rate (also known as a foreign-exchange rate, forex rate, FX rate or Agio) between two currencies is the rate at which one currency will be exchanged

Chapter 4 Research Methodology 4.1 Introduction An exchange rate (also known as a foreign-exchange rate, forex rate, FX rate or Agio) between two currencies is the rate at which one currency will be exchanged

CHAPTER 31 INTERNATIONAL CORPORATE FINANCE

Corporate Finance 11 th edition Solutions Manual Ross, Westerfield, Jaffe, and Jordan Completed download Solutions Manual, Answers, Instructors Resource Manual, Case Solutions, Excel Solutions are included:

Corporate Finance 11 th edition Solutions Manual Ross, Westerfield, Jaffe, and Jordan Completed download Solutions Manual, Answers, Instructors Resource Manual, Case Solutions, Excel Solutions are included:

ECN 160B SSI Midterm Exam July 11 th, 2012

ECN 160B SSI Midterm Exam July 11 th, 2012 Name: ID#: Instruction: Write your name and student ID number on both this exam and your scantron. Be sure to answer all multiple choice question on your scantron,

ECN 160B SSI Midterm Exam July 11 th, 2012 Name: ID#: Instruction: Write your name and student ID number on both this exam and your scantron. Be sure to answer all multiple choice question on your scantron,

EconS 327 Test 2 Spring 2010

1. Credit (+) items in the balance of payments correspond to anything that: a. Involves payments to foreigners b. Decreases the domestic money supply c. Involves receipts from foreigners d. Reduces international

1. Credit (+) items in the balance of payments correspond to anything that: a. Involves payments to foreigners b. Decreases the domestic money supply c. Involves receipts from foreigners d. Reduces international

Introduction to Foreign Exchange Slides for International Finance (KOM Chapter 14)

") Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Introduction to Foreign Exchange Slides for International Finance (KOM Chapter 14)

") Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Study Questions (with Answers) Lecture 15 International Macroeconomics

Lecture 15 International Macroeconomics") Study Questions (with Answers) Page 1 of 5 Study Questions (with Answers) Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply

Study Questions (with Answers) Page 1 of 5 Study Questions (with Answers) Lecture 15 International Macroeconomics Part 1: Multiple Choice Select the best answer of those given. 1. If the aggregate supply

OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS

17 OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS LEARNING OBJECTIVES: By the end of this chapter, students should understand: how net exports measure the international flow of goods and services. how net

17 OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS LEARNING OBJECTIVES: By the end of this chapter, students should understand: how net exports measure the international flow of goods and services. how net

ECON0302 International Finance Midterm Exam Fall 2004

ECON0302 International Finance Midterm Exam Fall 2004 Short Questions (60 points each) 1. If in ation in the US is projected at 2:5% annually for the next 3 years and at 0:9% annually in Switzerland for

ECON0302 International Finance Midterm Exam Fall 2004 Short Questions (60 points each) 1. If in ation in the US is projected at 2:5% annually for the next 3 years and at 0:9% annually in Switzerland for