100% Coverage with Practice Manual and last 12 attempts Exam Papers solved in CLASS

|

|

|

- Kristina Ford

- 5 years ago

- Views:

Transcription

1 1

2 2

3 3

4 4

5 5

6 6 FOREIGN EXCHANGE RISK MANAGEMENT (FOREX) + OTC Derivative Concept No. 1: Introduction Three types of transactions in FOREX market which associates two types of risks: 1. Loans(ECB) 2. Investments (Bonds & Equity) 3. Export & Import Foreign Exchange Risk Hedging Strategy Forward Contract Money Market Hedge Future Contract Option Contract Swap Points Premium/ Discount IRPT PPPT Interest Rate Risk Hedging Strategy FRA Interest Rate Swap Currency Swap Cap, Floor & Collar

7 What is Exchange Rate? 7 The rate of conversion is the Exchange Rate. Or An exchange rate is the price of one country s currency expressed in terms of the currency of another country. E.g. A rate of ` 50 per US $ implies that one US $ costs ` 50. Rule 1: in an exchange rate two currencies are involved. Rule2: in any transaction involving Foreign Currency, you are selling one currency and buying another. Concept No. 2: Home Currency & Foreign Currency Home Currency: Country s own currency. For India ` /INR is home currency For USA US $ or Dollar is a home currency Foreign Currency: Any currency other than home currency will be a Foreign Currency For India, $,, etc. will be a foreign currency. For US `, will be foreign currency. Concept No. 3: Bid & Ask Rate Bid Rate: Rate at which bank BUYS left hand side currency. Ask Rate: Rate at which bank SELLS left hand side currency. One-way Quote: [when Bid and Ask Rate are same] Example: 1$ = ` 65 Explanation: Bank buys 1$ at ` 65. Bank sells 1$ at ` 65. Two-way Quote: [when Bid and Ask Rate are separately given] Example: 1$ = ` ` 65 Left Hand Side Bid Rate/ Bank Buying Ask Rate/ Bank Selling Currency rate of left hand currency rate of left hand currency Note: Difference between Bid & Ask rate represents Profit Margin for the bank. Quotation/ Bid & Ask rate or Exchange Rate is always quoted from the point of view of bank. Bid Rate must always be less than Ask Rate. Or Ask Rate must always be greater than Bid Rate. Always solve question from the point of view of investor/ Customer unless otherwise stated. The difference between the Ask & Bid rates is called Spread, representing the profit margin of dealer. Spread = Ask Rate Bid Rate Concept No. 4: Direct Quote & Indirect Quote Direct Quote: Home Currency Price for 1 unit of foreign currency. Example: 1$ = ` 65 is DQ for Rupee.

8 8 Indirect Quote: Foreign Currency Price for 1 unit of Home Currency. Example: 1Re = $ is IDQ for Rupee. Note: If a given quotation is direct for one country, then the same quotation will be indirect for another country and vice-versa. Concept No. 5: Conversion of Direct Quote into Indirect Quote and vice-versa Case 1: One-way Quote [When bid & ask rates are same] Direct Quote can be converted into indirect quote by taking the reciprocal of direct quote. IDQ = 1 DQ Case 2: Two-way Quote [When bid & ask rates are separately given] Direct Quote (DQ) can be converted into Indirect Quote (IDQ) by taking the reciprocal of direct quote and switching the position. Example: $1 = ` ` (1 st Quote) Convert DQ into the IDQ. Solution: DQ => $1 = ` ` IDQ => 1 Re. = Re. = OR 1 Re. = (2 nd Quote) Conversion Rules : 1. Which currency is given in the question, we need that currency in the LHS of the quote. 2. Decide whether to Buy that currency or Sell. 3. If you Buy Bank Sells Use Ask R If you Sell Bank Buys Use Bid Rate 4. Always Solve question from the point of view of Customer. Concept No. 6: Spot Rate & Forward Rate Spot Rate: Rate used for buying & selling of foreign currency at As on Today or Immediately Forward rate: Rate used for buying & selling of foreign currency at some future Date i.e. Forward rate is the rate contracted today for exchange of currencies at a specified future date.

9 Concept No. 7: Premium or Discount 9 Premium: If the currency is costly or Expensive in future as compared to spot it is said to be at a premium. SR => 1$ = ` 45 FR => 1$ = ` 50 In the above quote $ is at Premium. Discount: If the currency is Cheaper in future as compared to spot it is said to be at a discount. SR => 1Re. = 1 45 $ = FR => 1Re. = 1 50 $ = 0.02 We can say that rupee is at discount. Calculation of Premium or Discount of left hand side Currency [ FR SR SR ] 12 Forward Period 100 Note: This formula is applicable only for left hand currency Conclusion: If one currency is at a premium, then another currency must be at a discount. However, the rate of premium may not be equal to the rate of discount. On account of base effect, premium is slightly higher than the discount. Concept No. 8 : Calculation of Forward Rate when Spot Rate & Premium or Discount is given Example 1: SR 1$ = ` $ is at premium = 5% Calculate FR? Solution: FR 1$ = ` ( ) 1$ = ` Concept No. 9 : SWAP POINTS/ Forward Margin/ Forward-Spot Differential Difference between Forward Rate and Spot Rate is known as Swap Points. How to ADD or DEDUCT Swap Points Swap Point should be Added or Deducted from the last decimal point in the Reverse Order. Premium Add Swap Points Discount Less Swap Points

10 10 If Premium / Discount is not mentioned, we observe the following rules: Case 1: When Swap Points are in increasing order: It indicates premium on left hand currency. In this case, we will add swap points with spot rates to calculate forward rates. Case 2: When Swap Points are in decreasing order: It indicates discount on left hand currency. In this case, we will deduct swap points from Spot Rate to calculate forward rates. Note Don t apply the rule if Premium or Discount is used in the question. Concept No. 10: Cross Rate Cross Rate between ant two currencies is derived with the help of quotations between these currencies & third currency. Cross Rate is normally used in finding out any missing exchange rate. The calculation of cross rate simply requires you to focus on cancellation of common currencies, to do so you have to multiply with DQ & IDQ. Always check ASK Rate > BID Rate. Concept No. 11: Squaring-up the position or Covering the Position or Closing-out the Position under FOREX Covering the Position means taking an opposite or reverse position to calculate profit and loss i.e. we cover our position to book Profit or Loss. Concept No. 12: Exchange Margin Long Position To Cover Short Position Short Position Long Position Exchange Margin is the extra amount or percentage charged by the bank over and above the rate quoted by it. Eg. Commission, transaction charges, etc. Actual Selling Rate of Bank: (Add Exchange Margin) = Ask Rate (1+ Exchange Margin) Actual Buying Rate of Bank: (Deduct Exchange Margin) = Bid Rate (1 Exchange Margin) Concept No. 13: Triangular Arbitrage It involves 3 currencies represented by 3 corner points of triangle. We will be starting with one currency, pass through the other two currencies and come back to the original currency. There are two paths clockwise and Anticlockwise One path will result in profit while the other path will result in Loss.

11 11 Concept No. 14: Purchasing Power Parity Theory (PPPT) Calculation of Spot Rate PPPT is based on the concept of Law of One Price. PPPT is based on the fact that price of a commodity in two different market will always be same. If Price of a commodity in two different market are not same, there will be an arbitrage opportunity exists in the market. Suppose Price of a Commodity in India is ` X & In USA is $Y. Spot Rate is 1$ = ` SR Then X = Y SR SR = X Y Exchange Rate = Price Ratio Spot Rate (` / $) = Current Price (Rs.) Current Price ($) Calculation of Forward Rate PPPT is also applicable in case of inflation. Suppose Inflation Rate of India is I Rs and in US is I $ Forward Rate 1$ = ` F. Now as per PPPT, we have after 1 year: X (1+ I`) = y (1+ I $ ) FR FR = X (1+ I Rs) Y (1+ I $ ) FR = SR 1+ I Rs 1+ I $ Note: FR (Rs./$) SR (Rs./$) = 1+Rupee Inflation 1+Dollar ($)Inflation The above equation is applicable for any two given currency. Determination of Premium or Discount with the help of Inflation Rate: If Inflation Rate of a country is higher, then the currency of that Country will be at a discount in future and Vice- Versa. Inflation rate in above equation must be adjusted according to forward period. Case1: When Period is less than 1 Year. FR (Rs./$) SR (Rs./$) = 1+Periodic Inflation Rate ( Rs.) 1+Periodic Inflation Rate ( $ ) Case2: When Period is more than 1 Year. n FR (Rs./$) (1+ Inflation Rate (Rs.)) = SR (Rs./$) (1+ Inflation Rate ($)) n Concept No. 15: Interest Rate Parity Theory (IRPT) IRPT states that exchange rate between currencies are directly affected by their Interest Rate. Assumption: Investment opportunity in any two different market will always be same. Formulae: FR (Rs./$) 1+Interest Rate (Rs.) = SR (Rs./$) 1+Interest Rate ($) Note: The above equation is applicable for any two given currency. Interest Rate should be adjusted according to forward period. Determination of Premium or Discount with the help of Interest Rate: If Interest rate of a country is higher, than the currency of that country will be at a discount in future and vice-versa. If IRPT holds, arbitrage is not possible. In that case, it doesn t matter whether you invest in domestic country or foreign country, your rate of return will be same.

12 Concept No. 16: Covered Interest Arbitrage 12 Type 1 Type 2 When Bid and Ask rates are same. If Bid & Ask rates are given separately. When Investment & Borrowing rates are same in one country. Investment & Borrowing rate of a given currency is separately given. # (Short cut is available) # (Hit & Trial method is used) When Investment opportunity in any two given countries are different, covered Interest Arbitrage is possible. When IRPT is not applicable, then covered interest arbitrage will be applicable. The rule is to Borrow from one country & Invest in another Country. Suppose Interest Rate of India is INT` And USA is INT $. Spot Rate is 1$ = ` SR, Forward Rate => 1$ = ` FR Let assume Investor is having ` A for investment Option 1: When investor invest ` A in India: Amount of ` Received after one year Option 2: When investor invest ` A in USA: Amount of Equivalent ` Received after one year A 1 = A (1 + INT`) A 2 = [ A $ (1 + INT$)] FR SR IF A 1 = A 2 IF A 1 > A 2 IF A 1 < A 2 No arbitrage opportunity. Arbitrage Opportunity is Possible. Arbitrager should invest in India (Home Country) & borrow from USA (Foreign Country) Arbitrage opportunity is possible. Arbitrager should invest in USA (Foreign Country) & borrow from India (Home Country) Note:If in 1 st try we have arbitrage profit, then no need to solve 2 nd case. If in 1 st try we have arbitrage loss, then 2 nd case must be solved. Concept No. 17: Forward Contract Transaction exposure arises when a firm has a known amount of foreign currency payable or receivable but home currency equivalent of which is unknown. Hedging is defined as an activity converted uncertainty into certainty. The simplest hedging strategy is hedging through forward contract. In case of foreign currency is to be received in future In case of foreign currency is to be Paid in future

13 Concept No. 18: Money Market Operations 13 Case 1 : If Foreign Currency is to be received in future: Step 1: Borrow in Foreign Currency: Amount of borrowing should be such that Amount Borrowed +Interest on it becomes equal to the amount to be received. Step 2: Convert the borrowed foreign currency into home currency by using spot Rate. Step 3: Invest this home currency amount for the required period. Step 4: Pay the borrowed amount of foreign currency with interest using the amount to be received in foreign currency. [May be Ignored] Case 2: Money Market Operation:- When foreign currency is to be paid in future Step 1: Invest in Foreign currency. Amount of investment should be such that, Amount Invested + Interest on it becomes equal to amount to be paid Step 2: Borrow in Home Currency, equivalent amount which is to be invested in foreign currency using Spot rate. Step 3: Pay the borrowed amount with interest in Home Currency on Maturity. Step 4: Pay the outstanding amount with the amount received from investment. [May be ignored] Concept No. 19: Exposure Netting Netting means adjusting receivable and payables (or inflows & Outflows) Two conditions must be fulfilled: 1. Netting can be done for same currency. 2. Netting can be done for same period.

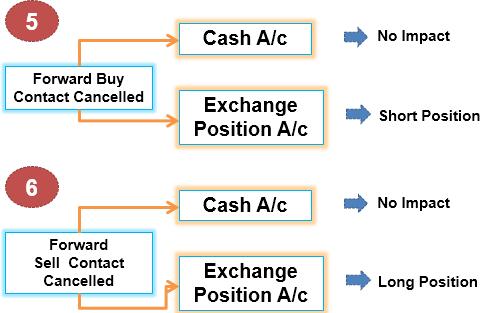

14 14 Note: In case of Netting, No. of forward contracts can be reduced. Concept No. 20: Adjusting Exchange rate quotation when exchange margin is attached to it Example: 1 Euro = ± Solution: 1 Euro = Concept No. 21: Modification under Forward Contract How to cancel Forward Contract Forward Contracts must be cancelled by entering into a reverse contract. Rate at which contract needs to be Cancelled a) Cancelled before due date: Forward Rate prevailing as on today for due date. b) Cancelled on due date: Spot Rate of Due Date. c) Cancelled after Due Date: Spot Rate of the date when customer contracted with the bank. d) Automatic Cancellation: Spot Rate prevailing on 15 th day i.e. when grace period ends. Settlement of Profit/Loss:

Cancel after due date or Customer will be eligible only for Loss Automatic Cancellation Concept No.")

Swap Difference b) Interest on Outlay of")

15 15 a) Cancel on or before due date Customer will be eligible for both profit/loss. b) Cancel after due date or Customer will be eligible only for Loss Automatic Cancellation Concept No. 22: Extension of Forward Contract Step 1: Cancellation of original Contract Step 2: Entering into a new forward contract for the extended period. Early Delivery The bank may accept the request of customer of delivery at the before due date of forward contract provided the customer is ready to bear the loss if any that may accrue to the bank as a result of this. In addition to some prescribed fixed charges bank may also charge additional charges comprising of: a) Swap Difference b) Interest on Outlay of Funds Cancellation after Due Date/ Automatic Cancellation Late Delivery / Extension after due date In these cases the following cancellation charges may be payable: 1. Exchange Difference 2. Swap Loss

16 16 3. Interest on outlay of funds Concept No. 23: Foreign Capital Budgeting Two approaches are followed in case investment is undertaken in foreign country: 1. Home Currency Approach 2. Foreign Currency Approach Home Currency Approach: Step 1: Compute all cash inflows & outflows arising in foreign currency. Step 2: Convert these cash Inflows & outflows into home currency by using appropriate exchange rates (i.e. Forward Rate) (Calculate through Swap Point or IRPT) Step 3: Compute a suitable discount rate. Step 4: Compute Home Currency (NPV) Foreign Currency Approach: Step 1: Compute all cash inflows & outflows arising in foreign currency. Step 2: Compute a suitable discount rate ( RADR). Step 3: Compute Foreign Currency (NPV) Step 4: Convert foreign currency NPV into Home currency by using Spot Rate Note: Answer by both approach will be same. Discount Rate to be used should be risk-adjusted discount rate (RADR), Since foreign project involves risk. (1 + RADR) = (1 + Risk-free rate) (1 + Risk Premium) Discount Rate or RADR of both the country are different. Risk Premium of both home country and foreign country are assumed to be same. Concept No. 24: Centralized Cash Management & Decentralized Cash Management System Under Decentralized Cash Management, every branch is viewed as separate undertaking. Cash Surplus and Cash Deficit of each branch should not be adjusted. Under Centralized Cash Management, every branch cash position is managed by single centralized authority. Hence, Cash Surplus and Cash Deficit of each branch with each other is accordingly adjusted Concept No. 25: Contribution to Sales Ratio based decision under FOREX Contribution ( Sales VC) Contribution to Sales Ratio = Sales Decision: Higher the C/S Ratio, Better the position. 100

17 Concept No. 26: Leading & Lagging 17 Leading means advancing the timing of payments and receipts. Lagging means postponing or delaying the timing of payments and receipts. Note: While deciding regarding leading and lagging, we must consider Opportunity cost of interest if given in question. Concept No. 27: Currency Pairs Currency Pairs are written by ISO Currency codes of the base currency and the counter currency, separating them with a slash character. Example: A price quote of EUR/USD at means 1 Euro = $ Concept No. 28: Gain/Loss under FOREX Concept No. 29: Evaluation of Quotation from two Banks When quotations are received from two banks, customer should select that quotation which is more beneficial to him. Example:

18 Concept No. 30: Expected Spot Rate 18 Concept No. 31: Currency Futures Spot Rates Probability = Expected Spot Rate

19 19 Concept No. 32: Currency Options

= [1 + P 1 P 0 + I ] (1+ C) 1 P 0 P 0 = Price at the beginning P 1 = Price at the End I = Income from Interest/Dividend C =")

20 20 Concept No. 33: Calculation of Return under FOREX Return (In terms of Home Currency) = [1 + P 1 P 0 + I ] (1+ C) 1 P 0 P 0 = Price at the beginning P 1 = Price at the End I = Income from Interest/Dividend C = Change in exchange rate. Concept No. 34: Broken Date Contracts A Broken Date Contract is a forward contract for which quotation is not readily available. Example: If quotes are available for 1 month and 3 months but a customer wants a quote for 2 months, it will be a Broken Date Contract. It can be calculated by interpolating between the available quotes for the preceding and succeeding maturities. Concept No. 35: International Fisher Effect International Fisher Effect reflect the relationship between real interest rate, inflation rate and nominal interest rate. Equation: (1+ Nominal Interest Rate) = (1+ Real Interest Rate) (1+ Inflation Rate)

21 21 Concept No. 36: Implied Differential in Interest Rate Interest rate is just another name of premium or discount of one country currency in relation to another country currency (As per IRPT). Premium or Discount = Difference in Interest Rate Equation: FR (Rs./$) SR(Rs./$) = SR = Interest Rate (`) Interest Rate($) Forward Period Concept No. 37: Savings due to Time Value (Discount) & Currency Fluctuation If the firm decides to pay today rather than in future he may get two types of benefits: (i) Benefit on account of discount for pre-payment. (ii) Benefit on account of currency fluctuation.

22 OTC Derivative 22 Concept No. 38: Forward Rate Agreement (FRA) A forward rate Agreement can be viewed as a forward contract to borrow/lend money at a certain rate at some future date. These Contracts settle in cash. The long position in an FRA is the party that would borrow the money. If the floating rate at contract expiration is above the rate specified in the forward agreement, the long position in the contract can be viewed as the right to borrow at below market rates & the long will receive a payment. If reference rate at the expiration date is below the contract rate, the short will receive a cash from the long. FRA helps borrower to eliminate interest rate risk associated with borrowing or investing funds. Adverse movement in the interest rates will not affect liability of the borrower. Payment to the long at settlement is: Notional Principal [Floating (LIBOR) Forward Rate] days Floating rate (LIBOR) days 360

23 Example: 23 Consider an FRA that: Expires/Settles in 30 days. Is based on notional principal amount of $ 1 million. Is based on 90 days LIBOR. Specifies a forward Rate of 5% Assume that actual 90 days LIBOR 30 days from now (at expiration) is 6%. Compute the cash settlement payment at expiration and identify at which party makes the payment. Solution: If the long could borrow at contract rate of 5% rather than the market rate of 6%, the interest saved on a 90 day $ 1 million loan would be: ( ) (90 / 360) 1 million = million = $ 2,500 The $ 2,500 in interest savings would not come until the end of the 90 days loan period. The value at settlement is the present value of these savings. The correct discount rate to use is the actual rate at settlement, 6%, not the contract rate of 5%. The payment at settlement date from the short to the long is: [(0.06) ] = $ 2,

24 24 Step 2 : Decide from where we should borrow and where should we invest Step 3 : Calculation of Arbitrage Profit Example: Suppose 3 months borrowing/ deposit rate = 8% 6 months borrowing/ deposit rate = 10% 3 months FR 3 months from now = 12% Check the Arbitrage Possibility? Solution: 3 Months = 8% Actual 3 months FR 3 months from now = 12% 6 months = 10% FIRST CALCULATE FAIR 3 MONTHS FR 3 MONTHS FROM NOW & COMPARE IT WITH ACTUAL RATE. (1 + 3 month rate) (1 + 3 month FR 3 months from now) = ( months FR) ( ) (1 + r % 3 ) = ( ) 12 Hence Fair 3 months FR 3 months from now is Suppose Notional amount = ` 100 Arbitrage gain = 100 {[12% %] 3 } = = 11.76% p.a 1) Borrowing for 6 10% 2) 8% for 3 months. 3) Further 12% for next 3 months 4) Arbitrage Gain. Deposit: 100 ( ) ( ) = Borrow: 100 ( ) 12 = Arbitrage Gain = 0.06 FRA Quotation: Suppose 3 9 FRA (Quoted by Bank) = 8% % Lending Rate Borrowing Rate FRA buying Rate for Bank FRA selling Rate for Bank FRA selling Rate for Customer FRA buying Rate for Customer

25 Concept No. 39: Currency SWAP Swap Initiation 25 The Australian firm wants USD Has or can Borrow AUD Swap Interest Payments Swap AUD for USD Swap USD for AUD The U.S firm wants AUD Has or can Borrow USD The Australian firm has use of the USD Swap Termination USD The Australian returned firm returns the USD borrowed Australian pays USD interest U.S firm pays AUD interest USD returned AUD returned The U.S firm has use of the AUD The U.S firm returns the AUD borrowed Concept No. 40: Interest Rate Swap [ Two Party] Two parties exchange their interest rate obligation. The plain vanilla interest rate swap involves trading fixed interest rate payments for floating rate payments. The party who wants fixed-rate interest payments agrees to pay fixed-rate interest. The Counter party, who receives the fixed payments agrees to pay variable-rate interest/floating rate interest. The difference between the fixed rate payment and the floating rate payment is calculated and paid to the appropriate counterparty. Net interest is paid by the one who owes it. Swaps are zero-sum game. What one party gains, the other party losses. The Net formulae for the Fixed-Rate payer, based on a 360-day year and a floating rate of LIBOR is: (Net Fixed Rate Payment) t = [Swap Fixed Rate LIBOR t-1] [ No.of Days 360 ] [National Principal]

26 26 Concept No. 41: Interest Rate Caps, Floor & Collar Interest Rate Cap: CAP Maximum Rate Borrowings Floating Rate FLOOR Minimum Rate Investments Floating Rate Interest Rate Cap: (Maximum Rate For Floating ) If a firm borrows at floating rate, it is afraid of interest rate rising, to hedge against the same, it will buy an interest rate cap i.e. Long call at X=Cap rate It is a series/portfolio of interest rate Call option on interest rates. Each particular call option being called a CAPLET. Caps pay when rate rises above the cap rate. Interest Rate Floor: Interest Rate Floor: Minimum Rate For Floating ) If a firm invest at floating rate, it is afraid of interest rate falling, to hedge against the same, it will buy an interest rate Floor i.e. Long put at X=Floor rate It is a series/portfolio of Interest rate put Option on interest rate. Such particular put option being called a FLOORLET Floor pays when rate falls below the Floor Rate. Interest Rate Collar: It is a combination of a Cap and a Floor. Premium paid on one option would be compensated with the premium received on selling another option. If premium paid on caps is equal to the premium received on floor, then it would be called Zero Cost Collar.

27 27 A floating rate borrower may buy a cap [C + ] & simultaneously sells a floor i.e.[p].initial outflow will reduce.( C + =Long Call & P - =Short Put) Similarly, a floating rate investor may buy a Floor (P + ) & simultaneously sell a Cap (C - ). Initial outflow will reduce.(p + =Long Put & C - =Short Call) Concept No. 42: Nostro Account, Vostro Account and LORO Account 1. Nostro Account [Ours account with you] This is a current account maintained by a domestic bank/dealer with a foreign bank in foreign currency. Example: Current account of SBI bank (an Indian Bank) with swizz bank in Swizz Franc. (CHF) is a Nastro account. Indian Bank Swizz Bank Nostro Account of Indian Bank 2. Vostro Account [Yours account with us] This is a current account maintained by a foreign bank with a domestic bank/dealer in Rupee currency. Example: Current account of Swizz bank in India with SBI bank in Rupee (`) currency. Indian Bank Swizz Bank Vastro Account of Swizz Bank

![28 3. Loro Account [Our account of their Money with you] This is a current account maintained by one domestic bank on behalf of other domestic bank in foreign bank in a foreign currency.](/docs-images/81/83720220/images/28-0.jpg "In other words, Loro account is a Nastro account for one bank who opened the bank and Loro account for other bank who refers first one account. Example: SBI opened Current account with swizz bank.")

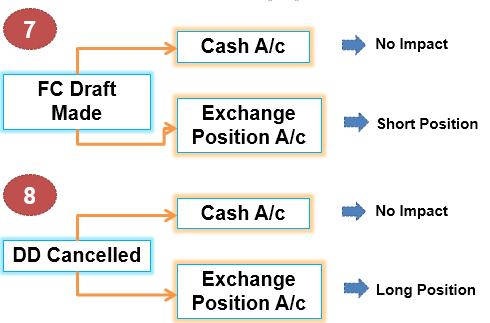

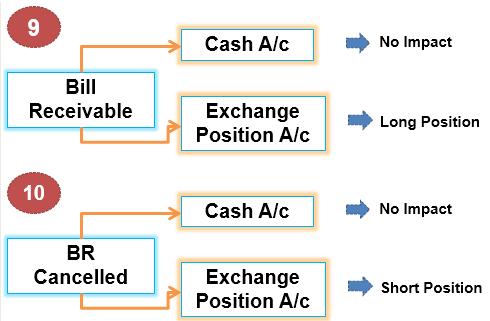

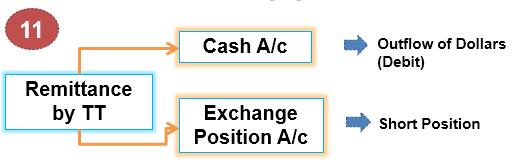

28 28 3. Loro Account [Our account of their Money with you] This is a current account maintained by one domestic bank on behalf of other domestic bank in foreign bank in a foreign currency. In other words, Loro account is a Nastro account for one bank who opened the bank and Loro account for other bank who refers first one account. Example: SBI opened Current account with swizz bank. If PNB refers that account of SBI for its correspondence, then it is called Loro account for PNB and it is Nostro account for SBI. SBI PNB Swizz Bank 1. Nostro Account of SBI 2. PNB refers a/c of SBI for its transaction then it is called Loro account for PNB. Note: SPOT purchase/sale of GHF affects both exchange position as well as Nostro account. However, forward purchase/sale affects only the exchange position. Nostro A/c (Cash A/c) in Foreign Currency

29 29

30 30

STRATEGIC FINANCIAL MANAGEMENT FOREX & OTC Derivatives Summary By CA. Gaurav Jain

1 SFM STRATEGIC FINANCIAL MANAGEMENT FOREX & OTC Derivatives Summary By CA. Gaurav Jain 100% Conceptual Coverage With Live Trading Session Complete Coverage of Study Material, Practice Manual & Previous

1 SFM STRATEGIC FINANCIAL MANAGEMENT FOREX & OTC Derivatives Summary By CA. Gaurav Jain 100% Conceptual Coverage With Live Trading Session Complete Coverage of Study Material, Practice Manual & Previous

CA - FINAL INTEREST RATE RISK MANAGEMENT. FCA, CFA L3 Candidate

CA - FINAL INTEREST RATE RISK MANAGEMENT FCA, CFA L3 Candidate 9.1 Interest Rate Risk Management Study Session 9 LOS 1: Forward Rate Agreement (FRA) A forward rate Agreement can be viewed as a forward

CA - FINAL INTEREST RATE RISK MANAGEMENT FCA, CFA L3 Candidate 9.1 Interest Rate Risk Management Study Session 9 LOS 1: Forward Rate Agreement (FRA) A forward rate Agreement can be viewed as a forward

Swaps: A Primer By A.V. Vedpuriswar

Swaps: A Primer By A.V. Vedpuriswar September 30, 2016 Introduction Swaps are agreements to exchange a series of cash flows on periodic settlement dates over a certain time period (e.g., quarterly payments

Swaps: A Primer By A.V. Vedpuriswar September 30, 2016 Introduction Swaps are agreements to exchange a series of cash flows on periodic settlement dates over a certain time period (e.g., quarterly payments

CHAPTER 29 DERIVATIVES

CHAPTER 29 DERIVATIVES 1 CHAPTER 29 DERIVATIVES INDEX Para No TOPIC Page No 29 Introduction 3 29 1 Foreign Currency Option 3 29 2 Foreign Currency Rupee Swaps 4 29 2 1 SWAPS 5 29 2 2 Currency Swaps 5 29

CHAPTER 29 DERIVATIVES 1 CHAPTER 29 DERIVATIVES INDEX Para No TOPIC Page No 29 Introduction 3 29 1 Foreign Currency Option 3 29 2 Foreign Currency Rupee Swaps 4 29 2 1 SWAPS 5 29 2 2 Currency Swaps 5 29

Financial Derivatives

Derivatives in ALM Financial Derivatives Swaps Hedge Contracts Forward Rate Agreements Futures Options Caps, Floors and Collars Swaps Agreement between two counterparties to exchange the cash flows. Cash

Derivatives in ALM Financial Derivatives Swaps Hedge Contracts Forward Rate Agreements Futures Options Caps, Floors and Collars Swaps Agreement between two counterparties to exchange the cash flows. Cash

NIRAJ THAPA FOREX. Foreign exchange constitutes the largest financial market in the world.

NIRAJ THAPA ON FOREX niraj_thapa@hotmail.com Foreign exchange constitutes the largest financial market in the world. TIM Weithers : Foreign Exchange:-It s not difficult; It s just confusing Contents Topic

NIRAJ THAPA ON FOREX niraj_thapa@hotmail.com Foreign exchange constitutes the largest financial market in the world. TIM Weithers : Foreign Exchange:-It s not difficult; It s just confusing Contents Topic

Introduction to Foreign Exchange. Education Module: 1

Introduction to Foreign Exchange Education Module: 1 Dated July 2002 Part 1 Spot Market Definition of a Foreign Exchange Rate A foreign exchange rate is the price at which one currency can be bought or

Introduction to Foreign Exchange Education Module: 1 Dated July 2002 Part 1 Spot Market Definition of a Foreign Exchange Rate A foreign exchange rate is the price at which one currency can be bought or

Derivative Instruments

Derivative Instruments Paris Dauphine University - Master I.E.F. (272) Autumn 2016 Jérôme MATHIS jerome.mathis@dauphine.fr (object: IEF272) http://jerome.mathis.free.fr/ief272 Slides on book: John C. Hull,

Derivative Instruments Paris Dauphine University - Master I.E.F. (272) Autumn 2016 Jérôme MATHIS jerome.mathis@dauphine.fr (object: IEF272) http://jerome.mathis.free.fr/ief272 Slides on book: John C. Hull,

Foreign Exchange Risk Management

C H A P T E R 2 Foreign Exchange Risk Management Coverage of FOREX in Past Examinations: Year May-2012 Nov-2011 May- 2011 SFM (New) MAFA (Old) 8+10(Theory) =18 11+8(With derivative)=19 Nov- 2010 NA NA

C H A P T E R 2 Foreign Exchange Risk Management Coverage of FOREX in Past Examinations: Year May-2012 Nov-2011 May- 2011 SFM (New) MAFA (Old) 8+10(Theory) =18 11+8(With derivative)=19 Nov- 2010 NA NA

NISM-Series-I: Currency Derivatives Certification Examination

SAMPLE QUESTIONS 1) The market where currencies are traded is known as the. (a) Equity Market (b) Bond Market (c) Fixed Income Market (d) Foreign Exchange Market 2) The USD/CAD (US Canadian Dollars) currency

SAMPLE QUESTIONS 1) The market where currencies are traded is known as the. (a) Equity Market (b) Bond Market (c) Fixed Income Market (d) Foreign Exchange Market 2) The USD/CAD (US Canadian Dollars) currency

S. No. Chapter Clip Name Total Time (min.) A INTRODUCTION 01 Clip - Introduction 14:39 02 Clip 15:29 03 Clip 27:47 04 Clip 10:57 05 Clip 25:06

A INTRODUCTION 01 Clip - Introduction 14:39 02 Clip 15:29 03 Clip 27:47 04 Clip 10:57 05 Clip 25:06") S. No. Chapter Clip Name Total Time (min.) A INTRODUCTION 01 Clip - Introduction 14:39 02 Clip 15:29 03 Clip 27:47 04 Clip 10:57 05 Clip 25:06 Total 92.78 B TIME VALUE OF MONEY 06 Clip - TVM 43:33 C SECURTIY

S. No. Chapter Clip Name Total Time (min.) A INTRODUCTION 01 Clip - Introduction 14:39 02 Clip 15:29 03 Clip 27:47 04 Clip 10:57 05 Clip 25:06 Total 92.78 B TIME VALUE OF MONEY 06 Clip - TVM 43:33 C SECURTIY

PRIME ACADEMY PVT LTD

ii STRATEGIC FINANCIAL MANAGEMENT Solutions to the November 2017 Strategic Financial Management Exam Question 1(a): 5 Marks SBI mutual fund has a NAV of Rs 8.50 at the beginning of the year. At the end

ii STRATEGIC FINANCIAL MANAGEMENT Solutions to the November 2017 Strategic Financial Management Exam Question 1(a): 5 Marks SBI mutual fund has a NAV of Rs 8.50 at the beginning of the year. At the end

Financial Markets & Risk

Financial Markets & Risk Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Session 3 Derivatives Binomial

Financial Markets & Risk Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Session 3 Derivatives Binomial

MCQ on International Finance

MCQ on International Finance 1. If portable disk players made in China are imported into the United States, the Chinese manufacturer is paid with a) international monetary credits. b) dollars. c) yuan,

MCQ on International Finance 1. If portable disk players made in China are imported into the United States, the Chinese manufacturer is paid with a) international monetary credits. b) dollars. c) yuan,

Efficacy of Interest Rate Futures for Corporate

Efficacy of Interest Rate Futures for Corporate The financial sector, corporate and even households are affected by interest rate risk. Interest rate fluctuations impact portfolios of banks, insurance

Efficacy of Interest Rate Futures for Corporate The financial sector, corporate and even households are affected by interest rate risk. Interest rate fluctuations impact portfolios of banks, insurance

Interest Rate Risk Management

Interest Rate Risk Management Product Features Booklet Dated 15 May 2014 Issued by Suncorp-Metway Ltd ABN 66 010 831 722 AFSL Number 229882 Level 28, Brisbane Square 266 George Street Brisbane QLD 4000

Interest Rate Risk Management Product Features Booklet Dated 15 May 2014 Issued by Suncorp-Metway Ltd ABN 66 010 831 722 AFSL Number 229882 Level 28, Brisbane Square 266 George Street Brisbane QLD 4000

FOREIGN EXCHANGE RISK MANAGEMENT

FOREIGN EXCHANGE RISK MANAGEMENT 1 RISKS BEING COVERED Foreign Exchange Risk Management primarily tries to mitigate the Exchange rate risk arising out on the risk of an investment's value changing due

FOREIGN EXCHANGE RISK MANAGEMENT 1 RISKS BEING COVERED Foreign Exchange Risk Management primarily tries to mitigate the Exchange rate risk arising out on the risk of an investment's value changing due

FOREIGN EXCHANGE MARKET. Luigi Vena 05/08/2015 Liuc Carlo Cattaneo

FOREIGN EXCHANGE MARKET Luigi Vena 05/08/2015 Liuc Carlo Cattaneo TABLE OF CONTENTS The FX market Exchange rates Exchange rates regimes Financial balances International Financial Markets 05/08/2015 Coopeland

FOREIGN EXCHANGE MARKET Luigi Vena 05/08/2015 Liuc Carlo Cattaneo TABLE OF CONTENTS The FX market Exchange rates Exchange rates regimes Financial balances International Financial Markets 05/08/2015 Coopeland

Lecture 2. Agenda: Basic descriptions for derivatives. 1. Standard derivatives Forward Futures Options

Lecture 2 Basic descriptions for derivatives Agenda: 1. Standard derivatives Forward Futures Options 2. Nonstandard derivatives ICON Range forward contract 1. Standard derivatives ~ Forward contracts:

Lecture 2 Basic descriptions for derivatives Agenda: 1. Standard derivatives Forward Futures Options 2. Nonstandard derivatives ICON Range forward contract 1. Standard derivatives ~ Forward contracts:

Swaps 7.1 MECHANICS OF INTEREST RATE SWAPS LIBOR

7C H A P T E R Swaps The first swap contracts were negotiated in the early 1980s. Since then the market has seen phenomenal growth. Swaps now occupy a position of central importance in derivatives markets.

7C H A P T E R Swaps The first swap contracts were negotiated in the early 1980s. Since then the market has seen phenomenal growth. Swaps now occupy a position of central importance in derivatives markets.

[SEMINAR ON SFM CA FINAL]

![[SEMINAR ON SFM CA FINAL]](/thumbs/89/98739560.jpg "[SEMINAR ON SFM CA FINAL]") 2013 Archana Khetan B.A, CFA (ICFAI), MS Finance, 9930812721, archana.khetan090@gmail.com [SEMINAR ON SFM CA FINAL] Derivatives A derivative is a financial contract which derives its value from some under

2013 Archana Khetan B.A, CFA (ICFAI), MS Finance, 9930812721, archana.khetan090@gmail.com [SEMINAR ON SFM CA FINAL] Derivatives A derivative is a financial contract which derives its value from some under

CS Professional Programme Module - II (New Syllabus) (Solution of June ) Paper - 5: Financial, Treasury and Forex Management

(Solution of June ) Paper - 5: Financial, Treasury and Forex Management") Solved Scanner Appendix CS Professional Programme Module - II (New Syllabus) (Solution of June - 2015) Paper - 5: Financial, Treasury and Forex Management Chapter - 1: Nature, Significance and Scope of

Solved Scanner Appendix CS Professional Programme Module - II (New Syllabus) (Solution of June - 2015) Paper - 5: Financial, Treasury and Forex Management Chapter - 1: Nature, Significance and Scope of

TEACHING NOTE 01-02: INTRODUCTION TO INTEREST RATE OPTIONS

TEACHING NOTE 01-02: INTRODUCTION TO INTEREST RATE OPTIONS Version date: August 15, 2008 c:\class Material\Teaching Notes\TN01-02.doc Most of the time when people talk about options, they are talking about

TEACHING NOTE 01-02: INTRODUCTION TO INTEREST RATE OPTIONS Version date: August 15, 2008 c:\class Material\Teaching Notes\TN01-02.doc Most of the time when people talk about options, they are talking about

Interest Rate Futures Products for Indian Market. By Golaka C Nath

Interest Rate Futures Products for Indian Market By Golaka C Nath Interest rate derivatives have been widely used in international markets by banks, institutions, corporate sector and common investors.

Interest Rate Futures Products for Indian Market By Golaka C Nath Interest rate derivatives have been widely used in international markets by banks, institutions, corporate sector and common investors.

Currency Futures Trade on YieldX

JOHANNESBURG STOCK EXCHANGE YieldX Currency Futures Currency Futures Trade on YieldX Currency futures are traded on YieldX, the JSE s interest rate market. YieldX offers an efficient, electronic, automatic

JOHANNESBURG STOCK EXCHANGE YieldX Currency Futures Currency Futures Trade on YieldX Currency futures are traded on YieldX, the JSE s interest rate market. YieldX offers an efficient, electronic, automatic

FIN 684 Fixed-Income Analysis Swaps

FIN 684 Fixed-Income Analysis Swaps Professor Robert B.H. Hauswald Kogod School of Business, AU Swap Fundamentals In a swap, two counterparties agree to a contractual arrangement wherein they agree to

FIN 684 Fixed-Income Analysis Swaps Professor Robert B.H. Hauswald Kogod School of Business, AU Swap Fundamentals In a swap, two counterparties agree to a contractual arrangement wherein they agree to

OPTION MARKETS AND CONTRACTS

NP = Notional Principal RFR = Risk Free Rate 2013, Study Session # 17, Reading # 63 OPTION MARKETS AND CONTRACTS S = Stock Price (Current) X = Strike Price/Exercise Price 1 63.a Option Contract A contract

NP = Notional Principal RFR = Risk Free Rate 2013, Study Session # 17, Reading # 63 OPTION MARKETS AND CONTRACTS S = Stock Price (Current) X = Strike Price/Exercise Price 1 63.a Option Contract A contract

Lecture 3: Interest Rate Forwards and Options

Lecture 3: Interest Rate Forwards and Options 01135532: Financial Instrument and Innovation Nattawut Jenwittayaroje, Ph.D., CFA NIDA Business School 1 Forward Rate Agreements (FRAs) Definition A forward

Lecture 3: Interest Rate Forwards and Options 01135532: Financial Instrument and Innovation Nattawut Jenwittayaroje, Ph.D., CFA NIDA Business School 1 Forward Rate Agreements (FRAs) Definition A forward

Fx Derivatives- Simplified CA NAVEEN JAIN AUGUST 1, 2015

1 Fx Derivatives- Simplified CA NAVEEN JAIN AUGUST 1, 2015 Agenda 2 History of Fx Overview of Forex Markets Understanding Forex Concepts Hedging Instruments RBI Guidelines Current Forex Markets History

1 Fx Derivatives- Simplified CA NAVEEN JAIN AUGUST 1, 2015 Agenda 2 History of Fx Overview of Forex Markets Understanding Forex Concepts Hedging Instruments RBI Guidelines Current Forex Markets History

Determining Exchange Rates. Determining Exchange Rates

Determining Exchange Rates Determining Exchange Rates Chapter Objectives To explain how exchange rate movements are measured; To explain how the equilibrium exchange rate is determined; and To examine

Determining Exchange Rates Determining Exchange Rates Chapter Objectives To explain how exchange rate movements are measured; To explain how the equilibrium exchange rate is determined; and To examine

PROF. RAHUL MALKAN CONTACT NO

CA - FINAL SFM - COMPILER FOREX PROF. RAHUL MALKAN WWW.RAHULMALKAN.COM CONTACT NO - 8369095160 2 SFM - COMPILER Forex Years May Nov RTP Paper RTP Paper 2008 NA NA Yes Yes 2009 Yes YES Yes Yes 2010 Yes

CA - FINAL SFM - COMPILER FOREX PROF. RAHUL MALKAN WWW.RAHULMALKAN.COM CONTACT NO - 8369095160 2 SFM - COMPILER Forex Years May Nov RTP Paper RTP Paper 2008 NA NA Yes Yes 2009 Yes YES Yes Yes 2010 Yes

Glossary of Swap Terminology

Glossary of Swap Terminology Arbitrage: The opportunity to exploit price differentials on tv~otherwise identical sets of cash flows. In arbitrage-free financial markets, any two transactions with the same

Glossary of Swap Terminology Arbitrage: The opportunity to exploit price differentials on tv~otherwise identical sets of cash flows. In arbitrage-free financial markets, any two transactions with the same

PAPER 2 : STRATEGIC FINANCIAL MANAGEMENT. Answers all the Questions

Question 1 (a) (b) PAPER : STRATEGIC FINANCIAL MANAGEMENT Answers all the Questions Following information is available for X Company s shares and Call option: Current share price Option exercise price

Question 1 (a) (b) PAPER : STRATEGIC FINANCIAL MANAGEMENT Answers all the Questions Following information is available for X Company s shares and Call option: Current share price Option exercise price

Financial Markets and Products

Financial Markets and Products 1. Which of the following types of traders never take position in the derivative instruments? a) Speculators b) Hedgers c) Arbitrageurs d) None of the above 2. Which of the

Financial Markets and Products 1. Which of the following types of traders never take position in the derivative instruments? a) Speculators b) Hedgers c) Arbitrageurs d) None of the above 2. Which of the

Swap Markets CHAPTER OBJECTIVES. The specific objectives of this chapter are to: describe the types of interest rate swaps that are available,

15 Swap Markets CHAPTER OBJECTIVES The specific objectives of this chapter are to: describe the types of interest rate swaps that are available, explain the risks of interest rate swaps, identify other

15 Swap Markets CHAPTER OBJECTIVES The specific objectives of this chapter are to: describe the types of interest rate swaps that are available, explain the risks of interest rate swaps, identify other

Efficacy of Interest Rate Futures for Retail

Efficacy of Interest Rate Futures for Retail The financial sector, corporate and even households are affected by interest rate risk. Interest rate fluctuations impact portfolios of banks, insurance companies,

Efficacy of Interest Rate Futures for Retail The financial sector, corporate and even households are affected by interest rate risk. Interest rate fluctuations impact portfolios of banks, insurance companies,

GLOSSARY OF TERMS -A- ASIAN SESSION 23:00 08:00 GMT. ASK (OFFER) PRICE

PRICE") GLOSSARY OF TERMS -A- ASIAN SESSION 23:00 08:00 GMT. ASK (OFFER) PRICE The price at which the market is prepared to sell a product. Prices are quoted two-way as Bid/Ask. The Ask price is also known as

GLOSSARY OF TERMS -A- ASIAN SESSION 23:00 08:00 GMT. ASK (OFFER) PRICE The price at which the market is prepared to sell a product. Prices are quoted two-way as Bid/Ask. The Ask price is also known as

QUESTION NO.5A 1 USD= Rs USD = Yen 1.20;Find 1 Yen = Rs. QUESTION NO.6 Rs./$ = 48/49, DM/$ = 4/5,Find Rs/DM =.../...?

QUESTION NO.1A Consider the following Rs/S$ direct quote of ICICI Mumbai:26.50-75 (i)what is the cost of buying Rs. 55,000? (ii)how much would you receive by selling 92,000 rupees? (iii)what is the cost

QUESTION NO.1A Consider the following Rs/S$ direct quote of ICICI Mumbai:26.50-75 (i)what is the cost of buying Rs. 55,000? (ii)how much would you receive by selling 92,000 rupees? (iii)what is the cost

Mathematics of Financial Derivatives

Mathematics of Financial Derivatives Lecture 11 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. Mechanics of interest rate swaps (continued)

Mathematics of Financial Derivatives Lecture 11 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. Mechanics of interest rate swaps (continued)

Based on the following data, estimate the Net Asset Value (NAV) 1st July 2016 on per unit basis of a Debt Fund: Maturity Date.

1st July 2016 on per unit basis of a Debt Fund: Maturity Date.") MUTUAL FUND (VOL - 1) - { Page No. 198, Question No. 7} Based on the following data, estimate the Net Asset Value (NAV) 1st July 2016 on per unit basis of a Debt Fund: Name of Security 10.71% GOI 2028

MUTUAL FUND (VOL - 1) - { Page No. 198, Question No. 7} Based on the following data, estimate the Net Asset Value (NAV) 1st July 2016 on per unit basis of a Debt Fund: Name of Security 10.71% GOI 2028

Note 8: Derivative Instruments

Note 8: Derivative Instruments Derivative instruments are financial contracts that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity prices

Note 8: Derivative Instruments Derivative instruments are financial contracts that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity prices

Note 10: Derivative Instruments

Note 10: Derivative Instruments Derivative instruments are financial that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity prices or

Note 10: Derivative Instruments Derivative instruments are financial that derive their value from underlying changes in interest rates, foreign exchange rates or other financial or commodity prices or

Swap hedging of foreign exchange and interest rate risk

Lecture notes on risk management, public policy, and the financial system of foreign exchange and interest rate risk Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: March 18, 2018 2

Lecture notes on risk management, public policy, and the financial system of foreign exchange and interest rate risk Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: March 18, 2018 2

Currency Swap or FX Swapd Difinition and Pricing Guide

or FX Swapd Difinition and Pricing Guide Michael Taylor FinPricing An FX swap or currency swap agreement is a contract in which both parties agree to exchange one currency for another currency at a spot

or FX Swapd Difinition and Pricing Guide Michael Taylor FinPricing An FX swap or currency swap agreement is a contract in which both parties agree to exchange one currency for another currency at a spot

Financial Markets and Products

Financial Markets and Products 1. Eric sold a call option on a stock trading at $40 and having a strike of $35 for $7. What is the profit of the Eric from the transaction if at expiry the stock is trading

Financial Markets and Products 1. Eric sold a call option on a stock trading at $40 and having a strike of $35 for $7. What is the profit of the Eric from the transaction if at expiry the stock is trading

INSTITUTE OF BANKING STUDIES (IBS) EXCHANGE ARITHMETICS: PRACTICAL EXAMPLES

EXCHANGE ARITHMETICS: PRACTICAL EXAMPLES") Question 01. EXCHANGE ARITHMETICS: PRACTICAL EXAMPLES You have received a Swift advice from your Middle East correspondent stating that: it has placed to the credit of your account with your New York correspondent

Question 01. EXCHANGE ARITHMETICS: PRACTICAL EXAMPLES You have received a Swift advice from your Middle East correspondent stating that: it has placed to the credit of your account with your New York correspondent

CHAPTER 10 INTEREST RATE & CURRENCY SWAPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 10 INTEREST RATE & CURRENCY SWAPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Describe the difference between a swap broker and a swap dealer. Answer:

CHAPTER 10 INTEREST RATE & CURRENCY SWAPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Describe the difference between a swap broker and a swap dealer. Answer:

Long-Term Debt Financing

18 Long-Term Debt Financing CHAPTER OBJECTIVES The specific objectives of this chapter are to: explain how an MNC uses debt financing in a manner that minimizes its exposure to exchange rate risk, explain

18 Long-Term Debt Financing CHAPTER OBJECTIVES The specific objectives of this chapter are to: explain how an MNC uses debt financing in a manner that minimizes its exposure to exchange rate risk, explain

22 Swaps: Applications. Answers to Questions and Problems

22 Swaps: Applications Answers to Questions and Problems 1. At present, you observe the following rates: FRA 0,1 5.25 percent and FRA 1,2 5.70 percent, where the subscripts refer to years. You also observe

22 Swaps: Applications Answers to Questions and Problems 1. At present, you observe the following rates: FRA 0,1 5.25 percent and FRA 1,2 5.70 percent, where the subscripts refer to years. You also observe

Mr. Lucky, a portfolio manager at Kotak Securities, own following three blue chip stocks in his portfolio:-

DERIVATIVES Q.1. Mr. Sharma is considering buying a 8-month future contract of GE Inc. which is quoting at $108 in spot market. Assuming CCRFI of 6% p.a. and the company is certain to pay dividends of

DERIVATIVES Q.1. Mr. Sharma is considering buying a 8-month future contract of GE Inc. which is quoting at $108 in spot market. Assuming CCRFI of 6% p.a. and the company is certain to pay dividends of

Lecture 2: Swaps. Topics Covered. The concept of a swap

Lecture 2: Swaps 01135532: Financial Instrument and Innovation Nattawut Jenwittayaroje, Ph.D., CFA NIDA Business School National Institute of Development Administration 1 Topics Covered The concept of

Lecture 2: Swaps 01135532: Financial Instrument and Innovation Nattawut Jenwittayaroje, Ph.D., CFA NIDA Business School National Institute of Development Administration 1 Topics Covered The concept of

Basics of Foreign Exchange Market in India

Basics of Foreign Exchange Market in India Foreign Exchange: Basics What is Foreign Exchange (Forex) How are currency prices determined What is foreign exchange rate policy in India Operation of Forex

Basics of Foreign Exchange Market in India Foreign Exchange: Basics What is Foreign Exchange (Forex) How are currency prices determined What is foreign exchange rate policy in India Operation of Forex

Foreign Exchange Markets: Key Institutional Features (cont)

") Foreign Exchange Markets FOREIGN EXCHANGE MARKETS Professor Anant Sundaram AGENDA Basic characteristics of FX markets: Institutional features Spot markets Forward markets Appreciation, depreciation, premium,

Foreign Exchange Markets FOREIGN EXCHANGE MARKETS Professor Anant Sundaram AGENDA Basic characteristics of FX markets: Institutional features Spot markets Forward markets Appreciation, depreciation, premium,

Derivatives: part I 1

Derivatives: part I 1 Derivatives Derivatives are financial products whose value depends on the value of underlying variables. The main use of derivatives is to reduce risk for one party. Thediverse range

Derivatives: part I 1 Derivatives Derivatives are financial products whose value depends on the value of underlying variables. The main use of derivatives is to reduce risk for one party. Thediverse range

Chapter 5. The Foreign Exchange Market. Foreign Exchange Markets: Learning Objectives. Foreign Exchange Markets. Foreign Exchange Markets

Chapter 5 The Foreign Exchange Market Foreign Exchange Markets: Learning Objectives Examine the functions performed by the foreign exchange (FOREX) market, its participants, size, geographic and currency

Chapter 5 The Foreign Exchange Market Foreign Exchange Markets: Learning Objectives Examine the functions performed by the foreign exchange (FOREX) market, its participants, size, geographic and currency

MTP_Final_Syllabus 2016_Dec2017_Set 2 Paper 14 Strategic Financial Management

Paper 14 Strategic Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 14 Strategic Financial Management Full

Paper 14 Strategic Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 14 Strategic Financial Management Full

Forwards, Futures, Options and Swaps

Forwards, Futures, Options and Swaps A derivative asset is any asset whose payoff, price or value depends on the payoff, price or value of another asset. The underlying or primitive asset may be almost

Forwards, Futures, Options and Swaps A derivative asset is any asset whose payoff, price or value depends on the payoff, price or value of another asset. The underlying or primitive asset may be almost

Derivatives Questions Question 1 Explain carefully the difference between hedging, speculation, and arbitrage.

Derivatives Questions Question 1 Explain carefully the difference between hedging, speculation, and arbitrage. Question 2 What is the difference between entering into a long forward contract when the forward

Derivatives Questions Question 1 Explain carefully the difference between hedging, speculation, and arbitrage. Question 2 What is the difference between entering into a long forward contract when the forward

DISCLAIMER. The Institute of Chartered Accountants of India

DISCLAIMER The Suggested Answers hosted on the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

DISCLAIMER The Suggested Answers hosted on the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

Practice set #3: FRAs, IRFs and Swaps.

International Financial Managment Professor Michel Robe What to do with this practice set? Practice set #3: FRAs, IRFs and Swaps. To help students with the material, seven practice sets with solutions

International Financial Managment Professor Michel Robe What to do with this practice set? Practice set #3: FRAs, IRFs and Swaps. To help students with the material, seven practice sets with solutions

PGDIB[ ] SEMESTER II CORE-FOREIGN EXCHANGE MANAGEMENT-281A Multiple Choice Questions.

![PGDIB[ ] SEMESTER II CORE-FOREIGN EXCHANGE MANAGEMENT-281A Multiple Choice Questions.](/thumbs/82/84979403.jpg "PGDIB[ ] SEMESTER II CORE-FOREIGN EXCHANGE MANAGEMENT-281A Multiple Choice Questions.") 1 of 23 1/19/2018, 1:07 PM Dr.G.R.Damodaran College of Science (Autonomous, affiliated to the Bharathiar University, recognized by the UGC)Reaccredited at the 'A' Grade Level by the NAAC and ISO 9001:2008

1 of 23 1/19/2018, 1:07 PM Dr.G.R.Damodaran College of Science (Autonomous, affiliated to the Bharathiar University, recognized by the UGC)Reaccredited at the 'A' Grade Level by the NAAC and ISO 9001:2008

List of Tables. Sr. No. Table

List of Tables 1 2.1 Salient features of Centuries on Derivatives. 14 2 2.2 Effect of Stock and Index Futures on Cash Stock Market 17 4 2.3 Effect of Stock and Index Options on Cash StockMarket 17 4 2.4

List of Tables 1 2.1 Salient features of Centuries on Derivatives. 14 2 2.2 Effect of Stock and Index Futures on Cash Stock Market 17 4 2.3 Effect of Stock and Index Options on Cash StockMarket 17 4 2.4

Agenda. Learning Objectives. Chapter 19. International Business Finance. Learning Objectives Principles Used in This Chapter

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

SWAPS. Types and Valuation SWAPS

SWAPS Types and Valuation SWAPS Definition A swap is a contract between two parties to deliver one sum of money against another sum of money at periodic intervals. Obviously, the sums exchanged should

SWAPS Types and Valuation SWAPS Definition A swap is a contract between two parties to deliver one sum of money against another sum of money at periodic intervals. Obviously, the sums exchanged should

Appendix A Financial Calculations

Derivatives Demystified: A Step-by-Step Guide to Forwards, Futures, Swaps and Options, Second Edition By Andrew M. Chisholm 010 John Wiley & Sons, Ltd. Appendix A Financial Calculations TIME VALUE OF MONEY

Derivatives Demystified: A Step-by-Step Guide to Forwards, Futures, Swaps and Options, Second Edition By Andrew M. Chisholm 010 John Wiley & Sons, Ltd. Appendix A Financial Calculations TIME VALUE OF MONEY

PAPER 2 : STRATEGIC FINANCIAL MANAGEMENT

Question 1 PAPER 2 : STRATEGIC FINANCIAL MANAGEMENT Question No.1 is compulsory. Attempt any five questions from the remaining six questions Working notes should form par t of the answer (a) Amal Ltd.

Question 1 PAPER 2 : STRATEGIC FINANCIAL MANAGEMENT Question No.1 is compulsory. Attempt any five questions from the remaining six questions Working notes should form par t of the answer (a) Amal Ltd.

FXBFI Broker Financial Invest Ltd. (Regulated by the Cyprus Securities & Exchange Commission)

") FXBFI Broker Financial Invest Ltd (Regulated by the Cyprus Securities & Exchange Commission) KEY INFORMATION DOCUMENT COMMODITY CFD Purpose This document provides you with key information about this investment

FXBFI Broker Financial Invest Ltd (Regulated by the Cyprus Securities & Exchange Commission) KEY INFORMATION DOCUMENT COMMODITY CFD Purpose This document provides you with key information about this investment

ISDA Glossary of Selected Provisions from the 2006 ISDA Definitions ~ Vietnamese Translation

ISDA Glossary of Selected Provisions from the 2006 ISDA Definitions ~ Vietnamese Translation [Apr 25, 2011] 1 OBJECTIVES of the ISDA Glossary of Selected Provisions from the 2006 ISDA Definitions ~ Vietnamese

ISDA Glossary of Selected Provisions from the 2006 ISDA Definitions ~ Vietnamese Translation [Apr 25, 2011] 1 OBJECTIVES of the ISDA Glossary of Selected Provisions from the 2006 ISDA Definitions ~ Vietnamese

Seminar on Issues in Accounting, WIRC ICAI

Accounting Application & Issues in Currency Derivatives Seminar on Issues in Accounting, Auditing & Taxation of Derivatives WIRC ICAI Mumbai Anagha Thatte, M P Chitale & Co. July 16, 2011 Disclaimers Thesearemypersonalviewsandcannotbeconstrued

Accounting Application & Issues in Currency Derivatives Seminar on Issues in Accounting, Auditing & Taxation of Derivatives WIRC ICAI Mumbai Anagha Thatte, M P Chitale & Co. July 16, 2011 Disclaimers Thesearemypersonalviewsandcannotbeconstrued

CHAPTER 14 SWAPS. To examine the reasons for undertaking plain vanilla, interest rate and currency swaps.

1 LEARNING OBJECTIVES CHAPTER 14 SWAPS To examine the reasons for undertaking plain vanilla, interest rate and currency swaps. To demonstrate the principle of comparative advantage as the source of the

1 LEARNING OBJECTIVES CHAPTER 14 SWAPS To examine the reasons for undertaking plain vanilla, interest rate and currency swaps. To demonstrate the principle of comparative advantage as the source of the

Vanilla interest rate options

Vanilla interest rate options Marco Marchioro derivati2@marchioro.org October 26, 2011 Vanilla interest rate options 1 Summary Probability evolution at information arrival Brownian motion and option pricing

Vanilla interest rate options Marco Marchioro derivati2@marchioro.org October 26, 2011 Vanilla interest rate options 1 Summary Probability evolution at information arrival Brownian motion and option pricing

MT4 Trading Manual. February 2017

MT4 Trading Manual February 2017 LMAX MT4 Trading Manual For all trades executed through the MT4 platform Effective date: 06 February 2017 This Trading Manual (the Manual) provides further information

MT4 Trading Manual February 2017 LMAX MT4 Trading Manual For all trades executed through the MT4 platform Effective date: 06 February 2017 This Trading Manual (the Manual) provides further information

INTERNATIONAL FINANCE

INTERNATIONAL FINANCE Ing. Zuzana STRÁPEKOVÁ, PhD. 1 10. 2017/2018 SUA-FEM Nitra The FOREX market is a two-tiered market: Interbank Market (Wholesale) FUNCTION AND STRUCTURE OF THE FOREX MARKET - about

INTERNATIONAL FINANCE Ing. Zuzana STRÁPEKOVÁ, PhD. 1 10. 2017/2018 SUA-FEM Nitra The FOREX market is a two-tiered market: Interbank Market (Wholesale) FUNCTION AND STRUCTURE OF THE FOREX MARKET - about

Lecture 11. SWAPs markets. I. Background of Interest Rate SWAP markets. Types of Interest Rate SWAPs

Lecture 11 SWAPs markets Agenda: I. Background of Interest Rate SWAP markets II. Types of Interest Rate SWAPs II.1 Plain vanilla swaps II.2 Forward swaps II.3 Callable swaps (Swaptions) II.4 Putable swaps

Lecture 11 SWAPs markets Agenda: I. Background of Interest Rate SWAP markets II. Types of Interest Rate SWAPs II.1 Plain vanilla swaps II.2 Forward swaps II.3 Callable swaps (Swaptions) II.4 Putable swaps

Product Disclosure Statement Structured Foreign Exchange Option Products 1 April 2019

Product Disclosure Statement Structured Foreign Exchange Option Products 1 April 2019 TABLE OF CONTENTS 1. INTRODUCTION... 1 1. INTRODUCTION... 3 2 ABOUT THIS PDS... 3 2.1 Purpose and Contents of this

Product Disclosure Statement Structured Foreign Exchange Option Products 1 April 2019 TABLE OF CONTENTS 1. INTRODUCTION... 1 1. INTRODUCTION... 3 2 ABOUT THIS PDS... 3 2.1 Purpose and Contents of this

ACI Dealing Certificate (008)

") ACI Dealing Certificate (008) Syllabus Prometric Code : 3I0-008 Examination Delivered in English and German Setting the benchmark in certifying the financial industry globally 8 Rue du Mail, 75002 Paris

ACI Dealing Certificate (008) Syllabus Prometric Code : 3I0-008 Examination Delivered in English and German Setting the benchmark in certifying the financial industry globally 8 Rue du Mail, 75002 Paris

Currency Derivatives

Currency Derivatives Objectives How to the read the quotes Evolution of Foreign Exchange Market Factors affecting the Currency Market Current scenario Currency Futures Opportunities & Advantages Currency

Currency Derivatives Objectives How to the read the quotes Evolution of Foreign Exchange Market Factors affecting the Currency Market Current scenario Currency Futures Opportunities & Advantages Currency

Essential Learning for CTP Candidates NY Cash Exchange 2018 Session #CTP-08

NY Cash Exchange 2018: CTP Track Cash Forecasting & Risk Management Session #8 (Thur. 4:00 5:00 pm) ETM5-Chapter 14: Cash Flow Forecasting ETM5-Chapter 16: Enterprise Risk Management ETM5-Chapter 17: Financial

NY Cash Exchange 2018: CTP Track Cash Forecasting & Risk Management Session #8 (Thur. 4:00 5:00 pm) ETM5-Chapter 14: Cash Flow Forecasting ETM5-Chapter 16: Enterprise Risk Management ETM5-Chapter 17: Financial

New York Cash Exchange: 2016 Essential Learning for CTP Candidates Session #8: Thursday Afternoon (6/02)

") New York Cash Exchange: 2016 Essential Learning for CTP Candidates Session #8: Thursday Afternoon (6/02) ETM4-Chapter 13: Cash Forecasting ETM4-Chapter 15: Operational Risk Management ETM4-Chapter 16:

New York Cash Exchange: 2016 Essential Learning for CTP Candidates Session #8: Thursday Afternoon (6/02) ETM4-Chapter 13: Cash Forecasting ETM4-Chapter 15: Operational Risk Management ETM4-Chapter 16:

Suggested Answer_Syl12_Dec2017_Paper 14 FINAL EXAMINATION

FINAL EXAMINATION GROUP III (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2017 Paper- 14: ADVANCED FINANCIAL MANAGEMENT Time Allowed: 3 Hours Full Marks: 100 The figures on the right margin indicate

FINAL EXAMINATION GROUP III (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2017 Paper- 14: ADVANCED FINANCIAL MANAGEMENT Time Allowed: 3 Hours Full Marks: 100 The figures on the right margin indicate

Question 1. Copyright -The Institute of Chartered Accountants of India

Question 1 PAPER 2 : STRATEGIC FINANCIAL MANAGEMENT Answer all questions. Working notes should form part of the answer. Wherever appropriate, suitable assumption should be made by the candidates. (a) XY

Question 1 PAPER 2 : STRATEGIC FINANCIAL MANAGEMENT Answer all questions. Working notes should form part of the answer. Wherever appropriate, suitable assumption should be made by the candidates. (a) XY

Question No. 1 is compulsory. Attempt any five questions from the remaining six questions. Working notes should form part of the answer.

Test Series: September, 2014 MOCK TEST PAPER 1 FINAL COURSE: GROUP I PAPER 2 : STRATEGIC FINANCIAL MANAGEMENT Question No. 1 is compulsory. Attempt any five questions from the remaining six questions.

Test Series: September, 2014 MOCK TEST PAPER 1 FINAL COURSE: GROUP I PAPER 2 : STRATEGIC FINANCIAL MANAGEMENT Question No. 1 is compulsory. Attempt any five questions from the remaining six questions.

Interest Rate Swap Vaulation Pratical Guide

Interest Rate Swap Vaulation Pratical Guide Alan White FinPricing http://www.finpricing.com Summary Interest Rate Swap Introduction The Use of Interest Rate Swap Swap or Swaplet Payoff Valuation Practical

Interest Rate Swap Vaulation Pratical Guide Alan White FinPricing http://www.finpricing.com Summary Interest Rate Swap Introduction The Use of Interest Rate Swap Swap or Swaplet Payoff Valuation Practical

Replies to one minute memos, 9/21/03

Replies to one minute memos, 9/21/03 Dear Students, Thank you for asking these great questions. The answer to my question (what is the difference b/n the covered & uncovered interest rate arbitrage? If

Replies to one minute memos, 9/21/03 Dear Students, Thank you for asking these great questions. The answer to my question (what is the difference b/n the covered & uncovered interest rate arbitrage? If

Borrowers Objectives

FIN 463 International Finance Cross-Currency and Interest Rate s Professor Robert Hauswald Kogod School of Business, AU Borrowers Objectives Lower your funding costs: optimal distribution of risks between

FIN 463 International Finance Cross-Currency and Interest Rate s Professor Robert Hauswald Kogod School of Business, AU Borrowers Objectives Lower your funding costs: optimal distribution of risks between

SOCIETY OF ACTUARIES FINANCIAL MATHEMATICS. EXAM FM SAMPLE QUESTIONS Financial Economics

SOCIETY OF ACTUARIES EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE QUESTIONS Financial Economics June 2014 changes Questions 1-30 are from the prior version of this document. They have been edited to conform

SOCIETY OF ACTUARIES EXAM FM FINANCIAL MATHEMATICS EXAM FM SAMPLE QUESTIONS Financial Economics June 2014 changes Questions 1-30 are from the prior version of this document. They have been edited to conform

DESCRIPTION OF FINANCIAL INSTRUMENTS AND RELATED RISKS

DESCRIPTION OF FINANCIAL INSTRUMENTS AND RELATED RISKS Pursuant to the requirements of legal acts and in order to enable the Client to make a reasoned investment decision, the Bank hereby presents a generalized

DESCRIPTION OF FINANCIAL INSTRUMENTS AND RELATED RISKS Pursuant to the requirements of legal acts and in order to enable the Client to make a reasoned investment decision, the Bank hereby presents a generalized

Part III: Swaps. Futures, Swaps & Other Derivatives. Swaps. Previous lecture set: This lecture set -- Parts II & III. Fundamentals

Futures, Swaps & Other Derivatives Previous lecture set: Interest-Rate Derivatives FRAs T-bills futures & Euro$ Futures This lecture set -- Parts II & III Swaps Part III: Swaps Swaps Fundamentals what,

Futures, Swaps & Other Derivatives Previous lecture set: Interest-Rate Derivatives FRAs T-bills futures & Euro$ Futures This lecture set -- Parts II & III Swaps Part III: Swaps Swaps Fundamentals what,

CHAPTER 10 OPTION PRICING - II. Derivatives and Risk Management By Rajiv Srivastava. Copyright Oxford University Press

CHAPTER 10 OPTION PRICING - II Options Pricing II Intrinsic Value and Time Value Boundary Conditions for Option Pricing Arbitrage Based Relationship for Option Pricing Put Call Parity 2 Binomial Option

CHAPTER 10 OPTION PRICING - II Options Pricing II Intrinsic Value and Time Value Boundary Conditions for Option Pricing Arbitrage Based Relationship for Option Pricing Put Call Parity 2 Binomial Option

As rates change continuously, the monthly discount factor should be calculated on a continuous time basis:

JUN-09 You are an importer of stone chippings for building purposes and you have entered into a fixed price contract for the delivery of 10,000 metric tonnes per month for the next six months. The first

JUN-09 You are an importer of stone chippings for building purposes and you have entered into a fixed price contract for the delivery of 10,000 metric tonnes per month for the next six months. The first

27 th Year of Publication. A monthly publication from South Indian Bank. To kindle interest in economic affairs... To empower the student community...

Experience Next Generation Banking A monthly publication from South Indian Bank To kindle interest in economic affairs... To empower the student community... www.southindianbank.com Student s corner ho2099@sib.co.in

Experience Next Generation Banking A monthly publication from South Indian Bank To kindle interest in economic affairs... To empower the student community... www.southindianbank.com Student s corner ho2099@sib.co.in

Financial Management in IB. Exercises

Financial Management in IB Exercises I. Foreign Exchange Market Locational Arbitrage Paris Interbank market: EUR/USD 1.2548/1.2552 London Interbank market: EUR/USD 1.2543/1.2546 =(1.2548-1.2546)*10000000=

Financial Management in IB Exercises I. Foreign Exchange Market Locational Arbitrage Paris Interbank market: EUR/USD 1.2548/1.2552 London Interbank market: EUR/USD 1.2543/1.2546 =(1.2548-1.2546)*10000000=

Table of contents. Slide No. Meaning Of Derivative 3. Specifications Of Futures 4. Functions Of Derivatives 5. Participants 6.

Derivatives 1 Table of contents Slide No. Meaning Of Derivative 3 Specifications Of Futures 4 Functions Of Derivatives 5 Participants 6 Size Of Market 7 Available Future Contracts 9 Jargons 10 Parameters

Derivatives 1 Table of contents Slide No. Meaning Of Derivative 3 Specifications Of Futures 4 Functions Of Derivatives 5 Participants 6 Size Of Market 7 Available Future Contracts 9 Jargons 10 Parameters

Plus500AU Pty Ltd. Product Disclosure Statement

Plus500AU Pty Ltd Product Disclosure Statement Product Disclosure Statement Our Contact Details Issuer: PLUS500AU Pty Ltd ACN 153 301 681 Address: P.O. Box H339, Australia Square, Sydney NSW 1215 Australia

Plus500AU Pty Ltd Product Disclosure Statement Product Disclosure Statement Our Contact Details Issuer: PLUS500AU Pty Ltd ACN 153 301 681 Address: P.O. Box H339, Australia Square, Sydney NSW 1215 Australia

Guidance regarding the completion of the Market Risk prudential reporting module for deposit-taking branches Issued May 2008

Guidance regarding the completion of the Market Risk prudential reporting module for deposit-taking branches Issued May 2008 Branch Market Risk Reporting Guide May 2008 1 Glossary The following abbreviations

Guidance regarding the completion of the Market Risk prudential reporting module for deposit-taking branches Issued May 2008 Branch Market Risk Reporting Guide May 2008 1 Glossary The following abbreviations

Paper 14 Syllabus 2016 MTP Set 1

Paper 14 Strategic Financial Management Full Marks : 100 Time allowed: 3 hours Answer Question No. 1 which is compulsory and carries 20 marks and any five from Question No. 2 to 8. Section A [20 marks]

Paper 14 Strategic Financial Management Full Marks : 100 Time allowed: 3 hours Answer Question No. 1 which is compulsory and carries 20 marks and any five from Question No. 2 to 8. Section A [20 marks]

Pinnacle Academy Mock Tests for November 2016 C A Final Examination

Downloaded from www.ashishlalaji.net Pinnacle Academy Mock Tests for November 2016 C A Final Examination 2 nd Floor, Florence Classic, 10, Ashapuri Soc, Opp. VUDA Flats, Jain Derasar Rd., Akota, Vadodara-20.

Downloaded from www.ashishlalaji.net Pinnacle Academy Mock Tests for November 2016 C A Final Examination 2 nd Floor, Florence Classic, 10, Ashapuri Soc, Opp. VUDA Flats, Jain Derasar Rd., Akota, Vadodara-20.

NOTES ON THE BANK OF ENGLAND UK YIELD CURVES

NOTES ON THE BANK OF ENGLAND UK YIELD CURVES The Macro-Financial Analysis Division of the Bank of England estimates yield curves for the United Kingdom on a daily basis. They are of three kinds. One set

NOTES ON THE BANK OF ENGLAND UK YIELD CURVES The Macro-Financial Analysis Division of the Bank of England estimates yield curves for the United Kingdom on a daily basis. They are of three kinds. One set

Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences.

5. ARBITRAGE AND SPOT EXCHANGE RATES 5 Arbitrage and Spot Exchange Rates Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences. Arbitrage is the most basic

5. ARBITRAGE AND SPOT EXCHANGE RATES 5 Arbitrage and Spot Exchange Rates Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences. Arbitrage is the most basic

Interest Rate Forwards and Swaps

Interest Rate Forwards and Swaps 1 Outline PART ONE Chapter 1: interest rate forward contracts and their pricing and mechanics 2 Outline PART TWO Chapter 2: basic and customized swaps and their pricing

Interest Rate Forwards and Swaps 1 Outline PART ONE Chapter 1: interest rate forward contracts and their pricing and mechanics 2 Outline PART TWO Chapter 2: basic and customized swaps and their pricing