5 th Annual CARISMA Conference MWB, Canada Square, Canary Wharf 2 nd February ialm. M A H Dempster & E A Medova. & Cambridge Systems Associates

|

|

|

- Richard Bates

- 6 years ago

- Views:

Transcription

1 5 th Annual CARISMA Conference MWB, Canada Square, Canary Wharf 2 nd February 2010 Individual Asset Liability Management ialm M A H Dempster & E A Medova Centre for Financial i Research, University it of Cambridge & Cambridge Systems Associates

2 Outline Personal finance and individual id financial i planning Is reconciliation of theory and practice possible? DSP model for individual Asset Liability Management: ialm General discussion of objectives Drivers of undertaken risks and returns Optimization of cashflows and portfolio construction Illustrative household examples ialm Performance testing Comparison with MVO Behavioural testing Adjustments to 2009 crisis

3 Because we humanoid primates had to struggle with personal finance, we became human Joseph Schumpeter We do not prosper by income or happiness alone Samuel Brittan Is wealth the long-term spending that our portfolio can sustain? This definition is close to the truth, but it ignores purchasing power. Is wealth, then, the inflation-indexed real income that our assets could sustain over time? For most investors, this is probably the most useful definition of wealth Robert Arnott

4 Common Practice Financial planners have traditionally resisted the academic solutions based on theoretical models Asset allocation puzzle of Canner et al [J. Campbell, 2002] Common practice is based on the qualitative assessment of risk attitude tude by financial a advisers s Rule of thumb: equity fraction of one s portfolio equals 100 one s age Is Personal Finance an exact science? An immediate flat no. It is a domain full of ordinary common sense. Alas, common sense is not the same thing as good sense. Good sense in these esoteric puzzles is hard to come by. Paul Samuelson

5 In the search for good sense Modelling methodology came from Operations Research -- decision making over an uncertain future The ialm system is a decision support tool for long-term investors, which allows interactive use and re-solving with modified d data on some individual id preferences and data inputs Therefore, not one financial plan is generated for the household but many contingency plans reflecting subjective opinion regarding future life events Principal ideas are brought together from behavioural and classical finance and stochastic optimization theory in separate modules of the system in order to help individuals with longterm financial planning

6 ialm Implementation Dynamic, multi-stage optimization problem with stochastic data: simulated cashflows (inflows and outflows) of incomes, liabilities, investment returns, etc What-if scenario analysis Implementable decisions correspond to the root node of the scenario tree Periodic recalibration of the model parameters to market and personal data -- ability to modify inputs periodically or at times of significant changes in life

7 Stochastic Programming Techniques for ALM Generation of scenario trees Data process simulation time steps Decision time points: stages of the tree Implementable decisions at root node the most constrained and robust decision taking into account all generated alternative scenarios Large scale linear optimization i i problem wealth or consumption maximization at each decision time subject to constraints such as risk, budget, cash flow balance and so on at simulator time steps

8 Gather Individual and Market Data Overview of individual ALM Personal data Market data Econometric and Actuarial Modelling Events model Liabilities model Model returns on investment classes Scenario Tree Simulation Events Cash-out flows forecast Cash-in flows forecasts Optimization Model: Tailored Portfolios, Goals Spendings, Cashflow balances, etc Dynamic optimization model for assets-liabilities Objective: maximize goal spending Visualization of decisions Various Constraints

9 Software for Dynamic Stochastic Programming Input GUI parameters Simulation key processes Tree construction scenario tree derived processes StochGen Model GSPL problem formulation STOCHASTICS TM Solver StochOpt Derived assets and processes results Output GUI

10 ialm Financial Plan ialm provides optimum values for many decision variables of interest --spending, amount of savings, tax-efficient allocation between multiple portfolios, etc -- across time simultaneously for multiple scenarios of random processes representing markets returns, foreseen liabilities and life events Current ialm model includes 20 random processes that vary over the client s lifetime and around 200 mathematically formulated conditions (constraints) per node of the scenario tree Average desktop computer solving times are 3-15 minutes (Problem size over 3mln non-zero entries) An interactive process for analysing retirement and saving alternatives

11 Key Modelling Features Problem with random time horizon individual life spans Portfolio return and risk are driven by desirable consumption subject to existing and future liabilities Risk management of portfolio by constraining i the expected shortfall Overall objectives to provide sustainable spending over household lifetime Each individual goal utility function is defined over gains or losses with respect to three reference points : a piece-wise linear utility function

12 Prospect Theory Value Function

13 Individual Goal Utility For each individual goal the level of spending y is in the range between acceptable (s) and desirable (g) subject to existing and foreseen liabilities, i.e. minimum (h) spending. These values specify the shape of the utility function for each goal Objective to maximize goal spending: piecewise linear utility functions for goal spending with priorities u (utility) g 1 α g 1 α s h α h s g y (spending) 1

14 Overall Objective The objective is to maximize the expected present value (over all scenarios) of life time consumption, i.e. spending on goals T E 1{any alive, t} ut t= 1 1 where u = u, z + I φ xs xs τi τ ( π + π I ) t g t t t g G t xs τ Here z is excess borrowing, I is total tax payment and φ is the inflation index at t t t t Consumption refers to all elective spending on chosen goals alive d m alive C =, s, (, +, ) + ˆ t αg t φ Fg t Fg t α gt g, t φg, ty g, t g G m g g G\ G m

15 Wealth Generation ialm objectives are achieved through optimum resource allocation over a network of cashflows Together with the stream of labour and other income the income from portfolio returns provides optimal spending on goals at minimal risk Fundamental constraints of portfolio allocation subproblem Initial holding Portfolio cashflow Asset inventory balance Investment limits, position limits Portfolio drawdown etc Optimal allocation between different types of account Two types of portfolio: taxable and savings portfolios such as 401K (USA) or SIPP and ISA (UK)

16 Cashflow Constraints Net wealth x r + x r tx+ tx + a a a a Transaction costs Returns Coupons and dividends Interest on bank deposits Regular income Employer pension contributions Qualified coupons and dividends Qualified returns I C I + I z ρ r D + cash t 1 t 1 I p + I qc P o qe 401 k q 401 k + + I qd Portfolio ( ) x a P qualified contributions q+ P P + asset purchases asset sales s P Qualified account ( 0 ) asset sales x q a q 401 k+ z P q qnr+ loan repaym yment x Margin cash m mr ( + r ) borrowing ( m m ) m new margin loans ma Cash holding + ( z ) q + a P q qualified withdraw wal asset purchases Qualified portfolio q ( ) x a argin loan repayment m excess borrowing at t + C goa oal spending Excess borrowing repayment xs z t income loan repa payment incom me borrowing Goal Equity (see below) L asset loan repayment asset borrowing z xs xs z t + r (1 ) 1 Excess borrowing xs z I, t z (1 + r + r ) cash s I, t 1 t 1 I Income borrowing z I Loans secured on assets x r z I + F τ τ av r P qp q τ cash s I, t 1 r t 1 + r I + ( ) z r xs xs t 1 1 x r q tx+ q tx a a a a Interest charges on margin loans Interest on goal loans Goal consumption (non capital) Liabilities Taxation Unauthorized qualified withdrawal penalty Interest charges on secured borrowing Interest charges on income loans Interest charges on excess borrowing Transaction costs (qualified portfolio)

17 Household Data FT weekly supplement Money Family member describes their financial position and goals and asks expert financial advisers for recommendations on investment, savings and appropriate spending Quantity and quality of data provided by household may vary significantly Adviser s opinions may differ significantly Example -- Pimlott household

18

19 Model Illustration: Pimlott Household

20

21

22

23

24

25 2007

26 2009

27 2007

28 2009

29

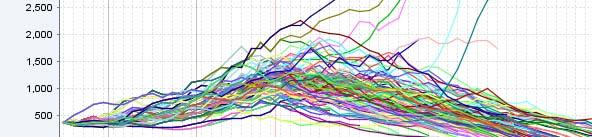

30 Performance of ialm Testing on real profiles of UK and US investors and comparison with recommendations of financial advisors Comparison with MVO based methodology Backtesting performance over 10 years: for US model Behavioural aspects tested using ability to analyse relationship between current wealth, earnings, savings and desirable consumption

31 Visual Summary of Profile Goals Getting an Overview Cash Flows Portfolio Wealth

32 Helping households become involved in managing their investments Linking Strategic and Tactical Decisions ialm decision tool takes a long term view of individual circumstances and recommends strategic allocations in market indices This gives a dynamic view of asset management over household lifetime which requires an implementation of the current year optimal portfolio Tactical allocation exploits financial advisors knowledge at the level of individual fund characteristics adding alpha without increasing beta and use the expertise of the financial adviser Both levels must consider the legal and institutional framework Taxation Pension regulations

33 References Dempster et al. (2006). Managing guarantees. Journal of Portfolio Management Dempster et al. (2009). Risk profiling defined benefit pension schemes. Journal of Portfolio Management Medova et al. (2008). Individual asset-liability management. Quantitative Finance Dempster &Medova (2010). Asset liability management for individual households. British Actuarial Journal. To be presented to a Sessional Meeting of the Institute of Actuaries, London

Individual Asset Liability Management: Dynamic Stochastic Programming Solution

EU HPCF Conference New Thinking in Finance 14.2.2014 Pensions & Insurance 1 Individual Asset Liability Management: Dynamic Stochastic Programming Solution Elena Medova joint work with Michael Dempster,

EU HPCF Conference New Thinking in Finance 14.2.2014 Pensions & Insurance 1 Individual Asset Liability Management: Dynamic Stochastic Programming Solution Elena Medova joint work with Michael Dempster,

Multi-Period Trading via Convex Optimization

Multi-Period Trading via Convex Optimization Stephen Boyd Enzo Busseti Steven Diamond Ronald Kahn Kwangmoo Koh Peter Nystrup Jan Speth Stanford University & Blackrock City University of Hong Kong September

Multi-Period Trading via Convex Optimization Stephen Boyd Enzo Busseti Steven Diamond Ronald Kahn Kwangmoo Koh Peter Nystrup Jan Speth Stanford University & Blackrock City University of Hong Kong September

GOAL PROGRAMMING TECHNIQUES FOR BANK ASSET LIABILITY MANAGEMENT

GOAL PROGRAMMING TECHNIQUES FOR BANK ASSET LIABILITY MANAGEMENT Applied Optimization Volume 90 Series Editors: Panos M. Pardalos University of Florida, U.S.A. Donald W. Hearn University of Florida, U.S.A.

GOAL PROGRAMMING TECHNIQUES FOR BANK ASSET LIABILITY MANAGEMENT Applied Optimization Volume 90 Series Editors: Panos M. Pardalos University of Florida, U.S.A. Donald W. Hearn University of Florida, U.S.A.

Portfolio Management and Optimal Execution via Convex Optimization

Portfolio Management and Optimal Execution via Convex Optimization Enzo Busseti Stanford University April 9th, 2018 Problems portfolio management choose trades with optimization minimize risk, maximize

Portfolio Management and Optimal Execution via Convex Optimization Enzo Busseti Stanford University April 9th, 2018 Problems portfolio management choose trades with optimization minimize risk, maximize

LIFECYCLE INVESTING : DOES IT MAKE SENSE

Page 1 LIFECYCLE INVESTING : DOES IT MAKE SENSE TO REDUCE RISK AS RETIREMENT APPROACHES? John Livanas UNSW, School of Actuarial Sciences Lifecycle Investing, or the gradual reduction in the investment

Page 1 LIFECYCLE INVESTING : DOES IT MAKE SENSE TO REDUCE RISK AS RETIREMENT APPROACHES? John Livanas UNSW, School of Actuarial Sciences Lifecycle Investing, or the gradual reduction in the investment

w w w. I C A o r g

w w w. I C A 2 0 1 4. o r g On improving pension product design Agnieszka K. Konicz a and John M. Mulvey b a Technical University of Denmark DTU Management Engineering Management Science agko@dtu.dk b

w w w. I C A 2 0 1 4. o r g On improving pension product design Agnieszka K. Konicz a and John M. Mulvey b a Technical University of Denmark DTU Management Engineering Management Science agko@dtu.dk b

Investments. ALTERNATIVES Build alternative investment portfolios. EQUITIES Build equities investment portfolios

Investments BlackRock was founded by eight entrepreneurs who wanted to start a very different company. One that combined the best of a financial leader and a technology pioneer. And one that focused many

Investments BlackRock was founded by eight entrepreneurs who wanted to start a very different company. One that combined the best of a financial leader and a technology pioneer. And one that focused many

Retirement. Optimal Asset Allocation in Retirement: A Downside Risk Perspective. JUne W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT

Putnam Institute JUne 2011 Optimal Asset Allocation in : A Downside Perspective W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT Once an individual has retired, asset allocation becomes a critical

Putnam Institute JUne 2011 Optimal Asset Allocation in : A Downside Perspective W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT Once an individual has retired, asset allocation becomes a critical

Modelling optimal decisions for financial planning in retirement using stochastic control theory

Modelling optimal decisions for financial planning in retirement using stochastic control theory Johan G. Andréasson School of Mathematical and Physical Sciences University of Technology, Sydney Thesis

Modelling optimal decisions for financial planning in retirement using stochastic control theory Johan G. Andréasson School of Mathematical and Physical Sciences University of Technology, Sydney Thesis

Non-qualified Annuities in After-tax Optimizations

Non-qualified Annuities in After-tax Optimizations by William Reichenstein Baylor University Discussion by Chester S. Spatt Securities and Exchange Commission and Carnegie Mellon University at Fourth Annual

Non-qualified Annuities in After-tax Optimizations by William Reichenstein Baylor University Discussion by Chester S. Spatt Securities and Exchange Commission and Carnegie Mellon University at Fourth Annual

Measuring Sustainability in the UN System of Environmental-Economic Accounting

Measuring Sustainability in the UN System of Environmental-Economic Accounting Kirk Hamilton April 2014 Grantham Research Institute on Climate Change and the Environment Working Paper No. 154 The Grantham

Measuring Sustainability in the UN System of Environmental-Economic Accounting Kirk Hamilton April 2014 Grantham Research Institute on Climate Change and the Environment Working Paper No. 154 The Grantham

Advanced Modern Macroeconomics

Advanced Modern Macroeconomics Analysis and Application Max Gillman UMSL 27 August 2014 Gillman (UMSL) Modern Macro 27 August 2014 1 / 23 Overview of Advanced Macroeconomics Chapter 1: Overview of the

Advanced Modern Macroeconomics Analysis and Application Max Gillman UMSL 27 August 2014 Gillman (UMSL) Modern Macro 27 August 2014 1 / 23 Overview of Advanced Macroeconomics Chapter 1: Overview of the

The case for professional financial advice

The case for professional financial advice Professional financial advisors provide several services that may help the performance of a long-term financial program, and offer value to investors who might

The case for professional financial advice Professional financial advisors provide several services that may help the performance of a long-term financial program, and offer value to investors who might

Alpha, Beta, and Now Gamma

Alpha, Beta, and Now Gamma David Blanchett, CFA, CFP Head of Retirement Research, Morningstar Investment Management Paul D. Kaplan, Ph.D., CFA Director of Research, Morningstar Canada 2012 Morningstar.

Alpha, Beta, and Now Gamma David Blanchett, CFA, CFP Head of Retirement Research, Morningstar Investment Management Paul D. Kaplan, Ph.D., CFA Director of Research, Morningstar Canada 2012 Morningstar.

Financial Giffen Goods: Examples and Counterexamples

Financial Giffen Goods: Examples and Counterexamples RolfPoulsen and Kourosh Marjani Rasmussen Abstract In the basic Markowitz and Merton models, a stock s weight in efficient portfolios goes up if its

Financial Giffen Goods: Examples and Counterexamples RolfPoulsen and Kourosh Marjani Rasmussen Abstract In the basic Markowitz and Merton models, a stock s weight in efficient portfolios goes up if its

Robust Models of Core Deposit Rates

Robust Models of Core Deposit Rates by Michael Arnold, Principal ALCO Partners, LLC & OLLI Professor Dominican University Bruce Lloyd Campbell Principal ALCO Partners, LLC Introduction and Summary Our

Robust Models of Core Deposit Rates by Michael Arnold, Principal ALCO Partners, LLC & OLLI Professor Dominican University Bruce Lloyd Campbell Principal ALCO Partners, LLC Introduction and Summary Our

Better decision making under uncertain conditions using Monte Carlo Simulation

IBM Software Business Analytics IBM SPSS Statistics Better decision making under uncertain conditions using Monte Carlo Simulation Monte Carlo simulation and risk analysis techniques in IBM SPSS Statistics

IBM Software Business Analytics IBM SPSS Statistics Better decision making under uncertain conditions using Monte Carlo Simulation Monte Carlo simulation and risk analysis techniques in IBM SPSS Statistics

A Multi-Stage Stochastic Programming Model for Managing Risk-Optimal Electricity Portfolios. Stochastic Programming and Electricity Risk Management

A Multi-Stage Stochastic Programming Model for Managing Risk-Optimal Electricity Portfolios SLIDE 1 Outline Multi-stage stochastic programming modeling Setting - Electricity portfolio management Electricity

A Multi-Stage Stochastic Programming Model for Managing Risk-Optimal Electricity Portfolios SLIDE 1 Outline Multi-stage stochastic programming modeling Setting - Electricity portfolio management Electricity

UPDATED IAA EDUCATION SYLLABUS

II. UPDATED IAA EDUCATION SYLLABUS A. Supporting Learning Areas 1. STATISTICS Aim: To enable students to apply core statistical techniques to actuarial applications in insurance, pensions and emerging

II. UPDATED IAA EDUCATION SYLLABUS A. Supporting Learning Areas 1. STATISTICS Aim: To enable students to apply core statistical techniques to actuarial applications in insurance, pensions and emerging

Optimization of a Real Estate Portfolio with Contingent Portfolio Programming

Mat-2.108 Independent research projects in applied mathematics Optimization of a Real Estate Portfolio with Contingent Portfolio Programming 3 March, 2005 HELSINKI UNIVERSITY OF TECHNOLOGY System Analysis

Mat-2.108 Independent research projects in applied mathematics Optimization of a Real Estate Portfolio with Contingent Portfolio Programming 3 March, 2005 HELSINKI UNIVERSITY OF TECHNOLOGY System Analysis

Dynamic Asset and Liability Management Models for Pension Systems

Dynamic Asset and Liability Management Models for Pension Systems The Comparison between Multi-period Stochastic Programming Model and Stochastic Control Model Muneki Kawaguchi and Norio Hibiki June 1,

Dynamic Asset and Liability Management Models for Pension Systems The Comparison between Multi-period Stochastic Programming Model and Stochastic Control Model Muneki Kawaguchi and Norio Hibiki June 1,

Stochastic Modelling: The power behind effective financial planning. Better Outcomes For All. Good for the consumer. Good for the Industry.

Stochastic Modelling: The power behind effective financial planning Better Outcomes For All Good for the consumer. Good for the Industry. Introduction This document aims to explain what stochastic modelling

Stochastic Modelling: The power behind effective financial planning Better Outcomes For All Good for the consumer. Good for the Industry. Introduction This document aims to explain what stochastic modelling

Reinsurance Optimization GIE- AXA 06/07/2010

Reinsurance Optimization thierry.cohignac@axa.com GIE- AXA 06/07/2010 1 Agenda Introduction Theoretical Results Practical Reinsurance Optimization 2 Introduction As all optimization problem, solution strongly

Reinsurance Optimization thierry.cohignac@axa.com GIE- AXA 06/07/2010 1 Agenda Introduction Theoretical Results Practical Reinsurance Optimization 2 Introduction As all optimization problem, solution strongly

ALM Analysis for a Pensionskasse

ALM Analysis for a Pensionskasse Asset Liability Management Study Francesco Sandrini MSc, PhD New Thinking in Finance London, February 14 th 2014 For Internal Use Only. Not to be Distributed to the Public.

ALM Analysis for a Pensionskasse Asset Liability Management Study Francesco Sandrini MSc, PhD New Thinking in Finance London, February 14 th 2014 For Internal Use Only. Not to be Distributed to the Public.

Quantitative Investment: Research and Implementation in MATLAB

Quantitative Investment: Research and Implementation in MATLAB Edward Hoyle Fulcrum Asset Management 6 Chesterfield Gardens London, W1J 5BQ ed.hoyle@fulcrumasset.com 24 June 2014 MATLAB Computational Finance

Quantitative Investment: Research and Implementation in MATLAB Edward Hoyle Fulcrum Asset Management 6 Chesterfield Gardens London, W1J 5BQ ed.hoyle@fulcrumasset.com 24 June 2014 MATLAB Computational Finance

Principles of Managerial Finance Solution Lawrence J. Gitman CHAPTER 10. Risk and Refinements In Capital Budgeting

Principles of Managerial Finance Solution Lawrence J. Gitman CHAPTER 10 Risk and Refinements In Capital Budgeting INSTRUCTOR S RESOURCES Overview Chapters 8 and 9 developed the major decision-making aspects

Principles of Managerial Finance Solution Lawrence J. Gitman CHAPTER 10 Risk and Refinements In Capital Budgeting INSTRUCTOR S RESOURCES Overview Chapters 8 and 9 developed the major decision-making aspects

In physics and engineering education, Fermi problems

A THOUGHT ON FERMI PROBLEMS FOR ACTUARIES By Runhuan Feng In physics and engineering education, Fermi problems are named after the physicist Enrico Fermi who was known for his ability to make good approximate

A THOUGHT ON FERMI PROBLEMS FOR ACTUARIES By Runhuan Feng In physics and engineering education, Fermi problems are named after the physicist Enrico Fermi who was known for his ability to make good approximate

How quantitative methods influence and shape finance industry

How quantitative methods influence and shape finance industry Marek Musiela UNSW December 2017 Non-quantitative talk about the role quantitative methods play in finance industry. Focus on investment banking,

How quantitative methods influence and shape finance industry Marek Musiela UNSW December 2017 Non-quantitative talk about the role quantitative methods play in finance industry. Focus on investment banking,

VOLATILITY EFFECTS AND VIRTUAL ASSETS: HOW TO PRICE AND HEDGE AN ENERGY PORTFOLIO

VOLATILITY EFFECTS AND VIRTUAL ASSETS: HOW TO PRICE AND HEDGE AN ENERGY PORTFOLIO GME Workshop on FINANCIAL MARKETS IMPACT ON ENERGY PRICES Responsabile Pricing and Structuring Edison Trading Rome, 4 December

VOLATILITY EFFECTS AND VIRTUAL ASSETS: HOW TO PRICE AND HEDGE AN ENERGY PORTFOLIO GME Workshop on FINANCIAL MARKETS IMPACT ON ENERGY PRICES Responsabile Pricing and Structuring Edison Trading Rome, 4 December

Exercises on the New-Keynesian Model

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

Advanced Macroeconomics II Professor Lorenza Rossi/Jordi Gali T.A. Daniël van Schoot, daniel.vanschoot@upf.edu Exercises on the New-Keynesian Model Schedule: 28th of May (seminar 4): Exercises 1, 2 and

Optimal decumulation into annuity after retirement: a stochastic control approach

Optimal decumulation into annuity after retirement: a stochastic control approach Nicolas Langrené, Thomas Sneddon, Geo rey Lee, Zili Zhu 2 nd Congress on Actuarial Science and Quantitative Finance, Cartagena,

Optimal decumulation into annuity after retirement: a stochastic control approach Nicolas Langrené, Thomas Sneddon, Geo rey Lee, Zili Zhu 2 nd Congress on Actuarial Science and Quantitative Finance, Cartagena,

Characterization of the Optimum

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

ROBUST OPTIMIZATION OF MULTI-PERIOD PRODUCTION PLANNING UNDER DEMAND UNCERTAINTY. A. Ben-Tal, B. Golany and M. Rozenblit

ROBUST OPTIMIZATION OF MULTI-PERIOD PRODUCTION PLANNING UNDER DEMAND UNCERTAINTY A. Ben-Tal, B. Golany and M. Rozenblit Faculty of Industrial Engineering and Management, Technion, Haifa 32000, Israel ABSTRACT

ROBUST OPTIMIZATION OF MULTI-PERIOD PRODUCTION PLANNING UNDER DEMAND UNCERTAINTY A. Ben-Tal, B. Golany and M. Rozenblit Faculty of Industrial Engineering and Management, Technion, Haifa 32000, Israel ABSTRACT

Alpha, Beta, and Now Gamma

Alpha, Beta, and Now Gamma Scott Mackenzie President & CEO Morningstar Canada 2013 Morningstar. All Rights Reserved. These materials are for information and/or illustrative purposes only. The Morningstar

Alpha, Beta, and Now Gamma Scott Mackenzie President & CEO Morningstar Canada 2013 Morningstar. All Rights Reserved. These materials are for information and/or illustrative purposes only. The Morningstar

XSG. Economic Scenario Generator. Risk-neutral and real-world Monte Carlo modelling solutions for insurers

XSG Economic Scenario Generator Risk-neutral and real-world Monte Carlo modelling solutions for insurers 2 Introduction to XSG What is XSG? XSG is Deloitte s economic scenario generation software solution,

XSG Economic Scenario Generator Risk-neutral and real-world Monte Carlo modelling solutions for insurers 2 Introduction to XSG What is XSG? XSG is Deloitte s economic scenario generation software solution,

Translating Strategic Objectives into Individual Decisions

Translating Strategic Objectives into Individual Decisions The Emerging Landscape of Decision Optimization Scott Horwitz Fair Isaac Ian Brodie Fair Isaac Session: UND-1 AGENDA Three Key Insurer Challenges

Translating Strategic Objectives into Individual Decisions The Emerging Landscape of Decision Optimization Scott Horwitz Fair Isaac Ian Brodie Fair Isaac Session: UND-1 AGENDA Three Key Insurer Challenges

The application of linear programming to management accounting

The application of linear programming to management accounting After studying this chapter, you should be able to: formulate the linear programming model and calculate marginal rates of substitution and

The application of linear programming to management accounting After studying this chapter, you should be able to: formulate the linear programming model and calculate marginal rates of substitution and

Scenario-Based Value-at-Risk Optimization

Scenario-Based Value-at-Risk Optimization Oleksandr Romanko Quantitative Research Group, Algorithmics Incorporated, an IBM Company Joint work with Helmut Mausser Fields Industrial Optimization Seminar

Scenario-Based Value-at-Risk Optimization Oleksandr Romanko Quantitative Research Group, Algorithmics Incorporated, an IBM Company Joint work with Helmut Mausser Fields Industrial Optimization Seminar

Savings, Investment and the Real Interest Rate in an Endogenous Growth Model

Savings, Investment and the Real Interest Rate in an Endogenous Growth Model George Alogoskoufis* Athens University of Economics and Business October 2012 Abstract This paper compares the predictions of

Savings, Investment and the Real Interest Rate in an Endogenous Growth Model George Alogoskoufis* Athens University of Economics and Business October 2012 Abstract This paper compares the predictions of

Online Appendix: Extensions

B Online Appendix: Extensions In this online appendix we demonstrate that many important variations of the exact cost-basis LUL framework remain tractable. In particular, dual problem instances corresponding

B Online Appendix: Extensions In this online appendix we demonstrate that many important variations of the exact cost-basis LUL framework remain tractable. In particular, dual problem instances corresponding

Valuing Early Stage Investments with Market Related Timing Risk

Valuing Early Stage Investments with Market Related Timing Risk Matt Davison and Yuri Lawryshyn February 12, 216 Abstract In this work, we build on a previous real options approach that utilizes managerial

Valuing Early Stage Investments with Market Related Timing Risk Matt Davison and Yuri Lawryshyn February 12, 216 Abstract In this work, we build on a previous real options approach that utilizes managerial

Understanding Longevity Risk Annuitization Decisionmaking: An Interdisciplinary Investigation of Financial and Nonfinancial Triggers of Annuity Demand

Understanding Longevity Risk Annuitization Decisionmaking: An Interdisciplinary Investigation of Financial and Nonfinancial Triggers of Annuity Demand Jing Ai The University of Hawaii at Manoa, Honolulu,

Understanding Longevity Risk Annuitization Decisionmaking: An Interdisciplinary Investigation of Financial and Nonfinancial Triggers of Annuity Demand Jing Ai The University of Hawaii at Manoa, Honolulu,

White Paper. Liquidity Optimization: Going a Step Beyond Basel III Compliance

White Paper Liquidity Optimization: Going a Step Beyond Basel III Compliance Contents SAS: Delivering the Keys to Liquidity Optimization... 2 A Comprehensive Solution...2 Forward-Looking Insight...2 High

White Paper Liquidity Optimization: Going a Step Beyond Basel III Compliance Contents SAS: Delivering the Keys to Liquidity Optimization... 2 A Comprehensive Solution...2 Forward-Looking Insight...2 High

MFE8825 Quantitative Management of Bond Portfolios

MFE8825 Quantitative Management of Bond Portfolios William C. H. Leon Nanyang Business School March 18, 2018 1 / 150 William C. H. Leon MFE8825 Quantitative Management of Bond Portfolios 1 Overview 2 /

MFE8825 Quantitative Management of Bond Portfolios William C. H. Leon Nanyang Business School March 18, 2018 1 / 150 William C. H. Leon MFE8825 Quantitative Management of Bond Portfolios 1 Overview 2 /

INTERTEMPORAL ASSET ALLOCATION: THEORY

INTERTEMPORAL ASSET ALLOCATION: THEORY Multi-Period Model The agent acts as a price-taker in asset markets and then chooses today s consumption and asset shares to maximise lifetime utility. This multi-period

INTERTEMPORAL ASSET ALLOCATION: THEORY Multi-Period Model The agent acts as a price-taker in asset markets and then chooses today s consumption and asset shares to maximise lifetime utility. This multi-period

Risk Management for Chemical Supply Chain Planning under Uncertainty

for Chemical Supply Chain Planning under Uncertainty Fengqi You and Ignacio E. Grossmann Dept. of Chemical Engineering, Carnegie Mellon University John M. Wassick The Dow Chemical Company Introduction

for Chemical Supply Chain Planning under Uncertainty Fengqi You and Ignacio E. Grossmann Dept. of Chemical Engineering, Carnegie Mellon University John M. Wassick The Dow Chemical Company Introduction

Income Taxation and Stochastic Interest Rates

Income Taxation and Stochastic Interest Rates Preliminary and Incomplete: Please Do Not Quote or Circulate Thomas J. Brennan This Draft: May, 07 Abstract Note to NTA conference organizers: This is a very

Income Taxation and Stochastic Interest Rates Preliminary and Incomplete: Please Do Not Quote or Circulate Thomas J. Brennan This Draft: May, 07 Abstract Note to NTA conference organizers: This is a very

The Use of Regional Accounts System when Analyzing Economic Development of the Region

Doi:10.5901/mjss.2014.v5n24p383 Abstract The Use of Regional Accounts System when Analyzing Economic Development of the Region Kadochnikova E.I. Khisamova E.D. Kazan Federal University, Institute of Management,

Doi:10.5901/mjss.2014.v5n24p383 Abstract The Use of Regional Accounts System when Analyzing Economic Development of the Region Kadochnikova E.I. Khisamova E.D. Kazan Federal University, Institute of Management,

A Proper Derivation of the 7 Most Important Equations for Your Retirement

A Proper Derivation of the 7 Most Important Equations for Your Retirement Moshe A. Milevsky Version: August 13, 2012 Abstract In a recent book, Milevsky (2012) proposes seven key equations that are central

A Proper Derivation of the 7 Most Important Equations for Your Retirement Moshe A. Milevsky Version: August 13, 2012 Abstract In a recent book, Milevsky (2012) proposes seven key equations that are central

STOCHASTIC PROGRAMMING FOR ASSET ALLOCATION IN PENSION FUNDS

STOCHASTIC PROGRAMMING FOR ASSET ALLOCATION IN PENSION FUNDS IEGOR RUDNYTSKYI JOINT WORK WITH JOËL WAGNER > city date

STOCHASTIC PROGRAMMING FOR ASSET ALLOCATION IN PENSION FUNDS IEGOR RUDNYTSKYI JOINT WORK WITH JOËL WAGNER > city date

MS-E2114 Investment Science Lecture 4: Applied interest rate analysis

MS-E2114 Investment Science Lecture 4: Applied interest rate analysis A. Salo, T. Seeve Systems Analysis Laboratory Department of System Analysis and Mathematics Aalto University, School of Science Overview

MS-E2114 Investment Science Lecture 4: Applied interest rate analysis A. Salo, T. Seeve Systems Analysis Laboratory Department of System Analysis and Mathematics Aalto University, School of Science Overview

The Duration Derby: A Comparison of Duration Based Strategies in Asset Liability Management

The Duration Derby: A Comparison of Duration Based Strategies in Asset Liability Management H. Zheng Department of Mathematics, Imperial College London SW7 2BZ, UK h.zheng@ic.ac.uk L. C. Thomas School

The Duration Derby: A Comparison of Duration Based Strategies in Asset Liability Management H. Zheng Department of Mathematics, Imperial College London SW7 2BZ, UK h.zheng@ic.ac.uk L. C. Thomas School

Comments on social insurance and the optimum piecewise linear income tax

Comments on social insurance and the optimum piecewise linear income tax Michael Lundholm May 999; Revised June 999 Abstract Using Varian s social insurance framework with a piecewise linear two bracket

Comments on social insurance and the optimum piecewise linear income tax Michael Lundholm May 999; Revised June 999 Abstract Using Varian s social insurance framework with a piecewise linear two bracket

HOUSEHOLD RISKY ASSET CHOICE: AN EMPIRICAL STUDY USING BHPS

HOUSEHOLD RISKY ASSET CHOICE: AN EMPIRICAL STUDY USING BHPS by DEJING KONG A thesis submitted to the University of Birmingham for the degree of DOCTOR OF PHILOSOPHY Department of Economics Birmingham Business

HOUSEHOLD RISKY ASSET CHOICE: AN EMPIRICAL STUDY USING BHPS by DEJING KONG A thesis submitted to the University of Birmingham for the degree of DOCTOR OF PHILOSOPHY Department of Economics Birmingham Business

Alpha, Beta, and Now Gamma

Alpha, Beta, and Now Gamma David Blanchett, CFA, CFP Head of Retirement Research Morningstar Investment Management 2012 Morningstar. All Rights Reserved. These materials are for information and/or illustration

Alpha, Beta, and Now Gamma David Blanchett, CFA, CFP Head of Retirement Research Morningstar Investment Management 2012 Morningstar. All Rights Reserved. These materials are for information and/or illustration

Life insurance portfolio aggregation

1/23 Life insurance portfolio aggregation Is it optimal to group policyholders by age, gender, and seniority for BEL computations based on model points? Pierre-Olivier Goffard Université Libre de Bruxelles

1/23 Life insurance portfolio aggregation Is it optimal to group policyholders by age, gender, and seniority for BEL computations based on model points? Pierre-Olivier Goffard Université Libre de Bruxelles

Evolutionary Behavioural Finance

Evolutionary Behavioural Finance Rabah Amir (University of Iowa) Igor Evstigneev (University of Manchester) Thorsten Hens (University of Zurich) Klaus Reiner Schenk-Hoppé (University of Manchester) The

Evolutionary Behavioural Finance Rabah Amir (University of Iowa) Igor Evstigneev (University of Manchester) Thorsten Hens (University of Zurich) Klaus Reiner Schenk-Hoppé (University of Manchester) The

About the Risk Quantification of Technical Systems

About the Risk Quantification of Technical Systems Magda Schiegl ASTIN Colloquium 2013, The Hague Outline Introduction / Overview Fault Tree Analysis (FTA) Method of quantitative risk analysis Results

About the Risk Quantification of Technical Systems Magda Schiegl ASTIN Colloquium 2013, The Hague Outline Introduction / Overview Fault Tree Analysis (FTA) Method of quantitative risk analysis Results

Economic optimization in Model Predictive Control

Economic optimization in Model Predictive Control Rishi Amrit Department of Chemical and Biological Engineering University of Wisconsin-Madison 29 th February, 2008 Rishi Amrit (UW-Madison) Economic Optimization

Economic optimization in Model Predictive Control Rishi Amrit Department of Chemical and Biological Engineering University of Wisconsin-Madison 29 th February, 2008 Rishi Amrit (UW-Madison) Economic Optimization

MACROECONOMICS. Prelim Exam

MACROECONOMICS Prelim Exam Austin, June 1, 2012 Instructions This is a closed book exam. If you get stuck in one section move to the next one. Do not waste time on sections that you find hard to solve.

MACROECONOMICS Prelim Exam Austin, June 1, 2012 Instructions This is a closed book exam. If you get stuck in one section move to the next one. Do not waste time on sections that you find hard to solve.

KELLY CAPITAL GROWTH

World Scientific Handbook in Financial Economic Series Vol. 3 THEORY and PRACTICE THE KELLY CAPITAL GROWTH INVESTMENT CRITERION Editors ' jj Leonard C MacLean Dalhousie University, USA Edward 0 Thorp University

World Scientific Handbook in Financial Economic Series Vol. 3 THEORY and PRACTICE THE KELLY CAPITAL GROWTH INVESTMENT CRITERION Editors ' jj Leonard C MacLean Dalhousie University, USA Edward 0 Thorp University

DO NOT OPEN THIS QUESTION PAPER UNTIL YOU ARE TOLD TO DO SO. Performance Pillar. P1 Performance Operations. Wednesday 27 August 2014

DO NOT OPEN THIS QUESTION PAPER UNTIL YOU ARE TOLD TO DO SO. Performance Pillar P1 Performance Operations Instructions to candidates Wednesday 27 August 2014 You are allowed three hours to answer this

DO NOT OPEN THIS QUESTION PAPER UNTIL YOU ARE TOLD TO DO SO. Performance Pillar P1 Performance Operations Instructions to candidates Wednesday 27 August 2014 You are allowed three hours to answer this

HEDGE FUND INVESTING INTERNATIONALLY

RESEARCH, MANAGER SELECTION, AND PORTFOLIO CONSTRUCTION FOCUSED ON INVESTORS FROM BRAZIL Risk Advisors Inc. assists Brazilian investors seeking to add international diversification to their portfolios.

RESEARCH, MANAGER SELECTION, AND PORTFOLIO CONSTRUCTION FOCUSED ON INVESTORS FROM BRAZIL Risk Advisors Inc. assists Brazilian investors seeking to add international diversification to their portfolios.

Member s Default Utility Function Version 1 (MDUF v1)

") Member s Default Utility Function Version 1 (MDUF v1) David Bell, Estelle Liu and Adam Shao MDUF Lead Authors This presentation has been prepared for the Actuaries Institute 2017 Actuaries Summit. The

Member s Default Utility Function Version 1 (MDUF v1) David Bell, Estelle Liu and Adam Shao MDUF Lead Authors This presentation has been prepared for the Actuaries Institute 2017 Actuaries Summit. The

Multistage risk-averse asset allocation with transaction costs

Multistage risk-averse asset allocation with transaction costs 1 Introduction Václav Kozmík 1 Abstract. This paper deals with asset allocation problems formulated as multistage stochastic programming models.

Multistage risk-averse asset allocation with transaction costs 1 Introduction Václav Kozmík 1 Abstract. This paper deals with asset allocation problems formulated as multistage stochastic programming models.

NATIONWIDE ASSET ALLOCATION INVESTMENT PROCESS

Nationwide Funds A Nationwide White Paper NATIONWIDE ASSET ALLOCATION INVESTMENT PROCESS May 2017 INTRODUCTION In the market decline of 2008, the S&P 500 Index lost more than 37%, numerous equity strategies

Nationwide Funds A Nationwide White Paper NATIONWIDE ASSET ALLOCATION INVESTMENT PROCESS May 2017 INTRODUCTION In the market decline of 2008, the S&P 500 Index lost more than 37%, numerous equity strategies

Dynamic Asset Allocation for Hedging Downside Risk

Dynamic Asset Allocation for Hedging Downside Risk Gerd Infanger Stanford University Department of Management Science and Engineering and Infanger Investment Technology, LLC October 2009 Gerd Infanger,

Dynamic Asset Allocation for Hedging Downside Risk Gerd Infanger Stanford University Department of Management Science and Engineering and Infanger Investment Technology, LLC October 2009 Gerd Infanger,

Vanguard Global Capital Markets Model

Vanguard Global Capital Markets Model Research brief March 1 Vanguard s Global Capital Markets Model TM (VCMM) is a proprietary financial simulation engine designed to help our clients make effective asset

Vanguard Global Capital Markets Model Research brief March 1 Vanguard s Global Capital Markets Model TM (VCMM) is a proprietary financial simulation engine designed to help our clients make effective asset

CFA Level III - LOS Changes

CFA Level III - LOS Changes 2016-2017 Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Topic LOS Level III - 2016 (332 LOS) LOS Level III - 2017 (337 LOS) Compared 1.1.a 1.1.b 1.2.a 1.2.b 2.3.a

CFA Level III - LOS Changes 2016-2017 Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Topic LOS Level III - 2016 (332 LOS) LOS Level III - 2017 (337 LOS) Compared 1.1.a 1.1.b 1.2.a 1.2.b 2.3.a

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Preliminary Examination: Macroeconomics Fall, 2009

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Preliminary Examination: Macroeconomics Fall, 2009 Instructions: Read the questions carefully and make sure to show your work. You

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Preliminary Examination: Macroeconomics Fall, 2009 Instructions: Read the questions carefully and make sure to show your work. You

Life-cycle Asset Allocation and Optimal Consumption Using Stochastic Linear Programming

Life-cycle Asset Allocation and Optimal Consumption Using Stochastic Linear Programming Preliminary draft; first version: December 21, 2006; this version: March 8, 2007 Abstract We consider optimal consumption

Life-cycle Asset Allocation and Optimal Consumption Using Stochastic Linear Programming Preliminary draft; first version: December 21, 2006; this version: March 8, 2007 Abstract We consider optimal consumption

5. Results

A stochastic programming model for asset liability management of a Finnish pension company Λ Petri Hilli, Matti Koivu, Teemu Pennanen Helsinki School of Economics Antero Ranne Mutual Pension Insurance

A stochastic programming model for asset liability management of a Finnish pension company Λ Petri Hilli, Matti Koivu, Teemu Pennanen Helsinki School of Economics Antero Ranne Mutual Pension Insurance

INTRODUCTION TO FINANCIAL MANAGEMENT

INTRODUCTION TO FINANCIAL MANAGEMENT Meaning of Financial Management As we know finance is the lifeblood of every business, its management requires special attention. Financial management is that activity

INTRODUCTION TO FINANCIAL MANAGEMENT Meaning of Financial Management As we know finance is the lifeblood of every business, its management requires special attention. Financial management is that activity

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Fixed-Income Securities Lecture 5: Tools from Option Pricing

Fixed-Income Securities Lecture 5: Tools from Option Pricing Philip H. Dybvig Washington University in Saint Louis Review of binomial option pricing Interest rates and option pricing Effective duration

Fixed-Income Securities Lecture 5: Tools from Option Pricing Philip H. Dybvig Washington University in Saint Louis Review of binomial option pricing Interest rates and option pricing Effective duration

Calibration of Stochastic Risk-Free Interest Rate Models for Use in CALM Valuation

Revised Educational Note Supplement Calibration of Stochastic Risk-Free Interest Rate Models for Use in CALM Valuation Committee on Life Insurance Financial Reporting August 2017 Document 217085 Ce document

Revised Educational Note Supplement Calibration of Stochastic Risk-Free Interest Rate Models for Use in CALM Valuation Committee on Life Insurance Financial Reporting August 2017 Document 217085 Ce document

Continuing Education Course #287 Engineering Methods in Microsoft Excel Part 2: Applied Optimization

1 of 6 Continuing Education Course #287 Engineering Methods in Microsoft Excel Part 2: Applied Optimization 1. Which of the following is NOT an element of an optimization formulation? a. Objective function

1 of 6 Continuing Education Course #287 Engineering Methods in Microsoft Excel Part 2: Applied Optimization 1. Which of the following is NOT an element of an optimization formulation? a. Objective function

Lecture outline W.B.Powell 1

Lecture outline What is a policy? Policy function approximations (PFAs) Cost function approximations (CFAs) alue function approximations (FAs) Lookahead policies Finding good policies Optimizing continuous

Lecture outline What is a policy? Policy function approximations (PFAs) Cost function approximations (CFAs) alue function approximations (FAs) Lookahead policies Finding good policies Optimizing continuous

Probability and Stochastics for finance-ii Prof. Joydeep Dutta Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur

Probability and Stochastics for finance-ii Prof. Joydeep Dutta Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur Lecture - 07 Mean-Variance Portfolio Optimization (Part-II)

Probability and Stochastics for finance-ii Prof. Joydeep Dutta Department of Humanities and Social Sciences Indian Institute of Technology, Kanpur Lecture - 07 Mean-Variance Portfolio Optimization (Part-II)

Lewis Coopersmith, Ph. D.

Making the Most of One s Nest Egg: Optimal Tax-wise Planning of Withdrawals from Retirement Accounts* INFORMS New York Metro Wednesday, December 12, 2007 Lewis Coopersmith, Ph. D. Associate Professor,

Making the Most of One s Nest Egg: Optimal Tax-wise Planning of Withdrawals from Retirement Accounts* INFORMS New York Metro Wednesday, December 12, 2007 Lewis Coopersmith, Ph. D. Associate Professor,

Comprehensive Exam. August 19, 2013

Comprehensive Exam August 19, 2013 You have a total of 180 minutes to complete the exam. If a question seems ambiguous, state why, sharpen it up and answer the sharpened-up question. Good luck! 1 1 Menu

Comprehensive Exam August 19, 2013 You have a total of 180 minutes to complete the exam. If a question seems ambiguous, state why, sharpen it up and answer the sharpened-up question. Good luck! 1 1 Menu

The Diversification of Employee Stock Options

The Diversification of Employee Stock Options David M. Stein Managing Director and Chief Investment Officer Parametric Portfolio Associates Seattle Andrew F. Siegel Professor of Finance and Management

The Diversification of Employee Stock Options David M. Stein Managing Director and Chief Investment Officer Parametric Portfolio Associates Seattle Andrew F. Siegel Professor of Finance and Management

Progressive Hedging for Multi-stage Stochastic Optimization Problems

Progressive Hedging for Multi-stage Stochastic Optimization Problems David L. Woodruff Jean-Paul Watson Graduate School of Management University of California, Davis Davis, CA 95616, USA dlwoodruff@ucdavis.edu

Progressive Hedging for Multi-stage Stochastic Optimization Problems David L. Woodruff Jean-Paul Watson Graduate School of Management University of California, Davis Davis, CA 95616, USA dlwoodruff@ucdavis.edu

1 Unemployment Insurance

1 Unemployment Insurance 1.1 Introduction Unemployment Insurance (UI) is a federal program that is adminstered by the states in which taxes are used to pay for bene ts to workers laid o by rms. UI started

1 Unemployment Insurance 1.1 Introduction Unemployment Insurance (UI) is a federal program that is adminstered by the states in which taxes are used to pay for bene ts to workers laid o by rms. UI started

THE OPTIMAL ASSET ALLOCATION PROBLEMFOR AN INVESTOR THROUGH UTILITY MAXIMIZATION

THE OPTIMAL ASSET ALLOCATION PROBLEMFOR AN INVESTOR THROUGH UTILITY MAXIMIZATION SILAS A. IHEDIOHA 1, BRIGHT O. OSU 2 1 Department of Mathematics, Plateau State University, Bokkos, P. M. B. 2012, Jos,

THE OPTIMAL ASSET ALLOCATION PROBLEMFOR AN INVESTOR THROUGH UTILITY MAXIMIZATION SILAS A. IHEDIOHA 1, BRIGHT O. OSU 2 1 Department of Mathematics, Plateau State University, Bokkos, P. M. B. 2012, Jos,

Understanding the Principles of Investment Planning Stochastic Modelling/Tactical & Strategic Asset Allocation

Understanding the Principles of Investment Planning Stochastic Modelling/Tactical & Strategic Asset Allocation John Thompson, Vice President & Portfolio Manager London, 11 May 2011 What is Diversification

Understanding the Principles of Investment Planning Stochastic Modelling/Tactical & Strategic Asset Allocation John Thompson, Vice President & Portfolio Manager London, 11 May 2011 What is Diversification

The Collective Model of Household : Theory and Calibration of an Equilibrium Model

The Collective Model of Household : Theory and Calibration of an Equilibrium Model Eleonora Matteazzi, Martina Menon, and Federico Perali University of Verona University of Verona University of Verona

The Collective Model of Household : Theory and Calibration of an Equilibrium Model Eleonora Matteazzi, Martina Menon, and Federico Perali University of Verona University of Verona University of Verona

On Effects of Asymmetric Information on Non-Life Insurance Prices under Competition

On Effects of Asymmetric Information on Non-Life Insurance Prices under Competition Albrecher Hansjörg Department of Actuarial Science, Faculty of Business and Economics, University of Lausanne, UNIL-Dorigny,

On Effects of Asymmetric Information on Non-Life Insurance Prices under Competition Albrecher Hansjörg Department of Actuarial Science, Faculty of Business and Economics, University of Lausanne, UNIL-Dorigny,

Classic and Modern Measures of Risk in Fixed

Classic and Modern Measures of Risk in Fixed Income Portfolio Optimization Miguel Ángel Martín Mato Ph. D in Economic Science Professor of Finance CENTRUM Pontificia Universidad Católica del Perú. C/ Nueve

Classic and Modern Measures of Risk in Fixed Income Portfolio Optimization Miguel Ángel Martín Mato Ph. D in Economic Science Professor of Finance CENTRUM Pontificia Universidad Católica del Perú. C/ Nueve

CSCI 1951-G Optimization Methods in Finance Part 00: Course Logistics Introduction to Finance Optimization Problems

CSCI 1951-G Optimization Methods in Finance Part 00: Course Logistics Introduction to Finance Optimization Problems January 26, 2018 1 / 24 Basic information All information is available in the syllabus

CSCI 1951-G Optimization Methods in Finance Part 00: Course Logistics Introduction to Finance Optimization Problems January 26, 2018 1 / 24 Basic information All information is available in the syllabus

Dynamic Risk Management in Electricity Portfolio Optimization via Polyhedral Risk Functionals

Dynamic Risk Management in Electricity Portfolio Optimization via Polyhedral Risk Functionals A. Eichhorn and W. Römisch Humboldt-University Berlin, Department of Mathematics, Germany http://www.math.hu-berlin.de/~romisch

Dynamic Risk Management in Electricity Portfolio Optimization via Polyhedral Risk Functionals A. Eichhorn and W. Römisch Humboldt-University Berlin, Department of Mathematics, Germany http://www.math.hu-berlin.de/~romisch

Axioma Research Paper No January, Multi-Portfolio Optimization and Fairness in Allocation of Trades

Axioma Research Paper No. 013 January, 2009 Multi-Portfolio Optimization and Fairness in Allocation of Trades When trades from separately managed accounts are pooled for execution, the realized market-impact

Axioma Research Paper No. 013 January, 2009 Multi-Portfolio Optimization and Fairness in Allocation of Trades When trades from separately managed accounts are pooled for execution, the realized market-impact

A Study on Optimal Limit Order Strategy using Multi-Period Stochastic Programming considering Nonexecution Risk

Proceedings of the Asia Pacific Industrial Engineering & Management Systems Conference 2018 A Study on Optimal Limit Order Strategy using Multi-Period Stochastic Programming considering Nonexecution Ris

Proceedings of the Asia Pacific Industrial Engineering & Management Systems Conference 2018 A Study on Optimal Limit Order Strategy using Multi-Period Stochastic Programming considering Nonexecution Ris

A MATHEMATICAL PROGRAMMING APPROACH TO ANALYZE THE ACTIVITY-BASED COSTING PRODUCT-MIX DECISION WITH CAPACITY EXPANSIONS

A MATHEMATICAL PROGRAMMING APPROACH TO ANALYZE THE ACTIVITY-BASED COSTING PRODUCT-MIX DECISION WITH CAPACITY EXPANSIONS Wen-Hsien Tsai and Thomas W. Lin ABSTRACT In recent years, Activity-Based Costing

A MATHEMATICAL PROGRAMMING APPROACH TO ANALYZE THE ACTIVITY-BASED COSTING PRODUCT-MIX DECISION WITH CAPACITY EXPANSIONS Wen-Hsien Tsai and Thomas W. Lin ABSTRACT In recent years, Activity-Based Costing

The Impact of Stochastic Volatility and Policyholder Behaviour on Guaranteed Lifetime Withdrawal Benefits

and Policyholder Guaranteed Lifetime 8th Conference in Actuarial Science & Finance on Samos 2014 Frankfurt School of Finance and Management June 1, 2014 1. Lifetime withdrawal guarantees in PLIs 2. policyholder

and Policyholder Guaranteed Lifetime 8th Conference in Actuarial Science & Finance on Samos 2014 Frankfurt School of Finance and Management June 1, 2014 1. Lifetime withdrawal guarantees in PLIs 2. policyholder

Solving dynamic portfolio choice problems by recursing on optimized portfolio weights or on the value function?

DOI 0.007/s064-006-9073-z ORIGINAL PAPER Solving dynamic portfolio choice problems by recursing on optimized portfolio weights or on the value function? Jules H. van Binsbergen Michael W. Brandt Received:

DOI 0.007/s064-006-9073-z ORIGINAL PAPER Solving dynamic portfolio choice problems by recursing on optimized portfolio weights or on the value function? Jules H. van Binsbergen Michael W. Brandt Received:

10 Steps to realising real cash value from Innovation and IC Assets. Ludo Pyis Areopa

10 Steps to realising real cash value from Innovation and IC Assets Ludo Pyis Areopa Areopa Trust Oct 2014 Topics The Fundamentals of Intellectual Capital and Intellectual Property Quick Scan of IC approach

10 Steps to realising real cash value from Innovation and IC Assets Ludo Pyis Areopa Areopa Trust Oct 2014 Topics The Fundamentals of Intellectual Capital and Intellectual Property Quick Scan of IC approach

Is the Maastricht debt limit safe enough for Slovakia?

Is the Maastricht debt limit safe enough for Slovakia? Fiscal Limits and Default Risk Premia for Slovakia Moderné nástroje pre finančnú analýzu a modelovanie Zuzana Múčka June 15, 2015 Introduction Aims

Is the Maastricht debt limit safe enough for Slovakia? Fiscal Limits and Default Risk Premia for Slovakia Moderné nástroje pre finančnú analýzu a modelovanie Zuzana Múčka June 15, 2015 Introduction Aims

PART II IT Methods in Finance

PART II IT Methods in Finance Introduction to Part II This part contains 12 chapters and is devoted to IT methods in finance. There are essentially two ways where IT enters and influences methods used

PART II IT Methods in Finance Introduction to Part II This part contains 12 chapters and is devoted to IT methods in finance. There are essentially two ways where IT enters and influences methods used

Sang-Wook (Stanley) Cho

Cho") Beggar-thy-parents? A Lifecycle Model of Intergenerational Altruism Sang-Wook (Stanley) Cho University of New South Wales March 2009 Motivation & Question Since Becker (1974), several studies analyzing

Beggar-thy-parents? A Lifecycle Model of Intergenerational Altruism Sang-Wook (Stanley) Cho University of New South Wales March 2009 Motivation & Question Since Becker (1974), several studies analyzing