ACCOUNTING RISK A CHALLENGE TO IFRS (A CASE STUDY OF RELIANCE AND TCS)

|

|

|

- Reynard Griffin

- 6 years ago

- Views:

Transcription

1 KAAV INTERNATIONAL JOURNAL OF ECONOMICS,COMMERCE & BUSINESS MANAGEMENT ACCOUNTING RISK A CHALLENGE TO IFRS (A CASE STUDY OF RELIANCE AND TCS) BHARAT KUMAR MEHER Research Scholar Department of Commerce Dr.HarisinghGour Central University LATASHA MOHAPATRA M.Com IV Semester Department of Commerce Dr.HarisinghGour Central University Abstract With the increase in the export and import of goods there is a need of more foreign exchange to make the Indian currency stronger. But due to the fluctuations in foreign exchange it may be costlier for importing of goods. These fluctuations not only affect the economy but also affect the accounting statements of Multinational Companies (MNCs) as they trade goods to/from other countries. The extent to which the foreign exchange rate fluctuations affect the financial statements of an organization is known as Accounting Risk also called as accounting exposure or translation risk. India is in the stage of adopting International Financial Reporting System (IFRS) and there is a need to covert the figures of financial statements from Indian Currency to dollars while reporting the financial statements under IFRS. The accounting standard related to the Effects of Changes in Foreign Exchange Rates is mentioned in Indian Accounting Standard 11 and also in International Accounting Standard 21. The prevailing accounting system covers the method to covert the figures of Financial Statements from Indian currency to other foreign currency. The accounting standard suggest a proper treatment of the Effects of Changes in Foreign Exchange Rates so as to maintain the uniformity in treatment but it cannot eliminate the effect of exchange rate on final statements. The paper is an attempt to know how accounting risk affect the financial statements of two big companies of India (i.e. Reliance and TCS)? Can it be possible for IFRS to reduce the chances of occurring accounting risk after the complete adoption of IFRS in India? Key Words : Accounting Risk, IFRS, IAS 21 6

2 Introduction Due to Globalization, our close economy has been converted into open economy. In this globalisation our national economyis integrating withtheeconomyof other countries by spreading its trade and business activities outside the country. Contract Manufacturing, Foreign Direct Investments, Foreign Institutional Investors, Licensing, Joint Venture, Merger and Acquisition,Franchising and Business Outsourcing are some examples of international transactions in global business.but the problem is maintaining and reporting of accounting transactions differ in different countries as the different countries do not follow uniform accounting standards. Hence for the integrity of different county's business together in the world market it was necessary for the businessto adopt a common set of accounting standard, since accounting is the language of a business. For this purpose in1973, many professionals from different countries established the International AccountingStandard Committee. The main objective to this committee is to issue International Accounting Standards. Atpresent time Ministry of Corporate Affairs notified 35 International Accounting Standards. In 2001 InternationalAccounting Standard Committee are superseded as International Accounting Standard Board. Now theboard issues the International Financial Reporting Standard (IFRS) formerly known as International AccountingStandards. The use of common set of accounting standards throughout the world provides an easy way of comparability and transparency of financial information. Hence for the purpose of common set of accounting standards, International Financial Reporting Standards (IFRS) have been proposed. IFRS is a set of accounting standards developed by an independent, not-for-profit organization called the International Accounting Standards Board (IASB).It also reduces the cost of preparing financialstatements. A constant use of accounting standards provide higher quality information which enables theinvestors to make a better decision, indirectly fund will allocate in more efficient manner in the market andthe company can reduce its overall cost of capital. The prime goal of IFRS is to provide a global framework for how public companies prepare and disclose their financial statements. IFRS provides general guidance for the preparation of financial statements, rather than setting rules for industry-specific reporting. Under IFRS the financial statements are to be reported in two currency i.e. one is home currency and another one is international currency i.e. Dollars. For the conversion of figures from home currency into foreign currency the International Accounting Standard 21 (IAS 21) is to be followed. 7

3 This paper shows a clear picture of how the amount of financial statements items in functional currency is converted into international currency while reporting under IFRS. Do the converted figures in international currency reflects the same activity ratios as from the figures in functional currency? Moreover the study is also concerned in determining the ability of IFRS in reduction of Accounting Risk which rises due to the fluctuations in exchange rate. Objective of the Study To know whether conversion of figures of Financial Statements of two selected Companies affects the Activity s. To study upto what extent IFRS can reduce the Accounting Risk. Hypotheses of the Study H 0 : The Activity s from the figures of financial statements of TCS reported in home currency are equal to that of figures of financial statements reported in International Currency i.e. Dollars. H 1 : The Activity s from the figures of financial statements of TCS reported in home currency are not equal to that of figures of financial statements reported in International Currency i.e. Dollars. H 0 : IFRS can reduce the chances of occurring Accounting Risk. H 1 : IFRS cannot reduce the chances of occurring Accounting Risk. Research Methodology The study is empirical in nature. The study is totally based on Secondary Data collected from various websites, journals and newspapers related to Indian Accounting Standard, International Accounting Standard and International Financial Reporting System (IFRS). Two Big Companies of India i.e. Reliance Industries and Tata Consultancy Services are selected for the study. The period taken into consideration in this study, is two years i.e and Activity s of both the companies of two years i.e & are taken into consideration to examine the existence of Accounting Risk. For the purpose of calculating the significant difference, a rule of thumb has been set and the variation in percentage is calculated 8

4 between the figures of financial statements reported in Rs. and figures of financial statements reported in Dollors. Importance of the Study IFRS has already been adopted by many companies of India and there is much more possibility that all the companies in India, trading across the world, will have to follow the IFRS in the near future. Under IFRS it will be quite mandatory for the companies to report the figures in both the currencies i.e. Functional Currency as well as International Currency. Hence it is important to understand how the financial statements are to be reported and converted into International Currency i.e. US Dollars under IFRS. But while conversion of functional currency into international currency, there is always a possibility of rising accounting risk due to the fluctuations in foreign exchange. The paper attempts to study whether the IFRS can reduce the chances of occurring accounting risk. The study will also be helpful to know the problem and lacunas in implementing IFRS in India. Limitations of the Study The study is limited to two companies i.e. Reliance India Limited and Tata Consultancy Services. Only Activity s are taken into consideration to study the Percentage Variation of Figures reported in Dollars and in Rs. There are many regulations which are to be taken into consideration while converting the financial statements under IAS into IFRS. Due to the lack of information related to the realisable value of assets, the financial statements reported under IAS are very difficult to be converted under IFRS. About the Problem The extent to which the financial statements of companies can be affected by exchange rate fluctuations is known as Accounting Risk. Accounting Risk is also known as Accounting Exposure or translation risk. Such type of risk came into existence when the countries are exposed to globalisation. As there are many transactions taking place between countries, there is a need to record the transactions and report these in both functional and reporting currency. For this purpose the International Accounting Standard 21 is to be followed by the companies. The objective of IAS 21 i.e. The Effects of Changes in Foreign Exchange Rates is to prescribed :- How to include foreign currency transactions and foreign operations in the financial statements of an entity; and 9

5 How to translate financial statements into a presentation currency. In other words, IAS 21 answers 2 basic questions: What exchange rates shall we use? How to report gains or losses from foreign exchange rates in the financial statements? An entity is required to translate its results and financial position from itsfunctional currency into a presentation currency (or currencies) using the method required for translating a foreign operation for inclusion in the reporting entity s financial statements. The results and financial position of an entity whose functional currency is not the currency of a hyperinflationary economy shall be translated into a different presentation currency using the following procedures: a) assets and liabilities for each statement of financial position presented (ie including comparatives) shall betranslated at the closing rate at the date of that statement of financial position; b) income and expenses for each statement of comprehensive income or separate income statement presented(ie including comparatives) shall be translated at exchange rates at the dates of the transactions; and c) all resulting exchange differences shall be recognised in other comprehensive income. Any goodwill arising on the acquisition of a foreign operation and any fair value adjustments to the carryingamounts of assets and liabilities arising on the acquisition of that foreign operation shall be treated as assetsand liabilities of the foreign operation. Foreign operation is an entity that is a subsidiary, associate, joint venture or branch of a reporting entity, the activities of which are based or conducted in a country or currency other than those of the reporting entity. On the disposal of a foreign operation, the cumulative amount of the exchange differences relating to that foreign operation, recognised in other comprehensive income and accumulated in the separate component of equity, shall be reclassified from equity to profit or loss (as a reclassification adjustment) when the gain or loss on disposal is recognised. Two companies are selected for showing the presentation of financial statements under IFRS. One is Reliance Industries and another one is Tata Consultancy Services. Both the companies are selected for the study as they are in the top 10 listed companies in India. Reliance Industries Ltd. is an Indian multinational conglomerate operating in various sectors in and outside India. Founded in 1966, RIL is based in Mumbai, Maharashtra. RIL deals in miscellaneous industries such as construction, energy, petrochemicals, communications, science 10

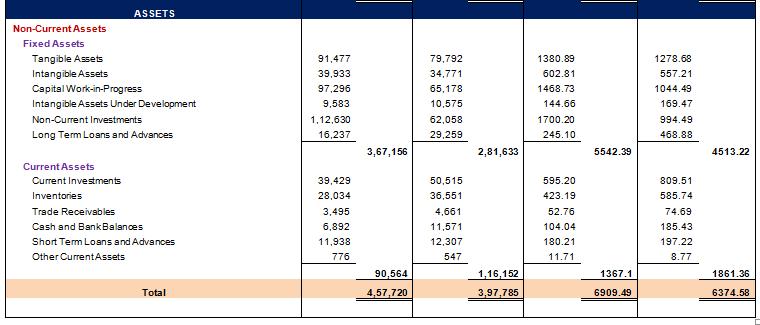

6 and technology, healthcare, textiles, retails, natural resources and logistics. The principal shareholders, the Ambani family, hold close to percent shares in the company, while the rest of the shares are held by approximately three million shareholders. In May 2015, the market capitalisation of RIL amounted to Rs. 2,85,051.72crore. At present, Reliance Industries Limited is not following the IFRS. Hence to explain the process of converting the figures from Rs. to Dollors RIL would be a suitable company which engages in both production activities and providing services. The other company i.e. Tata Consultancy Services (TCS) is a global leader in IT services, digital and business solutions that partners with its clients to simplify, strengthen and transform their businesses. It ensures the highest levels of certainty and satisfaction through a deep-set commitment to its clients, comprehensive industry expertise and a global network of innovation and delivery centres. The purpose for selecting TCS for the study is that the company is presenting its financial statements under 3 types of standards i.e. US GAAP, Indian Accounting Standard and IFRS. Profit and Loss Statement of Reliance Industries for the year ended on 31 st March 2016 (Amt. in Millions) The US Dollar to Indian Rupee Exchange Rate on 1 st April, USD INR The US Dollar to Indian Rupee Exchange Rate on 31 st March, USD INR The US Dollar to Indian Rupee Exchange Rate on 1 st April, USD INR The US Dollar to Indian Rupee Exchange Rate on 31 st March, USD INR Balance Sheet of Reliance Industries as on 31 st March 2016 (Amt. in Millions) 11

7 12

8 Profit and Loss Statement of TCS for the year ended on 31 st March (Amt. in Millions) TCS Consolidated Income Statement as per IFRS - FY Amt. Rs. FY 15-16Amt.Rs. FY 14-15Amt $ FY 15-16Amt $ Revenue Information Technology and Consultancy Services 9,27,017 0,86,462 15, , Sale of Equipment and Software Licenses 19, Total Revenue 9,46,484 10,86,462 15, , Cost of Revenues Cost of Services Employee Cost 3,62,844 4,18,829 5, , Fees to External Consultants 61,165 78, , Cost of Equipment and Software Licenses 18,601 25, Depreciation 12,719 13, Travel 14,567 15, Communication 7,515 8, Facility Expenses 21,662 21, Other Costs 26,210 26, Total Cost of Revenues 5,25,283 6,08,997 8, , Gross Profit 4,21,201 4,77,465 6, , Operating Expenses Selling, General and Administrative Expenses Employee Cost 1,18,164 1,34,666 1, , Fees to External Consultants 5,280 5, Provision for Doubtful Debts 1,605 1, Depreciation 5,980 5, Facility Expenses 10,175 12, Travel 9,452 10, Communication 3,045 2, Other Costs 13,256 16, Total Operating Expenses 1,66,957 1,89,565 2, , Operating Income 2,54,244 2,87,901 4, , Total Other Income/(Expense) 31,397 30, Income Before Income Taxes 2,85,641 3,18,403 4, , Total Taxes 66,566 75,026 1, , Net Profit After Taxes 2,19,075 2,43,376 3, , Adjustments for Minority Interests Non Controlling Interest -2,114-1, Net Income Before Extraordinary Items 2,16,961 2,42,149 3, , Net Income After Extraordinary Items 2,16,961 2,42,149 3, ,

9 Balance Sheet of TCS as on 31 st March (Amt. in Millions) If Reporting Under IFRS Amt $ Amt $ TCS Consolidated Balance Sheet as per IFRS - INR Mn 31-Mar Mar Mar Mar-16 ASSETS Current Assets Cash and Cash Equivalents 18,622 62, Bank Deposits 1,63, Accounts Receivable ( net of allowances ) 2,04,399 2,40, , Investments 15,009 2,24, , Other Current Financial Assets 27,142 40, Unbilled Revenue 38,271 39, Current Income Tax assets Other Current Assets 20,990 21, Total Current Assets 4,89,011 6,31, , Non Current assets Bank Deposits 5,001 4, Other Non Current Financial Assets 23,156 33, Non Current Income Tax Assets 40,930 44, Deferred Income Tax Assets 26,150 28, Property, Plant and Equipment, net 1,15,716 1,17, , Goodwill, net 37,115 38, Other Intangible Assets, net 2,193 1, Investments 2,534 3, Other Non-Current Assets 9,064 7, Total Non-Current Assets 2,61,859 2,80, , LIABILITIES AND SHAREHOLDER'S EQUITY Liabilities Current Liabilities Total Assets 7,50,868 9,12, , Trade and Other Payables 88,318 75, , Short-term Borrowings 2,434 1, Other Current Financial Liabilities 11,878 23, Unearned and Deferred Revenue 10,623 13, Employee Benefit Obligation 13,561 16, Other provisions 1,030 1, Current Income Tax Liabilities 5,456 8, Accrued Expenses and Other Current Liabilities 13,415 16, Total Current Liabilities 1,46,716 1,55, , Non Current Liabilities Long-Term Debt / Borrowings 1, Other Non Current Financial Liabilities 6,618 4, Employee Benefit Obligation 2,034 2, Other provisions

10 Deferred Income Tax Liabilities 5,473 8, Other Non-Current Liabilities 4,037 4, Total Non Current Liabilities 20,250 20, Total Liabilities 1,66,966 1,76, , Shareholders' Equity Common Stock - Par value / Share Capital 1,959 1, Additional Paid-in Capital / Share Premium 19,203 50, Accumulated Other Comprehensive Income/(Loss) 10,824 14, Retained Earnings 5,42,782 6,64, , Total Shareholders' Equity 5,74,767 7,31, , Non Controlling Interests 9,136 3, Total Liabilities and Shareholders' Equity 7,50,868 9,12, , Calculations of Activity s Activity s Inventory Turn Over Debtors Payables Fixed Assets Total Assets Working Capital Formula Rs Purchases Fees to External Consultants+ Cost of Equipment and Software Licenses Rs $ $

11 Capital Employed Application of Rule of Thumb for testing the effectiveness of IFRS in controlling Accounting Risk. Hypotheses Validation Assuming :- ~If Percentage Variation of Figures in Dollars from Figures in Rs. is less than ±0.25% then IFRS is more capable in controlling the Accounting Risk.(H 0 Accepted) ~If Percentage Variation of Figures in Dollars from Figures in Rs. is more than ±0.25% but less than ±0.5% then IFRS is fairly capable in controlling the Accounting Risk.(H 0 Accepted) ~If Percentage Variation of Figures in Dollars from Figures in Rs. is more than ±0.5% then IFRS is not capable in controlling the Accounting Risk.(H 0 Rejected) Table showing the variation in percentage while converting from Rs. to Dollars. Activity s Inventory Turn Over Debtors Payables Variation in Percentage Variation in Percentage Rs $ Rs $ Decision More Capable as %variation is less than ±0.25% More Capable as %variation is less than ±0.25% Fairly Capable as %variation is more than ±0.25%but less than 16

12 ±0.5% Fixed Assets Total Assets Working Capital Capital Employed Not Capable as %variation is more than ±0.5% Not Capable as %variation is more than ±0.5% More Capable as %variation is less than ±0.25% Not Capable as %variation is more than ±0.5% In the above observation out of 7 activity ratios 4 activity ratios i.e. Inventory turnover, Debtors, Payables and Working Capital do not show any significant difference as the percentage variation is less than 0.5% hence, Null Hypothesis is accepted and IFRS is capable to control the accounting risk. Application of Paired T test To examine the impact of IFRS on the Activity s, Paired t test can be used which could represent the before-and-after effect. If t<1.943 then there is no effect of IFRS on Activity s (Null Hypothesis Accepted) Activity s Inventory Turn Over Debtors After-Before Before IFRS After IFRS Rs If in $ d (d-d)

13 Payables Fixed Assets Total Assets Working Capital Capital Employed Total n 7 t As value of t<1.943 (5% level of Significance with 6 d.o.f.)hence, there is no effect of IFRS on Activity s and Null Hypothesis is Accepted. Activity s Before IFRS After IFRS Inventory Turn Over Debtors Payables Fixed Assets Total Assets After-Before Rs $ d (d-d) Working Capital Capital Employed Total

14 n As value of t<1.943 (5% level of Significance with 6 d.o.f.)hence, there is no effect of IFRS on Activity s and Null Hypothesis is Accepted. Conclusion From the above observation it is clear that IFRS is quite capable in controlling the accounting risk in most of the cases. Butthe major limitation should also be considered is that, only activity ratios of Tata Consultancy Services are calculated and compared. There is a possibility that if more companies for a larger period will be consider into study, then the result may vary. Again the activity ratios are taken because it deals with the items of both the balance sheet and profit and loss account. The variations in activity exist because of the two different foreign exchange rates used in converting the two different statements. If the ratios would be calculated by taking the two or more items from only one statement (i.e. either Profit or Loss statement or Balance Sheet)then no change or variation in the ratios would be observed. Again with the help of paired t test it is proved that there is no significant difference between the activity ratios after implementation of IFRS. Hence, reporting under IFRS by following IAS 21 in International Currency (Dollars) will not affect the ratios unless and until the items used in calculating ratio are taken from either of the statement. IFRS committee should also take few measures so that accounting risk can be reduced the extent that, those ratios which used items from both the statement should not be affected even after conversion of functional currency into reporting currency. References 1. Harris, P. (2016, January/February). A Case Study Of The Cash Flow Statement: US GAAP Conversion To IFRS. Journal of Business Case Studies, 12(1). 19

15 2. IFRS Foundation. (2011). IFRS Foundation: Training Material for the IFRS for SMEs. Retrieved from 3. Bhat, G., Callen, J., & Segal, D. (2014, December). Testing the Transparency Implications of Mandatory IFRS Adoption: The Spread/Maturity Relation of Credit Default Swaps. Retrieved from ANNUAL MEETINGS/2015-Amsterdam/papers/EFMA2015_0052_fullpaper.pdf 4. Borker, D. R. (2016, April). Global management accounting principles and the worldwide proliferation of IFRS. The Business and Management Review, 7(3), Retrieved from xpires &signatureoizlrggmk5ibqsexnm42+txvcxy&responsecontent-dispositioninline; filenameglobal_management_accounting_principles.pdf 5. Bodle, K. A., Cybinski, P., &Monem, R. (2016, August). Effect of IFRS adoption on financial reporting quality Evidence from bankruptcy prediction Retrieved from AL_2016_EFFECTS_OF_IFRS_ADOPTION_OF_FINANCIAL_REPORTING_QUALI TY 6. Tripathi, P., &Jha, B., Dr. (2016, May).IFRS:AGLOBALPARADIGMOFFINANCIALREPORTING. International Educational Scientific Research Journal, 2(5), Kumar, A., Prof., & Mishra, P., Dr. (2015, November). Convergence of Accounting Standards: An Overall View. Paripex : Indian Journal of Research, 4(11), Malone, L., Tarca, A., & Wee, M. (2016, February 24). IFRS non-gaap earnings disclosures and fair value measurement. Accounting and Finance/International Accounting Standards Board Research Forum. 9. Buchman, T., & Harris, P. (2014). GAAP VS. IFRS TREATMENT OF LEASES AND THE IMPACT ON FINANCIAL RATIOS. Global Conference on Business and Finance Proceedings, 9(2). 20

TCS Financial Results

TCS Financial Results Quarter IV & Year Ended FY 2015-16 April 18, 2016 1 Copyright 2014 Tata Consultancy Services Limited Disclaimer Certain statements in this release concerning our future prospects

TCS Financial Results Quarter IV & Year Ended FY 2015-16 April 18, 2016 1 Copyright 2014 Tata Consultancy Services Limited Disclaimer Certain statements in this release concerning our future prospects

INDIAN ACCOUNTING STANDARDS

Index 1- Brief Summary of Introduction of Ind-AS 2- Applicability of INDIAN ACCOUNTING STANDARDS () 3- List of with objective and scope BRIEF SUMMARY OF INTRODUCTION OF IND-AS Indian Accounting Standards

Index 1- Brief Summary of Introduction of Ind-AS 2- Applicability of INDIAN ACCOUNTING STANDARDS () 3- List of with objective and scope BRIEF SUMMARY OF INTRODUCTION OF IND-AS Indian Accounting Standards

WIPRO PROMAX ANALYTICS SOLUTIONS LLC FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015

WIPRO PROMAX ANALYTICS SOLUTIONS LLC FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 1 WIPRO PROMAX ANALYTICS SOLUTIONS LLC BALANCE SHEET (Amount in ` except share and per share data,

WIPRO PROMAX ANALYTICS SOLUTIONS LLC FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 1 WIPRO PROMAX ANALYTICS SOLUTIONS LLC BALANCE SHEET (Amount in ` except share and per share data,

Results for Quarter III FY

Results for Quarter III FY 2012-13 Copyright 2012 Tata Consultancy Services Limited 1 Disclaimer Certain statements in this release concerning our future prospects are forward-looking statements. Forward-looking

Results for Quarter III FY 2012-13 Copyright 2012 Tata Consultancy Services Limited 1 Disclaimer Certain statements in this release concerning our future prospects are forward-looking statements. Forward-looking

PRIME FOCUS TECHNOLOGIES INC. Notes to Standalone financial statements

Notes to Standalone financial statements 1. Corporate Information Prime Focus Technologies Inc. ("the Holding Company") was incorporated on 21st February, 2013 in USA. Prime Focus Technologies Private

Notes to Standalone financial statements 1. Corporate Information Prime Focus Technologies Inc. ("the Holding Company") was incorporated on 21st February, 2013 in USA. Prime Focus Technologies Private

OPPORTUNITIES AND CHALLENGES IN ADOPTING IFRS IN INDIA

OPPORTUNITIES AND CHALLENGES IN ADOPTING IFRS IN INDIA D.Venkatesh Ph.D. Research Scholar, Department of Commerce, S V University, Tirupathi, Andhra Pradesh, Mobile No: 9666588083, venkatesh.duvvuri8@gmail.com.

OPPORTUNITIES AND CHALLENGES IN ADOPTING IFRS IN INDIA D.Venkatesh Ph.D. Research Scholar, Department of Commerce, S V University, Tirupathi, Andhra Pradesh, Mobile No: 9666588083, venkatesh.duvvuri8@gmail.com.

INDEX TO UNAUDITED CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS

INDEX TO UNAUDITED CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS Unaudited Condensed Consolidated Interim Financial Statements of Tata Consultancy Services Limited Unaudited Condensed Consolidated

INDEX TO UNAUDITED CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS Unaudited Condensed Consolidated Interim Financial Statements of Tata Consultancy Services Limited Unaudited Condensed Consolidated

TCS Financial Results

TCS Financial Results Quarter IV & Year Ended FY 2014-15 April 16, 2015 1 Copyright 2014 Tata Consultancy Services Limited Disclaimer Certain statements in this release concerning our future prospects

TCS Financial Results Quarter IV & Year Ended FY 2014-15 April 16, 2015 1 Copyright 2014 Tata Consultancy Services Limited Disclaimer Certain statements in this release concerning our future prospects

INDEX TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

INDEX TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Unaudited Condensed Consolidated Financial Statements of Tata Consultancy Services Limited Unaudited Condensed Consolidated Statements of

INDEX TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Unaudited Condensed Consolidated Financial Statements of Tata Consultancy Services Limited Unaudited Condensed Consolidated Statements of

Financial Updates. Rajiv Bansal. Vice President and Head Finance

Financial Updates Rajiv Bansal Vice President and Head Finance Safe harbor Certain statements made here concerning Infosys future growth prospects are forward-looking statements which involve a number

Financial Updates Rajiv Bansal Vice President and Head Finance Safe harbor Certain statements made here concerning Infosys future growth prospects are forward-looking statements which involve a number

WIPRO NETWORKS PTE LIMITED FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015

WIPRO NETWORKS PTE LIMITED FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 1 WIPRO NETWORKS PTE LIMITED BALANCE SHEET (Amount in ` except share and per share data, unless otherwise stated)

WIPRO NETWORKS PTE LIMITED FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 1 WIPRO NETWORKS PTE LIMITED BALANCE SHEET (Amount in ` except share and per share data, unless otherwise stated)

Harrington Health Services, Inc. FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2016

Harrington Health Services, Inc. FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, Bangalore May 31, HARRINGTON HEALTH SERVICES INC. BALANACE SHEET AS AT 31ST MARCH (Amount in Rs, except share

Harrington Health Services, Inc. FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, Bangalore May 31, HARRINGTON HEALTH SERVICES INC. BALANACE SHEET AS AT 31ST MARCH (Amount in Rs, except share

Wipro Technologies SRL

BALANCE SHEET AS AT MARCH 31st, 2016 Wipro Technologies SRL ( Amt. in INR, Except Shares and per share Data, unless otherwise stated) As at As at Particulars Notes 31st March 2016 31st March 2015 A. EQUITY

BALANCE SHEET AS AT MARCH 31st, 2016 Wipro Technologies SRL ( Amt. in INR, Except Shares and per share Data, unless otherwise stated) As at As at Particulars Notes 31st March 2016 31st March 2015 A. EQUITY

Financial updates. Rajiv Bansal. Chief Financial Officer Infosys Limited

Financial updates Rajiv Bansal Chief Financial Officer Safe harbor Certain statements in this presentation concerning our future growth prospects are forward-looking statements regarding our future business

Financial updates Rajiv Bansal Chief Financial Officer Safe harbor Certain statements in this presentation concerning our future growth prospects are forward-looking statements regarding our future business

Indian Accounting Standards (Ind AS) are issued by Accounting Standard Board to converge Indian GAAP with International Financial Accounting

are issued by Accounting Standard Board to converge Indian GAAP with International Financial Accounting") Indian Accounting Standards (Ind AS) are issued by Accounting Standard Board to converge Indian GAAP with International Financial Accounting Standards (IFRS). Their objective is to remove variations in

Indian Accounting Standards (Ind AS) are issued by Accounting Standard Board to converge Indian GAAP with International Financial Accounting Standards (IFRS). Their objective is to remove variations in

Ind AS Transition Facilitation Group (ITFG) Clarification Bulletin 3

Clarification Bulletin 3") Ind AS Transition Facilitation Group (ITFG) Clarification Bulletin 3 Ind AS Transition Facilitation Group (ITFG) of Ind AS (IFRS) Implementation Committee has been constituted for providing clarifications

Ind AS Transition Facilitation Group (ITFG) Clarification Bulletin 3 Ind AS Transition Facilitation Group (ITFG) of Ind AS (IFRS) Implementation Committee has been constituted for providing clarifications

IND AS CONVERGED WITH IFRS

Volume 5, Issue 1 (January, 2016) Online ISSN-2277-1166 Published by: Abhinav Publication Abhinav National Monthly Refereed Journal of Research in IND AS CONVERGED WITH IFRS Hiral Desai Assistance Professor,

Volume 5, Issue 1 (January, 2016) Online ISSN-2277-1166 Published by: Abhinav Publication Abhinav National Monthly Refereed Journal of Research in IND AS CONVERGED WITH IFRS Hiral Desai Assistance Professor,

Indian Accounting Standard (Ind AS) 21. The Effects of Changes in Foreign Exchange Rates

21. The Effects of Changes in Foreign Exchange Rates") Indian Accounting Standard (Ind AS) 21 The Effects of Changes in Foreign Exchange Rates 1 2 Indian Accounting Standard (Ind AS) 21 The Effects of Changes in Foreign Exchange Rates Contents Paragraph OBJECTIVE

Indian Accounting Standard (Ind AS) 21 The Effects of Changes in Foreign Exchange Rates 1 2 Indian Accounting Standard (Ind AS) 21 The Effects of Changes in Foreign Exchange Rates Contents Paragraph OBJECTIVE

Affinity Names, Inc. AFFINITY NAMES, INC. 1

Affinity Names, Inc. AFFINITY NAMES, INC. 1 2 AFFINITY NAMES, INC. Independent Auditors Report To the Board of Directors Reliance Industries Limited Report on the Standalone Financial Statements We have

Affinity Names, Inc. AFFINITY NAMES, INC. 1 2 AFFINITY NAMES, INC. Independent Auditors Report To the Board of Directors Reliance Industries Limited Report on the Standalone Financial Statements We have

ANNUAL REPORT OF TATA TECHNOLOGIES INC, USA

ANNUAL REPORT OF TATA TECHNOLOGIES INC, USA TATA TECHNOLOGIES INC, USA Directors of the Company 1 Significant Accounting Policies 2-4 Financial Statements and notes forming part of financials 5-15 Directors

ANNUAL REPORT OF TATA TECHNOLOGIES INC, USA TATA TECHNOLOGIES INC, USA Directors of the Company 1 Significant Accounting Policies 2-4 Financial Statements and notes forming part of financials 5-15 Directors

INDEPENDENT AUDITOR S REPORT TO THE BOARD OF DIRECTORS OF HEXAWARE TECHNOLOGIES LIMITED

INDEPENDENT AUDITOR S REPORT TO THE BOARD OF DIRECTORS OF HEXAWARE TECHNOLOGIES LIMITED Report on the Condensed Interim Standalone Ind AS Financial Statements We have audited the accompanying condensed

INDEPENDENT AUDITOR S REPORT TO THE BOARD OF DIRECTORS OF HEXAWARE TECHNOLOGIES LIMITED Report on the Condensed Interim Standalone Ind AS Financial Statements We have audited the accompanying condensed

WIPRO HOLDINGS HUNGARY KORLATOLT FELEL.SSEG TARSASAG STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015

WIPRO HOLDINGS HUNGARY KORLATOLT FELEL.SSEG TARSASAG STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 1 WIPRO HOLDINGS HUNGARY KORLATOLT FELEL.SSEG TARSASAG BALANCE SHEET AS

WIPRO HOLDINGS HUNGARY KORLATOLT FELEL.SSEG TARSASAG STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 1 WIPRO HOLDINGS HUNGARY KORLATOLT FELEL.SSEG TARSASAG BALANCE SHEET AS

CONSOLIDATED FINANCIAL STATEMENTS. Year ended 31 December 2018

CONSOLIDATED FINANCIAL STATEMENTS Year ended 31 December 2018 CONTENTS CONSOLIDATED FINANCIAL STATEMENTS 4 PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 31 DECEMBER 2018 4 STATEMENT OF NET INCOME AND CHANGES

CONSOLIDATED FINANCIAL STATEMENTS Year ended 31 December 2018 CONTENTS CONSOLIDATED FINANCIAL STATEMENTS 4 PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 31 DECEMBER 2018 4 STATEMENT OF NET INCOME AND CHANGES

INDEX TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

INDEX TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Page Unaudited Condensed Consolidated Financial Statements of in Millions of USD Unaudited Condensed Consolidated Balance Sheets as of March

INDEX TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Page Unaudited Condensed Consolidated Financial Statements of in Millions of USD Unaudited Condensed Consolidated Balance Sheets as of March

INTERNATIONAL FINANCIAL REPORTING SYSTEM- A CASE STUDY OF ICICI BANK

INTERNATIONAL FINANCIAL REPORTING SYSTEM- A CASE STUDY OF ICICI BANK DR SUPRAVA SAHU,Assistant Professor, P.G. Dept of Commerce, Ravenshaw University ABSTRACT IFRS have been recognized as the global financial

INTERNATIONAL FINANCIAL REPORTING SYSTEM- A CASE STUDY OF ICICI BANK DR SUPRAVA SAHU,Assistant Professor, P.G. Dept of Commerce, Ravenshaw University ABSTRACT IFRS have been recognized as the global financial

EMC CORPORATION Consolidated Income Statements (in thousands, except per share amounts) Unaudited

Unaudited") EMC CORPORATION Consolidated Income Statements (in thousands, except per share amounts) Six Months Ended June 30, June 30, June 30, June 30, 2012 2011 2012 2011 Revenues: Product sales $ 3,178,737 $ 3,043,984

EMC CORPORATION Consolidated Income Statements (in thousands, except per share amounts) Six Months Ended June 30, June 30, June 30, June 30, 2012 2011 2012 2011 Revenues: Product sales $ 3,178,737 $ 3,043,984

Discoverture Solutions LLC Consolidated Balance Sheet as at March 31, (Amount in Rs.) Note no. As at March 31, 2015

Note no. As at March 31, 2015") Consolidated Balance Sheet as at March 31, 2015 A Particulars EQUITY AND LIABILITIES Note no. As at March 31, 2015 1 Shareholders funds Share capital 3.1.1 168,388,568 Reserves and surplus 3.1.2 18,566,445

Consolidated Balance Sheet as at March 31, 2015 A Particulars EQUITY AND LIABILITIES Note no. As at March 31, 2015 1 Shareholders funds Share capital 3.1.1 168,388,568 Reserves and surplus 3.1.2 18,566,445

IIPL USA LLC FINANCIAL STATEMENTS

FINANCIAL STATEMENTS - - (1) 0 - Balance sheet as at March Notes As at As at As at March March 31, April 1, 2015 ASSETS Non-current Assets (a) Property, plant and equipment 4 21,848,458 - - (b) Intangible

FINANCIAL STATEMENTS - - (1) 0 - Balance sheet as at March Notes As at As at As at March March 31, April 1, 2015 ASSETS Non-current Assets (a) Property, plant and equipment 4 21,848,458 - - (b) Intangible

ACERINOX, S.A. AND SUBSIDIARIES. 31 December 2015

ACERINOX, S.A. AND SUBSIDIARIES Annual Accounts of the Consolidated Group 31 December 2015 (Free translation from the original in Spanish. In the event of discrepancy, the Spanishlanguage version prevails.)

ACERINOX, S.A. AND SUBSIDIARIES Annual Accounts of the Consolidated Group 31 December 2015 (Free translation from the original in Spanish. In the event of discrepancy, the Spanishlanguage version prevails.)

[Pal, 5(7) July, 2018] ISSN: IMPACT FACTOR

![[Pal, 5(7) July, 2018] ISSN: IMPACT FACTOR](/thumbs/92/109897653.jpg "[Pal, 5(7) July, 2018] ISSN: IMPACT FACTOR") COMPARISON OF TOP INDIAN AND GLOBAL IT COMPANIES USING DU PONT 5 POINT ANALYSIS Shreya Pal *1 & Tishya Kapoor 2 *1&2 Indian Institute of Technology Delhi ABSTRACT The paper compares the top 4 companies

COMPARISON OF TOP INDIAN AND GLOBAL IT COMPANIES USING DU PONT 5 POINT ANALYSIS Shreya Pal *1 & Tishya Kapoor 2 *1&2 Indian Institute of Technology Delhi ABSTRACT The paper compares the top 4 companies

Notes to the consolidated financial statements A. General basis of presentation

86 Notes to the consolidated financial statements A. General basis of presentation Accounting principles The consolidated financial statements of Franz Haniel & Cie. GmbH, Duisburg, for the year ended

86 Notes to the consolidated financial statements A. General basis of presentation Accounting principles The consolidated financial statements of Franz Haniel & Cie. GmbH, Duisburg, for the year ended

ANNUAL REPORT OF TATA TECHNOLOGIES (CANADA) INC.

INC.") ANNUAL REPORT OF TATA TECHNOLOGIES (CANADA) INC. TATA TECHNOLOGIES (CANADA) INC, CANADA Directors of the Company 1 Directors Report 2-3 Financial Statements 4-7 Notes forming part of Financial Statements

ANNUAL REPORT OF TATA TECHNOLOGIES (CANADA) INC. TATA TECHNOLOGIES (CANADA) INC, CANADA Directors of the Company 1 Directors Report 2-3 Financial Statements 4-7 Notes forming part of Financial Statements

Oracle Financial Services Software Inc. Directors Report. FINANCIAL PERFORMANCE (Amount in ` Millions)

") Directors Report To the Members, Your Directors are pleased to present the Annual Report on the business and operations of your Company, together with the accounts for the year ended March 31, 2014 FINANCIAL

Directors Report To the Members, Your Directors are pleased to present the Annual Report on the business and operations of your Company, together with the accounts for the year ended March 31, 2014 FINANCIAL

COMPARISON OF INDIAN GAAP AND IFRS IN INDIA: AN EMPIRICAL ANALYSIS OF SELECTED COMPANIES

National Seminar on INDAS : A Road Map for IFRS in India COMPARISON OF INDIAN GAAP AND IFRS IN INDIA: AN EMPIRICAL ANALYSIS OF SELECTED COMPANIES Introduction Dr Prabhu M Assistant Professor, Department

National Seminar on INDAS : A Road Map for IFRS in India COMPARISON OF INDIAN GAAP AND IFRS IN INDIA: AN EMPIRICAL ANALYSIS OF SELECTED COMPANIES Introduction Dr Prabhu M Assistant Professor, Department

Auditors Report on Condensed Consolidated Financial Statements

Auditors Report on Condensed Consolidated Financial Statements TO THE BOARD OF DIRECTORS OF TATA CONSULTANCY SERVICES LIMITED 1. We have audited the attached condensed consolidated balance sheet of Tata

Auditors Report on Condensed Consolidated Financial Statements TO THE BOARD OF DIRECTORS OF TATA CONSULTANCY SERVICES LIMITED 1. We have audited the attached condensed consolidated balance sheet of Tata

IAS 21 The Effects of Changes in Foreign Exchange Rates - A Closer Look

MPRA Munich Personal RePEc Archive IAS 21 The Effects of Changes in Foreign Exchange Rates - A Closer Look K S Muthupandian The Institute of Cost and Works Accountants of India 20. September 2009 Online

MPRA Munich Personal RePEc Archive IAS 21 The Effects of Changes in Foreign Exchange Rates - A Closer Look K S Muthupandian The Institute of Cost and Works Accountants of India 20. September 2009 Online

Consolidated Balance Sheet

Consolidated Balance Sheet Note ASSETS Non-current assets (a) Property, plant and equipment 4 10,216 10,057 (b) Capital work-in-progress 1,278 1,541 (c) Intangible assets 5 12 47 (d) Goodwill 6 1,745 1,597

Consolidated Balance Sheet Note ASSETS Non-current assets (a) Property, plant and equipment 4 10,216 10,057 (b) Capital work-in-progress 1,278 1,541 (c) Intangible assets 5 12 47 (d) Goodwill 6 1,745 1,597

Oracle Financial Services Software Pte ltd. Directors Report

Oracle Financial Services Software Pte ltd. Directors Report To the Members, Your Directors are pleased to present Annual Report on the business and operations of your company, together with the accounts

Oracle Financial Services Software Pte ltd. Directors Report To the Members, Your Directors are pleased to present Annual Report on the business and operations of your company, together with the accounts

Oracle Financial Services Software (Shanghai) Limited. Directors Report. FINANCIAL PERFORMANCE (Rs. in lacs) Particulars

Limited. Directors Report. FINANCIAL PERFORMANCE (Rs. in lacs) Particulars") To the Members, Directors Report Your Directors are pleased to present Annual Report on the business and operations of your company, together with the accounts for the year ended March 31, 2011. FINANCIAL

To the Members, Directors Report Your Directors are pleased to present Annual Report on the business and operations of your company, together with the accounts for the year ended March 31, 2011. FINANCIAL

Statements Chapter 5 CHAPTER 5 STATEMENTS I. FINANCIAL STATEMENTS 71 II. CORPORATE RESPONSIBILTY STATEMENTS 141

CHAPTER 5 STATEMENTS I. FINANCIAL STATEMENTS 71 II. CORPORATE RESPONSIBILTY STATEMENTS 141 70 I. FINANCIAL STATEMENTS Consolidated statement of financial position 72 Consolidated income statement 73 Consolidated

CHAPTER 5 STATEMENTS I. FINANCIAL STATEMENTS 71 II. CORPORATE RESPONSIBILTY STATEMENTS 141 70 I. FINANCIAL STATEMENTS Consolidated statement of financial position 72 Consolidated income statement 73 Consolidated

WIPRO TECHNOLOGIES SDN BHD (formerly known as PLANET PSG SDN BHD), MALAYSIA FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015

, MALAYSIA FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015") WIPRO TECHNOLOGIES SDN BHD (formerly known as PLANET PSG SDN BHD), MALAYSIA FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 WIPRO TECHNOLOGIES SDN BHD (formerly known as PLANET PSG SDN

WIPRO TECHNOLOGIES SDN BHD (formerly known as PLANET PSG SDN BHD), MALAYSIA FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 WIPRO TECHNOLOGIES SDN BHD (formerly known as PLANET PSG SDN

Report on Condensed Interim Consolidated Ind AS Financial Statements

The Board of Directors Hexaware Technologies Limited 152, Millennium Business Park, Sector 3rd A Block, TTC Industrial Area Mahape, Navi Mumbai - 400710. Report on Condensed Interim Consolidated Ind AS

The Board of Directors Hexaware Technologies Limited 152, Millennium Business Park, Sector 3rd A Block, TTC Industrial Area Mahape, Navi Mumbai - 400710. Report on Condensed Interim Consolidated Ind AS

Oracle Financial Services Software Inc.

To the Members, Oracle Financial Services Software Inc. Directors Report Your Directors are pleased to present the Annual Report on the business and operations of your company, together with the accounts

To the Members, Oracle Financial Services Software Inc. Directors Report Your Directors are pleased to present the Annual Report on the business and operations of your company, together with the accounts

WIPRO HOLDINGS (MAURITIUS) LIMITED STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015

LIMITED STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015") STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 1 BALANCE SHEET AS AT MARCH 31, 2015 (Amount in INR, except share and per share data, unless otherwise stated) 2015 2014 I. EQUITY

STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 1 BALANCE SHEET AS AT MARCH 31, 2015 (Amount in INR, except share and per share data, unless otherwise stated) 2015 2014 I. EQUITY

SUPPLEMENT FOR COMPANY ACCOUNTS AND AUDITING PRACTICES (Relevant for students appearing in June, 2016 Examination)

") EXECUTIVE PROGRAMME SUPPLEMENT FOR COMPANY ACCOUNTS AND AUDITING PRACTICES (Relevant for students appearing in June, 2016 Examination) MODULE 2 - PAPER 5 Disclaimer- This document has been prepared purely

EXECUTIVE PROGRAMME SUPPLEMENT FOR COMPANY ACCOUNTS AND AUDITING PRACTICES (Relevant for students appearing in June, 2016 Examination) MODULE 2 - PAPER 5 Disclaimer- This document has been prepared purely

ITNL OFFSHORE THREE PTE. LTD. FINANCIAL STATEMENTS

ITNL OFFSHORE THREE PTE. LTD. FINANCIAL STATEMENTS - Special Purpose Financial Statements ITNL OFFSHORE THREE PTE. LTD., SINGAPORE Balance Sheet at March 31, Notes As at As at March 31, March 31, ASSETS

ITNL OFFSHORE THREE PTE. LTD. FINANCIAL STATEMENTS - Special Purpose Financial Statements ITNL OFFSHORE THREE PTE. LTD., SINGAPORE Balance Sheet at March 31, Notes As at As at March 31, March 31, ASSETS

WIPRO SHANGHAI LIMITED FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015

WIPRO SHANGHAI LIMITED FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 WIPRO SHANGHAI LIMITED BALANCE SHEET (Amount in ` except share and per share data, unless otherwise stated) As at

WIPRO SHANGHAI LIMITED FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 WIPRO SHANGHAI LIMITED BALANCE SHEET (Amount in ` except share and per share data, unless otherwise stated) As at

WENDT MIDDLE EAST FZE - HAMRIYAH FREE ZONE, SHARJAH - U.A.E. STATEMENT OF FINANCIAL POSITION AS AT 31ST MARCH, 2011

STATEMENT OF FINANCIAL POSITION AS AT Assets Note 2011 2010 2011 2010 AED AED Rs. Rs. Current assets Inventory 38,641 151,550 469,063 1,839,665 Goods in transit - 12,955-157,261 Accounts receivable 5 240,153-2,915,217

STATEMENT OF FINANCIAL POSITION AS AT Assets Note 2011 2010 2011 2010 AED AED Rs. Rs. Current assets Inventory 38,641 151,550 469,063 1,839,665 Goods in transit - 12,955-157,261 Accounts receivable 5 240,153-2,915,217

For Mindtree Software (Shanghai) Co., Ltd. Balance sheet

Co., Ltd. Balance sheet") Balance sheet Note As at As at EQUITY AND LIABILITIES Shareholders' funds Share capital 3.1.1 13,592,500 13,592,500 Reserves and surplus 3.1.2 (3,135,078) (4,086,508) 10,457,422 9,505,992 Current liabilities

Balance sheet Note As at As at EQUITY AND LIABILITIES Shareholders' funds Share capital 3.1.1 13,592,500 13,592,500 Reserves and surplus 3.1.2 (3,135,078) (4,086,508) 10,457,422 9,505,992 Current liabilities

WIPRO TECHNOLOGIES SA FINANCIAL STATEMENTS

WIPRO TECHNOLOGIES SA FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 WIPRO TECHNOLOGIES SA BALANCE SHEET AS AT MARCH 31,2015 (Amount in except share and per share data, unless otherwise

WIPRO TECHNOLOGIES SA FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 WIPRO TECHNOLOGIES SA BALANCE SHEET AS AT MARCH 31,2015 (Amount in except share and per share data, unless otherwise

A COMAPARATIVE STUDY ON REPORTING OF MERGERS AND ACQUISITIONS ACTIVITIES UNDER IGAAP AND IND AS

Indian Journal of Accounting (IJA) 111 ISSN : 0972-1479 (Print) 2395-6127 (Online) Vol. XLIX (1), June, 2017, pp. 111-116 A COMAPARATIVE STUDY ON REPORTING OF MERGERS AND ACQUISITIONS ACTIVITIES UNDER

Indian Journal of Accounting (IJA) 111 ISSN : 0972-1479 (Print) 2395-6127 (Online) Vol. XLIX (1), June, 2017, pp. 111-116 A COMAPARATIVE STUDY ON REPORTING OF MERGERS AND ACQUISITIONS ACTIVITIES UNDER

Net Current Assets (62,748,149) (2,858,178,175) (90,126,095) (4,225,111,319)

(2,858,178,175) (90,126,095) (4,225,111,319)") Balance Sheet as at December 31, 2010 SOURCES OF FUNDS Schedule 2010 2010 2009 2009 (Amount in USD) (Amount in INR) (Amount in USD) (Amount in INR) Shareholders' Funds Share capital A 28 1,275 28 1,313

Balance Sheet as at December 31, 2010 SOURCES OF FUNDS Schedule 2010 2010 2009 2009 (Amount in USD) (Amount in INR) (Amount in USD) (Amount in INR) Shareholders' Funds Share capital A 28 1,275 28 1,313

Impact of Ind AS adoption on Industry Applying it in simple way

Impact of Ind AS adoption on Industry Applying it in simple way CA Rakesh Agarwal Alumni - Harvard Business School Vice President Finance, Compliance and Accounts Centers of Excellence (CoE) Reliance Industries

Impact of Ind AS adoption on Industry Applying it in simple way CA Rakesh Agarwal Alumni - Harvard Business School Vice President Finance, Compliance and Accounts Centers of Excellence (CoE) Reliance Industries

WIPRO UK LIMITED (Formerly SAIC UK Limited) BALANCE SHEET (` in `, except share and per share data, unless otherwise stated) Notes

BALANCE SHEET (` in `, except share and per share data, unless otherwise stated) Notes") WIPRO UK LIMITED (Formerly SAIC UK Limited) BALANCE SHEET (` in `, except share and per share data, unless otherwise stated) Notes As on Mar 31, 2015 Mar 31, 2014 EQUITY AND LIABILITIES Shareholder's funds

WIPRO UK LIMITED (Formerly SAIC UK Limited) BALANCE SHEET (` in `, except share and per share data, unless otherwise stated) Notes As on Mar 31, 2015 Mar 31, 2014 EQUITY AND LIABILITIES Shareholder's funds

Financial statements. Financial strength

Financial statements Financial strength Consolidated Income Statement 66 Consolidated Statement of Comprehensive Income 67 Consolidated Statement of Financial Position 68 Consolidated Statement of Changes

Financial statements Financial strength Consolidated Income Statement 66 Consolidated Statement of Comprehensive Income 67 Consolidated Statement of Financial Position 68 Consolidated Statement of Changes

- JCDECAUX SA - COMMENTS ON THE TRANSITION TO IFRS AND FIGURES

- JCDECAUX SA - COMMENTS ON THE TRANSITION TO IFRS AND FIGURES Pursuant to EC Regulation No. 1606/2002 and in accordance with IFRS 1 First-time Adoption of IFRS, the JCDecaux Group consolidated financial

- JCDECAUX SA - COMMENTS ON THE TRANSITION TO IFRS AND FIGURES Pursuant to EC Regulation No. 1606/2002 and in accordance with IFRS 1 First-time Adoption of IFRS, the JCDecaux Group consolidated financial

International Accounting Standard 21. The Effects of Changes in Foreign Exchange Rates

International Accounting Standard 21 The Effects of Changes in Foreign Exchange Rates Basis for Conclusions on IAS 21 The Effects of Changes in Foreign Exchange Rates This Basis for Conclusions accompanies,

International Accounting Standard 21 The Effects of Changes in Foreign Exchange Rates Basis for Conclusions on IAS 21 The Effects of Changes in Foreign Exchange Rates This Basis for Conclusions accompanies,

AS 11: The Effects of Changes in Foreign Exchange Rates

AS 11: The Effects of Changes in Foreign Exchange Rates Introduction AS 11, (revised 2003), comes into effect in respect of accounting periods commencing on or after 1-4-2004. Mandatory in nature from

AS 11: The Effects of Changes in Foreign Exchange Rates Introduction AS 11, (revised 2003), comes into effect in respect of accounting periods commencing on or after 1-4-2004. Mandatory in nature from

Homeserve plc. Transition to International Financial Reporting Standards

Homeserve plc Transition to International Financial Reporting Standards 28 November 2005 1 Transition to International Financial Reporting Standards ( IFRS ) Homeserve is today announcing its interim results

Homeserve plc Transition to International Financial Reporting Standards 28 November 2005 1 Transition to International Financial Reporting Standards ( IFRS ) Homeserve is today announcing its interim results

Group Income Statement For the year ended 31 March 2015

Income Statement For the year ended 31 March Note Pre exceptionals Restated Exceptionals (note 11) Pre exceptionals Exceptionals (note 11) Continuing operations Revenue 5 10,606,080 10,606,080 11,044,763

Income Statement For the year ended 31 March Note Pre exceptionals Restated Exceptionals (note 11) Pre exceptionals Exceptionals (note 11) Continuing operations Revenue 5 10,606,080 10,606,080 11,044,763

RELIANCE TRADING LIMITED. Reliance Trading Limited Financial Statements

RELIANCE TRADING LIMITED 1 Reliance Trading Limited Financial Statements 2016-17 2 RELIANCE TRADING LIMITED Independent Auditor s Report To the Board of s of Reliance Trading Limited 1. We have audited

RELIANCE TRADING LIMITED 1 Reliance Trading Limited Financial Statements 2016-17 2 RELIANCE TRADING LIMITED Independent Auditor s Report To the Board of s of Reliance Trading Limited 1. We have audited

The Effects of Changes in Foreign Exchange Rates

International Accounting Standard 21 The Effects of Changes in Foreign Exchange Rates This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 21 The Effects of Changes

International Accounting Standard 21 The Effects of Changes in Foreign Exchange Rates This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 21 The Effects of Changes

WIPRO TECHNOLOGIES S.A DE C.V FINANCIAL STATEMENTS

WIPRO TECHNOLOGIES S.A DE C.V FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 WIPRO TECHNOLOGIES S.A DE C.V BALANCE SHEET AS AT MARCH 31,2015 (Amount in except share and per share data,

WIPRO TECHNOLOGIES S.A DE C.V FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015 WIPRO TECHNOLOGIES S.A DE C.V BALANCE SHEET AS AT MARCH 31,2015 (Amount in except share and per share data,

International Accounting Standards. Financial Reporting in Hyperinflationary Economies Understanding IAS 29

International Accounting Standards Financial Reporting in Hyperinflationary Economies Understanding IAS 29 PricewaterhouseCoopers (www.pwcglobal.com), is the world s largest professional services organisation.

International Accounting Standards Financial Reporting in Hyperinflationary Economies Understanding IAS 29 PricewaterhouseCoopers (www.pwcglobal.com), is the world s largest professional services organisation.

Tata Manufacturing Technologies(Shanghai)Co Ltd. Annual Financial Statements For the year ended March 31, 2018

Co Ltd. Annual Financial Statements For the year ended March 31, 2018") Manufacturing Technologies(Shanghai)Co Ltd. Annual Financial Statements For the year ended March 31, 2018 Manufacturing Technologies (Shanghai) Co. Ltd. DIRECTOR : JK Gupta REGISTERED: OFFICE Room 1606-1607,

Manufacturing Technologies(Shanghai)Co Ltd. Annual Financial Statements For the year ended March 31, 2018 Manufacturing Technologies (Shanghai) Co. Ltd. DIRECTOR : JK Gupta REGISTERED: OFFICE Room 1606-1607,

i-flex Solutions Limited

Consolidated Balance Sheets (Amount in thousands, except share and per share data) March 31, September 30, 2007 2007 2007 Rs Rs $ ASSETS Current assets: Cash and cash equivalents 3,338,320 3,225,148 81,136

Consolidated Balance Sheets (Amount in thousands, except share and per share data) March 31, September 30, 2007 2007 2007 Rs Rs $ ASSETS Current assets: Cash and cash equivalents 3,338,320 3,225,148 81,136

THE STUDY ON CHALLENGES AND ISSUES INVOLVED IN CONVERGENCEE OF IFRS IN INDIA

ISSN: 2320-4168 UGC Approval No: 44120 Impact Factor: 3.017 THE STUDY ON CHALLENGES AND ISSUES INVOLVED IN CONVERGENCEE OF IFRS IN INDIA Article Particulars Received: 7.7.2017 Accepted: 13.7.2017 Published:

ISSN: 2320-4168 UGC Approval No: 44120 Impact Factor: 3.017 THE STUDY ON CHALLENGES AND ISSUES INVOLVED IN CONVERGENCEE OF IFRS IN INDIA Article Particulars Received: 7.7.2017 Accepted: 13.7.2017 Published:

JOINT STOCK COMPANY ACRON. International Accounting Standard No. 34 Consolidated Condensed Interim Financial Information (six months) 30 June 2012

30 June 2012") JOINT STOCK COMPANY ACRON International Accounting Standard No. 34 Consolidated Condensed Interim Financial Information (six months) 30 June 2012 Contents Unaudited Consolidated Condensed Interim Statement

JOINT STOCK COMPANY ACRON International Accounting Standard No. 34 Consolidated Condensed Interim Financial Information (six months) 30 June 2012 Contents Unaudited Consolidated Condensed Interim Statement

Filling the GAAP India and IFRS

Filling the GAAP India and IFRS Global challenges to trade have been falling over the past decades and this has resulted in countries around the globe being linked by a thread of economic interdependence.

Filling the GAAP India and IFRS Global challenges to trade have been falling over the past decades and this has resulted in countries around the globe being linked by a thread of economic interdependence.

- (1.7) (6.6) Profit attributable to ordinary shareholders Earnings per share 5 Basic 2.3p 2.5p 10.6p Diluted 2.3p 2.5p 10.

(6.6) Profit attributable to ordinary shareholders Earnings per share 5 Basic 2.3p 2.5p 10.6p Diluted 2.3p 2.5p 10.") Consolidated Profit and Loss Account For the 13 weeks ended 1st May 2005 Notes Revenue 2 196.4 200.3 776.7 Cost of sales (117.5) (119.9) (462.2) Gross profit 78.9 80.4 314.5 Total operating expenses (61.4)

Consolidated Profit and Loss Account For the 13 weeks ended 1st May 2005 Notes Revenue 2 196.4 200.3 776.7 Cost of sales (117.5) (119.9) (462.2) Gross profit 78.9 80.4 314.5 Total operating expenses (61.4)

Overview of Transition to IND-AS. CA Sanjeev Maheshwari

Overview of Transition to IND-AS CA Sanjeev Maheshwari sm@gmj.co.in 98211 19043 Need for one Common language of Accounting GMJ & Co. 2 GMJ & Co. 3 GMJ & Co. 4 GMJ & Co. 5 GMJ & Co. 6 GMJ & Co. 7 GMJ &

Overview of Transition to IND-AS CA Sanjeev Maheshwari sm@gmj.co.in 98211 19043 Need for one Common language of Accounting GMJ & Co. 2 GMJ & Co. 3 GMJ & Co. 4 GMJ & Co. 5 GMJ & Co. 6 GMJ & Co. 7 GMJ &

IAS 1 Presentation of Financial Statement

IAS 1 Presentation of Financial Statement 1 By : Mehul Shah mehul@raseshca.comcom 9723459572 IASB Structure 2 IASC Foundation appoints oversees funds reports SAC advises IASB interprets IFRIC creates IFRS

IAS 1 Presentation of Financial Statement 1 By : Mehul Shah mehul@raseshca.comcom 9723459572 IASB Structure 2 IASC Foundation appoints oversees funds reports SAC advises IASB interprets IFRIC creates IFRS

Consolidated Balance Sheets

Consolidated Balance Sheets TEIJIN LIMITED As of March 31, and (Note 1) ASSETS Current assets: Cash and time deposits (Notes 3 and 4) 33,135 45,719 $ 380,453 Receivables: Notes and accounts receivable

Consolidated Balance Sheets TEIJIN LIMITED As of March 31, and (Note 1) ASSETS Current assets: Cash and time deposits (Notes 3 and 4) 33,135 45,719 $ 380,453 Receivables: Notes and accounts receivable

Report of Independent Auditor

Industrial and Commercial Bank of China (Thai) Public Company Limited and its subsidiary (Formerly known as ACL Bank Public Company Limited ) Report and financial statements 31 December 2010 and 2009 Report

Industrial and Commercial Bank of China (Thai) Public Company Limited and its subsidiary (Formerly known as ACL Bank Public Company Limited ) Report and financial statements 31 December 2010 and 2009 Report

Meridian Petroleum plc RESTATED INTERIM RESULTS FOLLOWING ADOPTION OF IFRS for the Six Month period ended 30 June 2006 (Unaudited)

") Meridian Petroleum plc Meridian Petroleum plc RESTATED INTERIM RESULTS FOLLOWING ADOPTION OF IFRS for the Six Month period ended 30 June 2006 (Unaudited) The results for the year ended December 2006 have

Meridian Petroleum plc Meridian Petroleum plc RESTATED INTERIM RESULTS FOLLOWING ADOPTION OF IFRS for the Six Month period ended 30 June 2006 (Unaudited) The results for the year ended December 2006 have

AS 11 (Revised 2003) The Effects of Changes in Foreign Exchange Rates

The Effects of Changes in Foreign Exchange Rates") Applicability AS 11 (Revised 2003) The Effects of Changes in Foreign Exchange Rates The revised 2003 Accounting Standard will replace the 1994 Accounting Standard and will come into effect in respect of

Applicability AS 11 (Revised 2003) The Effects of Changes in Foreign Exchange Rates The revised 2003 Accounting Standard will replace the 1994 Accounting Standard and will come into effect in respect of

RBI/ /34 RBI/ /DBR.FID.No. 1/ / August 04, 2016

RBI/2016-17/34 RBI/2016-17/DBR.FID.No. 1/01.02.000/2016-17 August 04, 2016 All India Financial Institutions (Exim Bank, NABARD, NHB and SIDBI) Madam / Dear Sir, Implementation of Indian Accounting Standards

RBI/2016-17/34 RBI/2016-17/DBR.FID.No. 1/01.02.000/2016-17 August 04, 2016 All India Financial Institutions (Exim Bank, NABARD, NHB and SIDBI) Madam / Dear Sir, Implementation of Indian Accounting Standards

S G M & Associates LLP Chartered Accountants

S G M & Associates LLP Chartered Accountants 444 Ground Floor, 6 th Cross, 7 th Main, J P Nagar 3 rd Phase, Bengaluru 560 078. CIN AAI-0262 INDEPENDENT AUDITOR S REPORT TO THE PARTNERS OF HEALTHCARE DIWANCHAND

S G M & Associates LLP Chartered Accountants 444 Ground Floor, 6 th Cross, 7 th Main, J P Nagar 3 rd Phase, Bengaluru 560 078. CIN AAI-0262 INDEPENDENT AUDITOR S REPORT TO THE PARTNERS OF HEALTHCARE DIWANCHAND

TNK-BP INTERNATIONAL LIMITED CONSOLIDATED FINANCIAL STATEMENTS AS OF AND FOR THE YEARS ENDED 31 DECEMBER 2012 AND 31 DECEMBER 2011

CONSOLIDATED FINANCIAL STATEMENTS AS OF AND FOR THE YEARS ENDED 31 DECEMBER 2012 AND 31 DECEMBER 2011 Consolidated Income Statement and Statement of Comprehensive Income (expressed in millions of USD)

CONSOLIDATED FINANCIAL STATEMENTS AS OF AND FOR THE YEARS ENDED 31 DECEMBER 2012 AND 31 DECEMBER 2011 Consolidated Income Statement and Statement of Comprehensive Income (expressed in millions of USD)

Notes to the Accounts

Notes to the Accounts 1. Accounting Policies Statement of compliance The Group financial statements consolidate those of the Company and its subsidiaries (together referred to as the Group ), equity account

Notes to the Accounts 1. Accounting Policies Statement of compliance The Group financial statements consolidate those of the Company and its subsidiaries (together referred to as the Group ), equity account

\WIPRO TECHNOLOGIES SPAIN STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2015

\WIPRO TECHNOLOGIES SPAIN STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 1 WIPRO TECHNOLOGIES SPAIN BALANCE SHEET AS AT MARCH 31, (Amount in INR, except share and per share data,

\WIPRO TECHNOLOGIES SPAIN STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 1 WIPRO TECHNOLOGIES SPAIN BALANCE SHEET AS AT MARCH 31, (Amount in INR, except share and per share data,

INDIA BUDGET

INDIA BUDGET 2018-19 Author Jairaj Purandare Tags Budget Business Connection Capital Gains India Investment Activity Tax Policy INTRODUCTION All eyes were set on the Indian Finance Minister on February

INDIA BUDGET 2018-19 Author Jairaj Purandare Tags Budget Business Connection Capital Gains India Investment Activity Tax Policy INTRODUCTION All eyes were set on the Indian Finance Minister on February

DETAILS OF RESEARCH PAPERS

DETAILS OF RESEARCH PAPERS RESEARCH PAPER-I Title: A Comparative Study on Cash Flow Statements of Tata Chemicals Ltd. and Pidilite Chemicals Ltd. Author-1: Kalpesh B. Gelda (Assistant Professor, National

DETAILS OF RESEARCH PAPERS RESEARCH PAPER-I Title: A Comparative Study on Cash Flow Statements of Tata Chemicals Ltd. and Pidilite Chemicals Ltd. Author-1: Kalpesh B. Gelda (Assistant Professor, National

KUWAIT FINANCE HOUSE K.S.C.P. AND SUBSIDIARIES

KUWAIT FINANCE HOUSE K.S.C.P. AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2015 CONSOLIDATED STATEMENT OF INCOME Year ended 31 December 2015 Notes INCOME Financing income 663,423 645,801

KUWAIT FINANCE HOUSE K.S.C.P. AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2015 CONSOLIDATED STATEMENT OF INCOME Year ended 31 December 2015 Notes INCOME Financing income 663,423 645,801

CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS First half of 2005 CONTENTS CONSOLIDATED FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS AS ADOPTED BY THE EUROPEAN UNION

CONSOLIDATED FINANCIAL STATEMENTS First half of 2005 CONTENTS CONSOLIDATED FINANCIAL STATEMENTS PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS AS ADOPTED BY THE EUROPEAN UNION

WIPRO TECHNOLOGY CHILE SPA FINANCIAL STATEMENTS

WIPRO TECHNOLOGY CHILE SPA FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2016 WIPRO TECHNOLOGY CHILE SPA BALANCE SHEET AS AT MARCH 31,2016 (Amount in except share and per share data, unless

WIPRO TECHNOLOGY CHILE SPA FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2016 WIPRO TECHNOLOGY CHILE SPA BALANCE SHEET AS AT MARCH 31,2016 (Amount in except share and per share data, unless

Safe harbor. Copyright 2011 Infosys Technologies Limited

Safe harbor Certain statements made here concerning Infosys future growth prospects are forward-looking statements which involve a number of risks and uncertainties that could cause actual results to differ

Safe harbor Certain statements made here concerning Infosys future growth prospects are forward-looking statements which involve a number of risks and uncertainties that could cause actual results to differ

DAX Cloud ULC. Standalone Financial Statement for the Year ended

Standalone Financial Statement for the Year ended March 31, 2018 Balance Sheet as on 31.03.2018 Particulars Notes 31.Mar.18 31.Mar.17 Assets 1. Non-current assets (a) Property, plant and equipment - -

Standalone Financial Statement for the Year ended March 31, 2018 Balance Sheet as on 31.03.2018 Particulars Notes 31.Mar.18 31.Mar.17 Assets 1. Non-current assets (a) Property, plant and equipment - -

WIPRO GALLAGHER SOLUTIONS INC

WIPRO GALLAGHER SOLUTIONS INC FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2016 WIPRO GALLAGHER SOLUTIONS INC. BALANCE SHEET (Amount in, e xcept share and per share data, unless otherwise

WIPRO GALLAGHER SOLUTIONS INC FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2016 WIPRO GALLAGHER SOLUTIONS INC. BALANCE SHEET (Amount in, e xcept share and per share data, unless otherwise

Acerinox, S.A. and Subsidiaries

Acerinox, S.A. and Subsidiaries Consolidated Annual Accounts 31 December 2016 Consolidated Directors' Report 2016 (With Auditors Report Thereon) (Free translation from the original in Spanish. In the event

Acerinox, S.A. and Subsidiaries Consolidated Annual Accounts 31 December 2016 Consolidated Directors' Report 2016 (With Auditors Report Thereon) (Free translation from the original in Spanish. In the event

Highlights of Financial Performance

Highlights of Financial Performance M. D. Ranganath Chief Financial Officer Safe Harbor Certain statements in this presentation concerning our future growth prospects are forward-looking statements regarding

Highlights of Financial Performance M. D. Ranganath Chief Financial Officer Safe Harbor Certain statements in this presentation concerning our future growth prospects are forward-looking statements regarding

Magnet 360, LLC Consolidated balance sheet Amount in Rs

Consolidated balance sheet Amount in Rs Note As at As at ASSETS Non-current assets Property, plant and equipment 3 37,150,482 39,436,733 Goodwill 451,087,694 460,860,681 Other intangible assets 4 486,098

Consolidated balance sheet Amount in Rs Note As at As at ASSETS Non-current assets Property, plant and equipment 3 37,150,482 39,436,733 Goodwill 451,087,694 460,860,681 Other intangible assets 4 486,098

3 Months ended. September 30, 2018

Sl. No. June 30, Months in period period UNAUDITED UNAUDITED* UNAUDITED* UNAUDITED UNAUDITED* AUDITED* (1) (2) (3) (4) (5) (6) Continuing operations I Revenue from operations 73,263 66,346 76,866 139,609

Sl. No. June 30, Months in period period UNAUDITED UNAUDITED* UNAUDITED* UNAUDITED UNAUDITED* AUDITED* (1) (2) (3) (4) (5) (6) Continuing operations I Revenue from operations 73,263 66,346 76,866 139,609

Bluefin Solutions Limited Consolidated balance sheet (Amount in Rs)

") Consolidated balance sheet (Amount in Rs) Note As at As at ASSETS Non-current assets Property, plant and equipment 3 17,872,206 23,342,943 Intangible assets 4 1,008,818 2,252,525 Financial assets 5 Loans

Consolidated balance sheet (Amount in Rs) Note As at As at ASSETS Non-current assets Property, plant and equipment 3 17,872,206 23,342,943 Intangible assets 4 1,008,818 2,252,525 Financial assets 5 Loans

TATA CONSULTANCY SERVICES LIMITED CONDENSED BALANCE SHEET AS AT SEPTEMBER 30, Schedule As at September 30, 2008 As at March 31, 2008

CONDENSED BALANCE SHEET AS AT SEPTEMBER 30, 2008 Schedule Rupees in crores Rupees in crores SOURCES OF FUNDS: 1 SHAREHOLDERS' FUND (a) Share Capital A 197.86 197.86 (b) Reserves and Surplus B 11891.28

CONDENSED BALANCE SHEET AS AT SEPTEMBER 30, 2008 Schedule Rupees in crores Rupees in crores SOURCES OF FUNDS: 1 SHAREHOLDERS' FUND (a) Share Capital A 197.86 197.86 (b) Reserves and Surplus B 11891.28

About the authors I-5 Chapter-heads I-7. u Clarification regarding Applicability of New Schedule VI Format 1

Contents About the authors I-5 Chapter-heads I-7 1 ACCOUNTING FOR CORPORATE RESTRUCTURING u Clarification regarding Applicability of New Schedule VI Format 1 SECTION I - AMALGAMATION AND EXTERNAL RECONSTRUCTION

Contents About the authors I-5 Chapter-heads I-7 1 ACCOUNTING FOR CORPORATE RESTRUCTURING u Clarification regarding Applicability of New Schedule VI Format 1 SECTION I - AMALGAMATION AND EXTERNAL RECONSTRUCTION

Mantas Inc. Directors Report. FINANCIAL PERFORMANCE (Amount in Rs. million)

") Directors Report To the Members, Your Directors are pleased to present the Annual Report on the business and operations of your Company, together with the accounts for the year ended March 31, 2012. FINANCIAL

Directors Report To the Members, Your Directors are pleased to present the Annual Report on the business and operations of your Company, together with the accounts for the year ended March 31, 2012. FINANCIAL

Auditor s Responsibility Our responsibility is to express an opinion on these standalone Ind AS financial statements based on our audit.

Independent Auditor s Report To the Board of Directors of Wipro Limited Report on the Standalone Ind AS Financial Statements At the request of Wipro Limited, the Ultimate Holding Company of Wipro Data

Independent Auditor s Report To the Board of Directors of Wipro Limited Report on the Standalone Ind AS Financial Statements At the request of Wipro Limited, the Ultimate Holding Company of Wipro Data

IFRS AS A TOOL FOR CROSS- BORDER FINANCIAL REPORTING

IFRS AS A TOOL FOR CROSS- BORDER FINANCIAL REPORTING A paper presented by Ismai la M. Zakari FBR, FCA Managing Partner, (Chartered Accountants) Council Member, ICAN Learning Outcomes What is IFRS? What

IFRS AS A TOOL FOR CROSS- BORDER FINANCIAL REPORTING A paper presented by Ismai la M. Zakari FBR, FCA Managing Partner, (Chartered Accountants) Council Member, ICAN Learning Outcomes What is IFRS? What

Impact of New Economic Policy on India s Foreign Trade

Impact of New Economic Policy on India s Foreign Trade SACHIN N. MEHTA Assistant Professor, D. R. Patel and R. B. Patel Commerce College, Bharthan (Vesu), Surat Gujarat (India) Abstract: This study examines

Impact of New Economic Policy on India s Foreign Trade SACHIN N. MEHTA Assistant Professor, D. R. Patel and R. B. Patel Commerce College, Bharthan (Vesu), Surat Gujarat (India) Abstract: This study examines