Financial Crises and Regulatory Responses. Bank Regulation: I) The Liability side of the Balance Sheet II) The Asset side of the Balance Sheet

|

|

|

- Loraine Porter

- 6 years ago

- Views:

Transcription

1 Financial Crises and Regulatory Responses Bank Regulation: I) The Liability side of the Balance Sheet II) The Asset side of the Balance Sheet

2 Higher Equity Capital Requirements Admati, DeMarzo, Hellwig and Pfleiderer: If a much larger fraction, at least 15%, of banks total, non-risk-weighted, assets were funded by equity, the social benefits would be substantial. And the social costs would be minimal, if any. What is the argument? MM: Using more equity changes how risk and reward are divided between equity holders and debt holders, but does not by itself affect funding costs

3 Equity Capital (2) MM 2: Tax codes that provide advantages to debt financing over equity encourage banks to borrow too much; Debt and equity should at least compete on even terms contingent capital is complex to design and tricky to implement. Increasing equity requirements is simpler and more effective

4 Equity Capital (3) the transition to much higher equity requirements can be implemented quickly and would not have adverse effects on the economy the policy goal must be a healthier banking system, rather than high returns for banks shareholders and managers, with taxpayers picking up losses and economies suffering the fallout

5 Equity Capital is more costly 1. Allen and Carletti (2013) Deposits and Bank Capital Structure Segmentation of bank deposit market and equity markets Total funds that can flow into deposits: D (Endogenous) cost of deposit funds: u 1 Total funds that can flow into equity markets: K

6 Allen and Carletti (2013) (Endogenous) cost of equity capital: ρ R/2 Risky technology: one unit of investment yields random gross return r ε [0, R] with E[r] = R/2 > 1. Depositors can only have access to risky technology through banks With no intermediation costs (h B = 1) the efficient allocation is to channel all deposits D into the risky technology given that R/2 1

7 Allen and Carletti (2013) Banks then simply serve as a conduit to channel funds trapped in the deposit sector to more productive use Competition among banks drives up the cost of deposit funding to the point where ρ = u = R/2. At these equilibrium prices MM holds! Add a friction to get deviations from MM friction in the form of intermediation costs, which take the form of bankruptcy costs (h B < 1)

8 Allen and Carletti (2013) Now, the nature of the exercise is to minimize bankruptcy costs! More equity leads to lower bankruptcy costs But equity financing is more expensive than deposit financing: ρ R/2 > 1. => Tradeoff: equity financing vs. bankruptcy costs In equilibrium cost of equity financing must be equal to the cost of deposit funding including bankruptcy costs

depositors get: Bank expected profits: rb R r rd 1 k B 1 R dr k")

9 Allen and Carletti (2013) Simplest case: set h B = 0 Then: bankruptcy occurs when r < r B = r D (1 k B ) depositors get: Bank expected profits: rb R r rd 1 k B 1 R dr k B

10 Equity Capital is more Costly 2. DeAngelo and Stulz (2013) Why High Leverage is Optimal for Banks : Also a segmented market model, Non-financial risky firms cannot support high leverage and produce liquidity (Walmart?) Banks step in to provide liquidity with high leverage balance sheets, Cheaper for bank to issue sh.t. debt, as bank can raise funds at a lower cost by providing liquidity

11 Equity Capital is more Costly 3. Bolton and Freixas (2006) Corporate Finance and the Monetary Transmission Mechanism, Review of Financial Studies: asymmetric information about banks net worth adds a cost to outside equity capital, asymmetric information particularly severe in a crisis Walter Bagehot: Every Banker knows that if he has to prove that he is worthy of credit, however good may be his arguments, in fact his credit is gone

12 Cost of Equity Capital Bolton and Freixas model produces multiple equilibria, one of which displays all the features of a credit crunch => i) bank lending constrained by equity capital requirements, ii) constraint is tighter in crisis times Evidence: Jimenez, Ongena, Peydro, and Saurina (2011) based on a natural experiment in Spain; when capital constraints become tighter banks uniformly respond by cutting back lending

13 Debt Structure and Wholesale Funding

14 It is not all about Equity Buffers Besides equity capital requirements need to pay attention to the structure of debt liabilities Heavy reliance on wholesale funding (e.g. shortterm repo funding from MMMFs) makes banks more fragile Why? No insurance equivalent to deposit insurance Special treatment of repos in bank resolution

15 Liability Structure of SIFIs *Other = CP, derivative payables, securities sold short Source: FSOC Report 2012

16 Wholesale Investors Source: FSOC Report 2012

17 Contingent Capital

18 Contingent Capital: Early Proposals 1. Flannery (2002, 2009): an automatic conversion of subordinated (unsecured) debt into common equity when the stock price crosses a pre-specified floor (common equity market value falls below 4% of total assets) 2. Duffie (2009): automatic conversion if ratio of tangible common equity to tangible assets falls below a threshold 3. Mc Donald (2010): two price triggers for conversion; one is the bank s own stock price and the other is a financial stock index

19 Motivation of Early Proposals A simple substitute for a bank resolution procedure An ex-ante commitment to private sector involvement Reduce reliance on bail-outs Mitigate moral hazard in lending No notion of Coasean bargain

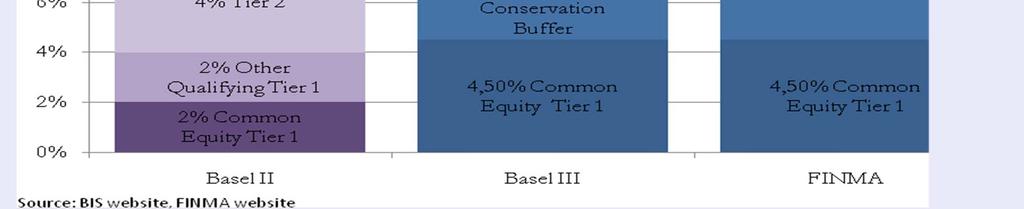

20 Swiss Equity Capital Regulation

21 Problems with Early Proposals 1. Conversion trigger based on ratio of tangible common equity to tangible assets is subject to accounting manipulation & is impossible to track continuously; ratio may move too slowly at the onset of a crisis 2. Conversion trigger based on stock price can give rise to multiple equilibria (Sundaresan and Wang, 2010) and lead to death spirals 3. Both types of CoCo instrument are difficult to price.

22 Early Examples 1. Lloyds bank: in November 2009 issued 7.5bn of Enhanced Capital Notes: sub. debt (lower Tier 2) of year maturities convert into common stock if Lloyds core Tier 1 capital ratio falls below 5% 2. Royal Bank of Scotland: gets access to recap. by UK Treasury if core Tier 1 ratio falls below 5% against a 4% annual premium 3. Rabobank: in March 2010 issued CoCos such that investors face a 75% automatic haircut if Tier 1 ratio falls below 7%

23 Lloyds Nov 2009 Rabobank Mar 2010 Jan 2011 Credit Suisse Feb 2011 Mar 2012 Mar 2012 UBS 2012 Feb 2012 Aug 2012 Instrument Enhanced capital note Senior contingent note Tier I perpetual capital securities Tier II buffer capital note Hybrid capital instrument Tier II buffer capital note Tier II capital note Tier II capital note Seniority Subordinate d Senior Subordinated Subordinated Subordinated Subordinated Trigger Core Tier I <5% Equity capital <7% Equity capital <8% Core Tier I <7% or bank declared nonviable Core Tier I <7% or bank declared non-viable Core Tier I < 5% Mechanism Conversion into a fixed number of shares 75% principal write-down & 25% repaid in cash Permanent write-down Conversion into dollar shares (min $20) Exchanged for cash or hybrid capital in Oct 2013 if trigger not pulled before Conversion into CHF shares (min CHF 20) Permanent writedown Coupon % 6.9% 8.4% 7.9% 9-9.5% 7.1% 7.3% 7.6% Maturity years 10 year 30 years 30 years 1.5 year 10 year 10 years 10 years Issue size $13.7bn $1.64bn $2bn $2bn $6.2bn $759 million $1bn $2bn Remarks - Subscribers: Senior debt holders of the bank ( Switch ) -Subscribers: mainly individual investors -1 st Basel III compliant CoCo issued -Orders amounted to $29bn (11 times oversubscription) -Subscribers: Qatar Holdings, Olayan Group -Small issuance to complete the 2011 issuance and meet the Swiss regulatory capital requirements -Directed at Asian investors -Mainly US & institutional investors -Orders amounted to $9bn

24 Other Examples Spain: Spanish bank reform (May 2012): The government will buy CoCos from distressed Spanish banks, through the FROB (Spain bank rescue fund) Structure of the CoCos: 5 years maturity and 10% coupon rate The 6th largest Spanish lender, Banco Popular has issued CoCos UK: Barclays CoCos (Nov and April 2013; 7% trigger)

25 Capital Access Bonds The right to issue equity in crisis events Main point of our article: Capital Access Bonds are a Coasean Bargain for Banks, Long-term Investors, and Regulators 1. Banks can ensure that they have sufficient (regulatory) capital when they need it most 2. Long-term investors can monetize their equity investments and obtain a premium for implementing counter-cyclical investment strategies 3. Bank Regulators gain by implementing a more efficient form of equity capital regulation

26 Contingent Capital (2) Equivalent to a line of credit commitment (LOC) but for equity! Commit to terms in advance, before asymmetric information problems get worse Many long-term investors are natural holders of contingent capital Counterparty risk, collateralization and reverse convertible bonds

27 Capital Access Bonds (3) A bond that is convertible by the issuer No automatic trigger Fixed maturity (say 10 years) Convertible any time before maturity (American option) If not converted investors get a regular coupon (interest + put premium) If converted investors get a fixed number of newly issued shares => A collateralized put option

28 Motivation for Capital Access Bonds Theory: Bolton, Santos and Scheinkman (2011) Outside and Inside Liquidity, QJE banks engage in maturity transformation and demand liquidity (capital) whenever there is a maturity mismatch can meet this demand with inside liquidity (equity capital) or with outside liquidity (asset sales; new equity issues) capital raised from long-term investors outside liquidity is more efficient, BUT outside liquidity does not flow easily to banks during crises, because of opaqueness of bank balance sheets =>

29 Motivation for CABs (2) Ex-ante (state contingent) capital line commitments are Pareto improvements over standard equity issues. Practice: the example of Berkshire Hathaway, who sells insurance against sharp equity-market crashes in the form of long-term index put options (up to ten years) In 2007 positions in excess of $37.1bn and premium revenues of $4.9bn. Potential problem: Counterparty risk => Collateralize the capital line commitment by raising cash upfront => get a CAB!

30 Basic Mechanism: Illustration (at maturity) Investors Cash ($100) CAB: pays either $100 or two shares Issuer (share price at $100) Either the share price is above $50: => redemption at par Or the share price is below $50: => two new shares are issued Before maturity get coupon payments Combination of: Callable bond American Put option

31 Flows in Case of Exercise Investors Issuer (initial share price at $100) Bond Part Put Part Bond Nominal ($100) Options/Bond Nominal ($100) 2 Shares If no Exercize: Payment of Nominal If Exercize : delivery of two shares The exercise (or not) of the put option will determine the payment in cash or in shares At maturity: depends on whether share price is above or below strike price Before: depends on endogenous optimal stopping price

32 Pricing of CABs: A Numerical Simulation Parameters Ways to price the CAB:

33 Solving for the Conversion Frontier (Debt to Equity) Before maturity the conversion price is low. (70% share price drop) Conversion price tends to increase near maturity

34 Expected Payoffs of Investors Stock price 3.50% 3.00% 2.50% 2.00% 1.50% 1.00% 0.50% 0.00% Effective stock price for the investor Years Probability of loss for the investor Time period Effective stock price = Strike price cumulative sum of coupon payments up to t Trade-off Probability of loss below 3.2% (over the whole life of the product) Additional coupon: % (57% increase)

35 Summing up Advantages for Bank Regulators: Delivers a market price of TBTF insurance Avoids pro-cyclical pitfalls of equity capital requirements What are the possible obstacles? What will be the credit rating of CABs? Taxation of CABs? Regulatory treatment of CABs under Basel III?

36 II) The Asset side of the Balance Sheet Asset side is connected to liability side through the risk-weighting of assets (RWA) Key Issues: How reliable are RWAs? How can they be improved? What are the costs and benefits of structural remedies? Volcker rule Vickers and Liikanen Ring-fencing rules

37 The Asset side of the Balance Sheet Volcker rule, Section 619: Prohibitions on proprietary trading and certain relationships with hedge funds and private equity funds. a banking entity shall not, (A) engage in proprietary trading; or (B) acquire or retain any equity, partnership, or other ownership interest in or sponsor a hedge fund or a private equity fund.

38 The Asset side of the Balance Sheet Any nonbank financial company supervised by the Board that engages in proprietary trading or takes or retains any equity, partnership, or other ownership interest in or sponsors a hedge fund or a private equity fund shall be subject to additional capital requirements for and additional quantitative limits except for permitted activities as described in subsection (d) permitted activities : (A) The purchase, sale, acquisition, or disposition of obligations of the United States or any agency thereof

39 The Asset side of the Balance Sheet permitted activities (continued) : (B) The purchase, sale, acquisition, or disposition of securities and other instruments in connection with underwriting or market-making related activities (C) Risk-mitigating hedging activities in connection with and related to individual or aggregated positions.. (D) The purchase, sale, acquisition, or disposition of securities on behalf of customers.

40 The Asset side of the Balance Sheet Note: much more detailed rule than Glass-Steagall sections + more detailed proposed rules by OCC, Fed, FDIC & SEC (530 pages): Open questions: Why do we need a Volcker rule? What will happen to proprietary trading? Will all BHCs be treated equally?

Capital Access Bonds: Contingent Capital with an Option to Convert 1

Capital Access Bonds: Contingent Capital with an Option to Convert 1 by Patrick Bolton Columbia University and Frederic Samama SWF Research Initiative Amundi - Credit Agricole Group September 2010 Revised

Capital Access Bonds: Contingent Capital with an Option to Convert 1 by Patrick Bolton Columbia University and Frederic Samama SWF Research Initiative Amundi - Credit Agricole Group September 2010 Revised

Maturity Transformation and Liquidity

Maturity Transformation and Liquidity Patrick Bolton, Tano Santos Columbia University and Jose Scheinkman Princeton University Motivation Main Question: Who is best placed to, 1. Transform Maturity 2.

Maturity Transformation and Liquidity Patrick Bolton, Tano Santos Columbia University and Jose Scheinkman Princeton University Motivation Main Question: Who is best placed to, 1. Transform Maturity 2.

Bank Capital under Basel 3: Open Issues

Bank Capital under Basel 3: Open Issues and Foreseeable Effects Giuliano Iannotta - Andrea Resti www.carefin.unibocconi.eu carefin@unibocconi.it www.carefin.unibocconi.eu Agenda The definition of capital:

Bank Capital under Basel 3: Open Issues and Foreseeable Effects Giuliano Iannotta - Andrea Resti www.carefin.unibocconi.eu carefin@unibocconi.it www.carefin.unibocconi.eu Agenda The definition of capital:

A Nonsupervisory Framework to Monitor Financial Stability

A Nonsupervisory Framework to Monitor Financial Stability Tobias Adrian, Daniel Covitz, Nellie Liang Federal Reserve Bank of New York and Federal Reserve Board June 11, 2012 The views in this presentation

A Nonsupervisory Framework to Monitor Financial Stability Tobias Adrian, Daniel Covitz, Nellie Liang Federal Reserve Bank of New York and Federal Reserve Board June 11, 2012 The views in this presentation

F R E Q U E N T L Y A S K E D Q U E S T I O N S A B O U T C O N T I N G E N T C A P I T A L

F R E Q U E N T L Y A S K E D Q U E S T I O N S A B O U T C O N T I N G E N T C A P I T A L How would you define contingent capital? Contingent capital securities are hybrid securities issued by financial

F R E Q U E N T L Y A S K E D Q U E S T I O N S A B O U T C O N T I N G E N T C A P I T A L How would you define contingent capital? Contingent capital securities are hybrid securities issued by financial

Shadow Maturity Transformation and Systemic Risk. Sandra Krieger Executive Vice President and Chief Risk Officer, Federal Reserve Bank of New York

Shadow Maturity Transformation and Systemic Risk Sandra Krieger Executive Vice President and Chief Risk Officer, Federal Reserve Bank of New York 8 March 2011 Overview of discussion What is shadow bank

Shadow Maturity Transformation and Systemic Risk Sandra Krieger Executive Vice President and Chief Risk Officer, Federal Reserve Bank of New York 8 March 2011 Overview of discussion What is shadow bank

Overview of financial regulation

Last updated February 1, 2018 Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz 2/25 Outline Purpose of financial regulation

Last updated February 1, 2018 Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz 2/25 Outline Purpose of financial regulation

Regulatory Capital: an overview and an update

Regulatory Capital: an overview and an update NY2 689993 Tom Humphreys Oliver Ireland Anna Pinedo July 7, 2011 2010 Morrison & Foerster LLP All Rights Reserved mofo.com Overview Evolution of new capital

Regulatory Capital: an overview and an update NY2 689993 Tom Humphreys Oliver Ireland Anna Pinedo July 7, 2011 2010 Morrison & Foerster LLP All Rights Reserved mofo.com Overview Evolution of new capital

Are Banks Special? International Risk Management Conference. IRMC2015 Luxembourg, June 15

Are Banks Special? International Risk Management Conference IRMC2015 Luxembourg, June 15 Michel Crouhy Natixis Wholesale Banking michel.crouhy@natixis.com and Dan Galai The Hebrew University and Sarnat

Are Banks Special? International Risk Management Conference IRMC2015 Luxembourg, June 15 Michel Crouhy Natixis Wholesale Banking michel.crouhy@natixis.com and Dan Galai The Hebrew University and Sarnat

A Comparative Assessment:

A Comparative Assessment: The U.S. Bank Holding Company Structure, the Volcker Rule, UK Banking Reform (Vickers), and the Liikanen Proposal November 2012 Davis Polk & Wardwell LLP Overview These slides

A Comparative Assessment: The U.S. Bank Holding Company Structure, the Volcker Rule, UK Banking Reform (Vickers), and the Liikanen Proposal November 2012 Davis Polk & Wardwell LLP Overview These slides

Samba Financial Group Basel III - Pillar 3 Disclosure Report. September 2017 PUBLIC

Basel III - Pillar 3 Disclosure Report September 2017 Basel III - Pillar 3 Disclosure Report as at September 30, 2017 Page 1 of 12 Table of contents Capital Structure Page Statement of financial position

Basel III - Pillar 3 Disclosure Report September 2017 Basel III - Pillar 3 Disclosure Report as at September 30, 2017 Page 1 of 12 Table of contents Capital Structure Page Statement of financial position

Deposits and Bank Capital Structure

Deposits and Bank Capital Structure Franklin Allen 1 Elena Carletti 2 Robert Marquez 3 1 University of Pennsylvania 2 Bocconi University 3 UC Davis June 2014 Franklin Allen, Elena Carletti, Robert Marquez

Deposits and Bank Capital Structure Franklin Allen 1 Elena Carletti 2 Robert Marquez 3 1 University of Pennsylvania 2 Bocconi University 3 UC Davis June 2014 Franklin Allen, Elena Carletti, Robert Marquez

Lombard Odier Group Pillar 3 Disclosures at 30 June 2018

Lombard Odier Group Pillar 3 Disclosures at 30 June 2018 Contents Introduction 5 Consolidation scope 5 Composition of capital 7 Risk-weighted assets and minimum capital requirements 9 Market Risks 10

Lombard Odier Group Pillar 3 Disclosures at 30 June 2018 Contents Introduction 5 Consolidation scope 5 Composition of capital 7 Risk-weighted assets and minimum capital requirements 9 Market Risks 10

TABLE 2: CAPITAL STRUCTURE - December 31, 2015

Frequency : Quarterly Location : Quarterly Financial Statement TABLE 2: CAPITAL STRUCTURE - December 31, 2015 Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published

Frequency : Quarterly Location : Quarterly Financial Statement TABLE 2: CAPITAL STRUCTURE - December 31, 2015 Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published

The Trouble with Bail-in : Pillar 2

The Trouble with Bail-in : Pillar 2 Mark J. Flannery Prepared for a conference on Achieving Financial Stability: Challenges to Prudential Regulation Federal Reserve Bank of Chicago November 4, 2016 1 The

The Trouble with Bail-in : Pillar 2 Mark J. Flannery Prepared for a conference on Achieving Financial Stability: Challenges to Prudential Regulation Federal Reserve Bank of Chicago November 4, 2016 1 The

WHY COCOS ARE LESS PROBLEMATIC THAN BAILING-IN OF LIABILITIES

WHY COCOS ARE LESS PROBLEMATIC THAN BAILING-IN OF LIABILITIES THE FOURTH SYMPOSIUM ON ENDING TOO BIG TO FAIL, FEDERAL RESERVE BANK OF MINNEAPOLIS SEPTEMBER 26 PROFESSOR EMILIOS AVGOULEAS CHAIR IN INTERNATIONAL

WHY COCOS ARE LESS PROBLEMATIC THAN BAILING-IN OF LIABILITIES THE FOURTH SYMPOSIUM ON ENDING TOO BIG TO FAIL, FEDERAL RESERVE BANK OF MINNEAPOLIS SEPTEMBER 26 PROFESSOR EMILIOS AVGOULEAS CHAIR IN INTERNATIONAL

Samba Financial Group Basel III - Pillar 3 Disclosure Report. March 2018 PUBLIC

Basel III - Pillar 3 Disclosure Report March 2018 Basel III - Pillar 3 Disclosure Report as at March 31, 2018 Page 1 of 11 Table of contents Capital structure Statement of financial position - Step 1 (

Basel III - Pillar 3 Disclosure Report March 2018 Basel III - Pillar 3 Disclosure Report as at March 31, 2018 Page 1 of 11 Table of contents Capital structure Statement of financial position - Step 1 (

How Curb Risk In Wall Street. Luigi Zingales. University of Chicago

How Curb Risk In Wall Street Luigi Zingales University of Chicago Banks Instability Banks are engaged in a transformation of maturity: borrow short term lend long term This transformation is socially valuable

How Curb Risk In Wall Street Luigi Zingales University of Chicago Banks Instability Banks are engaged in a transformation of maturity: borrow short term lend long term This transformation is socially valuable

Information on Capital Structure, Liquidity Coverage and Leverage Ratios as per Basel-III Framework as at June 30, 2016

Information on Capital Structure, Liquidity Coverage and Leverage Ratios as per Basel-III Framework as at June 30, 2016 Table of Contents Capital Structure Statement of Financial Position - Step 1 ( Table

Information on Capital Structure, Liquidity Coverage and Leverage Ratios as per Basel-III Framework as at June 30, 2016 Table of Contents Capital Structure Statement of Financial Position - Step 1 ( Table

Discussion of Liquidity, Moral Hazard, and Interbank Market Collapse

Discussion of Liquidity, Moral Hazard, and Interbank Market Collapse Tano Santos Columbia University Financial intermediaries, such as banks, perform many roles: they screen risks, evaluate and fund worthy

Discussion of Liquidity, Moral Hazard, and Interbank Market Collapse Tano Santos Columbia University Financial intermediaries, such as banks, perform many roles: they screen risks, evaluate and fund worthy

Central bank liquidity provision, risktaking and economic efficiency

Central bank liquidity provision, risktaking and economic efficiency U. Bindseil and J. Jablecki Presentation by U. Bindseil at the Fields Quantitative Finance Seminar, 27 February 2013 1 Classical problem:

Central bank liquidity provision, risktaking and economic efficiency U. Bindseil and J. Jablecki Presentation by U. Bindseil at the Fields Quantitative Finance Seminar, 27 February 2013 1 Classical problem:

Macroprudential Bank Capital Regulation in a Competitive Financial System

Macroprudential Bank Capital Regulation in a Competitive Financial System Milton Harris, Christian Opp, Marcus Opp Chicago, UPenn, University of California Fall 2015 H 2 O (Chicago, UPenn, UC) Macroprudential

Macroprudential Bank Capital Regulation in a Competitive Financial System Milton Harris, Christian Opp, Marcus Opp Chicago, UPenn, University of California Fall 2015 H 2 O (Chicago, UPenn, UC) Macroprudential

Credit Market Competition and Liquidity Crises

Credit Market Competition and Liquidity Crises Elena Carletti Agnese Leonello European University Institute and CEPR University of Pennsylvania May 9, 2012 Motivation There is a long-standing debate on

Credit Market Competition and Liquidity Crises Elena Carletti Agnese Leonello European University Institute and CEPR University of Pennsylvania May 9, 2012 Motivation There is a long-standing debate on

Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015

Instructor: Prof. Menzie Chinn UW Madison Fall 2015") Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015 14 2 14 3 The Sources and Consequences of Runs, Panics, and Crises Banks fragility arises from the fact

Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015 14 2 14 3 The Sources and Consequences of Runs, Panics, and Crises Banks fragility arises from the fact

U.S. Implementation of Basel III: Current Developments

U.S. Implementation of Basel III: Current Developments Practicing Law Institute March 12, 2012 Charles M. Horn Dwight C. Smith 2010 Morrison & Foerster LLP All Rights Reserved mofo.com Topics Current U.S.

U.S. Implementation of Basel III: Current Developments Practicing Law Institute March 12, 2012 Charles M. Horn Dwight C. Smith 2010 Morrison & Foerster LLP All Rights Reserved mofo.com Topics Current U.S.

Regulatory disclosures Credit Suisse Group Credit Suisse (Bank) Credit Suisse (Bank) parent company Credit Suisse International

Credit Suisse (Bank) parent company Credit Suisse International") Regulatory disclosures Credit Suisse (Bank) Credit Suisse (Bank) parent company Credit Suisse International August 14, 2015 2Q15 Regulatory disclosures 2Q15 2 u Refer to Capital management and Liquidity

Regulatory disclosures Credit Suisse (Bank) Credit Suisse (Bank) parent company Credit Suisse International August 14, 2015 2Q15 Regulatory disclosures 2Q15 2 u Refer to Capital management and Liquidity

Regulatory disclosures Credit Suisse Group Credit Suisse (Bank) Credit Suisse (Bank) parent company Credit Suisse International

Credit Suisse (Bank) parent company Credit Suisse International") Regulatory disclosures Credit Suisse (Bank) Credit Suisse (Bank) parent company Credit Suisse International March 24, 2016 2015 2 REGULATORY DISCLOSURES In connection with the implementation of Basel III,

Regulatory disclosures Credit Suisse (Bank) Credit Suisse (Bank) parent company Credit Suisse International March 24, 2016 2015 2 REGULATORY DISCLOSURES In connection with the implementation of Basel III,

DISSECTING A BANK S BALANCE SHEET

DISSECTING A BANK S BALANCE SHEET March 14, 2013 Presented by: Bill O Neill, CFA 100 Federal Street, 33 rd Floor, Boston, MA 02110 (617) 330-9333 www.incomeresearch.com BANK ANALYIS OVERVIEW Goal: Define

DISSECTING A BANK S BALANCE SHEET March 14, 2013 Presented by: Bill O Neill, CFA 100 Federal Street, 33 rd Floor, Boston, MA 02110 (617) 330-9333 www.incomeresearch.com BANK ANALYIS OVERVIEW Goal: Define

TABLE 2: CAPITAL STRUCTURE - March 31, 2016

c Frequency : Quarterly Location : Quarterly Financial Statement Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published financial statements Adjustment of banking

c Frequency : Quarterly Location : Quarterly Financial Statement Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published financial statements Adjustment of banking

Contingent Capital : The Case for COERCS

George Pennacchi (University of Illinois) Theo Vermaelen (INSEAD) Christian Wolff (University of Luxembourg) 10 November 2010 Contingent Capital : The Case for COERCS How to avoid the next financial crisis?

George Pennacchi (University of Illinois) Theo Vermaelen (INSEAD) Christian Wolff (University of Luxembourg) 10 November 2010 Contingent Capital : The Case for COERCS How to avoid the next financial crisis?

Deposits and Bank Capital Structure

Deposits and Bank Capital Structure Franklin Allen 1 Elena Carletti 2 Robert Marquez 3 1 Imperial College 2 Bocconi University 3 UC Davis 24 October 2014 Franklin Allen, Elena Carletti, Robert Marquez

Deposits and Bank Capital Structure Franklin Allen 1 Elena Carletti 2 Robert Marquez 3 1 Imperial College 2 Bocconi University 3 UC Davis 24 October 2014 Franklin Allen, Elena Carletti, Robert Marquez

Convertible Bonds and Bank Risk-taking

Natalya Martynova 1 Enrico Perotti 2 Bailouts, bail-in, and financial stability Paris, November 28 2014 1 De Nederlandsche Bank 2 University of Amsterdam, CEPR Motivation In the credit boom, high leverage

Natalya Martynova 1 Enrico Perotti 2 Bailouts, bail-in, and financial stability Paris, November 28 2014 1 De Nederlandsche Bank 2 University of Amsterdam, CEPR Motivation In the credit boom, high leverage

The Banking Crisis and Its Regulatory Response in Europe

The Banking Crisis and Its Regulatory Response in Europe Mathias Dewatripont National Bank of Belgium and Single Supervisory Mechanism Bruegel 10 th Anniversary Conference at NBB January 28, 2016 Outline

The Banking Crisis and Its Regulatory Response in Europe Mathias Dewatripont National Bank of Belgium and Single Supervisory Mechanism Bruegel 10 th Anniversary Conference at NBB January 28, 2016 Outline

THE ECONOMICS OF BANK CAPITAL

THE ECONOMICS OF BANK CAPITAL Edoardo Gaffeo Department of Economics and Management University of Trento OUTLINE What we are talking about, and why Banks are «special», and their capital is «special» as

THE ECONOMICS OF BANK CAPITAL Edoardo Gaffeo Department of Economics and Management University of Trento OUTLINE What we are talking about, and why Banks are «special», and their capital is «special» as

Basel III - Implementation issues facing the Industry. Patricia Jackson Head of Financial Regulation Advisory EMEIA

Basel III - Implementation issues facing the Industry Patricia Jackson Systemically Important Banks FSB paper on intensive supervision Other elements are under discussion Contains a number of components:

Basel III - Implementation issues facing the Industry Patricia Jackson Systemically Important Banks FSB paper on intensive supervision Other elements are under discussion Contains a number of components:

Sr. No. 1 Issuer Axis Bank Ltd. 2 Unique identifier ISIN: INE238A01026

XIII. MAIN FEATURES OF REGULATORY CAPITAL AS ON 8 th NOVEMBER 2018 The main features of equity capital are given below: Particulars Equity 1 Issuer Axis Bank Ltd. 2 Unique identifier ISIN: INE238A01026

XIII. MAIN FEATURES OF REGULATORY CAPITAL AS ON 8 th NOVEMBER 2018 The main features of equity capital are given below: Particulars Equity 1 Issuer Axis Bank Ltd. 2 Unique identifier ISIN: INE238A01026

Shadow Banking and Financial Stability

Shadow Banking and Financial Stability Tobias Adrian, November 8, 2013 The views expressed here are those of the author exclusively and do not necessarily represent those of the Federal Reserve Bank of

Shadow Banking and Financial Stability Tobias Adrian, November 8, 2013 The views expressed here are those of the author exclusively and do not necessarily represent those of the Federal Reserve Bank of

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended September 30, 2016 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended September 30, 2016 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

Banking Regulation: An introduction. By A V Vedpuriswar

Banking Regulation: An introduction By A V Vedpuriswar June 27, 2018 Thus small depositors across the world are protected by deposit 1 insurance. Introduction(1) For all their prestige and high profile,

Banking Regulation: An introduction By A V Vedpuriswar June 27, 2018 Thus small depositors across the world are protected by deposit 1 insurance. Introduction(1) For all their prestige and high profile,

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended December 31, 2015 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended December 31, 2015 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

Convertible Bonds and Bank Risk-taking

Natalya Martynova 1 Enrico Perotti 2 European Central Bank Workshop June 26, 2013 1 University of Amsterdam, Tinbergen Institute 2 University of Amsterdam, CEPR and ECB In the credit boom, high leverage

Natalya Martynova 1 Enrico Perotti 2 European Central Bank Workshop June 26, 2013 1 University of Amsterdam, Tinbergen Institute 2 University of Amsterdam, CEPR and ECB In the credit boom, high leverage

Bail-ins, Bank Resolution, and Financial Stability

, Bank Resolution, and Financial Stability NYU and ICL 29 November, 2014 Laws, says that illustrious rhymer Mr John Godfrey Saxe, like sausages, cease to inspire respect in proportion as we know how they

, Bank Resolution, and Financial Stability NYU and ICL 29 November, 2014 Laws, says that illustrious rhymer Mr John Godfrey Saxe, like sausages, cease to inspire respect in proportion as we know how they

Habib Bank AG Zurich. Annual disclosures according to Basel III (Year 2015)

") Annual disclosures according to Basel III (Year 2015) 1 Annual disclosures according to Basel III (Year 2015) 1. Scope of consolidation Scope of consolidation for capital adequacy purposes The scope of

Annual disclosures according to Basel III (Year 2015) 1 Annual disclosures according to Basel III (Year 2015) 1. Scope of consolidation Scope of consolidation for capital adequacy purposes The scope of

Institutional Finance

Institutional Finance Lecture 09 : Banking and Maturity Mismatch Markus K. Brunnermeier Preceptor: Dong Beom Choi Princeton University 1 Select/monitor borrowers Sharpe (1990) Reduce asymmetric info idiosyncratic

Institutional Finance Lecture 09 : Banking and Maturity Mismatch Markus K. Brunnermeier Preceptor: Dong Beom Choi Princeton University 1 Select/monitor borrowers Sharpe (1990) Reduce asymmetric info idiosyncratic

Samba Financial Group Basel III - Pillar 3 Disclosure Report. June 2018 PUBLIC

Basel III - Pillar 3 Disclosure Report June 2018 Basel III - Pillar 3 Disclosure Report as at June 30, 2018 Page 1 of 19 Table of Contents Capital Structure Page Statement of financial position - Step

Basel III - Pillar 3 Disclosure Report June 2018 Basel III - Pillar 3 Disclosure Report as at June 30, 2018 Page 1 of 19 Table of Contents Capital Structure Page Statement of financial position - Step

Reforming the structure of the EU banking sector

EUROPEAN COMMISSION Directorate General Internal Market and Services Reforming the structure of the EU banking sector Consultation paper This consultation paper outlines the main building blocks of the

EUROPEAN COMMISSION Directorate General Internal Market and Services Reforming the structure of the EU banking sector Consultation paper This consultation paper outlines the main building blocks of the

Regulatory Implementation Slides

Regulatory Implementation Slides Table of Contents 1. Nonbank Financial Companies: Path to Designation as Systemically Important 2. Systemic Oversight of Bank Holding Companies 3. Systemic Oversight of

Regulatory Implementation Slides Table of Contents 1. Nonbank Financial Companies: Path to Designation as Systemically Important 2. Systemic Oversight of Bank Holding Companies 3. Systemic Oversight of

Credit Suisse s approach to TLAC-eligible debt

Credit Suisse s approach to TLAC-eligible debt Theis Wenke Credit Suisse Group Deputy Treasurer & Swiss CFO DZ BANK Veranstaltung Praxistag Bankanleihen Investieren in Zeiten der neuen Haftungskaskade

Credit Suisse s approach to TLAC-eligible debt Theis Wenke Credit Suisse Group Deputy Treasurer & Swiss CFO DZ BANK Veranstaltung Praxistag Bankanleihen Investieren in Zeiten der neuen Haftungskaskade

DEPOSITS and BANK CAPITAL STRUCTURE by Allen, Carletti, and Marquez DISCUSSION. By Paolo Fulghieri UNC, CEPR, ECGI

DEPOSITS and BANK CAPITAL STRUCTURE by Allen, Carletti, and Marquez DISCUSSION By Paolo Fulghieri UNC, CEPR, ECGI Universita L. Bocconi CAREFIN October 24, 2014 1. INTRODUCTION This paper addresses an

DEPOSITS and BANK CAPITAL STRUCTURE by Allen, Carletti, and Marquez DISCUSSION By Paolo Fulghieri UNC, CEPR, ECGI Universita L. Bocconi CAREFIN October 24, 2014 1. INTRODUCTION This paper addresses an

CoCos: A Promising Idea Poorly Executed

CoCos: A Promising Idea Poorly Executed Richard J. Herring herring@wharton.upenn.edu Wharton School 19 th Annual International Banking Conference Federal Reserve Bank of Chicago. November 2, 2016 1 Background

CoCos: A Promising Idea Poorly Executed Richard J. Herring herring@wharton.upenn.edu Wharton School 19 th Annual International Banking Conference Federal Reserve Bank of Chicago. November 2, 2016 1 Background

BBK3253 Risk Management Prepared by Dr Khairul Anuar

BBK3253 Risk Management Prepared by Dr Khairul Anuar L6 - Managing Credit Risk 23-0 Content 1. Credit risk definition 2. Credit risk in the banking sector 3. Credit Risk vs. Market Risk 4. Credit Products

BBK3253 Risk Management Prepared by Dr Khairul Anuar L6 - Managing Credit Risk 23-0 Content 1. Credit risk definition 2. Credit risk in the banking sector 3. Credit Risk vs. Market Risk 4. Credit Products

The lender of last resort: liquidity provision versus the possibility of bail-out

The lender of last resort: liquidity provision versus the possibility of bail-out Rob Nijskens Sylvester C.W. Eijffinger June 24, 2010 The lender of last resort: liquidity versus bail-out 1 /20 Motivation:

The lender of last resort: liquidity provision versus the possibility of bail-out Rob Nijskens Sylvester C.W. Eijffinger June 24, 2010 The lender of last resort: liquidity versus bail-out 1 /20 Motivation:

Financial Stability Monitoring Fernando Duarte Federal Reserve Bank of New York March 2015

Financial Stability Monitoring Fernando Duarte Federal Reserve Bank of New York March 2015 The views in this presentation do not necessarily represent the views of the Federal Reserve Board, the Federal

Financial Stability Monitoring Fernando Duarte Federal Reserve Bank of New York March 2015 The views in this presentation do not necessarily represent the views of the Federal Reserve Board, the Federal

Deutsche Bank Credit Overview

Credit Overview As of 30 September 2017 Summary Progress: Wind-down of the non-core unit and resolved a significant number of large litigation items today Successful execution of the strategic measures

Credit Overview As of 30 September 2017 Summary Progress: Wind-down of the non-core unit and resolved a significant number of large litigation items today Successful execution of the strategic measures

Incentive effects of contingent capital 2013

ADVISORY Incentive effects of contingent capital 2013 kpmg.com KPMG INTERNATIONAL Foreword KPMG s Global Valuation Institute ( GVI ) is thrilled to introduce its fourth managerial paper since the launch

ADVISORY Incentive effects of contingent capital 2013 kpmg.com KPMG INTERNATIONAL Foreword KPMG s Global Valuation Institute ( GVI ) is thrilled to introduce its fourth managerial paper since the launch

SUBMISSION BY THE BRITISH BANKERS ASSOCIATION. Introduction

SUBMISSION BY THE BRITISH BANKERS ASSOCIATION Introduction The British Bankers Association welcomes the opportunity to input to the inquiry by the Economy, Energy and Tourism Committee on the implications

SUBMISSION BY THE BRITISH BANKERS ASSOCIATION Introduction The British Bankers Association welcomes the opportunity to input to the inquiry by the Economy, Energy and Tourism Committee on the implications

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended December 31, 2016 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended December 31, 2016 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

TSB Banking Group plc. Significant Subsidiary Disclosures. 31 December 2015

Significant Subsidiary Disclosures 31 December Pillar 3 Disclosures Contents CONTENTS... 2 INDEX OF TABLES... 3 1. INTRODUCTION... 4 2. EXECUTIVE SUMMARY... 4 3. OWN FUNDS... 5 3.1. CAPITAL RISK... 5 3.2.

Significant Subsidiary Disclosures 31 December Pillar 3 Disclosures Contents CONTENTS... 2 INDEX OF TABLES... 3 1. INTRODUCTION... 4 2. EXECUTIVE SUMMARY... 4 3. OWN FUNDS... 5 3.1. CAPITAL RISK... 5 3.2.

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended June 30, 2015 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended June 30, 2015 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

Counterparty risk externality: Centralized versus over-the-counter markets. Presentation at Stanford Macro, April 2011

: Centralized versus over-the-counter markets Viral Acharya Alberto Bisin NYU-Stern, CEPR and NBER NYU and NBER Presentation at Stanford Macro, April 2011 Introduction OTC markets have often been at the

: Centralized versus over-the-counter markets Viral Acharya Alberto Bisin NYU-Stern, CEPR and NBER NYU and NBER Presentation at Stanford Macro, April 2011 Introduction OTC markets have often been at the

Danske Bank Tier 2 Capital

Danske Bank Tier 2 Capital Henrik Ramlau-Hansen CFO & Member of the Executive Board Steen Blaafalk Head of Treasury Global Conference Call 23 September 2013 Agenda Financial results 3 Capital, liquidity

Danske Bank Tier 2 Capital Henrik Ramlau-Hansen CFO & Member of the Executive Board Steen Blaafalk Head of Treasury Global Conference Call 23 September 2013 Agenda Financial results 3 Capital, liquidity

Additional Tier 1 capital (Basel III-compliant)

") Additional Tier 1 capital (Basel III-compliant) Issuer UBS Group AG, or other employing entities of the UBS group ISIN - Issue Date 31.12.16 1 Currency Nominal (million) CHF 2 Coupon Rate 2.55% / 5.95%

Additional Tier 1 capital (Basel III-compliant) Issuer UBS Group AG, or other employing entities of the UBS group ISIN - Issue Date 31.12.16 1 Currency Nominal (million) CHF 2 Coupon Rate 2.55% / 5.95%

Presentation to Tier 1 Investors April 2005

Presentation to Tier 1 Investors April 2005 Michael Oliver Director of Investor Relations John Gillbe Group Capital and BSM Director Overview of Lloyds TSB Group plc 3 businesses* UK Retail Banking: GBP

Presentation to Tier 1 Investors April 2005 Michael Oliver Director of Investor Relations John Gillbe Group Capital and BSM Director Overview of Lloyds TSB Group plc 3 businesses* UK Retail Banking: GBP

Too Swiss To Fail? The new bank resolution package in Switzerland

www.unige.ch/cdbf Too Swiss To Fail? The new bank resolution package in Switzerland ILIAS PNEVMONIDIS, AEDBF Conference, Athens, 6/10/2012 There are advantages to size.in the case of the large international

www.unige.ch/cdbf Too Swiss To Fail? The new bank resolution package in Switzerland ILIAS PNEVMONIDIS, AEDBF Conference, Athens, 6/10/2012 There are advantages to size.in the case of the large international

Basel III Pillar 3 Disclosures. 30 June 2018

Basel III Pillar 3 Disclosures 30 June 2018 Table of Contents PART 2 OVERVIEW OF RISK MANAGEMENT AND RWA... 3 KM1 Key metrics (at consolidated group level)... 3 OV1 Overview of RWA... 4 PART 5 MICROPRUDENTIAL

Basel III Pillar 3 Disclosures 30 June 2018 Table of Contents PART 2 OVERVIEW OF RISK MANAGEMENT AND RWA... 3 KM1 Key metrics (at consolidated group level)... 3 OV1 Overview of RWA... 4 PART 5 MICROPRUDENTIAL

Top 5 Priorities in China s Financial Regulation

Top 5 Priorities in China s Financial Regulation Xie Ping (China Investment Corporation) China s financial sector has improved remarkably in the past decade, especially in the banking sector. It plays

Top 5 Priorities in China s Financial Regulation Xie Ping (China Investment Corporation) China s financial sector has improved remarkably in the past decade, especially in the banking sector. It plays

An Evaluation of Money Market Fund Reform Proposals

An Evaluation of Money Market Fund Reform Proposals Sam Hanson David Scharfstein Adi Sunderam Harvard University May 2014 Introduction The financial crisis revealed significant vulnerabilities of the global

An Evaluation of Money Market Fund Reform Proposals Sam Hanson David Scharfstein Adi Sunderam Harvard University May 2014 Introduction The financial crisis revealed significant vulnerabilities of the global

What should be of interest in Dodd-Frank to non-u.s. banks wanting to do business in the United States?

Dodd-Frank Update Full title of the law is The Dodd-Frank Wall Street Reform and Consumer Protection Act Public Law 111-203 was signed into law on July 21, 2010 Major changes made to financial regulation

Dodd-Frank Update Full title of the law is The Dodd-Frank Wall Street Reform and Consumer Protection Act Public Law 111-203 was signed into law on July 21, 2010 Major changes made to financial regulation

Key high-level comments by Nordea Bank AB (publ) on reforming the structure of the EU banking sector

on reforming the structure of the EU banking sector") 1 (8) Page To European Commission Email: MARKT-HLEG@ec.europa.eu Document title response to Consultation on the recommendations of the High-level Expert Group on Reforming the structure of the EU banking

1 (8) Page To European Commission Email: MARKT-HLEG@ec.europa.eu Document title response to Consultation on the recommendations of the High-level Expert Group on Reforming the structure of the EU banking

Keeping Capital Adequate

Keeping Capital Adequate Mark J. Flannery University of Florida Prepared for the Nykredit Symposium 2010, Financial Stability and Future Financial Regulation, December 13, 2010. 1 25 Figure 1: Market and

Keeping Capital Adequate Mark J. Flannery University of Florida Prepared for the Nykredit Symposium 2010, Financial Stability and Future Financial Regulation, December 13, 2010. 1 25 Figure 1: Market and

Reading Material: G-SIBs, D-SIBs and Contingent Capital

Reading Material: G-SIBs, D-SIBs and Contingent Capital 1. The G-SIB Rules The G-SIB rules published by the Basel Committee on Banking Supervision (BCBS) in November 2011 were updated and replaced in July

Reading Material: G-SIBs, D-SIBs and Contingent Capital 1. The G-SIB Rules The G-SIB rules published by the Basel Committee on Banking Supervision (BCBS) in November 2011 were updated and replaced in July

The Federal Reserve in the 21st Century Financial Stability Policies

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

Five Years after Lehman s Collapse: Where are we going to?

Five Years after Lehman s Collapse: Where are we going to? Luis M. Linde Governor XCVII MEETING OF CENTRAL BANK GOVERNORS OF THE CENTER FOR LATIN AMERICAN MONETARY STUDIES São Paulo 28 April 2014 LEHMAN

Five Years after Lehman s Collapse: Where are we going to? Luis M. Linde Governor XCVII MEETING OF CENTRAL BANK GOVERNORS OF THE CENTER FOR LATIN AMERICAN MONETARY STUDIES São Paulo 28 April 2014 LEHMAN

Chapter Fourteen. Chapter 10 Regulating the Financial System 5/6/2018. Financial Crisis

Chapter Fourteen Chapter 10 Regulating the Financial System Financial Crisis Disruptions to financial systems are frequent and widespread around the world. Why? Financial systems are fragile and vulnerable

Chapter Fourteen Chapter 10 Regulating the Financial System Financial Crisis Disruptions to financial systems are frequent and widespread around the world. Why? Financial systems are fragile and vulnerable

Re-establishing Market Discipline and Reducing Taxpayer Burden: Will Bail-in Do the Job?

Re-establishing Market Discipline and Reducing Taxpayer Burden: Will Bail-in Do the Job? George G. Pennacchi Department of Finance University of Illinois Financial Safety Net Conference 2015 Stockholm

Re-establishing Market Discipline and Reducing Taxpayer Burden: Will Bail-in Do the Job? George G. Pennacchi Department of Finance University of Illinois Financial Safety Net Conference 2015 Stockholm

TABLE 2: CAPITAL STRUCTURE - September 30, 2018

TABLE 2: CAPITAL STRUCTURE - September 30, 2018 Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published financial statements Adjustment of banking associates /

TABLE 2: CAPITAL STRUCTURE - September 30, 2018 Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published financial statements Adjustment of banking associates /

Capital adequacy and liquidity disclosures. Disclosure as at 30 June 2017

Capital adequacy and liquidity disclosures Disclosure as at 30 June 2017 Publication date: 25 August 2017 With the information showing its position as at 30 June 2017, the bank meets the requirements of

Capital adequacy and liquidity disclosures Disclosure as at 30 June 2017 Publication date: 25 August 2017 With the information showing its position as at 30 June 2017, the bank meets the requirements of

Debt Investor Presentation

Debt Investor Presentation November 2009 Agenda FirstRand and Group Treasury Funding & Liquidity Risk Management Capital Management 2 Agenda FirstRand and Group Treasury Funding & Liquidity Risk Management

Debt Investor Presentation November 2009 Agenda FirstRand and Group Treasury Funding & Liquidity Risk Management Capital Management 2 Agenda FirstRand and Group Treasury Funding & Liquidity Risk Management

Main Features of Regulatory Capital Instruments: Main Features of Regulatory Capital Instruments (Equity Shares & Bond SERIES I, II, III & IV)

") Main Features of Regulatory Capital s: Main Features of Regulatory Capital s (Equity Shares & Bond SERIES I, II, III & IV) 1. Issuer Unique identifier (e.g. 2. CUSIP, ISIN or Bloomberg INE614B01018 INE614B09011

Main Features of Regulatory Capital s: Main Features of Regulatory Capital s (Equity Shares & Bond SERIES I, II, III & IV) 1. Issuer Unique identifier (e.g. 2. CUSIP, ISIN or Bloomberg INE614B01018 INE614B09011

Basel Pillar 3 Disclosures

Basel Pillar 3 Disclosures September 30, 2017 TABLE OF CONTENTS Introduction................................................................................... Regulatory Framework........................................................................

Basel Pillar 3 Disclosures September 30, 2017 TABLE OF CONTENTS Introduction................................................................................... Regulatory Framework........................................................................

Shadow Banking, Central Banking, and the Future of Global Finance

Shadow Banking, Central Banking, and the Future of Global Finance Perry Mehrling Shadow Banking: A European Perspective City University London Feb 2, 2013 A Bagehot Moment A Money View of Financial Globalization

Shadow Banking, Central Banking, and the Future of Global Finance Perry Mehrling Shadow Banking: A European Perspective City University London Feb 2, 2013 A Bagehot Moment A Money View of Financial Globalization

Liquidity and Solvency Risks

Liquidity and Solvency Risks Armin Eder a Falko Fecht b Thilo Pausch c a Universität Innsbruck, b European Business School, c Deutsche Bundesbank WebEx-Presentation February 25, 2011 Eder, Fecht, Pausch

Liquidity and Solvency Risks Armin Eder a Falko Fecht b Thilo Pausch c a Universität Innsbruck, b European Business School, c Deutsche Bundesbank WebEx-Presentation February 25, 2011 Eder, Fecht, Pausch

Basel III as Anchor for Financial Regulation Is it Adequate, Feasible and Appropriate? Developed and Developing Countries Perspectives

Macroeconomic management and financial regulation in core countries and the periphery Workshop Organised by CAFRAL, Levy and IDEAs New Delhi, 6-10 January, 2014 Basel III as Anchor for Financial Regulation

Macroeconomic management and financial regulation in core countries and the periphery Workshop Organised by CAFRAL, Levy and IDEAs New Delhi, 6-10 January, 2014 Basel III as Anchor for Financial Regulation

Public Finance Limited

Semi-annual Disclosures For the period ended 30 June 2018 (Solo Basis and Unaudited) Table of contents Template KM1: Key prudential ratios.... 1 Template OV1: Overview of RWA... 3 Template CC1: Composition

Semi-annual Disclosures For the period ended 30 June 2018 (Solo Basis and Unaudited) Table of contents Template KM1: Key prudential ratios.... 1 Template OV1: Overview of RWA... 3 Template CC1: Composition

Design of Con+ngent Capital With Market Trigger for Conversion

Design of Con+ngent Capital With Market Trigger for Conversion Suresh Sundaresan Columbia University Zhenyu Wang Federal Reserve Bank of New York The views expressed in this presenta+on are those of the

Design of Con+ngent Capital With Market Trigger for Conversion Suresh Sundaresan Columbia University Zhenyu Wang Federal Reserve Bank of New York The views expressed in this presenta+on are those of the

Stylized Financial System

Procyclicality and Capital Flows: Emerging Market Perspective Hyun Song Shin Bank of Thailand International Symposium 2010: Challenges to Central Banks in the Era of the New Globalization October 14 15,

Procyclicality and Capital Flows: Emerging Market Perspective Hyun Song Shin Bank of Thailand International Symposium 2010: Challenges to Central Banks in the Era of the New Globalization October 14 15,

The Federal Reserve in the 21st Century Financial Stability Policies

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

as at 30 June 2016 Basel 3 common disclosure templates

as at 30 June 2016 Basel 3 common disclosure templates INTRODUCTION In accordance with Section 6(6) of the s Act and Basel III, the n Reserve issued directives impacting the group s Pillar 3 disclosures.

as at 30 June 2016 Basel 3 common disclosure templates INTRODUCTION In accordance with Section 6(6) of the s Act and Basel III, the n Reserve issued directives impacting the group s Pillar 3 disclosures.

RISK DISCLOSURE STATEMENT FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED LONDON BRANCH

RISK DISCLOSURE STATEMENT FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED LONDON BRANCH DECEMBER 2017 1. IMPORTANT INFORMATION This Risk Disclosure

RISK DISCLOSURE STATEMENT FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED LONDON BRANCH DECEMBER 2017 1. IMPORTANT INFORMATION This Risk Disclosure

Liquidity Coverage Ratio Disclosure. Bank AlBilad Liquidity Coverage Ratio Disclosure Dec 31, 2015

Bank AlBilad Liquidity Coverage Ratio Disclosure Dec 31, 2015 1 I. LIQUIDITY COVERAGE RATIO (LCR): QUANTITATIVE DISCLOSURE Date: 31 Dec 2015 LCR Common Disclosure Template (In SR 000`s) Total UNWEIGHTED

Bank AlBilad Liquidity Coverage Ratio Disclosure Dec 31, 2015 1 I. LIQUIDITY COVERAGE RATIO (LCR): QUANTITATIVE DISCLOSURE Date: 31 Dec 2015 LCR Common Disclosure Template (In SR 000`s) Total UNWEIGHTED

CoCos, Bail-In, and Tail Risk

CoCos, Bail-In, and Tail Risk Paul Glasserman Columbia Business School and U.S. Office of Financial Research Joint work with Nan Chen and Behzad Nouri Bank Structure Conference Federal Reserve Bank of

CoCos, Bail-In, and Tail Risk Paul Glasserman Columbia Business School and U.S. Office of Financial Research Joint work with Nan Chen and Behzad Nouri Bank Structure Conference Federal Reserve Bank of

Basel III Pillar 3 Disclosures Report. For the Quarterly Period Ended December 31, 2015

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended December 31, 2015 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy...

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended December 31, 2015 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy...

TABLE 2: CAPITAL STRUCTURE - September 30, 2017

Frequency : Quarterly Location : Quarterly Financial Statement TABLE 2: CAPITAL STRUCTURE September 30, 2017 Balance sheet Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published

Frequency : Quarterly Location : Quarterly Financial Statement TABLE 2: CAPITAL STRUCTURE September 30, 2017 Balance sheet Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published

Presentation at Morgan Stanley European Financials Conference

Presentation at Morgan Stanley European Financials Conference David Mathers, Chief Financial Officer London, March 30th, 2011 Cautionary statement Cautionary statement regarding forward-looking and non-gaap

Presentation at Morgan Stanley European Financials Conference David Mathers, Chief Financial Officer London, March 30th, 2011 Cautionary statement Cautionary statement regarding forward-looking and non-gaap

The Crisis and Beyond: Financial Sector Policies. Asli Demirguc-Kunt The World Bank May 2011

The Crisis and Beyond: Financial Sector Policies Asli Demirguc-Kunt The World Bank May 2011 Financial crisis crisis of confidence in policies The global crisis and the response to the crisis extensive

The Crisis and Beyond: Financial Sector Policies Asli Demirguc-Kunt The World Bank May 2011 Financial crisis crisis of confidence in policies The global crisis and the response to the crisis extensive

Do Low Interest Rates Sow the Seeds of Financial Crises?

Do Low nterest Rates Sow the Seeds of Financial Crises? Simona Cociuba, University of Western Ontario Malik Shukayev, Bank of Canada Alexander Ueberfeldt, Bank of Canada Second Boston University-Boston

Do Low nterest Rates Sow the Seeds of Financial Crises? Simona Cociuba, University of Western Ontario Malik Shukayev, Bank of Canada Alexander Ueberfeldt, Bank of Canada Second Boston University-Boston

Capital Adequacy and Liquidity in Banking Dynamics

Capital Adequacy and Liquidity in Banking Dynamics Jin Cao Lorán Chollete October 9, 2014 Abstract We present a framework for modelling optimum capital adequacy in a dynamic banking context. We combine

Capital Adequacy and Liquidity in Banking Dynamics Jin Cao Lorán Chollete October 9, 2014 Abstract We present a framework for modelling optimum capital adequacy in a dynamic banking context. We combine

Back to the Business of Banking. Thomas M. Hoenig President Federal Reserve Bank of Kansas City

Back to the Business of Banking Thomas M. Hoenig President Federal Reserve Bank of Kansas City 29th Annual Monetary and Trade Conference Global Interdependence Center and Drexel University LeBow College

Back to the Business of Banking Thomas M. Hoenig President Federal Reserve Bank of Kansas City 29th Annual Monetary and Trade Conference Global Interdependence Center and Drexel University LeBow College

Market Impact of TLAC Requirements. FIG DCM Bank Capital Solutions

Market Impact of TLAC Requirements FIG DCM Bank Capital Solutions December 17, 2015 RWA vs. SLR Driven TLAC Requirements Fed's SLR driven TLAC requirement is more stringent than FSB TLAC framework 25%

Market Impact of TLAC Requirements FIG DCM Bank Capital Solutions December 17, 2015 RWA vs. SLR Driven TLAC Requirements Fed's SLR driven TLAC requirement is more stringent than FSB TLAC framework 25%

Risk amplification mechanisms in the financial system Rama CONT

Risk amplification mechanisms in the financial system Rama CONT Stress testing and risk modeling: micro to macro 1. Microprudential stress testing: -exogenous shocks applied to bank portfolio to assess

Risk amplification mechanisms in the financial system Rama CONT Stress testing and risk modeling: micro to macro 1. Microprudential stress testing: -exogenous shocks applied to bank portfolio to assess