Are Banks Special? International Risk Management Conference. IRMC2015 Luxembourg, June 15

|

|

|

- Meryl Russell

- 6 years ago

- Views:

Transcription

1 Are Banks Special? International Risk Management Conference IRMC2015 Luxembourg, June 15 Michel Crouhy Natixis Wholesale Banking and Dan Galai The Hebrew University and Sarnat School of Management

2 Introduction Are banks so special that they can justify financing themselves mainly with debt? Prior to the crisis the risk-based capital ratio of banks fell as low as 1 to 3% The GFC unveiled the vulnerability of banks. Excessive borrowing of banks was identified as a major factor in the crisis. Three effects seem to have been responsible for the global impact of the GFC: First, when one institution s asset sales depressed prices, other institutions were also affected because of their holdings of these assets. Second, because banks had little capital, solvency concerns arose with rising fear of contagion. Third, since much of the borrowing by banks was in the form of short-term debt, liquidy dried out and precipitated the collapse of banks like Bear Stearns and Lehman. As a result, regulators took steps with Basel 2.5, Basel III and Dodd-Frank to strengthen capital requirements of banks, especially systemic banks.

3 Introduction Are banks special firms that they can only achieve their goals with high leverage, above and beyond what is considered acceptable for an industrial corporation? If we accept Modigliani-Miller (M&M) proposition (1958) then the capital structure is irrelevant for both the cost of capital and the value of the bank. Hence, we ask the question: whether banks are special firms such that M&M Proposition I does not apply to bank? 3

4 Introduction Are banks special because of the services they provide to the economy? Should banks be subsidized in order for these services to be supplied in the right quantity? Is a subsidy in the form of government insurance efficient? Liquidity and payment services: banks channel people s savings into credit for economic investment. Depositors, samll businesses and other borrowers are not equipped to monitor their banks and ensure that they remain trustworthy. So there is an essential role for public regulation of banks to maintain stable trust in channels of credit that are vital for the economy. Banks are engaged into maturity transformation to reconcile the needs of the depositors and the corporates with long-term financing needs. Governments are, implicitly or explicitly, insuring banks creditors, then increasing leverage can increase the value of this government insurance at the expense of the tax-payers. 4

5 Introduction Information processing: people lend their savings to banks for investment because banks have better information about how to find good investments. Managing risks: banks have the expertise and tools to help investors and corporations to hedge their risks. A smooth functioning of the economy then requires a stable banking system: solvency of banks and trust in the financial health of the banks is critical. 5

6 Basel I Basel regulation of banks on a global basis started with the publication of Basel I in 1988 to be implemented from January Basel I dealt with minimum capital requirements against credit risk. It introduced the concept of Risk Weighted Assets (RWAs), against which banks were required to hold at least 8% capital. Basel I also introduced the concept of Tier 1, 2 and 3 of capital, where only Tier 1 fits the classical, strict definition of equity. In practice, in many banks before the GFC classical equity amounted to 1-3% only of RWAs. 6

7 Basel III New Basel III capital requirements call for a minimum of 7 % common equity capital to riskweighted assets. Basel III requires also a backstop 3 % leverage ratio, defined as common equity to total assets, or more precisely total exposure taking into account off-balance sheet derivatives. Risk-weighting is a complex system in which some assets count less against capital requirements than others. For example, a dollar of residential mortgage might count as 50 cents, but it might count as 10 cents if it is a complex mortgagebacked security, and zero if it is government debt. 7

8 Definition of Capital Tier 1 capital: tangible common equity and retained earnings and other instruments such as CoCos that have a loss absorbing capacity on a going concern basis. Tier 2 capital will typically consist of subordinated debt and contingent convertible capital, such as CoCo bonds. It will continue to provide loss absorption on a gone concern basis, i.e., following insolvency and upon liquidation. Tier 3 capital, or sub-supplementary capital, consisted of short-term subordinated debt with an original maturity of at least two years. It had to be unsecured and fully paid up. (Not anymore under Basel III) 8

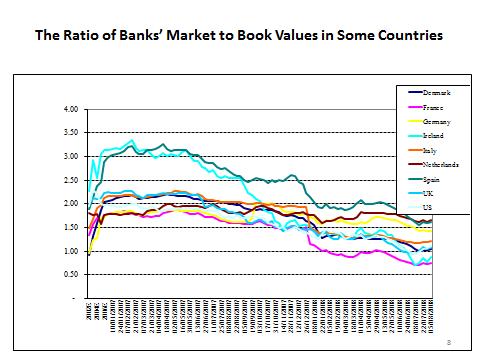

9 II. Conflicting Views on the Appropriate Leverage Ratio in Banking Shortcomings of capital regulation: Basel definition of capital is based on accounting equity (calculations based on book values) Does it provide a good enough indication of the solvency of the bank? Before the GFC market values were twice the accounting values and after the crisis it was the other way around for many banks: which information to trust more in order to assess the risk of insolvency? Financial theory is based on PCM and market values. What is the rational to regulate banks capital (doesn t exist for other non-financial firms)? 9

10

11 II. Conflicting Views on the Appropriate Leverage Ratio in Banking Empirical Evidence on Leverage in Banking: Gropp and Heider (2010) The same economic factors affect the differences in leverage ratios of banks as well as non-bank corporations in the US and Europe. Deposit insurance and capital regulation considerations " were of second order importance in determining the capital structure of large U.S. and European banks during 1991 to 2004." the increase in leverage in the sample period stemmed from nondeposit liabilities. Berg and Gider (2014) though banks have much larger leverage ratios (86%) than nonbank corporations (49%), they have much lower volatility on their assets (5.0% compared to 25.1% ). 11

12 II. Conflicting Views on the Appropriate Leverage Ratio in Banking Shortcomings of capital regulation: Current capital regulatory framework has become too complex, too costly to operate and to supervise, and not very transparent (Haldane The dog and the frisbee; Admati and Hellwig The banker new clothes) : Investors and supervisors have lost confidence in the calculation of RWAs: becomes harder and harder to relate regulatory capital to balance sheet risks. An alternative to current regulation would be to raise capital to 20% or more. Recent empirical research supports this view: Haldane (2012) : the leverage ratio is a statistically significant predictor of bank failure, while Tier 1 risk-based ratios are not. Blundell Wignall and Roulet (2012): same conclusion. Kapan and Minoiu (2013): better capitalized banks decreased their supply of credit less than other banks. 12

13 II. Conflicting Views on the Appropriate Leverage Ratio in Banking Bankers arguments against more capital: Equity capital is expensive because shareholders require higher returns on capital than debt holders. More capital will force banks to charge higher interest rates on loans and restrict banks ability to finance the economy. But why non-financial firms borrowing represents less than 50% of assets? Why successful companies like Apple do not borrow at all? 13

14 II. Conflicting Views on the Appropriate Leverage Ratio in Banking Bankers arguments against more capital: Banks have to generate a minimum ROE that won t be achievable with higher equity capital: banks will miss opportunities that would be attractive if they could fund themselves with more debt. Myers-Majluf effect: managers will be more likely to issue new equity when they have adverse private information suggesting that the market has over-valued the stock of the company. The public may take a firm s decision to issue new equity as bad news that will have a negative impact on the stock price. This effect can indeed make equity financing more expensive. But this effect would not apply if the regulator requires transparent public information. 14

15 II. Conflicting Views on the Appropriate Leverage Ratio in Banking Why these arguments are false? Crouhy and Galai (1986, 1991) and Admati and Hellwig (2013) More equity reduces the ability of banks to lend money: Bank capital is not a cash reserve: both debt and equity can be used to make loans and other investments. Capital and reserves are on different sides of the balance sheet: reserve requirements restrict how banks use their funds. Crouhy and Galai (1991) analyze the trade-off between equity and cash reserves. 15

16 II. Conflicting Views on the Appropriate Leverage Ratio in Banking Why these arguments are false? Crouhy and Galai (1986, 1991) and Admati and Hellwig (2013) Equity is expensive because shareholders require higher returns than debt holders: Required rates of return on debt and equity are not fixed and depend on the risk of the assets. But the overall cost of capital is not expected to change with the capital ratio under the PCM assumption and no tax advantage. The cost of debt and equity cannot be considered in isolation with out referring to the debt-equity mix. According to M&M (1958) a change in the funding mix that does not affect the total risk of the investment cannot have any effect on the overall funding costs. Any impact on the funding costs is only due to deviations from the M&M framework: the fact that using a different mix may impact taxes, the subsidies banks receive or their investment decision. 16

17 II. Conflicting Views on the Appropriate Leverage Ratio in Banking Why these arguments are false? Crouhy and Galai (1986, 1991) and Admati and Hellwig (2013) Banks have to generate a minimum ROE that won t be achievable if they have to increase capital. ROE is not fixed to say 15%. It depends on the firm s leverage: the required ROE should be lower when there is more capital in the funding mix. M&M Proposition II shows that the expected cost of equity increases as a linear function of leverage to fully compensate shareholders for the additional financial risk. But the cost of equity will also increase as a function of the business risk for any given leverage ratio. Hence the ROE is not a good ex-ante measure of performance: it may lead to wrong incentives for managers with bonuses related to ROE. 17

18 III. Why Banks are Different? Banks are different because they benefit from subsidies and from underpriced guarantees that make M&M propositions irrelevant: Since the GFC, U.S. banks have been able to borrow at close to zero interest rates from the FED and invest in U.S. Government bonds that are perfectly safe and pay 2% Banks can count on being bailed out by the government when they cannot pay back their debt. Then creditors do not worry much about banks defaulting and are willing to lend them for lower interest rates. The costs of bank borrowing is then partly borne by taxpayers. Underpriced deposits insurance is also an incentive for banks to take on more risk through higher leverage and more risky investments.

19 IV. The Contingent Claim Approach (CCA) Crouhy and Galai (1986, 1991) proposed a Contingent Claim Approach (CCA) under the assumption of PCM: Loans originated by a bank should be priced based on the credit standing of the obligor and is independent of the capital structure of the bank. The causality is such that once the loan portfolio of the bank is determined and the bank has raised equity capital, then depositors in an unregulated environment will ask for a return on their deposits that will reflect the risk to which they are exposed. If not fairly compensated, depositors will leave the bank. Banks failed in the past for lack of liquidity rather than shortage of capital: some of these claims change in a regulated environment.

20 IV. The Contingent Claim Approach (CCA) The problem faced by the bank is the rolling, or refinancing, of deposits since deposits can be withdrawn any time on demand: In the 1991 paper we model this liquidity issue and show how in an unregulated environment depositors, to keep their deposits in the bank, require a return on their deposits that fully compensates them for the credit risk they face: it is a function of α, β and σ (volatility of the rate of return on the risky assets V t )

21 IV. The Contingent Claim Approach (CCA) The CCA is helpful to analyze the distortive effects of bank regulation and free subsidies and guarantees that benefit the banks and make banks special with regard to non-financial firms. 1. If deposits β are guaranteed and deposit insurance is underpriced, there is an incentive for the bank to shift away to the insurer more credit risk by lowering the amount of equity financing α. If deposits are not insured, the equilibrium rate of interest paid by the bank on deposits should compensate depositors for the risk of default:

22 IV. The Contingent Claim Approach (CCA) Equilibrium relationship between the equity ratio α and the required interest rate on deposits, r 0 This figure shows that when regulators try to control at the same time the capital Ratio of the bank and impose an interest rate ceiling on the interest paid on deposits, one of the constraints become ineffective.

23 IV. The Contingent Claim Approach (CCA) Optimal insurance premium required by the FDIC to insure deposits G is the cost of insuring 1 $ of deposits paid at time 0 by the shareholders: S 0 = α + (1 α) g This condition ensures that both equity and the insurance premium are fairly priced. A value of α below its equilibrium value α* means that there is a wealth transfer from the FDIC to the shareholders. There is therfore an incentive for the bank to increase leverage since the FDIC subsidizes equity holders.

24 IV. The Contingent Claim Approach (CCA) The CCA is helpful to analyze the distortive effects of bank regulation and free subsidies and guarantees that benefit the banks and make banks special with regard to non-financial firms. If depositors and lenders know the government will step in if the bank defaults, credit risk is then shifted to the tax payers. In this situation banks are incentivized to increase their leverage without depositors asking to be compensated for the increased risk of default. These free subsidies and guarantees have led depositors to be less concerned, or not concerned at all, by the risk of default of the bank.

25 The Contingent Claim Approach (CCA) Another facet of the situation that deposits are considered by depositors to be risk-free, is the uncertainty on the amount of funding provided by depositors that is inherent to the contract between depositors and the banks that allow depositors to withdraw any amount of their deposits on demand. This is a situation quite different than the one faced by non-financial firms. This uncertainty on the sources of funding means that the investment decisions of a bank cannot be assumed as given and known as required in M&M propositions.

26 Conclusion If M&M propositions are irrelevant for banks it is not because of the tax argument: Banks have more interest income on their loans than interest expenses. For banks interest expenses are like any production cost for an industrial firm. Hence, the tax effect is irrelevant for banks. It is due primarily to: the explicit and implicit guarantees that are underpriced or not priced at all: banks can borrow at low interest rates with little capital. Bank default risk becomes a public problem, then the requirement that banks should have adequate equity; The uncertainty on the size of the banks and investment portfolio.

Why Bank Equity is Not Expensive

Why Bank Equity is Not Expensive Anat Admati Finance Watch Finance and Society Conference March 27, 2012 Beware: Confusing Jargon! Hold or set aside suggests capital is the same as idle reserves. This

Why Bank Equity is Not Expensive Anat Admati Finance Watch Finance and Society Conference March 27, 2012 Beware: Confusing Jargon! Hold or set aside suggests capital is the same as idle reserves. This

Safe to Fail? Client Alert December 5, 2014

Client Alert December 5, 2014 Safe to Fail? On 10 November 2014, the Financial Stability Board (FSB) launched a consultation 1 on the adequacy of the lossabsorbing capacity of global systemically important

Client Alert December 5, 2014 Safe to Fail? On 10 November 2014, the Financial Stability Board (FSB) launched a consultation 1 on the adequacy of the lossabsorbing capacity of global systemically important

Chapter Fourteen. Chapter 10 Regulating the Financial System 5/6/2018. Financial Crisis

Chapter Fourteen Chapter 10 Regulating the Financial System Financial Crisis Disruptions to financial systems are frequent and widespread around the world. Why? Financial systems are fragile and vulnerable

Chapter Fourteen Chapter 10 Regulating the Financial System Financial Crisis Disruptions to financial systems are frequent and widespread around the world. Why? Financial systems are fragile and vulnerable

How Curb Risk In Wall Street. Luigi Zingales. University of Chicago

How Curb Risk In Wall Street Luigi Zingales University of Chicago Banks Instability Banks are engaged in a transformation of maturity: borrow short term lend long term This transformation is socially valuable

How Curb Risk In Wall Street Luigi Zingales University of Chicago Banks Instability Banks are engaged in a transformation of maturity: borrow short term lend long term This transformation is socially valuable

Financial and Banking Regulation in the Aftermath of the Financial Crisis

Financial and Banking Regulation in the Aftermath of the Financial Crisis ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 12 Readings Text: Mishkin Ch. 10; Mishkin

Financial and Banking Regulation in the Aftermath of the Financial Crisis ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 12 Readings Text: Mishkin Ch. 10; Mishkin

Financial Institution Leverage: Some Notes. Kevin Davis. Department of Finance, University of Melbourne. and

Financial Institution Leverage: Some Notes Kevin Davis Department of Finance, University of Melbourne and Australian Centre for Financial Studies and Monash University Background and Summary 14 February

Financial Institution Leverage: Some Notes Kevin Davis Department of Finance, University of Melbourne and Australian Centre for Financial Studies and Monash University Background and Summary 14 February

Principles of Banking (II): Microeconomics of Banking (3) Bank Capital

: Microeconomics of Banking (3) Bank Capital") Principles of Banking (II): Microeconomics of Banking (3) Bank Capital Jin Cao (Norges Bank Research, Oslo & CESifo, München) Outline 1 2 3 Disclaimer (If they care about what I say,) the views expressed

Principles of Banking (II): Microeconomics of Banking (3) Bank Capital Jin Cao (Norges Bank Research, Oslo & CESifo, München) Outline 1 2 3 Disclaimer (If they care about what I say,) the views expressed

The Trouble with Bail-in : Pillar 2

The Trouble with Bail-in : Pillar 2 Mark J. Flannery Prepared for a conference on Achieving Financial Stability: Challenges to Prudential Regulation Federal Reserve Bank of Chicago November 4, 2016 1 The

The Trouble with Bail-in : Pillar 2 Mark J. Flannery Prepared for a conference on Achieving Financial Stability: Challenges to Prudential Regulation Federal Reserve Bank of Chicago November 4, 2016 1 The

Banking reform in Britain

Banking reform in Britain John Vickers All Souls College, Oxford University Hoover Institution, Stanford University 21 March 2017 Relative sizes of banking sectors Big hit to UK economy from the crisis

Banking reform in Britain John Vickers All Souls College, Oxford University Hoover Institution, Stanford University 21 March 2017 Relative sizes of banking sectors Big hit to UK economy from the crisis

Financial Crises and Regulatory Responses. Bank Regulation: I) The Liability side of the Balance Sheet II) The Asset side of the Balance Sheet

The Liability side of the Balance Sheet II) The Asset side of the Balance Sheet") Financial Crises and Regulatory Responses Bank Regulation: I) The Liability side of the Balance Sheet II) The Asset side of the Balance Sheet Higher Equity Capital Requirements Admati, DeMarzo, Hellwig

Financial Crises and Regulatory Responses Bank Regulation: I) The Liability side of the Balance Sheet II) The Asset side of the Balance Sheet Higher Equity Capital Requirements Admati, DeMarzo, Hellwig

An Evaluation of Money Market Fund Reform Proposals

An Evaluation of Money Market Fund Reform Proposals Sam Hanson David Scharfstein Adi Sunderam Harvard University May 2014 Introduction The financial crisis revealed significant vulnerabilities of the global

An Evaluation of Money Market Fund Reform Proposals Sam Hanson David Scharfstein Adi Sunderam Harvard University May 2014 Introduction The financial crisis revealed significant vulnerabilities of the global

Key high-level comments by Nordea Bank AB (publ) on reforming the structure of the EU banking sector

on reforming the structure of the EU banking sector") 1 (8) Page To European Commission Email: MARKT-HLEG@ec.europa.eu Document title response to Consultation on the recommendations of the High-level Expert Group on Reforming the structure of the EU banking

1 (8) Page To European Commission Email: MARKT-HLEG@ec.europa.eu Document title response to Consultation on the recommendations of the High-level Expert Group on Reforming the structure of the EU banking

For further questions, please contact Paulina Przewoska, senior policy analyst at Finance Watch.

Finance Watch response to FSB s consultation on Adequacy of Loss-Absorbing Capacity of Global Systemically Important Banks in resolution Brussels, 30 January 2015 Finance Watch is an independent, non-profit

Finance Watch response to FSB s consultation on Adequacy of Loss-Absorbing Capacity of Global Systemically Important Banks in resolution Brussels, 30 January 2015 Finance Watch is an independent, non-profit

Banking, Liquidity Transformation, and Bank Runs

Banking, Liquidity Transformation, and Bank Runs ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 30 Readings GLS Ch. 28 GLS Ch. 30 (don t worry about model

Banking, Liquidity Transformation, and Bank Runs ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 30 Readings GLS Ch. 28 GLS Ch. 30 (don t worry about model

The Banking Crisis and Its Regulatory Response in Europe

The Banking Crisis and Its Regulatory Response in Europe Mathias Dewatripont National Bank of Belgium and Single Supervisory Mechanism Bruegel 10 th Anniversary Conference at NBB January 28, 2016 Outline

The Banking Crisis and Its Regulatory Response in Europe Mathias Dewatripont National Bank of Belgium and Single Supervisory Mechanism Bruegel 10 th Anniversary Conference at NBB January 28, 2016 Outline

Macroprudential Bank Capital Regulation in a Competitive Financial System

Macroprudential Bank Capital Regulation in a Competitive Financial System Milton Harris, Christian Opp, Marcus Opp Chicago, UPenn, University of California Fall 2015 H 2 O (Chicago, UPenn, UC) Macroprudential

Macroprudential Bank Capital Regulation in a Competitive Financial System Milton Harris, Christian Opp, Marcus Opp Chicago, UPenn, University of California Fall 2015 H 2 O (Chicago, UPenn, UC) Macroprudential

Revised Basel III Leverage Ratio Framework and Disclosure Requirements 1

1 Revised Basel III Leverage Ratio Framework and Disclosure Requirements 1 Marianne Ojo 2 In view of the revisions relating to the denominator component of the Basel III Leverage Ratio such proposals having

1 Revised Basel III Leverage Ratio Framework and Disclosure Requirements 1 Marianne Ojo 2 In view of the revisions relating to the denominator component of the Basel III Leverage Ratio such proposals having

Shortcomings of Leverage Ratio Requirements

Shortcomings of Leverage Ratio Requirements August 2016 Shortcomings of Leverage Ratio Requirements For large U.S. banks, the leverage ratio requirement is now so high relative to risk-based capital requirements

Shortcomings of Leverage Ratio Requirements August 2016 Shortcomings of Leverage Ratio Requirements For large U.S. banks, the leverage ratio requirement is now so high relative to risk-based capital requirements

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

deposit insurance Financial intermediaries, banks, and bank runs

deposit insurance The purpose of deposit insurance is to ensure financial stability, as well as protect the interests of small investors. But with government guarantees in hand, bankers take excessive

deposit insurance The purpose of deposit insurance is to ensure financial stability, as well as protect the interests of small investors. But with government guarantees in hand, bankers take excessive

The following section discusses our responses to specific questions.

February 2, 2015 Comments on the Financial Stability Board s Consultative Document Adequacy of loss-absorbing capacity of global systemically important banks in resolution Japanese Bankers Association

February 2, 2015 Comments on the Financial Stability Board s Consultative Document Adequacy of loss-absorbing capacity of global systemically important banks in resolution Japanese Bankers Association

EC248-Financial Innovations and Monetary Policy Assignment. Andrew Townsend

EC248-Financial Innovations and Monetary Policy Assignment Discuss the concept of too big to fail within the financial sector. What are the arguments in favour of this concept, and what are possible negative

EC248-Financial Innovations and Monetary Policy Assignment Discuss the concept of too big to fail within the financial sector. What are the arguments in favour of this concept, and what are possible negative

The Federal Reserve in the 21st Century Financial Stability Policies

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

Globalisation and the limits on national capital adequacy policies a small country perspective

Globalisation and the limits on national capital adequacy policies a small country perspective Presentation to the 14 th Melbourne Money and Finance Conference Ian Harrison, Special Adviser, Reserve Bank

Globalisation and the limits on national capital adequacy policies a small country perspective Presentation to the 14 th Melbourne Money and Finance Conference Ian Harrison, Special Adviser, Reserve Bank

Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015

Instructor: Prof. Menzie Chinn UW Madison Fall 2015") Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015 14 2 14 3 The Sources and Consequences of Runs, Panics, and Crises Banks fragility arises from the fact

Economics 435 The Financial System (10/28/2015) Instructor: Prof. Menzie Chinn UW Madison Fall 2015 14 2 14 3 The Sources and Consequences of Runs, Panics, and Crises Banks fragility arises from the fact

THE FUNDING OF RESOLUTION. David G Mayes University of Auckland

THE FUNDING OF RESOLUTION David G Mayes University of Auckland THE RESEARCH QUESTION Who is likely to pay for bank resolution under the BRRD? Does this meet the objective of minimising the impact of bank

THE FUNDING OF RESOLUTION David G Mayes University of Auckland THE RESEARCH QUESTION Who is likely to pay for bank resolution under the BRRD? Does this meet the objective of minimising the impact of bank

14. What Use Can Be Made of the Specific FSIs?

14. What Use Can Be Made of the Specific FSIs? Introduction 14.1 The previous chapter explained the need for FSIs and how they fit into the wider concept of macroprudential analysis. This chapter considers

14. What Use Can Be Made of the Specific FSIs? Introduction 14.1 The previous chapter explained the need for FSIs and how they fit into the wider concept of macroprudential analysis. This chapter considers

Keeping Capital Adequate

Keeping Capital Adequate Mark J. Flannery University of Florida Prepared for the Nykredit Symposium 2010, Financial Stability and Future Financial Regulation, December 13, 2010. 1 25 Figure 1: Market and

Keeping Capital Adequate Mark J. Flannery University of Florida Prepared for the Nykredit Symposium 2010, Financial Stability and Future Financial Regulation, December 13, 2010. 1 25 Figure 1: Market and

The False Tradeoff between Economic Growth and Bank Capital

The False Tradeoff between Economic Growth and Bank Capital Anat R. Admati Stanford University June 22, 2011 The Purported Tradeoff More equity might increase the stability of banks. At the same time,

The False Tradeoff between Economic Growth and Bank Capital Anat R. Admati Stanford University June 22, 2011 The Purported Tradeoff More equity might increase the stability of banks. At the same time,

Chapter E: The US versus EU resolution regime

Chapter E: The US versus EU resolution regime 1. Introduction Resolution frameworks should always seek two objectives. First, resolving banks should be a quick process and must avoid negative spill over

Chapter E: The US versus EU resolution regime 1. Introduction Resolution frameworks should always seek two objectives. First, resolving banks should be a quick process and must avoid negative spill over

The lender of last resort: liquidity provision versus the possibility of bail-out

The lender of last resort: liquidity provision versus the possibility of bail-out Rob Nijskens Sylvester C.W. Eijffinger June 24, 2010 The lender of last resort: liquidity versus bail-out 1 /20 Motivation:

The lender of last resort: liquidity provision versus the possibility of bail-out Rob Nijskens Sylvester C.W. Eijffinger June 24, 2010 The lender of last resort: liquidity versus bail-out 1 /20 Motivation:

Re: Adequacy of loss-absorbing capacity of global systemically important banks in resolution - FSB Consultative Document

Financial Stability Board (FSB) Division Bank and Insurance Wiedner Hauptstraße 63 Postfach 320 1045 Wien T +43 (0)5 90 900-DW F +43 (0)5 90 900-272 E bsbv@wko.at W http://wko.at/bsbv Ihr Zeichen, Ihre

Financial Stability Board (FSB) Division Bank and Insurance Wiedner Hauptstraße 63 Postfach 320 1045 Wien T +43 (0)5 90 900-DW F +43 (0)5 90 900-272 E bsbv@wko.at W http://wko.at/bsbv Ihr Zeichen, Ihre

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

Economics and Finance,

Economics and Finance, 2014-15 Lecture 5 - Corporate finance under asymmetric information: Moral hazard and access to external finance Luca Deidda UNISS, DiSEA, CRENoS October 2014 Luca Deidda (UNISS,

Economics and Finance, 2014-15 Lecture 5 - Corporate finance under asymmetric information: Moral hazard and access to external finance Luca Deidda UNISS, DiSEA, CRENoS October 2014 Luca Deidda (UNISS,

2. If a bank meets a net deposit drain by borrowing money in the fed funds market it is using purchased liquidity.

Chapter 21: Managing Liquidity Risk on the Balance Sheet True/False 1. Large banks tend to rely more on purchased liquidity and small banks tend to rely more on stored liquidity. 2. If a bank meets a net

Chapter 21: Managing Liquidity Risk on the Balance Sheet True/False 1. Large banks tend to rely more on purchased liquidity and small banks tend to rely more on stored liquidity. 2. If a bank meets a net

Institutional Finance

Institutional Finance Lecture 09 : Banking and Maturity Mismatch Markus K. Brunnermeier Preceptor: Dong Beom Choi Princeton University 1 Select/monitor borrowers Sharpe (1990) Reduce asymmetric info idiosyncratic

Institutional Finance Lecture 09 : Banking and Maturity Mismatch Markus K. Brunnermeier Preceptor: Dong Beom Choi Princeton University 1 Select/monitor borrowers Sharpe (1990) Reduce asymmetric info idiosyncratic

Part C. Banks' Financial Reporting Lectures 6&7. Banks Balance Sheet (II)

") Part C. Banks' Financial Reporting Lectures 6&7. Banks Balance Sheet (II) Lecture 7 Outline 2 6.1. Banks' Assets 6.2. Banks' Liabilities 3 For bank liabilities, the ranking positions is reversed compared

Part C. Banks' Financial Reporting Lectures 6&7. Banks Balance Sheet (II) Lecture 7 Outline 2 6.1. Banks' Assets 6.2. Banks' Liabilities 3 For bank liabilities, the ranking positions is reversed compared

CoCos: A Promising Idea Poorly Executed

CoCos: A Promising Idea Poorly Executed Richard J. Herring herring@wharton.upenn.edu Wharton School 19 th Annual International Banking Conference Federal Reserve Bank of Chicago. November 2, 2016 1 Background

CoCos: A Promising Idea Poorly Executed Richard J. Herring herring@wharton.upenn.edu Wharton School 19 th Annual International Banking Conference Federal Reserve Bank of Chicago. November 2, 2016 1 Background

The Crisis and Beyond: Financial Sector Policies. Asli Demirguc-Kunt The World Bank May 2011

The Crisis and Beyond: Financial Sector Policies Asli Demirguc-Kunt The World Bank May 2011 Financial crisis crisis of confidence in policies The global crisis and the response to the crisis extensive

The Crisis and Beyond: Financial Sector Policies Asli Demirguc-Kunt The World Bank May 2011 Financial crisis crisis of confidence in policies The global crisis and the response to the crisis extensive

Statement by Adrian Blundell-Wignall and Paul Atkinson 1

German Bundestag Finance Committee Hearing on the Draft Bank-Separation Law (Drucksache 17/12601) 22 April 2013 Statement by Adrian Blundell-Wignall and Paul Atkinson 1 1 The authors are, respectively:

German Bundestag Finance Committee Hearing on the Draft Bank-Separation Law (Drucksache 17/12601) 22 April 2013 Statement by Adrian Blundell-Wignall and Paul Atkinson 1 1 The authors are, respectively:

Nobel Symposium Money and Banking

Nobel Symposium Money and Banking https://www.houseoffinance.se/nobel-symposium May 26-28, 2018 Clarion Hotel Sign, Stockholm MPI Collective Goods Martin Hellwig Discussion of Gorton s and Rajan s Presentations

Nobel Symposium Money and Banking https://www.houseoffinance.se/nobel-symposium May 26-28, 2018 Clarion Hotel Sign, Stockholm MPI Collective Goods Martin Hellwig Discussion of Gorton s and Rajan s Presentations

b. Financial innovation and/or financial liberalization (the elimination of restrictions on financial markets) can cause financial firms to go on a

can cause financial firms to go on a") Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

Financial Crises This lecture begins by examining the features of a financial crisis. It then describes the causes and consequences of the 2008 financial crisis and the resulting changes in financial regulations.

A Theory of Bank Liquidity Requirements

A Theory of Bank Liquidity Requirements Charles Calomiris Florian Heider Marie Hoerova Columbia GSB, SIPA ECB ECB Columbia SIPA February 9 th, 2018 The views expressed are solely those of the authors,

A Theory of Bank Liquidity Requirements Charles Calomiris Florian Heider Marie Hoerova Columbia GSB, SIPA ECB ECB Columbia SIPA February 9 th, 2018 The views expressed are solely those of the authors,

Banking reform five years on

Banking reform five years on John Vickers All Souls College, Oxford RPI Competition and Regulation Conference Oxford, 9 September 2013 Banking reform five years on: plan of talk How did it all go so wrong?

Banking reform five years on John Vickers All Souls College, Oxford RPI Competition and Regulation Conference Oxford, 9 September 2013 Banking reform five years on: plan of talk How did it all go so wrong?

International Money and Banking: 10. Incentive Problems in Banking

International Money and Banking: 10. Incentive Problems in Banking Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Incentive Problems in Banking Spring 2018 1 / 32 Why Do Banks Get Into

International Money and Banking: 10. Incentive Problems in Banking Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Incentive Problems in Banking Spring 2018 1 / 32 Why Do Banks Get Into

Do Increased Capital Requirements Lead to Higher Interest Margins? -A Study in the Swedish Banking Sector

Do Increased Capital Requirements Lead to Higher Interest Margins? -A Study in the Swedish Banking Sector Bachelor thesis in Financial Economics (15 credits) Department of Economics Lowe Rehnberg & Marcus

Do Increased Capital Requirements Lead to Higher Interest Margins? -A Study in the Swedish Banking Sector Bachelor thesis in Financial Economics (15 credits) Department of Economics Lowe Rehnberg & Marcus

Higher capital requirements for GSIBs: systemic risk vs. lending to the real economy

Higher capital requirements for GSIBs: systemic risk vs. lending to the real economy by Laurent Clerc 38 Higher capital requirements for GSIBs and Systemic risk: a. Are capital requirements for GSIBs an

Higher capital requirements for GSIBs: systemic risk vs. lending to the real economy by Laurent Clerc 38 Higher capital requirements for GSIBs and Systemic risk: a. Are capital requirements for GSIBs an

The Compelling Case for Stronger and More Effective Leverage Regulation in Banking

The Compelling Case for Stronger and More Effective Leverage Regulation in Banking Anat R. Admati * Graduate School of Business, Stanford University October 14, 2013 This Version September 30, 2014 Forthcoming,

The Compelling Case for Stronger and More Effective Leverage Regulation in Banking Anat R. Admati * Graduate School of Business, Stanford University October 14, 2013 This Version September 30, 2014 Forthcoming,

A Theory of Bank Liquidity Requirements

A Theory of Bank Liquidity Requirements Charles Calomiris Florian Heider Marie Hoerova Columbia GSB ECB ECB IAES Meetings Washington, D.C., October 15, 2016 The views expressed are solely those of the

A Theory of Bank Liquidity Requirements Charles Calomiris Florian Heider Marie Hoerova Columbia GSB ECB ECB IAES Meetings Washington, D.C., October 15, 2016 The views expressed are solely those of the

Simplicity and Complexity in Capital Regulation

EMBARGOED UNTIL Monday, Nov. 18, 2013, at 1 AM U.S. Eastern Time and 10 AM in Abu Dhabi, or upon delivery Simplicity and Complexity in Capital Regulation Eric S. Rosengren President & Chief Executive Officer

EMBARGOED UNTIL Monday, Nov. 18, 2013, at 1 AM U.S. Eastern Time and 10 AM in Abu Dhabi, or upon delivery Simplicity and Complexity in Capital Regulation Eric S. Rosengren President & Chief Executive Officer

Chapter 9. Banking and the Management of Financial Institutions. 9.1 The Bank Balance Sheet

Chapter 9 Banking and the Management of Financial Institutions 9.1 The Bank Balance Sheet 1) Which of the following statements are true? A) A bankʹs assets are its sources of funds. B) A bankʹs liabilities

Chapter 9 Banking and the Management of Financial Institutions 9.1 The Bank Balance Sheet 1) Which of the following statements are true? A) A bankʹs assets are its sources of funds. B) A bankʹs liabilities

Shadow Banking & the Financial Crisis

& the Financial Crisis April 24, 2013 & the Financial Crisis Table of contents 1 Backdrop A bit of history 2 3 & the Financial Crisis Origins Backdrop A bit of history Banks perform several vital roles

& the Financial Crisis April 24, 2013 & the Financial Crisis Table of contents 1 Backdrop A bit of history 2 3 & the Financial Crisis Origins Backdrop A bit of history Banks perform several vital roles

Basel III Between Global Thinking and Local Acting

Theoretical and Applied Economics Volume XIX (2012), No. 6(571), pp. 5-12 Basel III Between Global Thinking and Local Acting Vasile DEDU Bucharest Academy of Economic Studies vdedu03@yahoo.com Dan Costin

Theoretical and Applied Economics Volume XIX (2012), No. 6(571), pp. 5-12 Basel III Between Global Thinking and Local Acting Vasile DEDU Bucharest Academy of Economic Studies vdedu03@yahoo.com Dan Costin

SAFER. United States Senate Washington, DC May 14, 2010

ECONOMISTS' COMMITTEE FOR STABLE, ACCOUNTABLE, FAIR AND EFFICIENT FINANCIAL REFORM United States Senate Washington, DC 20510 May 14, 2010 Letter from Joseph Stiglitz re. Section 716: Prohibition Against

ECONOMISTS' COMMITTEE FOR STABLE, ACCOUNTABLE, FAIR AND EFFICIENT FINANCIAL REFORM United States Senate Washington, DC 20510 May 14, 2010 Letter from Joseph Stiglitz re. Section 716: Prohibition Against

EU Bank Capital Structure and Capital Requirements

LUND UNIVERSITY FACULTY OF ECONOMICS EU Bank Capital Structure and Capital Requirements What is the importance of CRD IV in determining bank leverage? Supervisor: Hossein Asgharian Spring 2011 Author:

LUND UNIVERSITY FACULTY OF ECONOMICS EU Bank Capital Structure and Capital Requirements What is the importance of CRD IV in determining bank leverage? Supervisor: Hossein Asgharian Spring 2011 Author:

Douglas W. Diamond and Raghuram G. Rajan

Fear of fire sales and credit freezes Douglas W. Diamond and Raghuram G. Rajan University of Chicago and NBER Motivation In the ongoing credit crisis arguments that Liquidity has dried up for certain categories

Fear of fire sales and credit freezes Douglas W. Diamond and Raghuram G. Rajan University of Chicago and NBER Motivation In the ongoing credit crisis arguments that Liquidity has dried up for certain categories

Chapter 02 Financial Services: Depository Institutions

Financial Institutions Management A Risk Management Approach 9th Edition Saunders Test Bank Full Download: http://testbanklive.com/download/financial-institutions-management-a-risk-management-approach-9th-edition-sau

Financial Institutions Management A Risk Management Approach 9th Edition Saunders Test Bank Full Download: http://testbanklive.com/download/financial-institutions-management-a-risk-management-approach-9th-edition-sau

Managing liquidity risk in a changed and global world

Managing liquidity risk in a changed and global world September 15 th, 2010 PwC Agenda 1) Introduction to Liquidity Risk and Monetary Policy 2) Liquidity Risk from a supranational regulatory perspective

Managing liquidity risk in a changed and global world September 15 th, 2010 PwC Agenda 1) Introduction to Liquidity Risk and Monetary Policy 2) Liquidity Risk from a supranational regulatory perspective

DODD-FRANK. November 14, 2012 SPONSORED BY MORTGAGE BANKERS OF THE BLUEGRASS

DODD-FRANK November 14, 2012 SPONSORED BY MORTGAGE BANKERS OF THE BLUEGRASS Agenda Objectives Dodd Frank Overview CFPB Mission and Initiatives Pending Legislation - Qualified Mortgages (QM) - Qualified

DODD-FRANK November 14, 2012 SPONSORED BY MORTGAGE BANKERS OF THE BLUEGRASS Agenda Objectives Dodd Frank Overview CFPB Mission and Initiatives Pending Legislation - Qualified Mortgages (QM) - Qualified

Competitive Advantage under the Basel II New Capital Requirement Regulations

Competitive Advantage under the Basel II New Capital Requirement Regulations I - Introduction: This paper has the objective of introducing the revised framework for International Convergence of Capital

Competitive Advantage under the Basel II New Capital Requirement Regulations I - Introduction: This paper has the objective of introducing the revised framework for International Convergence of Capital

Taxing Risk* Narayana Kocherlakota. President Federal Reserve Bank of Minneapolis. Economic Club of Minnesota. Minneapolis, Minnesota.

Taxing Risk* Narayana Kocherlakota President Federal Reserve Bank of Minneapolis Economic Club of Minnesota Minneapolis, Minnesota May 10, 2010 *This topic is discussed in greater depth in "Taxing Risk

Taxing Risk* Narayana Kocherlakota President Federal Reserve Bank of Minneapolis Economic Club of Minnesota Minneapolis, Minnesota May 10, 2010 *This topic is discussed in greater depth in "Taxing Risk

Answers to Questions: Chapter 5

Answers to Questions: Chapter 5 1. Figure 5-1 on page 123 shows that the output gaps fell by about the same amounts in Japan and Europe as it did in the United States from 2007-09. This is evidence that

Answers to Questions: Chapter 5 1. Figure 5-1 on page 123 shows that the output gaps fell by about the same amounts in Japan and Europe as it did in the United States from 2007-09. This is evidence that

Deposits and Bank Capital Structure

Deposits and Bank Capital Structure Franklin Allen 1 Elena Carletti 2 Robert Marquez 3 1 University of Pennsylvania 2 Bocconi University 3 UC Davis June 2014 Franklin Allen, Elena Carletti, Robert Marquez

Deposits and Bank Capital Structure Franklin Allen 1 Elena Carletti 2 Robert Marquez 3 1 University of Pennsylvania 2 Bocconi University 3 UC Davis June 2014 Franklin Allen, Elena Carletti, Robert Marquez

1-1. Chapter 1: Basic Concepts

TEST BANK 1-1 Chapter 1: Basic Concepts 1. Which of the following statements is (are) true? a. A risk-preferring individual always prefers the riskier of two gambles that involve different expected value.

TEST BANK 1-1 Chapter 1: Basic Concepts 1. Which of the following statements is (are) true? a. A risk-preferring individual always prefers the riskier of two gambles that involve different expected value.

Liquidity and capital: Substitutes or complements?

Marie Hoerova European Central Bank and CEPR Liquidity and capital: Substitutes or complements? Chicago Fed/ECB International Banking Conference November 3, 2016 The views expressed are those of the author

Marie Hoerova European Central Bank and CEPR Liquidity and capital: Substitutes or complements? Chicago Fed/ECB International Banking Conference November 3, 2016 The views expressed are those of the author

Repos and Bankruptcy Priority And Taxation, Tobin and Pigovian. Federal Reserve Bank of New York

Repos and Bankruptcy Priority And Taxation, Tobin and Pigovian Mark Roe Federal Reserve Bank of New York October 7, 2011 Source This talk is derived from and extends: Roe, 2011. The Derivatives Market

Repos and Bankruptcy Priority And Taxation, Tobin and Pigovian Mark Roe Federal Reserve Bank of New York October 7, 2011 Source This talk is derived from and extends: Roe, 2011. The Derivatives Market

The Evolving Complexity of Capital Regulation

The Evolving Complexity of Capital Regulation Richard J. Herring herring@wharton.upenn.edu Wharton School International Economic Association Washington, D.C. October 15, 2016 1 Overview ü How did capital

The Evolving Complexity of Capital Regulation Richard J. Herring herring@wharton.upenn.edu Wharton School International Economic Association Washington, D.C. October 15, 2016 1 Overview ü How did capital

Banking Regulation: The Risk of Migration to Shadow Banking

Banking Regulation: The Risk of Migration to Shadow Banking Sam Hanson Harvard University and NBER September 26, 2016 Micro- vs. Macro-prudential regulation Micro-prudential: Regulated banks should have

Banking Regulation: The Risk of Migration to Shadow Banking Sam Hanson Harvard University and NBER September 26, 2016 Micro- vs. Macro-prudential regulation Micro-prudential: Regulated banks should have

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 10 Banking and the Management of Financial Institutions

Chapter 10 Banking and the Management of Financial Institutions") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 10 Banking and the Management of Financial Institutions 10.1 The Bank Balance Sheet 1) Which of the following statements are true? A)

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 10 Banking and the Management of Financial Institutions 10.1 The Bank Balance Sheet 1) Which of the following statements are true? A)

ABI response to the FSB consultation on the adequacy of loss-absorbing capacity of global systemically important banks in resolution.

ABI response to the FSB consultation on the adequacy of loss-absorbing capacity of global systemically important banks in resolution 2 February 2015 POSITION PAPER 1/2015 The Italian Banking Association

ABI response to the FSB consultation on the adequacy of loss-absorbing capacity of global systemically important banks in resolution 2 February 2015 POSITION PAPER 1/2015 The Italian Banking Association

P2.T6. Credit Risk Measurement & Management. Michael Crouhy, Dan Galai and Robert Mark, The Essentials of Risk Management, 2nd Edition

P2.T6. Credit Risk Measurement & Management Michael Crouhy, Dan Galai and Robert Mark, The Essentials of Risk Management, 2nd Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com

P2.T6. Credit Risk Measurement & Management Michael Crouhy, Dan Galai and Robert Mark, The Essentials of Risk Management, 2nd Edition Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com

SUBMISSION BY THE BRITISH BANKERS ASSOCIATION. Introduction

SUBMISSION BY THE BRITISH BANKERS ASSOCIATION Introduction The British Bankers Association welcomes the opportunity to input to the inquiry by the Economy, Energy and Tourism Committee on the implications

SUBMISSION BY THE BRITISH BANKERS ASSOCIATION Introduction The British Bankers Association welcomes the opportunity to input to the inquiry by the Economy, Energy and Tourism Committee on the implications

Suggestions for the new version of the Astana Consensus

Suggestions for the new version of the Astana Consensus By Domingo Felipe Cavallo 1, May 7, 2012 This paper analyses in detail the first two of the five main priorities of the Mexican Presidency in G20

Suggestions for the new version of the Astana Consensus By Domingo Felipe Cavallo 1, May 7, 2012 This paper analyses in detail the first two of the five main priorities of the Mexican Presidency in G20

A Model with Costly Enforcement

A Model with Costly Enforcement Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) Costly-Enforcement December 25, 2012 1 / 43 A Model with Costly

A Model with Costly Enforcement Jesús Fernández-Villaverde University of Pennsylvania December 25, 2012 Jesús Fernández-Villaverde (PENN) Costly-Enforcement December 25, 2012 1 / 43 A Model with Costly

Managing Risk off the Balance Sheet with Derivative Securities

Managing Risk off the Balance Sheet Managing Risk off the Balance Sheet with Derivative Securities Managers are increasingly turning to off-balance-sheet (OBS) instruments such as forwards, futures, options,

Managing Risk off the Balance Sheet Managing Risk off the Balance Sheet with Derivative Securities Managers are increasingly turning to off-balance-sheet (OBS) instruments such as forwards, futures, options,

Bail-ins, Bank Resolution, and Financial Stability

, Bank Resolution, and Financial Stability NYU and ICL 29 November, 2014 Laws, says that illustrious rhymer Mr John Godfrey Saxe, like sausages, cease to inspire respect in proportion as we know how they

, Bank Resolution, and Financial Stability NYU and ICL 29 November, 2014 Laws, says that illustrious rhymer Mr John Godfrey Saxe, like sausages, cease to inspire respect in proportion as we know how they

Banking Regulation: An introduction. By A V Vedpuriswar

Banking Regulation: An introduction By A V Vedpuriswar June 27, 2018 Thus small depositors across the world are protected by deposit 1 insurance. Introduction(1) For all their prestige and high profile,

Banking Regulation: An introduction By A V Vedpuriswar June 27, 2018 Thus small depositors across the world are protected by deposit 1 insurance. Introduction(1) For all their prestige and high profile,

Rules versus discretion in bank resolution

Rules versus discretion in bank resolution Ansgar Walther (Oxford) Lucy White (HBS) May 2016 The post-crisis agenda Reducing the costs associated with failure of systemic banks: 1 Reduce probability of

Rules versus discretion in bank resolution Ansgar Walther (Oxford) Lucy White (HBS) May 2016 The post-crisis agenda Reducing the costs associated with failure of systemic banks: 1 Reduce probability of

Fannie, Freddie, and Housing Finance: What s It All About?

Fannie, Freddie, and Housing Finance: What s It All About? Lawrence J. White Stern School of Business New York University Lwhite@stern.nyu.edu Presentation to the Central Banking Seminar, Federal Reserve

Fannie, Freddie, and Housing Finance: What s It All About? Lawrence J. White Stern School of Business New York University Lwhite@stern.nyu.edu Presentation to the Central Banking Seminar, Federal Reserve

On the use of leverage caps in bank regulation

On the use of leverage caps in bank regulation Afrasiab Mirza Department of Economics University of Birmingham a.mirza@bham.ac.uk Frank Strobel Department of Economics University of Birmingham f.strobel@bham.ac.uk

On the use of leverage caps in bank regulation Afrasiab Mirza Department of Economics University of Birmingham a.mirza@bham.ac.uk Frank Strobel Department of Economics University of Birmingham f.strobel@bham.ac.uk

Introduction ( 1 ) The German Landesbanken cases a brief review CHIEF ECONOMIST SECTION

The German Landesbanken cases a brief review CHIEF ECONOMIST SECTION") Applying the Market Economy Investor Principle to State Owned Companies Lessons Learned from the German Landesbanken Cases Hans W. FRIEDERISZICK and Michael TRÖGE, Directorate-General Competition, Chief

Applying the Market Economy Investor Principle to State Owned Companies Lessons Learned from the German Landesbanken Cases Hans W. FRIEDERISZICK and Michael TRÖGE, Directorate-General Competition, Chief

16. Because of the large amount of equity on a typical commercial bank balance sheet, credit risk is not a significant risk to bank managers.

ch2 Student: 1. In recent years, the number of commercial banks in the U.S. has been increasing. 2. Most of the change in the number of commercial banks since 1990 has been due to bank failures. 3. Commercial

ch2 Student: 1. In recent years, the number of commercial banks in the U.S. has been increasing. 2. Most of the change in the number of commercial banks since 1990 has been due to bank failures. 3. Commercial

The Federal Reserve in the 21st Century Financial Stability Policies

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

The Federal Reserve in the 21st Century Financial Stability Policies Thomas Eisenbach, Research and Statistics Group Disclaimer The views expressed in the presentation are those of the speaker and are

Markus K. Brunnermeier

Markus K. Brunnermeier 1 Overview 1. Underlying mechanism Fire-sale externality + Liquidity spirals (due to maturity mismatch) Hoarding externality (interconnectedness) Runs 2. Crisis prevention Macro-prudential

Markus K. Brunnermeier 1 Overview 1. Underlying mechanism Fire-sale externality + Liquidity spirals (due to maturity mismatch) Hoarding externality (interconnectedness) Runs 2. Crisis prevention Macro-prudential

Update on Minneapolis Fed Ending Too Big to Fail Initiative. Neel Kashkari. President and CEO Federal Reserve Bank of Minneapolis

Update on Minneapolis Fed Ending Too Big to Fail Initiative Neel Kashkari President and CEO Federal Reserve Bank of Minneapolis Minneapolis, MN April 18, 2016 1 Update on Minneapolis Fed Ending Too Big

Update on Minneapolis Fed Ending Too Big to Fail Initiative Neel Kashkari President and CEO Federal Reserve Bank of Minneapolis Minneapolis, MN April 18, 2016 1 Update on Minneapolis Fed Ending Too Big

BERMUDA MONETARY AUTHORITY GUIDELINES ON STRESS TESTING FOR THE BERMUDA BANKING SECTOR

GUIDELINES ON STRESS TESTING FOR THE BERMUDA BANKING SECTOR TABLE OF CONTENTS 1. EXECUTIVE SUMMARY...2 2. GUIDANCE ON STRESS TESTING AND SCENARIO ANALYSIS...3 3. RISK APPETITE...6 4. MANAGEMENT ACTION...6

GUIDELINES ON STRESS TESTING FOR THE BERMUDA BANKING SECTOR TABLE OF CONTENTS 1. EXECUTIVE SUMMARY...2 2. GUIDANCE ON STRESS TESTING AND SCENARIO ANALYSIS...3 3. RISK APPETITE...6 4. MANAGEMENT ACTION...6

Optimal Capital Structure

Capital Structure Optimal Capital Structure What is capital structure? How should a firm choose a debt-toequity ratio? The goal: Which is done by: Which is done by: Financial Leverage Scenario A B C Market

Capital Structure Optimal Capital Structure What is capital structure? How should a firm choose a debt-toequity ratio? The goal: Which is done by: Which is done by: Financial Leverage Scenario A B C Market

A Proposal for the Resolution of Systemically Important Assets and Liabilities: The Case of the Repo Market

A Proposal for the Resolution of Systemically Important Assets and Liabilities: The Case of the Repo Market Viral V Acharya (NYU-Stern, CEPR and NBER) And T. Sabri Öncü (CAFRAL - Reserve Bank of India

A Proposal for the Resolution of Systemically Important Assets and Liabilities: The Case of the Repo Market Viral V Acharya (NYU-Stern, CEPR and NBER) And T. Sabri Öncü (CAFRAL - Reserve Bank of India

Fluctuations in the economy s output. 1. Three Components of Investment

ECON 3560/5040 INVESTMENT - Investment is the most volatile component of GDP Fluctuations in the economy s output - Why is investment negatively related to the interest rate? - What causes the investment

ECON 3560/5040 INVESTMENT - Investment is the most volatile component of GDP Fluctuations in the economy s output - Why is investment negatively related to the interest rate? - What causes the investment

Comment Letter Primer: Basel III Proposals

Comment Letter Primer: Basel III Proposals The Virginia Bankers Association urges member banks to review and submit comments on the proposed Basel III regulatory capital rules by the October 22, 2012 deadline.

Comment Letter Primer: Basel III Proposals The Virginia Bankers Association urges member banks to review and submit comments on the proposed Basel III regulatory capital rules by the October 22, 2012 deadline.

Measuring the Cost of Bailouts

Measuring the Cost of Bailouts Deborah Lucas Sloan Distinguished Professor of Finance and Director MIT Golub Center for Finance and Policy 2008 Financial Crisis: A Ten-Year Review New York, NY, November

Measuring the Cost of Bailouts Deborah Lucas Sloan Distinguished Professor of Finance and Director MIT Golub Center for Finance and Policy 2008 Financial Crisis: A Ten-Year Review New York, NY, November

FCF t. V = t=1. Topics in Chapter. Chapter 16. How can capital structure affect value? Basic Definitions. (1 + WACC) t

t") Topics in Chapter Chapter 16 Capital Structure Decisions Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

Topics in Chapter Chapter 16 Capital Structure Decisions Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

Stulz, Governance, Risk Management and Risk-Taking in Banks

P1.T1. Foundations of Risk Stulz, Governance, Risk Management and Risk-Taking in Banks Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com Stulz, Governance, Risk Management

P1.T1. Foundations of Risk Stulz, Governance, Risk Management and Risk-Taking in Banks Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com Stulz, Governance, Risk Management

Randall D. Guynn March 1, 2019

Ten Years Later: Vulnerabilities, Resiliency, Resolvability Randall D. Guynn March 1, 2019 Ten Years after the Global Financial Crisis: An Assessment Weil, Gotshal & Manges Roundtable Yale Law School Center

Ten Years Later: Vulnerabilities, Resiliency, Resolvability Randall D. Guynn March 1, 2019 Ten Years after the Global Financial Crisis: An Assessment Weil, Gotshal & Manges Roundtable Yale Law School Center

Articles Authored by Michael S. Barr January 20, 2009 October 31, 2009

Articles Authored by Michael S. Barr January 20, 2009 October 31, 2009 Michael Barr, Implementing Dodd-Frank To Fully End Too Big To Fain, national Mortgage News, August 30, 2010. To fully end "too-big-to-fail"

Articles Authored by Michael S. Barr January 20, 2009 October 31, 2009 Michael Barr, Implementing Dodd-Frank To Fully End Too Big To Fain, national Mortgage News, August 30, 2010. To fully end "too-big-to-fail"

Deposits and Bank Capital Structure

Deposits and Bank Capital Structure Franklin Allen 1 Elena Carletti 2 Robert Marquez 3 1 Imperial College 2 Bocconi University 3 UC Davis 24 October 2014 Franklin Allen, Elena Carletti, Robert Marquez

Deposits and Bank Capital Structure Franklin Allen 1 Elena Carletti 2 Robert Marquez 3 1 Imperial College 2 Bocconi University 3 UC Davis 24 October 2014 Franklin Allen, Elena Carletti, Robert Marquez

The cost of the Federal Government guarantee of Australia s commercial banks

Australian Centre for Financial Studies 19 th Money and Finance conference, Melbourne, July 2014 The cost of the Federal Government guarantee of Australia s commercial banks (Outline of paper work in progess)

Australian Centre for Financial Studies 19 th Money and Finance conference, Melbourne, July 2014 The cost of the Federal Government guarantee of Australia s commercial banks (Outline of paper work in progess)

FURTHER CHANGES IN THE LEVERAGE RATION OF BASEL III SESSION 4. Andrew Cornford Research Fellow Financial Markets Center

FURTHER CHANGES IN THE LEVERAGE RATION OF BASEL III SESSION 4 Andrew Cornford Research Fellow Financial Markets Center 1 LevRatio.Feb14 Further Changes in the Leverage Ratio of Basel III The new document

FURTHER CHANGES IN THE LEVERAGE RATION OF BASEL III SESSION 4 Andrew Cornford Research Fellow Financial Markets Center 1 LevRatio.Feb14 Further Changes in the Leverage Ratio of Basel III The new document

AFM 371 Practice Problem Set #2 Winter Suggested Solutions

AFM 371 Practice Problem Set #2 Winter 2008 Suggested Solutions 1. Text Problems: 16.2 (a) The debt-equity ratio is the market value of debt divided by the market value of equity. In this case we have

AFM 371 Practice Problem Set #2 Winter 2008 Suggested Solutions 1. Text Problems: 16.2 (a) The debt-equity ratio is the market value of debt divided by the market value of equity. In this case we have

10.2 Recent Shocks to the Macroeconomy Introduction. Housing Prices. Chapter 10 The Great Recession: A First Look

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused

Chapter 10 The Great Recession: A First Look By Charles I. Jones Media Slides Created By Dave Brown Penn State University 10.2 Recent Shocks to the Macroeconomy What shocks to the macroeconomy have caused