Argentina: two devaluation episodes. Maria Muniagurria University of Wisconsin September 27, 2017

|

|

|

- Berenice Charles

- 6 years ago

- Views:

Transcription

1 Argentina: two devaluation episodes Maria Muniagurria University of Wisconsin September 27, 2017

2 Two Episodes: Currency Board and 2001 Crisis (Sources: Sturzeneger talk at UW Madison 2002/ Feenstra Taylor, other) Cepo and Normalization of Jan 2016 (Econbrowser Blog Entry, other)

3 Some definitions: Nominal Exchange Rate: E= # pesos per dollar Real Exchange Rate: e = peso/dollar exchange rate = Argentinean prices in dollars /US Prices in dollars = (1/E). ( Prices Argentina in Pesos / Price in US in dollars)

4 Growth Rate of Real Exchange Rate Percentage of Change of e = (Argentina inflation rate- US Inflation rate) (percentage of change in E)

5 Currency Board As defined by the IMF, a currency board agreement is a monetary regime based on an explicit legislative commitment to exchange domestic currency for a specific foreign currency at a fixed exchange rate, combined with restrictions on the issuing authority. For currency boards to work properly, there has to be a longterm commitment to the system and automatic currency convertibility. This includes, but is not limited to, a limitation on printing new money, since this would affect the exchange rate.

6 Argentina Some History Rich Natural Resources High Human Capital Reasonable Infrastructure Great Performer in early 1900 s. Closed economy/populist policies Fiscal Problems, High Inflation, Macro Instability s

7 Reforms in the 90 s Opening, Privatization, Financial Reform Currency Board (Convertibility Law 1991) Fixed Peso/US dollar exchange rate Pesos issued had to be backed by dollar reserves (fiscal discipline) Results: End of Inflation Great Performance 90-98

8 Deterioration and Crisis: What Went Wrong? Combination: - External Shocks - Peso overvaluation relative to currencies of largest trading partners (from external shocks+currency board) - Fiscal dynamics (too weak during upswing, problem of provincial budgets, political issues) - Debt dynamics (unsustainable nature was not addressed - Self Fulfillment Pessimism?

9 External Shocks Mexico Crisis 1995 (Argentina recovered) Asian Crisis 1997 ( terms of trade) Russian Crisis 1998 (K-flows dried out) Brazilian devaluation January 1999 Euro depreciation against dollar 2000 World recession 2001 Country risk ok until January 1999 (similar to Mexico)

10 Robert C. Feenstra and Alan M. Taylor International Macroeconomics, Third Edition / International Economics, Third Edition Copyright 2014 by Worth Publishers

11 Fiscal issues/debt Circumvention of currency board implicit fiscal discipline through the issuance of quasi-moneys by both provinces and federal government. Interest payment Brady Bonds negotiated in 90 s ( interest rate increased cost of servicing foreign debt). After Russian crisis: interest rate in new debt Declining tax revenues, debt Attempts to collect more ( taxes in midst of recession) may have backfired

12 Declining output increasing unemployment K-outflows Decrease in reserves Decrease in deposits in banking system

13 Early/Mid 2001 Crisis Inevitable Big Problem: Not easy way out: Float? Default? Devaluation: Positive: effects on trade Negative: effects on Dollar denominated debt Abandoning the Currency Board: Monetary Policy: needs new discipline (inflation targeting? Other?) Issue of dollar deposits, contracts, debt (property rights, legal challenges)

14 December 2001/Jan 2002 December 2001: Frozen Deposits (corralito) Political Crisis Change of 4 presidents Riots, middle class protests Society s negative view of politicians Default Devaluation/Currency board abandoned Pesification

15 2002 0utput drop continues Unemployment reaches 20% Increase in poverty 52% in BsAs province Per capita income of those at the lower 10% of the income distribution decreased by 41%.

16 Very good economic Recovery Exports crucial in early stage Good export prices (soy boom 2004) Defaulted debt restructured and renegotiated Social indicators improve very slowly Some resurgency of inflation (12% 2005)

17 Other Issues (Populism) IMF Debt cancelled (Jan 2006) But it was the cheapest debt!!! Ban on beef exports (March 2006) to lower domestic price of beef!!!! China has become a leading trading partner!

18 Large increase in Social Spending (cash transfers)

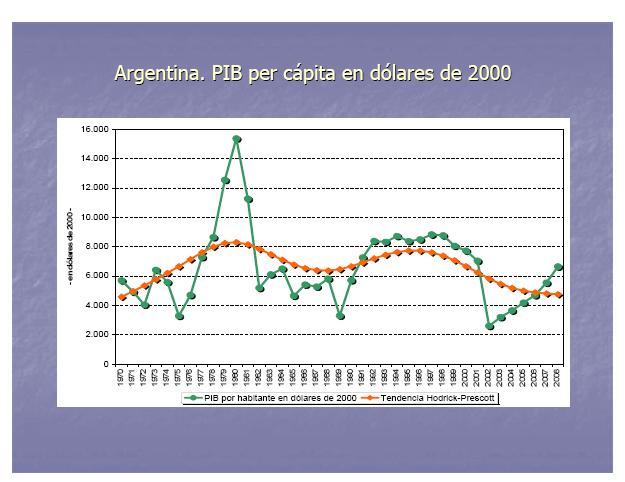

19 GDP Per capita (2000 USdollars)

20 Agricultural Production

21 Poverty Index in Buenos Aires Metropolitan area

22 Export and Import prices

23 China-Argentina Trade (million of US dollars)

24 China s participation in trade

25 Soy Prices

26

27 Dec 2015/Feb 2016 Argentina: A big change with problematic initial conditions A little over two months ago, Mauricio Macri began his tenure as president after his coalition of center-right parties prevailed over the ruling party s candidate by a small margin. This is the first significant political change in many years, since the left leaning branch of peronist party held the executive office since 2003 (both husband and wife Nestor and Cristina Kichner held the presidency). The following statement by former Finance Minister Kicillof summarizes the previous administration s approach to economic policy: since 2003, Argentina has been implementing an economic model of growth with social inclusion, where inclusion and redistribution of income are seen as a precondition for growth and not vice-versa, as stated by the mainstream economic precepts (October 2015 statement to the IMF).

28 Very favorable primary commodity prices and high export taxes financed large government expenditures (social programs, variety of subsidies) for many years but when the conditions started to reverse the country slipped into a path characterized by government deficits, inflation and foreign exchange controls. The 2001 default and the subsequent one in 2014 resulted in an almost complete exclusion of the country from international financial markets and since 2007 the government engaged in the manipulation of statistical data.

29 Since it took office last December 10th, the new administration has taken a number of important steps towards the elimination of major distortions, restoration of data transparency and return to international financial markets in the midst of a complicated political and social environment. The economic team inherited a very difficult situation with an inflation rate reaching about % a year, a government deficit of 7.1% of GDP and almost depleted foreign exchange reserves.

30 The main economic policy measures have been: 1) elimination of the foreign currency controls ( cepo or clamp ) and unification of the foreign exchange market; 2) declaration of an statistical emergency ; 3) partial elimination of utility subsidies; 4) decrease of export taxes on soy (from 35% to 30%) and elimination of those for beef, wheat and corn, 5) negotiations towards the return of the country international financial markets (negotiations with debt holdouts ).

31 Data Transparency Issues and Inflation

32

33 Foreign Exchange / Trade and Finance In November 2011 the government began to impose strict controls on the foreign exchange markets (trying to stop the decrease of the Central Bank s foreign reserves) what made almost impossible for ordinary citizens to purchase dollars and severely restricted imports. The cepo (or clamp) resulted in the emergence of a black market for foreign currency, and the official value of the dollar was kept artificially low. Exports suffered (producers were hoarding grain), import restrictions severely affected the availability of industrial inputs, and tourists expenses overseas (at an undervalued exchange rate) ballooned.

34 On December 16, after securing additional dollar reserves (due to a Yuan-dollar swap with China) and later a bridge loan from a group of international banks, the government fulfilled its campaign promise of lifting the cepo. The exchange rate adjusted: there was an immediate devaluation of 35% and a gradual depreciation of the peso afterwards to arrive to a 55% devaluation since the lifting of the cepo. The market has been operating without Central Bank intervention - except for one day last week - what should be considered as an important success. Figure 3 shows the paths of the official and black market rates and Figure 4 that of the international reserves.

35 Since the 2001 default, Argentina has been unable to borrow internationally and has been involved in a prolonged dispute with holdout bondholders (the 7% of that did not accept the restructuring). One of the judicial rulings (in New York courts) forced the default on the restructured debt in The current government has made significant progress in resolving the dispute and has stated its desire to return to the international financial markets (see The Economist ).

36 Exchange Rate (ARS per US dollar) /01/ /12/ /05/2012 1/10/ /02/2013 8/07/ /01/2014 6/06/ /10/ /06/ /01/2016 Official Rate Informal (black market rate)

37

38 High primary commodity prices resulted in a favorable Current Account for many years but the decline in those prices and large energy imports moved the balance into negative territory (see Figures 5 and 6). The new economic team reduced export taxes on soy by 5% and eliminated those on wheat, corn and beef. These adjustments together with the devaluation are expected to increase exports and the local supply of dollars.

39 Argentina: Primary Export Commodities Price Index in US Dollars 1995= Jan-00 May-00 Sep-00 Jan-01 May-01 Sep-01 Jan-02 May-02 Sep-02 Jan-03 May-03 Sep-03 Jan-04 May-04 Sep-04 Jan-05 May-05 Sep-05 Jan-06 May-06 Sep-06 Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10 Sep-10 Jan-11 May-11 Sep-11 Jan-12 May-12 Sep-12 Jan-13 May-13 Sep-13 Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15 Jan-16

40 Current Account Balance U$S Billion

41 Fiscal Situation Government Budget Balance (% GDP) General Gov net lending/borrowing % of GDP General Gov net primary lending/borrowing % of GDP

42 Last Update

43 Evolution of Exchange Rates: Official and Contado con Liquidacion

Argentina s Presidential Election - Implications for Argentine Agriculture Sector and Dry Bean Industry

Argentina s Presidential Election - Implications for Argentine Agriculture Sector and Dry Bean Industry By Randy Duckworth US Dry Bean Council Representative December 3, 2015 Ask 10 Argentines and you

Argentina s Presidential Election - Implications for Argentine Agriculture Sector and Dry Bean Industry By Randy Duckworth US Dry Bean Council Representative December 3, 2015 Ask 10 Argentines and you

Other similar crisis: Euro, Emerging Markets

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Lessons from the stabilization process in Argentina,

By Hyperinflation exploded in 1989. It was the final stage of a chronic inflationary process that began in 1945 and lasted 45 years. From the beginning of the century until the end of World War II, Argentina

By Hyperinflation exploded in 1989. It was the final stage of a chronic inflationary process that began in 1945 and lasted 45 years. From the beginning of the century until the end of World War II, Argentina

The fiscal adjustment after the crisis in Argentina

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

65 The fiscal adjustment after the 2001-02 crisis in Argentina 1 Mario Damill, Roberto Frenkel, and Martín Rapetti After the crisis of the convertibility regime, Argentina experienced a significant adjustment

The Open Economy Revisited: the Exchange-Rate Regime

C H A P T E R 12 : the Mundell-Fleming Model and the Exchange-Rate Regime MACROECONOMICS SIXTH EDITION N. GREGORY MANKIW PowerPoint Slides by Ron Cronovich 2008 Worth Publishers, all rights reserved In

C H A P T E R 12 : the Mundell-Fleming Model and the Exchange-Rate Regime MACROECONOMICS SIXTH EDITION N. GREGORY MANKIW PowerPoint Slides by Ron Cronovich 2008 Worth Publishers, all rights reserved In

MACROECONOMICS. The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime MANKIW N. GREGORY

C H A P T E R 12 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime MACROECONOMICS N. GREGORY MANKIW 2007 Worth Publishers, all rights reserved SIXTH EDITION PowerPoint

C H A P T E R 12 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime MACROECONOMICS N. GREGORY MANKIW 2007 Worth Publishers, all rights reserved SIXTH EDITION PowerPoint

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building 22-24 February 21 Debt Sustainability and the Implications

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building 22-24 February 21 Debt Sustainability and the Implications

Lecture 6: Intermediate macroeconomics, autumn Lars Calmfors

Lecture 6: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics Systems of fixed exchange rates Interest rate parity under a fixed exchange rate Stabilisation policy under a fixed exchange rate

Lecture 6: Intermediate macroeconomics, autumn 2009 Lars Calmfors 1 Topics Systems of fixed exchange rates Interest rate parity under a fixed exchange rate Stabilisation policy under a fixed exchange rate

Econ 340. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

L-3: BALANCE OF PAYMENT CRISES IRINA BUNDA MACROECONOMIC POLICIES IN TIMES OF HIGH CAPITAL MOBILITY VIENNA, MARCH 21 25, 2016

L-3: BALANCE OF PAYMENT CRISES IRINA BUNDA MACROECONOMIC POLICIES IN TIMES OF HIGH CAPITAL MOBILITY VIENNA, MARCH 21 25, 2016 THIS TRAINING MATERIAL IS THE PROPERTY OF THE JOINT VIENNA INSTITUTE (JVI)

L-3: BALANCE OF PAYMENT CRISES IRINA BUNDA MACROECONOMIC POLICIES IN TIMES OF HIGH CAPITAL MOBILITY VIENNA, MARCH 21 25, 2016 THIS TRAINING MATERIAL IS THE PROPERTY OF THE JOINT VIENNA INSTITUTE (JVI)

Chapter Eleven. The International Monetary System

Chapter Eleven The International Monetary System Introduction 11-3 The international monetary system refers to the institutional arrangements that govern exchange rates. Floating exchange rates occur when

Chapter Eleven The International Monetary System Introduction 11-3 The international monetary system refers to the institutional arrangements that govern exchange rates. Floating exchange rates occur when

Chapter 29 The Global Economy and Policy Principles of Economics in Context (Goodwin et al)

") Chapter 29 The Global Economy and Policy Principles of Economics in Context (Goodwin et al) Chapter Overview This chapter will take you through the basics of international trade and finance. The chapter

Chapter 29 The Global Economy and Policy Principles of Economics in Context (Goodwin et al) Chapter Overview This chapter will take you through the basics of international trade and finance. The chapter

Daniel Scioli leads the race to the presidency in October, but a runoff with Mauricio Macri in November is likely.

Latam in Depth Wednesday, September 09, 2015 ARGENTINA The day after Daniel Scioli leads the race to the presidency in October, but a runoff with Mauricio Macri in November is likely. The new administration

Latam in Depth Wednesday, September 09, 2015 ARGENTINA The day after Daniel Scioli leads the race to the presidency in October, but a runoff with Mauricio Macri in November is likely. The new administration

Greece, November 2011, in light of Argentinean Experience exactly ten years ago.

1 Greece, November 2011, in light of Argentinean Experience exactly ten years ago. Keynote speech by Domingo Cavallo at the CEO Summit, Doing More on Less, Athens, November 22, 2011 Let me be very sincere

1 Greece, November 2011, in light of Argentinean Experience exactly ten years ago. Keynote speech by Domingo Cavallo at the CEO Summit, Doing More on Less, Athens, November 22, 2011 Let me be very sincere

macro macroeconomics Aggregate Demand in the Open Economy N. Gregory Mankiw CHAPTER TWELVE PowerPoint Slides by Ron Cronovich fifth edition

macro CHAPTER TWELVE Aggregate Demand in the Open Economy macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved Learning objectives

macro CHAPTER TWELVE Aggregate Demand in the Open Economy macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved Learning objectives

Chapter 17. Exchange Rates and International Economic Policy

Chapter 17 Exchange Rates and International Economic Policy Preview To examine the financial market that determines exchange rates in the long and short runs To understand the role of exchange rates in

Chapter 17 Exchange Rates and International Economic Policy Preview To examine the financial market that determines exchange rates in the long and short runs To understand the role of exchange rates in

19.2 Exchange Rates in the Long Run Introduction 1/24/2013. Exchange Rates and International Finance. The Nominal Exchange Rate

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

THE GLOBAL ECONOMY AND POLICY Macroeconomics in Context (Goodwin, et al.)

") Chapter 14 THE GLOBAL ECONOMY AND POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter will take you through the basics of international trade and finance. The chapter introduces

Chapter 14 THE GLOBAL ECONOMY AND POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter will take you through the basics of international trade and finance. The chapter introduces

The Argentine economy in the new political and international environment. MIGUEL A. KIGUEL econviews

The Argentine economy in the new political and international environment MIGUEL A. KIGUEL econviews October 2009 1 Outline The international environment is helping Argentina once again The domestic financial

The Argentine economy in the new political and international environment MIGUEL A. KIGUEL econviews October 2009 1 Outline The international environment is helping Argentina once again The domestic financial

Greece should restructure its debt but stay in the Euro

Greece should restructure its debt but stay in the Euro By Domingo Cavallo Sep 23, 2011 Greece should restructure its debt and reorganize its economy, but stay in the Euro and accept its monetary discipline.

Greece should restructure its debt but stay in the Euro By Domingo Cavallo Sep 23, 2011 Greece should restructure its debt and reorganize its economy, but stay in the Euro and accept its monetary discipline.

Global Economic Prospects: Navigating strong currents

Global Economic Prospects: Navigating strong currents Andrew Burns World Bank January 18, 2011 http://www.worldbank.org/globaloutlook Main messages Most developing countries have passed with flying colors

Global Economic Prospects: Navigating strong currents Andrew Burns World Bank January 18, 2011 http://www.worldbank.org/globaloutlook Main messages Most developing countries have passed with flying colors

Asian Financial Crisis. Jianing Li/Wei Ye/Jingyan Zhang 2018/11/29

Asian Financial Crisis Jianing Li/Wei Ye/Jingyan Zhang 2018/11/29 Causes--Current account deficit 1. Liberalization of capital markets. 2. Large capital inflow due to the interest rates fall in developed

Asian Financial Crisis Jianing Li/Wei Ye/Jingyan Zhang 2018/11/29 Causes--Current account deficit 1. Liberalization of capital markets. 2. Large capital inflow due to the interest rates fall in developed

Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform

Developing Countries: Growth, Crisis, and Reform") Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform Preview Snapshots of rich and poor countries Characteristics of poor countries Borrowing and debt in poor and middle-income economies The

Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform Preview Snapshots of rich and poor countries Characteristics of poor countries Borrowing and debt in poor and middle-income economies The

External Factors, Macro Policies and Growth in LAC: Is Performance that Good?

External Factors, Macro Policies and Growth in LAC: Is Performance that Good? Alejandro Izquierdo IADB Emerging Powers in Global Governance Conference Paris, July 6, 2007 (based on work with Ernesto Talvi)

External Factors, Macro Policies and Growth in LAC: Is Performance that Good? Alejandro Izquierdo IADB Emerging Powers in Global Governance Conference Paris, July 6, 2007 (based on work with Ernesto Talvi)

Chapter 13 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime

Chapter 13 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016

Chapter 13 The Open Economy Revisited: the Mundell-Fleming Model and the Exchange-Rate Regime Modified by Yun Wang Eco 3203 Intermediate Macroeconomics Florida International University Summer 2017 2016

Depec Highlight - Bradesco

Depec Highlight - Bradesco May 9, 2018 Argentina s economic policy and its impact in Brazil Constantin Jancsó Andrea Bastos Damico The Central Bank of Argentina (BCRA) raised the base interest rate to

Depec Highlight - Bradesco May 9, 2018 Argentina s economic policy and its impact in Brazil Constantin Jancsó Andrea Bastos Damico The Central Bank of Argentina (BCRA) raised the base interest rate to

Prepared by Iordanis Petsas To Accompany. by Paul R. Krugman and Maurice Obstfeld

Chapter 22 Developing Countries: Growth, Crisis, and Reform Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld Chapter

Chapter 22 Developing Countries: Growth, Crisis, and Reform Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld Chapter

PRESS RELEASE Banco Hipotecario Sociedad Anónima Reports Third Quarter 2002 Results

FOR IMMEDIATE RELEASE Contacts: Marcelo Icikson Reuters BHI.BA Bloomberg - BHIP AR Bloomberg - BHIP Bloomberg BHN www.e-potecario.com Andrea Zelkowicz Gabriel G. Saidon

FOR IMMEDIATE RELEASE Contacts: Marcelo Icikson Reuters BHI.BA Bloomberg - BHIP AR Bloomberg - BHIP Bloomberg BHN www.e-potecario.com Andrea Zelkowicz Gabriel G. Saidon

Econ 102 Final Exam Name ID Section Number

Econ 102 Final Exam Name ID Section Number 1. Over time, contractionary monetary policy nominal wages and causes the short-run aggregate supply curve to shift. A) raises; leftward B) lowers; leftward C)

Econ 102 Final Exam Name ID Section Number 1. Over time, contractionary monetary policy nominal wages and causes the short-run aggregate supply curve to shift. A) raises; leftward B) lowers; leftward C)

3/9/2010. Topics PP542. Macroeconomic Goals (cont.) Macroeconomic Goals. Gold Standard. Macroeconomic Goals (cont.) International Monetary History

Macroeconomic Goals. Gold Standard. Macroeconomic Goals (cont.) International Monetary History") Topics PP542 International Monetary History Goals of macroeconomic policies Gold standard International monetary system during 98-939 Bretton Woods system: 944-973 Collapse of the Bretton Woods system

Topics PP542 International Monetary History Goals of macroeconomic policies Gold standard International monetary system during 98-939 Bretton Woods system: 944-973 Collapse of the Bretton Woods system

Foreign exchange intervention in Argentina: motives, techniques and implications

Foreign exchange intervention in Argentina: motives, techniques and implications Claudio Irigoyen 1. Introduction Finding the optimal degree of exchange rate flexibility is difficult. To a great extent

Foreign exchange intervention in Argentina: motives, techniques and implications Claudio Irigoyen 1. Introduction Finding the optimal degree of exchange rate flexibility is difficult. To a great extent

The challenges of financial globalization Roberto Frenkel 1

The challenges of financial globalization Roberto Frenkel 1 Introduction to Session 1: Global Challenges, Restrictions and Policy Space: Finance and Development SPIDER WEB Inaugural Workshop (School for

The challenges of financial globalization Roberto Frenkel 1 Introduction to Session 1: Global Challenges, Restrictions and Policy Space: Finance and Development SPIDER WEB Inaugural Workshop (School for

Exam Number. Section

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course ANSWER KEY Final Exam March 1, 2010 Note: These are only suggested answers. You may have received partial or full credit for your answers

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course ANSWER KEY Final Exam March 1, 2010 Note: These are only suggested answers. You may have received partial or full credit for your answers

What is Wrong with Market-Oriented Policies?

June 2003 In 1999, SigmaBleyzer initiated the International Private Capital Task Force (IPCTF) in Ukraine. Its objective was to benchmark transition economies to identify best practices in government policies

June 2003 In 1999, SigmaBleyzer initiated the International Private Capital Task Force (IPCTF) in Ukraine. Its objective was to benchmark transition economies to identify best practices in government policies

What Does Debt Relief Do for Development? Lessons from the Largest Household Bailout in History

What Does Debt Relief Do for Development? Lessons from the Largest Household Bailout in History Martin Kanz World Bank Research Department Policy Research Talk November 5, 2018 Motivation Economists have

What Does Debt Relief Do for Development? Lessons from the Largest Household Bailout in History Martin Kanz World Bank Research Department Policy Research Talk November 5, 2018 Motivation Economists have

Chapter 18. The International Financial System Intervention in the Foreign Exchange Market

Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding of foreign assets in the foreign exchange market

Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding of foreign assets in the foreign exchange market

Chapter 19 (8) International Monetary Systems: An Historical Overview

International Monetary Systems: An Historical Overview") Chapter 19 (8) International Monetary Systems: An Historical Overview Preview Goals of macroeconomic policies internal and external balance Gold standard era 1870 1914 International monetary system during

Chapter 19 (8) International Monetary Systems: An Historical Overview Preview Goals of macroeconomic policies internal and external balance Gold standard era 1870 1914 International monetary system during

Argentina s Challenges and Opportunities: Reasons for (Sober and Realistic) Optimism

Optimism") Argentina s Challenges and Opportunities: Reasons for (Sober and Realistic) Optimism Eugenio Diaz Bonilla Executive Director for Argentina and Haiti Inter American Development Bank Recent History Argentina:

Argentina s Challenges and Opportunities: Reasons for (Sober and Realistic) Optimism Eugenio Diaz Bonilla Executive Director for Argentina and Haiti Inter American Development Bank Recent History Argentina:

East Asia Crisis of Econ October 8, Team 5 Bryan Darch Svend Egholm Paramdeep Singh Sarah Zullo

East Asia Crisis of 1997 Econ 7920 October 8, 2008 Team 5 Bryan Darch Svend Egholm Paramdeep Singh Sarah Zullo The East Asian currency crisis of 1997 caused severe distress for the countries of East Asia

East Asia Crisis of 1997 Econ 7920 October 8, 2008 Team 5 Bryan Darch Svend Egholm Paramdeep Singh Sarah Zullo The East Asian currency crisis of 1997 caused severe distress for the countries of East Asia

The politics of Brazilian debt dynamics in the light of Argentina s default 1. By Domingo F. Cavallo

The politics of Brazilian debt dynamics in the light of Argentina s default 1 The political and economic decisions of Brazilian President Luis Inacio Lula da Silva in connection with the country s public

The politics of Brazilian debt dynamics in the light of Argentina s default 1 The political and economic decisions of Brazilian President Luis Inacio Lula da Silva in connection with the country s public

Public Disclosure Authorized. Public Disclosure Authorized. Public Disclosure Authorized. Public Disclosure Authorized. Report No.

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Report No. PID7125 Project Name Argentina-Special Structural Adjustment... Loan (SSAL)

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Report No. PID7125 Project Name Argentina-Special Structural Adjustment... Loan (SSAL)

Managing the Financial Crisis: Argentina (2002)

") Managing the Financial Crisis: Argentina (2002) Mario I. Blejer Director Centre for Central Banking Studies Bank of England Monthly Gross Domestic Product seasonally adjusted (Jan 98 = 100) 105.0 100.0

Managing the Financial Crisis: Argentina (2002) Mario I. Blejer Director Centre for Central Banking Studies Bank of England Monthly Gross Domestic Product seasonally adjusted (Jan 98 = 100) 105.0 100.0

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank The 11th International Academic Conference on Economic and Social Development April 6-8, 2010 Moscow

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank The 11th International Academic Conference on Economic and Social Development April 6-8, 2010 Moscow

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

Latin American Crises. Presentation 2 - EC/EIB 230 International Finance Mathew Cravens Venkatesh Ramamoorthy Jiong Zhou

Latin American Crises Presentation 2 - EC/EIB 230 International Finance Mathew Cravens Venkatesh Ramamoorthy Jiong Zhou Agenda Background of crisis - Economical & Political Transmission & Impact of crisis

Latin American Crises Presentation 2 - EC/EIB 230 International Finance Mathew Cravens Venkatesh Ramamoorthy Jiong Zhou Agenda Background of crisis - Economical & Political Transmission & Impact of crisis

PETROBRAS ARGENTINA S.A. (Exact name of Registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 20-F ANNUAL REPORT PURSUANT TO SECTION 13 OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended: December 31, 2015

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 20-F ANNUAL REPORT PURSUANT TO SECTION 13 OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended: December 31, 2015

Rich and Poor. Indicators of Economic Welfare for 4 groups of countries, 2003 GNP per capita (1995 US$)

") Rich and Poor Indicators of Economic Welfare for 4 groups of countries, 2003 GNP per capita (1995 US$) Life expectancy Low income 450 58 Lower-middle income 1480 69 Upper-middle income 5340 73 High income

Rich and Poor Indicators of Economic Welfare for 4 groups of countries, 2003 GNP per capita (1995 US$) Life expectancy Low income 450 58 Lower-middle income 1480 69 Upper-middle income 5340 73 High income

Chapter 10 (part 2) Exchange Rates, Business Cycles, and Macroeconomic Policy in the Open Economy. Copyright 2009 Pearson Education Canada

Exchange Rates, Business Cycles, and Macroeconomic Policy in the Open Economy. Copyright 2009 Pearson Education Canada") Chapter 10 (part 2) Exchange Rates, Business Cycles, and Macroeconomic Policy in the Open Economy Copyright 2009 Pearson Education Canada Today Last class we saw the policy implications in the Mundell-Fleming

Chapter 10 (part 2) Exchange Rates, Business Cycles, and Macroeconomic Policy in the Open Economy Copyright 2009 Pearson Education Canada Today Last class we saw the policy implications in the Mundell-Fleming

Chapter 18: Output and the Exchange Rate in the Short Run

Chapter 18: Output and the Exchange Rate in the Short Run Krugman, P.R., Obstfeld, M.: International Economics: Theory and Policy, 8th Edition, Pearson Addison-Wesley, 460-500 1 Preview Balance sheets

Chapter 18: Output and the Exchange Rate in the Short Run Krugman, P.R., Obstfeld, M.: International Economics: Theory and Policy, 8th Edition, Pearson Addison-Wesley, 460-500 1 Preview Balance sheets

Devaluation as a Reason for Economical Growth or Crisis

International Journal of Economics and Finance; Vol. 9, No. 2; 2017 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education Devaluation as a Reason for Economical Growth or

International Journal of Economics and Finance; Vol. 9, No. 2; 2017 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education Devaluation as a Reason for Economical Growth or

Improving Economic Outlook for Argentina

Improving Economic Outlook for Argentina J ULY 2017 Corporation Inc. Country Overview Abundant natural resources combined with combined with growth-oriented economic initiatives and responsible fiscal

Improving Economic Outlook for Argentina J ULY 2017 Corporation Inc. Country Overview Abundant natural resources combined with combined with growth-oriented economic initiatives and responsible fiscal

Chapter 18. The International Financial System

Chapter 18 The International Financial System Unsterilized Foreign Exchange Intervention Federal Reserve System Assets Liabilities Federal Reserve System Assets Liabilities Foreign Assets -$1B Currency

Chapter 18 The International Financial System Unsterilized Foreign Exchange Intervention Federal Reserve System Assets Liabilities Federal Reserve System Assets Liabilities Foreign Assets -$1B Currency

Chapter 19 International Monetary Systems: An Historical Overview

Chapter 19 International Monetary Systems: An Historical Overview Copyright 2012 Pearson Addison-Wesley. All rights reserved. Preview Goals of macroeconomic policies internal and external balance Gold

Chapter 19 International Monetary Systems: An Historical Overview Copyright 2012 Pearson Addison-Wesley. All rights reserved. Preview Goals of macroeconomic policies internal and external balance Gold

ARGENTINA: WHAT WENT WRONG? Guillermo Perry and Luis Servén World Bank May 2003

ARGENTINA: WHAT WENT WRONG? Guillermo Perry and Luis Servén World Bank May 2003 Performance in the nineties: Better than most up to 1998, worse than most afterwards Real GDP Growth Rate (Percentages) 1981-90

ARGENTINA: WHAT WENT WRONG? Guillermo Perry and Luis Servén World Bank May 2003 Performance in the nineties: Better than most up to 1998, worse than most afterwards Real GDP Growth Rate (Percentages) 1981-90

Final exam Non-detailed correction 3 hours. This are indicative directions on how structure the essay questions and what was expected.

International Finance Master PEI Fall 2011 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours This are indicative directions on how structure the essay questions and what was expected. 1. Multiple

International Finance Master PEI Fall 2011 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours This are indicative directions on how structure the essay questions and what was expected. 1. Multiple

Slides for International Finance Macroeconomic Policy (KOM Chapter 19)

") Macroeconomic Policy (KOM Chapter 19) American University 2010-09-17 Preview Macroeconomic Policy Goals of macroeconomic policies Monetary standards Gold standard International monetary system during 1918-1939

Macroeconomic Policy (KOM Chapter 19) American University 2010-09-17 Preview Macroeconomic Policy Goals of macroeconomic policies Monetary standards Gold standard International monetary system during 1918-1939

China s Currency: A Summary of the Economic Issues

Order Code RS21625 Updated July 11, 2007 China s Currency: A Summary of the Economic Issues Summary Wayne M. Morrison Foreign Affairs, Defense, and Trade Division Marc Labonte Government and Finance Division

Order Code RS21625 Updated July 11, 2007 China s Currency: A Summary of the Economic Issues Summary Wayne M. Morrison Foreign Affairs, Defense, and Trade Division Marc Labonte Government and Finance Division

Macroeconomic Issues and Policy. Stabilization Policy. Time Lags Regarding Monetary and Fiscal Policy

C H A P T E R 15 Macroeconomic Issues and Policy Prepared by: Fernando Quijano and Yvonn Quijano Stabilization Policy Stabilization policy describes both monetary and fiscal policy, the goals of which

C H A P T E R 15 Macroeconomic Issues and Policy Prepared by: Fernando Quijano and Yvonn Quijano Stabilization Policy Stabilization policy describes both monetary and fiscal policy, the goals of which

GLOBALIZATION FINAL REPORT. Why is Argentina an example of globalization failure?

GLOBALIZATION FINAL REPORT Why is Argentina an example of globalization failure? Raleigh Campus Globalization Seminar Group 12 Benoît PETIT - Clément PETIT - Rémi PETRELLA Pauline POIRIER - Vincent RACE

GLOBALIZATION FINAL REPORT Why is Argentina an example of globalization failure? Raleigh Campus Globalization Seminar Group 12 Benoît PETIT - Clément PETIT - Rémi PETRELLA Pauline POIRIER - Vincent RACE

Balance of Payments, Debt, Financial Crises, and Stabilization Policies

Chapter 9 Balance of Payments, Debt, Financial Crises, and Stabilization Policies Problems and Policies: international and macro 1 International Finance and Investment: Key Issues How major debt crises

Chapter 9 Balance of Payments, Debt, Financial Crises, and Stabilization Policies Problems and Policies: international and macro 1 International Finance and Investment: Key Issues How major debt crises

Suggested Solutions to Problem Set 6

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

Confronting the Global Crisis in Latin America: What is the Outlook? Coordinators

Confronting the Global Crisis in Latin America: What is the Outlook? Policy Trade-offs May for 20, Unprecedented 2009 - Maison Times: Confronting de l Amérique the Global Crisis Latine, America, ParisIADB,

Confronting the Global Crisis in Latin America: What is the Outlook? Policy Trade-offs May for 20, Unprecedented 2009 - Maison Times: Confronting de l Amérique the Global Crisis Latine, America, ParisIADB,

Interest and Exchange Rates: Impact on the Economy

Interest and Exchange Rates: Impact on the Economy Economists Point of View Saman Kelegama Institute of Policy Studies of Sri Lanka (IPS) Increase in Credit Supply Government borrowing strategy was supported

Interest and Exchange Rates: Impact on the Economy Economists Point of View Saman Kelegama Institute of Policy Studies of Sri Lanka (IPS) Increase in Credit Supply Government borrowing strategy was supported

Policy in Papua New Guinea: recent shocks, new directions

Policy in Papua New Guinea: recent shocks, new directions Keynote Address, CPA PNG Conference, Lae, August 24-25 2017 Martin Davies Associate Professor Washington and Lee University Visiting Associate

Policy in Papua New Guinea: recent shocks, new directions Keynote Address, CPA PNG Conference, Lae, August 24-25 2017 Martin Davies Associate Professor Washington and Lee University Visiting Associate

Argentina s Crisis and Recovery: A Demand Side Story Alberto Martin November 2013

Argentina s Crisis and Recovery: A Demand Side Story 1998 2006 by Ariel Burstein and Ivan Werning Alberto Martin November 2013 Overview Revisit argentine experience 1998 2002: Prolonged recession: 5.4%

Argentina s Crisis and Recovery: A Demand Side Story 1998 2006 by Ariel Burstein and Ivan Werning Alberto Martin November 2013 Overview Revisit argentine experience 1998 2002: Prolonged recession: 5.4%

PRESS RELEASE. Banco Hipotecario Sociedad Anónima Reports Third Quarter 2003 Results

Reuters BHI.BA Bloomberg - BHIP AR Bloomberg - BHIP Bloomberg BHN www.e-potecario.com FOR IMMEDIATE RELEASE Contacts: Marcelo Icikson Nicolás Vocos Capital Markets Tel.

Reuters BHI.BA Bloomberg - BHIP AR Bloomberg - BHIP Bloomberg BHN www.e-potecario.com FOR IMMEDIATE RELEASE Contacts: Marcelo Icikson Nicolás Vocos Capital Markets Tel.

/JordanStrategyForumJSF Jordan Strategy Forum. Amman, Jordan T: F:

The Jordan Strategy Forum (JSF) is a not-for-profit organization, which represents a group of Jordanian private sector companies that are active in corporate and social responsibility (CSR) and in promoting

The Jordan Strategy Forum (JSF) is a not-for-profit organization, which represents a group of Jordanian private sector companies that are active in corporate and social responsibility (CSR) and in promoting

Developing Countries Chapter 22

Developing Countries Chapter 22 1. Growth 2. Borrowing and Debt 3. Money-financed deficits and crises 4. Other crises 5. Currency board 6. International financial architecture for the future 1 Growth 1.1

Developing Countries Chapter 22 1. Growth 2. Borrowing and Debt 3. Money-financed deficits and crises 4. Other crises 5. Currency board 6. International financial architecture for the future 1 Growth 1.1

The Impact of the Crisis on Budget Policy in Central and Eastern Europe: A comparison to Middle East and North African countries

The Impact of the Crisis on Budget Policy in Central and Eastern Europe: A comparison to Middle East and North African countries Zsolt Darvas 2th Annual Meeting of OECD-MENA Senior Budget Officials Doha,

The Impact of the Crisis on Budget Policy in Central and Eastern Europe: A comparison to Middle East and North African countries Zsolt Darvas 2th Annual Meeting of OECD-MENA Senior Budget Officials Doha,

Banco Galicia. Investor Presentation. August 2014

Banco Galicia Investor Presentation August 214 Agenda» The Argentine Economy»The Argentine Financial System»Banco Galicia»Annex 2 GDP % Change Economic Activity 12% 9 9% 8,8% 9,% 9,2% 8,4% 8,% 9,1% 8.%

Banco Galicia Investor Presentation August 214 Agenda» The Argentine Economy»The Argentine Financial System»Banco Galicia»Annex 2 GDP % Change Economic Activity 12% 9 9% 8,8% 9,% 9,2% 8,4% 8,% 9,1% 8.%

THE JAPANESE ECONOMY AND THE AFTERMATH OF ITS UNUSUAL RECESSION SHIJURO OGATA. Occasional Paper No. 19

THE JAPANESE ECONOMY AND THE AFTERMATH OF ITS UNUSUAL RECESSION SHIJURO OGATA Occasional Paper No. 19 Mr. Shijuro Ogata Former Deputy Governor, The Japan Development Bank Former Deputy Governor for International

THE JAPANESE ECONOMY AND THE AFTERMATH OF ITS UNUSUAL RECESSION SHIJURO OGATA Occasional Paper No. 19 Mr. Shijuro Ogata Former Deputy Governor, The Japan Development Bank Former Deputy Governor for International

Iceland s crisis and recovery: are there lessons for the eurozone and its member countries?

Central Bank of Iceland Iceland s crisis and recovery: are there lessons for the eurozone and its member countries? Már Guðmundsson Governor, Central Bank of Iceland Levy Institute conference, Athens,

Central Bank of Iceland Iceland s crisis and recovery: are there lessons for the eurozone and its member countries? Már Guðmundsson Governor, Central Bank of Iceland Levy Institute conference, Athens,

Anti-crisis State Policy in Russia

1 Anti-crisis State Policy in Russia Vera Kononova Institute for Complex Strategic Studies 1 December 2016 Seminar Outline 1. Anti-crisis Policy Goals The main goals and targets adopted by the Government

1 Anti-crisis State Policy in Russia Vera Kononova Institute for Complex Strategic Studies 1 December 2016 Seminar Outline 1. Anti-crisis Policy Goals The main goals and targets adopted by the Government

Argentina Provincials: Fixed Income Review- August 18

Executive Summary Argentina Provincials: Fixed Income Review August 18 About the report: This report aims to determine the relative credit quality of all Argentine Provinces with outstanding international

Executive Summary Argentina Provincials: Fixed Income Review August 18 About the report: This report aims to determine the relative credit quality of all Argentine Provinces with outstanding international

BRAZILIAN INDIRECT TRADE IN STEEL IN November 2013

BRAZILIAN INDIRECT TRADE IN STEEL IN 197-211 November 213 1 Brazilian indirect trade in steel in 197-211 A working paper issued by the World Steel Association (worldsteel) Introduction This paper aims

BRAZILIAN INDIRECT TRADE IN STEEL IN 197-211 November 213 1 Brazilian indirect trade in steel in 197-211 A working paper issued by the World Steel Association (worldsteel) Introduction This paper aims

LECTURE XIV. 31 July Tuesday, July 31, 12

LECTURE XIV 31 July 2012 TOPIC 16 Exchange Rates and Policy BIG PICTURE What are different common exchange rate systems? How can exchange rates be manipulated to affect a country s real variables? What

LECTURE XIV 31 July 2012 TOPIC 16 Exchange Rates and Policy BIG PICTURE What are different common exchange rate systems? How can exchange rates be manipulated to affect a country s real variables? What

Volume Author/Editor: Gerardo della Paolera and Alan M. Taylor. Volume URL:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Straining at the Anchor: The Argentine Currency Board and the Search for Macroeconomic Stability,

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Straining at the Anchor: The Argentine Currency Board and the Search for Macroeconomic Stability,

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System

Chapter 18 The International Financial System") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding

The International Monetary System

The International Monetary System Eiteman et al., Chapter 2 Winter 2004 Outline of the Chapter Currency Terminology History of the International Monetary System Contemporary Currency Regimes Emerging Markets

The International Monetary System Eiteman et al., Chapter 2 Winter 2004 Outline of the Chapter Currency Terminology History of the International Monetary System Contemporary Currency Regimes Emerging Markets

The Future of Mexican Monetary Policy

The Future of Mexican Monetary Policy Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México* XP Securities Mexico Summit Mexico City, 2 March 2017 */ The views expressed herein are strictly personal.

The Future of Mexican Monetary Policy Mr. Javier Guzmán Calafell, Deputy Governor, Banco de México* XP Securities Mexico Summit Mexico City, 2 March 2017 */ The views expressed herein are strictly personal.

Inflation Report. July September 2012

July September 1 November 7, 1 1 Outline 1 External Conditions Economic Activity in Mexico 3 Monetary Policy and Inflation Determinants Forecasts and Balance of Risks External Conditions The growth rate

July September 1 November 7, 1 1 Outline 1 External Conditions Economic Activity in Mexico 3 Monetary Policy and Inflation Determinants Forecasts and Balance of Risks External Conditions The growth rate

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Economics Higher level Paper 2

Economics Higher level Paper 2 Tuesday 5 May 2015 (morning) 1 hour 30 minutes Instructions to candidates Do not open this examination paper until instructed to do so. You are not permitted access to any

Economics Higher level Paper 2 Tuesday 5 May 2015 (morning) 1 hour 30 minutes Instructions to candidates Do not open this examination paper until instructed to do so. You are not permitted access to any

Comité Latino Americano de Asuntos Financieros Latin American Shadow Financial Regulatory Committee Comitê Latino Americano de Assuntos Financeiros

Comité Latino Americano de Asuntos Financieros Latin American Shadow Financial Regulatory Committee Comitê Latino Americano de Assuntos Financeiros Statement No. 35 Washington D.C., April 5th, 2016 Argentina

Comité Latino Americano de Asuntos Financieros Latin American Shadow Financial Regulatory Committee Comitê Latino Americano de Assuntos Financeiros Statement No. 35 Washington D.C., April 5th, 2016 Argentina

China s macroeconomic imbalances: causes and consequences. John Knight and Wang Wei

China s macroeconomic imbalances: causes and consequences John Knight and Wang Wei 1. Introduction This paper is different from the specialist papers at this conference It is more general, and is more

China s macroeconomic imbalances: causes and consequences John Knight and Wang Wei 1. Introduction This paper is different from the specialist papers at this conference It is more general, and is more

internationally tradable goods, thus affecting inflation, an effect that has become more evident in recent months.

REMARKS BY MR. JAVIER GUZMÁN CALAFELL, DEPUTY GOVERNOR AT THE BANCO DE MÉXICO, AT THE PANEL OF CENTRAL BANK GOVERNORS ON NEW CHALLENGES FOR CENTRAL BANKS IN LATIN AMERICA. SEMINAR ON FINANCIAL VOLATILITY

REMARKS BY MR. JAVIER GUZMÁN CALAFELL, DEPUTY GOVERNOR AT THE BANCO DE MÉXICO, AT THE PANEL OF CENTRAL BANK GOVERNORS ON NEW CHALLENGES FOR CENTRAL BANKS IN LATIN AMERICA. SEMINAR ON FINANCIAL VOLATILITY

To Fix or Not to Fix?

To Fix or Not to Fix? Linda Tesar, Department of Economics Notes at: http://www.econ.lsa.umich.edu/~ltesar April 5, 2000 Fixed vs. Flexible Exchange rates The Theory: Money demand: M/P = L(Y,I) Interest

To Fix or Not to Fix? Linda Tesar, Department of Economics Notes at: http://www.econ.lsa.umich.edu/~ltesar April 5, 2000 Fixed vs. Flexible Exchange rates The Theory: Money demand: M/P = L(Y,I) Interest

Ten Lessons Learned from the Korean Crisis Center for International Development, 11/19/99. Jeffrey A. Frankel, Harpel Professor, Harvard University

Ten Lessons Learned from the Korean Crisis Center for International Development, 11/19/99 Jeffrey A. Frankel, Harpel Professor, Harvard University The crisis has now passed in Korea. The excessive optimism

Ten Lessons Learned from the Korean Crisis Center for International Development, 11/19/99 Jeffrey A. Frankel, Harpel Professor, Harvard University The crisis has now passed in Korea. The excessive optimism

PubPol 201. Module 1: International Trade Policy. Class 3 Trade Deficits; Currency Manipulation

PubPol 201 Module 1: International Trade Policy Class 3 Trade Deficits; Currency Manipulation Class 3 Outline Trade Deficits; Currency Manipulation Trade deficits Definitions What they do and do not mean

PubPol 201 Module 1: International Trade Policy Class 3 Trade Deficits; Currency Manipulation Class 3 Outline Trade Deficits; Currency Manipulation Trade deficits Definitions What they do and do not mean

Structure and Function of the Federal Reserve System

1/17/17 Economic Outlook Cortney Cowley Economist Federal Reserve Bank of Kansas City Omaha Branch October, 17 The views expressed are those of the author and do not necessarily reflect the opinions of

1/17/17 Economic Outlook Cortney Cowley Economist Federal Reserve Bank of Kansas City Omaha Branch October, 17 The views expressed are those of the author and do not necessarily reflect the opinions of

Good Bye Undervaluation, Hello Stagflation

Good Bye Undervaluation, Hello Stagflation Domingo Cavallo & Joaquín Cottani, November 2007 EXEC SUMMARY Argentina started its free fall descent into a likely recession in the last quarter of 2007. At

Good Bye Undervaluation, Hello Stagflation Domingo Cavallo & Joaquín Cottani, November 2007 EXEC SUMMARY Argentina started its free fall descent into a likely recession in the last quarter of 2007. At

Ten Years After The Asian Financial Crisis * Heh-Song Wang **

Ten Years After The Asian Financial Crisis * I. Introduction Heh-Song Wang ** It is indeed a great honor and pleasure for me to be here to talk about the topic Ten years after the Asian financial crisis.

Ten Years After The Asian Financial Crisis * I. Introduction Heh-Song Wang ** It is indeed a great honor and pleasure for me to be here to talk about the topic Ten years after the Asian financial crisis.

ECO 209Y MACROECONOMIC THEORY AND POLICY

Department of Economics Prof. Gustavo Indart University of Toronto December 7, 2011 ECO 209Y MACROECONOMIC THEORY AND POLICY Term Test #2 LAST NAME FIRST NAME STUDENT NUMBER Circle your section of the

Department of Economics Prof. Gustavo Indart University of Toronto December 7, 2011 ECO 209Y MACROECONOMIC THEORY AND POLICY Term Test #2 LAST NAME FIRST NAME STUDENT NUMBER Circle your section of the

THE IMF: INSTRUMENTS AND STRATEGIES. Lecture 5 LIUC 2009 ORIGINS OF THE IMF

THE IMF: INSTRUMENTS AND STRATEGIES Lecture 5 LIUC 2009 1 WHAT IS THE INTERNATIONAL MONETARY FUND? The IMF is an international cooperative financial institution. Each member deposits a sum of money into

THE IMF: INSTRUMENTS AND STRATEGIES Lecture 5 LIUC 2009 1 WHAT IS THE INTERNATIONAL MONETARY FUND? The IMF is an international cooperative financial institution. Each member deposits a sum of money into

Global Economic Prospects and the Developing Countries William Shaw December 1999

Global Economic Prospects and the Developing Countries 2000 William Shaw December 1999 Prospects for Growth and Poverty Reduction in Developing Countries Recovery from financial crisis uneven International

Global Economic Prospects and the Developing Countries 2000 William Shaw December 1999 Prospects for Growth and Poverty Reduction in Developing Countries Recovery from financial crisis uneven International

Central Banking in Emerging Markets

Central Banking in Emerging Markets International Center for Monetary and Banking Studies () Governor of the Central Bank of Brazil Ilan Goldfajn January 15, 2019 Monetary policy is challenging in Emerging

Central Banking in Emerging Markets International Center for Monetary and Banking Studies () Governor of the Central Bank of Brazil Ilan Goldfajn January 15, 2019 Monetary policy is challenging in Emerging

ABSTRACT. This paper shows that the Russian 1998 crisis had a big impact on capital flows to Emerging Market

Sudden Stop, Financial Factors and Economic Collapse in Latin America: Learning from Argentina and Chile Guillermo A. Calvo and Ernesto Talvi NBER Working Paper No. 11153 February 2005 JEL No. F31, F32,

Sudden Stop, Financial Factors and Economic Collapse in Latin America: Learning from Argentina and Chile Guillermo A. Calvo and Ernesto Talvi NBER Working Paper No. 11153 February 2005 JEL No. F31, F32,

Outlook for the Chilean Economy

Outlook for the Chilean Economy Jorge Marshall, Vice-President of the Board, Central Bank of Chile. Address to the Fifth Annual Latin American Banking Conference, Salomon Smith Barney, New York, March

Outlook for the Chilean Economy Jorge Marshall, Vice-President of the Board, Central Bank of Chile. Address to the Fifth Annual Latin American Banking Conference, Salomon Smith Barney, New York, March

Reform of Global Reserve System and China s Choice 1

Reform of Global Reserve System and China s Choice 1 Liqing Zhang Professor and Dean, School of Finance, Central University of Finance and Economics, Beijing Email: zhlq@cufe.edu.cn 1. Why the Regime should

Reform of Global Reserve System and China s Choice 1 Liqing Zhang Professor and Dean, School of Finance, Central University of Finance and Economics, Beijing Email: zhlq@cufe.edu.cn 1. Why the Regime should

Economic Reform in Uganda: Lessons for Africa 3 December Prof. E. Tumusiime-Mutebile, Governor

Economic Reform in Uganda: Lessons for Africa 3 December 2009 Prof. E. Tumusiime-Mutebile, Governor Introduction If I was asked what the one theme of this book is, I would say that the these is the relevance

Economic Reform in Uganda: Lessons for Africa 3 December 2009 Prof. E. Tumusiime-Mutebile, Governor Introduction If I was asked what the one theme of this book is, I would say that the these is the relevance