FUCHS PETROLUB SE. manufacturer of the world. Dr. Alexander Selent, Vice Chairman & CFO. April 2015

|

|

|

- Sheryl Caldwell

- 6 years ago

- Views:

Transcription

1 The leading independent lubricants manufacturer of the world Dr. Alexander Selent, Vice Chairman & CFO DagmarSteinert Steinert, Headof Investor Relations April 2015

2 The leading independent lubricants manufacturer of the world Founded in sales revenues: 1.9 bn 2014 number of employees: 4,112 in 50 operating companies worldwide 30 production facilities 100,000 customers in more than 150 countries ti Member of the MDAX, DAXplus Family 30 and STOXX Europe 600 2

3 FUCHS - business model FUCHS is fully focussed on lubricants (advantage over major oil companies) Technology, innovation and specialisation leadership in strategically important product areas Independence allows customer and market proximity, responsiveness, speed and flexibility (advantage over major oil companies) FUCHS is a full-line supplier (advantage over most independent companies) Global presence (advantage over most independent companies) 3

4 FUCHS - long-term strategic objectives Continue to be the world s largest independent d manufacturer of lubricants and related specialities Value-based growth through innovation and specialisation leadership Organic growth in emerging markets and organic and external growth in mature markets Creating shareholder value by generating returns above the cost of capital Remain independent which is decisive for FUCHS business model 4

36.4 35.")

5 Regional breakdown of world lubricants demand World lubricants demand 2014: 35 mn t Demand (mn t) Asia-Pacific biggest regional lubricants market with highest growth rate North thamerica and Western Europe mature markets; focus is more on a specialized product portfolio and specialties Source: FUCHS Global Competitive Intelligence 5

6 2014 per-capita lubricants demand shows significant growth opportunities kg Source: FUCHS Global Competitive Intelligence 6

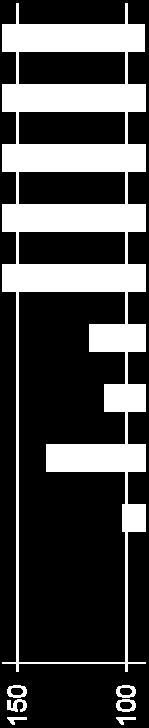

7 Top 20 lubricants countries 2014 Kt tons FUCHS is present in every important lubricants country. China and the USA cover more than one third of the world lubricants market. 7

8 Competition strong fragmentation manufacturers: 130 major oil companies 590 independent manufacturers 720 manufacturers High degree of fragmentation ti Concentration especially among smaller companies sizes: manufacturers volumes % top 10 > < Differences in the size of manufacturers are enormous Source: FUCHS Global Competitive Intelligence 8

9 Strategic Position 9

10 FUCHS is fully focused on lubricants Sales 2014: 1.9 bn Automotive lubricants 40.1% Other 3.1% Industrial lubricants 56.8% 100,000 customers Automotive industry Manufacturing Engineering Construction & Mining & Trade, services & transportation passenger cars & trucks steel & cement conveyer belt & aeronautic agriculture industry wind energy railway & food industry 10

11 FUCHS is strategically well positioned Worldwide among the top 10 of the lubricants manufacturers (by volume) Among 590 independent lubricant companies the number 1 (by volume) Source: FUCHS Global Competitive Intelligence 11

12 FUCHS is the specialist for lubricants *metalworking fluids/corrosion preventives/lubricating greases Source: FUCHS Global Competitive Intelligence 12

13 FUCHS is the specialist and occupies technology and market leadership positions in strategically important niche areas High-performance No. 1 speciality open gear lubricants (cement industry etc.) Metalworking No. 2-4 fluids Corrosion No. 2 preventives Mining specialities No. 1 (fire-resistant hydraulic fluids for underground coal Forging lubricants No. 2 mining and highperformance lubricants) Environmentally No. 1 friendly lubricants Greases No

14 FUCHS the niche specialist R & D expenses in mn Technical leadership through intensive Research & Development. 416 researchers around the globe help our customers to solve their problems. FUCHS PETROLUB spent 33 mn in R&D expenses during

15 Breakdown of group sales revenues by customer sector FUCHS sales revenues 2014: 1,866 mn As a percentage of sales * Manufacturing industry = producer goods, capital goods, consumer goods Source: FUCHS Global Competitive Intelligence 15

16 Worldwide network stronger networking production sites 16

17 FUCHS strategic position is a combination of Comments High Degree of specialisation & technical excellence Size & global presence Customer Focus and tailor-made products around 1.9 bn in sales (80% with customers outside Germany, Asia Pacific is FUCHS 2nd largest regional market), #9 worldwide and by far the largest independent producer, close to customers leader in innovation, specialisation & technology, clear focus on highvalue products & market segments, basis for strong profitability, high cash flows & value creation Local & flat Committed optimized and highly flexible cost organisation employees structure, highly committed teams in management, production, R&D, sales and administration supported by company s independence, steering via FVA tool successful Independence & Financial Strength 17

18 Our Business Model Has Paid Dividends 18

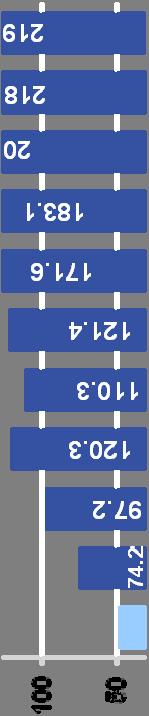

19 During the past 10 years, FUCHS Value Added has increased by 19.9 % p. a. and market capitalization has increased constantly and presently is close to 5 bn. FVA = Fuchs Value Added FUCHS market capitalization mn 5,000 4,000 3,000 2,000 1,000 19

20 During the past 10 years, sales revenues have increased by 5.5% 5% p.a. and earnings after tax by 16.3% p.a. Sales Earnings after tax mn 20

21 Since IPO in 1985 we have paid dividends during the past 10 years, dividends have been increased by 22.6% p.a. Dividend id d per preference share (adjusted for changes in equity structure)

22 Pay-out ratio almost 50% in % 22

23 Total return to FUCHS shareholders through dividends and share buyback Dividend id d payout and share buyback b since 2002 mn per share

24 The Year

25 Networking Strengths Growing together & networking strengths 25

26 FUCHS PETROLUB in figures 26

27 2014 Sales revenues increased by 3%; currency adjusments have significant impact Result at previous year s high level 2 acquisitions iti in Great Britain i and South Africa successfully completed Further increase of stronger networking Strengthening the FUCHS brand Proposed dividend increase of 10% 27

28 In 2014 the world economic growth was, despite expectations, not stronger than in the previous year Growth of GDP (gross domestic product) compared to previous year (in %) ,8 7,4 0,8 2,2 24 2,4 33 3,3 33 3,3-0,5 Euro area USA China world Quelle: IMF, Januar

29 Global development of key industries 2013/2014 Worldwide production 29 Source: FUCHS Competitive Intelligence

30 EBIT at previous year s level mn Mio. in % Sales revenues 1, , Gross profit Gross profit margin 37.2% 37.7% Admin., sales, R&D and other net operating expenses % Expenses as a percentage of sales 21.5% 21.4% EBIT before at equity income EBIT margin before at equity income 15.7% 16.3% Income from participations EBIT Earnings after tax Net profit margin 11.8% 11.9% Earnings per share in Ordinary Preference

Organic")

31 Organic sales growth of 2.7%, due to currency effects only slight increase in sales mn mn (1.9%) Organic growth 2.7% or 49.0 mn External growth 0.8% or 13.8 mn Currency effects -1.6% or mn 31

32 Organic sales growth in all three world regions high growth rate in Asia Regional sales growth 2014 Asia Pacific / Africa North- and South America Group* Organic growth Currency effects External growth mn ,8 4,3 0, Total growth + 0.8% + 3.7% + 2.8% + 1.9% Organic growth + 0.3% + 6.0% + 5.5% + 2.7% External growth + 0.9% + 0.9% 0.0% + 0.8% Currency effects - 0.4% - 3.2% - 2.7% - 1.6% * Consolidation effect mn 32

Europe* sales 1,112.9 +0.")

FUCHS sales revenues 1,865.")

North and South thamerica* sales")

33 Regional sales revenues and EBIT in 2014* mn (variance to previous year %) Asia-Pacific, Africa* sales % EBIT % EBIT margin** 16.8% (18.3) Europe* sales 1, % EBIT % EBIT margin** 14.4% (13.7) FUCHS sales revenues 1,865.9 EBIT margin** 15.7% (16.3) North and South thamerica* sales % EBIT % EBIT margin** 16.3%(20.2) * by companies location ** before at equity *** by customers location 33

34 Growth Initiative 34

35 Growth initiative we have significantly expanded our global footprint mn Main focus of investments were the construction of new plants in growth regions, the modernization and expansion of our large sites as well as an expansion of our R&D capacities. Capex Depreciation 35

36 Growth initiative: capital expenditure projects Specialty grease plants USA and China; copy German setup Test field Mannheim Modernisation of holding building Plant Mannheim

37 New jobs with focus on sales and technology 2,100 2,000 y 1,900 1,800 1,700 1,600 production & administration sales & technology Nearly 70 % of the 600 jobs created during the last 5 years were in sales and technology. 1, (Dec) 2010 (Dec) 2011 (Dec) 2012 (Dec) 2013 (Dec) 2014 (Dec) 37

38 Growth initiative: acquisitions Acquisition of the lubricant business of LUBRITENE group in May 2014 Sales approx. 15 mn p.a. Business mainly exists of lubricants for mining and the food industry Acquisition of the lubricant business of the Batoyle Freedom Group in June 2014 Sales approx. 15 mn p.a. Business exists of automotive and industrial lubricants as well as lubricants for the glass industry 38

39 Balance Sheet, Cash Flow, FVA

40 Solid balance sheet increase of equity ratio to 71.7% and net payment items of 1857mn mn Equity Equity ratio 61.1% 66.8% 70.5% 73.5% 71.7% Return on equity (ROE) 36.6% 31.0% 29.0% 26.7% 25.7% Return on capital employed (ROCE) 42.7% 39.1% 39.7% 39.7% 37.6% Net liquidity

41 Record free cash flow of 1879mn mn Gross cash flow Changes in net current asset -14,0-8.6 Changes in other current assets Operating cash flow Investments Acquisitions Other changes Free cash flow

42 Lower capital cost rate leads to an increase in FUCHS Value Added (FVA) by 3.5% FVA +3.5% EBIT 230 mn (FVA) EBIT 222 mn (FVA) EBIT +0.2% 313 mn 312 mn Cost of capital Cost of capital 83 mn 90 mn Capital employed 833 mn Cost of capital 10.0% Capital employed 786 mn Cost of capital 11.5% Capital Employed +5.9% 42

43 Outlook

44 The outlook for the world economy has brightened up at the turn of the year 2014/2015 Forecasted growth of GDP (gross domestic product) in 2015 compared to previous year (in %) Euro area USA China World Source: IMF, January

45 Development of key industries Continued strong demand for engineering and car production, recovering of chemical production, further decrease of steel production Worldwide production 45 Source: FUCHS Competitive Intelligence

46 Outlook 2015 FUCHS plans further growth in sales and volume in 2015 We expect an EBIT increase in the low digit percent range We plan investments to exceed the previous year s value and reach up to the investments of 2012 and 2013 Free cash flow is again expected to exceed 150 mn 46

47 Quarters

48 Development of quarters mn Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Sales revenues Gross profit (37.5%) (37.9%) (37.9%) (37.4%) (37.4%) (37.2%) (37.2%) (36.8%) Sales, admin., R&D expenses (21.6%) (21.5%) (20.8%) (21.5%) (21.5%) (21.6%) (20.2%) (22.6%) EBIT before income from at equity 70.2 (15.9%) 76.8 (16.4%) 80.1 (17.1 %) 71.7 (15.8 %) 72.6 (15.9%) 72.4 (15.7%) 81.9 (16.9%) 65.7 (14.2%) EBIT Earnings after ax Net profit margin 11.7 % 12.0 % 12.4 % 11.7 % 11.6% 11.4% 12.1% 12.1% 48

49 Good final spurt in the 4th quarter 2014 mn Development of sales revenues Q1 '13 Q2 '13 Q3 '13 Q4' 13 Q1 '14 Q2 '14 Q3 '14 Q4' % YoY 49

50 Good final spurt in the 4th quarter 2014 mn EBIT development Q1 '13 Q2 '13 Q3 '13 Q4 '13 Q1 '14 Q2 '14 Q3 '14 Q4 ' % YoY 50

51 Q1/2014: organic growth rose considerably in all three regions Regional sales growth 1 st quarter 2014 Asia-Pacific / Africa North- and South America Group* Organic growth Currency effects External growth mn Total growth + 7.2% + 1.4% - 0.3% + 3.3% Organic growth + 7.4% +11.0% + 7.4% + 7.3% Currency effects - 0.5% - 9.6% - 7.7% - 4.2% External growth + 0.3% 0.0% 0.0% + 0.2% * Consolidation effect mn 51

52 Q2/2014: organic growth in Asia-Pacific/Africa and Americas Regional sales growth 2 nd quarter 2014 Asia-Pacific/ Africa North and South America Group* mn Organic growth Currency effects External growth Total growth - 1.9% + 0.4% - 1.9% - 1.2% Organic growth - 1.7% + 8.3% + 5.5% + 2.3% Currency effects - 0.4% - 7.9% - 7.4% - 3.6% External growth + 0.2% 0.0% 0.0% + 0.1% * Consolidation effect 0.6 million 52

53 Q3/2014: all regions recorded growth Regional sales growth 3 rd quarter 2014 Asia-Pacific/ Africa North and South America Group* mn Organic growth Currency effects External growth Total growth + 1.5% + 7.8% + 3.3% + 3.2% Organic growth - 0.2% + 7.5% + 5.0% + 2.4% Currency effects + 0.1% - 0.3% - 1.7% - 0.3% External growth + 1.6% + 0.6% 0.0% + 1.1% * consolidation effect mn 53

54 Q4/2014: organic growth in Americas Regional sales growth 4 th quarter 2014 Asia/Pacific, Africa North and South America Group* mn Organic growth Currency effects External growth Total growth - 3.4% + 5.2% % + 2.3% Organic growth - 3.8% - 2.1% + 4.0% - 1.1% External growth + 1.3% + 2.7% 0.0% + 1.5% Currency effects - 0.9% + 4.6% + 6.8% + 1.9% * Consolidation effect mn 54

55 Shareholder Structure 55 FUCHS PETROLUB AG SE

56 Breakdown of shares Ordinary shares Preference shares Free float * 47 % Fuchs family 53 % Free float 100 % 69,500,000 ordinary shares 69,500,000 preference shares *) voting rights notification: DWS Investment, Frankfurt: 5.2% (15 Dec. 2003) 56

57 Thank you for your attention Disclaimer This presentation ti contains statements t t about future development thatt are based on assumptions and estimates by the management of FUCHS PETROLUB SE. Even if the management is of the opinion that these assumptions and estimates are accurate, future actual developments and future actual results may differ significantly from these assumptions and estimates due to a variety of factors. These factors can include changes in the overall economic climate, procurement prices, changes to exchange rates and interest rates, and changes in the lubricants industry. FUCHS PETROLUB SE provides no guarantee that future developments and the results actually achieved in the future will match the assumptions and estimates set out in this presentation and assumes no liability for such. 57

58 Investor Relations Friesenheimer Str Mannheim Telefon +49 (0) , Fax +49 (0)

FUCHS PETROLUB SE The leading independent lubricants manufacturer of the world

FUCHS PETROLUB SE The leading independent lubricants manufacturer of the world Dr. Alexander Selent, Vice Chairman & CFO Reiner Schmidt, GMC-Member Warburg Highlights - Handout June 2015 The leading independent

FUCHS PETROLUB SE The leading independent lubricants manufacturer of the world Dr. Alexander Selent, Vice Chairman & CFO Reiner Schmidt, GMC-Member Warburg Highlights - Handout June 2015 The leading independent

FUCHS PETROLUB SE The leading independent lubricants manufacturer of the world

The leading independent lubricants manufacturer of the world Dr. Alexander Selent, Vice Chairman & CFO Dagmar Steinert, Head of Investor Relations January 2015 The leading independent lubricants manufacturer

The leading independent lubricants manufacturer of the world Dr. Alexander Selent, Vice Chairman & CFO Dagmar Steinert, Head of Investor Relations January 2015 The leading independent lubricants manufacturer

FUCHS PETROLUB SE The leading independent lubricants manufacturer of the world

The leading independent lubricants manufacturer of the world Dr. Alexander Selent, Vice Chairman & CFO Dagmar Steinert, Head of Investor Relations September 2014 The leading independent lubricants manufacturer

The leading independent lubricants manufacturer of the world Dr. Alexander Selent, Vice Chairman & CFO Dagmar Steinert, Head of Investor Relations September 2014 The leading independent lubricants manufacturer

FUCHS PETROLUB SE The leading independent lubricants manufacturer of the world

The leading independent lubricants manufacturer of the world Dr. Alexander Selent, Vice Chairman & CFO Dagmar Steinert, Head of Investor Relations Main First Bank, Zurich, 5 June 2014 The leading independent

The leading independent lubricants manufacturer of the world Dr. Alexander Selent, Vice Chairman & CFO Dagmar Steinert, Head of Investor Relations Main First Bank, Zurich, 5 June 2014 The leading independent

FUCHS PETROLUB SE The leading independent lubricants manufacturer of the world

FUCHS PETROLUB SE The leading independent lubricants manufacturer of the world Dr. Alexander Selent, Vice Chairman & CFO Dagmar Steinert, Head of Investor Relations DZ BANK Equity Conference on 18 and

FUCHS PETROLUB SE The leading independent lubricants manufacturer of the world Dr. Alexander Selent, Vice Chairman & CFO Dagmar Steinert, Head of Investor Relations DZ BANK Equity Conference on 18 and

FUCHS PETROLUB AG The leading independent lubricants manufacturer of the world

The leading independent lubricants manufacturer of the world Dr. Alexander Selent, Vice Chairman & CFO Dagmar Steinert, Head of Investor Relations April 2013 FUCHS the leading independent lubricants manufacturer

The leading independent lubricants manufacturer of the world Dr. Alexander Selent, Vice Chairman & CFO Dagmar Steinert, Head of Investor Relations April 2013 FUCHS the leading independent lubricants manufacturer

FUCHS PETROLUB AG. manufacturer of the world. Tina Vogel, Head of Public Relations. MainFirst Chemicals One-on-One Forum 27 June 2013

The leading independent lubricants manufacturer of the world Reiner Schmidt, Member of the Group Management Committee Tina Vogel, Head of Public Relations MainFirst Chemicals One-on-One Forum 27 June 2013

The leading independent lubricants manufacturer of the world Reiner Schmidt, Member of the Group Management Committee Tina Vogel, Head of Public Relations MainFirst Chemicals One-on-One Forum 27 June 2013

FUCHS GROUP. Setting Standards - Worldwide

FUCHS GROUP Setting Standards - Worldwide dbaccess German, Swiss & Austrian Conference, 8 th June 2016, Berlin Stefan Fuchs, CEO Thomas Altmann, Investor Relations Agenda 01 The Leading Independent Lubricants

FUCHS GROUP Setting Standards - Worldwide dbaccess German, Swiss & Austrian Conference, 8 th June 2016, Berlin Stefan Fuchs, CEO Thomas Altmann, Investor Relations Agenda 01 The Leading Independent Lubricants

FUCHS GROUP. Setting Standards - Worldwide

FUCHS GROUP Setting Standards - Worldwide Commerzbank Sector Conference, 30 th August 2016, Frankfurt Dagmar Steinert, CFO Thomas Altmann, Investor Relations Agenda 01 The Leading Independent Lubricants

FUCHS GROUP Setting Standards - Worldwide Commerzbank Sector Conference, 30 th August 2016, Frankfurt Dagmar Steinert, CFO Thomas Altmann, Investor Relations Agenda 01 The Leading Independent Lubricants

FUCHS PETROLUB SE. Roadshow Presentation. 23 rd March 2016 Frankfurt Dagmar Steinert / Thomas Altmann

FUCHS PETROLUB SE Roadshow Presentation 23 rd March 2016 Frankfurt Dagmar Steinert / Thomas Altmann Agenda 01 02 03 04 Our company Consolidated Financial Statements 2015 Balance Sheet, Cash flow, FVA 2015

FUCHS PETROLUB SE Roadshow Presentation 23 rd March 2016 Frankfurt Dagmar Steinert / Thomas Altmann Agenda 01 02 03 04 Our company Consolidated Financial Statements 2015 Balance Sheet, Cash flow, FVA 2015

FUCHS GROUP. Setting Standards - Worldwide. September 2016, Munich Dagmar Steinert, CFO Thomas Altmann, Investor Relations

FUCHS GROUP Setting Standards - Worldwide September 2016, Munich Dagmar Steinert, CFO Thomas Altmann, Investor Relations Agenda 01 The Leading Independent Lubricants Company 02 H1 2016 03 Shares 04 Appendix

FUCHS GROUP Setting Standards - Worldwide September 2016, Munich Dagmar Steinert, CFO Thomas Altmann, Investor Relations Agenda 01 The Leading Independent Lubricants Company 02 H1 2016 03 Shares 04 Appendix

FUCHS GROUP. Setting Standards - Worldwide. Roadshow Presentation November 2016 Dagmar Steinert, CFO Thomas Altmann, Investor Relations

FUCHS GROUP Setting Standards - Worldwide Roadshow Presentation November 2016 Dagmar Steinert, CFO Thomas Altmann, Investor Relations Agenda 01 The Leading Independent Lubricants Company 02 Q1-3 2016 03

FUCHS GROUP Setting Standards - Worldwide Roadshow Presentation November 2016 Dagmar Steinert, CFO Thomas Altmann, Investor Relations Agenda 01 The Leading Independent Lubricants Company 02 Q1-3 2016 03

FUCHS GROUP. In Motion. Company Presentation, May 2017 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations

FUCHS GROUP In Motion Company Presentation, May 2017 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations Agenda 01 The Leading Independent Lubricants Company 02 Q1 2017 03 Shares 04 Appendix

FUCHS GROUP In Motion Company Presentation, May 2017 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations Agenda 01 The Leading Independent Lubricants Company 02 Q1 2017 03 Shares 04 Appendix

FUCHS GROUP. Setting Standards - Worldwide. Company Presentation, January 2017 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations

FUCHS GROUP Setting Standards - Worldwide Company Presentation, January 2017 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations Agenda 01 The Leading Independent Lubricants Company 02 Q1-3

FUCHS GROUP Setting Standards - Worldwide Company Presentation, January 2017 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations Agenda 01 The Leading Independent Lubricants Company 02 Q1-3

FUCHS GROUP. In Motion. Investor Presentation, June 2017 Stefan Fuchs, CEO Thomas Altmann, Head of Investor Relations

FUCHS GROUP In Motion Investor Presentation, June 2017 Stefan Fuchs, CEO Thomas Altmann, Head of Investor Relations Agenda 01 The Leading Independent Lubricants Company 02 Q1 2017 03 Shares 04 Appendix

FUCHS GROUP In Motion Investor Presentation, June 2017 Stefan Fuchs, CEO Thomas Altmann, Head of Investor Relations Agenda 01 The Leading Independent Lubricants Company 02 Q1 2017 03 Shares 04 Appendix

FUCHS GROUP. Setting Standards - Worldwide. Company Presentation, March 2017 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations

FUCHS GROUP Setting Standards - Worldwide Company Presentation, March 2017 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations Agenda 01 The Leading Independent Lubricants Company 02 FY 2016

FUCHS GROUP Setting Standards - Worldwide Company Presentation, March 2017 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations Agenda 01 The Leading Independent Lubricants Company 02 FY 2016

FUCHS GROUP. In Motion. Investor Presentation, November 2017 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations

FUCHS GROUP In Motion Investor Presentation, November 2017 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations Agenda 01 02 03 04 The Leading Independent Lubricants Company Q1-3 2017 Shares

FUCHS GROUP In Motion Investor Presentation, November 2017 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations Agenda 01 02 03 04 The Leading Independent Lubricants Company Q1-3 2017 Shares

FUCHS GROUP. In Motion. Investor Presentation, September 2017 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations

FUCHS GROUP In Motion Investor Presentation, September 2017 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations Agenda 01 02 The Leading Independent Lubricants Company H1 2017 03 Shares 04

FUCHS GROUP In Motion Investor Presentation, September 2017 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations Agenda 01 02 The Leading Independent Lubricants Company H1 2017 03 Shares 04

FUCHS PETROLUB AG. Dagmar Steinert, Head of Investor Relations. May 2013

The lubricants specialist Stefan Fuchs, CEO Dagmar Steinert, Head of Investor Relations May 2013 Overview and business model 2 FUCHS the lubricants specialist Founded d in 1931 2012 sales revenues: 1.8

The lubricants specialist Stefan Fuchs, CEO Dagmar Steinert, Head of Investor Relations May 2013 Overview and business model 2 FUCHS the lubricants specialist Founded d in 1931 2012 sales revenues: 1.8

FUCHS PETROLUB SE Capital Market Day

Capital Market Day Stefan Fuchs, Chairman of the Board Dr. Alexander Selent, Vice Chairman & CFO 17 September 2014 Group organisation Stefan Fuchs Dr. Alexander Selent Dr. Lutz Lindemann Dr. Ralph Rheinboldt

Capital Market Day Stefan Fuchs, Chairman of the Board Dr. Alexander Selent, Vice Chairman & CFO 17 September 2014 Group organisation Stefan Fuchs Dr. Alexander Selent Dr. Lutz Lindemann Dr. Ralph Rheinboldt

FUCHS GROUP. Setting Standards - Worldwide. FUCHS Capital Market Day, 8 th September 2016, Mannheim Stefan Fuchs, CEO Dagmar Steinert, CFO

FUCHS GROUP Setting Standards - Worldwide FUCHS Capital Market Day, 8 th September 2016, Mannheim Stefan Fuchs, CEO Dagmar Steinert, CFO The executive board Stefan Fuchs: CEO, Corporate Development, HR,

FUCHS GROUP Setting Standards - Worldwide FUCHS Capital Market Day, 8 th September 2016, Mannheim Stefan Fuchs, CEO Dagmar Steinert, CFO The executive board Stefan Fuchs: CEO, Corporate Development, HR,

FUCHS GROUP. New Thinking. FUCHS Capital Market Day, June 2018 Stefan Fuchs, CEO Dagmar Steinert, CFO

FUCHS GROUP New Thinking FUCHS Capital Market Day, June 2018 Stefan Fuchs, CEO Dagmar Steinert, CFO FUCHS at a glance Established 3 generations ago as a family-owned business No. 1 among the independent

FUCHS GROUP New Thinking FUCHS Capital Market Day, June 2018 Stefan Fuchs, CEO Dagmar Steinert, CFO FUCHS at a glance Established 3 generations ago as a family-owned business No. 1 among the independent

FUCHS PETROLUB SE The lubricants specialist

The lubricants specialist Stefan Fuchs, CEO Reiner Schmidt, Member of the Group Management Committee Commerzbank Sector Conference Week 27 August 2013 Overview and business model 2 FUCHS the lubricants

The lubricants specialist Stefan Fuchs, CEO Reiner Schmidt, Member of the Group Management Committee Commerzbank Sector Conference Week 27 August 2013 Overview and business model 2 FUCHS the lubricants

FUCHS PETROLUB / 1st half year 2014 Analyst Conference Call

FUCHS PETROLUB / 1st half year 2014 Analyst Conference Call Dr. Alexander Selent, Vice Chairman & CFO Reiner Schmidt, Member of the Group Management Committee Dagmar Steinert, Head of Investor Relations

FUCHS PETROLUB / 1st half year 2014 Analyst Conference Call Dr. Alexander Selent, Vice Chairman & CFO Reiner Schmidt, Member of the Group Management Committee Dagmar Steinert, Head of Investor Relations

FUCHS GROUP. In Motion. Investor Presentation, January 2018 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations

FUCHS GROUP In Motion Investor Presentation, January 2018 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations Agenda 01 02 03 04 The Leading Independent Lubricants Company Q1-3 2017 Shares

FUCHS GROUP In Motion Investor Presentation, January 2018 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations Agenda 01 02 03 04 The Leading Independent Lubricants Company Q1-3 2017 Shares

FUCHS PETROLUB / Q1 2013

FUCHS PETROLUB / Q1 2013 Conference Call Dr. Alexander Selent, Vice Chairman and CFO Reiner Schmidt, Member of the Group Management Committee Mannheim, 2 May 2013 FUCHS increases EBIT to 73.4 million and

FUCHS PETROLUB / Q1 2013 Conference Call Dr. Alexander Selent, Vice Chairman and CFO Reiner Schmidt, Member of the Group Management Committee Mannheim, 2 May 2013 FUCHS increases EBIT to 73.4 million and

FUCHS PETROLUB / Q2/2015 Conference Call

FUCHS PETROLUB / Q2/2015 Conference Call Dr. Alexander Selent, Vice Chairman & CFO Dagmar Steinert, Head of Investor Relations Mannheim, 4 August 2015 For the first time FUCHS generates group sales of

FUCHS PETROLUB / Q2/2015 Conference Call Dr. Alexander Selent, Vice Chairman & CFO Dagmar Steinert, Head of Investor Relations Mannheim, 4 August 2015 For the first time FUCHS generates group sales of

FUCHS PETROLUB / Q Conference Call

FUCHS PETROLUB / Q1 2014 Conference Call Dr. Alexander Selent, Vice Chairman & CFO Dagmar Steinert, Head of Investor Relations Mannheim, 5 May 2014 Changes in the Board of Directors of Dr. Georg Lingg,

FUCHS PETROLUB / Q1 2014 Conference Call Dr. Alexander Selent, Vice Chairman & CFO Dagmar Steinert, Head of Investor Relations Mannheim, 5 May 2014 Changes in the Board of Directors of Dr. Georg Lingg,

FUCHS GROUP. New Thinking. Investor Presentation, March 2018 Thomas Altmann, Head of Investor Relations

FUCHS GROUP New Thinking Investor Presentation, March 2018 Thomas Altmann, Head of Investor Relations Agenda 01 02 03 04 The Leading Independent Lubricants Company FY 2017 Shares Appendix l 2 01 The Leading

FUCHS GROUP New Thinking Investor Presentation, March 2018 Thomas Altmann, Head of Investor Relations Agenda 01 02 03 04 The Leading Independent Lubricants Company FY 2017 Shares Appendix l 2 01 The Leading

FUCHS GROUP. New Thinking. Investor Presentation, September 2018

FUCHS GROUP New Thinking Investor Presentation, September 2018 Agenda 01 02 03 04 The Leading Independent Lubricants Company H1 2018 Shares Appendix l 2 01 The Leading Independent Lubricants Company FUCHS

FUCHS GROUP New Thinking Investor Presentation, September 2018 Agenda 01 02 03 04 The Leading Independent Lubricants Company H1 2018 Shares Appendix l 2 01 The Leading Independent Lubricants Company FUCHS

FUCHS GROUP. New Thinking. Investor Presentation, June 2018 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations

FUCHS GROUP New Thinking Investor Presentation, June 2018 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations Agenda 01 02 03 04 The Leading Independent Lubricants Company Q1 2018 Shares Appendix

FUCHS GROUP New Thinking Investor Presentation, June 2018 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations Agenda 01 02 03 04 The Leading Independent Lubricants Company Q1 2018 Shares Appendix

FUCHS GROUP. Investor Presentation. November 2018 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations

FUCHS GROUP Investor Presentation November 2018 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations Agenda 01 02 03 04 The Leading Independent Lubricants Company Q1-3 2018 Shares Appendix l

FUCHS GROUP Investor Presentation November 2018 Dagmar Steinert, CFO Thomas Altmann, Head of Investor Relations Agenda 01 02 03 04 The Leading Independent Lubricants Company Q1-3 2018 Shares Appendix l

FUCHS Group. Financial Results Analysts' Conference, 21 st March 2017, Frankfurt Stefan Fuchs, CEO Dagmar Steinert, CFO

FUCHS Group Financial Results 2016 Analysts' Conference, 21 st March 2017, Frankfurt Stefan Fuchs, CEO Dagmar Steinert, CFO Agenda 01 Full Year 2016 02 Outlook 2017 l 2 01 Full Year 2016 Highlights FY

FUCHS Group Financial Results 2016 Analysts' Conference, 21 st March 2017, Frankfurt Stefan Fuchs, CEO Dagmar Steinert, CFO Agenda 01 Full Year 2016 02 Outlook 2017 l 2 01 Full Year 2016 Highlights FY

FUCHS GROUP. Financial Results Analyst s Conference, 21 st March 2018, Frankfurt Stefan Fuchs, CEO Dagmar Steinert, CFO

FUCHS GROUP Financial Results 2017 Analyst s Conference, 21 st March 2018, Frankfurt Stefan Fuchs, CEO Dagmar Steinert, CFO Highlights FY 2017 Sales +9% to 2.5 bn Strong organic growth in Asia-Pacific,

FUCHS GROUP Financial Results 2017 Analyst s Conference, 21 st March 2018, Frankfurt Stefan Fuchs, CEO Dagmar Steinert, CFO Highlights FY 2017 Sales +9% to 2.5 bn Strong organic growth in Asia-Pacific,

Q Quarterly Statement as at September 30, 2016

Q1 3 2016 Quarterly Statement as at September 30, 2016 Sales revenues increase by 11 % to 1.7 billion Earnings (EBIT) up 6 % to 276 million Outlook for the financial year 2016 reaffirmed: Organic and acquisition-based

Q1 3 2016 Quarterly Statement as at September 30, 2016 Sales revenues increase by 11 % to 1.7 billion Earnings (EBIT) up 6 % to 276 million Outlook for the financial year 2016 reaffirmed: Organic and acquisition-based

+2 % Earnings (EBIT) increase

increase") Statement as at September 30 Q3Quarterly 2017 Sales revenues rise by 9 % to 1,862 million +2 % Earnings (EBIT) increase Earnings outlook adjusted to 281 million Content FUCHS at a glance 03 Business development

Statement as at September 30 Q3Quarterly 2017 Sales revenues rise by 9 % to 1,862 million +2 % Earnings (EBIT) increase Earnings outlook adjusted to 281 million Content FUCHS at a glance 03 Business development

+ 6 % Earnings (EBIT) increase to 297 million

increase to 297 million") Quarterly statement as at September 30, 2018 Q3 / 2018 Sales revenues up by 5 % to 1,953 million + 6 % Earnings (EBIT) increase to 297 million (including one-off effect) Outlook updated: Sales revenue

Quarterly statement as at September 30, 2018 Q3 / 2018 Sales revenues up by 5 % to 1,953 million + 6 % Earnings (EBIT) increase to 297 million (including one-off effect) Outlook updated: Sales revenue

QUARTERLY REPORT. For the first half of >> Profit for first half considerably higher than previous year Second quarter confirms positive outlook

QUARTERLY REPORT For the first half of 2007 >> Profit for first half considerably higher than previous year Second quarter confirms positive outlook FUCHS PETROLUB AG THE FIRST HALF 2007 AT A GLANCE [in

QUARTERLY REPORT For the first half of 2007 >> Profit for first half considerably higher than previous year Second quarter confirms positive outlook FUCHS PETROLUB AG THE FIRST HALF 2007 AT A GLANCE [in

Outlook unchanged: Sales revenues up by 4 % to 643 million. Quarterly Statement as at March 31 Q1 / 2018

Quarterly Statement as at March 31 Q1 / 2018 Sales revenues up by 4 % to 643 million Currencies ( 6 %) burden organic (+ 10 %) EBIT of 92 million down 2 % on previous year s high level due to currency

Quarterly Statement as at March 31 Q1 / 2018 Sales revenues up by 4 % to 643 million Currencies ( 6 %) burden organic (+ 10 %) EBIT of 92 million down 2 % on previous year s high level due to currency

H Half-year financial report as at June 30

H1 2016 Half-year financial report as at June 30 Sales revenues up by 13 % to 1,136 million Earnings (EBIT) increase to 183 million (+7 %) Outlook reaffirmed Content FUCHS at a glance 03 Half-year financial

H1 2016 Half-year financial report as at June 30 Sales revenues up by 13 % to 1,136 million Earnings (EBIT) increase to 183 million (+7 %) Outlook reaffirmed Content FUCHS at a glance 03 Half-year financial

FUCHS GROUP. Financial Results Q Analyst s Conference, 30 th October 2018 Dagmar Steinert, CFO

FUCHS GROUP Financial Results Q1-3 2018 Analyst s Conference, 30 th October 2018 Dagmar Steinert, CFO Highlights Q1-3 2018 Sales +5% to 1,953 mn EBIT increase by 6% to 297 mn (including 12 mn one-off effect)

FUCHS GROUP Financial Results Q1-3 2018 Analyst s Conference, 30 th October 2018 Dagmar Steinert, CFO Highlights Q1-3 2018 Sales +5% to 1,953 mn EBIT increase by 6% to 297 mn (including 12 mn one-off effect)

FOR THE FIRST QUARTER OF

Fall in demand continues As expected the profit after tax of 16.2 million remained at the level of the fourth quarter of 2008 Cost-cutting measures are taking effect Free cash flow rose to 39 million Group

Fall in demand continues As expected the profit after tax of 16.2 million remained at the level of the fourth quarter of 2008 Cost-cutting measures are taking effect Free cash flow rose to 39 million Group

Henkel AG & Co. KGaA. Klaus Keutmann Frankfurt,

Henkel AG & Co. KGaA Klaus Keutmann Frankfurt, 21.01.2015 Disclaimer This information contains forward-looking statements which are based on current estimates and assumptions made by the corporate management

Henkel AG & Co. KGaA Klaus Keutmann Frankfurt, 21.01.2015 Disclaimer This information contains forward-looking statements which are based on current estimates and assumptions made by the corporate management

BUSINESS YEAR 2017/18 1 st QUARTER

BUSINESS YEAR 2017/18 1 st QUARTER Investor Relations September 2017 www.voestalpine.com voestalpine GROUP OVERVIEW» voestalpine is a leading technology and capital goods group with combined material and

BUSINESS YEAR 2017/18 1 st QUARTER Investor Relations September 2017 www.voestalpine.com voestalpine GROUP OVERVIEW» voestalpine is a leading technology and capital goods group with combined material and

2014 Interim report as at March 31

2014 Interim report as at March 31 sales revenues up 3.3 % despite unfavorable currency effects earnings before interest and tax (EBIT) increase by 3.0 % to 75.6 million outlook for the financial year

2014 Interim report as at March 31 sales revenues up 3.3 % despite unfavorable currency effects earnings before interest and tax (EBIT) increase by 3.0 % to 75.6 million outlook for the financial year

Quaker Chemical Corporation. Investor Presentation. August 2016

Quaker Chemical Corporation Investor Presentation August 2016 1 Risk and Uncertainties Statement Regulation G The attached charts include Company information that does not conform to generally accepted

Quaker Chemical Corporation Investor Presentation August 2016 1 Risk and Uncertainties Statement Regulation G The attached charts include Company information that does not conform to generally accepted

Investors Conference quirin Champions 2017

Investors Conference quirin Champions 2017 June 1, 2017, Frankfurt Clear focus. Sharpened profile. Draft, version 4, as of 3/8/2016, 11:20 a.m. Disclaimer Note: This presentation contains statements concerning

Investors Conference quirin Champions 2017 June 1, 2017, Frankfurt Clear focus. Sharpened profile. Draft, version 4, as of 3/8/2016, 11:20 a.m. Disclaimer Note: This presentation contains statements concerning

Investors Conference Commerzbank Sector Conference

Investors Conference Commerzbank Sector Conference August 30, 2017, Frankfurt Clear focus. Sharpened profile. Draft, version 4, as of 3/8/2016, 11:20 a.m. Disclaimer Note: This presentation contains statements

Investors Conference Commerzbank Sector Conference August 30, 2017, Frankfurt Clear focus. Sharpened profile. Draft, version 4, as of 3/8/2016, 11:20 a.m. Disclaimer Note: This presentation contains statements

Bilfinger Berger: Entering new growth phase

Bilfinger Berger: Entering new growth phase Roadshow London, Roland Koch, CEO Andreas Müller, Head of Corporate Accounting and Investor Relations Agenda 1. Bilfinger Berger Overview 2. Preliminary figures

Bilfinger Berger: Entering new growth phase Roadshow London, Roland Koch, CEO Andreas Müller, Head of Corporate Accounting and Investor Relations Agenda 1. Bilfinger Berger Overview 2. Preliminary figures

ThyssenKrupp AG 3rd Annual Stockholders Meeting

1 AG 3rd Annual Stockholders Meeting Essen, March 1, 2002 Report by the Executive Board Chairman 2 The Group s strategy stock An overview of fiscal year 2000/2001 1st quarter 2001/2002 and outlook strategic

1 AG 3rd Annual Stockholders Meeting Essen, March 1, 2002 Report by the Executive Board Chairman 2 The Group s strategy stock An overview of fiscal year 2000/2001 1st quarter 2001/2002 and outlook strategic

Stockholm & Copenhagen Cheuvreux

Stockholm & Copenhagen Cheuvreux November 7-8, 2012 1 // Stockholm & Copenhagen Cheuvreux November 7-8, 2012 OUTLINE 01 High profitability in first-half 2012 02 Structurally expanding markets 03 Widening

Stockholm & Copenhagen Cheuvreux November 7-8, 2012 1 // Stockholm & Copenhagen Cheuvreux November 7-8, 2012 OUTLINE 01 High profitability in first-half 2012 02 Structurally expanding markets 03 Widening

ANALYSTS CONFERENCE 2011

ANALYSTS CONFERENCE 2011 Metzingen March 29, 2011 Analysts Conference 2011 HUGO BOSS March 29, 2011 2 / 48 AGENDA 2010 HIGHLIGHTS GROWTH STRATEGY 2010 FINANCIAL YEAR OUTLOOK Analysts Conference 2011 HUGO

ANALYSTS CONFERENCE 2011 Metzingen March 29, 2011 Analysts Conference 2011 HUGO BOSS March 29, 2011 2 / 48 AGENDA 2010 HIGHLIGHTS GROWTH STRATEGY 2010 FINANCIAL YEAR OUTLOOK Analysts Conference 2011 HUGO

BUSINESS YEAR 2017/18 2 nd QUARTER, 1 st HALF

BUSINESS YEAR 2017/18 2 nd QUARTER, 1 st HALF Investor Relations November 2017 www.voestalpine.com OVERVIEW BUSINESS MODEL» voestalpine is a leading technology and capital goods group with combined material

BUSINESS YEAR 2017/18 2 nd QUARTER, 1 st HALF Investor Relations November 2017 www.voestalpine.com OVERVIEW BUSINESS MODEL» voestalpine is a leading technology and capital goods group with combined material

Report on financial year 2014 March 26, 2015, Frankfurt. Dr. h.c. Hans M. Schabert, CEO Oliver Schuster, CFO

Report on financial year 2014 March 26, 2015, Frankfurt Dr. h.c. Hans M. Schabert, CEO Oliver Schuster, CFO Transforming Vossloh Main areas of action 2014 Comprehensive analysis and re-evaluation of the

Report on financial year 2014 March 26, 2015, Frankfurt Dr. h.c. Hans M. Schabert, CEO Oliver Schuster, CFO Transforming Vossloh Main areas of action 2014 Comprehensive analysis and re-evaluation of the

FINANCIAL REPORT 30 NOVEMBER ST HALF OF FISCAL YEAR 2017/2018

FINANCIAL REPORT 30 NOVEMBER 2017 1ST HALF OF FISCAL YEAR 2017/2018 CONTENTS 03 KEY PERFORMANCE INDICATORS 04 HIGHLIGHTS 05 HELLA ON THE CAPITAL MARKET 07 INTERIM GROUP MANAGEMENT REPORT 07 Economic development

FINANCIAL REPORT 30 NOVEMBER 2017 1ST HALF OF FISCAL YEAR 2017/2018 CONTENTS 03 KEY PERFORMANCE INDICATORS 04 HIGHLIGHTS 05 HELLA ON THE CAPITAL MARKET 07 INTERIM GROUP MANAGEMENT REPORT 07 Economic development

FINANCIAL RESULTS 2012 CONTINUED REVENUE GROWTH, ABOVE AVERAGE INCREASE IN PROFIT AND FURTHER INVESTMENTS IN EMERGING MARKETS

FINANCIAL RESULTS 2012 CONTINUED REVENUE GROWTH, ABOVE AVERAGE INCREASE IN PROFIT AND FURTHER INVESTMENTS IN EMERGING MARKETS SIKA ROADSHOW PRESENTATION / BAAR MARCH 2013 SHORT LIST World market leader

FINANCIAL RESULTS 2012 CONTINUED REVENUE GROWTH, ABOVE AVERAGE INCREASE IN PROFIT AND FURTHER INVESTMENTS IN EMERGING MARKETS SIKA ROADSHOW PRESENTATION / BAAR MARCH 2013 SHORT LIST World market leader

Schaeffler AG 17 th GCC Kepler Cheuvreux. Jan 17, 2018 Frankfurt

Schaeffler AG 17 th GCC Kepler Cheuvreux Jan 17, 2018 Frankfurt Disclaimer This presentation contains forward-looking statements. The words "anticipate", "assume", "believe", "estimate", "expect", "intend",

Schaeffler AG 17 th GCC Kepler Cheuvreux Jan 17, 2018 Frankfurt Disclaimer This presentation contains forward-looking statements. The words "anticipate", "assume", "believe", "estimate", "expect", "intend",

SCHMOLZ + BICKENBACH. BNP Paribas 13 th Annual High Yield and Leveraged Finance Conference. London, 19 January 2017

SCHMOLZ + BICKENBACH BNP Paribas 13 th Annual High Yield and Leveraged Finance Conference London, 19 January 2017 DISCLAIMER Forward-looking statements Information in this presentation may contain forward-looking

SCHMOLZ + BICKENBACH BNP Paribas 13 th Annual High Yield and Leveraged Finance Conference London, 19 January 2017 DISCLAIMER Forward-looking statements Information in this presentation may contain forward-looking

Analysts Conference Full Year Results 2004 Frankfurt, March 22, pm

Analysts Conference Full Year Results 2004 Frankfurt, March 22, 2005 3.00pm Page 4 Page 17 Page 32 Presentation of Dr Wolfgang Reitzle President & CEO, Linde AG Presentation of Dr Peter Diesch CFO, Linde

Analysts Conference Full Year Results 2004 Frankfurt, March 22, 2005 3.00pm Page 4 Page 17 Page 32 Presentation of Dr Wolfgang Reitzle President & CEO, Linde AG Presentation of Dr Peter Diesch CFO, Linde

Full-Year / Fourth Quarter 2010 Results

Full-Year / Fourth Quarter 2010 Results 16 February 2011 Disclaimer This presentation contains certain statements that are neither reported financial results nor other historical information. This presentation

Full-Year / Fourth Quarter 2010 Results 16 February 2011 Disclaimer This presentation contains certain statements that are neither reported financial results nor other historical information. This presentation

Results FY 2017 Schaeffler AG. Conference Call March 7, 2018 Munich

Results FY 2017 Schaeffler AG Conference Call Munich Disclaimer This presentation contains forward-looking statements. The words "anticipate", "assume", "believe", "estimate", "expect", "intend", "may",

Results FY 2017 Schaeffler AG Conference Call Munich Disclaimer This presentation contains forward-looking statements. The words "anticipate", "assume", "believe", "estimate", "expect", "intend", "may",

2018 Results and Outlook. February 22, 2019

2018 Results and Outlook February 22, 2019 1. 2018 HIGHLIGHTS 2. 2018 RESULTS 3. STRATEGY 4. OUTLOOK 2 / Sales Actual Like-for-like Operating income Actual 41.8bn +2.4% +4.4% 3,122m +3.1% +4.5% Operating

2018 Results and Outlook February 22, 2019 1. 2018 HIGHLIGHTS 2. 2018 RESULTS 3. STRATEGY 4. OUTLOOK 2 / Sales Actual Like-for-like Operating income Actual 41.8bn +2.4% +4.4% 3,122m +3.1% +4.5% Operating

Press Release May 31, 2017

ISRA VISION AG: 1st half year 2016 / 2017 A further step to 150 +: Revenues and EBT each grow by +11% Double-digit growth in the first six months ISRA continues growth path with high order backlog Revenues

ISRA VISION AG: 1st half year 2016 / 2017 A further step to 150 +: Revenues and EBT each grow by +11% Double-digit growth in the first six months ISRA continues growth path with high order backlog Revenues

2007 Revenue and Results. 2007: strong increase in results Strengthened growth momentum. February 15 th, 2008

2007 Revenue and Results 2007: strong increase in results Strengthened growth momentum February 15 th, 2008 2007 revenue and results Agenda A successful 2007 Be the recognized industry leader John Glen

2007 Revenue and Results 2007: strong increase in results Strengthened growth momentum February 15 th, 2008 2007 revenue and results Agenda A successful 2007 Be the recognized industry leader John Glen

Strong performance in a challenging environment

Investor Relations News February 20, 2014 Henkel delivers on 2013 financial targets Strong performance in a challenging environment Solid organic sales growth of 3.5% Sales impacted by foreign exchange

Investor Relations News February 20, 2014 Henkel delivers on 2013 financial targets Strong performance in a challenging environment Solid organic sales growth of 3.5% Sales impacted by foreign exchange

Investors Conference HSBC SRI Conference. February 7, 2017, Frankfurt. Driving transformation. Shaping the future.

Investors Conference HSBC SRI Conference February 7, 2017, Frankfurt Driving transformation. Shaping the future. Disclaimer Note: This presentation contains statements concerning the future business trend

Investors Conference HSBC SRI Conference February 7, 2017, Frankfurt Driving transformation. Shaping the future. Disclaimer Note: This presentation contains statements concerning the future business trend

TUBOS REUNIDOS GROUP. Special Products & Integral Services Worldwide. Tubos Reunidos. February 2015

Special Products & Integral Services Worldwide Tubos Reunidos Content Tubos Reunidos Group 1. Company Overview 2. 2014 2017 Strategic Plan 3. TR-MISI-JFE: Strategic Agreement 4. Financials 2 1. Company

Special Products & Integral Services Worldwide Tubos Reunidos Content Tubos Reunidos Group 1. Company Overview 2. 2014 2017 Strategic Plan 3. TR-MISI-JFE: Strategic Agreement 4. Financials 2 1. Company

Henkel FY Kasper Rorsted Carsten Knobel. Düsseldorf, February 25th, 2016

Henkel FY 2015 Kasper Rorsted Carsten Knobel Düsseldorf, February 25th, 2016 Disclaimer This information contains forward-looking statements which are based on current estimates and assumptions made by

Henkel FY 2015 Kasper Rorsted Carsten Knobel Düsseldorf, February 25th, 2016 Disclaimer This information contains forward-looking statements which are based on current estimates and assumptions made by

The KME Group. Roadshow. July, 2006

The KME Group Roadshow July, 2006 Disclaimer THESE SLIDES HAVE BEEN PREPARED BY THE COMPANY SOLELY FOR THE USE AT THE ANALYST PRESENTATION THE INFORMATION CONTAINED HEREIN HAS NOT BEEN INDEPENDENTLY VERIFIED.

The KME Group Roadshow July, 2006 Disclaimer THESE SLIDES HAVE BEEN PREPARED BY THE COMPANY SOLELY FOR THE USE AT THE ANALYST PRESENTATION THE INFORMATION CONTAINED HEREIN HAS NOT BEEN INDEPENDENTLY VERIFIED.

Rosenbauer Group. Person. Date. Investors presentation April 6, 2018

Rosenbauer Group Person Investors presentation April 6, 2018 Date Industry development In 2017, world firefighting market falls behind strong global GDP growth Better investment climate and increased demand

Rosenbauer Group Person Investors presentation April 6, 2018 Date Industry development In 2017, world firefighting market falls behind strong global GDP growth Better investment climate and increased demand

2017: another year of progress. Q1 2018: Net sales up 1.4% at constant exchange rates guidance confirmed. Shareholder commitment

1 May 18, 2018 ANNUAL SHAREHOLDERS MEETING 1 2017: another year of progress 2 Q1 2018: Net sales up 1.4% at constant exchange rates 3 2018 guidance confirmed 4 Shareholder commitment 2 May 18, 2018 ANNUAL

1 May 18, 2018 ANNUAL SHAREHOLDERS MEETING 1 2017: another year of progress 2 Q1 2018: Net sales up 1.4% at constant exchange rates 3 2018 guidance confirmed 4 Shareholder commitment 2 May 18, 2018 ANNUAL

Full Year Results 2013

Full Year Results 17 March 2014 Senior management team Dr. Thomas Buchholz Sascha Rosengart Andreas Rydzewski CEO Pumps & Engine Components CFO Member of Management Board Brake Discs With SHW since 24

Full Year Results 17 March 2014 Senior management team Dr. Thomas Buchholz Sascha Rosengart Andreas Rydzewski CEO Pumps & Engine Components CFO Member of Management Board Brake Discs With SHW since 24

Schaeffler Group Mobility for tomorrow Klaus Rosenfeld Chief Executive Officer

Schaeffler Group Mobility for tomorrow Klaus Rosenfeld Chief Executive Officer Capital Markets Day July 20 th, 2016 London Agenda 1 Overview 2 Our Strategy 3 Our Action Plan 4 Our Financial Ambitions 5

Schaeffler Group Mobility for tomorrow Klaus Rosenfeld Chief Executive Officer Capital Markets Day July 20 th, 2016 London Agenda 1 Overview 2 Our Strategy 3 Our Action Plan 4 Our Financial Ambitions 5

2017 Results and Outlook. February 23, 2018

2017 Results and Outlook February 23, 2018 1. 2017 HIGHLIGHTS 2. 2017 RESULTS 3. STRATEGY 4. OUTLOOK 2017 KEY FIGURES Sales Actual Like-for-like Operating income Actual Like-for-like 40.8bn +4.4% +4.7%

2017 Results and Outlook February 23, 2018 1. 2017 HIGHLIGHTS 2. 2017 RESULTS 3. STRATEGY 4. OUTLOOK 2017 KEY FIGURES Sales Actual Like-for-like Operating income Actual Like-for-like 40.8bn +4.4% +4.7%

Linde Group. January - March 2006 Conference Call. April 26, Dr Peter Diesch, CFO

January - March 2006 Conference Call April 26, 2006 Dr Peter Diesch, CFO Contents 04 Linde Group 09 Gas & Engineering 11 Linde Gas 19 Linde Engineering 22 Material Handling 2 Disclaimer This investor presentation

January - March 2006 Conference Call April 26, 2006 Dr Peter Diesch, CFO Contents 04 Linde Group 09 Gas & Engineering 11 Linde Gas 19 Linde Engineering 22 Material Handling 2 Disclaimer This investor presentation

The Key to Mobility Creating Value with Financial Services

The Key to Mobility Creating Value with Financial Services Warburg Field Trip Volkswagen Financial Services; December 2014 Frank Fiedler, CFO Volkswagen Financial Services AG Disclaimer The following presentations

The Key to Mobility Creating Value with Financial Services Warburg Field Trip Volkswagen Financial Services; December 2014 Frank Fiedler, CFO Volkswagen Financial Services AG Disclaimer The following presentations

Imerys and S&B: A strategic combination

Accelerating development, strengthening core business, creating value Gilles MICHEL - Chairman & CEO Michel DELVILLE - CFO Disclaimer More comprehensive information about Imerys may be obtained on its

Accelerating development, strengthening core business, creating value Gilles MICHEL - Chairman & CEO Michel DELVILLE - CFO Disclaimer More comprehensive information about Imerys may be obtained on its

Investor Presentation 27 th march 2006

Investor Presentation 27 th march 2006 1 MIL key highlights Industry overview Industry overview Investor presentation Strategic partnership Huber Micro inks Overview of Hubergroup Global strengths Global

Investor Presentation 27 th march 2006 1 MIL key highlights Industry overview Industry overview Investor presentation Strategic partnership Huber Micro inks Overview of Hubergroup Global strengths Global

Henkel FY Kasper Rorsted Carsten Knobel. Düsseldorf March 4, 2015

Henkel FY 2014 Kasper Rorsted Carsten Knobel Düsseldorf March 4, 2015 Disclaimer This information contains forward-looking statements which are based on current estimates and assumptions made by the corporate

Henkel FY 2014 Kasper Rorsted Carsten Knobel Düsseldorf March 4, 2015 Disclaimer This information contains forward-looking statements which are based on current estimates and assumptions made by the corporate

Investor and Analyst Presentation. March 27, 2014, Report on Fiscal 2013

Investor and Analyst Presentation March 27, 2014, Report on Fiscal 2013 1 Disclaimer Note: This presentation contains statements concerning the future business trend of the Vossloh Group which are based

Investor and Analyst Presentation March 27, 2014, Report on Fiscal 2013 1 Disclaimer Note: This presentation contains statements concerning the future business trend of the Vossloh Group which are based

Schaeffler on track. Press and IR release

Press and IR release Schaeffler on track Revenue grows 5.8 percent at constant currency in the first six months Mid-year EBIT margin before special items of 11.1 percent flat with prior year (prior year:

Press and IR release Schaeffler on track Revenue grows 5.8 percent at constant currency in the first six months Mid-year EBIT margin before special items of 11.1 percent flat with prior year (prior year:

We create chemistry for a sustainable future

Dr. Hans-Ulrich Engel Chief Financial Officer CFO Roadshow Boston September 11, 2017 We create chemistry for a sustainable future Cautionary note regarding forward-looking statements This presentation

Dr. Hans-Ulrich Engel Chief Financial Officer CFO Roadshow Boston September 11, 2017 We create chemistry for a sustainable future Cautionary note regarding forward-looking statements This presentation

We create chemistry for a sustainable future

Dr. Stefanie Wettberg Senior Vice President Investor Relations Investor Visit Ludwigshafen June 27, 2017 We create chemistry for a sustainable future Cautionary note regarding forward-looking statements

Dr. Stefanie Wettberg Senior Vice President Investor Relations Investor Visit Ludwigshafen June 27, 2017 We create chemistry for a sustainable future Cautionary note regarding forward-looking statements

highlights key figures dividend outlook organic revenue growth +5% earnings per share +16% continued investments in growth and innovations

organic revenue growth +5% earnings per share +16% continued investments in growth and innovations Utrecht, 26 February 2019 highlights revenue +2% to EUR 2,759 million (organic +5%) operating profit (EBITA)

organic revenue growth +5% earnings per share +16% continued investments in growth and innovations Utrecht, 26 February 2019 highlights revenue +2% to EUR 2,759 million (organic +5%) operating profit (EBITA)

Analyst and Investor Conference 2016 Dieter Bellé, Bruno Fankhauser, Dr Frank Hiller. The Quality Connection

Analyst and Investor Conference 2016 Dieter Bellé, Bruno Fankhauser, Dr Frank Hiller The Quality Connection Agenda 1. Group (Dieter Bellé) 2. Wiring Systems (Dr Frank Hiller) 3. Wire & Cable Solutions

Analyst and Investor Conference 2016 Dieter Bellé, Bruno Fankhauser, Dr Frank Hiller The Quality Connection Agenda 1. Group (Dieter Bellé) 2. Wiring Systems (Dr Frank Hiller) 3. Wire & Cable Solutions

Annual General Meeting 2006

1 Annual General Meeting 2006 2 Review of 2004/2005 Overview of portfolio optimization Strategic goals for value growth Innovation capabilities Performance of stock 1st quarter and full year 2005/2006

1 Annual General Meeting 2006 2 Review of 2004/2005 Overview of portfolio optimization Strategic goals for value growth Innovation capabilities Performance of stock 1st quarter and full year 2005/2006

Linde Group. Full Year Results 2005

Full Year Results 2005 Disclaimer This presentation has been prepared independently by Linde AG ( Linde ). The presentation contains statements which address such key issues as Linde s growth strategy,

Full Year Results 2005 Disclaimer This presentation has been prepared independently by Linde AG ( Linde ). The presentation contains statements which address such key issues as Linde s growth strategy,

We create chemistry for a sustainable future

Ingo Rose Director Investor Relations Redburn Conference Toronto May 9-10, 2017 We create chemistry for a sustainable future Cautionary note regarding forward-looking statements This presentation contains

Ingo Rose Director Investor Relations Redburn Conference Toronto May 9-10, 2017 We create chemistry for a sustainable future Cautionary note regarding forward-looking statements This presentation contains

Financial Year 2011 Results. Frankfurt. Schaeffler Group March 20, 2012

Financial Year 2011 Results Schaeffler Group March 20, 2012 Frankfurt Page 1 Agenda Overview 2011 Results 2011 Senior Refinancing Outlook Page 2 1 Overview 2011 Targets overachieved Growth Profitability

Financial Year 2011 Results Schaeffler Group March 20, 2012 Frankfurt Page 1 Agenda Overview 2011 Results 2011 Senior Refinancing Outlook Page 2 1 Overview 2011 Targets overachieved Growth Profitability

Wacker Neuson SE. Analyst conference results for Q May 14, Dr.-Ing. Georg Sick, CEO - Mag. Günther Binder, CFO.

Wacker Neuson SE Analyst conference results for Q1 2009 May 14, 2009 Dr.-Ing. Georg Sick, CEO - Mag. Günther Binder, CFO Overview Summary Q1 2009 Financials Q1 2009 Outlook 2 Wacker Neuson SE maintained

Wacker Neuson SE Analyst conference results for Q1 2009 May 14, 2009 Dr.-Ing. Georg Sick, CEO - Mag. Günther Binder, CFO Overview Summary Q1 2009 Financials Q1 2009 Outlook 2 Wacker Neuson SE maintained

Drägerwerk AG & Co. KGaA Analysts Meeting. Frankfurt, March 14, 2012

Drägerwerk AG & Co. KGaA Analysts Meeting Frankfurt, March 4, 202 Disclaimer This presentation does not constitute an offer of securities for sale or a solicitation of an offer to purchase any securities.

Drägerwerk AG & Co. KGaA Analysts Meeting Frankfurt, March 4, 202 Disclaimer This presentation does not constitute an offer of securities for sale or a solicitation of an offer to purchase any securities.

The world s leading infrastructure developer. April 2012

The world s leading infrastructure developer Investors Presentation Company profile, strategy and key financials April 2012 Grupo ACS The world s leading infrastructure developer Engineering contractor

The world s leading infrastructure developer Investors Presentation Company profile, strategy and key financials April 2012 Grupo ACS The world s leading infrastructure developer Engineering contractor

Siemens Semiannual Press Conference. April 26, 2007

Siemens Semiannual Press Conference April 26, 2007 Siemens in the second quarter of FY 2007 Siemens successfully concluded its Fit4More program All Groups reached or exceeded their margin ranges Group

Siemens Semiannual Press Conference April 26, 2007 Siemens in the second quarter of FY 2007 Siemens successfully concluded its Fit4More program All Groups reached or exceeded their margin ranges Group

2015 Results and Outlook. February 26, 2016

2015 Results and Outlook February 26, 2016 2015 HIGHLIGHTS 2015 RESULTS STRATEGY OUTLOOK 2 2015 HIGHLIGHTS 3 2015 KEY FIGURES (Following the sale of the Packaging business and in accordance with IFRS 5,

2015 Results and Outlook February 26, 2016 2015 HIGHLIGHTS 2015 RESULTS STRATEGY OUTLOOK 2 2015 HIGHLIGHTS 3 2015 KEY FIGURES (Following the sale of the Packaging business and in accordance with IFRS 5,

Quarterly Report Q3 Financial Year 2016 / Touching the Future of Vision Automation

Quarterly Report Q3 Financial Year 2016 / 2017 Touching the Future of Vision Automation 150 ISRA VISION Quarterly Report Q3 Financial Year 2016 / 2017 2 rd ISRA VISION AG: 3 quarter 2016 / 2017 revenues

Quarterly Report Q3 Financial Year 2016 / 2017 Touching the Future of Vision Automation 150 ISRA VISION Quarterly Report Q3 Financial Year 2016 / 2017 2 rd ISRA VISION AG: 3 quarter 2016 / 2017 revenues

Koenig & Bauer AG at 15 th German Corporate Conference 2016 January 19, 2016, Frankfurt

People & Print Koenig & Bauer AG at 15 th German Corporate Conference 2016 January 19, 2016, Frankfurt Mathias Dähn, CFO Agenda Company overview Strategy & growth drivers Q3 2015 & outlook KBA Koenig &

People & Print Koenig & Bauer AG at 15 th German Corporate Conference 2016 January 19, 2016, Frankfurt Mathias Dähn, CFO Agenda Company overview Strategy & growth drivers Q3 2015 & outlook KBA Koenig &

Investors Day St.Galler Kantonalbank Bernhard A. Fuchs September 12, Holcim Ltd

Investors Day St.Galler Kantonalbank Bernhard A. Fuchs September 12, 2013 Agenda Holcim at a glance Holcim s Strategy House base for value creation Holcim Leadership Journey Proactive Asset Management

Investors Day St.Galler Kantonalbank Bernhard A. Fuchs September 12, 2013 Agenda Holcim at a glance Holcim s Strategy House base for value creation Holcim Leadership Journey Proactive Asset Management

Charts on Q1 2017/18 Facts & Figures

Charts on Q1 Facts & Figures Ticker: TKA (Share) TKAMY (ADR) February 2018 Strong earnings in Q1 confirming FY expectations SWF Portfolio reshaping towards a Diversified Industrial Due Diligence and Signing

Charts on Q1 Facts & Figures Ticker: TKA (Share) TKAMY (ADR) February 2018 Strong earnings in Q1 confirming FY expectations SWF Portfolio reshaping towards a Diversified Industrial Due Diligence and Signing

thyssenkrupp Equity Story Components Technology November 2017

thyssenkrupp Equity Story Components Technology November 2017 thyssenkrupp a diversified industrial group Sales 41.4 bn 1 ; EBIT adj. 1.7 bn 1 Continuing operations Components Technology (CT) 7.6 bn 377

thyssenkrupp Equity Story Components Technology November 2017 thyssenkrupp a diversified industrial group Sales 41.4 bn 1 ; EBIT adj. 1.7 bn 1 Continuing operations Components Technology (CT) 7.6 bn 377

Presentation of the Group

The world s leading infrastructure developer Presentation of the Group Key figures & Global Strategy July 2012 Grupo ACS The world s leading infrastructure & concessions developer Engineering contractor

The world s leading infrastructure developer Presentation of the Group Key figures & Global Strategy July 2012 Grupo ACS The world s leading infrastructure & concessions developer Engineering contractor