An International Monetary System Built on Sound Policy Rules

|

|

|

- Job Copeland

- 6 years ago

- Views:

Transcription

1 An International Monetary System Built on Sound Policy Rules John B. Taylor Presentation at the Bank of Greece May 24, 2016

2 Many Calls for International Monetary Reform Jaime Caruana: global instability shows need for reform Paul Volcker: the absence of an official, rules-based, cooperatively managed monetary system has not been a great success. Raghu Rajan: what we need are monetary rules that prevent a central bank s domestic mandate from trumping a country s international responsibility. Helena Rey and IMF: we need macro prudential policies or even capital controls (aka capital flow management) to slow down the flow of capital This proposal: A rules-based international monetary system built on policy rules in each country Research (old and new) shows it will work well even with capital mobility and flexible exchange rates

3 Research Economic research rules-based monetary policy leads to good macroeconomic economic performance in the national economy and in the global economy Empirical multi-country monetary models with highly integrated international capital markets no-arbitrage conditions in the term-structure forward-looking expectations price and wage rigidities Sometimes called new Keynesian

4 σ y σ y σ p Country 1 Country 2 σ p

5 σ y σ y B A σ p Country 1 Country 2 σ p

6 σ y B σ y A B A σ p Country 1 Country 2 σ p

7 σ y B C σ y A B A σ p Country 1 Country 2 σ p

8 σ y B C σ y A B C A σ p Country 1 Country 2 σ p

9 σ y B C σ y A B A σ p Country 1 Country 2 σ p

10 σ y B C σ y A B D A σ p Country 1 Country 2 σ p

11 Corroboration Central banks moved toward more transparent rulesbased policies in 1980s, 1990s including through a focus on price stability Detected by Clarida, Gali, and Gertler, and later confirmed by others Dramatic improvement compared with 1970s when policy was highly discretionary and unfocused. Mervyn King called it the NICE period But also a near internationally cooperative equilibrium (NICE) So Twice-NICE or NICE-squared. Many emerging market countries joined Including through Inflation targeting Performance improved & contributed to global stability

12 Then The Crisis The end of NICE in both senses of the word. Great Recession & Not-So-Great Recovery Concerns about international spillover effects Emerging market countries impacted Developed countries Japan express concerns about exchange rates. Small open economies take unusual actions Increased volatility

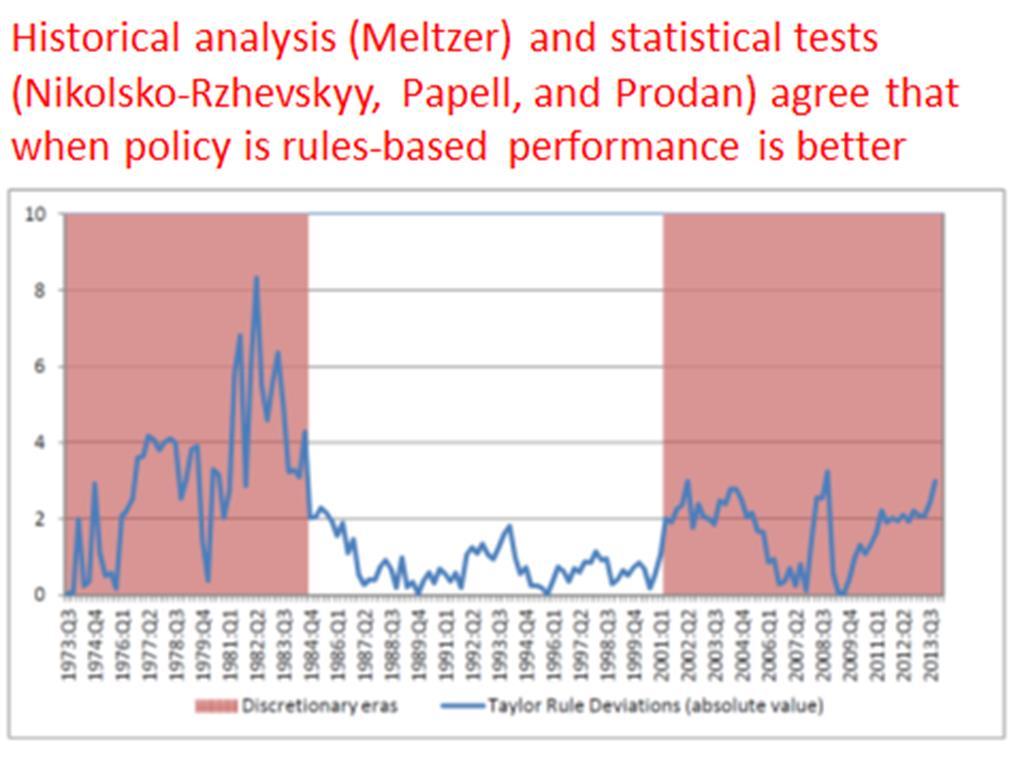

13 Policy Changes and the Crisis Evidence of monetary policy swinging away from rule-like policies Detected by many (Kahn, Ahrend) A decade ago before the financial crisis too low too long Causality versus correlation Econometric and historical evidence of effects Econometrics: Nikolsko-Rzhevskyy, Papell, Prodan History: Meltzer Global Great Deviation Hofmann & Bogdanova

14 Monetary policy gets more predictable, inflation targets, rules-based From Has the Fed Gotten Tougher on Inflation? The FRBSF Weekly Letter, March 31, 1995, by John P Judd and Bharat Trehan of the San Francisco Fed

15 Chart from Fed, St. Louis Review, William Poole (Jan/Feb 2007) Showing Shift Back Toward Discretion

16 Source: Taylor (2007)

17

18 Billions of dollars 3,000 QE3 2,500 2,000 1,500 Reserve Balances at the Fed QE1 QE2 1, /11 With liquidity support only Year 18

19

20 Percent Great Moderation Growth rate of real GDP

21 Housing Investment versus Deviations from Policy Rule in Europe During Source: OECD

22 Source: BIS, Shin

23 (post-2006). C S.D. Variance Period Output Inf. Sum Output Inf. Sum Source: Update of Ben Bernanke (2004) The Great Moderation

24 Alternative View: Curve Shifted for Other Reasons Source: Mervyn King s Stamp Lecture (2012)

25 The Global Benefits of Rules-Based Monetary Policy Move to a more rules-based policy in 1980s led to better national/international performance in the 1980s, 1990s and until recently (NICE 2 ) The spread and amplification of policy deviations from rules-based policy in recent years are drivers of current instabilities (not so NICE) Rules-based national policies could create another nearly international cooperative equilibrium. (another NICE)

26 Empirical Evidence on Global Effects econometric models of spillover effects of policy deviations regressions showing policy contagion and the multiplier effects of such contagion the spread of unconventional monetary policy as weapons in currency wars the impact of policy deviations on other policies that detract from economic performance direct evidence that global economic instability has increased.

27

28 Empirical Evidence on Global Effects econometric models of spillover effects of policy deviations regressions showing policy contagion and the multiplier effects of such contagion the spread of unconventional monetary policy as weapons in currency wars the impact of policy deviations on other policies that detract from economic performance direct evidence that global economic instability has increased.

29 Empirical Evidence Central bank reaction functions with foreign policy deviations Large and significant reaction coefficients Colin Gray (2012) Sebastian Edwards (2015) Agustin Carstens (2015) Examining actual central bank decisions

30 A cut in the Norges bank policy rate (black line to red line)

31 .because of interest From 1-10 rates were cut abroad.

32 A rise on the Norges Bank policy rate (from black to red Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 0 Source: Norges Bank

33 because interest rates were increased abroad Q3 09 Q1 09 Q3 10 Q1 10 Q3 11 Q1 11 Q Higher demand in Norway Higher inflation in Norway Higher interest rates abroad and developments in the foreign exchange market Lower growth abroad Higher risk premium in the money market

34 Key policy rate compared simple monetary policy rule with and without external interest rates Taylor Rule Key Policy Rate Rule with external interest rates Growth rule From MPR 1/10

35 Empirical Evidence on Global Effects econometric models of spillover effects of policy deviations regressions showing policy contagion and the multiplier effects of such contagion the spread of unconventional monetary policy as weapons in currency wars the impact of policy deviations on other policies that detract from economic performance direct evidence that global economic instability has increased.

36 yen per dollar Yen Dollar Exchange Rate Abe Election

37 dollars per euro August Euro dollar exchange rate Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan

38

39 Empirical Evidence on Global Effects econometric models of spillover effects of policy deviations regressions showing policy contagion and the multiplier effects of such contagion the spread of unconventional monetary policy as weapons in currency wars the impact of policy deviations on other policies that detract from economic performance direct evidence that global economic instability has increased.

40 Other Policy Impacts That May Detract From Economic Performance Capital Controls: aimed at containing volatile shifts in the demand for local currency and mitigating risks However, capital controls create distortions, lead to instability. IMF now suggests it, calling it capital flow management Currency Intervention: countries try to prevent unwanted changes in exchange rates--an alternative or supplement to deviations of interest rates from normal policy. Macro-Prudential Policies: another consequence of policy deviations from abroad. To be sure, a regulatory regime aimed at containing risk taking is entirely appropriate, but that entails getting the levels right, not manipulating them as a substitute for overall monetary policy.

41 Empirical Evidence on Global Effects econometric models of spillover effects of policy deviations regressions showing policy contagion and the multiplier effects of such contagion the spread of unconventional monetary policy as weapons in currency wars the impact of policy deviations on other policies that detract from economic performance direct evidence that global economic instability has increased.

42 Emerging market capital flows, weekly, Jan 2001 Sept 2015 Source: Emerging Portfolio Fund Research, Bank of Mexico

43 Standard deviation in post Plaza-Louvre period is 5.7 % and increases to 8.2 % in recent years.

44 Calls for a New Approach With memories of a more orderly, rulebased world Paul Volcker (June, 2014) asks: What is the approach (or presumably combination of approaches) that can better reconcile reasonably free and open markets with independent national policies, maintaining in the process the stability in markets and economies that is in the common interest?

45 Proposal Each country reports and commits to its monetary strategy and thus helps build the foundation of the international monetary system Analogies with other agreements: 1945, 1973, 1985 Avoid encroaching on other countries monetary rules Emerging market countries are all in. The IMF or BIS could help monitor. Barriers to implementing may be low. Major central banks have goals and discuss policy rules Wide-spread view that international reform is needed

46

47 No threat to national/international central bank independence Job of each central bank is to formulate and describe its strategy. Parties to the agreement would not have a say in strategies of other banks Strategies could be changed if the world changed or in an emergency

48 Key Feature Each country would choose its own independent monetary strategy, avoid interfering with the principles of free and open markets, and contribute to the common good of global stability and growth.

49 References Taylor (2016a) The Federal Reserve in a Globalized World Economy, in The Federal Reserve s Role in the Global Economy, M. Bordo and M. Wynne (Eds.) Taylor (2016b), A Rules-Based International Monetary System for the Future, International Monetary Cooperation: Lessons from the Plaza Accord after Thirty Years, C. F. Bergsten and R. Green (Eds.) Awarded 2016 Economics in Central Banking Award Taylor (2016c), Rethinking the International Monetary System, The Cato Journal Taylor, (1985), International Coordination in the Design of Macroeconomic Policy Rules, European Economic Review Carlozzi and Taylor (1985), International Capital Mobility and the Coordination of Monetary Rules in Exchange Rate Management Under Uncertainty, J. Bhandhari (Ed.)

The Federal Reserve in a Globalized World Economy

The Federal Reserve in a Globalized World Economy John B. Taylor Stanford University Prepared for the Conference The Federal Reserve s Role in the Global Economy: A Historical Perspective, Federal Reserve

The Federal Reserve in a Globalized World Economy John B. Taylor Stanford University Prepared for the Conference The Federal Reserve s Role in the Global Economy: A Historical Perspective, Federal Reserve

Re-Normalize, Don t New-Normalize Monetary Policy. John B. Taylor. Economics Working Paper 14109

Re-Normalize, Don t New-Normalize Monetary Policy John B. Taylor Economics Working Paper 14109 HOOVER INSTITUTION 434 GALVEZ MALL STANFORD UNIVERSITY STANFORD, CA 94305-6010 April 2014 This paper is a

Re-Normalize, Don t New-Normalize Monetary Policy John B. Taylor Economics Working Paper 14109 HOOVER INSTITUTION 434 GALVEZ MALL STANFORD UNIVERSITY STANFORD, CA 94305-6010 April 2014 This paper is a

Toward a Rules-Based International Monetary System

Toward a Rules-Based International Monetary System John B. Taylor Over the past few years I have been making the case for moving toward a more rules-based international monetary system (e.g., Taylor 2013,

Toward a Rules-Based International Monetary System John B. Taylor Over the past few years I have been making the case for moving toward a more rules-based international monetary system (e.g., Taylor 2013,

Remarks at the Panel Toward a Rules-Based International Monetary System. John B. Taylor 1

Remarks at the Panel Toward a Rules-Based International Monetary System John B. Taylor th Annual Monetary Conference The Future of Monetary Policy Cato Institute November, 7 It is a pleasure to be on this

Remarks at the Panel Toward a Rules-Based International Monetary System John B. Taylor th Annual Monetary Conference The Future of Monetary Policy Cato Institute November, 7 It is a pleasure to be on this

A Rules-Based Cooperatively Managed International Monetary System for the Future

Working Paper No. 559 A Rules-Based Cooperatively Managed International Monetary System for the Future John B. Taylor October 2015 A Rules-Based Cooperatively Managed International Monetary System for

Working Paper No. 559 A Rules-Based Cooperatively Managed International Monetary System for the Future John B. Taylor October 2015 A Rules-Based Cooperatively Managed International Monetary System for

Inflation Targeting In Emerging Markets: The Global Experience. John B. Taylor Stanford University

Inflation Targeting In Emerging Markets: The Global Experience John B. Taylor Stanford University Keynote Address at the Conference on Fourteen Years of Inflation Targeting in South Africa and The Challenge

Inflation Targeting In Emerging Markets: The Global Experience John B. Taylor Stanford University Keynote Address at the Conference on Fourteen Years of Inflation Targeting in South Africa and The Challenge

International Monetary Coordination And The Great Deviation. John B. Taylor. Economics Working Paper 13101

International Monetary Coordination And The Great Deviation John B. Taylor Economics Working Paper 13101 HOOVER INSTITUTION 434 GALVEZ MALL STANFORD UNIVERSITY STANFORD, CA 94305-6010 January 2013 This

International Monetary Coordination And The Great Deviation John B. Taylor Economics Working Paper 13101 HOOVER INSTITUTION 434 GALVEZ MALL STANFORD UNIVERSITY STANFORD, CA 94305-6010 January 2013 This

International monetary coordination and the great deviation

Available online at www.sciencedirect.com Journal of Policy Modeling xxx (2013) xxx xxx International monetary coordination and the great deviation John B. Taylor Department of Economics, Stanford University,

Available online at www.sciencedirect.com Journal of Policy Modeling xxx (2013) xxx xxx International monetary coordination and the great deviation John B. Taylor Department of Economics, Stanford University,

Rethinking the International Monetary System. John B. Taylor 1

Rethinking the International Monetary System John B. Taylor 1 Prepared for Presentation at the Cato Institute Monetary Conference on Rethinking Monetary Policy November 12, 2015 Abstract This paper shows

Rethinking the International Monetary System John B. Taylor 1 Prepared for Presentation at the Cato Institute Monetary Conference on Rethinking Monetary Policy November 12, 2015 Abstract This paper shows

The Federal Reserve in a Globalized World Economy. John B. Taylor 1 Stanford University September 2014

The Federal Reserve in a Globalized World Economy John B. Taylor 1 Stanford University September 2014 Economic research as far back as the early 1980s showed that simple rules-based monetary policy would

The Federal Reserve in a Globalized World Economy John B. Taylor 1 Stanford University September 2014 Economic research as far back as the early 1980s showed that simple rules-based monetary policy would

Keynote address Inflation targeting in emerging markets: the global experience

from Fourteen Years of Inflation Targeting in South Africa and the Challenge of a Changing Mandate South African Reserve Bank Conference Series 2014 Keynote address Inflation targeting in emerging markets:

from Fourteen Years of Inflation Targeting in South Africa and the Challenge of a Changing Mandate South African Reserve Bank Conference Series 2014 Keynote address Inflation targeting in emerging markets:

Government as a Cause of the 2008 Financial Crisis: A Reassessment After 10 Years. John B. Taylor 1

Government as a Cause of the 2008 Financial Crisis: A Reassessment After 10 Years John B. Taylor 1 Remarks prepared for the Causes Session Workshop Series on the 2008 Financial Crisis: Causes, The Panic,

Government as a Cause of the 2008 Financial Crisis: A Reassessment After 10 Years John B. Taylor 1 Remarks prepared for the Causes Session Workshop Series on the 2008 Financial Crisis: Causes, The Panic,

Monetary Policy in a Global Economy: Past and Future Research Challenges

Monetary Policy in a Global Economy: Past and Future Research Challenges Presentation at the Conference Globalization and the Macroeconomy 24 July 2007 John B. Taylor Stanford University Past Challenges

Monetary Policy in a Global Economy: Past and Future Research Challenges Presentation at the Conference Globalization and the Macroeconomy 24 July 2007 John B. Taylor Stanford University Past Challenges

Remarks on Monetary Policy Challenges. Bank of England Conference on Challenges to Central Banks in the 21st Century

Remarks on Monetary Policy Challenges Bank of England Conference on Challenges to Central Banks in the 21st Century John B. Taylor Stanford University March 26, 2013 It is an honor to participate in this

Remarks on Monetary Policy Challenges Bank of England Conference on Challenges to Central Banks in the 21st Century John B. Taylor Stanford University March 26, 2013 It is an honor to participate in this

International Monetary Policy Coordination: Past, Present and Future. John B. Taylor 1 Stanford University. June 21, 2013

International Monetary Policy Coordination: Past, Present and Future John B. Taylor 1 Stanford University Prepared for presentation at the 12th BIS Annual Conference, Navigating the Great Recession: What

International Monetary Policy Coordination: Past, Present and Future John B. Taylor 1 Stanford University Prepared for presentation at the 12th BIS Annual Conference, Navigating the Great Recession: What

Remarks on Monetary Policy Challenges

This work is distributed as a Discussion Paper by the STANFORD INSTITUTE FOR ECONOMIC POLICY RESEARCH SIEPR Discussion Paper No. 12-032 Remarks on Monetary Policy Challenges By John B. Taylor Stanford

This work is distributed as a Discussion Paper by the STANFORD INSTITUTE FOR ECONOMIC POLICY RESEARCH SIEPR Discussion Paper No. 12-032 Remarks on Monetary Policy Challenges By John B. Taylor Stanford

Two Views of International Monetary Policy Coordination

Two Views of International Monetary Policy Coordination James Bullard President and CEO, FRB-St. Louis 27 th Asia/Pacific Business Outlook Conference USC Marshall School of Business CIBER 7 April 2014

Two Views of International Monetary Policy Coordination James Bullard President and CEO, FRB-St. Louis 27 th Asia/Pacific Business Outlook Conference USC Marshall School of Business CIBER 7 April 2014

Monetary Policy Revised: January 9, 2008

Global Economy Chris Edmond Monetary Policy Revised: January 9, 2008 In most countries, central banks manage interest rates in an attempt to produce stable and predictable prices. In some countries they

Global Economy Chris Edmond Monetary Policy Revised: January 9, 2008 In most countries, central banks manage interest rates in an attempt to produce stable and predictable prices. In some countries they

Empirically Evaluating Economic Policy in Real Time. The Martin Feldstein Lecture 1 National Bureau of Economic Research July 10, John B.

Empirically Evaluating Economic Policy in Real Time The Martin Feldstein Lecture 1 National Bureau of Economic Research July 10, 2009 John B. Taylor To honor Martin Feldstein s distinguished leadership

Empirically Evaluating Economic Policy in Real Time The Martin Feldstein Lecture 1 National Bureau of Economic Research July 10, 2009 John B. Taylor To honor Martin Feldstein s distinguished leadership

The Importance of Being Predictable. John B. Taylor Stanford University. Remarks Prepared for the Policy Panel on Monetary Policy Under Uncertainty

The Importance of Being Predictable John B. Taylor Stanford University Remarks Prepared for the Policy Panel on Monetary Policy Under Uncertainty 23 rd Annual Policy Conference Federal Reserve Bank of

The Importance of Being Predictable John B. Taylor Stanford University Remarks Prepared for the Policy Panel on Monetary Policy Under Uncertainty 23 rd Annual Policy Conference Federal Reserve Bank of

THE POLICY RULE MIX: A MACROECONOMIC POLICY EVALUATION. John B. Taylor Stanford University

THE POLICY RULE MIX: A MACROECONOMIC POLICY EVALUATION by John B. Taylor Stanford University October 1997 This draft was prepared for the Robert A. Mundell Festschrift Conference, organized by Guillermo

THE POLICY RULE MIX: A MACROECONOMIC POLICY EVALUATION by John B. Taylor Stanford University October 1997 This draft was prepared for the Robert A. Mundell Festschrift Conference, organized by Guillermo

EE 631: MONETARY ECONOMICS 2 nd Semester 2013

EE 631: MONETARY ECONOMICS 2 nd Semester 2013 Times/location: Wed 9:30 am 12:30 pm Office: 60 th Building, Room #16 Phone: 02-613-2471 E-mail: pisut@econ.tu.ac.th Office Hours: Wed 1:30 4:30 pm or by appointment

EE 631: MONETARY ECONOMICS 2 nd Semester 2013 Times/location: Wed 9:30 am 12:30 pm Office: 60 th Building, Room #16 Phone: 02-613-2471 E-mail: pisut@econ.tu.ac.th Office Hours: Wed 1:30 4:30 pm or by appointment

Finnish Economic Papers Volume 24 Number 2 Autumn The Rules-Discretion Cycle in Monetary and Fiscal Policy* JOHN B. TAYLOR

Finnish Economic Papers Volume 24 Number 2 Autumn 2011 The Rules-Discretion Cycle in Monetary and Fiscal Policy* JOHN B. TAYLOR Stanfor University JohnBTaylor@Stanford.edu This lecture starts with a review

Finnish Economic Papers Volume 24 Number 2 Autumn 2011 The Rules-Discretion Cycle in Monetary and Fiscal Policy* JOHN B. TAYLOR Stanfor University JohnBTaylor@Stanford.edu This lecture starts with a review

Should the Monetary Policy Rule Be Different in a Financial Crisis? By Monika Piazzesi i

Should the Monetary Policy Rule Be Different in a Financial Crisis? By Monika Piazzesi i It s a pleasure to read and discuss this very nice and well-written paper by Nikolsko- Rzhevskyy, Papell and Prodan.

Should the Monetary Policy Rule Be Different in a Financial Crisis? By Monika Piazzesi i It s a pleasure to read and discuss this very nice and well-written paper by Nikolsko- Rzhevskyy, Papell and Prodan.

International Monetary Stability: A Multiple Equilibria Problem?

International Monetary Stability: A Multiple Equilibria Problem? James Bullard President and CEO, FRB-St. Louis International Monetary Stability Hoover Institution at Stanford University May 5, 2016 Stanford,

International Monetary Stability: A Multiple Equilibria Problem? James Bullard President and CEO, FRB-St. Louis International Monetary Stability Hoover Institution at Stanford University May 5, 2016 Stanford,

Alternatives for Reserve Balances and the Fed s Balance Sheet in the Future. John B. Taylor 1. June 2017

Alternatives for Reserve Balances and the Fed s Balance Sheet in the Future John B. Taylor 1 June 2017 Since this is a session on the Fed s balance sheet, I begin by looking at the Fed s balance sheet

Alternatives for Reserve Balances and the Fed s Balance Sheet in the Future John B. Taylor 1 June 2017 Since this is a session on the Fed s balance sheet, I begin by looking at the Fed s balance sheet

Excerpts from First Principles: Five Keys to Restoring America s Prosperity

Excerpts from First Principles: Five Keys to Restoring America s Prosperity In the most fundamental sense, the purpose of monetary reform is simple: restore and lock-in consistent rule-like policies that

Excerpts from First Principles: Five Keys to Restoring America s Prosperity In the most fundamental sense, the purpose of monetary reform is simple: restore and lock-in consistent rule-like policies that

Commentary: Challenges for Monetary Policy: New and Old

Commentary: Challenges for Monetary Policy: New and Old John B. Taylor Mervyn King s paper is jam-packed with interesting ideas and good common sense about monetary policy. I admire the clearly stated

Commentary: Challenges for Monetary Policy: New and Old John B. Taylor Mervyn King s paper is jam-packed with interesting ideas and good common sense about monetary policy. I admire the clearly stated

What Caused the Global Financial Crisis? Ouarda Merrouche (WB) and Erlend Nier (IMF)

and Erlend Nier (IMF)") What Caused the Global Financial Crisis? Ouarda Merrouche (WB) and Erlend Nier (IMF) What do we do? We document how ample liquidity ahead of the crisis encouraged increases in leverage sourced in wholesale

What Caused the Global Financial Crisis? Ouarda Merrouche (WB) and Erlend Nier (IMF) What do we do? We document how ample liquidity ahead of the crisis encouraged increases in leverage sourced in wholesale

Commentary. Olivier Blanchard. 1. Should We Expect Automatic Stabilizers to Work, That Is, to Stabilize?

Olivier Blanchard Commentary A utomatic stabilizers are a very old idea. Indeed, they are a very old, very Keynesian, idea. At the same time, they fit well with the current mistrust of discretionary policy

Olivier Blanchard Commentary A utomatic stabilizers are a very old idea. Indeed, they are a very old, very Keynesian, idea. At the same time, they fit well with the current mistrust of discretionary policy

Monetary Policy Options in a Low Policy Rate Environment

Monetary Policy Options in a Low Policy Rate Environment James Bullard President and CEO, FRB-St. Louis IMFS Distinguished Lecture House of Finance Goethe Universität Frankfurt 21 May 2013 Frankfurt-am-Main,

Monetary Policy Options in a Low Policy Rate Environment James Bullard President and CEO, FRB-St. Louis IMFS Distinguished Lecture House of Finance Goethe Universität Frankfurt 21 May 2013 Frankfurt-am-Main,

Monetary Policy Tools in an Environment of Low Interest Rates James Bullard

Monetary Policy Tools in an Environment of Low Interest Rates James Bullard President and CEO CFA Society of St. Louis February 5, 2009 The Economy Today A sharp recession. Declining output during 2008

Monetary Policy Tools in an Environment of Low Interest Rates James Bullard President and CEO CFA Society of St. Louis February 5, 2009 The Economy Today A sharp recession. Declining output during 2008

Teaching Inflation Targeting: An Analysis for Intermediate Macro. Carl E. Walsh * First draft: September 2000 This draft: July 2001

Teaching Inflation Targeting: An Analysis for Intermediate Macro Carl E. Walsh * First draft: September 2000 This draft: July 2001 * Professor of Economics, University of California, Santa Cruz, and Visiting

Teaching Inflation Targeting: An Analysis for Intermediate Macro Carl E. Walsh * First draft: September 2000 This draft: July 2001 * Professor of Economics, University of California, Santa Cruz, and Visiting

Macroeconomic Risks for Farmer Cooperatives

Macroeconomic Risks for Farmer Cooperatives KFSA Directors & Management Meeting Hutchinson, KS November 21 st, 2011 Brian C. Briggeman Associate Professor and Director of the Arthur Capper Cooperative

Macroeconomic Risks for Farmer Cooperatives KFSA Directors & Management Meeting Hutchinson, KS November 21 st, 2011 Brian C. Briggeman Associate Professor and Director of the Arthur Capper Cooperative

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 3 POSTWAR FLUCTUATIONS AND THE GREAT RECESSION JANUARY 24, 2018 I. CHANGES IN MACROECONOMIC VOLATILITY

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 3 POSTWAR FLUCTUATIONS AND THE GREAT RECESSION JANUARY 24, 2018 I. CHANGES IN MACROECONOMIC VOLATILITY

Part VIII: Short-Run Fluctuations and. 26. Short-Run Fluctuations 27. Countercyclical Macroeconomic Policy

Monetary Fiscal Part VIII: Short-Run and 26. Short-Run 27. 1 / 52 Monetary Chapter 27 Fiscal 2017.8.31. 2 / 52 Monetary Fiscal 1 2 Monetary 3 Fiscal 4 3 / 52 Monetary Fiscal Project funded by the American

Monetary Fiscal Part VIII: Short-Run and 26. Short-Run 27. 1 / 52 Monetary Chapter 27 Fiscal 2017.8.31. 2 / 52 Monetary Fiscal 1 2 Monetary 3 Fiscal 4 3 / 52 Monetary Fiscal Project funded by the American

Lecture 19 Interdependence & Coordination

Lecture 19 Interdependence & Coordination International Interdependence Theory: Interdependence results from capital mobility, even with floating rates. Empirical estimates of cross-country effects. International

Lecture 19 Interdependence & Coordination International Interdependence Theory: Interdependence results from capital mobility, even with floating rates. Empirical estimates of cross-country effects. International

Lessons of the Financial Crisis for the Design of the New International Financial Architecture

Lessons of the Financial Crisis for the Design of the New International Financial Architecture John B. Taylor Hoover Institution and Stanford University Written Version of Keynote Address Conference on

Lessons of the Financial Crisis for the Design of the New International Financial Architecture John B. Taylor Hoover Institution and Stanford University Written Version of Keynote Address Conference on

James Bullard. 13 January St. Louis, Missouri

Death of a Theory James Bullard President and CEO, FRB-St. Louis 13 January 2012 St. Louis, Missouri Any opinions expressed here are my own and do not necessarily reflect those of others on the Federal

Death of a Theory James Bullard President and CEO, FRB-St. Louis 13 January 2012 St. Louis, Missouri Any opinions expressed here are my own and do not necessarily reflect those of others on the Federal

Cost Shocks in the AD/ AS Model

Cost Shocks in the AD/ AS Model 13 CHAPTER OUTLINE Fiscal Policy Effects Fiscal Policy Effects in the Long Run Monetary Policy Effects The Fed s Response to the Z Factors Shape of the AD Curve When the

Cost Shocks in the AD/ AS Model 13 CHAPTER OUTLINE Fiscal Policy Effects Fiscal Policy Effects in the Long Run Monetary Policy Effects The Fed s Response to the Z Factors Shape of the AD Curve When the

Econ 340. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102. Recall Macro from Econ 102

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

Econ 34 Lecture 5 International Macroeconomics Outline: International Macroeconomics Recall Macro from Econ 2 Aggregate Supply and Demand Policies Effects ON the Exchange Expansion Interest Rate Depreciation

Has the Inflation Process Changed?

Has the Inflation Process Changed? by S. Cecchetti and G. Debelle Discussion by I. Angeloni (ECB) * Cecchetti and Debelle (CD) could hardly have chosen a more relevant and timely topic for their paper.

Has the Inflation Process Changed? by S. Cecchetti and G. Debelle Discussion by I. Angeloni (ECB) * Cecchetti and Debelle (CD) could hardly have chosen a more relevant and timely topic for their paper.

Response of Output Fluctuations in Costa Rica to Exchange Rate Movements and Global Economic Conditions and Policy Implications

Response of Output Fluctuations in Costa Rica to Exchange Rate Movements and Global Economic Conditions and Policy Implications Yu Hsing (Corresponding author) Department of Management & Business Administration,

Response of Output Fluctuations in Costa Rica to Exchange Rate Movements and Global Economic Conditions and Policy Implications Yu Hsing (Corresponding author) Department of Management & Business Administration,

Comment on: The zero-interest-rate bound and the role of the exchange rate for. monetary policy in Japan. Carl E. Walsh *

Journal of Monetary Economics Comment on: The zero-interest-rate bound and the role of the exchange rate for monetary policy in Japan Carl E. Walsh * Department of Economics, University of California,

Journal of Monetary Economics Comment on: The zero-interest-rate bound and the role of the exchange rate for monetary policy in Japan Carl E. Walsh * Department of Economics, University of California,

U.S. Monetary Policy: Still Appropriate

U.S. Monetary Policy: Still Appropriate James Bullard President and CEO, FRB-St. Louis Dialogue with the Fed 29 June 2012 Little Rock, Arkansas Any opinions expressed here are my own and do not necessarily

U.S. Monetary Policy: Still Appropriate James Bullard President and CEO, FRB-St. Louis Dialogue with the Fed 29 June 2012 Little Rock, Arkansas Any opinions expressed here are my own and do not necessarily

Part III. Cycles and Growth:

Part III. Cycles and Growth: UMSL Max Gillman Max Gillman () AS-AD 1 / 56 AS-AD, Relative Prices & Business Cycles Facts: Nominal Prices are Not Real Prices Price of goods in nominal terms: eg. Consumer

Part III. Cycles and Growth: UMSL Max Gillman Max Gillman () AS-AD 1 / 56 AS-AD, Relative Prices & Business Cycles Facts: Nominal Prices are Not Real Prices Price of goods in nominal terms: eg. Consumer

Monetary Policy during the Past 30 Years with Lessons for the Next 30 Years John B. Taylor

Monetary Policy during the Past 3 Years with Lessons for the Next 3 Years John B. Taylor The 3th anniversary of the Cato Institute s monetary conference series provides an excellent opportunity to take

Monetary Policy during the Past 3 Years with Lessons for the Next 3 Years John B. Taylor The 3th anniversary of the Cato Institute s monetary conference series provides an excellent opportunity to take

The Lack of an Empirical Rationale for a Revival of Discretionary Fiscal Policy. John B. Taylor Stanford University

The Lack of an Empirical Rationale for a Revival of Discretionary Fiscal Policy John B. Taylor Stanford University Prepared for the Annual Meeting of the American Economic Association Session The Revival

The Lack of an Empirical Rationale for a Revival of Discretionary Fiscal Policy John B. Taylor Stanford University Prepared for the Annual Meeting of the American Economic Association Session The Revival

Macroeconomics for Finance

Macroeconomics for Finance Joanna Mackiewicz-Łyziak Lecture 3 From tools to goals Tools of the Central Bank Open market operations Discount policy Reserve requirements Interest on reserves Large-scale

Macroeconomics for Finance Joanna Mackiewicz-Łyziak Lecture 3 From tools to goals Tools of the Central Bank Open market operations Discount policy Reserve requirements Interest on reserves Large-scale

Using Monetary Policy Rules in Emerging Market Economies * John B. Taylor. Stanford University. December (Revised)

") Using Monetary Policy Rules in Emerging Market Economies * By John B. Taylor Stanford University December 2000 (Revised) Abstract: This paper shows that the use of monetary policy rules in emerging market

Using Monetary Policy Rules in Emerging Market Economies * By John B. Taylor Stanford University December 2000 (Revised) Abstract: This paper shows that the use of monetary policy rules in emerging market

Modeling Federal Funds Rates: A Comparison of Four Methodologies

Loyola University Chicago Loyola ecommons School of Business: Faculty Publications and Other Works Faculty Publications 1-2009 Modeling Federal Funds Rates: A Comparison of Four Methodologies Anastasios

Loyola University Chicago Loyola ecommons School of Business: Faculty Publications and Other Works Faculty Publications 1-2009 Modeling Federal Funds Rates: A Comparison of Four Methodologies Anastasios

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9 THE CONDUCT OF POSTWAR MONETARY POLICY FEBRUARY 14, 2018 I. OVERVIEW A. Where we have been B.

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9 THE CONDUCT OF POSTWAR MONETARY POLICY FEBRUARY 14, 2018 I. OVERVIEW A. Where we have been B.

Testimony before the Joint Economic Committee at the Hearing on Monetary Policy Going Forward: Why a Sound Dollar Boosts Growth and Employment

Testimony before the Joint Economic Committee at the Hearing on Monetary Policy Going Forward: Why a Sound Dollar Boosts Growth and Employment March 27, 2012 John B. Taylor 1 Chairman Casey, Vice Chairman

Testimony before the Joint Economic Committee at the Hearing on Monetary Policy Going Forward: Why a Sound Dollar Boosts Growth and Employment March 27, 2012 John B. Taylor 1 Chairman Casey, Vice Chairman

Exam Number. Section

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor Antonio Fatás Final Exam February 24, 2011 9:00-12:00 Instructions: (PLEASE READ) SUGGESTED ANSWERS Space to answer the questions

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor Antonio Fatás Final Exam February 24, 2011 9:00-12:00 Instructions: (PLEASE READ) SUGGESTED ANSWERS Space to answer the questions

ECON MACROECONOMIC THEORY Instructor: Dr. Juergen Jung Towson University

ECON 310 - MACROECONOMIC THEORY Instructor: Dr. Juergen Jung Towson University Dr. Juergen Jung ECON 310 - Macroeconomic Theory Towson University 1 / 36 Disclaimer These lecture notes are customized for

ECON 310 - MACROECONOMIC THEORY Instructor: Dr. Juergen Jung Towson University Dr. Juergen Jung ECON 310 - Macroeconomic Theory Towson University 1 / 36 Disclaimer These lecture notes are customized for

Three-speed recovery. GDP growth. Percent Emerging and developing economies. World

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

Thoughts on US Monetary Policy Prepared for Hutchins Center Conference, March 21, 2016

Thoughts on US Monetary Policy Prepared for Hutchins Center Conference, March 21, 2016 Richard H. Clarida Professor of Economics and International Affairs Columbia University Global Strategic Advisor PIMCO

Thoughts on US Monetary Policy Prepared for Hutchins Center Conference, March 21, 2016 Richard H. Clarida Professor of Economics and International Affairs Columbia University Global Strategic Advisor PIMCO

Monetary Policy Rules Work and Discretion Doesn t: A Tale of Two Eras. John B. Taylor Stanford University

Monetary Policy Rules Work and Discretion Doesn t: A Tale of Two Eras John B. Taylor Stanford University The Journal of Money Credit and Banking Lecture 1 March 2012 Thirty years ago Milton Friedman delivered

Monetary Policy Rules Work and Discretion Doesn t: A Tale of Two Eras John B. Taylor Stanford University The Journal of Money Credit and Banking Lecture 1 March 2012 Thirty years ago Milton Friedman delivered

NBER WORKING PAPER SERIES THE FINANCIAL CRISIS AND THE POLICY RESPONSES: AN EMPIRICAL ANALYSIS OF WHAT WENT WRONG. John B. Taylor

NBER WORKING PAPER SERIES THE FINANCIAL CRISIS AND THE POLICY RESPONSES: AN EMPIRICAL ANALYSIS OF WHAT WENT WRONG John B. Taylor Working Paper 14631 http://www.nber.org/papers/w14631 NATIONAL BUREAU OF

NBER WORKING PAPER SERIES THE FINANCIAL CRISIS AND THE POLICY RESPONSES: AN EMPIRICAL ANALYSIS OF WHAT WENT WRONG John B. Taylor Working Paper 14631 http://www.nber.org/papers/w14631 NATIONAL BUREAU OF

Implications of Globalization for Monetary Policy. Academic Consultants Meeting Federal Reserve Board

Implications of Globalization for Monetary Policy Academic Consultants Meeting Federal Reserve Board John B. Taylor Stanford University 28 September 2006 The purpose of this note is to provide some background

Implications of Globalization for Monetary Policy Academic Consultants Meeting Federal Reserve Board John B. Taylor Stanford University 28 September 2006 The purpose of this note is to provide some background

Implications of Globalization for Monetary Policy. Academic Consultants Meeting Federal Reserve Board

Implications of Globalization for Monetary Policy Academic Consultants Meeting Federal Reserve Board John B. Taylor Stanford University 28 September 2006 The purpose of this note is to provide some background

Implications of Globalization for Monetary Policy Academic Consultants Meeting Federal Reserve Board John B. Taylor Stanford University 28 September 2006 The purpose of this note is to provide some background

Limits to central bank objectives in a small open economy

SPEECH DATE: October SPEAKER: Stefan Ingves LOCATION: Banco de Mexico, Mexico SVERIGES RIKSBANK SE- 7 Stockholm (Brunkebergstorg ) Tel +6 8 787 Fax +6 8 registratorn@riksbank.se www.riksbank.se Limits

SPEECH DATE: October SPEAKER: Stefan Ingves LOCATION: Banco de Mexico, Mexico SVERIGES RIKSBANK SE- 7 Stockholm (Brunkebergstorg ) Tel +6 8 787 Fax +6 8 registratorn@riksbank.se www.riksbank.se Limits

Financial Crisis What do we know?

Financial Crisis What do we know? Pedro Videla IESE Global Propagation of the Financial Crisis United Kingdom Ireland Iceland United States Spain January 2008 March 2008 June 2008 September 2008 January

Financial Crisis What do we know? Pedro Videla IESE Global Propagation of the Financial Crisis United Kingdom Ireland Iceland United States Spain January 2008 March 2008 June 2008 September 2008 January

Capital Flows and Monetary Coordination. Rakesh Mohan Executive Director International Monetary Fund

Capital Flows and Monetary Coordination Rakesh Mohan Executive Director International Monetary Fund June 9, 214 Capital Flows: Historical Overview Pre-WW I Debt flows, mostly long-term Gold standard stable

Capital Flows and Monetary Coordination Rakesh Mohan Executive Director International Monetary Fund June 9, 214 Capital Flows: Historical Overview Pre-WW I Debt flows, mostly long-term Gold standard stable

Monetary Policy Frameworks

Monetary Policy Frameworks Loretta J. Mester President and Chief Executive Officer Federal Reserve Bank of Cleveland Panel Remarks for the National Association for Business Economics and American Economic

Monetary Policy Frameworks Loretta J. Mester President and Chief Executive Officer Federal Reserve Bank of Cleveland Panel Remarks for the National Association for Business Economics and American Economic

The Effectiveness of Central Bank Independence Versus Policy Rules. John B. Taylor Stanford University

The Effectiveness of Central Bank Independence Versus Policy Rules John B. Taylor Stanford University Prepared for the session Central Bank Independence: Reality or Myth? American Economic Association

The Effectiveness of Central Bank Independence Versus Policy Rules John B. Taylor Stanford University Prepared for the session Central Bank Independence: Reality or Myth? American Economic Association

Comments on Monetary Policy at the Effective Lower Bound

BPEA, September 13-14, 2018 Comments on Monetary Policy at the Effective Lower Bound Janet Yellen, Distinguished Fellow in Residence Hutchins Center on Fiscal and Monetary Policy, Brookings Institution

BPEA, September 13-14, 2018 Comments on Monetary Policy at the Effective Lower Bound Janet Yellen, Distinguished Fellow in Residence Hutchins Center on Fiscal and Monetary Policy, Brookings Institution

Discussant remarks: monetary policy and exchange rate issues in Asia and the Pacific

Discussant remarks: monetary policy and exchange rate issues in Asia and the Pacific Kyungsoo Kim 1 First of all, let me thank the People s Bank of China and the Bank for International Settlements for

Discussant remarks: monetary policy and exchange rate issues in Asia and the Pacific Kyungsoo Kim 1 First of all, let me thank the People s Bank of China and the Bank for International Settlements for

Reflections on Secular Stagnation. Dr. Lawrence H. Summers February 19, 2015

Reflections on Secular Stagnation Dr. Lawrence H. Summers February 19, 2015 Outline I. Problematic post-crisis economic performance in the industrial world II. The secular stagnation hypothesis III. Why

Reflections on Secular Stagnation Dr. Lawrence H. Summers February 19, 2015 Outline I. Problematic post-crisis economic performance in the industrial world II. The secular stagnation hypothesis III. Why

Capital Flows in the Euro Area: Some lessons from the last boom-bust cycle. Angel Gavilan, Martin Hillebrand December 2017

Capital Flows in the Euro Area: Some lessons from the last boom-bust cycle Angel Gavilan, Martin Hillebrand December 217 The last boom in capital flows was largely a global phenomenon Sum of current account

Capital Flows in the Euro Area: Some lessons from the last boom-bust cycle Angel Gavilan, Martin Hillebrand December 217 The last boom in capital flows was largely a global phenomenon Sum of current account

Macroeconomic Theory II

Instructor: Balázs Világi Semester/term, year: Winter 2017 COURSE SYLLABUS Macroeconomic Theory II Course level: First year MA compulsory course No.of Credits (no. of ECTS Credits): 5 CEU credits (10 ECTS)

Instructor: Balázs Világi Semester/term, year: Winter 2017 COURSE SYLLABUS Macroeconomic Theory II Course level: First year MA compulsory course No.of Credits (no. of ECTS Credits): 5 CEU credits (10 ECTS)

Global Monetary and Financial Stability Policy

Global Monetary and Financial Stability Policy Fall 2016 Professor Zvi Eckstein FNCE 893/393 August 30, 2015 to October 13, 2015 Office hours: SH-DH room 2336, Tuesday 4:30 6:00 pm, by appointment Email:

Global Monetary and Financial Stability Policy Fall 2016 Professor Zvi Eckstein FNCE 893/393 August 30, 2015 to October 13, 2015 Office hours: SH-DH room 2336, Tuesday 4:30 6:00 pm, by appointment Email:

Understanding and Influencing the Yield Curve at the Zero Lower Bound

Understanding and Influencing the Yield Curve at the Zero Lower Bound Glenn D. Rudebusch Federal Reserve Bank of San Francisco September 9, 2014 European Central Bank and Bank of England workshop European

Understanding and Influencing the Yield Curve at the Zero Lower Bound Glenn D. Rudebusch Federal Reserve Bank of San Francisco September 9, 2014 European Central Bank and Bank of England workshop European

EC202 Macroeconomics

EC202 Macroeconomics Koç University, Summer 2014 by Arhan Ertan Study Questions - 3 1. Suppose a government is able to permanently reduce its budget deficit. Use the Solow growth model of Chapter 9 to

EC202 Macroeconomics Koç University, Summer 2014 by Arhan Ertan Study Questions - 3 1. Suppose a government is able to permanently reduce its budget deficit. Use the Solow growth model of Chapter 9 to

Cross-border spillovers of monetary policy: what changes during a banking crisis?

Cross-border spillovers of monetary policy: what changes during a banking crisis? Luciana Barbosa, Diana Bonfim, Sónia Costa (Banco de Portugal) Mary Everett (Central Bank of Ireland) (presenter) Disclaimer:

Cross-border spillovers of monetary policy: what changes during a banking crisis? Luciana Barbosa, Diana Bonfim, Sónia Costa (Banco de Portugal) Mary Everett (Central Bank of Ireland) (presenter) Disclaimer:

Rules of the Monetary Game

Rules of the Monetary Game Prachi Mishra Reserve Bank of India Raghuram Rajan University of Chicago Presentation at the South African Reserve Bank October 27-28, 2016 Qualifier Views are personal. Not

Rules of the Monetary Game Prachi Mishra Reserve Bank of India Raghuram Rajan University of Chicago Presentation at the South African Reserve Bank October 27-28, 2016 Qualifier Views are personal. Not

U.S. INTEREST RATES CHARTBOOK MARCH U.S. Interest Rates. Chartbook. March 2017

U.S. Interest Rates Chartbook March 2017 Takeaways The FOMC has raised the Fed funds rate for the third time since the start of the policy rate normalization cycle in 2015. The Committee has also reinforced

U.S. Interest Rates Chartbook March 2017 Takeaways The FOMC has raised the Fed funds rate for the third time since the start of the policy rate normalization cycle in 2015. The Committee has also reinforced

A Steadier Course for Monetary Policy. John B. Taylor. Economics Working Paper 13107

A Steadier Course for Monetary Policy John B. Taylor Economics Working Paper 13107 HOOVER INSTITUTION 434 GALVEZ MALL STANFORD UNIVERSITY STANFORD, CA 94305-6010 April 18, 2013 This testimony before the

A Steadier Course for Monetary Policy John B. Taylor Economics Working Paper 13107 HOOVER INSTITUTION 434 GALVEZ MALL STANFORD UNIVERSITY STANFORD, CA 94305-6010 April 18, 2013 This testimony before the

Assignment 5 The New Keynesian Phillips Curve

Econometrics II Fall 2017 Department of Economics, University of Copenhagen Assignment 5 The New Keynesian Phillips Curve The Case: Inflation tends to be pro-cycical with high inflation during times of

Econometrics II Fall 2017 Department of Economics, University of Copenhagen Assignment 5 The New Keynesian Phillips Curve The Case: Inflation tends to be pro-cycical with high inflation during times of

Chapter 14 Monetary Policy

Chapter Overview Chapter 14 Monetary Policy The objectives and the mechanics of monetary policy are covered in this chapter. It is organized around seven major topics: (1) interest rate determination;

Chapter Overview Chapter 14 Monetary Policy The objectives and the mechanics of monetary policy are covered in this chapter. It is organized around seven major topics: (1) interest rate determination;

Understanding the Macroeconomic Scenario: Global Demand, Global Supply Chains

Understanding the Macroeconomic Scenario: Global Demand, Global Supply Chains 12 June 2014 Fabio Sdogati, fabio.sdogati@polimi.it Table of Contents 1. Economic Scenario after the Great Recession 2. Structural

Understanding the Macroeconomic Scenario: Global Demand, Global Supply Chains 12 June 2014 Fabio Sdogati, fabio.sdogati@polimi.it Table of Contents 1. Economic Scenario after the Great Recession 2. Structural

Monetary Policy in the Wake of the Crisis Olivier Blanchard

Monetary Policy in the Wake of the Crisis Olivier Blanchard Let me start with my bottom line: Before the crisis, mainstream economists and policymakers had converged on a beautiful construction for monetary

Monetary Policy in the Wake of the Crisis Olivier Blanchard Let me start with my bottom line: Before the crisis, mainstream economists and policymakers had converged on a beautiful construction for monetary

MonetaryTrends. What is the slope of the yield curve telling us?

MonetaryTrends August What is the slope of the yield curve telling us? A yield curve is a graph of interest rates for bonds that have similar risk characteristics but differing maturities. Most of the

MonetaryTrends August What is the slope of the yield curve telling us? A yield curve is a graph of interest rates for bonds that have similar risk characteristics but differing maturities. Most of the

Global Monetary and Financial Stability Policy. Fall 2012 Professor Zvi Eckstein FNCE 893/393

Global Monetary and Financial Stability Policy Fall 2012 Professor Zvi Eckstein FNCE 893/393 September 5, 2012 to October 18, 2012 Office hours: SH-DH room 2336, Tuesday 4:30 6:00 pm, by appointment Email:

Global Monetary and Financial Stability Policy Fall 2012 Professor Zvi Eckstein FNCE 893/393 September 5, 2012 to October 18, 2012 Office hours: SH-DH room 2336, Tuesday 4:30 6:00 pm, by appointment Email:

Incorporating Macro-prudential Instruments into Monetary Policy: Thailand s experience

Incorporating Macro-prudential Instruments into Monetary Policy: Thailand s experience Dr. CHAYAWADEE CHAI-ANANT Division Executive, International Department Bank of Thailand Japan, 22 March 2012 Issues

Incorporating Macro-prudential Instruments into Monetary Policy: Thailand s experience Dr. CHAYAWADEE CHAI-ANANT Division Executive, International Department Bank of Thailand Japan, 22 March 2012 Issues

Capital Flows, Cross-Border Banking and Global Liquidity. May 2012

Capital Flows, Cross-Border Banking and Global Liquidity Valentina Bruno Hyun Song Shin May 2012 Bruno and Shin: Capital Flows, Cross-Border Banking and Global Liquidity 1 Gross Capital Flows Capital flows

Capital Flows, Cross-Border Banking and Global Liquidity Valentina Bruno Hyun Song Shin May 2012 Bruno and Shin: Capital Flows, Cross-Border Banking and Global Liquidity 1 Gross Capital Flows Capital flows

Comments: Monetary Policy in a Globalized Economy by Helene Rey

Comments: Monetary Policy in a Globalized Economy by Helene Rey José De Gregorio Universidad de Chile Peterson Institute for International Economics November 2015 Agenda 1 From the trilemma to the dilemma

Comments: Monetary Policy in a Globalized Economy by Helene Rey José De Gregorio Universidad de Chile Peterson Institute for International Economics November 2015 Agenda 1 From the trilemma to the dilemma

4/28/2015 PANICS OF THE PRE-FED ERA

A CENTURY OF THE FEDERAL RESERVE: SUCCESS OR FAILURE? Lawrence H. White George Mason U. Foundation for Teaching Economics 23 April 2015 WHY WAS THE FEDERAL RESERVE ESTABLISHED? Many people are freemarket

A CENTURY OF THE FEDERAL RESERVE: SUCCESS OR FAILURE? Lawrence H. White George Mason U. Foundation for Teaching Economics 23 April 2015 WHY WAS THE FEDERAL RESERVE ESTABLISHED? Many people are freemarket

Taylor Rules and the Great Inflation

Taylor Rules and the Great Inflation Alex Nikolsko-Rzhevskyy and David H. Papell San Francisco Fed November 9, 2010 Monetary Policy in the 1970s Result was the Great Inflation Did the Fed Conduct Bad Policy

Taylor Rules and the Great Inflation Alex Nikolsko-Rzhevskyy and David H. Papell San Francisco Fed November 9, 2010 Monetary Policy in the 1970s Result was the Great Inflation Did the Fed Conduct Bad Policy

Monetary Policy Report 1/09

.. Monetary Policy Report / Governor Svein Gjedrem London, March Norwegian banks equity capital ) Per cent of total assets. - Sources: Klovland (), Statistics Norway and Norges Bank ) Includes savings

.. Monetary Policy Report / Governor Svein Gjedrem London, March Norwegian banks equity capital ) Per cent of total assets. - Sources: Klovland (), Statistics Norway and Norges Bank ) Includes savings

R-Star Wars: The Phantom Menace

R-Star Wars: The Phantom Menace James Bullard President and CEO 34th Annual National Association for Business Economics (NABE) Economic Policy Conference Feb. 26, 2018 Washington, D.C. Any opinions expressed

R-Star Wars: The Phantom Menace James Bullard President and CEO 34th Annual National Association for Business Economics (NABE) Economic Policy Conference Feb. 26, 2018 Washington, D.C. Any opinions expressed

EXTENSIVE ABSTRACT. Can Phillips curve explain the recent behavior of inflation? Evidence from G7 countries

EXTENSIVE ABSTRACT Can Phillips curve explain the recent behavior of inflation? Evidence from G7 countries Michael Chletsos 1 University of Ioannina Vassiliki Drosou University of Ioannina The financial

EXTENSIVE ABSTRACT Can Phillips curve explain the recent behavior of inflation? Evidence from G7 countries Michael Chletsos 1 University of Ioannina Vassiliki Drosou University of Ioannina The financial

Experience Research Advisor Present Research Department, Federal Reserve Bank of San Francisco.

Kevin J. Lansing April 3, 2018 Research Department, Federal Reserve Bank of San Francisco, P.O. Box 7702 San Francisco CA 94120-7702, (415)-974-2393, email: kevin.j.lansing@sf.frb.org Education Ph.D. Economics,

Kevin J. Lansing April 3, 2018 Research Department, Federal Reserve Bank of San Francisco, P.O. Box 7702 San Francisco CA 94120-7702, (415)-974-2393, email: kevin.j.lansing@sf.frb.org Education Ph.D. Economics,

Shadow Interest Rates and the Stance of U.S. Monetary Policy

Shadow Interest Rates and the Stance of U.S. Monetary Policy James Bullard President and CEO, FRB-St. Louis 8 November 2012 Center for Finance and Accounting Research Annual Corporate Finance Conference

Shadow Interest Rates and the Stance of U.S. Monetary Policy James Bullard President and CEO, FRB-St. Louis 8 November 2012 Center for Finance and Accounting Research Annual Corporate Finance Conference

The Natural Rate. R- Star: The Natural Rate and Its Role in Monetary Policy CHAPTER TWO WHAT IS R- STAR AND WHY DOES IT MATTER?

CHAPTER TWO The Natural Rate SECTION ONE R- Star: The Natural Rate and Its Role in Monetary Policy Volker Wieland WHAT IS R- STAR AND WHY DOES IT MATTER? The natural or equilibrium real interest rate has

CHAPTER TWO The Natural Rate SECTION ONE R- Star: The Natural Rate and Its Role in Monetary Policy Volker Wieland WHAT IS R- STAR AND WHY DOES IT MATTER? The natural or equilibrium real interest rate has

April 2015 Fiscal Monitor

International Monetary Fund April 17, 2015 April 2015 Fiscal Monitor Now is the Time: Fiscal Policies for Sustainable Growth Xavier Debrun Deputy Chief, Fiscal Policy and Surveillance, Fiscal Affairs Department

International Monetary Fund April 17, 2015 April 2015 Fiscal Monitor Now is the Time: Fiscal Policies for Sustainable Growth Xavier Debrun Deputy Chief, Fiscal Policy and Surveillance, Fiscal Affairs Department

Session 1: What is the Impact of Negative Interest Rates on Europe s Financial System? How Do We Get Back to Normal?

: What is the Impact of Negative Interest Rates on Europe s Financial System? How Do We Get Back to Normal? Disclaimer: The views expressed in this presentation are those of the presenter and do not necessarily

: What is the Impact of Negative Interest Rates on Europe s Financial System? How Do We Get Back to Normal? Disclaimer: The views expressed in this presentation are those of the presenter and do not necessarily

Capital Flows, the IMF s Institutional View, and An Alternative. John B. Taylor 1

Capital Flows, the IMF s Institutional View, and An Alternative John B. Taylor 1 Remarks at the Policy Conference Currencies, Capital, and Central Bank Balances Hoover Institution Stanford University May

Capital Flows, the IMF s Institutional View, and An Alternative John B. Taylor 1 Remarks at the Policy Conference Currencies, Capital, and Central Bank Balances Hoover Institution Stanford University May

Lessons from the Subprime Crisis

Lessons from the Subprime Crisis Franklin Allen University of Pennsylvania Presidential Address International Atlantic Economic Society April 11, 2008 What caused the subprime crisis? Some of the usual

Lessons from the Subprime Crisis Franklin Allen University of Pennsylvania Presidential Address International Atlantic Economic Society April 11, 2008 What caused the subprime crisis? Some of the usual

Operation Twist: 1961 vs. 2011

Amol Agrawal amol@stcipd.com +91-22-66202234 Operation Twist: 1961 vs. 2011 Ever since the crisis, Federal Reserve (and other central banks following Fed) has introduced new innovative measures to stimulate

Amol Agrawal amol@stcipd.com +91-22-66202234 Operation Twist: 1961 vs. 2011 Ever since the crisis, Federal Reserve (and other central banks following Fed) has introduced new innovative measures to stimulate