S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * *

|

|

|

- Lynette Joseph

- 5 years ago

- Views:

Transcription

1 S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter of the application of CONSUMERS ENERGY COMPANY ) and THE DETROIT EDISON COMPANY ) Case No. U- 0 Requesting that the Commission Grant ) Accounting Approval of Depreciation ) Practices for the Ludington Pumped ) Storage Plant. ) ) QUALIFICATIONS AND DIRECT TESTIMONY OF DANIEL M. BIRKAM MICHIGAN PUBLIC SERVICE COMMISSION June 0, 0

2 QUALIFICATIONS OF DANIEL M. BIRKAM PART I Q: Would you please state your name and business address. A: My name is Daniel M. Birkam, and my business address is Mercantile Way Ste 7, Lansing, MI 89. Q: By whom are you employed, and what is your present position? A: I am employed by the Michigan Public Service Commission (MPSC) as an Auditor in the Revenue Requirements Section of the Regulated Energy Division. Q: How long have you been employed by the MPSC and what are your duties? A: I have been employed by the MPSC since March of 00. I have mainly been assigned to analyze and make recommendations regarding Rate Base, Net Operating Income, Depreciation, and Manufactured Gas Plant (MGP) site cleanup issues in general rate cases, depreciation rate cases, and special accounting cases. I have also performed GCR and PSCR reconciliation audits. Q: What is your educational background? A: In 99, I graduated from Western Michigan University with a B.A. in English, history and philosophy. In 00, I graduated from Davenport University with a B.S. in Accounting. I have also completed the National Association of Regulatory Utility Commissioners (NARUC) Annual Regulatory Studies program and the NARUC Accounting and Auditing for Utility Regulators and Consumer Advocates program, both in 00. I attended the Institute of Public Utilities (IPU) Advanced Regulatory Studies Program in 00, 00, 008, and 009. I completed the Society of Depreciation Professionals (SDP) Basic, Intermediate, and Advanced Depreciation Training in 00, 00, and 00. I am also an SDP member.

3 QUALIFICATIONS OF DANIEL M. BIRKAM PART I Q. Do you have any professional licenses? A. Yes. I am a Certified Public Accountant, licensed by the State of Michigan. Q. Have you previously prepared and filed testimony before the Commission? A. Yes. I have prepared and filed testimony before the MPSC in the following cases: Case No. U-7 - Consumers Energy gas rate case, Case No. U- - Detroit Edison electric rate case, Case No. U-9 - Consumers gas depreciation rate case, Case No. U- - Consumers electric rate case, Case No. U-99 - MichCon depreciation rate case, Case No. U-98 - WEPCo electric rate case, Case No. U-98 - Consumers gas rate case, Case No. U-98 - MichCon gas rate case, Case No. U-9 MGU depreciation case, Case No. U-9 Consumers electric rate case. I have prepared and filed testimony in the following settled cases: Case No. U-89 - SEMCO gas rate case, Case No. U-90 - Consumers gas rate case, Case No. U-0 - Consumers gas rate case, Case No. U SEMCO depreciation rate case, Case No. U-80 I&M electric rate case, Case No. U-8 - Consumers gas rate case, Case No. U-0 Consumers electric depreciation case.

4 QUALIFICATIONS OF DANIEL M. BIRKAM PART I I have also prepared and filed testimony in the following pending cases before the MPSC: Case No. U-7 Detroit Edison depreciation case, Case No. U-7 Detroit Edison rate case, Case No. U- MichCon MGP accounting approval case, Case No. U- Consumers wind plant depreciation case. Q. Have you worked on any other depreciation cases? A. Yes. I was Staff s case coordinator and lead auditor in the following settled depreciation cases: U-0, U-79, U-8, and U-; I also worked on U-989, U-9, and U-0. In addition I was Staff s case coordinator and worked on the General Accounting Case U-9.

5 DIRECT TESTIMONY OF DANIEL M. BIRKAM Part II Q. What is the purpose of your testimony? A. The purpose of my testimony is to present Staff s position on the depreciation rates for the Consumers Energy (Consumers) and Detroit Edison s (Edison) (collectively the Companies ) jointly owned Ludington Pumped Storage Electric Utility Plant. This will include supporting Staff s depreciation policy and the results of Staff s depreciation study compared to the Companies depreciation study, which will involve discussions of Remaining Life, Depreciation Reserve, and Net Salvage. I will also support Staff s net salvage adjustment. I will discuss Staff s position on the Standard Retirement Units (SRU s). Finally, I will discuss the Edison only adjustment for its portion of Ludington plant. Q. Are you sponsoring any exhibits? A. Yes, I have prepared the following exhibits: Exhibit S-, Schedule :Depreciation Rate and Expense Calculation, Exhibit S-, Schedule : Net Salvage Calculation. Q. Were these exhibits prepared by you or under your direction? A. Yes, they were. Depreciation Study: Q. Did Consumers and Edison perform a depreciation study as part of their Ludington Pumped Storage depreciation rate case? A. Yes. The Companies depreciation study was performed by Dane Watson, a partner of Alliance Consulting Group. Q. What depreciation methodology was used by the Companies in the depreciation study performed on their behalf by Mr. Watson?

6 DIRECT TESTIMONY OF DANIEL M. BIRKAM Part II A. As stated by Mr. Watson on page of his testimony: The straight-line, broad group, life span remaining-life depreciation system was employed to calculate annual and accrued depreciation in this study. Q. What is the Companies current method of calculating net salvage? A. The Companies currently uses the Traditional Method. Q. Does Staff agree that the Companies current depreciation methodology and method of calculating net salvage are reasonable? A. Yes. Staff agrees that this depreciation methodology and method of calculating net salvage produce a reasonable result in this case. Q. What is the resulting annual depreciation accrual and rate calculated by Mr. Watson, using of his recommended depreciation and net salvage methodologies and 008 plant in service? A. The result is an annual accrual of $,, for Consumers and $,, for Edison. This is an increase of $8,8, and $8,9,90 respectively. These increase the proposed depreciation rates to 8.7% and 7.9% respectively. Q. How are the results of the Study applied to each Company? A. The demolition is applied by percentage of ownership to each company, and the remainder of the study is applied to each Companies plant in service and depreciation reserve. Q. Does Staff agree with the results of this Study? A. No. While Staff agrees with the methodology, as explained below Staff disagrees with the Companies proposed net salvage and the remaining service life adjustments.

7 DIRECT TESTIMONY OF DANIEL M. BIRKAM Part II Q. Did Staff perform its own Depreciation Study? A. No. Staff did not perform its own Depreciation Study but adjusted the Companies Depreciation Study to be consistent with Staff s position. Q. Did the Companies perform an engineering demolition study for the purpose of calculating the net salvage the Ludington Pumped Storage Plant? A. Yes. Staff witnesses Jing Shi and James LaPan will be addressing the demolition study. Q. What is Staff s overall proposed depreciation rate and expense, given the year ended 008 plant in service? A. Staff s proposed overall depreciation rates are.% for Consumers and.% for Edison respectively, as shown on column (j) of Exhibit S-, Schedule, page. Staff s depreciation expenses given the year ended 008 are $,089,78 and $,7,987 respectively, as shown on column (i) of Exhibit S-, Schedule, page. This is lower than the current rates by $,,8, and $,77,09, respectively as shown on column (i) of Exhibit S-, Schedule, page. This is also lower than the Companies proposed rates by $,,770 and $,98,99 respectively as shown on column (k) of Exhibit S-, Schedule, page. Staff s overall proposed depreciation rate and expense result from Staff s adjustments to the demolition studies and the remaining life adjustment discussed below. Q. Please describe Schedule S-, Exhibit. A. Page of Schedule S-, Exhibit shows the computation of Staff s proposed depreciation accrual and accrual rate for the Ludington Pumped Storage plant. Lines through 7 shows this computation by account for Consumers Energy s

8 DIRECT TESTIMONY OF DANIEL M. BIRKAM Part II plant in service, and lines 8 through show this for Detroit Edison s plant in service. Columns (a) and (b) are the account descriptions. Column (c) is the year ended 008 plant in service balance (which is adjusted for Detroit Edison, as explained below). Column (d) is the allocated depreciation reserve for the 008 year ended balance. Column (e) is the net salvage percentage. Column (f) is the net salvage amount. Column (g) is the unaccrued balance of depreciation. Column (h) is the remaining life, which is the life remaining from 008 until the license expires in 09. Column (i) is the annual depreciation accrual expense based on the year end 008 balance. Column (j) is the proposed accrual rate. Page of Schedule S-, Exhibit is a comparison between the existing depreciation accrual expense and rates given 008 year ended plant with the Companies proposed rates, and Staff s proposed rates. Columns (d) and (e) are the existing expense and rate, columns (f) and (g) are the Companies proposed expense and rates, and columns (i) and (j) are the Staff s proposed expense and rates. Column (h) compares the Companies proposed accrual expense with the existing amount. Column (k) compares Staff s proposed accrual expense with the Companies. Column (j) compares Staff s proposed accrual expense with the existing amount. Remaining Life: Q. What is the Companies proposed retirement date for the Ludington Pumped Storage Plant? A. As stated on page, line of the testimony of Consumers witness Kehoe, The retirement date for the Ludington Plant is 09. 7

9 DIRECT TESTIMONY OF DANIEL M. BIRKAM Part II Q. Does Staff agree that the Companies determination of the retirement date is reasonable? A. Yes. Staff examined the remaining life, and agrees that the FERC License Date is reasonable for use as the retirement date of the plant. Q. What is the difference between Staff s projected remaining lives shown on Exhibit S-, Schedule, page, column (h) and the Companies projected remaining lives shown on Exhibit A- (DAW-) pages and? A. The Companies applied life curves to the remaining unaccrued balances to rebalance the depreciation reserve, and decided to carry these weighted remaining lives to calculate the proposed accrual rate, even though the Companies accepted the FERC license date as the terminal date for the Ludington Pumped Storage Plant. Staff disagrees with this approach. The reserve rebalancing already includes interim retirements, as does the net salvage rate used in the accrual computation. Staff finds that the remaining life for each account is more properly set by the plant retirement date. Depreciation Reserve: Q. Did Consumers propose rebalancing the depreciation reserve? A. Yes. This was supported by Mr. Watson. Q. Does Staff agree with Consumers rebalancing of the depreciation reserve? A. Staff agrees that the depreciation reserve should be rebalanced. Staff, however proposes rebalancing the reserve using Staff s proposed net salvage. The result of this is on column (d) of Exhibit S-, Schedule, page. Net Salvage: 8

10 DIRECT TESTIMONY OF DANIEL M. BIRKAM Part II Q. Does Staff agree with the Net Salvage amounts calculated by the Companies for their various individual rates for each depreciable account using the Traditional Method? A. No, Staff adjusted the Net Salvage amounts proposed by the Companies. These adjustments can be seen on Exhibit S-, Schedule. Q. Please describe Exhibit S-, Schedule. A. Exhibit S-, Schedule shows the computation of the Net Salvage rate. Lines through 7 show the computation for Consumers plant totals, and lines 8 through show the calculation for Edison s plant totals. Columns (a), (b), and (c) show the account numbers, names, and balances. Column (d) shows the terminal net salvage rate. Columns (e) and (f) show the interim retirements and rate. Column (g) shows the plant balance after interim retirements. Column (h) shows the inflated Removal Cost with Interim. Column (i) shows the Combined Net Salvage rate. Q. What is the basis for Staff s adjustments to the Net Salvage of these accounts? A. Staff disagrees with the demolition study for determining the net salvage for steam generation and hydroelectric generation. These adjustments are presented and supported by Staff witness James LaPan. Q. How did the Companies escalate the demolition study to the terminal dismantlement date? A. As described by Mr. Watson on page of his testimony the escalation rate was calculated using the Bureau of Labor Statistics Employment Cost Index- Total 9

11 DIRECT TESTIMONY OF DANIEL M. BIRKAM Part II Private Compensation index. As shown on Exhibit A- (DAW-), page 0 of, this used an ECI factor of., divided by a base year factor of.0. Q. Does Staff agree that this escalation rate is reasonable? A. Yes. Q. Did Staff examine the calculation of the Interim retirements in this case? A. Yes. Staff examined these calculations, and found them to be reasonable. Q. What is Staff s recommendation concerning the Companies Net Salvage in that case? A. Staff s adjustments to the Companies Net Salvage is negative $,,9 for Consumers and negative $,8,8 for Edison using 008 plant in service, as shown on column (h) of Exhibit S-, Schedule. The net salvage rates for each account can be seen on column (i). Traditional Method of Calculating Net Salvage: Q. Please explain the traditional method of determining net salvage? A. The traditional method of determining net salvage is to take the recent history of salvage values, net of the cost of removal, and compare them to the accompanying original costs to determine a percentage. Various types of analyses are then used as part of one s professional judgment to calculate this percentage, with the understanding that it is a reasonable estimate of the future cost of removal and salvage value. It is also understood that this value will be reviewed for adjustment every few years in future depreciation rate cases due to the likelihood of better information being available. Thus, the traditional method produces a reasonable present value of the net salvage expense to be recovered 0

12 DIRECT TESTIMONY OF DANIEL M. BIRKAM Part II without the need for a present valuation discount using an estimated discount rate of a future value reached with an estimated inflation rate. When net salvage is negative, customers recover the annual additional reduction in rate base; this recovery is at the company s rate of return, and occurs whenever a utility files a rate case. At the same time, the company recovers the additional depreciation expense as part of its net operating income. Q. Are there other methods for determining net salvage? A. Yes. The Commission required five different methods to be considered in its order in its General Accounting Case, Case No. U-9. Q. What are the five methods of determining net salvage that the Commission ordered in Case No. U-9? A. The five methods are:. The traditional method.. The traditional method using the Standard Retirement Units proposed by Staff.. The Inflation Adjusted method using the Standard Retirement Units proposed by Staff.. The FAS approach (time value of money).. The FAS approach using the Standard Retirement Units proposed by Staff. Q. Has the Commission, since the Order in Case No. U-9, indicated preference for any of the five methods? A. Yes. In this case, Case No. U-0, the Commission granted Consumers Motion for Extension and, the Commission ordered the Companies to use the

13 DIRECT TESTIMONY OF DANIEL M. BIRKAM Part II traditional method with the Standard Retirement Units proposed by Staff in its filing. Q. Does Staff agree with the use of the traditional method of determining net salvage in this case? A. Yes. Staff prefers the traditional method, because, as shown above, it produces the most reasonable estimate for calculating the rate for net salvage recovery in depreciation expense. Traditional Method using Staff s Proposed Standard Retirement Units (SRU s): Q. In Case No. U-9, what SRU s were proposed by Staff? A. Staff proposed the following SRU s: Account Overhead Wire Termini to Termini Account 7 Underground Wire Termini to Termini. Q. Does Staff continue to support these SRU s recommended in Case No. U-9? A. Yes. Staff supports these SRU s because these SRU s lead to lower costs of removal as a component of net salvage in these accounts. This was explained in more detail in the Testimony of Staff witness William Aldrich in Case. No. U- 9. Staff is aware that implementing these SRU s will cause some expenses that are currently capitalized to be expensed as O&M. Q. Are these SRU s currently in place for the Companies? A. These accounts are not part of the Ludington Pumped Storage Plant, but the Commission in U-9 ordered the Companies to address SRU s in this case. Detroit Edison Plant Adjustment:

14 DIRECT TESTIMONY OF DANIEL M. BIRKAM Part II Q. What was the adjustment to the Ludington Pumped Storage Plant made by Detroit Edison? A. This adjustment is explained by Edison witness Phillip Czech on page 7 of testimony: The Ludington plant and depreciation reserve at December, 008 for Edison should be adjusted to correct an inventory reconciliation improperly recorded in the year 00. Edison engaged Jefferson-Wells, an independent consulting firm, to reconcile Edison s Ludington plant detailed property records. The Jefferson-Wells final report detailed specific asset records that were mis-labeled and offsetting asset records that were not included on the Edison property records. Edison processed the accounting entry to record the mis-labeled asset records as a plant retirement in the year 00. The offsetting additions required to correct the Edison Ludington property records were, however, never recorded. This incomplete accounting transaction resulted in an understatement of Edison s Ludington plant and depreciation reserve since the year 00. Q. What is the result of this adjustment? A. According to an audit response from the Company, this would increase the net plant by $,8,09 and increase the depreciation expense by $08,08. Q. Does Staff agree with the results of this adjustment? A. Yes. Staff has examined this adjustment, and finds it reasonable. Conclusion: Q. What are Staff s recommendations in this depreciation rate case?

15 DIRECT TESTIMONY OF DANIEL M. BIRKAM Part II A. Staff has several recommendations in this case. Staff agrees that the Companies depreciation and net salvage methodologies proposed are reasonable, and recommends that the Traditional method for net salvage be accepted. Staff recommends that the remaining live proposed by the Companies be accepted, and that it be used to calculate the annual accruals. Staff recommends that the Commission adopt Staff s proposed rebalancing of the depreciation reserve. Staff further recommends that Consumers depreciation rates be adjusted for Staff s proposed adjustments to net salvage and that the Commission adopt Staff s overall depreciation rate proposed on Exhibit S-, Schedule of.% for Consumers and.% for Edison. Finally, Staff recommends that the Companies file a new depreciation rate case three years from the date of the Commission order in this case. Q. Does this conclude your testimony? A. Yes, it does.

16 S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter of the application of CONSUMERS ENERGY COMPANY ) and THE DETROIT EDISON COMPANY ) Case No. U- 0 Requesting that the Commission Grant ) Accounting Approval of Depreciation ) Practices for the Ludington Pumped ) Storage Plant. ) ) EXHIBITS OF DANIEL M. BIRKAM MICHIGAN PUBLIC SERVICE COMMISSION June 0, 0

17 Witness: Birkam, D.M. Exhibit No.: S- Schedule No.: Date: June 0, 0 Page: of LUDINGTON PUMPED STORAGE FACILITY COMPUTATION OF PROPOSED DEPRECIATION ACCRUAL RATE AT DECEMBER, 008 CONSUMERS ENERGY Line (a) (b) (c) (d) (e) (f) (g) (h) (i) (j) Allocated Future Net Proposed Plant Depreciation Net Salvage Unaccrued Remaining Annual Depr Depr Acct Description //008 //008 Salv % Amount Balance Life Accrual Accrual Structures & Improvements 7,70,8,,70-8% (,9,8) 9,,8.00,99.7% Reservoirs, Dams, Waterways 9,9, 79,7,988-8% (,8,),7,8.00,0,0.09% Waterwheels, Turbines, Gen,97,00,, -8% (,,) 9,, ,70.7% Accessory Electric Equip 7,7,07,8,89-7% (,8,88),79,.00, % Misc Power Plant Equip,9,0,,7-7% (,8) 9,98.00,00.% Roads, Railroads & Bridges,,8,9,7-8% (,7) 77,0.00,.08% 7 Grand Total,9,70,88,8 (,7,0) 8,8,,089,78.% LUDINGTON PUMPED STORAGE FACILITY COMPUTATION OF PROPOSED DEPRECIATION ACCRUAL RATE AT DECEMBER, 008 DETROIT EDISON Allocated Future Net Proposed Plant Depreciation Net Salvage Unaccrued Remaining Annual Depr Depr Acct Description //008 //008 Salv % Amount Balance Life Accrual Accrual 8 Structures & Improvements 9,8,,87,8 -% (,77,99) 9,9,0.00,7.9% 9 Reservoirs, Dams, Waterways,9,8 89,70,89 -% (7,0,),,9.00,,8.0% 0 Waterwheels, Turbines, Gen,98,7,7, -% (0,9,8) 0,0,.00 7,9.0% Accessory Electric Equip 7,9,0,00,0 -% (,,),08,.00 7,87 0.9% Misc Power Plant Equip,007,,, -% (0,9) 88,.00,7.07% Roads, Railroads & Bridges,8,78,7, -% (0,7) 8,8.00 0,7.09% Grand Total 9,00, 0,0, (,8,9) 9,87,8,7,987.%

18 Witness: Birkam, D.M. Exhibit No.: S- Schedule No.: Date: June 0, 0 Page: of LUDINGTON PUMPED STORAGE FACILITY COMPARISON OF EXISTING AND PROPOSED DEPRECIATION ACCRUAL AT DECEMBER, 008 CONSUMERS ENERGY Line (a) (b) (c) (d) (e) (f) (g) (h) (i) (j) (k) (l) Compnny Company Staff Staff Change in Staff Present Proposed Company Change Proposed Staff Depreciation Change Depreciation Present Depreciation Proposed in Depreciation Proposed Accrual in Plant at Accrual Depreciation Accrual Depreciation Depreciation Accrual Depreciation from Depreciation Acct Description //008 Rate Accrual Rate Accrual Accrual Rate Accrual Company Accrual Structures & Improvements 7,70,8..% 7, %,9,,08,.7%,99 (,7,) (8,89) Reservoirs, Dams, Waterways 9,9,.7.8%,8,77 8.% 8,9,,00,.09%,0,09 (7,9,) (,09,88) Waterwheels, Turbines, Gen,97,00.9.9%,, 9.08%,8,,70,9.7% 77,790 (,09,) (9,7) Accessory Electric Equip 7,7,07.7.8% 0,98 7.7%,,8 0.9%,89 (9,) (7,) Misc Power Plant Equip,9,0.0.7% 9,0 0.8% 09, 0,09.%, (87,09) (,0) Roads, Railroads & Bridges,,7.9.% 9, 9.0% 8,0 89,.08%,8 (,07) (,8) 7,9,70..%,7,9 8.7%,, 8,8,.%,09, (,,770) (,,8) LUDINGTON PUMPED STORAGE FACILITY COMPARISON OF EXISTING AND PROPOSED DEPRECIATION ACCRUAL AT DECEMBER, 008 DETROIT EDISON Company Company Staff Staff Change in Staff Present Proposed Company Change Proposed Staff Depreciation Change Depreciation Present Depreciation Proposed in Depreciation Proposed Accrual in Plant at Accrual Depreciation Accrual Depreciation Depreciation Accrual Depreciation from Depreciation Acct Description //008 Rate Accrual Rate Accrual Accrual Rate Accrual Company Accrual 8 Structures & Improvements 9,8,0.8.8% 9,0 7.%,, 9,.9%,900 (,7,) (,) 9 Reservoirs, Dams, Waterways,9,8.9.9%,7,9 7.7% 8,99,8,0,8.0%,,09 (7,,7) (,9,79) 0 Waterwheels, Turbines, Gen,98,7..0%,8,0 7.7%,7,0,70,9.0% 7,7 (,80,880) (,0,) Accessory Electric Equip 7,9,9.7.8% 7,8.7%,799 0,7 0.9% 7,8 (9,) (,) Misc Power Plant Equip,007,.8.98% 9,8 9.8% 97,9 8,8.07%,80 (7,) (8,) Roads, Railroads & Bridges,8, %, 7.7%, 9,7.09% 0,0 (,) (,00) 9,00,.7.9%,0,7 7.9%,, 8,9,90.%,7, (,98,99) (,77,09)

19 LUDINGTON PUMPED STORAGE FACILITY COMPUTATION OF NET SALVAGE RATE Witness: Birkam, D.M. Exhibit No.: S- Schedule No.: Date: June 0, 0 Line (a) (b) (c) (d) (e) (f) (g) (h) (i) CONSUMERS ELECTRIC Inflated Combined Total Plant Terminal Interim Interim Balance Removal Net Salvage Ret % Retirements RC % After Interim Ret Cost w Terim %.0 Ludington 7,70,8-8.%,08, %,,87 -,9,70-7.9%.0 Ludington 9,9, -8.% 8,,0 -.00% 87,8,0 -,80,99-8.0%.0 Ludington,97,00-8.% 7,80,8 -.00%,9, -,,00-7.9%.0 Ludington 7,7,07-8.%,9,9 -.00%,, -,8,7 -.9%.0 Ludington,9,0-8.% 90, %,0,08 -,8-7.%.0 Ludington,,8-8.% %,,8 -,7-8.% 7,9,70 ########,,9 -,,9 DETROIT EDISON 8.0 Ludington 9,8, -.%,88,8 -.00% 7,,8 -,77,0 -.80% 9.0 Ludington,9,8 -.% 0,8,9 -.00% 0,80,7-7,08,98 -.7% 0.0 Ludington,98,7 -.% 9,9, %,0, -0,9, %.0 Ludington 7,9,0 -.%,00,0 -.00%,99,0 -,,09 -.%.0 Ludington,007, -.% 98, -.00%,079,08-0,0 -.0%.0 Ludington,8,78 -.% %,8,78-0,7 -.% 9,00,,77,,,90 -,8,8 /7/00

20 S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter of the application of CONSUMERS ENERGY COMPANY ) and THE DETROIT EDISON COMPANY ) Case No. U-0 Requesting that the Commission Grant ) Accounting Approval of Depreciation ) Practices for the Ludington Pumped ) Storage Plant. ) ) QUALIFICATIONS AND DIRECT TESTIMONY OF JAMES E. LA PAN MICHIGAN PUBLIC SERVICE COMMISSION June 0, 0

21 QUALIFICATIONS OF JAMES E. LA PAN PART I Q. Please state your name and business address. A. My name is James E. LaPan. My business address is Mercantile Way, Lansing, MI Q. Where are you currently employed and in what position? A. I am employed by the Michigan Public Service Commission (MPSC or Commission) as a Public Utility Engineer in the Regulated Energy Division. Q. What are your responsibilities in your current position? A. Responsibilities in my current position consist of assisting the Commission with technical analysis of Gas Cost Recovery (GCR) plan and reconciliation proceedings, utility rate case filings and utility depreciation case filings. Furthermore, I provide oversight in the area of facility operations, environmental compliance, system integrity, and pipeline infrastructure. Since my employment with the Commission, I have successfully completed several onsite and offsite training activities. I have been involved in the development of MPSC Staff (Staff) Reports and Recommendations for the Commission. I am also an active participant in National Association of Regulatory Utility Commissioners (NARUC) Natural Gas Subcommittee work group and I ve successfully completed NARUC s two week training program for regulatory professionals held each year on the campus of Michigan State University (MSU). Q. Would you describe your educational background and work experience? A. I earned a Bachelor of Science in Biosystems Engineering from Michigan State University in August 00. I transferred to MSU from the honors program at Delta College.

22 QUALIFICATIONS OF JAMES E. LA PAN PART I While attending Delta College I was employed at the Delphi Corporation as an engineering student. During my apprenticeship at Delphi I worked with engineering professionals to address various technical issues including State and Federal regulatory and compliance issues related to onsite electric generation, hazardous material handling, and wastewater treatment. I was also directly involved in the activities surrounding the decommissioning and demolition of Delphi s Chassis Plant, Plant. In addition, I was responsible for the development of several programs and operational procedures that dealt with the capture and reuse of spent materials, in particular waste sludge from Delphi s wastewater treatment facility. After transferring to MSU, I was employed by the Michigan Department of Transportation, Statewide Planning Section. There I provided technical support for the implementation and assignment of Federal Grant money under the Congestion Mitigation and Air Quality Control (CMAQ) program for project proposals submitted to our division. My assistance with the development of modeling and forecasting programs was used to aid in the qualification, quantification, and prioritization, of those proposals. Q. Have you prepared testimony for any other proceedings? A. Yes, I have prepared testimony for the following proceedings: U-0 Consumers Energy Company s Rate Case U-70 SEMCO Energy Gas Company s GCR Plan Case U-98 Michigan Consolidated Gas Company s Rate Case U-89 Consumers Energy Gas Company Rate Case

23 QUALIFICATIONS OF JAMES E. LA PAN PART I U- SEMCO Energy Gas Company Capacity Improvement Case U-7 Detroit Edison Depreciation Case U-8 Consumers Energy Company Rate Case U-0 Consumers Energy Company Depreciation Case

24 DIRECT TESTIMONY OF JAMES E. LA PAN PART II 7 Q. Mr. LaPan, what is the purpose of your testimony in this proceeding? A. The purpose of my testimony is to discuss and support Staff s position and recommendations regarding Consumers Energy Company s and the Detroit Edison Company s (the Company s) proposed demolition cost estimates of decommissioning its Ludington Pumped Storage Plant. Q. Are you supporting any exhibits in this case? A. Yes, I am sponsoring Exhibit S- with the following Schedules: Schedule Schedule Schedule Schedule Schedule Decommissioning Cost Estimate Scrap Value from Powerhouse 998 Decommissioning Study Seeding Adjustment Item Calculations Schedule Response Question June 7, 0 7 Schedule 7 Schedule 8 Schedule 9 Schedule 0 Landfill Tipping Estimates August, 00 Questions Remaining Volume Estimate Updated Tipping Fees Q. Were these exhibits prepared by you or under your direction? A. Yes. Q. What documents have you reviewed and analyzed in this case? A. Staff reviewed the Company s application, testimony and exhibits in Case No. U- 0. Staff also reviewed the Company s responses to data requests from all parties including its 00 Study filed with the FERC. In addition, Staff reviewed

25 DIRECT TESTIMONY OF JAMES E. LA PAN PART II the engineering diagrams of the site and its facilities. Staff also reviewed the Commission s March, 000 order in Case No. U-7 and participated in an onsite review and audit of material and data related to this case. Q. Please summarize your findings. A. Staff found that the Company s Ludington Pump Storage Plant is current with its compliance of the Federal Energy Regulatory Commission s (FERC) licensing obligations and requirements. Furthermore, Staff recognized the Company s efforts to preserve and maintain the life of this facility through its improvements to the facility s infrastructure, its efficiency and with its continuous monitoring and routine maintenance regimen. In addition, Staff identified useful alternatives of this site s design features that will last past its FERC license expiration date. Lastly, Staff notes that there are areas in the Ludington Pumped Storage Project Decommissioning Report (Report) where the cost estimates for demolition and site remediation were overstated and/or incomplete. As a result of these findings, Staff supports the adjustments to the cost estimates of the Company s Report that Staff witness Jing Shi is recommending and include several additional adjustments to the decommissioning costs estimated in the Company s case. Q. Please summarize Staff s recommendations in this case. A. Staff s recommendation is to reduce the estimated cost of decommissioning the Ludington Pump Storage Plant by $,,0 to account for the fact that demolition of this plants reservoir will not be required when the Company s

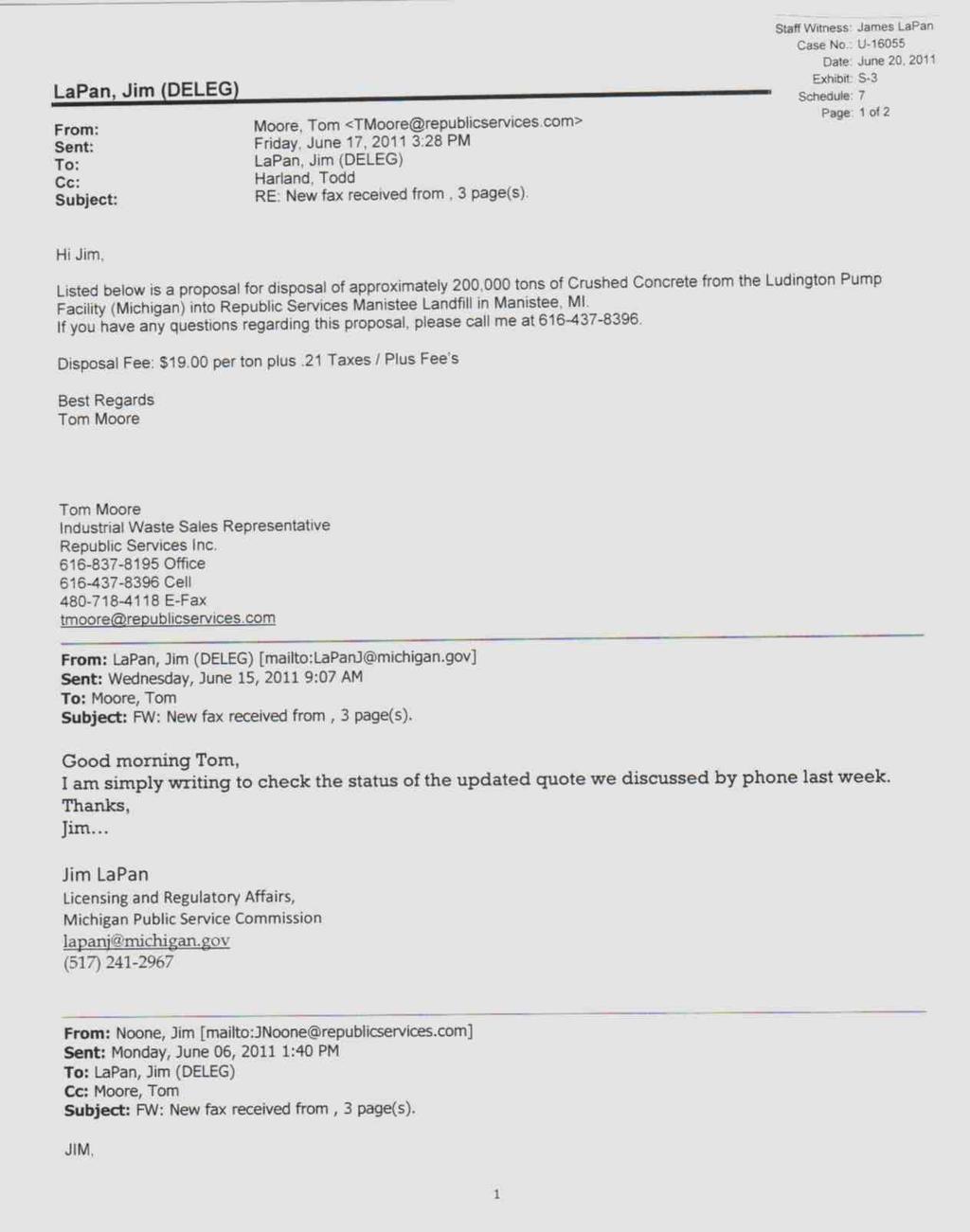

26 DIRECT TESTIMONY OF JAMES E. LA PAN PART II FERC license expires or when the facility is no longer being used for hydrogeneration. Q. Please list the recommendations and adjustments Staff supports that are in addition to those supported by Staff witness Jing Shi. A. In addition to the recommended adjustments presented by Staff witness Jing Shi, Staff recommends; ) reducing the estimates proposed in the Report for landfill charges; specifically tipping fees, ) removal of all equipment within the powerhouse, ) increasing the proposed revenue received for the scrap value associated with salvageable material, ) removal of all manufactured structures located on leased bottom land, ) reducing the cost estimate for cover and seeding the exposed reservoir bottom, ) removing the cost estimate for leveling the reservoir dikes, 7) removing the cost and salvage estimates for removing the reservoir intake apron, 8) removing the cost and salvage related to the project estimates for removing and sealing monitoring and relief wells and 9) adjusting cost estimates to accurately reflect inflation. Q. Please discuss Staff s proposed reduction to the Company s estimates for landfill charges. A. The Company, in their response to Staff audit request, 0-JShi Follow up Kleinschmidt responses 0 0 Item Calcs, Exhibit S-, Schedule, indicated that they relied on an old quote they received from Republic Services, Inc. for landfill tipping fees at Forest Lawn Landfill, Inc.. This quote, from Staff s Exhibit S-, Schedule is only pages of the Company s response due to the rest possibly containing Critical Infrastructure Information.

27 DIRECT TESTIMONY OF JAMES E. LA PAN PART II December, 00 listed the tipping fees at $0.00/ton. Staff contacted Republic Services and requested that they update this same quote. See Exhibit S-, Schedule 7 where it indicates that the cost of landfill tipping will be $9./ton. Staff recommends adjusting the Company s demolition estimates to reflect this updated cost of landfill tipping fees. Exhibit S-, Schedule 0 shows that this would result in an adjustment reducing demolition costs by $708,70. Q. Is the demolition cost reduction associated with landfill tipping fees, as explained above, included in Staff s total cost of demolition shown in column F on Exhibit S-, Schedule? A. No. Staff didn t receive this quote until one day before its filing deadline. It is Staff s intention to include this adjustment to all volumes calculated for landfill tipping. Q. Please discuss Staff s recommendation regarding section... Laying Up of Equipment, page of in Exhibit A-. A. Company consultant D. A. Dow proposes in his opinion of cost for decommissioning the Plant s powerhouse that the powerhouse be left largely intact. He explains on page in Exhibit A- that equipment at the site such as the turbine, the generator, storage tanks, piping, electrical equipment, etc. is expected to stay in place. Staff does not support this method of decommissioning the Plant s powerhouse for three reasons. The first is because Mr. Dow has indicated in Section... on page of his Exhibit A- that Some of the equipment left in place after decommissioning will require funds for permanent laying up. Second is due to the scrap salvage value of this 7

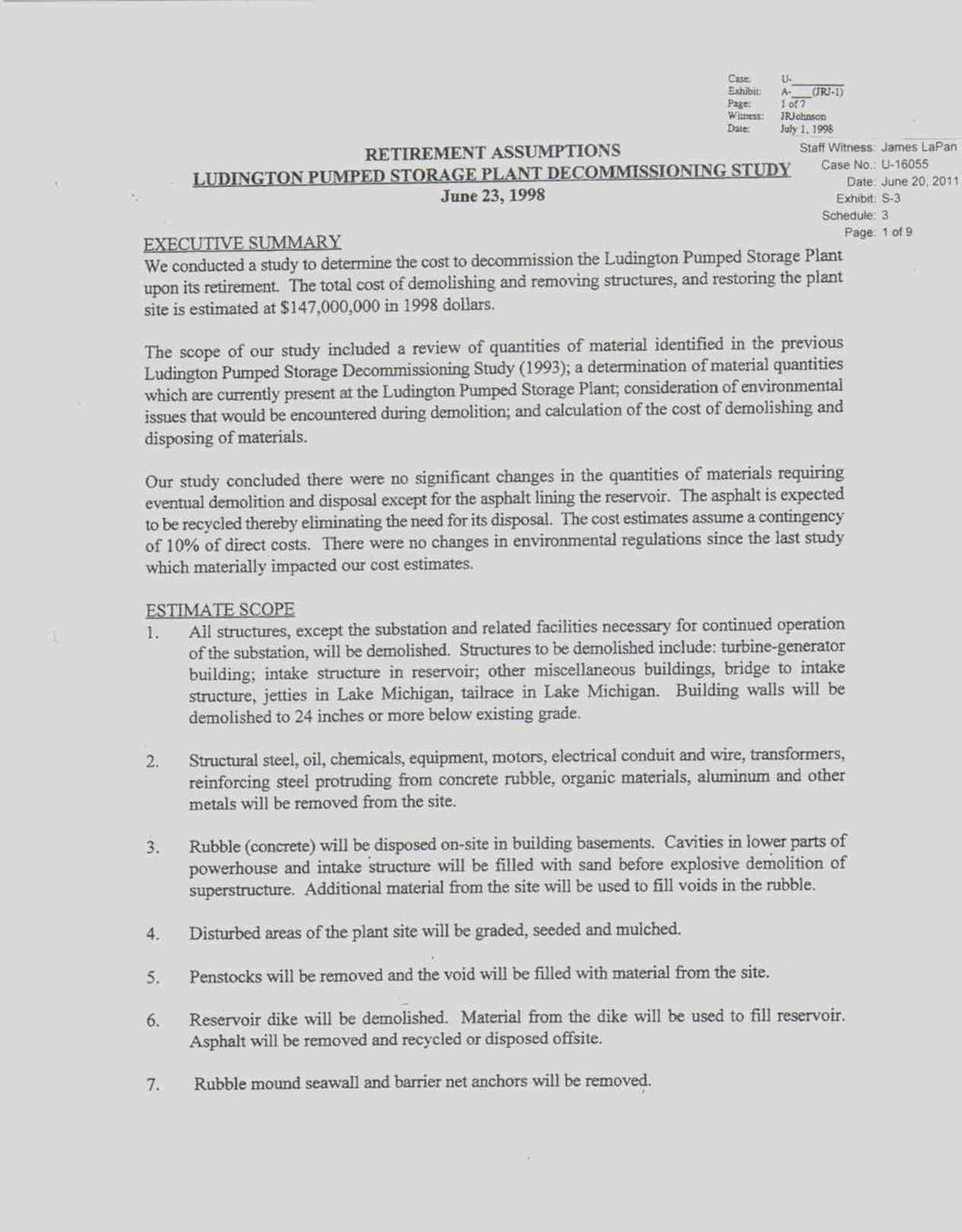

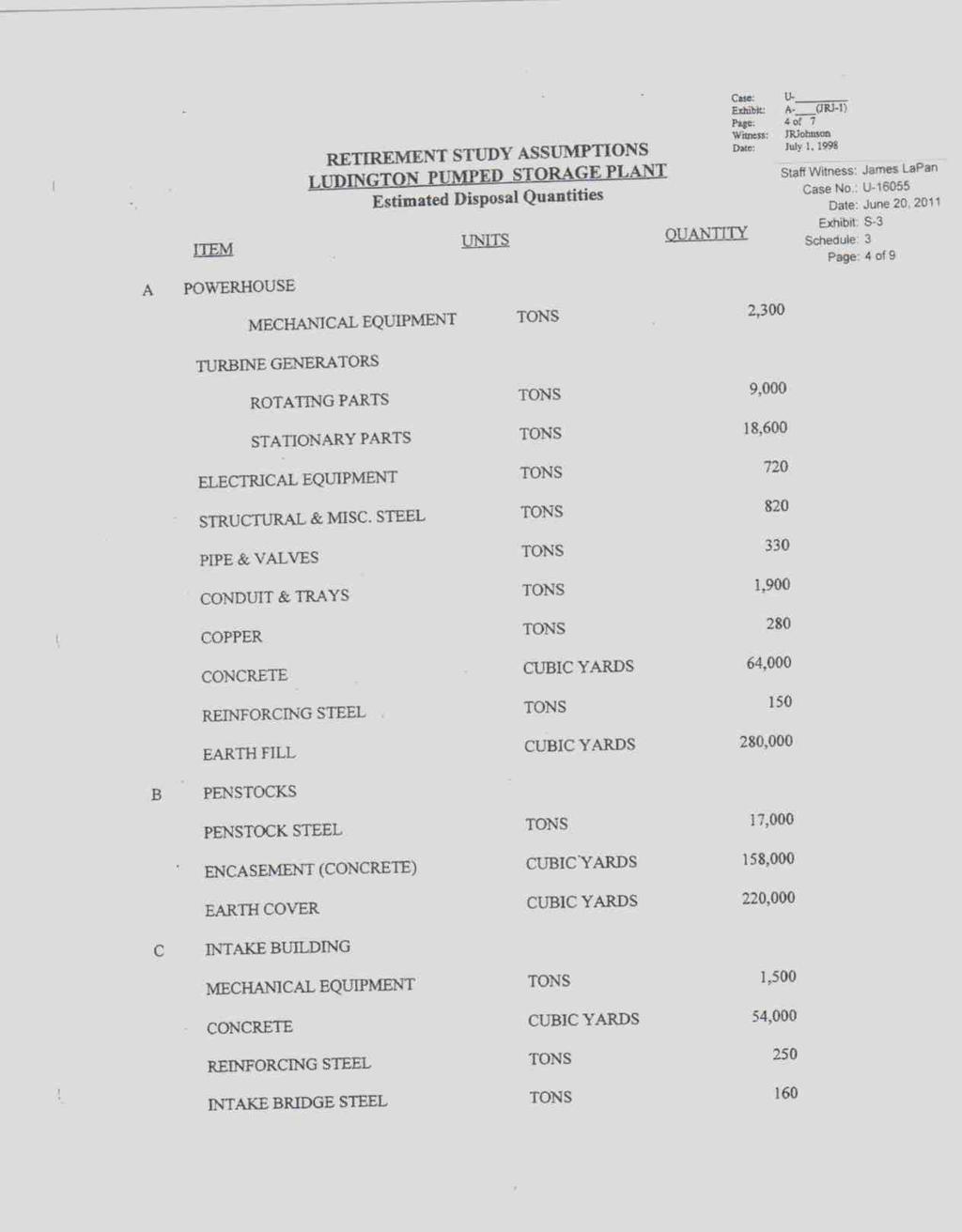

28 DIRECT TESTIMONY OF JAMES E. LA PAN PART II equipment. Removing this equipment would allow the Company to offset the additional costs required to remove the equipment. In addition, if it were to become public knowledge that this equipment was left in place its value could possibly incite others to attempt to retrieve it. Lastly, because of safety concerns. Instead, Staff recommends adopting the method of decommissioning the powerhouse that was presented in the Company s 998 decommissioning study, Case No. U-7, where after the removal of all equipment, the powerhouse would be filled with sand and demolished in place using explosives. Q. Please discuss Staff s proposed increase to the Company s estimates for the revenue received from the scrap value associated with the plants salvageable material. A. Staff is proposing that the Company s cost estimate reflect the value of scrap material retrieved from the powerhouse equipment. Staff estimates, based on the weights and types of material identified in the Company s 998 study, as shown in Exhibit S-, Schedule, that this would offset the cost of demolition an additional $,99,80, shown in Exhibit S-, Schedule. Q. Please explain Staff s calculation in Exhibit S-, Schedule. A. Staff received as part of the Company s response to an audit request a 9 page document entitled RETIREMENT ASSUMPTIONS LUDINGTON PUMPED STORAGE PLANT DECOMMISSIONING STUDY June, 998, Exhibit S-, Schedule. From this study and Staff s observation during its onsite evaluation, Staff estimates that the powerhouse and roof have approximately,0 tons of steel,,90 tons of copper, 0 tons of aluminum, and,00 tons 8

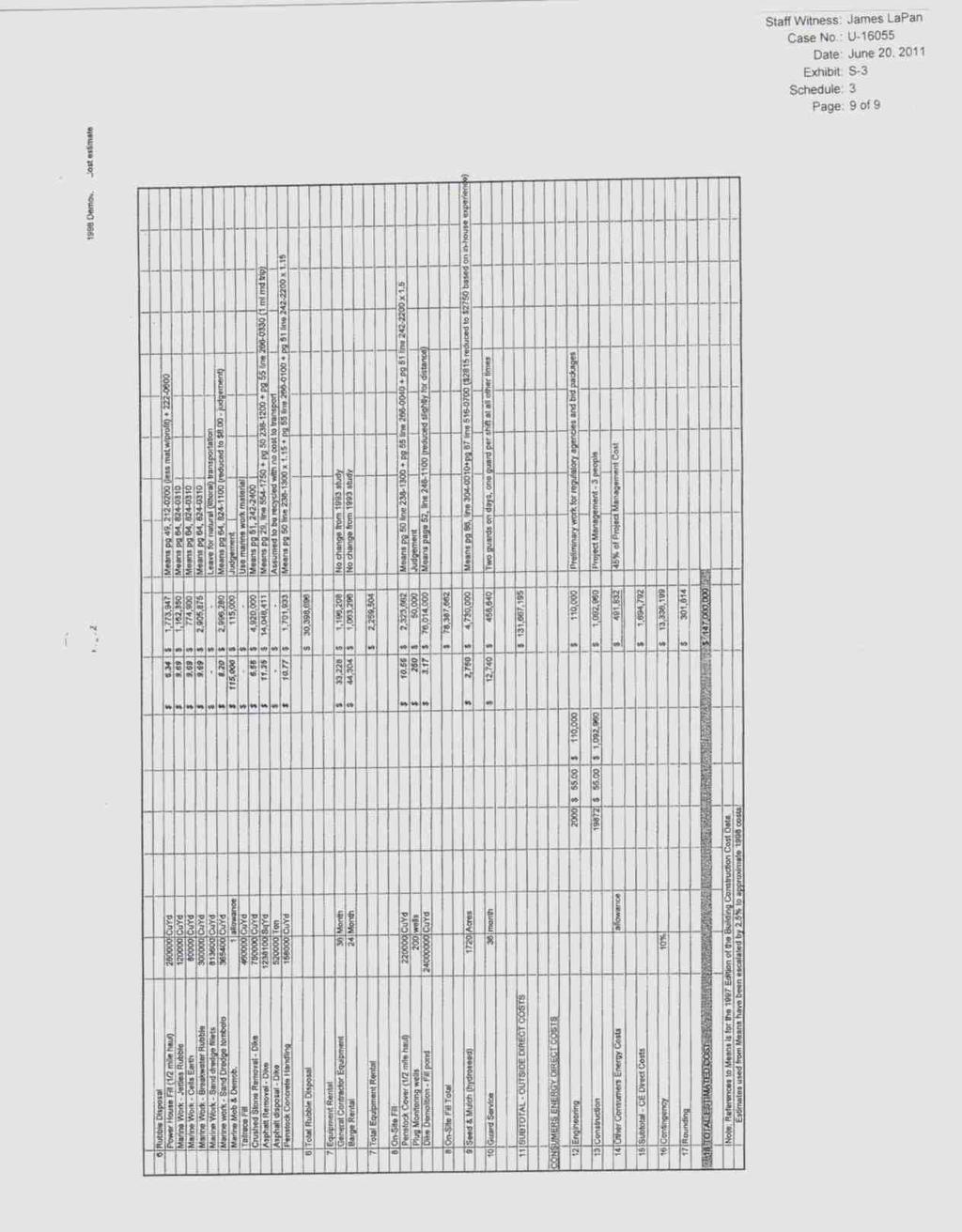

29 DIRECT TESTIMONY OF JAMES E. LA PAN PART II of stainless steel. When these weights of material are multiplied by their reasonable scrap value market price they provide a total value of $,7,00. Staff, however, has applied a salvage value of $,99,80 to the Company s opinion of cost for project item. The total value of $,7,00 was reduced to reflect the Company s account of $,00 in salvage estimated in its opinion of cost for item on page 8 of in Exhibit A-. Q. Please explain Staff s recommendation to remove all structures located in Lake Michigan. A. In the Company s Report, on page 7, Mr. Dow discusses the benefits and burdens to stakeholders and indicates that the Company s owners currently lease lands from the MDNR. These lands are the bottom lands in front of the plant lakefront. Mr. Dow goes on to explain that Some of the structures present on the leased area will remain and as a result, it is anticipated that the Owners will continue to be burdened with annual lease fees. Staff does not support only partial removal of the manufactured plant structures located in the bottom lands lease area and recommends full and complete removal of items necessary to terminate the Owner s lease for these bottom lands after decommissioning, and to restore full access to the lake, in order to comply with licensing requirements. Otherwise, Staff recommends that the Commission specifically note that the remaining obligations due to lease agreements and/or contracts related to the operation of the Ludington Pumped Storage Plant be the Case No. U-7 9

30 DIRECT TESTIMONY OF JAMES E. LA PAN PART II sole burden of the Owners and not of the ratepayers after the site has been decommissioned. Q. Please explain the Staff s adjustment reducing the Company s cost estimate for the seeding and covering the former reservoir bottom. A. Staff is recommending that the Company s cost estimate to cover and seed the leveled reservoir area, item on page 90 in Exhibit A-, be reduced by $,8,, as seen in Exhibit S-, Schedule, to reflect the fact that this cost was overstated by Mr. Dow in his calculations on page 90 of his Exhibit A-. Q. Please explain how Staff determined that this estimate was overstated. A. Section. of the Company s Report provides a site overview in the introductions. In that site overview, on page 7 of, the upper reservoir is clearly described by Mr. Dow as an 8 acre manmade reservoir located just east of the powerhouse. On page 90 of this same exhibit, Mr. Dow overstates the upper reservoir area by approximately acres by using 97 acres in his calculation. Therefore, Staff recommends that the cost to cover and seed the exposed reservoir bottom be reduced by $,8, to account for the additional acres. Q. Please explain why demolition of the Ludington Pumped Storage reservoir will not be required as part of demolition and should therefore be excluded from the estimated cost of decommissioning the site. A. The demolition of the Ludington Pumped Storage reservoir will not be required as part of decommissioning the site because there are other very specific useful purposes for it. In addition, Staff has not identified any licensing or permitting 0

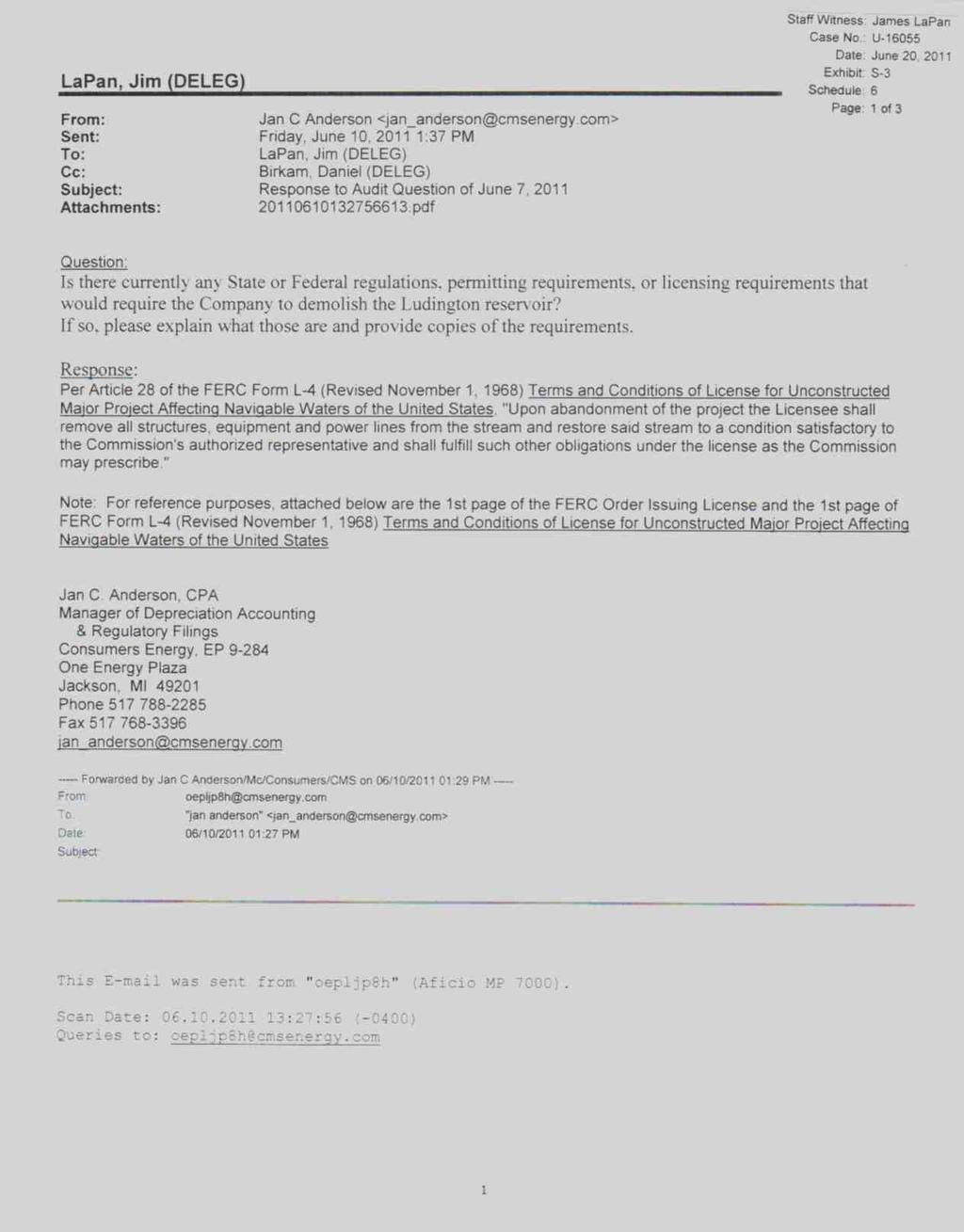

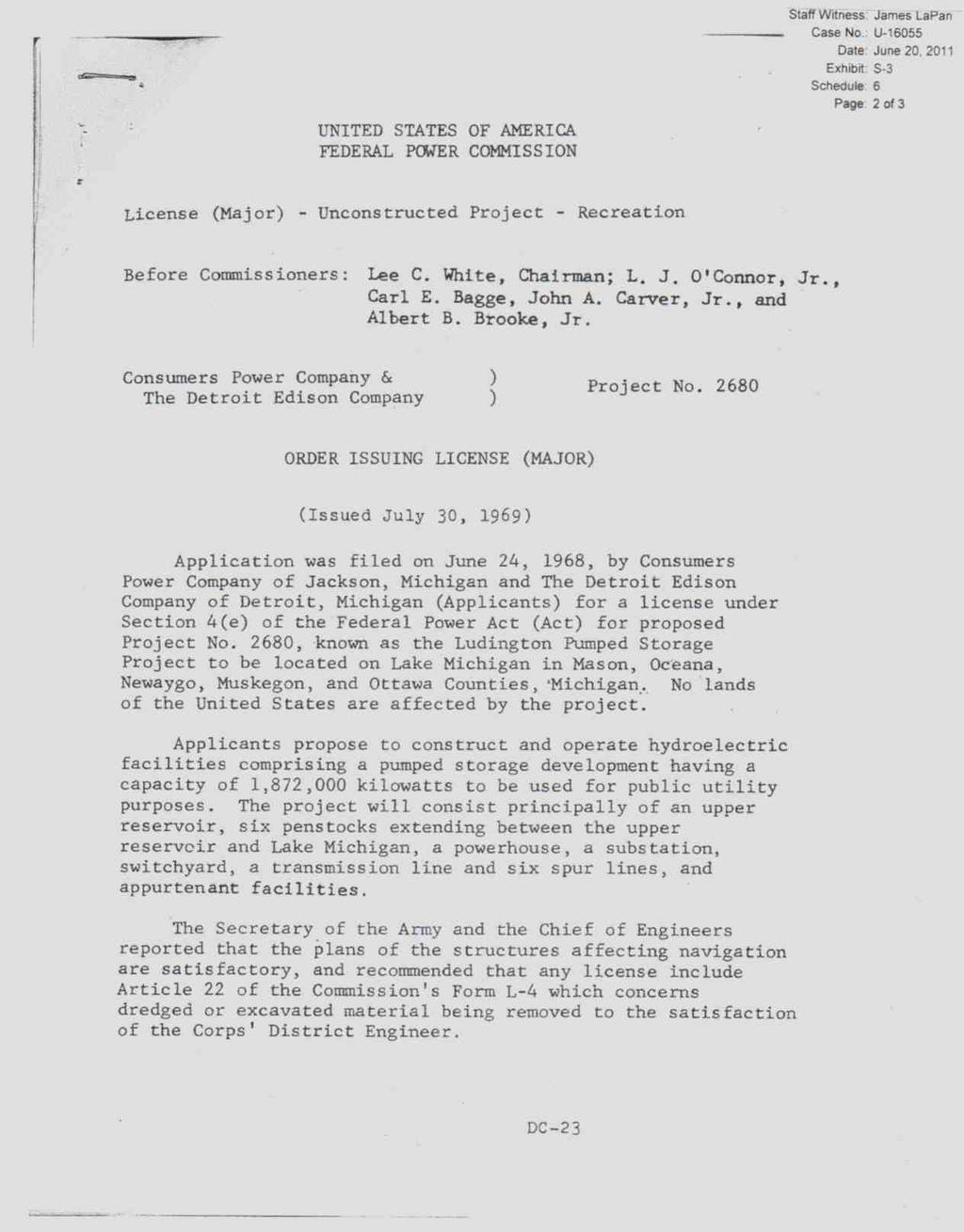

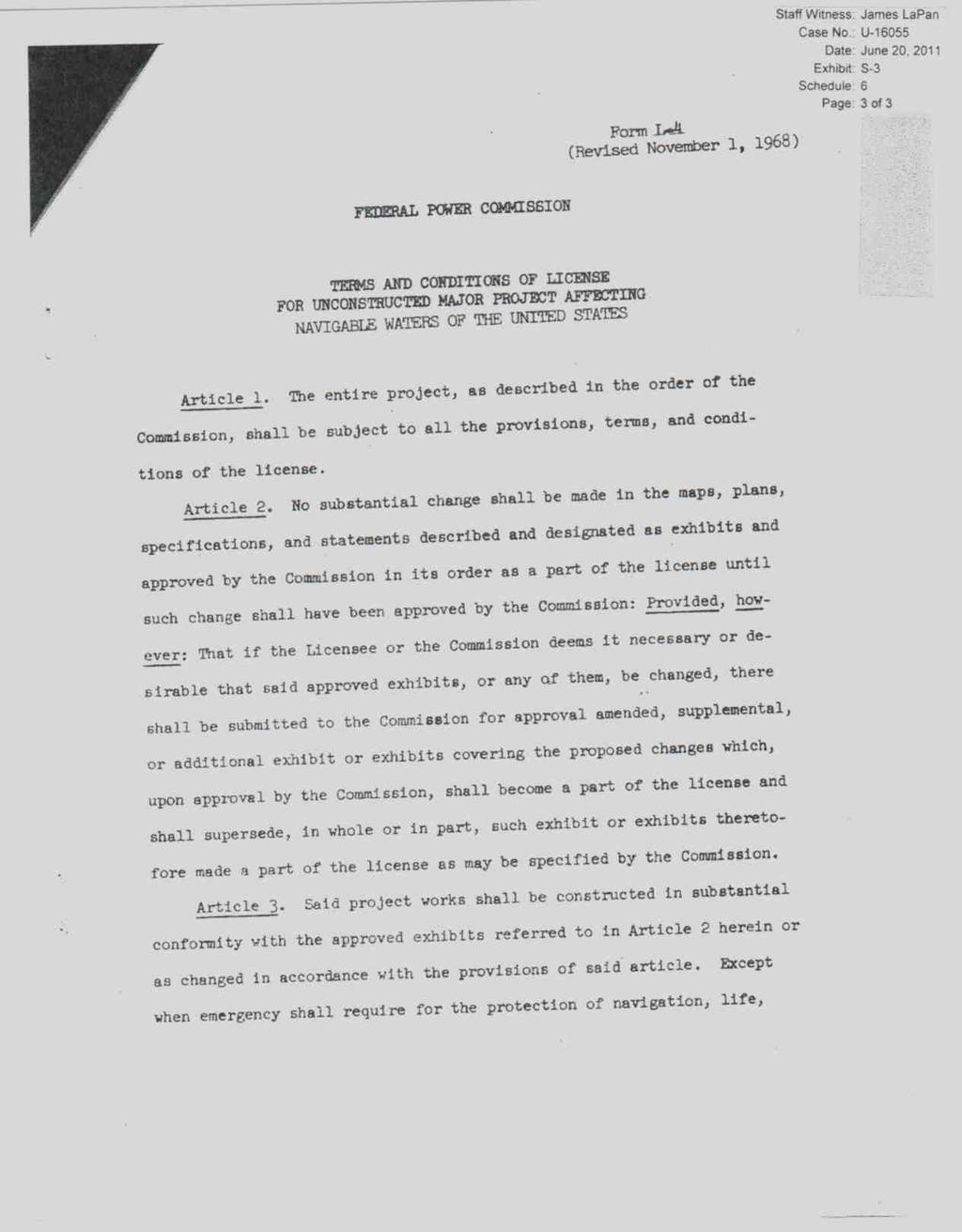

31 DIRECT TESTIMONY OF JAMES E. LA PAN PART II requirements that require demolition of the reservoir. Also leaving the reservoir in place reduces the threat of additional environmental disturbance. Q. Has the Company presented any supporting documents requiring the demolition of the reservoir? A. No. Consumers Energy witness David Kehoe states, on page, line through line 7, only that The Partial Project Removal end state is what the Company s 998 decommissioning study, which was filed in Case No. U-7, assumes. Mr. Kehoe goes on to explain that the other two end state options were done solely for the purpose of complying with a settlement agreement at the Federal Energy Regulatory Commission. Q. Has the Company presented any supporting documents suggesting the reservoir not be demolished? A. Yes. Please refer to page in Exhibit S-, Schedule 8, which is a copy of an , several questions, and the Company s response to those questions sent to the Ludington plant manager William A. Schoenlein by Kleinschmidt titled Questions to Client 8--0.doc. The Company explains, in its response to the second question, that the elevation of the reservoir after it is decommissioned will depend on what is ultimately done with the reservoir. The Company states For instance, if the reservoir is to be used as a landfill, the embankment may remain. Q. Anything else? A. Yes, during Staff s walkthrough of the Ludington site, I asked their current plant manager, William A. Schoenlein, how long they think this site will exist and his response was Forever. In addition, Exhibit S-, Schedule is the Company s

32 DIRECT TESTIMONY OF JAMES E. LA PAN PART II response to Staff s audit question specifically asking the Company if there were currently any State or Federal regulations, permitting requirements, or licensing requirements that would require the Company to demolish the Ludington reservoir. The Company s response and -page attachment only reference requirements for stream restoration, but did not include anything that required that the reservoir be demolished. Q. What alternative uses has Staff identified that will extend the useful life of the Ludington Pumped Storage reservoir? A. The reservoir s construction design meets preliminary design specifications found in Part, Solid Waste Management, of the Natural Resources and Environmental Protection Act, 99 PA, as amended, and the Michigan s Department of Environmental Quality s (DEQ) Administrative Rules. The unique structural design of this reservoir gives it the distinct ability of being used as a landfill and it is very plausible and even likely that it could be used as a landfill at some point. Q. Why does Staff feel that it is likely this reservoir will be used, as is, for an alternative purpose? A. Staff recognizes that at a minimum, the Company could use the reservoir as an ash pond to hold the ash produced by the burning of coal from its steam electric generation plants. Q. Is Staff recommending that the Ludington Pumped Storage reservoir be used as a landfill?

33 DIRECT TESTIMONY OF JAMES E. LA PAN PART II A. No. Staff is simply presenting the fact that use of this reservoir will continue long after the end of its current service life. While Staff does believe that the site will be repowered and continue to be relicensed by the FERC for the purpose of generating electricity it cannot rely on that speculation. Instead, Staff is relying on the fact that whether the reservoir is converted into a landfill or not, the reservoir will have other useful purposes and it does not require demolition. This is supported by Staff evidencing the possible future uses and showing that leveling the reservoir is not required for decommissioning. Q. What effect will this have on the Company s cost estimate for decommissioning the Ludington Pumped Storage Plant? A. Staff s recommendation will negate the $0,,0 that Exhibit A- includes as the cost of leveling the upper reservoir. Q. Would any other demolition costs be avoided as a result of accepting Staff s position? A. Yes. The decommissioning report (Exhibit A-), if considering reuse of the reservoir for the purpose of landfill or ash disposal, would no longer need (project item ) to remove office, maintenance, reservoir overlook, estimated on page7 to cost $7,0, (project item ) monitoring and relief wells, estimated on page 7 to cost $,99, or (project item ) to remove the reservoir intake and apron structures, estimated on page 89 to cost $,,. Q. Why is Staff also excluding the demolition costs for removal of the plant office, the site s monitoring and relief wells, and the reservoir intake and apron?

34 DIRECT TESTIMONY OF JAMES E. LA PAN PART II A. These demolition project items will no longer need to be performed once it s determined that leveling the reservoir is not required; specifically, if used as a landfill. For instance, one of the landfill construction requirements of Part is for ground water monitoring. The fact that the plant s extensive system of monitoring and relief wells are already in place supports even further the likelihood of this site being used as a landfill. Q. Is Staff recommending not to consider leveling the reservoir and also to include the adjustments of Staff witness Jing Shi? A. Yes. Staff is recommending leaving the upper reservoir intact for future use and incorporating the additional adjustments discussed in this testimony along with those Staff witness Jing Shi recommends. When eliminating the costs related to leveling the reservoir and incorporating Ms. Shi s adjustments, as well as these adjustments, the total cost of decommissioning the Ludington Pumped Storage Plant becomes $0,0,79. Q. Does Staff have any other information that would support the preservation of the plant s upper reservoir? A. Yes. Exhibit S-, Schedule 9 is support from the Michigan Department of Environmental Quality who calculated that, given the volume of landfill capacity available in Michigan and considering the current (FY-00) capacity use rate, that there is approximately 7 years of remaining disposal capacity left for use in this State. Q. Are there any more adjustments Staff is recommending?

35 DIRECT TESTIMONY OF JAMES E. LA PAN PART II A. Yes. If the Commission finds that demolition of the Ludington site s reservoir is a required part of decommissioning the site, Staff recommends an adjustment to the Company s cost estimate of leveling the reservoir for duplicative accounting of several project costs. Q. What material evidence are you basing this recommendation on? A. The evidence in the record does not provide any reasonable explanation or factual support to account for the significant cost increase over the 998 study, for the demolition costs estimated to demolish the site s reservoir. It is suggested by Consumers Energy witness Kehoe, based on his review of the Kleinschmidt Report, which was prepared for filing in this case, that The main difference between the 998 study and the Report is related to leveling the reservoir. Mr. Kehoe then identifies that Kleinschmidt s estimate identified similar quantities of materials required to level the reservoir that were included in the Company s 998 study. However, loading, hauling, spreading, and compacting these materials from the perimeter to the center of the reservoir were not included in the 998 study. Furthermore, on page of Mr. Kehoe s direct testimony, he goes on to state that Kleinschmidt estimates loading, hauling, spreading, and compacting these materials will cost an additional $79,000,000. Q. Why then is Staff recommending that the additional costs for leveling the reservoir added to the Company s 998 study in the Kleinschmidt Report are duplicative and should be adjusted accordingly? Direct Testimony of David B. Kehoe, page, line through line and page, line though line.

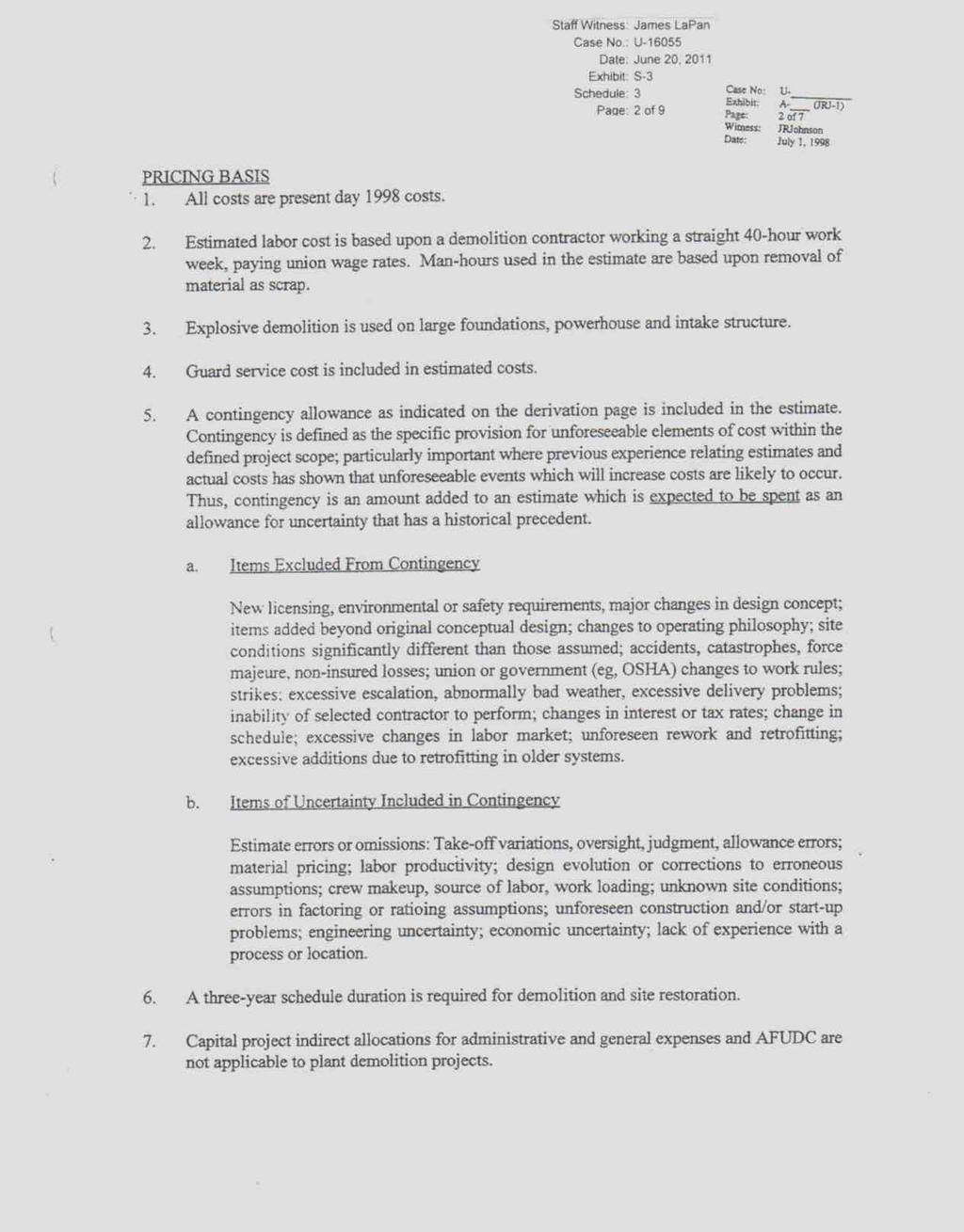

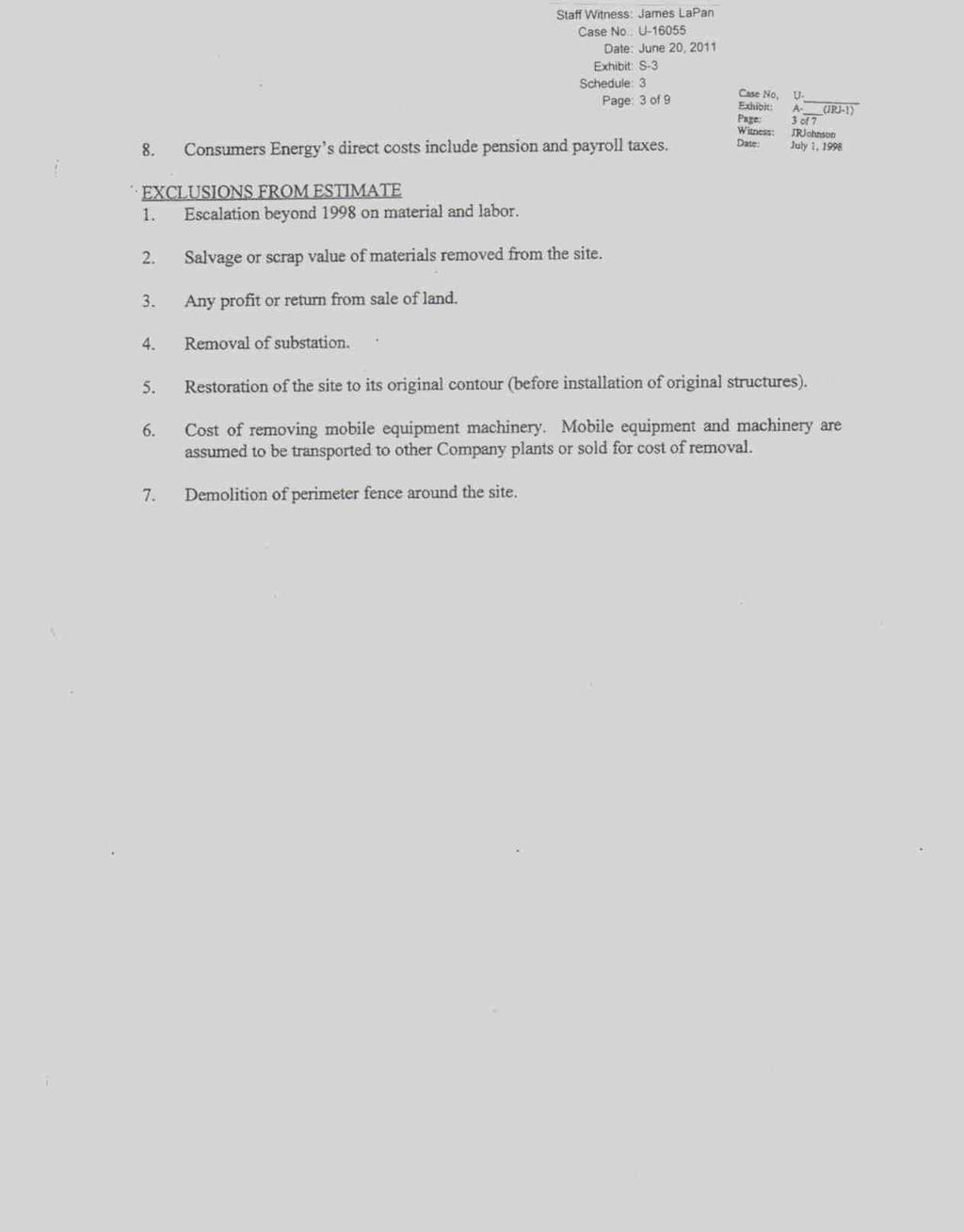

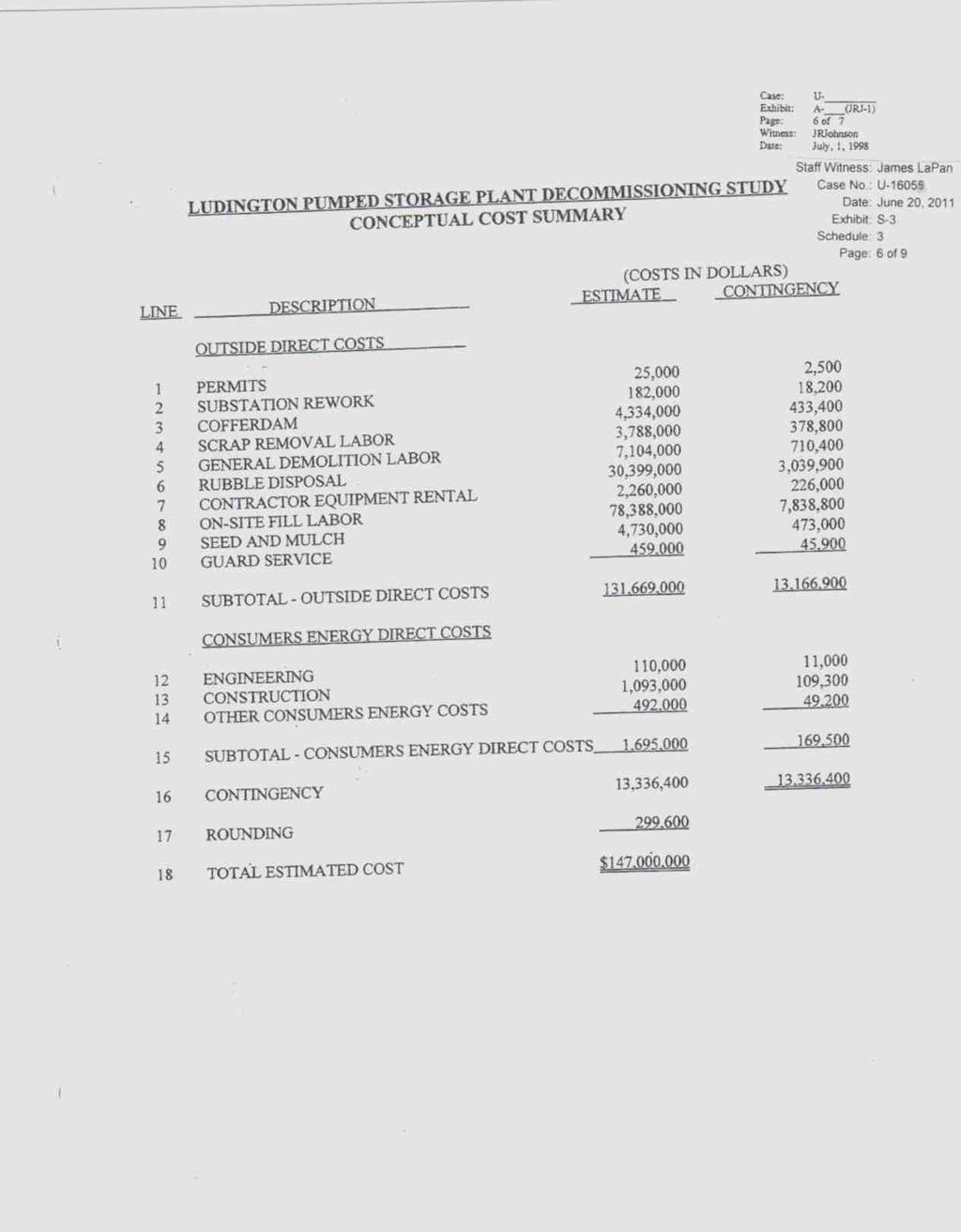

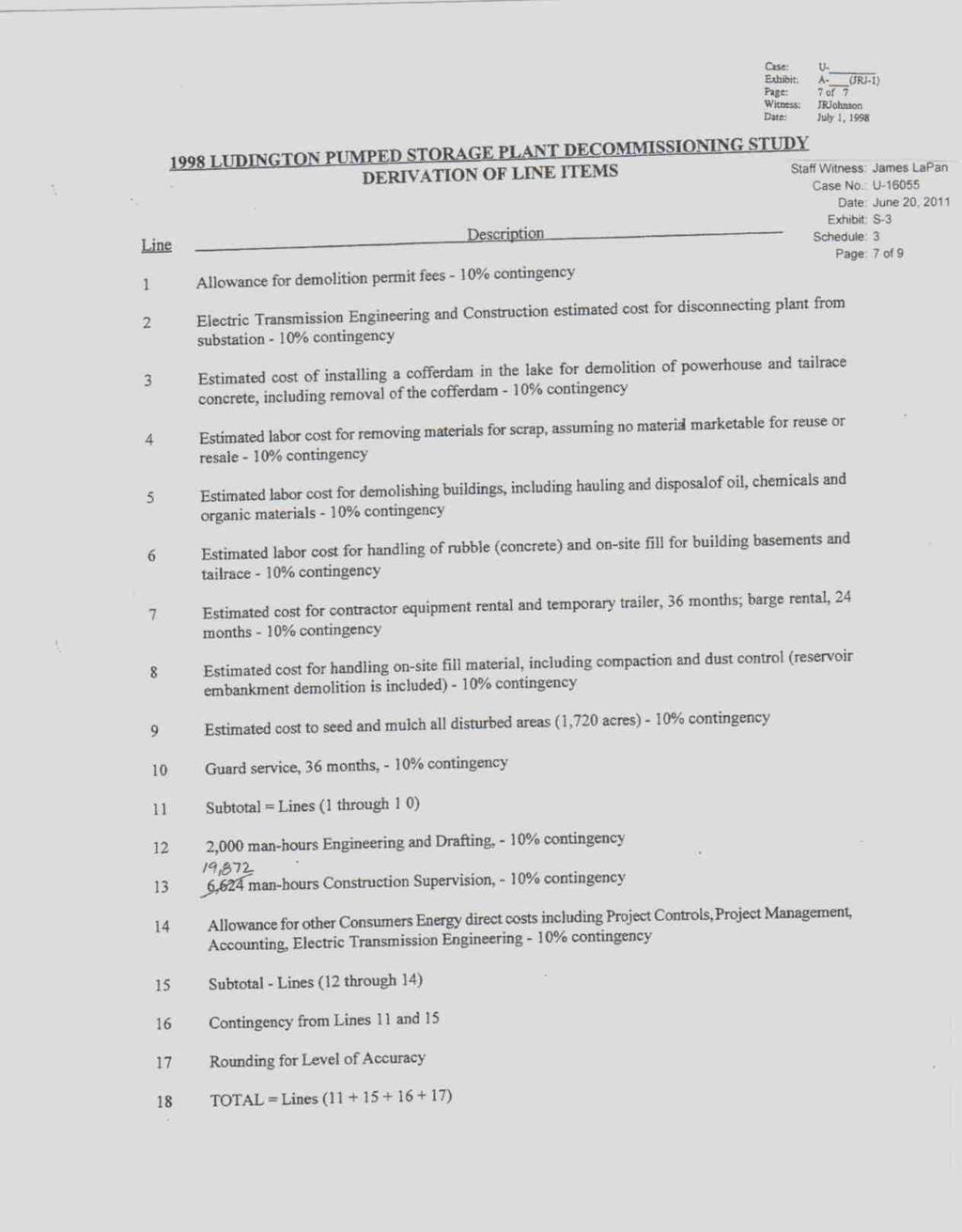

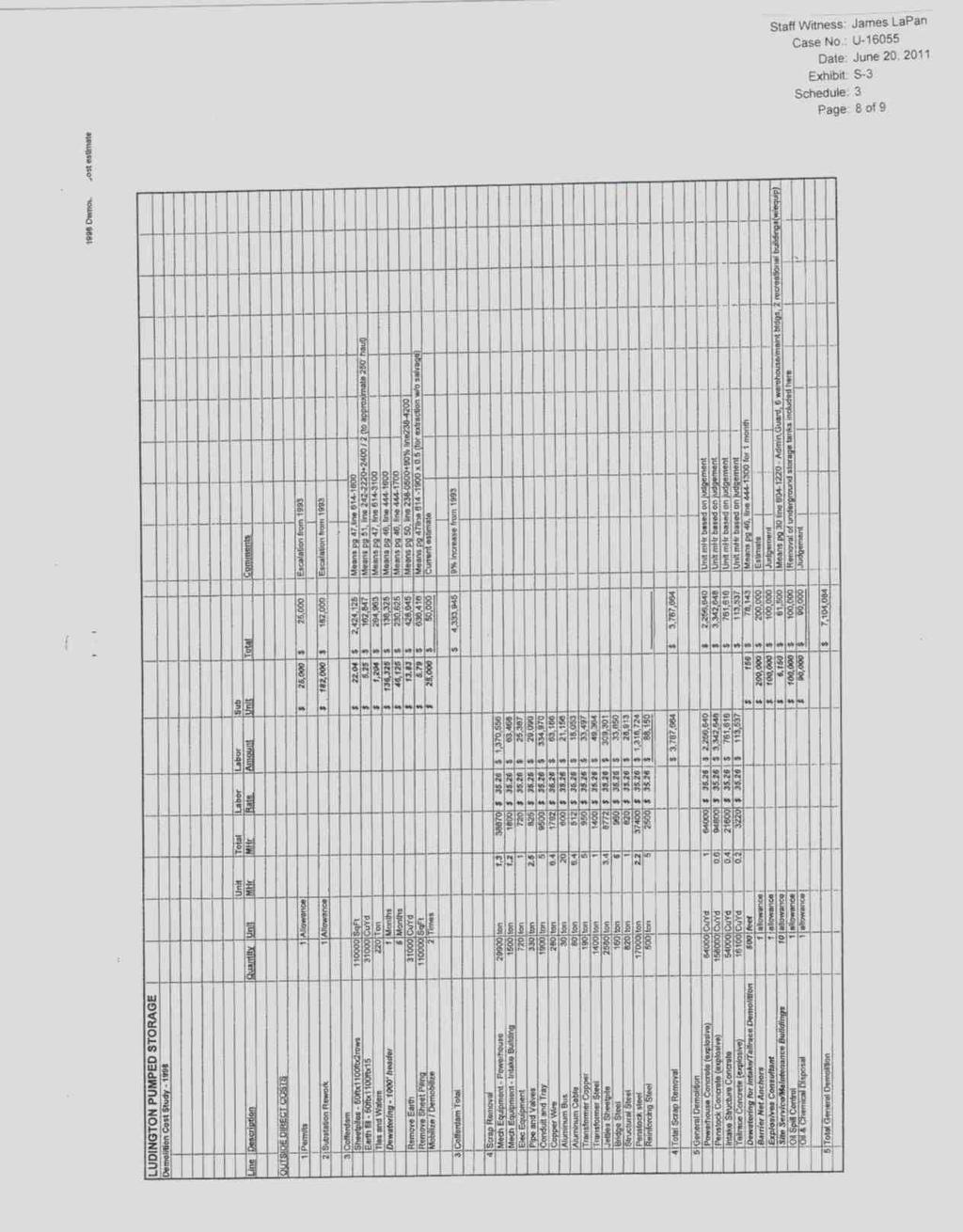

36 DIRECT TESTIMONY OF JAMES E. LA PAN PART II A. Please refer to Staff Exhibit S-, Schedule, which is the exhibit of Ludington plant manager Mr. JRJohnson supporting the 998 demolition study he performed. On page of 9, ESTIMATE SCOPE, number, Mr. Johnson explains that Material from the Dike will be used to fill reservoir. Also, please refer to page 7 of 9 where Mr. Johnson describes the costs he included in line item 8 as Estimated cost for handling on-site fill material, including compaction and dust control (reservoir embankment demolition is included). Therefore, it is evident that the Kleinschmidt Report incorrectly accounts for the cost of loading, hauling, spreading, and compacting the on-site fill materials twice. Additional evidence of this is where Mr. Kehoe explains that the time required for demolition and restoration is another factor that adds to the difference between the two studies. Kleinschmidt estimates 8 months for demolition and restoration, while the 998 Consumers Energy study assumed months, Kehoe, page, line through line 9. Considering the fact that the Kleinschmidt Report inaccurately accounts for leveling the reservoir twice, Staff recommends that a cost estimate and a time frame for demolition and site restoration match that of the Consumers Energy 998 study. Q. Please explain Staff s findings and recommendation for the cost estimates of construction and demolition of the cofferdam regarding any discrepancies

37 DIRECT TESTIMONY OF JAMES E. LA PAN PART II between the 998 demolition study and the Kleinschmidt Report prepared for filing in this case. A. Staff s evaluation of the estimated quantities of materials and labor required for the construction and demolition of the cofferdam which isolates the spillway apron, the north and south jetties, the break wall, and powerhouse in the Kleinschmidt Report versus the 998 demolition study show that both, the Report and study, considered; a) Sheet piles measuring 0ft x,00ft x rows, b) Earth fill with a volumetric measurement of 0ft x,00ft x ft, c) The same tonnage of tiles and wales, d) Dewatering,000ft header, e) Removing the earth fill, f) Removing the sheet pile, and g) Mobilize/demobilize two times. Furthermore, the 998 demolition study relied on the previous Ludington Pumped Storage Decommissioning Study prepared in 99; as noted by the Commission in its March, 000 order in Case No. U-7, both of which were previously reviewed by all parties to each case. Then, referring to Exhibit S-, Schedule, the plant manager notes in the 998 study, on page 8 of 9, for line item number, that the total cost estimated for cofferdam increased over those estimated in the 99 study 9% to $,,9. Staff then compared this to the Kleinschmidt Report, Exhibit A- page, where it estimates the 008 costs for cofferdam increase 8% over the 998 to $7,8,000. When Staff considered the Consumer Price Index filed by the Company in this case, it found that these costs should have only increased approximately.7% over those in the 998 study. Staff s analysis of the record in this case did not find support for these increases 7

38 DIRECT TESTIMONY OF JAMES E. LA PAN PART II and therefore recommends that the Commission order the Company to adjust its 008 opinion of cost to more accurately reflect actual inflation. Q. Does this conclude your testimony at this time? A. Yes it does. 8

39 S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter of the application of CONSUMERS ENERGY COMPANY ) and THE DETROIT EDISON COMPANY ) Case No. U-0 Requesting that the Commission Grant ) Accounting Approval of Depreciation ) Practices for the Ludington Pumped ) Storage Plant. ) ) EXHIBITS OF JAMES E. LA PAN MICHIGAN PUBLIC SERVICE COMMISSION June 0, 0

40 Staff Witness: James LaPan Case No.: U 0 Date: June 0, 0 Exhibit: S Schedule: Page: of Decommissioning Cost Estimate A B C D E F Company Company Company Staff Staff Total Cost to Item Activity 009 Extension Salvage Partial Removal Adjustment Adjustment Decommission Remove Main Powerfeeds to Substation $,7 $,7 ($,0) $8,09 Removel Towers from Powerhouse to Substation $7,09 $7,00 ($0,979) $,0 Remove Office, Maintenance, Reservoir Overlook $0,0 ($,00) $7,0 $0 ($7,0) $0 Monitoring and Relief Wells $,87 ($,8) $,99 $0 ($,99) $0 Removel Structures and Close Visitor Drives $0,8 $0,8 ($,8) $7,900 Remove Underground Fuel/Septic Tanks $,09 $,0 ($) ($,8) $7,78 7 Survey Site for Environmental Contamination $,8 $,9 ($8) ($9,800) $,87 8 Remove Barrier Net $,099,8 $,099,9 ($8,98) $,0, 9 Isolate Apron and Powerhouse from Lake Michigan $7,8,88 $7,8,8 ($0,80) $7,,88 0 Remove Apron $,77,8 $,77,8 ($8,) $,9, Remove North and South Jetties $,9,7 ($880,00) $,0,07 ($07,97) $,7,7 Remove Break Wall $,80,99 $,80,99 ($,89) $,,099 Survey Powerhouse for Hazardous Materials $,878 $,880 ($,7) $,7 Remove or Store Powerhouse Equipment $, $, ($,) ($,99,80) ($,8,78) Remove Powerhouse Roof and Fill $,,97 ($,00) $,08,9 ($0,0) $,,090 Close and Secure Penstock Isolation Gates $, $, ($,898) $9,77 7 Fill Upper Expansion Joint and Passage Way $7,79 $7,78 ($7,0) $0,8 8 Fill the Penstocks with Sand and Rip rap $,9, $,9,0 ($,0) $,78,08 9 Geotech. Study on Impact of Draining Reservoir $8,7 $8,7 ($,) $7,9 0 Level the Reservoir Dikes w/asphalt Liner $0,,0 $0,,0 $0 ($0,,0) $0 Remove Reservori Intake Structures/Apron $,9, ($,00) $,, $0 ($,,) $0 Cover and Seed the Leveled Former Reservoir Area $,0,7 $,0,7 ($,9,79) ($,8,) $,79,88 Remove Capital Improvements from $9,00 $9,00 $0 $9,00 Total $8,,8 ($,0,88) $8,,898 ($,8,9) ($8,,7) $0,0,79 Company Exhibit A Staff Exhibit S

41 Staff Witness: James LaPan Case No.: U 0 Date: June 0, 0 Exhibit: S Schedule: Page: of Scrap Salvage Value of Powerhouse Equipment Line Tons $/Ton Total Steel,0 $70 $,098,700 Copper,90 $,8 $,,0 Aluminum 0 $00 $,000 Stainless,00 $00 $,0,000 Total $,7,00 Report salvage from item ($,00) 7 $,99,80 Exhibit S, Schedule

42

43

44

45

46

47

48

49

50

51 Seeding Adjustment Staff Witness: James LaPan Case No.: U-0 Date: June 0, 0 Exhibit: S- Schedule: Page: of Line Quantity Unit 00 Price 00 Total 0-09 Esc. Factor 009 Total Cover,0 MSF $7.00 $,7,0. $,0,8 Seed,0 MSF $.00 $97,0. $,7, $,7,7 Acre is equal to,0 square feet Overstated Actual Adjusted Square Feet SF/Acre No. of Acres No. of Acres No. of Acres,0,000 SF, (),0,000 SF, () Adjusted No. of Acres SF/Acre Square Feet (),0 (,7,80) 7 (),0 (,7,80) Square Feet 8 (,7) MSF $7.00 ($,90,). ($,908,) 9 (,7) MSF $.00 ($,7). ($9,0) 0 ($,07,78) Sub-total Direct Labor and Material costs $,7,7 Staff Adjustment ($,07,78) $,9,89 General Contractors General Requirements (0%) $,,989 Contingency (0%) $,,989 Sub-total $,,979 $,79,87 7 Engineering (7%) $,0,. 8 Administration (7%) $,0,. 9 Insurance (.%) $, Sub-total $,7,70. $8,9,. $,0,7 Total Staff Adjustment $,8,.7

52

53

54

55

56

57

58

59

60

61

62

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION In the matter on the Commission s own ) motion, to consider changes in the rates ) of all the Michigan rate-regulated ) electric, steam,

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION In the matter on the Commission s own ) motion, to consider changes in the rates ) of all the Michigan rate-regulated ) electric, steam,

April 29, Ms. Mary Jo Kunkle Executive Secretary Michigan Public Service Commission 6545 Mercantile Way P.O. Box Lansing, MI 48909

A CMS Energy Company April, 0 Ms. Mary Jo Kunkle Executive Secretary Michigan Public Service Commission Mercantile Way P.O. Box 0 Lansing, MI 0 General Offices: LEGAL DEPARTMENT One Energy Plaza Jackson,

A CMS Energy Company April, 0 Ms. Mary Jo Kunkle Executive Secretary Michigan Public Service Commission Mercantile Way P.O. Box 0 Lansing, MI 0 General Offices: LEGAL DEPARTMENT One Energy Plaza Jackson,

2 BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION In the matter, on the Commission's Own Motion to consider changes in the rates of all of the Michigan rate-regulated Case U- electric, steam,

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION In the matter, on the Commission's Own Motion to consider changes in the rates of all of the Michigan rate-regulated Case U- electric, steam,

2 BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION. 8 Proceedings held in the above-entitled. 9 matter before Sharon L. Feldman, Administrative Law Judge

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION In the matter of the application of CONSUMERS ENERGY COMPANY for Case No. U- Accounting and Ratemaking Approval of Depreciation Rates for

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION In the matter of the application of CONSUMERS ENERGY COMPANY for Case No. U- Accounting and Ratemaking Approval of Depreciation Rates for

S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * *

S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter on the Commission s own ) motion, to consider changes in the rates ) of all the Michigan rate-regulated

S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter on the Commission s own ) motion, to consider changes in the rates ) of all the Michigan rate-regulated

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION. In the matter of the application of Case No. U UPPER PENINSULA POWER COMPANY

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION In the matter of the application of Case No. U-18467 UPPER PENINSULA POWER COMPANY (e-file paperless) for approval of depreciation rates

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION In the matter of the application of Case No. U-18467 UPPER PENINSULA POWER COMPANY (e-file paperless) for approval of depreciation rates

BEFORE THE ARKANSAS PUBLIC SERVICE COMMISSION

BEFORE THE ARKANSAS PUBLIC SERVICE COMMISSION IN THE MATTER OF THE APPLICATION OF ) FOR APPROVAL ) OF CHANGES IN RATES FOR RETAIL ) ELECTRIC SERVICE ) DIRECT TESTIMONY OF RONALD G. GARNER, CDP SENIOR CAPITAL

BEFORE THE ARKANSAS PUBLIC SERVICE COMMISSION IN THE MATTER OF THE APPLICATION OF ) FOR APPROVAL ) OF CHANGES IN RATES FOR RETAIL ) ELECTRIC SERVICE ) DIRECT TESTIMONY OF RONALD G. GARNER, CDP SENIOR CAPITAL

2 BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION. 8 Proceedings held in the above-entitled. 9 matter before Suzanne D. Sonneborn, Administrative

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION In the matter, on the Commission's Own Motion, establishing the method and Case No. U- avoided cost calculation for Upper Peninsula Power

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION In the matter, on the Commission's Own Motion, establishing the method and Case No. U- avoided cost calculation for Upper Peninsula Power

S T A T E O F M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * *

S T A T E O F M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter of the Commission s own ) motion, to consider changes in the rates ) of all the Michigan rate-regulated

S T A T E O F M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter of the Commission s own ) motion, to consider changes in the rates ) of all the Michigan rate-regulated

June 8, Enclosed find the Attorney General s Direct Testimony and Exhibits and related Proof of Service. Sincerely,

STATE OF MICHIGAN DEPARTMENT OF ATTORNEY GENERAL P.O. BOX 30755 LANSING, MICHIGAN 48909 BILL SCHUETTE ATTORNEY GENERAL June 8, 2018 Ms. Kavita Kale Michigan Public Service Commission 7109 West Saginaw

STATE OF MICHIGAN DEPARTMENT OF ATTORNEY GENERAL P.O. BOX 30755 LANSING, MICHIGAN 48909 BILL SCHUETTE ATTORNEY GENERAL June 8, 2018 Ms. Kavita Kale Michigan Public Service Commission 7109 West Saginaw

Miller, Canfield, Paddock and Stone, P.L.C. One Michigan Avenue, Suite 900 Lansing, Michigan TEL (517) FAX (517)

FAX (517)") Founded in 1852 by Sidney Davy Miller SHERRI A. WELLMAN TEL (517) 483-4954 FAX (517) 374-6304 E-MAIL wellmans@millercanfield.com Miller, Canfield, Paddock and Stone, P.L.C. One Michigan Avenue, Suite 900

Founded in 1852 by Sidney Davy Miller SHERRI A. WELLMAN TEL (517) 483-4954 FAX (517) 374-6304 E-MAIL wellmans@millercanfield.com Miller, Canfield, Paddock and Stone, P.L.C. One Michigan Avenue, Suite 900

S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * *

S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter of the application of ) CONSUMERS ENERGY COMPANY ) for authority to increase its rates for the ) Case No.

S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter of the application of ) CONSUMERS ENERGY COMPANY ) for authority to increase its rates for the ) Case No.

BEFORE THE ARKANSAS PUBLIC SERVICE COMMISSION

BEFORE THE ARKANSAS PUBLIC SERVICE COMMISSION IN THE MATTER OF THE APPLICATION OF ) OKLAHOMA GAS & ELECTRIC COMPANY FOR ) DOCKET NO. 0-0-U APPROVAL OF A GENERAL CHANGE IN RATES ) AND TARIFFS ) DIRECT TESTIMONY

BEFORE THE ARKANSAS PUBLIC SERVICE COMMISSION IN THE MATTER OF THE APPLICATION OF ) OKLAHOMA GAS & ELECTRIC COMPANY FOR ) DOCKET NO. 0-0-U APPROVAL OF A GENERAL CHANGE IN RATES ) AND TARIFFS ) DIRECT TESTIMONY

Exhibit 99.1 DTE Gas Company

Exhibit 99.1 DTE Gas Company Unaudited Consolidated Financial Statements as of and for the Three and Nine Months Ended September 30, 2013 Quarter Ended September 30, 2013 Table of Contents Page Consolidated

Exhibit 99.1 DTE Gas Company Unaudited Consolidated Financial Statements as of and for the Three and Nine Months Ended September 30, 2013 Quarter Ended September 30, 2013 Table of Contents Page Consolidated

S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * *

S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter of the application of ) DTE ELECTRIC COMPANY ) for reconciliation of its Power Supply Cost ) Case No. U-009

S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter of the application of ) DTE ELECTRIC COMPANY ) for reconciliation of its Power Supply Cost ) Case No. U-009

DIRECT TESTIMONY OF THE SITE INVESTIGATION AND REMEDIATION PANEL

BEFORE THE NEW YORK STATE PUBLIC SERVICE COMMISSION ----------------------------------------------------------------------------x Proceeding on Motion of the Commission as to the Rates, Charges, Rules

BEFORE THE NEW YORK STATE PUBLIC SERVICE COMMISSION ----------------------------------------------------------------------------x Proceeding on Motion of the Commission as to the Rates, Charges, Rules

S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * *

S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter on the Commission s own ) motion, to consider changes in the rates ) of all the Michigan rate-regulated

S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter on the Commission s own ) motion, to consider changes in the rates ) of all the Michigan rate-regulated

GILLARD, BAUER, MAZRUM, FLORIP, SMIGELSKI & GULDEN ATTORNEYS AT LAW 109 E. CHISHOLM STREET ALPENA, MICHIGAN March 29, 2018

ROGER C. BAUER JAMES L. MAZRUM JAMES D. FLORIP WILLIAM S. SMIGELSKI TIMOTHY M. GULDEN JOEL E. BAUER DANIEL J. FLORIP GILLARD, BAUER, MAZRUM, FLORIP, SMIGELSKI, & GULDEN ATTORNEYS AT LAW 109 E. CHISHOLM

ROGER C. BAUER JAMES L. MAZRUM JAMES D. FLORIP WILLIAM S. SMIGELSKI TIMOTHY M. GULDEN JOEL E. BAUER DANIEL J. FLORIP GILLARD, BAUER, MAZRUM, FLORIP, SMIGELSKI, & GULDEN ATTORNEYS AT LAW 109 E. CHISHOLM

EXHIBIT D STATEMENT OF COSTS AND FINANCING

EXHIBIT D STATEMENT OF COSTS AND FINANCING HOLT HYDROELECTRIC PROJECT FERC NO. 2203 DRAFT LICENSE APPLICATION Alabama Power Company Birmingham, Alabama Prepared by: July 2012 EXHIBIT D STATEMENT OF COSTS

EXHIBIT D STATEMENT OF COSTS AND FINANCING HOLT HYDROELECTRIC PROJECT FERC NO. 2203 DRAFT LICENSE APPLICATION Alabama Power Company Birmingham, Alabama Prepared by: July 2012 EXHIBIT D STATEMENT OF COSTS

BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PENNSYLVANIA PUBLIC UTILITY COMMISSION PECO ENERGY COMPANY ELECTRIC DIVISION

PECO ENERGY COMPANY STATEMENT NO. BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PENNSYLVANIA PUBLIC UTILITY COMMISSION v. PECO ENERGY COMPANY ELECTRIC DIVISION DOCKET NO. R-01-0001 DIRECT TESTIMONY

PECO ENERGY COMPANY STATEMENT NO. BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PENNSYLVANIA PUBLIC UTILITY COMMISSION v. PECO ENERGY COMPANY ELECTRIC DIVISION DOCKET NO. R-01-0001 DIRECT TESTIMONY

BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PENNSYLVANIA PUBLIC UTILITY COMMISSION PECO ENERGY COMPANY ELECTRIC DIVISION

PECO ENERGY COMPANY STATEMENT NO. BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PENNSYLVANIA PUBLIC UTILITY COMMISSION v. PECO ENERGY COMPANY ELECTRIC DIVISION DOCKET NO. R-01-1 DIRECT TESTIMONY WITNESS:

PECO ENERGY COMPANY STATEMENT NO. BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PENNSYLVANIA PUBLIC UTILITY COMMISSION v. PECO ENERGY COMPANY ELECTRIC DIVISION DOCKET NO. R-01-1 DIRECT TESTIMONY WITNESS:

MICHIGAN CONSOLIDATED GAS COMPANY. Unaudited Financial Statements as of and for the Quarter and Six Months ended June 30, 2008

MICHIGAN CONSOLIDATED GAS COMPANY Unaudited Financial Statements as of and for the Quarter and Six Months ended June 30, 2008 MICHIGAN CONSOLIDATED GAS COMPANY TABLE OF CONTENTS Page Consolidated Statements

MICHIGAN CONSOLIDATED GAS COMPANY Unaudited Financial Statements as of and for the Quarter and Six Months ended June 30, 2008 MICHIGAN CONSOLIDATED GAS COMPANY TABLE OF CONTENTS Page Consolidated Statements

MICHIGAN CONSOLIDATED GAS COMPANY. Unaudited Financial Statements as of and for the Quarter and Nine Months ended September 30, 2007

Unaudited Financial Statements as of and for the Quarter and Nine Months ended September 30, 2007 TABLE OF CONTENTS Page Consolidated Statements of Operations 1 Consolidated Statements of Financial Position

Unaudited Financial Statements as of and for the Quarter and Nine Months ended September 30, 2007 TABLE OF CONTENTS Page Consolidated Statements of Operations 1 Consolidated Statements of Financial Position

Exhibit 99.1 MICHIGAN CONSOLIDATED GAS COMPANY. Unaudited Consolidated Financial Statements as of and for the Three Months Ended March 31, 2011

Exhibit 99.1 Unaudited Consolidated Financial Statements as of and for the Three Months Ended March 31, 2011 TABLE OF CONTENTS Page Consolidated Statements of Operations (Unaudited) 3 Consolidated Statements

Exhibit 99.1 Unaudited Consolidated Financial Statements as of and for the Three Months Ended March 31, 2011 TABLE OF CONTENTS Page Consolidated Statements of Operations (Unaudited) 3 Consolidated Statements

S T A T E O F M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * QUALIFICATIONS AND DIRECT TESTIMONY OF NICHOLAS M.

S T A T E O F M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter of the application of ) CONSUMERS ENERGY COMPANY for a ) financing order approving the securitization )

S T A T E O F M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter of the application of ) CONSUMERS ENERGY COMPANY for a ) financing order approving the securitization )

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION. (e-file paperless) related matters. /

related matters. /") STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION In the matter of the application of DTE ELECTRIC COMPANY for approval Case No. U-18150 of depreciation accrual rates and other (e-file paperless)

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION In the matter of the application of DTE ELECTRIC COMPANY for approval Case No. U-18150 of depreciation accrual rates and other (e-file paperless)

MICHIGAN CONSOLIDATED GAS COMPANY Consolidated Financial Statements as of December 31, 2008 and 2007 and for each of the three years in the period

MICHIGAN CONSOLIDATED GAS COMPANY Consolidated Financial Statements as of December 31, 2008 and 2007 and for each of the three years in the period ended December 31, 2008 and Independent Auditors Report

MICHIGAN CONSOLIDATED GAS COMPANY Consolidated Financial Statements as of December 31, 2008 and 2007 and for each of the three years in the period ended December 31, 2008 and Independent Auditors Report

March 28, Ms. Kavita Kale Executive Secretary Michigan Public Service Commission 7109 W. Saginaw Highway Lansing, Michigan 48917

DTE Gas Company One Energy Plaza, WCB Detroit, MI - David S. Maquera () - david.maquera@dteenergy.com March, 0 Ms. Kavita Kale Executive Secretary Michigan Public Service Commission 0 W. Saginaw Highway

DTE Gas Company One Energy Plaza, WCB Detroit, MI - David S. Maquera () - david.maquera@dteenergy.com March, 0 Ms. Kavita Kale Executive Secretary Michigan Public Service Commission 0 W. Saginaw Highway

Miller, Canfield, Paddock and Stone, P.L.C. One Michigan Avenue, Suite 900 Lansing, Michigan TEL (517) FAX (517)

FAX (517)") Founded in 1852 by Sidney Davy Miller SHERRI A. WELLMAN TEL (517) 483-4954 FAX (517) 374-6304 E-MAIL wellmans@millercanfield.com Miller, Canfield, Paddock and Stone, P.L.C. One Michigan Avenue, Suite 900

Founded in 1852 by Sidney Davy Miller SHERRI A. WELLMAN TEL (517) 483-4954 FAX (517) 374-6304 E-MAIL wellmans@millercanfield.com Miller, Canfield, Paddock and Stone, P.L.C. One Michigan Avenue, Suite 900

GILLARD, BAUER, MAZRUM, FLORIP, SMIGELSKI & GULDEN ATTORNEYS AT LAW 109 E. CHISHOLM STREET ALPENA, MICHIGAN May 12, 2015

ROGER C. BAUER JAMES L. MAZRUM JAMES D. FLORIP WILLIAM S. SMIGELSKI TIMOTHY M. GULDEN JOEL E. BAUER DANIEL J. FLORIP GILLARD, BAUER, MAZRUM, FLORIP, SMIGELSKI, & GULDEN ATTORNEYS AT LAW 109 E. CHISHOLM

ROGER C. BAUER JAMES L. MAZRUM JAMES D. FLORIP WILLIAM S. SMIGELSKI TIMOTHY M. GULDEN JOEL E. BAUER DANIEL J. FLORIP GILLARD, BAUER, MAZRUM, FLORIP, SMIGELSKI, & GULDEN ATTORNEYS AT LAW 109 E. CHISHOLM

Asset Retirement Obligations

Basis for Conclusions Asset Retirement Obligations August 2018 Section PS 3280 CPA Canada Public Sector Accounting Handbook Prepared by the staff of the Public Sector Accounting Board Foreword CPA Canada

Basis for Conclusions Asset Retirement Obligations August 2018 Section PS 3280 CPA Canada Public Sector Accounting Handbook Prepared by the staff of the Public Sector Accounting Board Foreword CPA Canada

Establishing an Essential Records List Criteria and Reporting Essential Records to the University s Records Management and Archives Department

Establishing an Essential Records List Criteria and Reporting Essential Records to the University s Records Management and Archives Department December, 2015 ESTABLISHING AN ESSENTIAL RECORDS LIST What

Establishing an Essential Records List Criteria and Reporting Essential Records to the University s Records Management and Archives Department December, 2015 ESTABLISHING AN ESSENTIAL RECORDS LIST What

Exhibit 99.1 MICHIGAN CONSOLIDATED GAS COMPANY

Exhibit 99.1 MICHIGAN CONSOLIDATED GAS COMPANY Consolidated Financial Statements as of December 31, 2010 and 2009 and for each of the three years in the period ended December 31, 2010 and Report of Independent

Exhibit 99.1 MICHIGAN CONSOLIDATED GAS COMPANY Consolidated Financial Statements as of December 31, 2010 and 2009 and for each of the three years in the period ended December 31, 2010 and Report of Independent

Georgia EPD Update prepared for 2018 Georgia Brownfields Association Seminar. Rick Dunn April 19, 2018

Georgia EPD Update prepared for 2018 Georgia Brownfields Association Seminar Rick Dunn April 19, 2018 LEGISLATIVE WRAP-UP Approved legislation includes: HB 205 Fracking Bill EPD will develop rules packing

Georgia EPD Update prepared for 2018 Georgia Brownfields Association Seminar Rick Dunn April 19, 2018 LEGISLATIVE WRAP-UP Approved legislation includes: HB 205 Fracking Bill EPD will develop rules packing

SOCALGAS DIRECT TESTIMONY OF GARRY G. YEE RATE BASE. November 2014

Company: Southern California Gas Company (U 0 G) Proceeding: 01 General Rate Case Application: A.1-- Exhibit: SCG- SOCALGAS DIRECT TESTIMONY OF GARRY G. YEE RATE BASE November 01 BEFORE THE PUBLIC UTILITIES

Company: Southern California Gas Company (U 0 G) Proceeding: 01 General Rate Case Application: A.1-- Exhibit: SCG- SOCALGAS DIRECT TESTIMONY OF GARRY G. YEE RATE BASE November 01 BEFORE THE PUBLIC UTILITIES

STATE OF MICHIGAN DEPARTMENT OF ATTORNEY GENERAL BILL SCHUETTE ATTORNEY GENERAL. August 8, 2016

STATE OF MICHIGAN DEPARTMENT OF ATTORNEY GENERAL P.O. BOX 30755 LANSING, MICHIGAN 48909 BILL SCHUETTE ATTORNEY GENERAL August 8, 2016 Kavita Kale Executive Secretary Michigan Public Service Commission

STATE OF MICHIGAN DEPARTMENT OF ATTORNEY GENERAL P.O. BOX 30755 LANSING, MICHIGAN 48909 BILL SCHUETTE ATTORNEY GENERAL August 8, 2016 Kavita Kale Executive Secretary Michigan Public Service Commission

Colonial Gas Company d/b/a National Grid Financial Statements For the years ended March 31, 2013 and March 31, 2012

Colonial Gas Company d/b/a National Grid Financial Statements For the years ended March 31, 2013 and March 31, 2012 COLONIAL GAS COMPANY TABLE OF CONTENTS Page No. Independent Auditor's Report 2 Balance

Colonial Gas Company d/b/a National Grid Financial Statements For the years ended March 31, 2013 and March 31, 2012 COLONIAL GAS COMPANY TABLE OF CONTENTS Page No. Independent Auditor's Report 2 Balance

Michigan Public Service Commission The Detroit Edison Company Projected Net Operating Income "Total Electric" and "Jurisdictional Electric"

Projected Net Operating Income Schedule: C1 "Total Electric" and "Jurisdictional Electric" Witness: T. M. Uzenski Projected 12 Month Period Ending March 31, 2012 Page: 1 of 1 ($000) (a) (b) (c) Historical

Projected Net Operating Income Schedule: C1 "Total Electric" and "Jurisdictional Electric" Witness: T. M. Uzenski Projected 12 Month Period Ending March 31, 2012 Page: 1 of 1 ($000) (a) (b) (c) Historical

BIDS WILL BE OPENED AT 1:00 p.m., local prevailing time, WEDNESDAY, MARCH 13, 2019.

INSTRUCTIONS TO BIDDERS: This Proposal shall be legibly prepared with ink. UNIT PRICES, and LUMP SUM BIDS when called for on the itemized bid sheet, shall be entered with ink, in the Unit Price column.

INSTRUCTIONS TO BIDDERS: This Proposal shall be legibly prepared with ink. UNIT PRICES, and LUMP SUM BIDS when called for on the itemized bid sheet, shall be entered with ink, in the Unit Price column.

STATE OF INDIANA INDIANA UTILITY REGULATORY COMMISSION

STATE OF INDIANA INDIANA UTILITY REGULATORY COMMISSION VERIFIED PETITION OF SOUTHERN INDIANA GAS AND ELECTRIC COMPANY d/b/a VECTREN ENERGY DELIVERY OF IN DIANA, INC., FOR: ( AUTHORITY TO CONSTRUCT, OWN

STATE OF INDIANA INDIANA UTILITY REGULATORY COMMISSION VERIFIED PETITION OF SOUTHERN INDIANA GAS AND ELECTRIC COMPANY d/b/a VECTREN ENERGY DELIVERY OF IN DIANA, INC., FOR: ( AUTHORITY TO CONSTRUCT, OWN

S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * *

S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter of the application of ) DTE Electric Company for ) Reconciliation of its Power Supply ) Case No. U-7680-R

S T A T E OF M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter of the application of ) DTE Electric Company for ) Reconciliation of its Power Supply ) Case No. U-7680-R

MICHIGAN CONSOLIDATED GAS COMPANY. Unaudited Consolidated Financial Statements as of and for the Quarter and the Nine Months Ended September 30, 2011

Unaudited Consolidated Financial Statements as of and for the Quarter and the Nine Months Ended September 30, 2011 TABLE OF CONTENTS Page Consolidated Statements of Operations (Unaudited) 3 Consolidated

Unaudited Consolidated Financial Statements as of and for the Quarter and the Nine Months Ended September 30, 2011 TABLE OF CONTENTS Page Consolidated Statements of Operations (Unaudited) 3 Consolidated

June 20, Ms. Kavita Kale Executive Secretary Michigan Public Service Commission 7109 West Saginaw Hwy Lansing, MI 48917

DTE Gas Company One Energy Plaza, 688 WCB Detroit, MI 48226-1279 David S. Maquera (313) 235-3724 maquerad@dteenergy.com June 20, 2018 Ms. Kavita Kale Executive Secretary Michigan Public Service Commission

DTE Gas Company One Energy Plaza, 688 WCB Detroit, MI 48226-1279 David S. Maquera (313) 235-3724 maquerad@dteenergy.com June 20, 2018 Ms. Kavita Kale Executive Secretary Michigan Public Service Commission

RRl of

Commission/Docket Type of Proceeding Testimony FERC ER08-313E SPS Wholesale Transmission Rebuttal Testimony Formula ER10-192 PSCO Wholesale Production Direct Testimony Formula ER11-2853 PSCO Wholesale

Commission/Docket Type of Proceeding Testimony FERC ER08-313E SPS Wholesale Transmission Rebuttal Testimony Formula ER10-192 PSCO Wholesale Production Direct Testimony Formula ER11-2853 PSCO Wholesale

S T A T E O F M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * *

S T A T E O F M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter of the Application of ) CONSUMERS ENERGY COMPANY for ) Approval of Amendments to ) Case No. U-00 Gas Transportation

S T A T E O F M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter of the Application of ) CONSUMERS ENERGY COMPANY for ) Approval of Amendments to ) Case No. U-00 Gas Transportation

Q. PLEASE STATE YOUR NAME AND BUSINESS ADDRESS. A. My name is Suzanne E. Sieferman, and my business address is 1000 East Main

TESTIMONY OF, MANAGER RATES AND REGULATORY STRATEGY ON BEHALF OF DUKE ENERGY INDIANA, LLC CAUSE NO. BEFORE THE INDIANA UTILITY REGULATORY COMMISSION 0 I. INTRODUCTION Q. PLEASE STATE YOUR NAME AND BUSINESS

TESTIMONY OF, MANAGER RATES AND REGULATORY STRATEGY ON BEHALF OF DUKE ENERGY INDIANA, LLC CAUSE NO. BEFORE THE INDIANA UTILITY REGULATORY COMMISSION 0 I. INTRODUCTION Q. PLEASE STATE YOUR NAME AND BUSINESS

Miller, Canfield, Paddock and Stone, P.L.C. One Michigan Avenue, Suite 900 Lansing, Michigan TEL (517) FAX (517)

FAX (517)") Founded in 1852 by Sidney Davy Miller PAUL M. COLLINS TEL (517) 483-4908 FAX (517) 374-6304 E-MAIL collinsp@millercanfield.com Miller, Canfield, Paddock and Stone, P.L.C. One Michigan Avenue, Suite 900

Founded in 1852 by Sidney Davy Miller PAUL M. COLLINS TEL (517) 483-4908 FAX (517) 374-6304 E-MAIL collinsp@millercanfield.com Miller, Canfield, Paddock and Stone, P.L.C. One Michigan Avenue, Suite 900

BEFORE THE ARKANSAS PUBLIC SERVICE COMMISSION

BEFORE THE ARKANSAS PUBLIC SERVICE COMMISSION IN THE MATTER OF THE APPLICATION ) OF LIBERTY UTILITIES (PINE BLUFF WATER), ) INC. FOR GENERAL CHANGE OR ) MODIFICATION IN RATES, CHARGES, AND ) TARIFFS )

BEFORE THE ARKANSAS PUBLIC SERVICE COMMISSION IN THE MATTER OF THE APPLICATION ) OF LIBERTY UTILITIES (PINE BLUFF WATER), ) INC. FOR GENERAL CHANGE OR ) MODIFICATION IN RATES, CHARGES, AND ) TARIFFS )

Niagara Mohawk Power Corporation d/b/a National Grid

Niagara Mohawk Power Corporation d/b/a National Grid PROCEEDING ON MOTION OF THE COMMISSION AS TO THE RATES, CHARGES, RULES AND REGULATIONS OF NIAGARA MOHAWK POWER CORPORATION FOR ELECTRIC AND GAS SERVICE