Solution to Problem 11 Classify items for different statements. Solution to Problem 12 Classify items for different statements.

|

|

|

- Ginger Caroline Mosley

- 5 years ago

- Views:

Transcription

1 Solution to Problem 11 Classify items for different statements. The following items are found on financial statements. Identify each as BS (balance sheet), IS.{income statement), CF (statement of cash flows) or SHE (statement of changes in stockholders equity). CF Borrowed $ from bank (during year) BS CF Cash (at end of year) BS Note payable (at end of year) SHE CF New stock issued (during year) SHE Retained earnings (at beginning of year) SHE BS Retained earnings (at end of year) NI SHE Net income (for entire year) BS Accounts receivable (at end of year) BS Accounts payable (at end of year) BS Land (at end of year) CF Land purchased during year IS Service expense ( during year) IS Wages expense (during year) BS Wages payable (at end of year) CF Payments received from customers (during year) Solution to Problem 12 Classify items for different statements. The following items are found on financial statements. Identify each as BS (balance sheet), IS.{income statement), CF (statement of cash flows) or SHE (statement of changes in stockholders equity). SHE Retained earnings (at beginning of year) BS SHE Retained earnings IS SHE Net income BS Accounts receivable BS Accounts payable CF Borrowed from bank BS CF Cash BS Note payable CF Cash (at beginning of year) SHE CF Common stock issued BS Land CF Land purchased IS Service expense IS Wages expense BS Wages payable CF Payments received from customers 205

2 Balance sheet Cash 25,000 T Accounts receivable 18,000 T Supplies 10,000 T Prepaid insurance 8,000 T Current assets 61,000 Land 80,000 T Building 135,000 T PPE total 215,000 Total assets 276,000 addition Accounts payable 26,000 T Wages payable 7,000 T Unearned revenue 13,000 T Current liabilities 46,000 Note payable 24,000 T Total liabilities 70,000 Solution to Problem 13 Preparing a set of financial statements Common stock 40,000 T Retained earnings 166,000 subtraction Total SHE 206,000 subtraction, total L+SHE less total liabilities Total liabilities & SHE 276,000 carried over from total assets Income statement Interest Revenue 2,000 T Service revenue 310,000 T Total revenue 312,000 Wages expense 180,000 T Rent expense 70,000 T Insurance expense 8,000 T Supplies expense 13,000 T Interest expense 2,000 T Total expense 273,000 Net income 39,000 subtraction 206

3 Statement of cash flows Operating activities 50,000 T Investing activities (88,000) T Financing activities (2,000) T Net change in cash (40,000) + Beginning cash 65,000 subtraction Ending cash 25,000 carried down from balance sheet Statement of changes in stockholders equity Beginning common stock 30,000 subtraction Issue common stock 10,000 T Ending common stock 40,000 carried down Beginning retained earnings Net income Dividends paid Ending retained earnings 139,000 subtraction 39,000 carried down (12,000) T 166,000 carried down 207

4 Solution to Problem 14 Preparing a set of financial statements Balance sheet Cash 41,000 T Accounts receivable 12,000 T Supplies 6,000 T Prepaid insurance 4,000 T Current assets 63,000 Land 75,000 T Building 210,000 T PPE 285,000 Total assets 348,000 Accounts payable 32,000 T Wages payable 6,000 T Unearned revenue 5,000 T Current liabilities Note payable (long term) 72,000 T Total liabilities 115,000 Common stock 50,000 carried up from changes in SHE Retained earnings 181,000 subtraction Total SHE 231,000 subtract total liab from total L+SHE Total liabilities & SHE 346,000 carried over from total assets Income statement Interest Revenue 5,000 T Service revenue 285,000 T Total revenue 290,000 Wages expense 170,000 T Rent expense 60,000 T Insurance expense 11,000 T Supplies expense 7,000 T Interest expense 14,000 T Total expense 262,000 Net income 28,000 Statement of cash flows Operating activities 30,000 T Investing activities (98,000) T Financing activities (2,000) T Net change in cash (70,000) + Beginning cash 111,000 subtraction Ending cash 41,000 TCarried down from balance sheet 208

5 Statement of changes in stockholders equity Beginning common stock 35,000 T Issue common stock 15,000 T Ending common stock 50,000 Beginning retained earnings Net income Dividends paid Ending retained earnings 174,000 subtraction 28,000 carried down from income statement (21,000) T 181,000 carried down from balance sheet 209

6 Solution to Problem 15 A Look at Target s Financial Statements fiscal 2013 issued in

7 211

8 212

9 213

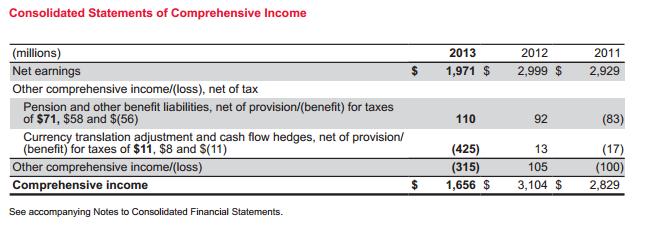

10 Target Corporation is a general retail company. Then answer the following questions. 1. The Target fiscal year starts and ends on which dates? [Hint: look to Note #1] It always starts on a Sunday and ends on a Saturday. Target s sale week always starts on Sunday, and prices are good through Saturday. 2. How many years are presented for the: Balance sheet? 2 Income statement? 3 Cash flows statement? 3 Statement of changes in stockholders equity? 3 3. Using totals for each category (total assets, total liabilities, total SHE), what is Target s balance sheet equation for current fiscal year? $ billion = $ billion + $ billion or $44,553,000,000 = $28,332,000,000 + $16,231,000,000 Please don t say $44,553 million, as its meaning isn t obvious to almost anyone in the world. 4. What is the debt percentage (total liabilities divided by total assets) for the current fiscal year? 63.59% = Conversely, the SHE percentage is 36.41% These are important numbers, as they identify the capital structure of a company. The capital structure of a company is the relative breakdown for the source of financing for a company s assets. How much financing comes from borrowed money (lenders) and how much comes from owners? 5. How many items are listed in the stockholders equity section of the balance sheet? Four, but in reality, three (as Common Stock par value and Common Stock additional paid in capital are usually added together. For the most recent year: Common stock billion Additional paid-in-capital billion Retained earnings billion Accumulated other comprehensive loss (0.891) billion 214

11 6. Using totals for each category (total revenues, total expenses), what is Target s income statement equation for the current fiscal year? Revenues! expenses + gains! losses = net income $ billion! $ billion + $0.391 billion = $1.971 billion 7. What is the value for net sales for the current fiscal year? $ billion 8. What is the value for gross margin for the current fiscal year? The gross margin percentage? $ billion! $ billion = $ billion 29.53% = What is the retained earnings equation for the current fiscal year? Do the values in this equation equal the numbers reported on the balance sheet and income statement? Beginning retained earnings $ Net income 1.971! Dividends (1.051)! Stock repurchase (1.476) Ending retained earnings In which two locations can you find out if Target paid dividends in the most recent fiscal year? How much, if anything, did it pay out in dividends for the current fiscal year? Dividends declared of $1.051 billion can be found on SHE statement. Dividends actually paid of $1.006 billion can be found on Cash Flows statement. 11. In which year did Target spend the most to acquire property, plant and equipment? How much did it spend that year? Why is the value for capital expenditures in brackets? $3.453 billion in 2013, $3.277 billion in 2012, and $4.368 billion in Capital expenditures amount is in brackets because it is a negative number signifying an outflow of cash from Target. 215

12 12. Who is the auditor (CPA firm) for Target. What words in the auditor s opinion are used to report that the financial statements are OK? 216

13 Tiffany & Co. is a jewelry company. Solution to Problem 16 A Look at Tiffany s Financial Statements fiscal 2013 issued in The Tiffany fiscal year starts and ends on which dates? February 1 through January What is the value of total assets for the most recent fiscal year? $4,752,351,000, or $4.752 billion 3. Using totals for each category (total assets, total liabilities, total SHE), what is Tiffany s balance sheet equation for the most recent fiscal year? $4.752 billion = $2.018 billion + $2.734 billion 4. What is the debt percentage (total liabilities divided by total assets) for the most recent fiscal year? = 42.47% 5. What is the value for net sales for the most recent fiscal year? $4,031,130,000 or $4.031 billion 6. What is the value for gross margin for the most recent fiscal year? The gross margin percentage? Net sales $ bill 100% Cost of sales bill 42% Gross profit bill 58% 7. What is operating income for the most recent fiscal year? What is operating income as a percentage of net sales? $304 million, 7.5% 217

14 8. What is the retained earnings equation for the most recent fiscal year? Do the values in this equation equal the numbers reported on the balance sheet and income statement? BRE + NI! Div = ERE $1.671 billion billion! billion = $1.682 billion YES, everything checks out. 9. In which two locations can you find out if Tiffany paid dividends in the most recent fiscal year? How much, if anything, did it pay out in dividends for the most recent fiscal year? Statement of SHE and Cash flows statement $ In which year did Tiffany spend the most on acquisitions? How much did it spend that year? Year ended 1/31/2014: $0.221 billion Year ended 1/31/2013: $0.220 billion Year ended 1/31/2012: $0.239 billion 11. Why is the value for capital expenditures in brackets? It is an outflow of cash, cash is being spent. 12. Who is the auditor (CPA firm) for Tiffany. What words in the auditor s opinion are used to report that the financial statements are OK? PWC. In our opinion, the accompanying

15 219

16 220

17 221

18 222

19 223

ACCT 356 First Exam Spring, 2011 Albrecht. Name. Exam Content:

ACCT 356 First Exam Spring, 2011 Albrecht Name Exam Content: Q1 Payroll accounting 9 min 12 pts Q2 Loan computations 12 min 20 pts Q3 Installment loan 18 min 25 pts Q4 Non-interest bearing loan 12 min

ACCT 356 First Exam Spring, 2011 Albrecht Name Exam Content: Q1 Payroll accounting 9 min 12 pts Q2 Loan computations 12 min 20 pts Q3 Installment loan 18 min 25 pts Q4 Non-interest bearing loan 12 min

Intermediate Acct 2 SBAD 332 First Exam. Exam Content:

Intermediate Acct 2 SBAD 332 First Exam Name Spring, 2013 Albrecht Exam Content: Q1 Payroll accounting 10 min 10 pts Q2 Installment loan accounting 20 min 26 pts Q3 Interest bearing loan with principal

Intermediate Acct 2 SBAD 332 First Exam Name Spring, 2013 Albrecht Exam Content: Q1 Payroll accounting 10 min 10 pts Q2 Installment loan accounting 20 min 26 pts Q3 Interest bearing loan with principal

Chapter 4 Mechanics of Financial Information

BUS210 Chapter 4 Mechanics of Financial Information What do you remember? Economic Events--> Transactions Reducing events to numbers Connecting the Accounting Equation with Transactions: Journal Entries,

BUS210 Chapter 4 Mechanics of Financial Information What do you remember? Economic Events--> Transactions Reducing events to numbers Connecting the Accounting Equation with Transactions: Journal Entries,

BUS :30 Fall TA Office Hours T&R 5-6pm W520

BUS210 9.3.14 8:30 Fall 2014 TA Office Hours T&R 5-6pm W520 After putting your name on your papers, Turn in TPI (only if attended first class), Student Consent form, and VARK Learning styles Financial

BUS210 9.3.14 8:30 Fall 2014 TA Office Hours T&R 5-6pm W520 After putting your name on your papers, Turn in TPI (only if attended first class), Student Consent form, and VARK Learning styles Financial

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

ACCOUNTING. bankerzhaus.wordpress.com 1

ACCOUNTING Income Statement (IS) -- a financial statement that measures a company's financial performance over a specific accounting period Revenue / COGS and Operating Expenses / Operating Income (EBIT)

ACCOUNTING Income Statement (IS) -- a financial statement that measures a company's financial performance over a specific accounting period Revenue / COGS and Operating Expenses / Operating Income (EBIT)

ACCT 356. Spring, 2011 Albrecht. Exam Content:

ACCT 356 First Exam Spring, 2011 Albrecht Name Exam Content: Q1 Payroll accounting 9 min 12 pts Q2 Loan computations 12 min 20 pts Q3 Installment loan 18 min 25 pts Q4 Non-interest bearing loan 12 min

ACCT 356 First Exam Spring, 2011 Albrecht Name Exam Content: Q1 Payroll accounting 9 min 12 pts Q2 Loan computations 12 min 20 pts Q3 Installment loan 18 min 25 pts Q4 Non-interest bearing loan 12 min

4. If cash is collected in advance for services, the revenue is recognized when the services are rendered.

ANSWERS TO QUESTIONS - CHAPTER 2 1. Accrual accounting attempts to record the effects of accounting events in the period when such events occur, regardless of when cash is received or paid. The goal is

ANSWERS TO QUESTIONS - CHAPTER 2 1. Accrual accounting attempts to record the effects of accounting events in the period when such events occur, regardless of when cash is received or paid. The goal is

The statement of cash flows reports cash flows, cash receipts, and cash payments, to show where cash came from and how it was spent.

Accounting Fundamentals Lesson 10 10.0 Cash Flow Statement The balance sheet reports financial position, and balance sheets from two periods show whether cash increased or decreased. But that doesn t tell

Accounting Fundamentals Lesson 10 10.0 Cash Flow Statement The balance sheet reports financial position, and balance sheets from two periods show whether cash increased or decreased. But that doesn t tell

4/10/2012. Statement of Cash Flows. Learning Objectives (LO) LO 1 - Purpose of Cash Flow Statement. Learning Objectives (LO)

LO 1 - Purpose of Cash Flow Statement. Learning Objectives (LO)") Statement of Flows CHAPTER Learning Objectives (LO) After studying this chapter, you should be able to 1. Identify the purposes of the statement of cash flows 2. Classify activities affecting cash as operating,

Statement of Flows CHAPTER Learning Objectives (LO) After studying this chapter, you should be able to 1. Identify the purposes of the statement of cash flows 2. Classify activities affecting cash as operating,

Full file at Chapter 02 - Solutions to Exercises - Series A

SOLUTIONS TO EXERCISES - SERIES A - CHAPTER 2 EXERCISE 2-1A Horizontal Statements Model Stock. Equity Type of Com. Ret. Net Cash Even t Event Asset s = Liab. + Stock + Earn. Rev. Exp. = Inc. Flows a. AS

SOLUTIONS TO EXERCISES - SERIES A - CHAPTER 2 EXERCISE 2-1A Horizontal Statements Model Stock. Equity Type of Com. Ret. Net Cash Even t Event Asset s = Liab. + Stock + Earn. Rev. Exp. = Inc. Flows a. AS

BUS210. Chapter 4 Sessions 4, 5, 6, & 7 Mechanics of Financial Information

BUS210 Chapter 4 Sessions 4, 5, 6, & 7 Mechanics of Financial Information Connecting the Accounting Equation with Transactions: Journal Entries, T Accounts E4-9 Prepare journal entries for each cash transaction

BUS210 Chapter 4 Sessions 4, 5, 6, & 7 Mechanics of Financial Information Connecting the Accounting Equation with Transactions: Journal Entries, T Accounts E4-9 Prepare journal entries for each cash transaction

Draw an Accountant. Who/What Information needs for business/financial decisions

Draw an Accountant. Who/What Information needs for business/financial decisions BUS210 Session 1 Handouts: To Do List Syllabus Teaching Perspectives Inventory (TPI) Class Handout Attendance: Sign roster!!!

Draw an Accountant. Who/What Information needs for business/financial decisions BUS210 Session 1 Handouts: To Do List Syllabus Teaching Perspectives Inventory (TPI) Class Handout Attendance: Sign roster!!!

Analysis of Financial Statements and Statement of Cash Flows BUS512M. November 21, 2014 Session 2 8:00-11:30 Susan Crosson

Analysis of Financial Statements and Statement of Cash Flows BUS512M November 21, 2014 Session 2 8:00-11:30 Susan Crosson Homework See Handout Today s Learning Outcomes Analyzing Financial Statementscommon

Analysis of Financial Statements and Statement of Cash Flows BUS512M November 21, 2014 Session 2 8:00-11:30 Susan Crosson Homework See Handout Today s Learning Outcomes Analyzing Financial Statementscommon

Analysis of Financial Statements and Statement of Cash Flows BUS512M. December 16, 2016 Session 2 8:00-noon Susan Crosson

Analysis of Financial Statements and Statement of Cash Flows BUS512M December 16, 2016 Session 2 8:00-noon Susan Crosson P4-20 Reverse T-account analysis You are a credit analyst for a bank. Badger Business

Analysis of Financial Statements and Statement of Cash Flows BUS512M December 16, 2016 Session 2 8:00-noon Susan Crosson P4-20 Reverse T-account analysis You are a credit analyst for a bank. Badger Business

4. If cash is collected in advance for services, the revenue is recognized when the services are rendered.

ANSWERS TO QUESTIONS - CHAPTER 2 1. Accrual accounting attempts to record the effects of accounting events in the period when such events occur, regardless of when cash is received or paid. The goal is

ANSWERS TO QUESTIONS - CHAPTER 2 1. Accrual accounting attempts to record the effects of accounting events in the period when such events occur, regardless of when cash is received or paid. The goal is

Intro to Financial Reporting

Intro to Financial Reporting Day 1: Learning the Language of Business Jane Kennedy September 20, 2011 Jump Start Goals? Introduce Accounting, the language of business, and its strange new jargon Learn

Intro to Financial Reporting Day 1: Learning the Language of Business Jane Kennedy September 20, 2011 Jump Start Goals? Introduce Accounting, the language of business, and its strange new jargon Learn

PIN# Spring, 2010 (no name, please) Albrecht. Exam Content:

Albrecht. Exam Content:") ACCT 356 First Exam PIN# Spring, 2010 (no name, please) Albrecht Exam Content: Q1 Classification of intangibles 5 min 6 pts Q2 Contingencies 7 min 8 pts Q3 Payroll accounting 9 min 12 pts Q4 Loan computations

ACCT 356 First Exam PIN# Spring, 2010 (no name, please) Albrecht Exam Content: Q1 Classification of intangibles 5 min 6 pts Q2 Contingencies 7 min 8 pts Q3 Payroll accounting 9 min 12 pts Q4 Loan computations

Solution Manual for Corporate Finance 10th Edition by Ross

Solution Manual for Corporate Finance 10th Edition by Ross Link download full: https://testbankservice.com/download/solution-manualfor-corporate-finance-10th-edition-by-ross Test Bank for Corporate Finance

Solution Manual for Corporate Finance 10th Edition by Ross Link download full: https://testbankservice.com/download/solution-manualfor-corporate-finance-10th-edition-by-ross Test Bank for Corporate Finance

Financial Statement Analysis for the Boardroom. An Attorney s Guide September 13, 2017

Financial Statement Analysis for the Boardroom An Attorney s Guide September 13, 2017 Contact information For more information, please contact one of the following members of the engagement team: Marc

Financial Statement Analysis for the Boardroom An Attorney s Guide September 13, 2017 Contact information For more information, please contact one of the following members of the engagement team: Marc

CHAPTER 2 Financial Statements: A Window on an Entity EXERCISES E2-1. Assets = Liabilities + Owners Equity Situation 1 $425,000 $236,000 $189,000

CHAPTER 2 Financial Statements: A Window on an Entity EXERCISES E2-1. Assets = Liabilities + Owners Equity Situation 1 $425,000 $236,000 $189,000 Situation 2 1,350,000 730,000 620,000 Situation 3 200,000

CHAPTER 2 Financial Statements: A Window on an Entity EXERCISES E2-1. Assets = Liabilities + Owners Equity Situation 1 $425,000 $236,000 $189,000 Situation 2 1,350,000 730,000 620,000 Situation 3 200,000

Using Financial Statements in the Credit Review Process. Wendi Rosenblatt, Hearst Television

Using Financial Statements in the Credit Review Process Wendi Rosenblatt, Hearst Television Agenda What is Available Financial Statement Overview DineEquity, Inc. Annual Report/Form 10K Review Availability

Using Financial Statements in the Credit Review Process Wendi Rosenblatt, Hearst Television Agenda What is Available Financial Statement Overview DineEquity, Inc. Annual Report/Form 10K Review Availability

4-1 COMPLETING THE ACCOUNTING CYCLE

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

Financial Statements, Taxes and Cash Flow

Financial Statements, Taxes and Cash Flow Faculty of Business Administration Lakehead University Spring 2003 May 5, 2003 2.1 The Balance Sheet 2.2 The Income Statement 2.3 Cash Flow 2.4 Taxes 2.5 Capital

Financial Statements, Taxes and Cash Flow Faculty of Business Administration Lakehead University Spring 2003 May 5, 2003 2.1 The Balance Sheet 2.2 The Income Statement 2.3 Cash Flow 2.4 Taxes 2.5 Capital

Solution to Problem 31 Adjusting entries. Solution to Problem 32 Closing entries.

Solution to Problem 31 Adjusting entries. 1. Utilities expense 27,000 Accounts payable 27,000 2. Rent revenue 4,000 Unearned revenue 4,000 3. Supplies 2,000 Supplies expense 2,000 4. Interest receivable

Solution to Problem 31 Adjusting entries. 1. Utilities expense 27,000 Accounts payable 27,000 2. Rent revenue 4,000 Unearned revenue 4,000 3. Supplies 2,000 Supplies expense 2,000 4. Interest receivable

NON-CURRENT (LONG-TERM) LIABILITIES

LIABILITIES") NON-CURRENT (LONG-TERM) LIABILITIES 1 MRI = Market Rate of Interest CR = Coupon Rate IE = Interest Expense FV = Fair Value PV = Present Value A&L = Assets & Liabilities CV = Carrying Value BS = Balance

NON-CURRENT (LONG-TERM) LIABILITIES 1 MRI = Market Rate of Interest CR = Coupon Rate IE = Interest Expense FV = Fair Value PV = Present Value A&L = Assets & Liabilities CV = Carrying Value BS = Balance

Fill-in-the-Blank Equations. Exercises

Chapter 3 The Adjusting Process Study Guide Solutions 1. Net book value Fill-in-the-Blank Equations 2. Depreciation expense 3. Supplies expense 4. Expense Exercises 1. Determine if each of the following

Chapter 3 The Adjusting Process Study Guide Solutions 1. Net book value Fill-in-the-Blank Equations 2. Depreciation expense 3. Supplies expense 4. Expense Exercises 1. Determine if each of the following

16 Statement of Cash Flows

Chapter 16 Statement of Cash Flows Learning Objectives: Learn about the purpose of the statement of cash flows Learn about the various sections of the statement of cash flows Learn how to prepare a statement

Chapter 16 Statement of Cash Flows Learning Objectives: Learn about the purpose of the statement of cash flows Learn about the various sections of the statement of cash flows Learn how to prepare a statement

CHAPTER 2 SOLUTIONS TO END OF CHAPTER MATERIAL QUESTIONS

CHAPTER 2 SOLUTIONS TO END OF CHAPTER MATERIAL QUESTIONS 1. The principal focus of financial accounting is to serve the needs of external decisionmakers. External decision makers need financial data about

CHAPTER 2 SOLUTIONS TO END OF CHAPTER MATERIAL QUESTIONS 1. The principal focus of financial accounting is to serve the needs of external decisionmakers. External decision makers need financial data about

Chapter 2: Main Financial Statements An overview

Chapter 2: Main Financial Statements An overview The objective of general purpose financial reporting is to provide information about the reporting entity that is useful to existing and potential investors,

Chapter 2: Main Financial Statements An overview The objective of general purpose financial reporting is to provide information about the reporting entity that is useful to existing and potential investors,

ACCOUNTING AND THE FINANCIAL STATEMENTS

1 ACCOUNTING AND THE FINANCIAL STATEMENTS DISCUSSION QUESTIONS 1. Accounting is a system for identifying, measuring, recording, and communicating financial information about an organization s activities

1 ACCOUNTING AND THE FINANCIAL STATEMENTS DISCUSSION QUESTIONS 1. Accounting is a system for identifying, measuring, recording, and communicating financial information about an organization s activities

REINFORCEMENT ACTIVITY 3, Part B, p. 715

REINFORCEMENT ACTIVITY 3, Part B, p. 715 10. Unadjusted Trial Balance December 31, 20X4 ACCOUNT TITLE DEBIT CREDIT Cash 25 0 0 1 40 Petty Cash 4 0 0 00 Accounts Receivable 15 7 8 9 20 Allowance for Uncollectible

REINFORCEMENT ACTIVITY 3, Part B, p. 715 10. Unadjusted Trial Balance December 31, 20X4 ACCOUNT TITLE DEBIT CREDIT Cash 25 0 0 1 40 Petty Cash 4 0 0 00 Accounts Receivable 15 7 8 9 20 Allowance for Uncollectible

Chapter 2 The Accounting Information System

Financial Accounting Making the Connection 1st Edition by Spiceland Chapter 2 The Accounting Information System REVIEW QUESTIONS Question 2-1 External transactions are transactions between the company

Financial Accounting Making the Connection 1st Edition by Spiceland Chapter 2 The Accounting Information System REVIEW QUESTIONS Question 2-1 External transactions are transactions between the company

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES INVESTING ACTIVITIES FINANCING ACTIVITIES

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

LEXMARK INTERNATIONAL GROUP, INC. AND SUBSIDIARIES CONSOLIDATED CONDENSED STATEMENTS OF EARNINGS (In Millions, Except Per Share Amounts) (Unaudited)

(Unaudited)") CONSOLIDATED CONDENSED STATEMENTS OF EARNINGS (In Millions, Except Per Share Amounts) Revenues Cost of revenues Gross profit Three Months Ended $787.0 501.8 285.20 $672.1 425.5 246.60 Percent Change 17%

CONSOLIDATED CONDENSED STATEMENTS OF EARNINGS (In Millions, Except Per Share Amounts) Revenues Cost of revenues Gross profit Three Months Ended $787.0 501.8 285.20 $672.1 425.5 246.60 Percent Change 17%

ANSWER SHEET EXAMINATION #1 29) Problem 1 30) 31) 32) 33) 34) 35) 36) 37) 10) 38) 11) 12) Problem 2 Problem 3 Problem 4 13) 14) 15) 16) 17) 18) 19)

Problem 1 30) 31) 32) 33) 34) 35) 36) 37) 10) 38) 11) 12) Problem 2 Problem 3 Problem 4 13) 14) 15) 16) 17) 18) 19)") ANSWER SHEET EXAMINATION #1 1) B 29) A Problem 1 2) B 30) D B 01 3) D 31) B A 02 4) D 32) B D 03 5) C 33) A A 04 6) C 34) C B 05 7) B 35) B A 06 8) B 36) B B 07 9) D 37) D C 08 10) B 38) D C 09 11) D D

ANSWER SHEET EXAMINATION #1 1) B 29) A Problem 1 2) B 30) D B 01 3) D 31) B A 02 4) D 32) B D 03 5) C 33) A A 04 6) C 34) C B 05 7) B 35) B A 06 8) B 36) B B 07 9) D 37) D C 08 10) B 38) D C 09 11) D D

Student Learning Outcomes

Chapter 2 Topic 1 Consolidated Statements: Date of Acquisition Dr. Chula King Advanced Accounting The University of West Florida 1 Student Learning Outcomes Net asset acquisition versus stock acquisition

Chapter 2 Topic 1 Consolidated Statements: Date of Acquisition Dr. Chula King Advanced Accounting The University of West Florida 1 Student Learning Outcomes Net asset acquisition versus stock acquisition

CHAPTER 12. Statement of Cash Flows. Study Objectives

CHAPTER 12 Statement of Cash Flows Study Objectives Indicate the primary purpose of the statement of cash flows. Distinguish among operating, investing, and financing activities. Explain the impact of

CHAPTER 12 Statement of Cash Flows Study Objectives Indicate the primary purpose of the statement of cash flows. Distinguish among operating, investing, and financing activities. Explain the impact of

BUSINESS FINANCIAL BASICS

BUSINESS FINANCIAL BASICS HERE ARE THREE BASIC FINANCIAL STATEMENTS THAT ARE IMPORTANT FOR YOUR SMALL BUSINESS: BALANCE SHEET. P&L. CASHFLOW STATEMENT 1 BALANCE SHEET A financial statement captures a person

BUSINESS FINANCIAL BASICS HERE ARE THREE BASIC FINANCIAL STATEMENTS THAT ARE IMPORTANT FOR YOUR SMALL BUSINESS: BALANCE SHEET. P&L. CASHFLOW STATEMENT 1 BALANCE SHEET A financial statement captures a person

Some deferred items for which adjusting entries would be made include: Prepaid insurance Prepaid rent Office supplies Depreciation Unearned revenue

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

CHAPTER 2: CONSTRUCTING FINANCIAL STATEMENTS

M2-18. a. no effect e. increase b. decrease f. increase c. decrease g. increase d. no effect M2-19. a. Balance sheet e. Balance sheet i. Income statement b. Income statement f. Balance sheet j. Income

M2-18. a. no effect e. increase b. decrease f. increase c. decrease g. increase d. no effect M2-19. a. Balance sheet e. Balance sheet i. Income statement b. Income statement f. Balance sheet j. Income

REVIEW Which of the following would be classified as external users of financial statements?

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

AGENDA: STATEMENT OF CASH FLOWS

TM 14-1 AGENDA: STATEMENT OF CASH FLOWS A. Foundational knowledge. B. Four key concepts for preparing the statement of cash flows. 1. Organizing the statement of cash flows. 2. Distinguishing between the

TM 14-1 AGENDA: STATEMENT OF CASH FLOWS A. Foundational knowledge. B. Four key concepts for preparing the statement of cash flows. 1. Organizing the statement of cash flows. 2. Distinguishing between the

32 Chapter 1 An Introduction to Financial Statements

32 Chapter 1 An Introduction to Financial Statements continued from previous page Balance Sheet at December 31, 2014 Property, plant and equipment (cost) Accumulated depreciation Land Goodwill 182,000

32 Chapter 1 An Introduction to Financial Statements continued from previous page Balance Sheet at December 31, 2014 Property, plant and equipment (cost) Accumulated depreciation Land Goodwill 182,000

Chapter 1: Accounting and the Business Environment

Chapter 1: Accounting and the Business Environment 1.1-1 Accounting is the information system that measures business activity, processes the data into reports, and communicates the results to decisions

Chapter 1: Accounting and the Business Environment 1.1-1 Accounting is the information system that measures business activity, processes the data into reports, and communicates the results to decisions

FEAR out. Taking the FEAR of Financial Statement Analysis. Toni Drake, CCE TRM Financial Services, Inc.

FEAR out Taking the FEAR of Financial Statement Analysis Toni Drake, CCE TRM Financial Services, Inc. FINANCIAL STATEMENTS Components of a Financial Statement Balance Sheet Income Statement Statement of

FEAR out Taking the FEAR of Financial Statement Analysis Toni Drake, CCE TRM Financial Services, Inc. FINANCIAL STATEMENTS Components of a Financial Statement Balance Sheet Income Statement Statement of

Corporate Accounting Recitation 3. June 18, 2004

15.511 Corporate Accounting Recitation 3 June 18, 2004 Why do we need CF/S? Accrual accounting is often based upon subjective judgments that can introduce measurement error and uncertainty into the reported

15.511 Corporate Accounting Recitation 3 June 18, 2004 Why do we need CF/S? Accrual accounting is often based upon subjective judgments that can introduce measurement error and uncertainty into the reported

CHAPTER 19 DIVIDENDS AND OTHER PAYOUTS

CHAPTER 19 DIVIDENDS AND OTHER PAYOUTS Answers to Concepts Review and Critical Thinking Questions 1. Dividend policy deals with the timing of dividend payments, not the amounts ultimately paid. Dividend

CHAPTER 19 DIVIDENDS AND OTHER PAYOUTS Answers to Concepts Review and Critical Thinking Questions 1. Dividend policy deals with the timing of dividend payments, not the amounts ultimately paid. Dividend

DIGITAL DISPATCH SYSTEMS INC. Consolidated Balance Sheets

Consolidated Balance Sheets Assets Current assets: March 31, June 30, September 30, December 31, 2004 2004 2004 2004 Restated Restated Restated Cash and cash equivalents $ 21,416,668 $ 19,377,082 $ 7,895,154

Consolidated Balance Sheets Assets Current assets: March 31, June 30, September 30, December 31, 2004 2004 2004 2004 Restated Restated Restated Cash and cash equivalents $ 21,416,668 $ 19,377,082 $ 7,895,154

Financial Accounting. Course: prof. univ. dr. Adriana TIRON-TUDOR, ( room 222) Seminar: Vasile CARDOS ( room 258)

Seminar: Vasile CARDOS ( room 258)") Financial Accounting Course: prof. univ. dr. Adriana TIRON-TUDOR, ( room 222) Seminar: Vasile CARDOS ( room 258) Recap: accounting fundamentals Why study accounting? Accounting provides information for

Financial Accounting Course: prof. univ. dr. Adriana TIRON-TUDOR, ( room 222) Seminar: Vasile CARDOS ( room 258) Recap: accounting fundamentals Why study accounting? Accounting provides information for

Exercises. 2) Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities

Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities") Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

Solutions to Final Exam, BA 202A, Fall 1999

Solutions to Final Exam, BA 202A, Fall 1999 Solution for Marketable Securities Question: a. Since A is a trading security, its unrealized gain or loss appears in income. Since it is the only trading security

Solutions to Final Exam, BA 202A, Fall 1999 Solution for Marketable Securities Question: a. Since A is a trading security, its unrealized gain or loss appears in income. Since it is the only trading security

Ch02 Solutions Manual pdf Ch02 Show.pdf

Ch02 Solutions Manual 2015-10-07.pdf Ch02 Show.pdf Chapter 2 Financial Statements, Cash Flow, and Taxes ANSWERS TO END-OF-CHAPTER QUESTIONS 2-1 a. The annual report is a report issued annually by a corporation

Ch02 Solutions Manual 2015-10-07.pdf Ch02 Show.pdf Chapter 2 Financial Statements, Cash Flow, and Taxes ANSWERS TO END-OF-CHAPTER QUESTIONS 2-1 a. The annual report is a report issued annually by a corporation

Chapter 12. The statement of cash flows categorizes cash receipts and cash payments as operating, investing, and financing activities.

1 Chapter 12 2 The statement of cash flows is a major financial statement as are the income statement, balance sheet, and statement of stockholders' equity. The statement of cash flows is required whenever

1 Chapter 12 2 The statement of cash flows is a major financial statement as are the income statement, balance sheet, and statement of stockholders' equity. The statement of cash flows is required whenever

STATEMENT OF CASH FLOWS

Chapter 16 STATEMENT OF CASH FLOWS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

Chapter 16 STATEMENT OF CASH FLOWS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

Financial Statement Analysis (22E00100) Assistant Professor Henry Jarva Aalto University

Assistant Professor Henry Jarva Aalto University") Financial Statement Analysis (22E00100) Assistant Professor Henry Jarva Aalto University Important topics Accounting analysis Earnings quality Motivations for earnings management Red flags Cash flow Analysis

Financial Statement Analysis (22E00100) Assistant Professor Henry Jarva Aalto University Important topics Accounting analysis Earnings quality Motivations for earnings management Red flags Cash flow Analysis

REVIEW PROBLEM Rockford Company s comparative balance sheet for 2012 and the company s income statement for the year follow:

REVIEW PROBLEM Rockford Company s comparative balance sheet for 2012 and the company s income statement for the year follow: Additional data: 1. Rockford paid a cash dividend in 2012. 2. The $4 million

REVIEW PROBLEM Rockford Company s comparative balance sheet for 2012 and the company s income statement for the year follow: Additional data: 1. Rockford paid a cash dividend in 2012. 2. The $4 million

ACCOUNTING - CLUTCH CH STATEMENT OF CASH FLOWS.

!! www.clutchprep.com CONCEPT: INTRODUCTION TO STATEMENT OF CASH FLOWS The Statement of Cash Flows shows what affected the Cash account balance throughout the period Predictive Value Helps predict future

!! www.clutchprep.com CONCEPT: INTRODUCTION TO STATEMENT OF CASH FLOWS The Statement of Cash Flows shows what affected the Cash account balance throughout the period Predictive Value Helps predict future

Disclaimer: This resource package is for studying purposes only EDUCATON

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Capítulo 1 Financial Statements and Accounting Concepts/Principles

Capítulo 1 Financial Statements and Accounting Concepts/Principles E2.7. Category Financial Statement(s) Cash A BS Accounts payable... L BS Common stock SE BS Depreciation expense.. E IS Net sales.. R

Capítulo 1 Financial Statements and Accounting Concepts/Principles E2.7. Category Financial Statement(s) Cash A BS Accounts payable... L BS Common stock SE BS Depreciation expense.. E IS Net sales.. R

PROBLEM 3-2B. (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...

J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...") PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

Statement of Cash Flows. Barry M Frohlinger

Statement of Cash Flows Barry M Frohlinger Statement of Cash Flows Page 1 Barry M Frohlinger, Inc. copyright 1981-2010 Companies are required to present a Statement of Cash Flows (cash statement) for each

Statement of Cash Flows Barry M Frohlinger Statement of Cash Flows Page 1 Barry M Frohlinger, Inc. copyright 1981-2010 Companies are required to present a Statement of Cash Flows (cash statement) for each

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson. The statement of cash flows is a required component of financial statements.

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson The statement of cash flows is a required component of financial statements. BASICS OF CASH FLOW REPORTING Purpose of the Statement

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson The statement of cash flows is a required component of financial statements. BASICS OF CASH FLOW REPORTING Purpose of the Statement

Class 12 Accountancy NCERT Solutions Cash Flow Statement

Class 12 Accountancy NCERT Solutions Cash Flow Statement TEST YOUR UNDERSTANDING I DO IT YOUR SELF I Question 1. The profit and loss account of Roy Limited is given here under Question 2. From the following

Class 12 Accountancy NCERT Solutions Cash Flow Statement TEST YOUR UNDERSTANDING I DO IT YOUR SELF I Question 1. The profit and loss account of Roy Limited is given here under Question 2. From the following

FAQ: Financial Statements

Question 1: What is the correct order in which financial reports must be created? Answer 1: The income statement is created first, then the owners' equity statement, and finally the balance sheet. This

Question 1: What is the correct order in which financial reports must be created? Answer 1: The income statement is created first, then the owners' equity statement, and finally the balance sheet. This

ACCT 151A WEEK 2, CHAP 2. Instructor: Michael Booth Cabrillo College

ACCT 151A WEEK 2, CHAP 2 Instructor: Michael Booth Cabrillo College ANALYZING BUSINESS TRANSACTIONS Property and Financial Objectives Interest 1. Record in equation form the financial effects of a business

ACCT 151A WEEK 2, CHAP 2 Instructor: Michael Booth Cabrillo College ANALYZING BUSINESS TRANSACTIONS Property and Financial Objectives Interest 1. Record in equation form the financial effects of a business

Vol. 1, Chapter 8 Introduction to Managerial Accounting

Vol. 1, Chapter 8 Introduction to Managerial Accounting Problem 1: Solution 1. Account 2. Adjusting entry 3. Balance sheet 4. Trial balance; Debit/Credit; Debit/Credit 5. Fundamental accounting equation

Vol. 1, Chapter 8 Introduction to Managerial Accounting Problem 1: Solution 1. Account 2. Adjusting entry 3. Balance sheet 4. Trial balance; Debit/Credit; Debit/Credit 5. Fundamental accounting equation

CHAPTER 12. The statement of cash flows categorizes cash receipts and cash payments as operating, investing, and financing activities.

CHAPTER 12 Purpose of the Statement of Cash Flows The statement of cash flows is considered a major financial statement, as are the income statement, balance sheet, and statement of stockholders' equity.

CHAPTER 12 Purpose of the Statement of Cash Flows The statement of cash flows is considered a major financial statement, as are the income statement, balance sheet, and statement of stockholders' equity.

FACTORISING EQUATIONS

STRIVE FOR EXCELLENCE TUTORING www.striveforexcellence.com.au Factorising expressions with 2 terms FACTORISING EQUATIONS There are only 2 ways of factorising a quadratic with two terms: 1. Look for something

STRIVE FOR EXCELLENCE TUTORING www.striveforexcellence.com.au Factorising expressions with 2 terms FACTORISING EQUATIONS There are only 2 ways of factorising a quadratic with two terms: 1. Look for something

CHAPTER 2 ANALYZING TRANSACTIONS: THE ACCOUNTING EQUATION

REVIEW QUESTIONS CHAPTER 2 ANALYZING TRANSACTIONS: THE ACCOUNTING EQUATION 1. It is necessary to distinguish between business assets and liabilities and nonbusiness assets and liabilities of a single proprietor

REVIEW QUESTIONS CHAPTER 2 ANALYZING TRANSACTIONS: THE ACCOUNTING EQUATION 1. It is necessary to distinguish between business assets and liabilities and nonbusiness assets and liabilities of a single proprietor

0. Introduction. What is finance? What are the two main branches of finance? What are the three main aspects of corporate finance?

1 0. Introduction What is finance? What are the two main branches of finance? What are the three main aspects of corporate finance? 2 1. Financial statements and cash flow A quick review of balance sheet

1 0. Introduction What is finance? What are the two main branches of finance? What are the three main aspects of corporate finance? 2 1. Financial statements and cash flow A quick review of balance sheet

Introduction. What exactly is the statement of cash flows? Composing the statement

Introduction The course about the statement of cash flows (also statement hereinafter to keep the text simple) is aiming to help you in preparing one of the apparently most complicated statements. Most

Introduction The course about the statement of cash flows (also statement hereinafter to keep the text simple) is aiming to help you in preparing one of the apparently most complicated statements. Most

ICMA s Requirements for CMA Designation

Part 1 Study Unit 1 ICMA s Requirements for CMA Designation Become a Member! Preferably of a local chapter (there are benefits). Pass both parts of the exam within 3 years (of starting the process). Satisfy

Part 1 Study Unit 1 ICMA s Requirements for CMA Designation Become a Member! Preferably of a local chapter (there are benefits). Pass both parts of the exam within 3 years (of starting the process). Satisfy

Digital River, Inc. Fourth Quarter Results (In thousands, except share data) Subject to reclassification

Subject to reclassification") (In thousands, except share data) Consolidated Balance Sheets (Unaudited) 2012 2011 Assets Current assets Cash and cash equivalents $ 542,851 $ 497,193 Short-term investments 162,794 223,349 Accounts receivable,

(In thousands, except share data) Consolidated Balance Sheets (Unaudited) 2012 2011 Assets Current assets Cash and cash equivalents $ 542,851 $ 497,193 Short-term investments 162,794 223,349 Accounts receivable,

Table of Contents Accounting Questions & Answers

Table of Contents Accounting Questions & Answers Overview & Key Rules of Thumb...2 Key Rule #1: The Income Statement...2 Key Rule #2: The Balance Sheet...5 Key Rule #3: The Cash Flow Statement...8 Key

Table of Contents Accounting Questions & Answers Overview & Key Rules of Thumb...2 Key Rule #1: The Income Statement...2 Key Rule #2: The Balance Sheet...5 Key Rule #3: The Cash Flow Statement...8 Key

Introduction To The Income Statement

Introduction To The Income Statement This is the downloaded transcript of the video presentation for this topic. More downloads and videos are available at The Kaplan Group Commercial Collection Agency

Introduction To The Income Statement This is the downloaded transcript of the video presentation for this topic. More downloads and videos are available at The Kaplan Group Commercial Collection Agency

CHAPTER17 DIVIDENDS AND DIVIDEND POLICY

CHAPTER17 DIVIDENDS AND DIVIDEND POLICY Learning Objectives LO1 Dividend types and how dividends are paid. LO2 The issues surrounding dividend policy decisions. LO3 The difference between cash and stock

CHAPTER17 DIVIDENDS AND DIVIDEND POLICY Learning Objectives LO1 Dividend types and how dividends are paid. LO2 The issues surrounding dividend policy decisions. LO3 The difference between cash and stock

Digital River, Inc. First Quarter Results (In thousands, except share data) Subject to reclassification

Subject to reclassification") (In thousands, except share data) Consolidated Balance Sheets (Unaudited) December 31, Assets Current assets Cash and cash equivalents $ 500,742 $ 542,851 Short-term investments 144,615 162,794 Accounts

(In thousands, except share data) Consolidated Balance Sheets (Unaudited) December 31, Assets Current assets Cash and cash equivalents $ 500,742 $ 542,851 Short-term investments 144,615 162,794 Accounts

Chapter 3. Learning Objectives. Distinguish accrual accounting from cash-basis accounting. Objective 1. The Adjusting Process

PowerPoint to accompany Chapter 3 The Adjusting Process Learning Objectives 1. Distinguish accrual accounting from cash-basis accounting. 2. Make adjusting entries at the end of the accounting period.

PowerPoint to accompany Chapter 3 The Adjusting Process Learning Objectives 1. Distinguish accrual accounting from cash-basis accounting. 2. Make adjusting entries at the end of the accounting period.

Financial Accounting Chapter 1 Review

Financial Accounting Chapter 1 Review Fall 2011 1. What are the Forms of Business Organization? Chapter 1: An Introduction to Accounting Sole Proprietorship a business owned by a individual; Advantages:

Financial Accounting Chapter 1 Review Fall 2011 1. What are the Forms of Business Organization? Chapter 1: An Introduction to Accounting Sole Proprietorship a business owned by a individual; Advantages:

Nature of Business and Accounting

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

ANSWER SHEET EXAMINATION #1

ANSWER SHEET EXAMINATION #1 NAME: DATE: 1) 29) Multiple-choice (38) 2) 30) Matching (46) 3) 31) Problems (16) 4) 32) Total (100) / Grade 5) 33) 6) 34) 7) 35) 8) 36) 9) 37) 10) 38) 11) 12) 13) 14) 15) 16)

ANSWER SHEET EXAMINATION #1 NAME: DATE: 1) 29) Multiple-choice (38) 2) 30) Matching (46) 3) 31) Problems (16) 4) 32) Total (100) / Grade 5) 33) 6) 34) 7) 35) 8) 36) 9) 37) 10) 38) 11) 12) 13) 14) 15) 16)

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything!

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything! What We Will Do in This Session: 1. Gauge your level of confidence regarding this topic area 2. Review

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything! What We Will Do in This Session: 1. Gauge your level of confidence regarding this topic area 2. Review

LONG-TERM LIABILITIES: NOTES, BONDS, AND LEASES

FINANCIAL ACCOUNTING Week 10 LONG-TERM LIABILITIES: NOTES, BONDS, AND LEASES I. Learning Objectives - Long-term Liabilities A. Understand what are long-term liabilities, e.g., longterm notes payable, bonds

FINANCIAL ACCOUNTING Week 10 LONG-TERM LIABILITIES: NOTES, BONDS, AND LEASES I. Learning Objectives - Long-term Liabilities A. Understand what are long-term liabilities, e.g., longterm notes payable, bonds

4 Chapter 2 Chapter 2: Financial Statement and Cash Flow Analysis

4 Chapter 2 Chapter 2: Financial Statement and Cash Flow Analysis Answers to End of Chapter Questions 2-1. Financial statement analysis provides information about the company s financial health, and its

4 Chapter 2 Chapter 2: Financial Statement and Cash Flow Analysis Answers to End of Chapter Questions 2-1. Financial statement analysis provides information about the company s financial health, and its

AccountingCoach.com Financial Ratios

AccountingCoach.com Financial Ratios All underlined words are defined in the attached Glossary (Pages 13 20). Introduction to Financial Ratios When analyzing computing financial ratios and when doing other

AccountingCoach.com Financial Ratios All underlined words are defined in the attached Glossary (Pages 13 20). Introduction to Financial Ratios When analyzing computing financial ratios and when doing other

Chapter 2 Analyzing Business Transactions

College Accounting Chapters 1 30 15th Edition Price Solutions Manual Full Download: http://testbanklive.com/download/college-accounting-chapters-1-30-15th-edition-price-solutions-manual/ Price, Haddock,

College Accounting Chapters 1 30 15th Edition Price Solutions Manual Full Download: http://testbanklive.com/download/college-accounting-chapters-1-30-15th-edition-price-solutions-manual/ Price, Haddock,

BODORP (Pty) Ltd's STATEMENT of FINANCIAL POSITION as at eoy 20X5

Ltd's STATEMENT of FINANCIAL POSITION as at eoy 20X5") Aufgabe QR-10.10: Direkte Methode mit Vergleich von Ein- und Auszahlungen (Direct Method with Comparison of Cash Inflow and Cash Outflow) BODORP (Pty) Ltd is a marketing consultancy. The company has 10

Aufgabe QR-10.10: Direkte Methode mit Vergleich von Ein- und Auszahlungen (Direct Method with Comparison of Cash Inflow and Cash Outflow) BODORP (Pty) Ltd is a marketing consultancy. The company has 10

CHAPTER 12 STATEMENT OF CASH FLOWS

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

Full file at

02 Student: Indicate how each event affects the elements of financial statements. Use the following letters to record your answer in the box shown below each element. You do not need to enter amounts.

02 Student: Indicate how each event affects the elements of financial statements. Use the following letters to record your answer in the box shown below each element. You do not need to enter amounts.

CHAPTER 2 FINANCIAL STATEMENTS, TAXES, AND CASH FLOWS

CHAPTER 2 FINANCIAL STATEMENTS, TAXES, AND CASH FLOWS Learning Objectives LO1 The difference between accounting value (or book value) and market value. LO2 The difference between accounting income and

CHAPTER 2 FINANCIAL STATEMENTS, TAXES, AND CASH FLOWS Learning Objectives LO1 The difference between accounting value (or book value) and market value. LO2 The difference between accounting income and

Chapter 1. assembled and processed

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3)

") MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following statement shows the revenues and expenses of the

MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following statement shows the revenues and expenses of the

DOOSAN CORPORATION AND SUBSIDARIES CONSOLIDATED STATEMENTS OF FINANCIAL POSITION AS OF DECEMBER 31, 2010 AND 2009

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION A S S E T S 2010 2009 CURRENT ASSETS Cash and cash equivalents (Notes 2, 3, 14 and 30) 2,768,730,812,677 2,258,946,984,813 Short-term financial instruments

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION A S S E T S 2010 2009 CURRENT ASSETS Cash and cash equivalents (Notes 2, 3, 14 and 30) 2,768,730,812,677 2,258,946,984,813 Short-term financial instruments

Chapter 4. The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Note on Cash Flow Statements

Note on Cash Flow Statements Indirect Cash Flow Statements can be pretty confusing, but they don't have to be if you think about their relationship to the other financial statements. Here I present several

Note on Cash Flow Statements Indirect Cash Flow Statements can be pretty confusing, but they don't have to be if you think about their relationship to the other financial statements. Here I present several

Chapter 7. Funds Analysis, Cash- Flow Analysis, and Financial Planning

Chapter 7 Funds Analysis, Cash- Flow Analysis, and Financial Planning 7-1 Pearson Education Limited 2004 Fundamentals of Financial Management, 12/e Created by: Gregory A. Kuhlemeyer, Ph.D. Carroll College,

Chapter 7 Funds Analysis, Cash- Flow Analysis, and Financial Planning 7-1 Pearson Education Limited 2004 Fundamentals of Financial Management, 12/e Created by: Gregory A. Kuhlemeyer, Ph.D. Carroll College,

Chapter 4 Question Review 1

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

Dr. Maddah ENMG 602 Intro. to Financial Eng g 11/04/09. Statement of Cash Flows (Chapter 4, Antle)

") Dr. Maddah ENMG 602 Intro. to Financial Eng g 11/04/09 Statement of Cash Flows (Chapter 4, Antle) Basic definitions Cash is readily transferable value. It is the most common way organizations acquire goods

Dr. Maddah ENMG 602 Intro. to Financial Eng g 11/04/09 Statement of Cash Flows (Chapter 4, Antle) Basic definitions Cash is readily transferable value. It is the most common way organizations acquire goods