BUS210. Chapter 4 Sessions 4, 5, 6, & 7 Mechanics of Financial Information

|

|

|

- Darcy Spencer

- 6 years ago

- Views:

Transcription

1 BUS210 Chapter 4 Sessions 4, 5, 6, & 7 Mechanics of Financial Information

2

3 Connecting the Accounting Equation with Transactions: Journal Entries, T Accounts

4 E4-9 Prepare journal entries for each cash transaction during January, (assume beginning balance is $5,000). 1. Issued 600 shares of stock for $25 each. 2. Sold services for $4, Paid wages of $1, Purchased land as a long-term investment for $9, Paid a $2,000 dividend. 6. Sold land with a book value of $3,000 for $3, Paid $1,500 to the bank: $900 to reduce the principal on the outstanding loan and $600 as an interest payment. 8. Paid miscellaneous expenses of $1,800.

5

6

7 E4-10a Show how the eight transactions affect the accounting equation, prepare journal entries, and prepare an income statement, statement of shareholders equity, balance sheet, and statement of cash flows. 1. Collected $12,000 in cash from shareholders. 2. Borrowed $5,000 from a bank. 3. Purchased two parcels of land for a total of $10, Paid $5,000 to rent lawn equipment for the remainder of the year. 5. Provided lawn services, receiving $10,000 in cash and $4,000 in receivables. 6. Paid miscellaneous expenses of $4, Sold one parcel of land with a cost of $3,000 for $2, Paid a $2,200 dividend to the shareholders.

8

9 E4-10a Financial statement relationships Balance Sheet- Beginning Balance Sheet -Ending Cash Statement of Cash Flows Cash Other CA Cash-Operating Other CA LT Assets Cash-Investing LT Assets T Assets Cash-Financing T Assets? Change in Cash C Liab. Cash C Liab. LT Liab. Cash ? LT Liab. CC CC RE Income Statement RE T L+SHE Revenue T L+SHE? Expenses Net Income? Statement of Shareholders Equity Contributed Capital Retained Earnings Beginning NI Dividends Stock Issue XXXXXXXXXXXXXX XXXXXXXXXXXXXX XXXXXXXXXXXXXXXXX Ending??

10 E4-4 Show how the five transactions affect the accounting equation, express as journal entries, post to T accounts, and prepare financial statements. 1. Shareholders contributed $10,000 cash in the first year of operations. 2. Performed services for $8,000, receiving $6,000 cash and a $2,000 receivable. 3. Incurred expenses of $6,000. Paid $3,000 in cash, and $3,000 is still payable. 4. Purchased land for $12,000. Paid $2,000 in cash and signed a long-term note for the remainder. 5. Paid shareholders $400 in the form of a dividend. 6. Sold one-half of the land purchased in (4.) for $7,000 cash.

11 Balance Sheet- Beginning E4-4 Financial statement relationships Balance Sheet -Ending Cash Statement of Cash Flows Cash Other CA Cash-Operating Other CA LT Assets Cash-Investing LT Assets T Assets Cash-Financing T Assets? Change in Cash C Liab. Cash C Liab. LT Liab. Cash ? LT Liab. CC CC RE Income Statement RE T L+SHE Revenue T L+SHE? Expenses Net Income? Statement of Shareholders Equity Contributed Capital Retained Earnings Beginning NI Dividends Stock Issue XXXXXXXXXXXXXX XXXXXXXXXXXXXX XXXXXXXXXXXXXXXXX Ending??

12 Matching & Accrual Accounting Basic to financial reporting of corporations. Concerned with the timing of revenue and expense recognition. Purpose is to accurately measure revenues and expenses (and profits) for each accounting period. Accrual accounting s Income Statement attempts to match revenues earned and the expenses incurred, NOT cash flows. Accrual accounting s Statement of Cash Flows reports the cash inflows and outflows for the period.

13 Accrual Income Statement Reported revenues include: Revenues collected in a prior period deferred to the current period (reported previously on the balance sheet as a liability, Unearned Revenues) Revenues collected in the current period that were also earned currently. Revenues earned (and accrued) currently that will be collected in future periods (reported currently on the balance sheet as an asset, Accounts Receivable.

14 Accrual Income Statement Reported expenses include: The cost of goods or services consumed in the current period that were paid for in a prior period, but deferred to the current period (reported previously on the balance sheet as an asset; i.e., Inventories, Prepaid Expenses). The cost of goods or services consumed in the current period that were also paid for in the current period. The cost of goods or services consumed in the current period that will be paid for in future periods (reported on the current balance sheet as a liability; i.e., Accounts Payable).

15 Accrual Balance Sheet Assets on the Balance Sheet include: Something that has future or potential value. Future expenses for which cash has already been paid. (Prepaid i.e., deferred Expenses) Past revenues for which cash has not been collected. (Accounts Receivable i.e., accrued revenues) Liabilities on the Balance Sheet include: Responsibilities or promises to others Past expenses for which cash has not been paid. (Accrued Expenses Payable) Future revenues for which cash has already been collected. (Deferred or Unearned Revenues)

16 Accruals and Deferrals A deferral asset or liability is created on the balance sheet anytime cash is collected or paid BEFORE the associated expense or revenue is recognized (deferred). Examples: Inventories, Prepaid expenses, Equipment, Unearned revenues. An accrual asset or liability is created on the balance sheet any time revenue or expense is recognized (accrued) BEFORE the associated cash flow is received or paid. Examples: Accounts Receivable, Interest Receivable, Accounts Payable, Taxes Payable.[Expense now, Pay later. OR Receive later, Revenue now.]

17 Adjusting Entries: 4 Kinds

18 Adjusting Entries: 4 Kinds

19 E4-12 Adjusting journal entries Explain each of the entries and classify each of the entries as either a deferral (cost expiration) AJE or an accrual AJE. Rent Expense 1,200 Rent Payable 1,200 Insurance Expense 5,000 Prepaid Insurance 5,000 Depreciation Expense 20,000 Accumulated Depreciation 20,000 Interest Receivable 1,500 Interest Revenue 1,500 Unearned Revenue 200 Fees Earned 200

20

21 P4-8 Preparing adjusting journal entries a. The supplies balance is $85,000. A count of supplies reveals that the company actually has $30,000 of supplies on hand. Supplies Exp 55,000 Supplies 55,000 b. As of the company had not paid the rent for the month. The monthly rent is $2,400. Rent Exp 2,400 Rent Pay 2,400 c. On the company collected $18,000 in customer advances for the subsequent performance of a service. As of two-thirds of the service had been performed. Unearned Service Rev 12,000 Fees Earned 12,000 d. The total cost of fixed assets is $500,000. The company estimates that the assets have a useful life of ten years and used straight-line depreciation. DE 50,000 AD 50,000

22 P4-8 Preparing adjusting journal entries e. The company borrowed $10,000 at an annual interest rate of 12% on The first interest payment will be made Interest Exp 600 Interest Pay 600 f. The company placed several ads in newspapers during the month. On the company received a $28,000 bill for the ads, which was not recorded at the time. Adv Exp 28,000 Adv Pay 28,000 g. On the company paid the premium for a one-year life insurance policy. The $350 cost of the premium was capitalized when paid. Insurance Exp 175 Prepaid Insurance 175

23

24

25 P4-9 Inferring adjusting journal entries from changes in T-account balances Account Balance before AJE Prepaid rent 14,500 Prepaid insurance 8,500 Accum. Deprec. 36,000 Rent expense 6,500 Insurance expense 5,500 Depreciation expense 0 Balance after AJE 11,800 7,800 38,400 9,200 6,200 2,400

26 P4-9 Inferring adjusting journal entries from changes in T-account balances Account Balance before AJE Salaries payable 1,300 Unearned revenues 800 Fees earned 87,600 Salary expense 3,500 Balance after AJE 2, ,800 4,700

27 E4-21 Reverse T-account analysis 1. Compute the wages payable: Wages Cash payments during 2012 $35,000 Wages Payable as of $17,000 Wages Expense on the 2012 IS $39,000

28 E4-21 Reverse T-account analysis 2. the 2012 cash payments for rent: Rent Prepaid Rent $12,000 Prepaid Rent $15,000 Rent Expense on the 2012 IS $21,000

29 E4-21 Reverse T-account analysis 3. the accounts receivable as of : Accounts Receivable Cash collected from customers during 2012 $38,000 Accounts Receivable as of $14,000 Sales Revenue on the 2012 IS $45,000

30 P4-20 Reverse T-account analysis You are a credit analyst for a bank. Badger Business has applied for a loan. The company claims to have more than tripled profits from 2011 to 2012 and believes that it should be given prime credit terms. In addition, you note that Badger has expanded its operations, recently paying $37,000 for new equipment that replaced old equipment, which was sold that same year. No other transactions affected the company s equipment account. Excerpts from the 2012 financial statements are provided below. Balance sheet: Equipment $97,400 $84,800 Acc. Depreciation (26,400) (24,300) Income statement: Net income $5,200 $1,500 Depreciation expense $8,700 $7,600 Statement of cash flows: Proceeds from equipment sale $23,400 0

31 E4-16 The difference between cash and accrual accounting Washington Forest Products began operations on January 1, On December 31, 2011, the company accountant ascertains that the following amounts should be reported as expenses on the income statement: Insurance Expense $20,000; Supplies Expense $11,000; Rent Expense $14,000. A Review of the company s cash disbursements indicates the company made related cash payments during 2011 as follows: Insurance $29,000; Supplies $27,000; Rent $8,000 Explain why the amounts shown as expenses do not equal the cash paid. For each expense account, compute the amount that should be shown in the related balance sheet account as of December 31, 2011 (remember the company begin operations this year).

32 4 Closing Entries: Income Statement and Dividend Accounts

33 2 Closing Entries: Income Statement and Dividend Accounts

34

35 Accounts Payable $62,800 Accounts Receivable $50,000 Accumulated Depreciation $3,000 Building $163,200 Cash $220,480 Common Stock $400,000 Depreciation Expense $3,000 Design Income $140,000 Dividends $30,000 Income Taxes Expense $8,000 Income Taxes Payable $8,000 Office Supplies $36,600 Office Supplies Expense $15,400 Prepaid Rent $16,000 Rent Expense $16,000 Unearned Income $1,680 Utilities Expense $6,800 Wages Expense $55,200 Wages Payable $7,200 Prepare closing entries from the adjusted trial balance shown above. Dr Design Income 140,000 Cr Retained Earnings 35,600 Cr Depreciation Exp 3,000; Inc Tx Exp 8,000; Off Supp Exp 15,400; Rent Exp 16,000; Util Exp 6,800; Wages Exp 55, ,400 Dr Retained Earnings 30,000 Cr Dividends 30,000

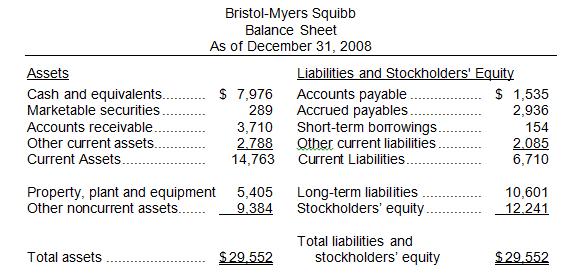

36 E4-7 Preparing financial statements Taken from the 2008 annual report of Bristol-Myers Squibb, a world-leading drug company (dollars in millions), reconstruct the financials. Cost of goods sold $ 6,396 Net cash from operations 3,707 Accounts receivable 3,710 Restructuring expense 218 Net cash from financing (2,582) Shareholders equity 12,241 Net cash from investing 5,079 Research & dev. expense 3,585 Other noncurrent assets 9,384 Other expenses 901 Marketable securities 289 Cash and equivalents $ 7,976 Short-term borrowings 154 Adv. & product expense 1,550 Accounts payable 1,535 Long-term liabilities 10,601 Net sales 20,597 Property, plant, & equip. 5,405 Other current assets 2,788 Other current liabilities 2,085 Sell. & adm. expenses 4,792 Accrued payables 2,936

37

Chapter 4 Mechanics of Financial Information

BUS210 Chapter 4 Mechanics of Financial Information What do you remember? Economic Events--> Transactions Reducing events to numbers Connecting the Accounting Equation with Transactions: Journal Entries,

BUS210 Chapter 4 Mechanics of Financial Information What do you remember? Economic Events--> Transactions Reducing events to numbers Connecting the Accounting Equation with Transactions: Journal Entries,

Chapter 4 Mechanics of Financial Information

BUS210 9.15.14 Chapter 4 Mechanics of Financial Information Before Class starts.(make sure your name is on all submissions) First Homework 14 Fall Emory Inc. Due 9/17 before class; No EXCEPTIONS Help Session

BUS210 9.15.14 Chapter 4 Mechanics of Financial Information Before Class starts.(make sure your name is on all submissions) First Homework 14 Fall Emory Inc. Due 9/17 before class; No EXCEPTIONS Help Session

Analysis of Financial Statements and Statement of Cash Flows BUS512M. December 16, 2016 Session 2 8:00-noon Susan Crosson

Analysis of Financial Statements and Statement of Cash Flows BUS512M December 16, 2016 Session 2 8:00-noon Susan Crosson P4-20 Reverse T-account analysis You are a credit analyst for a bank. Badger Business

Analysis of Financial Statements and Statement of Cash Flows BUS512M December 16, 2016 Session 2 8:00-noon Susan Crosson P4-20 Reverse T-account analysis You are a credit analyst for a bank. Badger Business

BUS :30 Fall TA Office Hours T&R 5-6pm W520

BUS210 9.3.14 8:30 Fall 2014 TA Office Hours T&R 5-6pm W520 After putting your name on your papers, Turn in TPI (only if attended first class), Student Consent form, and VARK Learning styles Financial

BUS210 9.3.14 8:30 Fall 2014 TA Office Hours T&R 5-6pm W520 After putting your name on your papers, Turn in TPI (only if attended first class), Student Consent form, and VARK Learning styles Financial

CHAPTER 12. The statement of cash flows categorizes cash receipts and cash payments as operating, investing, and financing activities.

CHAPTER 12 Purpose of the Statement of Cash Flows The statement of cash flows is considered a major financial statement, as are the income statement, balance sheet, and statement of stockholders' equity.

CHAPTER 12 Purpose of the Statement of Cash Flows The statement of cash flows is considered a major financial statement, as are the income statement, balance sheet, and statement of stockholders' equity.

Analysis of Financial Statements and Statement of Cash Flows BUS512M. November 21, 2014 Session 2 8:00-11:30 Susan Crosson

Analysis of Financial Statements and Statement of Cash Flows BUS512M November 21, 2014 Session 2 8:00-11:30 Susan Crosson Homework See Handout Today s Learning Outcomes Analyzing Financial Statementscommon

Analysis of Financial Statements and Statement of Cash Flows BUS512M November 21, 2014 Session 2 8:00-11:30 Susan Crosson Homework See Handout Today s Learning Outcomes Analyzing Financial Statementscommon

Reporting and Analyzing Cash Flows

Chapter 17 Reporting and Analyzing Cash Flows QUICK STUDY SOLUTIONS Quick Study 17-1 (10 minutes) 1. Operating 6. Operating 2. Operating 7. Investing 3. Financing 8 Operating 4. Financing 9. Operating

Chapter 17 Reporting and Analyzing Cash Flows QUICK STUDY SOLUTIONS Quick Study 17-1 (10 minutes) 1. Operating 6. Operating 2. Operating 7. Investing 3. Financing 8 Operating 4. Financing 9. Operating

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Accounting Cycle Review Problem. Michelle Clark. Accounting 1110 Section 401. Fall 2014

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

Adjusting the Accounts

HOSP 1860 (Financial Acct) Learning Centre Adjusting the Accounts Anytime we prepare financial statements or reach the end of an accounting period, there are account adjustments that need to be made to

HOSP 1860 (Financial Acct) Learning Centre Adjusting the Accounts Anytime we prepare financial statements or reach the end of an accounting period, there are account adjustments that need to be made to

Adjustments, Financial Statements and the Quality of Earnings

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

Draw an Accountant. Who/What Information needs for business/financial decisions

Draw an Accountant. Who/What Information needs for business/financial decisions BUS210 Session 1 Handouts: To Do List Syllabus Teaching Perspectives Inventory (TPI) Class Handout Attendance: Sign roster!!!

Draw an Accountant. Who/What Information needs for business/financial decisions BUS210 Session 1 Handouts: To Do List Syllabus Teaching Perspectives Inventory (TPI) Class Handout Attendance: Sign roster!!!

BUS 321 Intermediate Accounting I Jan. 24, 2016 Name

BUS 321 Intermediate Accounting I Jan. 24, 2016 Name 1. GAAP What does GAAP stand for? Generally Accepted Accounting Principles 2. OBJECTIVE OF FINANCIAL REPORTING Write the objective of Financial Reporting.

BUS 321 Intermediate Accounting I Jan. 24, 2016 Name 1. GAAP What does GAAP stand for? Generally Accepted Accounting Principles 2. OBJECTIVE OF FINANCIAL REPORTING Write the objective of Financial Reporting.

Week 3. Topic 3 Chapter 3. ACT102 Introduction to Accounting. Accounting for end of financial period adjustments 21/02/2018

ACT102 Introduction to Accounting Week 3 Accounting for end of financial period adjustments Topic 3 Chapter 3 2 RECAP Topic 2: Recording Business Transactions The accounting equation must always balance

ACT102 Introduction to Accounting Week 3 Accounting for end of financial period adjustments Topic 3 Chapter 3 2 RECAP Topic 2: Recording Business Transactions The accounting equation must always balance

Cash. Laundry Equipment. Hilda Dinero, Capital Oct. 31 Clos. 1,000 Oct. 31 Bal. 18, Clos. 12, Bal. 30,200

1, 3, 6. Oct. 31 Bal. 1,450 Cash Laundry Supplies Oct. 31 Bal. 3,750 Oct. 31 Adj. 2,800 31 Adj. Bal. 950 Prepaid Insurance Oct. 31 Bal. 2,400 Oct. 31 Adj. 2,000 31 Adj. Bal. 400 Oct. 31 Bal. 54,500 Laundry

1, 3, 6. Oct. 31 Bal. 1,450 Cash Laundry Supplies Oct. 31 Bal. 3,750 Oct. 31 Adj. 2,800 31 Adj. Bal. 950 Prepaid Insurance Oct. 31 Bal. 2,400 Oct. 31 Adj. 2,000 31 Adj. Bal. 400 Oct. 31 Bal. 54,500 Laundry

After studying this chapter, you should be able to: adjusted account balances.

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

Smith Equipment Corporation Part II Suggested Journal Entries

Smith Equipment Corporation Part II Suggested Journal Entries 1 To summarize purchases on account for $800,000 Merchandise inventory (a) 800,000 Accounts payable (l) 800,000 2 To summarize payments to

Smith Equipment Corporation Part II Suggested Journal Entries 1 To summarize purchases on account for $800,000 Merchandise inventory (a) 800,000 Accounts payable (l) 800,000 2 To summarize payments to

SOLUTIONS TO TEST I FALL 1996 PMBA

SOLUTIONS TO TEST I FALL 1996 PMBA 1. B A decrease in the items on the left is not balanced by an increase in the items on the right. For a., an increase on the left and right will balance out. For c.,

SOLUTIONS TO TEST I FALL 1996 PMBA 1. B A decrease in the items on the left is not balanced by an increase in the items on the right. For a., an increase on the left and right will balance out. For c.,

4-1 COMPLETING THE ACCOUNTING CYCLE

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield. Slide 3-2

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

Dec. 4: Paid $ 750 cash for office supplies. Date Accounts Debit Credit Dec. 4 Office Supplies 750 Cash 750

Requirement 1. Record each transaction in the journal. Explanations are not required. (Record debits first, then credits. Exclude explanations from journal entries.) 1: began operations by receiving $

Requirement 1. Record each transaction in the journal. Explanations are not required. (Record debits first, then credits. Exclude explanations from journal entries.) 1: began operations by receiving $

Chapter 4. The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Principles of Accounting II

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

Learning Outcomes. The Statement of Cash Flows. Chapter 4: The Income Statement, Comprehensive Income and The Statement of Cash Flows: Part 2

Chapter 4: The Income Statement, Comprehensive Income and The Statement of Cash Flows: Part 2 The Statement of Cash Flows Dr. Chula King Intermediate Accounting 1 Learning Outcomes After completing this

Chapter 4: The Income Statement, Comprehensive Income and The Statement of Cash Flows: Part 2 The Statement of Cash Flows Dr. Chula King Intermediate Accounting 1 Learning Outcomes After completing this

4. If cash is collected in advance for services, the revenue is recognized when the services are rendered.

ANSWERS TO QUESTIONS - CHAPTER 2 1. Accrual accounting attempts to record the effects of accounting events in the period when such events occur, regardless of when cash is received or paid. The goal is

ANSWERS TO QUESTIONS - CHAPTER 2 1. Accrual accounting attempts to record the effects of accounting events in the period when such events occur, regardless of when cash is received or paid. The goal is

4. If cash is collected in advance for services, the revenue is recognized when the services are rendered.

ANSWERS TO QUESTIONS - CHAPTER 2 1. Accrual accounting attempts to record the effects of accounting events in the period when such events occur, regardless of when cash is received or paid. The goal is

ANSWERS TO QUESTIONS - CHAPTER 2 1. Accrual accounting attempts to record the effects of accounting events in the period when such events occur, regardless of when cash is received or paid. The goal is

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything!

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything! What We Will Do in This Session: 1. Gauge your level of confidence regarding this topic area 2. Review

UIL 2017 Capital Conference UIL Accounting Accounting Accruals & Deferrals: Timing is Everything! What We Will Do in This Session: 1. Gauge your level of confidence regarding this topic area 2. Review

4 Criteria for Recognizing Revenue

What do you know? E4-7 Preparing financial statements Taken from the 2008 annual report of Bristol-Myers Squibb, a world-leading drug company (dollars in millions), reconstruct the financials. Cost of

What do you know? E4-7 Preparing financial statements Taken from the 2008 annual report of Bristol-Myers Squibb, a world-leading drug company (dollars in millions), reconstruct the financials. Cost of

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty

Chapter 2 Review of the Accounting Process AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty

Chapter 12. The statement of cash flows categorizes cash receipts and cash payments as operating, investing, and financing activities.

1 Chapter 12 2 The statement of cash flows is a major financial statement as are the income statement, balance sheet, and statement of stockholders' equity. The statement of cash flows is required whenever

1 Chapter 12 2 The statement of cash flows is a major financial statement as are the income statement, balance sheet, and statement of stockholders' equity. The statement of cash flows is required whenever

ACCT 100 Intro to Acct. Chapter 12: Accruals, Deferrals, and the Worksheet Johnson

ACCT 100 Intro to Acct. Chapter 12: Accruals, Deferrals, and the Worksheet Johnson Where we have been: We have learned a lot about the selling and buying functions of merchandiser. You have learned many

ACCT 100 Intro to Acct. Chapter 12: Accruals, Deferrals, and the Worksheet Johnson Where we have been: We have learned a lot about the selling and buying functions of merchandiser. You have learned many

CHAPTER 12. Statement of Cash Flows. Study Objectives

CHAPTER 12 Statement of Cash Flows Study Objectives Indicate the primary purpose of the statement of cash flows. Distinguish among operating, investing, and financing activities. Explain the impact of

CHAPTER 12 Statement of Cash Flows Study Objectives Indicate the primary purpose of the statement of cash flows. Distinguish among operating, investing, and financing activities. Explain the impact of

CHAPTER 2: FINANCIAL REPORTING MECHANISMS

Department of Management and Law CHAPTER 2: FINANCIAL REPORTING MECHANISMS Prof. Sandro Brunelli, Ph.D. brunelli@economia.uniroma2.it BUSINESS ACTIVITIES AND FINANCIAL STATEMENT ELEMENTS Business Activities

Department of Management and Law CHAPTER 2: FINANCIAL REPORTING MECHANISMS Prof. Sandro Brunelli, Ph.D. brunelli@economia.uniroma2.it BUSINESS ACTIVITIES AND FINANCIAL STATEMENT ELEMENTS Business Activities

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

FORENSIC ACCOUNTING VERSION

FORENSIC ACCOUNTING VERSION Fraudulent or incorrect transactions are presented below. Your job as a forensic accountant is to correct the financial statements and determine how income and total assets

FORENSIC ACCOUNTING VERSION Fraudulent or incorrect transactions are presented below. Your job as a forensic accountant is to correct the financial statements and determine how income and total assets

- A resource - Controlled by the entity - As a result of a past event - From economic benefits are expected to flow to the entity.

Elements and recognition criteria 1. Identify the definition for each of these elements: a. Assets b. Liabilities c. Equity d. Income e. Expenses - A resource - Controlled by the entity - As a result of

Elements and recognition criteria 1. Identify the definition for each of these elements: a. Assets b. Liabilities c. Equity d. Income e. Expenses - A resource - Controlled by the entity - As a result of

Chapter 2 Review of the Accounting Process

Intermediate Accounting 8th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-8th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 8th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-8th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

2014 Mar. 31 Balance 30, Adjusting 26 22,500 7, Mar. 31 Balance 3, Adjusting 26 1,800 1,800

Prob. 4 4A 1., 3., and 6. Cash Account No. 11 Mar. 31 12,000 Supplies Account No. 13 Mar. 31 30,000 31 Adjusting 26 22,500 7,500 Prepaid Insurance Account No. 14 Mar. 31 3,600 31 Adjusting 26 1,800 1,800

Prob. 4 4A 1., 3., and 6. Cash Account No. 11 Mar. 31 12,000 Supplies Account No. 13 Mar. 31 30,000 31 Adjusting 26 22,500 7,500 Prepaid Insurance Account No. 14 Mar. 31 3,600 31 Adjusting 26 1,800 1,800

The Accounting Cycle Accruals and Deferrals

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

Chapter 2 Review of the Accounting Process

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM. MULTIPLE CHOICE Conceptual. Test Bank Chapter 3

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM MULTIPLE CHOICE Conceptual Answer No. Description d 1. Purpose of an accounting system. d 2. Criteria for recording events. c 3. Purpose of trial balance. b

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM MULTIPLE CHOICE Conceptual Answer No. Description d 1. Purpose of an accounting system. d 2. Criteria for recording events. c 3. Purpose of trial balance. b

SOLUTIONS. Learning Goal 14

S1 Learning Goal 14 Multiple Choice 1. a 2. c The capital balance to use on the balance sheet is the final balance from the statement of owner s equity. The capital balance showing on the worksheet does

S1 Learning Goal 14 Multiple Choice 1. a 2. c The capital balance to use on the balance sheet is the final balance from the statement of owner s equity. The capital balance showing on the worksheet does

A. II. B. I. III. A. B.

II. A. B. I. III. A. B. Adjusting the Accounts Chapters 3 and 4 "Cash" Basis vs. "Accrual" Basis: Cash Accrual Revenue Expenses Generally Accepted Accounting Principles (GAAP) require using the basis.

II. A. B. I. III. A. B. Adjusting the Accounts Chapters 3 and 4 "Cash" Basis vs. "Accrual" Basis: Cash Accrual Revenue Expenses Generally Accepted Accounting Principles (GAAP) require using the basis.

Full file at Chapter 02 - Solutions to Exercises - Series A

SOLUTIONS TO EXERCISES - SERIES A - CHAPTER 2 EXERCISE 2-1A Horizontal Statements Model Stock. Equity Type of Com. Ret. Net Cash Even t Event Asset s = Liab. + Stock + Earn. Rev. Exp. = Inc. Flows a. AS

SOLUTIONS TO EXERCISES - SERIES A - CHAPTER 2 EXERCISE 2-1A Horizontal Statements Model Stock. Equity Type of Com. Ret. Net Cash Even t Event Asset s = Liab. + Stock + Earn. Rev. Exp. = Inc. Flows a. AS

SOLUTIONS. Learning Goal 13

S1 Learning Goal 13 Multiple Choice 1. b 2. c 3. c 4. b 5. c 6. a 7. b 8. d Whatever the beginning balance was in the Prepaid Insurance account, plus the insurance that was purchased during the period,

S1 Learning Goal 13 Multiple Choice 1. b 2. c 3. c 4. b 5. c 6. a 7. b 8. d Whatever the beginning balance was in the Prepaid Insurance account, plus the insurance that was purchased during the period,

Chapter 3 the Adjusting Process. Learning Objective 1 Describe the nature of the adjusting process.

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

After completing Chapter 2, your students should be able to answer these questions:

Solution Manual for Financial Accounting A Business Process Approach 3rd Edition by Reimers Link full download solution manual: http://testbankcollection.com/download/solution-manual-for-financial-accountinga-business-process-approach-3rd-edition-by-reimers/

Solution Manual for Financial Accounting A Business Process Approach 3rd Edition by Reimers Link full download solution manual: http://testbankcollection.com/download/solution-manual-for-financial-accountinga-business-process-approach-3rd-edition-by-reimers/

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES INVESTING ACTIVITIES FINANCING ACTIVITIES

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

CHAPTER3 Adjusting the Accounts

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

Business Background Management is responsible for preparing...

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Chapter 1. assembled and processed

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

1 Introduction to Accounting and Business Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature

Learning Module 5 Time Value of Money & Hodgepodge of Other Stuff

Learning Module 5 Time Value of Money & Hodgepodge of Other Stuff The Concept of Future Value If you have $100 today and put it in the bank, how much will you have in the future? In order to put this concept

Learning Module 5 Time Value of Money & Hodgepodge of Other Stuff The Concept of Future Value If you have $100 today and put it in the bank, how much will you have in the future? In order to put this concept

CHAPTER 4 EXERCISES: SET B. E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows.

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 5 Adjusting Entries and the Trial Balance Chapter 4 Adjusting entries Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this

ACC100 Introduction to Accounting Week 5 Adjusting Entries and the Trial Balance Chapter 4 Adjusting entries Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning Outcomes On completion of this

The Accounting Cycle: Accruals and Deferrals

The Accounting Cycle: Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Adjusting Entries Adjusting entries are needed whenever revenue

The Accounting Cycle: Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Adjusting Entries Adjusting entries are needed whenever revenue

4. A They increase retained earnings in the shareholders equity section. This is why we always credit revenues.

www.liontutors.com ACCTG 211 Exam 1 Practice Exam Solutions 1. B Historical cost 2. (1) Analyze transactions and create journal entries, (2) poster journal entries to ledger accounts, (3) Balance ledger

www.liontutors.com ACCTG 211 Exam 1 Practice Exam Solutions 1. B Historical cost 2. (1) Analyze transactions and create journal entries, (2) poster journal entries to ledger accounts, (3) Balance ledger

Chapter 02. Accounting for Accruals and Deferrals. Short Answer Questions

Chapter 02 Accounting for Accruals and Deferrals Short Answer Questions 1. Indicate how each event affects the elements of financial statements. Use the following letters to record your answer in the box

Chapter 02 Accounting for Accruals and Deferrals Short Answer Questions 1. Indicate how each event affects the elements of financial statements. Use the following letters to record your answer in the box

Unit five: Adjusting the accounts Accruals and Prepayments

Unit five: Adjusting the accounts Accruals and Prepayments اسم الطالب:... رقم الطالب:... الصف:... المدرسة:... الرقم التسلسلي Uploaded By: Ayman Ayyad (Danger3) Prepare by T. Abdul Jalil Alaiwi Uploaded

Unit five: Adjusting the accounts Accruals and Prepayments اسم الطالب:... رقم الطالب:... الصف:... المدرسة:... الرقم التسلسلي Uploaded By: Ayman Ayyad (Danger3) Prepare by T. Abdul Jalil Alaiwi Uploaded

The Adjustment Process and Financial Statements Irwin/McGraw-Hill

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Learning Outcomes. The Basic Accounting Cycle

Chapter 2: Review of the Accounting Process Part 3: Accounting Cycle with Emphasis on Year End Activities Intermediate Accounting 1 Dr. Chula King Learning Outcomes After completing this part, you should

Chapter 2: Review of the Accounting Process Part 3: Accounting Cycle with Emphasis on Year End Activities Intermediate Accounting 1 Dr. Chula King Learning Outcomes After completing this part, you should

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

CHAPTER 8 REVIEW EXERCISES (continued) Exercise 7, p. 326 A. Year Ended December 31, 20 8 BALANCE SHEET INCOME STATEMENT ADJUSTMENTS TRIAL BALANCE

Exercise 7, p. 326 A. Year Ended December 31, 20 8 BALANCE SHEET INCOME STATEMENT ADJUSTMENTS TRIAL BALANCE") Exercise 7, p. 326 A. Oakville Journal Worksheet Year Ended December, 28 TRIAL BALANCE ACCOUNTS ADJUSTMENTS INCOME STATEMENT BALANCE SHEET Bank Accounts Receivable Prepaid Insurance Land Buildings Acc.

Exercise 7, p. 326 A. Oakville Journal Worksheet Year Ended December, 28 TRIAL BALANCE ACCOUNTS ADJUSTMENTS INCOME STATEMENT BALANCE SHEET Bank Accounts Receivable Prepaid Insurance Land Buildings Acc.

Chapter 4: Completing the Accounting Cycle. Learning Objective 2 Prepare financial statements from adjusted account balances.

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

QUESTION 2 IAS 1 (CAF5 A15) Following is the summarised trial balance of Eagles Limited (EL) as at 30 June 2015: Debit Rs. in 000

Following is the summarised trial balance of Eagles Limited (EL) as at 30 June 2015: Debit Rs. in 000") QUESTION 2 IAS 1 (CAF5 A15) Following is the summarised trial balance of Eagles Limited (EL) as at 30 June 2015: Debit Credit Plant 2,500 Acc. depreciation at 1 July 2014 Equipment 700 Plant 1,000 Stock

QUESTION 2 IAS 1 (CAF5 A15) Following is the summarised trial balance of Eagles Limited (EL) as at 30 June 2015: Debit Credit Plant 2,500 Acc. depreciation at 1 July 2014 Equipment 700 Plant 1,000 Stock

download from https://testbankgo.eu/p/

CHAPTER 3 ADJUSTING THE ACCOUNTS SUMMARY OF QUESTIONS BY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 C 9. 2 C 17. 5 C 25. 5 K 33. 3

CHAPTER 3 ADJUSTING THE ACCOUNTS SUMMARY OF QUESTIONS BY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 C 9. 2 C 17. 5 C 25. 5 K 33. 3

MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3)

") MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following statement shows the revenues and expenses of the

MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following statement shows the revenues and expenses of the

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4)

") MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

Chapter 4: Completing the Accounting Cycle

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

Work4Me. Algorithmic Version. Problem Six. Adjusting Entries, Closing Entries, and Financial Analysis. 1 st Web-Based Edition

Work4Me Algorithmic Version 1 st Web-Based Edition Problem Six Adjusting Entries, Closing Entries, and Financial Analysis Page 1 Emory Legal Services, Incorporated CHART OF ACCOUNTS Problem 6 ASSETS REVENUE

Work4Me Algorithmic Version 1 st Web-Based Edition Problem Six Adjusting Entries, Closing Entries, and Financial Analysis Page 1 Emory Legal Services, Incorporated CHART OF ACCOUNTS Problem 6 ASSETS REVENUE

Solution to Problem 11 Classify items for different statements. Solution to Problem 12 Classify items for different statements.

Solution to Problem 11 Classify items for different statements. The following items are found on financial statements. Identify each as BS (balance sheet), IS.{income statement), CF (statement of cash

Solution to Problem 11 Classify items for different statements. The following items are found on financial statements. Identify each as BS (balance sheet), IS.{income statement), CF (statement of cash

Some deferred items for which adjusting entries would be made include: Prepaid insurance Prepaid rent Office supplies Depreciation Unearned revenue

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

ACCT1006 Notes TYPES OF FINANCIAL STATEMENTS

ACCT1006 Notes TYPES OF FINANCIAL STATEMENTS - 4 financial statements o Statement of changes in equity Changes in OE s capital, reserves, and earnings How aspects in OE change over the period o Statement

ACCT1006 Notes TYPES OF FINANCIAL STATEMENTS - 4 financial statements o Statement of changes in equity Changes in OE s capital, reserves, and earnings How aspects in OE change over the period o Statement

Measurement Fundamentals BUS 210. Chapter 3

Measurement Fundamentals BUS 210 Chapter 3 What do you know? Financial Accounting Fundamentals Valuation Input Market (purchase)-original, replacement Output Market (sell)-present, fair market Financial

Measurement Fundamentals BUS 210 Chapter 3 What do you know? Financial Accounting Fundamentals Valuation Input Market (purchase)-original, replacement Output Market (sell)-present, fair market Financial

ACC 131 Finals Blitz

ACC 131 Finals Blitz Note: This is just an overview of some key topics to understand. This is NOT a comprehensive list. Please consult your professor and/or class syllabus for more information on what

ACC 131 Finals Blitz Note: This is just an overview of some key topics to understand. This is NOT a comprehensive list. Please consult your professor and/or class syllabus for more information on what

BODORP (Pty) Ltd's STATEMENT of FINANCIAL POSITION as at eoy 20X5

Ltd's STATEMENT of FINANCIAL POSITION as at eoy 20X5") Aufgabe QR-10.10: Direkte Methode mit Vergleich von Ein- und Auszahlungen (Direct Method with Comparison of Cash Inflow and Cash Outflow) BODORP (Pty) Ltd is a marketing consultancy. The company has 10

Aufgabe QR-10.10: Direkte Methode mit Vergleich von Ein- und Auszahlungen (Direct Method with Comparison of Cash Inflow and Cash Outflow) BODORP (Pty) Ltd is a marketing consultancy. The company has 10

Exhibit 1: Trial balance. You are the accountant of GUGULETO Ltd. and have to make bookkeeping entries for the adjustments.

Aufgabe 0.13: Trial Balance The pizza restaurant GUGULETO Ltd. was formed on 1.01.20X3 and records during the accounting period of 20X3 all bookkeeping entries. The business is a limited company and comes

Aufgabe 0.13: Trial Balance The pizza restaurant GUGULETO Ltd. was formed on 1.01.20X3 and records during the accounting period of 20X3 all bookkeeping entries. The business is a limited company and comes

3. Balance sheet accounts are referred to as temporary accounts because their balances are always changing.

Chapter 02 Review of the Accounting Process True / False Questions 1. Owners' equity can be expressed as assets minus liabilities. True False 2. Debits increase asset accounts and decrease liability accounts.

Chapter 02 Review of the Accounting Process True / False Questions 1. Owners' equity can be expressed as assets minus liabilities. True False 2. Debits increase asset accounts and decrease liability accounts.

Module 3 Exhibits and Key Terms. Table of Contents. 1 Principles of Accounting Adjustments for Financial Reporting

Table of Contents Exhibit 14: Cash basis and accrual basis of accounting compared... 2 Exhibit 15: Summary fiscal year ending by Month... 2 Exhibit 16: Two classes and four types of adjusting entries...

Table of Contents Exhibit 14: Cash basis and accrual basis of accounting compared... 2 Exhibit 15: Summary fiscal year ending by Month... 2 Exhibit 16: Two classes and four types of adjusting entries...

Statement of Cash Flows. Barry M Frohlinger

Statement of Cash Flows Barry M Frohlinger Statement of Cash Flows Page 1 Barry M Frohlinger, Inc. copyright 1981-2010 Companies are required to present a Statement of Cash Flows (cash statement) for each

Statement of Cash Flows Barry M Frohlinger Statement of Cash Flows Page 1 Barry M Frohlinger, Inc. copyright 1981-2010 Companies are required to present a Statement of Cash Flows (cash statement) for each

The Accounting Cycle. End of the Period C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

Section 13 Liabilities

15-1 Section 13 Liabilities Probable future sacrifices of economic benefits. Arise from present obligations to other entities. Result from past transactions or events. What is a Current Liability? 15-2

15-1 Section 13 Liabilities Probable future sacrifices of economic benefits. Arise from present obligations to other entities. Result from past transactions or events. What is a Current Liability? 15-2

ENTRIES MADE PRIOR TO CLOSING

ENTRIES MADE PRIOR TO CLOSING There are a few entries that should be done before the end of the fiscal year that will make the closing process a little smoother. Included are some examples for your reference.

ENTRIES MADE PRIOR TO CLOSING There are a few entries that should be done before the end of the fiscal year that will make the closing process a little smoother. Included are some examples for your reference.

Section A: Multiple-Choice Questions (2 marks each; Total 30 marks)

") Name: Student ID: Section A: Multiple-Choice Questions (2 marks each; Total 30 marks) Choose the one best answer. 1. The accounting process involves all of the following except ( d ) a. identifying economic

Name: Student ID: Section A: Multiple-Choice Questions (2 marks each; Total 30 marks) Choose the one best answer. 1. The accounting process involves all of the following except ( d ) a. identifying economic

Introduction to Financial Accounting

Solutions Manual to Accompany Introduction to Financial Accounting Third Edition (v. 3.1) Based on International Financial Reporting Standards David Annand Copyright 2018 David Annand Published by David

Solutions Manual to Accompany Introduction to Financial Accounting Third Edition (v. 3.1) Based on International Financial Reporting Standards David Annand Copyright 2018 David Annand Published by David

Chapter 7. Funds Analysis, Cash- Flow Analysis, and Financial Planning

Chapter 7 Funds Analysis, Cash- Flow Analysis, and Financial Planning 7-1 Pearson Education Limited 2004 Fundamentals of Financial Management, 12/e Created by: Gregory A. Kuhlemeyer, Ph.D. Carroll College,

Chapter 7 Funds Analysis, Cash- Flow Analysis, and Financial Planning 7-1 Pearson Education Limited 2004 Fundamentals of Financial Management, 12/e Created by: Gregory A. Kuhlemeyer, Ph.D. Carroll College,

REVIEW Which of the following would be classified as external users of financial statements?

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

Chapter 12 - Reporting and Analyzing Cash Flows. Chapter Outline

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

4/9/2012. Accrual Accounting and Financial Statements. Learning Objectives (LO) LO 1 - Adjustments to the Accounts. Learning Objectives (LO)

LO 1 - Adjustments to the Accounts. Learning Objectives (LO)") Accrual Accounting and Financial s CHAPTER 4 Learning Objectives (LO) After studying this chapter, you should be able to 1. Understand the role of adjustments in accrual accounting 2. Make adjustments

Accrual Accounting and Financial s CHAPTER 4 Learning Objectives (LO) After studying this chapter, you should be able to 1. Understand the role of adjustments in accrual accounting 2. Make adjustments

Chapter 3. Learning Objectives. Distinguish accrual accounting from cash-basis accounting. Objective 1. The Adjusting Process

PowerPoint to accompany Chapter 3 The Adjusting Process Learning Objectives 1. Distinguish accrual accounting from cash-basis accounting. 2. Make adjusting entries at the end of the accounting period.

PowerPoint to accompany Chapter 3 The Adjusting Process Learning Objectives 1. Distinguish accrual accounting from cash-basis accounting. 2. Make adjusting entries at the end of the accounting period.

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

LEASES UPDATE. Marty D. Van Wagoner, CPA Partner, Mountainside Accounting & Consulting Professional in Residence Faculty, Utah Valley University

LEASES UPDATE Marty D. Van Wagoner, CPA Partner, Mountainside Accounting & Consulting Professional in Residence Faculty, Utah Valley University Scope and Definition Embedded leases in service agreements

LEASES UPDATE Marty D. Van Wagoner, CPA Partner, Mountainside Accounting & Consulting Professional in Residence Faculty, Utah Valley University Scope and Definition Embedded leases in service agreements

ANSWER ALL MULTIPLE CHOICE ON YOUR SCANTRON AND WRITE YOUR TEST COLOR ON THE SCANTRON.

Name: Perm # TEST VERSION: A Class: Date: ANSWER ALL MULTIPLE CHOICE ON YOUR SCANTRON AND WRITE YOUR TEST COLOR ON THE SCANTRON. THERE IS ONLY ONE PROBLEM-- ANSWER IT IN THE SPACE PROVIDED ON THIS EXAM.

Name: Perm # TEST VERSION: A Class: Date: ANSWER ALL MULTIPLE CHOICE ON YOUR SCANTRON AND WRITE YOUR TEST COLOR ON THE SCANTRON. THERE IS ONLY ONE PROBLEM-- ANSWER IT IN THE SPACE PROVIDED ON THIS EXAM.

Chapter 2 Review of the Accounting Process

True/False Questions 1. Owners' equity can be expressed as assets minus liabilities. True Learning Objective: 1 Level of Learning: 1 2. Debits increase asset accounts and decrease liability accounts. True

True/False Questions 1. Owners' equity can be expressed as assets minus liabilities. True Learning Objective: 1 Level of Learning: 1 2. Debits increase asset accounts and decrease liability accounts. True

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson. The statement of cash flows is a required component of financial statements.

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson The statement of cash flows is a required component of financial statements. BASICS OF CASH FLOW REPORTING Purpose of the Statement

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson The statement of cash flows is a required component of financial statements. BASICS OF CASH FLOW REPORTING Purpose of the Statement

Work4Me I Accounting Simulations. Problem Four

Work4Me I Accounting Simulations 3 rd Web-Based Edition Problem Four Daily and Adjusting Entries for Classic Accounting Services, Incorporated Page 1 Problem Four Classic Accounting Services, Inc. Trial

Work4Me I Accounting Simulations 3 rd Web-Based Edition Problem Four Daily and Adjusting Entries for Classic Accounting Services, Incorporated Page 1 Problem Four Classic Accounting Services, Inc. Trial

PORT EVERGLADES DEPARTMENT of Broward County, Florida Statements of Net Position March 31, 2016 and 2015 (Unaudited) (Dollars in Thousands)

(Dollars in Thousands)") Statements of Net Position March 31, 2016 and 2015 (Unaudited) ASSETS Current Assets Unrestricted assets Cash and cash equivalents $ 17,954 $ 14,339 Investments 223,700 214,935 Accounts receivable, trade

Statements of Net Position March 31, 2016 and 2015 (Unaudited) ASSETS Current Assets Unrestricted assets Cash and cash equivalents $ 17,954 $ 14,339 Investments 223,700 214,935 Accounts receivable, trade

Chapter 3: Accrual Accounting Basics

Chapter 3: Accrual Accounting Basics Revenues are recognized when resources are created as part of the organization's operating activities. Expenses are recognized when resources are consumed as part of

Chapter 3: Accrual Accounting Basics Revenues are recognized when resources are created as part of the organization's operating activities. Expenses are recognized when resources are consumed as part of

Solution to Problem 31 Adjusting entries. Solution to Problem 32 Closing entries.

Solution to Problem 31 Adjusting entries. 1. Utilities expense 27,000 Accounts payable 27,000 2. Rent revenue 4,000 Unearned revenue 4,000 3. Supplies 2,000 Supplies expense 2,000 4. Interest receivable

Solution to Problem 31 Adjusting entries. 1. Utilities expense 27,000 Accounts payable 27,000 2. Rent revenue 4,000 Unearned revenue 4,000 3. Supplies 2,000 Supplies expense 2,000 4. Interest receivable

Your gateway to the world of accounting 1

Your gateway to the world of accounting 1 Accounting 212 Explain all the lessons of Accounting 212 for the third grade of secondary Ayman Ayyad Students-BH.com 2012 1 Index No. Lesson Title Page 1 Index

Your gateway to the world of accounting 1 Accounting 212 Explain all the lessons of Accounting 212 for the third grade of secondary Ayman Ayyad Students-BH.com 2012 1 Index No. Lesson Title Page 1 Index