Completing the Accounting Cycle

|

|

|

- Tyrone Davidson

- 5 years ago

- Views:

Transcription

1 4 Completing the Accounting Cycle 4-1

2 Closing the Books At the end of the accounting period, the company gets the accounts ready for the next period. Very similar to what happens at AHS at the end of a marking period 4-2

3 Closing the Books Closing entries formally recognize, in the general ledger, the transfer of net income (or net loss) and owner s drawing to owner s capital. Closing entries are only at the end of the annual accounting period. 4-3

4 Journalizing and Posting Closing entries must be journalized and posted; it s a required step in the accounting cycle. Temporary revenue and expense accounts are closed to Income Summary The temporary account Owner s Drawing is closed directly to Owner s Equity 4-4

5 4-5 Closing the Books

6 Closing the Books Picture the number of revenue and expense accounts a company could have. If each one was closed directly to Owner s Equity, the OE account would be quite messy and confusing! To keep it clean and neat, we use a temporary account called Income Summary to minimize the amount of detail in the permanent OE account. 4-6

7 Closing the Books (this slide is in your notes) Note: Owner s Drawing is closed directly to Capital and not to Income Summary because Owner s Drawing is not an expense. Owner s Capital is a permanent account; all other accounts are temporary accounts. 4-7

8 Closing the Books (this slide is in your notes) Illustration 4-7 Closing entries journalized Closing Entries need to be Posted 4-8

9 Preparing a Post- Closing Trial Balance Purpose is to prove the equality of the permanent account balances after journalizing and posting of closing entries. Temporary accounts will have zero balances. 4-9

10 Summary of the Accounting Cycle 1. Analyze business transactions Illustration Prepare a post-closing trial balance 2. Journalize the transactions 8. Journalize and post closing entries 3. Post to ledger accounts 7. Prepare financial statements 4. Prepare a trial balance 6. Prepare an adjusted trial balance 5. Journalize and post adjusting entries 4-10

11 Financial Statements We need to quantify our results for the accounting period in question. Sometimes, we need to report to investors or other stakeholders. We do this by creating Financial Statements: Balance Sheet; Statement of Owner s Equity; Income Statement 4-11

12 The Classified Balance Sheet Presents a snapshot at a point in time. To improve understanding, companies group similar assets and similar liabilities together. Standard Classifications Assets Current assets Long-term investments Property, plant, and equipment Intangible assets Illustration 4-17 Liabilities and Owner s Equity Current liabilities Long-term liabilities Owner s (Stockholders ) equity 4-12

13 The Classified Balance Sheet Current Assets Assets that a company expects to convert to cash or use up within one year or the operating cycle, whichever is longer. Operating cycle is the average time it takes from the purchase of inventory to the collection of cash from customers Current assets are listed in order of liquidity (the ease with which they can be turned into cash)

14 The Classified Balance Sheet Current Assets Illustration 4-19 Companies usually list current asset accounts in the order they can convert them into cash. 4-14

15 The Classified Balance Sheet Long-Term Investments Investments in stocks and bonds of other companies. 4-15

16 The Classified Balance Sheet Property, Plant, and Equipment Assets with long useful lives, currently used in operations. Remember that Depreciation is allocating the cost of assets to a number of years, and Accumulated depreciation is the total amount of depreciation expensed thus far in the asset s life. 4-16

17 The Classified Balance Sheet Property, Plant, and Equipment Illustration

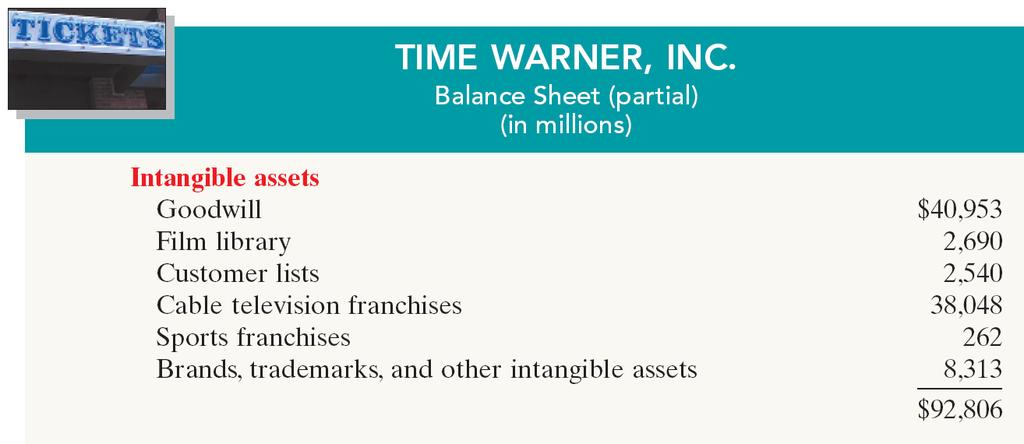

18 The Classified Balance Sheet Intangible Assets Assets with no physical substance, but can be very valuable. 4-18

19 4-19

20 The Classified Balance Sheet Current Liabilities Obligations the company is to pay within the coming year. Usually list notes payable first, followed by accounts payable. Other items follow in order of magnitude. Liquidity - ability to pay obligations expected to be due within the next year. 4-20

21 The Classified Balance Sheet Current Liabilities 4-21

22 The Classified Balance Sheet Long-Term Liabilities Obligations a company expects to pay after one year. 4-22

23 The Classified Balance Sheet Owner s Equity Proprietorship - one capital account. Partnership - capital account for each partner. Corporation it s called Stockholders Equity and consists of 2 accounts: Capital Stock & Retained Earnings. 4-23

24 The Classified Balance Sheet Balance Sheet Form Usually in Report Form, with assets above the liabilities and owner s equity Sometimes in Account Form, with assets section on the left and Liabilities & Owner s Equity on the right 4-24

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

Learning Objective. LO1 Prepare an income statement for a merchandising business organized as a corporation.

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Learning Objectives. LO1 Journalize and post closing entries for a service business organized as a proprietorship.

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

Curriculum Document for Business Education

Curriculum Document for Business Education Course Title: Accounting I Learner Objective #1: Students will learn the accounting equation and how business activities change the accounting equation. Identify

Curriculum Document for Business Education Course Title: Accounting I Learner Objective #1: Students will learn the accounting equation and how business activities change the accounting equation. Identify

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE LEARNING OBJECTIVES 1. PREPARE A WORKSHEET. 2. EXPLAIN THE PROCESS OF CLOSING THE BOOKS. 3. DESCRIBE THE CONTENT AND PURPOSE OF A POST-CLOSING TRIAL BALANCE. 4.

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE LEARNING OBJECTIVES 1. PREPARE A WORKSHEET. 2. EXPLAIN THE PROCESS OF CLOSING THE BOOKS. 3. DESCRIBE THE CONTENT AND PURPOSE OF A POST-CLOSING TRIAL BALANCE. 4.

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

Bixby Public Schools Essential Elements Grade: 10-12

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

Chapter 6 The annual report and accounts. The closure of the accounting cycle and Accounting information disclosed to the public

Chapter 6 The annual report and accounts The closure of the accounting cycle and Accounting information disclosed to the public 1 Six steps in the accounting cycle 1. Analyze transactions from the source

Chapter 6 The annual report and accounts The closure of the accounting cycle and Accounting information disclosed to the public 1 Six steps in the accounting cycle 1. Analyze transactions from the source

Financial Statements and Closing Entries for a Merchandising Business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Chapter 4: Posting from a General Journal to a General Ledger

Chapter 4: Posting from a General Journal to a General Ledger Goals of Chapter 4: Define accounting terms related to posting form a general journal to a general ledger Identify accounting concepts and

Chapter 4: Posting from a General Journal to a General Ledger Goals of Chapter 4: Define accounting terms related to posting form a general journal to a general ledger Identify accounting concepts and

Chapter 4: Completing the Accounting Cycle

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

Accounting 1. Lesson Plan. Name: Terry Wilhelmi Day/Date:

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Financial Statements and End-of-Fiscal-Period Entries Unit: 4 Chapter 27 for a Corporation I. Objective(s): By the end of today s lesson,

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Financial Statements and End-of-Fiscal-Period Entries Unit: 4 Chapter 27 for a Corporation I. Objective(s): By the end of today s lesson,

4-1 COMPLETING THE ACCOUNTING CYCLE

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

Chapter 4 Completing the Accounting Cycle 高立翰

Chapter 4 Completing the Accounting Cycle 高立翰 Study Objectives 1. Prepare a worksheet. 2. Explain the process of closing the books. 3. Describe the content and purpose of a postclosing trial balance. 4.

Chapter 4 Completing the Accounting Cycle 高立翰 Study Objectives 1. Prepare a worksheet. 2. Explain the process of closing the books. 3. Describe the content and purpose of a postclosing trial balance. 4.

Disclaimer: This resource package is for studying purposes only EDUCATON

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Accounting 1. Lesson Plan. Topic: Distributing Dividends and Preparing a Work Sheet for a Unit: 4 Chapter 26 Corporation

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Distributing Dividends and Preparing a Work Sheet for a Unit: 4 Chapter 26 Corporation I. Objective(s): By the end of today s lesson, the

Accounting 1 Lesson Plan Name: Terry Wilhelmi Day/Date: Topic: Distributing Dividends and Preparing a Work Sheet for a Unit: 4 Chapter 26 Corporation I. Objective(s): By the end of today s lesson, the

Let s look at how the term is used. Chapter 2 Granof-4e 3

Chapter 2 1 Chapter 2 2 Let s look at how the term is used Chapter 2 Granof-4e 3 May refer to working capital (current net assets) May refer to cash or investments available (bond sinking fund) May have

Chapter 2 1 Chapter 2 2 Let s look at how the term is used Chapter 2 Granof-4e 3 May refer to working capital (current net assets) May refer to cash or investments available (bond sinking fund) May have

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

Module 4. Instructions:

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Accounting for. Sole Proprietorship. 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

appendix F Accounting for Sole Proprietorships study objectives After studying this appendix, you should be able to: 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

appendix F Accounting for Sole Proprietorships study objectives After studying this appendix, you should be able to: 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

LESSON 8-1. Recording Adjusting Entries. CENTURY 21 ACCOUNTING Thomson/South-Western

LESSON 8-1 Recording Adjusting Entries 2 TERM REVIEW page 205 Adjusting Entries journal entries recorded to update general ledger accounts at the end of a fiscal period Adjustments must be journalized

LESSON 8-1 Recording Adjusting Entries 2 TERM REVIEW page 205 Adjusting Entries journal entries recorded to update general ledger accounts at the end of a fiscal period Adjustments must be journalized

ACCOUNTING STATE COMPETENCY TEST REVIEW

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

ACCOUNTING STATE COMPETENCY TEST REVIEW Source Documents Documents that are analyzed to determine what happened in a transaction Memorandum a note written by the company when there is no other source document

Chapter 3 Question Review 1

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Fundamentals of Finance and Accounting for Nonfinancial Managers

Fundamentals of Finance and Accounting for Nonfinancial Managers Third Edition Robert C. Waehler Anthony J. Matias Michael P. Griffin Contents About This Course How to Take This Course xi xiii 1 Introduction

Fundamentals of Finance and Accounting for Nonfinancial Managers Third Edition Robert C. Waehler Anthony J. Matias Michael P. Griffin Contents About This Course How to Take This Course xi xiii 1 Introduction

Chapter 6: Worksheets for a Service Business

Chapter 6: Worksheets for a Service Business Goals of Chapter 6: Define accounting terms related to a worksheet for a service business organized as a proprietorship Identify accounting concepts and practices

Chapter 6: Worksheets for a Service Business Goals of Chapter 6: Define accounting terms related to a worksheet for a service business organized as a proprietorship Identify accounting concepts and practices

Chapter 4: Completing the Accounting Cycle. Learning Objective 2 Prepare financial statements from adjusted account balances.

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

The Accounting Cycle. End of the Period C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

UNDERSTANDING FINANCIAL STATEMENTS, TAXES, AND CASH FLOWS. Chapter 3

1 UNDERSTANDING FINANCIAL STATEMENTS, TAXES, AND CASH FLOWS Chapter 3 2 Learning Objectives (1 of 2) 1. Describe the content of the four basic financial statements and discuss the importance of financial

1 UNDERSTANDING FINANCIAL STATEMENTS, TAXES, AND CASH FLOWS Chapter 3 2 Learning Objectives (1 of 2) 1. Describe the content of the four basic financial statements and discuss the importance of financial

Chapter 4. The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Full file at

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

CHAPTER 4 EXERCISES: SET B. E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows.

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

FBLA Accounting I Practice Test 2004

FBLA Accounting I Practice Test 2004 True/False Indicate whether the sentence or statement is true or false. 1. When a business uses a petty cash fund, the fund is debited each time it is replaced. 2.

FBLA Accounting I Practice Test 2004 True/False Indicate whether the sentence or statement is true or false. 1. When a business uses a petty cash fund, the fund is debited each time it is replaced. 2.

CHAPTER 2 QUESTIONS. revenue, and expense accounts of the

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

CHAPTER 2 QUESTIONS 1. The accounting system generates a variety of reports for use by various decision makers. Among the most common are generalpurpose financial statements, management reports, tax returns,

Learning Objectives. LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet.

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

ACCOUNTING SEMESTER 1. Final Exam Review

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities

ACCOUNTING SEMESTER 1 Final Exam Review 1 ACCOUNTING SEMESTER 1 30 T & F 70 MC Questions with pictures 5-Worksheet 6-Journals 3-Cash Payment Journal 2 CHAPTER 1 What is the accounting equation? Assets=Liabilities

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Total Test Questions: 57 Levels: Grades Units of Credit:.50

DESCRIPTION Students will develop advanced skills that build upon those acquired in Accounting I. Students continue applying concepts of double-entry accounting systems related to merchandising businesses.

DESCRIPTION Students will develop advanced skills that build upon those acquired in Accounting I. Students continue applying concepts of double-entry accounting systems related to merchandising businesses.

Accounting Glossary 1. an equation showing the relationship among assets, liabilities, and

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

ACCT Introduction to Accounting Chapter 6 - Closing Entries and the Post Closing Trial Balance Prof. Johnson

ACCT 100 - Introduction to Accounting Chapter 6 - Closing Entries and the Post Closing Trial Balance Prof. Johnson Purpose: The purpose of this handout is to summarize key concepts of Chapter 6. This represents

ACCT 100 - Introduction to Accounting Chapter 6 - Closing Entries and the Post Closing Trial Balance Prof. Johnson Purpose: The purpose of this handout is to summarize key concepts of Chapter 6. This represents

Exercises. 2) Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities

Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities") Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

2. Which of the following is an external user of accounting information? A) Labor unions. B) Finance directors. C) Company officers. D) Managers.

Labor unions. B) Finance directors. C) Company officers. D) Managers.") Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

Module 4. Table of Contents

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

FUNDAMENTAL ACCOUNTING (100) Secondary

Secondary") Page 1 of 12 FUNDAMENTAL ACCOUNTING (100) Secondary REGIONAL 2015 Multiple Choice & Short Answer Section: Contestant Number: Time: Rank: Multiple Choice (25 @ 2 points each) Account Classification (10

Page 1 of 12 FUNDAMENTAL ACCOUNTING (100) Secondary REGIONAL 2015 Multiple Choice & Short Answer Section: Contestant Number: Time: Rank: Multiple Choice (25 @ 2 points each) Account Classification (10

Investing and Financing Decisions and the Accounting System

Investing and Financing Decisions and the Accounting System Chapter 2 Conceptual Framework Objective of Financial Reporting To provide useful economic information to external users for decision making

Investing and Financing Decisions and the Accounting System Chapter 2 Conceptual Framework Objective of Financial Reporting To provide useful economic information to external users for decision making

Chapter 8. Recording Adjusting and Closing Entries

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Accounting 1A Class Notes Chapter 3 The Adjusting Process

Source Documents General Journal General Ledger Trial Balance Adjusting Entries Difference between TRANSACTIONS and ADJUSTMENTS Transactions occur through-out the accounting cycle and normally involve

Source Documents General Journal General Ledger Trial Balance Adjusting Entries Difference between TRANSACTIONS and ADJUSTMENTS Transactions occur through-out the accounting cycle and normally involve

1. The primary objective of financial reporting is to provide useful information to external decision makers.

Chapter 02 Investing and Financing Decisions and the Accounting System True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers.

Chapter 02 Investing and Financing Decisions and the Accounting System True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers.

LESSON Preparing an Income Statement. CENTURY 21 ACCOUNTING Thomson/South-Western

Preparing an Income Statement 2 Uses of Financial Statements Financial statements provide the source of information needed by owners and managers to make decisions on the future activity of a business

Preparing an Income Statement 2 Uses of Financial Statements Financial statements provide the source of information needed by owners and managers to make decisions on the future activity of a business

Financial Accounting. (Exam)

") Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Department of Recreation, Park & Tourism Administration Western Illinois University RPTA 323: Recreation Administration II Balance Sheet Overview

Department of Recreation, Park & Tourism Administration Western Illinois University RPTA 323: Recreation Administration II The basic principle of accounting is What you have minus what you owe is what

Department of Recreation, Park & Tourism Administration Western Illinois University RPTA 323: Recreation Administration II The basic principle of accounting is What you have minus what you owe is what

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4)

") MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

Accounting 303 Exam 1, Chapters 1 3 & 5 Fall 2014 Section Row

1 Accounting 303 Name Exam 1, Chapters 1 3 & 5 Fall 2014 Section Row I. Multiple Choice Questions. (2 points each, 54 points in total) Read each question carefully and indicate your answer by circling

1 Accounting 303 Name Exam 1, Chapters 1 3 & 5 Fall 2014 Section Row I. Multiple Choice Questions. (2 points each, 54 points in total) Read each question carefully and indicate your answer by circling

Unit 1 (Chapters 1-3 Question Review) 1

1") Unit 1 (Chapters 1-3 Question Review) 1 Unit 1 Exam (Chapters 1-3 Review) 1. When revenues exceed expenses, which of the following is true? a. a net income occurs b. a net loss occurs c. assets equal liabilities

Unit 1 (Chapters 1-3 Question Review) 1 Unit 1 Exam (Chapters 1-3 Review) 1. When revenues exceed expenses, which of the following is true? a. a net income occurs b. a net loss occurs c. assets equal liabilities

SENECA HIGH SCHOOL CURRICULUM MAP BUSINESS/COMPUTER EDUCATION ACCOUNTING II

UNIT 1 Accounting for Sales and Cash Receipts How do merchandising businesses keep track of what is sold and how much money is collected? How does this benefit the consumer? Accounting for a Merchandising

UNIT 1 Accounting for Sales and Cash Receipts How do merchandising businesses keep track of what is sold and how much money is collected? How does this benefit the consumer? Accounting for a Merchandising

Chapters 1-4 (Part One)

") Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

E4-E5 (Management) for BSNL internal circulation only

for BSNL internal circulation only") E4-E5 (Management) Corporate Accounts Introduction Basic understanding of finance is very relevant to our lives. Both in public and private sectors financial competence and understanding are essential

E4-E5 (Management) Corporate Accounts Introduction Basic understanding of finance is very relevant to our lives. Both in public and private sectors financial competence and understanding are essential

ACCOUNTING 201. PRACTICE MIDTERM - (Covering Chapters 1-5)

") Problem - I Multiple Choice (20 points) ACCOUNTING 201 PRACTICE MIDTERM - (Covering Chapters 1-5) 1. A private organization which establishes broad accounting principles as well as specific accounting

Problem - I Multiple Choice (20 points) ACCOUNTING 201 PRACTICE MIDTERM - (Covering Chapters 1-5) 1. A private organization which establishes broad accounting principles as well as specific accounting

The Accounting Cycle Revised Edition

Assessment The Accounting Cycle Revised Edition The objectives of this book are: To discuss record keeping systems To review the vocabulary of accounting To explain making adjusting and closing entries

Assessment The Accounting Cycle Revised Edition The objectives of this book are: To discuss record keeping systems To review the vocabulary of accounting To explain making adjusting and closing entries

FUNDAMENTAL ACCOUNTING (100) Secondary

Secondary") Page 1 of 12 FUNDAMENTAL ACCOUNTING (100) Secondary REGIONAL 2015 Multiple Choice & Short Answer Section: Contestant Number: Time: Rank: Multiple Choice (25 @ 2 points each) Account Classification (10

Page 1 of 12 FUNDAMENTAL ACCOUNTING (100) Secondary REGIONAL 2015 Multiple Choice & Short Answer Section: Contestant Number: Time: Rank: Multiple Choice (25 @ 2 points each) Account Classification (10

Full file at

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

REVIEW Which of the following would be classified as external users of financial statements?

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

Accounting 1A Class Notes Chapter 2 Analyzing Transactions. Chart of Accounts 1. Assets. Liabilities. 3. Owners Equity. Revenue. 5.

Chart of Accounts 1. Assets 2. Liabilities 3. Owners Equity 4. Revenue 5. Expense T- ACCOUNTS Title, Debit on the Left and Credit on the right Foot both sides (if more than one entry) Balance on the side

Chart of Accounts 1. Assets 2. Liabilities 3. Owners Equity 4. Revenue 5. Expense T- ACCOUNTS Title, Debit on the Left and Credit on the right Foot both sides (if more than one entry) Balance on the side

Analyzing Transactions

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

C H A P T E R 2 Analyzing Transactions QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 2. 1. Terminology is important

Accounting as a Source of Financial Information. Atanas Atanasov, Assist.prof., University of Economics - Varna

Accounting as a Source of Financial Information Atanas Atanasov, Assist.prof., University of Economics - Varna Fundamental concepts What is accounting? The language of business. A means to communicate

Accounting as a Source of Financial Information Atanas Atanasov, Assist.prof., University of Economics - Varna Fundamental concepts What is accounting? The language of business. A means to communicate

4. A They increase retained earnings in the shareholders equity section. This is why we always credit revenues.

www.liontutors.com ACCTG 211 Exam 1 Practice Exam Solutions 1. B Historical cost 2. (1) Analyze transactions and create journal entries, (2) poster journal entries to ledger accounts, (3) Balance ledger

www.liontutors.com ACCTG 211 Exam 1 Practice Exam Solutions 1. B Historical cost 2. (1) Analyze transactions and create journal entries, (2) poster journal entries to ledger accounts, (3) Balance ledger

Accounting for Merchandising Businesses

C H A P T E R 5 Accounting for Merchandising Businesses Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Operating Cycle The operating cycle is the process by which

C H A P T E R 5 Accounting for Merchandising Businesses Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Operating Cycle The operating cycle is the process by which

Nature of Business and Accounting

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

Lesson-1 BASIC CONCEPTS OF ACCOUNTING Accounting:- Accounting is the art of recording, summarizing, reporting, and analyzing financial transactions. OR Accounting is the art of recording, classifying,

Lesson-1 BASIC CONCEPTS OF ACCOUNTING Accounting:- Accounting is the art of recording, summarizing, reporting, and analyzing financial transactions. OR Accounting is the art of recording, classifying,

HS Accounting I 2013 Business and Technology

Course Description Students will learn the fundamentals and principles of double-entry accounting for service and merchandising businesses. This course focuses on financial reports along with transactions,

Course Description Students will learn the fundamentals and principles of double-entry accounting for service and merchandising businesses. This course focuses on financial reports along with transactions,

Answer: b Rationale: Journalizing means to record a transaction in a general journal.

Chapter 3 Financial Accounting, 5 th Edition by Dyckman, Hanlon, Magee, & Pfeiffer Solutions to Practice Quiz Topic: Accounting Cycle LO: 1 1. In the accounting cycle, preparing financial statements comes

Chapter 3 Financial Accounting, 5 th Edition by Dyckman, Hanlon, Magee, & Pfeiffer Solutions to Practice Quiz Topic: Accounting Cycle LO: 1 1. In the accounting cycle, preparing financial statements comes

Account Form. Used to summarize in one place all the changes to a single account A separate form for each account. Sample of a blank account form

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

DOWNLOAD PDF LIST OF DEBIT AND CREDIT ITEMS IN ACCOUNTING

Chapter 1 : Debits and Credits If the words "debits" and "credits" sound like a foreign language to you, you are more perceptive than you realizeâ "debits" and "credits" are words that have been traced

Chapter 1 : Debits and Credits If the words "debits" and "credits" sound like a foreign language to you, you are more perceptive than you realizeâ "debits" and "credits" are words that have been traced

District > Intermediate > Business Education > Accounting II ( ) (District) > Juett, David

(District) > Juett, David") Granite School District Accounting II (52.0322) (District) District > Intermediate > Business Education > Accounting II (52.0322) (District) > Juett, David Unit Essential Questions Content Skills Vocabulary

Granite School District Accounting II (52.0322) (District) District > Intermediate > Business Education > Accounting II (52.0322) (District) > Juett, David Unit Essential Questions Content Skills Vocabulary

MGT101 Financial Accounting Short Notes From Lecture No.01 to Lecture No.22 for Preparation of Midterm Exam

MGT101 Financial Accounting Short Notes From Lecture No.01 to Lecture No.22 for Preparation of Midterm Exam Lesson-1 BASIC CONCEPTS OF ACCOUNTING Accounting:- Accounting is the art of recording, summarizing,

MGT101 Financial Accounting Short Notes From Lecture No.01 to Lecture No.22 for Preparation of Midterm Exam Lesson-1 BASIC CONCEPTS OF ACCOUNTING Accounting:- Accounting is the art of recording, summarizing,

Accounting I. StraighterLine does not apply letter grades. Students earn a score as a percentage of 100%. A passing percentage is 70% or higher.

Accounting I Course Text Wild, John J., Kermit D. Larson, and Barbara Chiapetta. Fundamental Accounting Principles, Volume 1, 18th edition. McGraw-Hill/Irwin, 2007. ISBN 0-07-328661-3 Course Description

Accounting I Course Text Wild, John J., Kermit D. Larson, and Barbara Chiapetta. Fundamental Accounting Principles, Volume 1, 18th edition. McGraw-Hill/Irwin, 2007. ISBN 0-07-328661-3 Course Description

Debit and Credit Rules Module 2 part I. T- Accounts Assets = Liabilities + OE. T- Accounts: Basic Patterns A = L + OE

Debit and Credit Rules Module 2 part I Introducing T accounts Examining Account Patterns: the Increase and Decreases What s the Mystery? Debits and Credits 9/5/2005 Dr. Kathy Wigal 1 T- Accounts Assets

Debit and Credit Rules Module 2 part I Introducing T accounts Examining Account Patterns: the Increase and Decreases What s the Mystery? Debits and Credits 9/5/2005 Dr. Kathy Wigal 1 T- Accounts Assets

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 6 Closing entries and preparing financial statements Chapter 4 (p148-162); and Chapter 5 Completing the accounting cycle closing and reversing entries. Study Group

ACC100 Introduction to Accounting Week 6 Closing entries and preparing financial statements Chapter 4 (p148-162); and Chapter 5 Completing the accounting cycle closing and reversing entries. Study Group

Shared By: Hira Ali. If u like me than raise your hand with me If not than raise ur standard That s about me! Time: 60 min Marks: 50

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Asslam O Alikum FIN621- Financial Statement Analysis mid term paper shared n rechecked by Hira Ali Remember Us In Your Prayers

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Asslam O Alikum FIN621- Financial Statement Analysis mid term paper shared n rechecked by Hira Ali Remember Us In Your Prayers

BUS 321 Intermediate Accounting I Jan. 24, 2016 Name

BUS 321 Intermediate Accounting I Jan. 24, 2016 Name 1. GAAP What does GAAP stand for? Generally Accepted Accounting Principles 2. OBJECTIVE OF FINANCIAL REPORTING Write the objective of Financial Reporting.

BUS 321 Intermediate Accounting I Jan. 24, 2016 Name 1. GAAP What does GAAP stand for? Generally Accepted Accounting Principles 2. OBJECTIVE OF FINANCIAL REPORTING Write the objective of Financial Reporting.

Accounting Principles (203) Dr. Mishari Alfraih

Dr. Mishari Alfraih") 1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

1. Which of the following will cause owner's equity to increase? A. Expenses B. Owner s drawings D. loss 2. XYZ Co. provided the following information about its balance sheet: Cash K.D. 1,000 Account receivable

Reporting Financial Information

Learning Objectives LO1 Prepare an income statement for a service business. LO2 Calculate and analyze financial ratios using income statement amounts. Lesson 7-1 Reporting Financial Information LO1 The

Learning Objectives LO1 Prepare an income statement for a service business. LO2 Calculate and analyze financial ratios using income statement amounts. Lesson 7-1 Reporting Financial Information LO1 The

Financial Accounting (Sole Proprietorship)

") Financial Accounting (Sole Proprietorship) This course covers the topics shown below. Students navigate learning paths based on their level of readiness. Institutional users may customize the scope and

Financial Accounting (Sole Proprietorship) This course covers the topics shown below. Students navigate learning paths based on their level of readiness. Institutional users may customize the scope and

CHAPTER 2 ANALYZING TRANSACTIONS: THE ACCOUNTING EQUATION

REVIEW QUESTIONS CHAPTER 2 ANALYZING TRANSACTIONS: THE ACCOUNTING EQUATION 1. It is necessary to distinguish between business assets and liabilities and nonbusiness assets and liabilities of a single proprietor

REVIEW QUESTIONS CHAPTER 2 ANALYZING TRANSACTIONS: THE ACCOUNTING EQUATION 1. It is necessary to distinguish between business assets and liabilities and nonbusiness assets and liabilities of a single proprietor

Chapter III The Language of Accounting

Daubert, Madeline J. (1995). Money Talk: Accounting Fundamentals for Special Librarians. Special Library Association. (pp.12-31) Chapter III The Language of Accounting In order to communicate effectively

Daubert, Madeline J. (1995). Money Talk: Accounting Fundamentals for Special Librarians. Special Library Association. (pp.12-31) Chapter III The Language of Accounting In order to communicate effectively

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book Patrizia Tettamanzi Sophie Goodman Source: Kimmel/Weygandt/Kieso Financial Accounting

Management & Principles of Accounting Date: 08/11/2017 Recording transactions in the journal book and in the ledger book Patrizia Tettamanzi Sophie Goodman Source: Kimmel/Weygandt/Kieso Financial Accounting

True / False Questions

Chapter 02 Transaction Analysis True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers. True False 2. In order for information

Chapter 02 Transaction Analysis True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers. True False 2. In order for information

Investing and Financing Decisions and the Balance Sheet Irwin/McGraw-Hill

Chapter 2 Investing and Financing Decisions and the Balance Sheet Business Background To understand amounts appearing on a company s balance sheet we need to answer these questions: What business activities

Chapter 2 Investing and Financing Decisions and the Balance Sheet Business Background To understand amounts appearing on a company s balance sheet we need to answer these questions: What business activities

Madison Area Technical College

Madison Area Technical College Dual Credit Course Profile 2013-2014 Academic Year Instructor Name High School Instructor Contact Information Michael Cassidy Mount Horeb High School cassidymichael@mhasd.k12.wi.us

Madison Area Technical College Dual Credit Course Profile 2013-2014 Academic Year Instructor Name High School Instructor Contact Information Michael Cassidy Mount Horeb High School cassidymichael@mhasd.k12.wi.us

THE ACCOUNTING INFORMATION SYSTEM

Study Objectives THE ACCOUNTING INFORMATION SYSTEM 1. Analyze the effect of business transactions on the basic accounting equation. 2. Explain what an account is and how it helps in the recording process.

Study Objectives THE ACCOUNTING INFORMATION SYSTEM 1. Analyze the effect of business transactions on the basic accounting equation. 2. Explain what an account is and how it helps in the recording process.

Consultant CCI. Consulting Case Interview.

Consultant CCI Consulting Case Interview http://killexams.com/pass4sure/exam-detail/cci Question: 46 Which of the following transactions have a negative impact on cash? A. A decrease in supplies on hand

Consultant CCI Consulting Case Interview http://killexams.com/pass4sure/exam-detail/cci Question: 46 Which of the following transactions have a negative impact on cash? A. A decrease in supplies on hand

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

LESSON Posting to an Accounts Payable Ledger. CENTURY 21 ACCOUNTING Thomson/South-Western

LESSON - Posting to an Accounts Payable Ledger 2 Posting to an Accounts Payable Ledger There are two (2) major differences between the posting learned in this chapter (corporation) and the posting learned

LESSON - Posting to an Accounts Payable Ledger 2 Posting to an Accounts Payable Ledger There are two (2) major differences between the posting learned in this chapter (corporation) and the posting learned

District > Basic > Business Education > Accounting I ( ) (District) > Juett, David

(District) > Juett, David") Granite School District I (52.0312) (District) District > Basic > Business Education > I (52.0312) (District) > Juett, David Unit Essential Questions Content s Vocabulary Formative & Understanding (Week

Granite School District I (52.0312) (District) District > Basic > Business Education > I (52.0312) (District) > Juett, David Unit Essential Questions Content s Vocabulary Formative & Understanding (Week

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson. The statement of cash flows is a required component of financial statements.

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson The statement of cash flows is a required component of financial statements. BASICS OF CASH FLOW REPORTING Purpose of the Statement

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson The statement of cash flows is a required component of financial statements. BASICS OF CASH FLOW REPORTING Purpose of the Statement

CURRICULUM MAPPING FORM

Course Accounting 1 Teacher Mr. Garritano Aug. I. Starting a Proprietorship - 2 weeks A. The Accounting Equation B. How Business Activities Change the Accounting Equation C. Reporting Financial Information

Course Accounting 1 Teacher Mr. Garritano Aug. I. Starting a Proprietorship - 2 weeks A. The Accounting Equation B. How Business Activities Change the Accounting Equation C. Reporting Financial Information

Adjustments, Financial Statements, and the Quality of Earnings

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Business Background Management is responsible for preparing...

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

PELLISSIPPI STATE TECHNICAL COMMUNITY COLLEGE MASTER SYLLABUS PRINCIPLES OF ACCOUNTING I ACC 2110

PELLISSIPPI STATE TECHNICAL COMMUNITY COLLEGE MASTER SYLLABUS PRINCIPLES OF ACCOUNTING I ACC 2110 Class Hours: 3.0 Credit Hours: 3.0 Laboratory Hours: 0.0 Date Revised: Fall 1999 Catalog Course Description:

PELLISSIPPI STATE TECHNICAL COMMUNITY COLLEGE MASTER SYLLABUS PRINCIPLES OF ACCOUNTING I ACC 2110 Class Hours: 3.0 Credit Hours: 3.0 Laboratory Hours: 0.0 Date Revised: Fall 1999 Catalog Course Description:

Practical assessment: Various tasks demonstrating applied practical processes

Accounting 2010 Sample assessment instrument Practical assessment: Various tasks demonstrating applied These samples have been compiled by the QSA to help teachers plan and develop assessment instruments

Accounting 2010 Sample assessment instrument Practical assessment: Various tasks demonstrating applied These samples have been compiled by the QSA to help teachers plan and develop assessment instruments