Chapter 4 Completing the Accounting Cycle 高立翰

|

|

|

- Nigel Bishop

- 5 years ago

- Views:

Transcription

1 Chapter 4 Completing the Accounting Cycle 高立翰

2 Study Objectives 1. Prepare a worksheet. 2. Explain the process of closing the books. 3. Describe the content and purpose of a postclosing trial balance. 4. State the required steps in the accounting cycle. 5. Explain the approaches to preparing correcting entries. 6. Identify the sections of a classified statement of financial position. 會計學 ( 一 ) 2

http://ppt.")

3 PREVIEW OF CHAPTER 4 會計學 ( 一 ) 3

4 Using A Worksheet (1/2) Worksheet ( 工作底稿 ) A multiple-column form used in preparing financial statements. Not a permanent accounting record. May be a computerized worksheet using an electronic spreadsheet program such as Excel. Five step process. Use of worksheet is optional. 會計學 ( 一 ) 4

5 Using A Worksheet (2/2) Illustration: pp Illustration 4-1 會計學 ( 一 ) 5

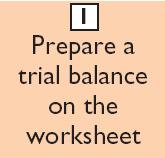

6 Steps in Preparing a Worksheet (1/5) 1. Prepare a Trial Balance on the Worksheet Adjusted Income Statement of Trial Balance Adjustments Trial Balance Statement Financial Position Account Titles Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Cash 15,200 Advertising Supplies 2,500 Prepaid Insurance 600 Office Equipment 5,000 Notes Payable 5,000 Accounts Payable 2,500 Unearned Revenue 1,200 Share Capital 10,000 Dividends 500 Service Revenue 10,000 Salaries Expense 4,000 Rent 900 Totals 28,700 28,700 Trial balance amounts come directly from ledger accounts. Include all accounts with balances. 會計學 ( 一 ) 6

7 Steps in Preparing a Worksheet Adjusting Journal Entries in Chapter 3 Illustration 3-23 General journal showing adjusting entries 會計學 ( 一 ) 7

8 Steps in Preparing a Worksheet (2/5) 2. Enter the Adjustments in the Adjustments Columns Adjusted Income Statement of Trial Balance Adjustments Trial Balance Statement Financial Position Account Titles Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Cash 15,200 Advertising Supplies 2,500 (a) 1,500 Prepaid Insurance 600 (b) 50 Office Equipment 5,000 Adjustments Key: Notes Payable 5,000 Accounts Payable 2,500 Unearned Revenue 1,200 (d) 400 Share Capital 10,000 Dividends 500 Service Revenue 10,000 (d) (e) Salaries Expense 4,000 (g) 1,200 Rent 900 Totals 28,700 28,700 Advertising Supplies Expense (a) 1,500 Insurance Expense (b) 50 Accumulated Depreciation (c) 40 Depreciation Expense (c) 40 (e) Accounts Receivable 200 (f) Interest Expense 50 Interest Payable (f) 50 (g) Salaries Payable 1,200 Totals 3,440 3,440 Add additional accounts as needed. (a) Supplies Used. (b) Insurance Expired. (c) Depreciation Expensed. (d) Service Revenue Earned. (e) Service Revenue Accrued. (f) Interest Accrued. (g) Salaries Accrued. Enter adjustment amounts, total adjustments columns, and check for equality. 會計學 ( 一 ) 8

9 Steps in Preparing a Worksheet (3/5) 3. Complete the Adjusted Trial Balance Columns Adjusted Income Statement of Trial Balance Adjustments Trial Balance Statement Financial Position Account Titles Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Cash 15,200 15,200 Advertising Supplies 2,500 (a) 1,500 1,000 Prepaid Insurance 600 (b) Office Equipment 5,000 5,000 Notes Payable 5,000 5,000 Accounts Payable 2,500 2,500 Unearned Revenue 1,200 (d) Share Capital 10,000 10,000 Dividends Service Revenue 10,000 (d) ,600 (e) 200 Salaries Expense 4,000 (g) 1,200 5,200 Rent Totals 28,700 28,700 Advertising Supplies Expense (a) 1,500 1,500 Insurance Expense (b) Accumulated Depreciation (c) Depreciation Expense (c) Accounts Receivable (e) (f) Interest Expense Interest Payable (f) (g) Salaries Payable 1,200 1,200 Totals 3,440 3,440 30,190 30,190 Total the adjusted trial balance columns and check for equality. 會計學 ( 一 ) 9

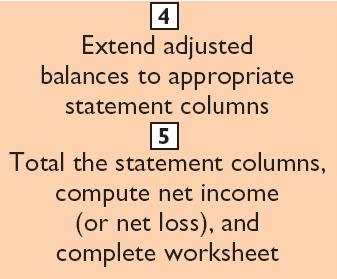

10 Steps in Preparing a Worksheet (4/5) 4. Extend Amounts to Financial Statement Columns Adjusted Income Statement of Trial Balance Adjustments Trial Balance Statement Financial Position Account Titles Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Cash 15,200 15,200 Advertising Supplies 2,500 (a) 1,500 1,000 Prepaid Insurance 600 (b) Office Equipment 5,000 5,000 Notes Payable 5,000 5,000 Accounts Payable 2,500 2,500 Unearned Revenue 1,200 (d) Share Capital 10,000 10,000 Dividends Service Revenue 10,000 (d) ,600 10,600 (e) 200 Salaries Expense 4,000 (g) 1,200 5,200 5,200 Rent Totals 28,700 28,700 Advertising Supplies Expense (a) 1,500 1,500 1,500 Insurance Expense (b) Accumulated Depreciation (c) Depreciation Expense (c) Accounts Receivable (e) (f) Interest Expense Interest Payable (f) (g) Salaries Payable 1,200 1,200 Totals 3,440 3,440 30,190 30,190 7,740 10,600 Extend all revenue and expense account balances to the income statement columns. 會計學 ( 一 ) 10

11 Steps in Preparing a Worksheet (5/5) 5. Total Columns, Compute Net Income (Loss) Adjusted Income Statement of Trial Balance Adjustments Trial Balance Statement Financial Position Account Titles Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Cash 15,200 15,200 15,200 Advertising Supplies 2,500 (a) 1,500 1,000 1,000 Prepaid Insurance 600 (b) Office Equipment 5,000 5,000 5,000 Notes Payable 5,000 5,000 5,000 Accounts Payable 2,500 2,500 2,500 Unearned Revenue 1,200 (d) Share Capital 10,000 10,000 10,000 Dividends Service Revenue 10,000 (d) ,600 10,600 (e) 200 Salaries Expense 4,000 (g) 1,200 5,200 5,200 Rent Totals 28,700 28,700 Advertising Supplies Expense (a) 1,500 1,500 1,500 Insurance Expense (b) Accumulated Depreciation (c) Depreciation Expense (c) Accounts Receivable (e) (f) Interest Expense Interest Payable (f) Salaries Payable (g) 1,200 1,200 1,200 Totals Q4 1. 3,440 3,440 30,190 30,190 7,740 10,600 22,450 19,590 Net income 2,860 2,860 Totals 10,600 10,600 22,450 22,450 Compute Net Income or Net Loss. 11

12 Preparing Financial Statements from a Worksheet Income Statement is prepared from the income statement columns. Statement of Financial Position and Retained Earnings Statement are prepared from the Statement of Financial Position columns. Companies can prepare financial statements before they journalize and post adjusting entries. 會計學 ( 一 ) 12

http://ppt.")

13 Income Statement from a Worksheet Illustration 4-3 會計學 ( 一 ) 13

http://ppt.")

14 Retained Earnings Statement from a Worksheet Illustration 4-3 會計學 ( 一 ) 14

http://ppt.cc/mjfq 15")

15 Statement of Financial Position from a Worksheet Illustration 4-3 會計學 ( 一 ) 15

16 Preparing Adjusting Entries from a Worksheet The adjusting entries are prepared from the adjustments columns of the worksheet. Journalizing and posting of adjusting entries follows the preparation of financial statements when a worksheet is used. Adjusting Journal Entries (Chapter 3) Illustration 3-23 General journal showing adjusting entries 會計學 ( 一 ) 16

and Permanent ( 永久性 ) accounts 會計學 ( 一 ) http://ppt.")

17 Closing the Books (1/4) At the end of the accounting period, the company makes the accounts ready for the next period. Temporary ( 暫時性 ) and Permanent ( 永久性 ) accounts 會計學 ( 一 ) 17

18 Closing the Books (2/4) Closing Entries ( 結帳分錄 ) formally recognize, in the general ledger, the transfer of Net Income (or Net Loss), and Dividends to Retained Earnings. Closing entries are only journalized and posted at the end of the annual accounting period. Closing entries produce a zero balance in each temporary account. Q4 2. 會計學 ( 一 ) 18

http://ppt.")

19 Note: Dividends are closed directly to Retained Earnings and not to Income Summary because Dividends are not an expense. 會計學 ( 一 ) 19

http://ppt.")

20 Closing the Books (3/4) Closing entries need to be posted Illustration 4-6 Closing entries journalized 會計學 ( 一 ) 20

http://ppt.")

21 Closing the Books (4/4) Posting closing entries Illustration 4-7 Posting of closing entries 會計學 ( 一 ) 21

22 Preparing a Post-Closing Trial Balance Post-Closing Trial Balance ( 結帳後試算表 ) Lists permanent accounts and their balances after the journalizing and posting of closing entries. To prove the equality of the permanent account balances after journalizing and posting of closing entries. Only contains balances for permanent statement of financial position accounts. All temporary accounts will have zero balances. Q4 3. 會計學 ( 一 ) 22

http://ppt.")

23 Illustration 4-8 Post-closing trial balance 會計學 ( 一 ) 23

24 Summary of the Accounting Cycle 1. Analyze business transactions Illustration Prepare a post-closing trial balance 2. Journalize the transactions 8. Journalize and post closing entries 3. Post to ledger accounts 7. Prepare financial statements 4. Prepare a trial balance 6. Prepare an adjusted trial balance 5. Journalize and post adjusting entries Q4 4. 會計學 ( 一 ) 24

25 Correcting Entries An Avoidable Step Correcting Entries ( 更正分錄 ) are unnecessary if the records are error-free are made whenever an error is discovered must be posted before closing entries Instead of preparing a correcting entry, it is possible to reverse the incorrect entry and then prepare the correct entry 會計學 ( 一 ) 25

26 Closing Entries Illustration (1/2) Case 1 On May 10, Bai Co. journalized and posted a NT$500 cash collection on account from a customer as a debit to Cash NT$500 and a credit to Service Revenue NT$500. The company discovered the error on May 20, when the customer paid the remaining balance in full. Incorrect entry Correct entry Correcting entry Cash 500 Service Revenue 500 Cash 500 Accounts Receivable 500 Service Revenue 500 Accounts Receivable 500 會計學 ( 一 ) 26

27 Closing Entries Illustration (2/2) Case 2 On May 18, Mercato purchased on account equipment costing NT$4,500. The transaction was journalized and posted as a debit to Equipment NT$450 and a credit to Accounts Payable NT$450. The error was discovered on June 3. Incorrect Equipment 450 entry Accounts Payable 450 Correct entry Correcting entry Equipment 4,500 Accounts Payable 4,500 Equipment 4,050 Accounts Payable 4,050 會計學 ( 一 ) 27

28 The Classified Statement of Financial Position Presents a snapshot at a point in time To improve understanding, companies group similar assets and similar liabilities together Assets accounts are listed by the reverse order of their liquidity Standard Classifications Illustration 4-16 Assets Intangible assets Property, plant, and equipment Long-term investments Current assets Equity and Liabilities Equity Non-current liabilities Current liabilities Q4 5. 會計學 ( 一 ) 28

")

29 Classified statement of financial position 會計學 ( 一 ) 29

30 Classified Statement of Financial Position (1/7) Intangible Assets ( 無形資產 ) Assets that do not have physical substance. Goodwill ( 商譽 ) Franchises ( 特許權 ) Trademark ( 商標 ) Illustration 4-18 Intangible assets section 會計學 ( 一 ) 30

http://ppt.cc/mjfq 31")

31 Classified Statement of Financial Position (2/7) Property, Plant, and Equipment ( 固定資產,PP&E) Long useful lives Currently used in operations Depreciation allocating the cost of assets to a number of years Accumulated depreciation total amount of depreciation expensed thus far in the asset s life 會計學 ( 一 ) 31

32 Classified Statement of Financial Position (3/7) Long-term investments ( 長期投資 ) Investments in stocks and bonds of other companies Investments in long-term assets such as land or buildings that a company is not currently using in its operating activities 房地產投資關聯企業投資 會計學 ( 一 ) 32

http://ppt.")

33 Classified Statement of Financial Position (4/7) Current Assets ( 流動資產 ) Assets that a company expects to convert to cash or use up within one year or the operating cycle, whichever is longer Operating cycle is the average time it takes from the purchase of inventory to the collection of cash from customers 低 流動性 高 Q4 6. 會計學 ( 一 ) 33

http://ppt.")

34 Classified Statement of Financial Position (5/7) Equity ( 權益 ) Proprietorship - one capital account (Owner s Equity) Partnership - capital account for each partner Corporation Share Capital and Retained Earnings 會計學 ( 一 ) 34

http://ppt.")

35 Classified Statement of Financial Position (6/7) Non-current Liabilities ( 非流動負債 ) Obligations a company expects to pay after one year. 會計學 ( 一 ) 35

ability to pay obligations expected to be due within the next year 會計學 ( 一 ) http://ppt.")

36 Classified Statement of Financial Position (7/7) Current Liabilities ( 流動負債 ) Obligations the company is to pay within the coming year Usually list notes payable first, followed by accounts payable. Other items follow in order of magnitude Liquidity ( 流動性 ) ability to pay obligations expected to be due within the next year 會計學 ( 一 ) 36

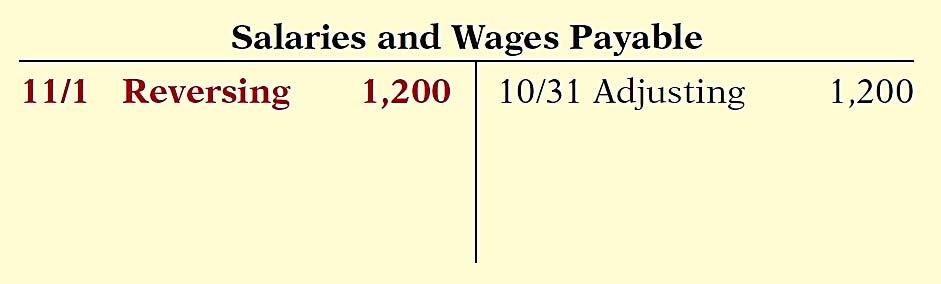

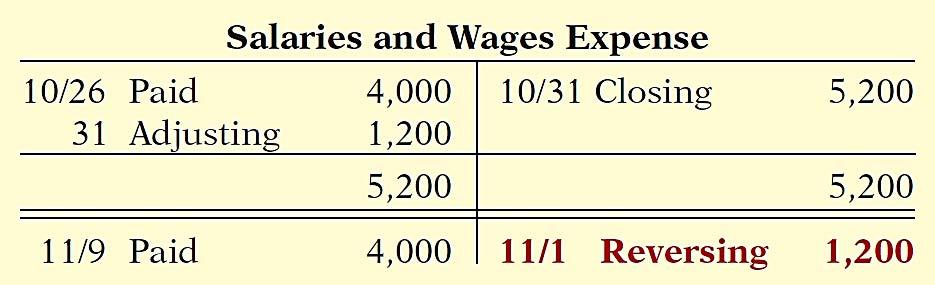

37 Appx. 4A: Reversing Entries ( 不考 ) Reversing Entries ( 迴轉分錄 ) It is often helpful to reverse some of the adjusting entries before recording the regular transactions of the next period Companies make a reversing entry at the beginning of the next accounting period Each reversing entry is the exact opposite of the adjusting entry made in the previous period The use of reversing entries does not change the amounts reported in the financial statements 會計學 ( 一 ) 37

38 Reversing Entries Example Illustration: To illustrate the optional use of reversing entries for accrued expenses, we will use the salaries expense transactions for Yazici Advertising A.S. 1. October 26 (initial salary entry): Pioneer pays 4,000 of salaries and wages earned between October 15 and October October 31 (adjusting entry): Salaries and wages earned between October 29 and October 31 are 1,200. The company will pay these in the November 9 payroll. 3. November 9 (subsequent salary entry): Salaries and wages paid are 4,000. Of this amount, 1,200 applied to accrued salaries and wages payable and 2,800 was earned between November 1 and November 9. 會計學 ( 一 ) 38

")

39 With Reversing Entries (per appendix) Oct. 26 Oct. 31 Oct. 31 Initial Salary Entry Same entry Adjusting Entry Same entry Closing Entry Same entry Nov. 1 Nov. 9 Reversing Entry Salaries and Wages Payable 1,200 Salaries and Wages Expense 1,200 Subsequent Salary Entry Salaries and Wages Expense 4,000 Cash 4,000 會計學 ( 一 ) 39

40 會計學 ( 一 ) 40

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

Chapter 3 Adjusting the Accounts 高立翰

Chapter 3 Adjusting the Accounts 高立翰 Study Objectives 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. ( 不考 ) 3. Explain the reasons for adjusting entries. 4. Identify

Chapter 3 Adjusting the Accounts 高立翰 Study Objectives 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. ( 不考 ) 3. Explain the reasons for adjusting entries. 4. Identify

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

CHAPTER 4 EXERCISES: SET B. E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows.

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

Chapter 6 The annual report and accounts. The closure of the accounting cycle and Accounting information disclosed to the public

Chapter 6 The annual report and accounts The closure of the accounting cycle and Accounting information disclosed to the public 1 Six steps in the accounting cycle 1. Analyze transactions from the source

Chapter 6 The annual report and accounts The closure of the accounting cycle and Accounting information disclosed to the public 1 Six steps in the accounting cycle 1. Analyze transactions from the source

Completing the Accounting Cycle

4 Completing the Accounting Cycle 4-1 Closing the Books At the end of the accounting period, the company gets the accounts ready for the next period. Very similar to what happens at AHS at the end of a

4 Completing the Accounting Cycle 4-1 Closing the Books At the end of the accounting period, the company gets the accounts ready for the next period. Very similar to what happens at AHS at the end of a

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE LEARNING OBJECTIVES 1. PREPARE A WORKSHEET. 2. EXPLAIN THE PROCESS OF CLOSING THE BOOKS. 3. DESCRIBE THE CONTENT AND PURPOSE OF A POST-CLOSING TRIAL BALANCE. 4.

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE LEARNING OBJECTIVES 1. PREPARE A WORKSHEET. 2. EXPLAIN THE PROCESS OF CLOSING THE BOOKS. 3. DESCRIBE THE CONTENT AND PURPOSE OF A POST-CLOSING TRIAL BALANCE. 4.

LESSON 8-1. Recording Adjusting Entries. CENTURY 21 ACCOUNTING Thomson/South-Western

LESSON 8-1 Recording Adjusting Entries 2 TERM REVIEW page 205 Adjusting Entries journal entries recorded to update general ledger accounts at the end of a fiscal period Adjustments must be journalized

LESSON 8-1 Recording Adjusting Entries 2 TERM REVIEW page 205 Adjusting Entries journal entries recorded to update general ledger accounts at the end of a fiscal period Adjustments must be journalized

Chapter 8. Recording Adjusting and Closing Entries

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

4-1 COMPLETING THE ACCOUNTING CYCLE

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

4-1 COMPLETING THE ACCOUNTING CYCLE Atanas Atanasov Assist.prof. University of Economics - Varna Steps in Accounting Cycle 4-2 134 Analyze source documents. Journalize transactions in the journal. Post

2. Which of the following is an external user of accounting information? A) Labor unions. B) Finance directors. C) Company officers. D) Managers.

Labor unions. B) Finance directors. C) Company officers. D) Managers.") Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

Name: Date: 1. The study of accounting is not useful for a business career unless your career objective is to become an accountant. A) True B) False 2. Which of the following is an external user of accounting

Adjustments, Financial Statements and the Quality of Earnings

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CENTURY 21 ACCOUNTING, 9e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

Accounting Basics Introduction To Financial Accounting

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

Accounting Basics Introduction To Financial Accounting ILLUSTRATION 1-5 BASIC ACCOUNTING EQUATION The Basic Accounting Equation Assets = Liabilities + Owner s Equity ASSETS AS A BUILDING BLOCK Assets are

The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about

1-1 2012 The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin 4 1 The Accounting Cycle Step 1 Analyze and transactions classify transactions Step 2 Journalize the transactions data about

Chapter 3 Question Review 1

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Chapter 3 Question Review 1 Chapter 3 Questions Multiple Choice 1. If services are rendered on account, then a. assets will decrease. b. liabilities will increase. c. stockholders equity will increase.

Financial Statements and Closing Entries for a Merchandising Business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield. Slide 3-2

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

Chapter 10 Partnership revaluation ( 合夥重估 )

") Chapter 10 Partnership revaluation ( 合夥重估 ) 10.2 Need for revaluation ( 需要重估的原因 ) Whenever there is a change in the profit and loss sharing ratio ( 損益分配比率改變 ) (A change in the profit and loss sharing ratio)

Chapter 10 Partnership revaluation ( 合夥重估 ) 10.2 Need for revaluation ( 需要重估的原因 ) Whenever there is a change in the profit and loss sharing ratio ( 損益分配比率改變 ) (A change in the profit and loss sharing ratio)

Accounting for. Sole Proprietorship. 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

appendix F Accounting for Sole Proprietorships study objectives After studying this appendix, you should be able to: 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

appendix F Accounting for Sole Proprietorships study objectives After studying this appendix, you should be able to: 1 Identify the differences in equity accounts between a corporation and a sole proprietorship.

Chapter 4: Completing the Accounting Cycle

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

Principles of Accounting II

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

BASIC FINANCIAL RATIO ANALYSIS AND IMPLICATION

BASIC FINANCIAL RATIO ANALYSIS AND IMPLICATION Dr. Stacy Wang Assistant Professor Hang Seng University of Hong Kong Hong Kong Institute of Certified Public Accountants, 2018. All rights reserved. 1 Companies

BASIC FINANCIAL RATIO ANALYSIS AND IMPLICATION Dr. Stacy Wang Assistant Professor Hang Seng University of Hong Kong Hong Kong Institute of Certified Public Accountants, 2018. All rights reserved. 1 Companies

Chapter 4. The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

東吳大學 106 學年度轉學生 ( 含進修學士班轉學生 ) 招生考試試題第 1 頁, 共 5 頁

招生考試試題第 1 頁, 共 5 頁") 東吳大學 106 學年度轉學生 ( 含進修學士班轉學生 ) 招生試題第 1 頁, 共 5 頁 商學 ( 進修學士班 ) 三年 鐘 注意事項 : 1. 計算題請詳列計算過程, 否則不予計分 如有無法整除之情形, 請四捨五入至小數點後第二位 2. 一律作答於所附之 招生答案卷 上, 並務必標明題號, 依序作答 若於試題卷上作答者, 一律不予計分 一 選擇題 ( 共 28 分, 每題 2 分 ) 請在答案卷上畫下列表格,

東吳大學 106 學年度轉學生 ( 含進修學士班轉學生 ) 招生試題第 1 頁, 共 5 頁 商學 ( 進修學士班 ) 三年 鐘 注意事項 : 1. 計算題請詳列計算過程, 否則不予計分 如有無法整除之情形, 請四捨五入至小數點後第二位 2. 一律作答於所附之 招生答案卷 上, 並務必標明題號, 依序作答 若於試題卷上作答者, 一律不予計分 一 選擇題 ( 共 28 分, 每題 2 分 ) 請在答案卷上畫下列表格,

Weygandt, Kieso, Kimmel, Trenholm, Kinnear, Barlow, Atkins: Principles of Financial Accounting, Canadian Edition CHAPTER 4

CHAPTER 4 Completion of the Accounting Cycle ASSIGNMENT CLASSIFICATION TABLE Study Objectives 1. Prepare closing entries and a postclosing trial balance. 2. Explain the steps in the accounting cycle including

CHAPTER 4 Completion of the Accounting Cycle ASSIGNMENT CLASSIFICATION TABLE Study Objectives 1. Prepare closing entries and a postclosing trial balance. 2. Explain the steps in the accounting cycle including

Chapter 4: Completing the Accounting Cycle. Learning Objective 2 Prepare financial statements from adjusted account balances.

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

Module 4. Table of Contents

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

13.3 Preparation of financial statements for limited companies ( 編製有限公司的財務報表 )

") Chapter 13 Regulatory Framework of Accounting in Hong Kong and Financial Statements for Limited Companies ( 香港的會計監管架構和有限公司的財務報表 ) 13.3 Preparation of financial statements for limited companies ( 編製有限公司的財務報表

Chapter 13 Regulatory Framework of Accounting in Hong Kong and Financial Statements for Limited Companies ( 香港的會計監管架構和有限公司的財務報表 ) 13.3 Preparation of financial statements for limited companies ( 編製有限公司的財務報表

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Learning Objectives. LO1 Journalize and post closing entries for a service business organized as a proprietorship.

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Curriculum Document for Business Education

Curriculum Document for Business Education Course Title: Accounting I Learner Objective #1: Students will learn the accounting equation and how business activities change the accounting equation. Identify

Curriculum Document for Business Education Course Title: Accounting I Learner Objective #1: Students will learn the accounting equation and how business activities change the accounting equation. Identify

Bixby Public Schools Essential Elements Grade: 10-12

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

Course: Accounting Essential Elements Grade: 10-12 Weeks 1-6 Chapter 1 describes how a proprietorship is started & the transactions that occur when the business is organized. The accounting equation is

After studying this chapter, you should be able to: adjusted account balances.

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

Completion of the Accounting Cycle

Completion of the Accounting Cycle Chapter 4 THE NAVIGATOR Understand Concepts for Review Read Feature Story Scan Study Objectives Read Preview Read text and answer Before You Go On p. 147 p. 157 p. 164

Completion of the Accounting Cycle Chapter 4 THE NAVIGATOR Understand Concepts for Review Read Feature Story Scan Study Objectives Read Preview Read text and answer Before You Go On p. 147 p. 157 p. 164

Chapter 12 - Reporting and Analyzing Cash Flows. Chapter Outline

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

SOLUTIONS. Learning Goal 14

S1 Learning Goal 14 Multiple Choice 1. a 2. c The capital balance to use on the balance sheet is the final balance from the statement of owner s equity. The capital balance showing on the worksheet does

S1 Learning Goal 14 Multiple Choice 1. a 2. c The capital balance to use on the balance sheet is the final balance from the statement of owner s equity. The capital balance showing on the worksheet does

Account Form. Used to summarize in one place all the changes to a single account A separate form for each account. Sample of a blank account form

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

Learning Objectives LO1 Construct a chart of accounts for a service business organized as a proprietorship. LO2 Demonstrate correct principles for numbering accounts. LO3 Apply file maintenance principles

銘傳大學九十一學年度轉學生招生考試八月四日第三節會計轉三會計學 ( 二 ) 試題

試題") 銘傳大學九十一學年度轉學生招生考試八月四日第三節會計轉三會計學 ( 二 ) 試題 * 可使用計算機一 Multiple Choice (20%) 1. In reporting extraordinary transactions on a statement of cash flows (indirect method), the a. gross amount of an extraordinary

銘傳大學九十一學年度轉學生招生考試八月四日第三節會計轉三會計學 ( 二 ) 試題 * 可使用計算機一 Multiple Choice (20%) 1. In reporting extraordinary transactions on a statement of cash flows (indirect method), the a. gross amount of an extraordinary

Graded Project. Lesson 1: Business Accounting and You OVERVIEW INSTRUCTIONS

Lesson 1: Business Accounting and You OVERVIEW The focus of this project is for the student to keep a set of books through an accounting period to perform the following functions: Set up the books of accounting

Lesson 1: Business Accounting and You OVERVIEW The focus of this project is for the student to keep a set of books through an accounting period to perform the following functions: Set up the books of accounting

Chapter 9 Recording Adjusting and Closing Entries

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

2/10/2009. The accounting ACCOUNTING TRANSACTIONS AND EVENTS. Analysing transactions. Chapter 2

Chapter 2 The accounting information system PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd ACCOUNTING TRANSACTIONS AND EVENTS Transactions are external

Chapter 2 The accounting information system PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd ACCOUNTING TRANSACTIONS AND EVENTS Transactions are external

FORENSIC ACCOUNTING VERSION

FORENSIC ACCOUNTING VERSION Fraudulent or incorrect transactions are presented below. Your job as a forensic accountant is to correct the financial statements and determine how income and total assets

FORENSIC ACCOUNTING VERSION Fraudulent or incorrect transactions are presented below. Your job as a forensic accountant is to correct the financial statements and determine how income and total assets

Assessment Schedule 2017 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176)

") NCEA Level 2 Accounting (91176) 2017 page 1 of 7 Assessment Schedule 2017 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176) Marking Instructions applied

NCEA Level 2 Accounting (91176) 2017 page 1 of 7 Assessment Schedule 2017 Accounting: Prepare financial information for an entity that operates accounting subsystems (91176) Marking Instructions applied

Chapter 4: Posting from a General Journal to a General Ledger

Chapter 4: Posting from a General Journal to a General Ledger Goals of Chapter 4: Define accounting terms related to posting form a general journal to a general ledger Identify accounting concepts and

Chapter 4: Posting from a General Journal to a General Ledger Goals of Chapter 4: Define accounting terms related to posting form a general journal to a general ledger Identify accounting concepts and

Week 4/5, Chap 4. The General Journal and the General Ledger. Instructor: Michael Booth

Week 4/5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth Complete the trial balance 1. Enter the trial balance heading showing the company name, report title, and closing date

Week 4/5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth Complete the trial balance 1. Enter the trial balance heading showing the company name, report title, and closing date

ACCOUNTING 201. PRACTICE MIDTERM - (Covering Chapters 1-5)

") Problem - I Multiple Choice (20 points) ACCOUNTING 201 PRACTICE MIDTERM - (Covering Chapters 1-5) 1. A private organization which establishes broad accounting principles as well as specific accounting

Problem - I Multiple Choice (20 points) ACCOUNTING 201 PRACTICE MIDTERM - (Covering Chapters 1-5) 1. A private organization which establishes broad accounting principles as well as specific accounting

Learning Objective. LO1 Prepare an income statement for a merchandising business organized as a corporation.

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Acct 151A Week 7, Chap 6. Instructor: Michael Booth Cabrillo College

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

Chapter 6: Worksheets for a Service Business

Chapter 6: Worksheets for a Service Business Goals of Chapter 6: Define accounting terms related to a worksheet for a service business organized as a proprietorship Identify accounting concepts and practices

Chapter 6: Worksheets for a Service Business Goals of Chapter 6: Define accounting terms related to a worksheet for a service business organized as a proprietorship Identify accounting concepts and practices

Exercises. 2) Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities

Owners Equity is ( ) (1). Occurs when Revenues exceed Expenses. (2) Debts owed by a business, (3). The excess of Assets over Liabilities") Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

Exercises 1 Please answer the following questions 1 Please explain Assets 2 Please explain Liabilities 3 Please explain Owner Equity 4 Please explain Revenues 5 Please explain Expenses 2 Please select

SOLUTIONS Learning Goal 8

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

Chapter 12 Introduction to Asset Liability Management

Chapter 12 Introduction to Asset Liability Management 1 Introduction Bank s structural position depositors borrowers checking accounts saving accounts fixed deposits commercial loans credit-card debt car

Chapter 12 Introduction to Asset Liability Management 1 Introduction Bank s structural position depositors borrowers checking accounts saving accounts fixed deposits commercial loans credit-card debt car

Adjusting the Accounts

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

Books of original entry and ledgers (I)

") Chapter 1 Books of original entry and ledgers (I) HKDSE (2016, 2) (Books of original entry and ledgers) ABC Company keeps the following four ledgers only: cash book, general ledger, purchases ledger and

Chapter 1 Books of original entry and ledgers (I) HKDSE (2016, 2) (Books of original entry and ledgers) ABC Company keeps the following four ledgers only: cash book, general ledger, purchases ledger and

Accounting 1A Class Notes Chapter 3 The Adjusting Process

Source Documents General Journal General Ledger Trial Balance Adjusting Entries Difference between TRANSACTIONS and ADJUSTMENTS Transactions occur through-out the accounting cycle and normally involve

Source Documents General Journal General Ledger Trial Balance Adjusting Entries Difference between TRANSACTIONS and ADJUSTMENTS Transactions occur through-out the accounting cycle and normally involve

The General Journal and the General Ledger

chapter College Accounting The General Journal and the General Ledger 11 th Edition 3 1 Learning Objectives After you have completed this chapter, you will be able to do the following: 3 2 The General

chapter College Accounting The General Journal and the General Ledger 11 th Edition 3 1 Learning Objectives After you have completed this chapter, you will be able to do the following: 3 2 The General

東吳大學九十八學年度轉學生 ( 含進修學士班 ) 招生考試試題第 1 頁, 共 5 頁

招生考試試題第 1 頁, 共 5 頁") 東吳大學九十八學年度轉學生 ( 含進修學士班 ) 招生考試試題第 1 頁, 共 5 頁 注意 : 1. 各題請以英文作答 2. 除題目另有要求外, 各題計算除不盡時, 請四捨五入到整數位 3. 若需現值請用計算機計算 一 Select the best answer for each of the following: (30%, 每小題答對 2 分, 答錯扣 3 分, 扣至本題零分為止 ) 1.

東吳大學九十八學年度轉學生 ( 含進修學士班 ) 招生考試試題第 1 頁, 共 5 頁 注意 : 1. 各題請以英文作答 2. 除題目另有要求外, 各題計算除不盡時, 請四捨五入到整數位 3. 若需現值請用計算機計算 一 Select the best answer for each of the following: (30%, 每小題答對 2 分, 答錯扣 3 分, 扣至本題零分為止 ) 1.

ILLUSTRATION 12-1 TYPES OF INTANGIBLE ASSETS

ILLUSTRATION 12-1 TYPES OF INTANGIBLE ASSETS INTANGIBLE ASSETS Identifiable Intangible Assets (Rights Type) Externally Acquired Internally Developed Financial Statement Treatment Unidentifiable Intangible

ILLUSTRATION 12-1 TYPES OF INTANGIBLE ASSETS INTANGIBLE ASSETS Identifiable Intangible Assets (Rights Type) Externally Acquired Internally Developed Financial Statement Treatment Unidentifiable Intangible

COMPLETING THE ACCOUNTING CYCLE

Chapter 04 COMPLETING THE ACCOUNTING CYCLE PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

Chapter 04 COMPLETING THE ACCOUNTING CYCLE PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin

Accounting Cycle Review Problem. Michelle Clark. Accounting 1110 Section 401. Fall 2014

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

Fundamentals of Accounting Resources

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

Contents Figure 1 - The Profit and Loss statement example... 2 Figure 2 - Balance sheet example... 3 Figure 3 - Example of a Balance Sheet... 4 Figure 4 - Example of a Profit & Loss Sheet... 5 Figure 5-10

PROBLEM 3-2B. (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...

J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...") PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

Cash. Laundry Equipment. Hilda Dinero, Capital Oct. 31 Clos. 1,000 Oct. 31 Bal. 18, Clos. 12, Bal. 30,200

1, 3, 6. Oct. 31 Bal. 1,450 Cash Laundry Supplies Oct. 31 Bal. 3,750 Oct. 31 Adj. 2,800 31 Adj. Bal. 950 Prepaid Insurance Oct. 31 Bal. 2,400 Oct. 31 Adj. 2,000 31 Adj. Bal. 400 Oct. 31 Bal. 54,500 Laundry

1, 3, 6. Oct. 31 Bal. 1,450 Cash Laundry Supplies Oct. 31 Bal. 3,750 Oct. 31 Adj. 2,800 31 Adj. Bal. 950 Prepaid Insurance Oct. 31 Bal. 2,400 Oct. 31 Adj. 2,000 31 Adj. Bal. 400 Oct. 31 Bal. 54,500 Laundry

Accounting 1A Class Notes Chapter 2 Analyzing Transactions. Chart of Accounts 1. Assets. Liabilities. 3. Owners Equity. Revenue. 5.

Chart of Accounts 1. Assets 2. Liabilities 3. Owners Equity 4. Revenue 5. Expense T- ACCOUNTS Title, Debit on the Left and Credit on the right Foot both sides (if more than one entry) Balance on the side

Chart of Accounts 1. Assets 2. Liabilities 3. Owners Equity 4. Revenue 5. Expense T- ACCOUNTS Title, Debit on the Left and Credit on the right Foot both sides (if more than one entry) Balance on the side

The Accounting Cycle Revised Edition

Assessment The Accounting Cycle Revised Edition The objectives of this book are: To discuss record keeping systems To review the vocabulary of accounting To explain making adjusting and closing entries

Assessment The Accounting Cycle Revised Edition The objectives of this book are: To discuss record keeping systems To review the vocabulary of accounting To explain making adjusting and closing entries

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Century 21 Accounting, 9e Multicolumn Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

The Adjustment Process and Financial Statements Irwin/McGraw-Hill

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Consolidation Refresher Workshop (Workshop 1) 8 October 2014

8 October 2014") Consolidation Refresher Workshop (Workshop 1) 8 October 2014 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust.) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2008-14 Nelson Consulting Limited 1

Consolidation Refresher Workshop (Workshop 1) 8 October 2014 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust.) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2008-14 Nelson Consulting Limited 1

(4915 (4915 TT) 3Q18 31 Oct 2018

3Q18 31 Oct 2018") 致伸科技 (4915 TT) 3Q18 財報法說 1 31 Oct 2018 3Q18 營運成果 Record Q3 REVENUES GP EPS Amount :NTD M Q3 18 Q2 18 Q3 17 QoQ YoY Net Sales 19,608 14,798 14,997 32.5% 30.7% COGS 17,266 13,081 13,016 Gross Profit 2,342

致伸科技 (4915 TT) 3Q18 財報法說 1 31 Oct 2018 3Q18 營運成果 Record Q3 REVENUES GP EPS Amount :NTD M Q3 18 Q2 18 Q3 17 QoQ YoY Net Sales 19,608 14,798 14,997 32.5% 30.7% COGS 17,266 13,081 13,016 Gross Profit 2,342

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES INVESTING ACTIVITIES FINANCING ACTIVITIES

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

CHAPTER 3 Selected Solutions. The Accounting Information System. Brief Topics Questions Exercises Exercises Problems

CHAPTER 3 Selected Solutions The Accounting Information System ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Brief Topics Questions Exercises Exercises Problems 1. Transaction identification. 1, 2, 3, 5,

CHAPTER 3 Selected Solutions The Accounting Information System ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Brief Topics Questions Exercises Exercises Problems 1. Transaction identification. 1, 2, 3, 5,

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT. (Manual Case, and Working Papers) Scott Osborne, CPA

Scott Osborne, CPA") DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

DE ANZA COLLEGE ACCOUNTING 1A EXTRA CREDIT ASSIGNMENT (Manual Case, and Working Papers) by Scott Osborne, CPA 1 EXPLANATION OF EXTRA CREDIT ASSIGNMENT The extra credit assignment consists of a manual accounting

Adjustments, Financial Statements, and the Quality of Earnings

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Learning Outcomes. The Basic Accounting Cycle

Chapter 2: Review of the Accounting Process Part 3: Accounting Cycle with Emphasis on Year End Activities Intermediate Accounting 1 Dr. Chula King Learning Outcomes After completing this part, you should

Chapter 2: Review of the Accounting Process Part 3: Accounting Cycle with Emphasis on Year End Activities Intermediate Accounting 1 Dr. Chula King Learning Outcomes After completing this part, you should

Chapter 4 Completing the Accounting Cyclt 163

Chapter 4 Completing the Accounting Cyclt 163 The company's chart of accounts follows: 101 Cash 405 Commissions Earned 106 Accounts Receivable 612 Depreciation Expense Computer Equip. 124 Office Supplies

Chapter 4 Completing the Accounting Cyclt 163 The company's chart of accounts follows: 101 Cash 405 Commissions Earned 106 Accounts Receivable 612 Depreciation Expense Computer Equip. 124 Office Supplies

Posting from a General Journal to a General Ledger. Tuesday, October 26, :48:47 PM ET

Posting from a General Journal to a General Ledger Account Form Based on the T account (Debit and Credit sides). Transaction Date and Journal page number. Balance-Ruled Account Form A form that has columns

Posting from a General Journal to a General Ledger Account Form Based on the T account (Debit and Credit sides). Transaction Date and Journal page number. Balance-Ruled Account Form A form that has columns

Section A: Multiple-Choice Questions (2 marks each; Total 30 marks)

") Name: Student ID: Section A: Multiple-Choice Questions (2 marks each; Total 30 marks) Choose the one best answer. 1. The accounting process involves all of the following except ( d ) a. identifying economic

Name: Student ID: Section A: Multiple-Choice Questions (2 marks each; Total 30 marks) Choose the one best answer. 1. The accounting process involves all of the following except ( d ) a. identifying economic

Business Background Management is responsible for preparing...

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

CHAPTER3 Adjusting the Accounts

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

THE ACCOUNTING INFORMATION SYSTEM

Study Objectives THE ACCOUNTING INFORMATION SYSTEM 1. Analyze the effect of business transactions on the basic accounting equation. 2. Explain what an account is and how it helps in the recording process.

Study Objectives THE ACCOUNTING INFORMATION SYSTEM 1. Analyze the effect of business transactions on the basic accounting equation. 2. Explain what an account is and how it helps in the recording process.

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 6 Closing entries and preparing financial statements Chapter 4 (p148-162); and Chapter 5 Completing the accounting cycle closing and reversing entries. Study Group

ACC100 Introduction to Accounting Week 6 Closing entries and preparing financial statements Chapter 4 (p148-162); and Chapter 5 Completing the accounting cycle closing and reversing entries. Study Group

a) Post-closing trial balance c) Income statement d) Statement of retained earnings

Post-closing trial balance c) Income statement d) Statement of retained earnings") Note: The formatting of financial statements is important. They follow Generally Accepted Accounting Principles (GAAP), which creates a uniformity of financial statements for analyzing. This allows for

Note: The formatting of financial statements is important. They follow Generally Accepted Accounting Principles (GAAP), which creates a uniformity of financial statements for analyzing. This allows for

Financial Accounting, 6Ce (Harrison) Chapter 2 Recording Business Transactions. 2.1 Describe common types of accounts

Chapter 2 Recording Business Transactions. 2.1 Describe common types of accounts") Financial Accounting, 6Ce (Harrison) Chapter 2 Recording Business Transactions 2.1 Describe common types of accounts 1) Interest payable, income tax payable and salary payable are all examples of: A) accrued

Financial Accounting, 6Ce (Harrison) Chapter 2 Recording Business Transactions 2.1 Describe common types of accounts 1) Interest payable, income tax payable and salary payable are all examples of: A) accrued

Module 4. Instructions:

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled in the author s accounting course

Adjusting The Accounts

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

FOR MORE CLASSES VISIT

HCS 380 Week 1 Individual Assignment Reference Chart Reference Chart Instructions: FOR MORE CLASSES VISIT www.hcs380rank.com Create a chart detailing the three different forms of business organizations

HCS 380 Week 1 Individual Assignment Reference Chart Reference Chart Instructions: FOR MORE CLASSES VISIT www.hcs380rank.com Create a chart detailing the three different forms of business organizations

Chapter 3 The Adjusting Process

Instant download and all chapters Solution Manual Horngren s Financial Managerial Accounting 4th Edition Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura https://testbankdata.com/download/solution-manual-horngrens-financialmanagerial-accounting-4th-edition-tracie-l-nobles-brenda-l-mattison-ella-maematsumura/

Instant download and all chapters Solution Manual Horngren s Financial Managerial Accounting 4th Edition Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura https://testbankdata.com/download/solution-manual-horngrens-financialmanagerial-accounting-4th-edition-tracie-l-nobles-brenda-l-mattison-ella-maematsumura/

Assessment Schedule 2011 Accounting: Prepare financial statements and related accounting entries for sole proprietors (90224)

") NEA Level 2 Accounting (90224) 2011 page 1 of 6 Assessment Schedule 2011 Accounting: Prepare financial statements and related accounting entries for sole proprietors (90224) Statement Part A $ $ Bowling

NEA Level 2 Accounting (90224) 2011 page 1 of 6 Assessment Schedule 2011 Accounting: Prepare financial statements and related accounting entries for sole proprietors (90224) Statement Part A $ $ Bowling

Week 5, Chap 4 Part 2

Slide 1 Week 5, Chap 4 Part 2 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal Objective Prepare compound journal entries. McGraw-Hill 2007 The McGraw-Hill

Slide 1 Week 5, Chap 4 Part 2 The General Journal and the General Ledger Instructor: Michael Booth Slide 2 The General Journal Objective Prepare compound journal entries. McGraw-Hill 2007 The McGraw-Hill

SinoPac Holdings. CEO Forum by HSBC. March 11 th, 2013

SinoPac Holdings CEO Forum by HSBC March 11 th, 2013 Disclaimer This presentation and the presentation materials distributed herewith may include forward-looking statements. 2012/3Q financial data are

SinoPac Holdings CEO Forum by HSBC March 11 th, 2013 Disclaimer This presentation and the presentation materials distributed herewith may include forward-looking statements. 2012/3Q financial data are

HCS 380 Week 1 Individual Assignment Reference Chart Reference Chart Instructions: For more course tutorials visit www.tutorialrank.com Create a chart detailing the three different forms of business organizations

HCS 380 Week 1 Individual Assignment Reference Chart Reference Chart Instructions: For more course tutorials visit www.tutorialrank.com Create a chart detailing the three different forms of business organizations

Errors Not Affecting the Trial Balance

Errors Not Affecting the Trial Balance With these types of errors, the debit and credit columns of the Trial Balance will still be the same total. These errors are corrected by means of JOURNAL ENTRIES.

Errors Not Affecting the Trial Balance With these types of errors, the debit and credit columns of the Trial Balance will still be the same total. These errors are corrected by means of JOURNAL ENTRIES.

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty

Chapter 2 Review of the Accounting Process AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty

東吳大學 104 學年度轉學生 ( 含進修學士班轉學生 ) 招生考試試題第 1 頁, 共 6 頁

招生考試試題第 1 頁, 共 6 頁") 東吳大學 104 學年度轉學生 ( 含進修學士班轉學生 ) 招生考試試題第 1 頁, 共 6 頁 系考試級時間科本科 目總分作答規定 a. 本試卷請依國際會計準則 (IAS) 或國際財務報導準則 (IFRS) 之規定作答 b. 除題目另有說明, 答案請四捨五入計算至整數位 c. 分錄之會計科目請以英文作答 d. 若為計算題, 務請列示計算過程, 否則不予計分 試題 ( 共計 10 大題, 請小心作答,

東吳大學 104 學年度轉學生 ( 含進修學士班轉學生 ) 招生考試試題第 1 頁, 共 6 頁 系考試級時間科本科 目總分作答規定 a. 本試卷請依國際會計準則 (IAS) 或國際財務報導準則 (IFRS) 之規定作答 b. 除題目另有說明, 答案請四捨五入計算至整數位 c. 分錄之會計科目請以英文作答 d. 若為計算題, 務請列示計算過程, 否則不予計分 試題 ( 共計 10 大題, 請小心作答,

HS Accounting I 2013 Business and Technology

Course Description Students will learn the fundamentals and principles of double-entry accounting for service and merchandising businesses. This course focuses on financial reports along with transactions,

Course Description Students will learn the fundamentals and principles of double-entry accounting for service and merchandising businesses. This course focuses on financial reports along with transactions,

1. The primary objective of financial reporting is to provide useful information to external decision makers.

Chapter 02 Investing and Financing Decisions and the Accounting System True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers.

Chapter 02 Investing and Financing Decisions and the Accounting System True / False Questions 1. The primary objective of financial reporting is to provide useful information to external decision makers.