2008 Half Year Results. 30 July 2008

|

|

|

- Joan Summers

- 5 years ago

- Views:

Transcription

1 1

2 2008 Half Year Results 30 July

3 This material may be deemed to include forward-looking statements within the meaning of Section 27A of the US Securities Act of 1933 and Section 21E of the US Securities Exchange Act of These forward-looking statements are only predictions and you should not rely unduly on them. Actual results might differ materially from those projected in any such forward-looking statements, which involve known and unknown risks, uncertainties and other factors that may cause our or our industry s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by the forward-looking statements. In evaluating forward-looking statements, which are generally identifiable by use of the words may, will, should, expect, anticipate, estimate, believe, intend or project or the negative of these words or other variations on these words or comparable terminology, you should consider various factors including the risks outlined in our Form 20-F filed with the SEC. Although we believe the expectations reflected in forward-looking statements are reasonable we cannot guarantee future results, levels of activity, performance or achievements. This presentation should be viewed in conjunction with our periodic interim and annual reports and registration statements filed with the Securities and Exchange Commission, copies of which are available from Cadbury plc, Cadbury House, Sanderson Road, Uxbridge UB8 1DH, UK. 3

4 4

5 Roger Carr Chairman

6 6

7 Todd Stitzer Chief Executive Officer Results Overview

8 First Half 2008: Strong Delivery Against Our Scorecard Performance Scorecard Organic revenue growth of 4%-6% pa Total confectionery share gain Mid-teen trading margins by end 2011 Strong dividend growth Efficient balance sheet Growth in ROIC Organic revenue growth +7% : ahead of goal range Fourth consecutive year of global share gain Underlying operating margins +190bps Price realisation covers input costs increases Dividends +6% Successful bond refinancing Reviewing structure of Australian Beverages Confident of strong growth in ROIC and earnings in

9 Confectionery Market Growth Momentum Continues in 2008 Source: IRI/Nielsen 9

10 Robust Developed Market Growth Through Economic Cycles UK Chocolate Market Growth Left-axis (data indexed to 100) Chocolate volume Chocolate value Source: BCCCA, Office of National Statistics Right-axis Real GDP growth rate (%) 10

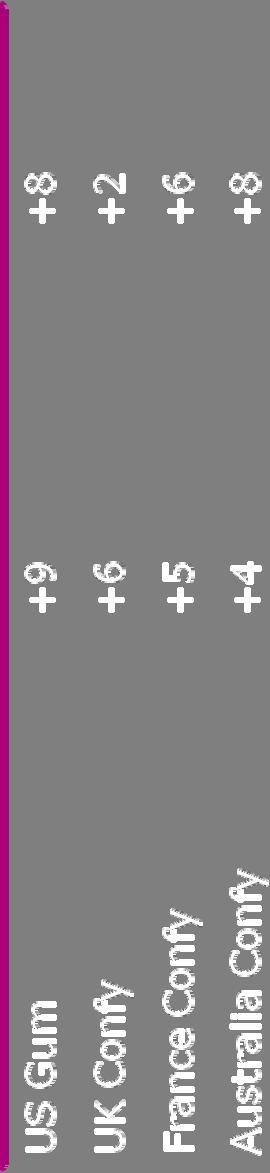

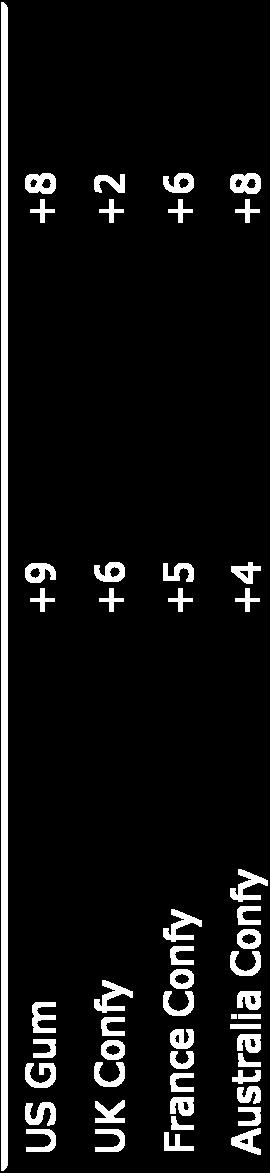

11 And Own-Label Penetration Remains Low Own-Label Penetration (% of total sales) Grocery Market Confectionery UK 38% 7% US 15% 2% Australia 11% 4% France 20% 8% Mexico 2% 1% India 1% 1% Source: Euromonitor/Mintel/IRI 11

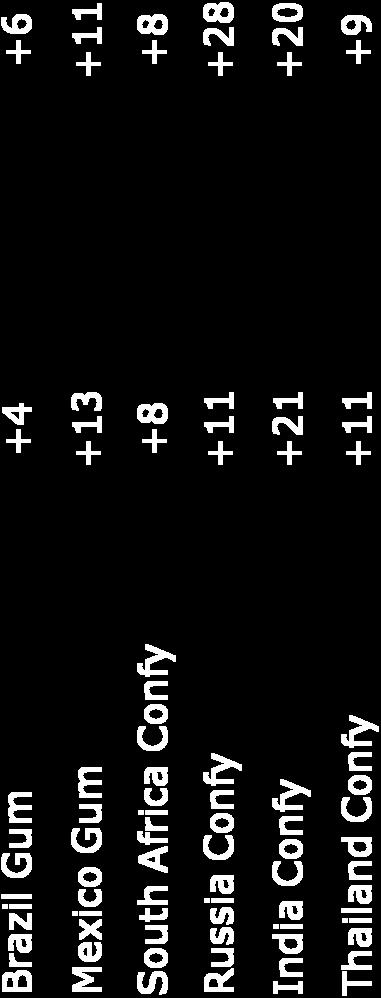

12 Emerging Market Growth Resilient Through Economic Cycles (%) Confectionery Market Growth BRIC* Markets Real GDP growth rate Aggregate confectionery growth rate * Brazil, Russia, India, China Source: Euromonitor, Goldman Sachs 12

13 Our Growth Momentum Continues in 2008 First half growth ahead of market and our four year trend Cadbury Confectionery Revenue Growth 6.2% 6.5% 7.1% 7.3% Cadbury 4-year average 6.2% pa 4.2% Market 4-year average 5.1% pa H 2008 Note: growth rates rebased to prior period exchange rates 13

14 With Double Digit Growth in Emerging Markets First half growth ahead of market and our four year trend Cadbury 4-year average 12% pa IH growth 13% Market 4-year average 9% pa H

15 And Strong Growth From All Our Categories Chocolate +6% Gum +10% Candy +7% 15

16 A Strengthened Total Confectionery Platform Global Confectionery Share +120bps share gain $ share Cadbury 9.2% 10.1% 10.4% Mars 9.5% 9.0% 9.0% Nestle 7.5% 7.6% 7.6% Wrigley 4.4% 5.7% 5.8% Hershey 5.7% 5.4% 5.1% Kraft 4.8% 4.4% 4.5% Ferrero 4.1% 4.2% 4.1% Source: Euromonitor

17 With Strong #1 Position Outside the US and in Emerging Markets Confectionery Market Shares 2007 $ share Outside US #1 positions in top 50* Emerging markets Cadbury 11.6% % Mars/Wrigley 9.5% % Nestle 8.1% 5 8.0% Kraft 5.3% 3 5.1% Ferrero 4.7% 1 2.3% * Top 50 markets account for 93% of global confectionery Source: Euromonitor

18 Growth: Fewer, Faster, Bigger, Better Governing Objective To Deliver Superior Shareowner Returns Vision Be the World s BIGGEST and BEST Confectionery Company Performance Scorecard Organic revenue growth of 4%-6% pa Total confectionery share gain Mid-teen trading margins by end 2011 Strong dividend growth Efficient balance sheet Growth in ROIC Priorities 1. Growth: fewer, faster, bigger, better 2. Efficiency: relentless focus on cost & efficiency 3. Capabilities: ensure world class quality 1.1 Category focus for scale & simplicity 1.1 Category focus for scale & simplicity 1.2 Drive advantaged, consumer preferred brands & products 1.2 Drive advantaged, consumer preferred brands & products 1.3 Accelerate white space market entry via Smart Variety 1.3 Accelerate white space market entry via Smart Variety 1.4 Create advantaged customer partnerships via total confectionery solutions 1.4 Create advantaged customer partnerships via total confectionery solutions 1.5 Expand platforms through acquisition 1.5 Expand platforms through acquisition 18

19 Driving our Focus Brands 13 Focus Brands +9% 19

20 Our Focus Markets 12 Focus Markets +9% 20

21 And Focus Global Customers Focus Global Customers +7% 21

22 Chocolate: Cadbury Dairy Milk CDM +9% 22

23 Candy: Eclairs Growth driven by successful format and flavour innovation Stick Pack in China Affordable trader friendly packs in South Africa Eclairs 23% 23

24 Gum: Longer Lasting Gum Centre-Filled Gum Launched in 2005 Sold in 25 countries Annual revenues c 250m Longer-Lasting Gum Launched in 2006 Sold in 12 countries Annual revenues c 180m Trident +12% 24

25 First Half 2008: Strong Commercial Delivery Revenue +7% Chocolate +6% Candy +7% Gum +10% Focus brands +9% Focus markets +9% Focus customers +7% Emerging markets +13% 2007 market share +30bps 25

26 26

27 Ken Hanna Chief Financial Officer Financial Review

28 Key Messages Delivery Growth momentum Efficiency programme Capital efficiency 28

29 Our Performance Scorecard Governing Objective To Deliver Superior Shareowner Returns Vision Be the World s BIGGEST and BEST Confectionery Company Performance Scorecard Organic revenue growth of 4%-6% pa Total confectionery share gain Mid-teen trading margins by end 2011 Strong dividend growth Efficient balance sheet Growth in ROIC Priorities 1. Growth: fewer, faster, bigger, better 2. Efficiency: relentless focus on cost & efficiency 3. Capabilities: ensure world class quality Organic revenue growth of 4%-6% pa Total confectionery share gain Mid-teen trading margins by end 2011 Strong dividend growth Efficient balance sheet Growth in ROIC 29

30 Revenue and Profit Growth Half Year ( m) Continuing Operations 2008 Re-presented 2007 % % (constant currency) Revenue 2,653 2,326 14% 7% Underlying profit from operations* % 35% margin 9.3% 7.2% +210bps +190bps Associates 4 5 Underlying net finance cost (29) (20) Underlying profit before tax % 33% Underlying taxation (65) (46) Underlying profit after tax % 35% Pro forma EPS 11.7p 8.0p 46% 34% Pro forma no. underlying shares 1,345 1,335 * Profit from operations before intangibles amortisation, goodwill impairment, restructuring, nontrading items and IAS39 adjustment 30

31 Growth Momentum Continuing First half revenue performance builds on strong run-rate Cadbury Confectionery Revenue Growth 8.0% 7.1% 7.3% 6.5% 6.2% 6.1% 4.2% 6.2% Cadbury CAGR % market CAGR H H H 2008 Note: growth rates rebased to prior period exchange rates 31

32 Regional Revenue Growth Drivers 46m +8.2% 170m +7.3% 33m +4.6% 10m +2.6% 81m +12.4% Developed Emerging 53% of growth 47% of growth BIMA Europe Americas Asia Pacific Group Base business growth (excluding FX and effect of acquisitions and disposals) 32

33 Growth Drivers: Volume, Price & Mix 7% 4% price/mix 7% 6% price/mix Price Realisation Format changes Promotions Mix Focus Brand price/mix up 5% Volume 3% vol 1% vol SKU rationalisation Portfolio review 1% volume impact FY H 2008 Focus Brand volumes up 4% 33

34 Mid-teens Margins by 2011 Central Costs Mix/Leverage Reinvestment SG&A Portfolio Cost Headwinds Supply Chain rationalisation 2007 Underperforming 2011 markets 34

35 Regional Underlying Profit Drivers 11m (2)m 9.1% 30m 6m 14m 0m 7.2% H BIMA Europe Americas APAC Group M&A H At constant currency Note: Regional uplifts given pre allocation of Business Improvement Costs 35

36 Run Rate Margin Operating margin improvement* Constant Currency Actual Currency 2H bps +70 bps 1H bps +210 bps Last Twelve Months +130 bps +130 bps *(excl. Business Improvement Costs) 36

37 Progress On Central Costs m Central costs pre BIC (69) (58) As percentage of revenue 3.0% 2.2% Reallocation Business Improvement Costs 4 (3) Revised central cost base (65) (61) As percentage of revenue 2.8% 2.3% Benefit of cost savings initiatives coming through On track for our target of below 2% of revenue 37

38 Americas SG&A Programme Move from 5 to 3 business units Eliminating duplication Functions aggregated for scale Double hatting 15% headcount reduction in G&A across the Americas SG&A down by 230bps 38

")

39 Britain & Ireland Supply Chain Reconfiguration Coolock (Ireland) headcount reduction 30% Closure of Somerdale and move of Milk Tray from Dublin Coolock Sheffield Bournville to Poland Somerdale Bournville Warsaw - UK headcount reduction by Wroclaw 2010 c.700 Skarbimierz 39

40 Focused Production at Scale Sites Skarbimierz Wroclaw Bournville 40

41 Portfolio Rationalisation in Egypt Major reconfiguration project to revitalise business and materially improve margins Improved profitability in lower income segments by changing the value proposition Reduced overheads to improve efficiencies 200 heads Accelerated growth in premium segments 41

42 Commodity Cost Increases m H average 2007 FY average H average % Change vs. FY 2007 Current (2) World sugar, c/lb (1) % 13.8 Cocoa, /tonne (1) ,306 37% 1,408 Oil, $/barrel (1) % 127 Milk (3), p/litre % 27.2 Effect of oil prices feeding through into 2H and beyond Cocoa - lagged impact of cost increases 5-6% increase in commodity costs for 2008 Commodity increases being managed by price realisation (1) Source: Bloomberg (2) As at 28 July 2008 (3) UK liquid milk farmgate price 42

43 Progress in Underperforming Markets Half year ( m) Sales Underlying operating loss (14) (10) Russia impacted by change to distribution platform Underperforming markets expected to show continued progress in the second half Aggregate of Nigeria, Russia and China. Values at the prevailing FX rate for the period 43

44 Restructuring Costs Half year ( m) Restructuring Restructuring - Vision into Action (22) (49) Americas Beverages separation costs (4) (14) Gumlink (8) (3) Acquisition integration - (5) Total (34) (71) Total demerger costs (including tax, financing and discontinued) around 145m (07/08) 44

45 Debt Profile Maintaining BBB rating; aiming for BBB+ Issued a new 350m 10-year bond at 7.25% in July 2008 Average interest rates will trend higher as older debt matures Over 1bn of undrawn bank facilities Bond Debt by Maturity billion 45

46 Balance Sheet Ratios Dec 2007 Jun 2008 Net debt m 3,219m 1,700m Net debt/ebitda # 2.5x 2.2x EBITDA # /Net interest 7.6x 8.6x EBIT/Net interest 5.9x 6.3x Note: 31 December 07 includes Americas beverages business 30 June 2008 EBITDA, EBIT and net interest on a continuing group basis Ratios calculated for the total group on a rolling 12 month basis # EBITDA is defined as earnings before interest, tax, depreciation, intangibles amortisation, goodwill impairment, restructuring costs, non-trading items, IAS 39 adjustment and excludes associates 46

47 47

48 Todd Stitzer Chief Executive Officer Summary and Close

49 First Half 2008: Summary Strong first revenue and margin performance Revenues ahead of goal range Strong growth across all categories Excellent margin progress Tight cost control Good price realisation Positive mix Benefits of VIA cost reduction 49

50 2008 Outlook Confectionery: a highly defensive category Demand has remained strong Cycling demanding 2H 2007 comparatives Strong revenue momentum and commercial programmes Detailed cost reduction plans Revenues around top end of goal range Margins in line with market consensus 50

51 Conclusion Revisiting cost structure Reviewing management talent pool Reappraising portfolio of assets and businesses Maintaining commitment to marketing and innovation Underpinning commitment to mid-teens margins by

52 52

53 Supplementary Information 53

54 Sales Analysis Half year ( m) 2007 Base Business M&A FX effects 2008 BIMA (26) Europe Americas (15) Asia Pacific (4) Central Total Group 2, (11) 168 2,653 54

55 Underlying Profit from Operations Half year ( m) 2007 Base Business M&A Change in BIC * FX effects 2008 BIMA (2) Europe 30-2 (4) 7 35 Americas (1) Asia Pacific 40 6 (1) Central costs (65) 11 - (7) - (61) Total (2) Underlying profit from operations before associates, intangibles amortisation, goodwill impairment, restructuring, non-trading items and IAS39 adjustment * Business improvement costs 55

56 Re-presented FY07 Income Statement, 1H and FY Re-presented H FY # Revenue 2,326 5,093 Underlying profit from operations * Associates 5 8 Net finance cost (20) (50) Underlying profit before tax * Restructuring (34) (165) Amortisation and impairment (15) (18) Non-trading items (2) 2 IAS 39 adjustment 10 4 Reported profit before tax Taxation (48) (112) Discontinued operations Minorities - (2) Reported earnings * Before intangibles amortisation, goodwill impairment, restructuring, non-trading items and IAS39 adjustment # 2007 results have been re-presented to include Americas Beverages within discontinued operations 56

57 EPS Drivers Half year ( m) Continuing ops UEPS pro forma % p - Base business growth 3.4p 42% Acquisitions and disposals (0.6)p (7)% Foreign exchange 1.0p 12% Change in number of shares (0.1)p (1)% p 46% 57

58 Technical Guidance FY 2008 Ongoing business improvement cost: Capital expenditure (confectionery only, incl. VIA) c. 0.5% of revenue c 400m VIA restructuring (P&L): c. 130m Underlying net interest rate: 6.0% Underlying tax rate: circa 29% 58

59 Separation costs Separation costs recognised in 2007 P&L 45m 2008 separation costs P&L impact (all 1H) discontinued: 98m 2008 confectionery separation costs P&L impact (all 1H) restructuring: 14m Total separation costs (P&L) 157m Net finance and tax benefit (14)m Net total P&L impact 143m Separation costs (cash, 2007) 35m Separation costs (cash, 1H 2008) 150m Separation costs expected in H2 (1) 40m Total separation costs cash (2) 260m (1) Separation costs expected in H2 and those settled by DPSG (2) Includes c. 35m costs paid post separation by DPSG. Net impact of post 2008 separation cash flows broadly neutral 59

60 Non-Trading Items Half year ( m) Disposal of properties 14 1 Disposal of non-core businesses Impairment of China property, plant and equipment (4) (7) (12) - Reported (2) (6) 60

61 Balance Sheet Half year ( m) Non-current assets 4,372 5,137 Net working capital Assets held for sale less associated liabilities 2,851 3 Net retirement benefit liability (66) (18) Provisions and deferred tax liabilities (387) (458) Net borrowings continuing group (3,062) (1,700) Net assets 3,803 3,015 Ordinary shareholders funds 3,793 3,006 Minority interests 10 9 Total capital employed 3,803 3,015 61

62 Cash Flow Half Year ( m) Underlying profit from operations* Restructuring (41) (78) Depreciation Other items (20) (12) Working capital (155) (163) Cash generated from operations Capital expenditure (178) (217) Disposal of fixed assets 31 4 Interest (81) (105) Tax (excluding disposals) (138) (87) Pension funding Free cash flow 2 (109) 2007 includes full period of Americas beverages, 2008 includes Americas beverages to date of demerger * Profit from operations before intangibles amortisation, goodwill impairment, restructuring, non-trading items and IAS39 adjustment Includes profit from discontinued operations 62

63 Borrowing Profile Half year Debt maturity profile Less than 1 year 43% 29% 1-3 years 38% 42% More than 3 years 19% 29% Fixed rate debt: % total debt 64% 73% Average length of fix 2.6yrs 2.2yrs Average interest rate 4.4% 4.5% Group average interest rate 5.2% 5.5% 2007 includes full period of Americas beverages 2008 average interest rate on confectionery business only Note: 2008 figures are as at 30 June 2008, prior to the issue of the 350m bond 63

64 Sales, Profits and Borrowings by Currency Half year ( m) 2008 % Sales generated in: US dollars % Sterling % Euro % Australian dollars % Other 1,133 43% Underlying operating profit* generated in: US dollars 49 20% Sterling (25) (10)% Euro 44 18% Australian dollars 35 14% Other % Net borrowing held in: US dollars % Sterling % Euro 61 3% Other 68 4% * Profit from operations before intangibles amortisation, restructuring, non-trading items and IAS39 adjustment 64

65 Exchange Rates Rate vs Sterling H average H average % mvt average US $ % Canadian $ (10.7)% Euro (12.5)% Australian $ (11.9)% South African Rand % Brazilian Real (16.5)% Mexican Peso (2.4)% 65

2009 Half Year Results. 29 July 2009

1 2009 Half Year Results 29 July 2009 2 Roger Carr Chairman 3 Agenda Chairman s comments Roger Carr First Half Highlights Todd Stitzer Operational and Financial Review Andrew Bonfield Strategic Update

1 2009 Half Year Results 29 July 2009 2 Roger Carr Chairman 3 Agenda Chairman s comments Roger Carr First Half Highlights Todd Stitzer Operational and Financial Review Andrew Bonfield Strategic Update

2007 Interim Results 1 August 2007

2 2007 Interim Results 1 August 2007 This material may be deemed to include forward-looking statements within the meaning of Section 27A of the US Securities Act of 1933 and Section 21E of the US Securities

2 2007 Interim Results 1 August 2007 This material may be deemed to include forward-looking statements within the meaning of Section 27A of the US Securities Act of 1933 and Section 21E of the US Securities

Cadbury Reports Record 2008 Results Strong Growth in Sales, Margins and Earnings

25 February 2009 2008 Highlights Cadbury Reports Record 2008 Results Strong Growth in Sales, Margins and Earnings Base business 1 revenue up 7%; strong growth across emerging markets and focus brands o

25 February 2009 2008 Highlights Cadbury Reports Record 2008 Results Strong Growth in Sales, Margins and Earnings Base business 1 revenue up 7%; strong growth across emerging markets and focus brands o

Mondelēz International 2013 Results. February 12, 2014

Mondelēz International 2013 Results February 12, 2014 1 Forward-looking statements This slide presentation contains a number of forward-looking statements. Words, and variations of words, such as will,

Mondelēz International 2013 Results February 12, 2014 1 Forward-looking statements This slide presentation contains a number of forward-looking statements. Words, and variations of words, such as will,

Higher. performance, Higher. value. Reject Kraft s offer

Higher performance, Higher value Reject Kraft s offer In addition to this document, we have published an Investor Presentation. This presentation and the recorded webcast are available online at: www.cadburyinvestors.com

Higher performance, Higher value Reject Kraft s offer In addition to this document, we have published an Investor Presentation. This presentation and the recorded webcast are available online at: www.cadburyinvestors.com

Full-year results 2017 Conference. February 15, 2018 Nestlé full-year results 2017

Full-year results 2017 Conference 1 Disclaimer This presentation contains forward looking statements which reflect Management s current views and estimates. The forward looking statements involve certain

Full-year results 2017 Conference 1 Disclaimer This presentation contains forward looking statements which reflect Management s current views and estimates. The forward looking statements involve certain

2017 Full Year. Results Presentation. 21 February 2018

2017 Full Year Results Presentation 21 February 2018 CAUTIONARY STATEMENT 2017 Full Year Results Slide 2 Full Year Highlights 2017 Full Year Results Presentation 8TH YEAR OF DOUBLE-DIGIT GROWTH 2017 FINANCIAL

2017 Full Year Results Presentation 21 February 2018 CAUTIONARY STATEMENT 2017 Full Year Results Slide 2 Full Year Highlights 2017 Full Year Results Presentation 8TH YEAR OF DOUBLE-DIGIT GROWTH 2017 FINANCIAL

Mondelēz International Q Results. July 27, 2016

Mondelēz International Q2 2016 Results July 27, 2016 1 Forward-Looking Statements This presentation contains a number of forward-looking statements. Words, and variations of words, such as will, expect,

Mondelēz International Q2 2016 Results July 27, 2016 1 Forward-Looking Statements This presentation contains a number of forward-looking statements. Words, and variations of words, such as will, expect,

Q4 & FY 2018 Results. January 30, 2019

Q4 & FY 2018 Results January 30, 2019 This presentation contains a number of forwardlooking statements. Words, and variations of words, such as will, expect, may, believe, estimate, deliver, potential,

Q4 & FY 2018 Results January 30, 2019 This presentation contains a number of forwardlooking statements. Words, and variations of words, such as will, expect, may, believe, estimate, deliver, potential,

Brambles reports results for the half-year ended 31 December 2017

Brambles Limited ABN 89 118 896 021 Level 10, 123 Pitt Street Sydney NSW 2000 Australia GPO Box 4173 Sydney NSW 2001 Tel +61 2 9256 5222 Fax +61 2 9256 5299 www.brambles.com 19 February 2018 The Manager

Brambles Limited ABN 89 118 896 021 Level 10, 123 Pitt Street Sydney NSW 2000 Australia GPO Box 4173 Sydney NSW 2001 Tel +61 2 9256 5222 Fax +61 2 9256 5299 www.brambles.com 19 February 2018 The Manager

Mondelēz International Reports Third Quarter 2013 Results

Contacts: Michael Mitchell (Media) Dexter Congbalay (Investors) +1-847-943-5678 +1-847-943-5454 news@mdlz.com ir@mdlz.com Mondelēz International Reports Third Quarter 2013 Results Q3 net revenues increased

Contacts: Michael Mitchell (Media) Dexter Congbalay (Investors) +1-847-943-5678 +1-847-943-5454 news@mdlz.com ir@mdlz.com Mondelēz International Reports Third Quarter 2013 Results Q3 net revenues increased

ARYZTA AG. H1 Results, FY March 2017

ARYZTA AG H1 Results, FY 2017 13 March 2017 Forward Looking Statement This document contains forward looking statements which reflect the Board of Directors' current views and estimates. The forward looking

ARYZTA AG H1 Results, FY 2017 13 March 2017 Forward Looking Statement This document contains forward looking statements which reflect the Board of Directors' current views and estimates. The forward looking

2017 HALF-YEAR RESULTS

I 1 I 2017 HALF-YEAR RESULTS July 27, 2017 Emmanuel Faber, CEO Cécile Cabanis, CFO I 2 I This document is presented by Danone. It contains certain forward-looking statements concerning Danone. In some

I 1 I 2017 HALF-YEAR RESULTS July 27, 2017 Emmanuel Faber, CEO Cécile Cabanis, CFO I 2 I This document is presented by Danone. It contains certain forward-looking statements concerning Danone. In some

INTERIM RESULTS July 2016

28 July 2016 Nicandro Durante Chief Executive Strong performance driven by organic growth Strong top-line growth volume and revenue Excellent corporate and GDB share growth continues Benefits from 2015

28 July 2016 Nicandro Durante Chief Executive Strong performance driven by organic growth Strong top-line growth volume and revenue Excellent corporate and GDB share growth continues Benefits from 2015

SABMiller plc. Full year results Twelve months ended 31 March Jamie Wilson, Chief Financial Officer Gary Leibowitz, SVP, Investor Relations

SABMiller plc Full year results Twelve months ended 31 March 2012 Jamie Wilson, Chief Financial Officer Gary Leibowitz, SVP, Investor Relations 24 May 2012 Forward looking statements This presentation

SABMiller plc Full year results Twelve months ended 31 March 2012 Jamie Wilson, Chief Financial Officer Gary Leibowitz, SVP, Investor Relations 24 May 2012 Forward looking statements This presentation

RPC GROUP PLC. Bringing Packaging to Life. 2014/15 Interim Results 27 November Company of. the Year. Processor of. the Year

Company of the Year Processor of the Year Bringing Packaging to Life RPC GROUP PLC 2014/15 Interim Results 27 November 2014 2 AGENDA Business Review Financial Review Outlook 3 BUSINESS REVIEW PROGRESS:

Company of the Year Processor of the Year Bringing Packaging to Life RPC GROUP PLC 2014/15 Interim Results 27 November 2014 2 AGENDA Business Review Financial Review Outlook 3 BUSINESS REVIEW PROGRESS:

Full-Year & Q Results. January 31, 2018

Full-Year & Q4 2017 Results January 31, 2018 Forward-looking statements This presentation contains a number of forward-looking statements. Words, and variations of words, such as will, expect, could, likely,

Full-Year & Q4 2017 Results January 31, 2018 Forward-looking statements This presentation contains a number of forward-looking statements. Words, and variations of words, such as will, expect, could, likely,

Full Year Results 2014/15. Analysts Conference November 4, 2015

Full Year Results 2014/15 Cautionary note Certain statements in this presentation regarding the business of Barry Callebaut are of a forwardlooking nature and are therefore based on management s current

Full Year Results 2014/15 Cautionary note Certain statements in this presentation regarding the business of Barry Callebaut are of a forwardlooking nature and are therefore based on management s current

2005 full year results conference call

2005 full year results conference call - February 2006 2005 full year results conference call 2 2005 full year results conference call - February 2006 2005: Delivering The Nestle Model: Improvement in

2005 full year results conference call - February 2006 2005 full year results conference call 2 2005 full year results conference call - February 2006 2005: Delivering The Nestle Model: Improvement in

Disclaimer: Forward Looking Statements

9 August 2018 Disclaimer: Forward Looking Statements This presentation/announcement may contain forward looking statements with projections regarding, among other things, the Group s strategy, revenues,

9 August 2018 Disclaimer: Forward Looking Statements This presentation/announcement may contain forward looking statements with projections regarding, among other things, the Group s strategy, revenues,

Welcome to the Full-Year 2016 Conference. February 16, 2017 Nestlé Full-Year Results 2016

Welcome to the Full-Year 2016 Conference 1 Disclaimer This presentation contains forward looking statements which reflect Management s current views and estimates. The forward looking statements involve

Welcome to the Full-Year 2016 Conference 1 Disclaimer This presentation contains forward looking statements which reflect Management s current views and estimates. The forward looking statements involve

SABMiller plc. Interim results Half year ended 30 September November 2005 also available on website

SABMiller plc Interim results Half year ended 30 September 2005 10 November 2005 also available on website www.sabmiller.com Forward-looking statements This presentation includes forward-looking statements.

SABMiller plc Interim results Half year ended 30 September 2005 10 November 2005 also available on website www.sabmiller.com Forward-looking statements This presentation includes forward-looking statements.

AEGIS GROUP PLC 2008 ANNUAL RESULTS. 19 March 2009

AEGIS GROUP PLC 2008 ANNUAL RESULTS 19 March 2009 AGENDA OVERVIEW OF RESULTS John Napier FINANCIAL REVIEW Alicja Lesniak OUTLOOK John Napier Q&A Aegis Group plc Page 2 OVERVIEW OF RESULTS John Napier,

AEGIS GROUP PLC 2008 ANNUAL RESULTS 19 March 2009 AGENDA OVERVIEW OF RESULTS John Napier FINANCIAL REVIEW Alicja Lesniak OUTLOOK John Napier Q&A Aegis Group plc Page 2 OVERVIEW OF RESULTS John Napier,

Half-year results July 27, 2017 Nestlé half-year results 2017

Half-year results 2017 1 Disclaimer This presentation contains forward looking statements which reflect Management s current views and estimates. The forward looking statements involve certain risks and

Half-year results 2017 1 Disclaimer This presentation contains forward looking statements which reflect Management s current views and estimates. The forward looking statements involve certain risks and

SABMiller plc US annual results presentation Year ended March 31, 2014

SABMiller plc US annual results presentation Year ended March 31, 2014 Presented by Jamie Wilson, Chief Financial Officer Gary Leibowitz, SVP Internal & Investor Engagement Forward looking statements This

SABMiller plc US annual results presentation Year ended March 31, 2014 Presented by Jamie Wilson, Chief Financial Officer Gary Leibowitz, SVP Internal & Investor Engagement Forward looking statements This

2010 Full Year Results Conference Call. James Singh Chief Financial Officer

2010 Full Year Results Conference Call James Singh Chief Financial Officer Disclaimer This presentation contains forward looking statements which reflect Management s current views and estimates. The forward

2010 Full Year Results Conference Call James Singh Chief Financial Officer Disclaimer This presentation contains forward looking statements which reflect Management s current views and estimates. The forward

Electrocomponents 2017 half-year financial results. 18 November 2016

Electrocomponents 2017 half-year financial results 18 November 2016 Agenda Overview of results Lindsley Ruth Financial results and performance update David Egan Performance Improvement Plan Lindsley Ruth

Electrocomponents 2017 half-year financial results 18 November 2016 Agenda Overview of results Lindsley Ruth Financial results and performance update David Egan Performance Improvement Plan Lindsley Ruth

Forward looking statements

Presentation to investors April 2008 1 Forward looking statements 2 This document contains certain forward-looking statements concerning Groupe DANONE. Although Groupe DANONE believes its expectations

Presentation to investors April 2008 1 Forward looking statements 2 This document contains certain forward-looking statements concerning Groupe DANONE. Although Groupe DANONE believes its expectations

Aegis Group plc Half Year Results. 27 August 2010

Aegis Group plc 2010 Half Year Results 27 August 2010 Agenda Introduction John Napier, Chairman Aegis Group overview Jerry Buhlmann, CEO Divisional review Aegis Media - Jerry Buhlmann, CEO Synovate Robert

Aegis Group plc 2010 Half Year Results 27 August 2010 Agenda Introduction John Napier, Chairman Aegis Group overview Jerry Buhlmann, CEO Divisional review Aegis Media - Jerry Buhlmann, CEO Synovate Robert

SABMiller plc. Full year results Twelve months ended 31 March Graham Mackay, Chief Executive Jamie Wilson, Chief Financial Officer.

SABMiller plc Full year results Twelve months ended 31 March 2012 Graham Mackay, Chief Executive Jamie Wilson, Chief Financial Officer 24 May 2012 Forward looking statements This presentation includes

SABMiller plc Full year results Twelve months ended 31 March 2012 Graham Mackay, Chief Executive Jamie Wilson, Chief Financial Officer 24 May 2012 Forward looking statements This presentation includes

July 26, 2017 LafargeHolcim Ltd 2015

Second Quarter 2017 Results Beat Hess, Chairman and Interim CEO Roland Köhler, Interim COO and Regional Head of Europe, Australia/NZ & Trading Ron Wirahadiraksa, CFO July 26, 2017 LafargeHolcim Ltd 2015

Second Quarter 2017 Results Beat Hess, Chairman and Interim CEO Roland Köhler, Interim COO and Regional Head of Europe, Australia/NZ & Trading Ron Wirahadiraksa, CFO July 26, 2017 LafargeHolcim Ltd 2015

April 1, 2011 Barry Callebaut H1 2010/11 results presentation

Half-Year Results 2010/11 Media presentation April 1, 2011 April 1, 2011 Barry Callebaut H1 2010/11 results presentation Cautionary note Certain statements in this presentation regarding the business of

Half-Year Results 2010/11 Media presentation April 1, 2011 April 1, 2011 Barry Callebaut H1 2010/11 results presentation Cautionary note Certain statements in this presentation regarding the business of

Carlsberg A/S. H interim results

Carlsberg A/S H1 2016 interim results Agenda H1 highlights Financial results Region performance Appendix Good H1 performance +140bp Organic GPaL margin improvement -1% +8% Organic decline in pro rata volumes

Carlsberg A/S H1 2016 interim results Agenda H1 highlights Financial results Region performance Appendix Good H1 performance +140bp Organic GPaL margin improvement -1% +8% Organic decline in pro rata volumes

Mondelēz International Reports Solid 2012 Results; Raises 2013 EPS Guidance

Contacts: Michael Mitchell (Media) Dexter Congbalay (Investors) +1-847-943-5678 +1-847-943-5454 news@mdlz.com ir@mdlz.com Mondelēz International Reports Solid 2012 Results; Raises 2013 EPS Guidance 2012

Contacts: Michael Mitchell (Media) Dexter Congbalay (Investors) +1-847-943-5678 +1-847-943-5454 news@mdlz.com ir@mdlz.com Mondelēz International Reports Solid 2012 Results; Raises 2013 EPS Guidance 2012

2017 Full Year Results. Tuesday 21 November 2017

2017 Full Year Results Tuesday 21 November 2017 Disclaimer Certain information included in the following presentation is forward looking and involves risks, assumptions and uncertainties that could cause

2017 Full Year Results Tuesday 21 November 2017 Disclaimer Certain information included in the following presentation is forward looking and involves risks, assumptions and uncertainties that could cause

Roadshow presentation 9 months Key Sales Figures 2016/17. July 2017

Roadshow presentation 9 months Key Sales Figures 2016/17 Agenda BC at a glance Highlights Q3 2016/17 Strategy & Outlook Page 2 BC at a glance Who are we? The heart and engine of the chocolate industry

Roadshow presentation 9 months Key Sales Figures 2016/17 Agenda BC at a glance Highlights Q3 2016/17 Strategy & Outlook Page 2 BC at a glance Who are we? The heart and engine of the chocolate industry

2007 half year results conference call

2007 half year results conference call 2007 half year results conference call - 15 August 2007 Disclaimer This presentation contains forward looking statements which reflect Management s current views

2007 half year results conference call 2007 half year results conference call - 15 August 2007 Disclaimer This presentation contains forward looking statements which reflect Management s current views

ARYZTA AG. FY 2016 Results. 26 September 2016

ARYZTA AG FY 2016 Results 26 September 2016 Forward Looking Statement This document contains forward looking statements which reflect management s current views and estimates. The forward looking statements

ARYZTA AG FY 2016 Results 26 September 2016 Forward Looking Statement This document contains forward looking statements which reflect management s current views and estimates. The forward looking statements

Britvic plc. Interims presentation 2015

Britvic plc Interims presentation 2015 Gerald Corbett Chairman John Gibney Chief Financial Officer Continued strong earnings growth in challenging trading conditions -0.7% +6.2% +60bps +11.6% 0.4x +9.8%

Britvic plc Interims presentation 2015 Gerald Corbett Chairman John Gibney Chief Financial Officer Continued strong earnings growth in challenging trading conditions -0.7% +6.2% +60bps +11.6% 0.4x +9.8%

Presented by Alan Clark, Chief Executive Domenic De Lorenzo, Chief Financial Officer

Presented by Alan Clark, Chief Executive Domenic De Lorenzo, Chief Financial Officer This presentation includes forward-looking statements with respect to certain of SABMiller plc s plans, current goals

Presented by Alan Clark, Chief Executive Domenic De Lorenzo, Chief Financial Officer This presentation includes forward-looking statements with respect to certain of SABMiller plc s plans, current goals

Ashmore Group plc. Results for six months ending 31 December February

Ashmore Group plc Results for six months ending 31 December 2017 8 February 2018 www.ashmoregroup.com Overview Accelerating growth and outperformance across Emerging Markets GDP growth driven by exports,

Ashmore Group plc Results for six months ending 31 December 2017 8 February 2018 www.ashmoregroup.com Overview Accelerating growth and outperformance across Emerging Markets GDP growth driven by exports,

SABMiller plc. F 12 first half results US call Six months ended September 30, November 17, 2011

SABMiller plc F 12 first half results US call Six months ended September 30, 2011 November 17, 2011 Jamie Wilson, Chief Financial Officer Gary Leibowitz, Senior Vice President, IR Forward looking statements

SABMiller plc F 12 first half results US call Six months ended September 30, 2011 November 17, 2011 Jamie Wilson, Chief Financial Officer Gary Leibowitz, Senior Vice President, IR Forward looking statements

Q Results. Strong start in May 3, 2016

Q1 2016 Results Strong start in 2016 May 3, 2016 Legal Disclaimer Information in this presentation may involve guidance, expectations, beliefs, plans, intentions or strategies regarding the future. These

Q1 2016 Results Strong start in 2016 May 3, 2016 Legal Disclaimer Information in this presentation may involve guidance, expectations, beliefs, plans, intentions or strategies regarding the future. These

ARYZTA AG. H1 Results, FY 2013 Fixed Income Investor Presentation 11 March 2013

ARYZTA AG H1 Results, FY 2013 Fixed Income Investor Presentation 11 March 2013 Forward Looking Statement This document contains forward looking statements which reflect management s current views and estimates.

ARYZTA AG H1 Results, FY 2013 Fixed Income Investor Presentation 11 March 2013 Forward Looking Statement This document contains forward looking statements which reflect management s current views and estimates.

Disclaimer: Forward Looking Statements

20 February 2018 Disclaimer: Forward Looking Statements This presentation/announcement may contain forward looking statements with projections regarding, among other things, the Group s strategy, revenues,

20 February 2018 Disclaimer: Forward Looking Statements This presentation/announcement may contain forward looking statements with projections regarding, among other things, the Group s strategy, revenues,

2017 Interim Results. Continuing Execution of Our Strategy. 3 August 2017

2017 Interim Results Continuing Execution of Our Strategy 3 August 2017 0 Disclaimer THIS PRESENTATION IS NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION, IN WHOLE OR IN PART, IN OR INTO THE UNITED STATES

2017 Interim Results Continuing Execution of Our Strategy 3 August 2017 0 Disclaimer THIS PRESENTATION IS NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION, IN WHOLE OR IN PART, IN OR INTO THE UNITED STATES

2013 Full Year Results Presentation 3 March 2014

2013 Full Year Results Presentation 3 March 2014 Wolfhart Hauser Chief Executive Officer Lloyd Pitchford Chief Financial Officer 1 Lloyd Pitchford Chief Financial Officer Financial Performance 2013 Full

2013 Full Year Results Presentation 3 March 2014 Wolfhart Hauser Chief Executive Officer Lloyd Pitchford Chief Financial Officer 1 Lloyd Pitchford Chief Financial Officer Financial Performance 2013 Full

DATATEC GROUP UNAUDITED INTERIM RESULTS FOR THE 6 MONTHS ENDED 31 AUGUST 2016

Technology Distribution Integration & Managed Services Consulting & Research UNAUDITED INTERIM RESULTS FOR THE 6 MONTHS ENDED 31 AUGUST 2016 AGENDA Results summary, market conditions & operational strategy

Technology Distribution Integration & Managed Services Consulting & Research UNAUDITED INTERIM RESULTS FOR THE 6 MONTHS ENDED 31 AUGUST 2016 AGENDA Results summary, market conditions & operational strategy

FULL YEAR RESULTS Conference call, February 2002

FULL YEAR RESULTS 2001 Conference call, February 2002 This presentation contains forward looking statements which reflect Management s current views and estimates. The forward looking statements involve

FULL YEAR RESULTS 2001 Conference call, February 2002 This presentation contains forward looking statements which reflect Management s current views and estimates. The forward looking statements involve

2017/18 Half Year Results De La Rue plc 21 November 2017

2017/18 Half Year Results De La Rue plc 21 November 2017 Page 1 Agenda Overview Martin Sutherland Financial performance Jitesh Sodha Strategic update Martin Sutherland Operational review Martin Sutherland

2017/18 Half Year Results De La Rue plc 21 November 2017 Page 1 Agenda Overview Martin Sutherland Financial performance Jitesh Sodha Strategic update Martin Sutherland Operational review Martin Sutherland

Mondelēz International Q Results. November 5, 2014

Mondelēz International Q3 2014 Results November 5, 2014 1 Forward-looking statements This slide presentation contains a number of forward-looking statements. Words, and variations of words, such as will,

Mondelēz International Q3 2014 Results November 5, 2014 1 Forward-looking statements This slide presentation contains a number of forward-looking statements. Words, and variations of words, such as will,

PRELIMINARY RESULTS February 2016

25 February 2016 Nicandro Durante Chief Executive A strong performance driven by market share growth Excellent underlying performance, despite significant FX headwinds Outstanding quality share performance,

25 February 2016 Nicandro Durante Chief Executive A strong performance driven by market share growth Excellent underlying performance, despite significant FX headwinds Outstanding quality share performance,

Q Results. October 29, 2018

Q3 2018 Results October 29, 2018 Forwardlooking Statements This presentation contains a number of forwardlooking statements. Words, and variations of words, such as will, expect, may, should, believe,

Q3 2018 Results October 29, 2018 Forwardlooking Statements This presentation contains a number of forwardlooking statements. Words, and variations of words, such as will, expect, may, should, believe,

Kerry Interim Results Presentation

Kerry - 2005 Interim Results Presentation Introduction and Overview Hugh Friel Financial Review Brian Mehigan Business Review Hugh Friel Prospects and Future Development Hugh Friel Q&A H1 2005: Solid Performance

Kerry - 2005 Interim Results Presentation Introduction and Overview Hugh Friel Financial Review Brian Mehigan Business Review Hugh Friel Prospects and Future Development Hugh Friel Q&A H1 2005: Solid Performance

Q SALES. Cécile Cabanis, CFO. October 17, 2017 I 1 I

Q3 2017 SALES October 17, 2017 Cécile Cabanis, CFO I 1 I DISCLAIMER This document is presented by Danone. It contains certain forward-looking statements concerning Danone. In some cases, you can identify

Q3 2017 SALES October 17, 2017 Cécile Cabanis, CFO I 1 I DISCLAIMER This document is presented by Danone. It contains certain forward-looking statements concerning Danone. In some cases, you can identify

SABMiller plc. First half results. 19 November Graham Mackay, Chief Executive Malcolm Wyman, CFO. Six months ended 30 September 2009

SABMiller plc First half results Six months ended 30 September 2009 19 November 2009 Graham Mackay, Chief Executive Malcolm Wyman, CFO Forward looking statements This presentation includes forward-looking

SABMiller plc First half results Six months ended 30 September 2009 19 November 2009 Graham Mackay, Chief Executive Malcolm Wyman, CFO Forward looking statements This presentation includes forward-looking

RESULTS FOR THE YEAR ENDED. 31 March 2018

RESULTS FOR THE YEAR ENDED 31 March 2018 SHARPEN ACCELERATE SIMPLIFY 2 Nick Hampton, Chief Executive Chris McLeish, Group VP Finance and Control AGENDA Financial Review Outlook Accelerating Business Performance

RESULTS FOR THE YEAR ENDED 31 March 2018 SHARPEN ACCELERATE SIMPLIFY 2 Nick Hampton, Chief Executive Chris McLeish, Group VP Finance and Control AGENDA Financial Review Outlook Accelerating Business Performance

Results presentation. For the year ended 31 March 2014

Results presentation For the year ended 31 March 214 The year in review 2 Improving operating environment Results impacted by strength of sterling against other operating currencies Equity markets Interest

Results presentation For the year ended 31 March 214 The year in review 2 Improving operating environment Results impacted by strength of sterling against other operating currencies Equity markets Interest

Presentation of results for the six months ended 30 th September st November 2017

Presentation of results for the six months ended 30 th September 2017 21 st November 2017 Cautionary statement This presentation contains forward looking statements that are subject to risk factors associated

Presentation of results for the six months ended 30 th September 2017 21 st November 2017 Cautionary statement This presentation contains forward looking statements that are subject to risk factors associated

Full-year results 2018

Full-year results 2018 Investor Call 1 Disclaimer This presentation contains forward looking statements which reflect Management s current views and estimates. The forward looking statements involve certain

Full-year results 2018 Investor Call 1 Disclaimer This presentation contains forward looking statements which reflect Management s current views and estimates. The forward looking statements involve certain

Aegis Group plc. 17 March 2011

Aegis Group plc 2010 Full Year Results 2010 Full Year Results 17 March 2011 Agenda Introduction John Napier, Chairman Aegis Group overview Jerry Buhlmann, CEO Divisional review Aegis Media - Jerry Buhlmann,

Aegis Group plc 2010 Full Year Results 2010 Full Year Results 17 March 2011 Agenda Introduction John Napier, Chairman Aegis Group overview Jerry Buhlmann, CEO Divisional review Aegis Media - Jerry Buhlmann,

Preliminary Results 2013 Imperial Tobacco Group PLC

Preliminary Results 2013 Imperial Tobacco Group PLC 5 November 2013 1 Disclaimer Certain statements in this document constitute or may constitute forward-looking statements. Any statement in this document

Preliminary Results 2013 Imperial Tobacco Group PLC 5 November 2013 1 Disclaimer Certain statements in this document constitute or may constitute forward-looking statements. Any statement in this document

RPC Group Plc 2015/16 Interim Results

RPC THE ESSENTIAL INGREDIENT RPC Group Plc 101 25 November 2015 Agenda Business Review Promens Update Financial Review Outlook PV FD SK PV 102 FOCUSED GROWTH *Proforma Group at constant exchange rates

RPC THE ESSENTIAL INGREDIENT RPC Group Plc 101 25 November 2015 Agenda Business Review Promens Update Financial Review Outlook PV FD SK PV 102 FOCUSED GROWTH *Proforma Group at constant exchange rates

Glanbia plc 2017 Half Year Results Presentation

Glanbia plc 2017 Half Year Results Presentation 10 August 2017 Siobhan Talbot Group Managing Director Mark Garvey Group Finance Director Cautionary Statement Half Year 2017 Performance Summary Adjusted

Glanbia plc 2017 Half Year Results Presentation 10 August 2017 Siobhan Talbot Group Managing Director Mark Garvey Group Finance Director Cautionary Statement Half Year 2017 Performance Summary Adjusted

Income taxes (excluding non-trading items) (89.2) (89.5)

(89.2) (89.5)") FINANCIAL REVIEW Delivering another year of solid performance + Group Key Performance Indicators pages 30-31 Financial Statements pages 138-202 The Group delivered another year of solid performance against

FINANCIAL REVIEW Delivering another year of solid performance + Group Key Performance Indicators pages 30-31 Financial Statements pages 138-202 The Group delivered another year of solid performance against

Unilever - CAGE Conference. Paul Polman CEO Roger Seabrook VP Investor Relations London - 19 th March 2012

Unilever - CAGE Conference Paul Polman CEO Roger Seabrook VP Investor Relations London - 19 th March 2012 Contents 1 2011 key takeaways 2 Our progress over the last 3 years 3 Your questions addressed 2011

Unilever - CAGE Conference Paul Polman CEO Roger Seabrook VP Investor Relations London - 19 th March 2012 Contents 1 2011 key takeaways 2 Our progress over the last 3 years 3 Your questions addressed 2011

GENERAL MILLS FISCAL 2019 FIRST-QUARTER EARNINGS SEPTEMBER 18, 2018

GENERAL MILLS FISCAL 2019 FIRST-QUARTER EARNINGS SEPTEMBER 18, 2018 A Reminder on Forward-looking Statements This presentation contains forward-looking statements within the meaning of the Private Securities

GENERAL MILLS FISCAL 2019 FIRST-QUARTER EARNINGS SEPTEMBER 18, 2018 A Reminder on Forward-looking Statements This presentation contains forward-looking statements within the meaning of the Private Securities

Strong start to the year with record partner signings in the USA

Strong start to the year with record partner signings in the USA Good customer growth up 14% to 7.5m Group profit up 9% to 28.7m Group retention at 82% Adjusted profit before tax 1 ( m) 26.0 26.2 8.4 9.4

Strong start to the year with record partner signings in the USA Good customer growth up 14% to 7.5m Group profit up 9% to 28.7m Group retention at 82% Adjusted profit before tax 1 ( m) 26.0 26.2 8.4 9.4

The Mondelēz International Pitch

The Mondelēz International Pitch Sector Manager: Richard Sparkes Senior Analyst: Patrick Folan Analysts: Ross Casey, Barry Fitzpatrick Introduction: Company Snapshot Graph of share price for past 12 months

The Mondelēz International Pitch Sector Manager: Richard Sparkes Senior Analyst: Patrick Folan Analysts: Ross Casey, Barry Fitzpatrick Introduction: Company Snapshot Graph of share price for past 12 months

2018 Full Year Results 20 November 2018

2018 Full Year Results 20 November 2018 Disclaimer Certain information included in the following presentation is forward looking and involves risks, assumptions and uncertainties that could cause actual

2018 Full Year Results 20 November 2018 Disclaimer Certain information included in the following presentation is forward looking and involves risks, assumptions and uncertainties that could cause actual

Ashmore Group plc. Results for year ending 30 June September

Ashmore Group plc Results for year ending 30 June 2018 7 September 2018 www.ashmoregroup.com Overview Strong operating and financial performance Active investment continues to produce outperformance (94%

Ashmore Group plc Results for year ending 30 June 2018 7 September 2018 www.ashmoregroup.com Overview Strong operating and financial performance Active investment continues to produce outperformance (94%

2010 Half yearly financial report

NEWS RELEASE Glanbia Corporate Communications Telephone + 353 56 777 2200 Facsimile + 353 56 77 50834 www.glanbia.com A world of nutritional ingredients and cheese 2010 Half yearly financial report 25

NEWS RELEASE Glanbia Corporate Communications Telephone + 353 56 777 2200 Facsimile + 353 56 77 50834 www.glanbia.com A world of nutritional ingredients and cheese 2010 Half yearly financial report 25

January March 2010 Conference Call. Georg Denoke Member of the Executive Board & CFO 4 May 2010

January March 2010 Conference Call Georg Denoke Member of the Executive Board & CFO 4 May 2010 Disclaimer This presentation contains forward-looking statements about Linde AG ( Linde ) and their respective

January March 2010 Conference Call Georg Denoke Member of the Executive Board & CFO 4 May 2010 Disclaimer This presentation contains forward-looking statements about Linde AG ( Linde ) and their respective

INTERIM RESULTS th July 2015

29 th July 2015 Nicandro Durante Chief Executive Financials Volume Current Revenue 6.4bn Profit 2.5bn Margin 39.2% EPS 100.2p Cigarettes 5.9% 2.4% 2.9% 322bn 6.0% flat 1.6% Constant 1.3% 0.4pp 3.9% Total

29 th July 2015 Nicandro Durante Chief Executive Financials Volume Current Revenue 6.4bn Profit 2.5bn Margin 39.2% EPS 100.2p Cigarettes 5.9% 2.4% 2.9% 322bn 6.0% flat 1.6% Constant 1.3% 0.4pp 3.9% Total

Strengthening the economic model

Strengthening the economic model Cécile CABANIS Executive Vice President, Chief Financial Officer Strategy and Information Systems DISCLAIMER This document is presented by Danone. It contains certain forward-looking

Strengthening the economic model Cécile CABANIS Executive Vice President, Chief Financial Officer Strategy and Information Systems DISCLAIMER This document is presented by Danone. It contains certain forward-looking

REXEL. Q3 & 9-month 2009 results. November 12, 2009

REXEL Q3 & 9-month 2009 results November 12, 2009 Q3 2009 & 9-month results Q3 and 9-month 2009 at a glance Financial review Outlook 3 Q3 & 9-month 2009 at a glance Q3 & 9-month 2009 highlights: Quarter-on-quarter

REXEL Q3 & 9-month 2009 results November 12, 2009 Q3 2009 & 9-month results Q3 and 9-month 2009 at a glance Financial review Outlook 3 Q3 & 9-month 2009 at a glance Q3 & 9-month 2009 highlights: Quarter-on-quarter

Croda International Plc

Croda International Plc 2018 Half Year Results July 2018 Cautionary statement and definitions Cautionary statement This review is intended to focus on matters which are relevant to the interests of shareholders

Croda International Plc 2018 Half Year Results July 2018 Cautionary statement and definitions Cautionary statement This review is intended to focus on matters which are relevant to the interests of shareholders

Year-end results. 18 May

Year-end results 18 May Highlights for the year Strong operational performance Good performance across all areas of activity Deepened our core franchise Sound levels of corporate client and private client

Year-end results 18 May Highlights for the year Strong operational performance Good performance across all areas of activity Deepened our core franchise Sound levels of corporate client and private client

2017 FULL YEAR RESULTS. February 28,

2017 FULL YEAR RESULTS February 28, 2018 1 Disclaimer This presentation contains both historical and forward-looking statements. These forward-looking statements are based on Carrefour management's current

2017 FULL YEAR RESULTS February 28, 2018 1 Disclaimer This presentation contains both historical and forward-looking statements. These forward-looking statements are based on Carrefour management's current

Q Results May 1, 2018

Q1 2018 Results May 1, 2018 1 Forward-looking statements This presentation contains a number of forward-looking statements. Words, and variations of words, such as will, expect, should, plan, believe,

Q1 2018 Results May 1, 2018 1 Forward-looking statements This presentation contains a number of forward-looking statements. Words, and variations of words, such as will, expect, should, plan, believe,

2017 Preliminary Results

2017 Preliminary Results 22 February 2018 All statements other than statements of historical fact included in this document, including, without limitation, those regarding the financial condition, results,

2017 Preliminary Results 22 February 2018 All statements other than statements of historical fact included in this document, including, without limitation, those regarding the financial condition, results,

PERNOD RICARD A value-creative business model. Deutsche Bank conference 20 June 2012

PERNOD RICARD A value-creative business model Deutsche Bank conference 20 June 2012 Deutsche Bank conference 20th June 2012 A value-creative business model Spirits within the consumers - TEXT goods universe

PERNOD RICARD A value-creative business model Deutsche Bank conference 20 June 2012 Deutsche Bank conference 20th June 2012 A value-creative business model Spirits within the consumers - TEXT goods universe

Half Year Results François-Xavier Roger Chief Financial Officer

Half Year Results 2016 François-Xavier Roger Chief Financial Officer Disclaimer This presentation contains forward looking statements which reflect Management s current views and estimates. The forward

Half Year Results 2016 François-Xavier Roger Chief Financial Officer Disclaimer This presentation contains forward looking statements which reflect Management s current views and estimates. The forward

Investor Presentation Q Results. 8 November 2018

Investor Presentation Q3 2018 Results 8 November 2018 Forward-looking statements This presentation contains forward-looking statements, including, but not limited to, the statements and expectations contained

Investor Presentation Q3 2018 Results 8 November 2018 Forward-looking statements This presentation contains forward-looking statements, including, but not limited to, the statements and expectations contained

Half-year results July 26, 2018 Nestlé half-year results

Half-year results 2018 July 26, 2018 Nestlé half-year results 2018 1 Disclaimer This presentation contains forward looking statements which reflect Management s current views and estimates. The forward

Half-year results 2018 July 26, 2018 Nestlé half-year results 2018 1 Disclaimer This presentation contains forward looking statements which reflect Management s current views and estimates. The forward

ARYZTA AG. FY 2011 Results 26 September 2011

ARYZTA AG FY 2011 Results 26 September 2011 Forward Looking Statement This document contains forward looking statements which reflect management s current views and estimates. The forward looking statements

ARYZTA AG FY 2011 Results 26 September 2011 Forward Looking Statement This document contains forward looking statements which reflect management s current views and estimates. The forward looking statements

6 MARCH 2017 FULL YEAR RESULTS

6 MARCH 2017 FULL YEAR RESULTS FOR THE YEAR ENDED 31 DECEMBER 2016 01 THE COLLAGEN CASING COMPANY Global Leader One of the world s leading providers of collagen casings for the processed meats sector Provides

6 MARCH 2017 FULL YEAR RESULTS FOR THE YEAR ENDED 31 DECEMBER 2016 01 THE COLLAGEN CASING COMPANY Global Leader One of the world s leading providers of collagen casings for the processed meats sector Provides

HALF YEAR RESULTS PRESENTATION 2018 RESULTS FOR THE SIX MONTHS ENDED 31 MAY 2018

HALF YEAR RESULTS PRESENTATION 2018 RESULTS FOR THE SIX MONTHS ENDED 31 MAY 2018 2018 Overview Encouraging first half performance with accelerated momentum in Q2 Adjusted operating profit +6% to 20.4m

HALF YEAR RESULTS PRESENTATION 2018 RESULTS FOR THE SIX MONTHS ENDED 31 MAY 2018 2018 Overview Encouraging first half performance with accelerated momentum in Q2 Adjusted operating profit +6% to 20.4m

Cover-More Group. UBS Australasia Conference. November 2015

Cover-More Group UBS Australasia Conference November 2015 Executive summary: FY15 overview Cover-More delivered another year of double digit earnings growth, with offshore business growing substantially.

Cover-More Group UBS Australasia Conference November 2015 Executive summary: FY15 overview Cover-More delivered another year of double digit earnings growth, with offshore business growing substantially.

Attached is an ASX and Media Release from Brambles Limited on its financial results for the year ended 30 June 2018.

Brambles Limited ABN 22 000 129 868 Level 10 Angel Place 123 Pitt Street Sydney NSW 2000 Australia GPO Box 4173 Sydney NSW 2001 Tel +61 2 9256 5222 Fax +61 2 9256 5299 www.brambles.com 24 August 2018 The

Brambles Limited ABN 22 000 129 868 Level 10 Angel Place 123 Pitt Street Sydney NSW 2000 Australia GPO Box 4173 Sydney NSW 2001 Tel +61 2 9256 5222 Fax +61 2 9256 5299 www.brambles.com 24 August 2018 The

PRELIMINARY RESULTS rd February 2012

23 rd February 2012 Nicandro Durante Chief Executive Proven strategy continues to deliver Superior shareholder returns Daily Relative performance to FTSE100 Price GBp 2,800 2,600 2,400 2,200 2,000 1,800

23 rd February 2012 Nicandro Durante Chief Executive Proven strategy continues to deliver Superior shareholder returns Daily Relative performance to FTSE100 Price GBp 2,800 2,600 2,400 2,200 2,000 1,800

1H FY19 RESULTS PRESENTATION 25 February 2019

RELIANCE WORLDWIDE CORPORATION LIMITED ACN 610855877 1H FY19 RESULTS PRESENTATION 25 February 2019 INVESTOR PRESENTATION 1H FY19 RESULTS PAGE 0 Important Notice This presentation contains general information

RELIANCE WORLDWIDE CORPORATION LIMITED ACN 610855877 1H FY19 RESULTS PRESENTATION 25 February 2019 INVESTOR PRESENTATION 1H FY19 RESULTS PAGE 0 Important Notice This presentation contains general information

Results for the year ended 31 March London, 28 May 2015

Results for the year ended 31 March 2015 London, 28 May 2015 Cautionary Statement This Statement of full year results contains certain forward-looking statements with respect to the financial condition,

Results for the year ended 31 March 2015 London, 28 May 2015 Cautionary Statement This Statement of full year results contains certain forward-looking statements with respect to the financial condition,

Kraft Foods Reports Strong Revenue and Income Growth As It Begins Cadbury Integration

May 6, Kraft Foods Reports Strong Revenue and Income Growth As It Begins Cadbury Integration Net revenues grew 26.0% to $11.3 billion; Combined Organic Net Revenues(1) grew 3.9%, reflecting 3.3 percent

May 6, Kraft Foods Reports Strong Revenue and Income Growth As It Begins Cadbury Integration Net revenues grew 26.0% to $11.3 billion; Combined Organic Net Revenues(1) grew 3.9%, reflecting 3.3 percent

FY17 Results. 25 September 2017

FY17 Results 25 September 2017 Forward Looking Statement This document contains forward looking statements, which reflect management s current views and estimates. The forward looking statements involve

FY17 Results 25 September 2017 Forward Looking Statement This document contains forward looking statements, which reflect management s current views and estimates. The forward looking statements involve

Financial Review. Strategic Report - Performance. Table 1: Performance Metrics

58 Financial Review Despite the challenge of a mild winter, the Group had a good year with revenue increasing by 6.2%, operating profits increasing 11.5%, adjusted earnings per share increasing by 11.7%,

58 Financial Review Despite the challenge of a mild winter, the Group had a good year with revenue increasing by 6.2%, operating profits increasing 11.5%, adjusted earnings per share increasing by 11.7%,

November Rick Goings. Chairman & CEO

November 2016 Rick Goings Chairman & CEO Forward looking statements We are making some forward looking statements today that use words like outlook or target or similar predictive words. Such forward looking

November 2016 Rick Goings Chairman & CEO Forward looking statements We are making some forward looking statements today that use words like outlook or target or similar predictive words. Such forward looking

Roadshow presentation 3-Month Key Sales Figures 2016/17. January 2017

Roadshow presentation 3-Month Key Sales Figures 2016/17 Agenda BC at a glance Highlights 3 months 2016/17 Strategy & Outlook Page 2 BC at a glance Who we are? The heart and engine of the chocolate industry

Roadshow presentation 3-Month Key Sales Figures 2016/17 Agenda BC at a glance Highlights 3 months 2016/17 Strategy & Outlook Page 2 BC at a glance Who we are? The heart and engine of the chocolate industry

2018 Half Year Results

A GLOBAL LEADER IN METAL FLOW ENGINEERING 2018 Half Year Results 26 July 2018 Patrick André Chief Executive 1 Disclaimer This presentation, which has been prepared by Vesuvius plc (the Company ), includes

A GLOBAL LEADER IN METAL FLOW ENGINEERING 2018 Half Year Results 26 July 2018 Patrick André Chief Executive 1 Disclaimer This presentation, which has been prepared by Vesuvius plc (the Company ), includes

COMPUTERSHARE LIMITED (ASX:CPU) FINANCIAL RESULTS FOR THE FULL YEAR ENDED 30 JUNE August 2014

FINANCIAL RESULTS FOR THE FULL YEAR ENDED 30 JUNE August 2014") COMPUTERSHARE LIMITED (ASX:CPU) FINANCIAL RESULTS FOR THE FULL YEAR ENDED 30 JUNE 2014 13 August 2014 NOTE: All figures (including comparatives) are presented in US Dollars (unless otherwise stated). The

COMPUTERSHARE LIMITED (ASX:CPU) FINANCIAL RESULTS FOR THE FULL YEAR ENDED 30 JUNE 2014 13 August 2014 NOTE: All figures (including comparatives) are presented in US Dollars (unless otherwise stated). The