Risk news shocks and the business cycle

|

|

|

- Rolf Parsons

- 5 years ago

- Views:

Transcription

1 Risk news shocks and the business cycle Gabor Pinter [BoE] Kostas Theodoridis [BoE] Tony Yates [BoE/Bristol] Workshop on empirical macroeconomics, Ghent University, 6-7 June 2013

2 What we do Consider shocks to ik risk, and corresponding news =changes in variance of cross section of returns, revelation about future changes Identify a risk news shock in US data [SW+3 financial series]...using a modification of Barsky Sims method (which they used to identify news in future tfp) Document contribution of risk+risk news shock to the business cycle Fit a DSGE model with credit frictions [SW+BGG] to the IRFs from the VAR

3 What we find Risk+risk news contribute about 20% to fluctuations in output in post WW2 US data Contrast with CMR (2013,AER(f)):(f)) 60% Risk news shocks had small effect on spreads during crisis, but sizeable effects on output DSGE model dlcan get near (shape (h of) IRFs to risk news shock IF we modify it to have rule of thumb consumers as in (eg) GLS (2004) Weak DSGE propagation means need larger shocks than in data

4 Risk/risk news shock In a DSGE (Eg SW+BGG, similar to CMR) model Entrepreneurs borrow frombanks, build capital, get hit by idiosyncratic shock, leading to variance in the amount of effective capital sold on to producers of intermediate goods Risk shock is a shock to this variance Risk news is revelation today about future Risk news is revelation today about future values of this variance

5 Examples of risk news shocks Announcement of invention of new technology e.g. mobile phones, internet, whose diffusion and effect will be uncertain Release of information about possible climate change CMR example: Steve Jobs Successes and failures indicate a distribution Revelation that his health was bad was news about future distribution of returns (being wider, as well as lower?)

6 Why is the risk news shock interesting? Anecdotal: changes in risk and perceptions of risk a central feature of the crisis according to market participants and policymakers Facts: prices of risky assets changed a lot during the crisis.

7 Previous work: news Beaudry Portier (2006) VAR identified using lr res.; tfp mostly news, news explains ½ variance in output; + ve +ve comovement between c,i,h, contrary to RBC Jaimovich and Rebello (2006) Modify RBC by using GHH preferences to turn off wealth effect, reconcilingeffects effects ofnews shock Barsky Sims (2009) SGU(2012) RBC + real rigidities, with many news shocks 80% of business cycle var due to tfp

8 Previous work: financial/risk shocks BGG(1999), KM(1997); financial frictions only weakly propagate p conventional (g (eg technology) shocks Finance can t therefore explain business cycles CMR s(2013) risk shock one of many, including: CMR(2008), Nolan Thoenissen(2009), Gertler Karadi(2011), Fuentes Albero(2012)

9 We are not considering aggregate uncertainty shocks Bloom (2009), Bloom et al (2012) Baker, Bloom and Davis (?) [economic policy] Bekaert et al (2012) Fernandez Villaverde et al (2011) [fiscal] Born and Pfeifer (2011) [fiscal]

10 Barsky Sims (2009) Construct tfp series from Solow residuals News shock to tfp: Orthogonal to tfp_t, contributes maximally to forecast errors up to and including tfp_t+ht+h Our paper: take proxy for uncertainty based on options prices and standard deviation of stock returns Risk news shock is orthogonal to risk_t Contributes maximally to risk_t+h Satisfies certain sign restrictions

11 Sign restrictions recap Var(1): Y t AY t 1 t,e t t Cholesky factorisation of VAR residuals: PP Decompose further: PDD P where D D,s.t.DD I Take Givens matrix, e.g. D 2 cos sin sin cos 1. draw 2. keep if sign PDA R 3. goto 1

12 Combining Barsky Sims with sign restrictions 1. Rotate only a sub-matrix, to preserve that surprise risk shock only thing that moves today s risk proxy D D 9 2. Once have sufficient draws, amongst those accepted... max i,j h e i h 0 A PD e j e j D P A e i h e i A 0 A e i

13 The sign restrictions encoded in our R

14 Estimation of VAR Bayesian VAR [not just in respect of sign restrictions..] Eliminates oscillatory impulse responses Pi Priors: Centred on zero for off diagonals (Minnesota) Tighter for more distant lags Conjugate priors chosen to produce analytical solutions for the posterior See, e.g. Doan et al (1984)/Kaddiyala and Karlsson (1997)

15 Data Updated [ ] Smets Wouters (2007) : C, I, Y, w/p, h, pi, r Plus: Uncertainty t proxy: VXO (Bloom,2009) net worth(cmr): Dow Jones Wilshire 5000 index deflated by GDP deflator Spread: BAA AAA

16

17

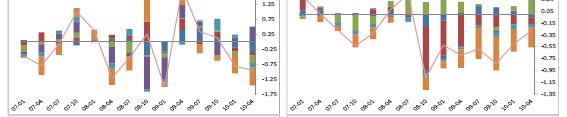

18 Crisis chart: key points Shocks that have small effect on spreads have sizeable effects on consumption, investment, inflation... Not large effects on output, suggesting that perhaps eg fiscal policy compensating

19 Some supportive evidence Monte Carlo Alternative risk proxy Alternative h s Sense check on the VAR IRFs

20 Monte Carlo evidence Barsky Sims conducted Monte Carlo experiment in an RBC laboratory We follow suit using a DSGE (SW+BGG) model with a risk news shock Generate 1000 datasets of 200 obs Ask whether the VAR identification applied to the DSGE generated data recovers the IRF computed directly from the DSGE model

21

22 Alternative risk proxy Risk proxy may be flawed: measured with error or capturing instead simply pyvolatility of an aggregate shock, not idiosyncratic shock. So do results survive use of other proxies?

23 Stock option based, uncertainty proxy Source: Bloom (2009)

24 Alternative measure of crosssectional uncertainty Source: Bloom

25 FEVD for cross section measure

26 IRF to a risk news shock: VIX vs CSR

27 Alternative h s hs Recall the horizon h, in: max h i,j h e i A PD e j e 0 j D P A e i e i h 0 A A e i

28 FEVD for alternative h s hs[vxo]

29 Sense check on the VARs IRFs Does the VARs other shocks do what you would expect? Yes. Does the VARs risk shocks do things that seem sensible?

30 VIX: IRF to contemp. risk shock

31 VIX: IRF to a risk news shock

32 VIX, IRFs to risk shocks, contemp. vs news

33 VIX: IRF to a technology shock

34 VIX: IRF to demand shock

35 VIX: IRF to a mon pol shock

36 The DSGE model Smets Wouters+BGG Patient consumers/impatient entrepreneurs Lending to entrepreneurs at spread related to net worth Entrepreneurs build capital and rent out to sticky price intermediate goods producers Imperfectly competitive intermediate t producers, final goods aggregator Central bank, govt

37 Frictions Credit friction a la BGG Habits in consumption Investment adjustment costs Sticky prices, price indexation Sticky wages, wage indexation Variable capacity utilisation

38 Estimation of the DSGE model Match responses of DSGE model to a risk news shock to those from the VAR e.g. CEE (2005) match to IRFs to a mon pol shock Partial information method: Cost: inefficiency, bias, worsens identification? Benefit: immunity to misspecification of the stochastic parts of the model about which we stay silent

39 DSGE vs the VAR, IRFs to a risk news shock

40 DSGE IRF to risk news shock with and without htm consumers

41 Effect of strength of ff on DSGE estimates

42 Recap Risk and risk news proposed as shock to explain the cycle eg in CMR (2013) )[nb 60%] Our VAR identified risk news shock implies much smaller contribution from these shocks (to eg output) [ie about 20%] Scheme works in MC, robust to using alternative risk proxy DSGE model has to be greatly modified with inclusion i of HTM consumers to get close to matching IRFs to risk news shock.

Uncertainty Shocks and the Relative Price of Investment Goods

Uncertainty Shocks and the Relative Price of Investment Goods Munechika Katayama 1 Kwang Hwan Kim 2 1 Kyoto University 2 Yonsei University SWET August 6, 216 1 / 34 This paper... Study how changes in uncertainty

Uncertainty Shocks and the Relative Price of Investment Goods Munechika Katayama 1 Kwang Hwan Kim 2 1 Kyoto University 2 Yonsei University SWET August 6, 216 1 / 34 This paper... Study how changes in uncertainty

Fluctuations. Roberto Motto

Financial Factors in Economic Fluctuations Lawrence Christiano Roberto Motto Massimo Rostagno What we do Integrate t financial i frictions into a standard d equilibrium i model and estimate the model using

Financial Factors in Economic Fluctuations Lawrence Christiano Roberto Motto Massimo Rostagno What we do Integrate t financial i frictions into a standard d equilibrium i model and estimate the model using

Financial Factors in Business Cycles

Financial Factors in Business Cycles Lawrence J. Christiano, Roberto Motto, Massimo Rostagno 30 November 2007 The views expressed are those of the authors only What We Do? Integrate financial factors into

Financial Factors in Business Cycles Lawrence J. Christiano, Roberto Motto, Massimo Rostagno 30 November 2007 The views expressed are those of the authors only What We Do? Integrate financial factors into

Risk news shocks and the business cycle

Risk news shocks and the business cycle Gabor Pinter Bank of England Konstantinos Theodoridis Bank of England May 21, 213 Tony Yates Bank of England Abstract We identify a risk news shock in a VAR, modifying

Risk news shocks and the business cycle Gabor Pinter Bank of England Konstantinos Theodoridis Bank of England May 21, 213 Tony Yates Bank of England Abstract We identify a risk news shock in a VAR, modifying

MA Advanced Macroeconomics: 11. The Smets-Wouters Model

MA Advanced Macroeconomics: 11. The Smets-Wouters Model Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) The Smets-Wouters Model Spring 2016 1 / 23 A Popular DSGE Model Now we will discuss

MA Advanced Macroeconomics: 11. The Smets-Wouters Model Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) The Smets-Wouters Model Spring 2016 1 / 23 A Popular DSGE Model Now we will discuss

News Shocks and the Term Structure of Interest Rates: Reply Online Appendix

News Shocks and the Term Structure of Interest Rates: Reply Online Appendix André Kurmann Drexel University Christopher Otrok University of Missouri Federal Reserve Bank of St. Louis March 14, 2017 This

News Shocks and the Term Structure of Interest Rates: Reply Online Appendix André Kurmann Drexel University Christopher Otrok University of Missouri Federal Reserve Bank of St. Louis March 14, 2017 This

Economic Policy Uncertainty and Inflation Expectations

Economic Policy Uncertainty and Inflation Expectations Klodiana Istrefi and Anamaria Piloiu Banque de France DB Research SEM Conference 215 22-24 July, Paris 1 / 3 The views expressed herein are those

Economic Policy Uncertainty and Inflation Expectations Klodiana Istrefi and Anamaria Piloiu Banque de France DB Research SEM Conference 215 22-24 July, Paris 1 / 3 The views expressed herein are those

Risk Shocks and Economic Fluctuations. Summary of work by Christiano, Motto and Rostagno

Risk Shocks and Economic Fluctuations Summary of work by Christiano, Motto and Rostagno Outline Simple summary of standard New Keynesian DSGE model (CEE, JPE 2005 model). Modifications to introduce CSV

Risk Shocks and Economic Fluctuations Summary of work by Christiano, Motto and Rostagno Outline Simple summary of standard New Keynesian DSGE model (CEE, JPE 2005 model). Modifications to introduce CSV

Risk Shocks. Lawrence Christiano (Northwestern University), Roberto Motto (ECB) and Massimo Rostagno (ECB)

, Roberto Motto (ECB) and Massimo Rostagno (ECB)") Risk Shocks Lawrence Christiano (Northwestern University), Roberto Motto (ECB) and Massimo Rostagno (ECB) Finding Countercyclical fluctuations in the cross sectional variance of a technology shock, when

Risk Shocks Lawrence Christiano (Northwestern University), Roberto Motto (ECB) and Massimo Rostagno (ECB) Finding Countercyclical fluctuations in the cross sectional variance of a technology shock, when

Endogenous risk in a DSGE model with capital-constrained financial intermediaries

Endogenous risk in a DSGE model with capital-constrained financial intermediaries Hans Dewachter (NBB-KUL) and Raf Wouters (NBB) NBB-Conference, Brussels, 11-12 October 2012 PP 1 motivation/objective introduce

Endogenous risk in a DSGE model with capital-constrained financial intermediaries Hans Dewachter (NBB-KUL) and Raf Wouters (NBB) NBB-Conference, Brussels, 11-12 October 2012 PP 1 motivation/objective introduce

Credit Shocks and the U.S. Business Cycle. Is This Time Different? Raju Huidrom University of Virginia. Midwest Macro Conference

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

MA Advanced Macroeconomics 3. Examples of VAR Studies

MA Advanced Macroeconomics 3. Examples of VAR Studies Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) VAR Studies Spring 2016 1 / 23 Examples of VAR Studies We will look at four different

MA Advanced Macroeconomics 3. Examples of VAR Studies Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) VAR Studies Spring 2016 1 / 23 Examples of VAR Studies We will look at four different

Financial Frictions in Macroeconomics. Lawrence J. Christiano Northwestern University

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Securities, etc. Bank Debt Bank Equity Frictions between

Financial Frictions in Macroeconomics Lawrence J. Christiano Northwestern University Balance Sheet, Financial System Assets Liabilities Bank loans Securities, etc. Bank Debt Bank Equity Frictions between

Credit Spreads and the Macroeconomy

Credit Spreads and the Macroeconomy Simon Gilchrist Boston University and NBER Joint BIS-ECB Workshop on Monetary Policy & Financial Stability Bank for International Settlements Basel, Switzerland September

Credit Spreads and the Macroeconomy Simon Gilchrist Boston University and NBER Joint BIS-ECB Workshop on Monetary Policy & Financial Stability Bank for International Settlements Basel, Switzerland September

MACROECONOMIC EFFECTS OF UNCERTAINTY SHOCKS: EVIDENCE FROM SURVEY DATA

MACROECONOMIC EFFECTS OF UNCERTAINTY SHOCKS: EVIDENCE FROM SURVEY DATA SYLVAIN LEDUC AND ZHENG LIU Abstract. We examine the effects of uncertainty on macroeconomic fluctuations. We measure uncertainty

MACROECONOMIC EFFECTS OF UNCERTAINTY SHOCKS: EVIDENCE FROM SURVEY DATA SYLVAIN LEDUC AND ZHENG LIU Abstract. We examine the effects of uncertainty on macroeconomic fluctuations. We measure uncertainty

Outline. 1. Overall Impression. 2. Summary. Discussion of. Volker Wieland. Congratulations!

ECB Conference Global Financial Linkages, Transmission of Shocks and Asset Prices Frankfurt, December 1-2, 2008 Discussion of Real effects of the subprime mortgage crisis by Hui Tong and Shang-Jin Wei

ECB Conference Global Financial Linkages, Transmission of Shocks and Asset Prices Frankfurt, December 1-2, 2008 Discussion of Real effects of the subprime mortgage crisis by Hui Tong and Shang-Jin Wei

Web Appendix for: What does Monetary Policy do to Long-Term Interest Rates at the Zero Lower Bound?

Web Appendix for: What does Monetary Policy do to Long-Term Interest Rates at the Zero Lower Bound? Jonathan H. Wright May 9, 212 This not-for-publication web appendix gives additional results for the

Web Appendix for: What does Monetary Policy do to Long-Term Interest Rates at the Zero Lower Bound? Jonathan H. Wright May 9, 212 This not-for-publication web appendix gives additional results for the

Are Predictable Improvements in TFP Contractionary or Expansionary: Implications from Sectoral TFP? *

Federal Reserve Bank of Dallas Globalization and Monetary Policy Institute Working Paper No. http://www.dallasfed.org/assets/documents/institute/wpapers//.pdf Are Predictable Improvements in TFP Contractionary

Federal Reserve Bank of Dallas Globalization and Monetary Policy Institute Working Paper No. http://www.dallasfed.org/assets/documents/institute/wpapers//.pdf Are Predictable Improvements in TFP Contractionary

slides chapter 6 Interest Rate Shocks

slides chapter 6 Interest Rate Shocks Princeton University Press, 217 Motivation Interest-rate shocks are generally believed to be a major source of fluctuations for emerging countries. The next slide

slides chapter 6 Interest Rate Shocks Princeton University Press, 217 Motivation Interest-rate shocks are generally believed to be a major source of fluctuations for emerging countries. The next slide

Communications Breakdown: The Transmission of Dierent types of ECB Policy Announcements

Communications Breakdown: The Transmission of Dierent types of ECB Policy Announcements Andrew Kane, John H. Rogers and Bo Sun April 27, 218 1 / 27 Background I Large literature using high-frequency changes

Communications Breakdown: The Transmission of Dierent types of ECB Policy Announcements Andrew Kane, John H. Rogers and Bo Sun April 27, 218 1 / 27 Background I Large literature using high-frequency changes

Output Gap, Monetary Policy Trade-Offs and Financial Frictions

Output Gap, Monetary Policy Trade-Offs and Financial Frictions Francesco Furlanetto Norges Bank Paolo Gelain Norges Bank Marzie Taheri Sanjani International Monetary Fund Seminar at Narodowy Bank Polski

Output Gap, Monetary Policy Trade-Offs and Financial Frictions Francesco Furlanetto Norges Bank Paolo Gelain Norges Bank Marzie Taheri Sanjani International Monetary Fund Seminar at Narodowy Bank Polski

Policy options at the zero lower bound

Policy options at the zero lower bound Session 5: How to implement stabilization policies with high public debt? Timo Wollmershäuser & Atanas Hristov Ifo Institute Introduction very weak recovery from

Policy options at the zero lower bound Session 5: How to implement stabilization policies with high public debt? Timo Wollmershäuser & Atanas Hristov Ifo Institute Introduction very weak recovery from

Comment. The New Keynesian Model and Excess Inflation Volatility

Comment Martín Uribe, Columbia University and NBER This paper represents the latest installment in a highly influential series of papers in which Paul Beaudry and Franck Portier shed light on the empirics

Comment Martín Uribe, Columbia University and NBER This paper represents the latest installment in a highly influential series of papers in which Paul Beaudry and Franck Portier shed light on the empirics

Online Appendixes to Missing Disinflation and Missing Inflation: A VAR Perspective

Online Appendixes to Missing Disinflation and Missing Inflation: A VAR Perspective Elena Bobeica and Marek Jarociński European Central Bank Author e-mails: elena.bobeica@ecb.int and marek.jarocinski@ecb.int.

Online Appendixes to Missing Disinflation and Missing Inflation: A VAR Perspective Elena Bobeica and Marek Jarociński European Central Bank Author e-mails: elena.bobeica@ecb.int and marek.jarocinski@ecb.int.

Real-Time DSGE Model Density Forecasts During the Great Recession - A Post Mortem

The views expressed in this talk are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of New York or the Federal Reserve System. Real-Time DSGE Model Density Forecasts

The views expressed in this talk are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of New York or the Federal Reserve System. Real-Time DSGE Model Density Forecasts

Business cycle fluctuations Part II

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

CONFIDENCE AND ECONOMIC ACTIVITY: THE CASE OF PORTUGAL*

CONFIDENCE AND ECONOMIC ACTIVITY: THE CASE OF PORTUGAL* Caterina Mendicino** Maria Teresa Punzi*** 39 Articles Abstract The idea that aggregate economic activity might be driven in part by confidence and

CONFIDENCE AND ECONOMIC ACTIVITY: THE CASE OF PORTUGAL* Caterina Mendicino** Maria Teresa Punzi*** 39 Articles Abstract The idea that aggregate economic activity might be driven in part by confidence and

On the Merits of Conventional vs Unconventional Fiscal Policy

On the Merits of Conventional vs Unconventional Fiscal Policy Matthieu Lemoine and Jesper Lindé Banque de France and Sveriges Riksbank The views expressed in this paper do not necessarily reflect those

On the Merits of Conventional vs Unconventional Fiscal Policy Matthieu Lemoine and Jesper Lindé Banque de France and Sveriges Riksbank The views expressed in this paper do not necessarily reflect those

On "Fiscal Volatility Shocks and Economic Activity" by Fernandez-Villaverde, Guerron-Quintana, Kuester, and Rubio-Ramirez

On "Fiscal Volatility Shocks and Economic Activity" by Fernandez-Villaverde, Guerron-Quintana, Kuester, and Rubio-Ramirez Julia K. Thomas September 2014 2014 1 / 13 Overview How does time-varying uncertainty

On "Fiscal Volatility Shocks and Economic Activity" by Fernandez-Villaverde, Guerron-Quintana, Kuester, and Rubio-Ramirez Julia K. Thomas September 2014 2014 1 / 13 Overview How does time-varying uncertainty

Household income risk, nominal frictions, and incomplete markets 1

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research

Fiscal Policy Uncertainty and the Business Cycle: Time Series Evidence from Italy

Fiscal Policy Uncertainty and the Business Cycle: Time Series Evidence from Italy Alessio Anzuini, Luca Rossi, Pietro Tommasino Banca d Italia ECFIN Workshop Fiscal policy in an uncertain environment Tuesday,

Fiscal Policy Uncertainty and the Business Cycle: Time Series Evidence from Italy Alessio Anzuini, Luca Rossi, Pietro Tommasino Banca d Italia ECFIN Workshop Fiscal policy in an uncertain environment Tuesday,

News-Driven Business Cycles in Small Open Economies. Güneş Kamber Konstantinos Theodoridis Christoph Thoenissen ISSN

News-Driven Business Cycles in Small Open Economies Güneş Kamber Konstantinos Theodoridis Christoph Thoenissen ISSN 749-8368 SERPS no. 47 Published: October 4 News-driven business cycles in small open

News-Driven Business Cycles in Small Open Economies Güneş Kamber Konstantinos Theodoridis Christoph Thoenissen ISSN 749-8368 SERPS no. 47 Published: October 4 News-driven business cycles in small open

44 ECB HOW HAS MACROECONOMIC UNCERTAINTY IN THE EURO AREA EVOLVED RECENTLY?

Box HOW HAS MACROECONOMIC UNCERTAINTY IN THE EURO AREA EVOLVED RECENTLY? High macroeconomic uncertainty through its likely adverse effect on the spending decisions of both consumers and firms is considered

Box HOW HAS MACROECONOMIC UNCERTAINTY IN THE EURO AREA EVOLVED RECENTLY? High macroeconomic uncertainty through its likely adverse effect on the spending decisions of both consumers and firms is considered

International Business Cycle Transmissions and News Shocks

International Business Cycle Transmissions and News Shocks Yingtong Xie Macalester College Abstract This paper examines how news shocks affect the business cycle comovements across countries. In the context

International Business Cycle Transmissions and News Shocks Yingtong Xie Macalester College Abstract This paper examines how news shocks affect the business cycle comovements across countries. In the context

Mood Swings and Business Cycles: Evidence from Sign Restrictions

Mood Swings and Business Cycles: Evidence from Sign Restrictions Deokwoo Nam 1 Jian Wang 2 1 Hanyang University 2 Chinese University of Hong Kong (Shenzhen) October 216 Introduction What drives business

Mood Swings and Business Cycles: Evidence from Sign Restrictions Deokwoo Nam 1 Jian Wang 2 1 Hanyang University 2 Chinese University of Hong Kong (Shenzhen) October 216 Introduction What drives business

Banking Industry Risk and Macroeconomic Implications

Banking Industry Risk and Macroeconomic Implications April 2014 Francisco Covas a Emre Yoldas b Egon Zakrajsek c Extended Abstract There is a large body of literature that focuses on the financial system

Banking Industry Risk and Macroeconomic Implications April 2014 Francisco Covas a Emre Yoldas b Egon Zakrajsek c Extended Abstract There is a large body of literature that focuses on the financial system

Discussion of: Financial Factors in Economic Fluctuations by Christiano, Motto, and Rostagno

Discussion of: Financial Factors in Economic Fluctuations by Christiano, Motto, and Rostagno Guido Lorenzoni Bank of Canada-Minneapolis FED Conference, October 2008 This paper Rich DSGE model with: financial

Discussion of: Financial Factors in Economic Fluctuations by Christiano, Motto, and Rostagno Guido Lorenzoni Bank of Canada-Minneapolis FED Conference, October 2008 This paper Rich DSGE model with: financial

Inflation in the Great Recession and New Keynesian Models

Inflation in the Great Recession and New Keynesian Models Marco Del Negro, Marc Giannoni Federal Reserve Bank of New York Frank Schorfheide University of Pennsylvania BU / FRB of Boston Conference on Macro-Finance

Inflation in the Great Recession and New Keynesian Models Marco Del Negro, Marc Giannoni Federal Reserve Bank of New York Frank Schorfheide University of Pennsylvania BU / FRB of Boston Conference on Macro-Finance

Financial Frictions Under Asymmetric Information and Costly State Verification

Financial Frictions Under Asymmetric Information and Costly State Verification General Idea Standard dsge model assumes borrowers and lenders are the same people..no conflict of interest. Financial friction

Financial Frictions Under Asymmetric Information and Costly State Verification General Idea Standard dsge model assumes borrowers and lenders are the same people..no conflict of interest. Financial friction

Macroeconomic Modelling at the Central Bank of Brazil. Angelo M. Fasolo Research Department

Macroeconomic Modelling at the Central Bank of Brazil Angelo M. Fasolo Research Department Introduction Economic analysis at the BCB based on three type of models: Small-scale semi-structural models, focused

Macroeconomic Modelling at the Central Bank of Brazil Angelo M. Fasolo Research Department Introduction Economic analysis at the BCB based on three type of models: Small-scale semi-structural models, focused

The Real Business Cycle Model

The Real Business Cycle Model Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) The Real Business Cycle Model Fall 2013 1 / 23 Business

The Real Business Cycle Model Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) The Real Business Cycle Model Fall 2013 1 / 23 Business

On the new Keynesian model

Department of Economics University of Bern April 7, 26 The new Keynesian model is [... ] the closest thing there is to a standard specification... (McCallum). But it has many important limitations. It

Department of Economics University of Bern April 7, 26 The new Keynesian model is [... ] the closest thing there is to a standard specification... (McCallum). But it has many important limitations. It

Involuntary (Unlucky) Unemployment and the Business Cycle. Lawrence Christiano Mathias Trabandt Karl Walentin

Unemployment and the Business Cycle. Lawrence Christiano Mathias Trabandt Karl Walentin") Involuntary (Unlucky) Unemployment and the Business Cycle Lawrence Christiano Mathias Trabandt Karl Walentin Background New Keynesian (NK) models receive lots of attention ti in central lbanks. People

Involuntary (Unlucky) Unemployment and the Business Cycle Lawrence Christiano Mathias Trabandt Karl Walentin Background New Keynesian (NK) models receive lots of attention ti in central lbanks. People

Capital and liquidity buffers and the resilience of the banking system in the euro area

Capital and liquidity buffers and the resilience of the banking system in the euro area Katarzyna Budnik and Paul Bochmann The views expressed here are those of the authors. Fifth Research Workshop of

Capital and liquidity buffers and the resilience of the banking system in the euro area Katarzyna Budnik and Paul Bochmann The views expressed here are those of the authors. Fifth Research Workshop of

Economics Letters 108 (2010) Contents lists available at ScienceDirect. Economics Letters. journal homepage:

Contents lists available at ScienceDirect. Economics Letters. journal homepage:") Economics Letters 108 (2010) 167 171 Contents lists available at ScienceDirect Economics Letters journal homepage: www.elsevier.com/locate/ecolet Is there a financial accelerator in US banking? Evidence

Economics Letters 108 (2010) 167 171 Contents lists available at ScienceDirect Economics Letters journal homepage: www.elsevier.com/locate/ecolet Is there a financial accelerator in US banking? Evidence

Starting with the measures of uncertainty related to future economic outcomes, the following three sets of indicators are considered:

Box How has macroeconomic uncertainty in the euro area evolved recently? High macroeconomic uncertainty through its likely adverse effect on the spending decisions of both consumers and firms is considered

Box How has macroeconomic uncertainty in the euro area evolved recently? High macroeconomic uncertainty through its likely adverse effect on the spending decisions of both consumers and firms is considered

Discussion of DSGE Models for Monetary Policy. Discussion of

ECB Conference Key developments in monetary economics Frankfurt, October 29-30, 2009 Discussion of DSGE Models for Monetary Policy by L. L. Christiano, M. Trabandt & K. Walentin Volker Wieland Goethe University

ECB Conference Key developments in monetary economics Frankfurt, October 29-30, 2009 Discussion of DSGE Models for Monetary Policy by L. L. Christiano, M. Trabandt & K. Walentin Volker Wieland Goethe University

Real Business Cycle (RBC) Theory

Theory") Real Business Cycle (RBC) Theory ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 17 Readings GLS Ch. 17 GLS Ch. 19 2 / 17 The Neoclassical Model and RBC

Real Business Cycle (RBC) Theory ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 17 Readings GLS Ch. 17 GLS Ch. 19 2 / 17 The Neoclassical Model and RBC

Banks balance sheets, uncertainty and macroeconomy

Banks balance sheets, uncertainty and macroeconomy Ekaterina Pirozhkova Birkbeck College, University of London Recent Developments in Money, Macroeconomics and Finance University of Portsmouth 3rd April

Banks balance sheets, uncertainty and macroeconomy Ekaterina Pirozhkova Birkbeck College, University of London Recent Developments in Money, Macroeconomics and Finance University of Portsmouth 3rd April

DSGE Models and Central Bank Policy Making: A Critical Review

DSGE Models and Central Bank Policy Making: A Critical Review Shiu-Sheng Chen Department of Economics National Taiwan University 12.16.2010 Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 1 / 37

DSGE Models and Central Bank Policy Making: A Critical Review Shiu-Sheng Chen Department of Economics National Taiwan University 12.16.2010 Shiu-Sheng Chen (NTU Econ) DSGE and Policy 12.16.2010 1 / 37

WestminsterResearch

WestminsterResearch http://www.westminster.ac.uk/westminsterresearch The Impact of Uncertainty Shocks under Measurement Error: A Proxy SVAR approach Carriero Andrea, Mumtaz Harron, Theodoridis Konstantinos,

WestminsterResearch http://www.westminster.ac.uk/westminsterresearch The Impact of Uncertainty Shocks under Measurement Error: A Proxy SVAR approach Carriero Andrea, Mumtaz Harron, Theodoridis Konstantinos,

WORKING PAPER SERIES TECHNOLOGY SHOCKS AND ROBUST SIGN RESTRICTIONS IN A EURO AREA SVAR NO. 373 / JULY by Gert Peersman and Roland Straub

WORKING PAPER SERIES NO. 373 / JULY 2004 TECHNOLOGY SHOCKS AND ROBUST SIGN RESTRICTIONS IN A EURO AREA SVAR by Gert Peersman and Roland Straub WORKING PAPER SERIES NO. 373 / JULY 2004 TECHNOLOGY SHOCKS

WORKING PAPER SERIES NO. 373 / JULY 2004 TECHNOLOGY SHOCKS AND ROBUST SIGN RESTRICTIONS IN A EURO AREA SVAR by Gert Peersman and Roland Straub WORKING PAPER SERIES NO. 373 / JULY 2004 TECHNOLOGY SHOCKS

Working Paper. Risk Shocks and Divergence between the Euro area and the US. Highlights. Thomas Brand & Fabien Tripier

No 2014-11 July Working Paper Risk Shocks and Divergence between the Euro area and the US Thomas Brand & Fabien Tripier Highlights Highly synchronized during the Great recession of 2008-2009, the Euro

No 2014-11 July Working Paper Risk Shocks and Divergence between the Euro area and the US Thomas Brand & Fabien Tripier Highlights Highly synchronized during the Great recession of 2008-2009, the Euro

A Policy Model for Analyzing Macroprudential and Monetary Policies

A Policy Model for Analyzing Macroprudential and Monetary Policies Sami Alpanda Gino Cateau Cesaire Meh Bank of Canada November 2013 Alpanda, Cateau, Meh (Bank of Canada) ()Macroprudential - Monetary Policy

A Policy Model for Analyzing Macroprudential and Monetary Policies Sami Alpanda Gino Cateau Cesaire Meh Bank of Canada November 2013 Alpanda, Cateau, Meh (Bank of Canada) ()Macroprudential - Monetary Policy

The Bank of England s forecasting platform

8 March 218 The forecast process: key features Each quarter, the Bank publishes an Inflation Report, including fan charts that depict the MPC s best collective judgement about the most likely paths for

8 March 218 The forecast process: key features Each quarter, the Bank publishes an Inflation Report, including fan charts that depict the MPC s best collective judgement about the most likely paths for

Incorporate Financial Frictions into a

Incorporate Financial Frictions into a Business Cycle Model General idea: Standard model assumes borrowers and lenders are the same people..no conflict of interest Financial friction models suppose borrowers

Incorporate Financial Frictions into a Business Cycle Model General idea: Standard model assumes borrowers and lenders are the same people..no conflict of interest Financial friction models suppose borrowers

Macroeconomic Effects of Financial Shocks: Comment

Macroeconomic Effects of Financial Shocks: Comment Johannes Pfeifer (University of Cologne) 1st Research Conference of the CEPR Network on Macroeconomic Modelling and Model Comparison (MMCN) June 2, 217

Macroeconomic Effects of Financial Shocks: Comment Johannes Pfeifer (University of Cologne) 1st Research Conference of the CEPR Network on Macroeconomic Modelling and Model Comparison (MMCN) June 2, 217

Uncertainty Traps. Pablo Fajgelbaum 1 Edouard Schaal 2 Mathieu Taschereau-Dumouchel 3. March 5, University of Pennsylvania

Uncertainty Traps Pablo Fajgelbaum 1 Edouard Schaal 2 Mathieu Taschereau-Dumouchel 3 1 UCLA 2 New York University 3 Wharton School University of Pennsylvania March 5, 2014 1/59 Motivation Large uncertainty

Uncertainty Traps Pablo Fajgelbaum 1 Edouard Schaal 2 Mathieu Taschereau-Dumouchel 3 1 UCLA 2 New York University 3 Wharton School University of Pennsylvania March 5, 2014 1/59 Motivation Large uncertainty

Real Business Cycle Model

Preview To examine the two modern business cycle theories the real business cycle model and the new Keynesian model and compare them with earlier Keynesian models To understand how the modern business

Preview To examine the two modern business cycle theories the real business cycle model and the new Keynesian model and compare them with earlier Keynesian models To understand how the modern business

Economic Policy Uncertainty and the Yield Curve

5th Conference on Fixed Income Markets Federal Reserve Bank of San Francisco and Bank of Canada Economic Policy Uncertainty and the Yield Curve by Markus Leippold and Felix Matthys Discussion by Anna Cieślak

5th Conference on Fixed Income Markets Federal Reserve Bank of San Francisco and Bank of Canada Economic Policy Uncertainty and the Yield Curve by Markus Leippold and Felix Matthys Discussion by Anna Cieślak

What Can We Learn about News Shocks from the Late 1990 s and Early 2000 s Boom-Bust Period?

What Can We Learn about News Shocks from the Late 99 s and Early s Boom-Bust Period? Nadav Ben Zeev European University Institute May 7, 3 Abstract The boom-bust period of 997-3 is commonly viewed as an

What Can We Learn about News Shocks from the Late 99 s and Early s Boom-Bust Period? Nadav Ben Zeev European University Institute May 7, 3 Abstract The boom-bust period of 997-3 is commonly viewed as an

Microeconomic Heterogeneity and Macroeconomic Shocks

Microeconomic Heterogeneity and Macroeconomic Shocks Greg Kaplan University of Chicago Gianluca Violante Princeton University BdF/ECB Conference on HFC In preparation for the Special Issue of JEP on The

Microeconomic Heterogeneity and Macroeconomic Shocks Greg Kaplan University of Chicago Gianluca Violante Princeton University BdF/ECB Conference on HFC In preparation for the Special Issue of JEP on The

Macro from Micro: Estimates and Implications of Sector-Specific Technical Change. Susanto Basu Boston College and NBER

Macro from Micro: Estimates and Implications of Sector-Specific Technical Change Susanto Basu Boston College and NBER CompNet Conference, Frankfurt, July 1, 2014 Why should central banks care about disaggregated

Macro from Micro: Estimates and Implications of Sector-Specific Technical Change Susanto Basu Boston College and NBER CompNet Conference, Frankfurt, July 1, 2014 Why should central banks care about disaggregated

Stock Market Cross-Sectional Skewness and Business Cycle Fluctuations 1

Stock Market Cross-Sectional Skewness and Business Cycle Fluctuations 1 2 nd CEBRA International Finance and Macroeconomics Meeting Risk, Volatility and Central Bank s Policies Madrid November 2018 1 The

Stock Market Cross-Sectional Skewness and Business Cycle Fluctuations 1 2 nd CEBRA International Finance and Macroeconomics Meeting Risk, Volatility and Central Bank s Policies Madrid November 2018 1 The

News-driven business cycles in small open economies

News-driven business cycles in small open economies Güneş Kamber Konstantinos Theodoridis Christoph Thoenissen 5 November 3 Abstract The focus of this paper is on expectations driven business cycles in

News-driven business cycles in small open economies Güneş Kamber Konstantinos Theodoridis Christoph Thoenissen 5 November 3 Abstract The focus of this paper is on expectations driven business cycles in

The Macroeconomic Impact of Financial and Uncertainty Shocks

The Macroeconomic Impact of Financial and Uncertainty Shocks Dario Caldara a, Cristina Fuentes-Albero a, Simon Gilchrist b, Egon Zakraj sek a a Board of Governors of the Federal Reserve System b Department

The Macroeconomic Impact of Financial and Uncertainty Shocks Dario Caldara a, Cristina Fuentes-Albero a, Simon Gilchrist b, Egon Zakraj sek a a Board of Governors of the Federal Reserve System b Department

The Analytics of the Greek Crisis

The Analytics of the Greek Crisis Gourinchas, Philippon, Vayanos Berkeley, NYU, LSE, NBER & CEPR July 216, Bank of Greece The Greek Depression In 27, Greek GDP per capita was around $35, and the unemployment

The Analytics of the Greek Crisis Gourinchas, Philippon, Vayanos Berkeley, NYU, LSE, NBER & CEPR July 216, Bank of Greece The Greek Depression In 27, Greek GDP per capita was around $35, and the unemployment

The bank lending channel in monetary transmission in the euro area:

The bank lending channel in monetary transmission in the euro area: evidence from Bayesian VAR analysis Matteo Bondesan Graduate student University of Turin (M.Sc. in Economics) Collegio Carlo Alberto

The bank lending channel in monetary transmission in the euro area: evidence from Bayesian VAR analysis Matteo Bondesan Graduate student University of Turin (M.Sc. in Economics) Collegio Carlo Alberto

Fiscal Consolidation in a Currency Union: Spending Cuts Vs. Tax Hikes

Fiscal Consolidation in a Currency Union: Spending Cuts Vs. Tax Hikes Christopher J. Erceg and Jesper Lindé Federal Reserve Board October, 2012 Erceg and Lindé (Federal Reserve Board) Fiscal Consolidations

Fiscal Consolidation in a Currency Union: Spending Cuts Vs. Tax Hikes Christopher J. Erceg and Jesper Lindé Federal Reserve Board October, 2012 Erceg and Lindé (Federal Reserve Board) Fiscal Consolidations

Fiscal Consolidations in Currency Unions: Spending Cuts Vs. Tax Hikes

Fiscal Consolidations in Currency Unions: Spending Cuts Vs. Tax Hikes Christopher J. Erceg and Jesper Lindé Federal Reserve Board June, 2011 Erceg and Lindé (Federal Reserve Board) Fiscal Consolidations

Fiscal Consolidations in Currency Unions: Spending Cuts Vs. Tax Hikes Christopher J. Erceg and Jesper Lindé Federal Reserve Board June, 2011 Erceg and Lindé (Federal Reserve Board) Fiscal Consolidations

Towards Technology-News- Driven Business Cycles

SVERIGES RIKSBANK 360 WORKING PAPER SERIES Towards Technology-News- Driven Business Cycles Paola Di Casola and Spyridon Sichlimiris November 2018 WORKING PAPERS ARE OBTAINABLE FROM www.riksbank.se/en/research

SVERIGES RIKSBANK 360 WORKING PAPER SERIES Towards Technology-News- Driven Business Cycles Paola Di Casola and Spyridon Sichlimiris November 2018 WORKING PAPERS ARE OBTAINABLE FROM www.riksbank.se/en/research

Shocks, frictions and monetary policy Frank Smets

Shocks, frictions and monetary policy Frank Smets OECD Workshop Paris, 14 June 2007 Outline Two results from the Inflation Persistence Network (IPN) and their monetary policy implications Based on Altissimo,

Shocks, frictions and monetary policy Frank Smets OECD Workshop Paris, 14 June 2007 Outline Two results from the Inflation Persistence Network (IPN) and their monetary policy implications Based on Altissimo,

News-driven business cycles in small open economies

News-driven business cycles in small open economies Güneş Kamber Konstantinos Theodoridis Christoph Thoenissen 7 January 6 Abstract The focus of this paper is on news-driven business cycles in small open

News-driven business cycles in small open economies Güneş Kamber Konstantinos Theodoridis Christoph Thoenissen 7 January 6 Abstract The focus of this paper is on news-driven business cycles in small open

Unemployment in an Estimated New Keynesian Model

Unemployment in an Estimated New Keynesian Model Jordi Galí Frank Smets Rafael Wouters March 24, 21 Abstract Following Gali (29), we introduce unemployment as an observable variable in the estimation of

Unemployment in an Estimated New Keynesian Model Jordi Galí Frank Smets Rafael Wouters March 24, 21 Abstract Following Gali (29), we introduce unemployment as an observable variable in the estimation of

Research proposal. Authored by: Hayk Sargsyan

Research proposal Authored by: Hayk Sargsyan mailto:hayk.a.sargsyan@cba.am Outline 1. Introduction a. Research Questions b. Literature review 2. Proposed Method a. Overview of research design b. Data and

Research proposal Authored by: Hayk Sargsyan mailto:hayk.a.sargsyan@cba.am Outline 1. Introduction a. Research Questions b. Literature review 2. Proposed Method a. Overview of research design b. Data and

Comment on Risk Shocks by Christiano, Motto, and Rostagno (2014)

") September 15, 2016 Comment on Risk Shocks by Christiano, Motto, and Rostagno (2014) Abstract In a recent paper, Christiano, Motto and Rostagno (2014, henceforth CMR) report that risk shocks are the most

September 15, 2016 Comment on Risk Shocks by Christiano, Motto, and Rostagno (2014) Abstract In a recent paper, Christiano, Motto and Rostagno (2014, henceforth CMR) report that risk shocks are the most

Principles of Banking (III): Macroeconomics of Banking (1) Introduction

: Macroeconomics of Banking (1) Introduction") Principles of Banking (III): Macroeconomics of Banking (1) Jin Cao (Norges Bank Research, Oslo & CESifo, München) Outline 1 2 Disclaimer (If they care about what I say,) the views expressed in this manuscript

Principles of Banking (III): Macroeconomics of Banking (1) Jin Cao (Norges Bank Research, Oslo & CESifo, München) Outline 1 2 Disclaimer (If they care about what I say,) the views expressed in this manuscript

News Shocks and In ation: Lessons for New Keynesians

News Shocks and In ation: Lessons for New Keynesians André Kurmann Drexel University Christopher Otrok University of Missouri Federal Reserve Bank of St Louis November, 24 Abstract News about future increases

News Shocks and In ation: Lessons for New Keynesians André Kurmann Drexel University Christopher Otrok University of Missouri Federal Reserve Bank of St Louis November, 24 Abstract News about future increases

Discussion of. An Estimated Two-Country DSGE Model for the Euro Area and the US Economy. by Gregory de Walque, Frank Smets and Raf Wouters

Discussion of An Estimated Two-Country DSGE Model for the Euro Area and the US Economy by Gregory de Walque, Frank Smets and Raf Wouters Martin Ellison University of Warwick and CEPR Summary of the contribution

Discussion of An Estimated Two-Country DSGE Model for the Euro Area and the US Economy by Gregory de Walque, Frank Smets and Raf Wouters Martin Ellison University of Warwick and CEPR Summary of the contribution

Contractionary volatility or volatile contractions?

Contractionary volatility or volatile contractions? David Berger, Ian Dew-Becker, and Stefano Giglio February 7, 16 Abstract There is substantial evidence that the volatility of the economy is countercyclical.

Contractionary volatility or volatile contractions? David Berger, Ian Dew-Becker, and Stefano Giglio February 7, 16 Abstract There is substantial evidence that the volatility of the economy is countercyclical.

Common Drifting Volatility in Large Bayesian VARs

Common Drifting Volatility in Large Bayesian VARs Andrea Carriero 1 Todd Clark 2 Massimiliano Marcellino 3 1 Queen Mary, University of London 2 Federal Reserve Bank of Cleveland 3 European University Institute,

Common Drifting Volatility in Large Bayesian VARs Andrea Carriero 1 Todd Clark 2 Massimiliano Marcellino 3 1 Queen Mary, University of London 2 Federal Reserve Bank of Cleveland 3 European University Institute,

Chapter 11. Market-Clearing Models of the Business Cycle. Copyright 2008 Pearson Addison-Wesley. All rights reserved.

Chapter 11 Market-Clearing Models of the Business Cycle Study Two Market-Clearing Business Cycle Models Real Business Cycle Model Keynesian Coordination Failure Model 11-2 Applying Bank Run Model to Financial

Chapter 11 Market-Clearing Models of the Business Cycle Study Two Market-Clearing Business Cycle Models Real Business Cycle Model Keynesian Coordination Failure Model 11-2 Applying Bank Run Model to Financial

Global Financial Conditions, Country Spreads and Macroeconomic Fluctuations in Emerging Countries: A Panel VAR Approach

Global Financial Conditions, Country Spreads and Macroeconomic Fluctuations in Emerging Countries: A Panel VAR Approach Ozge Akinci May, 22 Abstract This paper investigates the extent to which global financial

Global Financial Conditions, Country Spreads and Macroeconomic Fluctuations in Emerging Countries: A Panel VAR Approach Ozge Akinci May, 22 Abstract This paper investigates the extent to which global financial

Central bank losses and monetary policy rules: a DSGE investigation

Central bank losses and monetary policy rules: a DSGE investigation Western Economic Association International Keio University, Tokyo, 21-24 March 219. Jonathan Benchimol 1 and André Fourçans 2 This presentation

Central bank losses and monetary policy rules: a DSGE investigation Western Economic Association International Keio University, Tokyo, 21-24 March 219. Jonathan Benchimol 1 and André Fourçans 2 This presentation

Monetary policy and the asset risk-taking channel

Monetary policy and the asset risk-taking channel Angela Abbate 1 Dominik Thaler 2 1 Deutsche Bundesbank and European University Institute 2 European University Institute Trinity Workshop, 7 November 215

Monetary policy and the asset risk-taking channel Angela Abbate 1 Dominik Thaler 2 1 Deutsche Bundesbank and European University Institute 2 European University Institute Trinity Workshop, 7 November 215

If the Fed sneezes, who gets a cold?

If the Fed sneezes, who gets a cold? Luca Dedola Giulia Rivolta Livio Stracca (ECB) (Univ. of Brescia) (ECB) Spillovers of conventional and unconventional monetary policy: the role of real and financial

If the Fed sneezes, who gets a cold? Luca Dedola Giulia Rivolta Livio Stracca (ECB) (Univ. of Brescia) (ECB) Spillovers of conventional and unconventional monetary policy: the role of real and financial

Stock Market Cross-Sectional Skewness and Business Cycle Fluctuations 1

Stock Market Cross-Sectional Skewness and Business Cycle Fluctuations 1 Ninth BIS CCA Research Conference Rio de Janeiro June 2018 1 Previously presented as Cross-Section Skewness, Business Cycle Fluctuations

Stock Market Cross-Sectional Skewness and Business Cycle Fluctuations 1 Ninth BIS CCA Research Conference Rio de Janeiro June 2018 1 Previously presented as Cross-Section Skewness, Business Cycle Fluctuations

Multistep prediction error decomposition in DSGE models: estimation and forecast performance

Multistep prediction error decomposition in DSGE models: estimation and forecast performance George Kapetanios Simon Price Kings College, University of London Essex Business School Konstantinos Theodoridis

Multistep prediction error decomposition in DSGE models: estimation and forecast performance George Kapetanios Simon Price Kings College, University of London Essex Business School Konstantinos Theodoridis

MFE Macroeconomics Week 3 Exercise

MFE Macroeconomics Week 3 Exercise The first row in the figure below shows monthly data for the Federal Funds Rate and CPI inflation for the period 199m1-18m8. 1 FFR CPI inflation 8 1 6 4 1 199 1995 5

MFE Macroeconomics Week 3 Exercise The first row in the figure below shows monthly data for the Federal Funds Rate and CPI inflation for the period 199m1-18m8. 1 FFR CPI inflation 8 1 6 4 1 199 1995 5

Monetary Policy and a Stock Market Boom-Bust Cycle

Monetary Policy and a Stock Market Boom-Bust Cycle Lawrence Christiano, Cosmin Ilut, Roberto Motto, and Massimo Rostagno Asset markets have been volatile Should monetary policy react to the volatility?

Monetary Policy and a Stock Market Boom-Bust Cycle Lawrence Christiano, Cosmin Ilut, Roberto Motto, and Massimo Rostagno Asset markets have been volatile Should monetary policy react to the volatility?

Capital Flows, Financial Intermediation and Macroprudential Policies

Capital Flows, Financial Intermediation and Macroprudential Policies Matteo F. Ghilardi International Monetary Fund 14 th November 2014 14 th November Capital Flows, 2014 Financial 1 / 24 Inte Introduction

Capital Flows, Financial Intermediation and Macroprudential Policies Matteo F. Ghilardi International Monetary Fund 14 th November 2014 14 th November Capital Flows, 2014 Financial 1 / 24 Inte Introduction

Estimating Contract Indexation in a Financial Accelerator Model

Estimating Contract Indexation in a Financial Accelerator Model Charles T. Carlstrom a, Timothy S. Fuerst b, Alberto Ortiz c, Matthias Paustian d a Senior Economic Advisor, Federal Reserve Bank of Cleveland,

Estimating Contract Indexation in a Financial Accelerator Model Charles T. Carlstrom a, Timothy S. Fuerst b, Alberto Ortiz c, Matthias Paustian d a Senior Economic Advisor, Federal Reserve Bank of Cleveland,

An agnostic SVAR approach to financial shocks

An agnostic SVAR approach to financial shocks Jelena Zivanovic Abstract Since the onset of Great Recession financial factors gained a more prominent role in the business cycle research. In particular,

An agnostic SVAR approach to financial shocks Jelena Zivanovic Abstract Since the onset of Great Recession financial factors gained a more prominent role in the business cycle research. In particular,

Are Intrinsic Inflation Persistence Models Structural in the Sense of Lucas (1976)?

?") Are Intrinsic Inflation Persistence Models Structural in the Sense of Lucas (1976)? Luca Benati, European Central Bank National Bank of Belgium November 19, 2008 This talk is based on 2 papers: Investigating

Are Intrinsic Inflation Persistence Models Structural in the Sense of Lucas (1976)? Luca Benati, European Central Bank National Bank of Belgium November 19, 2008 This talk is based on 2 papers: Investigating

Effects of US Monetary Policy Shocks During Financial Crises - A Threshold Vector Autoregression Approach

Crawford School of Public Policy CAMA Centre for Applied Macroeconomic Analysis Effects of US Monetary Policy Shocks During Financial Crises - A Threshold Vector Autoregression Approach CAMA Working Paper

Crawford School of Public Policy CAMA Centre for Applied Macroeconomic Analysis Effects of US Monetary Policy Shocks During Financial Crises - A Threshold Vector Autoregression Approach CAMA Working Paper

ONLINE APPENDIX TO TFP, NEWS, AND SENTIMENTS: THE INTERNATIONAL TRANSMISSION OF BUSINESS CYCLES

ONLINE APPENDIX TO TFP, NEWS, AND SENTIMENTS: THE INTERNATIONAL TRANSMISSION OF BUSINESS CYCLES Andrei A. Levchenko University of Michigan Nitya Pandalai-Nayar University of Texas at Austin E-mail: alev@umich.edu

ONLINE APPENDIX TO TFP, NEWS, AND SENTIMENTS: THE INTERNATIONAL TRANSMISSION OF BUSINESS CYCLES Andrei A. Levchenko University of Michigan Nitya Pandalai-Nayar University of Texas at Austin E-mail: alev@umich.edu

Estimating and Accounting for the Output Gap with Large Bayesian Vector Autoregressions

Estimating and Accounting for the Output Gap with Large Bayesian Vector Autoregressions James Morley 1 Benjamin Wong 2 1 University of Sydney 2 Reserve Bank of New Zealand The view do not necessarily represent

Estimating and Accounting for the Output Gap with Large Bayesian Vector Autoregressions James Morley 1 Benjamin Wong 2 1 University of Sydney 2 Reserve Bank of New Zealand The view do not necessarily represent

Generalized Dynamic Factor Models and Volatilities: Recovering the Market Volatility Shocks

Generalized Dynamic Factor Models and Volatilities: Recovering the Market Volatility Shocks Paper by: Matteo Barigozzi and Marc Hallin Discussion by: Ross Askanazi March 27, 2015 Paper by: Matteo Barigozzi

Generalized Dynamic Factor Models and Volatilities: Recovering the Market Volatility Shocks Paper by: Matteo Barigozzi and Marc Hallin Discussion by: Ross Askanazi March 27, 2015 Paper by: Matteo Barigozzi

EC910 Econometrics B. Exchange Rate Pass-Through and Inflation Dynamics in. the United Kingdom: VAR analysis of Exchange Rate.

EC910 Econometrics B Exchange Rate Pass-Through and Inflation Dynamics in the United Kingdom: VAR analysis of Exchange Rate Pass-Through 0910249 Department of Economics The University of Warwick Abstract

EC910 Econometrics B Exchange Rate Pass-Through and Inflation Dynamics in the United Kingdom: VAR analysis of Exchange Rate Pass-Through 0910249 Department of Economics The University of Warwick Abstract

News Shocks under Financial Frictions *

News Shocks under Financial Frictions * Christoph Görtz University of Birmingham John D. Tsoukalas University of Glasgow Francesco Zanetti University of Oxford February 24, 27 Abstract We examine the dynamic

News Shocks under Financial Frictions * Christoph Görtz University of Birmingham John D. Tsoukalas University of Glasgow Francesco Zanetti University of Oxford February 24, 27 Abstract We examine the dynamic