Portfolio Optimization under Value-at-Risk Constraints

|

|

|

- Edgar Gaines

- 5 years ago

- Views:

Transcription

1 Portfolio Optimization under Value-at-Risk Constraints Director Chennai Mathematical Institute (Joint work with Prof Tapen Sinha, ITAM, Mexico)

2 1 Introduction Portfolio diversification has been a theme for the ages. In the Merchant of Venice, William Shakespeare had Antonio say: My ventures are not in one bottom trusted, Nor to one place; nor is my whole estate Upon the fortune of this present year

3 2 Introduction... A similar sentiment was echoed by R. L. Stevenson in Treasure Island (1883), where Long John Silver commented on where he keeps his wealth, I puts it all away, some here, some there, and none too much anywheres?

4 3 Introduction... Not all writers had the same belief about diversification. For example, Mark Twain had Pudd?nhead Wilson say: Put all your eggs in the one basket and? watch that basket (Twain, M., 1893, chap. 15). Curiously, Twain was writing the novel to sell it to stave off bankruptcy.

5 4 Introduction... Prior to Markowitz s work, some investors focused on assessing the risks and rewards of individual securities in constructing their portfolios. One view was to identify those securities that offered the best opportunities for gain with the least risk and then construct a portfolio from these.

6 5 Markowitz Markowitz proposed that mean return be taken as a proxy for reward while the standard deviation be taken as a proxy for risk. He argued that for a given level of return, an investor should look for a portfolio that minimizes the standard deviation or if she is comfortable with a given level of risk as measured by standard deviation, then she should look for a portfolio that maximizes the return (mean).

7 6 Markowitz... The next figure shows the risk-return plot for a data on 5 stocks. Here the mean and standard deviation are expressed in basis points (bp) - 1/10000 or 0.01 The points represent risk and return for a chosen portfolio.

8

9 8 Markowitz... Thus every investor should choose a portfolio from among the ones appearing in the next figure, called the efficient frontier.

10

11 10 Markowitz... Tobin argued that the Efficient frontier could be improved upon by adding cash (zero return, zero risk) to the portfolio.

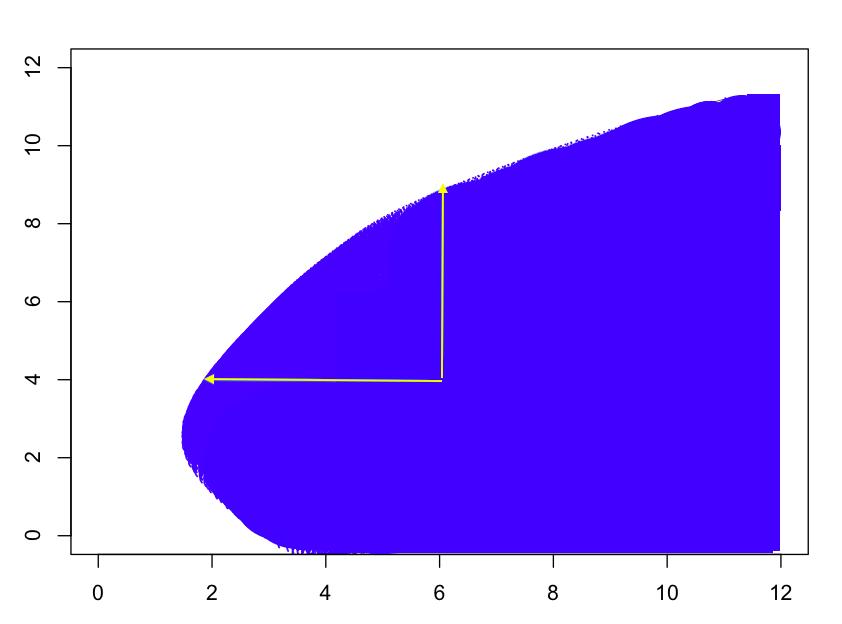

12

13 12 Markowitz... Sharp proposed adding risk free asset (zero risk bonds/ treasury bills) to produce portfolios that improve upon the Markowitz efficient frontier:

14

15 14 Markowitz... Now the efficient frontier is represented by the line that is a tangent to the Markowitz efficient frontier which intersects the vertical axis at the level of the risk-free asset. This line is called Capital Market Line. The slope of the Capital Market line is the Sharp Ratio: σ S = max P m(p) r f σ(p) where m(p),σ(p) are the mean and standard deviation of returns on a portfolio P and the maximum is taken over all portfolios.

16 15 Markowitz... This analysis intrinsically assumes that the returns on stocks follow multivariate normal distribution. Then the returns on any portfolio would follow normal distribution and then the risk can be measured by its standard deviation.

17 16 Beyond Markowitz and Normal distribution For decades it has been noted that the returns on stocks mostly do not follow normal distribution. In most cases, they tend to have fatter tails than normal distribution. In this case, standard deviation may not be a good measure of risk. As a result, for risk management purposes, Value-at-Risk (VaR) has been accepted as a measure of risk and is now part of international regulations on risk management.

18 17 Beyond Markowitz and Normal distribution However, standard deviation as a measure of risk is continued to be used when it comes to optimal portfolio selection via Markowitz paradigm. When we move away from Gaussian or normal distribution, we could also replace mean by median as a measure for return and the gap between median and VaR (say 5%) as a measure for risk.

19 18 Beyond Markowitz and Normal distribution... Recall that 5% VaR for a portfolio P would be the 95 th percentile of the distribution of R(P), where R(P) is the return on the portfolio P, so that R(P) is the loss. Thus we use gap between 50 th percentile and 5 th percentile of distribution of R(P), in other words, (median + VaR) as the measure of risk.

20 19 Beyond Markowitz and Normal distribution... Instead of plotting (median + VaR) vs median, in order to be compatible with Markowitz paradigm, we proceed as follows. For a normal distribution, the 5% VaR is σ away from the mean or median. Thus we plot (median + VaR)/ on x-axis and median on y-axis for the portfolios considered earlier to get the following picture:

21

22 21 Beyond Markowitz and Normal distribution... Now following Markowitz, we could argue that the analogue of the efficient frontier in this paradigm is given by

23

24 23 Beyond Markowitz and Normal distribution.. and the analogue of the Capital Market Line in this paradigm is given by

25

26 25 Beyond Markowitz and Normal distribution.. Here are the two graphs in a single figure.

27

28 27 Beyond Markowitz and Normal distribution.. The analogue of the Sharp Ratio here is the τ R - Tau-ratio, defined as follows: For a portfolio P, let α(p) denote the median of the distribution of the return for the portfolio P and let β 5 (P) denote its 5 th percentile. The 5% VaR is then β 5 (P)). The measure of risk is θ(p) = (α(p) β 5(P))

29 28 Beyond Markowitz and Normal distribution.. and the risk-return measure for the portfolio P is The Tau-ratio is: Γ(P) = α(p) r f θ(p) τ R = sup P Γ(P). If the returns follow multivariate normal distribution, τ R = σ S.

30 29 Computational issues.. If the number of stocks is in hundreds or in thousands, computation of τ R based on historical data and the corresponding portfolio is a difficult task. The sample quantiles of a portfolio are not convex functions of the weights and thus it is a computationally a difficult problem.

31 30 Computational issues.. We have come up with heuristics that seem to improve significantly Γ(P) as compared to the Γ of optimal portfolio achieving the Sharp Ratio. We start with the optimal portfolio achieving the Sharp Ratio for the given riskfree rate r f as well as for rates varying between r f 2 and 2r f. These are our initial set of portfolios.

32 31 Computational issues.. Also, we tweak the historical data to elongate the left tails of the stocks and get the optimal portfolios for the modified historical data, getting alternate set of portfolios.

33 32 Computational issues.. Starting with the initial portfolios, we consider convex combinations of each of these with alternate portfolios and, if it improves Γ, update the initial portfolio and proceed. Also we consider convex combinations of the (updated) initial portfolios with individual stocks and update, if Γ improves. We have done experiments with real market data: data on 496 stocks (out of 500 in SP) - for over 2 years and 2017.

34 33 Computational issues.. For the riskfree rate r f = , the optimal portfolio that achieves the sharp ratio has Γ(P) = The heuristic algorithm that we have developed yields Γ(P) = , a gain of about 30%. It may not be optimal as we have no means of checking this. On the other it provides significant improvement on the optimal portfolio in the Markowitz-Sharp framework as far as Γ is concerned.

35 34 Computational issues.. The current algorithm is taking about 1 hour on a stand alone machine. We have tried running the same with finer grid for convex combinations and have run it for 12 hours, but have not seen improvement as yet as far as maximum Γ(P) is concerned. But there is scope for improvement of the algorithm and we are working on the same.

Lecture 2: Fundamentals of meanvariance

Lecture 2: Fundamentals of meanvariance analysis Prof. Massimo Guidolin Portfolio Management Second Term 2018 Outline and objectives Mean-variance and efficient frontiers: logical meaning o Guidolin-Pedio,

Lecture 2: Fundamentals of meanvariance analysis Prof. Massimo Guidolin Portfolio Management Second Term 2018 Outline and objectives Mean-variance and efficient frontiers: logical meaning o Guidolin-Pedio,

Session 10: Lessons from the Markowitz framework p. 1

Session 10: Lessons from the Markowitz framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 10: Lessons from the Markowitz framework p. 1 Recap The Markowitz question:

Session 10: Lessons from the Markowitz framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 10: Lessons from the Markowitz framework p. 1 Recap The Markowitz question:

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS. BKM Ch 7

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

PORTFOLIO THEORY. Master in Finance INVESTMENTS. Szabolcs Sebestyén

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

Module 3: Factor Models

Module 3: Factor Models (BUSFIN 4221 - Investments) Andrei S. Gonçalves 1 1 Finance Department The Ohio State University Fall 2016 1 Module 1 - The Demand for Capital 2 Module 1 - The Supply of Capital

Module 3: Factor Models (BUSFIN 4221 - Investments) Andrei S. Gonçalves 1 1 Finance Department The Ohio State University Fall 2016 1 Module 1 - The Demand for Capital 2 Module 1 - The Supply of Capital

Return and Risk: The Capital-Asset Pricing Model (CAPM)

") Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

The risk/return trade-off has been a

Efficient Risk/Return Frontiers for Credit Risk HELMUT MAUSSER AND DAN ROSEN HELMUT MAUSSER is a mathematician at Algorithmics Inc. in Toronto, Canada. DAN ROSEN is the director of research at Algorithmics

Efficient Risk/Return Frontiers for Credit Risk HELMUT MAUSSER AND DAN ROSEN HELMUT MAUSSER is a mathematician at Algorithmics Inc. in Toronto, Canada. DAN ROSEN is the director of research at Algorithmics

Techniques for Calculating the Efficient Frontier

Techniques for Calculating the Efficient Frontier Weerachart Kilenthong RIPED, UTCC c Kilenthong 2017 Tee (Riped) Introduction 1 / 43 Two Fund Theorem The Two-Fund Theorem states that we can reach any

Techniques for Calculating the Efficient Frontier Weerachart Kilenthong RIPED, UTCC c Kilenthong 2017 Tee (Riped) Introduction 1 / 43 Two Fund Theorem The Two-Fund Theorem states that we can reach any

Asset Allocation. Cash Flow Matching and Immunization CF matching involves bonds to match future liabilities Immunization involves duration matching

Asset Allocation Strategic Asset Allocation Combines investor s objectives, risk tolerance and constraints with long run capital market expectations to establish asset allocations Create the policy portfolio

Asset Allocation Strategic Asset Allocation Combines investor s objectives, risk tolerance and constraints with long run capital market expectations to establish asset allocations Create the policy portfolio

Optimizing the Omega Ratio using Linear Programming

Optimizing the Omega Ratio using Linear Programming Michalis Kapsos, Steve Zymler, Nicos Christofides and Berç Rustem October, 2011 Abstract The Omega Ratio is a recent performance measure. It captures

Optimizing the Omega Ratio using Linear Programming Michalis Kapsos, Steve Zymler, Nicos Christofides and Berç Rustem October, 2011 Abstract The Omega Ratio is a recent performance measure. It captures

Yale ICF Working Paper No First Draft: February 21, 1992 This Draft: June 29, Safety First Portfolio Insurance

Yale ICF Working Paper No. 08 11 First Draft: February 21, 1992 This Draft: June 29, 1992 Safety First Portfolio Insurance William N. Goetzmann, International Center for Finance, Yale School of Management,

Yale ICF Working Paper No. 08 11 First Draft: February 21, 1992 This Draft: June 29, 1992 Safety First Portfolio Insurance William N. Goetzmann, International Center for Finance, Yale School of Management,

Economics 424/Applied Mathematics 540. Final Exam Solutions

University of Washington Summer 01 Department of Economics Eric Zivot Economics 44/Applied Mathematics 540 Final Exam Solutions I. Matrix Algebra and Portfolio Math (30 points, 5 points each) Let R i denote

University of Washington Summer 01 Department of Economics Eric Zivot Economics 44/Applied Mathematics 540 Final Exam Solutions I. Matrix Algebra and Portfolio Math (30 points, 5 points each) Let R i denote

Portfolio Optimization. Prof. Daniel P. Palomar

Portfolio Optimization Prof. Daniel P. Palomar The Hong Kong University of Science and Technology (HKUST) MAFS6010R- Portfolio Optimization with R MSc in Financial Mathematics Fall 2018-19, HKUST, Hong

Portfolio Optimization Prof. Daniel P. Palomar The Hong Kong University of Science and Technology (HKUST) MAFS6010R- Portfolio Optimization with R MSc in Financial Mathematics Fall 2018-19, HKUST, Hong

(High Dividend) Maximum Upside Volatility Indices. Financial Index Engineering for Structured Products

Maximum Upside Volatility Indices. Financial Index Engineering for Structured Products") (High Dividend) Maximum Upside Volatility Indices Financial Index Engineering for Structured Products White Paper April 2018 Introduction This report provides a detailed and technical look under the hood

(High Dividend) Maximum Upside Volatility Indices Financial Index Engineering for Structured Products White Paper April 2018 Introduction This report provides a detailed and technical look under the hood

Lecture 10-12: CAPM.

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

Mean-Variance Portfolio Theory

Mean-Variance Portfolio Theory Lakehead University Winter 2005 Outline Measures of Location Risk of a Single Asset Risk and Return of Financial Securities Risk of a Portfolio The Capital Asset Pricing

Mean-Variance Portfolio Theory Lakehead University Winter 2005 Outline Measures of Location Risk of a Single Asset Risk and Return of Financial Securities Risk of a Portfolio The Capital Asset Pricing

Risk, return, and diversification

Risk, return, and diversification A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction 2. Diversification and risk 3. Modern portfolio theory 4. Asset pricing models 5. Summary 1.

Risk, return, and diversification A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction 2. Diversification and risk 3. Modern portfolio theory 4. Asset pricing models 5. Summary 1.

Risk Aggregation with Dependence Uncertainty

Risk Aggregation with Dependence Uncertainty Carole Bernard (Grenoble Ecole de Management) Hannover, Current challenges in Actuarial Mathematics November 2015 Carole Bernard Risk Aggregation with Dependence

Risk Aggregation with Dependence Uncertainty Carole Bernard (Grenoble Ecole de Management) Hannover, Current challenges in Actuarial Mathematics November 2015 Carole Bernard Risk Aggregation with Dependence

Optimal Portfolio Selection Under the Estimation Risk in Mean Return

Optimal Portfolio Selection Under the Estimation Risk in Mean Return by Lei Zhu A thesis presented to the University of Waterloo in fulfillment of the thesis requirement for the degree of Master of Mathematics

Optimal Portfolio Selection Under the Estimation Risk in Mean Return by Lei Zhu A thesis presented to the University of Waterloo in fulfillment of the thesis requirement for the degree of Master of Mathematics

Portfolios that Contain Risky Assets 10: Limited Portfolios with Risk-Free Assets

Portfolios that Contain Risky Assets 10: Limited Portfolios with Risk-Free Assets C. David Levermore University of Maryland, College Park, MD Math 420: Mathematical Modeling March 21, 2018 version c 2018

Portfolios that Contain Risky Assets 10: Limited Portfolios with Risk-Free Assets C. David Levermore University of Maryland, College Park, MD Math 420: Mathematical Modeling March 21, 2018 version c 2018

Advanced Financial Economics Homework 2 Due on April 14th before class

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

The mean-variance portfolio choice framework and its generalizations

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

DIFFERENCES BETWEEN MEAN-VARIANCE AND MEAN-CVAR PORTFOLIO OPTIMIZATION MODELS

DIFFERENCES BETWEEN MEAN-VARIANCE AND MEAN-CVAR PORTFOLIO OPTIMIZATION MODELS Panna Miskolczi University of Debrecen, Faculty of Economics and Business, Institute of Accounting and Finance, Debrecen, Hungary

DIFFERENCES BETWEEN MEAN-VARIANCE AND MEAN-CVAR PORTFOLIO OPTIMIZATION MODELS Panna Miskolczi University of Debrecen, Faculty of Economics and Business, Institute of Accounting and Finance, Debrecen, Hungary

Lecture 10: Performance measures

Lecture 10: Performance measures Prof. Dr. Svetlozar Rachev Institute for Statistics and Mathematical Economics University of Karlsruhe Portfolio and Asset Liability Management Summer Semester 2008 Prof.

Lecture 10: Performance measures Prof. Dr. Svetlozar Rachev Institute for Statistics and Mathematical Economics University of Karlsruhe Portfolio and Asset Liability Management Summer Semester 2008 Prof.

Quantitative Risk Management

Quantitative Risk Management Asset Allocation and Risk Management Martin B. Haugh Department of Industrial Engineering and Operations Research Columbia University Outline Review of Mean-Variance Analysis

Quantitative Risk Management Asset Allocation and Risk Management Martin B. Haugh Department of Industrial Engineering and Operations Research Columbia University Outline Review of Mean-Variance Analysis

u (x) < 0. and if you believe in diminishing return of the wealth, then you would require

< 0. and if you believe in diminishing return of the wealth, then you would require") Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Portfolio Risk Management and Linear Factor Models

Chapter 9 Portfolio Risk Management and Linear Factor Models 9.1 Portfolio Risk Measures There are many quantities introduced over the years to measure the level of risk that a portfolio carries, and each

Chapter 9 Portfolio Risk Management and Linear Factor Models 9.1 Portfolio Risk Measures There are many quantities introduced over the years to measure the level of risk that a portfolio carries, and each

Modeling Portfolios that Contain Risky Assets Optimization II: Model-Based Portfolio Management

Modeling Portfolios that Contain Risky Assets Optimization II: Model-Based Portfolio Management C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling January 26, 2012

Modeling Portfolios that Contain Risky Assets Optimization II: Model-Based Portfolio Management C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling January 26, 2012

Adjusting discount rate for Uncertainty

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

Lecture 6: Non Normal Distributions

Lecture 6: Non Normal Distributions and their Uses in GARCH Modelling Prof. Massimo Guidolin 20192 Financial Econometrics Spring 2015 Overview Non-normalities in (standardized) residuals from asset return

Lecture 6: Non Normal Distributions and their Uses in GARCH Modelling Prof. Massimo Guidolin 20192 Financial Econometrics Spring 2015 Overview Non-normalities in (standardized) residuals from asset return

Diversification. Chris Gan; For educational use only

Diversification What is diversification Returns from financial assets display random volatility; and with risk being one of the main factor affecting returns on investments, it is important that portfolio

Diversification What is diversification Returns from financial assets display random volatility; and with risk being one of the main factor affecting returns on investments, it is important that portfolio

CSCI 1951-G Optimization Methods in Finance Part 07: Portfolio Optimization

CSCI 1951-G Optimization Methods in Finance Part 07: Portfolio Optimization March 9 16, 2018 1 / 19 The portfolio optimization problem How to best allocate our money to n risky assets S 1,..., S n with

CSCI 1951-G Optimization Methods in Finance Part 07: Portfolio Optimization March 9 16, 2018 1 / 19 The portfolio optimization problem How to best allocate our money to n risky assets S 1,..., S n with

Financial Economics: Risk Aversion and Investment Decisions, Modern Portfolio Theory

Financial Economics: Risk Aversion and Investment Decisions, Modern Portfolio Theory Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY April, 2015 1 / 95 Outline Modern portfolio theory The backward induction,

Financial Economics: Risk Aversion and Investment Decisions, Modern Portfolio Theory Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY April, 2015 1 / 95 Outline Modern portfolio theory The backward induction,

Log-Robust Portfolio Management

Log-Robust Portfolio Management Dr. Aurélie Thiele Lehigh University Joint work with Elcin Cetinkaya and Ban Kawas Research partially supported by the National Science Foundation Grant CMMI-0757983 Dr.

Log-Robust Portfolio Management Dr. Aurélie Thiele Lehigh University Joint work with Elcin Cetinkaya and Ban Kawas Research partially supported by the National Science Foundation Grant CMMI-0757983 Dr.

SDMR Finance (2) Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)

Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)") SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

FIN 6160 Investment Theory. Lecture 7-10

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

PORTFOLIO OPTIMIZATION AND EXPECTED SHORTFALL MINIMIZATION FROM HISTORICAL DATA

PORTFOLIO OPTIMIZATION AND EXPECTED SHORTFALL MINIMIZATION FROM HISTORICAL DATA We begin by describing the problem at hand which motivates our results. Suppose that we have n financial instruments at hand,

PORTFOLIO OPTIMIZATION AND EXPECTED SHORTFALL MINIMIZATION FROM HISTORICAL DATA We begin by describing the problem at hand which motivates our results. Suppose that we have n financial instruments at hand,

Handout 5: Summarizing Numerical Data STAT 100 Spring 2016

In this handout, we will consider methods that are appropriate for summarizing a single set of numerical measurements. Definition Numerical Data: A set of measurements that are recorded on a naturally

In this handout, we will consider methods that are appropriate for summarizing a single set of numerical measurements. Definition Numerical Data: A set of measurements that are recorded on a naturally

Sample Reports for The Expert Allocator by Investment Technologies

Sample Reports for The Expert Allocator by Investment Technologies Telephone 212/724-7535 Fax 212/208-4384 Support Telephone 203/364-9915 Fax 203/547-6164 e-mail support@investmenttechnologies.com Website

Sample Reports for The Expert Allocator by Investment Technologies Telephone 212/724-7535 Fax 212/208-4384 Support Telephone 203/364-9915 Fax 203/547-6164 e-mail support@investmenttechnologies.com Website

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

Asset Allocation with Exchange-Traded Funds: From Passive to Active Management. Felix Goltz

Asset Allocation with Exchange-Traded Funds: From Passive to Active Management Felix Goltz 1. Introduction and Key Concepts 2. Using ETFs in the Core Portfolio so as to design a Customized Allocation Consistent

Asset Allocation with Exchange-Traded Funds: From Passive to Active Management Felix Goltz 1. Introduction and Key Concepts 2. Using ETFs in the Core Portfolio so as to design a Customized Allocation Consistent

Introduction to Computational Finance and Financial Econometrics Introduction to Portfolio Theory

You can t see this text! Introduction to Computational Finance and Financial Econometrics Introduction to Portfolio Theory Eric Zivot Spring 2015 Eric Zivot (Copyright 2015) Introduction to Portfolio Theory

You can t see this text! Introduction to Computational Finance and Financial Econometrics Introduction to Portfolio Theory Eric Zivot Spring 2015 Eric Zivot (Copyright 2015) Introduction to Portfolio Theory

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College April 26, 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College April 26, 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

FINC 430 TA Session 7 Risk and Return Solutions. Marco Sammon

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

Lecture IV Portfolio management: Efficient portfolios. Introduction to Finance Mathematics Fall Financial mathematics

Lecture IV Portfolio management: Efficient portfolios. Introduction to Finance Mathematics Fall 2014 Reduce the risk, one asset Let us warm up by doing an exercise. We consider an investment with σ 1 =

Lecture IV Portfolio management: Efficient portfolios. Introduction to Finance Mathematics Fall 2014 Reduce the risk, one asset Let us warm up by doing an exercise. We consider an investment with σ 1 =

This appendix discusses two extensions of the cost concepts developed in Chapter 10.

CHAPTER 10 APPENDIX MATHEMATICAL EXTENSIONS OF THE THEORY OF COSTS This appendix discusses two extensions of the cost concepts developed in Chapter 10. The Relationship Between Long-Run and Short-Run Cost

CHAPTER 10 APPENDIX MATHEMATICAL EXTENSIONS OF THE THEORY OF COSTS This appendix discusses two extensions of the cost concepts developed in Chapter 10. The Relationship Between Long-Run and Short-Run Cost

Portfolio Selection using Kernel Regression. J u s s i K l e m e l ä U n i v e r s i t y o f O u l u

Portfolio Selection using Kernel Regression J u s s i K l e m e l ä U n i v e r s i t y o f O u l u abstract We use kernel regression to improve the performance of indexes Utilizing recent price history

Portfolio Selection using Kernel Regression J u s s i K l e m e l ä U n i v e r s i t y o f O u l u abstract We use kernel regression to improve the performance of indexes Utilizing recent price history

Chapter 7 One-Dimensional Search Methods

Chapter 7 One-Dimensional Search Methods An Introduction to Optimization Spring, 2014 1 Wei-Ta Chu Golden Section Search! Determine the minimizer of a function over a closed interval, say. The only assumption

Chapter 7 One-Dimensional Search Methods An Introduction to Optimization Spring, 2014 1 Wei-Ta Chu Golden Section Search! Determine the minimizer of a function over a closed interval, say. The only assumption

The Optimization Process: An example of portfolio optimization

ISyE 6669: Deterministic Optimization The Optimization Process: An example of portfolio optimization Shabbir Ahmed Fall 2002 1 Introduction Optimization can be roughly defined as a quantitative approach

ISyE 6669: Deterministic Optimization The Optimization Process: An example of portfolio optimization Shabbir Ahmed Fall 2002 1 Introduction Optimization can be roughly defined as a quantitative approach

Portfolios that Contain Risky Assets Portfolio Models 9. Long Portfolios with a Safe Investment

Portfolios that Contain Risky Assets Portfolio Models 9. Long Portfolios with a Safe Investment C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling March 21, 2016 version

Portfolios that Contain Risky Assets Portfolio Models 9. Long Portfolios with a Safe Investment C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling March 21, 2016 version

Mean-Variance Analysis

Mean-Variance Analysis Mean-variance analysis 1/ 51 Introduction How does one optimally choose among multiple risky assets? Due to diversi cation, which depends on assets return covariances, the attractiveness

Mean-Variance Analysis Mean-variance analysis 1/ 51 Introduction How does one optimally choose among multiple risky assets? Due to diversi cation, which depends on assets return covariances, the attractiveness

Risk Aversion & Asset Allocation in a Low Repo Rate Climate

Risk Aversion & Asset Allocation in a Low Repo Rate Climate Bachelor degree, Department of Economics 6/1/2017 Authors: Christoffer Clarin Gabriel Ekman Supervisor: Thomas Fischer Abstract This paper addresses

Risk Aversion & Asset Allocation in a Low Repo Rate Climate Bachelor degree, Department of Economics 6/1/2017 Authors: Christoffer Clarin Gabriel Ekman Supervisor: Thomas Fischer Abstract This paper addresses

23.1. Assumptions of Capital Market Theory

NPTEL Course Course Title: Security Analysis and Portfolio anagement Course Coordinator: Dr. Jitendra ahakud odule-12 Session-23 Capital arket Theory-I Capital market theory extends portfolio theory and

NPTEL Course Course Title: Security Analysis and Portfolio anagement Course Coordinator: Dr. Jitendra ahakud odule-12 Session-23 Capital arket Theory-I Capital market theory extends portfolio theory and

Risk Reward Optimisation for Long-Run Investors: an Empirical Analysis

GoBack Risk Reward Optimisation for Long-Run Investors: an Empirical Analysis M. Gilli University of Geneva and Swiss Finance Institute E. Schumann University of Geneva AFIR / LIFE Colloquium 2009 München,

GoBack Risk Reward Optimisation for Long-Run Investors: an Empirical Analysis M. Gilli University of Geneva and Swiss Finance Institute E. Schumann University of Geneva AFIR / LIFE Colloquium 2009 München,

Chapter 5. Asset Allocation - 1. Modern Portfolio Concepts

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

Efficient Frontier and Asset Allocation

Topic 4 Efficient Frontier and Asset Allocation LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of efficient frontier and Markowitz portfolio theory; 2. Discuss

Topic 4 Efficient Frontier and Asset Allocation LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of efficient frontier and Markowitz portfolio theory; 2. Discuss

CSCI 1951-G Optimization Methods in Finance Part 00: Course Logistics Introduction to Finance Optimization Problems

CSCI 1951-G Optimization Methods in Finance Part 00: Course Logistics Introduction to Finance Optimization Problems January 26, 2018 1 / 24 Basic information All information is available in the syllabus

CSCI 1951-G Optimization Methods in Finance Part 00: Course Logistics Introduction to Finance Optimization Problems January 26, 2018 1 / 24 Basic information All information is available in the syllabus

Mean Variance Analysis and CAPM

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

Asset Allocation and Risk Management

IEOR E4602: Quantitative Risk Management Fall 2016 c 2016 by Martin Haugh Asset Allocation and Risk Management These lecture notes provide an introduction to asset allocation and risk management. We begin

IEOR E4602: Quantitative Risk Management Fall 2016 c 2016 by Martin Haugh Asset Allocation and Risk Management These lecture notes provide an introduction to asset allocation and risk management. We begin

Ch. 8 Risk and Rates of Return. Return, Risk and Capital Market. Investment returns

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

University 18 Lessons Financial Management. Unit 12: Return, Risk and Shareholder Value

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

Derivatives and Asset Pricing in a Discrete-Time Setting: Basic Concepts and Strategies

Chapter 1 Derivatives and Asset Pricing in a Discrete-Time Setting: Basic Concepts and Strategies This chapter is organized as follows: 1. Section 2 develops the basic strategies using calls and puts.

Chapter 1 Derivatives and Asset Pricing in a Discrete-Time Setting: Basic Concepts and Strategies This chapter is organized as follows: 1. Section 2 develops the basic strategies using calls and puts.

Intermediate Microeconomics

Name Score Intermediate Microeconomics Ec303-Summer 03 Makeup Exam 1 Part I Please put your answers on the bubble sheet. Be sure to bubble your name in on the back side. 2 points each for a total of 80

Name Score Intermediate Microeconomics Ec303-Summer 03 Makeup Exam 1 Part I Please put your answers on the bubble sheet. Be sure to bubble your name in on the back side. 2 points each for a total of 80

Absolute Alpha by Beta Manipulations

Absolute Alpha by Beta Manipulations Yiqiao Yin Simon Business School October 2014, revised in 2015 Abstract This paper describes a method of achieving an absolute positive alpha by manipulating beta.

Absolute Alpha by Beta Manipulations Yiqiao Yin Simon Business School October 2014, revised in 2015 Abstract This paper describes a method of achieving an absolute positive alpha by manipulating beta.

Lecture 1 of 4-part series. Spring School on Risk Management, Insurance and Finance European University at St. Petersburg, Russia.

Principles and Lecture 1 of 4-part series Spring School on Risk, Insurance and Finance European University at St. Petersburg, Russia 2-4 April 2012 s University of Connecticut, USA page 1 s Outline 1 2

Principles and Lecture 1 of 4-part series Spring School on Risk, Insurance and Finance European University at St. Petersburg, Russia 2-4 April 2012 s University of Connecticut, USA page 1 s Outline 1 2

Risk and Return. CA Final Paper 2 Strategic Financial Management Chapter 7. Dr. Amit Bagga Phd.,FCA,AICWA,Mcom.

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Overnight Index Rate: Model, calibration and simulation

Research Article Overnight Index Rate: Model, calibration and simulation Olga Yashkir and Yuri Yashkir Cogent Economics & Finance (2014), 2: 936955 Page 1 of 11 Research Article Overnight Index Rate: Model,

Research Article Overnight Index Rate: Model, calibration and simulation Olga Yashkir and Yuri Yashkir Cogent Economics & Finance (2014), 2: 936955 Page 1 of 11 Research Article Overnight Index Rate: Model,

KEIR EDUCATIONAL RESOURCES

INVESTMENT PLANNING 2017 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com TABLE

INVESTMENT PLANNING 2017 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com TABLE

6.254 : Game Theory with Engineering Applications Lecture 3: Strategic Form Games - Solution Concepts

6.254 : Game Theory with Engineering Applications Lecture 3: Strategic Form Games - Solution Concepts Asu Ozdaglar MIT February 9, 2010 1 Introduction Outline Review Examples of Pure Strategy Nash Equilibria

6.254 : Game Theory with Engineering Applications Lecture 3: Strategic Form Games - Solution Concepts Asu Ozdaglar MIT February 9, 2010 1 Introduction Outline Review Examples of Pure Strategy Nash Equilibria

Mean-Variance Analysis

Mean-Variance Analysis If the investor s objective is to Maximize the Expected Rate of Return for a given level of Risk (or, Minimize Risk for a given level of Expected Rate of Return), and If the investor

Mean-Variance Analysis If the investor s objective is to Maximize the Expected Rate of Return for a given level of Risk (or, Minimize Risk for a given level of Expected Rate of Return), and If the investor

Modeling Portfolios that Contain Risky Assets Stochastic Models I: One Risky Asset

Modeling Portfolios that Contain Risky Assets Stochastic Models I: One Risky Asset C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling March 25, 2014 version c 2014

Modeling Portfolios that Contain Risky Assets Stochastic Models I: One Risky Asset C. David Levermore University of Maryland, College Park Math 420: Mathematical Modeling March 25, 2014 version c 2014

Principles of Finance Risk and Return. Instructor: Xiaomeng Lu

Principles of Finance Risk and Return Instructor: Xiaomeng Lu 1 Course Outline Course Introduction Time Value of Money DCF Valuation Security Analysis: Bond, Stock Capital Budgeting (Fundamentals) Portfolio

Principles of Finance Risk and Return Instructor: Xiaomeng Lu 1 Course Outline Course Introduction Time Value of Money DCF Valuation Security Analysis: Bond, Stock Capital Budgeting (Fundamentals) Portfolio

Intro to Economic analysis

Intro to Economic analysis Alberto Bisin - NYU 1 The Consumer Problem Consider an agent choosing her consumption of goods 1 and 2 for a given budget. This is the workhorse of microeconomic theory. (Notice

Intro to Economic analysis Alberto Bisin - NYU 1 The Consumer Problem Consider an agent choosing her consumption of goods 1 and 2 for a given budget. This is the workhorse of microeconomic theory. (Notice

Microeconomics of Banking: Lecture 2

Microeconomics of Banking: Lecture 2 Prof. Ronaldo CARPIO September 25, 2015 A Brief Look at General Equilibrium Asset Pricing Last week, we saw a general equilibrium model in which banks were irrelevant.

Microeconomics of Banking: Lecture 2 Prof. Ronaldo CARPIO September 25, 2015 A Brief Look at General Equilibrium Asset Pricing Last week, we saw a general equilibrium model in which banks were irrelevant.

Portfolio Management Under Epistemic Uncertainty Using Stochastic Dominance and Information-Gap Theory

Portfolio Management Under Epistemic Uncertainty Using Stochastic Dominance and Information-Gap Theory D. Berleant, L. Andrieu, J.-P. Argaud, F. Barjon, M.-P. Cheong, M. Dancre, G. Sheble, and C.-C. Teoh

Portfolio Management Under Epistemic Uncertainty Using Stochastic Dominance and Information-Gap Theory D. Berleant, L. Andrieu, J.-P. Argaud, F. Barjon, M.-P. Cheong, M. Dancre, G. Sheble, and C.-C. Teoh

Lecture Notes 9. Jussi Klemelä. December 2, 2014

Lecture Notes 9 Jussi Klemelä December 2, 204 Markowitz Bullets A Markowitz bullet is a scatter plot of points, where each point corresponds to a portfolio, the x-coordinate of a point is the standard

Lecture Notes 9 Jussi Klemelä December 2, 204 Markowitz Bullets A Markowitz bullet is a scatter plot of points, where each point corresponds to a portfolio, the x-coordinate of a point is the standard

Gains from Trade. Rahul Giri

Gains from Trade Rahul Giri Contact Address: Centro de Investigacion Economica, Instituto Tecnologico Autonomo de Mexico (ITAM). E-mail: rahul.giri@itam.mx An obvious question that we should ask ourselves

Gains from Trade Rahul Giri Contact Address: Centro de Investigacion Economica, Instituto Tecnologico Autonomo de Mexico (ITAM). E-mail: rahul.giri@itam.mx An obvious question that we should ask ourselves

Value-at-Risk Based Portfolio Management in Electric Power Sector

Value-at-Risk Based Portfolio Management in Electric Power Sector Ran SHI, Jin ZHONG Department of Electrical and Electronic Engineering University of Hong Kong, HKSAR, China ABSTRACT In the deregulated

Value-at-Risk Based Portfolio Management in Electric Power Sector Ran SHI, Jin ZHONG Department of Electrical and Electronic Engineering University of Hong Kong, HKSAR, China ABSTRACT In the deregulated

Efficient Portfolio and Introduction to Capital Market Line Benninga Chapter 9

Efficient Portfolio and Introduction to Capital Market Line Benninga Chapter 9 Optimal Investment with Risky Assets There are N risky assets, named 1, 2,, N, but no risk-free asset. With fixed total dollar

Efficient Portfolio and Introduction to Capital Market Line Benninga Chapter 9 Optimal Investment with Risky Assets There are N risky assets, named 1, 2,, N, but no risk-free asset. With fixed total dollar

Singular Stochastic Control Models for Optimal Dynamic Withdrawal Policies in Variable Annuities

1/ 46 Singular Stochastic Control Models for Optimal Dynamic Withdrawal Policies in Variable Annuities Yue Kuen KWOK Department of Mathematics Hong Kong University of Science and Technology * Joint work

1/ 46 Singular Stochastic Control Models for Optimal Dynamic Withdrawal Policies in Variable Annuities Yue Kuen KWOK Department of Mathematics Hong Kong University of Science and Technology * Joint work

Optimizing DSM Program Portfolios

Optimizing DSM Program Portfolios William B, Kallock, Summit Blue Consulting, Hinesburg, VT Daniel Violette, Summit Blue Consulting, Boulder, CO Abstract One of the most fundamental questions in DSM program

Optimizing DSM Program Portfolios William B, Kallock, Summit Blue Consulting, Hinesburg, VT Daniel Violette, Summit Blue Consulting, Boulder, CO Abstract One of the most fundamental questions in DSM program

CHAPTER 17 INVESTMENT MANAGEMENT. by Alistair Byrne, PhD, CFA

CHAPTER 17 INVESTMENT MANAGEMENT by Alistair Byrne, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Describe systematic risk and specific risk; b Describe

CHAPTER 17 INVESTMENT MANAGEMENT by Alistair Byrne, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Describe systematic risk and specific risk; b Describe

Financial Analysis The Price of Risk. Skema Business School. Portfolio Management 1.

Financial Analysis The Price of Risk bertrand.groslambert@skema.edu Skema Business School Portfolio Management Course Outline Introduction (lecture ) Presentation of portfolio management Chap.2,3,5 Introduction

Financial Analysis The Price of Risk bertrand.groslambert@skema.edu Skema Business School Portfolio Management Course Outline Introduction (lecture ) Presentation of portfolio management Chap.2,3,5 Introduction

FINANCIAL OPERATIONS RESEARCH: Mean Absolute Deviation And Portfolio Indexing

[1] FINANCIAL OPERATIONS RESEARCH: Mean Absolute Deviation And Portfolio Indexing David Galica Tony Rauchberger Luca Balestrieri A thesis submitted in partial fulfillment of the requirements for the degree

[1] FINANCIAL OPERATIONS RESEARCH: Mean Absolute Deviation And Portfolio Indexing David Galica Tony Rauchberger Luca Balestrieri A thesis submitted in partial fulfillment of the requirements for the degree

CHAPTER II LITERATURE STUDY

CHAPTER II LITERATURE STUDY 2.1. Risk Management Monetary crisis that strike Indonesia during 1998 and 1999 has caused bad impact to numerous government s and commercial s bank. Most of those banks eventually

CHAPTER II LITERATURE STUDY 2.1. Risk Management Monetary crisis that strike Indonesia during 1998 and 1999 has caused bad impact to numerous government s and commercial s bank. Most of those banks eventually

Lecture 7: Bayesian approach to MAB - Gittins index

Advanced Topics in Machine Learning and Algorithmic Game Theory Lecture 7: Bayesian approach to MAB - Gittins index Lecturer: Yishay Mansour Scribe: Mariano Schain 7.1 Introduction In the Bayesian approach

Advanced Topics in Machine Learning and Algorithmic Game Theory Lecture 7: Bayesian approach to MAB - Gittins index Lecturer: Yishay Mansour Scribe: Mariano Schain 7.1 Introduction In the Bayesian approach

Risk Aggregation with Dependence Uncertainty

Risk Aggregation with Dependence Uncertainty Carole Bernard GEM and VUB Risk: Modelling, Optimization and Inference with Applications in Finance, Insurance and Superannuation Sydney December 7-8, 2017

Risk Aggregation with Dependence Uncertainty Carole Bernard GEM and VUB Risk: Modelling, Optimization and Inference with Applications in Finance, Insurance and Superannuation Sydney December 7-8, 2017

INTRODUCTION TO MODERN PORTFOLIO OPTIMIZATION

INTRODUCTION TO MODERN PORTFOLIO OPTIMIZATION Abstract. This is the rst part in my tutorial series- Follow me to Optimization Problems. In this tutorial, I will touch on the basic concepts of portfolio

INTRODUCTION TO MODERN PORTFOLIO OPTIMIZATION Abstract. This is the rst part in my tutorial series- Follow me to Optimization Problems. In this tutorial, I will touch on the basic concepts of portfolio

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

First Welfare Theorem in Production Economies

First Welfare Theorem in Production Economies Michael Peters December 27, 2013 1 Profit Maximization Firms transform goods from one thing into another. If there are two goods, x and y, then a firm can

First Welfare Theorem in Production Economies Michael Peters December 27, 2013 1 Profit Maximization Firms transform goods from one thing into another. If there are two goods, x and y, then a firm can

RETURN AND RISK: The Capital Asset Pricing Model

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

Lecture 8: Producer Behavior

Lecture 8: Producer Behavior October 23, 2018 Overview Course Administration Basics of Production Production in the Short Run Production in the Long Run The Firm s Problem: Cost Minimization Returns to

Lecture 8: Producer Behavior October 23, 2018 Overview Course Administration Basics of Production Production in the Short Run Production in the Long Run The Firm s Problem: Cost Minimization Returns to

Section 7.5 The Normal Distribution. Section 7.6 Application of the Normal Distribution

Section 7.6 Application of the Normal Distribution A random variable that may take on infinitely many values is called a continuous random variable. A continuous probability distribution is defined by

Section 7.6 Application of the Normal Distribution A random variable that may take on infinitely many values is called a continuous random variable. A continuous probability distribution is defined by

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3 1. The following information is provided for GAP, Incorporated, which is traded on NYSE: Fiscal Yr Ending January 31 Close Price

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3 1. The following information is provided for GAP, Incorporated, which is traded on NYSE: Fiscal Yr Ending January 31 Close Price

Asset Allocation in the 21 st Century

Asset Allocation in the 21 st Century Paul D. Kaplan, Ph.D., CFA Quantitative Research Director, Morningstar Europe, Ltd. 2012 Morningstar Europe, Inc. All rights reserved. Harry Markowitz and Mean-Variance

Asset Allocation in the 21 st Century Paul D. Kaplan, Ph.D., CFA Quantitative Research Director, Morningstar Europe, Ltd. 2012 Morningstar Europe, Inc. All rights reserved. Harry Markowitz and Mean-Variance

Dr. Harry Markowitz The Father of Modern Portfolio Theory and the Insight of Behavioral Finance

Special Report Part 1 of 2 Dr. Harry Markowitz The Father of Modern Portfolio Theory and the Insight of Behavioral Finance A Special Interview with SkyView s Advisory Board Member Dr. Harry Markowitz Nobel

Special Report Part 1 of 2 Dr. Harry Markowitz The Father of Modern Portfolio Theory and the Insight of Behavioral Finance A Special Interview with SkyView s Advisory Board Member Dr. Harry Markowitz Nobel

Risk and Return: From Securities to Portfolios

FIN 614 Risk and Return 2: Portfolios Professor Robert B.H. Hauswald Kogod School of Business, AU Risk and Return: From Securities to Portfolios From securities individual risk and return characteristics

FIN 614 Risk and Return 2: Portfolios Professor Robert B.H. Hauswald Kogod School of Business, AU Risk and Return: From Securities to Portfolios From securities individual risk and return characteristics

Chapter 3. Consumer Behavior

Chapter 3 Consumer Behavior Question: Mary goes to the movies eight times a month and seldom goes to a bar. Tom goes to the movies once a month and goes to a bar fifteen times a month. What determine consumers

Chapter 3 Consumer Behavior Question: Mary goes to the movies eight times a month and seldom goes to a bar. Tom goes to the movies once a month and goes to a bar fifteen times a month. What determine consumers