Carbon Penalties & Incentives Project Report Launch

|

|

|

- Lionel Sutton

- 5 years ago

- Views:

Transcription

Partner, Deloitte (Carbon")

1 Carbon Penalties & Incentives Project Report Launch A presentation of the findings of a review of policy effectiveness for carbon reduction and energy efficiency in the commercial buildings sector Sir Robert Finch Bill Hughes Louise Ellison Miles Keeping Jon Lovell Nina Reid Sylvie Sasaki Chairman, Property Industry Alliance Managing Director, Legal & General Property (Chairman, Green Property Alliance) Head of Sustainability, Hammerson (Chair, Green Construction Board Valuation and Demand Working Group) Partner, Deloitte (Carbon Penalties and Incentives Project Team) Global Practice Leader - Real Estate Sustainability, Deloitte (Carbon Penalties and Incentives Project Team) Director: Responsible Property Investment, M&G Real Estate Plan A Project Manager, Marks and Spencer

2 The GCB/GPA Carbon Penalties & Incentives Project A review of policy effectiveness for carbon reduction and energy efficiency in the commercial property sector Launch Presentation 18 June 2014 Jon Lovell [@lovell_jon] #GCBGPACPI

3 Context Government should conduct a comprehensive assessment of nonresidential low-carbon policies to ensure they work effectively. Committee on Climate Change, Carbon Penalties & Incentives

4 Guiding Principles Carried out independently and impartially based on objectively assessed evidence from published sources. Builds upon and complements what has been and is being done elsewhere, including GCB studies. Neutral of all political parties and individual commercial interests. Does not make detailed recommendations on the design or implementation of individual policy instruments, but seeks to: make observations on the types of policies which have been successful in encouraging emissions reductions in commercial property; make positive recommendations for improvements to existing policies based on empirical observation; and make observations as to particular factors which are hampering the success of policies. Informed by structured dialogue with a range of stakeholders 4 Carbon Penalties & Incentives

5 Briefly, methods Scoping: Long-list of instruments prepared - those affecting/concerning the design, implementation and operation of commercial buildings in England & Wales Short-listed in agreement with study Steering Group Literature Review: Instruments consultation documents and responses from industry Regulatory Impact Assessments Academic, professional/industry publications Questionnaire: Online, 330 useable individual responses Respondents involved at all stages of the property lifecycle responded, with broad geographical & organisational size spreads Workshop: 25 participants from stakeholder groups and identified experts from government and industry Examined nature and complexity of instruments 5 Carbon Penalties & Incentives

6 Headlines Disconnected pre-conditions of policy effectiveness Strong consensus on the principles of good policy-making and execution Notable gap between stated importance and perceived adequacy of existing approaches Considerable scope for improving effectiveness of the policy framework Perceptions of complexity and burdensome administration Certain policy types held to be more effective than others Notable trend of declining effectiveness through policy implementation amongst certain policy types Opportunities for simplification, policy bundling and better targeting Overcome heavy bias on operational carbon Transparency and collaboration deficits on policy implementation Harness strong connection between policy familiarity and perceived benefit Clearer sign-posting and trajectories Better bottom-up data collection and analytics Greater independent scrutiny and stronger collaboration between government and industry on policy monitoring 6 Carbon Penalties & Incentives

7 Disconnected pre-conditions of policy effectiveness 7

8 Pre-conditions of policy effectiveness 1. Confidence in policy direction 2. Comprehensive consultations within prescribed timescales 3. Adequate framework for return on investment 4. Policies that make use of markets 5. Incentives that address the risks of efficiency improvements Clear sign-posting Encouraging markets 6. Policies that address all building areas and can be bundled 7. Effective co-ordination between policies 8. Alignment of energy efficiency with wider policy Policy connectivity 9. Complementary Government-led demand creation policies 10. Comprehensive, enforceable review mechanisms 11. Institutions that have resources to oversee implementation Enforcement 8 Carbon Penalties & Incentives

9 Gap between importance and adequacy Current Status Importance E D C B A Strong Weak Low High 9 Carbon Penalties & Incentives

10 Considerable scope for improving effectiveness of the policy framework 10

11 Policy mapping across the property lifecycle *Correct at the time of writing March Carbon Penalties & Incentives

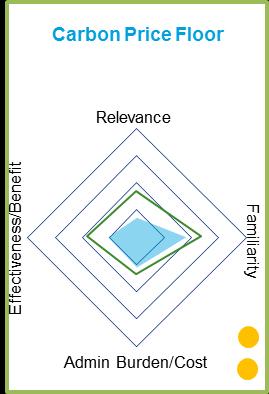

12 Some key market perceptions On the question of whether or not the current framework is sufficiently effective to help meet carbon reduction targets, considerations arise from: Complexity of framework and of individual instruments Industry perception of administrative burden Potential for greater market familiarity, which is likely to lead to greater perceptions of benefit 12 Carbon Penalties & Incentives

13 Some key market perceptions On the question of whether or not the current framework is sufficiently effective to help meet carbon reduction targets, considerations arise from: Complexity of framework and of individual instruments Industry perception of administrative burden Potential for greater market familiarity, which is likely to lead to greater perceptions of benefit 13 Carbon Penalties & Incentives

14 Effectiveness of policy design 14 Carbon Penalties & Incentives

15 Effectiveness of policy implementation 15 Carbon Penalties & Incentives

16 Wide spectrum of perceived effectiveness 16 Carbon Penalties & Incentives

17 Policies having the greatest beneficial effect Building regulations, codes, standards are considered to be the most cost efficient and effective way of changing market participants behaviour it is important to ensure these are dynamic, ambitious, have a clear developmental trajectory and are supported by a broad policy package Choice-editing by prohibiting the use of particular products, e.g. of a specific technology (e.g. HCFCs); products which fail to meet performance criteria (e.g. Eco Products Directive); reducing the liquidity of assets which do not meet pre-determined standards, as per MEPS. Policy bundles are effective: set a minimum standard; devise a label; provide overperformance financial incentives Broad impact policies (e.g. CCL) tend to be less effective. Similarly, those which require a processes or the gathering of information without any compulsion to act on the findings (e.g. Air-Con Assessments) are not found to be particularly effective, 17 Carbon Penalties & Incentives

18 Transparency and collaboration deficits on policy implementation 18

19 Determining the carbon impact of policies Cumulative RIA impact estimates of policy instruments to Carbon Penalties & Incentives

20 Headlines Disconnected pre-conditions of policy effectiveness Strong consensus on the principles of good policy-making and execution Notable gap between stated importance and perceived adequacy of existing approaches Considerable scope for improving effectiveness of the policy framework Perceptions of complexity and burdensome administration Certain policy types held to be more effective than others Notable trend of declining effectiveness through policy implementation amongst certain policy types Opportunities for simplification, policy bundling and better targeting Overcome heavy bias on operational carbon Transparency and collaboration deficits on policy implementation Harness strong connection between policy familiarity and perceived benefit Clearer sign-posting and trajectories Better bottom-up data collection and analytics Greater independent scrutiny and stronger collaboration between government and industry on policy monitoring 20 Carbon Penalties & Incentives

21 Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited ( DTTL ), a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see for a detailed description of the legal structure of DTTL and its member firms. Deloitte LLP is the United Kingdom member firm of DTTL. This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will depend upon the particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication. Deloitte LLP would be pleased to advise readers on how to apply the principles set out in this publication to their specific circumstances. Deloitte LLP accepts no duty of care or liability for any loss occasioned to any person acting or refraining from action as a result of any material in this publication. Deloitte LLP is a limited liability partnership registered in England and Wales with registered number OC and its registered office at 2 New Street Square, London EC4A 3BZ, United Kingdom. Tel: +44 (0) Fax: +44 (0)

22 Carbon Penalties & Incentives Project Report Launch PANEL DISCUSSION Sir Robert Finch Bill Hughes Louise Ellison Miles Keeping Nina Reid Sylvie Sasaki Chairman, Property Industry Alliance Managing Director, Legal & General Property (Chairman, Green Property Alliance) Head of Sustainability, Hammerson (Chair, Green Construction Board Valuation and Demand Working Group) Partner, Deloitte (Carbon Penalties and Incentives Project Team) Director: Responsible Property Investment, M&G Real Estate Plan A Project Manager, Marks and Spencer

Our tax advisory principles A distinctive approach. Blue heading Green heading

Our tax advisory principles A distinctive approach Blue heading Green heading Introduction Our vision at Deloitte is to be the distinctive firm; defined by the impact we have on the success and reputation

Our tax advisory principles A distinctive approach Blue heading Green heading Introduction Our vision at Deloitte is to be the distinctive firm; defined by the impact we have on the success and reputation

UK Indirect Tax Conference Environmental Tax Breakout Session

UK Indirect Tax Conference Environmental Tax Breakout Session Helen Thompson, Matt Parkes, Prem Mehta 14 November 2014 1 Agenda Environmental Tax Strategy News and Developments Case Studies Q&A 2 Environmental

UK Indirect Tax Conference Environmental Tax Breakout Session Helen Thompson, Matt Parkes, Prem Mehta 14 November 2014 1 Agenda Environmental Tax Strategy News and Developments Case Studies Q&A 2 Environmental

Need to know. GAAP: In depth. Non-Financial Reporting Regulations. Contents. In a nutshell

GAAP: In depth Need to know Non-Financial Reporting Regulations Contents In a nutshell Background Scope How has this been implemented into UK law? Groups The requirements How does this differ from existing

GAAP: In depth Need to know Non-Financial Reporting Regulations Contents In a nutshell Background Scope How has this been implemented into UK law? Groups The requirements How does this differ from existing

Find your way in the tax regulatory compliance maze Taxparency.

Find your way in the tax regulatory compliance maze Taxparency www.deloitte.com/ch/taxparency Contents The big picture 01 Business challenges 02 Taxparency Deloitte response 04 Subscription model 06 Regulatory

Find your way in the tax regulatory compliance maze Taxparency www.deloitte.com/ch/taxparency Contents The big picture 01 Business challenges 02 Taxparency Deloitte response 04 Subscription model 06 Regulatory

Shell + BG = An interesting time for share plans Pam Roffe (Shell), Nick Hipwell (Deloitte), Matt Stephen (Deloitte), Paul Churchill (Computershare),

, Nick Hipwell (Deloitte), Matt Stephen (Deloitte), Paul Churchill (Computershare),") Shell + BG = An interesting time for share plans Pam Roffe (Shell), Nick Hipwell (Deloitte), Matt Stephen (Deloitte), Paul Churchill (Computershare), Andy Willis (Computershare) 1 The panel 2 3 Computershare

Shell + BG = An interesting time for share plans Pam Roffe (Shell), Nick Hipwell (Deloitte), Matt Stephen (Deloitte), Paul Churchill (Computershare), Andy Willis (Computershare) 1 The panel 2 3 Computershare

Autumn Budget 2017: The Budget, in full

www.ukbudget.com 22 November 2017 Autumn Budget 2017: The Budget, in full Contents Introduction 1 Tackling tax avoidance, evasion and non-compliance 2 Real estate 2.1 UK real estate 2.2 CGT payment deadline

www.ukbudget.com 22 November 2017 Autumn Budget 2017: The Budget, in full Contents Introduction 1 Tackling tax avoidance, evasion and non-compliance 2 Real estate 2.1 UK real estate 2.2 CGT payment deadline

Feasibility study for the provision of universal telecare services of the over 75s

Feasibility study for the provision of universal telecare services of the over 75s Peter Lock November 2016 Project Context Number of over 75s in Scotland is increasing and emergency admissions from this

Feasibility study for the provision of universal telecare services of the over 75s Peter Lock November 2016 Project Context Number of over 75s in Scotland is increasing and emergency admissions from this

Tyne & Wear Archives & Museums Joint Committee. Annual audit letter to the Members of the Joint Committee for the year ended 31 March 2015

Tyne & Wear Archives & Museums Joint Committee to the Members of the Joint Committee for the year ended 31 March 2015 October 2015 Contents The big picture 2 Purpose and responsibilities 3 Financial reporting

Tyne & Wear Archives & Museums Joint Committee to the Members of the Joint Committee for the year ended 31 March 2015 October 2015 Contents The big picture 2 Purpose and responsibilities 3 Financial reporting

Thinking allowed Climate-related disclosure. Integrating climate-related information in the annual report

Thinking allowed Climate-related disclosure Integrating climate-related information in the annual report Corporate reporting continues to evolve to meet the expectations of investors as the environment

Thinking allowed Climate-related disclosure Integrating climate-related information in the annual report Corporate reporting continues to evolve to meet the expectations of investors as the environment

Hartlepool and Stockton on Tees CCG Annual Audit Letter On the Audit for the year ending 31 March 2015 July 2015

Hartlepool and Stockton on Tees CCG Annual Audit Letter On the Audit for the year ending 31 March 2015 July 2015 Contents 1. Introduction 2 2. Financial audit 3 3. Value for Money 5 4. Conclusions 6 Appendix

Hartlepool and Stockton on Tees CCG Annual Audit Letter On the Audit for the year ending 31 March 2015 July 2015 Contents 1. Introduction 2 2. Financial audit 3 3. Value for Money 5 4. Conclusions 6 Appendix

IFRS industry insights

IFRS Global Office September 2011 IFRS industry insights The new joint s standard insights for the real estate industry IFRS 11 Joint Arrangements may change how investors in the real estate industry account

IFRS Global Office September 2011 IFRS industry insights The new joint s standard insights for the real estate industry IFRS 11 Joint Arrangements may change how investors in the real estate industry account

The Rise of the Exponential Actuary TM

The Rise of the Exponential Actuary TM Actuaries have the opportunity to spend more time as business strategists and offering voices to the C-suite. Opportunity: The transformation of the actuarial profession

The Rise of the Exponential Actuary TM Actuaries have the opportunity to spend more time as business strategists and offering voices to the C-suite. Opportunity: The transformation of the actuarial profession

Ballot begins for IFRS 4 Phase II and Deloitte comments on the IFRS 9 decoupling ED

Ballot begins for IFRS 4 Phase II and Deloitte comments on the IFRS 9 decoupling ED The IASB moves towards completion Francesco Nagari Deloitte Global IFRS Insurance Lead Partner 23 February 2016 Agenda

Ballot begins for IFRS 4 Phase II and Deloitte comments on the IFRS 9 decoupling ED The IASB moves towards completion Francesco Nagari Deloitte Global IFRS Insurance Lead Partner 23 February 2016 Agenda

IFRS industry insights

IFRS Global Office Issue 2, June 2011 IFRS industry insights The Revenue Recognition Project An update for the telecommunications industry Several Board members noted that the objective of the revenue

IFRS Global Office Issue 2, June 2011 IFRS industry insights The Revenue Recognition Project An update for the telecommunications industry Several Board members noted that the objective of the revenue

IFRS 4 Phase II will be IFRS 17, effective from 1/1/21

IFRS 4 Phase II will be IFRS 17, effective from 1/1/21 Many changes approved on the likely final meeting of the multi-year insurance contracts project Francesco Nagari, Deloitte Global IFRS Insurance Leader

IFRS 4 Phase II will be IFRS 17, effective from 1/1/21 Many changes approved on the likely final meeting of the multi-year insurance contracts project Francesco Nagari, Deloitte Global IFRS Insurance Leader

29 th European Hotel Investment Conference Heading into thin air? Andreas Scriven Wednesday 8 November

29 th European Hotel Investment Conference Heading into thin air? Andreas Scriven Wednesday 8 November Chairman s welcome Andreas Scriven Partner - Head of Hospitality & Leisure Deloitte #DeloitteEHIC

29 th European Hotel Investment Conference Heading into thin air? Andreas Scriven Wednesday 8 November Chairman s welcome Andreas Scriven Partner - Head of Hospitality & Leisure Deloitte #DeloitteEHIC

Changes to UK share plan reporting Are you ready?

Changes to UK share plan reporting Are you ready? Significant changes to the UK share plans reporting regime have been introduced. The changes increase the reporting and disclosure requirements for companies,

Changes to UK share plan reporting Are you ready? Significant changes to the UK share plans reporting regime have been introduced. The changes increase the reporting and disclosure requirements for companies,

Hartlepool and Stockton on Tees CCG Annual Audit Letter On the Audit for the year ending 31 March 2014 July 2014

Hartlepool and Stockton on Tees CCG Annual Audit Letter On the Audit for the year ending 31 March 2014 July 2014 Contents 1. Introduction 2 2. Financial audit 3 3. Value for Money 5 4. Conclusions 6 Appendix

Hartlepool and Stockton on Tees CCG Annual Audit Letter On the Audit for the year ending 31 March 2014 July 2014 Contents 1. Introduction 2 2. Financial audit 3 3. Value for Money 5 4. Conclusions 6 Appendix

Governance in brief The longer term viability statement a how to summary guide

October 2015 Governance in brief The longer term viability statement a how to summary guide Headlines The UK Corporate Governance Code requires a longer term viability statement for September 2015 year

October 2015 Governance in brief The longer term viability statement a how to summary guide Headlines The UK Corporate Governance Code requires a longer term viability statement for September 2015 year

Update on recent tax & legal issues relating to global share plans. Andrew Moreton & Richard Wilson

Update on recent tax & legal issues relating to global share plans Andrew Moreton & Richard Wilson 29 September 2016 Introduction 2 Agenda Global updates of the last six months Key trends in employee share

Update on recent tax & legal issues relating to global share plans Andrew Moreton & Richard Wilson 29 September 2016 Introduction 2 Agenda Global updates of the last six months Key trends in employee share

Governance in brief Risk, internal control and viability how September year end reporters have tackled the new Code provisions

January 2016 Governance in brief Risk, internal control and viability how September year end reporters have tackled the new Code provisions Headlines No companies reported any non-compliance for either

January 2016 Governance in brief Risk, internal control and viability how September year end reporters have tackled the new Code provisions Headlines No companies reported any non-compliance for either

PPP Seminar : Education Barnsley Case study

PPP Seminar : Education Barnsley Case study Gavin Quantock Deloitte Corporate Finance 23 July 2014 Case study Barnsley building schools for the future programme PPP and Education Project background Project

PPP Seminar : Education Barnsley Case study Gavin Quantock Deloitte Corporate Finance 23 July 2014 Case study Barnsley building schools for the future programme PPP and Education Project background Project

Indirect Tax Conference Public Sector Breakout. Mark Dyer Ben Powell Nick Comer 14 November 2014

Indirect Tax Conference Public Sector Breakout Mark Dyer Ben Powell Nick Comer 14 November 2014 Agenda Supplies of Staff Partial Exemption and economic use Longridge on the Thames Compliance Trends 2 Case

Indirect Tax Conference Public Sector Breakout Mark Dyer Ben Powell Nick Comer 14 November 2014 Agenda Supplies of Staff Partial Exemption and economic use Longridge on the Thames Compliance Trends 2 Case

The biotech IPO landscape

Biotech IPO Remuneration considerations for biotechs considering an IPO on the Nasdaq August 2018 The biotech IPO landscape This paper examines the executive remuneration planning involved for biotechs

Biotech IPO Remuneration considerations for biotechs considering an IPO on the Nasdaq August 2018 The biotech IPO landscape This paper examines the executive remuneration planning involved for biotechs

The cash paradox: How record cash reserves are influencing corporate behaviour

M&APerspectives January 214 The cash paradox: How record cash reserves are influencing corporate behaviour IDEA IN BRIEF The top 1 non-financial companies globally are holding $2.8 trillion in cash. Commentators

M&APerspectives January 214 The cash paradox: How record cash reserves are influencing corporate behaviour IDEA IN BRIEF The top 1 non-financial companies globally are holding $2.8 trillion in cash. Commentators

A sea of change in new IFRS Standards Impact on the shipping industry

A sea of change in new IFRS Standards Impact on the shipping industry What could the changes mean to the shipping industry? The shipping industry commonly operates through various structures and arrangements

A sea of change in new IFRS Standards Impact on the shipping industry What could the changes mean to the shipping industry? The shipping industry commonly operates through various structures and arrangements

Responsible Tax An integrated approach to tax transparency

Responsible Tax An integrated approach to tax transparency Contents Executive summary 1 Introduction 2 Understanding your stakeholders 3 Making and explaining your case 5 Gathering the right information

Responsible Tax An integrated approach to tax transparency Contents Executive summary 1 Introduction 2 Understanding your stakeholders 3 Making and explaining your case 5 Gathering the right information

Another step closer to finalising IFRS 4 Phase II More education on participating contracts while IFRS 9 is issued in final text

Another step closer to finalising IFRS 4 Phase II More education on participating contracts while IFRS 9 is issued in final text Francesco Nagari Deloitte Global IFRS Insurance Lead Partner 31 July 2014

Another step closer to finalising IFRS 4 Phase II More education on participating contracts while IFRS 9 is issued in final text Francesco Nagari Deloitte Global IFRS Insurance Lead Partner 31 July 2014

IFRS industry insights

IFRS Global Office May 2011 IFRS industry insights The Revenue Recognition Project An update for the consumer business industry Respondents requested that the Boards clarify how to evaluate the transfer

IFRS Global Office May 2011 IFRS industry insights The Revenue Recognition Project An update for the consumer business industry Respondents requested that the Boards clarify how to evaluate the transfer

Annual Shared Services and BPO Conference 2013 How to successfully include tax activities within your shared services organisation

Annual Shared Services and BPO Conference 2013 How to successfully include tax activities within your shared services organisation Nandor Makos, James Tooley & Pippa Booth Introductions Nándor Makos Pippa

Annual Shared Services and BPO Conference 2013 How to successfully include tax activities within your shared services organisation Nandor Makos, James Tooley & Pippa Booth Introductions Nándor Makos Pippa

UK Indirect Tax Conference 2014 Compliance in Perspective Consumer Business Case Law. Oliver Jarratt 14 November 2014

UK Indirect Tax Conference 2014 Compliance in Perspective Consumer Business Case Law Oliver Jarratt 14 November 2014 1 Contents Place of supply Finance exemption Adjustments Barter, free stuff and no supply

UK Indirect Tax Conference 2014 Compliance in Perspective Consumer Business Case Law Oliver Jarratt 14 November 2014 1 Contents Place of supply Finance exemption Adjustments Barter, free stuff and no supply

IFRS in Focus. IASB issues an Interpretation and minor changes to IFRS. Contents. The Bottom Line. IFRS Global Office December 2016

IFRS Global Office December 2016 IFRS in Focus IASB issues an Interpretation and minor changes to IFRS Contents Transfers of Investment Property (Amendments to IAS 40) IFRIC 22 Foreign Currency Transactions

IFRS Global Office December 2016 IFRS in Focus IASB issues an Interpretation and minor changes to IFRS Contents Transfers of Investment Property (Amendments to IAS 40) IFRIC 22 Foreign Currency Transactions

The Deloitte CFO Survey Political risk and corporate expansion

The Deloitte CFO Survey Political risk and corporate expansion Political risk has eclipsed worries about the economy as a concern for the Chief Financial Officers of the UK s largest companies. CFOs rank

The Deloitte CFO Survey Political risk and corporate expansion Political risk has eclipsed worries about the economy as a concern for the Chief Financial Officers of the UK s largest companies. CFOs rank

Link n Learn Client Asset rules across Europe

Link n Learn Client Asset rules across Europe May 2016 Presenters Dennis Cheng Director Dennis leads the firm s Banking and Capital Markets CASS proposition and has over 9 years of experience assisting

Link n Learn Client Asset rules across Europe May 2016 Presenters Dennis Cheng Director Dennis leads the firm s Banking and Capital Markets CASS proposition and has over 9 years of experience assisting

MiFID II & MiFIR Update. Link`n Learn August 2016

MiFID II & MiFIR Update Link`n Learn 2016 11 August 2016 Speakers Manmeet Rana Director Risk Advisory Deloitte UK E: mrana@deloitte.co.uk T: +44 20 7303 8624 Ciara O Grady Manager Audit Deloitte Ireland

MiFID II & MiFIR Update Link`n Learn 2016 11 August 2016 Speakers Manmeet Rana Director Risk Advisory Deloitte UK E: mrana@deloitte.co.uk T: +44 20 7303 8624 Ciara O Grady Manager Audit Deloitte Ireland

Need to know FRC proposals on going concern: Implementing the recommendations of the Sharman Panel

Need to know FRC proposals on going concern: Implementing the recommendations of the Sharman Panel In a nutshell The FRC is proposing new Guidance on Going Concern 2013, applicable to all UK companies,

Need to know FRC proposals on going concern: Implementing the recommendations of the Sharman Panel In a nutshell The FRC is proposing new Guidance on Going Concern 2013, applicable to all UK companies,

UK Taxation of Real Estate. Kathryn Wintle & Barry Curtis 23 April 2015

UK Taxation of Real Estate Kathryn Wintle & Barry Curtis 23 April 2015 Contents Background UK NRL compliance VAT considerations Stamp Duty Land Tax Annual Tax on Enveloped Dwellings Capital Gains Tax on

UK Taxation of Real Estate Kathryn Wintle & Barry Curtis 23 April 2015 Contents Background UK NRL compliance VAT considerations Stamp Duty Land Tax Annual Tax on Enveloped Dwellings Capital Gains Tax on

Private Equity Tax Autumn Briefing

Private Equity: Tax Autumn Briefing Private Equity Tax Autumn Briefing HMRC consultations seem to have been the flavour of the summer, with a large number of recent or ongoing HMRC consultations of importance

Private Equity: Tax Autumn Briefing Private Equity Tax Autumn Briefing HMRC consultations seem to have been the flavour of the summer, with a large number of recent or ongoing HMRC consultations of importance

June The new remuneration report Disclosure regulations

June 2013 The new remuneration report Disclosure regulations The new remuneration disclosure regulations have now been laid in Parliament for approval. Assuming they are approved, they will come into force

June 2013 The new remuneration report Disclosure regulations The new remuneration disclosure regulations have now been laid in Parliament for approval. Assuming they are approved, they will come into force

London Borough of Hillingdon. Annual audit letter to the Members of the Council for the year ended 31 March 2015

London Borough of Hillingdon to the Members of the Council for the year ended 31 March 2015 29 September 2015 Contents The big picture 2 Purpose and responsibilities 3 Financial reporting 4 Value for Money

London Borough of Hillingdon to the Members of the Council for the year ended 31 March 2015 29 September 2015 Contents The big picture 2 Purpose and responsibilities 3 Financial reporting 4 Value for Money

VAT and e- Publishing Update on current issues. Abi Briggs, David Latief and Vivien Pereira 9 September 2014

VAT and e- Publishing Update on current issues Abi Briggs, David Latief and Vivien Pereira 9 September 2014 Agenda Introductions VAT on e-publishing Overview The issue Current market activity and what

VAT and e- Publishing Update on current issues Abi Briggs, David Latief and Vivien Pereira 9 September 2014 Agenda Introductions VAT on e-publishing Overview The issue Current market activity and what

PULSE Quarterly Newsletter of Deloitte s Charities and Not for Profit Group

Spring 2014 PULSE Quarterly Newsletter of Deloitte s Charities and Not for Profit Group Happy New Year! Welcome to the first edition of Pulse in 2014. A new year brings with it many challenges, but all

Spring 2014 PULSE Quarterly Newsletter of Deloitte s Charities and Not for Profit Group Happy New Year! Welcome to the first edition of Pulse in 2014. A new year brings with it many challenges, but all

Inspiring consumer confidence in challenging economic times. Graham Pickett Lead Partner Travel, Hospitality & Leisure June 2013

Inspiring consumer confidence in challenging economic times Graham Pickett Lead Partner Travel, Hospitality & Leisure June 2013 Inspiring consumer confidence in challenging economic times Agenda Europe

Inspiring consumer confidence in challenging economic times Graham Pickett Lead Partner Travel, Hospitality & Leisure June 2013 Inspiring consumer confidence in challenging economic times Agenda Europe

Discussion Paper DP 2014/1 Accounting for Dynamic Risk Management: a Portfolio Revaluation Approach to Macro Hedging

Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London United Kingdom EC4M 6XH Deloitte Touche Tohmatsu Limited 2 New Street Square London EC4A 3BZ United Kingdom Tel:

Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London United Kingdom EC4M 6XH Deloitte Touche Tohmatsu Limited 2 New Street Square London EC4A 3BZ United Kingdom Tel:

Consultative Document - Guidance on accounting for expected credit losses

Basel Committee on Banking Supervision Bank for International Settlements Centralbahnplatz 2 4051 Basel Switzerland Deloitte Touche Tohmatsu Limited 2 New Street Square London EC4A 3BZ United Kingdom Tel:

Basel Committee on Banking Supervision Bank for International Settlements Centralbahnplatz 2 4051 Basel Switzerland Deloitte Touche Tohmatsu Limited 2 New Street Square London EC4A 3BZ United Kingdom Tel:

Listed private equity Key investor considerations for understanding listed private equity portfolio valuations

Listed private equity Key investor considerations for understanding listed private equity portfolio valuations Contacts Deloitte Garrath Marshall Audit Partner gmarshall@deloitte.co.uk Yasir Aziz Audit

Listed private equity Key investor considerations for understanding listed private equity portfolio valuations Contacts Deloitte Garrath Marshall Audit Partner gmarshall@deloitte.co.uk Yasir Aziz Audit

Re: Exposure Draft, Proposed Revisions Pertaining to Safeguards in the Code Phase 2 and Related Conforming Amendments

Deloitte Touche Tohmatsu Limited 30 Rockefeller Plaza New York, NY 10112-0015 USA April 26, 2017 Tel: +1 212 492 4000 Fax: +1 212 492 4001 www.deloitte.com Chair International Ethics Standards Board for

Deloitte Touche Tohmatsu Limited 30 Rockefeller Plaza New York, NY 10112-0015 USA April 26, 2017 Tel: +1 212 492 4000 Fax: +1 212 492 4001 www.deloitte.com Chair International Ethics Standards Board for

UK Indirect Tax Conference 2015 Public Sector. Mark Dyer 11 November 2015

UK Indirect Tax Conference 2015 Public Sector Mark Dyer 11 November 2015 Agenda Health & Social Care Integration Better Care Fund Alternative Delivery Models and Tax Consequences Taxable Adult Social Care,

UK Indirect Tax Conference 2015 Public Sector Mark Dyer 11 November 2015 Agenda Health & Social Care Integration Better Care Fund Alternative Delivery Models and Tax Consequences Taxable Adult Social Care,

We are pleased to respond to your request for comments on the proposals set out in PCP 2012/1.

Deloitte LLP Athene Place 66 Shoe Lane London EC4A 3BQ Tel: +44 (0) 20 7936 3000 Fax: +44 (0) 20 7583 1198 www.deloitte.co.uk The Secretary to the Code Committee The Takeover Panel 10 Paternoster Square

Deloitte LLP Athene Place 66 Shoe Lane London EC4A 3BQ Tel: +44 (0) 20 7936 3000 Fax: +44 (0) 20 7583 1198 www.deloitte.co.uk The Secretary to the Code Committee The Takeover Panel 10 Paternoster Square

Exposure Draft ED 2015/6 Clarifications to IFRS 15

Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London United Kingdom EC4M 6XH Deloitte Touche Tohmatsu Limited 2 New Street Square London EC4A 3BZ United Kingdom Tel:

Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London United Kingdom EC4M 6XH Deloitte Touche Tohmatsu Limited 2 New Street Square London EC4A 3BZ United Kingdom Tel:

Talent in Insurance 2015 The Netherlands in Focus. UK Financial Services Insight

Talent in Insurance 2015 The Netherlands in Focus UK Financial Services Insight Report contents The Netherlands in Focus Key findings Macroeconomic and industry context Survey findings 2 Key findings 3

Talent in Insurance 2015 The Netherlands in Focus UK Financial Services Insight Report contents The Netherlands in Focus Key findings Macroeconomic and industry context Survey findings 2 Key findings 3

Deloitte LLP welcomes the opportunity to comment on the Financial Reporting Council s Discussion Paper: Improving the Statement of Cash Flows.

Deloitte LLP 2 New Street Square London EC4A 3BZ Phone: +44 (0)20 7936 3000 Fax: +44 (0)20 7583 1198 www.deloitte.co.uk 3 April 2017 Direct phone: +44 20 7007 0084 vepoole@deloitte.co.uk Andrew Lennard

Deloitte LLP 2 New Street Square London EC4A 3BZ Phone: +44 (0)20 7936 3000 Fax: +44 (0)20 7583 1198 www.deloitte.co.uk 3 April 2017 Direct phone: +44 20 7007 0084 vepoole@deloitte.co.uk Andrew Lennard

XSG. Economic Scenario Generator. Risk-neutral and real-world Monte Carlo modelling solutions for insurers

XSG Economic Scenario Generator Risk-neutral and real-world Monte Carlo modelling solutions for insurers 2 Introduction to XSG What is XSG? XSG is Deloitte s economic scenario generation software solution,

XSG Economic Scenario Generator Risk-neutral and real-world Monte Carlo modelling solutions for insurers 2 Introduction to XSG What is XSG? XSG is Deloitte s economic scenario generation software solution,

Need to know. FRC publishes Triennial review 2017 Incremental improvements and clarifications (Amendments to FRS 102) Contents

Contents") FRC publishes Triennial review 2017 Incremental improvements and clarifications (Amendments to FRS 102) Contents Background What are the main areas of improvement or clarification? Effective date and early

FRC publishes Triennial review 2017 Incremental improvements and clarifications (Amendments to FRS 102) Contents Background What are the main areas of improvement or clarification? Effective date and early

Directors remuneration in FTSE 100 companies the story of the 2015 AGM season so far Initial findings and the reaction of shareholders

Directors remuneration in FTSE 100 companies the story of the 2015 AGM season so far Initial findings and the reaction of shareholders The Deloitte Academy: Promoting excellence in the boardroom June 2015

Directors remuneration in FTSE 100 companies the story of the 2015 AGM season so far Initial findings and the reaction of shareholders The Deloitte Academy: Promoting excellence in the boardroom June 2015

The Deloitte-Brazilian Chamber of Commerce in Great Britain Survey 2015

The Deloitte-Brazilian Chamber of Commerce in Great Britain Survey 2015 UK companies are optimistic about their short term prospects in Brazil despite the headwinds in the economy. Deloitte and the Brazilian

The Deloitte-Brazilian Chamber of Commerce in Great Britain Survey 2015 UK companies are optimistic about their short term prospects in Brazil despite the headwinds in the economy. Deloitte and the Brazilian

Divestments can create shareholder value for both buyers and sellers, if done with clarity of purpose on both sides.

Upfront in brief Divestments: Creating shareholder value IDEA IN BRIEF Divestments are set to play an increasingly large role in company strategies as they seek to realign their business models for growth.

Upfront in brief Divestments: Creating shareholder value IDEA IN BRIEF Divestments are set to play an increasingly large role in company strategies as they seek to realign their business models for growth.

The Deloitte CFO Survey

20 The Deloitte CFO Survey The year ahead: A cautious start to 2016 Support among the Chief Financial Officers of the UK s largest corporates for staying in the EU has narrowed, mirroring a drift towards

20 The Deloitte CFO Survey The year ahead: A cautious start to 2016 Support among the Chief Financial Officers of the UK s largest corporates for staying in the EU has narrowed, mirroring a drift towards

Draft Head of Internal Audit Opinion 2012/13 Isle of Wight NHS Trust

Draft Head of Internal Audit Opinion 2012/13 Isle of Wight NHS Trust. Contents Introduction 1 The Head of Internal Audit Opinion 2 Commentary 3 Appendix 1 - Key to Assurance Levels 7 Appendix 2 - Statement

Draft Head of Internal Audit Opinion 2012/13 Isle of Wight NHS Trust. Contents Introduction 1 The Head of Internal Audit Opinion 2 Commentary 3 Appendix 1 - Key to Assurance Levels 7 Appendix 2 - Statement

The Deloitte Consumer Tracker Confidence pauses as consumers react to wider uncertainty

2016 The Deloitte Consumer Tracker Confidence pauses as consumers react to wider uncertainty The latest Deloitte Consumer Tracker shows a fall in consumer confidence in the first quarter of 2016, a sign

2016 The Deloitte Consumer Tracker Confidence pauses as consumers react to wider uncertainty The latest Deloitte Consumer Tracker shows a fall in consumer confidence in the first quarter of 2016, a sign

2016 Swiss Tax Management Survey Executive summary

2016 Swiss Tax Management Survey Executive summary Survey overview The survey was undertaken to understand how companies are responding to international tax reform and the increasing pressure to respond

2016 Swiss Tax Management Survey Executive summary Survey overview The survey was undertaken to understand how companies are responding to international tax reform and the increasing pressure to respond

MCGILL GUIDE TO UNIT-LEVEL CLIMATE AND SUSTAINABILITY ACTION PLANNING

MCGILL GUIDE TO UNIT-LEVEL CLIMATE AND SUSTAINABILITY ACTION PLANNING Prepared by the McGill Office of Sustainability January 2018 Introduction Context McGill adopted a Climate and Sustainability Action

MCGILL GUIDE TO UNIT-LEVEL CLIMATE AND SUSTAINABILITY ACTION PLANNING Prepared by the McGill Office of Sustainability January 2018 Introduction Context McGill adopted a Climate and Sustainability Action

The Deloitte Consumer Tracker. Confidence remains undented Q Key indicators. Authors -5% -6% -4% -4% +5% +12% -2% 0% -1.1% +7.1% +0.2% +1.

Q4 The Deloitte Consumer Tracker Confidence remains undented In a sign that consumer sentiment has remained resilient following the Brexit vote, the latest Deloitte Consumer Tracker shows that despite

Q4 The Deloitte Consumer Tracker Confidence remains undented In a sign that consumer sentiment has remained resilient following the Brexit vote, the latest Deloitte Consumer Tracker shows that despite

30 th European Hotel Investment Conference Experience the future. Simon Oaten & Guy Langford Wednesday 7 November

30 th European Hotel Investment Conference Experience the future Simon Oaten & Guy Langford Wednesday 7 November Passion for leisure Both strong economic fundamentals as well as changes in consumer behaviour

30 th European Hotel Investment Conference Experience the future Simon Oaten & Guy Langford Wednesday 7 November Passion for leisure Both strong economic fundamentals as well as changes in consumer behaviour

Time to get focused 2016 Manufacturing & Industrials M&A Predictions

Time to get focused 2 Manufacturing & Industrials M&A Predictions Contents Foreword 1 UK Industrial Products M&A Survey and Outlook 2 The UK environment 4 Britain means Brexit 5 Looking ahead 8 Our Manufacturing

Time to get focused 2 Manufacturing & Industrials M&A Predictions Contents Foreword 1 UK Industrial Products M&A Survey and Outlook 2 The UK environment 4 Britain means Brexit 5 Looking ahead 8 Our Manufacturing

Exposure Draft ED 2013/10 Equity Method in Separate Financial Statements

Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London United Kingdom EC4M 6XH Deloitte Touche Tohmatsu Limited 2 New Street Square London EC4A 3BZ United Kingdom Tel:

Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London United Kingdom EC4M 6XH Deloitte Touche Tohmatsu Limited 2 New Street Square London EC4A 3BZ United Kingdom Tel:

The Deloitte Consumer Tracker Consumer confidence sees its largest increase in 18 months

The Deloitte Consumer Tracker Consumer confidence sees its largest increase in 18 months Q3 The latest Deloitte Consumer Tracker shows that UK consumers have shrugged off postreferendum pessimism, with

The Deloitte Consumer Tracker Consumer confidence sees its largest increase in 18 months Q3 The latest Deloitte Consumer Tracker shows that UK consumers have shrugged off postreferendum pessimism, with

September 2017 IFRS Interpretations Committee Meeting Project IAS 12 Income Taxes Interest and penalties Introduction

Agenda ref 5B STAFF PAPER IFRS Interpretations Committee Meeting September 2017 Project Paper topic IAS 12 Income Taxes Interest and penalties Agenda decision to finalise CONTACT(S) Craig Smith csmith@ifrs.org

Agenda ref 5B STAFF PAPER IFRS Interpretations Committee Meeting September 2017 Project Paper topic IAS 12 Income Taxes Interest and penalties Agenda decision to finalise CONTACT(S) Craig Smith csmith@ifrs.org

Tax Strategy for The Bahamas as an IFC 2 March 2018

Tax Strategy for The Bahamas as an IFC 2 March 2018 Agenda Tax Strategy for The Bahamas Current global environment Tax strategies of other IFCs Potential impacts of corporate tax Policy considerations

Tax Strategy for The Bahamas as an IFC 2 March 2018 Agenda Tax Strategy for The Bahamas Current global environment Tax strategies of other IFCs Potential impacts of corporate tax Policy considerations

The calm before the reform Basel III

The calm before the reform Basel III The publication of the Basel III 2017 reforms was a watershed moment for capital regulation globally. In contrast to the fundamental changes which the reforms represent

The calm before the reform Basel III The publication of the Basel III 2017 reforms was a watershed moment for capital regulation globally. In contrast to the fundamental changes which the reforms represent

The proposed solution to the de-coupling of IFRS 9 and IFRS 4 Phase II

The proposed solution to the de-coupling of IFRS 9 and IFRS 4 Phase II Overlay Approach and Deferral Approach Francesco Nagari Deloitte Global IFRS Insurance Lead Partner 12 January 2016 Agenda Summary

The proposed solution to the de-coupling of IFRS 9 and IFRS 4 Phase II Overlay Approach and Deferral Approach Francesco Nagari Deloitte Global IFRS Insurance Lead Partner 12 January 2016 Agenda Summary

A launch pad for growth How UK big businesses are planning to increase investment

A launch pad for growth How UK big businesses are planning to increase investment Key points Deloitte LLP estimates that businesses based in the UK with a turnover of more than 1 billion will invest around

A launch pad for growth How UK big businesses are planning to increase investment Key points Deloitte LLP estimates that businesses based in the UK with a turnover of more than 1 billion will invest around

James Tooley and Demian de Souza, Deloitte

Deloitte Shared Services, GBS & BPO Conference Breakout 7: Transforming your Tax operating model James Tooley and Demian de Souza, Deloitte 14-15 September 2016 Lisbon, Portugal #DeloitteSharedServices

Deloitte Shared Services, GBS & BPO Conference Breakout 7: Transforming your Tax operating model James Tooley and Demian de Souza, Deloitte 14-15 September 2016 Lisbon, Portugal #DeloitteSharedServices

Defined Benefit Pension Schemes Deloitte Funding Tracker Q How does your scheme compare?

Defined Benefit Pension Schemes Deloitte Funding Tracker The Deloitte Scheme Funding Deficit Tracker shows how the deficit of three illustrative schemes with Return Seeking, Lower Risk and Hedging investment

Defined Benefit Pension Schemes Deloitte Funding Tracker The Deloitte Scheme Funding Deficit Tracker shows how the deficit of three illustrative schemes with Return Seeking, Lower Risk and Hedging investment

Chief Internal Auditor Conference 2017 Building Trust. Making an Impact.

Chief Internal Auditor Conference 2017 Building Trust. Making an Impact. 6 January 2017 Welcome Peter Astley EMEA Internal Audit Lead Risk Advisory 2 Deloitte s Global Chief Audit Executive Survey Evolution

Chief Internal Auditor Conference 2017 Building Trust. Making an Impact. 6 January 2017 Welcome Peter Astley EMEA Internal Audit Lead Risk Advisory 2 Deloitte s Global Chief Audit Executive Survey Evolution

CONTACT(S) Craig Smith +44 (0)

Craig Smith +44 (0)") Agenda ref 5A STAFF PAPER IFRS Interpretations Committee Meeting September 2017 Project Paper topic IFRS 9 Financial Instruments Financial assets eligible for the election to present changes in fair value

Agenda ref 5A STAFF PAPER IFRS Interpretations Committee Meeting September 2017 Project Paper topic IFRS 9 Financial Instruments Financial assets eligible for the election to present changes in fair value

Measuring the return from pharmaceutical innovation 2017 Methodology

Measuring the return from pharmaceutical innovation 2017 Methodology Contents Introduction 01 Methodology 02 Original cohort 03 Extension cohort 03 Assets evaluated 03 Methodology amendments and restatements

Measuring the return from pharmaceutical innovation 2017 Methodology Contents Introduction 01 Methodology 02 Original cohort 03 Extension cohort 03 Assets evaluated 03 Methodology amendments and restatements

Employment status and. Off-payroll working in the public sector. June 2017

Employment status and Off-payroll working in the public sector June 2017 Agenda Background Assessing employment status for tax purposes Using HMRC s web based tool CEST (formerly ESS, formerly ESI) What

Employment status and Off-payroll working in the public sector June 2017 Agenda Background Assessing employment status for tax purposes Using HMRC s web based tool CEST (formerly ESS, formerly ESI) What

Responsible Tax Tax transparency developments in 2014

Responsible Tax Tax transparency developments in 2014 Contents 1. Executive summary 1 2. A look back at 2014 2 3. The evolving response of business 8 4. Where next? 9 Appendix: Comparison of tax transparency

Responsible Tax Tax transparency developments in 2014 Contents 1. Executive summary 1 2. A look back at 2014 2 3. The evolving response of business 8 4. Where next? 9 Appendix: Comparison of tax transparency

GOOD BEST BETTER. Charity Accounting and Tax update We go under the skin of SORP FRS 102 and recap on various tax topics

Charity Accounting and Tax update We go under the skin of SORP FRS 102 and recap on various tax topics Tuesday 3 March 2015, Leeds or Thursday 12 March 2015, Manchester BEST GOOD BETTER A free workshop

Charity Accounting and Tax update We go under the skin of SORP FRS 102 and recap on various tax topics Tuesday 3 March 2015, Leeds or Thursday 12 March 2015, Manchester BEST GOOD BETTER A free workshop

Building bridges for growth. Viewpoint from Davos David Sproul, Senior Partner and Chief Executive

Building bridges for growth Viewpoint from Davos David Sproul, Senior Partner and Chief Executive Building bridges for growth Trust, or the lack of it, between business, government and the public is now

Building bridges for growth Viewpoint from Davos David Sproul, Senior Partner and Chief Executive Building bridges for growth Trust, or the lack of it, between business, government and the public is now

Higher Education Finance Directors Survey The Prudence Paradox. Thinking people.

Higher Education Finance Directors Survey The Prudence Paradox Thinking people. Contents Foreword 1 Key messages 2 Section 1: Financial prospects 3 Section 2: Balance sheet considerations 4 Section 3:

Higher Education Finance Directors Survey The Prudence Paradox Thinking people. Contents Foreword 1 Key messages 2 Section 1: Financial prospects 3 Section 2: Balance sheet considerations 4 Section 3:

Integrating Climate Change-related Factors in Institutional Investment

ROUND TABLE ON SUSTAINABLE DEVELOPMENT Integrating Climate Change-related Factors in Institutional Investment Summary of the 36 th Round Table on Sustainable Development 1 8-9 February 2018, Château de

ROUND TABLE ON SUSTAINABLE DEVELOPMENT Integrating Climate Change-related Factors in Institutional Investment Summary of the 36 th Round Table on Sustainable Development 1 8-9 February 2018, Château de

APPG Challenges the gig economy poses to the tax system

APPG Challenges the gig economy poses to the tax system Mark Groom 20 November 2017 Agenda Key challenges What is the gig economy? Employment law Income tax and NI Defining the population Objectives? Compliance;

APPG Challenges the gig economy poses to the tax system Mark Groom 20 November 2017 Agenda Key challenges What is the gig economy? Employment law Income tax and NI Defining the population Objectives? Compliance;

Integrated Risk Management Delivering improved outcomes

Integrated Management Delivering improved outcomes Funding Investment Covenant Governance Legal The issue The Pensions Regulator's (TPR) guidance on Integrated Management (IRM) is relevant for all pension

Integrated Management Delivering improved outcomes Funding Investment Covenant Governance Legal The issue The Pensions Regulator's (TPR) guidance on Integrated Management (IRM) is relevant for all pension

Defined Benefit Pension Schemes Deloitte Funding Tracker Q How does your scheme compare?

Defined Benefit Pension Schemes Deloitte Funding Tracker The Deloitte Scheme Funding Deficit Tracker shows how the deficit of three illustrative schemes with Return Seeking, Lower Risk and Hedging investment

Defined Benefit Pension Schemes Deloitte Funding Tracker The Deloitte Scheme Funding Deficit Tracker shows how the deficit of three illustrative schemes with Return Seeking, Lower Risk and Hedging investment

Brentwood Borough Council

Brentwood Borough Council Year ending 31 March 2017 Audit Plan 03 March 2017 Ernst & Young LLP Ernst & Young LLP 400 Capability Green Luton Bedfordshire LU1 3LU Tel: 01582 643000 Fax: 01582 643001 www.ey.com/uk

Brentwood Borough Council Year ending 31 March 2017 Audit Plan 03 March 2017 Ernst & Young LLP Ernst & Young LLP 400 Capability Green Luton Bedfordshire LU1 3LU Tel: 01582 643000 Fax: 01582 643001 www.ey.com/uk

Payments Disrupted Open forum discussion. Amsterdam, 23 rd September 2015

Payments Disrupted Open forum discussion Amsterdam, 23 rd September 2015 Agenda Open forum discussion 15:15 Welcome bytimo Span 15:25 Presentation Payments Disrupted report by Ian Foottit, partner Deloitte

Payments Disrupted Open forum discussion Amsterdam, 23 rd September 2015 Agenda Open forum discussion 15:15 Welcome bytimo Span 15:25 Presentation Payments Disrupted report by Ian Foottit, partner Deloitte

M&AIndexQ Growth is back on the corporate agenda. The Deloitte. Contacts. Key points

The Deloitte M&AIndex 214 Growth is back on the corporate agenda Contacts Key points Deloitte forecasts a strong resurgence in deal volumes for 214, bolstered by strong economic figures from the US and

The Deloitte M&AIndex 214 Growth is back on the corporate agenda Contacts Key points Deloitte forecasts a strong resurgence in deal volumes for 214, bolstered by strong economic figures from the US and

Request for Information Post-implementation Review IFRS 3 Business Combinations

Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London United Kingdom EC4M 6XH Deloitte Touche Tohmatsu Limited 2 New Street Square London EC4A 3BZ United Kingdom Tel:

Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London United Kingdom EC4M 6XH Deloitte Touche Tohmatsu Limited 2 New Street Square London EC4A 3BZ United Kingdom Tel:

Accounting by Limited Liability Partnerships Statement of Recommended Practice Exposure Draft (draft LLP SORP)

") Deloitte LLP 2 New Street Square London EC4A 3BZ Tel: +44 (0) 02 7007 0884 www.deloitte.co.uk vepoole@deloitte.co.uk Sharon Grant CCAB Moorgate Place London EC2P 2BJ 17 January 2014 Dear Sharon Accounting

Deloitte LLP 2 New Street Square London EC4A 3BZ Tel: +44 (0) 02 7007 0884 www.deloitte.co.uk vepoole@deloitte.co.uk Sharon Grant CCAB Moorgate Place London EC2P 2BJ 17 January 2014 Dear Sharon Accounting

The Deloitte CFO Survey. Post-election dip in confidence Q Authors. Key contacts

Q2 The Deloitte CFO Survey Post-election dip in confidence In the wake of the General Election on 8th June, optimism among Chief Financial Officers has fallen back from the 18-month high seen in the first

Q2 The Deloitte CFO Survey Post-election dip in confidence In the wake of the General Election on 8th June, optimism among Chief Financial Officers has fallen back from the 18-month high seen in the first

RED EXPAT. Moving employees from Spain to the United Kingdom. Pablo Álvarez y María Teresa López 20 th September 2016

RED EXPAT Moving employees from Spain to the United Kingdom Pablo Álvarez y María Teresa López 20 th September 2016 Agenda Introduction UK / Spanish Tax Systems The Example Assignment to the UK Local transfer

RED EXPAT Moving employees from Spain to the United Kingdom Pablo Álvarez y María Teresa López 20 th September 2016 Agenda Introduction UK / Spanish Tax Systems The Example Assignment to the UK Local transfer

FATCA and CRS compliance Understanding the requirements

FATCA and CRS compliance Understanding the requirements Foreign Account Tax Compliance Act (FATCA) FATCA is a U.S. legislation which aims to combat tax evasion by U.S. persons. The intent behind the law

FATCA and CRS compliance Understanding the requirements Foreign Account Tax Compliance Act (FATCA) FATCA is a U.S. legislation which aims to combat tax evasion by U.S. persons. The intent behind the law

Studies carried out in 2015

Shutterstock Studies carried out in 2015 COMPENDIUM European Economic and Social Committee Studies carried out in 2015 COMPENDIUM Table of Contents The potential effects on consumers of the real lifetime

Shutterstock Studies carried out in 2015 COMPENDIUM European Economic and Social Committee Studies carried out in 2015 COMPENDIUM Table of Contents The potential effects on consumers of the real lifetime

Enhanced disclosures: Leading practices and current trends

Enhanced disclosures: Leading practices and current trends The Dbriefs Governance, Risk & Compliance series Deb DeHaas, Vice chairman, National Managing Partner, Deloitte Consuelo Hitchcock, Management

Enhanced disclosures: Leading practices and current trends The Dbriefs Governance, Risk & Compliance series Deb DeHaas, Vice chairman, National Managing Partner, Deloitte Consuelo Hitchcock, Management

The Kuala Lumpur Statement on Financing Sources for Public-Private Partnerships in South-East Asia

Sub-Regional Expert Group Meeting (EGM) for South-East Asian Countries Financing Sources for Public-Private Partnerships (PPPs) The Kuala Lumpur Statement on Financing Sources for Public-Private Partnerships

Sub-Regional Expert Group Meeting (EGM) for South-East Asian Countries Financing Sources for Public-Private Partnerships (PPPs) The Kuala Lumpur Statement on Financing Sources for Public-Private Partnerships

New transparency requirements for the Swiss insurance market. 30 September 2015

New transparency requirements for the Swiss insurance market 30 September 2015 1 Challenges and opportunities of the FINMA Circular 2016/xx disclosure insurers (Public Disclosure) This publication is part

New transparency requirements for the Swiss insurance market 30 September 2015 1 Challenges and opportunities of the FINMA Circular 2016/xx disclosure insurers (Public Disclosure) This publication is part

CFTC and EU OTC Derivatives Regulation An Outcomes-based Comparison

CFTC and EU OTC Derivatives Regulation An Outcomes-based Comparison July 2013 Contents Executive summary 2 1 Introduction 3 2 EU US derivatives regulatory landscape 5 3 Comparison of EU and CFTC regulatory

CFTC and EU OTC Derivatives Regulation An Outcomes-based Comparison July 2013 Contents Executive summary 2 1 Introduction 3 2 EU US derivatives regulatory landscape 5 3 Comparison of EU and CFTC regulatory

CFOs have also brought forward their estimates for the timing of interest rate rises, with 96% expecting rates to be higher in a year s time.

2018 The Deloitte CFO Survey Transition deal boosts sentiment The first quarter survey of Chief Financial Officers shows slightly firmer business confidence and an easing of Brexit concerns. The announcement

2018 The Deloitte CFO Survey Transition deal boosts sentiment The first quarter survey of Chief Financial Officers shows slightly firmer business confidence and an easing of Brexit concerns. The announcement