Affordable Care Act Update. Agenda. Maximum Out of Pocket Costs for /1/2015. July 1, 2015

|

|

|

- Leon Fields

- 5 years ago

- Views:

Transcription

1 Affordable Care Act Update July 1, 2015 Agenda ACA Individual Mandate What is needed for the Application Process What is Minimum Essential Coverage Changes that occur in the tax year Form 1095 A for 2015 Affordable Care Act Exemptions Affordable Care Act Affordability The Premium Tax Credit Navigating the Forms Maximum Out of Pocket Costs for 2015 Maximum out of pocket costs for any Marketplace plan for 2015 are $6,600 for an individual plan and $13,200 for a family plan. This means when the amount you ve paid in deductibles, copayments, and coinsurance reaches these limits, the insurance company pays 100% of your costs for covered care. Even if you choose a catastrophic coverage plan your out of pocket costs shouldn t exceed this limit. 1

2 ACA Individual Mandate What is needed for the Application Process What is Minimum Essential Coverage Changes that occur in the tax year Form 1095 A for 2015 HHS & Role of the Health Insurance Marketplace HHS: Administers the Marketplace Marketplace Health Insurance Options Bronze and Silver Plan Amounts Assists in determining affordability Healthcare.gov has more information 2

3 IRS Role Reconcile the Premium Tax Credit Issue reporting forms to health insurance providers to comply with the law drafts are available Announce the poverty level amounts used to determine affordability determined by HHS Calculate Individual Responsibility Payment (penalty) What Does ACA Require of Your Client? The Affordable Care Act requires your client and each member of their family to have qualifying health care coverage (known as minimum essential coverage) or Qualify for an exemption from the responsibility to have minimum essential coverage, or Make an individual shared responsibility payment when they file their federal income tax return Documentation IRS Has Changed It s Tune!!! Taxpayers do not need to attach documentation or proof of insurance coverage to the tax return Nothing in the IRS rules or regulations require your client to provide proof of coverage at the time they file CALT recommends that if your clients have documents that verify their coverage they should provide them to you The IRS will follow its normal compliance approach to filed tax returns, and may ask your client to substantiate the information on their tax return, therefore if documents are provided to you, you should keep these documents with thier tax records 3

4 Documentation Individuals can Gather in Advance Per IRS recommendations Proof of Insurance Taxpayers are not required to send in proof of health care coverage to the IRS when filing their tax return However, it s a good idea to keep these records on hand to verify coverage This documentation includes: Insurance cards Explanation of benefits statements from your insurer W 2 or payroll statements reflecting health insurance deductions Records of advance payments of the premium tax credit Other statements indicating that you, or a member of your family, had health care coverage Documentation Individuals can Gather in Advance Documents supporting exemptions and hardships Anyone who qualifies for a health coverage exemption will need to apply through the Marketplace or claim the exemption on his or her tax return Individuals may need information to support their coverage exemption claim This includes documentation to support : A hardship Income documents Social Security information Household information If an exemption application is granted by the Marketplace the applicant will receive a notice with a unique Exemption Certificate Number, also known as an ECN Documentation Individuals can Gather in Advance 1095 A, Health Insurance Marketplace Statement If your client had coverage through a Marketplace the Marketplace will send them information about the coverage on Form 1095 A The form will show details of an individual s insurance coverage such as The effective date The amount of the premium The advance payments of the premium tax credit or subsidy Individuals/Practitioner will use the information on Form 1095 A to complete Form 8962, Premium Tax Credit (PTC) in order to claim the premium tax credit or to reconcile advance credit payments on the federal tax return Individuals may receive more than one Form 1095 A if anyone in their households Switched plans in 2015 Reported life changes after their coverage began Or if they had more than one policy covering people in the same household Individuals will get a Form 1095 A even if they only had Marketplace coverage for part of

5 Minimum Essential Coverage Group health insurance coverage for employees under A governmental plan, such as the Federal Employees Health Benefit program A plan or coverage offered in the small or large group market within a state A grandfathered health plan offered in a group market A self insured group health plan for employees COBRA coverage Retiree coverage Certain foreign coverage Certain coverage for business owners Minimum Essential Coverage If you re under 26, coverage under a parent s plan Self funded health coverage offered to students by universities for plan or policy years that started on or before Dec. 31, 2014 (check with your university to see if the plan counts as minimum essential coverage) Health coverage for Peace Corps volunteers Certain types of veterans health coverage through the Department of Veterans Affairs Most TRICARE plans Department of Defense Non appropriated Fund Health Benefits Program Minimum Essential Coverage State high risk pools for plan or policy years that started on or before December 31, 2014 Health insurance you purchase directly from an insurance company Health insurance you purchase through the Health Insurance Marketplace Catastrophic plans Medicare Part A coverage Medicare Advantage plans Most Medicaid coverage Children s Health Insurance Program (CHIP) Health coverage provided to Peace Corps volunteers Refugee Medical Assistance 5

6 Minimum Essential Coverage Does Not Include Coverage consisting solely of excepted benefits, such as: Stand alone vision care or dental care Workers' compensation Accident or disability policies Medicaid providing only family planning services Medicaid providing only tuberculosis related services Medicaid providing only coverage limited to treatment of emergency medical conditions Pregnancy related Medicaid coverage Minimum Essential Coverage Does Not Include Medicaid coverage for the medically needy Section 1115 Medicaid demonstration projects AmeriCorps coverage for those serving in programs receiving AmeriCorps State and National grants AfterCorps coverage purchased by returning members of the PeaceCorps Minimum Essential Coverage Does Not Include Special Circumstances Space available TRICARE coverage provided under chapter 55 of title 10 of the United States Code for individuals who are not eligible for TRICARE coverage for health care services from private sector providers Line of duty TRICARE coverage provided under chapter 55 of title 10 of the United States Code In Notice , the IRS announced relief from the individual shared responsibility payment for months in 2014 in which individuals are covered under one of these programs See the instructions for Form 8965, Health Coverage Exemptions, for information on how to claim an exemption for one of these programs on your income tax return. 6

7 Applying to the MarketPlace Issues Clients need to estimate Income for 2015 Client do not understand what MAGI is and what additions need to be added into AGI to reach MAGI More than likely the estimated income will result in balance dues due to lack of understanding This causes payback of subsidies Changes in the year have a great impact Clients do not understand the changes will effect the subsidy Clients are not reporting changes Changes within the Year Taxpayer must report a change if they: Get married or divorced Have a child, adopt a child, or place a child for adoption Have a change in income Get health coverage through a job or a program like Medicare or Medicaid Change the place of residence Have a change in disability status Gain or lose a dependent Become pregnant Experience other changes that may affect your income and household size Other changes to report: change in tax filing status; change of citizenship or immigration status; incarceration or release from incarceration; change in status as an American Indian/Alaska Native or tribal status; correction to name, date of birth, or Social Security number. How to Report Changes? Your client should report these changes to the Marketplace as soon as possible If the changes qualify your client for more or less savings, it s important to make adjustments as soon as possible. Important: Do not report these changes by mail. You can report these changes 2 ways: Online The client needs to log into their account Select their application, then select Report a life change from the menu on the left. By phone. Contact the Marketplace Call Center at (TTY: ) 7

8 After your Client reports a change After your client report changes to the Marketplace, they will get a new eligibility notice that will explain: Whether they qualify for a special enrollment period that allows them to change plans Whether they are eligible for lower costs based on the new income, household size, or other changed information They may become eligible for the first time, for a different amount of savings, or for coverage through Medicaid or the Children s Health Insurance Program (CHIP IRS Forms Form 1095 A Issues by the insurance company whom the client chose when applying through the Marketplace Possible Premium Tax Credit Issue Shows coverage by month Premiums Any advance Premium tax Credit Received by January 31, Form 1095 A 8

9 2015 Form 1095 A Summary How to Help Your Client? Estimate 2015 Income Review issues of dependents and filing status Explain the importance of family and income changes during the year Inform them as to what forms and documentation they may need to bring to you next year Exemptions and Affordability 9

10 ACA Purpose Provide Affordable Health Coverage to Americans But, if the coverage meets certain criteria individuals can be considered EXEMPT from coverage and EXEMPT from the penalties What is an Exemption? An exemption from complying with ACA is available for certain conditions What qualifies for an exemption? How is the exemption obtained through the Marketplace? When should your client apply? Other exemptions, how are they determined and how will your client be able to get the exemption What Exemptions Qualify? You re client is uninsured for less than 3 months of the year The lowest priced coverage available to your client would cost more than 8.05% in 2015 of their household income THE AFFORDIBILITY FACTOR (2014 the percentage was 8%) There is no filing requirement because their income is too low You client is a member of a federally recognized tribe or eligible for services through an Indian Health Services provider Your client is a member of a recognized health care sharing ministry Your client is a member of a recognized religious sect with religious objections to insurance, including Social Security and Medicare Your client is incarcerated (either detained or jailed), and not being held pending disposition of charges Your client is not lawfully present in the U.S. 10

11 Hardship Exemptions Your client meets one of the following conditions: Homeless Eviction in the past 6 months or were facing eviction or foreclosure. A shut off notice from a utility company Recently experienced domestic violence Experienced the death of a close family member (undefined) Experienced a fire, flood, or other natural or human caused disaster that caused substantial damage to your property Filed for bankruptcy in the last 6 months. Had medical expenses the client couldn t pay in the last 24 months which resulted in substantial debt Hardship Exemptions Your client experienced unexpected increases in necessary expenses due to caring for an ill, disabled, or aging family member Your client expect to claim a child as a tax dependent who s been denied coverage in Medicaid and CHIP, and another person is required by court order to give medical support to the child In this case, you do not have the pay the penalty for the child As a result of an eligibility appeals decision, your client is eligible for enrollment in a qualified health plan (QHP) through the Marketplace, lower costs on their monthly premiums, or cost sharing reductions for a time period when they weren t enrolled in a QHP through the Marketplace Your client was determined ineligible for Medicaid because your state didn t expand eligibility for Medicaid under the Affordable Care Act Your client s individual insurance policy was cancelled and they believe other Marketplace plans are unaffordable The client experienced another hardship in obtaining health insurance How to apply for an exemption If you're applying for an exemption based on Coverage being unaffordable Membership in a health care sharing ministry Membership in a federally recognized tribe Incarcerated: You have 2 options: You can claim these exemptions when you fill out your 2015 federal tax return, which is due in April 2016 or file for an exemption through the Marketplace 11

12 Exemptions Exemptions There is an Appeal Process If your client doesn t agree with the results of the application, the client can request an appeal The Appeal The Health Insurance Marketplace must receive the appeal request within 90 days of the date of the notice of the application results The client can have someone request or participate in your appeal That person can be a friend, relative, lawyer, or other individual The outcome of an appeal could change the eligibility of other members of your household To appeal the results of the exemption application, there is a phone number your client can call They can also mail an appeal request form or their own letter requesting an appeal to Health Insurance Marketplace Exemption Processing, 465 Industrial Blvd., London, KY Sign this application. 12

13 What happens after I apply for an exemption? After the application is submitted, The Marketplace will review and determine the eligibility The time it takes to receive a response will depend on how complicated the request is, how complete your application is, and whether the client needs to submit additional supporting documentation after they apply The Marketplace will mail the client a notice of the exemption eligibility result If your client is granted an exemption, the Marketplace notice will show their unique exemption certificate number (ECN) As the tax preparer you will use the ECN when you complete their taxes for the 2015 tax year beginning in January 2016 to avoid paying the shared responsibility payment. How long will a hardship exemption last? Hardship exemptions are usually provided for the month before the hardship, the months of the hardship, and the month after the hardship. However, the Marketplace may provide the exemption for additional months after the hardship, including up to a full calendar year. For a hardship exemption based on affordability, the exemption will be granted for the remaining months in the coverage year. For individuals ineligible for Medicaid solely based on a state s decision not to expand coverage, the hardship exemption will be granted for the entire calendar year. For individuals eligible for Indian Health Services, the hardship exemption will be granted on a continuing basis It may be kept for future years without having to submit another application as long as there are no changes to the membership in a tribe or eligibility for services from an Indian health care provider Form 8965 Form 8965 is the Exemption Certificate that must be attached to the tax return No 2015 Draft of form is available Part 1 Marketplace granted exemption Part 2 Exemption for the household Part 3 Exemption for individuals 13

Income $35,000 X 8.")

14 Form 8965 Form 8965 Determination of Affordability Household Income for the most recent year for which income is available Determines whether coverage is affordable Magic 8.05% calculation (Maximum Contribution) Income $35,000 X 8.05% = $2,818 Revenue Procedure

15 Household Income for Purpose of Affordability of Minimum Essential Coverage 8.05%Caculation for 2015 Modified Adjusted Gross Income PLUS The aggregate MAGI of all other individuals taken into account to determine the family s size BUT Only if those individuals are required to file a tax return Does not include a return to claim a full refund of tax withhold or report a tax other than income tax (i.e.: IRA early distribution penalty or Self employment income) Must increase Household Income by: Tax Exempt Foreign Income Tax exempt Social Security benefits/railroad retirement benefits Tax Exempt interest Chart to Assist 8.05% for 2015 Required Contribution Percentage Determined on an annual basis For Minimum Essential Coverage (MEC) Deemed Affordable Coverage Example: Household Income $35,000 $35,000 wages $35,000 X 8.05% = $2818 $2,818 is the required contribution 15

16 Example: Rebecca A65 Income $35,000 Persons in Household 1= $11,670 Poverty Guideline Amount Premiums possible Bronze $4700 Silver $5000 (Benchmark Plan) Step One Review the 2014 Poverty Guidelines Alaska and Hawaii 16

17 Calculate the Federal Poverty Guideline Income $35,000/$11,670 = 2.99 = 9.47% Table 2 of the Form 8962 Instructions will be updated for 2015, a draft is not available in our example we are using the 2014 version Form 8962 Premium Tax Credit Table 2 Applicable Figure Step Two Calculate the Premium Assistance Credit Use Benchmark Premium (second lowest cost for selfonly silver plan $5,000) $5,000 ($35,000 X 9.47%) = $3,315 $5,000 $3,315 = $1,685 (PAC) Bronze Plan $4,700 $1,685 =$3015 (required taxpayer contribution) $1685 can be paid in advance by the exchange to the insurance company or taken as a credit at year end, if Rebecca enrolls in plan 17

18 Step Three Does Rebecca have affordable coverage? Rebecca s Contribution $3,015 Rebecca s Magic 8.05% +$2,818 No, Rebecca does not have affordable coverage and is exempt from the individual mandate, no penalty Example Unmarried employee with No Dependents Taxpayer A is an unmarried individual with no dependents In November 2014, A is eligible to enroll in self only coverage under a plan offered by A s employer for calendar year 2015 If A enrolls in the coverage, A is required to pay $5,000 of the total annual premium In 2015, A s household income is $60,000 A's required contribution is $5,000, the portion of the annual premium A pays for self only coverage A has affordable coverage for 2015 because A s required contribution ($5,000) is less than 8.05 percent of A s household income ($5,100). Example: Married employee with dependents Taxpayers B and C are married and file a joint return for B and C have two children, D and E. In November 2014, B is eligible to enroll in self only coverage under a plan offered by B s employer for calendar year 2015 at a cost of $5,000 to B. C, D, and E are eligible to enroll in family coverage under the same plan for 2015 at a cost of $20,000 to B B, C, D, and E s household income is $90,000 B's required contribution is B's share of the cost for self only coverage, $5,000 B has affordable coverage for 2015 because B s required contribution ($5,000) does not exceed 8.05 percent of B s household income ($7,650) The required contribution for C, D, and E is B's share of the cost for family coverage, $20,000 C, D, and E lack affordable coverage for 2016 because their required contribution ($20,000) exceeds 8.05 percent of their household income ($7,650). 18

19 The Premium Tax Credit Topics Premium Tax Credit Basics Determining the amount of the Premium Tax Credit Factors that effect the credit Impact of changes during the year How to get the Premium Tax Credit What is the Premium Tax Credit? Refundable tax credit Helps eligible individuals and families pay for health insurance Administered through the tax system and the Marketplaces Available starting January 1, 2014 Two Payment Options Get it Now advance credit payments Get it Later without advance credit payment 19

20 Family Size Number of individuals the taxpayer is allowed a deduction under 151 for the taxable year Household Income Modified Adjusted Gross Income of the taxpayer, PLUS The MAGI of all individuals who were taken into account in determining the family size AND Were required to file a tax return for the taxable year Household may or may not be the same as who is in the insurance plan Lawfully Present An individual shall be treated as lawfully present only if The individual it is reasonable expected to be a citizen or national of the United States or an alien lawfully present in the United States 20

21 Families including Individuals not Lawfully Present The family size is determined by not taking those individuals into account AND The household income is determined without regard to those individuals Benchmark Plan Second lowest cost silver plan available to each eligible household member When no one plan covers every member it may be based on one or more policies Plans available Bronze 60% Silver 70% Gold 80% Platinum 90% Catastrophic Eligibility for PTC To be eligible the individual must: Be an applicable taxpayer: Income between 100 and 400% Federal Poverty Level (for the family size) with some exceptions Must be US citizens or lawfully present in the US Must not be eligible for other minimal essential coverage Lawfully residing immigrants with incomes below 100% FPL who are not eligible for Medicaid because of their immigration status Cannot be claimed as a dependent AND If married, files a joint return (with some exceptions) Have a Coverage Month Enrolled in a qualified health plan through the Marketplace Not eligible for other minimal essential coverage AND Premiums are paid 21

22 How is the Amount of Credit Determined? The Credit Amount is Affected By: Individual or family s expected contribution based on their income Premium cost for benchmark plan Income Limits Based on 2014 Federal Poverty Level One individual $11,670 (100% FPL) $46,680 (400% of FPL) Family of Two $15,730 (100% of FPL) $62,920 (400% of FPL) Family of Four $23,850 (100% of FPL) $95,400 (400% of FPL) Example: Based on the 2014 FPL, a family of four could have a household income up to and including $95,400 and still be eligible for the PTC 22

23 2014 FPL for Most States Alaska and Hawaii Income $23,340, age 24 Plan Cost $5,000 Expected Contribution? Example A : John $23,340/$11,670 = 2.00% $23,340 X 6.3% = $1470 John s Contribution Plan Cost $5,000 $1470 = $3530 Premium Tax Credit 23

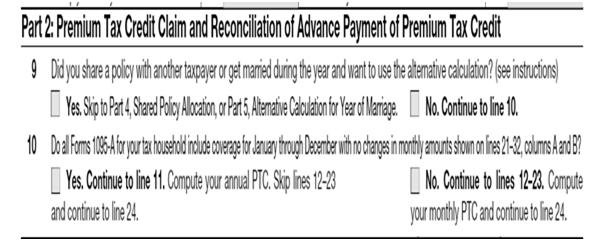

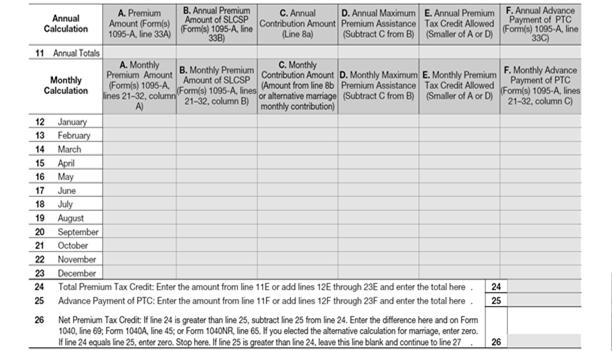

24 Income $35,010, age 24 Plan Cost $5,000 Expected Contribution? Example B: John $35,010/$11,670 = 3.00% $35,010 X 9.5% = $3,325 John s Contribution Plan Cost $5,000 $3,325 = $1,,675 Premium Tax Credit Form 1095 A Issued by the Health Insurance Marketplace Sent by January 31 of each year Shows: Documentation of coverage by month Premiums AND Advanced Payments of the Premium Tax Credit Form 8962 Part 1 Annual and Monthly Contribution Part 2 PTC Claim and Reconciliation Part 3 Repayments of Excess of Advanced Payment Part 4 Shared Policy Allocations Part 5 Alternative Calculation for Marriage 24

25 How Does the Reconciliation Work? Advance payments $4,000 Calculation of the PTC $3,000 Difference $1,000 Repayment Amount $1,000* *Amount from the Form 8962 that will be entered on Form 1040 A tax return must be filed to reconcile advance credit payments regardless of other filing requirements 36B This calculation will be indexed for inflation 1412 of the Patient Protection Act and the Affordable Care Act provides for the tax to be increased by any excess advanced payment 36B(f)(2)(B) places a limit on the increase What are Repayment Caps? Regulation 1.36B 4(a)(3) 25

26 Repayment Cap Situation Client applies for coverage and is approved for a premium tax credit. Single Client decides to receive the entire premium tax credit in advance Estimated Income $29,175 (250% FPL) Eligible Premium Tax Credit = $2818 ($235/month) What are Repayment Caps? Regulation 1.36B 4(a)(3) Repayment Cap Situation Part 2 Actual Return Income $44,811 (3.84% FPL) Eligible Premium Tax Credit $943 ($79/mo) Actual Credit $ 943 Amount Received in Advance $2,818 Excess Advanced Payment $1,875 Because the annual household income is 300% 400% FPL, her repayment amount is capped at $1,250 26

(3) No Cap on Repayment Obligations for Individuals with income of more than 400% FPL If the client received a APTC based on an estimate that annual income would be less than 400% All APTC if")

27 What are Repayment Caps? Regulation 1.36B 4(a)(3) No Cap on Repayment Obligations for Individuals with income of more than 400% FPL If the client received a APTC based on an estimate that annual income would be less than 400% All APTC if income is more than 400% FPL must be paid back There is no cap on the repayment obligation if the ACTUAL income is above 400$ FPL Annual Household Income below 100% FPL Generally, if client s income is less than 100% FPL, they are not eligible for the premium tax credit If income anticipated allows a client to qualify for the premium tax credit (estimated income above the 100% FPL) and they received the advance premium tax credit but at year end If ACTUAL income less than 100% FPL the client is not required to repay the advanced premium tax credit 27

28 Special Rules for Newly Married or Newly Divorced Couples When taxpayer marry the household income often become higher due to multiple sources of income When taxpayer divorce the opposite is true The law allows an alternate calculation in this scenario Newly Married Credit for the single months is computed separately for each spouse as if each taxpayer s annual income was 50% of the actual household income for the year The credit for the married months is computed using the actual household income for the year The Premium Tax Credit is the sum of the single and married months Newly Married One More Step The total is capped by the amount of additional credit that result from computing the credit under the general rule 28

29 Newly Divorced Allocate the premium for the applicable period they were married on the: Benchmark plan Premium for the plan they enroll in Advance Premium Tax Credit payments If the couple cannot agree the items will be allocated 50% to each taxpayer The final regulations do allow the allocation between the couple in proportion to household income if they choose Information would have to be shared for this to be accomplished doubtful in most divorces Married Filing Separately No premium Tax credit is allowed If advance payments are received and a MFJ return is not filed the advance must be repaid Exceptions allowed Notice For calendar year 2015, a married taxpayer will satisfy the joint filing requirement of 36B(c)(1)(C) if the taxpayer files a 2015 tax return using a filing status of married filing separately and the taxpayer (i) is living apart from the individual s spouse at the time the taxpayer files his or her tax return, (ii) is unable to file a joint return because the taxpayer is a victim of domestic abuse, and (iii) indicates on his or her 2015 income tax return in accordance with the relevant instructions that the taxpayer meets the criteria under (i) and (ii). Review of Who Must Allocate Taxpayers who must allocate policy amounts because of a divorce or legal separation in 2015 and also must allocate policy amounts with another taxpayer (for example, a grandparent who claims the personal exemption amount for a child enrolled with the former spouses) Taxpayers who must allocate policy amounts because they are legally married but are not filing a joint return (for example, filing their returns as married filing separately), and also must allocate policy amounts with another taxpayer (for example, a grandparent who claims the personal exemption amount for a child enrolled with the spouses) Three or more taxpayers who are claiming personal exemptions for individuals enrolled together in a qualified health plan 29

30 Kara and David Kara and David and their two children, Meredith and Sam, enroll in a qualified health plan for 2015 Kara and David were married at the beginning of 2015 and divorce in 2015 Meredith and Sam move in with their grandmother, Lydia, in May of 2015 Lydia claims Meredith and Sam as dependents on her 2014 income tax return Kara, David, and Lydia must allocate policy amounts to compute their respective PTC and reconcile PTC with the APTC paid Kara and David Kara and David use the allocation method under Taxpayers Allocating Due to a 2015 Divorce or Legal Separation and Also Allocating With Another Taxpayer Lydia uses the allocation method under Taxpayer Allocating With Taxpayers Who Divorced or Legally Separated in 2015 Kara and David Taxpayers Allocating Due to a 2015 Divorce or Legal Separation and Also Allocating With Another Taxpayer Step 1. Determine an allocation percentage with the former spouse Use this percentage to allocate the total enrollment premiums, the applicable SLCSP premiums, and APTC for coverage under the plan during the months the client was married You will find these amounts on your Form(s) 1095 A, Part III, columns A, B, and C, respectively The couple can allocate these amounts using any percentage they agree on between zero and one hundred percent, but they must allocate all amounts using the same percentage If they cannot agree on a percentage, the couple must allocate 50% of each of these amounts 30

31 Agreed Percentage Part 1 Kara 30% David 70% Agreed Amount for Dependents Lydia Kara agrees on 80% David agrees on 50% Kara Step 1 31

32 Kara and David Step 2. Separately from the first allocation, determine an allocation percentage with the taxpayer(s) claiming the personal exemption(s) for the individual(s) enrolled in the plan with a member of the tax family or a member of the former spouse s tax family They may agree on any allocation percentage between zero and one hundred percent They may use the percentage they agreed on for every month that this allocation rule applies, or you may agree on different percentages for different months However, they must use the same allocation percentage for all policy amounts (enrollment premiums, applicable SLCSP premiums, and APTC) in a month Kara and David If they cannot agree on an allocation percentage, the allocation percentage is equal to the number of individuals for whom the other taxpayer claims a personal exemption for the tax year who were enrolled in the plan for which they are allocating policy amounts, divided by the total number of individuals enrolled in the qualified health plan The allocation percentage is the percentage that applies to the amounts the taxpayer claiming the personal exemption must use to compute PTC and reconcile it with APTC The clients must compute PTC and reconcile APTC using the remaining amounts. Kara and David Step 3 Look at Part 4 of Form 8962 If the client use the same percentage in Step 2 above for every month to which this allocation method applies, use only one of lines in Part 4 to report the allocation If you use different percentages for different months under Step 2, use a separate line in Part 4 for each allocation percentage 32

33 Kara and David Form 8962 Columns Column a. Enter the Marketplace assigned policy number from Form 1095 A, line 2. If the policy number on the Form 1095 A is more than 15 characters, enter only the last 15 characters Column b. Enter the SSN of your former spouse Column c. Enter the first month you are allocating policy amounts. For example, if you are allocating a percentage from January through June, enter 01 in column c Kara and David Column d. Enter the last month you are allocating pol icy amounts. For example, if you are allocating a percent age from January through June, enter 06 in column d Column e. Enter the decimal percentage agreed upon Column f. If APTC was paid, enter the decimal from Worksheet C, line 5. If no APTC was paid, enter the decimal from Worksheet C, line 1. Column g. If APTC was paid, enter the decimal from Worksheet C, line 5. If no APTC was paid, leave this column blank. Kara s Part 4 Shared Policy Allocation 33

34 Kara s Form 1095 A One of 2 What s Next After completing Part 4 Kara multiplies the amounts from Form 1095 A, Part III, by the corresponding percentages in Part 4 Entering these allocated amounts on Form 8962, lines 12 20, columns A, B, and F On each of those lines she will enter $42 in column A (enrollment premiums of $700 x 0.06) $39 in column B (applicable SLCSP premium of $650 x 0.06) $26 in column F (APTC of $425 x 0.06) Complete Form 8962 She completes her Form 8962, lines 21 23, columns A, B, and F, by entering the monthly amounts from her separate Form 1095 A for her self only coverage from October through December She does not allocate those amounts 34

35 Kara Allocated Form 8962 David s Worksheet Step 2 David s Form 8962 Part 4 35

36 Completing David sform 8962 Lydia Return Lydia s Form

37 Lydia Form 8962 Why Did We Use Kara s SSN on Lydia s Form 8962? Kara is the the individual who applied for the assistance Review to Worksheets Step1 Left/ Step 2 Middle/Step 3 Right Kara Calculation David s Calculation Lydia s Calculation 37

Total Premium for the coverage without regard to the credit The aggregated amount of the advanced payment Name, address and TIN of")

38 Summary Column F Kara s Advance $ 26 David s Advance $149 Lydia s Advance $251 The sum equal s the total years Advance within one dollar 36B What Information is Required to be Reported? Level of Coverage (bronze, silver, gold platinum or catastrophic) Total Premium for the coverage without regard to the credit The aggregated amount of the advanced payment Name, address and TIN of the primary insured and name and TIN of each other individual obtaining coverage under the policy Any information provided to the exchange including any change in circumstances necessary to determine eligibility Information to determine whether a taxpayer has received excess advanced payments Form 1095A 38

39 Form 1095 A ACA Penalties Individual Shared Responsibility Provision Individual Shared Responsibility Payment (ISRP) Starting in 2014 EVERYONE must either: Have Minimal Essential Coverage Or Have a Coverage Exemption Or Make a Shared Responsibility Payment 39

40 When Would an Individual Need to Make a Payment? A payment may be due for an individual and dependents if they do not have: MEC for every month of the year An exemption for the months without MEC This information is reported on the federal income tax return Individual Shared Responsibility Payment Lesser of: The sum of monthly penalty amounts for each individual in the shared responsibility family or The sum of the monthly average BRONZE plan premiums for the share responsibility family How is the Payment Computed? 40

41 Calculating Shared Responsibility Penalty The penalty is the greater of: a flat dollar amount; or a specific percentage of income. For 2014, the penalty amount will be the greater of $95 per adult and $47.50 per child under age 18 or 1% of income over the tax filing threshold (currently, $20,300 for a 2014 joint return) For 2015, the penalty amount will be the greater of $325 per adult and $ for a child under 18 or 2% of income over the tax filing threshold (currently, $20,600 for a 2015 joint return) Sample Calculation Single Facts Single individual, no dependents No minimum essential coverage for anymonth Does not qualify for an exemption Household income of $50,000/filing threshold = $10,300 Penalty Calculation: Percentage of Income $50,000 10,300 = $39,700 2% X $39,700 = $ Flat Dollar amount: $ ISRP = $ ($ is > $325.00) < then the monthly national average bronze level coverage ($ per month X 12 =$ ) National Average for Bronze Level Coverage Penalty amount is CAPPED at the cost of the national average premium for the bronze level plan available through the Marketplace in Monthly Nation Bronze Level Plan Premium for 2014 = $204 per individual 2015 = $ per individual Maximum Monthly National Average Bronze Plan Premium for a family of Five or more members = $1,020 for 2014 $1,035 for

42 Prorated for each Month without Coverage The 2015 shared responsibility penalties are payable when individuals file their 2015 federal income tax returns in 2016 If the penalty applies for less than a full calendar year, it is prorated to 1/12 of the annual penalty for each month without coverage Sample Calculation Family Facts: Married w/two children under 18 No minimum essential coverage for any month Does not qualify for an exemption Household income = $70,000/filing threshold = $20,600 Payment calculation Percentage of income: $70,000 20,600 = $49,400, 2% x $49,400 = $988 Flat dollar: $975 = (325 x 2) + ($325.00/2 x 2)) 2015 ISRP = $975 ($988 is > $975) < the national average for bronze level coverage $1035 X 12 =$12,420 What Information Documents Will be Issued in 2014? Form 1095 A Marketplace Purchase For 2015 tax year Received By January 31,

43 Form 1095 A Issued by the Health Insurance Marketplace Sent by January 31 of each year Shows: Documentation of coverage by month Premiums AND Advanced Payments of the Premium Tax Credit Form 8962 Applies Only to Form 1095 A Part 1 Annual and Monthly Contribution Part 2 PTC Claim and Reconciliation Part 3 Repayments of Excess of Advanced Payment Part 4 Shared Policy Allocations Part 5 Alternative Calculation for Marriage 2015 There is currently no delay in the reporting requirement for the following Forms: Form 1095 B Health Insurance Coverage Form 1095 C, Employer Provided Health Insurance Coverage 43

44 Form W 2 Box 12 of Form W 12 generally will be used in 2015 to report health insurance BUT Only reports a gross amount Does not report who was covered Does not report months covered Does not report when insurance was offered Does not provide adequate information to determine the penalties Information Required on Form 1095 B Name, address and EIN for the person required to file the return Name, address and TIN, or date of birth of the responsible individual Name and TIN or date of birth for each individual covered under the policy or program For each covered individual, the months for which the individual was enrolled in coverage and entitled to receive benefits In addition, name, address and EIN of the employer sponsored plan Whether the coverage is a qualified health plan enrolled through the Small Business Health Options Program (SHOP) and the SHOP s unique identifier Finally, any other information specified in the forms, instructions or published guidance Information Required on Form 1095 C The employer s name, address, EIN; Name and phone number of the employer s contact person; Identification of the calendar year for which the information is reported; Certification as to whether the employer offered to its full time employees (and their dependents) the opportunity to enroll in minimum essential coverage under its group health plan by calendar month; The months during the calendar year for which coverage under the plan was available; Each full time employee's share of the lowest cost monthly premium (self only) for coverage providing minimum value offered to that full time employee under the employer sponsored plan, by calendar month; The number of full time employees for each month during the calendar year; and The name, address, and taxpayer identification number of each full time employee during the calendar year and the months, if any, during which the employee was covered under the plan. 44

45 Highlights of the Final Regulations Here are some of the highlights of the final regulations: Form 1094 Transmittal and Form 1095 information returns will be used to report health care information and are subject to the 250 e file threshold requirements Reporting will be required for all individuals unless specifically excepted No reporting required for onsite medical clinics or Medicare Part B considered supplements to MEC Wellness or self insured employee provided retiree benefits considered supplemental to MEC Controlled groups are allowed flexibility in information reporting to allow combined reporting, rather than each entity reporting For Statutory Employees the plan sponsor is responsible for the reporting Highlights of the Final Regulations Insurance purchased through the Market Place, the exchange (Market Place) must report this information on Form 1095 A SHOP reporting, an area where small business can purchase an employer plan through the exchange the insurers are required to report, rather than the Market Place Government Employees reporting hinges on the undefined agency or instrumentality term. Until further guidance, use a reasonable cause standard to make that determination of whether to file The Medicare Advantage Program issuers are not considered MEC therefore they are not required to report this coverage Highlights of the Final Regulations Taxpayer Identification Number s (TIN s) must be provided for ALL individuals covered If the TIN is not available a date of birth is an alternate way to report but only after reasonable attempts to obtain the TIN (Due Diligence) This enables IRS to match and avoid notices to verify coverage or erroneous issue of penalties. The final regulations clarify that reporting entities are permitted to use Truncated TIN s on 6055 statements For Combined Reporting, coverage must be reported using the new 1095 information returns and transmittals rather than the Form W 2 45

46 Highlights of the Final Regulations Reporting is required for a deceased participant Forms 1095 can be provided at the same time as the Form W 2 and in the same envelope without restrictions. The required forms must be mailed to the last known address or the address the reporting entity uses for requesting information about coverage The IRS TIN matching program is not permitted to verify TIN s for the 6055 reporting When Does Your Client Pay the Penalty? Payment, if due, is reported and paid with the tax return IRS cannot place a lien or levy to collect the penalty but Can take the penalty due from refund of current year return or future returns Navigating the Affordable Care Act Forms 46

47 Forms, Worksheets and Charts Form 1095 A Form 1095 B Form 1095 C Form 8962 The Premium Tax Credit Form 8965 Health Coverage Exemptions Forms 1040, 1040A, 1040EZ Worksheets Penalties Affordability Exemptions Marketplace Application Shared Policy Allocation Alternative Calculation for Year of Marriage Eligibility Repayment Limitation Charts Poverty Line Charts Filing Requirement Form 1095 A The Marketplace Form 1095 A The Marketplace 47

48 Form 1095 A Moving Line 1 = state where client enrolled in coverage, if client moved, they must notify the Marketplace What happens if an individual moves from one state to another after signing up for a plan? The client is living in one area of California for the first few months of 2015, but then moves a different area of California. Will it be possible to transfer my plan to a different address partway through the year? It depends on the insurer. If your client has a plan that also is offered in the new locale, they keep that plan If they want to change the plan, they will have to wait until the next openenrollment period Form 1095 A Moving If they can't get the same plan in the new hometown, they will be eligible for a special enrollment period and can sign up for a new plan If they move to another state, they will need to enroll in a new plan through that state's exchange or buy on the open market If that state doesn't run its own exchange, they would use the federal exchange, healthcare.gov Moving to another state also triggers a special enrollment period, so they will be able to choose a new plan immediately Other Information Only the person who registered and filed for the coverage will receive a copy of Form 1095 A Was client eligible for Medicare in mid year or sometime in 2015? 48

49 Form 1095 A The Marketplace Form is issued by The Marketplace by January 31 SSN s are allowed to be truncated The Premium Tax Credit will be a factor A reconciliation or credit computation will be required on Form 8962 It is possible a cap calculation may apply in some situations A shared allocation issue may arise from newly divorced or newly married Calculated on Form 8962 and worksheets Form 1095 A The Marketplace You could have both a Form 1095 A and another 1095 a Form 1095 B or C in 2015 Example: Jack and Jill were married in Jack had employer coverage, and Judy purchased coverage before the marriage from the Marketplace. Example: Roger and Rita were married with 2 dependents. Roger has employer provided health coverage, but Rita purchased through the Marketplace for her and the children because the employer family plan was considered unaffordable B Health Coverage 49

The return and transmittal form must be filed with the IRS on or before February 28 (March 31 if filed electronically) of the year following the calendar year of coverage You will meet")

50 1095 B Health Coverage 1095 B Health Coverage Health insurance issuers will file Form 1095 B to report on coverage for employees of small employers obtained through the Small Business Health Options Program (SHOP) The return and transmittal form must be filed with the IRS on or before February 28 (March 31 if filed electronically) of the year following the calendar year of coverage You will meet the requirement to file if the form is properly addressed and mailed on or before the due date If the regular due date falls on a Saturday, Sunday, or legal holiday, file by the next business day Form 1095 B Every person that provides minimum essential coverage to an individual during a calendar year must file an information return and a transmittal Most filers will use Forms 1094 B (transmittal) and 1095 B (return) However, employers (including government employers) subject to the employer shared responsibility provisions sponsoring self insured group health plans will report information about the coverage in Part III of Form 1095 C, 50

51 1095 C Employer Provided Health Insurance Offer and Coverage 1095 C Employer Provided Health Insurance Offer and Coverage 1095 C Employer Provided Health Insurance Offer and Coverage An employer subject to the employer shared responsibility provisions under section 4980H must file one or more Forms 1094 C (including a Form 1094 C designated as the Authoritative Transmittal, whether or not filing multiple Forms 1094 C), and must file a Form 1095 C (or a substitute form) for each employee who was a full time employee of the employer for any month of the calendar year Generally, the employer is required to furnish a copy of the Form 1095 C to the employee 51

52 1095 C Employer Provided Health Insurance Offer and Coverage Each employer has its own reporting obligation related to the health coverage the employer offered (or did not offer) to each of its full time employees An employer subject to the employer shared responsibility provisions under section 4980H generally refers to an employer with 50 or more full time employees (including full time equivalent employees) during the prior calendar year An employer that offers health coverage through an employer sponsored selfinsured health plan must complete Form 1095 C, Parts I, II and III, for any employee who enrolls in the health coverage, whether or not the employee is a full time employee for any month of the calendar year If the employee who enrolled in self insured coverage is a full time employee for any month of the calendar year, the employer must also complete Part II If the employee who enrolled is not a full time employee, for any months of the calendar year (meaning that for all 12 calendar months the employee was not a full time employee), the employer must complete Form 1095 C, Part III and on Part II, must enter code 1G on line 14 in the All 12 Months column or in each separate monthly box (the employer need not complete Part II, lines 15 and 16 in this case) 1095 C Employer Provided Health Insurance Offer and Coverage If an employer is offering health coverage to employees in another manner, such as through an insured health plan or a multiemployer health plan, the issuer of the insurance or the sponsor of the plan providing the coverage is required to furnish the information about their health coverage to any enrolled employees, and the employer should not complete Form 1095 C, Part III, for those employees An employer that offers employer sponsored self insured health coverage but is not an applicable large employer subject to the employer shared responsibility provisions under section 4980H, should not file Forms 1094 C and 1095 C, but should instead file Forms 1094 B and 1095 B to report information for employees who enrolled in the employer sponsored self insured health coverage Medicare Issues 52

53 Time of eligibility Taxpayer E turns 65 on June 3, 2015, and becomes eligible for Medicare. Under section 5000A(f)(1)(A)(i), Medicare is minimum essential coverage. However, E must enroll in Medicare to receive benefits. E enrolls in Medicare in September, which is the last month of E s initial enrollment period. Thus, E may receive Medicare benefits on December 1, Because E completed the requirements necessary to receive Medicare benefits by the last day of the third full calendar month after the event that establishes E s eligibility (E turning 65), under paragraph (c)(2)(i) and (c)(2)(ii) of this section E is eligible for government sponsored minimum essential coverage on December 1, 2015, the first day of the first full month that E may receive benefits under the program. Determination of Medicaid ineligibility. In November 2014, Taxpayer G applies through the Exchange to enroll in health coverage for The Exchange determines that G is not eligible for Medicaid and estimates that G s household income will be 140 percent of the Federal poverty line for G s family size for purposes of determining advance credit payments. G enrolls in a qualified health plan and begins receiving advance credit payments. G experiences a reduction in household income during the year and his household income for 2015 is 130 percent of the Federal poverty line (within the Medicaid income threshold). However, under paragraph (c)(2)(v) of this section, G is treated as not eligible for Medicaid for Mid year Medicaid eligibility redetermination The facts are the same as in Example 5, except that G returns to the Exchange in July 2015 and the Exchange determines that G is eligible for Medicaid. Medicaid approves G for coverage and the Exchange discontinues G s advance credit payments effective August 1. Under paragraphs (c)(2)(iv) and (c)(2)(v) of this section, G is treated as not eligible for Medicaid for the months when G is covered by a qualified health plan. G is eligible for government sponsored minimum essential coverage for the months after G is approved for Medicaid and can receive benefits, August through December

54 Tax Family Individuals for whom the client can claim as a dependent or personal exemption Family size = the number of individuals in your tax family Coverage family includes all the individuals in the tax family who are enrolled in a qualified health plan and are not eligible for MEC elsewhere Child Born, Adopted or Placed in Foster Care Considered enrolled as of the first day of the month the child was born, adopted or placed in foster care The child is included in the coverage family for the month of birth, adoption or placement Other Issues Form 1095 A will provide details on months covered for each member of the household If no coverage for some months, is there available exemption that could apply? Is proration of the penalty an issue? If your client has received the Form 1095 A Form 8962 is required 54

55 Form 8962 Form 8962 Part 2 Form 8962 Part 2 55

56 Form 8962 Part 3 Form 8962 Part 4 Form 8962 Part 5 56

57 Form 8962 Example Family of Four: Couple with 2 children Adjusted Gross Income $ 68,000 + Tax Exempt Income = $1,212 Total Modified Adjusted Gross Income = $69,212 = Line 2a Dependents no income no filing requirement = line 2b Lives in Iowa = check Box 4c Determine Poverty Level Qualifications Table 2 Page 6 Form

Line 6 = Is the result on Line 5 less than or equal to 400% = Check the Yes Box Line 7 = Table 2 in the instructions Line 7 =.0950 Line 8a = $78,523 X.")

58 Determine Poverty Level Qualifications Line 4 = $23,850 Line 5 = 3.29 ( must be between 1.00 and 3.99) Line 6 = Is the result on Line 5 less than or equal to 400% = Check the Yes Box Line 7 = Table 2 in the instructions Line 7 =.0950 Line 8a = $78,523 X.095 = $7,460 Annual Contribution Line 8b = $7,460/12 = Monthly Contribution of $ Form 8962 Form 8962 Relief Box Upper RH Corner Domestic abuse. Domestic abuse includes physical, psychological, sexual, or emotional abuse, including efforts to control, isolate, humiliate, and intimidate, or to undermine the victim's ability to reason independently. All the facts and circumstances are considered in determining whether an individual is abused, including the effects of alcohol or drug abuse by the victim s spouse. Depending on the facts and circumstances, abuse of the victim s child or other family member living in the household may constitute abuse of the victim. Spousal abandonment. A taxpayer is a victim of spousal abandonment for a tax year if, taking into account all facts and circumstances, the taxpayer is unable to locate his or her spouse after reasonable diligence. To certify that you are eligible for an exception to the requirement to file a joint return under Situation 2, check the Relief box in the top right hand corner of Form Do not attach documentation of the abuse or abandonment to your tax return. Keep any documentation you may have with your tax return records. For examples of what documentation to keep, see Pub

59 Other Factors to Consider If Form 1095=A is not received by February 15, 2015 client must contact the Insurance company IRS cannot assist Changes in Family Divorce Married Taxpayers Filing Separate Returns. The premium tax credit is allowed to married taxpayers only if they file joint returns. See 1.36B 2(b)(2). A married taxpayer who receives advance credit payments and files an income tax return as married filing separately has received excess advance payments. Taxpayers who receive advance credit payments as married taxpayers and do not file a joint return must allocate the advance credit payments equally to each taxpayer. The repayment limitation applies to each taxpayer based on the household income and family size reported on that taxpayer s return. Taxpayers Filing returns as Head of Household and Married Filing Separately. If taxpayers enroll in one qualified health plan and receive advance credit payments based on a filing status of married filing a joint tax return, and one taxpayer properly files a tax return as head of household and the other taxpayer files a tax return as married filing separately for that taxable year, advance credit payments are allocated to each taxpayer equally for any period the taxpayers are enrolled in the same qualified health plan. 59

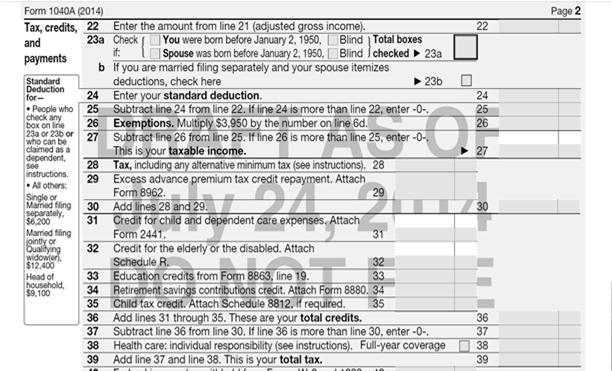

60 Form 1040 Series What Lines are Important?

61 A 1040A 61

62 1040 EZ Form 1094 B Transmittal 1095 B 62

63 1095 B 1094 C Transmittal 1094 C Transmittal, Part 2 63

64 Form 1095 C Transmittal, Part 3 Form 1095 C Transmittal Part Farm Tax Schools November 9, 2015 to December 15, Locations in Iowa Registration and the Fall Brochure will be out in August The program is intended for tax professionals and is designed to provide up to date training on current tax law and regulations. The program stresses practical information to facilitate the filing of individual and small business returns, in addition to farm returns. 64

65 2015 Farm Tax Schools Dates and Locations Waterloo: Nov 9 10 Sheldon: Nov Red Oak: Nov Ottumwa: Nov Mason City: Nov Maquoketa: Nov Denison: Dec. 7 8 Ames: Dec live as well as attendance via webinar available July Webinars Foreign Account Tax Compliance Act (FATCA) July 2, Noon to 1:00 The Foreign Account Tax Compliance Act (FATCA) is a United States federal law that requires United States persons, including individuals who live outside the United States, to report their financial accounts held outside of the United States, and requires foreign financial institutions to report to the Internal Revenue Service (IRS) about their U.S. clients. We will provide an overview of the law and filing requirements. Preparing for a Gambling Audit July 6, Noon to 1:00 Your client gambles, whether it slots or poker we will review the recent IRS issues as they relate to auditing your client who has gaming income. What advice should you give a client with this type of income and what records will IRS accept during the audit process will be discussed. July Webinars The Partnership Form K 1 July 8, Noon to 1:00 An overview of Form 1065 K 1 preparation and the resulting Form 1040 income issues will be discussed. Bartering and Trading Income July 13, Noon to 1:00 A question IRS auditor always ask, Dow you have any bartering or trading income? How this income is reported and the adjustments needed to be made on the tax return will be discussed. Correspondence Audits July 14, Noon 1:00 IRS s chief audit stream is correspondence audit. They do more of them than face to face and other types of audits combined. Responding to the audit request and providing logical and concise information to resolve the issue is an important part of the audit process. What are the do s and don ts in providing the information and how best to handle the audit will be discussed. Issues Related to Estates, Procedures and Developments in Estate Tax Law July 23, Noon to 1:00 What s new with Estates tax law? An overview of some of the recent estate issues and a review of typical estate tax issues that you face with your clients. 65

66 CALT Website Tour of the CALT Website CALT Staff Roger A. McEowen CALT Director and is a Leonard Dolezal Professor in Agricultural Law mceowen@iastate.edu Phone: (515) Fax: (515) Kristine A. Tidgren Staff Attorney E mail: ktidgren@iastate.edu Phone: (515) Fax: (515)

296 3810 Fax: (515) 294 0700 Tiffany Kayser Program")

294 5217 Fax: (515) 294 0700 Scoop Dates for Post Filing Season")

67 CALT Staff Kristy S. Maitre Tax Specialist E mail: ksmaitre@iastate.edu Phone: (515) Fax: (515) Tiffany Kayser Program Administrator tlkayser@iastate.edu Phone: (515) Fax: (515) Scoop Dates for Post Filing Season July 15, 2015 August 5, 2015 September 23, 2015 October 21,

FACTS ABOUT THE ACA INDIVIDUAL MANDATE

FACTS ABOUT THE ACA INDIVIDUAL MANDATE Beginning 2014, every U.S. citizen and resident alien must have health insurance (minimum essential coverage). Failure to do so will result in a penalty (an additional

FACTS ABOUT THE ACA INDIVIDUAL MANDATE Beginning 2014, every U.S. citizen and resident alien must have health insurance (minimum essential coverage). Failure to do so will result in a penalty (an additional

AFFORDABLE CARE ACT SURVIVAL KIT

AFFORDABLE CARE ACT SURVIVAL KIT This tool was developed to help VITA/TCE volunteers understand the ACA-related tax provisions and how to complete a return in TaxWise. Approaching the ACA Ask each person

AFFORDABLE CARE ACT SURVIVAL KIT This tool was developed to help VITA/TCE volunteers understand the ACA-related tax provisions and how to complete a return in TaxWise. Approaching the ACA Ask each person

Exemptions and the Share Responsibility Payment. Exemption from What? What Exemptions Are Available? 10/19/2015

Exemptions and the Share Responsibility Payment Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 20, 2015 Exemption from What? Having to have insurance coverage Having to pay

Exemptions and the Share Responsibility Payment Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 20, 2015 Exemption from What? Having to have insurance coverage Having to pay

ACA & the Tax Season

ACA & the Tax Season Common Cents Tara Straw September 9, 2014 The ACA on the Tax Return 2 Reporting health coverage For every month For everyone on the return Exemptions from the individual responsibility

ACA & the Tax Season Common Cents Tara Straw September 9, 2014 The ACA on the Tax Return 2 Reporting health coverage For every month For everyone on the return Exemptions from the individual responsibility

Instructions for Form 8962

2017 Instructions for Form 8962 Premium Tax Credit (PTC) Department of the Treasury Internal Revenue Service Purpose of Form Use Form 8962 to figure the amount of your premium tax credit (PTC) and reconcile

2017 Instructions for Form 8962 Premium Tax Credit (PTC) Department of the Treasury Internal Revenue Service Purpose of Form Use Form 8962 to figure the amount of your premium tax credit (PTC) and reconcile

Instructions for Form 8962

2018 Instructions for Form 8962 Premium Tax Credit (PTC) Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Purpose of Form

2018 Instructions for Form 8962 Premium Tax Credit (PTC) Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Purpose of Form

Caution: DRAFT NOT FOR FILING

Caution: DRAFT NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information as a courtesy. Do not file draft forms. Also,

Caution: DRAFT NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information as a courtesy. Do not file draft forms. Also,

AFFORDABLE CARE ACT (ACA)

") AFFORDABLE CARE ACT (ACA) Select this box if anyone in the tax household had MEC at any time during the year. (See page ACA-4) A Yes answer will prompt another question about health insurance purchased

AFFORDABLE CARE ACT (ACA) Select this box if anyone in the tax household had MEC at any time during the year. (See page ACA-4) A Yes answer will prompt another question about health insurance purchased

2014 AFFORDABLE CARE ACT (OBAMA CARE)

") 2014 AFFORDABLE CARE ACT (OBAMA CARE) Planning for 2014 Tax Return Filings O Beginning 2014, the ACA requires all persons be covered by health insurance O Individuals not covered by Medicare, their employers,

2014 AFFORDABLE CARE ACT (OBAMA CARE) Planning for 2014 Tax Return Filings O Beginning 2014, the ACA requires all persons be covered by health insurance O Individuals not covered by Medicare, their employers,

Basic Information 1. What is the individual shared responsibility provision?

Affordable Care Act Topics Individuals and Families Employers Other Organizations For Tax Pros What's Trending News Health Care Tax Tips Questions and Answers Legal Guidance and Other Resources Affordable

Affordable Care Act Topics Individuals and Families Employers Other Organizations For Tax Pros What's Trending News Health Care Tax Tips Questions and Answers Legal Guidance and Other Resources Affordable

The Affordable Care Act and Taxes

The Affordable Care Act and Taxes ACA Reference Guide» ACA and Taxes > Quick Reference Guide 1 2 4 5 9 10 11 > Section 1 ACA Basics > Section 2 Coverage Exemptions > Section 3 Individual Shared Responsibility

The Affordable Care Act and Taxes ACA Reference Guide» ACA and Taxes > Quick Reference Guide 1 2 4 5 9 10 11 > Section 1 ACA Basics > Section 2 Coverage Exemptions > Section 3 Individual Shared Responsibility

2016 Instructions for Form 8965

Department of the Treasury Internal Revenue Service 2016 Instructions for Form 8965 Health Coverage Exemptions (and Instructions for Figuring Your Shared Responsibility Payment) For each month you must

Department of the Treasury Internal Revenue Service 2016 Instructions for Form 8965 Health Coverage Exemptions (and Instructions for Figuring Your Shared Responsibility Payment) For each month you must

2018 Instructions for Form 8965

Department of the Treasury Internal Revenue Service 2018 Instructions for Form 8965 Health Coverage Exemptions (and Instructions for Figuring Your Shared Responsibility Payment) Section references are

Department of the Treasury Internal Revenue Service 2018 Instructions for Form 8965 Health Coverage Exemptions (and Instructions for Figuring Your Shared Responsibility Payment) Section references are

Other Taxes and Payments

Other Taxes and Payments TaxSlayer provides all the forms and schedules you need in order to figure and report these taxes, and in most cases, performs the calculations. Self-Employment Tax Entered automatically

Other Taxes and Payments TaxSlayer provides all the forms and schedules you need in order to figure and report these taxes, and in most cases, performs the calculations. Self-Employment Tax Entered automatically

Affordable Care Act. Introduction. What is the Affordable Care Act? Objectives

Affordable Care Act Introduction This lesson covers some of the tax provisions of the Affordable Care Act (ACA). You will learn how to determine if taxpayers satisfy the individual shared responsibility

Affordable Care Act Introduction This lesson covers some of the tax provisions of the Affordable Care Act (ACA). You will learn how to determine if taxpayers satisfy the individual shared responsibility

Beyond the Basics of Exemptions and Special Enrollment Periods

Beyond the Basics of Exemptions and Special Enrollment Periods Center on Budget and Policy Priorities March 26, 2014 2 Part I: SPECIAL ENROLLMENT PERIODS 3 Open Enrollment Annual Period When All Eligible

Beyond the Basics of Exemptions and Special Enrollment Periods Center on Budget and Policy Priorities March 26, 2014 2 Part I: SPECIAL ENROLLMENT PERIODS 3 Open Enrollment Annual Period When All Eligible

Sales Division Webinar #9

Disclaimer: The information contained in this presentation is a brief overview and should not be construed as tax advice or exhausted coverage of the topic. 1 Sales Division Webinar #9 ALL SERVICE CHANNELS

Disclaimer: The information contained in this presentation is a brief overview and should not be construed as tax advice or exhausted coverage of the topic. 1 Sales Division Webinar #9 ALL SERVICE CHANNELS

Caution: DRAFT NOT FOR FILING

Caution: DRAFT NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information as a courtesy. Do not file draft forms. Also,

Caution: DRAFT NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information as a courtesy. Do not file draft forms. Also,

Guidelines for Quality Reviewing ACA Issues

Attachment 1 Guidelines for Quality Reviewing ACA Issues Form 13614-C, Intake/Interview Sheet Is Form 13614-C complete? Every question is answered Yes or No? Unsure responses have been answered Yes or

Attachment 1 Guidelines for Quality Reviewing ACA Issues Form 13614-C, Intake/Interview Sheet Is Form 13614-C complete? Every question is answered Yes or No? Unsure responses have been answered Yes or

2014 Affordable Care Act Provisions for Individuals, Families and Small Business. Brian Wozniak

2014 Affordable Care Act Provisions for Individuals, Families and Small Business Brian Wozniak January 13, 2015 1 Agenda Health Insurance Marketplace Individual Shared Responsibility Provision Overview

2014 Affordable Care Act Provisions for Individuals, Families and Small Business Brian Wozniak January 13, 2015 1 Agenda Health Insurance Marketplace Individual Shared Responsibility Provision Overview

Marketplace 101. Find health care options that meet your needs and fit your budget

Marketplace 101 Find health care options that meet your needs and fit your budget Objectives This session will help you Explain the Health Insurance Marketplace Define who might be eligible Define options

Marketplace 101 Find health care options that meet your needs and fit your budget Objectives This session will help you Explain the Health Insurance Marketplace Define who might be eligible Define options

VITA/TCE Basic Certification Topics on Affordable Care Act. Current as of November 20, 2017

VITA/TCE Basic Certification Topics on Affordable Care Act Current as of November 20, 2017 MEC & SRP REFRESHER What does the ACA require? 3 or or Coverage Exemption SRP Minimum Essential Coverage (MEC)

VITA/TCE Basic Certification Topics on Affordable Care Act Current as of November 20, 2017 MEC & SRP REFRESHER What does the ACA require? 3 or or Coverage Exemption SRP Minimum Essential Coverage (MEC)

Affordable Care Act. Pub 4012 ACA Tab Pub 4491 Lesson 3

Affordable Care Act Pub 4012 ACA Tab Pub 4491 Lesson 3 ACA IT s The Law Like it or not Repeal or change possible But, Applies to 2016 Deal with it The Good News Most of clients have Medicare 2 ACA Summary

Affordable Care Act Pub 4012 ACA Tab Pub 4491 Lesson 3 ACA IT s The Law Like it or not Repeal or change possible But, Applies to 2016 Deal with it The Good News Most of clients have Medicare 2 ACA Summary

What Happens at Tax Time? Tax Penalties and Premium Tax Credit Reconciliation. Tricia Brooks OACHC Training March 11, 2015

What Happens at Tax Time? Tax Penalties and Premium Tax Credit Reconciliation Tricia Brooks OACHC Training March 11, 2015 What happens at tax time? 1 2 3 Uninsured individuals will pay a tax penalty, unless

What Happens at Tax Time? Tax Penalties and Premium Tax Credit Reconciliation Tricia Brooks OACHC Training March 11, 2015 What happens at tax time? 1 2 3 Uninsured individuals will pay a tax penalty, unless

Marketplace Model Eligibility Notice for 2016 Coverage Special Enrollment Verification Process

Marketplace Model Eligibility Notice for 2016 Coverage Special Enrollment Verification Process Special Enrollment Periods provide an important pathway to coverage for consumers who experience qualifying

Marketplace Model Eligibility Notice for 2016 Coverage Special Enrollment Verification Process Special Enrollment Periods provide an important pathway to coverage for consumers who experience qualifying

MARKET STABILITY WORKGROUP 2.0. Tuesday, November 13, :30 10:30 a.m. The United Way of Rhode Island

MARKET STABILITY WORKGROUP 2.0 Tuesday, November 13, 2018 8:30 10:30 a.m. The United Way of Rhode Island 1 UPDATES SINCE OUR LAST MEETING Meeting 3 Follow-ups: 1332 Guidance HRA rule Brief overview of

MARKET STABILITY WORKGROUP 2.0 Tuesday, November 13, 2018 8:30 10:30 a.m. The United Way of Rhode Island 1 UPDATES SINCE OUR LAST MEETING Meeting 3 Follow-ups: 1332 Guidance HRA rule Brief overview of

Part I: Premium Tax Credits

Part I: Premium Tax Credits Coverage Year 2018 Center on Budget and Policy Priorities September 19, 2017 Overview of Upcoming Open Enrollment Shorter Open Enrollment for OE5 3 Nov 1: Open enrollment begins

Part I: Premium Tax Credits Coverage Year 2018 Center on Budget and Policy Priorities September 19, 2017 Overview of Upcoming Open Enrollment Shorter Open Enrollment for OE5 3 Nov 1: Open enrollment begins

AFORDABLE CARE ACT (ACA)

") AFORDABLE CARE ACT (ACA) The Patient Protection and Affordable Care Act of 2010, commonly known as the Affordable Care Act (ACA), contain several key programs and mandates for employers and individuals.

AFORDABLE CARE ACT (ACA) The Patient Protection and Affordable Care Act of 2010, commonly known as the Affordable Care Act (ACA), contain several key programs and mandates for employers and individuals.

STARTING STRONG FOR COMMUNITY HEALTH! WEBINAR

STARTING STRONG FOR COMMUNITY HEALTH! WEBINAR The ACA and Taxes: Tips for Enrollment Assisters February 26, 2016 Today s Presenters: Alicia Siani, Policy Analyst, EverThrive IL asiani@everthriveil.org

STARTING STRONG FOR COMMUNITY HEALTH! WEBINAR The ACA and Taxes: Tips for Enrollment Assisters February 26, 2016 Today s Presenters: Alicia Siani, Policy Analyst, EverThrive IL asiani@everthriveil.org

AFFORDABLE CARE ACT INTRODUCTION CAUTION!

AFFORDABLE CARE ACT INTRODUCTION Last summer, the United States Supreme Court upheld the constitutionality of the Affordable Care Act (ACA) removing most of the constitutional issues surrounding health

AFFORDABLE CARE ACT INTRODUCTION Last summer, the United States Supreme Court upheld the constitutionality of the Affordable Care Act (ACA) removing most of the constitutional issues surrounding health

Everyone must have Healthcare Insurance. Exemptions are available (Form 8965) No Insurance and No Exemption?

No Insurance and No Exemption?") Three Main Elements Everyone must have Healthcare Insurance Exemptions are available (Form 8965) No Insurance and No Exemption? Additional tax Individual Shared Responsibility Payment ( SRP ) Financial

Three Main Elements Everyone must have Healthcare Insurance Exemptions are available (Form 8965) No Insurance and No Exemption? Additional tax Individual Shared Responsibility Payment ( SRP ) Financial

Patient Protection and Affordable Care Act (PPACA) Better known as ACA

Better known as ACA") Patient Protection and Affordable Care Act (PPACA) Better known as ACA Status The following presentation is an overview of the Affordable Care Act (ACA) Some forms and specific documentation are in draft

Patient Protection and Affordable Care Act (PPACA) Better known as ACA Status The following presentation is an overview of the Affordable Care Act (ACA) Some forms and specific documentation are in draft

Key Facts: Premium Tax Credit

Updated September 13, 2018 Key Facts: Premium Tax Credit As a result of the Affordable Care Act (ACA), millions of Americans are eligible for a premium tax credit that helps them pay for health coverage.

Updated September 13, 2018 Key Facts: Premium Tax Credit As a result of the Affordable Care Act (ACA), millions of Americans are eligible for a premium tax credit that helps them pay for health coverage.

VITA/TCE Basic Certification Topics on Affordable Care Act. Current as of November 20, 2017

VITA/TCE Basic Certification Topics on Affordable Care Act Current as of November 20, 2017 Agenda 2 Webinar #1 Basic Certification Topics Minimum essential coverage Shared responsibility payment Exemptions

VITA/TCE Basic Certification Topics on Affordable Care Act Current as of November 20, 2017 Agenda 2 Webinar #1 Basic Certification Topics Minimum essential coverage Shared responsibility payment Exemptions

The Affordable Care Act and the Income Tax. By Greg Martinez December 2013

The Affordable Care Act and the Income Tax By Greg Martinez December 2013 Overview Health insurance mandate Individual Shared Responsibility Provision Exemptions Minimum essential coverage Penalties Covered

The Affordable Care Act and the Income Tax By Greg Martinez December 2013 Overview Health insurance mandate Individual Shared Responsibility Provision Exemptions Minimum essential coverage Penalties Covered

FEDERAL INCOME TAX IMPLICATONS OF THE ACA MANDATE FOR INDIVIDUAL TAXPAYERS

FEDERAL INCOME TAX IMPLICATONS OF THE ACA MANDATE FOR INDIVIDUAL TAXPAYERS Starting in 2014, the Patient Protection and Affordable Care Act (ACA) mandates that individuals carry minimum essential health

FEDERAL INCOME TAX IMPLICATONS OF THE ACA MANDATE FOR INDIVIDUAL TAXPAYERS Starting in 2014, the Patient Protection and Affordable Care Act (ACA) mandates that individuals carry minimum essential health

Quickfinder. Health Care Reform Quickfinder Handbook (2018 Edition) Updates for the Tax Cuts and Jobs Act of 2017 and Other Recent Guidance

Updates for the Tax Cuts and Jobs Act of 2017 and Other Recent Guidance") Quickfinder Health Care Reform Quickfinder Handbook (2018 Edition) Updates for the Tax Cuts and Jobs Act of 2017 and Other Recent Guidance Instructions: This packet contains marked up changes to the pages

Quickfinder Health Care Reform Quickfinder Handbook (2018 Edition) Updates for the Tax Cuts and Jobs Act of 2017 and Other Recent Guidance Instructions: This packet contains marked up changes to the pages

Premium Tax Credit (PTC)

") Department of the Treasury Internal Revenue Service Publication 974 Cat. No. 66452Q Premium Tax Credit (PTC) For use in preparing 2017 Returns Contents Future Developments... 1 Reminders... 2 Introduction...

Department of the Treasury Internal Revenue Service Publication 974 Cat. No. 66452Q Premium Tax Credit (PTC) For use in preparing 2017 Returns Contents Future Developments... 1 Reminders... 2 Introduction...

Open Enrollment is here!

Navigating the Federal Marketplace AFFORDABLE CARE Open Enrollment is here! Reminders On November 20 at 9:30 AM ET, IPHCA is hosting a call with Matt Cesnik from FSSA again. CMS has released guidance on

Navigating the Federal Marketplace AFFORDABLE CARE Open Enrollment is here! Reminders On November 20 at 9:30 AM ET, IPHCA is hosting a call with Matt Cesnik from FSSA again. CMS has released guidance on

Premium Tax Credit (PTC)

") Department of the Treasury Internal Revenue Service Publication 974 Cat. No. 66452Q Premium Tax Credit (PTC) For use in preparing 2016 Returns Contents Future Developments... 1 Reminders... 1 Introduction...

Department of the Treasury Internal Revenue Service Publication 974 Cat. No. 66452Q Premium Tax Credit (PTC) For use in preparing 2016 Returns Contents Future Developments... 1 Reminders... 1 Introduction...

How Minimum Is Your Health Insurance Coverage? IRS Proposes Regulations on Offering and Maintaining Minimum Essential Coverage Starting in 2014

How Minimum Is Your Health Insurance Coverage? IRS Proposes Regulations on Offering and Maintaining Minimum Essential Coverage Starting in 2014 February 2013 Proposed regulations issued by the Treasury

How Minimum Is Your Health Insurance Coverage? IRS Proposes Regulations on Offering and Maintaining Minimum Essential Coverage Starting in 2014 February 2013 Proposed regulations issued by the Treasury

Taxes and Consumer Education

Outreach and Enrollment Distance Learning Series Taxes and Consumer Education August 13, 2015 Welcome to the Outreach and Enrollment Webcast Series All lines are muted. Please use chat to ask a question

Outreach and Enrollment Distance Learning Series Taxes and Consumer Education August 13, 2015 Welcome to the Outreach and Enrollment Webcast Series All lines are muted. Please use chat to ask a question