ACA 2 years Later Getting Ready for the 2017 Tax Season. Obamacarefacts.com. Affordable Car Act and the Patient Protection Act 10/6/2016

|

|

|

- Edward White

- 5 years ago

- Views:

Transcription

1 ACA 2 years Later Getting Ready for the 2017 Tax Season Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 6, 2016 Obamacarefacts.com Affordable Car Act and the Patient Protection Act The first part of the comprehensive health care reform law enacted on March 23, 2010 The law was amended by the Health Care and Education Reconciliation Act on March 30, 2010 The name Affordable Care Act is usually used to refer to the final, amended version of the law The law provides numerous rights and protections that make health coverage more fair and easy to understand, and more affordable The law also expands the Medicaid program to cover more people with low incomes in certain states 1

2 States and Medicaid Status as of July 6, 2016 States expanding Medicaid AK, AZ, AR, CA, CO, CT, DE, DC, HI, IL, IA, IN, KY, LA, MD, MA, MI, MN, MA, MT, NV, NH, NJ, NM, NY, ND, OH, OR, PA, RI, VT, WA, WV States not expanding Medicaid at this time AL, FL, GA, ID, KS, ME, MO, MS, NE, NC, OK, SC, SD, TN, TX, UT, VA, WI, WY How the Health Care Law Protects Individuals Taxpayers Requires insurance plans to cover people with pre existing health conditions, including pregnancy, without charging more Provides free preventive care Gives young adults more coverage options Ends lifetime and yearly dollar limits on coverage of essential health benefits How the Health Care Law Protects Individuals Taxpayers Helps understand the coverage taxpayer s are getting Holds insurance companies accountable for rate increases Makes it illegal for health insurance companies to cancel health insurance just because a taxpayer is sick Protects the choice of doctors Protects the taxpayer from employer retaliation 2

3 Additional Rights and Benefits Breastfeeding equipment and support Birth control methods and counseling Mental health and substance abuse services The right to appeal a health plan decision The right to choose an individual Marketplace plan rather than the one the employer offers What Was the Law Intended to Accomplish? Increase health insurance quality and affordability Lower the uninsured rate by expanding insurance coverage and reduce the costs of healthcare It introduced mechanisms including mandates, subsidies and insurance exchanges The law requires insurers to accept all applicants Cover a specific list of conditions Charge the same rates regardless of pre existing conditions or sex In 2011, the Congressional Budget Office projected that the ACA would lower future deficits and Medicare spending Source: Wikipedia The Law Introduced new Forms and Filing Requirements Form 8962 the Premium Tax Credit If subsidies are received it creates a filing requirement Form 8965 Health Coverage Exemptions Form 1095 series Form 1095 A Health Insurance Marketplace Statement Form 1095 B Health Coverage Form 1095 C Employer Provided Health Insurance Offer and Coverage 3

for whom the client told the Marketplace they would claim")

4 Minimum Essential Coverage Who Must File The client must file Form 8962 with the income tax return (Form 1040, Form 1040A, or Form 1040NR) if any of the following apply to the client They took the Premium Tax Credit APTC was paid to the client or another individual in the tax family APTC was paid for an individual (including the client) for whom the client told the Marketplace they would claim a personal exemption and neither the client nor anyone else claims a personal exemption for that individual The Marketplace 4

5 Report Changes in Circumstances When Enroll in Coverage and During the Year If APTC is being paid in 2016 for an individual in the tax family, the client has to report certain changes in circumstances to the Marketplace where they enrolled Reporting changes in circumstances promptly will allow the Marketplace to adjust the APTC to more accurately reflect the PTC estimated Adjusting the APTC can help avoid owing tax when the client files the tax return Report Changes in Circumstances When Enroll in Coverage and During the Year Changes that should be reported to the Marketplace include: Changes in household income Moving to a different address Gaining or losing eligibility for other health care coverage Gaining, losing, or other changes to employment Birth or adoption Marriage or divorce Other changes affecting the composition of the tax family Where To Start 5

6 Using the Forms to Help Your Client Clients do not always know If they are within the Federal Poverty Level window Understand the terminology discussed on the Marketplace What income to include in the application Who to include in the tax family unit Household Income Worksheet Household Income Modified AGI For purposes of the PTC, modified AGI is the AGI on the tax return plus certain income that is not subject to tax Foreign earned income Foreign housing Tax exempt interest Social security benefits that are not taxable RR Retirement Tier 1 non taxable benefits 6

7 Household Income For purposes of the PTC, household income is the modified adjusted gross income of the client and their spouse (if filing a joint return) Plus the modified AGI of each individual whom they claim as a dependent and who is required to file an income tax return because his or her income meets the income tax return filing threshold (added in on Form 8962) Household income does not include the modified AGI of those individuals whom the client is claiming as a dependent and who are filing a 2016 return only to claim a refund of withheld income tax or estimated tax Client s Tax Return Includes Income of a Dependent Child A taxpayer who includes the gross income of a dependent child on the taxpayer s tax return must include the child s tax exempt interest and the portion of the child s social security benefits that is not taxable Individual Enrolled for Whom No Taxpayer Will Claim a Personal Exemption If the client indicated to the Marketplace at enrollment that they would claim the personal exemption for an individual (including themselves) but no taxpayer claims a personal exemption for the individual, they must report and reconcile APTC paid for that individual's coverage 7

8 Affordability The Affordability Factor 2016 = 8.13% Household income X 8.13% = affordability factor The affordability factor in 2017 will be 8.16% Employer Requirements Affordable coverage for self only Affordable coverage for dependents Family coverage offered does not have to be affordable 8

9 Example 1 Tammy is unmarried and has no dependents Her household income is $60,000 and she did not participate in a contribution to a salary reduction agreement If there was participation in a salary reduction agreement, Tammy would have to include the amount into the household income to determine affordability A taxpayer cannot reduce income through an agreement where it would make insurance unaffordable During 2016, Tammy could purchase self only coverage through her employer at a total cost to her of $5,000 Tammy can claim the exemption for unaffordable coverage because her required contribution ($5,000) is more than 8.13% of her household income ($4,878, which is $60,000 multiplied by ) Example 2 Jessica and Josh are married and file a joint return for 2016 They have two children, Betty and Sam whom they claim as dependents on their return During 2016, Jessica could purchase self only coverage under a plan offered by her employer at a cost to her of $4,000 Jessica could also purchase family coverage under the plan, which would cover her, Josh, Betty and Sam at a cost to her of $12,000 Josh could not purchase health insurance through his employer Their household income for 2016 is $90,000 Example 2, cont d Jessica is ineligible for the exemption for unaffordable coverage for 2016 because her required contribution ($4,000) is not more than 8.13% of her household income ($7,317, which is $90,000 multiplied by ) If Jessica choses not to take the coverage and she does not qualify for another coverage exemption, she would make a shared responsibility payment for the months during which she did not have coverage The required contribution for Josh, Betty and Sam is Jessica s share of the cost for family coverage ($12,000), which is more than 8.13% of their household income ($7,317) 9

10 Example 2, cont d Josh, Betty and Sam could possibly obtain affordable coverage at the Marketplace using the Marketplace Affordability Worksheet Josh, Betty and Sam are eligible for the exemption for unaffordable coverage for 2016 if affordability coverage is not available at the Marketplace No shared responsibility payment is required for Josh, Betty and Sam Affordability Worksheet for Employer Sponsored Coverage Result If Jessica took employer coverage she would receive a 1095 B or C depending on the insurance coverage If the remaining family members went to the Marketplace, they would receive a Form 1095 A 10

The family size equals the number of individuals in the tax family Applicable Taxpayer The client must be an applicable taxpayer to take the PTC Generally,")

11 Tax Family For purposes of the PTC, the tax family consists of the individuals for whom the client claims a personal exemption on the tax return (generally the client, the spouse with whom they are filing a joint return, and the dependents) The family size equals the number of individuals in the tax family Applicable Taxpayer The client must be an applicable taxpayer to take the PTC Generally, they are an applicable taxpayer if the household income for 2016 is at least 100% but not more than 400% of the Federal poverty line for the family size and no one else can claim the client as a dependent for 2016 In addition, if married at the end of 2016, the client must file a joint return to be an applicable taxpayer unless they meet one of the exceptions outlined in married taxpayers Other Points 11

12 Other Points Household Income Below 100% of the Federal Poverty Line If the amount on line 5 of Form 8962 is less than 100%, you can take the PTC if the client meets the requirements under Estimated household income at least 100% of the Federal poverty line or Alien lawfully present in the United States Line 5 of Form

13 Estimated Household Income at Least 100% of the Federal Poverty Line The client or an individual in the tax family enrolled in a qualified health plan through a Marketplace The Marketplace estimated at the time of the enrollment that the household income would be at least 100% but not more than 400% of the Federal poverty line for the family size for 2016 APTC was paid for the coverage for one or more months during 2016 You otherwise qualify as an applicable taxpayer (except for the Federal poverty line percentage) Alien Lawfully Present in the United States Certain aliens with household income below 100% of the Federal poverty line are not eligible for Medicaid because of their immigration status They may qualify for the PTC if the household income is less than 100% of the Federal poverty line if they meet all of the following requirements They or an individual in the tax family enrolled in a qualified health plan through a Marketplace The enrolled individual is lawfully present in the United States and is not eligible for Medicaid because of immigration status They otherwise qualify as an applicable taxpayer (except for the Federal poverty line percentage) Lines 6 & 7 of Form 8962 If the client meets all of the requirements under either Estimated household income at least 100% of the Federal poverty line or Alien lawfully present in the United States, check the No box on line 6 and continue to line 7 If your household income is less than 100% of the Federal poverty line and they did not meet the requirements under Estimated household income at least 100% of the Federal poverty line or Alien lawfully present in the United States, they are not an applicable taxpayer and they are not eligible to take the PTC Check the Yes box on line 6, skip lines 7 and 8, and go to line 9 However, if no APTC was paid for any individuals in the tax family, Form 8962 is not required to be completed 13

14 Lines 8 and 9 of Form 8962 Household Income Above 400% of the Federal Poverty Line If the amount on line 5 is 401%, an individual cannot take the PTC Generally, the PTC must be repaid There are two exceptions: If the household income is above 400% of the Federal poverty line but the client qualifies for the alternative calculation for the year of marriage, they may be able to reduce the amount of APTC they have to repay If they enrolled an individual for whom another taxpayer will claim a personal exemption, the other taxpayer may be responsible to repay all or part of the APTC Federal Poverty Level 14

15 Federal Poverty Level Every year, the perimeters of the Federal Poverty Level (FPL) increase based on the cost of living Families need to understand where they fall on the FPL so they know whether they are eligible for Medicaid in their state or whether they are eligible for a federal subsidy If they earn between 100 and 400 percent of the FPL, and/or Whether they are eligible for a tax credit Federal Poverty Level 48 Continuous States Federal Poverty Level Alaska 15

16 Federal Poverty Level Hawaii Form 8962 Using Form 8962 to Figure FPL 16

17 Using Form 8962 to Figure Annual Contribution Amount Applicable Figure Amount Located in the Form 8962 instructions May be automatically input into the software Form

18 Form 8962 How to Find the 1095 A Online Log in to your Marketplace account Click the green "Start a new application or update an existing one" button Choose "Go to my applications & coverage" at the bottom of the screen How to Find the 1095 A Online Under "Your existing applications," select your 2016 application not your 2017 application It will be below your 2017 application Select Tax forms from the menu on the left Download all 1095 As shown on the screen If you can t find it in your Marketplace account, contact the Marketplace Call Center 18

19 What s on Form 1095 A and Why Does Your Client Need It? The 1095 A contains information about Marketplace plans any member of the household had in 2016, including: Premiums paid Premium tax credits used A figure called the second lowest cost silver plan They will use information from the 1095 A to fill out Form 8962 This is how they will "reconcile" find out if there's any difference between the premium tax credit used and the amount the client may qualify for The Forms Form

20 Form 8962 Part II Form 8962 Part II Form 1095 Series 20

21 Form 1095 A Form 1095 A Form 1095 B 21

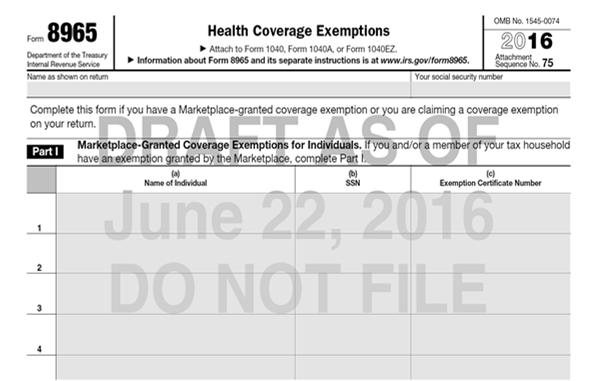

22 Form 1095 C Exemptions Form

23 Form 8965 Answers to Concerns What should I do if I don t receive a Form 1095 A? If the client purchased coverage through the Marketplace and has not received the Form 1095 A, they should contact the Marketplace from which they received coverage They should wait to receive the Form 1095 A before filing taxes Individuals who did not purchase coverage through the Marketplace, including those with Medicaid or CHIP coverage, will not receive a Form 1095 A 23

24 What Should the Client Do if Form 1095 A is Incorrect and Has Not Received a Corrected Form? If the client believes the Form 1095 A is incorrect, they should contact the state or federal Marketplace from which they received coverage The Marketplace may need to send them a corrected Form 1095 A What should the Client do if a Corrected or Voided Form 1095 A is Received? When a corrected or voided Form 1095 A, is received an amend return may need to be filed What is the Second Lowest Cost Silver Plan Shown on the Form 1095 A? Also known as SLCSP, this is reported on Form 1095 A in Part III, column B If the client was eligible to claim the premium tax credit, the premium for a SLCSP applies to some or all of the family members enrolled in coverage It is an important factor that determines the monthly amount of the premium tax credit If there were changes in the family or if the client moved and did not notify the Marketplace of these changes, the premium for the applicable SLCSP reported on the Form 1095 A, Part III, column B, may not be accurate for one or more months The applicable SLCSP premium on the Form 1095 A also may be incorrect if the client did not request advance payments of the premium tax credit 24

25 What is the Second Lowest Cost Silver Plan Shown on the Form 1095 A? If one of these situations applies, the client must determine the correct premium for the applicable SLCSP for the months affected Why Did the Client Get More than One Form 1095 A? The client may receive more than one Form 1095 A if members of the household were not all enrolled in the same health plan The client must updated the family information during the year, if they switched plans during the year, or had family members enrolled in different states What to Do if Multiple Forms 1095A are Received? If the client receives more than one Form 1095 A from the same Marketplace that reports coverage for different months, you will enter the information for the corresponding month on Form 8962, lines 12 through 23 You will find this information in Part III of the Form 1095 A 25

26 Why Did the Client Get a Letter from the IRS Asking for More Information and a Copy of the Form 1095 A? The client does not have to send the Form 1095 A to the IRS with their tax return when they file and claim the premium tax credit Using the information on the Form 1095 A the client must complete and file Form 8962, Premium Tax Credit The IRS verifies the information on the Form 8962 by comparing it to information received from the Marketplace and to other information entered on the tax return Before IRS can send a refund, the IRS may send a letter, 12C, asking the client to clarify or verify information that was entered on the income tax return The letter may ask for a copy of the Form 1095 A Some Common Examples of Issues or Questions that May Arise It appears that the client is required to reconcile but did not include Form 8962 The Form 8962 submitted is incomplete Based on the income that reported, it appears that the client is not eligible for the credit The income or other entries on the Form 8962 are inconsistent with information on the tax return Some Common Examples of Issues or Questions that May Arise The premium that was entered on the Form 8962 appears to be an annual amount, rather than monthly There are questions about entries on the Form 8962 that may be clarified by a review of the 1095 A IRS needs to review the Form 1095 A to verify the Marketplace coverage 26

27 Letter 12 C IRS is sending the letter because: The Health Insurance Marketplace notified IRS that they made advance payments of the premium tax credit to the client When the Health Insurance Marketplace pays advance payments of the premium tax credit on the client s behalf, the client must file Form 8962 to reconcile the advance payments to the actual amount of the Premium Tax Credit that they are eligible for based on the actual household income and family size Will the Client Receive any New Health Care Tax Forms in 2016 to Help Complete the Tax Returns? In early in 2017, the client will receive one or more forms providing information about the health care coverage that they had or were offered during the previous year The health care forms provide information that the client will need when they file the individual income tax return These new forms will be provided to the IRS by the entity that provides the form The new forms are: Form 1095 A, Health Insurance Marketplace Statement Form 1095 B, Health Coverage. Form 1095 C, Employer Provided Health Insurance Offer and Coverage Time for Coffee 27

28 Special Situations Employer Sponsored Coverage for Part of the Year If the client or another member of the tax household becomes unemployed or changes employers during the year, the affordability of coverage must be calculated for that individual separately for each employment period Similarly, if the required contribution for any employer plan changes during the year (such as when one plan year ends and another one starts during the year), test the affordability of the coverage separately for each period Employer Sponsored Coverage for Part of the Year Coverage under an employer plan is considered unaffordable for a part year period if the annualized premium for self only coverage (in the case of an employee) or family coverage (in the case of a related individual) under the plan for the part year period is more than 8.13% of the household income 28

29 Annualized Premium Worksheet Individuals Who are Incarcerated Individuals who are incarcerated are not eligible for coverage in a qualified health plan through a Marketplace However, these individuals may be applicable taxpayers and take the PTC for the coverage of individuals in their tax families who are eligible for coverage in a qualified health plan Married Taxpayers If the client is considered married for federal income tax purposes, they must file a joint return unless one of the two exceptions apply The client is not considered married for federal income tax purposes if they are divorced or legally separated according to the state law under a decree of divorce or separate maintenance 29

30 Exception 1 Certain Married Persons Living Apart The client files a separate return from the spouse due to meeting the requirements for Married persons who live apart under Head of Household Exception 2 Victim of Domestic Abuse or Spousal Abandonment If the client is a victim of domestic abuse or spousal abandonment, they can file a return as married filing separately and take the PTC if they meet all of the following They are living apart from the spouse at the time they file the 2016 tax return They are unable to file a joint return because they are a victim of domestic abuse or spousal abandonment In addition, don t forget to check the box on Form 8962 to certify that the client is a victim of domestic abuse or spousal abandonment Married Filing Separately If APTC was paid for coverage but the client cannot take the PTC because they are married filing a separate return and they do not qualify for an exception to the joint filing requirement, complete lines 1 through 5 of Form 8962 to figure the separate household income as a percentage of the Federal poverty line Complete lines 9 and 10 (and Part IV, if applicable) When completing line 11 or lines 12 through 23, complete only column (f) Then complete the rest of the form to determine how much you must repay 30

31 Form 8962 Annual and Monthly Contribution Amount Form

32 Part II Premium Tax Credit Claim and Reconciliation of Advance Payment of Premium Tax Credit Shared Allocation If an individual in the tax family was enrolled in a policy with an individual in another tax family and they are not taking the PTC, the taxpayer who is claiming the individual not in the tax family may agree to reconcile all APTC paid for the policy This is called a shared allocation Allocating Policy Amounts If the taxpayer is allocating amounts they must complete Part IV before the continuing with Form 8962 If the taxpayer wants to use the Alternative calculation for year of marriage, they must complete Part V 32

33 Form 8962 Parts IV and V Allocating Policy Amounts You need to allocate policy amounts (enrollment premiums, SLCSP premiums, and/or APTC) on the Form 1095 A between the tax family and another tax family if: The policy covered at least one individual in the tax family and at least one individual in another tax family, and the client received a Form 1095 A for the policy that does not accurately represent the members of the tax family who were enrolled in the policy Meaning that it either lists someone who is not in the tax family or does not list a member of the tax family who was enrolled in the policy or The other tax family received a Form 1095 A for the policy that includes a member of the client s tax family Allocating Policy Amounts A qualified health plan may have covered at least one individual in the tax family and one individual not in the tax family if: The client got divorced during the year The client is married but filing a separate return from the spouse The client or an individual in the tax family were enrolled in a qualified health plan by someone who is not part of the tax family (for example, the ex spouse enrolled a child whom the client is claiming as a dependent) or The client or an individual in the tax family enrolled someone not part of the tax family in a qualified health plan (for example, they enrolled a child whom the exspouse is claiming as a dependent) 33

34 Multiple Allocations in the Same Month If a qualified health plan covers individuals in the tax family and individuals in two or more other tax families for one or more months you will need to do Multiple Shared Policy Allocations Example One qualified health plan covers Bret, his spouse Paulette, and their daughter Sophia from January through August, and APTC is paid for the coverage of all three Bret and Paulette divorce on August 26 Bret and Paulette each file a tax return using a filing status of single Sophia is claimed as a dependent by her grandfather, Mike Bret, Paulette, and Mike must allocate the amounts from Form 1095 A for the months of January through August on their tax returns Amounts on Form 1095 A must be allocated among three tax families (Bret s, Paulette s, and Mike s) Multiple Allocations in Different Months The client may need to allocate policy amounts under a qualified health plan using different rules for different months if they had a change in circumstance Use Table 3 34

, they will allocate the amounts from the policy on")

35 Table 3 of the Form 8962 Instructions Example Jarrod enrolled himself, his spouse, Sally, and their two dependent children, Heidi and Matt, in a policy for 2016 purchased at the Marketplace APTC was paid on behalf of each The couple divorced on June 30, and Sally purchased different health insurance at the Marketplace for July through December in which she enrolls with Heidi and Matt Example Jarrod claims Heidi as a dependent on his tax return Sally claims Matt as a dependent on her tax return For the months Jarrod and Sally were married (January through June), they will allocate the amounts from the policy on line 30 35

36 Allocation Situation 1 The client and the former spouse must allocate policy amounts on the separate returns to figure the PTC if both of the following apply The client and the former spouse were married to each other at some point during 2016 but were no longer married to each other at the end of 2016 At any time during 2016, the client and the former spouse were enrolled in the same qualified health plan, or The client or an individual in the tax family was enrolled in the same policy as the former spouse or as an individual in the former spouse's tax family Allocation Situation 1 The client will allocate with the former spouse a percentage of the total enrollment premiums, the applicable SLCSP premium, and APTC for coverage under the plan during the months they were married You will find these amounts on the Form(s) 1095 A, Part III, columns A, B, and C, The client and the former spouse can allocate these amounts using any percentage they agree on from zero through one hundred percent, but you must allocate all amounts using the same percentage If they do not agree on a percentage, they must allocate 50% of each of these amounts to the client and 50% of each to the former spouse For the Months Divorced For the months Jarrod and Sally were divorced (July through December), they will allocate the amounts from the policy on line 30 36

37 Allocation Situation 4 Other Situations Where a Policy is Shared Between Two Tax Families Complete Part IV using the rules in this section if Allocation Situations 1 through 3 do not apply A taxpayer claiming the personal exemption for an individual or individuals (including the individual himself or herself) on behalf of whom APTC was paid may be able to take the PTC for the individual or individuals coverage, but in any event must reconcile the APTC for the individual or individuals' coverage Allocation Situation 4 Other Situations Where a Policy is Shared Between Two Tax Families If another taxpayer indicated to the Marketplace that he or she would claim the personal exemption for an individual the taxpayer is claiming, or The client indicated to the Marketplace that they would claim the personal exemption for an individual being claimed by another taxpayer The Form 1095 A sent by the Marketplace for the policy does not accurately reflect the members of the coverage family and the other taxpayer s coverage family In that case, the client and the other tax family must allocate the enrollment premiums, the APTC, and the applicable SLCSP premium Allocation Situation 4 Other Situations Where a Policy is Shared Between Two Tax Families The client and the other taxpayer may agree on any allocation percentage from zero through one hundred percent The clients may use the percentage they agreed on for every month for which this allocation rule applies, or they may agree on different percentages for different months However, they must use the same allocation percentage for all policy amounts (enrollment premiums, applicable SLCSP premiums, and APTC) in a month 37

38 Allocation Situation 4 Other Situations Where a Policy is Shared Between Two Tax Families If they cannot agree on an allocation percentage, the allocation percentage is equal to the number of individuals enrolled by one taxpayer for whom the other taxpayer claims a personal exemption for the tax year divided by the total number of individuals enrolled in the same policy as the individual The allocation percentage the client uses and that they put on line 30 of Form 8962 is the percentage of the policy amounts for the coverage that they will use to compute the PTC and reconcile APTC Alternative Calculation for Year of Marriage If the client got married during 2016 and APTC was paid for an individual in the tax family, they may want to use the alternative calculation for year of marriage, an optional calculation that may reduce the amount of excess APTC they would have to repay under the general rules Alternative Calculation for Year of Marriage 38

39 Alternative Calculation for Year of Marriage If the client elects to use the HCTC on Form 8885 for a coverage month, they cannot use the alternative calculation for year of marriage for the same coverage they received APTC If the client does not use the allocating policy amounts and is not using the alternative calculation for the year of marriage, check the No box and Line 9 and go to line 10 Alternative Calculation for Year of Marriage Alternative Calculation for Year of Marriage Confirm the entries for start and stop months These months should be inclusive of all months they are using a reduced monthly contribution Either the client or the spouse should have a start date that is the same as the first month the claim PTC on lines 12 through 23 For example, if the first monthly entry in Part II is on line 14 for March, either the client or the spouse should show 03 as the start date when completing Part V 39

40 Situations with the Form 1095 A Missing or Incorrect SLCSP Premium on Form 1095 A Generally, there are two situations where the SLCSP premium may not be accurately reflected on the Form 1095 A If either of these two situations apply, the client must determine the correct applicable SLCSP premium for every month If the correct applicable SLCSP premium is not the same for every month of 2016, check the No box and continue to lines The Two Situations in Which the SLCSP May not be Accurately Reflected on the Form 1095 A No APTC was paid for the coverage If no APTC was paid for the family member s coverage, the SLCSP premium reported in Part III, column B, lines 21 through 32 of Form 1095 A may be wrong, or may be left blank, or reported as 0 To determine the applicable SLCSP premium for each month the client must go to the Marketplace using tax tools in the search engine If the correct applicable SLCSP premium is not the same for all 12 months, check the No box on Line 10 of Form 8962 and continue to lines

41 The Two Situations in Which the SLCSP May not be Accurately Reflected on the Form 1095 A If the client has a change in circumstances during 2016 that they did not report to the Marketplace, the SLCSP premium reported in Part III, column B, lines 21 through 32 of Form 1095 A may be wrong Examples of Changes in Circumstances that May Affect the Applicable SLCSP Premium Include The client enrolled an individual newly added to the tax family during 2016 (for example, a newborn) An individual in the tax family was not enrolled in the qualified health plan for all of 2016 An individual in the coverage family became eligible for/or lost eligibility for employer coverage or other minimum essential coverage during 2016 Examples of Changes in Circumstances that May Affect the Applicable SLCSP Premium Include The client indicated to the Marketplace at enrollment that they would claim the personal exemption for an individual, but they are not do so An individual enrolled in the coverage died during 2016 but the client did not remove the individual from the policy The client moved during

42 Example 1 Mike and Susan enroll together in a qualified health plan through the Marketplace They did not have a change in circumstance during the year They receive a Form 1095 A, which reports $800 for the enrollment premiums in column A on lines 21 through 32 and $850 for the applicable SLCSP premium in column B on lines 21 through 32, for January through December They check the Yes box on Form 8962, line 10 and complete line 11 because for each of columns A and B there is an amount for all 12 months and the amounts did not change Form 8962 Line 10 Form 1095 A 42

43 Example 2 Same facts as Example 1, but starting on August 1, Mike is eligible for Medicare, and does not notify the Marketplace Because Mike is eligible for other minimum essential coverage, their coverage family changed starting in August As a result, Mike and Susan must update the applicable SLCSP premium reported in column B for the months of August through December (Form 1095 A, lines 28 through 32, column B) Since the SLCSP premium is not the same for every month of the year, Mike and Susan cannot use line 11 and must complete lines 12 through 23 on Form 8962 How Do We Update the SLCSP? Example 2 Mike and Susan check the No box on Form 8962, line 10 and complete lines 12 through 23 They determine that the applicable SLCSP premium for the coverage family of one (Susan) for August through December is $400 each month Mike and Susan enter $850 in Form 8962, lines 12 through 18, column (b), and $400 in lines 19 through 23, column (b) 43

")

44 Form 8962 Lee Example Lee receives a Form 1095 A, which reports in column A $1,000 on lines 21 through 32 for January through December and in column B $900 on lines 21 through 31 for January through November However, column B reports $650 on line 32 because an individual included in Lee's coverage family was eligible for minimum essential coverage (other than coverage in the individual market) for the entire month of December and Lee reported the change to the Marketplace Lee checks the No box on line 10 and completes lines 12 through 23 Form 1095 A 44

Note that in order to use Line 11 all amounts must be")

45 Form 8962 Line 11 Annual Totals Column A If you checked the Yes box on line 10 and the client is completing line 11, there is no need to complete lines 12 through 23 Enter the annual premiums from Form 1095 A, line 33, column A If there are multiple Forms 1095 A, add the amounts together and enter the total on Form 8962, line 11, column (a) Note that in order to use Line 11 all amounts must be the same for each entry in the columns This is the total of the enrollment premiums for the year, including the portion paid by APTC Once Line 11 is completed, skip to line 24 Line 11 Annual Totals Column B Enter the annual applicable SLCSP premium from Form 1095 A, line 33, in column B Combine if there are multiple Forms 1095 A However: If individuals in the coverage family enrolled in more than one policy in the same state they will receive a Form 1095 A for each policy The Marketplace should have entered the same SLCSP premium, which applies to all members of the coverage family, on each Form 1095 A Enter the amount from column B of only one Form 1095 A do not add the values from each form 45

46 Line 11 Annual Totals Column B However, if the client married in December of 2016 and the client and spouse, or individuals in the client s or spouse s tax family, were enrolled in separate qualified health plans, add the amounts from Form 1095 A, column B, for each plan (or plans) and enter the total If you got married in a month other than December, the applicable SLCSP premium may not be the same for every month Remember if the amounts are not the same for every month, do not use Line 11 Line 11 Annual Totals Column B Different States For individuals enrolled in qualified health plans in different states, add together the amounts from column B of the Forms 1095 A from each state and enter the total on Form 8962, line 11, column (b) Do You Need to Determine the Applicable SLCSP Premium? If during 2016, the coverage family changed or the client moved and they did not notify the Marketplace, or If no APTC was paid, the applicable SLCSP premium reported on the Form(s) 1095 A may be missing or incorrect This will require you to determine the correct SLCSP amount based on the facts of the client 46

47 tool/ HealthCare. Gov HealthCare. Gov 47

48 HealthCare. Gov HealthCare. Gov HealthCare. Gov 48

49 HealthCare. Gov HealthCare. Gov HealthCare. Gov 49

will be placed in Column ( c )")

50 HealthCare. Gov HealthCare. Gov Form 8962 Line 8A Enter the amount from line 8a of Form 8962 on Line 11 Column ( c ) The monthly amounts determined on Line 8(b) will be placed in Column ( c ) of line as needed 50

51 Form 8962 Form 8962, Column (d) and ( e ) A simple subtraction of the amount in column (c) from the amount in column (b) will need to be performed If the result is zero or less, enter 0 In Column (e), enter the lesser of the amount in column (a) or the amount in column (d) Form 8962, Column (d) and ( e ) 51

52 Not an Applicable Taxpayer 401% If the client is not an applicable taxpayer because the household income is over 400% of the Federal poverty line or they are using filing status married filing separately and does not meet one of the exceptions for that filing status they cannot take the PTC They must repay some or all of the APTC depending on the circumstances Form 8962 must be completed to determine the repayment if any Lines 12 through 23 Monthly Calculation If the client checked the No box on line 10 then they must complete lines 12 through 23 If they checked the Yes box on line 6 and they did not elect the alternative calculation for the year of marriage or they are using filing status married filing separately and no exception applies complete only Column (f), it is not necessary to complete the other columns Example Melissa and Ryan Melissa and Ryan were married at the beginning of 2016 They have no dependents They were enrolled under the same qualified health plan through a Marketplace from January through April The monthly APTC of $1,000 was paid for them, for a total of $4,000 They divorced April 10 Melissa enrolled in single coverage from May through December and a monthly APTC of $100 was paid for a total of $800 Ryan did not enroll in coverage Both incomes will result in amounts over 400% 52

53 Example Melissa and Ryan Example Melissa and Ryan Example Melissa and Ryan At the end of the year, Melissa or Ryan will receive a Form 1095 A reporting the coverage for January through April The recipient of the Form 1095 A should provide a copy to the non recipient Melissa will also receive a Form 1095 A reporting her coverage for May through December 53

54 Example Melissa and Ryan For 2016, Melissa's family size is one and her household income is over 400% of the Federal poverty line Ryan s family size is one and his household income is also over 400% of the Federal poverty line They must follow the rules under a shared allocation They agree to allocate the APTC 60% to Melissa and 40% to Ryan get it in writing The allocation applies only for the period of time Melissa and Ryan were married Example Melissa and Ryan The sum of the APTC allocated to Melissa is $2,400 ($1,000 x 0.6 x 4 months) Melissa must add this sum to her APTC of $800 for her single coverage She enters the monthly amounts on lines 12 23, column (f), and the total of $3,200 on Form 8962, lines 25, 27, and 29 Melissa enters the amount from line 29 on the applicable line of her tax return The sum of the APTC allocated to Ryan is $1,600 ($1,000 x 0.4 x 4 months) Ryan enters the monthly amounts on Form 8962, lines 12 23, column (f), and the total of $1,600 on lines 25, 27, and 29 Ryan enters the $1,600 from line 29 on the applicable line of his tax return Example Melissa 54

55 Example Ryan One More Step Part IV of Form 8962 One More Step Part IV of Form

56 Repayment and Caps Repayment Cap Situations Line 28 The excess APTC the client must repay may be limited If one of the situations applies, there is no repayment limitation and the client must repay the full amount shown on line 27 Repayment Cap Situations Line 28 The entry on Form 8962, line 5, is 401% The client is electing to take the HCTC on Form 8885 for the same coverage that they received APTC If either of these situations apply, leave line 28 blank and enter the amount from line 27 on line 29 56

57 Repayment Cap Situations Line 28 If neither situation applies enter the appropriate amount from Repayment Cap Table on line 28 If the client was married at the end of 2016 but is filing separately from the spouse, the repayment applies to the client and the spouse based on the household income reported on each return Repayment Cap Table Not Lawfully Present If APTC was paid for the coverage in a qualified health plan of an individual who was not lawfully present, the limitation does not apply to APTC paid for individuals who are not lawfully present 57

58 Lawfully/Non Lawfully Present A calculation will be necessary to figure the repayment limitation if an individual not lawfully present enrolled with one or more family members who are lawfully present for one or more months of the year Shared Allocations Specific Allocation Situations Taxpayers divorced or legally separated in 2016 Taxpayers married at year end but filing separate returns No APTC Other situations where a policy is shared between two tax families 58

59 Taxpayers Divorced or Legally Separated in 2016 The client and the former spouse must allocate policy amounts on their separate returns to figure the PTC if both of the following apply: The client and the former spouse were married to each other at some point during 2016 but are no longer married to each other at the end of 2016 If at any time during 2016, the client and the former spouse were enrolled in the same qualified health plan, or The client or an individual in the tax family (as shown on the tax return) were enrolled in the same policy as the former spouse or as an individual in the former spouse's tax family Taxpayers Divorced or Legally Separated in 2016 The client will allocate with the former spouse: A percentage of the total enrollment premiums The applicable SLCSP premium, and APTC for coverage under the plan during the months they were married The amounts can be found on Form(s) 1095 A, Part III, columns A, B, and C The client can allocate these amounts using any percentage they you agree on from zero through one hundred percent, but they must allocate all amounts using the same percentage If they cannot agree on a percentage, the client and the former spouse must allocate 50% of each of these amounts to the client and the former spouse Policy Amounts Allocated 100% If 100% of policy amounts are allocated to one spouse the client would check the Yes box on line 9 and complete Part IV by entering 100 in the appropriate box(es) for the allocation percentage If 0% of the policy amounts are allocated to the client, complete Part IV by entering 0 in the appropriate box(es) for the allocation percentage 59

60 Example: Keith and Stephanie Keith and Stephanie are married at the beginning of 2016 and have three children, Ben, Grace, and Max In January, Keith enrolls Ben, Grace, and Max in a qualified health plan beginning in January Keith and Stephanie divorce in July The children become eligible for and enroll in government sponsored health coverage and disenroll from the qualified health plan, effective August 1 First Keith will receive the Form 1095 A Stephanie will not get a copy of the Form 1095 A Example: Keith and Stephanie Keith claims Ben and Grace as dependents Stephanie claims Max as a dependent for 2016 Keith and Stephanie agree to allocate the policy amounts 33% to Stephanie and 67% to Keith 60

61 Example: Keith and Stephanie Therefore, 33% of the enrollment premium, the applicable SLCSP premiums, and APTC are allocated to Stephanie 67% of these amounts are allocated to Keith The allocation is only for the months Keith and Stephanie were married Stephanie s Form 8962 Part IV Keith s Form 8962 Part IV 61

62 Of Note If the client enrolled in coverage in the Marketplace with their spouse or another individual who is not in the tax family, the coverage family and applicable SLCSP premium may be different from the coverage family and applicable SLCSP premium the Marketplace used to determine the amount of the APTC If that is the case, the client must use a different applicable SLCSP premium to calculate the credit than the amount reported on Form 1095 A, Part III, column B Taxpayers Married at Year End but Filing Separate Returns If the client was married at the end of 2016 and they are filing a separate return from the spouse, and the client or an individual in the tax family was enrolled in the same policy as the spouse or an individual in the spouse s tax family at any time during 2016, the client and the spouse must equally allocate (50% to each spouse) certain policy amounts Married individuals who file separate returns are generally not eligible to take the PTC Taxpayers Married at Year End but Filing Separate Returns However, the client may be able to take the PTC if they file a return as of head of household or they file a return as married filing separately due to domestic abuse or spousal abandonment 62

63 Example No APTC If this allocation situation applies, the enrollment premiums are allocated in proportion to the SLCSP premium that applies to each taxpayer s coverage family If no APTC was paid for the policy, the Marketplace may not know which enrollees are in which tax family, and therefore may furnish only one Form 1095 A showing the total premium When this happens, the taxpayer receiving the Form 1095 A should provide a copy to the other taxpayers The client and the other party need to only complete column (e) on the appropriate line in Part IV to allocate the enrollment premiums to each family Example Gary Gary and his 25 year old nondependent son, Jim, enroll in a qualified health plan Jim has no dependents The policy covers Gary, Jim, and Gary s two young daughters who are Gary s dependents No APTC is paid for this policy The Form 1095 A furnished by the Marketplace to Gary shows an enrollment premium of $15,000 for the year and the SLCSP premium that applies to a coverage family that incorrectly includes Gary, Gary's daughters, and Jim (Some states may report 0 or leave column B blank on the Form 1095 A when no APTC is paid) $18,000 SLCSP 63

64 Example Gary Gary and Jim determine that the SLCSP premium that applies to Gary and his two dependents is $12,000 and the SLCSP premium that applies to Jim is $6,000 Gary and Jim are applicable taxpayers and each can take the PTC Gary computes his credit using his household income and family size of three, and the applicable SLCSP premium for a coverage family of three of $12,000 Jim computes his credit using his household income and family size of one, and the applicable SLCSP premium for a coverage family of one of $6,000 Example Gary Gary and Jim must allocate the enrollment premiums of $15,000 reported on the Form 1095 A, Part III, column A, in proportion to each taxpayer's applicable SLCSP premium as follows Gary s allocated enrollment premiums are $10,000 ($15,000 x $12,000/$18,000) (67% of the total premiums of $15,000) Jim s allocated enrollment premiums are $5,000 ($15,000 x $6,000/$18,000) (33% of the total premiums of $15,000) Form 8962, Part IV Gary enters Jim s social security number on line 30, column (b), and enters 0.67 in column (e) Jim enters Gary s social security number on line 30, column (b), and enters 0.33 in column (e) Gary and Jim leave line 30, columns (f) and (g), blank 64

on behalf of whom APTC was paid may be able to take the PTC for the individual or individuals coverage, but must reconcile the APTC for the individual or individuals' coverage Other")

65 Form 8962, Part IV Other Situations Where a Policy is Shared Between Two Tax Families A taxpayer claiming the personal exemption for an individual or individuals (including the individual himself or herself) on behalf of whom APTC was paid may be able to take the PTC for the individual or individuals coverage, but must reconcile the APTC for the individual or individuals' coverage Other Situations Where a Policy is Shared Between Two Tax Families If another taxpayer indicated to the Marketplace that he or she would claim the personal exemption for an individual the taxpayer is claiming, or Indicated to the Marketplace that the taxpayer would claim the personal exemption for an individual being claimed by another taxpayer The Form 1095 A sent by the Marketplace for the policy does not accurately reflect the members of the coverage family and the other taxpayer s coverage family If this occurs, the client and the other family must allocate the enrollment premiums, the APTC, and the applicable SLCSP premium 65

66 Other Situations Where a Policy is Shared Between Two Tax Families The client and the other taxpayer may agree on any allocation percentage from zero through one hundred percent They may use the percentage they agreed on for every month for which this allocation rule applies, or they may agree on different percentages for different months However, they must use the same allocation percentage for all policy amounts (enrollment premiums, applicable SLCSP premiums, and APTC) in a month Other Situations Where a Policy is Shared Between Two Tax Families If they cannot agree on an allocation percentage, the allocation percentage is equal to the number of individuals enrolled by one taxpayer for whom the other taxpayer claims a personal exemption for the tax year divided by the total number of individuals enrolled in the same policy as the individual The allocation percentage used and that will be placed on Line 30 of Form 8962 is the percentage of the policy amounts for the coverage that the client will use to compute the PTC and reconcile APTC Example Joe and Alice Joe and Alice have been divorced since January 2014 and have two children, Chris and Jane Joe enrolls himself, Chris, and Jane in a qualified health plan for 2016 The premium for the plan is $13,000 Based on a family size and coverage family of three and an applicable SLCSP premium of $12,000, Joe is approved for and receives APTC computed as follows: Joe s projected household income for 2016 is $59,370 (295% of the Federal poverty line for a family size of three) Joe s APTC for 2016 is $6414 ($12,000 applicable SLCSP premium less $5,586 contribution amount (household income $59,370 x applicable figure ) 66

67 Federal Poverty Level 48 Continuous States How Joe s Estimated Income Would Appear on Form 8962 with a Family of 3 Where Did the 295% Come From? 67

68 Example Joe and Alice Joe s actual household income for 2016 is $59,774 Remember Joe s family unit has changed from 3 to 2 Form 8962 Still a Family of 3 Actual Income Let s See How Joe s Form 8962 Changes Since he Cannot Claim Jane 68

69 Let s Look at Alice The Mom Jane lives with Alice for more than half of 2016 and Alice claims Jane as a dependent Joe and Alice agree to an allocation percentage of 20% to determine how policy amounts for the qualified health plan are for Jane s coverage Therefore, 20% of the enrollment premiums, APTC, and the applicable SLCSP premium are allocated to Alice and 80% are allocated to Joe Let s Look at Alice The Mom In computing PTC, Joe takes into account $10,400 of enrollment premiums ($13,000 x 0.80) Joe must reconcile $5,131 of APTC ($6,414 x 0.80) Joe s tax family for 2016 includes only Joe and Chris, and Joe s household income of $59,774 is 375% of the Federal poverty line for a family size of two Joe s applicable SLCSP premium for 2016 is $9,600 (the applicable SLCSP premium covering Joe, Chris, and Jane of $12,000, minus the amount allocated to Alice of $2,400 ($12,000 x 0.20)) Let s Look at Alice The Mom Joe s PTC for 2016 is $3,386 (the lesser of $3,386, the excess of Joe s applicable SLCSP premium of $9,600 (80% of the $12,00SLCSP) minus the contribution amount of $5,714 ($59,774 x ), and $10,400, 80% of Joe's enrollment premiums) Joe has excess APTC of $1,245 (the excess of the APTC of $5,131 (80% of the $6414 amount) over the PTC of $3,886) 69

70 Summary of the Form 8962 Part IV Exemptions 70

or to claim a coverage exemption on the tax")

71 Form 8965 Form 8965 Form 8965 Exemptions Individuals must have health care coverage, have a health coverage exemption, or make a shared responsibility payment with their tax return Form 8965 is used to report a coverage exemption granted by the Marketplace (also called the Exchange ) or to claim a coverage exemption on the tax return 71

72 Exemptions Exemptions Change As of September 1, 2016, the coverage exemptions for members of health care sharing ministries, members of Indian tribes, and those who are incarcerated are no longer granted by the Marketplace, except in Connecticut Taxpayers who have an ECN issued by the Marketplace for one or more of these three exemptions may report the ECN on a Form 8965 filed with their income tax return for 2016 Taxpayers who qualify for one or more of these exemptions but who do not have an ECN issued by the Marketplace may claim these exemptions on Part III of Form

with dependent child $16,650")

73 Penalties Chart Filing Requirement for 2016 Single $10,350 Head of household $13,350 Married filing jointly $20,700 Married filing separately $4,050 Qualifying widow(er) with dependent child $16,650 73

74 National Average Bronze Plan for 2016 Comparison Worksheet Form

75 Marketplace Opens CALT Website Tour of the CALT Website 75

76 Fall Tax Schools Though they are named the Farm and Urban Tax Schools the schools cover more than farm issues Common return issues for all kinds of returns are covered All kinds of business entities Problematic issues Sometimes we even get into to issues that you many encounter only once or twice a year or tax season The Tax Schools are a blend of diverse topics of interest to all tax professionals This year: New instructors with diverse backgrounds Your adventure awaits at Iowa State s Center for Agricultural Law and Taxation Farm and Urban Tax Schools 2016 November 2, 2016 to December 13, Locations in Iowa and Online Webinar Save the Date for the 2016 Annual Farm and Urban Income Tax Schools The program is intended for tax professionals and is designed to provide up to date training on current tax law and regulations November 2 3: Maquoketa November 7 8: Red Oak November 9 10: Sheldon November 14 15: Mason City November 17 18: Ottumwa November 21 22: Waterloo December 5 6: Denison December 12 13: Ames and Live Webinar Winter Webinars Tax Research with Limited Resources Miscellaneous Income New Developments Tax Update Form 8867 Due Diligence Learn about Coops Free webinar 76

77 Beginning Tax Preparers Class CALT is working on offering a basic class for NEW tax preparers this fall in October The week long webinar will cover the basics an individual needs to know such as: Requirement to file and Filing Status Dependents Itemized deductions Child and Dependent care Education Credits Other issues a first or second year preparer needs to know as well as a refresher for others who need to brush up on issues The class will be a week long or more and will be offered at a special rate The Scoop Throughout the filing season two Scoops will be held on Scoop Dates 8:00 8:30 am Central time 12:00 12:30 Central time This assists with accommodating our west coast practitioners The same information will be shared at both sessions You have the option of registering for whatever session suits your schedule node fieldseminar date/month Future Scoop Dates October 5, 2016 October 19, 2016 November 16, 2016 December 14, nodefield seminar date/month 77

78 The CALT Staff John D. Lawrence Interim Director Associate Dean, College of Agriculture & Life Sciences Extension Programs and Outreach Director, Agriculture & Natural Resources Extension 132 Curtiss Hall Iowa State University Ames, Iowa Kristine A. Tidgren Assistant Director E mail: ktidgren@iastate.edu Phone: (515) Fax: (515) The CALT Staff Kristy S. Maitre Tax Specialist E mail: ksmaitre@iastate.edu Phone: (515) Fax: (515) Tiffany L. Kayser Program Administrator E mail: tlkayser@iastate.edu Phone: (515) Fax: (515)

Instructions for Form 8962

2017 Instructions for Form 8962 Premium Tax Credit (PTC) Department of the Treasury Internal Revenue Service Purpose of Form Use Form 8962 to figure the amount of your premium tax credit (PTC) and reconcile

2017 Instructions for Form 8962 Premium Tax Credit (PTC) Department of the Treasury Internal Revenue Service Purpose of Form Use Form 8962 to figure the amount of your premium tax credit (PTC) and reconcile

Caution: DRAFT NOT FOR FILING

Caution: DRAFT NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information as a courtesy. Do not file draft forms. Also,

Caution: DRAFT NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information as a courtesy. Do not file draft forms. Also,

Instructions for Form 8962

2018 Instructions for Form 8962 Premium Tax Credit (PTC) Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Purpose of Form

2018 Instructions for Form 8962 Premium Tax Credit (PTC) Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Purpose of Form

Caution: DRAFT NOT FOR FILING

Caution: DRAFT NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information as a courtesy. Do not file draft forms. Also,

Caution: DRAFT NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information as a courtesy. Do not file draft forms. Also,

The Affordable Care Act and Taxes

The Affordable Care Act and Taxes ACA Reference Guide» ACA and Taxes > Quick Reference Guide 1 2 4 5 9 10 11 > Section 1 ACA Basics > Section 2 Coverage Exemptions > Section 3 Individual Shared Responsibility

The Affordable Care Act and Taxes ACA Reference Guide» ACA and Taxes > Quick Reference Guide 1 2 4 5 9 10 11 > Section 1 ACA Basics > Section 2 Coverage Exemptions > Section 3 Individual Shared Responsibility

CHAPTER 5: ADVANCE PREMIUM TAX CREDIT RECONCILIATION

CHAPTER 5: ADVANCE PREMIUM TAX CREDIT RECONCILIATION TABLE OF CONTENTS A. Advance Premium Tax Credit (APTC) Reconciliation Overview... 1 B. Option to Receive Premium Tax Credit in Advance... 2 1) Reconciling

CHAPTER 5: ADVANCE PREMIUM TAX CREDIT RECONCILIATION TABLE OF CONTENTS A. Advance Premium Tax Credit (APTC) Reconciliation Overview... 1 B. Option to Receive Premium Tax Credit in Advance... 2 1) Reconciling

Guidelines for Quality Reviewing ACA Issues

Attachment 1 Guidelines for Quality Reviewing ACA Issues Form 13614-C, Intake/Interview Sheet Is Form 13614-C complete? Every question is answered Yes or No? Unsure responses have been answered Yes or

Attachment 1 Guidelines for Quality Reviewing ACA Issues Form 13614-C, Intake/Interview Sheet Is Form 13614-C complete? Every question is answered Yes or No? Unsure responses have been answered Yes or

Cost and Coverage Implications of the ACA Medicaid Expansion: National and State by State Analysis

Cost and Coverage Implications of the ACA Medicaid Expansion: National and State by State Analysis Report Authors: John Holahan, Matthew Buettgens, Caitlin Carroll, and Stan Dorn Urban Institute November

Cost and Coverage Implications of the ACA Medicaid Expansion: National and State by State Analysis Report Authors: John Holahan, Matthew Buettgens, Caitlin Carroll, and Stan Dorn Urban Institute November

Presented by: Matt Turkstra

Presented by: Matt Turkstra 1 » What s happening in Ohio?» How is health insurance changing? Individual and Group Health Insurance» Important employer terms» Impact small businesses that do not offer insurance?

Presented by: Matt Turkstra 1 » What s happening in Ohio?» How is health insurance changing? Individual and Group Health Insurance» Important employer terms» Impact small businesses that do not offer insurance?

FEDERAL INCOME TAX IMPLICATONS OF THE ACA MANDATE FOR INDIVIDUAL TAXPAYERS

FEDERAL INCOME TAX IMPLICATONS OF THE ACA MANDATE FOR INDIVIDUAL TAXPAYERS Starting in 2014, the Patient Protection and Affordable Care Act (ACA) mandates that individuals carry minimum essential health

FEDERAL INCOME TAX IMPLICATONS OF THE ACA MANDATE FOR INDIVIDUAL TAXPAYERS Starting in 2014, the Patient Protection and Affordable Care Act (ACA) mandates that individuals carry minimum essential health

Patient Protection and. Affordable Care Act: The Impact on Employers

Patient Protection and Affordable Care Act: The Impact on Employers April 2013 Agenda Introductions Individual Mandate Healthcare Exchange Overview Impact on Employers Essential Health Benefits Fees &

Patient Protection and Affordable Care Act: The Impact on Employers April 2013 Agenda Introductions Individual Mandate Healthcare Exchange Overview Impact on Employers Essential Health Benefits Fees &

The Affordable Care Act (ACA)

") The Affordable Care Act (ACA) An Overview by the Kaiser Family Foundation NBC News Editorial Roundtable June 26, 2013 1. The Basics of the Affordable Care Act (ACA) Expanded Medicaid Coverage Starting

The Affordable Care Act (ACA) An Overview by the Kaiser Family Foundation NBC News Editorial Roundtable June 26, 2013 1. The Basics of the Affordable Care Act (ACA) Expanded Medicaid Coverage Starting

Older consumers and student loan debt by state

August 2017 Older consumers and student loan debt by state New data on the burden of student loan debt on older consumers In January, the Bureau published a snapshot of older consumers and student loan

August 2017 Older consumers and student loan debt by state New data on the burden of student loan debt on older consumers In January, the Bureau published a snapshot of older consumers and student loan

Obamacare in Pictures

Obamacare in Pictures VISUALIZING THE EFFECTS OF THE PATIENT PROTECTION AND AFFORDABLE CARE ACT Spring 2014 If you like your health care plan, can you really keep it? At least 4.7 million health care plans

Obamacare in Pictures VISUALIZING THE EFFECTS OF THE PATIENT PROTECTION AND AFFORDABLE CARE ACT Spring 2014 If you like your health care plan, can you really keep it? At least 4.7 million health care plans

The Impact of Health Reform s State Exchanges

The Impact of Health Reform s State Exchanges May 2, 2013 Orlando, Florida Presented by: Layna S. Cook 225-381-7083 lcook@bakerdonelson.com The Affordable Care Act The Patient Protection and Affordable

The Impact of Health Reform s State Exchanges May 2, 2013 Orlando, Florida Presented by: Layna S. Cook 225-381-7083 lcook@bakerdonelson.com The Affordable Care Act The Patient Protection and Affordable

Affordable Care Act: what tax directors need to know. 14 May 2013

Affordable Care Act: what tax directors need to know 14 May 2013 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young global llimited, each of which is a separate

Affordable Care Act: what tax directors need to know 14 May 2013 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young global llimited, each of which is a separate

SCHIP: Let the Discussions Begin

Figure 0 SCHIP: Let the Discussions Begin Diane Rowland, Sc.D. Executive Vice President, Henry J. Kaiser Family Foundation and Executive Director, Kaiser Commission on for Alliance for Health Reform February

Figure 0 SCHIP: Let the Discussions Begin Diane Rowland, Sc.D. Executive Vice President, Henry J. Kaiser Family Foundation and Executive Director, Kaiser Commission on for Alliance for Health Reform February

Name of Applicant Soc Sec # _ / / Marital Status (Circle One): Single Married Divorced Widow(er) Name of Spouse Date of Birth / / Soc Sec # _ / /

: Single Married Divorced Widow(er) Name of Spouse Date of Birth / / Soc Sec # _ / /") PLAN NUMBER 766570 20 IBEW LOCAL 102 SURETY FUND C/O I.E. SHAFFER & CO. 830 BEAR TAVERN RD 2 ND FLOOR PO BOX 1028 TRENTON NJ 08628-0230 PHONE (800)792-3666 FAX (609) 883-7560 Application for Benefits (Please

PLAN NUMBER 766570 20 IBEW LOCAL 102 SURETY FUND C/O I.E. SHAFFER & CO. 830 BEAR TAVERN RD 2 ND FLOOR PO BOX 1028 TRENTON NJ 08628-0230 PHONE (800)792-3666 FAX (609) 883-7560 Application for Benefits (Please

Alternative Paths to Medicaid Expansion

Alternative Paths to Medicaid Expansion Robin Rudowitz Kaiser Commission on Medicaid and the Uninsured Kaiser Family Foundation National Health Policy Forum March 28, 2014 Figure 1 The goal of the ACA

Alternative Paths to Medicaid Expansion Robin Rudowitz Kaiser Commission on Medicaid and the Uninsured Kaiser Family Foundation National Health Policy Forum March 28, 2014 Figure 1 The goal of the ACA

Property Tax Relief in New England

Property Tax Relief in New England January 23, 2015 Adam H. Langley Senior Research Analyst Lincoln Institute of Land Policy www.lincolninst.edu Property Tax as a % of Personal Income OK AL IN UT SD MS

Property Tax Relief in New England January 23, 2015 Adam H. Langley Senior Research Analyst Lincoln Institute of Land Policy www.lincolninst.edu Property Tax as a % of Personal Income OK AL IN UT SD MS

NOTICE OF FEDERAL AND STATE TAX INFORMATION FOR PSA PLAN PAYMENTS YOUR ROLLOVER OPTIONS

NOTICE OF FEDERAL AND STATE TAX INFORMATION FOR PSA PLAN PAYMENTS YOUR ROLLOVER OPTIONS Retain this Notice for Future Reference You are receiving this notice because all or a portion of a payment you are

NOTICE OF FEDERAL AND STATE TAX INFORMATION FOR PSA PLAN PAYMENTS YOUR ROLLOVER OPTIONS Retain this Notice for Future Reference You are receiving this notice because all or a portion of a payment you are

IRA Distribution Form

Use this form to request distributions from your IRA account and to close an IRA. Instructions 1. Complete the form and include any necessary supporting documents. 2. Sign and send us the completed form.

Use this form to request distributions from your IRA account and to close an IRA. Instructions 1. Complete the form and include any necessary supporting documents. 2. Sign and send us the completed form.

Obamacare in Pictures. Visualizing the Effects of the Patient Protection and Affordable Care Act

Visualizing the Effects of the Patient Protection and Affordable Care Act Fall 2012 expands dependence on government health care dumps millions into Medicaid and creates new federal subsidies for government-approved

Visualizing the Effects of the Patient Protection and Affordable Care Act Fall 2012 expands dependence on government health care dumps millions into Medicaid and creates new federal subsidies for government-approved

Medicaid Expansion and Section 1115 Waivers

Medicaid Expansion and Section 1115 Waivers Council of State Governments National Conference December 11, 2015 Figure 1 The goal of the ACA is to make coverage more available, more reliable, and more affordable.

Medicaid Expansion and Section 1115 Waivers Council of State Governments National Conference December 11, 2015 Figure 1 The goal of the ACA is to make coverage more available, more reliable, and more affordable.

The Medicaid Landscape

The Medicaid Landscape Robin Rudowitz Associate Director, Kaiser Commission on Medicaid and the Uninsured Kaiser Family Foundation Council of State Governments Washington, DC June 18, 2014 Figure 1 Medicaid

The Medicaid Landscape Robin Rudowitz Associate Director, Kaiser Commission on Medicaid and the Uninsured Kaiser Family Foundation Council of State Governments Washington, DC June 18, 2014 Figure 1 Medicaid

Request for Systematic Disbursement

Instructions Request for Systematic Disbursement ALAMEDA COUNTY DEFERRED COMPENSATION PLAN Please print using blue or black ink. Return this form to: Alameda County Treasurer s Office, Attn: DC Administration,

Instructions Request for Systematic Disbursement ALAMEDA COUNTY DEFERRED COMPENSATION PLAN Please print using blue or black ink. Return this form to: Alameda County Treasurer s Office, Attn: DC Administration,

Request for Disbursement

Instructions Request for Disbursement Deferred Salary Plan of the Electrical Industry Please print using blue or black ink. This request must be authorized by your Fund Office. Please forward this form

Instructions Request for Disbursement Deferred Salary Plan of the Electrical Industry Please print using blue or black ink. This request must be authorized by your Fund Office. Please forward this form

Distribution of Account Balance up to $5,000 under a 457 Plan

About You Plan number 3 0 0 4 1 1 Social Security number - - First name MI Last name Sub plan number 000001 State of Hawaii 000004 County of Maui 000002 County of Hawaii 000005 County of Hawaii Water District

About You Plan number 3 0 0 4 1 1 Social Security number - - First name MI Last name Sub plan number 000001 State of Hawaii 000004 County of Maui 000002 County of Hawaii 000005 County of Hawaii Water District

Request for Systematic Disbursement

Instructions About You Request for Systematic Disbursement NC 401(k) PLAN Please print using blue or black ink. Please send completed form to the following address or fax it to 1-866-439-8602. Questions?

Instructions About You Request for Systematic Disbursement NC 401(k) PLAN Please print using blue or black ink. Please send completed form to the following address or fax it to 1-866-439-8602. Questions?

Report of Termination/Request for Disbursement

Instructions Please print using blue or black ink. This request must be authorized by your employer. Please forward this form to your benefits/human resources office to complete the Your Plan Authorization

Instructions Please print using blue or black ink. This request must be authorized by your employer. Please forward this form to your benefits/human resources office to complete the Your Plan Authorization

PRODUCER ANNUITY SUITABILITY TRAINING REQUIREMENTS BY STATE As of September 11, 2017

PRODUCER ANNUITY SUITABILITY TRAINING REQUIREMENTS BY STATE As of September 11, 2017 This document provides a summary of the annuity training requirements that agents are required to complete for each

PRODUCER ANNUITY SUITABILITY TRAINING REQUIREMENTS BY STATE As of September 11, 2017 This document provides a summary of the annuity training requirements that agents are required to complete for each

Attention; Benefits/Human Resources office - Please send completed form to our address or fax number. Questions?

21 Request for Systematic Disbursement Vermont Deferred Compensation Plan Instructions Please print using blue or black ink. Please forward this form to your benefits/human resources office to complete

21 Request for Systematic Disbursement Vermont Deferred Compensation Plan Instructions Please print using blue or black ink. Please forward this form to your benefits/human resources office to complete

IBEW Local 716 Marital status. - - Married - spousal signature required*. First name MI Last name. City State ZIP code

21 Request for Systematic Disbursement IBEW Local Union No. 716 Retirement Plan Instructions Please print using blue or black ink. Please forward this form to your Fund office to complete the 'Your Plan

21 Request for Systematic Disbursement IBEW Local Union No. 716 Retirement Plan Instructions Please print using blue or black ink. Please forward this form to your Fund office to complete the 'Your Plan

Administrative handbook Aetna Funding Advantage SM

Quality health plans & benefits Healthier living Financial well-being Intelligent solutions Administrative handbook Aetna Funding Advantage SM For self-insured groups with less than 100 eligible employees

Quality health plans & benefits Healthier living Financial well-being Intelligent solutions Administrative handbook Aetna Funding Advantage SM For self-insured groups with less than 100 eligible employees

Robin Rudowitz, Associate Director, Kaiser Commission on Medicaid and the Uninsured The Henry J. Kaiser Family Foundation

Medicaid Overview Robin Rudowitz, Associate Director, Kaiser Commission on Medicaid and the Uninsured The Henry J. Kaiser Family Foundation Council of State Governments / Medicaid Leadership Policy Academy

Medicaid Overview Robin Rudowitz, Associate Director, Kaiser Commission on Medicaid and the Uninsured The Henry J. Kaiser Family Foundation Council of State Governments / Medicaid Leadership Policy Academy

Report of Termination/Request for Disbursement Plumbers Local Union No. 1 Employee 401(k) Savings Plan

Savings Plan") Instructions About You Please print using blue or black ink. Send completed form to the following address or fax it to 1-866-439-8602. If faxing, please keep original for your records. Prudential PO Box

Instructions About You Please print using blue or black ink. Send completed form to the following address or fax it to 1-866-439-8602. If faxing, please keep original for your records. Prudential PO Box

State Treatment of Social Security Treatment of Pension Income Other Income Tax Breaks Property Tax Breaks

State-By-State Tax Breaks for Seniors, 2016 State Treatment of Social Security Treatment of Pension Income Other Income Tax Breaks Property Tax Breaks AL Payments from defined benefit private plans are

State-By-State Tax Breaks for Seniors, 2016 State Treatment of Social Security Treatment of Pension Income Other Income Tax Breaks Property Tax Breaks AL Payments from defined benefit private plans are

THE TATITLEK CORPORATION 401(K) PLAN FINAL DISTRIBUTION FORM (907)

PLAN FINAL DISTRIBUTION FORM (907)") Return Form To: Human Resources Department 561 East 36 th Avenue Anchorage, AK 99503 Fax (907) 334-1981 THE TATITLEK CORPORATION 401(K) PLAN FINAL DISTRIBUTION FORM (907) 278-4000 Participant Information

Return Form To: Human Resources Department 561 East 36 th Avenue Anchorage, AK 99503 Fax (907) 334-1981 THE TATITLEK CORPORATION 401(K) PLAN FINAL DISTRIBUTION FORM (907) 278-4000 Participant Information

The Affordable Care Act

The Affordable Care Act What are the employer requirements and what is the current status? NCSL Health Summit Atlanta, Georgia August 11, 2013 Nancy Taylor taylorn@gtlaw.com 202.331.3133 GREENBERG TRAURIG,

The Affordable Care Act What are the employer requirements and what is the current status? NCSL Health Summit Atlanta, Georgia August 11, 2013 Nancy Taylor taylorn@gtlaw.com 202.331.3133 GREENBERG TRAURIG,

TCJA and the States Responding to SALT Limits

TCJA and the States Responding to SALT Limits Kim S. Rueben Tuesday, January 29, 2019 1 What does this mean for Individuals under TCJA About two-thirds of taxpayers will receive a tax cut with the largest

TCJA and the States Responding to SALT Limits Kim S. Rueben Tuesday, January 29, 2019 1 What does this mean for Individuals under TCJA About two-thirds of taxpayers will receive a tax cut with the largest

The State of Children s Health

Figure 0 The State of Children s Health Robin Rudowitz Principal Policy Analyst Kaiser Commission on NCSL Annual Meeting Boston, MA August 8, 2007 Figure 1 SCHIP Builds on Medicaid for Children s Coverage

Figure 0 The State of Children s Health Robin Rudowitz Principal Policy Analyst Kaiser Commission on NCSL Annual Meeting Boston, MA August 8, 2007 Figure 1 SCHIP Builds on Medicaid for Children s Coverage

Patient Protection & Affordable Care Act

Patient Protection & Affordable Care Act Joshua D. Goldberg National Association of Insurance Commissioners Symposium on Health Reform University of Iowa Public Policy Center July 20, 2010 Opportunities

Patient Protection & Affordable Care Act Joshua D. Goldberg National Association of Insurance Commissioners Symposium on Health Reform University of Iowa Public Policy Center July 20, 2010 Opportunities

2016 GEHA. dental. FEDVIP Plans. let life happen. gehadental.com

2016 GEHA dental FEDVIP Plans let life happen gehadental.com Smile, you re covered, with great benefits and a large national network. High maximum benefits $25,000 for High Option Growing network of dentists

2016 GEHA dental FEDVIP Plans let life happen gehadental.com Smile, you re covered, with great benefits and a large national network. High maximum benefits $25,000 for High Option Growing network of dentists

Premium Tax Credit (PTC)

") Department of the Treasury Internal Revenue Service Publication 974 Cat. No. 66452Q Premium Tax Credit (PTC) For use in preparing 2017 Returns Contents Future Developments... 1 Reminders... 2 Introduction...

Department of the Treasury Internal Revenue Service Publication 974 Cat. No. 66452Q Premium Tax Credit (PTC) For use in preparing 2017 Returns Contents Future Developments... 1 Reminders... 2 Introduction...

Presented by: Daniel J. Prescott Regional Senior Vice President