HKFRS/IFRS Update 11 May 2010

|

|

|

- Neil Cross

- 5 years ago

- Views:

Transcription

1 HKFRS/IFRS Update 11 May 2010 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) FCCA FCPA FHKIoD MSCA Nelson Consulting Limited 1 Effective for Year-End Selected new interpretations and amendments to HKFRSs Effective for periods beginning on/after Amendments to HKFRS 2 Vesting Conditions and Cancellations 1 Jan HKFRS 8 Operating Segments 1Jan Jan HKAS 1 (Revised) Presentation of Financial Statements 1 Jan HKAS 23 (Revised) Borrowing Costs 1 Jan Amendments to HKFRS 1 and HKAS 27 Cost of an Investment in 1 Jan a Subsidiary, Jointly Controlled Entity or Associate Amendments to HKAS 32 and HKAS 1 Puttable Financial 1 Jan Instruments and Obligations Arising on Liquidation HK(IFRIC) 13 Customer Loyalty Programmes 1 Jul HK(IFRIC) 15 Agreements for the Construction of Real Estate 1 Jan HK(IFRIC) 16 Hedges of a Net Investment in a Foreign Operation Annual improvements to HKFRSs 2008 HK(IFRIC) 18 Transfers of Assets from Customers Amendments to HKFRS 7 Improving Disclosure about Financial Instruments Amendments to HK(IFRIC) 9 and HKAS 39 Embedded Derivatives 1 Oct Jan Jul (trans. date) 1 Jan Ended on/after 30 Jun Nelson Consulting Limited Updated from HKICPA, HKFRS Update, 6 Nov

2 Effective for Year-End Selected new interpretations and amendments to HKFRSs HKFRS 1 (Revised) First-time Adoption of HKFRS Amendments to HKFRS 1 Additional Exemptions for First-time time Adopters Amendments to HKFRS 2 Share-based Payment Group Cashsettled Share-based Payment Transactions HKAS 27 (Revised) Consolidated and Separate Financial Statements HKFRS 3 (Revised) Business Combination Amendments to HKAS 39 Eligible Hedged Items HK(IFRIC) 17 Distributions of Non-cash Assets to Owners Annual Improvements to HKFRSs 2009 HK(IFRIC) Interpretation 19 Extinguishing Financial Liabilities with Equity Instruments HKFRS for Private Entities (or IFRS for SME) Amendments to HK Interpretation 4 Leases Determination of the Length of Lease Term in respect of Hong Kong Land Leases Effective for periods beginning on/after 1 Jul Jan Jan Jul Jul Jul Jul Jan (unless specified) 1 Jan Effective upon issue Not specified Nelson Consulting Limited Updated from HKICPA, HKFRS Update, 6 Nov Effective after Year-End Selected new interpretations and amendments to HKFRSs Amendments to HKAS 32 Classification of Rights Issues HKAS 24(Revised) Related Party Disclosures HKFRS 9 Financial Instruments Amendments to HK(IFRIC) 14 HKAS 19 The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction Amendment to HKFRS 1 First-time Adoption of Hong Kong Financial Reporting Standards Limited Exemption from Comparative HKFRS 7 Disclosures for First-time Adopters Effective for periods beginning on/after 1 Feb Jan Jan Jan Jul Nelson Consulting Limited Updated from HKICPA, HKFRS Update, 6 Nov

3 Today s Agenda Recap of Amendments to HKFRS effective from 2009/10 Update of Amendments to HKFRS effective for 2010/11 Update of Amendments to HKFRS effective after 2010/ Nelson Consulting Limited 5 Presentation of Financial Statements (HKAS 1 Revised in 2007) Nelson Consulting Limited 6 3

a statement of financial position as at the end of the period; b) a statement of comprehensive income for the period; c) a statement of")

4 Complete Set of Fin. Statements A complete set of financial statements comprises: a) a statement of financial position as at the end of the period; b) a statement of comprehensive income for the period; c) a statement of changes in equity for the period; d) a statement of cash flows for the period; e) notes, comprising a summary of significant accounting policies and other explanatory information; and f) a statement of financial position as at the beginning of the earliest comparative period when an entity applies an accounting policy retrospectively or makes a retrospective restatement of items in its financial statements, or when it reclassifies items in its financial statements. An entity may use titles for the statements other than those used in HKAS 1. Previously, we call it Balance Sheet Previously, we call it Income Statement 3 years balance sheets Nelson Consulting Limited 7 Complete Set of Fin. Statements Complete Set of Financial Statements Statement of Financial Position as at the end of the period Previous title or changes Previous title: Balance Sheet To use a single statement to present all items of income and expense Statement of Comprehensive Income for the period To use two statements to present all items of income and expense Income Statement for the period Statement of Comprehensive Income for the period No title change New statement Statement of Changes in Equity for the period Statement of Cash Flows for the period Notes A statement of financial position as at the beginning of the earliest comparative period, if required No title change (but restructured) Previous title: Cash Flow Statement No title change New requirement Nelson Consulting Limited Sourced from Intermediate Financial Reporting (2009) by Nelson Lam and Peter Lau 8 4

5 Changes in Equity During a Period Non-owner changes Owner changes Changes in equity in a period Components of profit or loss Components of other comprehensive income Components of owner changes in equity HKAS 1 requires that The non-owner changes in equity during a period are further separated into two categories: 1. Components of profit or loss ; and 2. Components of other comprehensive income. All owner changes in equity must be presented separately from non-owner changes in equity and presented in the statement of changes in equity Nelson Consulting Limited 9 Changes in Equity During a Period Changes in equity in a period Two-Statement Approach Single Statement Approach Non-owner changes Components of profit or loss Components of other comprehensive income HKAS 1 revised in requires an entity to present such non-owner changes in equity in a period in the statement of comprehensive income by using either: 1. Single statement approach present all items of income and expense recognised in a period in a single statement of comprehensive income, or 2. Two-statement approach present all items of income and expense recognised in a period in 2 statements: a. a statement displaying components of profit or loss (i.e. a separate income statement) and b. a second statement beginning with profit or loss and displaying components of other comprehensive income (i.e. a statement of comprehensive income) Nelson Consulting Limited 10 5

6 Changes in Equity During a Period Changes in equity in a period Two-Statement Approach Single Statement Approach Before amendment Non-owner changes Owner changes Components of profit or loss Components of other comprehensive income Components of owner changes in equity Income statement Statement of comprehensive income Statement of changes in equity Statement of Comprehensive income Statement of changes in equity Income Statement Statement of changes in equity Nelson Consulting Limited 11 Statement of Comprehensive Income Other comprehensive income Comprises items of income and expense (including reclassification adjustments) that are not recognised in profit or loss as required or permitted by other HKFRSs. Components of other comprehensive income Nelson Consulting Limited 12 6

7 Statement of Comprehensive Income Example The components of other comprehensive income include: 1. changes in revaluation surplus recognised in accordance with HKAS 16 Property, Plant and Equipment; 2. changes in revaluation surplus recognised in accordance with HKAS 38 Intangible Assets; 3. actuarial gains and losses on defined benefit plans recognised in accordance with HKAS 19 Employee Benefits; Components of 4. gains and other losses arising from translating the financial statements of a foreign comprehensive operation in accordance with HKAS 21 The Effects of Changes in Foreign Exchange income Rates; 5. gains and losses on remeasuring available-for-sale (AFS) financial assets in accordance with HKAS 39 Financial Instruments: Recognition and Measurement (amended by HKFRS 9 and the category of AFS is deleted with a new category of fair value through other comprehensive income); and 6. the effective portion of gains and losses on hedging instruments in a cash flow hedge recognised in accordance with HKAS Nelson Consulting Limited Sourced from Intermediate Financial Reporting (2009) by Nelson Lam and Peter Lau 13 Statement of Comprehensive Income Components of other comprehensive income Other comprehensive income their components classified by nature to be reported in the statement of comprehensive income and to be presented either: 1. net of related tax effects, or 2. before related tax effects with one amount shown for the aggregate amount of income tax relating to those components. the amount of income tax relating to each component, including reclassification adjustments, either 1. in the statement of comprehensive income or 2. in the notes Nelson Consulting Limited 14 7

8 Statement of Comprehensive Income Components of other comprehensive income Other comprehensive income also comprises reclassification adjustments. Reclassification adjustments are defined as: amounts reclassified to profit or loss in the current period that were recognised in other comprehensive income in the current or previous periods. An entity is required to disclose reclassification adjustments relating to components of other comprehensive income either: in the statement of comprehensive income, or in the notes (then presents the components of other comprehensive income after any related reclassification adjustments in the statement of comprehensive income) Nelson Consulting Limited 15 Statement of Comprehensive Income Example Reclassification adjustments arise, for example: 1. on disposal of a foreign operation (see HKAS 21); 2. on derecognition of available-for-sale financial assets in accordance with HKAS 39 (amended by HKFRS 9 & no reclassification adjustment then); and 3. when a hedged forecast transaction affects profit or loss in accordance with HKAS 39 in relation to cash flow hedges. Reclassification Components adjustments of do not arise on: 1. changes in other revaluation surplus recognised in accordance with HKAS 16 or comprehensive 2. changes in revaluation surplus recognised in accordance with HKAS 38; or income 3. actuarial gains and losses on defined benefit plans recognised in accordance with HKAS 19. These two components are recognised in other comprehensive income and are not reclassified to profit or loss in subsequent periods. Changes in revaluation surplus may be transferred to retained earnings in subsequent periods as the asset is used or when it is derecognised. Actuarial gains and losses are reported in retained earnings in the period that they are recognised as other comprehensive income Nelson Consulting Limited 16 8

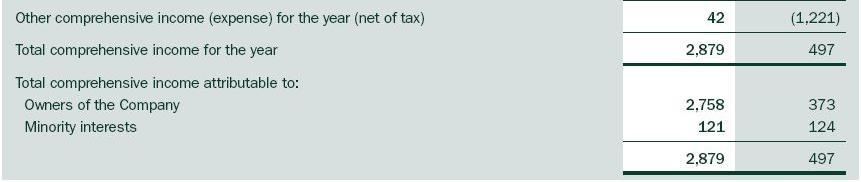

9 Statement of Comprehensive Income Case Nelson Consulting Limited 17 Statement of Comprehensive Income Case Nelson Consulting Limited 18 9

10 Statement of Comprehensive Income Case Consolidated statement of comprehensive income Nelson Consulting Limited 19 Statement of Comprehensive Income Case Consolidated Statement of Comprehensive Income Nelson Consulting Limited 20 10

11 Statement of Comprehensive Income Case Consolidated Statement of Comprehensive Income Nelson Consulting Limited 21 Improvement to HKFRSs Nelson Consulting Limited 22 11

12 Introduction Annual Improvement Project A vehicle for making non-urgent but necessary amendments to IFRS (and consequentially HKFRSs) Introduced by the IASB in 2007 and issued each year 2008 Annual Improvement Project is the first one The project has two parts: Part I contains amendments that result in accounting changes for presentation, recognition or measurement purposes, with the IASB s rationale included in related Bases for Conclusions. Part II contains amendments that are terminology or editorial changes only, which the IASB expects to have no or minimal effect on accounting Project has 24 Amendments to 15 HKFRSs 11 Amendments to 9 HKFRSs Nelson Consulting Limited 23 Part I: Summary HKFRS 5 Non-current Assets Held for Sale and Discontinued Operations HKAS 1 Presentation of Financial Statements HKAS 16 Property, Plant and Equipment HKAS 19 Employee Benefits HKAS 20 Accounting for Government Grants and Disclosure of Government Assistance HKAS 23 Borrowing Costs HKAS 27 Consolidated and Separate Financial Statements HKAS 28 Investments in Associates and HKAS 31 Interests in Joint Ventures HKAS 29 Financial i Reporting in Hyperinflationary Economies HKAS 36 Impairment of Assets HKAS 38 Intangible Assets HKAS 39 Financial Instruments: Recognition and Measurement HKAS 40 Investment Property HKAS 41 Agriculture Nelson Consulting Limited 24 12

13 Amendments to HKAS 1 HKAS 1 Presentation of Financial Statements (as revised in 2007) Previously, some considered that HKAS 1.71 implied that financial liabilities classified as held for trading in accordance with HKAS 39 Financial Instruments: Recognition and Measurement are always required to be presented as current. The current amendment clarifies that : The held for trading category in HKAS 39.9 is for measurement purposes and includes financial assets and liabilities that may not be held primarily for trading purposes. In consequence, such financial assets and liabilities that may not be held primarily for trading purposes should be presented as current or non-current on the basis of its settlement date. IASB thus removed the identified inconsistency by amending examples of current liabilities in HKAS The IASB also amended HKAS 1.68 in respect of current assets to remove a similar inconsistency. Affect presentation only Nelson Consulting Limited 25 Amendments to HKAS 1 Example A financial liability that is not held for trading purposes, such as a derivative that is not a financial guarantee contract or a designated hedging instrument, should be presented as current or non-current on the basis of its settlement date. For example, derivatives that have a maturity of more than twelve months and are expected to be held for more than twelve months after the reporting period should be presented as non-current assets or liabilities Nelson Consulting Limited 26 13

14 Amendments to HKAS 1 Case Annual report 2009 states that Derivative financial assets and liabilities were previously classified as current assets and current liabilities. However, with the adoption of HKAS 1 (revised), derivative financial instruments that are not expected to be realised within 12 months after the reporting period are classified as non-current assets or non-current liabilities. The effects of the reclassification of derivative financial instruments as at 31st December for 2007 to 2009 are as follows: HK$M HK$M HK$M Increase in other long-term receivables & investments 1,891 1,862 1,600 Increase in long-term payables 843 4,325 1,222 Decrease in trade, other receivables & other assets 1,891 1,365 1,548 Decrease in trade and other payables 843 3,828 1, Nelson Consulting Limited 27 Amendments to HKAS 16 HKAS 16 Property, Plant and Equipment Gain (on derecognition of PPE) shall not be classified as revenue. (HKAS 16.68) 68) Amendment introduces HKAS 16.68A that: However, an entity that, in the course of its ordinary activities, routinely sells items of PPE that it has held for rental to others shall transfer such assets to inventories at their carrying amount when they cease to be rented and become held for sale. The proceeds from the sale of such assets shall be recognised as revenue in accordance with HKAS 18 Revenue. HKFRS 5 does not apply when assets that are held for sale in the ordinary course of business are transferred to inventories. In some industries, entities are in the business of renting and subsequently selling the same assets, for example, car rental company Nelson Consulting Limited 28 14

15 Amendments to HKAS 16 Effective Date An entity shall apply those amendments for annual periods beginning on or after 1 January Earlier application is permitted. If an entity applies the amendments for an earlier period it shall disclose that fact and at the same time apply the related amendments to HKAS 7 Statement of Cash Flows. No specific transition stated Imply Retrospectively Comparatives should be reclassified Consistent with HKAS 16.68A: the cash receipts from rents and subsequent sales of such assets are also cash flows from operating activities Nelson Consulting Limited 29 Amendments to HKAS 20 HKAS 20 Accounting for Government Grants and Disclosure of Government Assistance Previously, HKAS states that loans at nil or low interest rates are a form of government assistance, but the benefit is not quantified by the imputation of interest. HKAS is now deleted and HKAS 20.10A is added as follows: The benefit of a government loan at a below-market rate of interest is treated as a government grant. The loan shall be recognised and measured in accordance with HKAS 39 Financial Instruments: Recognition and Measurement Nelson Consulting Limited 30 15

16 Amendments to HKAS 20 Using valuation techniques, e.g. discounting method HKAS 20 Accounting for Government Grants and Disclosure of Government Assistance HKAS 20.10A is added as follows: The benefit of the below-market rate of interest shall be measured as the difference between the initial carrying value of the loan determined in accordance with HKAS 39 and the proceeds received. The benefit is accounted for in accordance with HKAS 20. The entity shall consider the conditions and obligations that have been, or must be, met when identifying the costs for which the benefit of the loan is intended to compensate Nelson Consulting Limited 31 Amendments to HKAS 20 Effective Date An entity shall apply those amendments prospectively to government loans received in periods beginning on or after 1 January Earlier application is permitted. If an entity applies the amendments for an earlier period it shall disclose that fact. Apply Prospectively Nelson Consulting Limited 32 16

17 Amendments to HKAS 38 HKAS 38 Intangible Assets HKAS is amended as: In some cases, expenditure is incurred to provide future economic benefits to an entity, but no intangible asset or other asset is acquired or created that can be recognised. In the cases of the supply of goods, the entity recognises such expenditure as an expense when it has a right to access those goods. In the case of the supply of services, the entity recognises the expenditure as an expense when it receives the services. Previously, an entity recognises expense when it is incurred New requirements Implication: An entity might have got the right, for example television advertisement, but not yet broadcasted it Nelson Consulting Limited 33 Amendments to HKAS 38 HKAS 38 Intangible Assets Specific example is given in HKAS 38.69(c) Other examples of expenditure that t is recognised as an expense when it is incurred include: (c) expenditure on advertising and promotional activities (including mail order catalogues). Implication: An entity might have to recognise the expense when the catalogues are printed and received (but not yet delivered or mailed to the customers) Nelson Consulting Limited 34 17

18 Amendments to HKAS 40 HKAS 40 Investment Property The following property is added as an example of investment property: Property that is being constructed or developed for future use as investment property (HKAS 40.8) Previously, such property is accounted for in accordance with HKAS 16. To align with this scope amendment, HKAS and 53 are amended to extend the fair value model to such property Nelson Consulting Limited 35 Amendments to HKAS 40 HKAS 40 Investment Property HKAS is added with: If an entity determines that the fair value of an investment property under construction is not reliably determinable but expects the fair value of the property to be reliably determinable when construction is complete, it shall measure that investment property under construction at cost until either its fair value becomes reliably determinable or construction is completed (whichever is earlier). If an entity determines that the fair value of an investment property (other than an investment property under construction) is not reliably determinable on a continuing basis, the entity shall measure that investment property using the cost model in HKAS Nelson Consulting Limited 36 18

19 Amendments to HKAS 40 HKAS 40 Investment Property HKAS 40.53A and 53B are also added: Once an entity becomes able to measure reliably the fair value of an investment property under construction that has previously been measured at cost, it shall measure that property at its fair value. Once construction of that property is complete, it is presumed that fair value can be measured reliably... The presumption that the fair value of investment property under construction can be measured reliably can be rebutted only on initial recognition. An entity that has measured an item of investment property under construction at fair value may not conclude that the fair value of the completed investment property cannot be determined reliably Nelson Consulting Limited 37 Improving Disclosures about Financial Instruments (Amendments to HKFRS 7) Nelson Consulting Limited 38 19

20 Amendments to HKFRS 7 in 03/2009 The aim of the amendments was to enhance disclosures about fair value and liquidity risk SFAS 157 of US FASB requires disclosures that are based on a three-level fair value hierarchy for the inputs used in valuation techniques to measure fair value. IASB concluded that such a hierarchy would improve comparability between entities about the effects of fair value measurements as well as increase the convergence of IFRSs and US GAAP. to require disclosures for financial instruments on the basis of a fair value hierarchy Nelson Consulting Limited Fair Value Disclosure If there has been a change in valuation technique, the entity shall disclose that change and the reasons for making it. A fair value hierarchy for disclosure is also required: classify fair value measurements using a fair value hierarchy that reflects the significance of the inputs used in making the measurements Nelson Consulting Limited 40 20

21 1. Fair Value Disclosure The fair value hierarchy shall have the following levels: a. quoted prices (unadjusted) d) in active markets for identical assets or liabilities (Level 1); b. inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly (i.e. as prices) or indirectly (i.e. derived from prices) (Level 2); and c. inputs for the asset or liability that are not based on observable bl market data (unobservable bl inputs) (Level 3) Nelson Consulting Limited Fair Value Disclosure The level in the fair value hierarchy within which the fair value measurement is categorised in its entirety shall be determined on the basis of the lowest level input that is significant to the fair value measurement in its entirety. For this purpose, the significance of an input is assessed against the fair value measurement in its entirety. If a fair value measurement uses observable inputs that require significant adjustment based on unobservable inputs, that measurement is a Level 3 measurement. Assessing the significance of a particular input to the fair value measurement in its entirety requires judgement, considering factors specific to the asset or liability Nelson Consulting Limited 42 21

22 1. Fair Value Disclosure For fair value measurements recognised in the statement of financial position an entity shall disclose for each class of financial instruments: 1. the level in the fair value hierarchy 2. any significant transfers between Level 1 and Level 2 of the fair value hierarchy (with other details) 3. Further details for Level 3. An entity shall present the quantitative disclosures as required above in tabular format unless another format is more appropriate Nelson Consulting Limited Fair Value Disclosure Further details for Level 3: 1. total gains or losses for the period recognised in profit or loss, and a description of where they are presented in the statement of comprehensive income or the separate income statement (if presented) 2. total gains or losses recognised in other comprehensive income 3. purchases, sales, issues and settlements (each type of movement disclosed separately) 4. transfers into or out of Level 3 (e.g. transfers attributable to changes in the observability of market data) and the reasons for those transfers. (If significant, separate transfers into and out of Level 3) 5. the fact and the effect of changes (for the inputs to assumptions if their changes affect fair value significantly) Nelson Consulting Limited 44 22

23 1. Fair Value Disclosure Case Annual report Nelson Consulting Limited Fair Value Disclosure Case Annual report Nelson Consulting Limited 46 23

Quoted prices (unadjusted) in active markets for identical")

24 1. Fair Value Disclosure Case Annual report 2009 Effective from 1 January 2009, the Group adopted the amendment to HKFRS 7 for financial instruments that are measured in the statement of financial position at fair value, which requires disclosure of fair value measurements by level of the following fair value measurement hierarchy: a) Quoted prices (unadjusted) in active markets for identical assets or liabilities (level 1); b) Inputs other than quoted prices included within level 1 that are observable for the asset or liability, either directly (that is, as prices) or indirectly (that is, derived from prices) (level 2); and c) Inputs for the asset or liability that are not based on observable market data (that is, unobservable inputs) (level 3). As at 31 December 2009, the fair value measurement of the Group s financial assets available-for-sale financial assets is classified in level Nelson Consulting Limited Liquidity Risk Disclosure An entity shall disclose: a. a maturity analysis for non-derivative financial liabilities (including issued financial i guarantee contracts) t that t shows the remaining contractual maturities; b. a maturity analysis for derivative financial liabilities. The maturity analysis shall include the remaining contractual maturities for those derivative financial liabilities for which contractual maturities are essential for an understanding of the timing of the cash flows. For example, this would be the case for: i. an interest t rate swap with a remaining i maturity of five years in a cash flow hedge of a variable rate financial asset or liability. ii. all loan commitments. c. a description of how it manages the liquidity risk inherent in (a) and (b) Nelson Consulting Limited 48 24

25 HKFRS 7 Amendments Effective Date An entity shall apply those amendments for annual periods beginning on or after 1 January In the first year of application, an entity need not provide comparative information for the disclosures required by the amendments. Earlier application is permitted. If an entity applies the amendments for an earlier period, it shall disclose that fact Nelson Consulting Limited 49 Today s Agenda Update of Amendments to HKFRS effective for 2010/ Nelson Consulting Limited 50 25

26 Effective for Year-End Selected new interpretations and amendments to HKFRSs HKFRS 1 (Revised) First-time Adoption of HKFRS Amendments to HKFRS 1 Additional Exemptions for First-time time Adopters Amendments to HKFRS 2 Share-based Payment Group Cashsettled Share-based Payment Transactions HKAS 27 (Revised) Consolidated and Separate Financial Statements HKFRS 3 (Revised) Business Combination Amendments to HKAS 39 Eligible Hedged Items HK(IFRIC) 17 Distributions of Non-cash Assets to Owners Annual Improvements to HKFRSs 2009 HK(IFRIC) Interpretation 19 Extinguishing Financial Liabilities with Equity Instruments HKFRS for Private Entities (or IFRS for SME) Amendments to HK Interpretation 4 Leases Determination of the Length of Lease Term in respect of Hong Kong Land Leases Effective for periods beginning on/after 1 Jul Jan Jan Jul Jul Jul Jul Jan (unless specified) 1 Jan Effective upon issue Not specified Nelson Consulting Limited Updated from HKICPA, HKFRS Update, 6 Nov Consolidated Financial Statements (HKAS 27 Revised in 2008) Nelson Consulting Limited 52 26

27 HKAS 27 (Revised in 2008) Scope and definitions Presentation of consolidated financial statements Scope of consolidated financial statements Consolidation procedures Significant changes Loss of control New section Accounting in separate financial statements Nelson Consulting Limited 53 Consolidation Procedures Consolidation procedures are similar to previous standard, but Minority interests renamed as non-controlling interests, which is the equity in a subsidiary not attributable, directly or indirectly, to a parent Nelson Consulting Limited 54 27

28 Consolidation Procedures Non-controlling Interests Profit or loss and each component of other comprehensive income are attributed t to the owners of the parent and to the non-controlling interests. Total comprehensive income is attributed to the owners of the parent and to the non-controlling interests even if this results in the non-controlling interests Amended d having a deficit balance Nelson Consulting Limited 55 Consolidation Procedures Most critical Changes in a parent s ownership interest in a subsidiary that do not result in a loss of control are accounted for as equity transactions (i.e. transactions with owners in their capacity as owners) i.e. no gain or loss on disposal of interests in subsidiary can be recognised in profit or loss if the subsidiary is still a subsidiary Nelson Consulting Limited 56 28

29 Consolidation Procedures Example Entity A holds 80% of Entity X since its incorporation and their financial statements are set out below: Consol A X pre-change Disposed of 20% interest at $50 Property, plant & equipment 3,500 2,000 Interest in subsidiary 80 - Net current liabilities (1,000) (2,600) Net assets 2,580 (600) 5,500 - (3,600) 1,900 Share capital (200) (100) Reserves (2,380) 700 (2,580) 600 Non-controlling interests (Assume fair value = carrying amount) (200) (1,820) (2,020) 120 (1,900) Nelson Consulting Limited 57 Consolidation Procedures Example Entity A holds 80% of Entity X since its incorporation and their financial statements are set out below: Consol A X pre-change In such circumstances the carrying amounts of the Property, plant & equipment 3,500 2,000 5,500 controlling and non-controlling interests shall be adjusted Interest in subsidiary to reflect the changes in their relative interests in the Net current liabilities (1,000) (2,600) (3,600) subsidiary. Net Any assets difference between 2,580 (600) 1,900 the amount by which the non-controlling interests are adjusted d and Share the capital fair value of the consideration (200) paid (100) or received (200) Reserves (2,380) 700 (1,820) shall be recognised directly in equity and attributed to the (2,580) 600 (2,020) owners of the parent. Non-controlling interests (Assume fair value = carrying amount) 120 (1,900) Disposed of 20% interest at $50 NCI to be adjusted d (120) Consideration 50 Difference to equity Nelson Consulting Limited 58 29

30 Consolidation Procedures Example Entity A holds 80% of Entity X since its incorporation and their financial statements are set out below: Consol A X pre-change Disposed of 20% interest at $50 Consol. Dr/(Cr) after change Property, plant & equipment 3,500 2,000 Interest in subsidiary 80 - Net current liabilities (1,000) (2,600) 5,500 - (3,600) 50 5,500 - (3,550) Net assets 2,580 (600) 1,900 1,950 Share capital (200) (100) Reserves (2,380) 700 (2,580) 600 (200) (1,820) (2,020) (170) (200) (1,990) (2,190) Non-controlling interests (Assume fair value = carrying amount) 120 (1,900) (1,950) Nelson Consulting Limited 59 Loss of Control Specific requirements introduced when a parent loses control of a subsidiary: If a parent loses control of a subsidiary, it: a) derecognises the assets (including any goodwill) and liabilities of the subsidiary at their carrying amounts at the date when control is lost; b) derecognises the carrying amount of any non-controlling interests in the former subsidiary at the date when control is lost (including any components of other comprehensive income attributable to them); c) recognises: i) the fair value of the consideration received, if any, from the transaction, event or circumstances that resulted in the loss of control; and ii) if the transaction that resulted in the loss of control involves a distribution of shares of the subsidiary to owners in their capacity as owners, that distribution; Nelson Consulting Limited 60 30

31 Loss of Control Specific requirements introduced when a parent loses control of a subsidiary: If a parent loses control of a subsidiary, it: d) recognises any investment retained in the former subsidiary at its fair value at the date when control is lost; e) reclassifies to profit or loss, or transfers directly to retained earnings if required in accordance with other HKFRSs, the amounts identified in HKAS (discussed in next slide); and f) recognises any resulting difference as a gain or loss in profit or loss attributable to the parent Nelson Consulting Limited 61 Loss of Control If a parent loses control of a subsidiary, the parent shall account for all amounts recognised in other comprehensive income in relation to that subsidiary on the same basis as would be required if the parent had directly disposed of the related assets or liabilities. Therefore, if a gain or loss previously recognised in other comprehensive income would be reclassified to profit or loss on the disposal of the related assets or liabilities, the parent reclassifies the gain or loss from equity to profit or loss (as a reclassification adjustment) when it loses control of the subsidiary Nelson Consulting Limited 62 31

32 Loss of Control Example Think about 2 different cases with similar figures: HK$ Sub. A Sub. B Sale proceeds Carrying amount of the subsidiary s net assets in consolidated financial statements Anything recognised in profit or loss? What is the further information you have to ask? Nelson Consulting Limited 63 Loss of Control Example What if Think about 2 different cases with similar figures: HK$ Sub. A Sub. B Sale proceeds Carrying amount of the subsidiary s net assets in consolidated financial statements Representing: - Revalued amount of available-for-sale Revalued amount of PPE 100 Revaluation reserves Anything recognised in profit or loss? Nelson Consulting Limited 64 32

33 Loss of Control A parent loses control of a subsidiary and the subsidiary has the following assets: The subsidiary has available-forsale financial assets The subsidiary has property, plant and equipment with revaluation surplus previously recognised in other comprehensive income Example The parent shall reclassify to profit or loss the gain or loss previously recognised in other comprehensive income in relation to those assets. The parent transfers the revaluation surplus directly to retained earnings when it loses control of the subsidiary since the revaluation surplus would be transferred directly to retained earnings on the disposal of the asset Nelson Consulting Limited 65 Loss of Control Example What if Think about 2 different cases with similar figures: HK$ Sub. A Sub. B Sale proceeds Carrying amount of the subsidiary s net assets in consolidated financial statements Representing: - Revalued amount of available-for-sale Revalued amount of PPE 100 Revaluation reserves Revaluation reserves relating to availablefor-sale reclassified to profit or loss Revaluation reserves relating to PPE transferred directly to retained earnings Nelson Consulting Limited 66 33

34 Business Combinations (HKFRS 3 Revised in 2008) Nelson Consulting Limited 67 Introduction Scope Method of accounting Application of the method The objective of HKFRS 3 (revised 2008) is to improve the relevance, reliability and comparability of the information that a reporting entity provides in its financial statements about a business combination and its effects. To accomplish that, HKFRS 3 establishes principles and requirements for how the acquirer: a) recognises and measures in its financial statements the identifiable assets acquired, the liabilities assumed and any non-controlling interest in the acquiree; b) recognises and measures the goodwill acquired in the business combination or a gain from a bargain purchase; and What is it? c) determines what information to disclose to enable users of the financial statements to evaluate the nature and financial effects of the business combination Nelson Consulting Limited 68 34

35 The Acquisition Method Scope Method of accounting Application of the method An entity shall account for each business combination by applying the acquisition method. (HKFRS 3.4) Applying the acquisition method requires: a) identifying the acquirer; b) determining the acquisition date; c) recognising g and measuring the identifiable assets acquired, the liabilities assumed and any non-controlling interest in the acquiree; and d) recognising and measuring goodwill or a gain from a bargain purchase. (HKFRS 3.5) Nelson Consulting Limited 69 The Acquisition Method Recognising and measuring the identifiable assets acquired, the liabilities assumed and any non-controlling interest in the acquiree The acquirer s application of the recognition principle and conditions may result in recognising some assets and liabilities that the acquiree had not previously recognised as assets and liabilities in its financial statements Nelson Consulting Limited 70 35

If the terms of an operating lease in which the acquiree is the lessor are either favourable or unfavourable when compared with market terms The acquirer does not recognise a separate asset or")

2008-10 Nelson Consulting Limited 71 The Acquisition Method Recognising and measuring the identifiable assets acquired, the liabilities assumed and any non-controlling interest in the acquiree")

36 The Acquisition Method Example Recognising and measuring the identifiable assets acquired, the liabilities assumed and any non-controlling interest in the acquiree An operating lease in which the acquiree is the lessee is normally not recognised as assets or liabilities except for: if the terms of an operating lease are favourable relative to market terms the acquirer shall recognise an intangible asset if the terms are unfavourable relative to market terms the acquirer shall recognise a liability (HKFRS 3.B29) If the terms of an operating lease in which the acquiree is the lessor are either favourable or unfavourable when compared with market terms The acquirer does not recognise a separate asset or liability(hkfrs 3.B42) Nelson Consulting Limited 71 The Acquisition Method Recognising and measuring the identifiable assets acquired, the liabilities assumed and any non-controlling interest in the acquiree The acquirer shall measure the identifiable assets acquired and the liabilities assumed at their acquisition-date fair values. Affect acquisition in stages (HKFRS 3.18) For each business combination, the acquirer shall measure any non-controlling interest in the acquiree either at fair value or New alternative ( full goodwill method ) at the non-controlling interest s proportionate share of the acquiree s identifiable net assets. (HKFRS 3.19) Existing practice Nelson Consulting Limited 72 36

37 The Acquisition Method Example Existing practice New alternative ( Full goodwill method ) HK$ HK$ Fair value of identifiable net assets of Entity A 100 Purchase 75% interest in Entity A Fair value of Entity A as a (consideration is $120) HK$ 120 whole ($120 75%) HK$ 160 Parent s interest 75% of fair value of fidentifiable net assets ($100 75%) 75 Non-controlling interest ($100 25%) 25 NCI ($160 25%) 40 (at its proportionate share of Entity A s (at fair value) identifiable net assets) Goodwill ($120 - $75) 45 Goodwill ($160 $100) Nelson Consulting Limited 73 The Acquisition Method Critical Amendment Recognising and measuring goodwill or a gain from a bargain purchase Application of the method If fair value is adopted, it will affect the amount of goodwill Practices changed The acquirer shall recognise goodwill as of the acquisition date measured as the excess of (a) over (b) below: a) the aggregate of: i) the consideration transferred measured in accordance with HKFRS 3, which generally requires acquisition-date fair value; ii) the amount of any non-controlling interest in the acquiree measured in accordance with HKFRS 3; and iii) in a business combination achieved in stages, the acquisition-date fair value of the acquirer s previously held equity interest in the acquiree. b) the net of the acquisition-date amounts of the identifiable assets acquired and the liabilities assumed measured in accordance with HKFRS 3. (HKFRS 3. 32) Nelson Consulting Limited 74 37

38 The Acquisition Method Example Existing practice HK$ Fair value of Fair identifiable value of net identifiable assets of net a Entity A 100 HK$ 100 Purchase 75% Purchase interest 75% in Entity interest A in Entit (consideration (consideration is $120) is $120) HK$ 120 HK$ 120 a(i) Parent s interest Parent s 75% interest of fair value 75% of fairf of identifiable eidentifiable net assets e net ($100 assets 75%) 75 Non-controlling Non-controlling interest ($100 interest 25%) 25 (at its proportionate share of Entity A s 145 identifiable net assets) Goodwill Goodwill ($120 - $75) $( ) $100 = $ Nelson Consulting Limited 75 b a(ii) The Acquisition Method Example Existing practice New alternative ( Full goodwill method ) HK$ HK$ Fair value of identifiable net assets of Entity A 100 b Purchase 75% interest in Entity A (consideration is $120) HK$ 120 Fair value of Entity A ($120 a(i) 75%) HK$ 160 Parent s interest 75% of fair value of identifiable e net assets ($100 75%) 75 Non-controlling interest ($100 25%) 25 NCI a(ii) ($160 25%) 40 a(ii) (at its proportionate share of Entity A s (at fair value) identifiable net assets) Goodwill ($120 - $75) 45 Goodwill ($160 $100) 60 $( ) $100 $( ) $100 = $45 = $ Nelson Consulting Limited 76 38

39 The Acquisition Method Additional guidance Amended practices on business combination achieved in stages In a business combination achieved in stages, the acquirer shall remeasure its previously held equity interest in the acquiree at its acquisition-date fair value and recognise the resulting gain or loss, if any, in profit or loss. (HKFRS 3.42) Nelson Consulting Limited 77 The Acquisition Method Additional guidance Amended practices on business combination achieved in stages In prior reporting periods, the acquirer may have recognised changes in the value of its equity interest in the acquiree in other comprehensive income (for example, because the investment was classified as available for sale). If so, the amount that was recognised in other comprehensive income shall be recognised on the same basis as would be required if the acquirer had disposed directly of the previously held equity interest. (HKFRS 3.42) In other words, the amount recognised directly in other comprehensive income is reclassified and included in the calculation of the gain or loss recognised in profit or loss. (KPMG-UK, ) Nelson Consulting Limited 78 39

40 Improvements to HKFRSs Nelson Consulting Limited 79 Introduction Annual Improvement Project A vehicle for making non-urgent but necessary amendments to IFRS (and consequentially HKFRSs) Introduced by the IASB in 2007 and issued each year Improvement to HKFRSs 2009 is the one finalised in 2009 The project has amended 10 HKFRSs and 2 HK(IFRIC) Interpretations Nelson Consulting Limited 80 40

41 Summary Amendments to HKFRS 2 Share-based Payment HKFRS 5 Non-current Assets Held for Sale and Discontinued Operations HKFRS 8 Operating Segments HKAS 1 Presentation of Financial Statements HKAS 7 Statement of Cash Flows HKAS 17 Leases HKAS 18 Revenue HKAS 36 Impairment of Assets HKAS 38 Intangible Assets HKAS 39 Financial Instruments: Recognition and Measurement HK(IFRIC)-Int 9 Reassessment of Embedded Derivatives HK(IFRIC)-Int 16 Hedges of a Net Investment in a Foreign Operation Nelson Consulting Limited 81 Amendments to HKAS 1 HKAS 1 Presentation of Financial Statements An entity shall classify a liability as current when: a) it expects to settle the liability in its normal operating cycle; b) it hold the liability primarily for the purpose of trading; c) The liability is due to be settled within 12 months after the reporting period; or d) It does not have an unconditional right to defer settlement of the liability for at least 12 months after the reporting period (see HKAS 1.73). Terms of a liability that could, at the option of the counterparty, result in its settlement by the issue of equity instruments do not affect its classification. New requirements All other liabilities shall be classified as non-current Nelson Consulting Limited 82 41

42 Amendments to HKAS 1 HKAS 1 Presentation of Financial Statements The IASB concluded that classifying the liability on the basis of the requirements to transfer cash or other assets rather than on settlement better reflects the liquidity and solvency position of an entity, and therefore it decided to amend IAS 1 (HKAS 1) accordingly. Terms of a liability that could, at the option of the counterparty, result in its settlement by the issue of equity instruments do not affect its classification. New requirements Nelson Consulting Limited 83 Amendments to HKAS 17 HKAS 17 Leases Do you remember these 2 paragraphs in HKAS 17? Leases of land and of buildings are classified as operating or finance leases in the same way as leases of other assets. However, a characteristic of land is that it normally has an indefinite economic life and, if title is not expected to pass to the lessee by the end of the lease term, the lessee normally does not receive substantially all of the risks and rewards incidental to ownership, in which case the lease of land will be an operating lease. A payment made on entering into or acquiring a leasehold that is accounted for as an operating lease represents prepaid lease payments... The land and buildings elements of a lease of land and buildings are considered separately for the purposes p of lease classification. If title to both elements is expected to pass to the lessee by the end of the lease term, both elements are classified as a finance lease. When the land has an indefinite economic life, the land element is normally classified as an operating lease unless title is expected to pass to the lessee by the end of the lease term, in accordance with para. 14. The buildings element is classified as a finance or operating lease in accordance with para Nelson Consulting Limited 84 42

43 Amendments to HKAS 17 HKAS 17 Leases Do you remember these 2 paragraphs in HKAS 17? Leases of land and of buildings are classified as operating or finance leases in the same way as leases of other assets. However, a characteristic of land is that it normally has an indefinite economic life and, if title is not expected to pass to the As lessee part of by its the annual end improvements of the lease term, project the lessee in 2007, normally the does not receive substantially IASB reconsidered all of the the risks decisions and rewards it made incidental 2003, to ownership, in which case the specifically lease of land the perceived will be an inconsistency operating lease. between A payment made on entering into or acquiring the general a leasehold lease that classification is accounted guidance for as an in operating HKAS lease represents prepaid lease payments and... The land the and specific buildings lease elements classification of a guidance lease of land in HKAS and buildings are considered separately for and the 15 purposes related p to of long-term lease classification. leases of land If title and to both elements is expected buildings. to pass to the lessee by the end of the lease term, both elements are classified as a finance lease. When the land has an indefinite economic The IASB concluded that the guidance in HKAS life, the land element is normally classified as an operating lease unless title is and 15 might lead to a conclusion on the classification of expected to pass to the lessee by the end of the lease term, in accordance with land leases that does not reflect the substance of the para. 14. The buildings element is classified as a finance or operating lease in transaction. accordance with para Nelson Consulting Limited 85 Amendments to HKAS 17 HKAS 17 Leases HKAS and 15 are deleted and HKAS 17.15A is added as follows: When a lease includes both land and buildings elements, an entity assesses the classification of each element as a finance or an operating lease separately in accordance with HKAS In determining whether the land element is an operating or a finance lease, an important consideration is that land normally has an indefinite economic life Nelson Consulting Limited 86 43

44 Amendments to HKAS 17 Example IASB describes in HKAS 17.BC8B and BC8C that: For example, consider a 999-year lease of land and buildings. In this situation, significant risks and rewards associated with the land during the lease term would have been transferred to the lessee despite there being no transfer of title. The Board noted that the lessee in leases of this type will typically be in a position economically similar to an entity that purchased the land and buildings. The present value of the residual value of the property in a lease with a term of several decades would be negligible. The Board concluded that the accounting for the land element as a finance lease in such circumstances would be consistent with the economic position of the lessee. Unclear how long the lease term must be for the IASB to conclude that a lessee and a purchaser are in the same economic position Nelson Consulting Limited 87 Amendments to HKAS 17 Case Financial Statements 2009 Note 2 states (for early adoption of Amendment to HKAS 17 in 2009): The early adoption of the amendment to HKAS 17 has resulted in a change in accounting policy for the classification of leasehold land of the Group. Previously, leasehold land was classified as an operating lease and stated at cost less accumulated amortisation. In accordance with the amendment, leasehold land is classified as a finance lease and stated at cost less accumulated depreciation if substantially all risks and rewards of the leasehold land have been transferred to the Group. As the present value of the minimum lease payments (ie, the transaction price) of the land held by the Group amounted to substantially all of the fair value of the land as if it were freehold, the leasehold land of the Group has been classified as a finance lease. The amendment has been applied retrospectively to unexpired leases at the date of adoption of the amendment on the basis of information existing at the inception of the leases. The amendment does not apply to the leasehold land disposed of by the Group in prior years Nelson Consulting Limited 88 44

45 Today s Agenda Update of Amendments to HKFRS effective after 2010/ Nelson Consulting Limited 89 Effective after Year-End Selected new interpretations and amendments to HKFRSs Amendments to HKAS 32 Classification of Rights Issues HKAS 24(Revised) Related Party Disclosures HKFRS 9 Financial Instruments Amendments to HK(IFRIC) 14 HKAS 19 The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction Amendment to HKFRS 1 First-time Adoption of Hong Kong Financial Reporting Standards Limited Exemption from Comparative HKFRS 7 Disclosures for First-time Adopters Effective for periods beginning on/after 1 Feb Jan Jan Jan Jul Nelson Consulting Limited Updated from HKICPA, HKFRS Update, 6 Nov

46 Financial Instruments (HKFRS 9) Nelson Consulting Limited 91 Background In response to the input received on its work responding to the financial crisis, and following the conclusions of the G20 leaders and the recommendations of international bodies, the IASB announced an accelerated timetable for replacing IAS 39 in April 2009, and finally, IFRS 9 Financial Instruments in Nov HKFRS 9 was issued to maintain international convergence with the issuance of IFRS Nelson Consulting Limited 92 46

47 Background HKFRS 9 issued so far includes only the chapters relating to the classification and measurement of financial assets. HKFRS 9 addressed those matters first because they form the foundation of a standard on reporting financial instruments. Moreover, many of the concerns expressed during the financial crisis arose from the classification and measurement requirements for financial assets in HKAS 39. Financial Assets Only Nelson Consulting Limited 93 Structure of HKFRS 9 Chapters 1 Objective 2 Scope 3 Recognition and Derecognition 4 Classification 5 Measurement 6 Hedge Accounting (not used yet) 7 Disclosures (not used yet) 8 Effective Date and Transition Nelson Consulting Limited 94 47

48 Chapter 1 and 2 Objective The objective of HKFRS 9 is to establish principles for the financial reporting of financial assets that will present relevant and useful information to users of financial statements for their assessment of the amounts, timing and uncertainty of the entity s future cash flows. (para. 1.1) Scope An entity shall apply HKFRS 9 to all assets within the scope of HKAS 39 Financial Instruments: Recognition and Measurement. (para. 2.1) Nelson Consulting Limited 95 Chapter 3 Recognition & Derecognition Recognition and Derecognition An entity shall recognise a financial asset in its statement of financial position when, and only when, the entity becomes party to the contractual provisions of the instrument. When an entity first recognises a financial asset, it shall classify it in accordance with paragraphs and measure it in accordance with paragraph A regular way purchase or sale of a financial asset shall be recognised and derecognised in accordance with paragraphs 38 and AG53 AG56 of HKAS 39. (para to 3.1.2) Same as before Amended (Ch. 4 of HKFRS 9) Amended (Ch. 5 of HKFRS 9) Same as before Nelson Consulting Limited 96 48

49 Chapter 4 Classification Unless para. 4.5 of HKFRS 9 (so-called fair value option ) applies, an entity shall classify financial assets as subsequently measured at either amortised cost or fair value on the basis of both: a) the entity s business model for managing the financial assets; and b) the contractual cash flow characteristics of the financial asset. (para. 4.1) Amortised cost Fair value Nelson Consulting Limited 97 Chapter 4 Classification Assets within the scope of HKAS 39 classified on initial recognition Held within a business model whose objective is to hold assets in order to collect contractual cash flows? Yes Asset s terms give rise on specified dates to cash flows that are solely payments of principal and interest? Yes Fair value option? No No Yes No Amortised cost Fair value Through other comprehensive income Through profit or loss Nelson Consulting Limited 98 49

50 Chapter 4 Classification Assets within the scope of HKAS 39 classified on initial recognition Held within a business model whose objective is to hold assets in order to collect contractual cash flows? Yes Asset s terms give rise on specified dates to cash flows that are solely payments of principal and interest? Yes Amortised cost A financial asset shall be measured at amortised cost if both of the following conditions are met: a. the asset is held within a business model whose objective is to hold assets in order to collect contractual cash flows. b. the contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding. (para. 4.2) Nelson Consulting Limited 99 Chapter 4 Classification Assets within the scope of HKAS 39 classified on initial recognition Held within a business model whose objective is to hold assets in order to collect contractual cash flows? Yes Asset s terms give rise on specified dates to cash flows that are solely payments of principal and interest? No No A financial asset shall be measured at fair value unless it is measured at amortised cost in accordance with para (para. 4.4) Fair value Nelson Consulting Limited

51 Chapter 4 Classification Assets within the scope of HKAS 39 classified on initial recognition Held within a business model whose objective is to hold assets in order to collect contractual cash flows? Yes Asset s terms give rise on specified dates to cash flows that are solely payments of principal and interest? Yes Fair value option? Notwithstanding para , an entity may, at initial recognition, designate a financial asset as measured at fair value through profit or loss if doing so eliminates or significantly reduces a measurement or recognition inconsistency (i.e. an accounting mismatch ). (para. 4.5) Yes No Amortised cost Fair value Through profit or loss Nelson Consulting Limited 101 Chapter 4 Classification Assets within the scope of HKAS 39 classified on initial recognition Reclassification restricted to change in business model Held within a business model whose objective is to hold assets in order to collect contractual cash flows? Yes Asset s terms give rise on specified dates to cash flows that are solely payments of principal and interest? Yes Fair value option? No No Yes No Amortised cost Fair value When, and only when, an entity changes its business model for managing financial assets it shall reclassify all affected financial assets in accordance with para (para. 4.9) Nelson Consulting Limited

52 Chapter 4 Classification HKFRS 9 requires an entity to reclassify financial assets if the objective of the entity s business model for managing those financial assets changes. Such changes are expected to be very infrequent. Such changes must be determined by the entity s senior management as a result of external or internal changes and must be significant to the entity s operations and demonstrable to external parties. (para. B5.9) Amortised cost Fair value Nelson Consulting Limited 103 Chapter 4 Classification Case Financial statements 2009 states that: In the fourth quarter of 2009, the Group early adopted all new/revised HKFRSs issued up to 31 December 2009 which were pertinent to its operations where early adoption is permitted. The applicable HKFRSs are set out below: HKFRS 9: Financial Instruments HKFRS 9 is the first part of a project to replace HKAS 39: Financial Instruments: Recognition and Measurement, and it replaces the classification and measurement requirements in HKAS 39 for financial assets. Amortised cost Fair value Nelson Consulting Limited

53 Chapter 4 Classification Case Financial statements 2009 states that: Previously, financial assets of the Group were classified as financial assets at fair value through profit or loss, available-for-sale financial assets or loans and receivables (which included bank deposits) The early adoption of HKFRS 9 has resulted in a change in accounting policy, and financial assets are classified into financial assets measured at fair value through profit or loss or financial i assets measured at amortised cost. Amortised cost Fair value Through profit or loss Nelson Consulting Limited 105 Chapter 4 Classification Case Nelson Consulting Limited

54 Chapter 5 Measurement Initial measurement (same as HKAS 39) At initial recognition, an entity shall measure a financial asset at its fair value plus, in the case of a financial asset not at fair value through profit or loss, transaction costs that are directly attributable to the acquisition of the financial asset. (para ) Initial Measurement Fair Value + Transaction Cost Nelson Consulting Limited 107 Chapter 5 Measurement Subsequent Measurement After initial recognition, an entity shall measure financial assets in accordance with para (as discussed above) at fair value or amortised cost. (para ) An entity shall apply the impairment requirements of HKAS 39 to all financial assets measured at amortised cost. (para ) No impairment requirements on financial assets measured at fair value An entity shall apply the hedge accounting requirements of HKAS 39 to financial assets that are designated as hedged items. (para ) Amortised cost Fair value Nelson Consulting Limited

55 Chapter 5 Measurement Assets within the scope of HKAS 39 classified on initial recognition Held within a business model whose objective is to hold assets in order to collect contractual cash flows? Yes Asset s terms give rise on specified dates to cash flows that are solely payments of principal and interest? Yes A gain or loss on a financial asset that is measured at amortised cost and is not part of a hedging g relationship shall be recognised in profit or loss when the financial asset is derecognised, impaired or reclassified, and through the amortisation process. (para ) Fair value option? No Amortised cost Nelson Consulting Limited 109 Chapter 5 Measurement For those classified as measured at fair value Part of hedging relationship No Fair value option? No Equity instrument? Yes Elected to present gains and losses in other comprehensive income? Yes Held for trading? No Fair value through other comprehensive income Yes Yes No No Yes Hedge accounting (IAS to 102) Fair value through profit or loss Nelson Consulting Limited

Financial Instrument Standards Recap and Update 1 December 2009

Financial Instrument Standards Recap and Update 1 December 2009 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) FCCA FCPA FHKIoD MSCA 2008-09 Nelson Consulting Limited 1 Today s Agenda Recap

Financial Instrument Standards Recap and Update 1 December 2009 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) FCCA FCPA FHKIoD MSCA 2008-09 Nelson Consulting Limited 1 Today s Agenda Recap

HKAS 27 and HKFRS 3 9 January 2009

HKAS 27 and HKFRS 3 9 January 2009 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust.) CPA(US) FCCA FCPA(Practising) MSCA 2006-09 Nelson 1 Today s Agenda Consolidated and Separate Financial Statements (HKAS

HKAS 27 and HKFRS 3 9 January 2009 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust.) CPA(US) FCCA FCPA(Practising) MSCA 2006-09 Nelson 1 Today s Agenda Consolidated and Separate Financial Statements (HKAS

HKFRS/IFRS 9 and Update on Fin. Instruments 20 October 2010

HKFRS/IFRS 9 and Update on Fin. Instruments 20 October 2010 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) CTA FCCA FCPA FTIHK MSCA 2008-10 Nelson Consulting Limited 1 Background In response

HKFRS/IFRS 9 and Update on Fin. Instruments 20 October 2010 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) CTA FCCA FCPA FTIHK MSCA 2008-10 Nelson Consulting Limited 1 Background In response

Consolidated Financial Statements (Workshop 1) 24 April 2012

24 April 2012") Consolidated Financial Statements (Workshop 1) 24 April 2012 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2005-12 Nelson Consulting Limited 1

Consolidated Financial Statements (Workshop 1) 24 April 2012 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2005-12 Nelson Consulting Limited 1

Financial Reporting Update June 2012

Financial Reporting Update 2012 14 June 2012 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2008-12 Nelson Consulting Ltd 1 Effective for 2011 Dec.

Financial Reporting Update 2012 14 June 2012 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2008-12 Nelson Consulting Ltd 1 Effective for 2011 Dec.

HKFRS for Private Entities 27 October 2010

HKFRS for Private Entities 27 October 2010 Small vs. Large Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) CTA FCCA FCPA FTIHK MSCA 2010 Nelson Consulting Limited 1 Today s Agenda Introduction

HKFRS for Private Entities 27 October 2010 Small vs. Large Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) CTA FCCA FCPA FTIHK MSCA 2010 Nelson Consulting Limited 1 Today s Agenda Introduction

HKFRS and IFRS Update June 2012

HKFRS and IFRS Update 2012 6 June 2012 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2008-12 Nelson Consulting Ltd 1 Effective for 2011 Dec. Year-End

HKFRS and IFRS Update 2012 6 June 2012 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2008-12 Nelson Consulting Ltd 1 Effective for 2011 Dec. Year-End

Financial Reporting Update March 2014

Financial Reporting Update 2014 13 March 2014 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(US) CTA FCCA FCPA FCPA(Aust.) FHKIoD FTIHK MHKSI MSCA 2011-14 Nelson Consulting Limited 1 Effective for

Financial Reporting Update 2014 13 March 2014 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(US) CTA FCCA FCPA FCPA(Aust.) FHKIoD FTIHK MHKSI MSCA 2011-14 Nelson Consulting Limited 1 Effective for

Consolidated Financial Statements (Part 1) 15 March 2010

15 March 2010") Consolidated Financial Statements (Part 1) 15 March 2010 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-10 Nelson Consulting Limited 1 Regulatory Framework in

Consolidated Financial Statements (Part 1) 15 March 2010 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-10 Nelson Consulting Limited 1 Regulatory Framework in

Consolidated Financial Statements

1. General The Company is a public limited company incorporated in Hong Kong and its shares are listed on The Stock Exchange of Hong Kong Limited (the Stock Exchange ). The address of the registered office

1. General The Company is a public limited company incorporated in Hong Kong and its shares are listed on The Stock Exchange of Hong Kong Limited (the Stock Exchange ). The address of the registered office

SME FRS and Other Updates 27 November 2014

SME FRS and Other Updates 27 November 2014 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CGMA CPA(US) CTA FCCA FCPA FCPA(Aust.) FHKIoD FTIHK MHKSI MSCA 2014 Nelson Consulting Limited 1 Effective for

SME FRS and Other Updates 27 November 2014 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CGMA CPA(US) CTA FCCA FCPA FCPA(Aust.) FHKIoD FTIHK MHKSI MSCA 2014 Nelson Consulting Limited 1 Effective for

Consolidated Financial Statements (Workshop 2) 23 March Consolidated Financial Statements

23 March Consolidated Financial Statements") Consolidated Financial Statements (Workshop 2) 23 March 2011 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA MHKSI MSCA 2005-11 Nelson Consulting Limited 1 Consolidated Financial

Consolidated Financial Statements (Workshop 2) 23 March 2011 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA MHKSI MSCA 2005-11 Nelson Consulting Limited 1 Consolidated Financial

HKFRSs / IFRSs UPDATE 2011/02

28 FEBRUARY 2011 WWW.BDO.COM.HK HKFRSs / IFRSs UPDATE 2011/02 NEW AND REVISED HKFRSs 2010 YEAR ENDS REPORTING (A) New and revised HKFRSs that are mandatory for the first time for 2010 year ends 1. HKFRS

28 FEBRUARY 2011 WWW.BDO.COM.HK HKFRSs / IFRSs UPDATE 2011/02 NEW AND REVISED HKFRSs 2010 YEAR ENDS REPORTING (A) New and revised HKFRSs that are mandatory for the first time for 2010 year ends 1. HKFRS

Financial Reporting Update January 2018

Financial Reporting Update 2018 29 January 2018 LAM Chi Yuen Nelson 林智遠 CFA Charter Holder, FCPA(Practising) MBA MSc BBA CPA(U.S.) FCA FCCA FCPA(Aust.) FSCA Cairo @ Egypt Stephanie & Nelson 2008 www.facebook.com/nelsoncfa

Financial Reporting Update 2018 29 January 2018 LAM Chi Yuen Nelson 林智遠 CFA Charter Holder, FCPA(Practising) MBA MSc BBA CPA(U.S.) FCA FCCA FCPA(Aust.) FSCA Cairo @ Egypt Stephanie & Nelson 2008 www.facebook.com/nelsoncfa

Annual Accounting Update October 2008

Annual Accounting Update 2008 4 October 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust.) CPA(US) FCCA FCPA(Practising) FHKIoD MSCA 2007-08 Nelson 1 Amendment Effective After 1.1.2008 Selected new

Annual Accounting Update 2008 4 October 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust.) CPA(US) FCCA FCPA(Practising) FHKIoD MSCA 2007-08 Nelson 1 Amendment Effective After 1.1.2008 Selected new

Consolidated Financial Statements (Workshop 3) 16 September 2011

16 September 2011") Consolidated Financial Statements (Workshop 3) 16 September 2011 Lam Chi Yuen, Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2005-11 Nelson Consulting Limited

Consolidated Financial Statements (Workshop 3) 16 September 2011 Lam Chi Yuen, Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2005-11 Nelson Consulting Limited

Consolidated Financial Statements (Workshop 3) 27 April 2012

27 April 2012") Consolidated Financial Statements (Workshop 3) 27 April 2012 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2005-12 Nelson Consulting Limited 1

Consolidated Financial Statements (Workshop 3) 27 April 2012 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2005-12 Nelson Consulting Limited 1

Preparation and Presentation of Financial Statements Part 1 17 September 2013

Preparation and Presentation of Financial Statements Part 1 17 September 2013 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(US) CTA FCCA FCPA FCPA(Aust.) FHKIoD FTIHK MHKSI MSCA 2008-13 Nelson Consulting

Preparation and Presentation of Financial Statements Part 1 17 September 2013 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(US) CTA FCCA FCPA FCPA(Aust.) FHKIoD FTIHK MHKSI MSCA 2008-13 Nelson Consulting

Financial Reporting Update 2015 (with Sample Financial Statements for Year Ended 31 December 2014) 5 May 2015

5 May 2015") Financial Reporting Update 2015 (with Sample Financial Statements for Year Ended 31 December 2014) 5 May 2015 LAM Chi Yuen Nelson 林智遠 MBA(HKUST) MSc BBA ACS CFA CGMA CPA(US) CTA FCA FCCA FCPA FCPA(Aust.)

Financial Reporting Update 2015 (with Sample Financial Statements for Year Ended 31 December 2014) 5 May 2015 LAM Chi Yuen Nelson 林智遠 MBA(HKUST) MSc BBA ACS CFA CGMA CPA(US) CTA FCA FCCA FCPA FCPA(Aust.)

Financial Reporting in Hong Kong Closing out for 2013 Financial Year

China National Technical Financial Reporting in Hong Kong Closing out for 2013 Financial Year January 2014 Authors: Candy Fong Stephen Taylor There are many accounting standards that become mandatorily

China National Technical Financial Reporting in Hong Kong Closing out for 2013 Financial Year January 2014 Authors: Candy Fong Stephen Taylor There are many accounting standards that become mandatorily

Financial Reporting Update May 2015

Financial Reporting Update 2015 15 May 2015 LAM Chi Yuen Nelson 林智遠 MBA(HKUST) MSc BBA ACS CFA CGMA CPA(US) CTA FCA FCCA FCPA FCPA(Aust.) FHKIoD FTIHK MHKSI MSCA 2014-15 Nelson Consulting Limited 1 Today

Financial Reporting Update 2015 15 May 2015 LAM Chi Yuen Nelson 林智遠 MBA(HKUST) MSc BBA ACS CFA CGMA CPA(US) CTA FCA FCCA FCPA FCPA(Aust.) FHKIoD FTIHK MHKSI MSCA 2014-15 Nelson Consulting Limited 1 Today

Update on HKFRS (or IFRS) 10 September 2008

10 September 2008") Update on HKFRS (or IFRS) 10 September 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust.) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Today s Agenda Update on IFRIC 12 and HK(IFRIC) 12 Brief

Update on HKFRS (or IFRS) 10 September 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust.) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Today s Agenda Update on IFRIC 12 and HK(IFRIC) 12 Brief

Hong Kong Financial Reporting Standards Illustrative Annual Financial Statements 2009

Hong Kong Financial Reporting Standards Illustrative Annual Financial Statements 2009 Audit IAS Plus Hong Kong Financial Reporting Standards Illustrative Annual Financial Statements 2009 Foreword Welcome

Hong Kong Financial Reporting Standards Illustrative Annual Financial Statements 2009 Audit IAS Plus Hong Kong Financial Reporting Standards Illustrative Annual Financial Statements 2009 Foreword Welcome

Ajisen (China) Holdings Limited

Holdings Limited") Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness

Financial Instruments Standards (Part 1) 18 August 2011

18 August 2011") Instruments Standards (Part 1) 18 August 2011 Lam Chi Yuen, Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2006-11 Nelson Consulting Limited 1 HKAS 32, HKAS

Instruments Standards (Part 1) 18 August 2011 Lam Chi Yuen, Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2006-11 Nelson Consulting Limited 1 HKAS 32, HKAS

Financial Instruments Standards (Part 1) 13 April 2010

13 April 2010") Instruments Standards (Part 1) 13 April 2010 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) FCCA FCPA FHKIoD MSCA 2006-10 Nelson Consulting Limited 1 HKAS 32, HKAS 39, HKFRS 7 and HKFRS 9 Anyone

Instruments Standards (Part 1) 13 April 2010 Nelson Lam 林智遠 MBA MSc BBA ACA ACIS CFA CPA(Aust.) CPA(US) FCCA FCPA FHKIoD MSCA 2006-10 Nelson Consulting Limited 1 HKAS 32, HKAS 39, HKFRS 7 and HKFRS 9 Anyone

Notes to the Consolidated Financial Statements

1. General The Company is a public limited company incorporated in Hong Kong and its shares are listed on The Stock Exchange of Hong Kong Limited (the Stock Exchange ). The address of the registered office

1. General The Company is a public limited company incorporated in Hong Kong and its shares are listed on The Stock Exchange of Hong Kong Limited (the Stock Exchange ). The address of the registered office

NOTES TO THE FINANCIAL STATEMENTS

1 GENERAL INFORMATION Kerry Properties Limited (the Company ) is a limited liability company incorporated in Bermuda. The address of its registered office is Canon s Court, 22 Victoria Street, Hamilton

1 GENERAL INFORMATION Kerry Properties Limited (the Company ) is a limited liability company incorporated in Bermuda. The address of its registered office is Canon s Court, 22 Victoria Street, Hamilton

Notes to the Financial Statements

1. Principal activities The Company is an investment holding company and its subsidiaries are principally engaged in the provision of banking and related financial services. The Company is a limited liability

1. Principal activities The Company is an investment holding company and its subsidiaries are principally engaged in the provision of banking and related financial services. The Company is a limited liability

First Time Adoption of HKFRSs (HKFRS 1) 27 September Nelson 1

27 September Nelson 1") First Time Adoption of HKFRSs (HKFRS 1) 27 September 2006 Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Today s Agenda Simple and Comprehensive Introduction Real Cases and

First Time Adoption of HKFRSs (HKFRS 1) 27 September 2006 Nelson Lam CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Today s Agenda Simple and Comprehensive Introduction Real Cases and

HKFRSs for SME and SMP 26 March 2007

HKFRSs for SME and SMP 26 March 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) 2005-07 Nelson 1 Today s Agenda Overview of of SME-FRF and SME-FRS Real Cases and Examples

HKFRSs for SME and SMP 26 March 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) 2005-07 Nelson 1 Today s Agenda Overview of of SME-FRF and SME-FRS Real Cases and Examples

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 1. GENERAL The Company is a public listed limited liability company incorporated in Hong Kong and with its shares listed on The Stock Exchange of Hong Kong

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 1. GENERAL The Company is a public listed limited liability company incorporated in Hong Kong and with its shares listed on The Stock Exchange of Hong Kong

Comparison of HKFRS and IFRS 2007 (Based on statements that were effective for financial years ended 31 December 2007)

") Comparison of HKFRS and IFRS 2007 (Based on statements that were effective for financial years ended 31 December 2007) This comparison was developed by the Institute s Financial Reporting Standards Committee

Comparison of HKFRS and IFRS 2007 (Based on statements that were effective for financial years ended 31 December 2007) This comparison was developed by the Institute s Financial Reporting Standards Committee

Notes to the Financial Statements

1. Principal activities The Company is an investment holding company and its subsidiaries are principally engaged in the provision of banking and related financial services. The Company is a limited liability

1. Principal activities The Company is an investment holding company and its subsidiaries are principally engaged in the provision of banking and related financial services. The Company is a limited liability

SME FRS and Other Updates 20 November 2014

SME FRS and Other Updates 20 November 2014 Ms CHUA Suk Lin Ivy Mr LAM Chi Yuen Nelson 2014 Nelson Consulting Limited 1 Effective for 2015 Dec. Year End Selected new interpretations and amendments to HKFRSs

SME FRS and Other Updates 20 November 2014 Ms CHUA Suk Lin Ivy Mr LAM Chi Yuen Nelson 2014 Nelson Consulting Limited 1 Effective for 2015 Dec. Year End Selected new interpretations and amendments to HKFRSs

Notes to the Consolidated Financial Statements

84 1. General and Basis of Preparation The Company is a public limited company incorporated in the Cayman Islands on 16 November 2000 under the Companies Law (Revised) Chapter 22 of the Cayman Islands

84 1. General and Basis of Preparation The Company is a public limited company incorporated in the Cayman Islands on 16 November 2000 under the Companies Law (Revised) Chapter 22 of the Cayman Islands

Financial Instruments Standards 11 November Nelson Lam 林智遠 CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA Nelson 1

MBA MSc BBA CPA(US) ACA Nelson 1") Instruments Standards 11 November 2006 Nelson Lam 林智遠 CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Instruments HKAS 32 Disclosure and presentation HKAS 39 Recognition and measurement