Quincy Mutual Group MASSACHUSETTS MANDATORY ENDORSEMENT QM-0099-S (10 13)

|

|

|

- Chad Glenn

- 5 years ago

- Views:

Transcription

1 Quincy Mutual Group MASSACHUSETTS MANDATORY ENDORSEMENT QM-0099-S (10 13) This endorsement includes changes that affect your auto insurance. Please read this endorsement carefully to see how it affects your policy. Optional Insurance (Page 13): Paragraph 5. is deleted and replaced by the following: 5. For bodily injury or property damage caused by intentional acts committed or caused by you, a household member, or any other person using your auto with your consent. This exclusion applies even if the bodily injury or property damage is different from, or greater than, that which is expected or intended. Part 5. Optional Bodily Injury to Others (Page 14): Paragraph 5. is deleted and replaced by the following: 5. While anyone is using a vehicle in the course of any business other than the business of selling, servicing, repairing or parking autos. This exclusion does not apply to: 1. private passenger autos, or 2. pick-up trucks, vans, or similar vehicles having a gross weight of less than 10,000 pounds; not used for the delivery or transportation of goods, products, or materials unless such use is incidental to your business of installing, maintaining, or repairing furnishings or equipment. General Provisions and Exclusions (Page 30): The following are added to your policy: 21. Actual Cash Value Whenever the appraised cost of repair of an auto plus the probable salvage value of the auto may be reasonably expected to exceed the actual cash value of the auto, we shall determine the auto s actual cash value. Our determination shall be based on a consideration of all of the following factors: 1.) the retail book value for an auto of like kind and quality, but for the damage incurred; 2.) the price paid for the auto plus the value of prior improvements to the auto at the time of the accident, less appropriate depreciation; 3.) the decrease in value of the auto resulting from prior unrelated damage which is detected by the appraiser; and 4.) the actual cost of purchase of an available auto of like kind and quality, but for the damage sustained. Page 1 of 1 QM-0099-S (10 13)

2 MASSACHUSETTS AUTOMOBILE RENEWAL FORM (STATEMENT OF FACTS) ISSUED BY: POLICY NUMBER: POLICY RENEWAL DATE: INSURED NAME AND ADDRESS: AGENT NAME AND ADDRESS: Dear Insured, It is very important that we have accurate driver and garaging information. All household members who are licensed to drive and any individual(s) that regularly use your autos must be listed on your policy s Coverage Selection Page. You must also verify where your vehicles are garaged. Failure to list all licensed household members and individual(s) who regularly operate your autos, and the failure to provide accurate garaging information may reduce or eliminate coverages under your policy. Please verify this information and make any necessary changes. It is your obligation to review this renewal form. You further warrant that the information contained is true, accurate, and complete and that no material facts have been omitted, misrepresented or misstated. Operators currently shown on your policy: Our records show the following individuals are licensed household members or have regular access to your autos. Lic. Date First Licensed % of Use for Auto Please indicate the reason for any changes Opr. Operator Name Date of Birth License Number St. Auto Motorcycle Veh Veh Veh Veh (for example, "Driver Added" or No. mm/dd/yy mm/dd/yy mm/dd/yy "Corrected Information") Vehicles currently shown on your policy: Our records show the following automobiles are listed on your policy and are garaged at the location(s) listed below. Veh # Year Make and Model of Vehicle Garaging Location Please indicate the reason for any changes (for example, "Vehicle Deleted" or "Garaging Location Changed") Important Notice: If you or someone on your behalf knowingly gives us false, deceptive, misleading or incomplete information in this application and if such false, deceptive, misleading or incomplete information increases our risk of loss, we may refuse to pay claims under any or all of the Optional Insurance Parts, we may also limit payments under Part 3 and Part 4, and we may cancel your policy. Such information includes the description and the place of garaging of the vehicles to be insured, the names of household members, and customary operators required to be listed. IF YOU ARE MAKING CHANGES OR CORRECTING INFORMATION, PLEASE SIGN THIS FORM AND RETURN IT TO YOUR AGENT AT THE ADDRESS LISTED ABOVE. DATE INSURED'S SIGNATURE DO NOT RETURN THIS FORM IF THE VEHICLE, VEHICLE GARAGING AND DRIVER INFORMATION LISTED ABOVE IS ACCURATE OR IF YOU ARE NOT ATTACHING ANY DOCUMENTATION FOR CREDITS/DISCOUNTS (SEE REVERSE FOR DESCRIPTION OF CREDITS/DISCOUNTS AND REQUIRED DOCUMENTATION) amvrenewalquest 10 13

3 Credits and Discounts Available: Please review the following questions. If you answer "YES" to any of these questions, you may be eligible for a credit/discount. If you have any questions about these credits/discounts, or the verification information required in order to receive the credit/discount, please contact your agent. YES NO 1. Do you travel less than 7,500 miles a year? If YES, you may be eligible for a discount, contact your agent for further information. If we can verify this information from the Registry of Motor Vehicles we will apply the credit, otherwise, you must reapply on an annual basis. YES NO 2. Is your home insured by Quincy Mutual Group (Quincy Mutual Fire Insurance Company or New England Mutual Insurance Company) or Andover Companies (Cambridge Mutual, Merrimack Mutual, Baystate Mutual) or the Massachusetts Property Insurance Underwriting Association)? If YES, you may be eligible for up to 30% credit on your Homeowners policy. Include the policy number and the name of the insurance company or contact your agent for further information. YES NO 3. Are there any inexperienced operators (less than 6 years of driving experience) listed on your policy who maintain a grade point average of 3.0 (B) or better? If YES attach a certificate completed by a school official who can verify the operator's academic record or contact your agent for further information. (This discount is removed when the policy expires. You must apply for this Good Student discount every time the policy is renewed.) YES NO 4. Are there any inexperienced operators (less than 6 years of driving experience) listed on your policy who is a student and lives more than 100 miles or more from your residence premises? If YES provide the name of the school and where it is located. (This discount is removed when the policy expires. You must apply for this Student Away discount every time the policy is renewed.) Important Coverage Questions: Please review the following questions. If you answer "YES" to any of these questions you should contact your agent immediately in order to verify that you have the correct coverage on your policy. YES NO 1. Have you customized any vehicle or motorcycle listed on your policy? Examples of customization includes installing electronic equipment or custom furnishings; non-auto antennas; awnings, cabanas, or any equipment that creates additional living space. YES NO 2. Are any of your vehicles listed on your policy used for business or occupational duties other than commuting to and from work? For example, deliveries, business calls or transporting someone for a fee. YES NO 3. Are there any licensed driver(s) not currently listed on your policy who regularly operate any vehicle that is currently listed on your policy? YES NO 4. Are there any licensed household members that are not currently listed on your policy? YES NO 5. Are you, or any licensed household member, operating a motor vehicle without a Massachusetts license? Note that Massachusetts law requires that you obtain a Massachusetts license within one year. Failure to obtain a MA license could result in non-renewal of your policy. For more information on this matter consult the Registry of Motor Vehicles website at www. mass.gov/rmv If you answered YES to any of the above questions, please contact your Insurance agency: It is a crime to knowingly provide false, incomplete or misleading information to an insurance company for the purpose of defrauding the company. Penalties include imprisonment, fines or a denial of insurance benefits. amvrenewalquest 10 13

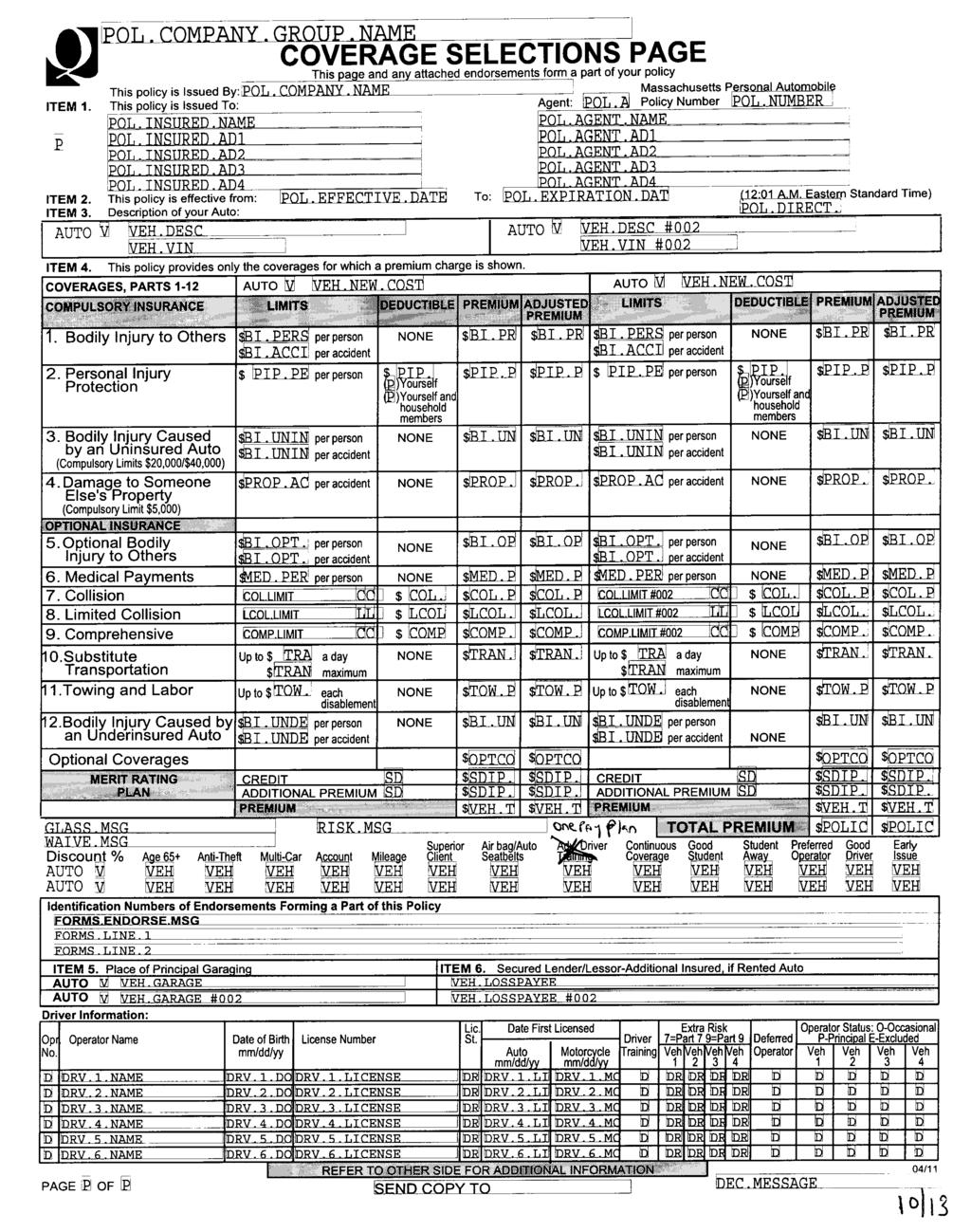

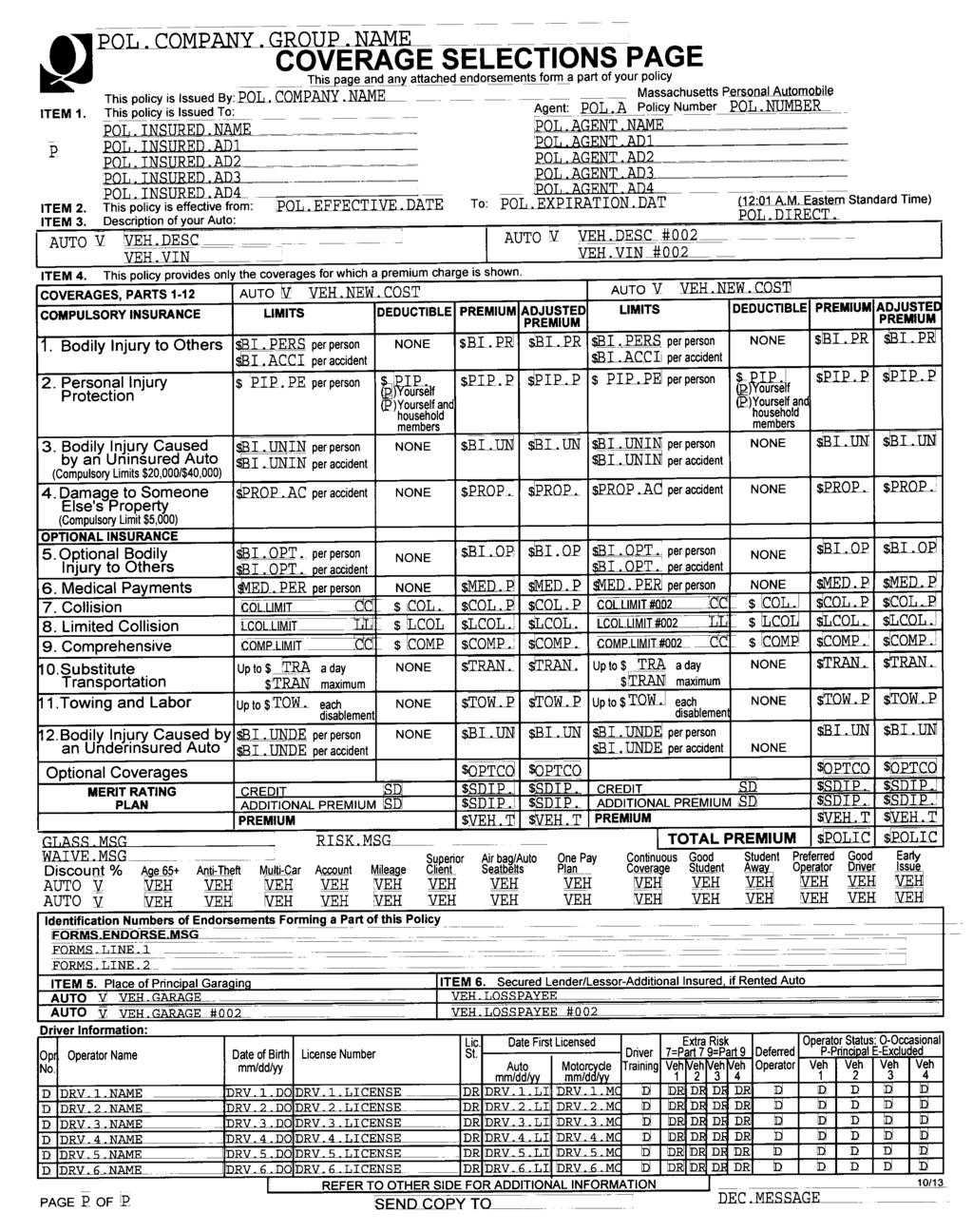

4 POL.COMPANY.GROUP.NAME COVERAGE SELECTIONS PAGE This page and any attached endorsements form a part of your policy This policy is Issued By: POL.COMPANY.NAME Massachusetts Personal Automobile ITEM 1. This policy is Issued To: Agent: Policy Number POL.A POL.INSURED.NAME POL.AGENT.NAME P POL.INSURED.AD1 POL.AGENT.AD1 POL.INSURED.AD2 POL.AGENT.AD2 POL.INSURED.AD3 POL.AGENT.AD3 POL.INSURED.AD4 POL.AGENT.AD4 POL.EFFECTIVE.DATE POL.EXPIRATION.DAT ITEM 2. This policy is effective from: To: (12:01 A.M. Eastern Standard Time) ITEM 3. Description of your Auto: AUTO ITEM 4. This policy provides only the coverages for which a premium charge is shown. AUTO COVERAGES, PARTS 1-12 AUTO AUTO COMPULSORY INSURANCE LIMITS DEDUCTIBLE PREMIUM ADJUSTED PREMIUM 1. Bodily Injury to Others 2. Personal Injury Protection 3. Bodily Injury Caused by an Uninsured Auto (Compulsory Limits $20,000/$40,000) 4.Damage to Someone Else's Property (Compulsory Limit $5,000) OPTIONAL INSURANCE 5.Optional Bodily Injury to Others 6. Medical Payments 7. Collision 8. Limited Collision 9. Comprehensive 10.Substitute Transportation 11.Towing and Labor 12.Bodily Injury Caused by an Underinsured Auto Optional Coverages MERIT RATING PLAN $ per person $ per accident $ $ per person $ per accident NONE $ $ per person $ $ $ ( )Yourself ( P)Yourself and household members NONE $ $ $ PROP.AC per accident NONE $ PROP. $ PROP. $ per person NONE $ $ $ per person NONE $ $ $ BI.OPT. per accident $ BI.OPT. per accident $ MED.PER per person NONE $ MED.P $ MED.P $ per person NONE $ $ COL.LIMIT CC $ COL. $ COL.P $ COL.P $ $ $ LCOL.LIMIT LL $ LCOL $ LCOL. $ LCOL. $ $ $ COMP.LIMIT CC $ COMP $ COMP. $ COMP. $ $ $ Up to $ a day NONE $ $ $ TRAN maximum Up to $ TOW. each NONE $ TOW.P $ TOW.P disablement $ $ per person per accident NONE $ $ CREDIT $ $ ADDITIONAL PREMIUM $ $ PREMIUM $ $ LIMITS $ per person $ per accident $ $ per person $ per accident DEDUCTIBLE PREMIUM ADJUSTED PREMIUM NONE $ $ per person $ $ $ ( )Yourself ( P)Yourself and household members NONE $ $ $ PROP.AC per accident NONE $ PROP. $ PROP. Up to $ a day NONE $ $ $ TRAN maximum Up to $ TOW. each NONE $ TOW.P $ TOW.P disablement $ $ per person per accident NONE $ $ $ $ $ $ CREDIT $ $ ADDITIONAL PREMIUM $ $ PREMIUM $ $ TOTAL PREMIUM $ $ WAIVE.MSG Superior Air bag/auto One Pay Continuous Good Student Preferred Good Early Discount % Age 65+ Anti-Theft Multi-Car Account Mileage Client Seatbelts Plan Coverage Student Away Operator Driver Issue AUTO AUTO V GLASS.MSG V V VEH.DESC VEH.VIN VEH VEH VEH VEH BI.PERS BI.ACCI PIP.PE BI.UNIN BI.UNIN BI.OPT. Identification Numbers of Endorsements Forming a Part of this Policy FORMS.ENDORSE.MSG FORMS.LINE.1 FORMS.LINE.2 V VEH.DESC #002 VEH.VIN #002 POL.NUMBER POL.DIRECT. V VEH.NEW.COST V VEH.NEW.COST TRA BI.UNDE BI.UNDE VEH VEH PIP. BI.PR PIP.P BI.UN BI.OP TRAN. BI.UN BI.PR PIP.P BI.UN BI.OP TRAN. BI.UN OPTCO OPTCO SD SDIP. SDIP. SD SDIP. SDIP. VEH.T VEH.T RISK.MSG VEH VEH VEH VEH VEH VEH VEH VEH BI.PERS BI.ACCI PIP.PE BI.UNIN BI.UNIN BI.OPT. BI.PR OPTCO OPTCO SD SDIP. SDIP. SD SDIP. SDIP. VEH.T VEH.T POLIC POLIC ITEM 5. Place of Principal Garaging ITEM 6. Secured Lender/Lessor-Additional Insured, if Rented Auto AUTO V VEH.GARAGE VEH.LOSSPAYEE AUTO V VEH.GARAGE #002 VEH.LOSSPAYEE #002 Driver Information: Opr. Operator Name Date of Birth License Number Lic. St. Date First Licensed Driver Extra Risk 7=Part 7 9=Part 9 Deferred Operator Status: O-Occasional P-Principal E-Excluded No. mm/dd/yy Auto mm/dd/yy Motorcycle mm/dd/yy Training Veh Veh Veh Veh Operator Veh 1 Veh 2 Veh 3 Veh 4 D DRV.1.NAME DRV.1.DO DRV.1.LICENSE DR DRV.1.LI DRV.1.MC D DR DR DR DR D D D D D D DRV.2.NAME DRV.2.DO DRV.2.LICENSE DR DRV.2.LI DRV.2.MC D DR DR DR DR D D D D D D DRV.3.NAME DRV.3.DO DRV.3.LICENSE DR DRV.3.LI DRV.3.MC D DR DR DR DR D D D D D D DRV.4.NAME DRV.4.DO DRV.4.LICENSE DR DRV.4.LI DRV.4.MC D DR DR DR DR D D D D D D DRV.5.NAME DRV.5.DO DRV.5.LICENSE DR DRV.5.LI DRV.5.MC D DR DR DR DR D D D D D D DRV.6.NAME DRV.6.DO DRV.6.LICENSE DR DRV.6.LI DRV.6.MC D DR DR DR DR D D D D D PAGE P OF P REFER TO OTHER SIDE FOR ADDITIONAL INFORMATION MADEC13 10/13 SEND COPY TO DEC.MESSAGE VEH VEH PIP. PIP.P BI.UN BI.OP PIP.P BI.UN BI.OP MED.PER MED.P MED.P COL.LIMIT #002 LCOL.LIMIT #002 CC LL COL. LCOL COL.P LCOL. COL.P LCOL. COMP.LIMIT #002 CC COMP COMP. COMP. TRA TRAN. TRAN. BI.UNDE BI.UNDE VEH VEH VEH VEH VEH VEH VEH VEH BI.UN VEH VEH BI.PR BI.UN VEH VEH

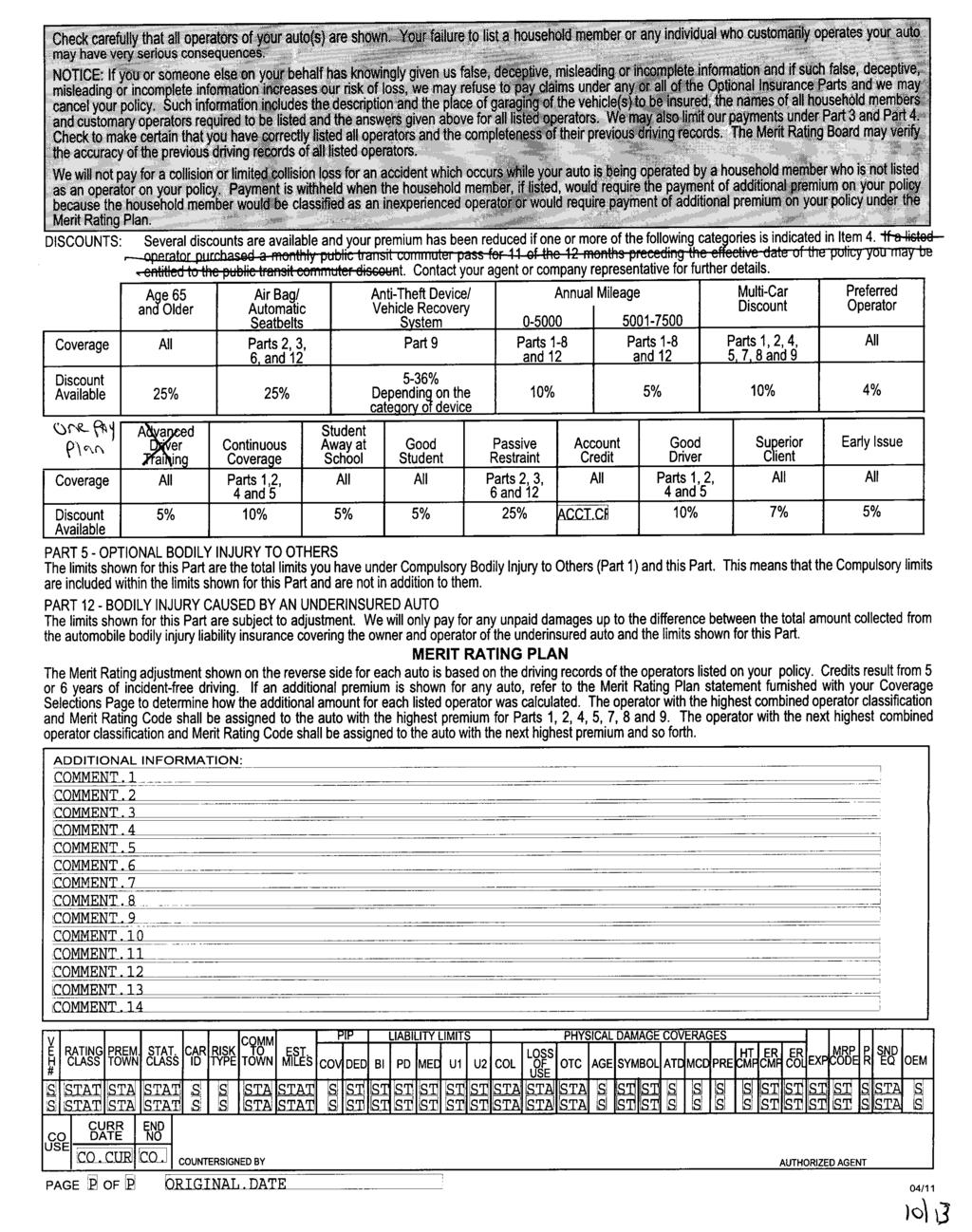

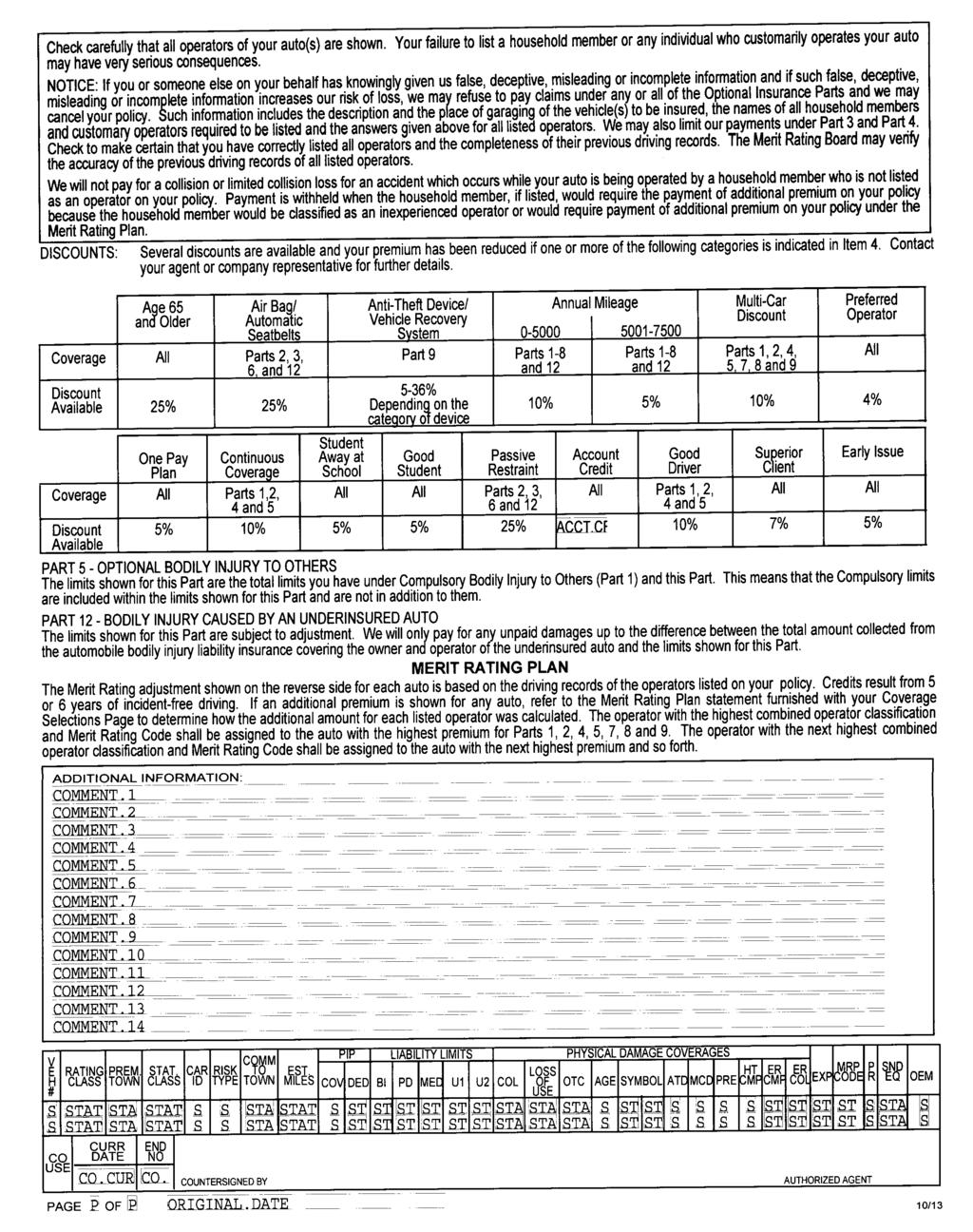

5 Check carefully that all operators of your auto(s) are shown. Your failure to list a household member or any individual who customarily operates your auto may have very serious consequences. NOTICE: If you or someone else on your behalf has knowingly given us false, deceptive, misleading or incomplete information and if such false, deceptive, misleading or incomplete information increases our risk of loss, we may refuse to pay claims under any or all of the Optional Insurance Parts and we may cancel your policy. Such information includes the description and the place of garaging of the vehicle(s) to be insured, the names of all household members and customary operators required to be listed and the answers given above for all listed operators. We may also limit our payments under Part 3 and Part 4. Check to make certain that you have correctly listed all operators and the completeness of their previous driving records. The Merit Rating Board may verify the accuracy of the previous driving records of all listed operators. We will not pay for a collision or limited collision loss for an accident which occurs while your auto is being operated by a household member who is not listed as an operator on your policy. Payment is withheld when the household member, if listed, would require the payment of additional premium on your policy because the household member would be classified as an inexperienced operator or would require payment of additional premium on your policy under the Merit Rating Plan. DISCOUNTS: Several discounts are available and your premium has been reduced if one or more of the following categories is indicated in Item 4. Age 65 Air Bag/ Anti-Theft Device/ Annual Mileage Multi-Car Preferred and Older Automatic Vehicle Recovery Discount Operator Seatbelts System Coverage All Parts 2, 3, Part 9 Parts 1-8 Parts 1-8 Parts 1, 2, 4, All 6, and 12 and 12 and 12 5, 7, 8 and 9 Discount 5-36% Available 25% 25% Depending on the 10% 5% 10% 4% category of device Student One Pay Continuous Away at Good Passive Account Good Superior Billing Coverage School Student Restraint Credit Driver Client Early Issue Coverage All Parts 1,2, 4 and 5 All All Parts 2, 3, 6 and 12 All Parts 1, 2, 4 and 5 All All Discount Available 5% 10% 5% 5% 25% ACCT.CR 10% 7% 5% PART 5 - OPTIONAL BODILY INJURY TO OTHERS The limits shown for this Part are the total limits you have under Compulsory Bodily Injury to Others (Part 1) and this Part. This means that the Compulsory limits are included within the limits shown for this Part and are not in addition to them. PART 12 - BODILY INJURY CAUSED BY AN UNDERINSURED AUTO The limits shown for this Part are subject to adjustment. We will only pay for any unpaid damages up to the difference between the total amount collected from the automobile bodily injury liability insurance covering the owner and operator of the underinsured auto and the limits shown for this Part. MERIT RATING PLAN The Merit Rating adjustment shown on the reverse side for each auto is based on the driving records of the operators listed on your policy. Credits result from 5 or 6 years of incident-free driving. If an additional premium is shown for any auto, refer to the Merit Rating Plan statement furnished with your Coverage Selections Page to determine how the additional amount for each listed operator was calculated. The operator with the highest combined operator classification and Merit Rating Code shall be assigned to the auto with the highest premium for Parts 1, 2, 4, 5, 7, 8 and 9. The operator with the next highest combined operator classification and Merit Rating Code shall be assigned to the auto with the next highest premium and so forth. ADDITIONAL INFORMATION: COMMENT.1 COMMENT.2 COMMENT.3 COMMENT.4 COMMENT.5 COMMENT.6 COMMENT.7 COMMENT.8 COMMENT.9 COMMENT.10 COMMENT.11 COMMENT.12 COMMENT.13 COMMENT.14 V E H # CO USE PAGE RATING CLASS PREM. TOWN CURR DATE CLASS STAT. CAR ID TYPE RISK END NO COMM TO TOWN COUNTERSIGNED BY P OF P ORIGINAL.DATE EST. MILES PIP LIABILITY LIMITS COV DED BI PD MED U1 U2 COL LOSS OF USE PHYSICAL DAMAGE COVERAGES HT OTC AGE SYMBOL ATD MCD PRE CMP CMP ER COL ER EXP MRP CODE AUTHORIZED AGENT P R SND EQ OEM S STAT STA STAT S S STA STAT S ST ST ST ST ST ST STA STA STA S ST ST S S S S ST ST ST ST S STA S S STAT STA STAT S S STA STAT S ST ST ST ST ST ST STA STA STA S ST ST S S S S ST ST ST ST S STA S CO.CUR CO. MADEC13 10/13

6 RULE 11. PREMIUM CALCULATION RULE The appropriate Rating Tier assignment must first be determined from Rule 26.1 A. This premium determination Rule applies separately to Private Passenger vehicles as defined in Rule 27. and to Motorcycles. For Miscellaneous type vehicles, refer to the Miscellaneous rate pages of the manual to calculate the premium. Once the Tier and type of vehicle is determined, follow the appropriate calculation rule below. A. Private Passenger Vehicles in Rating Tiers I-IV only Liability Coverages: Bodily Injury Liability (Part 1) 1. Refer to the Territory Definition pages to determine the territory code for the location where the auto is principally garaged. 2. Refer to Rule 28. to determine the appropriate driver classification applicable to each vehicle. 3. Determine the base premium from the Part 1 manual rate page based upon the Tier, territory and classification for this coverage part. 4. Multiply by the appropriate tier factor from Rule B., round. 5. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on the rating worksheet on page RW-1 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/ class 15 discount. Personal Injury Protection (Part 2) 1. Refer to the Territory Definition pages to determine the territory code for the location where the auto is principally garaged. 2. Refer to Rule 28. to determine the appropriate driver classification applicable to each vehicle. 3. Determine the base premium from the Part 2 manual rate page based upon the Tier, territory and classification for this coverage part. 4. Multiply by the appropriate tier factor from Rule B., round. 5. Multiply by the deductible % shown on the rate page for a deductible buy-back credit, if applicable. Round. 6. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on the rating worksheet on page RW-1 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/ class 15 discount. Property Damage Liability (Part 4) 1. Refer to the Territory Definition pages to determine the territory code for the location where the auto is principally garaged. 2. Refer to Rule 28. to determine the appropriate driver classification applicable to each vehicle. 3. Determine the base premium from the Part 4 manual rate page based upon the tier, territory, and classification. 4. Multiply by the appropriate tier factor from Rule B., round. 5. Multiply by the increased limits factor shown on the rate page, if applicable. Round. 6. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on the rating worksheet on page RW-1 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Optional Bodily Injury (Part 5) 1. Refer to the Territory Definition pages to determine the territory code for the location where the auto is principally garaged. 2. Refer to Rule 28. to determine the appropriate driver classification applicable to each vehicle. 3. Determine the base premium from the Part 5 manual rate page based upon the tier, territory, classification. 4. Multiply by the appropriate tier factor from Rule B., round. 7

7 5. If increased limits are desired, skip steps 3 and 4 and instead take Part 1 base premium based upon tier, territory and classification and add to Part 5 base premium based upon tier, territory and classification. Take result and multiply by increased limit factors shown on the Part 5 rate page and then subtract Part 1 base. Round. 6. Multiply by the appropriate tier factor from Rule B. Round. 7. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on the rating worksheet on page RW-1 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Bodily Injury caused by an Uninsured Auto (Part 3), Bodily Injury caused by an Underinsured Auto (Part 12), and Medical Payments Coverage (Part 6). 1. Determine the Rating Tier Assignment from Rule A. 2. Determine the base premium from the Statewide manual rate page based upon the tier, and amount of coverage desired for these coverage parts. 3. Multiply by the appropriate tier factor from Rule B. 4. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on the rating worksheet on page RW-1 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Physical Damage Coverages: Collision (Part 7) 1. Refer to the Territory Definition pages to determine the territory code for the location where the auto is principally garaged. 2. Refer to Rule 28. to determine the appropriate driver classification applicable to each vehicle. 3. Determine the base premium from the Part 7 manual rate page based upon the tier, territory, and classification. 4. Multiply by the appropriate tier factor from Rule B., round. 5. Refer to Rule 20. to determine the model year of the auto. 6. For Model Years 2010 and Prior, refer to the ISO Symbol and Identification Manual for the appropriate symbol of the auto. For Model Years 2011 and after, refer to the AIB Vehicle Rating Group Program to determine the appropriate Vehicle Rating Group of the auto. 7. Multiply by the appropriate Model Year/Symbol factor shown in the model year/symbol pages or the appropriate Model Year/VRG factor from the Model Year/Vehicle Rating Group pages for this coverage part. Round. (Refer to Rule 22. to determine the base premium for rating vehicles for which a symbol is not shown on the rate pages.) (Refer to Rule 21.B. to determine the base premium for rating vehicles not assigned a Vehicle Rating Group.) 8. The costs to reduce the deductible and credits to increase the deductible are shown on the rate page. If applicable, determine premium for change in deductible provision. Round. 9. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on our rating worksheet, page RW-1 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Limited Collision (Part 8) Follow instructions for rating collision coverage above and charge 6% of the Collision base premium for the same model year and symbol (for model years 2010 and prior) or the same model year and Vehicle Rating Group (for model years 2011 and greater with policy effective dates on or after ) for the $500 deductible option. The cost to reduce the deductible is shown on the rate page by tier. Comprehensive (Part 9) 1. Refer to the Territory Definition pages to determine the territory code for the location where the auto is principally garaged. 2. Determine the base premium from the manual rate page based upon the tier, and territory. 3. Multiply by the appropriate tier factor from Rule B., Round. 4. Refer to Rule 20. to determine the model year of the auto. 8

8 5. For Model Years 2010 and Prior, refer to the ISO Symbol and Identification Manual for the appropriate symbol of the auto. For Model Years 2011 and after, refer to the AIB Vehicle Rating Group Program to determine the appropriate Vehicle Rating Group of the auto. 6. Refer to Rule 20. to determine the base premium for rating vehicles for which a model year is not displayed on the rate pages. 7. Refer to Rule 22. to determine the base premium for rating vehicles for which a symbol is not shown on the rate pages. (Refer to Rule 21 to determine the base premium for rating vehicles not assigned a Vehicle Rating Group.) 8. Multiply by the appropriate Model Year/Symbol factor shown in the model year/symbol pages or the appropriate Model Year/VRG factor from the Model Year/Vehicle Rating Group pages for this coverage part. Round. 9. The costs to reduce the deductible and credits to increase the deductible are shown on the rate page. If applicable, determine premium for change in deductible provision. Round. 10. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on our rating worksheet, page RW-1 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Substitute Transportation (Part 10) and Towing and Labor (Part 11) 1. Refer to the Statewide Rate pages by tier to determine base premium. The charge is per vehicle based upon the desired coverage limit. 2. Multiply the premium determined above by the tier factor for Rule B and then by any other applicable rating debit and credit factors as shown on our rating worksheet, page RW-1 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Exceptions: See Rule 32. and Miscellaneous rate pages for premium calculation of Non-Symbolled or Non-Specific Vehicle Rating Group Pickups. See Rule 34. and Miscellaneous rate pages for premium calculation of Trailers. See Rule 39. and Miscellaneous rate pages for premium calculation of Motor Homes. See Rule 40. and Miscellaneous rate pages for premium calculation of Antique Motor Cars and Motorcycles. See Rule 43. and Miscellaneous rate pages for premium calculation of Low Speed vehicles. See Rule 46. and Miscellaneous rate pages for premium calculation of Excess Electronic Equipment Coverage. See Rule 50. Use of Other Automobiles. B. Private Passenger Vehicles in Rating Tier V. Liability Coverages Bodily Injury Liability (Part 1) and Personal Injury Protection (Part2) 1. Refer to the Territory Definition pages to determine the territory code for the location where the auto is principally garaged. 2. Refer to Rule 28. to determine the appropriate driver classification applicable to each vehicle. 3. Determine the base premium from the manual rate page based upon the tier, territory and classification for these coverage parts. 4. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on the rating worksheet on page RW-2 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/ class 15 discount. Property Damage Liability (Part 4) and Optional Bodily Injury (Part 5) 1. Refer to the Territory Definition pages to determine the territory code for the location where the auto is principally garaged. 2. Refer to Rule 28. to determine the appropriate driver classification applicable to each vehicle. 3. Determine the base premium from the manual rate page based upon the tier, territory, classification and amount of coverage desired for these coverage parts. 4. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on the rating worksheet on page RW-2 of this manual. Premiums are calculated in the consecutive, cumulative 9

9 order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Bodily Injury caused by an Uninsured Auto (Part 3), Bodily Injury caused by an Underinsured Auto (Part 12), and Medical Payments Coverage (Part 6). 1. Refer to the Territory Definition pages to determine the territory code for the location where the auto is principally garaged. 2. Determine the base premium from the manual rate page based upon the tier, territory and amount of coverage desired for these coverage parts. 3. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on the rating worksheet on page RW-2 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Physical Damage Coverages: Collision (Part 7) 1. Refer to the Territory Definition pages to determine the territory code for the location where the auto is principally garaged. 2. Refer to Rule 28. to determine the appropriate driver classification applicable to each vehicle. 3. Determine the base premium from the Part 7 manual rate page based upon the tier, territory, and classification. 4. Refer to Rule 20. to determine the model year of the auto. 5. For Model Years 2010 and prior, refer to the ISO Symbol and Identification Manual for the appropriate symbol of the auto. For Model Years 2011 and after, refer to the AIB Vehicle Rating Group Program to determine the appropriate Vehicle Rating Group of the auto. 6. Multiply by the appropriate Model Year/Symbol factor shown in the model year /symbol pages or the appropriate Model Year/VRG factor from the Model Year/Vehicle Rating Group Pages for this coverage part. Round.(Refer to Rule 22 to determine the base premium for rating vehicles for which a symbol is not shown on the page. (Refer to Rule 21. B. to determine the base premium for rating vehicles not assigned a Vehicle Rating Group.) 7. Refer to Rule 20. to determine the base premium for rating vehicles for which a model year is not displayed on the rate pages. 8. The costs to reduce the deductible and credits to increase the deductible are shown on the rate page. If applicable, determine the premium for change in the deductible provision. Round. 9. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on our rating worksheet, page RW-2 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Limited Collision (Part 8) Follow instructions for rating collision coverage above and charge 6% of the Collision base premium for the same model year and symbol or the same model year and Vehicle Rating Group for the $500 deductible option. The cost to reduce the deductible is shown on the rate page by tier by territory. Comprehensive (Part 9) 1. Refer to the Territory Definition pages to determine the territory code for the location where the auto is principally garaged. 2. Determine the base premium from the manual rate page based upon the tier, and territory. 3. Refer to Rule 20. to determine the model year of the auto. 4. For Model Years 2010 and prior, refer to the ISO Symbol and Identification Manual for the appropriate symbol of the auto. For Model Years 2011 and after, refer to the AIB Vehicle Rating Group Program to determine the appropriate Vehicle Rating Group of the auto. 5. Refer to Rule 20. to determine the base premium for rating vehicles for which a model year is not displayed on the rate pages. 6. Refer to Rule 22. to determine the base premium for rating vehicles for which a symbol is not shown on the rate pages. Refer to Rule 21.B. to determine the base premium for rating vehicles not assigned a Vehicle Rating Group. 10

10 7. Multiply by the appropriate Model year/symbol factor shown in the Model/Year Symbol pages or by the appropriate Model Year/VRG factor from the Model Year/Vehicle Rating Group pages for this coverage part. Round. 8. The costs to reduce the deductible and credits to increase the deductible are shown on the rate page. If applicable, determine premium change in deductible provision. Round. 9. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on our rating worksheet, page RW-2 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Substitute Transportation (Part 10) and Towing and Labor (Part 11) 1. Refer to Statewide rate pages by tier to determine base premium. The charge is per vehicle for automobiles and motorcycles based upon the desired coverage limit. 2. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on our rating worksheet, page RW-2 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Exceptions: See Rule 32. and Miscellaneous rate pages for premium calculation of Non-Symbolled or Non-Specific Vehicle Rating Group Pickups. See Rule 34. and Miscellaneous rate pages for premium calculation of Trailers. See Rule 39. and Miscellaneous rate pages for premium calculation of Motor Homes. See Rule 40. and Miscellaneous rate pages for premium calculation of Antique Motor Cars and Motorcycles. See Rule 43. and Miscellaneous rate pages for premium calculation of Low Speed vehicles. See Rule 46. and Miscellaneous rate pages for premium calculation of Excess Electronic Equipment Coverage. See Rule 50. Use of Other Automobiles. C. Motorcycles Tiers I-V Liability Coverages: Bodily Injury Liability (Part 1), Personal Injury Protection (Part2) and Property Damage (Part 4) 1. Refer to the Territory Definition pages to determine the territory code for the location where the motorcycle is principally garaged. 2. Refer to group definitions on the rate pages to determine the appropriate group classification applicable to each motorcycle. 3. Determine the base premium from the manual motorcycle rate page based upon the tier, territory and group classification for these coverage parts. 4. Multiply by the appropriate tier factor from Rule B. Round. 5. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on our Motorcycle rating worksheet, page RW-3 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/ class 15 discount. Optional Bodily Injury (Part 5) 1. Refer to the Territory Definition pages to determine the territory code for the location where the motorcycle is principally garaged. 2. Refer to group definitions on the rate pages to determine the appropriate group classification applicable to each motorcycle. 3. Determine the base premium from the manual motorcycle rate page based upon the tier, territory, group classification and whether or not guest coverage will be provided. 4. Multiply by the appropriate tier factor from Rule B. Round. 5. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on our rating worksheet, page RW-3 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. 11

11 Bodily Injury caused by an Uninsured Auto (Part 3), Bodily Injury caused by an Underinsured Auto (Part 12), and Medical Payments Coverage (Part 6). 1. Determine the base premium from the manual motorcycle rate page based upon the tier, group classification and amount of coverage desired for these coverage parts. 2. Multiply by the appropriate tier factor from Rule 26.1.B. Round. 3. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on our rating worksheet, page RW-3 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Physical Damage Coverages: Collision (Part 7) 1. Refer to the Territory Definition pages to determine the territory code for the location where the motorcycle is principally garaged. 2. Determine the motorcycle s value as original cost new in hundreds of dollars. 3. Multiply the value determined by the rate per $100 for its tier and territory.round. 4. Multiply by the appropriate tier factor from Rule B. Round. 5. Multiply by MC Age Factor. Round. 6. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on our rating worksheet, page RW-3 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Limited Collision (Part 8) Follow instructions for rating collision coverage above and charge 8% of the Collision base premium for the same $500 deductible option. The cost to reduce the deductible is shown on the rate page by tier by territory. Comprehensive (Part 9) 1. Refer to the Territory Definition pages to determine the territory code for the location where the motorcycle is principally garaged. 2. Determine the motorcycle s value in hundreds of dollars. 3. Multiply the value determined by the rate per $100 for its tier and territory. Round. 4. Multiply by the appropriate tier factor from Rule B. Round. 5. Multiply by MC Age Factor. Round. 6. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on our rating worksheet, page RW-3 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Substitute Transportation (Part 10) and Towing and Labor (Part 11) 1. Refer to Motorcycle Miscellaneous rate pages by tier to determine base premium. The charge is per vehicle for automobiles and motorcycles based upon the desired coverage limit. 2. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on our rating worksheet, page RW-3 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Exceptions: See Rule 32. and Miscellaneous rate pages for premium calculation of Non-Symbolled or Non-Specific Vehicle Rating Group Pickups. See Rule 34. and Miscellaneous rate pages for premium calculation of Trailers. See Rule 39. and Miscellaneous rate pages for premium calculation of Motor Homes. See Rule 40. and Miscellaneous rate pages for premium calculation of Antique Motor Cars and Motorcycles. See Rule 43. and Miscellaneous rate pages for premium calculation of Low Speed vehicles. See Rule 46. and Miscellaneous rate pages for premium calculation of Excess Electronic Equipment Coverage. See Rule 50. Use of Other Automobiles. C. Motorcycles Tier-V Liability Coverages: Bodily Injury Liability (Part 1), Personal Injury Protection (Part2) and Property Damage (Part 4) 12

12 1. Refer to the Territory Definition pages to determine the territory code for the location where the motorcycle is principally garaged. 2. Refer to group definitions on the rate pages to determine the appropriate group classification applicable to each motorcycle. 3. Determine the base premium from the manual rate page based upon the tier, territory and group classification for these coverage parts. 4. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on our Motorcycle rating worksheet, page RW-4 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/ class 15 discount. Optional Bodily Injury (Part 5) 1. Refer to the Territory Definition pages to determine the territory code for the location where the motorcycle is principally garaged. 2. Refer to group definitions on the rate pages to determine the appropriate group classification applicable to each motorcycle. 3. Determine the base premium from the manual rate page based upon the tier, territory, group classification and whether or not guest coverage will be provided. 4. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on our rating worksheet, page RW-4 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Bodily Injury caused by an Uninsured Auto (Part 3), Bodily Injury caused by an Underinsured Auto (Part 12), and Medical Payments Coverage (Part 6). 1. Determine the base premium from the manual rate page based upon the tier, group classification and amount of coverage desired for these coverage parts. 2. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on our rating worksheet, page RW-4 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Physical Damage Coverages: Collision (Part 7) 1. Refer to the Territory Definition pages to determine the territory code for the location where the motorcycle is principally garaged. 2. Determine the motorcycle s value in hundreds of dollars. 3. Multiply the value determined by the rate per $100 for its tier and territory. Round. 4. Multiply by MC Age Factor. Round. 5. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on our rating worksheet, page RW-4 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Limited Collision (Part 8) Follow instructions for rating collision coverage above and charge 8% of the Collision base premium for the same $500 deductible option. The cost to reduce the deductible is shown on the rate page by tier by territory. Comprehensive (Part 9) 1. Refer to the Territory Definition pages to determine the territory code for the location where the motorcycle is principally garaged. 2. Determine the motorcycle s value in hundreds of dollars. 3. Multiply the value determined by the rate per $100 for its tier and territory. Round. 4. Multiply by MC Age Factor. Round. 5. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on our rating worksheet, page RW-4 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. 13

13 Substitute Transportation (Part 10) and Towing and Labor (Part 11) 1. Refer to Miscellaneous rate pages by tier to determine base premium. The charge is per vehicle for automobiles and motorcycles based upon the desired coverage limit. 2. Multiply the premium determined above by any other applicable rating debit and credit factors as shown on our rating worksheet, page RW-4 of this manual. Premiums are calculated in the consecutive, cumulative order shown on the worksheet. Premiums are rounded after each step except after the age 65/class 15 discount. Exceptions: See Rule 32. and Miscellaneous rate pages for premium calculation of Non-Symbolled or Non-Specific Vehicle Rating Group Pickups. See Rule 34. and Miscellaneous rate pages for premium calculation of Trailers. See Rule 39. and Miscellaneous rate pages for premium calculation of Motor Homes. See Rule 40. and Miscellaneous rate pages for premium calculation of Antique Motor Cars and Motorcycles. See Rule 43. and Miscellaneous rate pages for premium calculation of Low Speed vehicles. See Rule 46. and Miscellaneous rate pages for premium calculation of Excess Electronic Equipment Coverage. See Rule 50. Use of Other Automobiles. RULE 12. WHOLE DOLLAR PREMIUM RULE The premium for each exposure shall be rounded at each step to the nearest whole dollar, separately for each coverage provided by the policy. A premium involving $0.50 or more shall be rounded to the next whole dollar at the end of each step. This does not apply to Part 5, 20/40 limits and Part 6, $5,000 limit where rates displayed in the manual may be used or rounded to the lower whole dollar. This procedure shall apply to all interim premium adjustments, including endorsements or cancellations at the request of the insured. In the case of cancellation by the company, the return premium may be carried to the next higher whole dollar. NOTE: The premium for each exposure means the premium developed for each coverage for each automobile after the application of all applicable discounts. RULE 13. INSTALLMENT PAYMENT OF PREMIUMS All motor vehicle insurance policy premium charges are due and payable on the effective date of the policy, subject to the provisions of the Deposit Premium Rule (Rule 14), unless an installment payment plan is used. RULE 14. DEPOSIT PREMIUM RULE A company, its producer or any broker may require deposit premium prior to the issuance of a policy provided the per vehicle deposit does not exceed 30% of the applicable annual premium for the insurance requested. If the applicant has been in default in the payment of any premium for automobile insurance or merit rating adjustment during the preceding 24 months, the entire policy premium charges are payable in advance. RULE 15. EMPLOYERS SUBJECT TO MASSACHUSETTS WORKERS COMPENSATION ACT Motor vehicles owned by an employer subject to the Massachusetts workers compensation law not used at any time to transport persons other than employees of the named insured shall be eligible for a 25% reduction in the Personal Injury Protection premium otherwise applicable. A vehicle which qualifies for this reduction is not eligible for any Personal Injury Protection deductible. RULE 16. DEDUCTIBLES - PARTS 7, 8 and 9 Deductibles, higher than the standard deductible, are available for Collision, Limited Collision and Comprehensive Coverages. Refer to Rate pages for parts 7, 8, and 9 by Tier for applicable factors. 14

14 RULE 19. DISCOUNTS Rule 19. Discounts are applicable to private passenger vehicles defined under Rule 27. See the Miscellaneous rate pages and rules for discounts applicable to Miscellaneous Type vehicles. A. Multi-Car- Not applicable in Tier V 1. A policyholder who owns two or more automobiles and purchases coverage from the same company for at least two such automobiles, shall be entitled to a 10 % reduction of the premium applicable to Coverage Parts 1, 2, 4, 5, 7, 8 and 9. At least two of the automobiles must be private passenger vehicles as defined in Rule 27, except that vehicles classified as antiques are not eligible. The premium reduction applies only to private passenger vehicles as defined in Rule The 10% reduction in premium as outlined in 1. above may also be applied if one private passenger auto is owned by the named insured(s) and a company vehicle is furnished to the named insured or resident spouse. A copy of the company car s registration must be provided. B. Anti-Theft Device Refer to Anti-Theft Devices Standards and Discounts Rule 54. C. Class 15 Premiums otherwise applicable to class 11, 12, 13, and 14 automobiles shall be reduced by 25% for insureds age 65 or older. If the principal operator becomes age 65 during the policy year, the class 11, 12, 13, and 14 premium must be adjusted as of that date. The premium adjustment shall be credited to the policyholder on that date unless that date is within sixty days of the expiration date of the policy, in which case the adjustment may be credited to the renewal policy. A notice of this classification change must be sent to the policyholder either prior to or with the proposed adjustment. The policyholder is required to notify the company of any change in operator usage which would affect entitlement to the discount. The 25% discount is applied to the final premium for each part after all other discounts and rating factors have been completed. It is the last step in the rating process prior to the application of the merit rating plan adjustment. D. Annual Mileage Discount A discount of the premium paid for Parts 1, 2, 3, 4, 5, 6, 7, 8 and 12 will be given to eligible policyholders on request, when the annual mileage of the vehicle falls into one of two categories. The discount will be based on the actual mileage driven in the previous policy year as determined by a comparison of two odometer readings, at least six months apart, from Registry of Motor Vehicle information or the Annual Mileage Discount Form and other standard automobile insurance forms available to the company. Refer to the Miscellaneous Rating Factors page by Tier for the applicable categories and discounts. 1. Eligibility The vehicle must be a private passenger vehicle as defined in Rule 27, except that vehicles classified as Antiques are not eligible. The company may request that the applicant for the discount complete the Annual Mileage Discount Form for the verification of eligibility for the discount. 2. Verification The company may use the odometer readings provided by the applicant on the Annual Mileage Discount Form or other standard forms available to the company, in order to verify the mileage driven in the past year. The company shall compute the annualized difference between the odometer reading at the time of application and the previous odometer reading to determine eligibility. If a vehicle replaces a vehicle which is receiving the discount, the annual mileage of the prior vehicle will be attributed to the replacement vehicle. The company may use information from the Vehicle Inspection System of the Registry of Motor Vehicles to verify annual mileage. The difference in the two most recent odometer readings reported by the Registry, if at least six months apart, shall be annualized to determine eligibility for the discount. If the Registry reports 20

15 only one reading, which is more than six months before the application for the discount, the applicant may provide a current odometer reading on the Annual Mileage Discount Form, and the difference shall be annualized to determine eligibility. If two odometer readings, at least six months apart, are not available to the company through the Registry of Motor Vehicles, the Annual Mileage Discount Form or other standard forms, the vehicle is not eligible for the annual mileage discount. 3. Application of Discount The applicable discount applies to rates otherwise determined for each insured vehicle by; a. coverage, limits purchased, territory, driver class, and model year and symbol for model years 2010 and prior or, b. by coverage, limits purchased, territory, driver class, and model year and Vehicle Rating Group for model years 2011 and greater, prior to the application of the merit rating plan adjustment. E. Passive Restraint Discount- Not applicable in Tier V A 25% discount of the premium paid for Parts 2, 3, 6 and 12 will be given to eligible policyholders for qualifying vehicles which contain occupant safety features approved by the Commissioner of Insurance. These features are: an airbag installed for either the driver s seating position or both front outboard designated seating positions or an automatic seatbelt installed for either the driver s seating positions or both front outboard designated seating positions. F. Preferred Operator Discount-Not applicable to Tier V On a renewal policy, a 4% premium credit is applied against all coverage parts on a per vehicle basis where a premium is shown on the coverage selections page for that vehicle. In order to be eligible for the credit the vehicle must be: Rated in classes Have Bodily Injury limits, Part 5, equal to or above $50,000 per person. The rated operator must have a merit rating code of 99 (Excellent Driver Discount Plus), 98 (Excellent Driver Discount) or 00 (Neutral). This discount applies to vehicles as defined under Rule 27. G. Account Credit-Not applicable to Tier V A 10% premium credit is applied against all coverage parts on a per vehicle basis where a premium is shown on the coverage selections page for that vehicle. For the purposes of this discount, vehicle includes personal automobiles, miscellaneous vehicles, trailers and motorcycles. To be eligible for the premium credit, the Named insured must have a supporting homeowners policy (all policy forms) that is written with Quincy Mutual, The Andover Companies, (Merrimack Mutual, Cambridge Mutual or Bay State) or MPIUA (FAIR Plan). This discount does not apply to Use of Other Auto coverage. H. Good Student Discount- Not applicable in Tier V A 5% Good Student Discount applies to all coverage parts when the rated operator is an inexperienced operator, driver classifications17,18,20,21,25, or 26, is a full time high school, college or university student and meets one of the following requirements: Is in the top 20% of his/her class or has been recognized on a Dean s list or honor roll. Has maintained at least a B average in a letter grading system or a 3.0 average in a 4 point system or any equivalent. If the operator is home schooled, evidence of scoring in the top 20% of standardized national exams or a third party certification indicating that the student has met the requirements stated above are acceptable. 21

16 The company must be presented certification signed by a school official that verifies the operator s academic achievements when the discount is requested and at subsequent renewals in order for the discount to be applied. This discount applies to vehicles as defined under Rule 27. I. Student Away From Home Discount- Not applicable in Tier V A 5% credit will be applied to all coverage parts when the rated operator meets the following criteria: The rated operator is an inexperienced operator, driver classes 17, 18, 20, 21, 25 or 26. The rated operator is student residing at an educational facility over one hundred road miles from the autos place of garaging, The rated operator does not have regular access to any covered vehicle shown on the coverage selection page. Policies with the Student Away From Home Discount will renew without the discount. In order for the discount to be applied, the Named Insured or rated operator must confirm that the rated operator continues to be eligible. The company may require written confirmation. This discount applies to vehicles as defined under Rule 27. J. Continuously Insured Discount A 10% discount will be applied to coverage parts 1, 2, 4 and 5 on a per vehicle basis when the rated operator has been continuously insured without a lapse in coverage during the 12 months preceding the effective date of the policy. A rated operator is considered continuously insured if the operator was the named, listed, or rated insured on an automobile insurance policy for the 12 months preceding the effective date of the policy. For new policies, proof of continuous coverage may be required under certain circumstances when the company is unable to substantiate or verify 12 months of continuous insurance coverage. The discount will automatically be applied at renewal provided the policy was in effect for 12 continuous months. This discount applies to vehicles as defined under Rule 27. K. Good Driver Discount (This is the equivalent to Low Frequency Discount in the MAIP program.) A 10% discount will be applied to coverage parts 1,2, 4 and 5 on a per vehicle basis when the rated operator has no more than 4 merit rating points reported by the Merit Rating Board as provided by Rule 56, Merit rating Plan. This discount applies to vehicles as defined under Rule 27. L. Superior Client Discount- Not applicable in Tier V A 7% premium credit is applied against all coverage parts on a per vehicle basis where a premium is shown on the coverage selections page for that vehicle. In order to be eligible for the credit the vehicle must be: Rated in classes Have Bodily Injury limits, Part 5, equal to or above $250,000 per person. The rated operator must have a merit rating code of 99 (excellent driver discount plus). This discount applies to vehicles as defined under Rule 27. M. Early Issue Client Discount- Not applicable in Tier V A 5% premium credit will be applied against all coverage parts on a per vehicle basis where a premium is shown on the coverage selections page for that vehicle. In order to be eligible for the credit the policy must be: New business to Quincy Mutual Be entered for issuance into Quincy On-Line at least 5 days prior to the effective date or received at Quincy Mutual in paper format at least 5 days prior to the effective date All vehicle types except trailers This discount will be applied to new business for one year only. 22

17 N. One Pay Plan Discount A 5% premium credit will be applied against all coverage parts on a per vehicle basis when a One Payment Billing Plan is chosen, subject to the following: For new business policies, payment must be made in full upon the initial down payment. For renewal policies, payment must be made in full upon the first installment due date. The policy must not be paid by a finance company. This discount applies to all vehicle types on a policy. O. Qualified Book Transfer credit- Not applicable in Tier V A 4% premium credit will be applied against all coverage parts on a per vehicle basis for any qualified book transfer meeting the underwriting rules established by the company. The discount will be subject to the following criteria: The book transfer was prearranged and agreed upon by the company and agency. The discount will apply for one year only. This discount applies to all vehicle types on the policy. P. Household Member / Family Account Discount Progam- Not applicable in Tier V Quincy Mutual will the extend eligibility of: The Account Credit as shown in paragraph G.;and The Multi Car Discount as shown in paragraph A; to any automobile policy we insure for household members subject to the following criteria: The household member meets the definition in the MA Auto policy; and The household member is listed as a deferred operator on the original or primary insured s Quincy Mutual policy. In addition, the tier assignment from Rule A. will reflect the extended eligibility for the account credit and multi car discounts. All other aspects of the tier assignment will remain the same. Rule 20. MODEL YEAR RATING Model Year Defined The model year of an auto is used in rating physical damage coverage on an actual cash value basis. The model year of the auto is the year assigned by the auto manufacturer. The model year of rebuilt or structurally altered autos is determined by the model year of the chassis. 23

18 Material Misrepresentation 1.5 (1.2) 1.5 (1.2) Salvage Title Coverage not available NOTE: For the first instance of a material misrepresentation in the application for insurance, the lower indicated factor may be used, at the option of the company. Application of Factors A. Single Vehicle Policies Where more than one category applies to the same operator or vehicle, the highest applicable factor shall be used respectively for Collision and Comprehensive. For example, if a listed operator is convicted of vehicular homicide and also has a high-theft vehicle, the factor for both Collision and Comprehensive is 1.5. The factors do not compound. In cases where separate policies are issued by the same insurer to the common owner of two or more vehicles, the highest applicable factors for Collision and Comprehensive shall be assigned to the vehicle with the highest premium for Collision and Comprehensive respectively. For each subsequent vehicle, the next highest applicable factor shall be assigned to the next highest premium for Collision and Comprehensive respectively, etc. If one or more of the extra-risk categories of insurance fraud, auto theft or material misrepresentation apply to such common owner, the applicable factor shall be used for both Collision and Comprehensive for each insured vehicle. B. Multi-Vehicle Policies The highest applicable factors for Collision and Comprehensive shall be assigned to the vehicle with the highest premium for Collision and Comprehensive respectively. Each subsequent vehicle shall be assigned the next highest applicable factor and so forth. If one or more of the extra-risk categories of insurance fraud, auto theft or material misrepresentation apply to the insured owner, the applicable factor shall be used for both Collision and Comprehensive for each insured vehicle. RULE 25. VEHICLE SERIES RATING (Applicable to Model Years 2010 and Prior) Vehicle Series Rating (VSR) is a program applied by the Insurance Services Office (ISO) to adjust the Price New Symbols of vehicles to increase or decrease the symbol due to loss experience reflecting crash damage, ease of repair, cost of repair parts, and theft for the particular vehicle, resulting in the Rating Symbol. The Rating Symbol is used to determine a vehicle s premium for Collision, Limited Collision and Comprehensive coverage. The VSR program reviews the symbol assignments for all vehicle series up to five times: when the model year is introduced and in each of the subsequent annual VSR review years. The symbol for a particular series may be upsymbolled, downsymbolled, or may remain the same. Reassignment of symbols shall be effective with 2006 and subsequent model year vehicles and may only be applied at policy issuance or renewal. A policy shall not be changed mid-term solely due to a change in symbol assignment based on symbol review. RULE 26.1 TIER ASSIGNMENT This rule applies to all vehicle types. A. DeterminingThe Assigned Tier Tier assignment is determined at the policy s inception, at renewal and when a policy is endorsed. Tier assignments are on a policy level but determined by evaluating policy and operator characteristics. To determine the tier begin by identifying the risk characteristics for each policy and rated operator. Apply the characteristics to the tier definition shown below in consecutive order. If a policy or rated operator does not meet the requirement of a tier, continue onto the next tier until a tier has been determined. Tier I. Corresponding Account with Personal Umbrella Liability Endorsement. 1. The Named insured must have a supporting homeowners policy (all policy forms) that is written with Quincy Mutual, The Andover Companies, (Merrimack Mutual, Cambridge Mutual or Bay State) and; 2. Have a Personal Umbrella Liability Endorsement attached to the Homeowners policy and; 3. Have 3 or fewer intent -to- cancel notices in each of the last three years. 27

19 Tier II. Corresponding Account 1. The Named insured must have a supporting homeowners policy (all policy forms) that is written with Quincy Mutual, The Andover Companies, (Merrimack Mutual, Cambridge Mutual or Bay Sate) or MPIUA (Fair Plan) and; 2. Have 3 or fewer intent -to- cancel notices in each of the last three years. Tier III. Renewal Policies-(without a supporting homeowners and or personal umbrella.) Tier IV. 1. Any policy that has been insured with Quincy Mutual for more than one continuous year that does not have a supporting account or supporting account with an umbrella; and 2. Has three or fewer intent -to- cancel notices in each of the last three years. 1. New Business Policy With: a. Continuously Insured Rated Operator; or b. Multiple vehicles or the Multi-Car Discount has been applied; or 2. Renewal Policy with four or more intent -to- cancel notices in any one of the previous three years. A rated operator has been continuously insured if they have been without a lapse in coverage during the 12 months preceding the effective date of the policy. A rated operator is considered continuously insured if the operator was the named, listed, or rated insured on an automobile insurance policy for the 12 months preceding the effective date of the policy. Tier V. Basic Tier- New Business Policy- All Other *This tier includes any rated operator not otherwise eligible for Tiers I through IV. The basic tier will be made up of new policies that are not supported by a homeowner policy and are single car policies where the rated operator is not continuously insured. B. Tier Rating Factor Apply the appropriate tier factor below to the base premiums as shown on the appropriate rating worksheet from pages RW 1-6 and in accordance with Rule. 11. Premium Determination. The factor applies to all coverage parts on a per vehicle basis for which a premium is shown on the coverage selections page. Tier I Tier II Tier III Tier IV Tier V See Tier V rate pages. RULE 26.2 RISK UNDERWRITING FACTOR- Not applicable in Tier V This rule applies to private passenger vehicles as defined in Rule 27. A Risk Underwriting Factor will be applied to each vehicle based upon an evaluation of policy and operator risk characteristics. The Risk Underwriting Factor is applied to the Base Premiums as shown in Rule 11. Premium Determination Rule. The rating sequence is shown on our Rating worksheet page RW-1. The factor applies to all coverage parts on a per vehicle basis for which a premium is shown on the coverage selections page. The Risk Underwriting Factor is determined at policy inception and will be updated upon renewal and when a policy is endorsed. The Risk Underwriting Factor will be determined based upon the following six criteria: 28

20 Tier II. Corresponding Account 1. The Named insured must have a supporting homeowners policy (all policy forms) that is written with Quincy Mutual, The Andover Companies, (Merrimack Mutual, Cambridge Mutual or Bay Sate) or MPIUA (Fair Plan) and; 2. Have 3 or fewer intent -to- cancel notices in each of the last three years. Tier III. Renewal Policies-(without a supporting homeowners and or personal umbrella.) Tier IV. 1. Any policy that has been insured with Quincy Mutual for more than one continuous year that does not have a supporting account or supporting account with an umbrella; and 2. Has three or fewer intent -to- cancel notices in each of the last three years. 1. New Business Policy With: a. Continuously Insured Rated Operator; or b. Multiple vehicles or the Multi-Car Discount has been applied; or 2. Renewal Policy with four or more intent -to- cancel notices in any one of the previous three years. A rated operator has been continuously insured if they have been without a lapse in coverage during the 12 months preceding the effective date of the policy. A rated operator is considered continuously insured if the operator was the named, listed, or rated insured on an automobile insurance policy for the 12 months preceding the effective date of the policy. Tier V. Basic Tier- New Business Policy- All Other *This tier includes any rated operator not otherwise eligible for Tiers I through IV. The basic tier will be made up of new policies that are not supported by a homeowner policy and are single car policies where the rated operator is not continuously insured. B. Tier Rating Factor Apply the appropriate tier factor below to the base premiums as shown on the appropriate rating worksheet from pages RW 1-6 and in accordance with Rule. 11. Premium Determination. The factor applies to all coverage parts on a per vehicle basis for which a premium is shown on the coverage selections page. Tier I Tier II Tier III Tier IV Tier V See Tier V rate pages. RULE 26.2 RISK UNDERWRITING FACTOR- Not applicable in Tier V This rule applies to private passenger vehicles as defined in Rule 27. A Risk Underwriting Factor will be applied to each vehicle based upon an evaluation of policy and operator risk characteristics. The Risk Underwriting Factor is applied to the Base Premiums as shown in Rule 11. Premium Determination Rule. The rating sequence is shown on our Rating worksheet page RW-1. The factor applies to all coverage parts on a per vehicle basis for which a premium is shown on the coverage selections page. The Risk Underwriting Factor is determined at policy inception and will be updated upon renewal and when a policy is endorsed. The Risk Underwriting Factor will be determined based upon the following six criteria: 28

21 Minimum years licensed of all operators listed on the policy(including deferred and excluded) Years licensed of the assigned operator Count of number of operators listed on the policy (including deferred and excluded) Policy status new or renewal Presence of a deferred operator on the policy Minimum infraction count of at fault accidents and traffic violations for all operators listed on the policy. The experience period for infractions is the six years immediately preceding the effective date of the policy. To determine your Risk Underwriting Factor, find the description above one of the following three tables that meets the policy characteristics. The years of driver experience is based upon a listed operators date first licensed. The number of years licensed will be determined by the number of full years the operator has held a valid driver s license as of the effective date of the policy. If the minimum years of driving experience for ALL operators listed on a policy is 12 to 45 years, apply the Underwriting factors as follows: Criteria Factor Assigned operators with years of experience 1.00 Assigned operators with 20 + years of experience and 1.00 only one operator listed Assigned operators with 20 + years of experience and or more operators listed and no infractions for any listed operator Assigned operators with 20 + years of experience and or more operators listed with 1 or more infractions for any operator listed If the minimum years of driving experience for ALL operators listed on a policy is 46 or greater, apply the Underwriting factors as follows: Criteria Factor Assigned operators with years of experience.99 New Business with Assigned operators with 1.08 > 55 years of experience Renewal Business with Assigned Drivers with 1.08 > 55 years of experience and only one operator listed on the policy Renewal Business with Assigned operators with > years of experience and no deferred operators and 2 or more listed operators on the policy Renewal Business with Assigned operators with > years of experience and having a deferred operator If the minimum years of driving experience for ANY operator listed on a policy is <12, apply the Underwriting factors as follows: Criteria Factor Assigned operators with years of experience.99 New Business with Assigned operators with <20 or > years of experience Renewal Business with Assigned operators with <20 or > years of experience and no deferred operators and only one operator listed on the policy Renewal Business with Assigned operators with <20 or > years of experience and no deferred operators and 2 or more operators listed on the policy Renewal Business with Assigned operators with <20 or 1.00 > 55 years of experience and having a deferred operator and 2 or more operators listed on the policy. 29

22 SECTION II - PRIVATE PASSENGER AUTOMOBILES RULE 27. PRIVATE PASSENGER DEFINITION A. A motor vehicle of the private passenger or station wagon type that is owned or leased under contract for a continuous period of at least twelve months by one or more individuals, excluding (1) partnerships, (2) corporations, (3) unincorporated business associations, and (4) other legal business entities with a federal employer identification number, and is not used as a public or livery conveyance nor rented to others. A vehicle which meets the conditions of Rule 31, regarding the transportation of fellow employees, students or others for consideration, is included in this definition, provided such vehicle is not registered for carrying passengers for hire. B. A motor vehicle that is a pick-up or van, that is owned or leased under contract for a continuous period of at least 12 months by one or more individuals, excluding (1) partnerships, (2) corporations, (3) unincorporated business associations, and (4) other legal business entities with a federal employer identification number, and 1. has a gross vehicle weight rating of less than 10,000 pounds or has a rating symbol assigned to it (for model years 2010 and prior) by the Insurance Services Office (ISO) or a Vehicle Rating Group (for model years 2011 and greater)by the Automobile Insurers Bureau (AIB), and 2. is not used for the delivery or transportation of goods or materials unless such use is incidental to the insured s business of installing, maintaining or repairing furnishings or equipment. C. Gross Vehicle Weight Rating means the value specified by the manufacturer as the loaded weight of a single vehicle. D. At the option of the company, an eligible vehicle under this rule whose title has been transferred to a trust may be written under the Massachusetts Automobile Insurance Policy, subject to the following requirements: the grantor of the trust must be an individual or lawfully married individuals residing in the same household, and must be the only insured(s) named in Item 1 of the Coverage Selections Page. All vehicle(s) insured under the policy must be owned by the trust. A vehicle owned by a trust in which the grantor is a partnership or corporation must be written under a commercial auto policy. If a motor vehicle is leased as described in the foregoing paragraphs, and the lessee is obtaining the insurance, the policy must be issued to the lessee as named insured and Endorsement M-0070-S, Coverage For Anyone Renting An Auto To You, must be attached to the policy. RULE 28. PRIVATE PASSENGER CLASSIFICATIONS A. Operator Classes *10 Experienced Operator- (Tier V only)- The operator has been licensed at least 6 yrs and is under the age of 65 and the automobile is not used in the occupation, profession or business of the insured. *11 Experienced Operator-The Operator has been licensed at least 6 yrs but less than 10 and is under the age of 65 and the automobile is not used in the occupation, profession or business of the insured. This is Class 10 in Tier V. *12 Experienced Operator-The Operator has been licensed at least 10 years but less than 15 and is under the age of 65 and the automobile is not used in the occupation, profession or business of the insured. This is Class10 in Tier V. *13 Experienced Operator-The Operator has been licensed at least 15 years but less than 20 and is under the age of 65 and the automobile is not used in the occupation, profession or business of the insured. This is Class 10 in Tier V. *14 Experienced Operator-The Operator has been licensed at least 20 years and is under the age of 65 and the automobile is not used in the occupation, profession or business of the insured. This is Class 10 in Tier V. 32