Funds Transfer Pricing ALMIS Webinar 20 December 2011

|

|

|

- Katherine Barker

- 6 years ago

- Views:

Transcription

1 Funds Transfer Pricing ALMIS Webinar 20 December 2011 A way forward using ALMIS Joe Di Rollo Dean Carter

2 Introduction FTP Webinar FTP - What does it mean for firms A way forward using ALMIS Q & A

3 Introduction What is transfer pricing Banking crisis Strengthening Liquidity Risk adjusted cost of capital Regulation scrutiny Relevance for ALMIS

4 FTP What does it mean for firms Dean Carter Associate Director, ALMIS International

5 FTP - What is it? Definition of 'Funds Transfer Pricing FTP 'A method used to individually measure how much each source of funding is contributing to overall profitability. The funds transfer pricing (FTP) process is most often used in the banking industry as a means of outlining the areas of strength and weakness within the funding of the institution. FTP can also be used to indicate the profitability of the different product lines and each staff member, as well as act as a great medium for comparison between employees, branches, etc. (investopedia 2011) Or A method of measuring the performance of mortgages, conducted by an internal model which determines the value or rate of return that each unit contributes to profitability.

6 FTP Ernest & Young Product pricing Risk return based Product pricing Products priced on market benchmarks Basis for differential product pricing Profitability management Ability to centrally control NIM Control cost of funds Set targets for interest income and fee based income FUNDS TRANSFER PRICING OBJECTIVES Balance sheet management Manage structural liquidity mis-matches Transfer interest rate risk and liquidity risk to a central unit Re-allocate capital based on risk-weighted performance parameters Liquidity Management Net liquidity across the business units Fund liquidity mis-matches at optimal costs Centralise the deployment of surplus liquidity

7 FTP What does it mean to the FSA? The overriding focus of the FSA is to ensure firms have a sustainable business model Their current focus is on Funds Transfer Pricing They, as always, start from a position of best in class which means they look at very comprehensive models in big institutions (which may not always be relevant to all firms!) What they will want from building societies is; Appropriate models proportionate to the businesses complexity, and Risk Profile Engagement and understanding from Boards, ALCO s and senior management

8 FTP What is it? It means different things to different institutions For HSBC it will mean many things and they will have many versions For a medium sized building society it will not be completely straight forward, but much less complicated than HSBC For a building society on the administered approach it will be a very simple structure, but will still be relevant

9 FTP What is it? The following four types of FTP methodologies are utilized by the financial institutions: 1. Single Pool Rate Matching utilizes one rate to credit all fund providers and debit all fund users, respectively. This rate might be the weighted average cost of funds for the reporting institution, prime rate, or some other capital market rate. The single pool approach is simple, but does not take into consideration any maturity or imbedded risk characteristics. 2. Specific Matching is a mostly academic approach. The objective of specific matching is to match every specific liability with every specific asset of an equal amount, maturity and imbedded risk characteristic. 3. Multiple Pool Rate Matching is an extension of single pool rate transfer pricing. Essentially, each side of the balance sheet is split into pools of assets and liabilities sorted by criteria such as maturity characteristic, rate and yield, imbedded risk, or credit factors. Then the pools from each side of the balance sheet are matched to the opposite side of the balance sheet to establish a related funds charge or credit.

10 FTP What is it? The following types of FTP methodologies are utilised by the financial institutions: 4. Matched Maturity is basically a gap approach. Each individual customer account is matched to a market driven index such as the Treasury Yield Curve, the swap curve, or LIBOR (London Inter-Bank Offer Rate) based curve. Transfer pricing rates should represent the alternative opportunity rate for the bank s sources or use funds and vary according to repricing term and other attributes. The Matched Maturity has become the preferred approach to Funds Transfer Pricing because: Business units are more willing to accept FTP when transfer prices have a transparent, rational basis and are applied consistently throughout the organizational structure and across timelines. Marginal spread for each product is accurately measured The earning attributable to interest rate mismatching is correctly identified Each product spread is independent of any other balance sheet element

11 FTP Why use it? FTP helps financial institutions to allocate margin, better understand where profits come from, isolate and manage the interest-rate risk component of the margin. An effective FTP analysis enables a firm to increase profitability by: 1. Evaluating alternative investment/mortgage and funding decisions 2. Improving the strategic allocation of resources 3. Helping to identify high-performing products, segments, channels 4. Enhancing understanding of poor-performing products, segments, Channels 5. Making better pricing decisions 6. Evaluating the performance of the treasury group 7. Improving the planning budgeting process (Levey, 2008). 8. Ensure liquidity risk is priced into products and the decision making process

12 FTP What needs to be addressed? Building Societies need to ensure they remain competitive whilst retaining an adequate margin and controlling the risk life is a compromise: 1. Margin Management control over the margin including comprehensive reporting and forecasting help maintain Net Interest Income 2. Product Pricing ensuring all elements of running the business are included in product pricing (Liquidity costs are central to the FSA s focus). Especially the cost of liquidity, the costs of managing risk and the relevant level of sustainable profitability 3. ALM ensuring capital is deployed most effectively (in line with risk weighted performance measurements), and interest rate mis-matches are adequately controlled 4. Liquidity management ever more important (since the credit crunch) and a current focus of the FSA. Ensuring borrowed short and lent long doesn t come home to bite you in normal times and stressed environments!!

13 Typical Policy Considerations? What is the minimum rate of return for a mortgage product? What is the minimum rate this product is profitable at? Who decides on the hurdle rate? Should it be a Board policy decision? FD or Executive Committee Who manages the process Marketing, Treasury, FD, Finance Dept.? Should it be a Margin Committee? Does it pass a minimum hurdle rate? Will there be different pricing models for the different types of mortgages? Will there be different pricing models for the different types of channel? How will a Fixed Rate Mortgage be treated if the policy is not to hedge it? What happens if it is priced un-hedged and then hedged Can the pricing be adjusted relevant to business conditions? For example, what happens if no more FRM can be written, but other types do not meet the hurdle rate If the years profit target has been met, can the hurdle rate be lowered?

14 Typical Model What is included in the price? Product type During product Post product Category House purchase Re-mortgage Rollover BTL LTV Term Base Rate SVR/Tracker Rate Product Rate Inflows Expected Actual Hedging Channel Swap rate Percentage hedged % Direct % Indirect Fee income/costs Product fee Application fee Broker fee Legal fees Valuation fee MIG fee Expected loss charge Capital Weighting Amount required Funding Type a /b split Average v marginal Liquidity costs Cash flows Mortgage Pipeline Average balance Income in / out Cash flows - Admin Marketing costs Admin costs Branch costs Sales costs

15 FSA View Funds Transfer Pricing The importance of pricing liquidity risk derives from our Principles for Businesses 3: 'a firm must take reasonable care to organise and control its affairs responsibly and effectively, with adequate risk management systems'. Importance for firms of focusing on FTP as part of the preparation for their Individual Liquidity Adequacy Assessment (ILAA). The need for the pricing of liquidity risk is set out in BIPRU and this review yielded insights into current state and future development of firms FTP processes. Liquidity stresses are low frequency, but extreme severity events, which firms have historically neglected, in the interests of short run efficiencies. We aim to reduce risks to the UK financial system by encouraging more resilient, sustainable business models. The thematic review covered FTP practices pertaining to liquidity and asset liability management (ALM) risk, NOT, other common uses of FTP, for instance fixed cost contribution accounting, taxation and credit and operational risk pricing.

16 FSA View Key Messages The key messages for senior management are : FTP is a regulatory requirement and an important tool in the management of firms balance sheet structure, and in the measurement of risk adjusted profitability and liquidity and ALM risk. By attributing the cost, benefits and risks of liquidity to business lines within a firm, the FTP process strongly influences the volume and terms upon which business lines trade in the market and promotes more resilient, sustainable business models. Whilst firms are making progress in addressing FTP shortcomings, there is still more to do before FTP is effectively utilised to drive business strategy in line with firm wide objectives. Good practice was most in evidence in firms where senior management took a direct interest in their firm's FTP regime, with a view to harnessing it to achieve strategic objectives.

17 P&L attribution FSA View Summary Conclusions Many firms did not attribute some elements of the costs, benefits and risks of liquidity to business lines, instead holding costs at the centre. This acted to blunt the signalling of the same to business lines and thus compromised incentives and the progression of strategic objectives. FTP granularity Of the costs, benefits and risks that were attributed, most firms did not apply FTP to a sufficiently granular level to effectively incentivise business transaction decision makers. This was observed both in the attribution of centrally generated funding costs and of the cost of holding liquid asset buffers. This again acted to blunt the signalling of costs, benefits and risks of liquidity to business lines. FTP consistency Most firms did not apply consistent FTP methodologies across constituent businesses. Therefore an asset, liability or off balance sheet risk could be priced differently, simply on the basis of where it arose in the firm. In turn this skewed business incentives and behaviours to the detriment of the overall firm. In addition, this could convey confusing signals to the market, which in turn would harm the firm s franchise.

18 Responsiveness of FTP FSA View Summary Conclusions Many firms relied on offline systems requiring manual intervention or simplistic assumptions in order to implement their FTP regime. Offline processes make the FTP system less amenable to effective oversight and less responsive in volatile markets, due to the time taken to generate information manually. This heightened the risk of inaccurate pricing of liquidity and weakened the signalling of the costs, benefits and risks of liquidity to business lines and the FTP regime s impact on business line behaviours. FTP as a business signalling and strategic tool Many firms charged FTP by reference to the weighted average cost of funding already on balance sheet or weighted average cost of funding projected in annual budgetary processes. There was no additional overlay allowing senior management to adjust FTP rates to incentivise or discourage particular business activities based on a forward looking management view or in response to current inventory or risk levels. Furthermore, there was no consideration regarding the marginal cost of funding for the firm when appropriate. The cost was expressed as a reference rate + spread, which was then applied to business line balance sheets. Attribution did not differentiate between long and short dated balance sheet items.

19 FSA View Summary Conclusions FTP as a business signalling and strategic tool (contd.) These features risked mispricing liquidity, particularly in volatile markets, leaving firms vulnerable to conditions witnessed in the past two years. Effective use of FTP as a business signalling and strategic tool was most in evidence in firms where senior management took a direct interest in their firm's FTP processes, with a view to harnessing it to further strategic objectives. Furthermore the use of a weighted averaging methodology applied to business line balance sheets, irrespective of duration, entailed the cross subsidisation of longer dated risk at the expense of shorter dated risk, since the weighted average cost did not discriminate between these. All other things being equal, longer dated assets present greater risk than short dated assets, yet the weighted averaging methodology makes no distinction between them. This therefore has the potential to skew business incentives and behaviours to the detriment of the overall firm.

20 FSA View Summary Conclusions Stress testing processes and off balance sheet risk Some firms either did not price all undrawn off balance sheet contingent commitment types to which they were exposed, or else applied unsubstantiated charges to them. Therefore, business lines risked writing options for customers at levels where the risk was not commensurate with rewards, skewing business incentives and behaviours to the detriment of the overall firm. This was at least in part borne out of: the lack of comprehensive stress and scenario testing to inform risk appetite for undrawn off balance sheet commitments; and an ad hoc approach to reviews of behavioural models. Our Conclusion FTP is firmly on the FSA radar, and is good strategic and risk management practice However, it needs to be clear, well thought out and appropriate for the size and type of business There is no right answer, nor is there a simple generic model to employ, but there is a common theme

21 Objectives of an FTP system Highly flexible to fit in with institutions own business model / business strategy Robust calculation of cost of liquidity, cost of capital and term structure of interest Forward looking Capable of back testing

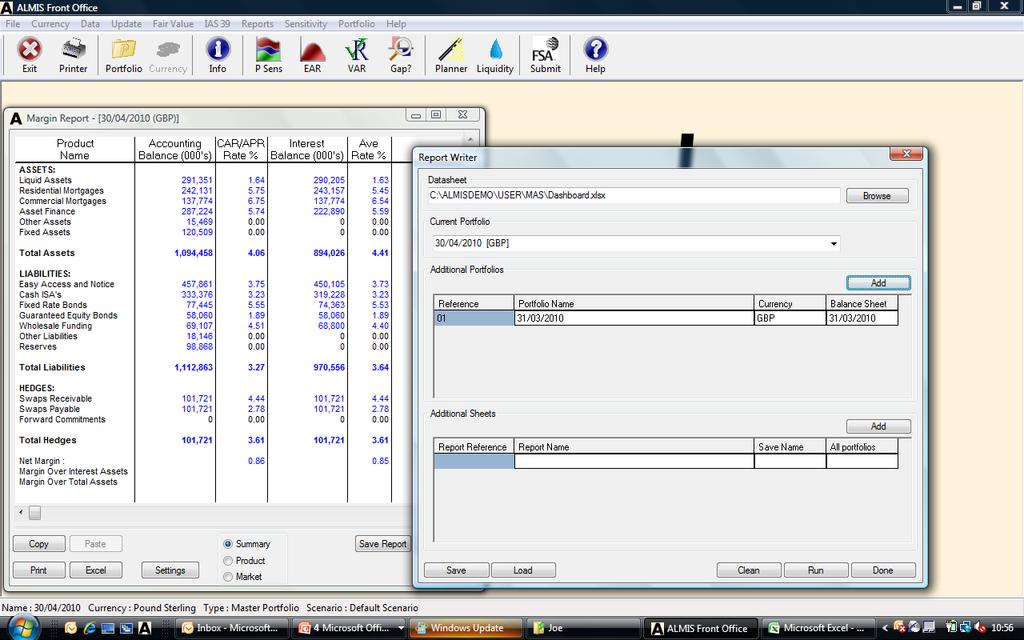

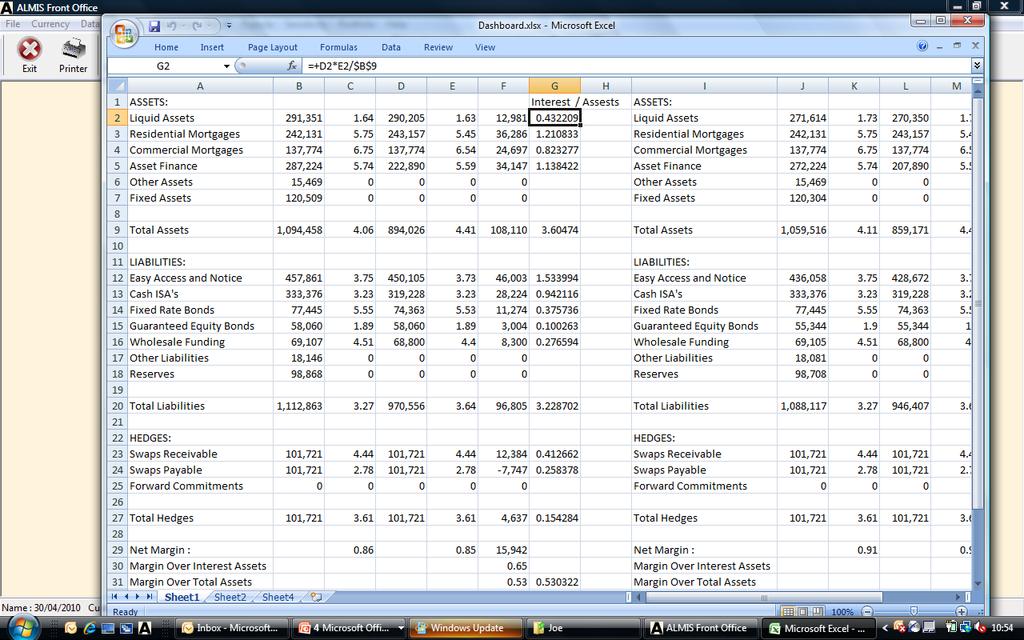

22 ALMIS Report Writer Overview

23 Objectives Allow users to view summary data from multiple portfolios, multiple currencies, multiple reports in one customisable document. Allow it to be easily updated every day, week or month with different data, including forward data Allow it to show trends in data Allow ALMIS clients to easily share reporting templates

24 Quick Guide Report Writer takes data from ALMIS reports Using OLE and Excel s Names to dynamically link ALMIS data into a spreadsheet template. Uses Excel to present data

25 Types of Name Cell Range Whole Report

26 Naming Convention

27 Naming Convention

28 Row Titles

29 Row Titles

30

31

32 Title 001 Margin and Balance Sheet by Summary 002 Margin and Balance Sheet by Product 003 Margin and Balance Sheet by Market 004 Basis Risk 005 FSA Basis Risk 006 FSA Gap Report 007 Custom Repricing Gap report 008 Custom Maturity Gap Report 009 FSA017 Gap Report Title 021 Interest Repricing Exposure Detail P1 022 Interest Repricing Exposure Detail P2 023 Interest Repricing Exposure Detail P3 024 Maturity Exposure Summary P1 025 Maturity Exposure Summary P2 026 Maturity Exposure Summary P3 027 Maturity Exposure Detail P1 028 Maturity Exposure Detail P2 029 Maturity Exposure Detail P3 Title 061 Counterparty Risk report by Sector - Summary 062 Counterparty Risk report by Sector - Detail 063 Loan to Value by Lend Code 064 Loan to Value by Category 065 Loan to Value by Product 066 Value in Arrears by Lend Code 067 Value in Arrears by Category 068 Value in Arrears by Product 069 Percentage of Loans in Arrears by Lend Code 010 FSA FSA Exposure Summary Report 030 Repricing Break Even Cumulative Summary P1 070 Percentage of Loans in Arrears by Category 031 Repricing Break Even Cumulative Summary P2 071 Percentage of Loans in Arrears by Product 032 Repricing Break Even Cumulative Summary P3 072 Fair Value Swaps - Summary 013 Repricing Gap Cumulative 014 Repricing Gap Periodic 015 Maturity Gap Cumulative 016 Maturity Gap Periodic 017 Basis Gap 018 Interest Repricing Exposure Summary P1 019 Interest Repricing Exposure Summary P2 020 Interest Repricing Exposure Summary P3 033 Repricing Break Even Cumulative Detail P1 034 Repricing Break Even Cumulative Detail P2 035 Repricing Break Even Cumulative Detail P3 036 Repricing Break Even Periodic Summary P1 037 Repricing Break Even Periodic Summary P2 038 Repricing Break Even Periodic Summary P3 039 Repricing Break Even Periodic Detail P1 040 Repricing Break Even Periodic Detail P2 073 Fair Value Swaps - Detail 074 Fair Value Swaps by Counterparty - Summary 075 Fair Value Swaps by Counterparty - Detail Fair Value Swaps by Counterparty - More 076 Detail 077 Liquidity Stress report - Daily 078 Liquidity Stress report - Weekly 079 Liquidity Stress Report - Daily No totals 080 Liquidity Summary

33 ALMIS Approach a way forward ALMIS FTP January workshop To develop a suitable standard pricing template(s) ALMIS FTP March Seminar, presented jointly with FSA ALMIS Consulting to provide individual approach training / workshops with CEO involvement to implement individual approach (February June)

34 Joe Di Rollo Founder & Managing Director ALMIS International Limited

F T P - W h i t e P a p e r

F T P - W h i t e P a p e r Funds Transfer Pricing for banks and building societies, who are not operating profit centre treasuries Introduction This White Paper has been produced by ALMIS Consulting to

F T P - W h i t e P a p e r Funds Transfer Pricing for banks and building societies, who are not operating profit centre treasuries Introduction This White Paper has been produced by ALMIS Consulting to

Consultation paper on CEBS s Guidelines on Liquidity Cost Benefit Allocation

10 March 2010 Consultation paper on CEBS s Guidelines on Liquidity Cost Benefit Allocation (CP 36) Table of contents 1. Introduction 2 2. Main objectives.. 3 3. Contents.. 3 4. The guidelines. 5 Annex

10 March 2010 Consultation paper on CEBS s Guidelines on Liquidity Cost Benefit Allocation (CP 36) Table of contents 1. Introduction 2 2. Main objectives.. 3 3. Contents.. 3 4. The guidelines. 5 Annex

Asset and liability management: suggestions for greater effectiveness

Supervisory Statement LSS1/13 Asset and liability management: suggestions for greater effectiveness April 2013 Supervisory Statement LSS1/13 Asset and liability management: suggestions for greater effectiveness

Supervisory Statement LSS1/13 Asset and liability management: suggestions for greater effectiveness April 2013 Supervisory Statement LSS1/13 Asset and liability management: suggestions for greater effectiveness

Funds Transfer Pricing A gateway to enhanced business performance

Funds Transfer Pricing A gateway to enhanced business performance Jean-Philippe Peters Partner Governance, Risk & Compliance Deloitte Luxembourg Arnaud Duchesne Senior Manager Governance, Risk & Compliance

Funds Transfer Pricing A gateway to enhanced business performance Jean-Philippe Peters Partner Governance, Risk & Compliance Deloitte Luxembourg Arnaud Duchesne Senior Manager Governance, Risk & Compliance

Analysis of FSA Regulation

10 august 2009 REGULATORY ANALYSIS Authors Alain Maure & Pierre Mesnard, Liquidity Risk Solution Specialists Xavier Pernot, Balance Sheet Management Product Manager Table of Contents: History 2 International

10 august 2009 REGULATORY ANALYSIS Authors Alain Maure & Pierre Mesnard, Liquidity Risk Solution Specialists Xavier Pernot, Balance Sheet Management Product Manager Table of Contents: History 2 International

Funds Transfer Pricing

Funds Transfer Pricing Balance Sheet shaping and the role of the Funds Transfer Pricing process in banks This course can be presented in-house either on your premises or via live webinar for a group of

Funds Transfer Pricing Balance Sheet shaping and the role of the Funds Transfer Pricing process in banks This course can be presented in-house either on your premises or via live webinar for a group of

Constitution The Assets & Liabilities Committee ("ALCO") is an executive committee that reports into the Risk Committee.

is an executive committee that reports into the Risk Committee.") TERMS OF REFERENCE ASSETS & LIABILITIES COMMITTEE Constitution The Assets & Liabilities Committee ("ALCO") is an executive committee that reports into the Risk Committee. Membership The ALCO shall comprise

TERMS OF REFERENCE ASSETS & LIABILITIES COMMITTEE Constitution The Assets & Liabilities Committee ("ALCO") is an executive committee that reports into the Risk Committee. Membership The ALCO shall comprise

Guidance consultation. Senior Asset and Liability Management Committee Practices. Proposed Dear DEO letter ASSET AND LIABILITY MANAGEMENT

Financial Services Authority Guidance consultation Senior Asset and Liability Management Committee Practices Proposed Dear DEO letter November 2010 ASSET AND LIABILITY MANAGEMENT Dear CEO, I am writing

Financial Services Authority Guidance consultation Senior Asset and Liability Management Committee Practices Proposed Dear DEO letter November 2010 ASSET AND LIABILITY MANAGEMENT Dear CEO, I am writing

Bridgewater Bank Regulatory Disclosures December 31, 2017

Bridgewater Bank Regulatory Disclosures December 31, 2017 This document was prepared to fulfill regulatory requirements of the Office of the Superintendent of Financial Institutions Canada. Public disclosure

Bridgewater Bank Regulatory Disclosures December 31, 2017 This document was prepared to fulfill regulatory requirements of the Office of the Superintendent of Financial Institutions Canada. Public disclosure

Bridgewater Bank Regulatory Disclosures March 31, 2017

Bridgewater Bank Regulatory Disclosures March 31, 2017 This document was prepared to fulfill regulatory requirements of the Office of the Superintendent of Financial Institutions Canada. Public disclosure

Bridgewater Bank Regulatory Disclosures March 31, 2017 This document was prepared to fulfill regulatory requirements of the Office of the Superintendent of Financial Institutions Canada. Public disclosure

Index. Managing Risks in Commercial and Retail Banking By Amalendu Ghosh Copyright 2012 John Wiley & Sons Singapore Pte. Ltd.

Index A absence of control criteria, as cause of operational risk, 395 accountability, 493 495 additional exposure, incremental loss from, 115 advances and loans, ratio of core deposits to, 308 309 advances,

Index A absence of control criteria, as cause of operational risk, 395 accountability, 493 495 additional exposure, incremental loss from, 115 advances and loans, ratio of core deposits to, 308 309 advances,

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure. For the quarterly period ended March 31, 2018

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended March 31, 2018 0 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. LCR Drivers.

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended March 31, 2018 0 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. LCR Drivers.

Aldermore Bank Plc. Pillar 3 Disclosures

Aldermore Bank Plc Pillar 3 Disclosures December 31 2010 Contents 1. Introduction... 2 2. Scope... 2 3. Risk Management... 3 3.1 Risk Management Objectives... 3 3.2 Principal Risks... 3 3.3 Risk Appetite...

Aldermore Bank Plc Pillar 3 Disclosures December 31 2010 Contents 1. Introduction... 2 2. Scope... 2 3. Risk Management... 3 3.1 Risk Management Objectives... 3 3.2 Principal Risks... 3 3.3 Risk Appetite...

Bridgewater Bank Regulatory Disclosures March 31, 2016

Bridgewater Bank Regulatory Disclosures March 31, 2016 This document was prepared to fulfill regulatory requirements of the Office of the Superintendent of Financial Institutions Canada. Public disclosure

Bridgewater Bank Regulatory Disclosures March 31, 2016 This document was prepared to fulfill regulatory requirements of the Office of the Superintendent of Financial Institutions Canada. Public disclosure

Regulatory Disclosures March 31, 2018

Regulatory Disclosures March 31, 2018 SCOPE of DISCLOSURE... 3 CORPORATE PROFILE... 3 CAPITAL... 3 Capital structure... 4 Common shares... 4 Subordinated debt... 4 RISK MANAGEMENT... 4 Risk management

Regulatory Disclosures March 31, 2018 SCOPE of DISCLOSURE... 3 CORPORATE PROFILE... 3 CAPITAL... 3 Capital structure... 4 Common shares... 4 Subordinated debt... 4 RISK MANAGEMENT... 4 Risk management

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure. For the quarterly period ended June 30, 2018

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended June 30, 2018 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. Main Drivers

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended June 30, 2018 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. Main Drivers

Asset Liability Management. Craig Roodt Australian Prudential Regulation Authority

Asset Liability Management Craig Roodt Australian Prudential Regulation Authority Outline of Topics 1. ALM Defined 2. Role of ALM in the Organisation 3. Some History 4. Main Approaches - Measurement 5.

Asset Liability Management Craig Roodt Australian Prudential Regulation Authority Outline of Topics 1. ALM Defined 2. Role of ALM in the Organisation 3. Some History 4. Main Approaches - Measurement 5.

Asset-Liability Management in Banks

Asset-Liability Management (ALM) Asset-Liability Management in Banks Bankers make decisions every day about buying and selling securities, about whether to make particular loans, and about how to fund

Asset-Liability Management (ALM) Asset-Liability Management in Banks Bankers make decisions every day about buying and selling securities, about whether to make particular loans, and about how to fund

Managing liquidity risk under regulatory pressure. Kunghehian Nicolas

Managing liquidity risk under regulatory pressure Kunghehian Nicolas May 2012 Impact of the new Basel III regulation on the liquidity framework 2 Liquidity and business strategy alignment 79% of respondents

Managing liquidity risk under regulatory pressure Kunghehian Nicolas May 2012 Impact of the new Basel III regulation on the liquidity framework 2 Liquidity and business strategy alignment 79% of respondents

Bridgewater Bank Regulatory Disclosures June 30, 2014

Bridgewater Bank Regulatory Disclosures June 30, 2014 This document was prepared to fulfill regulatory requirements of the Office of the Superintendent of Financial Institutions Canada. Public disclosure

Bridgewater Bank Regulatory Disclosures June 30, 2014 This document was prepared to fulfill regulatory requirements of the Office of the Superintendent of Financial Institutions Canada. Public disclosure

BERMUDA MONETARY AUTHORITY BANKS AND DEPOSIT COMPANIES ACT 1999: PRINCIPLES FOR SOUND LIQUIDITY RISK MANAGEMENT AND SUPERVISION

BERMUDA MONETARY AUTHORITY BANKS AND DEPOSIT COMPANIES ACT 1999: PRINCIPLES FOR SOUND LIQUIDITY RISK MANAGEMENT AND SUPERVISION DECEMBER 2010 Table of Contents Introduction... 3 1. Approach to liquidity

BERMUDA MONETARY AUTHORITY BANKS AND DEPOSIT COMPANIES ACT 1999: PRINCIPLES FOR SOUND LIQUIDITY RISK MANAGEMENT AND SUPERVISION DECEMBER 2010 Table of Contents Introduction... 3 1. Approach to liquidity

Nottingham Building Society. Basel II - Pillar 3 Disclosures 2012

Nottingham Building Society Basel II - Pillar 3 Disclosures 2012 1 Contents 1. Overview 1.1 Background 1.2 Basis and Frequency of Disclosures 1.3 Location and Verification 1.4 Scope of Application Page

Nottingham Building Society Basel II - Pillar 3 Disclosures 2012 1 Contents 1. Overview 1.1 Background 1.2 Basis and Frequency of Disclosures 1.3 Location and Verification 1.4 Scope of Application Page

LIQUIDITY RISK MANAGEMENT MODULE

LIQUIDITY RISK MANAGEMENT MODULE MODULE: LM (Liquidity Risk Management) Table of Contents Date Last Changed LM-A Introduction LM A.1 Purpose 08/2018 LM A.2 Module History 08/2018 LM-1 Governance of Liquidity

LIQUIDITY RISK MANAGEMENT MODULE MODULE: LM (Liquidity Risk Management) Table of Contents Date Last Changed LM-A Introduction LM A.1 Purpose 08/2018 LM A.2 Module History 08/2018 LM-1 Governance of Liquidity

Internal bank funds pricing is a key element in liquidity risk management. An inappropriate or artificial internal funds

VISIONS OF RISK B A N K F U N D I N G & L I Q U I D I T Y CHALLENGES IN BANK FUNDING AND LIQUIDITY: A 3-PART FEATURE Part 2: Business best-practice bank internal funds pricing policy PROFESSOR MOORAD CHOUDHRY

VISIONS OF RISK B A N K F U N D I N G & L I Q U I D I T Y CHALLENGES IN BANK FUNDING AND LIQUIDITY: A 3-PART FEATURE Part 2: Business best-practice bank internal funds pricing policy PROFESSOR MOORAD CHOUDHRY

Loan Profitability Report and Applications key words: return on investment, ALCO, RAROC, loan pricing

, Loan Profitability Report and Applications key words: return on investment, ALCO, RAROC, loan pricing THC Asset-Liability Management (ALM) Insight Issue 8 Introduction Loan portfolio profitability is

, Loan Profitability Report and Applications key words: return on investment, ALCO, RAROC, loan pricing THC Asset-Liability Management (ALM) Insight Issue 8 Introduction Loan portfolio profitability is

Bridgewater Bank Regulatory Disclosures March 31, 2015

Bridgewater Bank Regulatory Disclosures March 31, 2015 This document was prepared to fulfill regulatory requirements of the Office of the Superintendent of Financial Institutions Canada. Public disclosure

Bridgewater Bank Regulatory Disclosures March 31, 2015 This document was prepared to fulfill regulatory requirements of the Office of the Superintendent of Financial Institutions Canada. Public disclosure

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure. For the quarterly period ended December 31, 2017

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended December 31, 2017 0 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. LCR

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended December 31, 2017 0 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. LCR

PILLAR 3 Disclosures

PILLAR 3 Disclosures Published April 2016 Contacts: Rajeev Adrian Sedjwick Joseph Chief Financial Officer Chief Risk Officer 0207 776 4006 0207 776 4014 Rajeev.adrian@bank-abc.com sedjwick.joseph@bankabc.com

PILLAR 3 Disclosures Published April 2016 Contacts: Rajeev Adrian Sedjwick Joseph Chief Financial Officer Chief Risk Officer 0207 776 4006 0207 776 4014 Rajeev.adrian@bank-abc.com sedjwick.joseph@bankabc.com

Solvency Assessment and Management: Stress Testing Task Group Discussion Document 96 (v 3) General Stress Testing Guidance for Insurance Companies

General Stress Testing Guidance for Insurance Companies") Solvency Assessment and Management: Stress Testing Task Group Discussion Document 96 (v 3) General Stress Testing Guidance for Insurance Companies 1 INTRODUCTION AND PURPOSE The business of insurance is

Solvency Assessment and Management: Stress Testing Task Group Discussion Document 96 (v 3) General Stress Testing Guidance for Insurance Companies 1 INTRODUCTION AND PURPOSE The business of insurance is

Pillar 3 Disclosures. Liquidity Coverage Ratio ( LCR ) For the quarter ended 31 March 2016

For the quarter ended 31 March 2016") Pillar 3 Disclosures Liquidity Coverage Ratio ( LCR ) For the quarter ended 31 March 016 DBS Group Holdings Ltd Incorporated in the Republic of Singapore Company Registration Number: 19990115M The following

Pillar 3 Disclosures Liquidity Coverage Ratio ( LCR ) For the quarter ended 31 March 016 DBS Group Holdings Ltd Incorporated in the Republic of Singapore Company Registration Number: 19990115M The following

National Australia Bank Limited, Mumbai Branch (Incorporated in Australia with limited liability)

") Background National Australia Bank Limited (NAB), which is incorporated and registered in Australia with limited liability, is one of Australia's largest banks and has been in existence for over 150 years.

Background National Australia Bank Limited (NAB), which is incorporated and registered in Australia with limited liability, is one of Australia's largest banks and has been in existence for over 150 years.

Risk Management - CAIIB

UNIT 1: COMPONENTS OF ASSETS AND LIABILITIES IN BANK S BALANCE THEIR MANAGEMENT SHEET AND ALM encompasses the analysis and development of goals and objectives, the development of long term strategic plans,

UNIT 1: COMPONENTS OF ASSETS AND LIABILITIES IN BANK S BALANCE THEIR MANAGEMENT SHEET AND ALM encompasses the analysis and development of goals and objectives, the development of long term strategic plans,

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure. For the quarterly period ended December 31, 2018

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended December 31, 2018 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. Main Drivers

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended December 31, 2018 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. Main Drivers

DARLINGTON BUILDING SOCIETY CAPITAL REQUIREMENTS DIRECTIVE

DARLINGTON BUILDING SOCIETY CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT AS AT 31 st DECEMBER 2016 CONTENTS Section Title 1 Introduction 2 Risk Management Objectives and Policies 3 Capital

DARLINGTON BUILDING SOCIETY CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT AS AT 31 st DECEMBER 2016 CONTENTS Section Title 1 Introduction 2 Risk Management Objectives and Policies 3 Capital

Valu-Trac Investment Management Limited Pillar 3 Disclosure

Valu-Trac Investment Management Limited Pillar 3 Disclosure The Capital Requirements Directive (CRD) of the European Union created a revised regulatory capital framework across Europe governing how much

Valu-Trac Investment Management Limited Pillar 3 Disclosure The Capital Requirements Directive (CRD) of the European Union created a revised regulatory capital framework across Europe governing how much

Pillar 3 Disclosures. Sterling ISA Managers Limited Year Ending 31 st December 2017

Pillar 3 Disclosures Sterling ISA Managers Limited Year Ending 31 st December 2017 1. Background and Scope 1.1 Background Sterling ISA Managers Limited (the Company) is supervised by the Financial Conduct

Pillar 3 Disclosures Sterling ISA Managers Limited Year Ending 31 st December 2017 1. Background and Scope 1.1 Background Sterling ISA Managers Limited (the Company) is supervised by the Financial Conduct

PEOPLES TRUST COMPANY PUBLIC DISCLOSURES (BASEL III PILLAR 3 and Leverage Ratio)

") PEOPLES TRUST COMPANY PUBLIC DISCLOSURES (BASEL III PILLAR 3 and Leverage Ratio) As at December 31, 2017 TABLE OF CONTENTS Disclosure Policy... 1 Location and Verification... 1 Background... 1 Statement

PEOPLES TRUST COMPANY PUBLIC DISCLOSURES (BASEL III PILLAR 3 and Leverage Ratio) As at December 31, 2017 TABLE OF CONTENTS Disclosure Policy... 1 Location and Verification... 1 Background... 1 Statement

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million. May Ce document est également disponible en français.

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million May 2017 Ce document est également disponible en français. Applicability This Guidance Note is for use by all credit unions

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million May 2017 Ce document est également disponible en français. Applicability This Guidance Note is for use by all credit unions

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure. For the quarterly period ended September 30, 2017

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended September 30, 2017 1 Table of Contents 1. Overview... 3 2. Liquidity Coverage Ratio Template... 4 3. LCR Drivers

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended September 30, 2017 1 Table of Contents 1. Overview... 3 2. Liquidity Coverage Ratio Template... 4 3. LCR Drivers

Financial Services Authority

Financial Services Authority FINAL NOTICE To: Of: Credit Suisse International and Credit Suisse Securities (Europe) Limited (the UK operations of Credit Suisse ) One Cabot Square, London E14 4QL Dated

Financial Services Authority FINAL NOTICE To: Of: Credit Suisse International and Credit Suisse Securities (Europe) Limited (the UK operations of Credit Suisse ) One Cabot Square, London E14 4QL Dated

IIF s Final Report on Market Best Practices for Financial Institutions and Financial Products

IIF s Final Report on Market Best Practices for Financial Institutions and Financial Products By Peter Green and Jeremy Jennings-Mares he Institute of International Finance (IIF) s T Board of Directors

IIF s Final Report on Market Best Practices for Financial Institutions and Financial Products By Peter Green and Jeremy Jennings-Mares he Institute of International Finance (IIF) s T Board of Directors

General Bank of Canada

General Bank of Canada Regulatory Disclosures The Basel Committee of Banking Supervision sets out expectations for public disclosure of a bank s risk management objectives and policies, reporting systems,

General Bank of Canada Regulatory Disclosures The Basel Committee of Banking Supervision sets out expectations for public disclosure of a bank s risk management objectives and policies, reporting systems,

Opinion of the EBA on Good Practices for ETF Risk Management

EBA-Op-2013-01 7 March 2013 Opinion of the EBA on Good Practices for ETF Risk Management Table of contents Table of contents 2 Introduction 4 I. Good Practices for ETF business 6 II. Considerations for

EBA-Op-2013-01 7 March 2013 Opinion of the EBA on Good Practices for ETF Risk Management Table of contents Table of contents 2 Introduction 4 I. Good Practices for ETF business 6 II. Considerations for

EBF RESPONSES TO THE IASB DISCUSSION PAPER ON ACCOUNTING FOR DYNAMIC RISK MANAGEMENT: A PORTFOLIO REVALUATION APPROACH TO MACRO HEDGING

EBF_010548 17.10.2014 APPENDIX EBF RESPONSES TO THE IASB DISCUSSION PAPER ON ACCOUNTING FOR DYNAMIC RISK MANAGEMENT: A PORTFOLIO REVALUATION APPROACH TO MACRO HEDGING QUESTION 1 NEED FOR AN ACCOUNTING

EBF_010548 17.10.2014 APPENDIX EBF RESPONSES TO THE IASB DISCUSSION PAPER ON ACCOUNTING FOR DYNAMIC RISK MANAGEMENT: A PORTFOLIO REVALUATION APPROACH TO MACRO HEDGING QUESTION 1 NEED FOR AN ACCOUNTING

DARLINGTON BUILDING SOCIETY CAPITAL REQUIREMENTS DIRECTIVE

DARLINGTON BUILDING SOCIETY CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT AS AT 31 st DECEMBER 2018 Contents 1 Introduction 2 Risk Management 3 Capital 4 Credit Risk (Mortgages) 5 Provisions

DARLINGTON BUILDING SOCIETY CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT AS AT 31 st DECEMBER 2018 Contents 1 Introduction 2 Risk Management 3 Capital 4 Credit Risk (Mortgages) 5 Provisions

Pillar 2 Liquidity. Our response to PRA CP 21/16. August 2016

Our response to PRA CP 21/16 August 2016 Introduction and context We welcome this consultation, and the PRA s engagement with BSA members on this subject at a meeting on 22 June. We appreciate that the

Our response to PRA CP 21/16 August 2016 Introduction and context We welcome this consultation, and the PRA s engagement with BSA members on this subject at a meeting on 22 June. We appreciate that the

Guidelines for Asset Liability Management (ALM) System in Financial Institutions (FIs)

System in Financial Institutions (FIs)") Guidelines for Asset Liability Management (ALM) System in Financial Institutions (FIs) In the normal course, FIs are exposed to credit and market risks in view of the asset-liability transformation. With

Guidelines for Asset Liability Management (ALM) System in Financial Institutions (FIs) In the normal course, FIs are exposed to credit and market risks in view of the asset-liability transformation. With

A New Approach to Manage Profitability THC FUND TRANSFER PRICING (FTP) MODEL

MODEL") , A New Approach to Manage Profitability THC FUND TRANSFER PRICING (FTP) MODEL THC Asset-Liability Management (ALM) Insight Issue 3 Post 2009 financial crisis, a new approach to enhance profitability is

, A New Approach to Manage Profitability THC FUND TRANSFER PRICING (FTP) MODEL THC Asset-Liability Management (ALM) Insight Issue 3 Post 2009 financial crisis, a new approach to enhance profitability is

Hot Financial and Risk Management Topics

Hot Financial and Risk Management Topics Brief survey on the most interesting issues regarding ALM, FTP and RM KPMG d.o.o. Beograd February 2017 1 Foreword Dušan Tomic, Partner, Head of Financial Institutions

Hot Financial and Risk Management Topics Brief survey on the most interesting issues regarding ALM, FTP and RM KPMG d.o.o. Beograd February 2017 1 Foreword Dušan Tomic, Partner, Head of Financial Institutions

Finalised guidance. Individual Liquidity Systems Assessment (ILSA) Simplified ILAS BIPRU Firms (ILSA) Simplified ILAS BIPRU Firms.

Simplified ILAS BIPRU Firms (ILSA) Simplified ILAS BIPRU Firms.") Financial Services Authority Finalised guidance Individual Liquidity Systems Assessment (ILSA) Simplified ILAS BIPRU Firms April 2011 Individual Liquidity Systems Assessment (ILSA) Simplified ILAS BIPRU

Financial Services Authority Finalised guidance Individual Liquidity Systems Assessment (ILSA) Simplified ILAS BIPRU Firms April 2011 Individual Liquidity Systems Assessment (ILSA) Simplified ILAS BIPRU

I should firstly like to say that I am entirely supportive of the objectives of the CD, namely:

From: Paul Newson Email: paulnewson@aol.com 27 August 2015 Dear Task Force Members This letter constitutes a response to the BCBS Consultative Document on Interest Rate Risk in the Banking Book (the CD)

From: Paul Newson Email: paulnewson@aol.com 27 August 2015 Dear Task Force Members This letter constitutes a response to the BCBS Consultative Document on Interest Rate Risk in the Banking Book (the CD)

Stepping up to the Liquidity Challenge: The Changing Role of Credit Portfolio Management

Stepping up to the Liquidity Challenge: The Changing Role of Credit Portfolio Management RESULTS ANALYSIS OF IACPM KPMG BENCHMARKING SURVEY 2012 In 2011-2012 the IACPM, in collaboration with KPMG, undertook

Stepping up to the Liquidity Challenge: The Changing Role of Credit Portfolio Management RESULTS ANALYSIS OF IACPM KPMG BENCHMARKING SURVEY 2012 In 2011-2012 the IACPM, in collaboration with KPMG, undertook

Collateral upgrade transactions and asset encumbrance: expectations in relation to firms risk management practices

Supervisory Statement LSS2/13 Collateral upgrade transactions and asset encumbrance: expectations in relation to firms risk management practices April 2013 Supervisory Statement LSS2/13 Collateral upgrade

Supervisory Statement LSS2/13 Collateral upgrade transactions and asset encumbrance: expectations in relation to firms risk management practices April 2013 Supervisory Statement LSS2/13 Collateral upgrade

1 SIGNIFICANT ACCOUNTING POLICIES The principal accounting policies adopted in the preparation of these financial statements as set out below have

1 SIGNIFICANT ACCOUNTING POLICIES The principal accounting policies adopted in the preparation of these financial statements as set out below have been applied consistently to all periods presented in

1 SIGNIFICANT ACCOUNTING POLICIES The principal accounting policies adopted in the preparation of these financial statements as set out below have been applied consistently to all periods presented in

Financial Literacy Mastery

Financial Literacy Mastery Presented by Eileen Iles Colette Wagner Crowe Horwath LLP Session Objectives Satisfy your NCUA financial literacy requirement by taking your knowledge of financial statements

Financial Literacy Mastery Presented by Eileen Iles Colette Wagner Crowe Horwath LLP Session Objectives Satisfy your NCUA financial literacy requirement by taking your knowledge of financial statements

Re: Consultative Document: Capitalisation of bank exposures to central counterparties

Via E Mail (BaselCommittee@bis.org) February 4, 2011 The Secretariat of the Basel Committee on Banking Supervision Bank for International Settlements CH 4002 Basel, Switzerland Re: Consultative Document:

Via E Mail (BaselCommittee@bis.org) February 4, 2011 The Secretariat of the Basel Committee on Banking Supervision Bank for International Settlements CH 4002 Basel, Switzerland Re: Consultative Document:

PEOPLES TRUST COMPANY. PUBLIC DISCLOSURES (BASEL III PILLAR 3) As at December 31, 2013

As at December 31, 2013") PEOPLES TRUST COMPANY PUBLIC DISCLOSURES (BASEL III PILLAR 3) As at December 31, 2013 TABLE OF CONTENTS Disclosure Policy... 1 Location and Verification... 1 Background... 1 Statement of Risk Appetite...

PEOPLES TRUST COMPANY PUBLIC DISCLOSURES (BASEL III PILLAR 3) As at December 31, 2013 TABLE OF CONTENTS Disclosure Policy... 1 Location and Verification... 1 Background... 1 Statement of Risk Appetite...

PEOPLES TRUST COMPANY PUBLIC DISCLOSURES (BASEL III PILLAR 3 and Leverage Ratio)

") PEOPLES TRUST COMPANY PUBLIC DISCLOSURES (BASEL III PILLAR 3 and Leverage Ratio) As at December 31, 2015 TABLE OF CONTENTS Disclosure Policy... 1 Location and Verification... 1 Background... 1 Statement

PEOPLES TRUST COMPANY PUBLIC DISCLOSURES (BASEL III PILLAR 3 and Leverage Ratio) As at December 31, 2015 TABLE OF CONTENTS Disclosure Policy... 1 Location and Verification... 1 Background... 1 Statement

Liquidity & Treasury Management Conference. Reporting to the Board Writing a Winning Treasury Report

Liquidity & Treasury Management Conference Reporting to the Board Writing a Winning Treasury Report Martin Watts Head of Treasury, L&Q email: mwatts@lqgroup.org.uk Introduction Post TSA abolishment, the

Liquidity & Treasury Management Conference Reporting to the Board Writing a Winning Treasury Report Martin Watts Head of Treasury, L&Q email: mwatts@lqgroup.org.uk Introduction Post TSA abolishment, the

ASSET & LIABILITY MANAGEMENT

ASSET & LIABILITY MANAGEMENT Best-Practice Balance Sheet Management and Capital Planning Workshop Overview SimArch NV Interleuvenlaan 62 3001 Heverlee BELGIUM Phone +32 16 39 4732 Fax +32 16 39 4731 Email

ASSET & LIABILITY MANAGEMENT Best-Practice Balance Sheet Management and Capital Planning Workshop Overview SimArch NV Interleuvenlaan 62 3001 Heverlee BELGIUM Phone +32 16 39 4732 Fax +32 16 39 4731 Email

Guidance on Liquidity Risk Management

Guidance on Liquidity Risk Management XXXX 2016 CONTENTS 1. Introduction... 3 2. Standard Liquidity Approach (SLA)... 4 3. Enhanced Liquidity Approach (ELA): Maximum Mismatch Limits... 5 4. Enhanced Liquidity

Guidance on Liquidity Risk Management XXXX 2016 CONTENTS 1. Introduction... 3 2. Standard Liquidity Approach (SLA)... 4 3. Enhanced Liquidity Approach (ELA): Maximum Mismatch Limits... 5 4. Enhanced Liquidity

Liquidity Coverage Ratio ( LCR ) For the quarter ended 31 Mar 2017

For the quarter ended 31 Mar 2017") Liquidity Coverage Ratio ( LCR ) For the quarter ended 31 Mar 017 DBS Group Holdings Ltd Incorporated in the Republic of Singapore Company Registration Number: 19990115M The following disclosures for the

Liquidity Coverage Ratio ( LCR ) For the quarter ended 31 Mar 017 DBS Group Holdings Ltd Incorporated in the Republic of Singapore Company Registration Number: 19990115M The following disclosures for the

Current status of Solvency II and challenges down the line. Matthew Edwards 11 October 2011

Current status of Solvency II and challenges down the line Matthew Edwards 11 October 2011 Solvency II Timeline Page 2 15 September 2011 UK Life Solvency II Discussion Forum Regulatory timelines Level

Current status of Solvency II and challenges down the line Matthew Edwards 11 October 2011 Solvency II Timeline Page 2 15 September 2011 UK Life Solvency II Discussion Forum Regulatory timelines Level

Regulatory Impact Assessment RBNZ Liquidity requirements for locally incorporated banks

Regulatory Impact Assessment RBNZ Liquidity requirements for locally incorporated banks Executive summary 1 A strong liquidity profile across banks is important for the maintenance of a sound and efficient

Regulatory Impact Assessment RBNZ Liquidity requirements for locally incorporated banks Executive summary 1 A strong liquidity profile across banks is important for the maintenance of a sound and efficient

STRESS TESTING GUIDELINE

c DRAFT STRESS TESTING GUIDELINE November 2011 TABLE OF CONTENTS Preamble... 2 Introduction... 3 Coming into effect and updating... 6 1. Stress testing... 7 A. Concept... 7 B. Approaches underlying stress

c DRAFT STRESS TESTING GUIDELINE November 2011 TABLE OF CONTENTS Preamble... 2 Introduction... 3 Coming into effect and updating... 6 1. Stress testing... 7 A. Concept... 7 B. Approaches underlying stress

PEOPLES TRUST COMPANY PUBLIC DISCLOSURES (BASEL III PILLAR 3 and Leverage Ratio)

") PEOPLES TRUST COMPANY PUBLIC DISCLOSURES (BASEL III PILLAR 3 and Leverage Ratio) As at December 31, 2016 TABLE OF CONTENTS Disclosure Policy... 1 Location and Verification... 1 Background... 1 Statement

PEOPLES TRUST COMPANY PUBLIC DISCLOSURES (BASEL III PILLAR 3 and Leverage Ratio) As at December 31, 2016 TABLE OF CONTENTS Disclosure Policy... 1 Location and Verification... 1 Background... 1 Statement

Scottish Friendly Assurance Society Ltd. Principles and Practices of Financial Management for Unitised Ordinary Branch Business

Scottish Friendly Assurance Society Ltd Principles and Practices of Financial Management for Unitised Ordinary Branch Business CONTENTS 1. Introduction 3 2. With-Profits Policies.. 5 3. Overriding Principles...6

Scottish Friendly Assurance Society Ltd Principles and Practices of Financial Management for Unitised Ordinary Branch Business CONTENTS 1. Introduction 3 2. With-Profits Policies.. 5 3. Overriding Principles...6

Supervising building societies treasury and lending activities

Supervisory Statement SS20/15 Supervising building societies treasury and lending activities April 2015 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation Authority, registered

Supervisory Statement SS20/15 Supervising building societies treasury and lending activities April 2015 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation Authority, registered

INSTITUTE AND FACULTY OF ACTUARIES. Curriculum 2019 SPECIMEN SOLUTIONS

INSTITUTE AND FACULTY OF ACTUARIES Curriculum 2019 SPECIMEN SOLUTIONS Subject SP5 Investment and Finance Specialist Principles Institute and Faculty of Actuaries 1 (i) The term risk budgeting refers to

INSTITUTE AND FACULTY OF ACTUARIES Curriculum 2019 SPECIMEN SOLUTIONS Subject SP5 Investment and Finance Specialist Principles Institute and Faculty of Actuaries 1 (i) The term risk budgeting refers to

THC Asset-Liability Management (ALM) Insight Issue 5

Insight Issue 5") , WHOLE LOAN SALE TO AGENCIES: A Strategy key words: risk capacity, G-spread, LLPA, yield attribution, fixed rate 1-4 family mortgage, whole loan pricing THC Asset-Liability Management (ALM) Insight Issue

, WHOLE LOAN SALE TO AGENCIES: A Strategy key words: risk capacity, G-spread, LLPA, yield attribution, fixed rate 1-4 family mortgage, whole loan pricing THC Asset-Liability Management (ALM) Insight Issue

Alpha Bank AD Skopje. Financial Statements for the year ended 31 December 2007

for the year ended 31 December 2007 Contents Auditors' report Balance sheet 2 Income statement 3 Statement of changes in equity 4 Statement of cash flows 5 Notes to the financial statement 6 Balance sheet

for the year ended 31 December 2007 Contents Auditors' report Balance sheet 2 Income statement 3 Statement of changes in equity 4 Statement of cash flows 5 Notes to the financial statement 6 Balance sheet

Capital Requirements Directive. Pillar 3 Disclosures

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2016 INDEX Page INTRODUCTION 2 RISK MANAGEMENT POLICIES AND OBJECTIVES 3 CAPITAL ADEQUACY ASSESSMENT, CAPITAL RESOURCES

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2016 INDEX Page INTRODUCTION 2 RISK MANAGEMENT POLICIES AND OBJECTIVES 3 CAPITAL ADEQUACY ASSESSMENT, CAPITAL RESOURCES

Current perspectives on funds transfer pricing

Current perspectives on funds transfer pricing kpmg.com Executive summary Funds Transfer Pricing (FTP) evolved in the 1980s to help financial institutions effectively manage interest rate risk (IRR) and

Current perspectives on funds transfer pricing kpmg.com Executive summary Funds Transfer Pricing (FTP) evolved in the 1980s to help financial institutions effectively manage interest rate risk (IRR) and

1. Purpose Frequency and Basis of Disclosures Overview Risk Management Objectives and Policies 5

PILLAR 3 DISCLOSURE DOCUMENT June 2013 CONTENTS PAGE 1. Purpose 3 1.1 Frequency and Basis of Disclosures 3 2. Overview 4 3. Risk Management Objectives and Policies 5 4. Risk Management Framework 6 4.1

PILLAR 3 DISCLOSURE DOCUMENT June 2013 CONTENTS PAGE 1. Purpose 3 1.1 Frequency and Basis of Disclosures 3 2. Overview 4 3. Risk Management Objectives and Policies 5 4. Risk Management Framework 6 4.1

African Bank Holdings Limited and African Bank Limited

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 7 3. Supplementary

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 7 3. Supplementary

Implementing the new liquidity risk management frameworks the lessons learned

Implementing the new liquidity risk management frameworks the lessons learned September 15 th, 2010 PwC Agenda 1) Linking liquidity management and liquidity risk management 2) Setting strategic objectives

Implementing the new liquidity risk management frameworks the lessons learned September 15 th, 2010 PwC Agenda 1) Linking liquidity management and liquidity risk management 2) Setting strategic objectives

Pillar III Disclosure Report 2017

Pillar III Disclosure Report 2017 Content Section 1. Introduction and basis for preparation 3 Section 2. Risk management objectives and policies 5 Section 3. Information on the scope of application of

Pillar III Disclosure Report 2017 Content Section 1. Introduction and basis for preparation 3 Section 2. Risk management objectives and policies 5 Section 3. Information on the scope of application of

BAC BAHAMAS BANK LIMITED

Financial Statements of BAC BAHAMAS BANK LIMITED BAC BAHAMAS BANK LIMITED Financial Statements Page Independent Auditors Report 1-2 Statement of Financial Position 3 Statement of Comprehensive Income 4

Financial Statements of BAC BAHAMAS BANK LIMITED BAC BAHAMAS BANK LIMITED Financial Statements Page Independent Auditors Report 1-2 Statement of Financial Position 3 Statement of Comprehensive Income 4

Retail credit portfolio management

Retail credit portfolio management IACPM Spring General Meeting - Munich May 2008 Gert Kruger, FirstRand Banking Group 2008 IACPM Context Only 47% of CPM units manage retail credit exposures (McKinsey

Retail credit portfolio management IACPM Spring General Meeting - Munich May 2008 Gert Kruger, FirstRand Banking Group 2008 IACPM Context Only 47% of CPM units manage retail credit exposures (McKinsey

ASSET LIABILITY MANAGEMENT POLICY

ASSET LIABILITY MANAGEMENT POLICY DECEMBER 2017 1. Introduction This Asset Liability Management (ALM) Policy establishes a framework for the sound management of ALM and sets forth the principles and practices

ASSET LIABILITY MANAGEMENT POLICY DECEMBER 2017 1. Introduction This Asset Liability Management (ALM) Policy establishes a framework for the sound management of ALM and sets forth the principles and practices

BATH BUILDING SOCIETY

BATH BUILDING SOCIETY Pillar 3 Disclosure Document Index Page 1. Introduction 3 2. Risk management policies and objectives 5 3. Main Board and committee structure 10 4. Capital resources and capital ratios

BATH BUILDING SOCIETY Pillar 3 Disclosure Document Index Page 1. Introduction 3 2. Risk management policies and objectives 5 3. Main Board and committee structure 10 4. Capital resources and capital ratios

PILLAR 3 DISCLOSURES DECEMBER 2013

PILLAR 3 DISCLOSURES DECEMBER 2013 TABLE OF CONTENTS 1 Introduction 3 1.1 Objective 3 1.2 Disclosure Policy 3 1.3 Scope 3 1.4 Relevant Changes 4 2 Risk Management 5 2.1 Risk Oversight Framework 5 2.2

PILLAR 3 DISCLOSURES DECEMBER 2013 TABLE OF CONTENTS 1 Introduction 3 1.1 Objective 3 1.2 Disclosure Policy 3 1.3 Scope 3 1.4 Relevant Changes 4 2 Risk Management 5 2.1 Risk Oversight Framework 5 2.2

BAILLIE GIFFORD. Governance, Risk Management and Capital Disclosures ( Pillar 3 ) June 2018

June 2018") BAILLIE GIFFORD Governance, Risk Management and Capital Disclosures ( Pillar 3 ) June 2018 Contents Introduction and Context 3 Purpose of Disclosures Scope Basis of Preparation Governance Arrangements

BAILLIE GIFFORD Governance, Risk Management and Capital Disclosures ( Pillar 3 ) June 2018 Contents Introduction and Context 3 Purpose of Disclosures Scope Basis of Preparation Governance Arrangements

Scottish Friendly Assurance Society Ltd. Principles and Practices of Financial Management for Conventional With Profits Business

Scottish Friendly Assurance Society Ltd Principles and Practices of Financial Management for Conventional With Profits Business CONTENTS 1. Introduction 2 2. With-Profits Policies.. 4 3. Overriding Principles...5

Scottish Friendly Assurance Society Ltd Principles and Practices of Financial Management for Conventional With Profits Business CONTENTS 1. Introduction 2 2. With-Profits Policies.. 4 3. Overriding Principles...5

FSA Mortgage Market Review Distribution & Disclosure (CP10/28) Response by the Building Societies Association

Response by the Building Societies Association") FSA Mortgage Market Review Distribution & Disclosure (CP10/28) Response by the Building Societies Association 1 Mortgage Market Review: Distribution & Disclosure CP 10/28 Response by the Building Societies

FSA Mortgage Market Review Distribution & Disclosure (CP10/28) Response by the Building Societies Association 1 Mortgage Market Review: Distribution & Disclosure CP 10/28 Response by the Building Societies

Interest Rate Risk in the Banking Book. Taking a close look at the latest IRRBB developments

Interest Rate Risk in the Banking Book Taking a close look at the latest IRRBB developments Interest Rate Risk in the Banking Book Interest rate risk in the banking book (IRRBB) can be a significant risk

Interest Rate Risk in the Banking Book Taking a close look at the latest IRRBB developments Interest Rate Risk in the Banking Book Interest rate risk in the banking book (IRRBB) can be a significant risk

Application Guide. Securitization. November Ce document est aussi disponible en français.

Application Guide Securitization November 2017 Ce document est aussi disponible en français. Applicability The Securitization Application Guide (Application Guide) is for use by all credit unions. It is

Application Guide Securitization November 2017 Ce document est aussi disponible en français. Applicability The Securitization Application Guide (Application Guide) is for use by all credit unions. It is

EUROPEAN SYSTEMIC RISK BOARD

2.9.2014 EN Official Journal of the European Union C 293/1 I (Resolutions, recommendations and opinions) RECOMMENDATIONS EUROPEAN SYSTEMIC RISK BOARD RECOMMENDATION OF THE EUROPEAN SYSTEMIC RISK BOARD

2.9.2014 EN Official Journal of the European Union C 293/1 I (Resolutions, recommendations and opinions) RECOMMENDATIONS EUROPEAN SYSTEMIC RISK BOARD RECOMMENDATION OF THE EUROPEAN SYSTEMIC RISK BOARD

King & Shaxson Group Pillar 3 Disclosures 2016

1. Introduction 1.1 Background The European Union Capital Requirements Directive ( CRD ) established a regulatory framework for capital adequacy across the European Union. CRD was replaced by the Capital

1. Introduction 1.1 Background The European Union Capital Requirements Directive ( CRD ) established a regulatory framework for capital adequacy across the European Union. CRD was replaced by the Capital

Response to FSA Discussion Paper 09/2 1 : A regulatory response to the global banking crisis

Response to FSA Discussion Paper 09/2 1 : A regulatory response to the global banking crisis Introduction The Hedge Fund Standards Board (HFSB) was set up to act as custodian of the Best Practice Standards

Response to FSA Discussion Paper 09/2 1 : A regulatory response to the global banking crisis Introduction The Hedge Fund Standards Board (HFSB) was set up to act as custodian of the Best Practice Standards

Portfolio (macro) hedge accounting

hedge accounting") Portfolio (macro) hedge accounting Cancelled swaps creating amortisation challenges? ALMIS has the solution 1. Introduction An IASB 2014 Discussion Paper proposed a new approach to macro hedge accounting

Portfolio (macro) hedge accounting Cancelled swaps creating amortisation challenges? ALMIS has the solution 1. Introduction An IASB 2014 Discussion Paper proposed a new approach to macro hedge accounting

The Hongkong and Shanghai Banking Corporation Limited - Macau Branch. Disclosure of Financial Information 31 December 2012

The Hongkong and Shanghai Banking Corporation Limited Disclosure of Financial Information 31 December 2012 Year ended 31 December 2012 Report of the Branch management Principal place of business and activities

The Hongkong and Shanghai Banking Corporation Limited Disclosure of Financial Information 31 December 2012 Year ended 31 December 2012 Report of the Branch management Principal place of business and activities

Securities Lending Outlook

WORLDWIDE SECURITIES SERVICES Outlook Managing Value Generation and Risk Securities lending and its risk/reward profile have been in the headlines as the credit and liquidity crisis has continued to unfold.

WORLDWIDE SECURITIES SERVICES Outlook Managing Value Generation and Risk Securities lending and its risk/reward profile have been in the headlines as the credit and liquidity crisis has continued to unfold.

Framework on Analysis of Balance Sheets

DBOD.No.BP.BC.3/21.04.109/99 name=reference> DBOD.No.BP.BC.3/21.04.109/99 February 8, 1999 All Scheduled Commercial Banks Dear Sir, Framework on Analysis of Balance Sheets As you are aware, the analysis

DBOD.No.BP.BC.3/21.04.109/99 name=reference> DBOD.No.BP.BC.3/21.04.109/99 February 8, 1999 All Scheduled Commercial Banks Dear Sir, Framework on Analysis of Balance Sheets As you are aware, the analysis

Liquidity risk management

Liquidity risk management 10 by Richard Barfield and Shyam Venkat Richard Barfield Director, Advisory, Financial Services (UK) Tel: 44 20 7804 6658 richard.barfield@uk.pwc.com Shyam Venkat Partner, Advisory,

Liquidity risk management 10 by Richard Barfield and Shyam Venkat Richard Barfield Director, Advisory, Financial Services (UK) Tel: 44 20 7804 6658 richard.barfield@uk.pwc.com Shyam Venkat Partner, Advisory,

DO YOU TRUST YOUR STRATEGIC COMPASS? WHY IT S TIME TO TAKE A RENEWED LOOK AT FUNDS TRANSFER PRICING PRACTICES

DO YOU TRUST YOUR STRATEGIC COMPASS? WHY IT S TIME TO TAKE A RENEWED LOOK AT FUNDS TRANSFER PRICING PRACTICES AUTHORS Deepak Kollali Jai Sooklal Amal Rahuman 1. EXECUTIVE SUMMARY Traditional views of profitability

DO YOU TRUST YOUR STRATEGIC COMPASS? WHY IT S TIME TO TAKE A RENEWED LOOK AT FUNDS TRANSFER PRICING PRACTICES AUTHORS Deepak Kollali Jai Sooklal Amal Rahuman 1. EXECUTIVE SUMMARY Traditional views of profitability

Enhanced Requirements for IRRBB Management. Insights from EY European IRRBB Survey 2016 for banks

Enhanced Requirements for IRRBB Management Insights from EY European IRRBB Survey 2016 for banks Contents Executive summary... 1 About this survey... 3 Governance roles and responsibilities... 4 Metrics,

Enhanced Requirements for IRRBB Management Insights from EY European IRRBB Survey 2016 for banks Contents Executive summary... 1 About this survey... 3 Governance roles and responsibilities... 4 Metrics,

Basel Committee on Banking Supervision. Liquidity coverage ratio disclosure standards

Basel Committee on Banking Supervision Liquidity coverage ratio disclosure standards January 2014 This publication is available on the BIS website (www.bis.org). Bank for International Settlements 2014.

Basel Committee on Banking Supervision Liquidity coverage ratio disclosure standards January 2014 This publication is available on the BIS website (www.bis.org). Bank for International Settlements 2014.

Risk and Capital Management 2007

Risk and Capital Management Contents RISK MANAGEMENT 5 Risk profile 5 - Types of risk 5 Special events in 5 - Nykredit Bank rated by Moody's 5 - EMTN programme 5 - The international financial crisis 5

Risk and Capital Management Contents RISK MANAGEMENT 5 Risk profile 5 - Types of risk 5 Special events in 5 - Nykredit Bank rated by Moody's 5 - EMTN programme 5 - The international financial crisis 5

14. What Use Can Be Made of the Specific FSIs?

14. What Use Can Be Made of the Specific FSIs? Introduction 14.1 The previous chapter explained the need for FSIs and how they fit into the wider concept of macroprudential analysis. This chapter considers

14. What Use Can Be Made of the Specific FSIs? Introduction 14.1 The previous chapter explained the need for FSIs and how they fit into the wider concept of macroprudential analysis. This chapter considers