Insurance solutions for catastrophic events Basic approach, conceptual design and examples

|

|

|

- Leslie Wilcox

- 6 years ago

- Views:

Transcription

1 Insurance solutions for catastrophic events Basic approach, conceptual design and examples AIIF Azerbaijan International Insurance Forum Baku - June19th & 20th, 2014 Jürgen Brucker

2 About Munich Re Baku - June19th & 20th, 2014

PLC KA Köln.")

3 Munich Re (Group) Added value within the group Diversified structure More security Munich Re (Group)* Reinsurance Munich Health Primary insurance Corporate Insurance Partner Great Lakes Reinsurance (UK) PLC KA Köln.Assekuranz Agentur GmbH MSF Pritchard Syndicate 318 Temple Insurance Company Watkins Syndicate Belgium Asset Management * This listing is incomplete and provides no precise indication of shareholdings. 3

4 Financial figures Munich Re (Group) All segments contributing to strong Group result Munich Re (Group) FY 2013 Net result 3,342m ( 1,198m in Q4) Delivering good net result supported by sound core business and low tax rate Shareholders' equity 26.2bn (+1.4% vs ) Strong capital position according to all metrics allowing for dividend increase and share buy-back Investment result RoI of 3.5% (3.7% in Q4) Solid result given low interest rates and moderate risk profile Reinsurance Primary insurance Munich Health Net result 2,797m ( 1,089m in Q4) Net result 433m ( 73m in Q4) Net result 150m ( 56m in Q4) 2, P-C Combined ratio 92.1% (89.3% in Q4) Better than target of 94% Life Technical result close to target mix of positive and adverse developments P-C Combined ratio 97.2% (97.5% in Q4) Nat cats in Germany Life Result in line with expectations Health Solid, stable performance Primary insurance Combined ratio 93.5% (93.7% in Q4) Good result largely driven by improved US Medicare business 4

5 Financial figures Munich Re (Group) Significant currency effects partially offset by organic growth Gross premiums written in m ,969 Foreign-exchange effects 1,498 Divestment/Investment 105 Organic growth ,060 Segmental breakdown in m Reinsurance property-casualty 17,013 (33%) ( 0.2%) Primary insurance property-casualty 5,507 (11%) ( 0.8%) Reinsurance life 10,829 (21%) ( 2.7%) Primary insurance life 5,489 (11%) ( 5.3%) Primary insurance health 5,671 (11%) ( 1.1%) Munich Health 6,551 (13%) ( 2.3%) 5

6 Financial figures Solvency and ratings Ratings Rating agency Rating Outlook Last Modification A.M. Best A+ (Superior) Stable 7 Sept Fitch AA- (Very strong) Stable 19 July 2005 Moody s Aa3 (Excellent) Stable 17 March 2005 Standard & Poor s AA- (Very strong) Stable 22 Dec

7 Financial figures Munich Re (Group) Active asset management on the basis of a well-diversified investment portfolio Investment portfolio 1 in % Portfolio management Land and buildings 2.5 (2.4) Shares, equity funds and participating interests (3.7) Miscellaneous (10.0) Loans 28.2 (28.2) TOTAL 218bn Fixed-interest securities 52.9 (55.7) Decreasing market values due to rising interest rates and devaluation of foreign exchange rates Reduction of German, US, UK and Australian government bonds Reduction and ongoing geographic diversification of covered bonds Further cautious expansion of corporate bonds across all industries Increase of equity-backing ratio to 4.5% 2 1 Fair values as at ( ). 2 Net of hedges: 4.5% (3.4%). 3 Deposits retained on assumed reinsurance, unit-linked investments, deposits with banks, investment funds (excl. equities), derivatives and investments in renewable energies/infrastructure and gold. 7

8 Reinsurance Present in all markets Amelia Atlanta Chicago Columbus Hartford Montreal Philadelphia New York Princeton San Francisco Toronto Vancouver Munich London Madrid Malta Milan Moscow Paris Zurich Beijing Calcutta Dubai Hong Kong Kuala Lumpur Mumbai Seoul Shanghai Singapore Taipei Tokyo Bogotá Buenos Aires Caracas Mexico Santiago de Chile São Paulo Accra Cape Town Johannesburg Nairobi Port Louis Auckland Melbourne Sydney 8

9 Agenda 1. Current situation 2. Motivation for new Insurance Solutions 3. Risk awareness/exposure 4. Considerations prior to establishment of pools 5. Pool characteristics 6. Pool structure & protection 7. Further considerations 8. Next steps 9

10 Current situation 1. Worldwide trend - increasing nat cat events 2. Better standard of living combined with increased claims awareness 3. Social changes in the society (lesser reliance on family members in case of an emergency) 4. Urban growth with high value concentration >> higher losses to be expected 5. Severe economic losses if industrialized areas or infrastructure is severely effected 6. High cost burden for governments following a large event may result in cost savings in other public financed sectors of the economy 10

11 NatCatSERVICE Natural catastrophes worldwide Number of events with trend Number Geophysical events (Earthquake, tsunami, volcanic eruption) Meteorological events (Storm) Hydrological events (Flood, mass movement) Climatological events (Extreme temperature, drought, forest fire) 2013 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE As at January

12 NatCatSERVICE Natural catastrophes worldwide Overall and insured losses with trend US$ bn Overall losses (in 2012 values) Insured losses (in 2012 values) Trend overall losses Trend insured losses 2013 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE As at January

Overall losses*: US$ 85bn Insured losses*: US$ 0.3bn Fatalities: 84,000 Floods 1998 China (Yangtze, Songhua) Overall losses*: US$ 30.")

13 NatCatSERVICE Natural catastrophes in Asia Earthquake 2005 Pakistan, India (Kashmir) Overall losses*: US$ 5.2bn Fatalities: 88,000 Earthquake 2008 China (Sichuan) Overall losses*: US$ 85bn Insured losses*: US$ 0.3bn Fatalities: 84,000 Floods 1998 China (Yangtze, Songhua) Overall losses*: US$ 30.7bn Insured losses*: US$ 1bn Fatalities: 4,159 Floods 1996 China Overall losses*: US$ 24bn Insured losses*: US$ 0.45bn Fatalities: 3,048 Earthquake 2004 Japan (Niigata) Overall losses*: US$ 28bn Insured losses*: US$ 0.76bn Natural disasters Significant events * Losses in original values Geophysical events (Earthquake, tsunami, volcanic eruption) Meteorological events (Storm) Hydrological events (Flood, mass movement) Climatological events (Extreme temperature, drought, wildfire) Cyclone, storm surge 1991 Bangladesh Overall losses*: US$ 3bn Insured losses*: US$ 0.1bn Fatalities: 139,000 Cyclone Nargis, storm surge 2008 Myanmar Overall losses*: US$ 4bn Fatalities: 140,000 Earthquake, tsunami 2004 South/Southeast Asia Overall losses*: US$ 11.2bn Insured losses*: US$ 1bn Fatalities: 220,000 Earthquake, tsunami 2011 Japan Overall losses*: US$ 210bn Insured losses*: US$ 35-40bn Fatalities: 15,840 Earthquake 1995 Japan (Kobe) Overall losses*: US$ 100bn Insured losses*: US$ 3bn Fatalities: 6,430 Typhoon Bopha, storm surge 2012 Philippines Overall losses*: US$ 0.3bn Fatalities: >1,000 Missing: >600 Floods, Thailand 2011 Overall losses*: US$ 43bn Insured losses*: US$ 16bn Fatalities: Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE As at January

14 Agenda 1. Current situation 2. Motivation for new Insurance Solutions 3. Risk awareness/exposure 4. Considerations prior to establishment of pools 5. Pool characteristics 6. Pool structure & protection 7. Further considerations 8. Next steps 14

15 Motivation for new Insurance Solutions 1. Disparity of economic losses versus insured losses 2. Severe Cat events could have significant impacts on national budgets 3. Possible collapse of entire economy 4. Stagnation in the economic development for several years 5. Adequate pre loss considerations have proved enormous recovery effects helping to keep downside effects as low as possible 6. More and more countries are looking for possibilities to improve their catastrophe management 7. In general, the risk awareness and (pre loss) risk management of a wider public will improve 15

16 NatCatSERVICE Natural catastrophes worldwide Percentage distribution ordered by continent 21,000 Loss events 2,300,000 Fatalities 32% <1% 8% 12% 2% 24% 7% 6% 52% 27% 9% 21% Overall losses* US$ 3,800bn 3% Insured losses* US$ 970bn 5% 41% 37% 16% 14% 64% 1% 15% 3% *in 2012 values 1% *in 2012 values North America, incl. Central America and Caribbean South America Europe Africa Asia Australia/Oceania 2013 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE As at January

17 NatCatSERVICE Natural catastrophes worldwide Overall losses US$ 3,800bn - Percentage distribution per continent 37% 15% 41% 1% 3% 3% Continent Overall losses US$ m America (North and South America) 1,500,000 Europe 500,000 Africa 45,000 Asia 1,600,000 Australia/Oceania 105, Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE As at January

630,000 Europe 160,000 Africa 2,100 Asia 130,000 Australia/Oceania 42,000 Overall losses US$ m 1,500,000 500,000 45,000 1,600,000 105,000 2013 Münchener Rückversicherungs-Gesellschaft, Geo")

18 NatCatSERVICE Natural catastrophes worldwide Insured losses US$ 970bn - Percentage distribution per continent 64% 16% 14% <1% 1% 5% Continent Insured losses US$ m America (North and South America) 630,000 Europe 160,000 Africa 2,100 Asia 130,000 Australia/Oceania 42,000 Overall losses US$ m 1,500, ,000 45,000 1,600, , Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE As at January

Income Groups 2012 (defined by World Bank, July 2012): High income economies Upper")

(GNI 1,025 US$) 2012 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE As at")

19 NatCatSERVICE Income Groups defined by World Bank 2012 Source: Munich Re based on World Bank (income classification was estimated, if data was not available) Income Groups 2012 (defined by World Bank, July 2012): High income economies Upper middle income economies Lower middle income economies Low income economies (GNI 12,476 US$) (GNI 4,036 12,475 US$) (GNI 1,026 4,035 US$) (GNI 1,025 US$) 2012 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE As at April 2012

20 NatCatSERVICE Natural catastrophes worldwide Income Groups defined by World Bank ,500 Loss events** 2,300,000 Fatalities 9% 6% 18% 47% 46% 18% 26% 30% ** Events reported at individual country level: i.e. storm could affected three countries and is reported as three events. Overall losses* US$ 3,800bn 7% 3% Insured losses* US$ 970bn 1% 5% 23% 67% 94% Income Groups 2012 (defined by World Bank, July 2012): *in 2012 values *in Werten von 2009 *in 2012 values High income economies Upper middle income economies Lower middle income economies Low income economies (GNI 12,476 US$) (GNI 4,036 12,475 US$) (GNI 1,026 4,035 US$) (GNI 1,025 US$) 2013 Münchener Rückversicherungs-Gesellschaft, Geo Risks Research, NatCatSERVICE As at April 2013

21 Agenda 1. Current situation 2. Motivation for new Insurance Solutions 3. Risk awareness/exposure 4. Considerations prior to establishment of pools 5. Pool characteristics 6. Pool structure & protection 7. Further considerations 8. Next steps 21

22 Risk awareness 1. Many countries are characterized by Low risk awareness Lack of corresponding risk management Low insurance penetration 22

23 Reasons for low risk awarnesss 1. People tend to repress bad experiences quite fast 2. Tendency to believe: It won t hit me 3. Large return periods of Nat Cat events 4. Underestimation in most parts of the world 5. People have other priorities instead of buying insurance cover 23

24 Pre loss vs. post loss management 1. Many countries neglect pre loss considerations Advantage: No capital allocation necessary Existing budget can be used for more popular projects Disadvantage: Lack of appropriate monetary funds in case of an event Random distribution of money Politically influenced indemnification, particularly in election years 24

25 Options for the future 1. Joint efforts to change situation prospectively 2. Nationwide insurance as an option 3. Parties needed: Government Insurance industry Individuals (insured) Strong commitment of all parties involved required! 25

26 Overview Azerbaijan Population 26

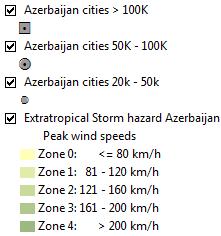

27 Overview Azerbaijan Extratropical Storm 27

28 Overview Azerbaijan Hail 28

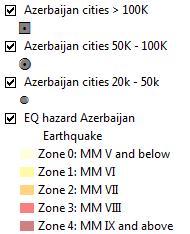

29 Overview Azerbaijan Earthquake 29

30 Azerbaijan EQ Analyses: affected cities / total affected population Affected Population Affected cities (Population > ) EQ Zone Pop. (Mio) Percentage % % % Sum Pop % 30

31 Kazakhstan Analyses: Affected cities / population by EQ Affected Population Affected cities (Population > ) EQ Zone Pop. (Mio) Percentage % % % % % Sum Pop % 31

32 Agenda 1. Current situation 2. Motivation for new Insurance Solutions 3. Risk awareness/exposure 4. Considerations prior to establishment of pools 5. Pool characteristics 6. Pool structure & protection 7. Further considerations 8. Next steps 32

33 Pool considerations Hypothesis 1. Established pools are structured rather individual 2. High level of solidarity in most existing NatCat pools 3. Compulsory insurance recommended for penetration purposes 33

34 Pool Considerations Insurers View Differentiation between public and private liabilities 1. Insured perils 2. Policy construction 3. Territorial scope 4. Insured objects 5. Insured individuals 6. Pool participation 7. Premium 34

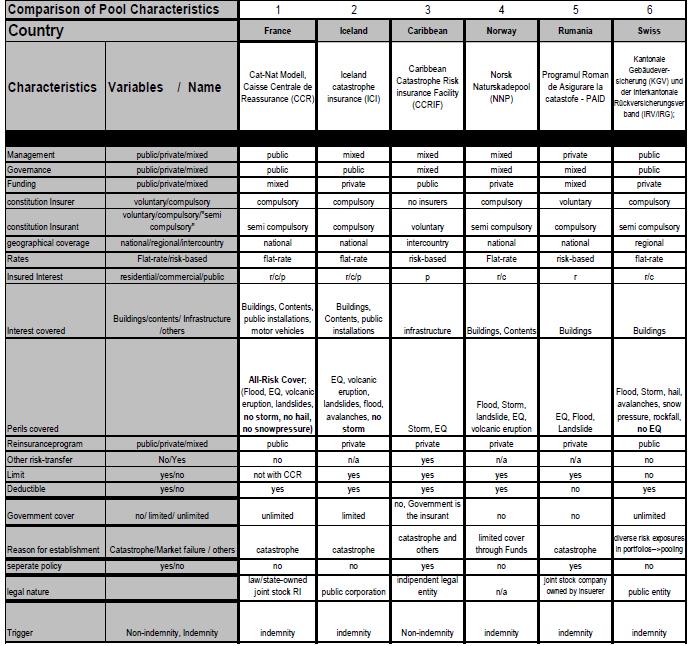

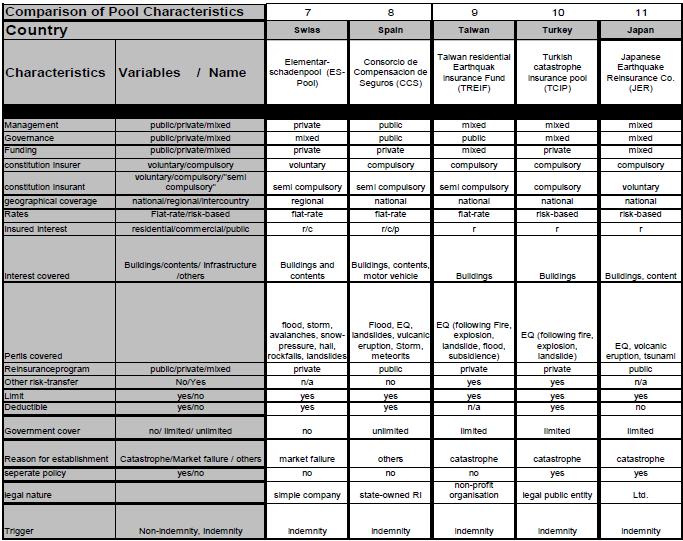

35 Drawing a line between public and private liabilities Catastrophe Insurance Solutions National Pool Solutions Government Covers Overview Role of Government: - Legal framework, - Legal framework, - Supervision, regulation, and/or operation of the insurance pool - Supervision, regulation, and/or operation of a fund, captive or facility Two possible insurance solutions were identified a) Government plays no further role b) Government subsidize the fund - Paying of (re-)insurance premiums from annual budget - Decision about the allocation of resources in cases of natural disasters Policyholder: Private households or companies Public Agencies or Institutions The first option is mostly used for rebuilding private property; second is used for rebuilding public property in case of catastrophic events Funding: Insurance cover is (mostly) financed by private policyholders Insured Assets: Private interest Public property and Examples: a) Turkish Catastrophe Insurance Pool Insurance cover is part of the federal budget and is financed by taxes (and/or donors) bridging of liquidity gaps in federal budgets CCRIF b) Taiwan Residential Earthquake Insurance Pool FONDEN

36 1. Insured perils 1 Single NatCat perils vs. multi NatCat perils Single NatCat peril (EQ only) Advantage: Simple modeling and premium calculation High transparency Disadvantage: No diversification Possible antiselection 36

37 1. Insured perils 2 Single NatCat perils vs. multi NatCat perils Multi NatCat perils (EQ + Flood + Storm + ) Advantage: Wide scope of cover Increased diversification Reduced anti-selection Disadvantage: Complex modeling Lack of transparency 37

38 2. Policy construction - 1 NatCat perils only vs. combination with other perils NatCat perils only Advantage: Transparent Independent from additional perils Disadvantage: No diversification Adverse selection Limited market penetration 38

39 2. Policy construction - 2 NatCat perils only vs. combination with other perils Multi peril policy Advantage: Increased diversification Reduced anti-selection High level of market penetration Disadvantage: Compulsory correlation of different perils 39

40 3. Territorial Scope National National Advantage: Reasonable diversification effects Large number of insured's Easy to agree Disadvantage: Lack of acceptance in less exposed areas 40

41 4. Insured objects - 1 Buildings / Contents / Consequential loss Buildings only Advantage: Protection of large values Easy to administer Disadvantage: Limited protection of values 41

42 4. Insured objects - 2 Buildings / Contents / Consequential loss Buildings & Contents Advantage: Comprehensive cover for private individuals Large collective Disadvantage: Increased loss potential Higher premium for individuals Lack of interest to insure contents Increased administration 42

43 4. Insured objects - 3 Buildings / Contents / Consequential loss Consequential loss Advantage: Comprehensive cover for the industry Reduction of economic losses Disadvantage: Increased loss potential Higher premium for individuals Difficult and time consuming loss adjustment Increased administration 43

44 5. Insured individuals 1 Private vs. Commercial/Industry Private only Advantage: Protection of human population High level of transparency Disadvantage: Limited compensation compared to overall loss 44

45 5. Insured individuals - 2 Private vs. Commercial/Industry Commercial/Industry Advantage: Huge risk collective High level of compensation for incurred losses Disadvantage: Complex modeling Complex premium calculation Lack of transparency 45

46 6. Pool participation - 1 Voluntary vs. compulsory Voluntary Advantage: Fair Limited moral hazard Disadvantage: Reduced market penetration Adverse selection 46

47 6. Pool participation - 2 Voluntary vs. compulsory Compulsory Advantage: High market penetration High level of solidarity Diversification of risks No adverse selection of risks Disadvantage: Increased moral hazard Huge loss potential 47

48 7. Premium -1 Individual vs. flat premium Individual premium Advantage: Fair Reduced anti-selection Reduced moral hazard Disadvantage: More complex Increased operating expenses 48

49 7. Premium - 2 Individual vs. flat premium Flat premium Advantage: Easy to administer Disadvantage: Unfair Does not reflect exposure Increased moral hazard Adverse selection 49

50 Agenda 1. Current situation 2. Motivation for new Insurance Solutions 3. Risk awareness/exposure 4. Considerations prior to establishment of pools 5. Pool characteristics 6. Pool structure & protection 7. Further considerations 8. Next steps 50

51 Pool characteristics Premium pool Premium collection through insurers Transfer of premium to pool Transfer of risk to pool Commission paid to insurers as compensation for distribution efforts Claims settlement: Insurers manpower and expertise used for loss adjustment Specialized loss adjusters on behalf of pool organization 51

52 Pool characteristics Loss pool Premium collection through insurers Premium is retained by insurers Pool organizes reinsurance Claims settlement: Agreed percentage of loss is retained by individual insurers Excess loss is aggregated through pool Distribution of pool-loss according to market share of insurers 52

53 Agenda 1. Current situation 2. Motivation for new Insurance Solutions 3. Risk awareness/exposure 4. Considerations prior to establishment of pools 5. Pool characteristics 6. Pool structure & protection 7. Further considerations 8. Next steps 53

54 Possible pool structure 54

55 International Cat Pools 55

56 International Cat Pools 56

57 International Cat Pools 57

58 Basis of indemnification It needs to be distinguished between the different parties involved Insured Insurer Indemnification of actual sustained loss net of deductible Insurer/Pool Reinsurer/Capital market Depending on structure, a priority and a maximum limit will be applied Government Depending on involvement, government may act as lender of last resort 58

59 Basis of indemnification - pool perspective - 1 Actual sustained loss vs. parametric trigger Actual sustained loss Advantage: Fair No base risk Loss adequate indemnification, subject to capacity Disadvantage: Time consuming to establish the ultimate loss High degree of administration 59

60 Basis of indemnification - pool perspective - 2 Actual sustained loss vs. parametric trigger Parametric trigger (an independent indicator is used to trigger the cover, e.g. amplitude >7.5 on the Mercalli scale at a given gauging station, economical loss) Advantage: Quick compensation Low administration (post loss) Limited moral hazard Disadvantage: Based on synthetic trigger, irrespective of actual loss Gauging station may not record the required amplitude, despite a significant loss elsewhere 60

61 Basis of indemnification - pool perspective - 3 Actual sustained loss vs. parametric trigger Possible trigger: - Subjective measure of the strength of an earthquake, assessed on the basis of local damage - Discrete twelve-graded Mercalli scale - Decreases with increasing focal distance Epicentre Km IX VIII VII VI 61

62 Pool protection - 1 Low return periods vs. high return periods Low return periods (low capacity) Advantage: Easy to finance Easy to reinsure Disadvantage: Limited compensation Not in line with principle aim to achieve reasonable protection Lack of acceptance 62

63 Pool protection - 2 Low return periods vs. high return periods High return periods (>200 years return period high capacity) Advantage: High comfort level High level of acceptance Disadvantage: Difficult to structure and finance 63

64 Possible pool funding & protection Capacity e.g. 1bn Government protection Cession to capital market Reinsurer Y Retention pool Reinsurer X Retention pool 64

65 Agenda 1. Current situation 2. Motivation for new Insurance Solutions 3. Risk awareness/exposure 4. Considerations prior to establishment of pools 5. Pool characteristics 6. Pool structure & protection 7. Further considerations 8. Next steps 65

66 Further considerations Disaster management Recovery considerations Building codes Tax incentives 66

67 Agenda 1. Current situation 2. Motivation for new Insurance Solutions 3. Risk awareness/exposure 4. Considerations prior to establishment of pools 5. Pool characteristics 6. Pool structure & protection 7. Further considerations 8. Next steps 67

68 Next steps 1. Commitment of all involved parties to proceed 2. Discussion of proposed options 3. Involvement of further stakeholders 4. Az EQ Model 68

< 1,000 1,000-3,000 3,000-6,000 6,000-10,000 > 10,000 Mio.")

69 % Major Nagasaki Kita Kyushu % % % Fukuoka Hiroshima % Kyoto % Kobe % % Osaka % Nagoya Tokyo % % % Kawasaki Yokohama % % Aomori Sapporo The Munich Re risk model: MRHazard Hazard information Value distribution Cities Industrial Sum Insured (Earthquake) < 1,000 1,000-3,000 3,000-6,000 6,000-10,000 > 10,000 Mio. Individual exposure Set of scenarios Risk curve Vulnerability function Kilometers Expected loss/ loss occurrence probability Statistics 69

70 Thank you very much indeed for your attention Jürgen Brucker

WEATHER EXTREMES, CLIMATE CHANGE,

WEATHER EXTREMES, CLIMATE CHANGE, DURBAN 2011 ELECTRONIC PRESS FOLDER Status: 25.11.2011 Contents 1. Current meteorological knowledge 2. Extreme weather events 3. Political action required 4. Insurance

WEATHER EXTREMES, CLIMATE CHANGE, DURBAN 2011 ELECTRONIC PRESS FOLDER Status: 25.11.2011 Contents 1. Current meteorological knowledge 2. Extreme weather events 3. Political action required 4. Insurance

AND IPCC. Who is Munich RE? Insurance Industry, one of the First Alerter s of Global Warming. Outline. MR-Publication Flood / Inundation (August 1973)

") Who is Munich RE? Insurer of Insurances Founded 1880 The world s largest re-insurer Premium income ca. 22 bn Leading role in insurance of natural catastrophes SEMINAR: SYDNEY COASTAL COUNCILS GROUP FORUM

Who is Munich RE? Insurer of Insurances Founded 1880 The world s largest re-insurer Premium income ca. 22 bn Leading role in insurance of natural catastrophes SEMINAR: SYDNEY COASTAL COUNCILS GROUP FORUM

The Emerging Importance of Improving Resilience to Hazards. Presentation to: West Michigan Sustainable Business Forum November 14, 2016 Dale Sands

The Emerging Importance of Improving Resilience to Hazards Presentation to: West Michigan Sustainable Business Forum November 14, 216 Dale Sands Agenda Resilience Defined Driving Forces Of Resilience Improvement

The Emerging Importance of Improving Resilience to Hazards Presentation to: West Michigan Sustainable Business Forum November 14, 216 Dale Sands Agenda Resilience Defined Driving Forces Of Resilience Improvement

BADEN-BADEN 2011 IS THE MARKET READY TO CHANGE?

BADEN-BADEN 2011 IS THE MARKET READY TO CHANGE? 24 October 2011 Ludger Arnoldussen Key topics and challenging issues for the insurance business Low-interest-rate environment High natural catastrophe losses

BADEN-BADEN 2011 IS THE MARKET READY TO CHANGE? 24 October 2011 Ludger Arnoldussen Key topics and challenging issues for the insurance business Low-interest-rate environment High natural catastrophe losses

Climate Change and Natural Disasters: Economic Impacts and Possible Countermeasures

Climate Change and Natural Disasters: Economic Impacts and Possible Countermeasures Prof. Dr. Gerhard Berz, ret. Head, Geo Risks Research Dept., Munich Reinsurance Company Natural Disasters 1980-2005

Climate Change and Natural Disasters: Economic Impacts and Possible Countermeasures Prof. Dr. Gerhard Berz, ret. Head, Geo Risks Research Dept., Munich Reinsurance Company Natural Disasters 1980-2005

Insurers as Data Providers. Raising Awareness of Changing Risks. What can Insurers Contribute to Increase Resilience Against Weather Extremes?

What can Insurers Contribute to Increase Resilience Against Weather Extremes? Prof. Dr. Peter Hoeppe, Head Geo Risks Research/Corporate Climate Centre, Munich Re 5 th European Communications Workshop for

What can Insurers Contribute to Increase Resilience Against Weather Extremes? Prof. Dr. Peter Hoeppe, Head Geo Risks Research/Corporate Climate Centre, Munich Re 5 th European Communications Workshop for

Insuring Climate Change-related Risks

Insuring Climate Change-related Risks 19 February 2016 Austrian Climate Change Workshop Day 2 Tobias Grimm Senior Project Manager Corporate Climate Centre Climate & Renewables Munich Re some facts About

Insuring Climate Change-related Risks 19 February 2016 Austrian Climate Change Workshop Day 2 Tobias Grimm Senior Project Manager Corporate Climate Centre Climate & Renewables Munich Re some facts About

Economic Risk and Potential of Climate Change

Economic Risk and Potential of Climate Change Prof. Dr. Peter Hoeppe; Dr. Ernst Rauch This document appeared in Detlef Stolten, Bernd Emonts (Eds.): 18th World Hydrogen Energy Conference 2010 - WHEC 2010

Economic Risk and Potential of Climate Change Prof. Dr. Peter Hoeppe; Dr. Ernst Rauch This document appeared in Detlef Stolten, Bernd Emonts (Eds.): 18th World Hydrogen Energy Conference 2010 - WHEC 2010

Source: NOAA 2011 NATURAL CATASTROPHE YEAR IN REVIEW

Source: NOAA 2011 NATURAL CATASTROPHE YEAR IN REVIEW January 4, 4 2012 U.S. NATURAL CATASTROPHE UPDATE Carl Hedde, SVP, Head of Risk Accumulation Munich Reinsurance America, Inc. MR NatCatSERVICE One of

Source: NOAA 2011 NATURAL CATASTROPHE YEAR IN REVIEW January 4, 4 2012 U.S. NATURAL CATASTROPHE UPDATE Carl Hedde, SVP, Head of Risk Accumulation Munich Reinsurance America, Inc. MR NatCatSERVICE One of

NAT-CAT RISK MANAGEMENT. Thomas Mahl, RID 1.3

NAT-CAT RISK MANAGEMENT Thomas Mahl, RID 1.3 Global Loss Trend and its Drivers The last 30 years have seen a significant increase in losses caused by natural disasters Natural catastrophes in Asia 1980

NAT-CAT RISK MANAGEMENT Thomas Mahl, RID 1.3 Global Loss Trend and its Drivers The last 30 years have seen a significant increase in losses caused by natural disasters Natural catastrophes in Asia 1980

Sal. Oppenheim European Financial Conference

Sal. Oppenheim European Financial Conference Zurich November 20, 2007 Renato Fassbind, Chief Financial Officer Cautionary statement Cautionary statement regarding forward-looking and non-gaap information

Sal. Oppenheim European Financial Conference Zurich November 20, 2007 Renato Fassbind, Chief Financial Officer Cautionary statement Cautionary statement regarding forward-looking and non-gaap information

Megacities - Megarisks. Munich Re media conference 11 January 2005

Munich Re media conference 11 January 2005 Agenda The climate in megacities 3 Prof. Peter Höppe 10 Dr. Anselm Smolka 2 The climate in megacities Impact on the health of the population and on life and health

Munich Re media conference 11 January 2005 Agenda The climate in megacities 3 Prof. Peter Höppe 10 Dr. Anselm Smolka 2 The climate in megacities Impact on the health of the population and on life and health

The Strategic Risk Forum The Insurance Institute of South Africa Breakfast Session on HAIL. 30 May 2014

The Strategic Risk Forum The Insurance Institute of South Africa Breakfast Session on HAIL 30 May 2014 Hail exposure and risk management in crop production Global view and focus on South Africa 30.05.2014

The Strategic Risk Forum The Insurance Institute of South Africa Breakfast Session on HAIL 30 May 2014 Hail exposure and risk management in crop production Global view and focus on South Africa 30.05.2014

Methodology Overview. Dr. Andrew Coburn. Director of Advisory Board of Cambridge Centre for Risk Studies and Senior Vice President of RMS Inc.

Methodology Overview Dr. Andrew Coburn Director of Advisory Board of Cambridge Centre for Risk Studies and Senior Vice President of RMS Inc. 3 September 2015 What s ground breaking about this study? This

Methodology Overview Dr. Andrew Coburn Director of Advisory Board of Cambridge Centre for Risk Studies and Senior Vice President of RMS Inc. 3 September 2015 What s ground breaking about this study? This

9,697 Dead people. 96 million People affected. Lower mortality, higher cost

335 Reported disasters 9,697 Dead people 96 million People affected 334 billion US$ economic damage Lower mortality, higher cost Executive Summary In, 335 natural disasters affected over 95.6 million people,

335 Reported disasters 9,697 Dead people 96 million People affected 334 billion US$ economic damage Lower mortality, higher cost Executive Summary In, 335 natural disasters affected over 95.6 million people,

Catastrophe Risk Financing Instruments. Abhas K. Jha Regional Coordinator, Disaster Risk Management East Asia and the Pacific

Catastrophe Risk Financing Instruments Abhas K. Jha Regional Coordinator, Disaster Risk Management East Asia and the Pacific Structure of Presentation Impact of Disasters in developing Countries The Need

Catastrophe Risk Financing Instruments Abhas K. Jha Regional Coordinator, Disaster Risk Management East Asia and the Pacific Structure of Presentation Impact of Disasters in developing Countries The Need

Natural Catastrophes in the Bond Market - A Trader s View

Natural Catastrophes in the Bond Market - A Trader s View Risk Trading Unit Trading risk into value Innsbruck, July 2007 Marcel Grandi 1 Agenda 1. Market development and functional areas 2. Examining the

Natural Catastrophes in the Bond Market - A Trader s View Risk Trading Unit Trading risk into value Innsbruck, July 2007 Marcel Grandi 1 Agenda 1. Market development and functional areas 2. Examining the

The Strategic Risk Forum The Insurance Institute of South Africa Breakfast Session on HAIL. 30 May 2014

The Strategic Risk Forum The Insurance Institute of South Africa Breakfast Session on HAIL 30 May 2014 Hail exposure and risk management in crop production Global view and focus on South Africa 30.05.2014

The Strategic Risk Forum The Insurance Institute of South Africa Breakfast Session on HAIL 30 May 2014 Hail exposure and risk management in crop production Global view and focus on South Africa 30.05.2014

Investor Presentation

Investor Presentation May 2013 48,000 employees 200 offices 70 countries 1 global platform Table of Contents I. Company Description II. Global Growth Strategy III. Financial Overview IV. Appendix 2 Company

Investor Presentation May 2013 48,000 employees 200 offices 70 countries 1 global platform Table of Contents I. Company Description II. Global Growth Strategy III. Financial Overview IV. Appendix 2 Company

Merrill Lynch Banking & Insurance Conference

Merrill Lynch Banking & Insurance Conference October 8, 2008 London Brady W. Dougan, Chief Executive Officer Cautionary statement Cautionary statement regarding forward-looking and non-gaap information

Merrill Lynch Banking & Insurance Conference October 8, 2008 London Brady W. Dougan, Chief Executive Officer Cautionary statement Cautionary statement regarding forward-looking and non-gaap information

watsonwyatt.com Compensation Discussion and Analysis Scorecard

Compensation Discussion and Analysis Scorecard The Securities and Exchange Commission s (SEC) proxy disclosure rules, effective for 2007 proxy filings, require extremely detailed and complicated disclosures

Compensation Discussion and Analysis Scorecard The Securities and Exchange Commission s (SEC) proxy disclosure rules, effective for 2007 proxy filings, require extremely detailed and complicated disclosures

Does M&A insurance close the gap? German M&A and Private Equity Forum March Clemens Küppers Private Equity and M&A Practice

Does M&A insurance close the gap? German M&A and Private Equity Forum 2015 19 March 2015 Clemens Küppers Private Equity and M&A Practice Marsh & McLennan Companies delivers advice and solutions that help

Does M&A insurance close the gap? German M&A and Private Equity Forum 2015 19 March 2015 Clemens Küppers Private Equity and M&A Practice Marsh & McLennan Companies delivers advice and solutions that help

Emerging risks and insurability in a complex environment

Emerging risks and insurability in a complex environment Dr. Markus Wadé Integrated Risk Management Group Accumulation & Emerging Risks Sopot, 7 May 2014 Organisation of Munich Re Munich Re (Group)* Reinsurance

Emerging risks and insurability in a complex environment Dr. Markus Wadé Integrated Risk Management Group Accumulation & Emerging Risks Sopot, 7 May 2014 Organisation of Munich Re Munich Re (Group)* Reinsurance

CORPORATE PROFILE. Mitsui Sumitomo Insurance

CORPORATE PROFILE Mitsui Sumitomo Insurance Corporate Data ( As of March 31, 2017 ) Responsible for non-life insurance business, which is a core business of the MS&AD Insurance Group, Mitsui Sumitomo Insurance

CORPORATE PROFILE Mitsui Sumitomo Insurance Corporate Data ( As of March 31, 2017 ) Responsible for non-life insurance business, which is a core business of the MS&AD Insurance Group, Mitsui Sumitomo Insurance

Vontobel Summer Conference

Pierre L. Ozendo Member of the Executive board Head of Asia Division Cautionary note on forward-looking statements Slide 2 Certain statements contained herein are forward-looking. These statements provide

Pierre L. Ozendo Member of the Executive board Head of Asia Division Cautionary note on forward-looking statements Slide 2 Certain statements contained herein are forward-looking. These statements provide

The financial implications of climate change: the North East and beyond. Focus on Climate Change, Pace Energy and Climate Center, June 27, 2012

The financial implications of climate change: the North East and beyond Focus on Climate Change, Pace Energy and Climate Center, June 27, 2012 Agenda Introduction Financial impacts of weather extremes

The financial implications of climate change: the North East and beyond Focus on Climate Change, Pace Energy and Climate Center, June 27, 2012 Agenda Introduction Financial impacts of weather extremes

Chapter 2: Natural Disasters and Sustainable Development

Chapter 2: Natural Disasters and Sustainable Development This chapter addresses the importance of the link between disaster reduction frameworks and development initiatives, based on the disaster trends

Chapter 2: Natural Disasters and Sustainable Development This chapter addresses the importance of the link between disaster reduction frameworks and development initiatives, based on the disaster trends

Chapter 2: Natural Disasters and Sustainable Development

Chapter 2: Natural Disasters and Sustainable Development This chapter addresses the importance of the link between disaster reduction frameworks and development initiatives, based on the disaster trends

Chapter 2: Natural Disasters and Sustainable Development This chapter addresses the importance of the link between disaster reduction frameworks and development initiatives, based on the disaster trends

Reinsurance: Emerging vs. Mature markets

Reinsurance: Emerging vs. Mature markets AM Best conference - 17 October 2013 Denis Kessler CEO & Chairman of SCOR Section 1 Emerging markets growth is widely recognised as key for the future of the (re)insurance

Reinsurance: Emerging vs. Mature markets AM Best conference - 17 October 2013 Denis Kessler CEO & Chairman of SCOR Section 1 Emerging markets growth is widely recognised as key for the future of the (re)insurance

Innovative Insurance Solutions for Climate Change: How to integrate climate risk insurance into a comprehensive climate risk management approach

Innovative Insurance Solutions for Climate Change: How to integrate climate risk insurance into a comprehensive climate risk management approach Number 500 NatCatSERVICE Natural catastrophes worldwide,

Innovative Insurance Solutions for Climate Change: How to integrate climate risk insurance into a comprehensive climate risk management approach Number 500 NatCatSERVICE Natural catastrophes worldwide,

Insurance Industry solutions for disaster risk financing. 22 th October 2013 Michael Spranger

Insurance Industry solutions for disaster risk financing 22 th October 2013 Michael Spranger A reminder - Asian EQ hazard Aon Benfield APAC Proprietary & Confidential 1 Seismicity and EQ hazard map Philippines

Insurance Industry solutions for disaster risk financing 22 th October 2013 Michael Spranger A reminder - Asian EQ hazard Aon Benfield APAC Proprietary & Confidential 1 Seismicity and EQ hazard map Philippines

ICRM Seminar 2014General

Closing the Nat Cat protection gap: Jakarta General Agenda What is Nat Cat protection gap? Nat Cat risk to Jakarta Estimation of insured and insurable portfolio Assumptions for Nat Cat modeling Nat Cat

Closing the Nat Cat protection gap: Jakarta General Agenda What is Nat Cat protection gap? Nat Cat risk to Jakarta Estimation of insured and insurable portfolio Assumptions for Nat Cat modeling Nat Cat

Natural catastrophes: A risk transfer concept for Italy

Natural catastrophes: A risk transfer concept for Italy AIDA Michael seminar Schwarz, on natural December catastrophes 2007 Milan, 19 January 2009 AIDA Seminar, 19 January 10 Nat Cat Insurance Solutions

Natural catastrophes: A risk transfer concept for Italy AIDA Michael seminar Schwarz, on natural December catastrophes 2007 Milan, 19 January 2009 AIDA Seminar, 19 January 10 Nat Cat Insurance Solutions

INTERNATIONAL ACCOUNTING

A Seventh Edition INTERNATIONAL ACCOUNTING INTERNATIONAL EDITION Frederick D. S. Choi New York University Gary K. Meek Oklahoma State University Boston Columbus Indianapolis New York San Francisco Upper

A Seventh Edition INTERNATIONAL ACCOUNTING INTERNATIONAL EDITION Frederick D. S. Choi New York University Gary K. Meek Oklahoma State University Boston Columbus Indianapolis New York San Francisco Upper

Business Performance & Strategy. Separate Financial Result as of FY

W Business Performance & Strategy Separate Financial Result as of FY 2016. 6 Korean Re Profile 2 Korean Re Key Facts History 1963 : Established as Korean non-life reinsurance corporation (state run company)

W Business Performance & Strategy Separate Financial Result as of FY 2016. 6 Korean Re Profile 2 Korean Re Key Facts History 1963 : Established as Korean non-life reinsurance corporation (state run company)

Post July 2013 Renewal Update

Catastrophe Reinsurance Post July 213 Renewal Update 1 July 213 Australian and New Zealand Catastrophe reinsurance renewals saw an additional AUD1.2 billion of vertical catastrophe reinsurance purchased

Catastrophe Reinsurance Post July 213 Renewal Update 1 July 213 Australian and New Zealand Catastrophe reinsurance renewals saw an additional AUD1.2 billion of vertical catastrophe reinsurance purchased

MICROINSURANCE SCHEMES FOR PROPERTY: EXAMPLES FROM LATIN AMERICA

MICROINSURANCE SCHEMES FOR PROPERTY: EXAMPLES FROM LATIN AMERICA A. Smolka 1, A. Moser 2, A. Allmann 3, D. Hollnack 3, and M. Spranger 4 1 Head, Risk Evaluation Natural Perils, GeoRisks Research, Munich

MICROINSURANCE SCHEMES FOR PROPERTY: EXAMPLES FROM LATIN AMERICA A. Smolka 1, A. Moser 2, A. Allmann 3, D. Hollnack 3, and M. Spranger 4 1 Head, Risk Evaluation Natural Perils, GeoRisks Research, Munich

EVALUATING CDM PROJECT RISKS: AN INSURER'S PERSPECTIVE. Johannesburg, November Jonathan Young Underwriter, Carbon Risks

EVALUATING CDM PROJECT RISKS: AN INSURER'S PERSPECTIVE Johannesburg, Jonathan Young Underwriter, Carbon Risks http://www.nasa.gov/audience/foreducators/topnav/materials/listbytype/apollo.17.view.of.earth.html

EVALUATING CDM PROJECT RISKS: AN INSURER'S PERSPECTIVE Johannesburg, Jonathan Young Underwriter, Carbon Risks http://www.nasa.gov/audience/foreducators/topnav/materials/listbytype/apollo.17.view.of.earth.html

INVEST WITH A GLOBAL LEADER

INVEST WITH A GLOBAL LEADER Since 1947, our firm has been dedicated to delivering exceptional asset management for our institutional, retail, and high-net-worth clients. By bringing together multiple,

INVEST WITH A GLOBAL LEADER Since 1947, our firm has been dedicated to delivering exceptional asset management for our institutional, retail, and high-net-worth clients. By bringing together multiple,

Munich Re THE RISKS OF CLIMATE CHANGE INNOVATIVE PROJECTS OF MUNICH RE. Prof. Dr. Peter Hoeppe Head of Geo Risks Research/Corporate Climate Centre

THE RISKS OF CLIMATE CHANGE INNOVATIVE PROJECTS OF MUNICH RE Prof. Dr. Peter Hoeppe Head of Geo Risks Research/Corporate Climate Centre Lunchtime Colloquium, Rachel Carson Center, Munich, April 12, 2012

THE RISKS OF CLIMATE CHANGE INNOVATIVE PROJECTS OF MUNICH RE Prof. Dr. Peter Hoeppe Head of Geo Risks Research/Corporate Climate Centre Lunchtime Colloquium, Rachel Carson Center, Munich, April 12, 2012

Employers pension consultation obligations

Financial institutions Energy Infrastructure, mining and commodities Transport Technology and innovation Life sciences and healthcare Employers pension consultation obligations Briefing December 2017 Introduction

Financial institutions Energy Infrastructure, mining and commodities Transport Technology and innovation Life sciences and healthcare Employers pension consultation obligations Briefing December 2017 Introduction

Supplemental Information Fourth Quarter 2011 Earnings Call

Supplemental Information Fourth Quarter 2011 Earnings Call Market & Financial Overview Capital Values Q4 2010 Shanghai, Washington DC, London Singapore Q4 2011 Hong Kong Shanghai Beijing Milan, New York

Supplemental Information Fourth Quarter 2011 Earnings Call Market & Financial Overview Capital Values Q4 2010 Shanghai, Washington DC, London Singapore Q4 2011 Hong Kong Shanghai Beijing Milan, New York

China A-Shares: Too Big to Ignore

RESEARCH SPOTLIGHT China A-Shares: Too Big to Ignore China A-shares make up 34% of the total China investment opportunity set yet are often missing from a typical institutional investor s portfolio due

RESEARCH SPOTLIGHT China A-Shares: Too Big to Ignore China A-shares make up 34% of the total China investment opportunity set yet are often missing from a typical institutional investor s portfolio due

This Is Commerzbank. An Overview. Commerzbank AG Group Communications Frankfurt, 8 February 2018

This Is Commerzbank An Overview Commerzbank AG Group Communications Frankfurt, 8 February 2018 Agenda 1 Facts and Figures page 2 5 2 Board of Managing Directors page 6 3 Strategic Positioning page 7 4

This Is Commerzbank An Overview Commerzbank AG Group Communications Frankfurt, 8 February 2018 Agenda 1 Facts and Figures page 2 5 2 Board of Managing Directors page 6 3 Strategic Positioning page 7 4

UNDERSTANDING FINANCIAL STATEMENTS

UNDERSTANDING FINANCIAL STATEMENTS N I N T H E D I T I O N Lyn M. Fraser Aileen Ormiston Boston Columbus Indianapolis New York San Francisco Upper Saddle River Amsterdam Cape Town Dubai London Madrid Milan

UNDERSTANDING FINANCIAL STATEMENTS N I N T H E D I T I O N Lyn M. Fraser Aileen Ormiston Boston Columbus Indianapolis New York San Francisco Upper Saddle River Amsterdam Cape Town Dubai London Madrid Milan

Desalination Performance Cover DME-Seminar S in Jeddah

Desalination Performance Cover DME-Seminar S-006-2013 in Jeddah Green Tech Solutions 2013 Dr. Volker Kraus Munich RE Diversified structure Diversified risk Munich Re (Group)* Reinsurance Munich Health

Desalination Performance Cover DME-Seminar S-006-2013 in Jeddah Green Tech Solutions 2013 Dr. Volker Kraus Munich RE Diversified structure Diversified risk Munich Re (Group)* Reinsurance Munich Health

May Global Growth Strategy

May 2012 Global Growth Strategy Jones Lang LaSalle Global Growth Strategy G1 G3 Build our local and regional leasing and capital markets businesses G5 Connections Capture the leading share of global capital

May 2012 Global Growth Strategy Jones Lang LaSalle Global Growth Strategy G1 G3 Build our local and regional leasing and capital markets businesses G5 Connections Capture the leading share of global capital

Sponsored by the Government of Japan

Sponsored by the Government of Japan GLOBAL SEMINAR ON DISASTER RISK FINANCING: TOWARDS THE DEVELOPMENT OF EFFECTIVE APPROACHES TO THE FINANCIAL MANAGEMENT OF DISASTER RISKS 17-18 September 2015 Kuala

Sponsored by the Government of Japan GLOBAL SEMINAR ON DISASTER RISK FINANCING: TOWARDS THE DEVELOPMENT OF EFFECTIVE APPROACHES TO THE FINANCIAL MANAGEMENT OF DISASTER RISKS 17-18 September 2015 Kuala

IT ONLY TAKES ONE INDEX TO CAPTURE THE WORLD THE MODERN INDEX STRATEGY. msci.com

IT ONLY TAKES ONE INDEX TO CAPTURE THE WORLD THE MODERN INDEX STRATEGY msci.com MSCI DELIVERS THE MODERN INDEX STRATEGY The MSCI ACWI Index, MSCI s flagship global equity benchmark, is designed to represent

IT ONLY TAKES ONE INDEX TO CAPTURE THE WORLD THE MODERN INDEX STRATEGY msci.com MSCI DELIVERS THE MODERN INDEX STRATEGY The MSCI ACWI Index, MSCI s flagship global equity benchmark, is designed to represent

Retail: Competing in the New World J.P. Morgan UK Financials Conference Wednesday, 8 December 2010

Retail: Competing in the New World J.P. Morgan UK Financials Conference Wednesday, 8 December 2010 James Cardew Global Head of Marketing Schroders plc Agenda Schroders Global business Schroders UK intermediary

Retail: Competing in the New World J.P. Morgan UK Financials Conference Wednesday, 8 December 2010 James Cardew Global Head of Marketing Schroders plc Agenda Schroders Global business Schroders UK intermediary

Rising dividend after good result Preliminary financial statements as at 31 December 2014

Rising dividend after good result 5 February 205 Jörg Schneider Munich Re (Group) Financial highlights Q4 204 Good annual profit of 3.2bn Dividend increasing to 7.75 per share Munich Re (Group) Q4 204

Rising dividend after good result 5 February 205 Jörg Schneider Munich Re (Group) Financial highlights Q4 204 Good annual profit of 3.2bn Dividend increasing to 7.75 per share Munich Re (Group) Q4 204

Natural Disasters in 2007: An Analytical Overview

Natural Disasters in 2007: An Analytical Overview Chapter 1: Impact of Natural Disasters This chapter deals with the overall trends in natural disasters and their impacts for the year 2007. It also addresses

Natural Disasters in 2007: An Analytical Overview Chapter 1: Impact of Natural Disasters This chapter deals with the overall trends in natural disasters and their impacts for the year 2007. It also addresses

Opportunities for Action in Financial Services. Crafting New Approaches to Offshore Markets

OffshoreMarkets 12/8/03 2:55 PM Page 1 Opportunities for Action in Financial Services Crafting New Approaches to Offshore Markets Crafting New Approaches to Offshore Markets The European offshore-wealth

OffshoreMarkets 12/8/03 2:55 PM Page 1 Opportunities for Action in Financial Services Crafting New Approaches to Offshore Markets Crafting New Approaches to Offshore Markets The European offshore-wealth

A LIQUID BENCHMARK FOR PRIVATE REAL ESTATE

A LIQUID BENCHMARK FOR PRIVATE REAL ESTATE Commercial real estate represents an important element of the asset allocation process but is difficult to access directly, with high barriers to entry and exit.

A LIQUID BENCHMARK FOR PRIVATE REAL ESTATE Commercial real estate represents an important element of the asset allocation process but is difficult to access directly, with high barriers to entry and exit.

Catastrophic risks do we have enough protection reinsurers view

Image: used under license from Shutterstock.com Catastrophic risks do we have enough protection reinsurers view IV. International Istanbul Insurance Conference Istanbul, 25 th September 2014 Jürgen Brucker

Image: used under license from Shutterstock.com Catastrophic risks do we have enough protection reinsurers view IV. International Istanbul Insurance Conference Istanbul, 25 th September 2014 Jürgen Brucker

Conference Call on Interim Report 3/2017

Conference Call on Interim Report 3/2017 Hannover, 8 November 2017 Q3 losses absorbed within quarterly earnings Positive Q3 result supported by sale of listed equities Group Gross written premium: EUR

Conference Call on Interim Report 3/2017 Hannover, 8 November 2017 Q3 losses absorbed within quarterly earnings Positive Q3 result supported by sale of listed equities Group Gross written premium: EUR

NEUBERGER BERMAN Environmental, Social and Governance Policy

NEUBERGER BERMAN Environmental, Social and Governance Policy SEPTEMBER 2017 OUR FIRM Founded in 1939, Neuberger Berman is a private, 100% independent, employee-owned investment manager. From offices in

NEUBERGER BERMAN Environmental, Social and Governance Policy SEPTEMBER 2017 OUR FIRM Founded in 1939, Neuberger Berman is a private, 100% independent, employee-owned investment manager. From offices in

An Overview of Disaster Risk Financing Instruments in the World Bank Operations

GFDRR sponsored BBL, Washington DC An Overview of Disaster Risk Financing Instruments in the World Bank Operations Eugene N. Gurenko, Ph.D., CPCU, ARe Lead Insurance Specialist March 4, 2009 Contents Disaster

GFDRR sponsored BBL, Washington DC An Overview of Disaster Risk Financing Instruments in the World Bank Operations Eugene N. Gurenko, Ph.D., CPCU, ARe Lead Insurance Specialist March 4, 2009 Contents Disaster

LOOKING TO EXPAND YOUR INVESTMENT HORIZON? THE MODERN INDEX STRATEGY. msci.com

LOOKING TO EXPAND YOUR INVESTMENT HORIZON? THE MODERN INDEX STRATEGY msci.com MSCI DELIVERS THE MODERN INDEX STRATEGY The MSCI Emerging Markets Index is designed to represent the performance of large-

LOOKING TO EXPAND YOUR INVESTMENT HORIZON? THE MODERN INDEX STRATEGY msci.com MSCI DELIVERS THE MODERN INDEX STRATEGY The MSCI Emerging Markets Index is designed to represent the performance of large-

2016 FULL YEAR RESULTS. February 28th, 2017

2016 FULL YEAR RESULTS February 28th, 2017 INTRODUCTORY MATERS Forward-Looking Information This document contains certain forward-looking statements which speak only as of the date on which they are made.

2016 FULL YEAR RESULTS February 28th, 2017 INTRODUCTORY MATERS Forward-Looking Information This document contains certain forward-looking statements which speak only as of the date on which they are made.

DEMYSTIFYING THE MARKET STORM: A FACTOR PERSPECTIVE

DEMYSTIFYING THE MARKET STORM: A FACTOR PERSPECTIVE Many market observers could see signs of a coming storm long before stock prices started to slide. Among these indicators were outflows from the large

DEMYSTIFYING THE MARKET STORM: A FACTOR PERSPECTIVE Many market observers could see signs of a coming storm long before stock prices started to slide. Among these indicators were outflows from the large

Financial Solutions for Risk Management. Sovereign Debt Management Forum Washington DC October 20, 2016

Financial Solutions for Risk Management Sovereign Debt Management Forum Washington DC October 20, 2016 Uninsured losses from natural catastrophes are a growing burden for governments Natural catastrophe

Financial Solutions for Risk Management Sovereign Debt Management Forum Washington DC October 20, 2016 Uninsured losses from natural catastrophes are a growing burden for governments Natural catastrophe

Schroders. KBW European Financials Conference. Massimo Tosato Vice Chairman. 17 September trusted heritage advanced thinking

Schroders KBW European Financials Conference Massimo Tosato Vice Chairman trusted heritage advanced thinking 17 September 2008 Schroders plc Overview Independent Exclusive focus on asset management Global

Schroders KBW European Financials Conference Massimo Tosato Vice Chairman trusted heritage advanced thinking 17 September 2008 Schroders plc Overview Independent Exclusive focus on asset management Global

Goldman Sachs 18 th Annual European Financials Conference. Edouard Schmid, Head Property & Specialty Reinsurance Madrid, 10 June 2014

Goldman Sachs 18 th Annual European Financials Conference Edouard Schmid, Head Property & Specialty Reinsurance Madrid, 10 June 2014 Agenda Introduction to Swiss Re Differentiation through knowledge Protection

Goldman Sachs 18 th Annual European Financials Conference Edouard Schmid, Head Property & Specialty Reinsurance Madrid, 10 June 2014 Agenda Introduction to Swiss Re Differentiation through knowledge Protection

When insight matters. TM. Insight changes everything

When insight matters. TM Insight changes everything Insight creates opportunities The advantage of knowing Scotiabank At Scotiabank, our Global Banking and Markets division provides corporate and investment

When insight matters. TM Insight changes everything Insight creates opportunities The advantage of knowing Scotiabank At Scotiabank, our Global Banking and Markets division provides corporate and investment

Insurance that pays out without proof of loss? Dr. Alexander Pui Nat Cat Manager (APAC) Swiss Re Corporate Solutions

Swiss Re Corporate Solutions") Insurance that pays out without proof of loss? Dr. Alexander Pui Nat Cat Manager (APAC) Swiss Re Corporate Solutions Natural Catastrophe Losses in Asia (1970 present) 2011:Thai Floods, Tohoku EQ, Christchurch

Insurance that pays out without proof of loss? Dr. Alexander Pui Nat Cat Manager (APAC) Swiss Re Corporate Solutions Natural Catastrophe Losses in Asia (1970 present) 2011:Thai Floods, Tohoku EQ, Christchurch

Seeking Diversification Through Emerging Markets July 2009

Seeking Diversification Through Emerging Introduction The ongoing shakeout in global markets has had far-reaching consequences for equities across the world. For developed market investors seeking diversification

Seeking Diversification Through Emerging Introduction The ongoing shakeout in global markets has had far-reaching consequences for equities across the world. For developed market investors seeking diversification

Innovative Solutions for Disaster Relief

Innovative Solutions for Disaster Relief How development organizations and foundations can use Capital Markets to prepare and leverage funds for future natural disasters Agenda Natural catastrophes in

Innovative Solutions for Disaster Relief How development organizations and foundations can use Capital Markets to prepare and leverage funds for future natural disasters Agenda Natural catastrophes in

NatCatSERVICE. Methodology. March 2018

NatCatSERVICE Methodology Natural catastrophe know-how for risk management and research Many decades of acquired experience in researching, documenting, analysing and evaluating natural catastrophes have

NatCatSERVICE Methodology Natural catastrophe know-how for risk management and research Many decades of acquired experience in researching, documenting, analysing and evaluating natural catastrophes have

HEALTH. CHARLES E. PHELPS University of Rochester PEARSON

FIFTH EDITION HEALTH ECONOMICS CHARLES E. PHELPS University of Rochester PEARSON Boston Columbus Indianapolis New York San Francisco Upper Saddle River Amsterdam Cape Town Dubai London Madrid Milan Munich

FIFTH EDITION HEALTH ECONOMICS CHARLES E. PHELPS University of Rochester PEARSON Boston Columbus Indianapolis New York San Francisco Upper Saddle River Amsterdam Cape Town Dubai London Madrid Milan Munich

Global insured losses from disaster events were USD 54 billion in 2016, up 43% from 2015, latest Swiss Re Institute sigma says

News release Global insured losses from disaster events were USD 54 billion in 2016, up 43% from 2015, latest Swiss Re Institute sigma says Global total economic losses from disaster events were USD 175

News release Global insured losses from disaster events were USD 54 billion in 2016, up 43% from 2015, latest Swiss Re Institute sigma says Global total economic losses from disaster events were USD 175

An overview of the recommendations regarding Catastrophe Risk and Solvency II

An overview of the recommendations regarding Catastrophe Risk and Solvency II Designing and implementing a regulatory framework in the complex field of CAT Risk that lies outside the traditional actuarial

An overview of the recommendations regarding Catastrophe Risk and Solvency II Designing and implementing a regulatory framework in the complex field of CAT Risk that lies outside the traditional actuarial

Global. Real Estate Outlook. Jeremy Kelly Global Research. David Green-Morgan Global Capital Markets Research

Global Real Estate Outlook Jeremy Kelly Global Research David Green-Morgan Global Capital Markets Research Ben Breslau Director of Research, Americas 7 th February 2013 Global Real Estate Outlook Road

Global Real Estate Outlook Jeremy Kelly Global Research David Green-Morgan Global Capital Markets Research Ben Breslau Director of Research, Americas 7 th February 2013 Global Real Estate Outlook Road

UBS Conference. May 14, 2007

UBS Conference May 14, 2007 Notice The information provided herein may include certain non-gaap financial measures. The reconciliation of such measures to the comparable GAAP figures are included in the

UBS Conference May 14, 2007 Notice The information provided herein may include certain non-gaap financial measures. The reconciliation of such measures to the comparable GAAP figures are included in the

Insurance: Limiting the Impact of Natural Catastrophes on the Balance Sheet. Dr. Oliver Kübler Dr. Matthias Schaub

Insurance: Limiting the Impact of Natural Catastrophes on the Balance Sheet Dr. Oliver Kübler Dr. Matthias Schaub This has only been possible by insurers. They are the ones who really built this city.

Insurance: Limiting the Impact of Natural Catastrophes on the Balance Sheet Dr. Oliver Kübler Dr. Matthias Schaub This has only been possible by insurers. They are the ones who really built this city.

Small Cap Allocation for Japanese Investors December 2007

Small Cap Allocation for Japanese Investors Introduction For many years, the equity allocation of Japanese institutional investors has typically been split between domestic and international assets and

Small Cap Allocation for Japanese Investors Introduction For many years, the equity allocation of Japanese institutional investors has typically been split between domestic and international assets and

AIRCurrents by David A. Lalonde, FCAS, FCIA, MAAA and Pascal Karsenti

SO YOU WANT TO ISSUE A CAT BOND Editor s note: In this article, AIR senior vice president David Lalonde and risk consultant Pascal Karsenti offer a primer on the catastrophe bond issuance process, including

SO YOU WANT TO ISSUE A CAT BOND Editor s note: In this article, AIR senior vice president David Lalonde and risk consultant Pascal Karsenti offer a primer on the catastrophe bond issuance process, including

CATASTROPHIC RISK AND INSURANCE Hurricane and Hydro meteorological Risks

CATASTROPHIC RISK AND INSURANCE Hurricane and Hydro meteorological Risks INTRODUCTORY REMARKS OECD IAIS ASSAL VII Conference on Insurance Regulation and Supervision in Latin America Lisboa, 24-28 April

CATASTROPHIC RISK AND INSURANCE Hurricane and Hydro meteorological Risks INTRODUCTORY REMARKS OECD IAIS ASSAL VII Conference on Insurance Regulation and Supervision in Latin America Lisboa, 24-28 April

Global Real Estate Outlook

Global Real Estate Outlook Jeremy Kelly Global Research David Green-Morgan Global Capital Markets Research 7 August 2014 Global Real Estate Market Outlook Jeremy Kelly Director, Global Research Jeremy.Kelly@eu.jll.com

Global Real Estate Outlook Jeremy Kelly Global Research David Green-Morgan Global Capital Markets Research 7 August 2014 Global Real Estate Market Outlook Jeremy Kelly Director, Global Research Jeremy.Kelly@eu.jll.com

HOW DO YOU DEFINE YOUR BORDERS? THE MODERN INDEX STRATEGY. msci.com

HOW DO YOU DEFINE YOUR BORDERS? THE MODERN INDEX STRATEGY msci.com MSCI DELIVERS THE MODERN INDEX STRATEGY The MSCI EAFE Index is designed to represent the performance of large- and mid-cap securities

HOW DO YOU DEFINE YOUR BORDERS? THE MODERN INDEX STRATEGY msci.com MSCI DELIVERS THE MODERN INDEX STRATEGY The MSCI EAFE Index is designed to represent the performance of large- and mid-cap securities

NHO Sundwall - presentation Natural Catastrophes. Dorte Birkebæk, Swiss Re Corporate Solutions, Country Manager Nordics, 11 and 12 of November 2014

NHO Sundwall - presentation Natural Catastrophes Dorte Birkebæk, Swiss Re Corporate Solutions, Country Manager Nordics, 11 and 12 of November 2014 Table of Contents / Agenda 40 Years of Loss History Various

NHO Sundwall - presentation Natural Catastrophes Dorte Birkebæk, Swiss Re Corporate Solutions, Country Manager Nordics, 11 and 12 of November 2014 Table of Contents / Agenda 40 Years of Loss History Various

Consolidated Statement of Financial Condition May 30, 2003

Consolidated Statement of Financial Condition May 30, 2003 Goldman, Sachs & Co. Established 1869 New York Hong Kong London Tokyo Atlanta Baltimore Bangkok Beijing Bermuda Boston Buenos Aires Calgary Chicago

Consolidated Statement of Financial Condition May 30, 2003 Goldman, Sachs & Co. Established 1869 New York Hong Kong London Tokyo Atlanta Baltimore Bangkok Beijing Bermuda Boston Buenos Aires Calgary Chicago

How Can Insurance Contribute to Increase Resilience of Most Vulnerable People

How Can Insurance Contribute to Increase Resilience of Most Vulnerable People Prof. Dr. Peter Hoeppe, Head Geo Risks Research/Corporate Climate Centre, Munich Re, Munich Uniting for Climate Action, BMUB,

How Can Insurance Contribute to Increase Resilience of Most Vulnerable People Prof. Dr. Peter Hoeppe, Head Geo Risks Research/Corporate Climate Centre, Munich Re, Munich Uniting for Climate Action, BMUB,

Supplemental Information Earnings Call

Supplemental Information Earnings Call Fourth-Quarter 2015 Market volume & outlook JLL Research Investment volumes remain solid; outlook steady Market Volumes Actual Forecast Capital Markets (1) LC USD

Supplemental Information Earnings Call Fourth-Quarter 2015 Market volume & outlook JLL Research Investment volumes remain solid; outlook steady Market Volumes Actual Forecast Capital Markets (1) LC USD

Trade Risk Mitigation. Michelle Hui Managing Director Head of Trade and Supply Chain Finance - APAC BNY Mellon

Trade Risk Mitigation Michelle Hui Managing Director Head of Trade and Supply Chain Finance - APAC BNY Mellon BNY Mellon Global Footprint BNY Mellon s global presence comprises a large network of branches,

Trade Risk Mitigation Michelle Hui Managing Director Head of Trade and Supply Chain Finance - APAC BNY Mellon BNY Mellon Global Footprint BNY Mellon s global presence comprises a large network of branches,

Chapter 2: Natural Disasters and Sustainable Development

Chapter 2: Natural Disasters and Sustainable Development This Chapter deals with the importance of the link between disaster reduction frameworks and development initiatives, as well as frameworks based

Chapter 2: Natural Disasters and Sustainable Development This Chapter deals with the importance of the link between disaster reduction frameworks and development initiatives, as well as frameworks based

Loss and Damage Associated with Climate Change Impacts The (possible) role of Disaster Risk Financing and Insurance

role of Disaster Risk Financing and Insurance") UNFCC regional expert meeting on loss and damage August 27 29, 2012 Bangkok, Thailand Loss and Damage Associated with Climate Change Impacts The (possible) role of Disaster Risk Financing and Insurance

UNFCC regional expert meeting on loss and damage August 27 29, 2012 Bangkok, Thailand Loss and Damage Associated with Climate Change Impacts The (possible) role of Disaster Risk Financing and Insurance

1 Jan 2018 Property & Casualty Treaty Renewals. and guidance update 2017 and 2018

Property & Casualty Treaty Renewals and guidance update 2017 and 2018 Renewals Conference Call Hannover, 7 February 2018 Reinsurance markets Our results Our portfolio Structured reinsurance Outlook 2018

Property & Casualty Treaty Renewals and guidance update 2017 and 2018 Renewals Conference Call Hannover, 7 February 2018 Reinsurance markets Our results Our portfolio Structured reinsurance Outlook 2018

Compulsory versus Optional Disaster Insurance

Compulsory versus Optional Disaster Insurance IRSG Frankfurt 28.4.2015 Marie Gemma Dequae Ioannis Papanikolaou 28.4.2015 MGD&IP_2015 1 agenda The context Goal of European Union Timeline EU actions Current

Compulsory versus Optional Disaster Insurance IRSG Frankfurt 28.4.2015 Marie Gemma Dequae Ioannis Papanikolaou 28.4.2015 MGD&IP_2015 1 agenda The context Goal of European Union Timeline EU actions Current

Southeast Asia Disaster Risk Insurance Facility

Southeast Asia Disaster Risk Insurance Facility PROTECT THE GREATEST HOME OF ALL: OUR COUNTRIES SEADRIF is a regional platform to provide ASEAN countries with financial solutions and technical advice to

Southeast Asia Disaster Risk Insurance Facility PROTECT THE GREATEST HOME OF ALL: OUR COUNTRIES SEADRIF is a regional platform to provide ASEAN countries with financial solutions and technical advice to

Allianz Global Corporate & Specialty

Allianz Global Corporate & Specialty Company presentation January 2012 Allianz An Introduction Allianz Group is one of the world s leading insurers and financial services providers Founded in 1890 in Berlin,

Allianz Global Corporate & Specialty Company presentation January 2012 Allianz An Introduction Allianz Group is one of the world s leading insurers and financial services providers Founded in 1890 in Berlin,

Franklin Templeton Investments Our Global Perspective

Greg Johnson Chief Executive Officer Franklin Resources, Inc. Franklin Templeton Investments Our Global Perspective Dealer Use Only / Not for Distribution to the Public World-Class Investment Management

Greg Johnson Chief Executive Officer Franklin Resources, Inc. Franklin Templeton Investments Our Global Perspective Dealer Use Only / Not for Distribution to the Public World-Class Investment Management

QUARTERLY FINANCIAL STATEMENTS AS AT 30 JUNE 2011

QUARTERLY FINANCIAL STATEMENTS AS AT 30 JUNE 2011 Telephone conference with analysts and investors 4 August 2011 Agenda Overview 2 Financial reporting 2011 Munich Re (Group) 6 Primary insurance 12 Munich

QUARTERLY FINANCIAL STATEMENTS AS AT 30 JUNE 2011 Telephone conference with analysts and investors 4 August 2011 Agenda Overview 2 Financial reporting 2011 Munich Re (Group) 6 Primary insurance 12 Munich

Insuring against natural hazards

Insuring against natural hazards Insuring against hydro- geomorphological risks and disasters G. BRUGNOT, Cemagref 27/09/00 1 Which natural risks we will consider We will mainly concentrate on : Floods

Insuring against natural hazards Insuring against hydro- geomorphological risks and disasters G. BRUGNOT, Cemagref 27/09/00 1 Which natural risks we will consider We will mainly concentrate on : Floods

NATURAL PERILS - PREPARATION OR RECOVERY WHICH IS HARDER?

NATURAL PERILS - PREPARATION OR RECOVERY WHICH IS HARDER? Northern Territory Insurance Conference Jim Filer Senior Risk Engineer Date : 28 October 2016 Version No. 1.0 Contents Introduction Natural Perils

NATURAL PERILS - PREPARATION OR RECOVERY WHICH IS HARDER? Northern Territory Insurance Conference Jim Filer Senior Risk Engineer Date : 28 October 2016 Version No. 1.0 Contents Introduction Natural Perils

Frank J. Fabozzi, CFA

SEVENTH EDITION Frank J. Fabozzi, CFA Professor in the Practice of Finance Yale School of Management Boston San Francisco New York London Toronto Sydney Tokyo Singapore Madrid Mexico City Munich Paris

SEVENTH EDITION Frank J. Fabozzi, CFA Professor in the Practice of Finance Yale School of Management Boston San Francisco New York London Toronto Sydney Tokyo Singapore Madrid Mexico City Munich Paris

Global Real Estate Investments Opportunities and Risks in the Late Stage of the Cycle. Wolfgang Kubatzki, Managing Director, Scope Investor Services

Global Real Estate Investments Opportunities and Risks in the Late Stage of the Cycle Wolfgang Kubatzki, Managing Director, Scope Investor Services Global Real Estate Investments Current Situation Structural

Global Real Estate Investments Opportunities and Risks in the Late Stage of the Cycle Wolfgang Kubatzki, Managing Director, Scope Investor Services Global Real Estate Investments Current Situation Structural

What is executive remuneration in high definition?

Executive remuneration in high definition Article one a high definition approach to relative TSR Our latest series of papers turns a high definition lens to different aspects of executive reward. This

Executive remuneration in high definition Article one a high definition approach to relative TSR Our latest series of papers turns a high definition lens to different aspects of executive reward. This

Schroders Wealth Accumulation Programme (SWAP) For Accredited Investors Only

For Accredited Investors Only") Schroders Wealth Accumulation Programme (SWAP) For Accredited Investors Only What is SWAP? Schroders Wealth Accumulation Programme (SWAP) is an actively managed approach to portfolio management, with an

Schroders Wealth Accumulation Programme (SWAP) For Accredited Investors Only What is SWAP? Schroders Wealth Accumulation Programme (SWAP) is an actively managed approach to portfolio management, with an

chätti, Swiss Re Analysis of an Insurance Company s Balance Sheet

, Swiss Re Analysis of an Insurance Company s Balance Sheet Agenda 1. Introduction 2. Insurance and reinsurance overview 3. Assets and liabilities 4. Risk assessment 5. Economic risk capital 6. Summary

, Swiss Re Analysis of an Insurance Company s Balance Sheet Agenda 1. Introduction 2. Insurance and reinsurance overview 3. Assets and liabilities 4. Risk assessment 5. Economic risk capital 6. Summary