As Helmuth Karl Bernhard Graf von Moltke (German Field Marshal from the 18 th century) noted, no plan survives contact with the enemy.

|

|

|

- Pierce Briggs

- 5 years ago

- Views:

Transcription

1 As Helmuth Karl Bernhard Graf von Moltke (German Field Marshal from the 18 th century) noted, no plan survives contact with the enemy. In P&C actuarial speak, the equivalent is no reserving method survives contact with the future. Presenter: Timothy J Pratt, FIAA, FCAS, MAAA Contributors: Timothy J Pratt, Andy Moriarty CLRS, San Diego, Sept 16 th

2 Introduction Approach Outline Reserving has no* impact on Profit Stochastic Claim Model Reserving Methods Measures Results Questions? Note: The views expressed during this presentation are our views and do not represent the views of our current (or prior) employers 2

3 3

4 We* got to thinking about this this subject by comparing and contrasting claim volatility; reserve volatility and; the non-dynamic nature of the existing reserving methods Due to the volatile nature of P&C claims We know that the current unpaid claims estimate is going to be wrong We know that the final value will likely fall within a range of $X to $Y Is there a reserving approach that will help us smooth out the claims volatility? * Contributors: Timothy J Pratt, Andy Moriarty 4

5 Has something similar every happened to you? You have a moderate size excess liability book Quarter after quarter, nothing happened on the claim front (typical for excess) You use the Bornhuetter-Ferguson method Each Quarter, the BF IBNR reduces by $2m This happens for (say) 8 quarters in a row Then a $15m claim is reported Management remembers the $15m hit but didn t remember the $16m release 5

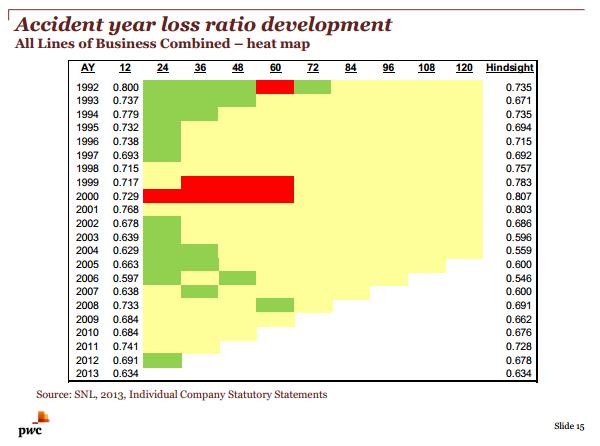

6 At a recent CAGNY meeting, Lela Patrick & Timothy Landick presented a paper / discussion on reserve variability * One slide showed a heat map of reserve increases (red) or decreases (green) outside a certain threshold * 6

7 7

8 There was some discussion regarding the runs of red and green that were observed in the heat map One of the observations was this is an artifact of using the Bornhuetter-Ferguson method Does the BF method contain a bias? 8

9 Another goal that came up during our model development phase was that we wanted to assist actuaries with the following situation You ve just completed your analysis in record time (15 days post quarter close) Claims manager comes to you and says We ve just received notification of a claim with an accident date of 6 months ago is it covered by the IBNR? Your first question is How big is it? 9

10 How big is it? $2 $20 $200 $2,000 $2m $2b $2t Is it covered? Yes Yes Yes Should be Could be No No 10

11 Summary Is there a reserving approach that will help us smooth out the claims volatility? Does the BF method contained a bias? Can we provide some assistance in answering Is this claim covered by IBNR? Finally Can we help with management s memory issues? Management remembers the $15m hit but didn t remember the $16m release 11

12 12

13 Construct a per-claim simulation model Simulate a bunch of claims Observe the mean claim reporting pattern Use this as input into the various actuarial unpaid claims estimation methods Simulate a bunch of claims (again) Calculate the unpaid claims estimate using various reserving methods Review the impact of these methods on profitability and accuracy 13

14 14

15 When considering a cohort of policies Reserving has a profit impact (short term) Reserves go up, profit in the year goes down However, once all claims from this cohort have been settled and paid, reserving has no profit impact 15

16 But Reserving has a huge impact on the view of profitability And can lead to management mistakes i.e. Writing lots of unprofitable business because you thought it was profitable Or Exiting a profitable line because you thought it was unprofitable 16

17 17

18 Below is the life cycle of a particular simulated claim Simulate Report and Settlement Quarter Simulate possibility and size of claim change movement between report and settlement quarters 18

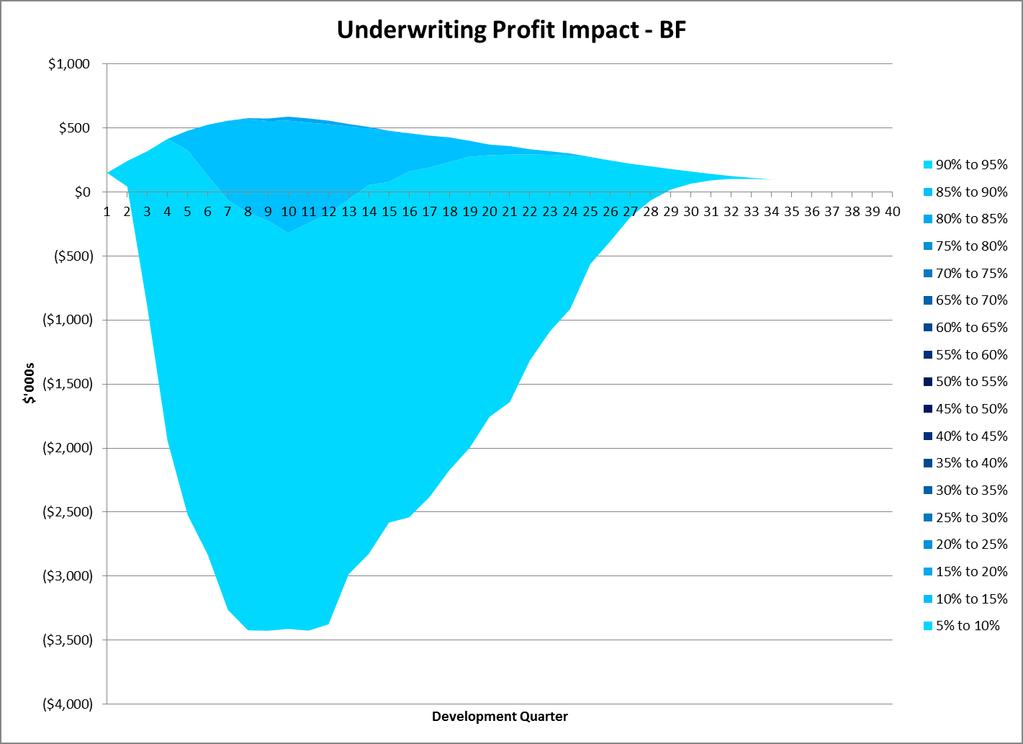

19 Illustration of a BF Ultimate Estimate using an initial expected of $2m for the previous claim 19

20 Benefit of stochastic model - it can peer through the fog of war 21

21 Which chart of cumulative loss lines is observed and which is modeled? 22

22 Model Process Steps 1. Review experience and select required assumptions 2. Run model (1m simulations) Extract mean dollar reporting pattern 3. Use reporting pattern to calculate Age to Ultimate LDFs 4. Hard code LDFs into reserving methods 5. Rerun model Extract results to test profit impact and reserve accuracy 23

23 Step 1 Determine the expected reporting pattern Claim Assumptions Claim Reporting Pattern Settlement Pattern Probability of claim movement Size of claim movement Simulation Engine Simulation Engine Individual Claim Details & History Expected Claim Reporting Pattern 24

24 Step 2 Calculate the unpaid claims estimates Claim Reporting Pattern Claim Assumptions Settlement Pattern Probability of claim movement Simulation Engine Size of claim movement Expected Claim Reporting Pattern Simulation Engine Individual Claim Details, History & Unpaid Claims Estimates 40 Qtrs of Profit & unpaid claims estimates 25

25 26

26 The Usual Suspects Fixed Estimate / Initial Expected Bornhuetter- Ferguson Loss Development / Chain Ladder Additional Methods Bounded Bornhuetter- Ferguson Mixed / blended 27

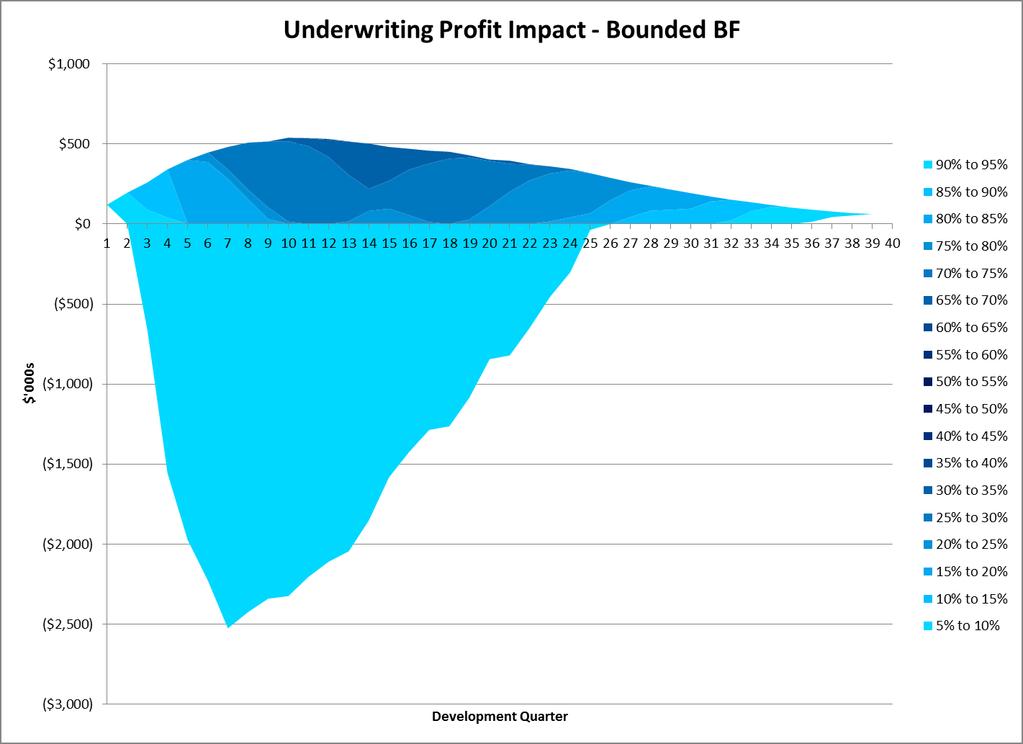

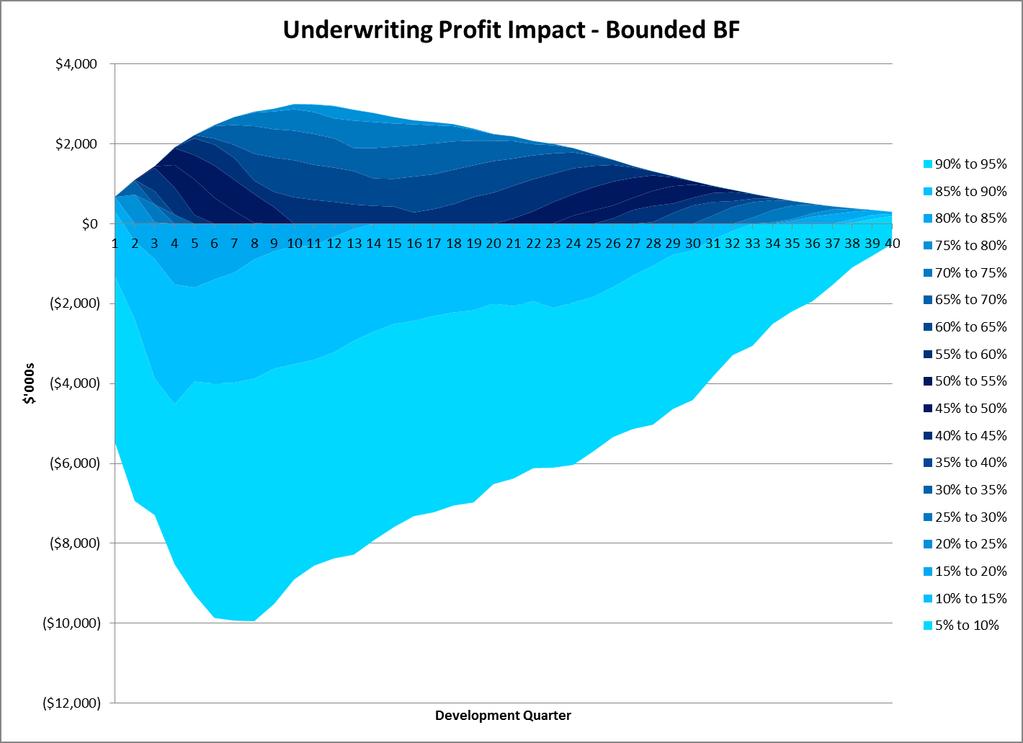

27 Bounded Bornhuetter-Ferguson (BBF) Reserve approach is Current Ultimate Estimate is equal to the prior review s Ultimate Estimate Unless the calculated ultimate estimate breaches an upper or lower limit Effectively means that the ultimate is sticky and doesn t move until the weight of information moves it 28

28 Approach used here is two (2) related Bornhuetter-Ferguson estimates One BF gives the upper bound One BF gives the lower bound Q: How do you determine the upper and lower bounds? Modify the IELR? Modify the expected reporting pattern? We only used the latter 29

29 How do you select the upper and lower bounds? Option 1 Use stochastic or bootstrapping results 30

30 How do you select the upper and lower bounds? Option 2 Adjust the expected reporting pattern up and down 31

31 How do you select the upper and lower bounds? Option 3 Adjust the expected reporting pattern left and right 32

32 How do you select the upper and lower bounds? Option 4 Modify the reported Age to Ult factors to get two new patterns 33

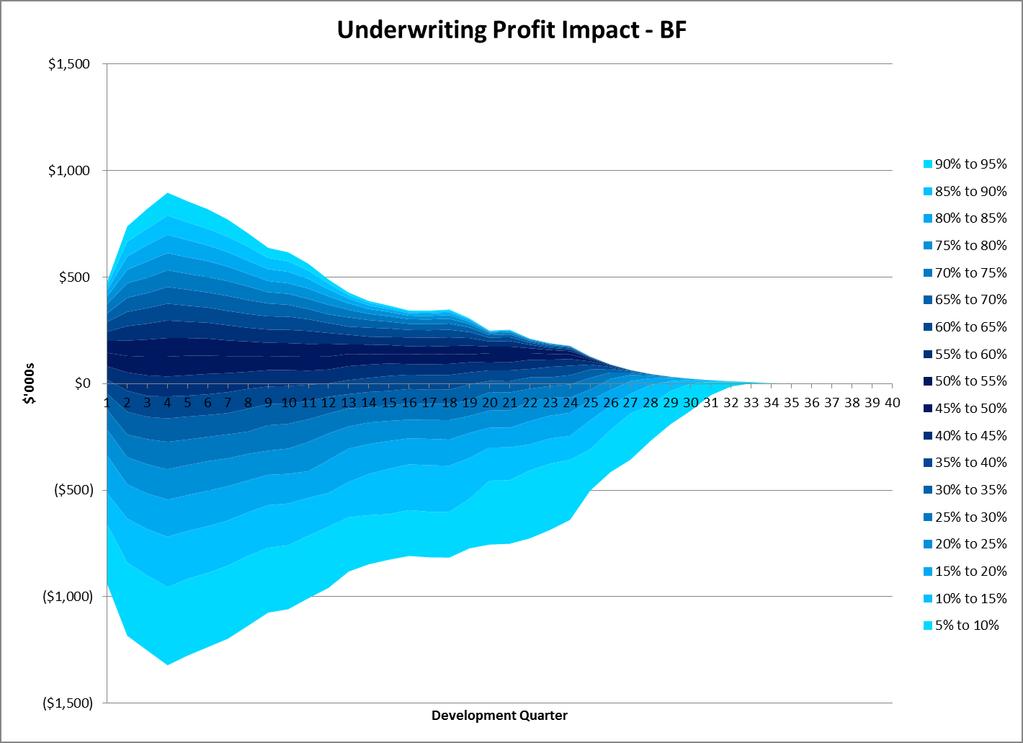

33 Illustration of a BBF Ultimate Estimate using an initial expected of $2m Claim Size Millions Development Quarter Claim Value Final Value BF Ult Estimate BBF 34

34 Examples of using the BBF method 35

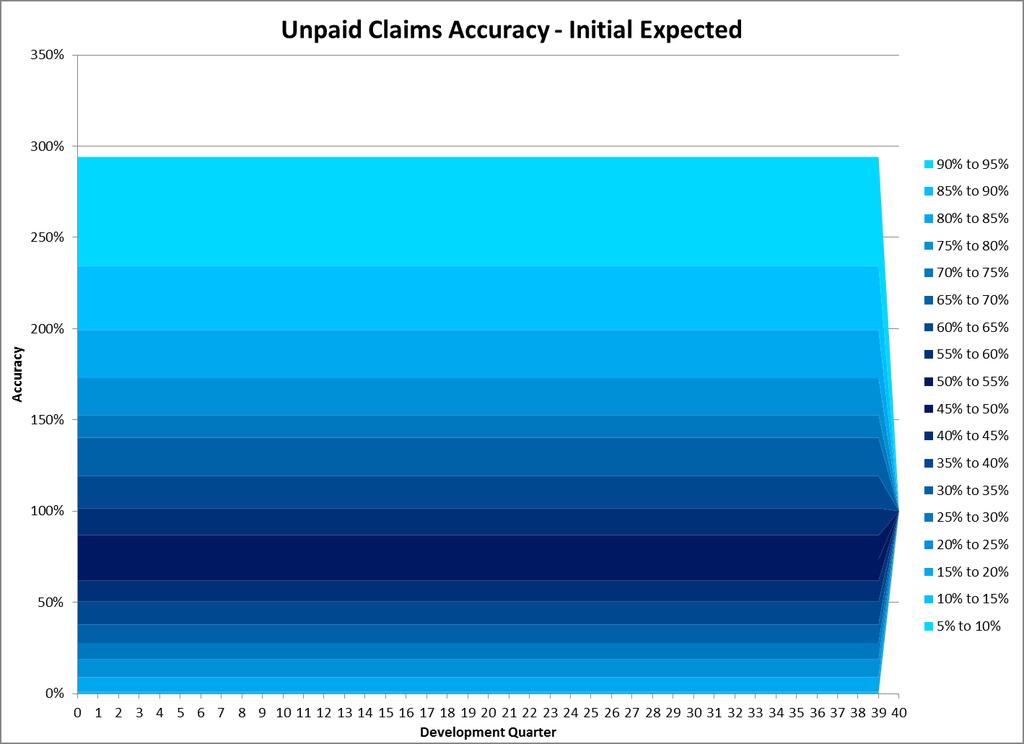

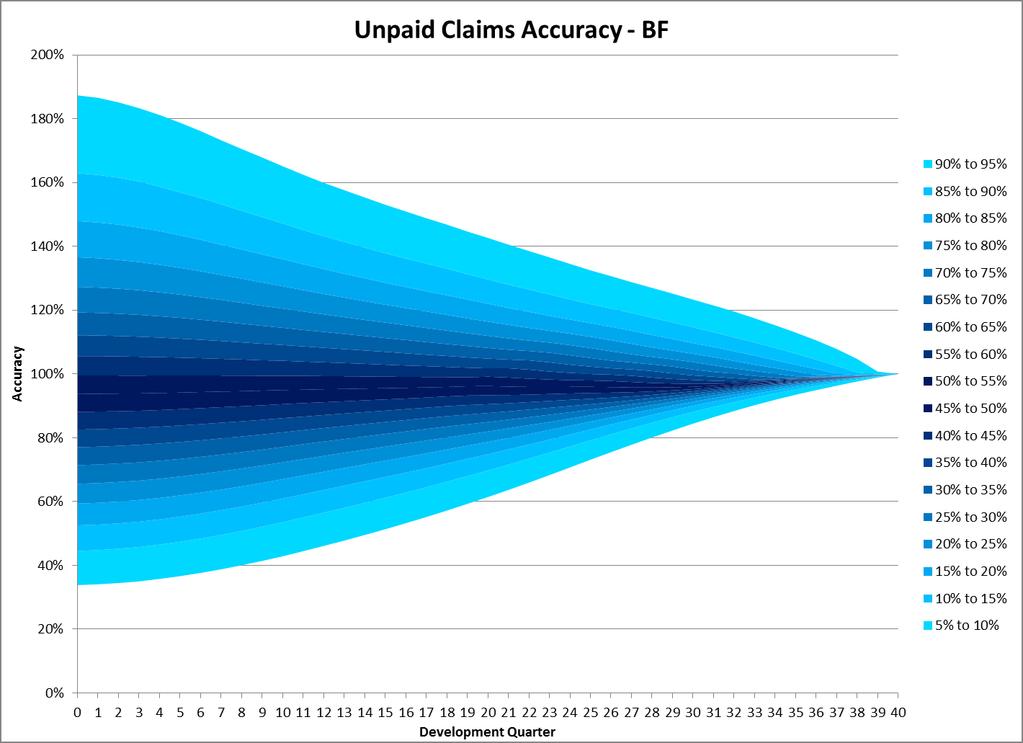

35 Examples of using the BBF method Ultimate increased by $3.4m for BBF against $5.4 for BF 36

36 Examples of using the BBF method 37

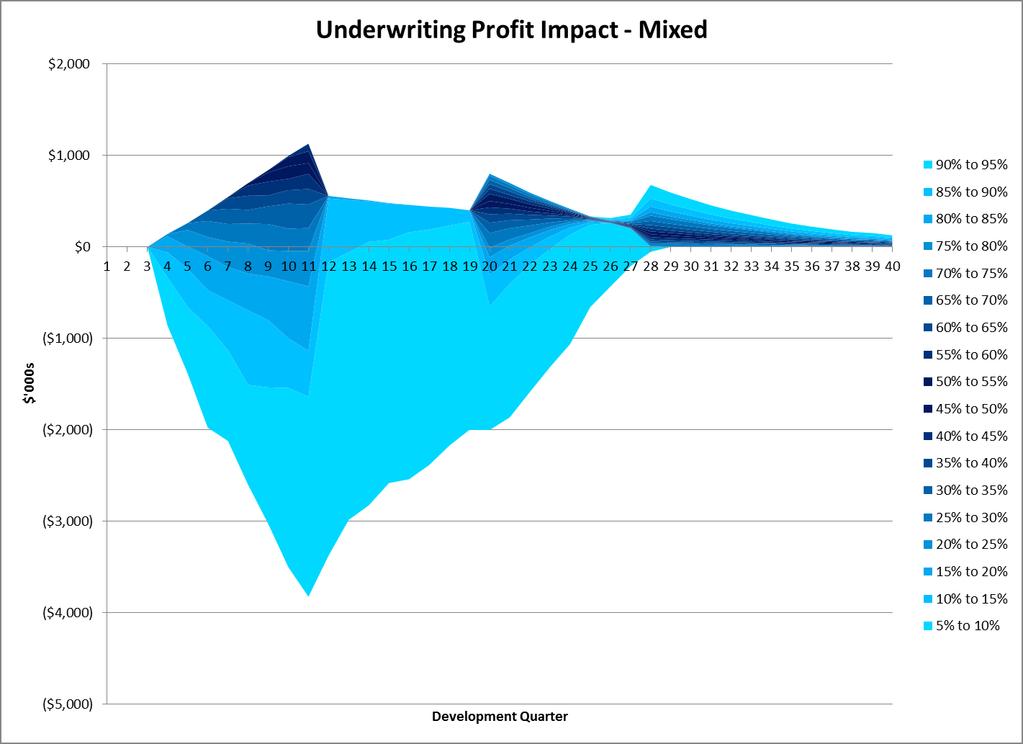

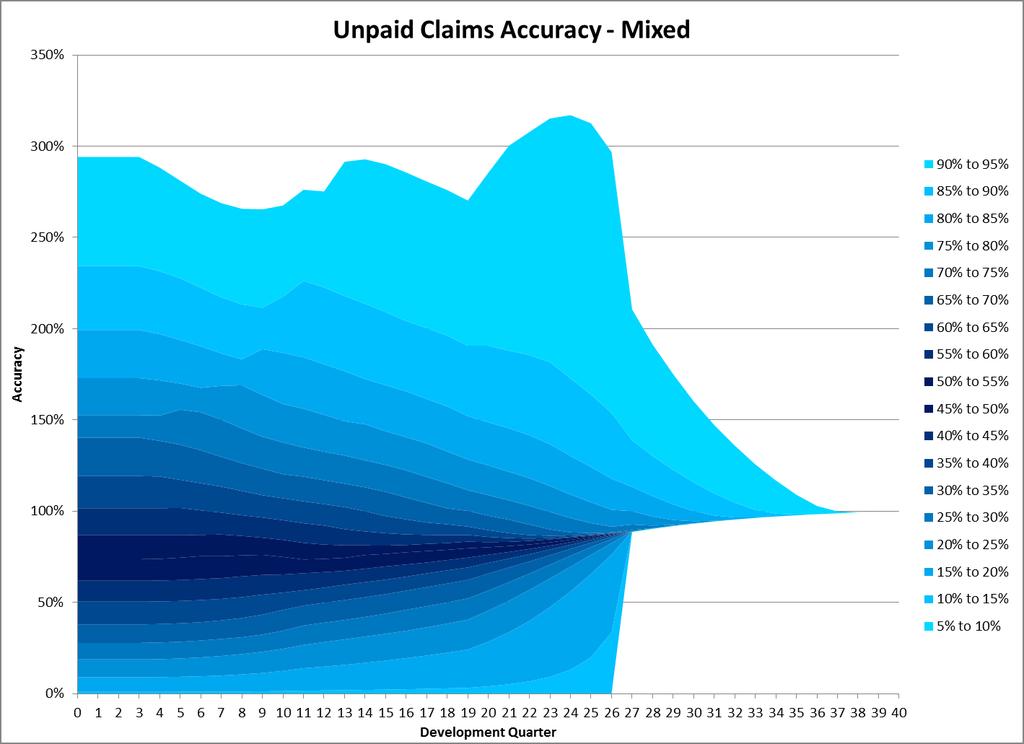

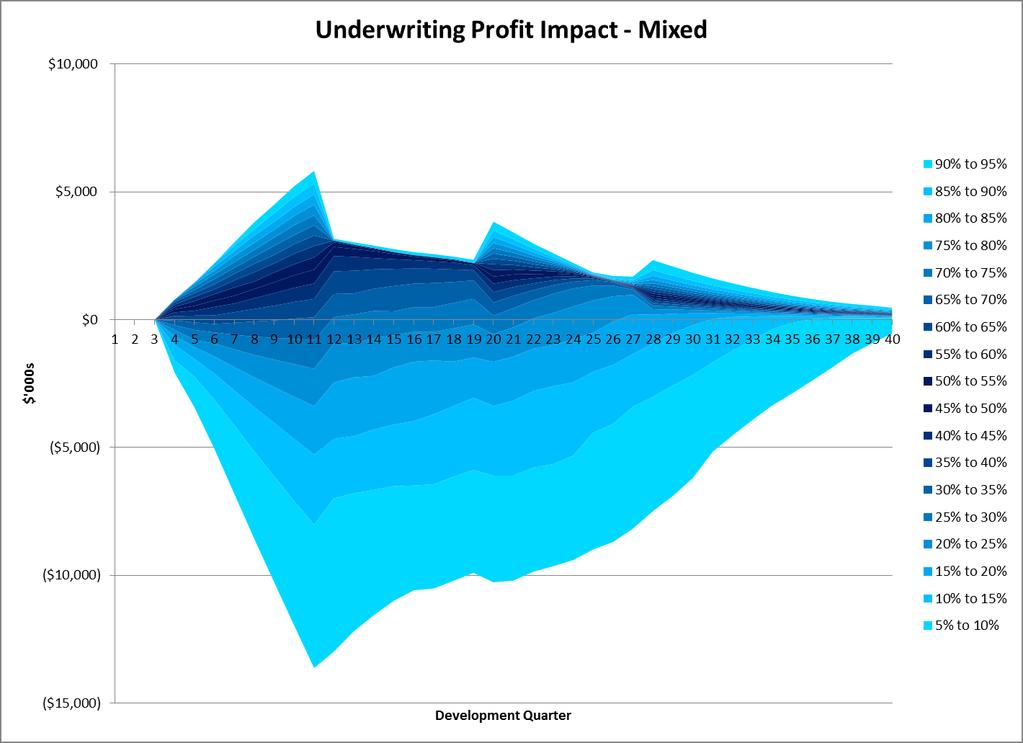

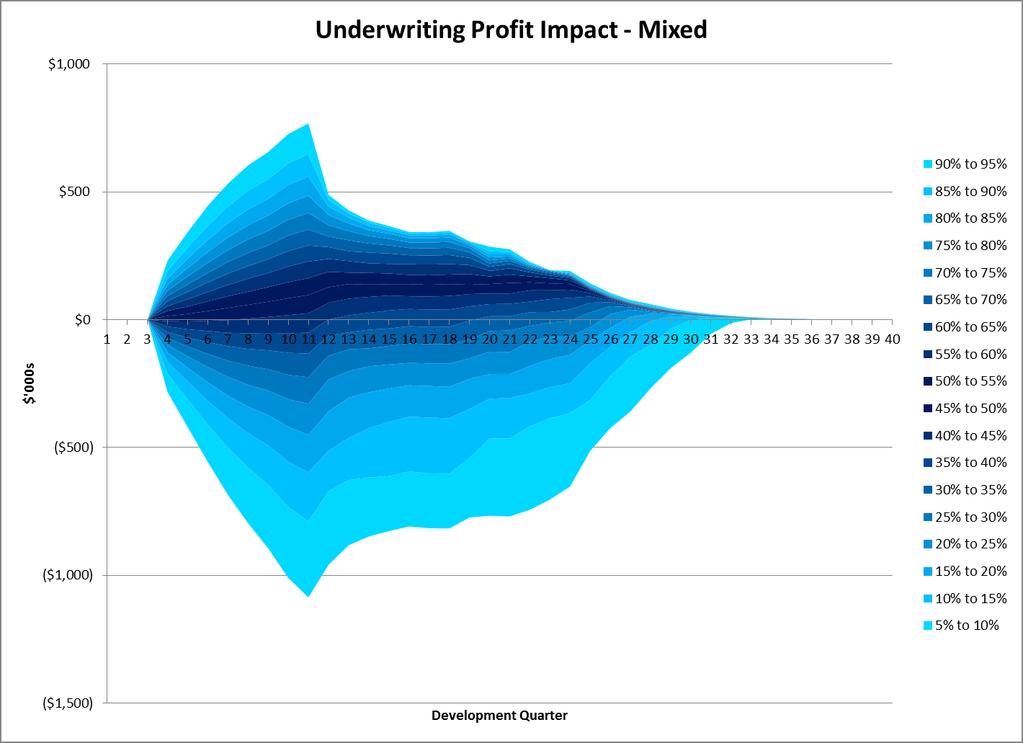

37 Mixed / Blended Approach The mixed / blended approach calculates the ultimate estimate by combining the ultimate estimate from the following: Initial Expected (IE) Bornhuetter-Ferguson (BF) Loss Development Method (LDM) The blending rules we used are: Qtrs 0-3: 100% IE Qtrs 11-19: 100% BF Qtrs 27+: 100% LDM Linear interpolation for other Qtrs The blending rules we used are: Qtrs 0-3: 100% IE Qtr 4: 87½% IE + 12½% BF Qtr 5: 75% IE + 25% BF Qtr 9: 25% IE + 75% BF Qtr 10: 12½% IE + 87½% BF Qtrs 11-19: 100% BF Qtr 20: 87½% BF + 12½% LDM Qtr 21: 75% BF + 25% LDM Qtr 25: 25% BF + 75% LDM Qtr 26: 12½% BF + 87½% LDM Qtrs 27+: 100% LDM 38

38 39

39 There are two measures that we are using to gauge each reserving approach These measures are: Impact on Profitability Accuracy 40

40 The Impact on Profitability measure looks at the quarter on quarter change in the ultimate estimate For Example: The quarter on quarter change in the profitability for the Initial Expected method is zero for all quarters except the last quarter The final ultimate estimate for the Initial Expected method is what was actually paid 41

41 Profitability impact using the prior illustrated claim Total under the purple lines sums to $250k 42

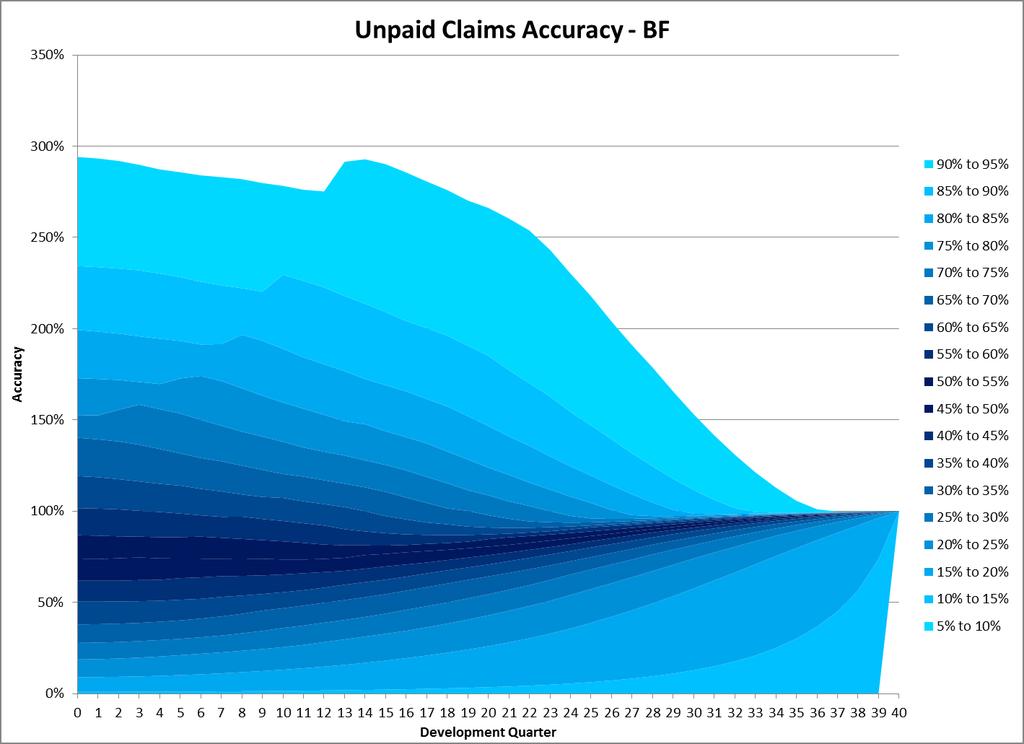

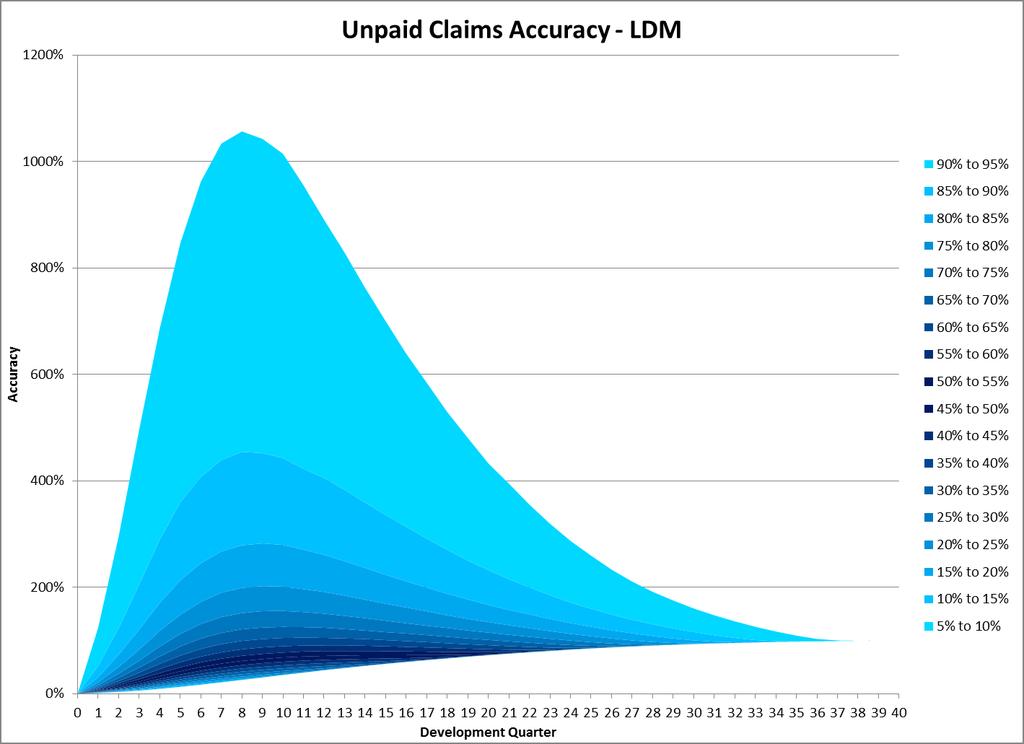

42 The Accuracy measure examines how accurate the estimate is at each quarter compared to the final result A stochastic model knows the final result The actual measure we are using is Final Value / Estimate So A value of 50% means that the current estimate is twice the final value (i.e. too high) A value of 100% means that the current estimate is equal to the final value (i.e. just right) A value of 200% means that the current estimate is half the final value (i.e. too low) 43

43 Accuracy illustration using the prior illustrated claim At Qtr 11, est = $1.71m, final value is $1.75m, accuracy is 102.5% 44

44 45

45 Product 1 Excess Liability Product High Severity Low Frequency Low volume, hence very low claim count All policies have $20m limit Product 2 Excess Liability Product Same as Product 1 but more volume Product 3 General Liability Higher Frequency Different reporting / settlement assumptions All policies have $1m limit 46

46 Product 1 Excess Liability Product High Severity Low Frequency Very low claim count 47

47 48

48 49

49 50

50 51

51 52

52 Product 1 Excess Liability Product High Severity Low Frequency Very low claim count 53

53 54

54 55

55 56

56 57

57 58

58 Product 2 Excess Liability Product High Severity Low Frequency More Volume, more claims 59

59 The 2 nd product we looked at is identical to the first except it has higher volume Product 1 61

60 The 2 nd product we looked at is identical to the first except it has higher volume Product 2 62

61 63

62 64

63 65

64 66

65 67

66 Product 2 Excess Liability Product High Severity Low Frequency More Volume, more claims 68

67 69

68 70

69 71

70 72

71 73

72 Product 3 General Liability Slightly higher Frequency Lower Severity 74

73 75

74 76

75 77

76 78

77 79

78 Product 3 General Liability Slightly higher Frequency Lower Severity 80

79 81

80 82

81 83

82 84

83 85

84 86

85 Stochastic Model Bounded BF Can the stochastic claims model as outlined be improved? If so, how? Are there other uses for such a model? RESULTS Could this be a functional actuarial reserving method? How should the upper and lower bounds be determined? Should we include changing the IELR as an option? What observations can be drawn from the results? 87

86 As Helmuth Karl Bernhard Graf von Moltke (German Field Marshal from the 18 th century) noted, no plan survives contact with the enemy. In P&C actuarial speak, the equivalent is no reserving method survives contact with the future. Presenter: Timothy J Pratt, FIAA, FCAS, MAAA Contributors: Timothy J Pratt, Andy Moriarty CLRS, San Diego, Sept 16 th

87 89

88 90

89 When considering a cohort of policies Reserving has a profit impact (short term) Reserves go up, profit in the year goes down However, once all claims from this cohort have been settled and paid, reserving has no profit impact 91

90 Consider an insurance product cohort that will eventually result in 75% loss ratio 20% expense & commission ratio 5% profit margin Note: Losses are reported evenly over 3 years They are paid as they are reported What does the profit look like using a Bornhuetter-Ferguson approach with a 0% IELR? 50% IELR? 75% IELR? 100% IELR? 92

91 Reserving with a 0% IELR End of Exp Reported Δ IBNR Year Premium Comm Losses IELR of 0% Profit (25) (25) Total

92 Reserving with a 50% IELR End of Exp Reported Δ IBNR Year Premium Comm Losses IELR of 50% Profit (17) (8) 3 25 (17) (8) Total

93 Reserving with a 75% IELR End of Exp Reported Δ IBNR Year Premium Comm Losses IELR of 75% Profit (25) (25) - Total

94 Reserving with a 100% IELR End of Exp Reported Δ IBNR Year Premium Comm Losses IELR of 100% Profit (12) 2 25 (33) (33) 8 Total

95 So Over the life of the cohort, 5% profit Low IELR leads to large profits followed by losses High IELR leads to losses followed by profits Hence Reserving has no impact on (eventual) profits 97

96 But Reserving has a huge impact on the view of profitability And can lead to management mistakes i.e. Writing lots of unprofitable business because you thought it was profitable Or Exiting a profitable line because you thought it was unprofitable 98

97 99

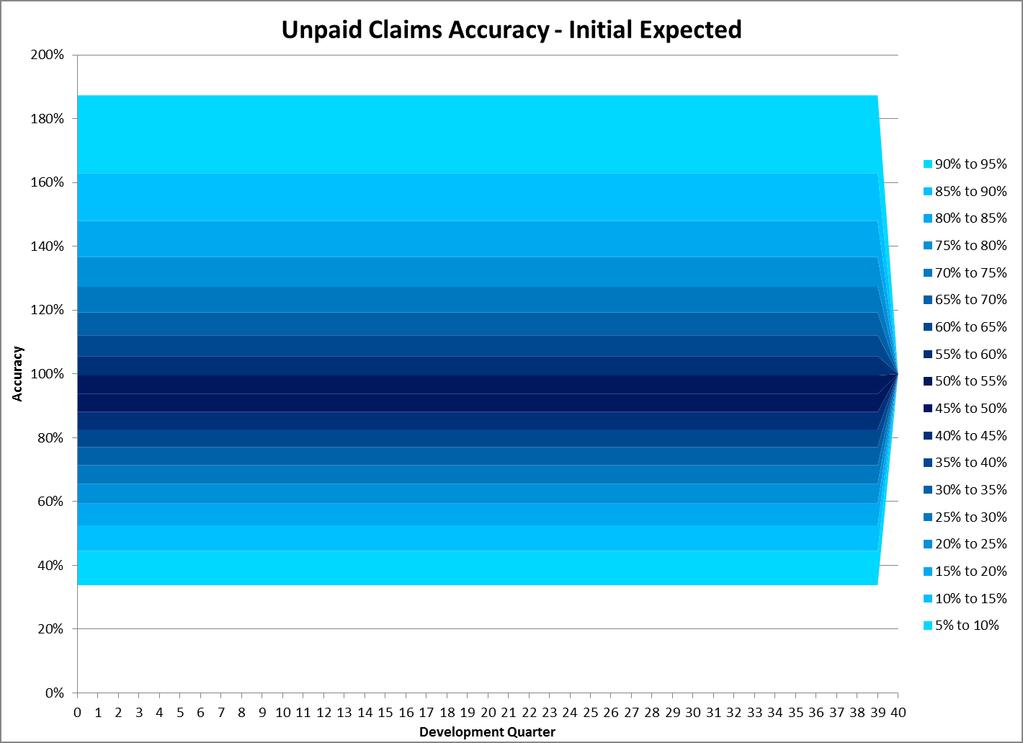

98 Claim Model built in MS Excel Advantage of Claim Model v. Actual Results Ultimate values are known Unlimited scenarios are available to test methods Historical results can be used to build the assumptions in the Claim Model 100

99 # of Reported Claims Simulated # of Reported Claims that result in any payment Individual Claim Report Period Settlement Period Interim Movement modeled based on frequency of: Upward Movement No Movement Downward Movement Attachment point and Limit Applied Claims aggregated to get Modeled Experience 101

100 Model Assumptions: All claims are closed by year 10 Upward and Downward movements are a function of the policy limit # of Reported Claims can be modelled using InverseGaussian distribution # of Reported Claims that result in payment can be modeled using Binominal distribution All other variables were modeled using a discrete distribution using observed/hypothetical scenarios 102

101 Below is the life cycle of a particular simulated claim Simulate Report and Settlement Quarter Simulate possibility and size of claim change movement between report and settlement quarters 103

102 Illustration of a BF Ultimate Estimate using an initial expected of $2m for the previous claim 104

103 Which chart of cumulative loss lines is observed and which is modeled? 105

104 106

105 Fixed Estimate The ultimate is a fixed amount The IBNR is a balancing item (Ultimate less reported) 107

106 Bornhuetter-Ferguson Independent future expectation Past from actual results Credibility weighted of historic reported and future reported for ultimate estimate 108

107 Loss Development / Chain Ladder Ultimate estimate is reported times up-lift factor 109

108 Mixed Approach The mixed approach blends the following together: Initial Expected (IE) Bornhuetter-Ferguson (BF) Loss Development Method (LDM) The blending rules we used are: Quarters 0-3: 100% IE Quarters 11-19: 100% BF Quarters 27+: 100% LDM Others interpolated between adjacent methods eg: Qtr 4: 87½% IE + 12½% BF 110

109 111

Structured Tools to Help Organize One s Thinking When Performing or Reviewing a Reserve Analysis

Structured Tools to Help Organize One s Thinking When Performing or Reviewing a Reserve Analysis Jennifer Cheslawski Balester Deloitte Consulting LLP September 17, 2013 Gerry Kirschner AIG Agenda Learning

Structured Tools to Help Organize One s Thinking When Performing or Reviewing a Reserve Analysis Jennifer Cheslawski Balester Deloitte Consulting LLP September 17, 2013 Gerry Kirschner AIG Agenda Learning

Introduction to Casualty Actuarial Science

Introduction to Casualty Actuarial Science Executive Director Email: ken@theinfiniteactuary.com 1 Casualty Actuarial Science Two major areas are measuring 1. Written Premium Risk Pricing 2. Earned Premium

Introduction to Casualty Actuarial Science Executive Director Email: ken@theinfiniteactuary.com 1 Casualty Actuarial Science Two major areas are measuring 1. Written Premium Risk Pricing 2. Earned Premium

Casualty Loss Reserve Seminar Roll-forward Reserve Estimates September 15, 2014

www.pwc.com 2014 Casualty Loss Reserve Seminar Roll-forward Reserve Estimates Mechanics Underlying Roll-forward Reserve Estimates 2 Agenda Section 1 Roll-forward Example Section 2 Potential roll-forward

www.pwc.com 2014 Casualty Loss Reserve Seminar Roll-forward Reserve Estimates Mechanics Underlying Roll-forward Reserve Estimates 2 Agenda Section 1 Roll-forward Example Section 2 Potential roll-forward

IASB Educational Session Non-Life Claims Liability

IASB Educational Session Non-Life Claims Liability Presented by the January 19, 2005 Sam Gutterman and Martin White Agenda Background The claims process Components of claims liability and basic approach

IASB Educational Session Non-Life Claims Liability Presented by the January 19, 2005 Sam Gutterman and Martin White Agenda Background The claims process Components of claims liability and basic approach

Introduction to Casualty Actuarial Science

Introduction to Casualty Actuarial Science Director of Property & Casualty Email: ken@theinfiniteactuary.com 1 Casualty Actuarial Science Two major areas are measuring 1. Written Premium Risk Pricing 2.

Introduction to Casualty Actuarial Science Director of Property & Casualty Email: ken@theinfiniteactuary.com 1 Casualty Actuarial Science Two major areas are measuring 1. Written Premium Risk Pricing 2.

What to Do When the Actuary s Answer is Too High. Timothy C. Mosler, FCAS, MAAA

What to Do When the Actuary s Answer is Too High Timothy C. Mosler, FCAS, MAAA February 25, 2016 Agenda Tim Mosler s Background Disclaimer Basics of Reserve/Funding Analysis 3 Reactions When the Client

What to Do When the Actuary s Answer is Too High Timothy C. Mosler, FCAS, MAAA February 25, 2016 Agenda Tim Mosler s Background Disclaimer Basics of Reserve/Funding Analysis 3 Reactions When the Client

Obtaining Predictive Distributions for Reserves Which Incorporate Expert Opinions R. Verrall A. Estimation of Policy Liabilities

Obtaining Predictive Distributions for Reserves Which Incorporate Expert Opinions R. Verrall A. Estimation of Policy Liabilities LEARNING OBJECTIVES 5. Describe the various sources of risk and uncertainty

Obtaining Predictive Distributions for Reserves Which Incorporate Expert Opinions R. Verrall A. Estimation of Policy Liabilities LEARNING OBJECTIVES 5. Describe the various sources of risk and uncertainty

With the Benefit of Hindsight An Analysis of Loss Reserving Methods. So Many Methods, So Little Time. Overview

With the Benefit of Hindsight An Analysis of Loss Reserving Methods Prepared for: Prepared by: International Congress of Actuaries Washington, D.C. Susan J. Forray, FCAS, MAAA Principal and Consulting

With the Benefit of Hindsight An Analysis of Loss Reserving Methods Prepared for: Prepared by: International Congress of Actuaries Washington, D.C. Susan J. Forray, FCAS, MAAA Principal and Consulting

Basic Reserving: Estimating the Liability for Unpaid Claims

Basic Reserving: Estimating the Liability for Unpaid Claims September 15, 2014 Derek Freihaut, FCAS, MAAA John Wade, ACAS, MAAA Pinnacle Actuarial Resources, Inc. Loss Reserve What is a loss reserve? Amount

Basic Reserving: Estimating the Liability for Unpaid Claims September 15, 2014 Derek Freihaut, FCAS, MAAA John Wade, ACAS, MAAA Pinnacle Actuarial Resources, Inc. Loss Reserve What is a loss reserve? Amount

Exam-Style Questions Relevant to the New Casualty Actuarial Society Exam 5B G. Stolyarov II, ARe, AIS Spring 2011

Exam-Style Questions Relevant to the New CAS Exam 5B - G. Stolyarov II 1 Exam-Style Questions Relevant to the New Casualty Actuarial Society Exam 5B G. Stolyarov II, ARe, AIS Spring 2011 Published under

Exam-Style Questions Relevant to the New CAS Exam 5B - G. Stolyarov II 1 Exam-Style Questions Relevant to the New Casualty Actuarial Society Exam 5B G. Stolyarov II, ARe, AIS Spring 2011 Published under

University of California, Los Angeles Bruin Actuarial Society Information Session. Property & Casualty Actuarial Careers

University of California, Los Angeles Bruin Actuarial Society Information Session Property & Casualty Actuarial Careers November 14, 2017 Adam Adam Hirsch, Hirsch, FCAS, FCAS, MAAA MAAA Oliver Wyman Oliver

University of California, Los Angeles Bruin Actuarial Society Information Session Property & Casualty Actuarial Careers November 14, 2017 Adam Adam Hirsch, Hirsch, FCAS, FCAS, MAAA MAAA Oliver Wyman Oliver

Statistical Modeling Techniques for Reserve Ranges: A Simulation Approach

Statistical Modeling Techniques for Reserve Ranges: A Simulation Approach by Chandu C. Patel, FCAS, MAAA KPMG Peat Marwick LLP Alfred Raws III, ACAS, FSA, MAAA KPMG Peat Marwick LLP STATISTICAL MODELING

Statistical Modeling Techniques for Reserve Ranges: A Simulation Approach by Chandu C. Patel, FCAS, MAAA KPMG Peat Marwick LLP Alfred Raws III, ACAS, FSA, MAAA KPMG Peat Marwick LLP STATISTICAL MODELING

Reserve Estimates: May 26, Raunak Jha

Reserve Estimates: The Blended Way May 26, 2011 Raunak Jha Deloitte Consulting India Pvt. Ltd Agenda Robust Reserving Process Popular Methods Blended Methods Bornhuetter- Ferguson Method The Cape Cod approach

Reserve Estimates: The Blended Way May 26, 2011 Raunak Jha Deloitte Consulting India Pvt. Ltd Agenda Robust Reserving Process Popular Methods Blended Methods Bornhuetter- Ferguson Method The Cape Cod approach

Basic non-life insurance and reserve methods

King Saud University College of Science Department of Mathematics Basic non-life insurance and reserve methods Student Name: Abdullah bin Ibrahim Al-Atar Student ID#: 434100610 Company Name: Al-Tawuniya

King Saud University College of Science Department of Mathematics Basic non-life insurance and reserve methods Student Name: Abdullah bin Ibrahim Al-Atar Student ID#: 434100610 Company Name: Al-Tawuniya

CENTRAL OHIO RISK MANAGEMENT ASSOCIATION (CORMA) ACTUARIAL REPORT ON UNPAID LOSS AND LOSS ADJUSTMENT EXPENSES AS OF SEPTEMBER 30, 2017

ACTUARIAL REPORT ON UNPAID LOSS AND LOSS ADJUSTMENT EXPENSES AS OF SEPTEMBER 30, 2017") CENTRAL OHIO RISK MANAGEMENT ASSOCIATION (CORMA) ACTUARIAL REPORT ON UNPAID LOSS AND LOSS ADJUSTMENT EXPENSES AS OF SEPTEMBER 30, 2017 October 25, 2017 October 25, 2017 Sent Via Email Ms. Angel Mumma Director

CENTRAL OHIO RISK MANAGEMENT ASSOCIATION (CORMA) ACTUARIAL REPORT ON UNPAID LOSS AND LOSS ADJUSTMENT EXPENSES AS OF SEPTEMBER 30, 2017 October 25, 2017 October 25, 2017 Sent Via Email Ms. Angel Mumma Director

Basic Track I CLRS September 2009 Chicago, IL

Basic Track I 2009 CLRS September 2009 Chicago, IL Introduction to Loss 2 Reserving CAS Statement of Principles Definitions Principles Considerations Basic Reserving Techniques Paid Loss Development Method

Basic Track I 2009 CLRS September 2009 Chicago, IL Introduction to Loss 2 Reserving CAS Statement of Principles Definitions Principles Considerations Basic Reserving Techniques Paid Loss Development Method

Non parametric IBNER projection

Non parametric IBNER projection Claude Perret Hannes van Rensburg Farshad Zanjani GIRO 2009, Edinburgh Agenda Introduction & background Why is IBNER important? Method description Issues Examples Introduction

Non parametric IBNER projection Claude Perret Hannes van Rensburg Farshad Zanjani GIRO 2009, Edinburgh Agenda Introduction & background Why is IBNER important? Method description Issues Examples Introduction

Chapter 5 Normal Probability Distributions

Chapter 5 Normal Probability Distributions Section 5-1 Introduction to Normal Distributions and the Standard Normal Distribution A The normal distribution is the most important of the continuous probability

Chapter 5 Normal Probability Distributions Section 5-1 Introduction to Normal Distributions and the Standard Normal Distribution A The normal distribution is the most important of the continuous probability

Covert Code. (previously known as Currency Messenger System 1)

") Covert Code (previously known as Currency Messenger System 1) COVERT CODE INDICATORS Covert Code uses 5 different indicators Mes Signal 1 Indicator which gives you buy and sell arrow signal on the screen.

Covert Code (previously known as Currency Messenger System 1) COVERT CODE INDICATORS Covert Code uses 5 different indicators Mes Signal 1 Indicator which gives you buy and sell arrow signal on the screen.

Ohio Bureau of Workers Compensation Actuarial Committee

Ohio Bureau of Workers Compensation Actuarial Committee Private Employer (PA) Rate Recommendations to be Effective July 1, 2012 Bob Miccolis, FCAS, MAAA Dave Heppen, FCAS, MAAA Deloitte Consulting LLP

Ohio Bureau of Workers Compensation Actuarial Committee Private Employer (PA) Rate Recommendations to be Effective July 1, 2012 Bob Miccolis, FCAS, MAAA Dave Heppen, FCAS, MAAA Deloitte Consulting LLP

Clark. Outside of a few technical sections, this is a very process-oriented paper. Practice problems are key!

Opening Thoughts Outside of a few technical sections, this is a very process-oriented paper. Practice problems are key! Outline I. Introduction Objectives in creating a formal model of loss reserving:

Opening Thoughts Outside of a few technical sections, this is a very process-oriented paper. Practice problems are key! Outline I. Introduction Objectives in creating a formal model of loss reserving:

Exploring the Fundamental Insurance Equation

Exploring the Fundamental Insurance Equation PATRICK STAPLETON, FCAS PRICING MANAGER ALLSTATE INSURANCE COMPANY PSTAP@ALLSTATE.COM CAS RPM March 2016 CAS Antitrust Notice The Casualty Actuarial Society

Exploring the Fundamental Insurance Equation PATRICK STAPLETON, FCAS PRICING MANAGER ALLSTATE INSURANCE COMPANY PSTAP@ALLSTATE.COM CAS RPM March 2016 CAS Antitrust Notice The Casualty Actuarial Society

Actuarial Highlights FARM Valuation as at December 31, Ontario Alberta. Facility Association Actuarial 11/9/2012

FARM Valuation as at December 31, 2011 Ontario Alberta Facility Association Actuarial 11/9/2012 Contents A. Executive Summary... 3 B. General Information... 7 B.1 Transition to Hybrid Model for Actuarial

FARM Valuation as at December 31, 2011 Ontario Alberta Facility Association Actuarial 11/9/2012 Contents A. Executive Summary... 3 B. General Information... 7 B.1 Transition to Hybrid Model for Actuarial

Ohio Petroleum Underground Storage Tank Release Compensation Board. Estimated Unpaid Claims Liability As ofjune 30, 2012

Ohio Petroleum Underground Storage Tank Release Compensation Board Estimated Unpaid Claims Liability As ofjune 30, 2012 Petroleum Underground Storage Tank Release Compensation Board Estimate of Unpaid

Ohio Petroleum Underground Storage Tank Release Compensation Board Estimated Unpaid Claims Liability As ofjune 30, 2012 Petroleum Underground Storage Tank Release Compensation Board Estimate of Unpaid

IMIA Working Group Paper 73 (11) Reserving - how to reserve an Engineering portfolio with its specific characteristics

Reserving - how to reserve an Engineering portfolio with its specific characteristics") IMIA Conference 2011 Amsterdam IMIA Working Group Paper 73 (11) - how to reserve an Engineering portfolio with its specific characteristics September 2011 Working Group Contributors 28.05.2009 2 Jürg Buff

IMIA Conference 2011 Amsterdam IMIA Working Group Paper 73 (11) - how to reserve an Engineering portfolio with its specific characteristics September 2011 Working Group Contributors 28.05.2009 2 Jürg Buff

FAV i R This paper is produced mechanically as part of FAViR. See for more information.

Basic Reserving Techniques By Benedict Escoto FAV i R This paper is produced mechanically as part of FAViR. See http://www.favir.net for more information. Contents 1 Introduction 1 2 Original Data 2 3

Basic Reserving Techniques By Benedict Escoto FAV i R This paper is produced mechanically as part of FAViR. See http://www.favir.net for more information. Contents 1 Introduction 1 2 Original Data 2 3

Developing a reserve range, from theory to practice. CAS Spring Meeting 22 May 2013 Vancouver, British Columbia

Developing a reserve range, from theory to practice CAS Spring Meeting 22 May 2013 Vancouver, British Columbia Disclaimer The views expressed by presenter(s) are not necessarily those of Ernst & Young

Developing a reserve range, from theory to practice CAS Spring Meeting 22 May 2013 Vancouver, British Columbia Disclaimer The views expressed by presenter(s) are not necessarily those of Ernst & Young

Comparison of IBNR Methods

Comparison of IBNR Methods 2009 Spring ACSW Meeting Background & Purpose Health actuaries need to deliver reliable estimates of claim costs Number of methods available Time span since practical analysis

Comparison of IBNR Methods 2009 Spring ACSW Meeting Background & Purpose Health actuaries need to deliver reliable estimates of claim costs Number of methods available Time span since practical analysis

A Comprehensive, Non-Aggregated, Stochastic Approach to. Loss Development

A Comprehensive, Non-Aggregated, Stochastic Approach to Loss Development By Uri Korn Abstract In this paper, we present a stochastic loss development approach that models all the core components of the

A Comprehensive, Non-Aggregated, Stochastic Approach to Loss Development By Uri Korn Abstract In this paper, we present a stochastic loss development approach that models all the core components of the

2011 CLRS - MPLI Reserving 101 9/15/2011

Medical Professional Liability Reserving 101 Common Reserving Techniques and Considerations 2011 Casualty Loss Reserve Seminar September 15, 2011 Kevin M. Dyke, FCAS, MAAA Michigan Office of Financial

Medical Professional Liability Reserving 101 Common Reserving Techniques and Considerations 2011 Casualty Loss Reserve Seminar September 15, 2011 Kevin M. Dyke, FCAS, MAAA Michigan Office of Financial

Reinsurance Loss Reserving Patrik, G. S. pp

Section Description Reinsurance Loss Reserving 1 Reinsurance Loss Reserving Problems 2 Components of a Reinsurer s Loss Reserve 3 Steps in Reinsurance Loss Reserving Methodology 4 Methods for Short, Medium

Section Description Reinsurance Loss Reserving 1 Reinsurance Loss Reserving Problems 2 Components of a Reinsurer s Loss Reserve 3 Steps in Reinsurance Loss Reserving Methodology 4 Methods for Short, Medium

374 Meridian Parke Lane, Suite C Greenwood, IN Phone: (317) Fax: (309)

Fax: (309)") 374 Meridian Parke Lane, Suite C Greenwood, IN 46142 Phone: (317) 889-5760 Fax: (309) 807-2301 John E. Wade, ACAS, MAAA JWade@PinnacleActuaries.com October 15, 2009 Eric Lloyd Manager Department of Financial

374 Meridian Parke Lane, Suite C Greenwood, IN 46142 Phone: (317) 889-5760 Fax: (309) 807-2301 John E. Wade, ACAS, MAAA JWade@PinnacleActuaries.com October 15, 2009 Eric Lloyd Manager Department of Financial

RESERVEPRO Technology to transform loss data into valuable information for insurance professionals

RESERVEPRO Technology to transform loss data into valuable information for insurance professionals Today s finance and actuarial professionals face increasing demands to better identify trends for smarter

RESERVEPRO Technology to transform loss data into valuable information for insurance professionals Today s finance and actuarial professionals face increasing demands to better identify trends for smarter

Integrating Reserve Variability and ERM:

Integrating Reserve Variability and ERM: Mark R. Shapland, FCAS, FSA, MAAA Jeffrey A. Courchene, FCAS, MAAA International Congress of Actuaries 30 March 4 April 2014 Washington, DC What are the Issues?

Integrating Reserve Variability and ERM: Mark R. Shapland, FCAS, FSA, MAAA Jeffrey A. Courchene, FCAS, MAAA International Congress of Actuaries 30 March 4 April 2014 Washington, DC What are the Issues?

Estimation and Application of Ranges of Reasonable Estimates. Charles L. McClenahan, FCAS, ASA, MAAA

Estimation and Application of Ranges of Reasonable Estimates Charles L. McClenahan, FCAS, ASA, MAAA 213 Estimation and Application of Ranges of Reasonable Estimates Charles L. McClenahan INTRODUCTION Until

Estimation and Application of Ranges of Reasonable Estimates Charles L. McClenahan, FCAS, ASA, MAAA 213 Estimation and Application of Ranges of Reasonable Estimates Charles L. McClenahan INTRODUCTION Until

QUARTERLY VALUATION HIGHLIGHTS RISK SHARING POOLS. as at September 30, Ontario Alberta Grid and Alberta Non Grid New Brunswick and Nova Scotia

QUARTERLY VALUATION HIGHLIGHTS RISK SHARING POOLS as at September 30, 2018 Ontario Alberta Grid and Alberta NonGrid New Brunswick and Nova Scotia FA Actuarial 1/16/2019 Should you require any further information,

QUARTERLY VALUATION HIGHLIGHTS RISK SHARING POOLS as at September 30, 2018 Ontario Alberta Grid and Alberta NonGrid New Brunswick and Nova Scotia FA Actuarial 1/16/2019 Should you require any further information,

Where s the Beef Does the Mack Method produce an undernourished range of possible outcomes?

Where s the Beef Does the Mack Method produce an undernourished range of possible outcomes? Daniel Murphy, FCAS, MAAA Trinostics LLC CLRS 2009 In the GIRO Working Party s simulation analysis, actual unpaid

Where s the Beef Does the Mack Method produce an undernourished range of possible outcomes? Daniel Murphy, FCAS, MAAA Trinostics LLC CLRS 2009 In the GIRO Working Party s simulation analysis, actual unpaid

DRAFT 2011 Exam 7 Advanced Techniques in Unpaid Claim Estimation, Insurance Company Valuation, and Enterprise Risk Management

2011 Exam 7 Advanced Techniques in Unpaid Claim Estimation, Insurance Company Valuation, and Enterprise Risk Management The CAS is providing this advanced copy of the draft syllabus for this exam so that

2011 Exam 7 Advanced Techniques in Unpaid Claim Estimation, Insurance Company Valuation, and Enterprise Risk Management The CAS is providing this advanced copy of the draft syllabus for this exam so that

Follow Price Action Trends By Laurentiu Damir Copyright 2012 Laurentiu Damir

Follow Price Action Trends By Laurentiu Damir Copyright 2012 Laurentiu Damir All rights reserved. No part of this book may be reproduced or transmitted in any form or by any means, electronic or mechanical,

Follow Price Action Trends By Laurentiu Damir Copyright 2012 Laurentiu Damir All rights reserved. No part of this book may be reproduced or transmitted in any form or by any means, electronic or mechanical,

Jacob: What data do we use? Do we compile paid loss triangles for a line of business?

PROJECT TEMPLATES FOR REGRESSION ANALYSIS APPLIED TO LOSS RESERVING BACKGROUND ON PAID LOSS TRIANGLES (The attached PDF file has better formatting.) {The paid loss triangle helps you! distinguish between

PROJECT TEMPLATES FOR REGRESSION ANALYSIS APPLIED TO LOSS RESERVING BACKGROUND ON PAID LOSS TRIANGLES (The attached PDF file has better formatting.) {The paid loss triangle helps you! distinguish between

Technical Provisions in Reinsurance: The Actuarial Perspective

Technical Provisions in Reinsurance: The Actuarial Perspective IAIS Reinsurance Subcommittee Copenhagen May 30, 2002 Presented by Dr. Hans Peter Boller, Converium Ltd (Switzerland) on behalf of the International

Technical Provisions in Reinsurance: The Actuarial Perspective IAIS Reinsurance Subcommittee Copenhagen May 30, 2002 Presented by Dr. Hans Peter Boller, Converium Ltd (Switzerland) on behalf of the International

The Fundamentals of Reserve Variability: From Methods to Models Central States Actuarial Forum August 26-27, 2010

The Fundamentals of Reserve Variability: From Methods to Models Definitions of Terms Overview Ranges vs. Distributions Methods vs. Models Mark R. Shapland, FCAS, ASA, MAAA Types of Methods/Models Allied

The Fundamentals of Reserve Variability: From Methods to Models Definitions of Terms Overview Ranges vs. Distributions Methods vs. Models Mark R. Shapland, FCAS, ASA, MAAA Types of Methods/Models Allied

EMB Consultancy LLP. Reserving for General Insurance Companies

EMB Consultancy LLP Reserving for General Insurance Companies Jonathan Broughton FIA March 2006 Programme Use of actuarial reserving techniques Data Issues Chain ladder projections: The core tool Bornhuetter

EMB Consultancy LLP Reserving for General Insurance Companies Jonathan Broughton FIA March 2006 Programme Use of actuarial reserving techniques Data Issues Chain ladder projections: The core tool Bornhuetter

CVS CAREMARK INDEMNITY LTD. NOTES TO THE FINANCIAL STATEMENTS DECEMBER 31, 2017 AND 2016 (expressed in United States dollars) 1. Operations CVS Carema

1. Operations CVS Carema") NOTES TO THE FINANCIAL STATEMENTS 1. Operations CVS Caremark Indemnity Ltd. ("The Company"), formerly known as Twinsurance Limited, was incorporated in Bermuda on March 27, 1980, and is a wholly owned

NOTES TO THE FINANCIAL STATEMENTS 1. Operations CVS Caremark Indemnity Ltd. ("The Company"), formerly known as Twinsurance Limited, was incorporated in Bermuda on March 27, 1980, and is a wholly owned

An Enhanced On-Level Approach to Calculating Expected Loss Costs

An Enhanced On-Level Approach to Calculating Expected s Marc B. Pearl, FCAS, MAAA Jeremy Smith, FCAS, MAAA, CERA, CPCU Abstract. Virtually every loss reserve analysis where loss and exposure or premium

An Enhanced On-Level Approach to Calculating Expected s Marc B. Pearl, FCAS, MAAA Jeremy Smith, FCAS, MAAA, CERA, CPCU Abstract. Virtually every loss reserve analysis where loss and exposure or premium

SOCIETY OF ACTUARIES Introduction to Ratemaking & Reserving Exam GIIRR MORNING SESSION. Date: Wednesday, April 29, 2015 Time: 8:30 a.m. 11:45 a.m.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, April 29, 2015 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, April 29, 2015 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

Xiaoli Jin and Edward W. (Jed) Frees. August 6, 2013

Frees. August 6, 2013") Xiaoli and Edward W. (Jed) Frees Department of Actuarial Science, Risk Management, and Insurance University of Wisconsin Madison August 6, 2013 1 / 20 Outline 1 2 3 4 5 6 2 / 20 for P&C Insurance Occurrence

Xiaoli and Edward W. (Jed) Frees Department of Actuarial Science, Risk Management, and Insurance University of Wisconsin Madison August 6, 2013 1 / 20 Outline 1 2 3 4 5 6 2 / 20 for P&C Insurance Occurrence

City of San José Federated City Employees Retirement System

City of San José Federated City Employees Retirement System Actuarial Valuation Report as of June 30, 2016 Produced by Cheiron January 11, 2017 TABLE OF CONTENTS Section Page Section I Board Summary...1

City of San José Federated City Employees Retirement System Actuarial Valuation Report as of June 30, 2016 Produced by Cheiron January 11, 2017 TABLE OF CONTENTS Section Page Section I Board Summary...1

9/5/2013. An Approach to Modeling Pharmaceutical Liability. Casualty Loss Reserve Seminar Boston, MA September Overview.

An Approach to Modeling Pharmaceutical Liability Casualty Loss Reserve Seminar Boston, MA September 2013 Overview Introduction Background Model Inputs / Outputs Model Mechanics Q&A Introduction Business

An Approach to Modeling Pharmaceutical Liability Casualty Loss Reserve Seminar Boston, MA September 2013 Overview Introduction Background Model Inputs / Outputs Model Mechanics Q&A Introduction Business

Analysis of Methods for Loss Reserving

Project Number: JPA0601 Analysis of Methods for Loss Reserving A Major Qualifying Project Report Submitted to the faculty of the Worcester Polytechnic Institute in partial fulfillment of the requirements

Project Number: JPA0601 Analysis of Methods for Loss Reserving A Major Qualifying Project Report Submitted to the faculty of the Worcester Polytechnic Institute in partial fulfillment of the requirements

Trading Strategy Tested and fluid strategy is essential

Trading Strategy Tested and fluid Roman Sadowski Making $1.000.000.000 in Forex aint easy but many traders do it! The goal of any forex trader is to maximize profits. But it ain t easy unless you have

Trading Strategy Tested and fluid Roman Sadowski Making $1.000.000.000 in Forex aint easy but many traders do it! The goal of any forex trader is to maximize profits. But it ain t easy unless you have

Poseidon FX System (previously known as Currency Messenger System 2) Poseidon system indicators:

Poseidon system indicators:") Poseidon FX System (previously known as Currency Messenger System 2) Poseidon system indicators: It uses 5 different indicators Mes Signal 2 Indicator which gives you buy and sell arrow signal on the screen.

Poseidon FX System (previously known as Currency Messenger System 2) Poseidon system indicators: It uses 5 different indicators Mes Signal 2 Indicator which gives you buy and sell arrow signal on the screen.

Structure & Learning Objectives

U1 Structure & Learning Objectives In this part of the course, we will study the newly revamped IMF framework for public debt sustainability in market-access countries A historical overview of debt-to-gdp

U1 Structure & Learning Objectives In this part of the course, we will study the newly revamped IMF framework for public debt sustainability in market-access countries A historical overview of debt-to-gdp

Stochastic Claims Reserving _ Methods in Insurance

Stochastic Claims Reserving _ Methods in Insurance and John Wiley & Sons, Ltd ! Contents Preface Acknowledgement, xiii r xi» J.. '..- 1 Introduction and Notation : :.... 1 1.1 Claims process.:.-.. : 1

Stochastic Claims Reserving _ Methods in Insurance and John Wiley & Sons, Ltd ! Contents Preface Acknowledgement, xiii r xi» J.. '..- 1 Introduction and Notation : :.... 1 1.1 Claims process.:.-.. : 1

State of Florida Division of Workers Compensation - Self Insurance Section

State of Florida Division of Workers Compensation - Self Insurance Section Checklist to accompany the annual actuarial report for loss reserve calculation INSTRUCTIONS: This form should be completed by

State of Florida Division of Workers Compensation - Self Insurance Section Checklist to accompany the annual actuarial report for loss reserve calculation INSTRUCTIONS: This form should be completed by

Tax Loss Harvesting at Vanguard A Primer

Tax Loss Harvesting at Vanguard A Primer In June of this year, there was a period of time where stocks dropped for about 6 days straight. In fact, if you look carefully at the chart, there were similar

Tax Loss Harvesting at Vanguard A Primer In June of this year, there was a period of time where stocks dropped for about 6 days straight. In fact, if you look carefully at the chart, there were similar

JOHN MORIKIS: SEAN HENNESSY:

JOHN MORIKIS: You ll be hearing from Jay Davisson, our president of the Americas Group, Cheri Pfeiffer, our president of our Diversified Brands Division, Joel Baxter, our president of our Global Supply

JOHN MORIKIS: You ll be hearing from Jay Davisson, our president of the Americas Group, Cheri Pfeiffer, our president of our Diversified Brands Division, Joel Baxter, our president of our Global Supply

Looking Ahead PROJECTING ONTARIO S PENSION BENEFITS GUARANTEE FUND

Looking Ahead PROJECTING ONTARIO S PENSION BENEFITS GUARANTEE FUND The Pension Benefits Guarantee Fund (PBGF) is governed by the Ontario Pension Benefits Act ( the Act ) and regulations made under the

Looking Ahead PROJECTING ONTARIO S PENSION BENEFITS GUARANTEE FUND The Pension Benefits Guarantee Fund (PBGF) is governed by the Ontario Pension Benefits Act ( the Act ) and regulations made under the

Solutions to the Fall 2013 CAS Exam 5

Solutions to the Fall 2013 CAS Exam 5 (Only those questions on Basic Ratemaking) Revised January 10, 2014 to correct an error in solution 11.a. Revised January 20, 2014 to correct an error in solution

Solutions to the Fall 2013 CAS Exam 5 (Only those questions on Basic Ratemaking) Revised January 10, 2014 to correct an error in solution 11.a. Revised January 20, 2014 to correct an error in solution

Exam 7 High-Level Summaries 2018 Sitting. Stephen Roll, FCAS

Exam 7 High-Level Summaries 2018 Sitting Stephen Roll, FCAS Copyright 2017 by Rising Fellow LLC All rights reserved. No part of this publication may be reproduced, distributed, or transmitted in any form

Exam 7 High-Level Summaries 2018 Sitting Stephen Roll, FCAS Copyright 2017 by Rising Fellow LLC All rights reserved. No part of this publication may be reproduced, distributed, or transmitted in any form

An Interview with Renaud Laplanche. Renaud Laplanche, CEO, Lending Club, speaks with Growthink University s Dave Lavinsky

An Interview with Renaud Laplanche Renaud Laplanche, CEO, Lending Club, speaks with Growthink University s Dave Lavinsky Dave Lavinsky: Hello everyone. This is Dave Lavinsky from Growthink. Today I am

An Interview with Renaud Laplanche Renaud Laplanche, CEO, Lending Club, speaks with Growthink University s Dave Lavinsky Dave Lavinsky: Hello everyone. This is Dave Lavinsky from Growthink. Today I am

APS310: Regulators and the search for better quality & more timely data post GFC

APS310: Regulators and the search for better quality & more timely data post GFC David Rule, Account Manager, Australia, New Zealand, Pacific, Wolters Kluwer Douglas Cheung, Regulatory Product Manager,

APS310: Regulators and the search for better quality & more timely data post GFC David Rule, Account Manager, Australia, New Zealand, Pacific, Wolters Kluwer Douglas Cheung, Regulatory Product Manager,

Double Chain Ladder and Bornhutter-Ferguson

Double Chain Ladder and Bornhutter-Ferguson María Dolores Martínez Miranda University of Granada, Spain mmiranda@ugr.es Jens Perch Nielsen Cass Business School, City University, London, U.K. Jens.Nielsen.1@city.ac.uk,

Double Chain Ladder and Bornhutter-Ferguson María Dolores Martínez Miranda University of Granada, Spain mmiranda@ugr.es Jens Perch Nielsen Cass Business School, City University, London, U.K. Jens.Nielsen.1@city.ac.uk,

Bornhuetter Ferguson Initial Expected Loss Ratio Report. September 17 th, 2013 Boston CLRS

Bornhuetter Ferguson Initial Expected Loss Ratio Report September 17 th, 2013 Boston CLRS Antitrust Notice The Casualty Actuarial Society is committed to adhering strictly to the letter and spirit of the

Bornhuetter Ferguson Initial Expected Loss Ratio Report September 17 th, 2013 Boston CLRS Antitrust Notice The Casualty Actuarial Society is committed to adhering strictly to the letter and spirit of the

Funding DB pension schemes: Getting the numbers right

Aon Hewitt Consulting Retirement & Investment Funding DB pension schemes: Risk. Reinsurance. Human Resources. Funding DB pension schemes: Executive summary There is considerable debate in the UK pensions

Aon Hewitt Consulting Retirement & Investment Funding DB pension schemes: Risk. Reinsurance. Human Resources. Funding DB pension schemes: Executive summary There is considerable debate in the UK pensions

Grasp Your Actuarial Report In 15 Minutes. Mujtaba Datoo, ACAS, MAAA, FCA Actuarial Practice Leader Aon Global Risk Consulting

Grasp Your Actuarial Report In 15 Minutes Mujtaba Datoo, AS, MAAA, F Actuarial Practice Leader Aon Global Risk Consulting SEPTEMBER 13-16, 2016 SOUTH LAKE TAHOE, Contextual Let s set up the context of

Grasp Your Actuarial Report In 15 Minutes Mujtaba Datoo, AS, MAAA, F Actuarial Practice Leader Aon Global Risk Consulting SEPTEMBER 13-16, 2016 SOUTH LAKE TAHOE, Contextual Let s set up the context of

2012 Health Care Workers Compensation Barometer

Aon Risk Solutions 2012 Health Care Workers Compensation Barometer Actuarial Analysis September 2012 Risk. Reinsurance. Human Resources. Empower Results 2012 Health Care Workers Compensation Barometer

Aon Risk Solutions 2012 Health Care Workers Compensation Barometer Actuarial Analysis September 2012 Risk. Reinsurance. Human Resources. Empower Results 2012 Health Care Workers Compensation Barometer

Western Power Distribution: consumerled pension strategy

www.pwc.com Western Power Distribution: consumerled pension strategy Workstream 3: Stakeholder engagement Phase 2 Domestic and Business bill-payers focus groups October 2016 Contents Workstream overview

www.pwc.com Western Power Distribution: consumerled pension strategy Workstream 3: Stakeholder engagement Phase 2 Domestic and Business bill-payers focus groups October 2016 Contents Workstream overview

GI IRR Model Solutions Spring 2015

GI IRR Model Solutions Spring 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1l) Adjust historical earned

GI IRR Model Solutions Spring 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1l) Adjust historical earned

Study Guide on Testing the Assumptions of Age-to-Age Factors - G. Stolyarov II 1

Study Guide on Testing the Assumptions of Age-to-Age Factors - G. Stolyarov II 1 Study Guide on Testing the Assumptions of Age-to-Age Factors for the Casualty Actuarial Society (CAS) Exam 7 and Society

Study Guide on Testing the Assumptions of Age-to-Age Factors - G. Stolyarov II 1 Study Guide on Testing the Assumptions of Age-to-Age Factors for the Casualty Actuarial Society (CAS) Exam 7 and Society

Solutions to the New STAM Sample Questions

Solutions to the New STAM Sample Questions 2018 Howard C. Mahler For STAM, the SOA revised their file of Sample Questions for Exam C. They deleted questions that are no longer on the syllabus of STAM.

Solutions to the New STAM Sample Questions 2018 Howard C. Mahler For STAM, the SOA revised their file of Sample Questions for Exam C. They deleted questions that are no longer on the syllabus of STAM.

This page intentionally left blank

P&C P&C Reserving Reserving 213 213 Development of claim of claim ratios ratios by line by line of business of business This page intentionally left blank Table of Contents Introduction P&C Reserving Basics

P&C P&C Reserving Reserving 213 213 Development of claim of claim ratios ratios by line by line of business of business This page intentionally left blank Table of Contents Introduction P&C Reserving Basics

Analysis of Liabilities Of the South Carolina Second Injury Fund. Including

Analysis of Liabilities Of the South Carolina Second Injury Fund Including Analysis of Current Liabilities Analysis of Future Liabilities, and Future Assessment Activity April 30, 2007 Prepared by Martin

Analysis of Liabilities Of the South Carolina Second Injury Fund Including Analysis of Current Liabilities Analysis of Future Liabilities, and Future Assessment Activity April 30, 2007 Prepared by Martin

A Stochastic Reserving Today (Beyond Bootstrap)

") A Stochastic Reserving Today (Beyond Bootstrap) Presented by Roger M. Hayne, PhD., FCAS, MAAA Casualty Loss Reserve Seminar 6-7 September 2012 Denver, CO CAS Antitrust Notice The Casualty Actuarial Society

A Stochastic Reserving Today (Beyond Bootstrap) Presented by Roger M. Hayne, PhD., FCAS, MAAA Casualty Loss Reserve Seminar 6-7 September 2012 Denver, CO CAS Antitrust Notice The Casualty Actuarial Society

WHS FutureStation - Guide LiveStatistics

WHS FutureStation - Guide LiveStatistics LiveStatistics is a paying module for the WHS FutureStation trading platform. This guide is intended to give the reader a flavour of the phenomenal possibilities

WHS FutureStation - Guide LiveStatistics LiveStatistics is a paying module for the WHS FutureStation trading platform. This guide is intended to give the reader a flavour of the phenomenal possibilities

SOCIETY OF ACTUARIES Introduction to Ratemaking & Reserving Exam GIIRR MORNING SESSION. Date: Wednesday, November 1, 2017 Time: 8:30 a.m. 11:45 a.m.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, November 1, 2017 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, November 1, 2017 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

Best counterstrategy for C

Best counterstrategy for C In the previous lecture we saw that if R plays a particular mixed strategy and shows no intention of changing it, the expected payoff for R (and hence C) varies as C varies her

Best counterstrategy for C In the previous lecture we saw that if R plays a particular mixed strategy and shows no intention of changing it, the expected payoff for R (and hence C) varies as C varies her

You have many choices when it comes to money and investing. Only one was created with you in mind. A Structured Settlement can provide hope and a

You have many choices when it comes to money and investing. Only one was created with you in mind. A Structured Settlement can provide hope and a secure future. Tax-Free. Guaranteed Benefits. Custom-Designed.

You have many choices when it comes to money and investing. Only one was created with you in mind. A Structured Settlement can provide hope and a secure future. Tax-Free. Guaranteed Benefits. Custom-Designed.

RECORD, Volume 22, No. 2 *

RECORD, Volume 22, No. 2 * Colorado Springs Meeting June 26 28, 1996 Session 34IF General Agreement on Tariffs & Trade (GATT) Funding Managing Contribution Volatility Track: Key words: Facilitators: Pension

RECORD, Volume 22, No. 2 * Colorado Springs Meeting June 26 28, 1996 Session 34IF General Agreement on Tariffs & Trade (GATT) Funding Managing Contribution Volatility Track: Key words: Facilitators: Pension

International Practice of Calculation of Insurance Reserves and Shares of Reinsurers in Insurance Reserves for Non-life Insurance

International Practice of Calculation of Insurance Reserves and Shares of Reinsurers in Insurance Reserves for Non-life Insurance Andrey Safonov Russian Guild of Actuaries (Russia) Types of Reserves Start

International Practice of Calculation of Insurance Reserves and Shares of Reinsurers in Insurance Reserves for Non-life Insurance Andrey Safonov Russian Guild of Actuaries (Russia) Types of Reserves Start

DRAFT for Campus Discussion August 10, 2017

Technical Notes for the Draft Shared Responsibility Budget Model FY16, FY17, FY18 versions for Oregon State University, Corvallis Campus, Education and General Budget Author Note Principal changes from

Technical Notes for the Draft Shared Responsibility Budget Model FY16, FY17, FY18 versions for Oregon State University, Corvallis Campus, Education and General Budget Author Note Principal changes from

Stochastic Loss Reserving with Bayesian MCMC Models Revised March 31

w w w. I C A 2 0 1 4. o r g Stochastic Loss Reserving with Bayesian MCMC Models Revised March 31 Glenn Meyers FCAS, MAAA, CERA, Ph.D. April 2, 2014 The CAS Loss Reserve Database Created by Meyers and Shi

w w w. I C A 2 0 1 4. o r g Stochastic Loss Reserving with Bayesian MCMC Models Revised March 31 Glenn Meyers FCAS, MAAA, CERA, Ph.D. April 2, 2014 The CAS Loss Reserve Database Created by Meyers and Shi

Technical analysis & Charting The Foundation of technical analysis is the Chart.

Technical analysis & Charting The Foundation of technical analysis is the Chart. Charts Mainly there are 2 types of charts 1. Line Chart 2. Candlestick Chart Line charts A chart shown below is the Line

Technical analysis & Charting The Foundation of technical analysis is the Chart. Charts Mainly there are 2 types of charts 1. Line Chart 2. Candlestick Chart Line charts A chart shown below is the Line

SOCIETY OF ACTUARIES Introduction to Ratemaking & Reserving Exam GIIRR MORNING SESSION. Date: Wednesday, April 25, 2018 Time: 8:30 a.m. 11:45 a.m.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, April 25, 2018 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, April 25, 2018 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

INTRODUCTION TO EXPERIENCE RATING Reinsurance Boot Camp Dawn Happ, Senior Vice President Willis Re

INTRODUCTION TO EXPERIENCE RATING 2013 Reinsurance Boot Camp Dawn Happ, Senior Vice President Willis Re Agenda Basic experience rating methodology Credibility weighting with exposure rate Diagnostics:

INTRODUCTION TO EXPERIENCE RATING 2013 Reinsurance Boot Camp Dawn Happ, Senior Vice President Willis Re Agenda Basic experience rating methodology Credibility weighting with exposure rate Diagnostics:

Budget Template: Guide for Sports Clubs

Budget Template: Guide for Sports Clubs Budget template guide for Sports Groups 1 Budget Template: Guide for Sports Clubs This guide is designed to be used alongside the Budget Template for Sports Groups.

Budget Template: Guide for Sports Clubs Budget template guide for Sports Groups 1 Budget Template: Guide for Sports Clubs This guide is designed to be used alongside the Budget Template for Sports Groups.

BOND MODEL COMMENTARY FOR APRIL 9, 2007

BOND MODEL COMMENTARY FOR APRIL 9, 2007 Charts and technical commentary by David Chapman Union Securities Ltd, 33 Yonge Street, Suite 901, Toronto, Ontario, M5E 1G4 fax (416) 604-0533, (416) 604-0557,

BOND MODEL COMMENTARY FOR APRIL 9, 2007 Charts and technical commentary by David Chapman Union Securities Ltd, 33 Yonge Street, Suite 901, Toronto, Ontario, M5E 1G4 fax (416) 604-0533, (416) 604-0557,

General Takaful Workshop

building value together 5 December 2012 General Takaful Workshop Tiffany Tan Ema Zaghlol www.actuarialpartners.com Contents Quarterly IBNR Valuation Provision of Risk Margin for Adverse Deviation (PRAD)

building value together 5 December 2012 General Takaful Workshop Tiffany Tan Ema Zaghlol www.actuarialpartners.com Contents Quarterly IBNR Valuation Provision of Risk Margin for Adverse Deviation (PRAD)

EARN 38 to 54%+ Returns Spending Under 30 Minutes a Day. Presented by: Todd Mitchell CEO & Founder Trading Concepts, Inc.

EARN 38 to 54%+ Returns Spending Under 30 Minutes a Day Presented by: Todd Mitchell CEO & Founder Trading Concepts, Inc. Who is Todd Mitchell? I have been involved with the markets and actively trading

EARN 38 to 54%+ Returns Spending Under 30 Minutes a Day Presented by: Todd Mitchell CEO & Founder Trading Concepts, Inc. Who is Todd Mitchell? I have been involved with the markets and actively trading

INSTITUTE AND FACULTY OF ACTUARIES. Curriculum 2019 SPECIMEN SOLUTIONS

INSTITUTE AND FACULTY OF ACTUARIES Curriculum 2019 SPECIMEN SOLUTIONS Subject CM1A Actuarial Mathematics Institute and Faculty of Actuaries 1 ( 91 ( 91 365 1 0.08 1 i = + 365 ( 91 365 0.980055 = 1+ i 1+

INSTITUTE AND FACULTY OF ACTUARIES Curriculum 2019 SPECIMEN SOLUTIONS Subject CM1A Actuarial Mathematics Institute and Faculty of Actuaries 1 ( 91 ( 91 365 1 0.08 1 i = + 365 ( 91 365 0.980055 = 1+ i 1+

SYLLABUS OF BASIC EDUCATION 2018 Estimation of Policy Liabilities, Insurance Company Valuation, and Enterprise Risk Management Exam 7

The syllabus for this four-hour exam is defined in the form of learning objectives, knowledge statements, and readings. set forth, usually in broad terms, what the candidate should be able to do in actual

The syllabus for this four-hour exam is defined in the form of learning objectives, knowledge statements, and readings. set forth, usually in broad terms, what the candidate should be able to do in actual

A new -package for statistical modelling and forecasting in non-life insurance. María Dolores Martínez-Miranda Jens Perch Nielsen Richard Verrall

A new -package for statistical modelling and forecasting in non-life insurance María Dolores Martínez-Miranda Jens Perch Nielsen Richard Verrall Cass Business School London, October 2013 2010 Including

A new -package for statistical modelling and forecasting in non-life insurance María Dolores Martínez-Miranda Jens Perch Nielsen Richard Verrall Cass Business School London, October 2013 2010 Including

13 EXPENDITURE MULTIPLIERS: THE KEYNESIAN MODEL* Chapter. Key Concepts

Chapter 3 EXPENDITURE MULTIPLIERS: THE KEYNESIAN MODEL* Key Concepts Fixed Prices and Expenditure Plans In the very short run, firms do not change their prices and they sell the amount that is demanded.

Chapter 3 EXPENDITURE MULTIPLIERS: THE KEYNESIAN MODEL* Key Concepts Fixed Prices and Expenditure Plans In the very short run, firms do not change their prices and they sell the amount that is demanded.

PRESENTS. COG Master Strategy. Trading Forex Using the Center Of Gravity Master Strategy. Wesley Govender

PRESENTS COG Master Strategy Trading Forex Using the Center Of Gravity Master Strategy Copyright 2013 by Old Tree Publishing CC, KZN, ZA Wesley Govender Reproduction or translation of any part of this

PRESENTS COG Master Strategy Trading Forex Using the Center Of Gravity Master Strategy Copyright 2013 by Old Tree Publishing CC, KZN, ZA Wesley Govender Reproduction or translation of any part of this

Becoming a Consistent Trader

presented by Thomas Wood MicroQuant SM Divergence Trading Workshop Day One Becoming a Consistent Trader Risk Disclaimer Trading or investing carries a high level of risk, and is not suitable for all persons.

presented by Thomas Wood MicroQuant SM Divergence Trading Workshop Day One Becoming a Consistent Trader Risk Disclaimer Trading or investing carries a high level of risk, and is not suitable for all persons.

Tommy s Revenge 2.0 Module 2 Part 2

1 Mark Deaton here with your follow-up to Module 2. Going to cover a few things in this video and try to keep it short and sweet. We re going to look at Stock Fetcher and how we can use Stock Fetcher to

1 Mark Deaton here with your follow-up to Module 2. Going to cover a few things in this video and try to keep it short and sweet. We re going to look at Stock Fetcher and how we can use Stock Fetcher to

GIIRR Model Solutions Fall 2015

GIIRR Model Solutions Fall 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1k) Estimate written, earned

GIIRR Model Solutions Fall 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1k) Estimate written, earned

The Analysis of All-Prior Data

Mark R. Shapland, FCAS, FSA, MAAA Abstract Motivation. Some data sources, such as the NAIC Annual Statement Schedule P as an example, contain a row of all-prior data within the triangle. While the CAS

Mark R. Shapland, FCAS, FSA, MAAA Abstract Motivation. Some data sources, such as the NAIC Annual Statement Schedule P as an example, contain a row of all-prior data within the triangle. While the CAS

Methods and Models of Loss Reserving Based on Run Off Triangles: A Unifying Survey

Methods and Models of Loss Reserving Based on Run Off Triangles: A Unifying Survey By Klaus D Schmidt Lehrstuhl für Versicherungsmathematik Technische Universität Dresden Abstract The present paper provides

Methods and Models of Loss Reserving Based on Run Off Triangles: A Unifying Survey By Klaus D Schmidt Lehrstuhl für Versicherungsmathematik Technische Universität Dresden Abstract The present paper provides

A Comprehensive, Non-Aggregated, Stochastic Approach to Loss Development

A Comprehensive, Non-Aggregated, Stochastic Approach to Loss Development by Uri Korn ABSTRACT In this paper, we present a stochastic loss development approach that models all the core components of the

A Comprehensive, Non-Aggregated, Stochastic Approach to Loss Development by Uri Korn ABSTRACT In this paper, we present a stochastic loss development approach that models all the core components of the