INTRODUCTION TO EXPERIENCE RATING Reinsurance Boot Camp Dawn Happ, Senior Vice President Willis Re

|

|

|

- Gladys Gilmore

- 6 years ago

- Views:

Transcription

1 INTRODUCTION TO EXPERIENCE RATING 2013 Reinsurance Boot Camp Dawn Happ, Senior Vice President Willis Re

2 Agenda Basic experience rating methodology Credibility weighting with exposure rate Diagnostics: telling the story 2

3 Steps in Experience Rating: 1. Compile historical premium and loss data Exclude catastrophe and shock losses and price separately 2. Adjust subject premium to future level 3. Adjust historical losses to future price and treaty coverage levels 4. Develop adjusted layer losses to ultimate 5. Select the non-cat / non-shock experience (loss cost) rate 6. Load for catastrophe/shock losses 3

4 1. Compile historical experience Review contract or placement slip if possible: What is the treaty term? What is the exposure basis? What is the definition of a risk? What is the definition of ultimate net loss? ALAE pro-rata or included? ECO/XPL? If multiline, is there a basket retention? 4

5 1. Compile historical experience Need historical premiums and losses on same basis Experience Rate (Loss Cost)= Trended Ultimate Layer Losses Trended On-Level Subject Premium Treaty accounting period may be Policy Year Risks Attaching Losses Occurring on Risks Attaching Accident Year Losses Occurring Losses Occurring During 5

6 PY WP = Written Premium on policies issued during the year PY Loss = (Paid + OS) on all claims attaching to policies issued during the year 100% earned 1/1/2013 1/1/2014 1/1/2015 6

7 AY EP = WP UEPR ending + UEPR prior = (WP) (Increase in UEPR) AY Inc. Loss = (Paid + OS) on all claims occurring during the year AY Premium Earnings AY Loss Occurrences 1/1/ /1/2013 1/1/2014 1/1/2015 7

8 1. Compile historical experience Get all the details on historical losses Include all historical losses that would trend into the layer (rule of thumb: get all losses > half of your attachment point) Split out ALAE for each loss Include historical policy limits (and SIR if applicable) Confirm that losses are assembled by occurrence, not by claimant Include line of business detail Include catastrophe/clash indicator, if applicable 8

9 Other data considerations Portfolio has changed over time Ceding company has exited contractors class Minimum deductibles have been increased from 5k to 10k ALAE Treatment ALAE Excluded ALAE Included ALAE Pro Rata 9

10 2. Adjust subject premium to future level Filed (manual) rate changes Price-level changes Schedule-rating, company tiers, etc. Also include soft changes such as terms & conditions, changes in underwriting standards, etc. Exposure trend For inflation-sensitive exposure bases 10

11 2. Adjust subject premium to future level Goal is to adjust historical premium to a level as if it has been written during the future period. The split between rate and price is not always obvious (e.g. where are LCM s or package factors included?) Often times ceding company provides renewal price changes, which include rate and other price-level changes How are limit and deductible changes accounted for? How has exposure change been factored in? 11

12 2. Adjust subject premium to future level Trended and Onlevel 12

13 2. Adjust subject premium to future level Note to actuaries coming from a primary rate-filing background: In a rate filing, you typically adjust premium to the current rate level. In reinsurance pricing, you want to adjust premium to the average rate level in the future period. CAS papers on this topic: Burt D. Jones s An Introduction to Premium Trend; CAS Exam Study Note, 2002 Trent Vaughn s Commercial Lines Price Monitoring; CAS Forum Fall 2004 Ira Robbin s paper Monitoring Renewal Rate Change on Cat-Exposed Excess Property Business; CAS E-Forum 2009 Winter Neil Bodoff s Measuring Rate Change; CAS E-Forum, Winter

14 3. Adjust historical losses to future price and treaty coverage levels Need to adjust historical losses up to the midpoint of the treaty period Typically we apply trend to the ground-up loss then cap the trended loss at the historical policy limit Trended and capped losses are then layered 14

15 3. Adjust historical losses to future price and treaty coverage levels Trend period depends on the treaty basis Experience Period (AY) Losses Occurring Treaty Experience Period (AY) Risks Attaching Treaty 15

16 3. Adjust historical losses to future price and treaty coverage levels Leveraged effect of trend on excess layers 1,200,000 1,000,000 trend 16

17 3. Adjust historical losses to future price and treaty coverage levels Trend impact on excess layer Layer: 500,000 excess of 500,000 Untrended Trended Trend % Total # Claims Ground-up Loss 17,723,204 19,141,060 Ground-up Severity 177, , % Layer count % Layer Severity 263, , % Layer Loss 2,106,590 2,475, % A numbers are for illustration only, and not for use in pricing 17

18 3. Adjust historical losses to future price and treaty coverage levels Inclusion of excess policies Supported Excess Unsupported Excess Excess Policy 1M xs 1M 2M Exposed Excess Policy 1M xs 1M 1M Exposed Primary Policy 1M Limit 18

19 3. Adjust historical losses to future price and treaty coverage levels Proper application of inflation trend on excess losses Add underlying loss or SIR to excess loss amount before trending or Use a higher trend percent to reflect leverage 19

20 4. Develop losses to ultimate Factors depend on layer of reinsurance being priced We apply LDFs to trended layer losses so that all years are on the same basis Development is an aggregate loss concept Includes new claims (true IBNR), development on known claims, reopening of closed claims, etc. 20

21 4. Develop losses to ultimate A numbers are for illustration only, and not for use in pricing 21

22 4. Develop losses to ultimate Note on loss development: Most recent periods are very green and may have zero losses reported to date. Should these years be included? If there are losses, then they are hit with a huge LDF. Alternative methods: ELR Bornhuetter-Ferguson (B-F) Cape Cod 22

23 4. Develop losses to ultimate LDF Method: Ultimate = Reported loss x LDF B-F method: Ultimate = Reported loss + premium x ELR x (1-1/LDF) But what ELR do we use? 23

24 4. Develop losses to ultimate Average of prior year ultimate loss ratios: ELR = Ultimate Loss Subject Premium Cape Cod ELR: ELR = Reported Loss Premium / LDF 24

25 4. Develop losses to ultimate ABC Insurance Company General Liability 500,000 excess of 500,000 - Loss plus ALAE included Historical Layered Trended Trended Subject Rate/Price Adjusted Adj. Subject Loss+ALAE Trended LDF Ult. Ultimate Ultimate Accident Earned OnLevel Exposure Subject Premium Evaluated Layered Loss Layered Loss Year Premium Factor Trend Premium LDF / LDF 12/31/2012 Loss+ALAE Rate Loss+ALAE* Rate (1) (2) (3) (4)=(1)*(2)*(3) (5) (6)=(4)/(5) (7) (8) (9)=(8)/(6) (10) (11)=(10)/(4) ,215, ,686, ,958,752 9, , % 763, % ,273, ,802, ,871, , , % 1,113, % ,676, ,920, ,761, , % 189, % ,924, ,755, ,374, ,711 1,096, % 1,293, % ,628, ,559, ,657, , , % 815, % ,458, ,739, ,893, ,081 1,213, % 1,612, % ,810, ,893, ,616,269 1,052,224 1,210, % 1,809, % ,121, ,266, ,651,043 18, , % 1,080, % ,142, ,101, ,018, , % 1,265, % ,714, ,313, ,191, % 1,463, % Total 194,967, ,037, ,995,350 2,429,115 5,813, % 11,407, % ,252, ,723,521 99,804,235 2,429,115 5,813, % 9,944, % Prospective Premium: 27,000,000 1,555, % (6) = "Exposed Premium" * "Cape Cod" Calculation: (10) = (8)+(4)*Total(9)*[1-1/(5)] 25

26 ALAE Treatment Layer: $300K xs $200K Gross Loss & ALAE ($K) ALAE Excluded Reinsurance Recovery ($K) ALAE Pro Rata ALAE Included Loss ALAE Loss + ALAE Loss Loss ALAE Loss + ALAE Loss + ALAE

27 Layer: $300K xs $200K Gross Loss & ALAE ($K) ALAE Excluded Reinsurance Recovery ($K) ALAE Pro Rata ALAE Included Loss ALAE Loss + ALAE Loss Loss ALAE Loss + ALAE Loss + ALAE

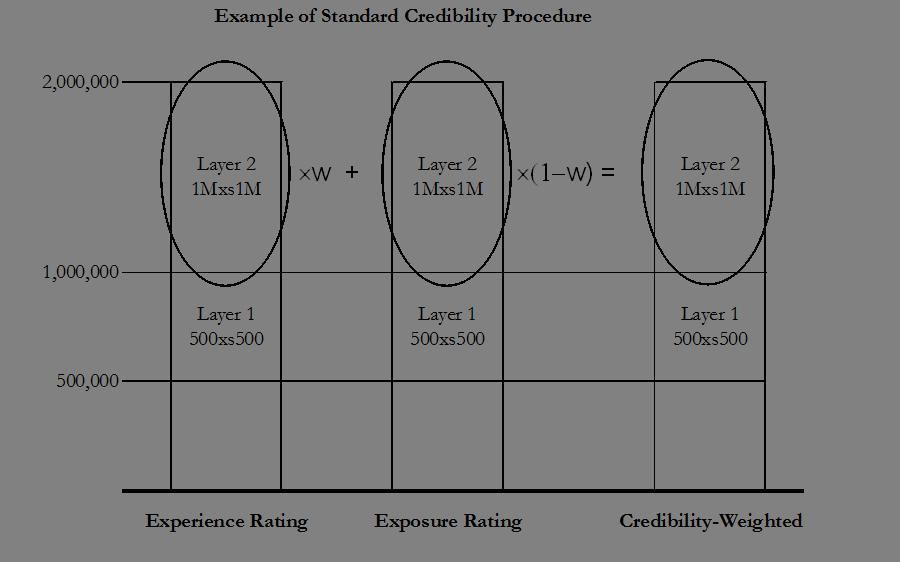

28 Credibility Experience rating = projection of losses based only on what took place for this specific account Accuracy of claim cost trend factors Accuracy of excess loss development factors Accuracy of subject premium on-level factors Stability of excess loss cost Changes in underlying exposure or policy limits over time Exposure rating = projection of losses using expected loss ratio, ceding company s inforce portfolio characteristics and severity curves Accuracy of ground up loss ratio/elr Accuracy of predicted portfolio distribution by line/ilf table/policy limit Accuracy of bureau ILFs in treaty layer Exposure not contemplated by ILFs, e.g. clash potential Niche business unlike industry average in exposure rating curves 28

29 Credibility Final loss cost = experience loss cost x (credibility) + exposure loss cost x (1 credibility) No single right measure of credibility Factors that increase credibility: Large # of claims expected Low attachment point Stability in historical loss costs 29

30 Credibility 30

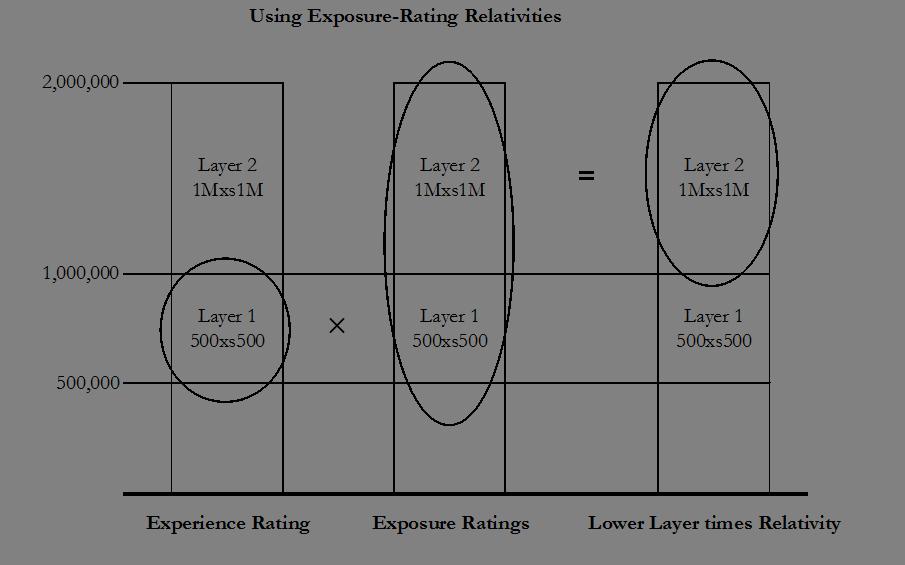

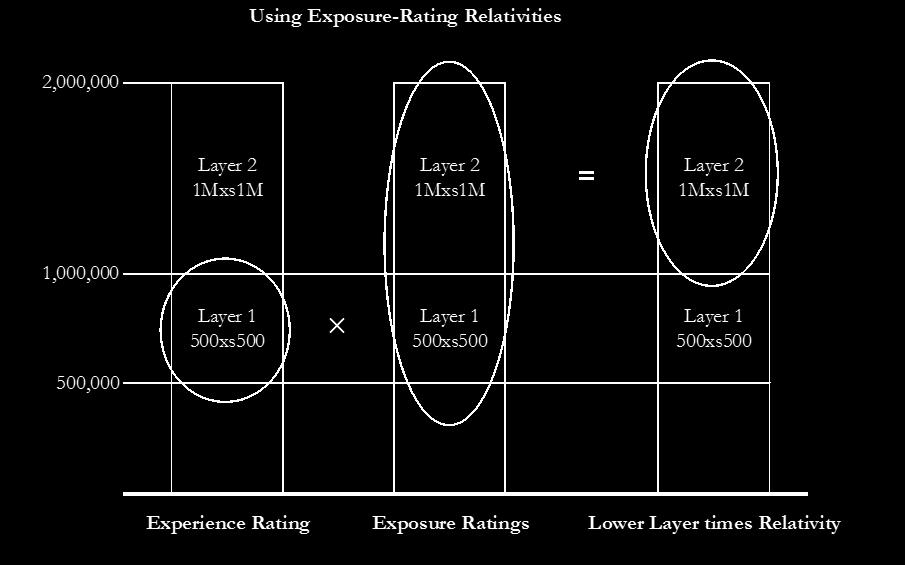

31 Credibility An additional estimate can be produced using exposure-rating relativities applied to a lower layer (e.g. 500,000 xs 500,000) 31

32 Credibility 32

33 Diagnostics: telling the story Does the experience rating make sense? Graphical display Use ground-up loss ratio experience to evaluate trend and onlevel Comparisons Prior years experience rating Exposure rating 33

34 Diagnostics: telling the story Simple test of actual versus expected: Actual versus Expected Analysis Accident Evaluated Evaluated Expected Expected Actual Year 12/31/2011 LDF 12/31/2012 LDF Link Ratio Development Development , , ,787 28, , , ,959 66, , , , , ,762, ,831, ,944 68, , , ,508 34, , , , , , , , , , , , , , , , ,799 Total 4,779,452 6,440, ,890 1,661,155 34

35 Diagnostics: telling the story Some questions to ask when reconciling with prior rating or exposure rating: Is the experience rating distorted by large losses? Is the ELR used in the exposure rating consistent with the ceding company s experience? Is the ALAE ratio the same? How has the business changed? Is the experience even relevant? Is this niche business unlike the industry average in the exposure rating curves? 35

36 Questions? Thank you for your attention. Dawn Happ, FCAS, MAAA Senior Vice President, Willis Re 36

37 Legal Disclaimer This analysis has been prepared by Willis Limited and/or Willis Re Inc ( Willis Re ) on condition that it shall be treated as strictly confidential and shall not be communicated in whole, in part, or in summary to any third party without written consent from Willis Re. Willis Re has relied upon data from public and/or other sources when preparing this analysis. No attempt has been made to verify independently the accuracy of this data. Willis Re does not represent or otherwise guarantee the accuracy or completeness of such data nor assume responsibility for the result of any error or omission in the data or other materials gathered from any source in the preparation of this analysis. Willis Re, its parent companies, sister companies, subsidiaries and affiliates (hereinafter Willis ) shall have no liability in connection with any results, including, without limitation, those arising from based upon or in connection with errors, omissions, inaccuracies, or inadequacies associated with the data or arising from, based upon or in connection with any methodologies used or applied by Willis Re in producing this analysis or any results contained herein. Willis expressly disclaims any and all liability arising from, based upon or in connection with this analysis. Willis assumes no duty in contract, tort or otherwise to any party arising from, based upon or in connection with this analysis, and no party should expect Willis to owe it any such duty. There are many uncertainties inherent in this analysis including, but not limited to, issues such as limitations in the available data, reliance on client data and outside data sources, the underlying volatility of loss and other random processes, uncertainties that characterize the application of professional judgment in estimates and assumptions, etc. Ultimate losses, liabilities and claims depend upon future contingent events, including but not limited to unanticipated changes in inflation, laws, and regulations. As a result of these uncertainties, the actual outcomes could vary significantly from Willis Re s estimates in either direction. Willis makes no representation about and does not guarantee the outcome, results, success, or profitability of any insurance or reinsurance program or venture, whether or not the analyses or conclusions contained herein apply to such program or venture. Willis does not recommend making decisions based solely on the information contained in this analysis. Rather, this analysis should be viewed as a supplement to other information, including specific business practice, claims experience, and financial situation. Independent professional advisors should be consulted with respect to the issues and conclusions presented herein and their possible application. Willis makes no representation or warranty as to the accuracy or completeness of this document and its contents. This analysis is not intended to be a complete actuarial communication, and as such is not intended to be relied upon. A complete communication can be provided upon request. Willis Re actuaries are available to answer questions about this analysis. Willis does not provide legal, accounting, or tax advice. This analysis does not constitute, is not intended to provide, and should not be construed as such advice. Qualified advisers should be consulted in these areas. Willis makes no representation, does not guarantee and assumes no liability for the accuracy or completeness of, or any results obtained by application of, this analysis and conclusions provided herein. Where data is supplied by way of CD or other electronic format, Willis accepts no liability for any loss or damage caused to the Recipient directly or indirectly through use of any such CD or other electronic format, even where caused by negligence. Without limitation, Willis shall not be liable for: loss or corruption of data, damage to any computer or communications system, indirect or consequential losses. The Recipient should take proper precautions to prevent loss or damage including the use of a virus checker. This limitation of liability does not apply to losses or damage caused by death, personal injury, dishonesty or any other liability which cannot be excluded by law. This analysis is not intended to be a complete Financial Analysis communication. A complete communication can be provided upon request. Willis Re analysts are available to answer questions about this analysis. Willis does not guarantee any specific financial result or outcome, level of profitability, valuation, or rating agency outcome with respect to A.M. Best or any other agency. Willis specifically disclaims any and all liability for any and all damages of any amount or any type, including without limitation, lost profits, unrealized profits, compensatory damages based on any legal theory, punitive, multiple or statutory damages or fines of any type, based upon, arising from, in connection with or in any manner related to the services provided hereunder. Acceptance of this document shall be deemed agreement to the above. 37

Risks. Insurance. Credit Inflation Liquidity Operational Strategic. Market. Risk Controlling Achieving Mastery over Unwanted Surprises

CONTROLLING INSURER TOP RISKS Risk Controlling Achieving Mastery over Unwanted Surprises Risks Insurance Underwriting - Nat Cat Underwriting Property Underwriting - Casualty Reserve Market Equity Interest

CONTROLLING INSURER TOP RISKS Risk Controlling Achieving Mastery over Unwanted Surprises Risks Insurance Underwriting - Nat Cat Underwriting Property Underwriting - Casualty Reserve Market Equity Interest

OWN RISK AND SOLVENCY ASSESSMENT. ERM Seminar Compliance All Dealing from the same deck now

OWN RISK AND SOLVENCY ASSESSMENT ERM Seminar - 2014 Compliance All Dealing from the same deck now Own and Solvency Assessment! Originated in the UK about 10 years ago Now a global insurance regulatory

OWN RISK AND SOLVENCY ASSESSMENT ERM Seminar - 2014 Compliance All Dealing from the same deck now Own and Solvency Assessment! Originated in the UK about 10 years ago Now a global insurance regulatory

Neil Bodoff, FCAS, MAAA CAS Annual Meeting November 16, Stanhope by Hufton + Crow

CAPITAL ALLOCATION BY PERCENTILE LAYER Neil Bodoff, FCAS, MAAA CAS Annual Meeting November 16, 2009 Stanhope by Hufton + Crow Actuarial Disclaimer This analysis has been prepared by Willis Re on condition

CAPITAL ALLOCATION BY PERCENTILE LAYER Neil Bodoff, FCAS, MAAA CAS Annual Meeting November 16, 2009 Stanhope by Hufton + Crow Actuarial Disclaimer This analysis has been prepared by Willis Re on condition

Reinsurance Structures and Pricing Pro-Rata Treaties. Care Reinsurance Boot Camp Josh Fishman, FCAS, MAAA August 12, 2013

Reinsurance Structures and Pricing Pro-Rata Treaties Care Reinsurance Boot Camp Josh Fishman, FCAS, MAAA August 12, 2013 Motivations for Purchasing Reinsurance 1) Limiting Liability [on specific risks]

Reinsurance Structures and Pricing Pro-Rata Treaties Care Reinsurance Boot Camp Josh Fishman, FCAS, MAAA August 12, 2013 Motivations for Purchasing Reinsurance 1) Limiting Liability [on specific risks]

An Analysis of the Market Price of Cat Bonds

An Analysis of the Price of Cat Bonds Neil Bodoff, FCAS and Yunbo Gan, PhD 2009 CAS Reinsurance Seminar Disclaimer The statements and opinions included in this Presentation are those of the individual

An Analysis of the Price of Cat Bonds Neil Bodoff, FCAS and Yunbo Gan, PhD 2009 CAS Reinsurance Seminar Disclaimer The statements and opinions included in this Presentation are those of the individual

The Real World: Dealing With Parameter Risk. Alice Underwood Senior Vice President, Willis Re March 29, 2007

The Real World: Dealing With Parameter Risk Alice Underwood Senior Vice President, Willis Re March 29, 2007 Agenda 1. What is Parameter Risk? 2. Practical Observations 3. Quantifying Parameter Risk 4.

The Real World: Dealing With Parameter Risk Alice Underwood Senior Vice President, Willis Re March 29, 2007 Agenda 1. What is Parameter Risk? 2. Practical Observations 3. Quantifying Parameter Risk 4.

Reinsurance Loss Reserving Patrik, G. S. pp

Section Description Reinsurance Loss Reserving 1 Reinsurance Loss Reserving Problems 2 Components of a Reinsurer s Loss Reserve 3 Steps in Reinsurance Loss Reserving Methodology 4 Methods for Short, Medium

Section Description Reinsurance Loss Reserving 1 Reinsurance Loss Reserving Problems 2 Components of a Reinsurer s Loss Reserve 3 Steps in Reinsurance Loss Reserving Methodology 4 Methods for Short, Medium

EVEREST RE GROUP, LTD LOSS DEVELOPMENT TRIANGLES

2017 Loss Development Triangle Cautionary Language This report is for informational purposes only. It is current as of December 31, 2017. Everest Re Group, Ltd. ( Everest, we, us, or the Company ) is under

2017 Loss Development Triangle Cautionary Language This report is for informational purposes only. It is current as of December 31, 2017. Everest Re Group, Ltd. ( Everest, we, us, or the Company ) is under

Calculating a Loss Ratio for Commercial Umbrella. CAS Seminar on Reinsurance June 6-7, 2016 Ya Jia, ACAS, MAAA Munich Reinsurance America, Inc.

Calculating a Loss Ratio for Commercial Umbrella CAS Seminar on Reinsurance June 6-7, 2016 Ya Jia, ACAS, MAAA Munich Reinsurance America, Inc. Antitrust Notice The Casualty Actuarial Society is committed

Calculating a Loss Ratio for Commercial Umbrella CAS Seminar on Reinsurance June 6-7, 2016 Ya Jia, ACAS, MAAA Munich Reinsurance America, Inc. Antitrust Notice The Casualty Actuarial Society is committed

Solutions to the New STAM Sample Questions

Solutions to the New STAM Sample Questions 2018 Howard C. Mahler For STAM, the SOA revised their file of Sample Questions for Exam C. They deleted questions that are no longer on the syllabus of STAM.

Solutions to the New STAM Sample Questions 2018 Howard C. Mahler For STAM, the SOA revised their file of Sample Questions for Exam C. They deleted questions that are no longer on the syllabus of STAM.

Patrik. I really like the Cape Cod method. The math is simple and you don t have to think too hard.

Opening Thoughts I really like the Cape Cod method. The math is simple and you don t have to think too hard. Outline I. Reinsurance Loss Reserving Problems Problem 1: Claim report lags to reinsurers are

Opening Thoughts I really like the Cape Cod method. The math is simple and you don t have to think too hard. Outline I. Reinsurance Loss Reserving Problems Problem 1: Claim report lags to reinsurers are

Reinsurance Pricing 101 How Reinsurance Costs Are Created November 2014

Reinsurance Pricing 101 How Reinsurance Costs Are Created November 2014 Course Description Reinsurance Pricing 101: How reinsurance costs are created. This session will cover the basics of pricing reinsurance

Reinsurance Pricing 101 How Reinsurance Costs Are Created November 2014 Course Description Reinsurance Pricing 101: How reinsurance costs are created. This session will cover the basics of pricing reinsurance

Basic Reserving: Estimating the Liability for Unpaid Claims

Basic Reserving: Estimating the Liability for Unpaid Claims September 15, 2014 Derek Freihaut, FCAS, MAAA John Wade, ACAS, MAAA Pinnacle Actuarial Resources, Inc. Loss Reserve What is a loss reserve? Amount

Basic Reserving: Estimating the Liability for Unpaid Claims September 15, 2014 Derek Freihaut, FCAS, MAAA John Wade, ACAS, MAAA Pinnacle Actuarial Resources, Inc. Loss Reserve What is a loss reserve? Amount

Structured Tools to Help Organize One s Thinking When Performing or Reviewing a Reserve Analysis

Structured Tools to Help Organize One s Thinking When Performing or Reviewing a Reserve Analysis Jennifer Cheslawski Balester Deloitte Consulting LLP September 17, 2013 Gerry Kirschner AIG Agenda Learning

Structured Tools to Help Organize One s Thinking When Performing or Reviewing a Reserve Analysis Jennifer Cheslawski Balester Deloitte Consulting LLP September 17, 2013 Gerry Kirschner AIG Agenda Learning

Negative Frequency Trends? 2013 CAS Seminar on Reinsurance June 6-7,2013. Jill Cecchini FCAS, MAAA Vice President SCOR Reinsurance

Negative Frequency Trends? 2013 CAS Seminar on Reinsurance June 6-7,2013 Jill Cecchini FCAS, MAAA Vice President SCOR Reinsurance Antitrust Notice The Casualty Actuarial Society is committed to adhering

Negative Frequency Trends? 2013 CAS Seminar on Reinsurance June 6-7,2013 Jill Cecchini FCAS, MAAA Vice President SCOR Reinsurance Antitrust Notice The Casualty Actuarial Society is committed to adhering

Reinsurance (Passing grade for this exam is 74)

") Supplemental Background Material NAIC Examiner Project Course CFE 3 (Passing grade for this exam is 74) Please note that this study guide is a tool for learning the materials you need to effectively study

Supplemental Background Material NAIC Examiner Project Course CFE 3 (Passing grade for this exam is 74) Please note that this study guide is a tool for learning the materials you need to effectively study

P&C Reinsurance Pricing 101 Ohio Chapter IASA. Prepared by Aon Benfield Inpoint Operations

P&C Reinsurance Pricing 101 Ohio Chapter IASA Prepared by Aon Benfield Inpoint Operations Agenda Focus on Treaty, P&C Reinsurance Certain concepts apply to Facultative and/or LYH Reinsurance Pro-Rata Reinsurance

P&C Reinsurance Pricing 101 Ohio Chapter IASA Prepared by Aon Benfield Inpoint Operations Agenda Focus on Treaty, P&C Reinsurance Certain concepts apply to Facultative and/or LYH Reinsurance Pro-Rata Reinsurance

General Insurance Introduction to Ratemaking & Reserving Exam

Learn Today. Lead Tomorrow. ACTEX Study Manual for General Insurance Introduction to Ratemaking & Reserving Exam Spring 2018 Edition Ke Min, ACIA, ASA, CERA ACTEX Study Manual for General Insurance Introduction

Learn Today. Lead Tomorrow. ACTEX Study Manual for General Insurance Introduction to Ratemaking & Reserving Exam Spring 2018 Edition Ke Min, ACIA, ASA, CERA ACTEX Study Manual for General Insurance Introduction

CENTRAL OHIO RISK MANAGEMENT ASSOCIATION (CORMA) ACTUARIAL REPORT ON UNPAID LOSS AND LOSS ADJUSTMENT EXPENSES AS OF SEPTEMBER 30, 2017

ACTUARIAL REPORT ON UNPAID LOSS AND LOSS ADJUSTMENT EXPENSES AS OF SEPTEMBER 30, 2017") CENTRAL OHIO RISK MANAGEMENT ASSOCIATION (CORMA) ACTUARIAL REPORT ON UNPAID LOSS AND LOSS ADJUSTMENT EXPENSES AS OF SEPTEMBER 30, 2017 October 25, 2017 October 25, 2017 Sent Via Email Ms. Angel Mumma Director

CENTRAL OHIO RISK MANAGEMENT ASSOCIATION (CORMA) ACTUARIAL REPORT ON UNPAID LOSS AND LOSS ADJUSTMENT EXPENSES AS OF SEPTEMBER 30, 2017 October 25, 2017 October 25, 2017 Sent Via Email Ms. Angel Mumma Director

Reinsurance 101: an Overview Session 107

Reinsurance 101: an Overview Session 107 Monday, June 9, 2014 1:30pm 3:00pm IASA 86 TH ANNUAL EDUCATIONAL CONFERENCE & BUSINESS SHOW Introductions Tim Corley Tim is a Senior Solutions Executive for Inpoint

Reinsurance 101: an Overview Session 107 Monday, June 9, 2014 1:30pm 3:00pm IASA 86 TH ANNUAL EDUCATIONAL CONFERENCE & BUSINESS SHOW Introductions Tim Corley Tim is a Senior Solutions Executive for Inpoint

Solutions to the Fall 2013 CAS Exam 5

Solutions to the Fall 2013 CAS Exam 5 (Only those questions on Basic Ratemaking) Revised January 10, 2014 to correct an error in solution 11.a. Revised January 20, 2014 to correct an error in solution

Solutions to the Fall 2013 CAS Exam 5 (Only those questions on Basic Ratemaking) Revised January 10, 2014 to correct an error in solution 11.a. Revised January 20, 2014 to correct an error in solution

DRAFT 2011 Exam 5 Basic Ratemaking and Reserving

2011 Exam 5 Basic Ratemaking and Reserving The CAS is providing this advanced copy of the draft syllabus for this exam so that candidates and educators will have a sense of the learning objectives and

2011 Exam 5 Basic Ratemaking and Reserving The CAS is providing this advanced copy of the draft syllabus for this exam so that candidates and educators will have a sense of the learning objectives and

California Joint Powers Insurance Authority

An Actuarial Analysis of the Self-Insurance Program as of June 30, 2018 October 26, 2018 Michael L. DeMattei, FCAS, MAAA Jonathan B. Winn, FCAS, MAAA Table of Contents INTRODUCTION... 1 Purpose of Report...

An Actuarial Analysis of the Self-Insurance Program as of June 30, 2018 October 26, 2018 Michael L. DeMattei, FCAS, MAAA Jonathan B. Winn, FCAS, MAAA Table of Contents INTRODUCTION... 1 Purpose of Report...

IASB Educational Session Non-Life Claims Liability

IASB Educational Session Non-Life Claims Liability Presented by the January 19, 2005 Sam Gutterman and Martin White Agenda Background The claims process Components of claims liability and basic approach

IASB Educational Session Non-Life Claims Liability Presented by the January 19, 2005 Sam Gutterman and Martin White Agenda Background The claims process Components of claims liability and basic approach

Technical Provisions in Reinsurance: The Actuarial Perspective

Technical Provisions in Reinsurance: The Actuarial Perspective IAIS Reinsurance Subcommittee Copenhagen May 30, 2002 Presented by Dr. Hans Peter Boller, Converium Ltd (Switzerland) on behalf of the International

Technical Provisions in Reinsurance: The Actuarial Perspective IAIS Reinsurance Subcommittee Copenhagen May 30, 2002 Presented by Dr. Hans Peter Boller, Converium Ltd (Switzerland) on behalf of the International

Exploring the Fundamental Insurance Equation

Exploring the Fundamental Insurance Equation PATRICK STAPLETON, FCAS PRICING MANAGER ALLSTATE INSURANCE COMPANY PSTAP@ALLSTATE.COM CAS RPM March 2016 CAS Antitrust Notice The Casualty Actuarial Society

Exploring the Fundamental Insurance Equation PATRICK STAPLETON, FCAS PRICING MANAGER ALLSTATE INSURANCE COMPANY PSTAP@ALLSTATE.COM CAS RPM March 2016 CAS Antitrust Notice The Casualty Actuarial Society

Bornhuetter Ferguson Initial Expected Loss Ratio Report. September 17 th, 2013 Boston CLRS

Bornhuetter Ferguson Initial Expected Loss Ratio Report September 17 th, 2013 Boston CLRS Antitrust Notice The Casualty Actuarial Society is committed to adhering strictly to the letter and spirit of the

Bornhuetter Ferguson Initial Expected Loss Ratio Report September 17 th, 2013 Boston CLRS Antitrust Notice The Casualty Actuarial Society is committed to adhering strictly to the letter and spirit of the

Property / Casualty State of the Market. Greg Williams Vice President

IASA Fall Meeting Property / Casualty State of the Market Greg Williams Vice President Agenda State of the Market Market Forces Financial Indicators & Underwriting Details Outlooks In the News Cyber Security

IASA Fall Meeting Property / Casualty State of the Market Greg Williams Vice President Agenda State of the Market Market Forces Financial Indicators & Underwriting Details Outlooks In the News Cyber Security

PAYROLL SERVICE AGREEMENT

PAYROLL SERVICE AGREEMENT YOUR NAME: DATE: This Payroll Services Agreement (this Agreement ) is made as of the day of, 20 for the effective service commencement date of, between Client identified above

PAYROLL SERVICE AGREEMENT YOUR NAME: DATE: This Payroll Services Agreement (this Agreement ) is made as of the day of, 20 for the effective service commencement date of, between Client identified above

CARe Seminar on Reinsurance - Loss Sensitive Treaty Features. June 6, 2011 Matthew Dobrin, FCAS

CARe Seminar on Reinsurance - Loss Sensitive Treaty Features June 6, 2011 Matthew Dobrin, FCAS 2 Table of Contents Ø Overview of Loss Sensitive Treaty Features Ø Common reinsurance structures for Proportional

CARe Seminar on Reinsurance - Loss Sensitive Treaty Features June 6, 2011 Matthew Dobrin, FCAS 2 Table of Contents Ø Overview of Loss Sensitive Treaty Features Ø Common reinsurance structures for Proportional

Cboe Global Markets Subscriber Agreement

Cboe Global Markets Subscriber Agreement Vendor may not modify or waive any term of this Agreement. Any attempt to modify this Agreement, except by Cboe Data Services, LLC ( CDS ) or its affiliates, is

Cboe Global Markets Subscriber Agreement Vendor may not modify or waive any term of this Agreement. Any attempt to modify this Agreement, except by Cboe Data Services, LLC ( CDS ) or its affiliates, is

SYLLABUS OF BASIC EDUCATION 2018 Basic Techniques for Ratemaking and Estimating Claim Liabilities Exam 5

The syllabus for this four-hour exam is defined in the form of learning objectives, knowledge statements, and readings. Exam 5 is administered as a technology-based examination. set forth, usually in broad

The syllabus for this four-hour exam is defined in the form of learning objectives, knowledge statements, and readings. Exam 5 is administered as a technology-based examination. set forth, usually in broad

Reinsurance Symposium 2016

Reinsurance Symposium 2016 MAY 10 12, 2016 GEN RE HOME OFFICE, STAMFORD, CT A Berkshire Hathaway Company Reinsurance Symposium 2016 MAY 10 12, 2016 GEN RE HOME OFFICE, STAMFORD, CT Developing a Treaty

Reinsurance Symposium 2016 MAY 10 12, 2016 GEN RE HOME OFFICE, STAMFORD, CT A Berkshire Hathaway Company Reinsurance Symposium 2016 MAY 10 12, 2016 GEN RE HOME OFFICE, STAMFORD, CT Developing a Treaty

CVS CAREMARK INDEMNITY LTD. NOTES TO THE FINANCIAL STATEMENTS DECEMBER 31, 2017 AND 2016 (expressed in United States dollars) 1. Operations CVS Carema

1. Operations CVS Carema") NOTES TO THE FINANCIAL STATEMENTS 1. Operations CVS Caremark Indemnity Ltd. ("The Company"), formerly known as Twinsurance Limited, was incorporated in Bermuda on March 27, 1980, and is a wholly owned

NOTES TO THE FINANCIAL STATEMENTS 1. Operations CVS Caremark Indemnity Ltd. ("The Company"), formerly known as Twinsurance Limited, was incorporated in Bermuda on March 27, 1980, and is a wholly owned

What to Do When the Actuary s Answer is Too High. Timothy C. Mosler, FCAS, MAAA

What to Do When the Actuary s Answer is Too High Timothy C. Mosler, FCAS, MAAA February 25, 2016 Agenda Tim Mosler s Background Disclaimer Basics of Reserve/Funding Analysis 3 Reactions When the Client

What to Do When the Actuary s Answer is Too High Timothy C. Mosler, FCAS, MAAA February 25, 2016 Agenda Tim Mosler s Background Disclaimer Basics of Reserve/Funding Analysis 3 Reactions When the Client

Introduction to Casualty Actuarial Science

Introduction to Casualty Actuarial Science Director of Property & Casualty Email: ken@theinfiniteactuary.com 1 Casualty Actuarial Science Two major areas are measuring 1. Written Premium Risk Pricing 2.

Introduction to Casualty Actuarial Science Director of Property & Casualty Email: ken@theinfiniteactuary.com 1 Casualty Actuarial Science Two major areas are measuring 1. Written Premium Risk Pricing 2.

Antitrust Notice 31/05/2016. Evaluating a Commercial Umbrella Rating Plan Using ISO. Table of Contents / Agenda

Antitrust Notice The Casualty Actuarial Society is committed to adhering strictly to the letter and spirit of the antitrust laws. Seminars conducted under the auspices of the CAS are designed solely to

Antitrust Notice The Casualty Actuarial Society is committed to adhering strictly to the letter and spirit of the antitrust laws. Seminars conducted under the auspices of the CAS are designed solely to

Introduction to Casualty Actuarial Science

Introduction to Casualty Actuarial Science Executive Director Email: ken@theinfiniteactuary.com 1 Casualty Actuarial Science Two major areas are measuring 1. Written Premium Risk Pricing 2. Earned Premium

Introduction to Casualty Actuarial Science Executive Director Email: ken@theinfiniteactuary.com 1 Casualty Actuarial Science Two major areas are measuring 1. Written Premium Risk Pricing 2. Earned Premium

To Members of the Actuarial Committee, WCIRB Members and All Interested Parties:

Meeting Agenda Date Time Location Staff Contact August 1, 2018 9:30 AM WCIRB California David M. Bellusci 1221 Broadway, Suite 900 Oakland, CA 1221 Broadway, Suite 900 Oakland, CA 94612 415.777.0777 Fax

Meeting Agenda Date Time Location Staff Contact August 1, 2018 9:30 AM WCIRB California David M. Bellusci 1221 Broadway, Suite 900 Oakland, CA 1221 Broadway, Suite 900 Oakland, CA 94612 415.777.0777 Fax

Measuring the Rate Change of a Non-Static Book of Property and Casualty Insurance Business

Measuring the Rate Change of a Non-Static Book of Property and Casualty Insurance Business Neil M. Bodoff, * FCAS, MAAA Copyright 2008 by the Society of Actuaries. All rights reserved by the Society of

Measuring the Rate Change of a Non-Static Book of Property and Casualty Insurance Business Neil M. Bodoff, * FCAS, MAAA Copyright 2008 by the Society of Actuaries. All rights reserved by the Society of

2015 Statutory Combined Annual Statement Schedule P Disclosure

2015 Statutory Combined Annual Statement Schedule P Disclosure This disclosure provides supplemental facts and methodologies intended to enhance understanding of Schedule P reserve data. It provides additional

2015 Statutory Combined Annual Statement Schedule P Disclosure This disclosure provides supplemental facts and methodologies intended to enhance understanding of Schedule P reserve data. It provides additional

3/10/2014. Exploring the Fundamental Insurance Equation. CAS Antitrust Notice. Fundamental Insurance Equation

Exploring the Fundamental Insurance Equation Eric Schmidt, FCAS Associate Actuary Allstate Insurance Company escap@allstate.com CAS RPM 2014 CAS Antitrust Notice The Casualty Actuarial Society is committed

Exploring the Fundamental Insurance Equation Eric Schmidt, FCAS Associate Actuary Allstate Insurance Company escap@allstate.com CAS RPM 2014 CAS Antitrust Notice The Casualty Actuarial Society is committed

GI IRR Model Solutions Spring 2015

GI IRR Model Solutions Spring 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1l) Adjust historical earned

GI IRR Model Solutions Spring 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1l) Adjust historical earned

Workers Compensation Exposure Rating Gerald Yeung, FCAS, MAAA Senior Actuary Swiss Re America Holding Corporation

Workers Compensation Exposure Rating Gerald Yeung, FCAS, MAAA Senior Actuary Swiss Re America Holding Corporation Table of Contents NCCI Excess Loss Factors 3 WCIRB Loss Elimination Ratios 7 Observations

Workers Compensation Exposure Rating Gerald Yeung, FCAS, MAAA Senior Actuary Swiss Re America Holding Corporation Table of Contents NCCI Excess Loss Factors 3 WCIRB Loss Elimination Ratios 7 Observations

SOCIETY OF ACTUARIES Introduction to Ratemaking & Reserving Exam GIIRR MORNING SESSION. Date: Wednesday, November 1, 2017 Time: 8:30 a.m. 11:45 a.m.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, November 1, 2017 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, November 1, 2017 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

GIIRR Model Solutions Fall 2015

GIIRR Model Solutions Fall 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1k) Estimate written, earned

GIIRR Model Solutions Fall 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1k) Estimate written, earned

PITTSBURGH LOGISTICS SYSTEMS(PLS PRO)CARRIER TERMS OF USE

CARRIER TERMS OF USE") PITTSBURGH LOGISTICS SYSTEMS(PLS PRO)CARRIER TERMS OF USE PLSPRO.com 1 PROVIDES A WEB SITE LOCATED ON THE INTERNET AT http://www.plspro.com (THE SITE ) TO FACILITATE TRANSPORTATION SERVICES. THROUGH THE

PITTSBURGH LOGISTICS SYSTEMS(PLS PRO)CARRIER TERMS OF USE PLSPRO.com 1 PROVIDES A WEB SITE LOCATED ON THE INTERNET AT http://www.plspro.com (THE SITE ) TO FACILITATE TRANSPORTATION SERVICES. THROUGH THE

Years ended December 31, 2017 and 2016 with Report of Independent Auditors

Audited Financial Statements Years ended December 31, 2017 and 2016 with Report of Independent Auditors Audited Financial Statements Years ended December 31, 2017 and 2016 Contents Report of Independent

Audited Financial Statements Years ended December 31, 2017 and 2016 with Report of Independent Auditors Audited Financial Statements Years ended December 31, 2017 and 2016 Contents Report of Independent

Revenue Share Purchase Agreement

Revenue Share Purchase Agreement This Investment Agreement (the "Agreement" ) is entered into between the Investor and the Issuer, as defined below. 1. Defined Terms: The terms below are defined for the

Revenue Share Purchase Agreement This Investment Agreement (the "Agreement" ) is entered into between the Investor and the Issuer, as defined below. 1. Defined Terms: The terms below are defined for the

RISK CULTURE HOW IT DRIVES EVERYTHING. David Ingram, CERA, FRM, PRM June 2014

RISK CULTURE HOW IT DRIVES EVERYTHING David Ingram, CERA, FRM, PRM June 2014 Risk Culture Who is talking about Risk Culture? Regulators & Rating Agencies Companies - GSIIs Case Study SCOR Ten Risk Culture

RISK CULTURE HOW IT DRIVES EVERYTHING David Ingram, CERA, FRM, PRM June 2014 Risk Culture Who is talking about Risk Culture? Regulators & Rating Agencies Companies - GSIIs Case Study SCOR Ten Risk Culture

Supplemental Background Material. Course CFE 3. Reinsurance. (Passing grade for this exam is 74%)

") Supplemental Background Material Course (Passing grade for this exam is 74%) Please note that this study guide is a tool for learning the materials you need to effectively study for this examination. As

Supplemental Background Material Course (Passing grade for this exam is 74%) Please note that this study guide is a tool for learning the materials you need to effectively study for this examination. As

Exam-Style Questions Relevant to the New Casualty Actuarial Society Exam 5B G. Stolyarov II, ARe, AIS Spring 2011

Exam-Style Questions Relevant to the New CAS Exam 5B - G. Stolyarov II 1 Exam-Style Questions Relevant to the New Casualty Actuarial Society Exam 5B G. Stolyarov II, ARe, AIS Spring 2011 Published under

Exam-Style Questions Relevant to the New CAS Exam 5B - G. Stolyarov II 1 Exam-Style Questions Relevant to the New Casualty Actuarial Society Exam 5B G. Stolyarov II, ARe, AIS Spring 2011 Published under

To Members of the Actuarial Committee, WCIRB Members and All Interested Parties:

Actuarial Committee Meeting Agenda Date Time Location Staff Contact April 3, 2018 9:30 AM WCIRB California David M. Bellusci 1221 Broadway, Suite 900 Oakland, CA 1221 Broadway, Suite 900 Oakland, CA 94612

Actuarial Committee Meeting Agenda Date Time Location Staff Contact April 3, 2018 9:30 AM WCIRB California David M. Bellusci 1221 Broadway, Suite 900 Oakland, CA 1221 Broadway, Suite 900 Oakland, CA 94612

The Reinsurance Placement Cycle

The Reinsurance Placement Cycle Session 507 Tuesday, June 9, 2015 1:30pm Overview Interactive session among four parties: Insurance Company Reinsurance Company Reinsurance Broker Audience Panel Members

The Reinsurance Placement Cycle Session 507 Tuesday, June 9, 2015 1:30pm Overview Interactive session among four parties: Insurance Company Reinsurance Company Reinsurance Broker Audience Panel Members

Service Level Agreement

Service Level Agreement Continental U.S.A. & Canada Updated: April 2011 Worldwide Headquarters: KEMP Technologies Inc. 12 Old Dock Road Yaphank, N Y 11980 U.S.A. EMEA Headquarters: KEMP Technologies Ltd

Service Level Agreement Continental U.S.A. & Canada Updated: April 2011 Worldwide Headquarters: KEMP Technologies Inc. 12 Old Dock Road Yaphank, N Y 11980 U.S.A. EMEA Headquarters: KEMP Technologies Ltd

ACTEX ACTEX Study Manual for Spring 2018 Edition Volume I Peter J. Murdza, Jr., FCAS David Deacon, ACAS, MAAA, CPCU, CLU, ChFC

Learn Today. Lead Tomorrow. ACTEX Study Manual for CAS Exam 5 Spring 2018 Edition Volume I Peter J. Murdza, Jr., FCAS David Deacon, ACAS, MAAA, CPCU, CLU, ChFC ACTEX Study Manual for CAS Exam 5 Spring

Learn Today. Lead Tomorrow. ACTEX Study Manual for CAS Exam 5 Spring 2018 Edition Volume I Peter J. Murdza, Jr., FCAS David Deacon, ACAS, MAAA, CPCU, CLU, ChFC ACTEX Study Manual for CAS Exam 5 Spring

Solvency II: Best Practice in Loss Reserving in Property and Casualty Insurance the foundation is critical

Solvency II: Best Practice NFT in Loss Reserving 1/2007... Solvency II: Best Practice in Loss Reserving in Property and Casualty Insurance the foundation is critical by Heike Klappach Heike Klappach heike.klappach@towersperrin.com

Solvency II: Best Practice NFT in Loss Reserving 1/2007... Solvency II: Best Practice in Loss Reserving in Property and Casualty Insurance the foundation is critical by Heike Klappach Heike Klappach heike.klappach@towersperrin.com

University of California, Los Angeles Bruin Actuarial Society Information Session. Property & Casualty Actuarial Careers

University of California, Los Angeles Bruin Actuarial Society Information Session Property & Casualty Actuarial Careers November 14, 2017 Adam Adam Hirsch, Hirsch, FCAS, FCAS, MAAA MAAA Oliver Wyman Oliver

University of California, Los Angeles Bruin Actuarial Society Information Session Property & Casualty Actuarial Careers November 14, 2017 Adam Adam Hirsch, Hirsch, FCAS, FCAS, MAAA MAAA Oliver Wyman Oliver

GLOBAL MULTI-INDEX STRATEGY AMENDMENT GLOBAL MULTI-INDEX STRATEGY

GLOBAL MULTI-INDEX STRATEGY AMENDMENT This Amendment is part of the Fixed Indexed Annuity Contract to which it is attached. All capitalized terms used in this Amendment that are not otherwise defined shall

GLOBAL MULTI-INDEX STRATEGY AMENDMENT This Amendment is part of the Fixed Indexed Annuity Contract to which it is attached. All capitalized terms used in this Amendment that are not otherwise defined shall

ECCLESIA ASSURANCE COMPANY. Financial Statements. December 31, 2010 and (With Independent Auditors Report Thereon)

") Financial Statements (With Independent Auditors Report Thereon) KPMG LLP 345 Park Avenue New York, NY 10154 Independent Auditors Report The Board of Directors Ecclesia Assurance Company: We have audited

Financial Statements (With Independent Auditors Report Thereon) KPMG LLP 345 Park Avenue New York, NY 10154 Independent Auditors Report The Board of Directors Ecclesia Assurance Company: We have audited

NEW YORK COMPENSATION INSURANCE RATING BOARD Loss Cost Revision

NEW YORK COMPENSATION INSURANCE RATING BOARD 2010 Loss Cost Revision Effective October 1, 2010 2010 New York Compensation Insurance Rating Board All rights reserved. No portion of this filing may be reproduced

NEW YORK COMPENSATION INSURANCE RATING BOARD 2010 Loss Cost Revision Effective October 1, 2010 2010 New York Compensation Insurance Rating Board All rights reserved. No portion of this filing may be reproduced

RESERVEPRO Technology to transform loss data into valuable information for insurance professionals

RESERVEPRO Technology to transform loss data into valuable information for insurance professionals Today s finance and actuarial professionals face increasing demands to better identify trends for smarter

RESERVEPRO Technology to transform loss data into valuable information for insurance professionals Today s finance and actuarial professionals face increasing demands to better identify trends for smarter

THE PITFALLS OF EXPOSURE RATING A PRACTITIONERS GUIDE

THE PITFALLS OF EXPOSURE RATING A PRACTITIONERS GUIDE June 2012 GC Analytics London Agenda Some common pitfalls The presentation of exposure data Banded limit profiles vs. banded limit/attachment profiles

THE PITFALLS OF EXPOSURE RATING A PRACTITIONERS GUIDE June 2012 GC Analytics London Agenda Some common pitfalls The presentation of exposure data Banded limit profiles vs. banded limit/attachment profiles

Ratemaking for Captives and Alternative Market Vehicles

Ratemaking for Captives and Alternative Market Vehicles Ann M. Conway, FCAS, MAAA Abstract: Although captives represent a significant part of the insurance market, there is relatively little information

Ratemaking for Captives and Alternative Market Vehicles Ann M. Conway, FCAS, MAAA Abstract: Although captives represent a significant part of the insurance market, there is relatively little information

WCIRB Actuarial Committee Meeting

W o r k e r s C o m p e n s a t i o n I n s u r a n c e R a t i n g B u r e a u o f C a l i f o r n i a WCIRB Actuarial Committee Meeting Materials Presented at the WCIRB Actuarial Committee Meeting June

W o r k e r s C o m p e n s a t i o n I n s u r a n c e R a t i n g B u r e a u o f C a l i f o r n i a WCIRB Actuarial Committee Meeting Materials Presented at the WCIRB Actuarial Committee Meeting June

Drybulk market outlook

Drybulk market outlook Have we reached the bottom? 12 th Mare Forum Shipfinance 2012 Burak Cetinok Senior Analyst Amsterdam, Baltic Dry Index THE GREAT SHIPPING CYCLE 2001-08 Growth Fleet 46% Trade 5 CHINESE

Drybulk market outlook Have we reached the bottom? 12 th Mare Forum Shipfinance 2012 Burak Cetinok Senior Analyst Amsterdam, Baltic Dry Index THE GREAT SHIPPING CYCLE 2001-08 Growth Fleet 46% Trade 5 CHINESE

ERM in the Rating Process: A Practical Perspective

ERM in the Rating Process: A Practical Perspective Jeffrey Mango, Group Vice President, A.M. Best Michelle Baurkot, Assistant Vice President, A.M. Best Tom Zitelli, Managing Senior Financial Analyst, A.M.

ERM in the Rating Process: A Practical Perspective Jeffrey Mango, Group Vice President, A.M. Best Michelle Baurkot, Assistant Vice President, A.M. Best Tom Zitelli, Managing Senior Financial Analyst, A.M.

2012 Health Care Workers Compensation Barometer

Aon Risk Solutions 2012 Health Care Workers Compensation Barometer Actuarial Analysis September 2012 Risk. Reinsurance. Human Resources. Empower Results 2012 Health Care Workers Compensation Barometer

Aon Risk Solutions 2012 Health Care Workers Compensation Barometer Actuarial Analysis September 2012 Risk. Reinsurance. Human Resources. Empower Results 2012 Health Care Workers Compensation Barometer

2011 CLRS - MPLI Reserving 101 9/15/2011

Medical Professional Liability Reserving 101 Common Reserving Techniques and Considerations 2011 Casualty Loss Reserve Seminar September 15, 2011 Kevin M. Dyke, FCAS, MAAA Michigan Office of Financial

Medical Professional Liability Reserving 101 Common Reserving Techniques and Considerations 2011 Casualty Loss Reserve Seminar September 15, 2011 Kevin M. Dyke, FCAS, MAAA Michigan Office of Financial

Article from: ARCH Proceedings

Article from: ARCH 214.1 Proceedings July 31-August 3, 213 Neil M. Bodoff, FCAS, MAAA Abstract Motivation. Excess of policy limits (XPL) losses is a phenomenon that presents challenges for the practicing

Article from: ARCH 214.1 Proceedings July 31-August 3, 213 Neil M. Bodoff, FCAS, MAAA Abstract Motivation. Excess of policy limits (XPL) losses is a phenomenon that presents challenges for the practicing

Protective Indexed Choice SM UL

Protective Indexed Choice SM UL Indexed Universal Life Insurance Product Guide Life insurance provides financial protection for your loved ones. But it also gives you flexibility and benefits that can

Protective Indexed Choice SM UL Indexed Universal Life Insurance Product Guide Life insurance provides financial protection for your loved ones. But it also gives you flexibility and benefits that can

International Practice of Calculation of Insurance Reserves and Shares of Reinsurers in Insurance Reserves for Non-life Insurance

International Practice of Calculation of Insurance Reserves and Shares of Reinsurers in Insurance Reserves for Non-life Insurance Andrey Safonov Russian Guild of Actuaries (Russia) Types of Reserves Start

International Practice of Calculation of Insurance Reserves and Shares of Reinsurers in Insurance Reserves for Non-life Insurance Andrey Safonov Russian Guild of Actuaries (Russia) Types of Reserves Start

Lindsay Grimes Marsh USA Inc.

Lindsay Grimes Vice President Marsh USA Inc. 3560 Lenox Road NE Suite 2400 Atlanta, GA 30326 Lindsay.Grimes@marsh.com Date Client Name Title Address Subject: NFIP Engagement Letter Client Name, We are

Lindsay Grimes Vice President Marsh USA Inc. 3560 Lenox Road NE Suite 2400 Atlanta, GA 30326 Lindsay.Grimes@marsh.com Date Client Name Title Address Subject: NFIP Engagement Letter Client Name, We are

Solvency II Risk Management Forecasting. Presenter(s): Peter M. Phillips

: Peter M. Phillips") Sponsored by and Solvency II Risk Management Forecasting Presenter(s): Peter M. Phillips Solvency II Risk Management Forecasting Peter M Phillips Equity Based Insurance Guarantees 2015 Nov 17, 2015 8:30

Sponsored by and Solvency II Risk Management Forecasting Presenter(s): Peter M. Phillips Solvency II Risk Management Forecasting Peter M Phillips Equity Based Insurance Guarantees 2015 Nov 17, 2015 8:30

Attachment C. Bickmore. Self- Insured Workers' Compensation Program Feasibility Study

Attachment C Bickmore Wednesday, May 21, 2014 Mr. David Wilson City of West Hollywood 8300 Santa Monica Blvd. West Hollywood, CA 90069 Re: Self- Insured Workers' Compensation Program Feasibility Study

Attachment C Bickmore Wednesday, May 21, 2014 Mr. David Wilson City of West Hollywood 8300 Santa Monica Blvd. West Hollywood, CA 90069 Re: Self- Insured Workers' Compensation Program Feasibility Study

CME Group Non-Professional Self-Certification Form & Market Data Subscription Agreement

CME Group Non-Professional Self-Certification Form & Market Data Subscription Agreement tastyworks, Inc. ("tastyworks") agrees to make "Market Data" available to you pursuant to the terms and conditions

CME Group Non-Professional Self-Certification Form & Market Data Subscription Agreement tastyworks, Inc. ("tastyworks") agrees to make "Market Data" available to you pursuant to the terms and conditions

The old Exam 6 Second Edition G. Stolyarov II,

The Actuary s Free Study GUIDE for The old Exam 6 Second Edition G. Stolyarov II, ASA, ACAS, MAAA, CPCU, ARe, ARC, API, AIS, AIE, AIAF First Edition Published in July-October 2010 Second Edition Published

The Actuary s Free Study GUIDE for The old Exam 6 Second Edition G. Stolyarov II, ASA, ACAS, MAAA, CPCU, ARe, ARC, API, AIS, AIE, AIAF First Edition Published in July-October 2010 Second Edition Published

End User Subscription Agreement. 1. Scope; Procurement and Provisioning by Affiliates; Subscription Services Users.

End User Subscription Agreement Marketo EMEA, Limited ( Marketo ) and Customer hereby agree as follows: 1. Scope; Procurement and Provisioning by Affiliates; Subscription Services Users. 1.1 Scope. This

End User Subscription Agreement Marketo EMEA, Limited ( Marketo ) and Customer hereby agree as follows: 1. Scope; Procurement and Provisioning by Affiliates; Subscription Services Users. 1.1 Scope. This

Deluxe Corporation Purchase Terms and Conditions

Deluxe Corporation Purchase Terms and Conditions The following standard purchase terms and conditions only apply to purchasing transactions (including but not limited to purchase orders) that do not have

Deluxe Corporation Purchase Terms and Conditions The following standard purchase terms and conditions only apply to purchasing transactions (including but not limited to purchase orders) that do not have

OHIO PLAN RISK MANAGEMENT, INC. Columbus, Ohio. FINANCIAL STATEMENTS December 31, 2016 and 2015

OHIO PLAN RISK MANAGEMENT, INC. Columbus, Ohio FINANCIAL STATEMENTS Columbus, Ohio FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 MANAGEMENT S DISCUSSION AND ANALYSIS (UNAUDITED)... 3

OHIO PLAN RISK MANAGEMENT, INC. Columbus, Ohio FINANCIAL STATEMENTS Columbus, Ohio FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 MANAGEMENT S DISCUSSION AND ANALYSIS (UNAUDITED)... 3

US P&C Industry Statutory Reserve Study

US P&C Industry Statutory Reserve Study Based on NAIC data through March 31, 2017 August 7, 2017 Prepared by Disclaimer This study provides directional evidence about the aggregate adequacy of industry

US P&C Industry Statutory Reserve Study Based on NAIC data through March 31, 2017 August 7, 2017 Prepared by Disclaimer This study provides directional evidence about the aggregate adequacy of industry

Solutions to the Spring 2018 CAS Exam Five

Solutions to the Spring 2018 CAS Exam Five (Only those questions on Basic Ratemaking) There were 26 questions worth 55.5 points, of which 15.5 were on ratemaking worth 29.25 points. (Question 8a covered

Solutions to the Spring 2018 CAS Exam Five (Only those questions on Basic Ratemaking) There were 26 questions worth 55.5 points, of which 15.5 were on ratemaking worth 29.25 points. (Question 8a covered

WEBSITE TERMS & CONDITIONS OF ACCESS & USE

WEBSITE TERMS & CONDITIONS OF ACCESS & USE Original Issue Date: June 2017 Approver(s): Board of Directors Owner(s): TTCM CAPITAL MARKETS LIMITED Contact Person: Chief Executive Officer Classification:

WEBSITE TERMS & CONDITIONS OF ACCESS & USE Original Issue Date: June 2017 Approver(s): Board of Directors Owner(s): TTCM CAPITAL MARKETS LIMITED Contact Person: Chief Executive Officer Classification:

Business Process Outsourcing April 27, 2010 Enrico J. Treglia

Business Process Outsourcing April 27, 2010 Enrico J. Treglia This material is informational only, and is not intended as an offer or a solicitation to buy or sell any securities or enter into any insurance,

Business Process Outsourcing April 27, 2010 Enrico J. Treglia This material is informational only, and is not intended as an offer or a solicitation to buy or sell any securities or enter into any insurance,

Loss Reserving 201 It's More than Numbers

Loss Reserving 201 It's More than Numbers Derek W. Freihaut September 17, 2015 Agenda Background/Loss Reserving 101 Key Considerations Claims Handling Reinsurance Underwriting Rates External Influences

Loss Reserving 201 It's More than Numbers Derek W. Freihaut September 17, 2015 Agenda Background/Loss Reserving 101 Key Considerations Claims Handling Reinsurance Underwriting Rates External Influences

Revised Educational Note. Premium Liabilities. Committee on Property and Casualty Insurance Financial Reporting. March 2015.

Revised Educational Note Premium Liabilities Committee on Property and Casualty Insurance Financial Reporting March 2015 Document 215017 Ce document est disponible en français 2015 Canadian Institute of

Revised Educational Note Premium Liabilities Committee on Property and Casualty Insurance Financial Reporting March 2015 Document 215017 Ce document est disponible en français 2015 Canadian Institute of

Perspectives on European vs. US Casualty Costing

Perspectives on European vs. US Casualty Costing INTMD-2 International Pricing Approaches --- Casualty, Robert K. Bender, PhD, FCAS, MAAA CAS - Antitrust Notice The Casualty Actuarial Society is committed

Perspectives on European vs. US Casualty Costing INTMD-2 International Pricing Approaches --- Casualty, Robert K. Bender, PhD, FCAS, MAAA CAS - Antitrust Notice The Casualty Actuarial Society is committed

Casualty Loss Reserve Seminar Roll-forward Reserve Estimates September 15, 2014

www.pwc.com 2014 Casualty Loss Reserve Seminar Roll-forward Reserve Estimates Mechanics Underlying Roll-forward Reserve Estimates 2 Agenda Section 1 Roll-forward Example Section 2 Potential roll-forward

www.pwc.com 2014 Casualty Loss Reserve Seminar Roll-forward Reserve Estimates Mechanics Underlying Roll-forward Reserve Estimates 2 Agenda Section 1 Roll-forward Example Section 2 Potential roll-forward

TERM OF USE. 1. General 1.1. This website is owned and operated by Vinum Pte Ltd (Vinum Fine Wines)

") 1. General 1.1. This website is owned and operated by Vinum Pte Ltd (Vinum Fine Wines) (hereinafter "Vinum"). By accessing and using any part of this website, you unconditionally agree and accept to be

1. General 1.1. This website is owned and operated by Vinum Pte Ltd (Vinum Fine Wines) (hereinafter "Vinum"). By accessing and using any part of this website, you unconditionally agree and accept to be

January 1, 2019 Pure Premium Rate Filing Summary of Actuarial Committee Recommendations Governing Committee Meeting August 8, 2018

January 1, 2019 Pure Premium Rate Filing Summary of Actuarial Committee Recommendations Governing Committee Meeting August 8, 2018 Dave Bellusci Executive Vice President & Chief Actuary ANTITRUST NOTICE

January 1, 2019 Pure Premium Rate Filing Summary of Actuarial Committee Recommendations Governing Committee Meeting August 8, 2018 Dave Bellusci Executive Vice President & Chief Actuary ANTITRUST NOTICE

RCM-2: Cost of Capital and Capital Attribution- A Primer for the Property Casualty Actuary

Moderator/Tour Guide: RCM-2: Cost of Capital and Capital Attribution- A Primer for the Property Casualty Actuary CAS Ratemaking and Product Management Seminar March 10, 2015 Robert Wolf, FCAS, CERA, MAAA,

Moderator/Tour Guide: RCM-2: Cost of Capital and Capital Attribution- A Primer for the Property Casualty Actuary CAS Ratemaking and Product Management Seminar March 10, 2015 Robert Wolf, FCAS, CERA, MAAA,

An Actuarial Model of Excess of Policy Limits Losses

by Neil Bodoff Abstract Motivation. Excess of policy limits (XPL) losses is a phenomenon that presents challenges for the practicing actuary. Method. This paper proposes using a classic actuarial framewor

by Neil Bodoff Abstract Motivation. Excess of policy limits (XPL) losses is a phenomenon that presents challenges for the practicing actuary. Method. This paper proposes using a classic actuarial framewor

Miller Insurance Services (Singapore) Pte Ltd. Terms of Business Agreement ( TOBA )

Pte Ltd. Terms of Business Agreement ( TOBA )") Miller Insurance Services (Singapore) Pte Ltd Terms of Business Agreement ( TOBA ) 1. Miller 1.1 Miller Insurance Services (Singapore) Pte Ltd (Miller Singapore) is a subsidiary of Miller Insurance Services

Miller Insurance Services (Singapore) Pte Ltd Terms of Business Agreement ( TOBA ) 1. Miller 1.1 Miller Insurance Services (Singapore) Pte Ltd (Miller Singapore) is a subsidiary of Miller Insurance Services

Actuarial Review of the Self-Insured Liability Program

Actuarial Review of the Self-Insured Liability Program Outstanding Liabilities as of June 30, 2013 and June 30, 2014 Forecast for Program Years 2013-14 and 2014-15 Presented to Mendocino County December

Actuarial Review of the Self-Insured Liability Program Outstanding Liabilities as of June 30, 2013 and June 30, 2014 Forecast for Program Years 2013-14 and 2014-15 Presented to Mendocino County December

Ground Rules. CAS Antitrust Notice. Calculating the Profit Provision. Page 1. CAS Ratemaking and Product Management Seminar - March 2014

CAS Ratemaking and Product Management Seminar - March 2014 RR-2. Risk and Return Considerations in Ratemaking-Calculating the Profit Provision Ira Robbin, PhD Ground Rules 2 The purpose of this session

CAS Ratemaking and Product Management Seminar - March 2014 RR-2. Risk and Return Considerations in Ratemaking-Calculating the Profit Provision Ira Robbin, PhD Ground Rules 2 The purpose of this session

Measuring the Importance of Seaborne Trade. IMSF Annual Meeting 2013 Selena Yan, Manager Oil & Tanker Demand London, 15 April 2013

Measuring the Importance of Seaborne Trade IMSF Annual Meeting 2013 Selena Yan, Manager Oil & Tanker Demand London, Disclaimer The material and the information (including, without limitation, any future

Measuring the Importance of Seaborne Trade IMSF Annual Meeting 2013 Selena Yan, Manager Oil & Tanker Demand London, Disclaimer The material and the information (including, without limitation, any future

CL-3: Catastrophe Modeling for Commercial Lines

CL-3: Catastrophe Modeling for Commercial Lines David Lalonde, FCAS, FCIA, MAAA Casualty Actuarial Society, Ratemaking and Product Management Seminar March 12-13, 2013 Huntington Beach, CA 2013 AIR WORLDWIDE

CL-3: Catastrophe Modeling for Commercial Lines David Lalonde, FCAS, FCIA, MAAA Casualty Actuarial Society, Ratemaking and Product Management Seminar March 12-13, 2013 Huntington Beach, CA 2013 AIR WORLDWIDE

SOCIETY OF ACTUARIES Introduction to Ratemaking & Reserving Exam GIIRR MORNING SESSION. Date: Wednesday, April 25, 2018 Time: 8:30 a.m. 11:45 a.m.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, April 25, 2018 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, April 25, 2018 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

WCIRB Report on December 31, 2013 Insurer Experience Released: April 4, 2014

Workers Compensation Insurance Rating Bureau of California WCIRB Report on December 31, 2013 Insurer Experience Released: April 4, 2014 WCIRB California 525 Market Street, Suite 800 San Francisco, CA 94105-2767

Workers Compensation Insurance Rating Bureau of California WCIRB Report on December 31, 2013 Insurer Experience Released: April 4, 2014 WCIRB California 525 Market Street, Suite 800 San Francisco, CA 94105-2767

Actuarial Review of the Self-Insured Liability & Property Program

Actuarial Review of the Self-Insured Liability & Property Program Outstanding Liabilities as of June 30, 2017 Forecast for Program Year 2017-18 Presented to Santa Clara County Schools Insurance Group March

Actuarial Review of the Self-Insured Liability & Property Program Outstanding Liabilities as of June 30, 2017 Forecast for Program Year 2017-18 Presented to Santa Clara County Schools Insurance Group March