CITY AND COUNTY OF SAN FRANCISCO UNDERSTANDING THE UNIFORM GUIDANCE & NONPROFIT UPDATE

|

|

|

- Irma Stewart

- 5 years ago

- Views:

Transcription

1 CITY AND COUNTY OF SAN FRANCISCO UNDERSTANDING THE UNIFORM GUIDANCE & NONPROFIT UPDATE

2 Agenda Understanding the Uniform Guidance Katherine V. Lai, Assurance Leader, MGO Mark Tillotson, Nonprofit Industry Leader, MGO o Background and Overview o o o Subpart D Administrative Principles Subpart E Cost Principles Subpart F Audit Requirements KATHERINE V. LAI, CPA Assurance Leader Nonprofit Update Mark Tillotson, Nonprofit Industry Leader, MGO o The State of Nonprofits o o o Audit Issues and Developments Accounting Issues and Developments NFP Financial Statements MARK TILLOTSON, CPA Nonprofit Industry Leader 2

3 3 BRIDGING THE GAP Understanding The Uniform Guidance AN OVERVIEW OF THE KEY ELEMENTS

4 Federal Expenditures 8% Other $36,327,085 8% United States Department of Agriculture $ 34,643,054 8% 8% 57% Department of Health & Human Services $238,336,537 13% Department of Homeland Security $ 52,580,122 13% 14% Total CCSF Federal Expenditures 57% 14% Department of Housing & Urban Development $58,055,972 Total Federal Expenditures: $419,942,770 4

5 5 BRIDGING THE GAP Background A VIEW FROM THE BRIDGE

6 Introducing COFAR TWO-YEAR TERM: Department of State, FY For more information visit: Department of Transportation Department of Trans-portation Office of of Management and and Budget Department Department of of Agriculture Agriculture Department of Labor Department of of Housing and Urban and Development Urban Development Council on Financial Assistance Reform Reform COFAR COFAR Department of of Education Education Department Department of of Energy Energy Department of Homeland Security Department Department of Health and of Health Human and Services Human Services 6

7 Office of Management and Budget (OMB) issued: Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards; Final Rule (Uniform Guidance) December 26, 2013 Federal Register Notice UNIFORM GUIDANCE $1000M MGOnavigator.com. 7

8 Previously A-110 A A-110 A-50 A-21 A A-21 A-102 A A-102 GUIDANCE GUIDANCE FOR FOR FEDERAL FEDERAL AWARDS A-87 A A-87 A-89A A A A-122 A A-122 A-133 A A

9 Currently SIX SUBPARTS (A-F) SUBPART A 200.XX Acronyms & Definitions SUBPART D 200.3XX Post Award Recipients SUBPART B 200.1XX General SUBPART E 200.4XX Cost Principles SUBPART C 200.2XX Pre Award - Federal SUBPART F 200.5XX Audit 9

10 Uniform Guidance SUBPART A. Acronyms and Definitions B. General Provisions C. Pre-Federal Award Requirements and Contents of Federal Awards D. Post-Federal Award Requirements E. Cost Principles F. Audit Requirements OLD CIRCULAR A. All B. All C. All D. A-110 and A-102 E. A-21, A-87, A-122 F. A-133 APPENDICES 10

11 Effective Date - Federal FEDERAL AGENCIES MUST IMPLEMENT POLICIES AND PROCEDURES BY PROMULGATING REGULATIONS TO BE EFFECTIVE BY DECEMBER 26, 2014 Accomplished with issuance of December 2014 Joint Interim Final Rule 11

12 Effective Date Non-Federal NON-FEDERAL ENTITIES WILL NEED TO IMPLEMENT THE NEW ADMINISTRATIVE REQUIREMENTS AND COST PRINCIPLES FOR ALL NEW FEDERAL AWARDS MADE ON OR AFTER DECEMBER 26, 2014, AND TO ADDITIONAL FUNDING TO EXISTING AWARDS (REFERRED TO AS FUNDING INCREMENTS) MADE AFTER THAT RULE Non-federal entities wishing to implement entity-wide systems changes to comply with the guidance on or after December 26, 2014, will not be penalized for doing so 12

13 Funding Increments UG applies to funding increments to existing awards in cases where the federal agency considers the funding increments to be an opportunity to modify the terms and conditions of the award COFAR FAQ and 13 Existing federal awards that do not receive incremental funding with new terms and conditions will continue to be governed by the terms and conditions of the federal award 13

14 Effective Date - audit AUDIT REQUIREMENTS EFFECTIVE FOR FISCAL YEARS BEGINNING ON OR AFTER DECEMBER 26, 2014 Not permitted to early implement any of the audit provisions 14

15 Complexities PLANNING CONSIDERATIONS VERY IMPORTANT THIS YEAR Several years for old funding to run out Lack of PTE information Joint Interim Final Rule Agency Final Regulations 15

DOT Department of Transportation (DOT) DOI Department of the Interior (DOI) HUD Department of Housing and Urban Development (HUD) DOJ Department of Justice (DOJ) ED Department of")

16 Multiple Federal Agency Implementation Rules NEH National Endowment for the Humanities (NEH) DOL Department of Labor (DOL) EPA Environmental Protection Agency (EPA) HHS Department of Health and Human Services (HHS) DOT Department of Transportation (DOT) DOI Department of the Interior (DOI) HUD Department of Housing and Urban Development (HUD) DOJ Department of Justice (DOJ) ED Department of Education (ED) DHS Department of Homeland Security (DHS) DOC Department of Commerce (DOC) DOJ Department of Energy (DOE) USDA United States Department of Agriculture (USDA) DOD Department of Defense (DOD) 16

17 17 BRIDGING THE GAP SUBPART D: Administrative Principles IDENTIFYING THE ROAD BLOCKS

18 Part 200 Contents Of Uniform Guidance For Federal Awards Subpart D - Post Federal Award Requirements Financial management Internal controls Bonds Payment Cost sharing and matching Program income Revision of budget and program plans Property standards Procurement standards Performance and financial monitoring and reporting Subrecipient monitoring and management Record retention and access Remedies for noncompliance Closeout 18

19 Financial Management System Must include: Identification of all federal awards received and expended and the federal programs under which they were received. Effective control over, and accountability for all funds, property, and other assets. Comparison of expenditures with budget amounts for each federal award Written procedures - cash management and allowable costs 19

20 Internal Controls Internal controls. The non-federal entity must: (a) Establish and maintain effective internal control over the Federal award that provides reasonable assurance that the non-federal entity is managing the Federal award in compliance with Federal statutes, regulations, and the terms and conditions of the Federal award. These internal controls should be in compliance with guidance in Standards for Internal Control in the Federal Government [Green Book] issued by the Comptroller General of the United States and the Internal Control Integrated Framework, issued by the Committee of Sponsoring Organizations of the Treadway Commission $1000M (COSO). 20

21 Internal Control OMB has stated that the should is meant to be a best practice and not a presumptively mandatory requirement 21

22 Payment (Cash Management) Must minimize the time elapsing between transfer of funds from the US Treasury or PTE and the disbursements Payment must be in advance when the non-federal entity: o o Has written procedures to implement the requirements of cash management, and Has a compliant financial management system If the above requirements are not met, reimbursement method is used 22

23 Budget Revisions FOR NON-CONSTRUCTION FEDERAL AWARDS, PRIOR APPROVAL IS ONLY REQUIRED FOR: Change in the scope or the objective Change in key person Disengagement from the project for more than three months or a 25% reduction in time devoted to the project Inclusion of costs that require prior approval according to Cost Principles Transfer of funds budgeted for participant support costs to other categories of expenses The subawarding, transferring or contracting out of any work under a Federal award Changes in amount of approved cost-sharing or matching *Pre-approval requirements are waived for research projects unless the federal awarding agency indicates otherwise

24 Budget Revisions Federal awarding agencies have the option to: Waive prior approval requirements, except for the change in the scope or the objective Allow the non-federal agency to incur project costs 90 days before the award date Initiate a one-time extension of the period of performance by up to 12 months Carry forward unobligated balances to subsequent periods of performance 24

25 Budget Revisions For awards that exceed the simplified acquisition threshold the federal awarding agency may restrict the transfer of funds among direct cost categories when such transfers exceeds or is expected to exceed 10% of the total budget Federal awarding agency responsibilities 25

26 Procurement New procurement standards adopt the majority of the language used from Circular 102. Therefore, non-federal entities that are currently subject to Circular A-110 will likely be affected more significantly. Type of recipients with greatest impact of new procurement guidance Higher Educational Institutions Not-for-Profit Organizations 26

27 Procurement Types 01 Micro Purchases $3,000 Aggregate - $2,000 if it is for Construction and subject to Davis-Bacon Act. There does not need to be quotations. Equitable distribution among qualified vendors 02 Small Purchases Simple and informal procurement methods Not more than the simplified acquisition threshold - currently $150,000 Price and rate quotations must be obtained from adequate number of qualified sources. 03 Sealed Bids Above simplified threshold greater than $150,000 Preferred for construction projects Must be publicly advertised 04 Competitive Proposals Above simplified threshold currently $150,000 More than one source for proposal Usually used for fixed fee or cost reimbursement A written method of evaluation and selection. Award must go to most advantageous proposal 05 Must meet at least one of Sole Source the criteria: Single source availability Public emergency Written request has been made and approved by federal or PTE Competition is determined to be inadequate 27

28 FAQ states, for compliance with the new procurement standards only, the federal government is providing a grace period of one full fiscal year after the effective date of the Uniform Guidance for Federal Awards. DEFINITIONS Procurement Grace Period $1000M 28

29 Subrecipient A non-federal entity that receives a subaward from a PTE to carry out part of a Federal program; but does not include an individual that is a beneficiary of such program. (section ) DEFINITIONS Subrecipient $1000M 29

30 Contractor* An entity that receives a contract, i.e. a legal instrument by which a non-federal entity purchases property or services needed to carry out the project or program under a Federal award. (section ) *Contractor replaces the term Vendor from OMB Circular A-133. DEFINITIONS Contractor $1000M 30

31 Requirements for Pass-Through Entities Subaward Information 1 6 Consider Enforcement Action Evaluate Subrecipient Risk of Non- Compliance 2 REQUIREMENTS FOR PASS-THROUGH ENTITIES 5 Review Results of Monitoring Review Subrecipient Audit Reports 4 Determine Appropriate Monitoring 3 31

32 Subaward Information Federal Award Identification must include: o Subrecipient name o Subrecipient s unique entity identifier o Federal award identification number (FAIN) o Federal award date o Subaward period of performance o Amount of federal funds obligated by the action o Total amount of federal funds obligated to the subrecipient o Total amount of the federal award o Federal award project description o Name of the federal awarding agency, PTE, and contact information for awarding official o CFDA number and name o Whether the award is R&D o Indirect cost rate for the federal award 32

33 Subaward Information Subaward agreement must include: Additional PTE requirements Allow PTE auditors access to subrecipient records Indirect cost rate Closeout procedures 33

34 Evaluate Risk Of Subrecipient Noncompliance Consider: Subrecipient prior experience with the same or similar subawards; Results of previous audits, Whether subrecipient has new personnel or substantially changed systems; and Extent and results of Federal awarding agency monitoring. 34

35 Required Subrecipient Monitoring Activities Review financial and programmatic reports Follow-up and ensure that the subrecipient takes timely and appropriate action on all deficiencies pertaining to the federal award through audits, onsite reviews, and other means Issue management decisions for audit findings pertaining to the federal award provided to the subrecipient 35

36 Potential PTE Monitoring Tools Consider tools that may be useful for the PTE to monitor subrecipients: Providing training and technical assistance Performing on-site reviews of program operations Arranging for agreed-upon procedures (AUP) engagements 36

37 Review Subrecipient Audit Reports Verify every subrecipient is audited as required by Subpart F Audit Requirements and consider: Size of the award Percentage of award vs. total federal awards received by the agency Audit findings internal control and/or compliance Corrective action plan 37

38 Review Monitoring Results Upon conclusion of all monitoring, consider any impact on PTE records. Document the execution of monitoring activities and corrective action taken. 38

39 Consider Enforcement Action If noncompliance cannot be remedied, the PTE may take one or more of the following actions, as appropriate: Temporarily withhold cash payments Disallow all or part of cost of the activity not in compliance Wholly or partly suspend or terminate the federal award Recommend that the federal agency initiate suspension and debarment proceedings Withhold further federal awards Take other remedies that may be legally available 39

40 40 BRIDGING THE GAP SUBPART E: Cost Principles PAYING THE TOLL

41 Cost Principles with Little Or No Change: 424 Alumni(ae) activities 425 Audit services 426 Bad Debts 423 Alcoholic beverages 421 Advertising and public relations Little or No Change 429 Commencement and convocation costs 445 Goods and services for personal use 41

42 Cost Principles with Little or No Change: 450 Lobbying Little or No Change 458 Pre-award costs 455 Organization costs 457 Plant and security costs 459 Processional service costs 467 Selling and marketing costs 469 Student activity costs 42

43 Cost Principles with Changes: 431 Compensation Fringe benefits 433 Contingency provisions 434 Contributions and donations 430 Compensation personal services 436 Depreciation 427 Bonding Costs Little or No Change 437 Employee health and welfare costs 43

44 Cost Principles With Changes: Little or No Change 439 Equipment and other capital expenditures 453 Materials and supplies costs, including costs of computing devices 441 Fines, penalties, damages and other settlements 454 Memberships, subscriptions, and professional activity costs 449 Interest 467 Selling and marketing costs 447 Insurance and indemnification 44

45 Cost Principles With Changes: 474 Travel Costs 461 Publication and printing costs 462 Rearrangement and reconversion costs 472 Training and education Costs 463 Recruiting costs With WITH CHANGES Changes 471 Termination costs 464 Relocation Cost of employees 470 Taxes (including Value Added Taxes) 468 Specialized service facilities 465 Rental costs of real property and equipment 45

46 Compensation Personal Services: Purpose was to reduce the administrative burden of documenting time and effort More principles based Less prescriptive on documentation and places more emphasis on internal controls over personnel-related costs 46

47 Compensation Personal Services: FOUR STANDARDS FOR DOCUMENTATION OF PERSONNEL EXPENSES Charges for salaries must be based on records that accurately reflect the work performed Must be supported by a system of internal controls which provides reasonable assurances the amounts charged are accurate, allowable and properly allocated Be incorporated into official records Reasonably reflect total activity for which employees is compensated 47

48 Depreciation Use allowance no longer allowed No depreciation on assets that are fully depreciated New: depreciation over life of the asset 48

49 Equipment And Other Capital Expenditures Computing devices do not meet the threshold requirements so are considered supplies o Tablets o Laptops o Smart phones Lesser of $5,000 or entity capitalization threshold Revisit policy if below this amount 49

50 Proposal Costs Allowable as an indirect cost o Preparing proposals for both Federal and non- Federal o Successful and not successful bids o Allocated to all activities of the organization This was in college and university and government cost circular, but not NFP 50

51 Required Certifications Subpart E Similar in A-87 but not A-21 or A-122 Certification on annual and final fiscal reports or vouchers requesting payment o Assurance that expenditures are proper and in accordance with the terms and conditions of the federal award and approved budget Require on EVERY voucher requesting payment? Does this apply to drawdowns also? 51

52 Required Certifications Subpart E Signed by an official who is authorized to legally bind the entity o Who will be designated at the organization? o CFO? CEO? o Organizations should start thinking about this Subject to criminal, civil or administrative penalties for fraud, false statements or false claims 52

53 INDIRECT COST REIMBURSEMENT 53

54 F&A Rate Changes Indirect (F&A) Costs (c) Federal Agency Acceptance of Negotiated Indirect Cost Rates o o o The negotiated rates must be accepted by all federal agencies A Federal agency may use a rate different from the negotiated rate for a class of federal awards or a single federal award only when required by federal statute or regulation, or when approved by a federal agency head or delegate based on documented justification Agencies must notify OMB of any exceptions approved by the agency head 54

55 F&A Rate Changes Indirect (F&A) Costs (f) Any non-federal entity that has never received a negotiated indirect cost rate, except for those non-federal entities described in Appendix VII to part 200 o o o May elect to charge a de minimis rate of 10% of Modified Total Direct Costs (MTDC) which may be used indefinitely As described in factors affecting allowability of costs, costs must be consistently charged as either indirect or direct costs, but may not be double charged or inconsistently charged as both If chosen, this methodology once elected must be used consistently for all federal awards until such time as a non-federal entity chooses to negotiate for a rate, which the non-federal entity may apply to do at any time 55

56 F&A Rate Changes Indirect (F&A) Costs o All Pass-through entities must: o o o May elect to charge a de minimis rate of 10% of Modified Total Direct Costs (MTDC) which may be used indefinitely As described in factors affecting allowability of costs, costs must be consistently charged as either indirect or directs costs, but may not be double charged or inconsistently charged as both If chosen, this methodology once elected must be used consistently for all federal awards until such time as a non-federal entity chooses to negotiate for a rate, which the non-federal entity may apply to do at any time 56

57 Requirement for Pass-through Entities Pass-through entities must Ensure that every subaward is clearly identified to the subricipient as a subaward and includes the following information at the time of the subaward and if any of these data elements change, include the changes in the subsequent subaward modification. When some of this information is not available, the pass-through entity must provide the best information available to describe the Federal award and subaward. Required information includes: o (xiii) Indirect cost rate for the Federal Award (Including if the de minimis rate is charged per Indirect (F&A) costs) An approved federally recognized indirect cost rate negotiated between the subricipient and the Federal Government or, pass-through entity and the subrecipient (in compliance with this part), or a de minimis indirect cost rate as defined in Indirect (F&A) costs, paragraph (f) 57

58 MTDC Defined Modified Total Direct Cost (MTDC) MTDC means all direct salaries and wages, applicable fringe benefits, materials and supplies, services, travel, and up to the first $25,000 of each subaward (regardless of the period of performance of the subawards under the award) MTDC excludes equipment, capital expenditures, charges for patient care, rental costs, tuition remission, scholarships and fellowships, participant support costs and the portion of each subawards in excess of $25,000 Other items may only be excluded when necessary to avoid a serious inequity in the distribution of indirect costs, and with the approval of the cognizant agency for indirect costs 58

59 MTDC Example Simple Example of one project s MTDC: Total Direct costs in our Budget: $160,000 Salaries/benefits $ 95,000 Supplies 5,000 Subaward A 25,000 Subaward B 20,000 Capital Equipment 10,000 Participant Support Costs 5,000 Modified Total Direct Costs: = $160,000 - $10,000 - $20,000 - $5,000 = $125,000 MTDC * 10% = $12,500 (IDC) 59

60 F&A Rate Changes Indirect (F&A) Costs (g) Allows a one-time extension of Federally negotiated F&A rates for up to four years o Subject to reviews and approval of the cognizant agency for indirect costs o If an extension is granted the non-federal entity may not request a rate review until the extension period ends o At the end of the 4-year extension, the non-federal entity must negotiate a new rate o Subsequent one-time extensions (up to four years) are permitted if a renegotiation is completed between each extension request 60

61 Frequently Asked Questions Question: Pass through entities are expected to honor a subrecipient s negotiated F&A rate agreement, or use a 10% MTDC de minimis rate, or negotiate an F&A rate with the subrecipient. Is it acceptable to require a subrecipient to accept a rate lower than 10% MTDC via negotiation, or in lieu of their negotiated F&A rate? If the subrecipient requests to establish a rate via negotiation, does the pass through entity have to establish the rate via negotiation? Answer: If the subrecipient already as a negotiated F&A rate with the federal government, the negotiated rate must be used. It is not permissible for pass through entities to force or entice a subrecipient without a negotiated rate to accept less than the de minimis rate. 61

62 Frequently Asked Questions Question: What should I do if my pass through entity won t honor my entity s federally negotiated indirect cost rate agreement? Answer: You may wish to remind your pass though entity of their obligation under the uniform guidance in part (basically they are required to accept the negotiated rate). 62

63 63 BRIDGING THE GAP SUBPART F: Audit Requirements NAVIGATING THE AUDIT

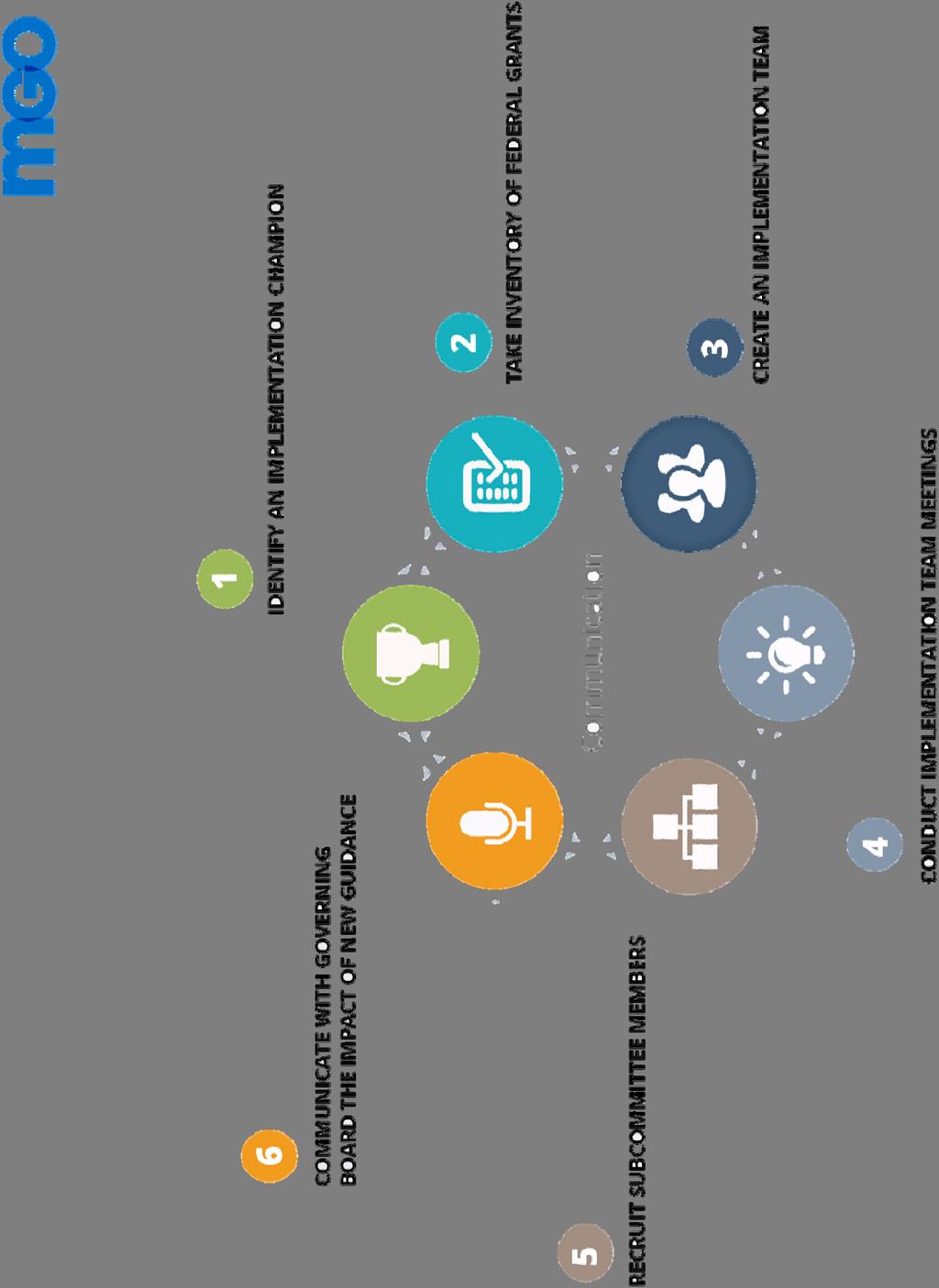

64 Overview Increases audit threshold from $500,000 to $750,000 Strengthens risk-based approach to determine Major Programs Greater transparency of audit results Focuses on compliance requirements of highest risk 64

65 Bridging the Gap Type A Threshold TYPE A THRESHOLD TOTAL FEDERAL AWARDS EXPENDED (FAE) $750,000 Equal to $750,000 but less than or equal to $25M Total FAE times.03 Exceed $25M but less than or equal to $100M $3,000,000 Exceed $100M but less than or equal to $1B Total FAE times.003 Exceed $1B but less than or equal to $10B $30M Exceed $10B but less than or equal to $20B Total FAE times.0015 Exceed $20B

66 Bridging The Gap High Risk Type A Assessments OMB CIRCULAR A-133, SECTION.520 (C ) FISCAL YEAR 2015 UNIFORM GRANT GUIDANCE, SECTION FISCAL YEAR 2016 Not audited as a major program in 1 of the 2 most recent audit periods Same In the most recent audit period had the following findings: A modified opinion on the program in the auditor's report on major programs. Material compliance finding Material Weakness in internal controls over direct and material compliance requirements Significant Deficiency in internal controls over direct and material compliance requirements Same Not applicable Other auditor judgment (i.e. current and prior audit experience, Federal agency oversight, Inherent risk of the program) Same Known or likely questioned costs exceeding 5% of the total program expenditures

67 Type B Risk Assessments Options OMB CIRCULAR A-133, SECTION.520 (D) Fiscal Year Beginning Before December 26, 2014 OPTION 1 OPTION 2 Perform risk assessments on all Type B programs and select at least 50% of Type B programs identified as high risk up to number of low-risk Type A programs Perform risk assessments on all Type B programs until as many high-risk type b programs have been identified as there are low-risk Type A programs. UNIFORM GRANT GUIDANCE, SECTION Fiscal Year Beginning on or After December 26, 2014 REQUIREMENT Perform risk assessments on Type B programs until high-risk Type B programs have been identified up to at least 25% of the number of low-risk Type A programs.

68 Percentage of Coverage Section (f) Percentage of Coverage Guidance reduces the minimum coverage as follows: Type of Auditee Current New Not low-risk 50% 40% Low-risk 25% 20% * If auditee voluntarily prepares financial statements on a non-gaap basis of accounting (e.g., cash or modified cash), auditee cannot be considered low-risk auditee 68

69 Schedule of Expenditures of Federal Awards Total amount provided to subrecipients from each federal program: o Previous guidance only required to the extent practical Federal Grantor/Pass Through Grantor/Program Title Federal CFDA Number Pass Through Entity Identifying Number Federal Expenditures Expenditures to Subrecipients Department of Education Direct Program Title I Grants to Local Educational Agencies N/A $1,000,000 $800,000 69

70 Audit Findings Section Audit Findings Increases the threshold for reporting known and likely questioned costs from $10,000 to $25,000 Requires that questioned costs be identified by CFDA number and applicable award number Requires identification of whether audit finding is a repeat from the immediately prior audit and if so the prior year audit finding number Provides that audit finding numbers be in the format prescribed by the data collection form 70

71 Single Audit Reports On The Web All auditees must submit the reporting package and the DCF electronically to the FAC Subrecipient only required to submit report to FAC and no longer required to submit to pass-through entity Auditors and auditees must ensure reports do not include PPII o Auditee will have to sign certification statement that reporting package does not include PPII 71

72 Implementation Roadmap 72

73 73 BRIDGING THE GAP Nonprofit Update THE STATE OF NONPROFITS

74 Current Economy Important Considerations Key Economic Indicators 74

75 State of NFPs NFPs continue to play a large role in the world economy Currently more than 1.6 million NFPs register with the IRS Contributions to NFP s in 2013 exceeded $335 billion Total revenues in sector exceeded $2 trillion 25.4% of US population (approximately 62 million people) volunteered at a NFP 75

76 Governance & Accountability What are our risks? How do we know? What are we doing about them? How can we take advantage of the risks to enhance our performance? 76

77 Governance & Accountability Enterprise risk management is a process, effected by an entity s board of directors, management and other personnel, applied in strategy setting and across the enterprise, designed to identify potential events that may affect the entity, and manage risk to be within its risk appetite, to provide reasonable assurance regarding the achievement of entity objectives. - Committee of Sponsoring Organizations of the Treadway Commission (COSO) 77

78 Governance & Accountability Enterprise Risk Management Organizational Culture that embraces all employees collective responsibility for risk management Beyond risk identification Foundational Elements While 45% of public companies reported having an ERM protocol in place, only 12% of NFPs 5 Stage of ERM Adoption 78

79 Measuring the Effectiveness of NFPS Reporting trends of leading-edge NFPs include: Fact sheets about how and why and NFP s program is effective, descriptions of key components of an NFP s program model, and summary results from evaluations External third party studies of an NFP s work, including quantifying results from single or multi-year evaluations Visual illustration of NFP s Theory of Change, displaying how an NFP approaches its programmatic work Enhanced impact information included within an NFP s ongoing, required reporting 79

80 Donor-advised Funds A donor-advised fund is a charitable giving vehicle that a donor establishes with a section 501(c)(3) organization (the recipient organization), such as a community foundation or university In order to receive that tax deduction, the donor must grant variance power over the donated assets to the recipient organization. Variance power is the unilateral power to redirect the use of the transferred assets to another beneficiary 80

81 Cyber Security As technologies advance and NFPs become more sophisticated in using them, sensitive data that is stored internally or transmitted across networks becomes more vulnerable While resources at NFPs may be limited, the costs of dealing with breach can be high. A breach can expose the organization to steep fines as well as litigation and remediation expenses NFPs should consider putting policies and process in place to manage data privacy and security 81

82 Generally Accepted Privacy Principles GAPP is designed to assist management in creating an effective privacy program that addresses their privacy obligations, risks, and business opportunities The privacy principles and criteria are founded on key concepts from significant local, national, and international privacy laws, regulations, guidelines, and good business practices 82

83 Socially Responsible Investing Socially responsible investing (SRI) also known as sustainable, socially conscious, green, ethical, or values-based investing is an investment strategy that continues to get attention by organizations as well as their boards and supporters SRI has a goal of aligning corporate ethics with investments strategies related to the environment, consumer protection, human rights, and other social stewardship concerns The three common approaches to SRI are as follows: Negative screen Positive screen Restricted screens 83

84 Crowd Funding NFP Fund-raising Trends Social Media o Twitter, Facebook & Blogs o Need to consider donor base who do not use/own smartphone Crowd Funding o Accountability/Controls o Joint Cost Allocation 84

85 AUDIT ISSUES AND DEVELOPMENTS

86 The AICPA Enhancing Audit Quality Initiative The AICPA has embarked on a far-reaching effort to help reinforce CPAs commitment to quality The goal is to align the objectives of all auditrelated AICPA efforts to continue improving audit performance 86

87 COSO s Updated Internal Control Integrated Framework Originally issued in 1992 Recognized as leading guidance for designing, implementing, and conducting a system of internal control Auditors use in analyzing entities internal control 87

88 Original 1992 Framework Defined Internal Control Internal control is a process, effected by an entity s board of directors, management and other personnel, designed to provide reasonable assurance regarding the achievement of objectives in the following categories: o Effectiveness and efficiency of operations o o Reliability of financial reporting Compliance with applicable laws and regulations 5 Interrelated Components 1. Control environment 2. Risk assessment 3. Control activities 4. Information & communication 5. Monitoring 88

89 Updated Framework Issued In 2013 Defined Internal Control What didn t change Enhancements/clarifications Old framework transitioned out 12/15/2014 Applying the 2013 framework o NFPs o Auditors 89

90 Other Audit And Attestation Issues And Developments Investment Policy Impact on the Audit UPMIFA and Endowment Spending Policies o UPMIFA and the Rule of Prudence Spending Policies Auditing Endowments Auditing Donor Intent Auditing Contributions Auditing Agency Transactions Change in Donor Intent Construction Fraud Schemes Auditing Reporting on Forms Prescribed by Regulators Clarification and Recodification of Statements on Standards for Accounting and Review Services 90

91 ACCOUNTING ISSUES AND DEVELOPMENTS

92 Revenue From Contracts With Customers New revenue recognition model replaces virtually all existing revenue guidance Impacts public, private and NFP entities New qualitative and quantitative disclosure requirements Based on the core principle that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods and services 92

93 Revenue From Contracts With Customers Comprehensive framework for determining how much revenue to recognize and when it should be recognized 5 step approach to revenue recognition: 01 Step 1 Step 2 Identify the contract with a Determine the customer transaction price Step 3 Step 4 Determine the transaction Allocate the transaction price price Step 5 Recognize revenue when or as the entity satisfies performance obligation 93

94 NFP FINANCIAL STATEMENTS

95 NFP Financial Statement Model Last overhauled approximately 20 years ago o FAS 117 (now codified within Topic 958 of the ASC) FAS 117 represented significant change from previous guidance o Significant differences across the sector o Significant differences from business entities FAS 117 kept at a somewhat high level, with expectation that guidance would evolve in certain areas (e.g., operating measure) o Has happened, but only to a certain degree 95

96 NFP Financial Statements Project Key Objectives Recommended by FASB s NFP Advisory Committee (NAC) Refresh, not overhaul, the current model Improve net asset classification scheme Improve information in financial statements and notes about: o Liquidity o Financial performance o Cash flows Better enable NFPs to tell their financial story 96

97 Financial Statements of NFPs Net Asset Classification Liquidity information Financial Performance: Operating Measure/Activities Statement Format Reporting of Expenses Cash Flow Statements NFP Note Disclosures 97

98 Questions? Let s Talk.

99 UNIFORM GUIDANCE Navigator o Enhanced Search & Navigation o Quick Links to Major Sections o Mobile Device Optimized o Additional Resources o Implementation Roadmap o Frequently-Asked-Questions o COFAR Training Webcasts 99

SINGLE AUDIT UPDATE. Presented By Joel Knopp, CPA

SINGLE AUDIT UPDATE Presented By Joel Knopp, CPA Session Covers Uniform Guidance Circular Components Single Audit Changes Auditee and Auditor Impact Scope of Audit under Uniform Guidance Florida Single

SINGLE AUDIT UPDATE Presented By Joel Knopp, CPA Session Covers Uniform Guidance Circular Components Single Audit Changes Auditee and Auditor Impact Scope of Audit under Uniform Guidance Florida Single

Uniform Guidance. Diane E. Edelstein, CPA. Sources

Uniform Guidance August 29, 2016 Central KY Chapter of AGA Diane E. Edelstein, CPA Diane is a partner at Maher Duessel, a regional firm in Pennsylvania. Diane has over 25 years of experience with auditing

Uniform Guidance August 29, 2016 Central KY Chapter of AGA Diane E. Edelstein, CPA Diane is a partner at Maher Duessel, a regional firm in Pennsylvania. Diane has over 25 years of experience with auditing

Amy Roberts, Appalachian State University

Amy Roberts, Appalachian State University Originally referred to as A-81, the Super Circular, or the Omni Circular Consolidates 8 previous Circulars All Federal funding agencies are required to implement

Amy Roberts, Appalachian State University Originally referred to as A-81, the Super Circular, or the Omni Circular Consolidates 8 previous Circulars All Federal funding agencies are required to implement

The Basics of F&A and How the Uniform Guidance Impacts Indirect Costs

The Basics of F&A and How the Uniform Guidance Impacts Indirect Costs Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Indirect Costs / Facilities and Admistrative Cost

The Basics of F&A and How the Uniform Guidance Impacts Indirect Costs Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Indirect Costs / Facilities and Admistrative Cost

Illinois Coalition Against Domestic Violence. Understanding the Uniform Guidance and Indirect Cost Rate March 16, 2016

Illinois Coalition Against Domestic Violence Understanding the Uniform Guidance and Indirect Cost Rate March 16, 2016 1 Understanding the Uniform Guidance and Indirect Cost Rate Presented by: Teri L. Taylor,

Illinois Coalition Against Domestic Violence Understanding the Uniform Guidance and Indirect Cost Rate March 16, 2016 1 Understanding the Uniform Guidance and Indirect Cost Rate Presented by: Teri L. Taylor,

Nonprofit Financial Management Network

August 14, 2015 1 Nonprofit Financial Management Network Gregory Demetriades, CPA CFO, Community Partners David J. Thomas, CPA, CGMA Managing Partner, 2 1 8:30am-9:00am Registration & Breakfast 9:00am-9:10am

August 14, 2015 1 Nonprofit Financial Management Network Gregory Demetriades, CPA CFO, Community Partners David J. Thomas, CPA, CGMA Managing Partner, 2 1 8:30am-9:00am Registration & Breakfast 9:00am-9:10am

Indirect Cost Rates A Non-Profit Perspective. Alex Weekes Principal ML Weekes & Company, PC

Indirect Cost Rates A Non-Profit Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Old School versus new regulations Review of 2CFR 200 (not so new

Indirect Cost Rates A Non-Profit Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Old School versus new regulations Review of 2CFR 200 (not so new

2017 Single Audit Update

2017 Single Audit Update July 25, 2017 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Outline Components of a Single

2017 Single Audit Update July 25, 2017 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Outline Components of a Single

Uniform Guidance for Federal Awards Key Changes and Lessons

Uniform Guidance for Federal Awards Key Changes and Lessons Learned Kinman Tong, Senior Manager Moss Adams LLP 1 PRESENTER Kinman Tong, Senior Manager Kinman has been in public accounting since 2003. He

Uniform Guidance for Federal Awards Key Changes and Lessons Learned Kinman Tong, Senior Manager Moss Adams LLP 1 PRESENTER Kinman Tong, Senior Manager Kinman has been in public accounting since 2003. He

10/30/2015 OBJECTIVES. CPAs & ADVISORS. Present an overview of the Super Circular. Contents of the Super Circular. Discuss Administrative Requirements

CPAs & ADVISORS experience direction // 2 CFR 200 UNIFORM GRANT GUIDANCE Presented by Andy Richards, CPA, Partner October 30, 2015 OBJECTIVES Present an overview of the Super Circular Contents of the Super

CPAs & ADVISORS experience direction // 2 CFR 200 UNIFORM GRANT GUIDANCE Presented by Andy Richards, CPA, Partner October 30, 2015 OBJECTIVES Present an overview of the Super Circular Contents of the Super

2 CFR 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR. Kirsten Rigg

2 CFR 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Kirsten Rigg WYDOT Internal Review 307-777-4252 kirsten.rigg@wyo.gov TRAINING OBJECTIVES Background

2 CFR 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Kirsten Rigg WYDOT Internal Review 307-777-4252 kirsten.rigg@wyo.gov TRAINING OBJECTIVES Background

2 CFR 215 (A-110) or 2 CFR 230 (A-122) Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards.

or 2 CFR 230 (A-122) Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards.") Significant Changes for Selected Items of Cost Office of Management and Budget Guidance PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Item of

Significant Changes for Selected Items of Cost Office of Management and Budget Guidance PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Item of

2018 Single Audit Update

2018 Single Audit Update July 24, 2018 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Outline Components of a Single

2018 Single Audit Update July 24, 2018 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Outline Components of a Single

Single Audit Fundamentals Part 3: Understanding and Testing Compliance Requirements and Related Internal Control over Compliance

Governmental Audit Quality Center Single Audit Fundamentals Part 3: Understanding and Testing Compliance Requirements and Related Internal Control over Compliance A Governmental Audit Quality Center Web

Governmental Audit Quality Center Single Audit Fundamentals Part 3: Understanding and Testing Compliance Requirements and Related Internal Control over Compliance A Governmental Audit Quality Center Web

Uniform Guidance Update

National Head Start Association 44 th Annual Head Start Conference and Expo April 7 10, 2017 Nashville, TN Hyatt Regency Chicago Uniform Guidance Update Sunday, April 9, 2017 4:00 pm 5:00 pm Presented

National Head Start Association 44 th Annual Head Start Conference and Expo April 7 10, 2017 Nashville, TN Hyatt Regency Chicago Uniform Guidance Update Sunday, April 9, 2017 4:00 pm 5:00 pm Presented

Do You Get Federal Funds? Find out What s Changing with Uniform Guidance

Minnesota Council of Nonprofits 2015 MCN Annual Conference October 1 2, 2015 St. Paul, MN St. Paul RiverCentre Find out What s Changing with Uniform Guidance Thursday, October 1, 2015 3:45 pm 5:00 pm Presented

Minnesota Council of Nonprofits 2015 MCN Annual Conference October 1 2, 2015 St. Paul, MN St. Paul RiverCentre Find out What s Changing with Uniform Guidance Thursday, October 1, 2015 3:45 pm 5:00 pm Presented

PART 3 COMPLIANCE REQUIREMENTS

PART 3 COMPLIANCE REQUIREMENTS INTRODUCTION The objectives of most compliance requirements for Federal programs administered by States, local governments, Indian tribal governments, and non-profit organizations

PART 3 COMPLIANCE REQUIREMENTS INTRODUCTION The objectives of most compliance requirements for Federal programs administered by States, local governments, Indian tribal governments, and non-profit organizations

Uniform Guidance Overview

Compliance Auditing Update NC Local Government Auditing, Reporting and Review June 14, 2016 Uniform Guidance Overview Course Objectives-Uniform Administrative Requirements, Cost Principles, and Audit Requirements

Compliance Auditing Update NC Local Government Auditing, Reporting and Review June 14, 2016 Uniform Guidance Overview Course Objectives-Uniform Administrative Requirements, Cost Principles, and Audit Requirements

How to Prepare for The New EDGAR Auditing Requirements Tiffany R. Winters, Esq. Brustein & Manasevit April 2015

Listen to audio overview here: https://meetny.webex.com/meetny/lsr.php?rcid=e28880f578fc4958b34178599f485530 How to Prepare for The New EDGAR Auditing Requirements Tiffany R. Winters, Esq. Brustein & Manasevit

Listen to audio overview here: https://meetny.webex.com/meetny/lsr.php?rcid=e28880f578fc4958b34178599f485530 How to Prepare for The New EDGAR Auditing Requirements Tiffany R. Winters, Esq. Brustein & Manasevit

Frequently Asked Questions

Frequently Asked Questions Updated: July 2017 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200 The

Frequently Asked Questions Updated: July 2017 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200 The

Uniform Grant Guidance Policies & Procedures

Guidance related to the uniform grant guidance can be found in Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards: CFR 200 Full Text - ecfr Code of

Guidance related to the uniform grant guidance can be found in Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards: CFR 200 Full Text - ecfr Code of

SuperCircular and Budget and Accounting PIN

SuperCircular and Budget and Accounting PIN Presented by: Gil Bernhard, CPA October 31, 2015 HMA Overview New Federal Grants Management Requirements OMB SuperCircular Budget and Accounting PIN 2 New Federal

SuperCircular and Budget and Accounting PIN Presented by: Gil Bernhard, CPA October 31, 2015 HMA Overview New Federal Grants Management Requirements OMB SuperCircular Budget and Accounting PIN 2 New Federal

OMB. Uniform Guidance

2014 OMB Uniform Guidance Assessing the OMB Uniform Guidance: Major Changes and Impacts The Office of Management and Budget (OMB) consolidated the federal government s guidance on Uniform Administrative

2014 OMB Uniform Guidance Assessing the OMB Uniform Guidance: Major Changes and Impacts The Office of Management and Budget (OMB) consolidated the federal government s guidance on Uniform Administrative

Accounting and Auditing Update. Nick D. Lombardo

Accounting and Auditing Update Nick D. Lombardo Agenda ASU 2014-09: Revenue from Contracts with Customers Leases Other Highlights Recently issued/newly effective ASUs Other projects/initiatives of interest

Accounting and Auditing Update Nick D. Lombardo Agenda ASU 2014-09: Revenue from Contracts with Customers Leases Other Highlights Recently issued/newly effective ASUs Other projects/initiatives of interest

Initial COGR observations on definitions are intertwined with the applicable sections below.

COGR Preliminary Assessment of Selected Items OMB Uniform Administrative Requirements, Cost Principles, and Administrative Requirements for Federal Awards January 14, 2014 Below is COGR s preliminary assessment

COGR Preliminary Assessment of Selected Items OMB Uniform Administrative Requirements, Cost Principles, and Administrative Requirements for Federal Awards January 14, 2014 Below is COGR s preliminary assessment

COGR Guide to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards VERSION 2: SEPTEMBER 17, 2014

COGR Guide to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards VERSION 2: SEPTEMBER 17, 2014 Introduction The OMB Uniform Administrative Requirements,

COGR Guide to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards VERSION 2: SEPTEMBER 17, 2014 Introduction The OMB Uniform Administrative Requirements,

PART 3 COMPLIANCE REQUIREMENTS

PART 3 COMPLIANCE REQUIREMENTS INTRODUCTION Overview The objectives of most compliance requirements for Federal programs administered by States, local governments, Indian tribes, institutions of higher

PART 3 COMPLIANCE REQUIREMENTS INTRODUCTION Overview The objectives of most compliance requirements for Federal programs administered by States, local governments, Indian tribes, institutions of higher

10 Frequently Asked Questions on Indirect Costs

1 10 Frequently Asked Questions on Indirect Costs Bonnie Graham, Esq. bgraham@bruman.com (202) 965-3652 www.bruman.com First, some background 2 Total Cost of Federal Awards Indirect 10% Direct Indirect

1 10 Frequently Asked Questions on Indirect Costs Bonnie Graham, Esq. bgraham@bruman.com (202) 965-3652 www.bruman.com First, some background 2 Total Cost of Federal Awards Indirect 10% Direct Indirect

Basics of F&A: A University Perspective. Alex Weekes Principal ML Weekes & Company, PC

Basics of F&A: A University Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Accountant s reconciliation of the old to new rules Overview of F&A General

Basics of F&A: A University Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Accountant s reconciliation of the old to new rules Overview of F&A General

Uniform Guidance. Jeremy Dunn. Senior Manager November 4, Elliott Davis Decosimo, LLC Elliott Davis Decosimo, PLLC

Uniform Guidance Jeremy Dunn Senior Manager November 4, 2015 This material was used by Elliott Davis Decosimo during an oral presentation; it is not a complete record of the discussion. This presentation

Uniform Guidance Jeremy Dunn Senior Manager November 4, 2015 This material was used by Elliott Davis Decosimo during an oral presentation; it is not a complete record of the discussion. This presentation

The COGR Perspective on the OMB Uniform Guidance: A First Look

The COGR Perspective on the OMB Uniform Guidance: A First Look COGR Meeting Thursday, February 27, 2014 Washington Marriott Hotel Washington, D.C. Agenda for this Session The Big Picture and the Next 12

The COGR Perspective on the OMB Uniform Guidance: A First Look COGR Meeting Thursday, February 27, 2014 Washington Marriott Hotel Washington, D.C. Agenda for this Session The Big Picture and the Next 12

STATE AND FEDERAL REVENUE SOURCES

STATE AND REVENUE SOURCES PERKINS GRANTS RETIREMENT CONTRIBUTIONS ADMINISTRATION OF AWARDS Except as provided in 20 U.S.C. 2352(b) and (c) and 20 U.S.C. 2353, each eligible agency, including the Coordinating

STATE AND REVENUE SOURCES PERKINS GRANTS RETIREMENT CONTRIBUTIONS ADMINISTRATION OF AWARDS Except as provided in 20 U.S.C. 2352(b) and (c) and 20 U.S.C. 2353, each eligible agency, including the Coordinating

T-203 F&A Cost Rates and the Uniform Guidance, A Non-Profit Perspective

T-203 F&A Cost Rates and the Uniform Guidance, A Non-Profit Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Regulations (Current and New) Rate Types

T-203 F&A Cost Rates and the Uniform Guidance, A Non-Profit Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Regulations (Current and New) Rate Types

October 20, 2014 Uniform Guidance Topics Administrative Salaries UG 200.413 Publication and Printing UG 200.461 Travel Costs UG 200.474 Visas Costs UG 200.463 Computing Devices (under $5,000) UG 200.453

October 20, 2014 Uniform Guidance Topics Administrative Salaries UG 200.413 Publication and Printing UG 200.461 Travel Costs UG 200.474 Visas Costs UG 200.463 Computing Devices (under $5,000) UG 200.453

COST ISSUES PART 2: INDIRECT COST RATES, WHAT THEY ARE & WHAT YOU NEED TO KNOW

COST ISSUES PART 2: INDIRECT COST RATES, WHAT THEY ARE & WHAT YOU NEED TO KNOW Edward (Ted) Waters, Esq. Scott Sheffler, Esq. August 4, 2016 1 AGENDA Cost Allocation and Indirect Costs Direct Costs vs

COST ISSUES PART 2: INDIRECT COST RATES, WHAT THEY ARE & WHAT YOU NEED TO KNOW Edward (Ted) Waters, Esq. Scott Sheffler, Esq. August 4, 2016 1 AGENDA Cost Allocation and Indirect Costs Direct Costs vs

OMB Uniform Guidance Hot Topics and Implementation. July 18, 2014: The University of Alabama in Huntsville

Special attention will be paid to those sections of the that carry the most uncertainty and that may require significant institutional planning and preparation. The purpose of this session is not to provide

Special attention will be paid to those sections of the that carry the most uncertainty and that may require significant institutional planning and preparation. The purpose of this session is not to provide

Frequently Asked Questions Updated: November 2014

Frequently Asked Questions Updated: November 2014 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200

Frequently Asked Questions Updated: November 2014 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200

COGR Guide to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards VERSION 1: APRIL 17, 2014

COGR Guide to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards VERSION 1: APRIL 17, 2014 Introduction The OMB Uniform Administrative Requirements,

COGR Guide to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards VERSION 1: APRIL 17, 2014 Introduction The OMB Uniform Administrative Requirements,

U.S. Department of Housing and Urban Development Office of Housing Counseling

U.S. Department of Housing and Urban Development Office of Housing Counseling Understanding Indirect Cost Rates, De Minimis Rate, and Cost Allocation Plans Booth Management Consulting 7230 Lee Deforest

U.S. Department of Housing and Urban Development Office of Housing Counseling Understanding Indirect Cost Rates, De Minimis Rate, and Cost Allocation Plans Booth Management Consulting 7230 Lee Deforest

Navigating the OMB Super Circular

Navigating the OMB Super Circular New Mexico Association of Community Partners 2014 Conference June 5, 2014 Eleanor Evans, Esq. CAPLAW (617) 357-6915 eleanor.evans@caplaw.org www.caplaw.org Navigating

Navigating the OMB Super Circular New Mexico Association of Community Partners 2014 Conference June 5, 2014 Eleanor Evans, Esq. CAPLAW (617) 357-6915 eleanor.evans@caplaw.org www.caplaw.org Navigating

Ins and Outs of Super Circular II: Cost Principles & Audit Requirements

Ins and Outs of Super Circular II: Cost Principles & Audit Requirements CAPLAW Strategic Issues Facing CAAs Webinar Series April 23, 2014 CAPLAW www.caplaw.org 617.357.6915 Subpart E Cost Principles 2

Ins and Outs of Super Circular II: Cost Principles & Audit Requirements CAPLAW Strategic Issues Facing CAAs Webinar Series April 23, 2014 CAPLAW www.caplaw.org 617.357.6915 Subpart E Cost Principles 2

The Uniform Guidance: Changes and Strategies for Implementation

The Uniform Guidance: Changes and Strategies for Implementation Mark Davis Attain LLC Cindy Hope University of Alabama Kim Moreland University of Wisconsin Madison Jeffrey Silber Cornell University Topics

The Uniform Guidance: Changes and Strategies for Implementation Mark Davis Attain LLC Cindy Hope University of Alabama Kim Moreland University of Wisconsin Madison Jeffrey Silber Cornell University Topics

5/17/2016 GASB UPDATE. Tara Fenner, CPA, CMFO. How we really feel about GASB!

GASB UPDATE Tara Fenner, CPA, CMFO How we really feel about GASB! 1 No worries! We are here to help! GASB 68 & 71: PENSIONS We Made It! Now What? 2 Review GASB 68, Accounting and Financial Reporting for

GASB UPDATE Tara Fenner, CPA, CMFO How we really feel about GASB! 1 No worries! We are here to help! GASB 68 & 71: PENSIONS We Made It! Now What? 2 Review GASB 68, Accounting and Financial Reporting for

OMB CIRCULAR A-133 COMPLIANCE SUPPLEMENTS INCLUDING ARRA AWARDS

OMB CIRCULAR A-133 COMPLIANCE SUPPLEMENTS INCLUDING ARRA AWARDS Georgia Loidl, CPA Long Chilton, LLP 1 The Auditor s Roadmap... SINGLE AUDITS TABLE OF CONTENTS Statement on Auditing Standards (SAS 117)

OMB CIRCULAR A-133 COMPLIANCE SUPPLEMENTS INCLUDING ARRA AWARDS Georgia Loidl, CPA Long Chilton, LLP 1 The Auditor s Roadmap... SINGLE AUDITS TABLE OF CONTENTS Statement on Auditing Standards (SAS 117)

Indirect Cost Rates & What Happens Under. Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager

Indirect Cost Rates & What Happens Under the New Super Circular Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com www.linkedin.com/pub/paul-calabrese/20/293/645/

Indirect Cost Rates & What Happens Under the New Super Circular Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com www.linkedin.com/pub/paul-calabrese/20/293/645/

What Happens to Indirect Rates under the Uniform Guidance Bag Lunch Webinar November 19, 2015

What Happens to Indirect Rates under the Uniform Guidance Bag Lunch Webinar November 19, 2015 Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com

What Happens to Indirect Rates under the Uniform Guidance Bag Lunch Webinar November 19, 2015 Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com

Implementation and Readiness Guide for the OMB Uniform Guidance Prepared by the Council on Governmental Relations (COGR) Introduction

Introduction") Implementation and Readiness Guide for the OMB Uniform Guidance Prepared by the Council on Governmental Relations (COGR) DECEMBER 12, 2014 VERSION Introduction The Implementation and Readiness Guide for

Implementation and Readiness Guide for the OMB Uniform Guidance Prepared by the Council on Governmental Relations (COGR) DECEMBER 12, 2014 VERSION Introduction The Implementation and Readiness Guide for

WHAT THE PI NEEDS TO KNOW

The UC Uniform Guidance Workgroup would like to acknowledge and thank the Council on Governmental Relations, the University of Minnesota, and Columbia University for their resources on which much of this

The UC Uniform Guidance Workgroup would like to acknowledge and thank the Council on Governmental Relations, the University of Minnesota, and Columbia University for their resources on which much of this

UNIFORM GRANT GUIDANCE POLICY REGARDING FEDERAL REVENUE SOURCES

No. 721 UNIFORM GRANT GUIDANCE POLICY REGARDING FEDERAL REVENUE SOURCES I. PURPOSE The purpose of this policy is to ensure compliance with the requirements of the federal Uniform Grant Guidance regulations

No. 721 UNIFORM GRANT GUIDANCE POLICY REGARDING FEDERAL REVENUE SOURCES I. PURPOSE The purpose of this policy is to ensure compliance with the requirements of the federal Uniform Grant Guidance regulations

IMPLEMENTATION QUICK START ACTION PLANNER. UNIFORM GUIDANCE - 2 CFR Parts 200 and 2900 COMPLETION. Policies and Procedures

Policies and Procedures Develop or update financial and administrative policies and procedures to implement the requirements in the Uniform Guidance and OMB's approved exceptions for DOL. Obtain management

Policies and Procedures Develop or update financial and administrative policies and procedures to implement the requirements in the Uniform Guidance and OMB's approved exceptions for DOL. Obtain management

OMB Super Circular Proposed Uniform Guidance. RAC Forum April 10, 2013

OMB Super Circular Proposed Uniform Guidance RAC Forum April 10, 2013 Change is Coming Good news A-21 is gone! Bad news It s back and bigger than ever Circular Consolidation Super Storm? Extreme Makeover:

OMB Super Circular Proposed Uniform Guidance RAC Forum April 10, 2013 Change is Coming Good news A-21 is gone! Bad news It s back and bigger than ever Circular Consolidation Super Storm? Extreme Makeover:

FEDERAL SINGLE AUDIT

FEDERAL SINGLE AUDIT Uniform Guidance: Lessons learned post-implementation and continuing developments Presented by: Gil Bernhard, CPA Learning Objectives To summarize the changes created by Uniform Guidance

FEDERAL SINGLE AUDIT Uniform Guidance: Lessons learned post-implementation and continuing developments Presented by: Gil Bernhard, CPA Learning Objectives To summarize the changes created by Uniform Guidance

Selected Items of Cost - Exhibit 1. States, Local Governments, Indian Tribes. Allowable with restrictions Unallowable Unallowable Unallowable

List of Selected Contained in 2 CFR part 200 The following exhibit provides a listing of selected items of cost contained in cost principles in 2 CFR part 200, subpart E. Several cost items are unique

List of Selected Contained in 2 CFR part 200 The following exhibit provides a listing of selected items of cost contained in cost principles in 2 CFR part 200, subpart E. Several cost items are unique

Introduction to Indirect Costs

Introduction to Indirect Costs GMS Summit St. Petersburg, FL June 12 16, 2016 Presented by: Jason D. Brooks, CPA 1 About the Author Jason D. Brooks, CPA is a partner with Watkins, Ward and Stafford, PLLC

Introduction to Indirect Costs GMS Summit St. Petersburg, FL June 12 16, 2016 Presented by: Jason D. Brooks, CPA 1 About the Author Jason D. Brooks, CPA is a partner with Watkins, Ward and Stafford, PLLC

Uniform Guidance Super Circular 2 CFR Part 200

Uniform Guidance Super Circular 2 CFR Part 200 MSU First Looks and Future Plans May 27, 2014 Dan Evon, Contract & Grant Administration The Rules Contracts Federal Acquisition Regulations (FAR) Grants and

Uniform Guidance Super Circular 2 CFR Part 200 MSU First Looks and Future Plans May 27, 2014 Dan Evon, Contract & Grant Administration The Rules Contracts Federal Acquisition Regulations (FAR) Grants and

Accounting Update: What s Now, New and Next. Convergence 2014 By Amy Michie, CPA and Bill Moss, CPA

Accounting Update: What s Now, New and Next Convergence 2014 By Amy Michie, CPA and Bill Moss, CPA FASB Pronouncements FASB Developments Relevant AICPA Technical Practice Updates FASB NFP Advisory Committee

Accounting Update: What s Now, New and Next Convergence 2014 By Amy Michie, CPA and Bill Moss, CPA FASB Pronouncements FASB Developments Relevant AICPA Technical Practice Updates FASB NFP Advisory Committee

PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS

PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Subpart A Acronyms and Definitions Contents 200.0 Acronyms. 200.1 Definitions. 200.2 Acquisition

PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Subpart A Acronyms and Definitions Contents 200.0 Acronyms. 200.1 Definitions. 200.2 Acquisition

Subrecipient monitoring responsibilities are shared among the following:

SUBRECIPIENT MONITORING PURPOSE The OMB Uniform Guidance, 2 CFR Part 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS section 200.331 requires prime recipients

SUBRECIPIENT MONITORING PURPOSE The OMB Uniform Guidance, 2 CFR Part 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS section 200.331 requires prime recipients

5/23/2016. Nonprofit Hot topics. Questions and Answers

Nonprofit Hot topics Questions and Answers 1 Statistics How many exempt organizations in the United States (as of November 2015) 1,549,296 Nonprofits 1,178,739 Charitable Organizations 1,076,309 Public

Nonprofit Hot topics Questions and Answers 1 Statistics How many exempt organizations in the United States (as of November 2015) 1,549,296 Nonprofits 1,178,739 Charitable Organizations 1,076,309 Public

MEMO CODE: SP ; CACFP ; SFSP Questions and Answers on the Transition to and Implementation of 2 CFR Part 200

Food and Nutrition Service Park Office Center 3101 Park Center Drive Alexandria VA 22302 DATE: MEMO CODE: SP 02-2016; CACFP 02-2016; SFSP 02-2016 SUBJECT: TO: Questions and Answers on the Transition to

Food and Nutrition Service Park Office Center 3101 Park Center Drive Alexandria VA 22302 DATE: MEMO CODE: SP 02-2016; CACFP 02-2016; SFSP 02-2016 SUBJECT: TO: Questions and Answers on the Transition to

PART 6 - INTERNAL CONTROL

PART 6 - INTERNAL CONTROL INTRODUCTION The A-102 Common Rule and OMB Circular A-110 (2 CFR part 215) require that non-federal entities receiving Federal awards (i.e., auditee management) establish and

PART 6 - INTERNAL CONTROL INTRODUCTION The A-102 Common Rule and OMB Circular A-110 (2 CFR part 215) require that non-federal entities receiving Federal awards (i.e., auditee management) establish and

University of Missouri System Accounting Policies and Procedures

University of Missouri System Accounting Policies and Procedures Policy Number: APM-60.85 Policy Name: Subrecipient Monitoring Procedures General Policy and Procedure Overview: The University of Missouri

University of Missouri System Accounting Policies and Procedures Policy Number: APM-60.85 Policy Name: Subrecipient Monitoring Procedures General Policy and Procedure Overview: The University of Missouri

January 16, DATES: Effective date: This interim final rule is effective on December 26, 2014

COGR Summary of Background and Technical Corrections to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards January 16, 2015 The interim joint final

COGR Summary of Background and Technical Corrections to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards January 16, 2015 The interim joint final

Uniform Guidance: Key Points of the UNC Implementation - Getting to the Real Impacts of 2 CFR Part 200

Uniform Guidance: Key Points of the UNC Implementation - Getting to the Real Impacts of 2 CFR Part 200 Sharon Brooks Director of Award Management Services and Cash Management Robin Cyr Associate Vice Chancellor

Uniform Guidance: Key Points of the UNC Implementation - Getting to the Real Impacts of 2 CFR Part 200 Sharon Brooks Director of Award Management Services and Cash Management Robin Cyr Associate Vice Chancellor

BELOW ARE SOME SELECTED QUESTIONS FROM THE FAQ. FOR THE COMPLETE FAQ DOCUMENT GO TO

Frequently Asked Questions Updated: July 2017 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200 The

Frequently Asked Questions Updated: July 2017 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200 The

FACILITATED BY: Robin Booth, CPA

U.S. Department of Housing and Urban Development Office of Housing Counseling Applying and Computing the 10% De Minimis Rate November 22, 2016 2:00 PM (EST) Facilitated by Booth Management Consulting,

U.S. Department of Housing and Urban Development Office of Housing Counseling Applying and Computing the 10% De Minimis Rate November 22, 2016 2:00 PM (EST) Facilitated by Booth Management Consulting,

Grants Administrative Changes under the New EDGAR. Steven A. Spillan, Esq. Brustein & Manasevit February 2015

Grants Administrative Changes under the New EDGAR Steven A. Spillan, Esq. Brustein & Manasevit www.bruman.com February 2015 1 The Importance and Structure of the New EDGAR Part 76 Part 3474 Part 200 Major

Grants Administrative Changes under the New EDGAR Steven A. Spillan, Esq. Brustein & Manasevit www.bruman.com February 2015 1 The Importance and Structure of the New EDGAR Part 76 Part 3474 Part 200 Major

Introduction to Indirect Costs

Introduction to Indirect Costs Questions to be Answered What are indirect costs? How are they documented? How are they recovered? Points to Keep in Mind Indirect costs tend to be support costs (e.g., telephone,

Introduction to Indirect Costs Questions to be Answered What are indirect costs? How are they documented? How are they recovered? Points to Keep in Mind Indirect costs tend to be support costs (e.g., telephone,

Youth For Understanding USA, Inc. Financial Statements Including Uniform Guidance Reports and Independent Auditors Report

Financial Statements Including Uniform Guidance Reports and Independent Auditors Report For the Eighteen-Month Period Ended June 30, 2017 Financial Statements For the Eighteen-Month Period Ended June 30,

Financial Statements Including Uniform Guidance Reports and Independent Auditors Report For the Eighteen-Month Period Ended June 30, 2017 Financial Statements For the Eighteen-Month Period Ended June 30,

2 CFR Part 200 Uniform Guidance

2 CFR Part 200 Uniform Guidance Lisa Mosley Executive Director, Research Operations Michele Wrapp Associate Director, Research Operations December 15, 2014 200.110 Effective/applicability date Applies

2 CFR Part 200 Uniform Guidance Lisa Mosley Executive Director, Research Operations Michele Wrapp Associate Director, Research Operations December 15, 2014 200.110 Effective/applicability date Applies

TUCSON URBAN LEAGUE, INC.

TUCSON URBAN LEAGUE, INC. INDEPENDENT AUDITOR S REPORT AND FINANCIAL STATEMENTS (INCLUDING OMB UNIFORM GUIDANCE SUPPLEMENTAL COMPLIANCE AND INTERNAL CONTROL REPORTS) YEARS ENDED JUNE 30, 2017 AND 2016

TUCSON URBAN LEAGUE, INC. INDEPENDENT AUDITOR S REPORT AND FINANCIAL STATEMENTS (INCLUDING OMB UNIFORM GUIDANCE SUPPLEMENTAL COMPLIANCE AND INTERNAL CONTROL REPORTS) YEARS ENDED JUNE 30, 2017 AND 2016

PROCEDURE Determination of Allowable vs. Unallowable Expenses

PROCEDURE Determination of Allowable vs. Unallowable Expenses Background and Purpose In order to comply with Uniform Guidance Section 200.302(b)(7) which requires Written procedures for determining the

PROCEDURE Determination of Allowable vs. Unallowable Expenses Background and Purpose In order to comply with Uniform Guidance Section 200.302(b)(7) which requires Written procedures for determining the

GULF COAST COMMUNITY SERVICES ASSOCIATION (A Texas Nonprofit Organization) ANNUAL FINANCIAL AND COMPLIANCE AUDIT REPORTS

ANNUAL FINANCIAL AND COMPLIANCE AUDIT REPORTS") GULF COAST COMMUNITY SERVICES ASSOCIATION ANNUAL FINANCIAL AND COMPLIANCE AUDIT REPORTS YEARS ENDED SEPTEMBER 30, 2014 AND 2013 SEPTEMBER 30, 2014 AND 2013 TABLE OF CONTENTS Page Number INDEPENDENT AUDITORS

GULF COAST COMMUNITY SERVICES ASSOCIATION ANNUAL FINANCIAL AND COMPLIANCE AUDIT REPORTS YEARS ENDED SEPTEMBER 30, 2014 AND 2013 SEPTEMBER 30, 2014 AND 2013 TABLE OF CONTENTS Page Number INDEPENDENT AUDITORS

COMMUNITY PROGRESS COUNCIL, INC.

COMMUNITY PROGRESS COUNCIL, INC. FINANCIAL STATEMENTS With Supplementary Information YEARS ENDED JUNE 30, 2013 AND 2012 TABLE OF CONTENTS PAGE NUMBER INDEPENDENT AUDITORS' REPORT 1-3 FINANCIAL STATEMENTS

COMMUNITY PROGRESS COUNCIL, INC. FINANCIAL STATEMENTS With Supplementary Information YEARS ENDED JUNE 30, 2013 AND 2012 TABLE OF CONTENTS PAGE NUMBER INDEPENDENT AUDITORS' REPORT 1-3 FINANCIAL STATEMENTS

U.S. Department of Housing and Urban Development Office of Housing Counseling

U.S. Department of Housing and Urban Development Office of Housing Counseling Facilitated by Booth Management Consulting 7230 Lee Deforest Drive, Suite 202 Columbia, MD 21046 Best Practices & Lessons Learned,

U.S. Department of Housing and Urban Development Office of Housing Counseling Facilitated by Booth Management Consulting 7230 Lee Deforest Drive, Suite 202 Columbia, MD 21046 Best Practices & Lessons Learned,

Bring SPF. Take CPE. JULY 6, 7, & 8. Ocean City, MD Clarion Resort Fontainebleau Hotel

Bring SPF. Take CPE. JULY 6, 7, & 8 Ocean City, MD Clarion Resort Fontainebleau Hotel SEPTEMBER 19 Government Contractors CONFERENCE Managing government engagements with precision The Government Contractors

Bring SPF. Take CPE. JULY 6, 7, & 8 Ocean City, MD Clarion Resort Fontainebleau Hotel SEPTEMBER 19 Government Contractors CONFERENCE Managing government engagements with precision The Government Contractors

Partner Baker Tilly Virchow Krause, LLP

JJason Coyle, y, CPA Partner Baker Tilly Virchow Krause, LLP Recent GASB pronouncements What are they? How do they affect your financial statements and your audit? Agenda items and research projects at

JJason Coyle, y, CPA Partner Baker Tilly Virchow Krause, LLP Recent GASB pronouncements What are they? How do they affect your financial statements and your audit? Agenda items and research projects at

Child Care Associates

FINANCIAL STATEMENTS For the Year Ended December 31, 2017 Table of Contents December 31, 2017 REPORT Independent Auditors Report 1 FINANCIAL STATEMENTS Statements of Financial Position 3 Statements of

FINANCIAL STATEMENTS For the Year Ended December 31, 2017 Table of Contents December 31, 2017 REPORT Independent Auditors Report 1 FINANCIAL STATEMENTS Statements of Financial Position 3 Statements of

MANAGED ACCESS TO CHILD HEALTH, INC. (A Nonprofit Organization) JACKSONVILLE, FLORIDA FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2016 AND 2015

JACKSONVILLE, FLORIDA FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2016 AND 2015") (A Nonprofit Organization) JACKSONVILLE, FLORIDA FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2016 AND 2015 JACKSONVILLE, FLORIDA TABLE OF CONTENTS INDEPENDENT AUDITORS REPORT 1-2 Page FINANCIAL STATEMENTS

(A Nonprofit Organization) JACKSONVILLE, FLORIDA FINANCIAL STATEMENTS FOR THE YEARS ENDED JUNE 30, 2016 AND 2015 JACKSONVILLE, FLORIDA TABLE OF CONTENTS INDEPENDENT AUDITORS REPORT 1-2 Page FINANCIAL STATEMENTS

GULF COAST COMMUNITY SERVICES ASSOCIATION (A Texas Nonprofit Organization) ANNUAL FINANCIAL AND COMPLIANCE AUDIT REPORTS

ANNUAL FINANCIAL AND COMPLIANCE AUDIT REPORTS") GULF COAST COMMUNITY SERVICES ASSOCIATION ANNUAL FINANCIAL AND COMPLIANCE AUDIT REPORTS YEARS ENDED SEPTEMBER 30, 2013 AND 2012 SEPTEMBER 30, 2013 AND 2012 TABLE OF CONTENTS Page Number INDEPENDENT AUDITORS

GULF COAST COMMUNITY SERVICES ASSOCIATION ANNUAL FINANCIAL AND COMPLIANCE AUDIT REPORTS YEARS ENDED SEPTEMBER 30, 2013 AND 2012 SEPTEMBER 30, 2013 AND 2012 TABLE OF CONTENTS Page Number INDEPENDENT AUDITORS

Ohio Department of Education Perkins CTE Workshop January 21, 2014 MICHAEL BRUSTEIN, ESQ.

Ohio Department of Education Perkins CTE Workshop January 21, 2014 1 MICHAEL BRUSTEIN, ESQ. WWW.BRUMAN.COM MBRUSTEIN@BRUMAN.COM Agenda 1. Update on Reauthorization 2. Funding / Obligations 3. Allowable

Ohio Department of Education Perkins CTE Workshop January 21, 2014 1 MICHAEL BRUSTEIN, ESQ. WWW.BRUMAN.COM MBRUSTEIN@BRUMAN.COM Agenda 1. Update on Reauthorization 2. Funding / Obligations 3. Allowable

Compliance Issues and Update /22/17

Compliance Update 2017 NC State Treasurer s NC and Review June 22, 2017 Compliance Audit Update 2017 Potential changes to the Yellow Book New standards for auditing and attestation Uniform Guidance (UG)

Compliance Update 2017 NC State Treasurer s NC and Review June 22, 2017 Compliance Audit Update 2017 Potential changes to the Yellow Book New standards for auditing and attestation Uniform Guidance (UG)

Allowability of Costs Federal Programs

626. ATTACHMENT Allowability of Costs Federal Programs Expenditures must be aligned with approved budgeted items. Any changes or variations from the state-approved budget and grant application need prior

626. ATTACHMENT Allowability of Costs Federal Programs Expenditures must be aligned with approved budgeted items. Any changes or variations from the state-approved budget and grant application need prior

UNIFORM GRANT GUIDANCE POLICY REGARDING FEDERAL REVENUE SOURCES 721 Adopted 6/27/2016

UNIFORM GRANT GUIDANCE POLICY REGARDING FEDERAL REVENUE SOURCES 721 Adopted 6/27/2016 I. PURPOSE A. The purpose of this policy is to ensure compliance with the requirements of the federal Uniform Grant

UNIFORM GRANT GUIDANCE POLICY REGARDING FEDERAL REVENUE SOURCES 721 Adopted 6/27/2016 I. PURPOSE A. The purpose of this policy is to ensure compliance with the requirements of the federal Uniform Grant

TUCSON URBAN LEAGUE, INC.

TUCSON URBAN LEAGUE, INC. INDEPENDENT AUDITOR S REPORT AND FINANCIAL STATEMENTS (INCLUDING OMB UNIFORM GUIDANCE SUPPLEMENTAL COMPLIANCE & INTERNAL CONTROL REPORTS) YEARS ENDED JUNE 30, 2016 AND 2015 TUCSON

TUCSON URBAN LEAGUE, INC. INDEPENDENT AUDITOR S REPORT AND FINANCIAL STATEMENTS (INCLUDING OMB UNIFORM GUIDANCE SUPPLEMENTAL COMPLIANCE & INTERNAL CONTROL REPORTS) YEARS ENDED JUNE 30, 2016 AND 2015 TUCSON

AUDIT REPORT FINANCIAL AND FEDERAL AWARD COMPLIANCE EXAMINATION

AUDIT REPORT FINANCIAL AND FEDERAL AWARD COMPLIANCE EXAMINATION FOR THE YEAR ENDED SEPTEMBER 30, 2016 AYUDA, INC. CONTENTS PAGE NO. I. Financial Section Financial Statements, for the Year Ended September

AUDIT REPORT FINANCIAL AND FEDERAL AWARD COMPLIANCE EXAMINATION FOR THE YEAR ENDED SEPTEMBER 30, 2016 AYUDA, INC. CONTENTS PAGE NO. I. Financial Section Financial Statements, for the Year Ended September

Subrecipient Monitoring Guide

Office of Research Subrecipient Monitoring Guide The purpose of this document is to communicate the University of Florida s guidelines pertaining to the programmatic and financial monitoring of its sponsored

Office of Research Subrecipient Monitoring Guide The purpose of this document is to communicate the University of Florida s guidelines pertaining to the programmatic and financial monitoring of its sponsored

City of Spokane Spokane County

Washington State Auditor s Office Financial Statements and Federal Single Audit Report City of Spokane Spokane County Audit Period January 1, 2008 through December 31, 2008 Report No. 1002267 Issue Date

Washington State Auditor s Office Financial Statements and Federal Single Audit Report City of Spokane Spokane County Audit Period January 1, 2008 through December 31, 2008 Report No. 1002267 Issue Date

WILLIAMSON-BURNETCOUNTYOPPORTUNITIES,INC.Financial Statements

WILLIAMSON-BURNETCOUNTYOPPORTUNITIES,INC.Financial Statements Independent Auditor s Reports Single Audit Reports Other Information November 30, 2016 WEST, DAVIS & COMPANY, LLP Certified Public Accountants

WILLIAMSON-BURNETCOUNTYOPPORTUNITIES,INC.Financial Statements Independent Auditor s Reports Single Audit Reports Other Information November 30, 2016 WEST, DAVIS & COMPANY, LLP Certified Public Accountants

Child Care Associates

FINANCIAL STATEMENTS For the Year Ended December 31, 2016 Table of Contents December 31, 2016 REPORT Independent Auditors Report 1 FINANCIAL STATEMENTS Statements of Financial Position 3 Statements of