Amy Roberts, Appalachian State University

|

|

|

- Garry Fleming

- 5 years ago

- Views:

Transcription

1 Amy Roberts, Appalachian State University

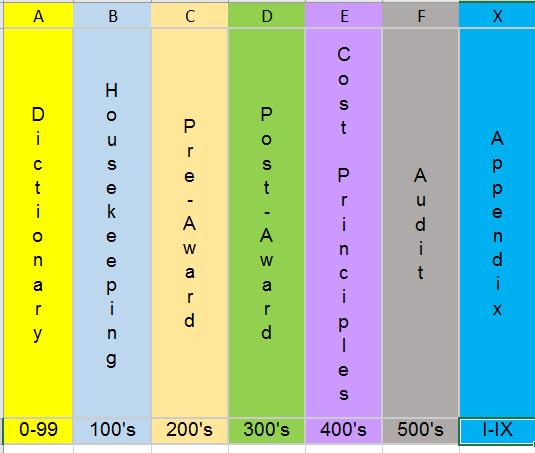

2 Originally referred to as A-81, the Super Circular, or the Omni Circular Consolidates 8 previous Circulars All Federal funding agencies are required to implement the Uniform Guidance. Included in the new guidance are definitions, uniform administrative requirements (both pre- and post-award), cost principles, and audit requirements.

3 Administrative requirements and cost principles apply to new and incremental funding awarded after December 26, Existing Federal awards will continue to be governed by the terms and conditions under which they were awarded. Subpart F, Audit Requirements applies to audits of non-federal entity fiscal years beginning on or after December 26, 2014 ( or the first fiscal year that begins after December 26, 2014). From the university perspective, the Uniform Guidance will supersede OMB Circulars A- 110, A-21, and A-133.

4 OMB Circular A-133 (Audits) OMB Circular A-110 (Administrative Requirements for Higher Ed, Hospitals and Non-Profits) OMB Circular A-21 (University cost principles) OMB Circular A-87 (State, Local and Indian Tribal Gov. cost principles) OMB Circular A-122 (Not for profit cost principles) OMB Circular A-89 (Catalog of Federal Domestic Assistance CFDA) OMB Circular A-102 (Grants and Cooperative Agreements with State and Local Government) OMB CircularA-50 (Audit follow up)

Subpart D Post Federal Award Requirements (.300-.399) Subpart E The Cost Principles (.400-.499) Subpart F Audit Requirements (.500-.")

5 Subpart A Acronyms and Definitions (.0-.99) Subpart B General Provisions ( ) Subpart C Pre-Award Requirements and Contents of Federal Awards ( ) Subpart D Post Federal Award Requirements ( ) Subpart E The Cost Principles ( ) Subpart F Audit Requirements ( ) Appendices I Funding Opportunities; II Contract Provisions; III Indirect Costs (F&A) +more!

6

of Higher")

7 COSO Committee of Sponsoring Organizations of the Treadway Commission COFAR Council on Financial Assistance Reform EUI Energy Usage Index FAIN Federal Award Identification No. FAC Federal Audit Clearing house FAPIIS Federal Awardee Performance & Integrity Information System GOCO Government Owned Contractor Operated IBS Institutional Base Salary IHE Institution(s) of Higher Ed PII Personally Identifiable Information PRHP Post Retirement Health Plans PTE Pass through entity REUI Relative Energy Usage Index SPOC Single Point of Contact TFM Treasury Financial Manual VAT Value Added Tax

for printing, transmitting and")

8 Capital assets - now includes intangibles: IP and software Computing devices - machines used to acquire, store, analyze, process, and publish data and other information electronically, including accessories (or peripherals ) for printing, transmitting and receiving, or storing electronic information Contract - legal instrument by which a non-federal entity purchases property or services needed to carry out the project or program under a Federal award unless transaction meets the definition of subaward. Focus on the nature of the relationship not what the agreement is called Contractor - entity that receives a contract as defined in (Moving away from vendor terminology) General Purpose Equipment now includes information technology equipment /systems Information Technology Systems includes computing devices /software Internal Controls -process designed to provide reasonable assurance regarding achievement of objectives: (a) Effectiveness and efficiency of operations (b) Reliability of reporting for internal /external use (c) Compliance with applicable laws and regs

9 Micro-purchase - purchase of supplies or services using simplified acquisition procedures, where aggregate amount the micro-purchase threshold currently $10k for IHE s Participant support costs - direct costs for items such as stipends or subsistence allowances, travel allowances, registration fees paid to or on behalf of participants or trainees (but not employees) in connection with conferences, or training projects Program Income - now includes license fees and royalties on patents and copyrights. The Federal awarding agency may negotiate agreements with recipients regarding appropriate uses of income earned after the period of performance as part of the grant closeout process Supplies - tangible personal property not described in as Equipment (200.33). A computing device is a supply if the acquisition cost is less than the lesser of the capitalization level established by the non-federal entity for financial statement purposes or $5,000, regardless of the length of its useful life.

10 Conflict of interest - The Federal awarding agency must establish conflict of interest policies for Federal awards. The non-federal entity must disclose in writing any *potential* conflict of interest to the Federal awarding agency or pass-through entity in accordance with applicable Federal awarding agency policy Mandatory disclosures - The non-federal entity or applicant for a Federal award must disclose, in a timely manner, in writing to the Federal awarding agency or pass-through entity all violations of Federal criminal law involving fraud, bribery, or gratuity violations potentially affecting the Federal award. Failure to make required disclosures can result in any of the remedies described in Remedies for noncompliance, including suspension or debarment.

11 : Provides a standard set of 15 data elements which must be provided in all Federal awards either in full text or by reference Provides guidance on Federal Awarding Agency, Program, or Award Specific Terms and Conditions Requires Federal awarding agencies to include an indication of the timing and scope of expected performance as related to the outcomes intended to be achieved In some instances, (e.g., discretionary research awards) this may be limited to submission of technical performance reports

12 : Provides more robust guidance to Federal agencies to measure performance in a way that will help the Federal awarding agency and other non-federal entities to improve program outcomes, share lessons learned, and spread the adoption of promising practices. Federal awarding agencies must require recipients to use OMB-approved standard government-wide information collections to provide financial and performance information. Recipients must be required to relate financial data to performance accomplishments, and must also provide cost information to demonstrate cost effective practices.

13 , Entities must: Establish and maintain effective internal control over the award to provide reasonable assurance that the entity is managing the Federal award in compliance with Federal statutes, regulations, and the terms and conditions of the award. Evaluate and monitor compliance Take prompt action on audit findings Safeguard protected personally identifiable information

14 : For federal research proposals, voluntary committed cost sharing is not expected, and cannot be used as a factor during the merit review of applications or proposals, except where required by statute. May be considered if it is both in accordance with Federal awarding agency regulations and specified in a notice of funding opportunity. Only mandatory cost sharing or cost sharing specifically committed in the project budget must be included in the organized research base for computing the indirect (F&A) cost rate or reflected in allocation of indirect costs.

15 : Prior approval to transfer from participant support costs Restriction on re-budgeting of training costs removed New language better reflects that project directors can be away from campus yet remain engaged in the project at proposed /awarded levels. Prior approval only required in the event that disengagement from the project occurs during the absence. The disengagement from the project for more than 3 months, or a 25 % reduction in time devoted to the project, by the approved project director or principal investigator.

16 , Property records must be maintained that include: description of the property serial number or other identification number source of funding for the property (including FAIN who holds title acquisition date cost of the property % of Federal participation in the project costs for the award under which the property was acquired location, use and condition of the property any ultimate disposition data including the date of disposal and sale price of the property.

17 : Title to supplies vest in the non- Federal entity upon acquisition : Residual inventory of unused supplies > $5k at completion of the federal project and not needed for any other Federal award, can be retained for use on other activities or sold, but the federal government must be compensated for its share. The amount of compensation is computed in the same manner as equipment sold to 3 rd party.

(2) new provision that covers organizational conflict of interest 200.")

18 (c)(1) The non-federal entity must maintain written standards of conduct covering conflicts of interest and governing the performance of its employees engaged in the selection, award, and administration of contracts (c)(2) new provision that covers organizational conflict of interest : Competition - The non-federal entity must conduct procurements in a manner providing full and open competition, and that prohibits the use of statutorily or administratively imposed state or local geographical preferences in the evaluations of bids or proposals, except in those cases where applicable Federal statutes expressly mandate or encourage geographic preference.

19 Methods of procurement to be followed Includes a prescriptive list of 5 procurement methods (a) Procurement by micro-purchases (b) Procurement by small purchase procedures. (c) Procurement by sealed bids (formal advertising). (d) Procurement by competitive proposals. (f) Procurement by noncompetitive proposals. Procurement by micro-purchase: acquisition of supplies/services $10k. To the extent practicable, the non-federal entity must distribute micro-purchases equitably among qualified suppliers (equitable distribution). Micro-purchases may be awarded without soliciting competitive quotations if the non-federal entity considers the price to be reasonable. New category which allows purchases without competition

20

21 : Pass-through entities must determine when agreements made for disbursement of Federal program funds casts the party receiving the funds in the role of subrecipient or contractor Contractors: Contract executed to obtain goods and services for the non-federal entity s own use and creates a procurement relationship with the contractor Provide goods and services within normal business operations Provide similar goods and services to many different purchasers Normally operate in a competitive environment Provide goods /services ancillary to the operation of the Federal program Not subject to compliance requirements as a result of the agreement Subrecipients: Carry out a portion of a Federal award and creates a Federal assistance relationship Entity is eligible to receive Federal assistance Has its performance measured in relation to whether objectives of Federal program were met Has responsibility for programmatic decision making Is responsible for adherence to applicable Federal program requirements specified in award Uses the Federal funds to carry out a program for a public purpose specified in authorizing statute, as opposed to providing goods and services for the benefit of a pass-through entity

22 (b): Must evaluate subrecipients risk of non-compliance with Federal statutes, regulations, and terms and conditions of the subaward to determine the appropriate subrecipient monitoring. May include such factors as: Experience with the same or similar awards Results of previous audits Whether subrecipient has new personnel or new / substantially changed systems Extent and result of federal awarding agency monitoring of the subrecipient Depending on the risk assessment: Consider if specific subaward conditions are needed Provide subrecipients with training/technical assistance Perform on-site reviews Arrange for agreed-upon-procedure engagements (requires prior approval, ).

23 , The pass-through entity must: Include in the subaward (and when changes are made): Federal award identification, e.g., DUNS number Indirect cost rate for the Federal Award (including if de minimis rate is charged) Requirements imposed by the pass-through entity Requirement to provide access to records for audit Monitor subrecipients Verify subrecipients have audits in accordance with Subpart F Make any necessary adjustment to the pass-through entity s records based on reviews and audits of subrecipients Consider actions to address subrecipient noncompliance Ensure award is used for authorized purpose and goals are achieved Ensure financial and programmatic reports are received and reviewed Follow-up to ensure subrecipient takes appropriate action on all deficiencies pertaining to the subaward from the pass-through entity identified through audits, on-site reviews, and other means Issue management decision for audit findings pertaining to subawards

24 Required Certifications By signing this report, I certify to the best of my knowledge and belief that the report is true, complete, and accurate, and the expenditures, disbursements and cash receipts are for the purposes and objectives set forth in the terms and conditions of the Federal award. I am aware that any false, fictitious, or fraudulent information, or the omission of any material fact, may subject me to criminal, civil or administrative penalties for fraud, false statements, false claims or otherwise. (U.S. Code Title 18, Section 1001 and Title 31, Sections and ).

25 (c) The salaries of administrative & clerical staff should normally be treated as indirect (F&A) costs. Direct charging may be appropriate if all of the following conditions are met: Administrative /clerical services are integral to the project or activity Individuals involved can be specifically identified with the project or activity Such costs are explicitly included in the budget or have the prior written approval of the Federal awarding agency The costs are not also recovered as indirect costs

26 Indirect Costs (F&A).. Any non-federal entity that has a federally negotiated indirect cost rate may apply for a onetime extension of a current negotiated indirect cost rates for a period of up to four years Appendix 111 to Part 200 A utility cost adjustment of up to 1.3 percentage points may be included in the negotiated indirect cost rate of the IHE for organized research

27 Periodic certifications of effort are no longer explicitly required and previously described acceptable methods of allocating payroll to sponsored projects have been removed. There is an increased emphasis placed on the non-federal entity s system of internal controls. The concept of IBS is now included (h) (4) (ii): The non-federal entity establishes a consistent written definition of work covered by institutional base salary (IBS) which is specific enough to determine when work beyond that level has occurred. This may be described in appointment letter or other documentation (8) (viii) (c) (x): It is recognized that teaching, research, service, and administration are often inextricably intermingled in an academic setting. When recording salaries and wages charged to Federal awards for IHEs, a precise assessment of factors that contribute to costs is therefore not always feasible, nor is it expected.

Costs - A 10% de minimis IDC rate is now available to any non-federal entity that has never received a negotiated indirect cost rate, except for those non-federal entities")

28 Direct Costs - Removal of major project requirement and recognition of administrative workload Indirect (F&A) Costs - A 10% de minimis IDC rate is now available to any non-federal entity that has never received a negotiated indirect cost rate, except for those non-federal entities described in Appendix VII to Part may elect to charge a de minimis rate of 10% of modified total direct costs (MTDC) which may be used indefinitely. Importantly, if chosen, the non-federal entity must use the 10% rate on all federal awards until the entity negotiates an approved rate with their cognizant agency.

as direct costs is allowable for devices essential and")

29 Exchange Rates (new): Allows for cost increases from fluctuations in exchange rates with certain conditions being met and of course, the availability of funds Materials /Supplies Costs, Including Computing Devices: Charging computing devices (laptop and desktop computers and associated supplies) as direct costs is allowable for devices essential and allocable, but not solely dedicated, to performance of a federal award. Computing devices, defined as supplies when the cost is the lesser of the entity s capitalization level of $5000, are subject to the less burdensome administrative requirements of supplies (as opposed to equipment) if the acquisition cost is less than the capitalization threshold Publication and Printing Costs: Paragraph (c) resolves a long-standing issue with charges necessary to publish research results, which typically occur after expiration, but are otherwise allowable costs of an award.

(6) Requires that questioned costs be identified by CFDA number and FAIN 200.")

30 Single Audit threshold increased from $500k to $750k in federal award during FY Audit Findings threshold for reportable questioned costs increased from $10k to $25k (b)(6) Requires that questioned costs be identified by CFDA number and FAIN (b)(8) Requires identification of whether audit finding is a repeat from the immediately prior audit and if so the prior year audit finding number (c) Requires findings numbers be in format prescribed by the data collection form (see )

31 Questions or Comments?

2 CFR 215 (A-110) or 2 CFR 230 (A-122) Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards.

or 2 CFR 230 (A-122) Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards.") Significant Changes for Selected Items of Cost Office of Management and Budget Guidance PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Item of

Significant Changes for Selected Items of Cost Office of Management and Budget Guidance PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Item of

SINGLE AUDIT UPDATE. Presented By Joel Knopp, CPA

SINGLE AUDIT UPDATE Presented By Joel Knopp, CPA Session Covers Uniform Guidance Circular Components Single Audit Changes Auditee and Auditor Impact Scope of Audit under Uniform Guidance Florida Single

SINGLE AUDIT UPDATE Presented By Joel Knopp, CPA Session Covers Uniform Guidance Circular Components Single Audit Changes Auditee and Auditor Impact Scope of Audit under Uniform Guidance Florida Single

Initial COGR observations on definitions are intertwined with the applicable sections below.

COGR Preliminary Assessment of Selected Items OMB Uniform Administrative Requirements, Cost Principles, and Administrative Requirements for Federal Awards January 14, 2014 Below is COGR s preliminary assessment

COGR Preliminary Assessment of Selected Items OMB Uniform Administrative Requirements, Cost Principles, and Administrative Requirements for Federal Awards January 14, 2014 Below is COGR s preliminary assessment

OMB. Uniform Guidance

2014 OMB Uniform Guidance Assessing the OMB Uniform Guidance: Major Changes and Impacts The Office of Management and Budget (OMB) consolidated the federal government s guidance on Uniform Administrative

2014 OMB Uniform Guidance Assessing the OMB Uniform Guidance: Major Changes and Impacts The Office of Management and Budget (OMB) consolidated the federal government s guidance on Uniform Administrative

OMB Uniform Guidance Hot Topics and Implementation. July 18, 2014: The University of Alabama in Huntsville

Special attention will be paid to those sections of the that carry the most uncertainty and that may require significant institutional planning and preparation. The purpose of this session is not to provide

Special attention will be paid to those sections of the that carry the most uncertainty and that may require significant institutional planning and preparation. The purpose of this session is not to provide

How to Prepare for The New EDGAR Auditing Requirements Tiffany R. Winters, Esq. Brustein & Manasevit April 2015

Listen to audio overview here: https://meetny.webex.com/meetny/lsr.php?rcid=e28880f578fc4958b34178599f485530 How to Prepare for The New EDGAR Auditing Requirements Tiffany R. Winters, Esq. Brustein & Manasevit

Listen to audio overview here: https://meetny.webex.com/meetny/lsr.php?rcid=e28880f578fc4958b34178599f485530 How to Prepare for The New EDGAR Auditing Requirements Tiffany R. Winters, Esq. Brustein & Manasevit

Uniform Grant Guidance Policies & Procedures

Guidance related to the uniform grant guidance can be found in Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards: CFR 200 Full Text - ecfr Code of

Guidance related to the uniform grant guidance can be found in Part 200 Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards: CFR 200 Full Text - ecfr Code of

Webinar: Are you Prepared for the Supercircular? February 2014

Webinar: Are you Prepared for the Supercircular? February 2014 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee,

Webinar: Are you Prepared for the Supercircular? February 2014 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee,

The COGR Perspective on the OMB Uniform Guidance: A First Look

The COGR Perspective on the OMB Uniform Guidance: A First Look COGR Meeting Thursday, February 27, 2014 Washington Marriott Hotel Washington, D.C. Agenda for this Session The Big Picture and the Next 12

The COGR Perspective on the OMB Uniform Guidance: A First Look COGR Meeting Thursday, February 27, 2014 Washington Marriott Hotel Washington, D.C. Agenda for this Session The Big Picture and the Next 12

COGR Guide to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards VERSION 1: APRIL 17, 2014

COGR Guide to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards VERSION 1: APRIL 17, 2014 Introduction The OMB Uniform Administrative Requirements,

COGR Guide to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards VERSION 1: APRIL 17, 2014 Introduction The OMB Uniform Administrative Requirements,

COGR Guide to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards VERSION 2: SEPTEMBER 17, 2014

COGR Guide to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards VERSION 2: SEPTEMBER 17, 2014 Introduction The OMB Uniform Administrative Requirements,

COGR Guide to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards VERSION 2: SEPTEMBER 17, 2014 Introduction The OMB Uniform Administrative Requirements,

Uniform Guidance Update

National Head Start Association 44 th Annual Head Start Conference and Expo April 7 10, 2017 Nashville, TN Hyatt Regency Chicago Uniform Guidance Update Sunday, April 9, 2017 4:00 pm 5:00 pm Presented

National Head Start Association 44 th Annual Head Start Conference and Expo April 7 10, 2017 Nashville, TN Hyatt Regency Chicago Uniform Guidance Update Sunday, April 9, 2017 4:00 pm 5:00 pm Presented

Do You Get Federal Funds? Find out What s Changing with Uniform Guidance

Minnesota Council of Nonprofits 2015 MCN Annual Conference October 1 2, 2015 St. Paul, MN St. Paul RiverCentre Find out What s Changing with Uniform Guidance Thursday, October 1, 2015 3:45 pm 5:00 pm Presented

Minnesota Council of Nonprofits 2015 MCN Annual Conference October 1 2, 2015 St. Paul, MN St. Paul RiverCentre Find out What s Changing with Uniform Guidance Thursday, October 1, 2015 3:45 pm 5:00 pm Presented

Uniform Guidance Super Circular 2 CFR Part 200

Uniform Guidance Super Circular 2 CFR Part 200 MSU First Looks and Future Plans May 27, 2014 Dan Evon, Contract & Grant Administration The Rules Contracts Federal Acquisition Regulations (FAR) Grants and

Uniform Guidance Super Circular 2 CFR Part 200 MSU First Looks and Future Plans May 27, 2014 Dan Evon, Contract & Grant Administration The Rules Contracts Federal Acquisition Regulations (FAR) Grants and

Grants Administrative Changes under the New EDGAR. Steven A. Spillan, Esq. Brustein & Manasevit February 2015

Grants Administrative Changes under the New EDGAR Steven A. Spillan, Esq. Brustein & Manasevit www.bruman.com February 2015 1 The Importance and Structure of the New EDGAR Part 76 Part 3474 Part 200 Major

Grants Administrative Changes under the New EDGAR Steven A. Spillan, Esq. Brustein & Manasevit www.bruman.com February 2015 1 The Importance and Structure of the New EDGAR Part 76 Part 3474 Part 200 Major

October 20, 2014 Uniform Guidance Topics Administrative Salaries UG 200.413 Publication and Printing UG 200.461 Travel Costs UG 200.474 Visas Costs UG 200.463 Computing Devices (under $5,000) UG 200.453

October 20, 2014 Uniform Guidance Topics Administrative Salaries UG 200.413 Publication and Printing UG 200.461 Travel Costs UG 200.474 Visas Costs UG 200.463 Computing Devices (under $5,000) UG 200.453

The Uniform Guidance: Changes and Strategies for Implementation

The Uniform Guidance: Changes and Strategies for Implementation Mark Davis Attain LLC Cindy Hope University of Alabama Kim Moreland University of Wisconsin Madison Jeffrey Silber Cornell University Topics

The Uniform Guidance: Changes and Strategies for Implementation Mark Davis Attain LLC Cindy Hope University of Alabama Kim Moreland University of Wisconsin Madison Jeffrey Silber Cornell University Topics

10/30/2015 OBJECTIVES. CPAs & ADVISORS. Present an overview of the Super Circular. Contents of the Super Circular. Discuss Administrative Requirements

CPAs & ADVISORS experience direction // 2 CFR 200 UNIFORM GRANT GUIDANCE Presented by Andy Richards, CPA, Partner October 30, 2015 OBJECTIVES Present an overview of the Super Circular Contents of the Super

CPAs & ADVISORS experience direction // 2 CFR 200 UNIFORM GRANT GUIDANCE Presented by Andy Richards, CPA, Partner October 30, 2015 OBJECTIVES Present an overview of the Super Circular Contents of the Super

Frequently Asked Questions Updated: November 2014

Frequently Asked Questions Updated: November 2014 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200

Frequently Asked Questions Updated: November 2014 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200

The Uniform Guidance (2 CFR 200)*

*") The Uniform Guidance (2 CFR 200)* 1 * T H E B R V E N E W W O R L D O F F E D E R L S S I S T N C E ndrew Boulter, UCOP Joao Pires, UCOP The Uniform Guidance: History The Uniform Guidance resulted from

The Uniform Guidance (2 CFR 200)* 1 * T H E B R V E N E W W O R L D O F F E D E R L S S I S T N C E ndrew Boulter, UCOP Joao Pires, UCOP The Uniform Guidance: History The Uniform Guidance resulted from

PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS

PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Subpart A Acronyms and Definitions Contents 200.0 Acronyms. 200.1 Definitions. 200.2 Acquisition

PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Subpart A Acronyms and Definitions Contents 200.0 Acronyms. 200.1 Definitions. 200.2 Acquisition

Uniform Guidance for Federal Awards Key Changes and Lessons

Uniform Guidance for Federal Awards Key Changes and Lessons Learned Kinman Tong, Senior Manager Moss Adams LLP 1 PRESENTER Kinman Tong, Senior Manager Kinman has been in public accounting since 2003. He

Uniform Guidance for Federal Awards Key Changes and Lessons Learned Kinman Tong, Senior Manager Moss Adams LLP 1 PRESENTER Kinman Tong, Senior Manager Kinman has been in public accounting since 2003. He

Implementation and Readiness Guide for the OMB Uniform Guidance Prepared by the Council on Governmental Relations (COGR) Introduction

Introduction") Implementation and Readiness Guide for the OMB Uniform Guidance Prepared by the Council on Governmental Relations (COGR) DECEMBER 12, 2014 VERSION Introduction The Implementation and Readiness Guide for

Implementation and Readiness Guide for the OMB Uniform Guidance Prepared by the Council on Governmental Relations (COGR) DECEMBER 12, 2014 VERSION Introduction The Implementation and Readiness Guide for

WHAT THE PI NEEDS TO KNOW

The UC Uniform Guidance Workgroup would like to acknowledge and thank the Council on Governmental Relations, the University of Minnesota, and Columbia University for their resources on which much of this

The UC Uniform Guidance Workgroup would like to acknowledge and thank the Council on Governmental Relations, the University of Minnesota, and Columbia University for their resources on which much of this

Uniform Guidance Overview

Compliance Auditing Update NC Local Government Auditing, Reporting and Review June 14, 2016 Uniform Guidance Overview Course Objectives-Uniform Administrative Requirements, Cost Principles, and Audit Requirements

Compliance Auditing Update NC Local Government Auditing, Reporting and Review June 14, 2016 Uniform Guidance Overview Course Objectives-Uniform Administrative Requirements, Cost Principles, and Audit Requirements

Uniform Guidance: Key Points of the UNC Implementation - Getting to the Real Impacts of 2 CFR Part 200

Uniform Guidance: Key Points of the UNC Implementation - Getting to the Real Impacts of 2 CFR Part 200 Sharon Brooks Director of Award Management Services and Cash Management Robin Cyr Associate Vice Chancellor

Uniform Guidance: Key Points of the UNC Implementation - Getting to the Real Impacts of 2 CFR Part 200 Sharon Brooks Director of Award Management Services and Cash Management Robin Cyr Associate Vice Chancellor

Uniform Guidance. Jeremy Dunn. Senior Manager November 4, Elliott Davis Decosimo, LLC Elliott Davis Decosimo, PLLC

Uniform Guidance Jeremy Dunn Senior Manager November 4, 2015 This material was used by Elliott Davis Decosimo during an oral presentation; it is not a complete record of the discussion. This presentation

Uniform Guidance Jeremy Dunn Senior Manager November 4, 2015 This material was used by Elliott Davis Decosimo during an oral presentation; it is not a complete record of the discussion. This presentation

FEDERAL SINGLE AUDIT

FEDERAL SINGLE AUDIT Uniform Guidance: Lessons learned post-implementation and continuing developments Presented by: Gil Bernhard, CPA Learning Objectives To summarize the changes created by Uniform Guidance

FEDERAL SINGLE AUDIT Uniform Guidance: Lessons learned post-implementation and continuing developments Presented by: Gil Bernhard, CPA Learning Objectives To summarize the changes created by Uniform Guidance

SuperCircular and Budget and Accounting PIN

SuperCircular and Budget and Accounting PIN Presented by: Gil Bernhard, CPA October 31, 2015 HMA Overview New Federal Grants Management Requirements OMB SuperCircular Budget and Accounting PIN 2 New Federal

SuperCircular and Budget and Accounting PIN Presented by: Gil Bernhard, CPA October 31, 2015 HMA Overview New Federal Grants Management Requirements OMB SuperCircular Budget and Accounting PIN 2 New Federal

UNIFORM GRANT GUIDANCE POLICY REGARDING FEDERAL REVENUE SOURCES

No. 721 UNIFORM GRANT GUIDANCE POLICY REGARDING FEDERAL REVENUE SOURCES I. PURPOSE The purpose of this policy is to ensure compliance with the requirements of the federal Uniform Grant Guidance regulations

No. 721 UNIFORM GRANT GUIDANCE POLICY REGARDING FEDERAL REVENUE SOURCES I. PURPOSE The purpose of this policy is to ensure compliance with the requirements of the federal Uniform Grant Guidance regulations

STATE AND FEDERAL REVENUE SOURCES

STATE AND REVENUE SOURCES PERKINS GRANTS RETIREMENT CONTRIBUTIONS ADMINISTRATION OF AWARDS Except as provided in 20 U.S.C. 2352(b) and (c) and 20 U.S.C. 2353, each eligible agency, including the Coordinating

STATE AND REVENUE SOURCES PERKINS GRANTS RETIREMENT CONTRIBUTIONS ADMINISTRATION OF AWARDS Except as provided in 20 U.S.C. 2352(b) and (c) and 20 U.S.C. 2353, each eligible agency, including the Coordinating

University of Missouri System Accounting Policies and Procedures

University of Missouri System Accounting Policies and Procedures Policy Number: APM-60.85 Policy Name: Subrecipient Monitoring Procedures General Policy and Procedure Overview: The University of Missouri

University of Missouri System Accounting Policies and Procedures Policy Number: APM-60.85 Policy Name: Subrecipient Monitoring Procedures General Policy and Procedure Overview: The University of Missouri

Ohio Department of Education Perkins CTE Workshop January 21, 2014 MICHAEL BRUSTEIN, ESQ.

Ohio Department of Education Perkins CTE Workshop January 21, 2014 1 MICHAEL BRUSTEIN, ESQ. WWW.BRUMAN.COM MBRUSTEIN@BRUMAN.COM Agenda 1. Update on Reauthorization 2. Funding / Obligations 3. Allowable

Ohio Department of Education Perkins CTE Workshop January 21, 2014 1 MICHAEL BRUSTEIN, ESQ. WWW.BRUMAN.COM MBRUSTEIN@BRUMAN.COM Agenda 1. Update on Reauthorization 2. Funding / Obligations 3. Allowable

2 CFR 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR. Kirsten Rigg

2 CFR 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Kirsten Rigg WYDOT Internal Review 307-777-4252 kirsten.rigg@wyo.gov TRAINING OBJECTIVES Background

2 CFR 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Kirsten Rigg WYDOT Internal Review 307-777-4252 kirsten.rigg@wyo.gov TRAINING OBJECTIVES Background

Navigating the OMB Super Circular

Navigating the OMB Super Circular New Mexico Association of Community Partners 2014 Conference June 5, 2014 Eleanor Evans, Esq. CAPLAW (617) 357-6915 eleanor.evans@caplaw.org www.caplaw.org Navigating

Navigating the OMB Super Circular New Mexico Association of Community Partners 2014 Conference June 5, 2014 Eleanor Evans, Esq. CAPLAW (617) 357-6915 eleanor.evans@caplaw.org www.caplaw.org Navigating

The Uniform Guidance: Key Issues for Universities. Slide 1

The Uniform Guidance: Key Issues for Universities Slide 1 Today s Panel Michelle Christy, Director, Office of Sponsored Programs, Massachusetts Institute of Technology David Kennedy, Director of Costing

The Uniform Guidance: Key Issues for Universities Slide 1 Today s Panel Michelle Christy, Director, Office of Sponsored Programs, Massachusetts Institute of Technology David Kennedy, Director of Costing

In-Depth Review of OMB s NEW Super Circular (2 CFR Part 200)

") In-Depth Review of OMB s NEW Super Circular (2 CFR Part 200) Trainers: Denes L. Tobie, CPA, Partner Tammy T. Jelinek, MBA, Senior Manager 1 Training Agenda Monday, March 30, 2015 9:00 a.m. Noon General

In-Depth Review of OMB s NEW Super Circular (2 CFR Part 200) Trainers: Denes L. Tobie, CPA, Partner Tammy T. Jelinek, MBA, Senior Manager 1 Training Agenda Monday, March 30, 2015 9:00 a.m. Noon General

Exhibit B ADMINISTRATIVE PROCEDURE DJ-R: FEDERAL PROCUREMENT MANUAL

Exhibit B ADMINISTRATIVE PROCEDURE DJ-R: FEDERAL PROCUREMENT MANUAL FEDERAL PROCUREMENT MANUAL (For School Unit Procurements Using Federal Awards Subject to Uniform Grant Guidance) This Federal Procurement

Exhibit B ADMINISTRATIVE PROCEDURE DJ-R: FEDERAL PROCUREMENT MANUAL FEDERAL PROCUREMENT MANUAL (For School Unit Procurements Using Federal Awards Subject to Uniform Grant Guidance) This Federal Procurement

2 CFR Part 200 Uniform Guidance

2 CFR Part 200 Uniform Guidance Lisa Mosley Executive Director, Research Operations Michele Wrapp Associate Director, Research Operations December 15, 2014 200.110 Effective/applicability date Applies

2 CFR Part 200 Uniform Guidance Lisa Mosley Executive Director, Research Operations Michele Wrapp Associate Director, Research Operations December 15, 2014 200.110 Effective/applicability date Applies

UNIFORM GRANT GUIDANCE POLICY REGARDING FEDERAL REVENUE SOURCES 721 Adopted 6/27/2016

UNIFORM GRANT GUIDANCE POLICY REGARDING FEDERAL REVENUE SOURCES 721 Adopted 6/27/2016 I. PURPOSE A. The purpose of this policy is to ensure compliance with the requirements of the federal Uniform Grant

UNIFORM GRANT GUIDANCE POLICY REGARDING FEDERAL REVENUE SOURCES 721 Adopted 6/27/2016 I. PURPOSE A. The purpose of this policy is to ensure compliance with the requirements of the federal Uniform Grant

IMPLEMENTATION QUICK START ACTION PLANNER. UNIFORM GUIDANCE - 2 CFR Parts 200 and 2900 COMPLETION. Policies and Procedures

Policies and Procedures Develop or update financial and administrative policies and procedures to implement the requirements in the Uniform Guidance and OMB's approved exceptions for DOL. Obtain management

Policies and Procedures Develop or update financial and administrative policies and procedures to implement the requirements in the Uniform Guidance and OMB's approved exceptions for DOL. Obtain management

PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS

PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS 200.33 Equipment. Equipment means tangible personal property (including information technology systems)

PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS 200.33 Equipment. Equipment means tangible personal property (including information technology systems)

Frequently Asked Questions

Frequently Asked Questions Updated: July 2017 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200 The

Frequently Asked Questions Updated: July 2017 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200 The

Uniform Guidance. Diane E. Edelstein, CPA. Sources

Uniform Guidance August 29, 2016 Central KY Chapter of AGA Diane E. Edelstein, CPA Diane is a partner at Maher Duessel, a regional firm in Pennsylvania. Diane has over 25 years of experience with auditing

Uniform Guidance August 29, 2016 Central KY Chapter of AGA Diane E. Edelstein, CPA Diane is a partner at Maher Duessel, a regional firm in Pennsylvania. Diane has over 25 years of experience with auditing

BELOW ARE SOME SELECTED QUESTIONS FROM THE FAQ. FOR THE COMPLETE FAQ DOCUMENT GO TO

Frequently Asked Questions Updated: July 2017 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200 The

Frequently Asked Questions Updated: July 2017 For The Office of Management and Budget s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards At 2 CFR 200 The

EDUCATION DEPARTMENT GENERAL ADMINISTRATIVE REGULATIONS (EDGAR)

") EDUCATION DEPARTMENT GENERAL ADMINISTRATIVE REGULATIONS (EDGAR) Presented for the North County Educational Purchasing Consortium by: Guiselle Carreon, SDCOE Luke Boughen, Fagen Freidman & Fulfrost WHAT

EDUCATION DEPARTMENT GENERAL ADMINISTRATIVE REGULATIONS (EDGAR) Presented for the North County Educational Purchasing Consortium by: Guiselle Carreon, SDCOE Luke Boughen, Fagen Freidman & Fulfrost WHAT

Mentor Public Schools Board of Education 8.18 Policy Manual page 1 Chapter VIII Fiscal Management PROCUREMENT WITH FEDERAL GRANTS/FUNDS

Policy Manual page 1 PROCUREMENT WITH FEDERAL GRANTS/FUNDS Procurement of all supplies, materials, equipment, and services paid for with federal funds or District matching funds shall be made in accordance

Policy Manual page 1 PROCUREMENT WITH FEDERAL GRANTS/FUNDS Procurement of all supplies, materials, equipment, and services paid for with federal funds or District matching funds shall be made in accordance

2 CFR Part 200 Series #2 New Definitions

This is the second of a series dedicated to the topic of new citations found in 2 CFR Part 200 Uniform Administrative Requirements, Cost Principles and Audit Requirements for Federal Grants. The following

This is the second of a series dedicated to the topic of new citations found in 2 CFR Part 200 Uniform Administrative Requirements, Cost Principles and Audit Requirements for Federal Grants. The following

Single Audit Fundamentals Part 3: Understanding and Testing Compliance Requirements and Related Internal Control over Compliance

Governmental Audit Quality Center Single Audit Fundamentals Part 3: Understanding and Testing Compliance Requirements and Related Internal Control over Compliance A Governmental Audit Quality Center Web

Governmental Audit Quality Center Single Audit Fundamentals Part 3: Understanding and Testing Compliance Requirements and Related Internal Control over Compliance A Governmental Audit Quality Center Web

OMB Super Circular Proposed Uniform Guidance. RAC Forum April 10, 2013

OMB Super Circular Proposed Uniform Guidance RAC Forum April 10, 2013 Change is Coming Good news A-21 is gone! Bad news It s back and bigger than ever Circular Consolidation Super Storm? Extreme Makeover:

OMB Super Circular Proposed Uniform Guidance RAC Forum April 10, 2013 Change is Coming Good news A-21 is gone! Bad news It s back and bigger than ever Circular Consolidation Super Storm? Extreme Makeover:

CITY AND COUNTY OF SAN FRANCISCO UNDERSTANDING THE UNIFORM GUIDANCE & NONPROFIT UPDATE

CITY AND COUNTY OF SAN FRANCISCO UNDERSTANDING THE UNIFORM GUIDANCE & NONPROFIT UPDATE Agenda Understanding the Uniform Guidance Katherine V. Lai, Assurance Leader, MGO Mark Tillotson, Nonprofit Industry

CITY AND COUNTY OF SAN FRANCISCO UNDERSTANDING THE UNIFORM GUIDANCE & NONPROFIT UPDATE Agenda Understanding the Uniform Guidance Katherine V. Lai, Assurance Leader, MGO Mark Tillotson, Nonprofit Industry

Indirect Cost Rates A Non-Profit Perspective. Alex Weekes Principal ML Weekes & Company, PC

Indirect Cost Rates A Non-Profit Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Old School versus new regulations Review of 2CFR 200 (not so new

Indirect Cost Rates A Non-Profit Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Old School versus new regulations Review of 2CFR 200 (not so new

Let s Talk About EDGAR Part 200 is in effect, what now? Bonnie Graham, Esq. Brustein & Manasevit

Let s Talk About EDGAR Part 200 is in effect, what now? Bonnie Graham, Esq. bgraham@bruman.com Brustein & Manasevit www.bruman.com January 2017 1 The Importance and Structure of the EDGAR Part 76 Part

Let s Talk About EDGAR Part 200 is in effect, what now? Bonnie Graham, Esq. bgraham@bruman.com Brustein & Manasevit www.bruman.com January 2017 1 The Importance and Structure of the EDGAR Part 76 Part

The Basics of F&A and How the Uniform Guidance Impacts Indirect Costs

The Basics of F&A and How the Uniform Guidance Impacts Indirect Costs Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Indirect Costs / Facilities and Admistrative Cost

The Basics of F&A and How the Uniform Guidance Impacts Indirect Costs Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Indirect Costs / Facilities and Admistrative Cost

TABLE OF CONTENTS CHAPTER 1 PROCUREMENT THRESHOLDS AND PROCEDURES...

TABLE OF CONTENTS CHAPTER 1 THRESHOLDS AND PROCEDURES... 2 SECTION 1.1 OVERVIEW... 2 SECTION 1.2 METHODS OF... 2 Subsection 1.2.a Micro-purchases... 2 Subsection 1.2.b Small Purchase Procedures... 3 Subsection

TABLE OF CONTENTS CHAPTER 1 THRESHOLDS AND PROCEDURES... 2 SECTION 1.1 OVERVIEW... 2 SECTION 1.2 METHODS OF... 2 Subsection 1.2.a Micro-purchases... 2 Subsection 1.2.b Small Purchase Procedures... 3 Subsection

2017 Single Audit Update

2017 Single Audit Update July 25, 2017 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Outline Components of a Single

2017 Single Audit Update July 25, 2017 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Outline Components of a Single

REDLINE COMPARISON OF 24 CFR PART 85 AND 2 CFR 200 PREPARED BY SHAYLA SIMMONS, ESQ. DEPUTY GENERAL COUNSEL, CAMBRIDGE HOUSING AUTHORITY

REDLINE COMPARISON OF 24 CFR PART 85 AND 2 CFR 200 PREPARED BY SHAYLA SIMMONS, ESQ. DEPUTY GENERAL COUNSEL, CAMBRIDGE HOUSING AUTHORITY Key: Black Text language which is the same or substantively similar

REDLINE COMPARISON OF 24 CFR PART 85 AND 2 CFR 200 PREPARED BY SHAYLA SIMMONS, ESQ. DEPUTY GENERAL COUNSEL, CAMBRIDGE HOUSING AUTHORITY Key: Black Text language which is the same or substantively similar

Procurement Policies and Procedures

Procurement Policies and Procedures 1. Purpose of procurement standards. The purpose of these standards is to establish procedures for the U.S. Naval Sea Cadet Corps (USNSCC) for the procurement of supplies

Procurement Policies and Procedures 1. Purpose of procurement standards. The purpose of these standards is to establish procedures for the U.S. Naval Sea Cadet Corps (USNSCC) for the procurement of supplies

Weston School District E2511 HWY S Cazenovia, WI July 1, 2017

Federal Funds Procedural Manual DRAFT Weston School District E2511 HWY S Cazenovia, WI 53924 July 1, 2017 TABLE OF CONTENTS TABLE OF CONTENTS 1 FEDERAL GRANT SUBAWARD INFORMATION FORM 2 1 SAMPLE - FEDERAL

Federal Funds Procedural Manual DRAFT Weston School District E2511 HWY S Cazenovia, WI 53924 July 1, 2017 TABLE OF CONTENTS TABLE OF CONTENTS 1 FEDERAL GRANT SUBAWARD INFORMATION FORM 2 1 SAMPLE - FEDERAL

The Texas A&M University System Uniform Guidance Cost Principles Reference Guide. Selected Items of Cost

The The Uniform Guidance issued by the White House Office of Management and Budget includes revised cost principles for federal awards made on or after December 26, 2014. This Cost Principles Reference

The The Uniform Guidance issued by the White House Office of Management and Budget includes revised cost principles for federal awards made on or after December 26, 2014. This Cost Principles Reference

ATTACHMENT C: FINANCIAL AND ADMINISTRATIVE REQUIREMENTS

ATTACHMENT C: FINANCIAL AND ADMINISTRATIVE REQUIREMENTS The selected applicant must comply with Federal administrative requirements and cost principles, codified in the Office of Management and Budget

ATTACHMENT C: FINANCIAL AND ADMINISTRATIVE REQUIREMENTS The selected applicant must comply with Federal administrative requirements and cost principles, codified in the Office of Management and Budget

Navigating the OMB Super Circular Changes

Legal and financial information for the Community Action network special edition 2014 Navigating the OMB Super Circular Changes By Eleanor A. Evans, Esq. Community Action Agencies (CAAs), states and other

Legal and financial information for the Community Action network special edition 2014 Navigating the OMB Super Circular Changes By Eleanor A. Evans, Esq. Community Action Agencies (CAAs), states and other

January 16, DATES: Effective date: This interim final rule is effective on December 26, 2014

COGR Summary of Background and Technical Corrections to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards January 16, 2015 The interim joint final

COGR Summary of Background and Technical Corrections to the OMB Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards January 16, 2015 The interim joint final

Vendor vs. Subrecipient: Guidance on Appropriate. Classification of Legal Relationships

Vendor vs. Subrecipient: Guidance on Appropriate Classification of Legal Relationships Preamble/Note on Terminology Under the OMB Uniform Administrative Requirements, Cost Principles and Audit Requirements

Vendor vs. Subrecipient: Guidance on Appropriate Classification of Legal Relationships Preamble/Note on Terminology Under the OMB Uniform Administrative Requirements, Cost Principles and Audit Requirements

What Happens to Indirect Rates under the Uniform Guidance Bag Lunch Webinar November 19, 2015

What Happens to Indirect Rates under the Uniform Guidance Bag Lunch Webinar November 19, 2015 Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com

What Happens to Indirect Rates under the Uniform Guidance Bag Lunch Webinar November 19, 2015 Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com

2018 Single Audit Update

2018 Single Audit Update July 24, 2018 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Outline Components of a Single

2018 Single Audit Update July 24, 2018 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Outline Components of a Single

SOUTHWEST TRANSIT Eden Prairie, Minnesota COMMUNICATIONS LETTER. Year Ended December 31, 2014

Eden Prairie, Minnesota COMMUNICATIONS LETTER Year Ended TABLE OF CONTENTS REPORT ON MATTERS IDENTIFIED AS A RESULT OF THE AUDIT OF THE FINANCIAL STATEMENTS... 1 REQUIRED COMMUNICATION... 2 FINANCIAL ANALYSIS...

Eden Prairie, Minnesota COMMUNICATIONS LETTER Year Ended TABLE OF CONTENTS REPORT ON MATTERS IDENTIFIED AS A RESULT OF THE AUDIT OF THE FINANCIAL STATEMENTS... 1 REQUIRED COMMUNICATION... 2 FINANCIAL ANALYSIS...

The Procurement Paw. Presented by: Clint Everhart, CPA Senior Manager

The Procurement Paw Presented by: Clint Everhart, CPA Senior Manager Learning Objectives: Explain each of the five purchase types in the Uniform Guidance (Sections 200.317-.326) Explain the written policies

The Procurement Paw Presented by: Clint Everhart, CPA Senior Manager Learning Objectives: Explain each of the five purchase types in the Uniform Guidance (Sections 200.317-.326) Explain the written policies

Uniform Guidance and DOL Exceptions PRIOR APPROVAL

The Uniform Guidance contains 25 prior approval areas and DOL s exceptions add one additional prior approval. Additionally, DOL s exceptions place parameters around prior approval requirements, including

The Uniform Guidance contains 25 prior approval areas and DOL s exceptions add one additional prior approval. Additionally, DOL s exceptions place parameters around prior approval requirements, including

Ohio Department of Transportation Project Auditing and Cost Terminology (as copied from 2 CFR 200, unless noted otherwise.)

") Acronyms Ohio Department of Transportation Project Auditing and Cost Terminology (as copied from 2 CFR 200, unless noted otherwise.) As copied from 2 CFR 200 200.00 CFR Code of Federal Regulations DUNS

Acronyms Ohio Department of Transportation Project Auditing and Cost Terminology (as copied from 2 CFR 200, unless noted otherwise.) As copied from 2 CFR 200 200.00 CFR Code of Federal Regulations DUNS

Grants 101. Florida School Finance Officers Association. June, Slide 1

Grants 101 Florida School Finance Officers Association June, 2016 Slide 1 Grant vs. Project/Subgrant Be cautious of references to the term Grant. When used in federal Uniform Grant Guidance (UGG), the

Grants 101 Florida School Finance Officers Association June, 2016 Slide 1 Grant vs. Project/Subgrant Be cautious of references to the term Grant. When used in federal Uniform Grant Guidance (UGG), the

U.S. Department of Housing and Urban Development Office of Housing Counseling

U.S. Department of Housing and Urban Development Office of Housing Counseling Facilitated by Booth Management Consulting 7230 Lee Deforest Drive, Suite 202 Columbia, MD 21046 Best Practices & Lessons Learned,

U.S. Department of Housing and Urban Development Office of Housing Counseling Facilitated by Booth Management Consulting 7230 Lee Deforest Drive, Suite 202 Columbia, MD 21046 Best Practices & Lessons Learned,

OFFICE OF RESEARCH AND PROJECT ADMINISTRATION Updated December 2014 UNIVERSITY OF ROCHESTER

OFFICE OF RESEARCH AND PROJECT ADMINISTRATION Updated December 2014 POLICIES AND PROCEDURES FOR THE ADMINISTRATION OF SUBAGREEMENTS ISSUED TO A THIRD PARTY UNIVERSITY OF ROCHESTER December 2014 TABLE OF

OFFICE OF RESEARCH AND PROJECT ADMINISTRATION Updated December 2014 POLICIES AND PROCEDURES FOR THE ADMINISTRATION OF SUBAGREEMENTS ISSUED TO A THIRD PARTY UNIVERSITY OF ROCHESTER December 2014 TABLE OF

Indirect Cost Rates & What Happens Under. Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager

Indirect Cost Rates & What Happens Under the New Super Circular Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com www.linkedin.com/pub/paul-calabrese/20/293/645/

Indirect Cost Rates & What Happens Under the New Super Circular Presenter: Paul H. Calabrese Rubino & Company, CPAs & Consultants Senior Manager Tel: 301-214-4137 pcalabrese@rubino.com www.linkedin.com/pub/paul-calabrese/20/293/645/

6/5/2014. Cost Allocation Overview. Overview (continued) Overview. Overview (continued) Overview (continued)

Overview. Overview (continued) Overview (continued)") Cost Allocation Overview OHIO ASSOCIATION OF PUBLIC TREASURERS Public Finance Officer Training Institute June 2014 MAXIMUS Robert Fink, Sheri Smith, & Linda Hlebak Learning Objectives Cost Allocation Plan

Cost Allocation Overview OHIO ASSOCIATION OF PUBLIC TREASURERS Public Finance Officer Training Institute June 2014 MAXIMUS Robert Fink, Sheri Smith, & Linda Hlebak Learning Objectives Cost Allocation Plan

NCDA 2018 Winter Conference Procurement under Part 200

NCDA 2018 Winter Conference Procurement under Part 200 PROCUREMENT STANDARDS 2 CFR PART 200 Slide 2 Regulatory Requirements 200.317-200.326 of 2 CFR part 200, Uniform Administrative Requirements, Cost

NCDA 2018 Winter Conference Procurement under Part 200 PROCUREMENT STANDARDS 2 CFR PART 200 Slide 2 Regulatory Requirements 200.317-200.326 of 2 CFR part 200, Uniform Administrative Requirements, Cost

NOVA SOUTHEASTERN UNIVERSITY OFFICE OF SPONSORED PROGRAMS POLICIES AND PROCEDURES

PAGE 1 OF 5 PURPOSE: To establish the policy and procedures when the university will engage a third party in performing a substantive programmatic role under a sponsored award to the university. This policy

PAGE 1 OF 5 PURPOSE: To establish the policy and procedures when the university will engage a third party in performing a substantive programmatic role under a sponsored award to the university. This policy

March 23, /1/2018 WASHINGTON STATE UNIVERSITY. Subcontracting. Overview. Recording date of this workshop is

Subcontracting Presented by: Derek Brown, ORSO Anke Moore, SPS Lucas Sanchez, ORSO Ty Simanson, IPN March 2018 Recording date of this workshop is March 23, 2018 Some of the rules and procedures discussed

Subcontracting Presented by: Derek Brown, ORSO Anke Moore, SPS Lucas Sanchez, ORSO Ty Simanson, IPN March 2018 Recording date of this workshop is March 23, 2018 Some of the rules and procedures discussed

Budget Preparation under Uniform Guidance 2 CFR 200

Budget Preparation under Uniform Guidance 2 CFR 200 Kim C. Carter Associate Director, Office of Sponsored Programs The Ohio State University carter.552@osu.edu Florida Research Administration Conference

Budget Preparation under Uniform Guidance 2 CFR 200 Kim C. Carter Associate Director, Office of Sponsored Programs The Ohio State University carter.552@osu.edu Florida Research Administration Conference

Procurements by states General procurement standards.

e-cfr data is current as of June 2, 2017 200.317 Procurements by states. When procuring property and services under a Federal award, a state must follow the same policies and procedures it uses for procurements

e-cfr data is current as of June 2, 2017 200.317 Procurements by states. When procuring property and services under a Federal award, a state must follow the same policies and procedures it uses for procurements

Florida MIECHV Initiative Provider Fiscal Policy Manual

2018 Florida MIECHV Initiative Provider Fiscal Policy Manual Florida MIECHV Initiative This project is supported by the Health Resources and Services Administration (HRSA) of the U.S. Department of Health

2018 Florida MIECHV Initiative Provider Fiscal Policy Manual Florida MIECHV Initiative This project is supported by the Health Resources and Services Administration (HRSA) of the U.S. Department of Health

Uniform Guidance vs. OMB Circulars

Cost Allocation 101 Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements Designed for governing DOL-ETA cost direct principles, recipients and administrative their subrecipients

Cost Allocation 101 Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements Designed for governing DOL-ETA cost direct principles, recipients and administrative their subrecipients

PROCUREMENT POLICY. EDD Revision Date: 8/24/00 WDB Review Date: 6/21/07; 12/20/07; 12/17/15 EXECUTIVE SUMMARY: Purpose:

PROCUREMENT POLICY EDD Revision Date: 8/24/00 WDB Review Date: 6/21/07; 12/20/07; 12/17/15 EXECUTIVE SUMMARY: Purpose: This document establishes the Madera County Workforce Development Board s policy regarding

PROCUREMENT POLICY EDD Revision Date: 8/24/00 WDB Review Date: 6/21/07; 12/20/07; 12/17/15 EXECUTIVE SUMMARY: Purpose: This document establishes the Madera County Workforce Development Board s policy regarding

Introduction to Indirect Costs

Introduction to Indirect Costs GMS Summit St. Petersburg, FL June 12 16, 2016 Presented by: Jason D. Brooks, CPA 1 About the Author Jason D. Brooks, CPA is a partner with Watkins, Ward and Stafford, PLLC

Introduction to Indirect Costs GMS Summit St. Petersburg, FL June 12 16, 2016 Presented by: Jason D. Brooks, CPA 1 About the Author Jason D. Brooks, CPA is a partner with Watkins, Ward and Stafford, PLLC

Subrecipient monitoring responsibilities are shared among the following:

SUBRECIPIENT MONITORING PURPOSE The OMB Uniform Guidance, 2 CFR Part 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS section 200.331 requires prime recipients

SUBRECIPIENT MONITORING PURPOSE The OMB Uniform Guidance, 2 CFR Part 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS section 200.331 requires prime recipients

Nonprofit Financial Management Network

August 14, 2015 1 Nonprofit Financial Management Network Gregory Demetriades, CPA CFO, Community Partners David J. Thomas, CPA, CGMA Managing Partner, 2 1 8:30am-9:00am Registration & Breakfast 9:00am-9:10am

August 14, 2015 1 Nonprofit Financial Management Network Gregory Demetriades, CPA CFO, Community Partners David J. Thomas, CPA, CGMA Managing Partner, 2 1 8:30am-9:00am Registration & Breakfast 9:00am-9:10am

Ins and Outs of Super Circular II: Cost Principles & Audit Requirements

Ins and Outs of Super Circular II: Cost Principles & Audit Requirements CAPLAW Strategic Issues Facing CAAs Webinar Series April 23, 2014 CAPLAW www.caplaw.org 617.357.6915 Subpart E Cost Principles 2

Ins and Outs of Super Circular II: Cost Principles & Audit Requirements CAPLAW Strategic Issues Facing CAAs Webinar Series April 23, 2014 CAPLAW www.caplaw.org 617.357.6915 Subpart E Cost Principles 2

Uniform Grant Guidance for Higher Educational Institutions: Personal Services and Fringe Benefits

Uniform Grant Guidance for Higher Educational Institutions: Personal Services and Fringe Benefits Higher education institutions applying for and receiving federal grants and cooperative agreements are

Uniform Grant Guidance for Higher Educational Institutions: Personal Services and Fringe Benefits Higher education institutions applying for and receiving federal grants and cooperative agreements are

Basics of F&A: A University Perspective. Alex Weekes Principal ML Weekes & Company, PC

Basics of F&A: A University Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Accountant s reconciliation of the old to new rules Overview of F&A General

Basics of F&A: A University Perspective Alex Weekes Principal ML Weekes & Company, PC 203-458-0872 alex.weekes@mlweekes.com Agenda Accountant s reconciliation of the old to new rules Overview of F&A General

Procurement Standards Under Uniform Guidance

Florida Research Administration Conference (FRAC) WELCOME Doug Backman, Director Office of Compliance Research & Commercialization University of Central Florida Gloria Greene, Director Office of Sponsored

Florida Research Administration Conference (FRAC) WELCOME Doug Backman, Director Office of Compliance Research & Commercialization University of Central Florida Gloria Greene, Director Office of Sponsored

PART 6 - INTERNAL CONTROL

PART 6 - INTERNAL CONTROL INTRODUCTION The A-102 Common Rule and OMB Circular A-110 (2 CFR part 215) require that non-federal entities receiving Federal awards (i.e., auditee management) establish and

PART 6 - INTERNAL CONTROL INTRODUCTION The A-102 Common Rule and OMB Circular A-110 (2 CFR part 215) require that non-federal entities receiving Federal awards (i.e., auditee management) establish and

MEMO CODE: SP ; CACFP ; SFSP Questions and Answers on the Transition to and Implementation of 2 CFR Part 200

Food and Nutrition Service Park Office Center 3101 Park Center Drive Alexandria VA 22302 DATE: MEMO CODE: SP 02-2016; CACFP 02-2016; SFSP 02-2016 SUBJECT: TO: Questions and Answers on the Transition to

Food and Nutrition Service Park Office Center 3101 Park Center Drive Alexandria VA 22302 DATE: MEMO CODE: SP 02-2016; CACFP 02-2016; SFSP 02-2016 SUBJECT: TO: Questions and Answers on the Transition to

Glossary. A cost that is reasonable and allocable to sponsored agreements under the principles and methods provided for sponsored projects.

Glossary Term Definition A-21 Office of Management & Budget (OMB) Circular A-21 Contains Cost Principles for Educational Institutions (Replaced by OMB Uniform Guidance or 2 CFR 200). See CFR Title 2, Part

Glossary Term Definition A-21 Office of Management & Budget (OMB) Circular A-21 Contains Cost Principles for Educational Institutions (Replaced by OMB Uniform Guidance or 2 CFR 200). See CFR Title 2, Part

UNIVERSITY OF ARIZONA SUBRECIPIENT MONITORING GUIDE

UNIVERSITY OF ARIZONA SUBRECIPIENT MONITORING GUIDE Contents Introduction... 2 Roles and Responsibilities Chart... 3 Subrecipient Monitoring at Proposal Stage... 4 Subrecipient Monitoring at Subaward Issuance

UNIVERSITY OF ARIZONA SUBRECIPIENT MONITORING GUIDE Contents Introduction... 2 Roles and Responsibilities Chart... 3 Subrecipient Monitoring at Proposal Stage... 4 Subrecipient Monitoring at Subaward Issuance

FEDERAL GRANTS MANAGEMENT: NEW EDGAR/OMB UNIFORM GUIDANCE

CALIFORNIA COMMUNITY COLLEGE WORKSHOP ON THE NEW EDGAR FEDERAL GRANTS MANAGEMENT: NEW EDGAR/OMB UNIFORM GUIDANCE Michael L. Brustein, Esq. mbrustein@bruman.com Brustein & Manasevit, PLLC March 2016 1 The

CALIFORNIA COMMUNITY COLLEGE WORKSHOP ON THE NEW EDGAR FEDERAL GRANTS MANAGEMENT: NEW EDGAR/OMB UNIFORM GUIDANCE Michael L. Brustein, Esq. mbrustein@bruman.com Brustein & Manasevit, PLLC March 2016 1 The

Subrecipient Monitoring Guide

Office of Research Subrecipient Monitoring Guide The purpose of this document is to communicate the University of Florida s guidelines pertaining to the programmatic and financial monitoring of its sponsored

Office of Research Subrecipient Monitoring Guide The purpose of this document is to communicate the University of Florida s guidelines pertaining to the programmatic and financial monitoring of its sponsored

PART 3 COMPLIANCE REQUIREMENTS

PART 3 COMPLIANCE REQUIREMENTS INTRODUCTION Overview The objectives of most compliance requirements for Federal programs administered by States, local governments, Indian tribes, institutions of higher

PART 3 COMPLIANCE REQUIREMENTS INTRODUCTION Overview The objectives of most compliance requirements for Federal programs administered by States, local governments, Indian tribes, institutions of higher

U.S. Department of Housing and Urban Development Office of Housing Counseling

U.S. Department of Housing and Urban Development Office of Housing Counseling Understanding Indirect Cost Rates, De Minimis Rate, and Cost Allocation Plans Booth Management Consulting 7230 Lee Deforest

U.S. Department of Housing and Urban Development Office of Housing Counseling Understanding Indirect Cost Rates, De Minimis Rate, and Cost Allocation Plans Booth Management Consulting 7230 Lee Deforest

Michigan State University. ERA Hot Topics 11/6/14 Dan Evon, Director Contract and Grant Administration. UG, NSF Audit, Procurement

Michigan State University ERA Hot Topics 11/6/14 Dan Evon, Director Contract and Grant Administration UG, NSF Audit, Procurement Uniform Guidance 2 CFR Part 200 Effective 12/26/2014 Grants Reform A 122

Michigan State University ERA Hot Topics 11/6/14 Dan Evon, Director Contract and Grant Administration UG, NSF Audit, Procurement Uniform Guidance 2 CFR Part 200 Effective 12/26/2014 Grants Reform A 122

FEDERAL GRANTS MANAGEMENT FOR HEALTH CENTERS

FEDERAL GRANTS MANAGEMENT FOR HEALTH CENTERS MISSION: ACHIEVEMENT Operational Excellence Alabama Primary Health Care Association October 5, 2017 Presenter: Adrienne Hurtt Introduction Adrienne Hurtt, CEO

FEDERAL GRANTS MANAGEMENT FOR HEALTH CENTERS MISSION: ACHIEVEMENT Operational Excellence Alabama Primary Health Care Association October 5, 2017 Presenter: Adrienne Hurtt Introduction Adrienne Hurtt, CEO