Analyzing Financial Performance Reports

|

|

|

- Neal Blankenship

- 6 years ago

- Views:

Transcription

1 Analyzing Financial Performance Reports

2 Calculating Variances Effective systems identify variances down to the lowest level of management. Variances are hierarchical. As shown in Exhibit 10.2, they begin with the total business unit performance, which is divided into revenue variances and expense variances. Revenue variances are further divided into volume and price variances for the total business unit and for each marketing responsibility center within the unit.

3 Calculating Variances They can be further divided by sales area and sales district. Expense variances can be divided between manufacturing expenses and other expenses. Manufacturing expenses can be further subdivided by factories and departments within factories. It is possible to identify each variance with the individual manager who is responsible for it.

4

5

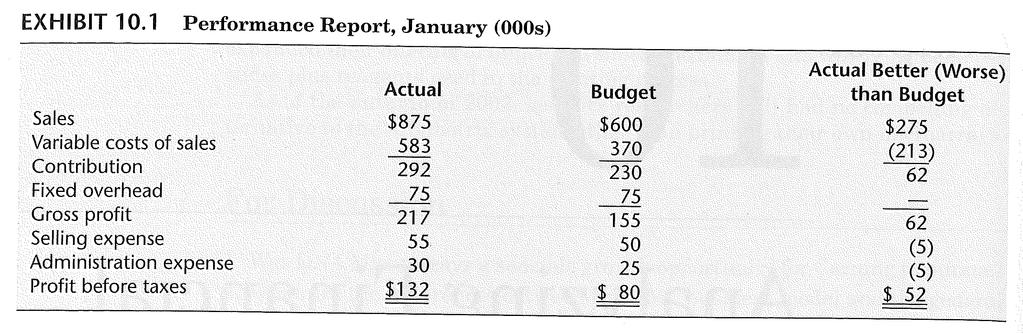

6 Details of the budget of the business unit whose performance is reported in Exhibit 10.1.

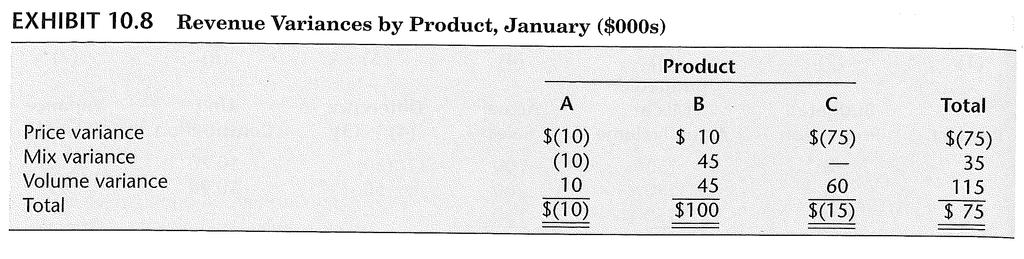

7 Revenue Variances

8 Revenue Variances In this section, we describe how to calculate selling price, volume, and mix variances. The calculation is made for each product line, and the product line results are then aggregated to calculate the total variance. A positive variance is favorable, because it indicates that actual profit exceeded budgeted profit, and a negative variance is unfavorable.

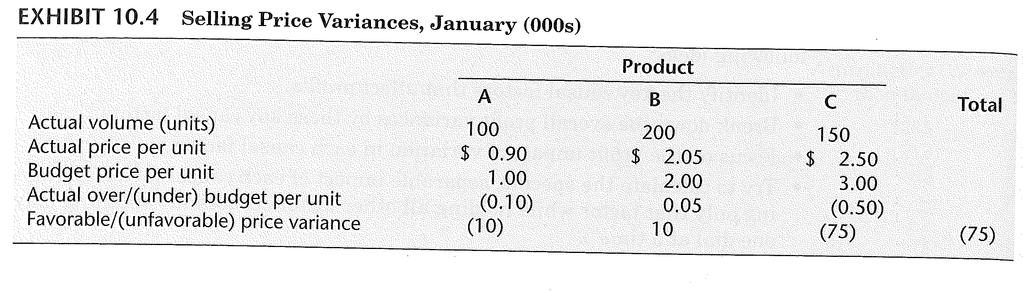

9 Selling Price Variance The selling price variance is calculated by multiplying the difference between the actual price and the standard price by the actual volume. The calculation is shown in Exhibit It shows that the price variance is $75,000, unfavorable.

10

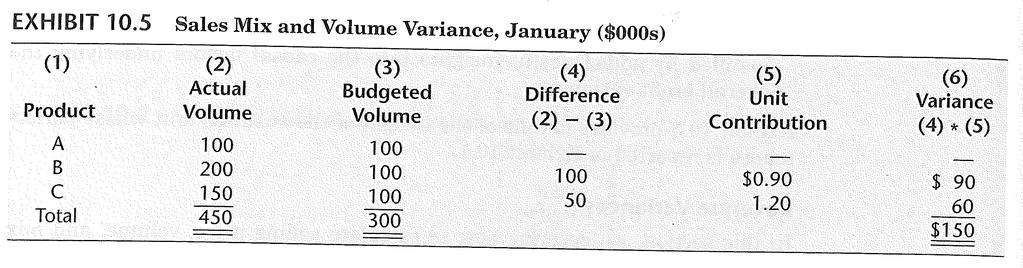

11 Mix and Volume Variance Often the mix and volume variances are not separated. The equation for the combined mix and volume variance is: Mix and volume variance = (Actual volume Budgeted volume) * Budgeted unit contribution The calculation of mix and volume variance is shown in Exhibit 10.5; it is $150,000 favorable.

12

13 Mix and Volume Variance The volume variance results from selling more units than budgeted. The mix variance results from selling a different proportion of products from that assumed in the budget. Because products earn different contributions per unit, the sale of different proportions of products from those budgeted will result in a variance. If the business unit has a richer mix (i.e., a higher proportion of products with a high contribution margin), the actual profit will be higher than budgeted; and if it has a leaner mix, the profit will be lower.

14 Mix Variance The mix variance for each product is found from the following equation: Mix variance = [(Actual volume of sales) (Total actual volume of sales * Budgeted proportion) * Budgeted unit contribution] The calculation of the mix variance is shown in Exhibit It shows that a higher proportion of product B and a lower proportion of product A were sold.

15 Since product B has a higher unit contribution than product A, the mix variance is favorable, by $35,000

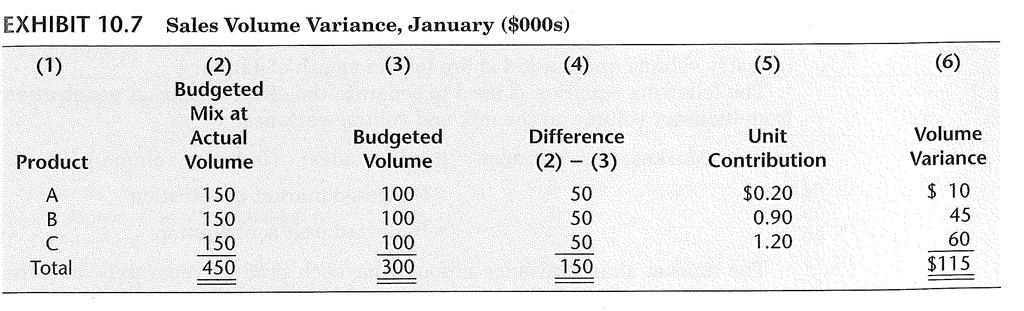

16 Volume Variance The volume variance can be calculated by subtracting the mix variance from the combined mix and volume variance. This is $150,000 minus $35,000, or $115,000. It can also be calculated for each product as follows: Volume variance = [(Total actual volume of sales) * (Budgeted percentage)-(budgeted sales)] * (Budgeted unit contribution) The calculation of the volume variance is shown in Exhibit 10.7.

17

18

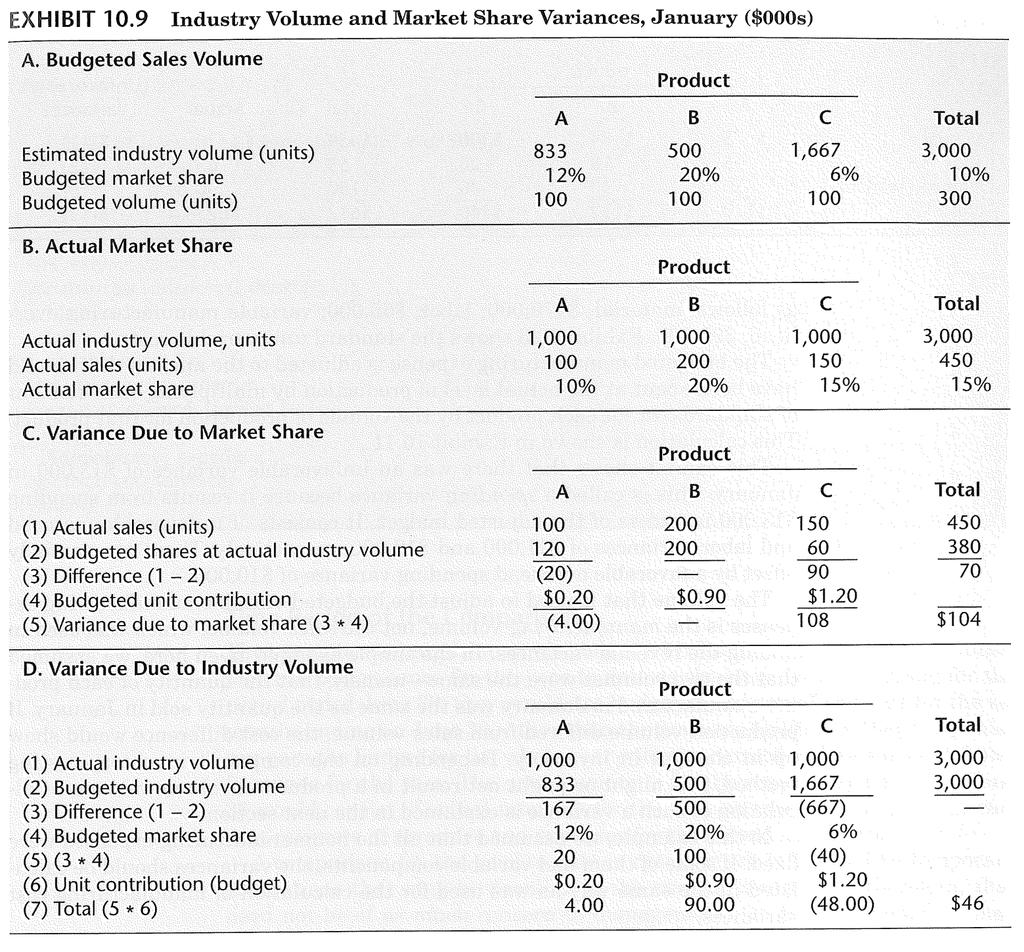

19 Market Penetration and Industry Volume One extension of revenue analysis is to separate the mix and volume variance into the amount caused by differences in market share and the amount caused by differences in industry volume. The principle is that the business unit managers are responsible for market share, but they are not responsible for the industry volume because that is largely influenced by the state of the economy

20 Market share variance The following equation is used to separate the effect of market penetration from industry volume on the mix and volume variance: Market share variance = [(Actual sales) - (Industry volume)] * Budgeted market penetration * Budgeted unit contribution

21 Market share variance The market share variance is found for each product separately, and the total variance is the algebraic sum. The calculation is shown in Section C. (Exhibit 10.9) It shows that $104,000 of the favorable mix and volume variance of $150,000 resulted from the fact that market penetration was better than budget. The remaining $46,000 resulted from the fact that actual industry dollar volume was higher than the amount assumed in the budget

22 Industry volume variance The $46,000 industry volume variance can also be calculated for each product as follows: Industry volume variance = (Actual industry volume Budgeted industry volume) * Budgeted market penetration * Budgeted unit contribution This calculation of variance due to industry volume is shown in Section D.

23

24 Expense Variances

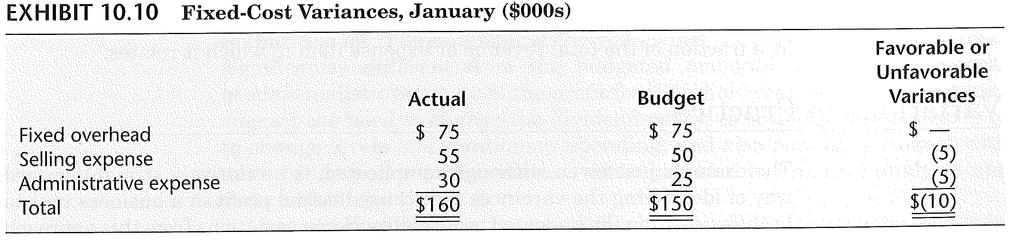

25 Fixed Costs Variances between actual and budgeted fixed costs are obtained simply by subtraction, since these costs are not affected by either the volume of sales or the volume of production. This is shown in Exhibit

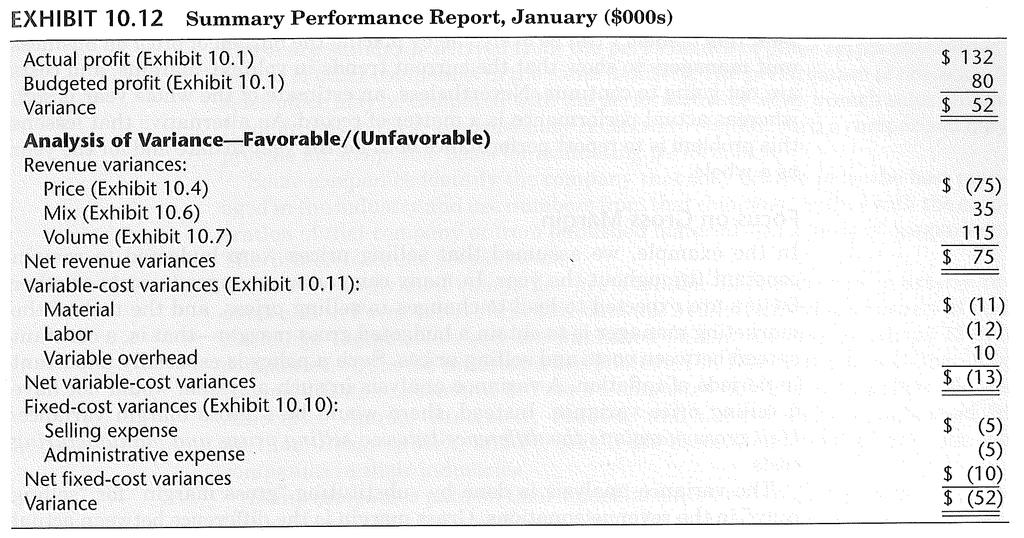

26

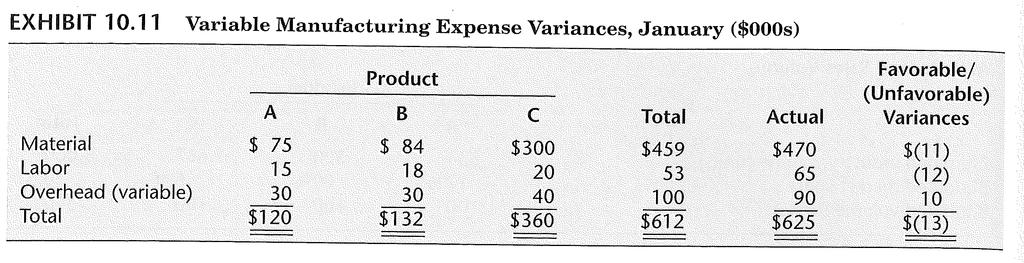

27 Variable Costs Variable costs are costs that vary directly and proportionately with volume. The budgeted variable manufacturing costs must be adjusted to the actual volume of production. Assume that the January production was as follows: product A, 150,000 units; product B, 120,000 units; product C, 200,000 units.

28 Variable Costs Assume also that the variable manufacturing costs incurred in January were as follows: material, $470,000; labor, $65,000; variable manufacturing overhead, $90,000. Exhibit 10.3 shows the standard unit variable costs

29 Variable Costs The budgeted manufacturing expense is adjusted to the amount that should have been spent at the actual level of production by multiplying each element of standard cost for each product by the volume of production for that product. This calculation is shown in Exhibit

30

31 Variable Costs This exhibit shows that there was an unfavorable variance of $13,000 in January. This is called a spending variance because it results from spending $13,000 in excess of the adjusted budget. It consists of unfavorable material and labor variances of $11,000 and $12,000, respectively. These are partially offset by a favorable overhead spending variance of $10,000.

32 Variable Costs The volume that is used to adjust the budgeted variable manufacturing expenses is the manufacturing volume, not the sales volume, which was used in finding the revenue variances. In the simple example given here, we assumed that the two volumes were the same namely, that the quantity of each product manufactured in January was the same as the quantity sold in January. If production volume differed from sales volume, the cost difference would show up in changes in inventory.

33 Summary of Variances There are several ways in which the variances can be summarized in a report for management. One possibility is shown in Exhibit Another form of presentation is to show the actual amounts, as well as the variances. This gives an indication of the relative importance of each variance as a fraction of the total revenue or expense item to which it relates.

34

Adding and Subtracting Fractions

Adding and Subtracting Fractions Adding Fractions with Like Denominators In order to add fractions the denominators must be the same If the denominators of the fractions are the same we follow these two

Adding and Subtracting Fractions Adding Fractions with Like Denominators In order to add fractions the denominators must be the same If the denominators of the fractions are the same we follow these two

CHAPTER 8 Budgetary Control and Variance Analysis

CHAPTER 8 Budgetary Control and Variance Analysis Learning Objectives After studying this chapter, you will be able to: 1. Understand how companies use budgets for control. 2. Perform variance analysis.

CHAPTER 8 Budgetary Control and Variance Analysis Learning Objectives After studying this chapter, you will be able to: 1. Understand how companies use budgets for control. 2. Perform variance analysis.

AGGREGATE EXPENDITURE AND EQUILIBRIUM OUTPUT. Chapter 20

1 AGGREGATE EXPENDITURE AND EQUILIBRIUM OUTPUT Chapter 20 AGGREGATE EXPENDITURE AND EQUILIBRIUM OUTPUT The level of GDP, the overall price level, and the level of employment three chief concerns of macroeconomists

1 AGGREGATE EXPENDITURE AND EQUILIBRIUM OUTPUT Chapter 20 AGGREGATE EXPENDITURE AND EQUILIBRIUM OUTPUT The level of GDP, the overall price level, and the level of employment three chief concerns of macroeconomists

Part 2 : 11/11/10 07:41:20

Question 1 - CMA 694 3-29 - Performance Measurement Part 2 : 11/11/10 07:41:20 One approach to measuring divisional performance is return on investment. Return on investment is expressed as operating income

Question 1 - CMA 694 3-29 - Performance Measurement Part 2 : 11/11/10 07:41:20 One approach to measuring divisional performance is return on investment. Return on investment is expressed as operating income

Section 6.4 Adding & Subtracting Like Fractions

Section 6.4 Adding & Subtracting Like Fractions ADDING ALGEBRAIC FRACTIONS As you now know, a rational expression is an algebraic fraction in which the numerator and denominator are both polynomials. Just

Section 6.4 Adding & Subtracting Like Fractions ADDING ALGEBRAIC FRACTIONS As you now know, a rational expression is an algebraic fraction in which the numerator and denominator are both polynomials. Just

AGENDA: STATEMENT OF CASH FLOWS

TM 14-1 AGENDA: STATEMENT OF CASH FLOWS A. Foundational knowledge. B. Four key concepts for preparing the statement of cash flows. 1. Organizing the statement of cash flows. 2. Distinguishing between the

TM 14-1 AGENDA: STATEMENT OF CASH FLOWS A. Foundational knowledge. B. Four key concepts for preparing the statement of cash flows. 1. Organizing the statement of cash flows. 2. Distinguishing between the

Multiple Choice Questions

Multiple Choice Questions 1. The difference between the actual price and the standard price, multiplied by the actual quantity of materials purchased is the a) direct labor price variance b) direct labor

Multiple Choice Questions 1. The difference between the actual price and the standard price, multiplied by the actual quantity of materials purchased is the a) direct labor price variance b) direct labor

(x + 2)(x + 3) + (x + 2)(x + 3) 5(x + 3) (x + 2)(x + 3) + x(x + 2) 5x + 15 (x + 2)(x + 3) + x 2 + 2x. 5x x 2 + 2x. x 2 + 7x + 15 x 2 + 5x + 6

(x + 3) + (x + 2)(x + 3) 5(x + 3) (x + 2)(x + 3) + x(x + 2) 5x + 15 (x + 2)(x + 3) + x 2 + 2x. 5x x 2 + 2x. x 2 + 7x + 15 x 2 + 5x + 6") Which is correct? Alex s add the numerators and the denominators way 5 x + 2 + x Morgan s find a common denominator way 5 x + 2 + x 5 x + 2 + x I added the numerator plus the numerator and the denominator

Which is correct? Alex s add the numerators and the denominators way 5 x + 2 + x Morgan s find a common denominator way 5 x + 2 + x 5 x + 2 + x I added the numerator plus the numerator and the denominator

COST-VOLUME-PROFIT ANALYSIS

COST-VOLUME-PROFIT ANALYSIS 1. COST-VOLUME-PROFIT (CVP) ANALYSIS CVP analysis, often referred to as break-even analysis, examines the interrelationship of sales activity, prices, costs, and profits in

COST-VOLUME-PROFIT ANALYSIS 1. COST-VOLUME-PROFIT (CVP) ANALYSIS CVP analysis, often referred to as break-even analysis, examines the interrelationship of sales activity, prices, costs, and profits in

Standard Cost System Practice Problems

When setting up a standard cost system, the concepts of standards in material, labor, and overhead must be explored in a simple manner to start the process. Practice Standard Cost Variances: Simple Example

When setting up a standard cost system, the concepts of standards in material, labor, and overhead must be explored in a simple manner to start the process. Practice Standard Cost Variances: Simple Example

Statement of Cash Flows (SCF)

") Statement of Cash Flows (SCF) The statement of cash flows (SCF) or cash flow statement reports a corporation's significant cash inflows and outflows that occurred during an accounting period. This financial

Statement of Cash Flows (SCF) The statement of cash flows (SCF) or cash flow statement reports a corporation's significant cash inflows and outflows that occurred during an accounting period. This financial

Exam: RR - Budgeting; Standard Cost Accounting

Exam: 061572RR - Budgeting; Standard Cost Accounting When you have completed your exam and reviewed your answers, click Submit Exam. Answers will not be recorded until you hit Submit Exam. If you need

Exam: 061572RR - Budgeting; Standard Cost Accounting When you have completed your exam and reviewed your answers, click Submit Exam. Answers will not be recorded until you hit Submit Exam. If you need

Page 1. 9 Standard. planning. cost and different. and. activity assumed in. different to $30 for. different particula

Standard Costing By Dr. Michael Constas Page 1 9 Standard Costing: A Functional-Based Control Approach Companies prepare cost budgets as part of their planning process. These budgets assume a given level

Standard Costing By Dr. Michael Constas Page 1 9 Standard Costing: A Functional-Based Control Approach Companies prepare cost budgets as part of their planning process. These budgets assume a given level

This is Appendix B: Extensions of the Aggregate Expenditures Model, appendix 2 from the book Economics Principles (index.html) (v. 2.0).

(v. 2.0).") This is Appendix B: Extensions of the Aggregate Expenditures Model, appendix 2 from the book Economics Principles (index.html) (v. 2.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

This is Appendix B: Extensions of the Aggregate Expenditures Model, appendix 2 from the book Economics Principles (index.html) (v. 2.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a

10 1 Aggregate Expenditure & Income A dollar spent (expenditure) Translates directly into a dollar earned (income) Aggregate expenditure components Consumption, C - varies with income Investment, I - autonomous

10 1 Aggregate Expenditure & Income A dollar spent (expenditure) Translates directly into a dollar earned (income) Aggregate expenditure components Consumption, C - varies with income Investment, I - autonomous

Gleim CMA Review Updates to Part Edition, 1st Printing July 2018

Page 1 of 5 Gleim CMA Review Updates to Part 1 2018 Edition, 1st Printing July 2018 NOTE: Text that should be deleted is displayed with a line through it. New text is shown with a blue background. Study

Page 1 of 5 Gleim CMA Review Updates to Part 1 2018 Edition, 1st Printing July 2018 NOTE: Text that should be deleted is displayed with a line through it. New text is shown with a blue background. Study

Chapter 9 Activity-Based Costing

Chapter 9 Activity-Based Costing SUMMARY This chapter deals with the allocation of indirect costs to products. Product cost information helps managers make numerous decisions, such as pricing, keeping

Chapter 9 Activity-Based Costing SUMMARY This chapter deals with the allocation of indirect costs to products. Product cost information helps managers make numerous decisions, such as pricing, keeping

Grade 8 Exponents and Powers

ID : ae-8-exponents-and-powers [] Grade 8 Exponents and Powers For more such worksheets visit wwwedugaincom Answer the questions ()? (2) Simplify (a -2 + b -2 ) - (3) Simplify 32-3/5 (4) Find value of

ID : ae-8-exponents-and-powers [] Grade 8 Exponents and Powers For more such worksheets visit wwwedugaincom Answer the questions ()? (2) Simplify (a -2 + b -2 ) - (3) Simplify 32-3/5 (4) Find value of

Chapter 23 Performance Evaluation for Decentralized Operations Study Guide Solutions Fill-in-the-Blank Equations. Exercises

Chapter 23 Performance Evaluation for Decentralized Operations Study Guide Solutions Fill-in-the-Blank Equations 1. Service department expense 2. Income from operations 3. Profit margin 4. Invested assets

Chapter 23 Performance Evaluation for Decentralized Operations Study Guide Solutions Fill-in-the-Blank Equations 1. Service department expense 2. Income from operations 3. Profit margin 4. Invested assets

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Variances A variance is the difference between a planned, budgeted, or standard cost and the actual cost incurred.

Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Variances A variance is the difference between a planned, budgeted, or standard cost and the actual cost incurred.

Practice Costing and Operation Control

Note to student: Some of the following activities will require the student to use a calculator. Scenario: You are an accountant for Scrumptious, a large food manufacturing plant, and you work in the accounting

Note to student: Some of the following activities will require the student to use a calculator. Scenario: You are an accountant for Scrumptious, a large food manufacturing plant, and you work in the accounting

Chapter 12 Module 4. AMIS 310 Foundations of Accounting

Chapter 12, Module 4 AMIS 310: Foundations of Accounting Slide 1 CHAPTER 1 MODULE 1 AMIS 310 Foundations of Accounting Professor Marc Smith Hi everyone welcome back! Let s continue our discussion of cost

Chapter 12, Module 4 AMIS 310: Foundations of Accounting Slide 1 CHAPTER 1 MODULE 1 AMIS 310 Foundations of Accounting Professor Marc Smith Hi everyone welcome back! Let s continue our discussion of cost

Chapter 23 Flexible Budgets and Standard Cost Systems

Chapter 23 Flexible Budgets and Standard Cost Systems Review Questions 1. What is a variance? A variance is the difference between an actual amount and the budgeted amount. 2. Explain the difference between

Chapter 23 Flexible Budgets and Standard Cost Systems Review Questions 1. What is a variance? A variance is the difference between an actual amount and the budgeted amount. 2. Explain the difference between

DEPARTMENT OF EDUCATION LEA

Combined Balance Sheet -- All Fund Types and Account Groups Exhibit F-I-A GOVERNMENTAL PROPRIETARY FIDUCIARY ACCOUNT Special Debt Capital Enterp/ GROUPS Description General Revenue Service Projects Internal

Combined Balance Sheet -- All Fund Types and Account Groups Exhibit F-I-A GOVERNMENTAL PROPRIETARY FIDUCIARY ACCOUNT Special Debt Capital Enterp/ GROUPS Description General Revenue Service Projects Internal

DEPARTMENT OF EDUCATION LEA

Combined Balance Sheet -- All Fund Types and Account Groups Exhibit F-I-A GOVERNMENTAL PROPRIETARY FIDUCIARY ACCOUNT Special Debt Capital Enterp/ GROUPS Description General Revenue Service Projects Internal

Combined Balance Sheet -- All Fund Types and Account Groups Exhibit F-I-A GOVERNMENTAL PROPRIETARY FIDUCIARY ACCOUNT Special Debt Capital Enterp/ GROUPS Description General Revenue Service Projects Internal

EXPENDITURE MULTIPLIERS

27 EXPENDITURE MULTIPLIERS After studying this chapter, you will be able to: Explain how expenditure plans are determined Explain how real GDP is determined at a fixed price level Explain the expenditure

27 EXPENDITURE MULTIPLIERS After studying this chapter, you will be able to: Explain how expenditure plans are determined Explain how real GDP is determined at a fixed price level Explain the expenditure

Dr. M.D. Chase Accounting 610 Examination 1 Chapters 1-8,11 Horngren et.al. 15 th. Spring 2011

Exam No: Dr. M.D. Chase Accounting 610 Examination 1 Chapters 1-8,11 Horngren et.al. 15 th Spring 2011 Business ethics are the cornerstone of a successful free enterprise economy. Personal ethics are the

Exam No: Dr. M.D. Chase Accounting 610 Examination 1 Chapters 1-8,11 Horngren et.al. 15 th Spring 2011 Business ethics are the cornerstone of a successful free enterprise economy. Personal ethics are the

5.06 Rationalizing Denominators

.0 Rationalizing Denominators There is a tradition in mathematics of eliminating the radicals from the denominators (or numerators) of fractions. The process is called rationalizing the denominator (or

.0 Rationalizing Denominators There is a tradition in mathematics of eliminating the radicals from the denominators (or numerators) of fractions. The process is called rationalizing the denominator (or

MSM Course 1 Flashcards. Associative Property. base (in numeration) Commutative Property. Distributive Property. Chapter 1 (p.

Commutative Property. Distributive Property. Chapter 1 (p.") 1 Chapter 1 (p. 26, 1-5) Associative Property Associative Property: The property that states that for three or more numbers, their sum or product is always the same, regardless of their grouping. 2 3 8

1 Chapter 1 (p. 26, 1-5) Associative Property Associative Property: The property that states that for three or more numbers, their sum or product is always the same, regardless of their grouping. 2 3 8

BALIUAG UNIVERSITY CPA REVIEW MANAGEMENT ADVISORY SERVICES STANDARD COST AND VARIANCE ANALYSIS THEORY

STANDARD COST AND VARIANCE ANALYSIS THEORY 1. How is labor rate variance computed? a. The difference between standard and actual rate multiplied by actual hours b. The difference between standard and actual

STANDARD COST AND VARIANCE ANALYSIS THEORY 1. How is labor rate variance computed? a. The difference between standard and actual rate multiplied by actual hours b. The difference between standard and actual

VARIANCE ANALYSIS: ILLUSTRATION

VARIANCE ANALYSIS: ILLUSTRATION The following information relates to the production of product Alpha for the month of August Standard Cost Card Budgeted production overhead based on 10,000 units $ $ Selling

VARIANCE ANALYSIS: ILLUSTRATION The following information relates to the production of product Alpha for the month of August Standard Cost Card Budgeted production overhead based on 10,000 units $ $ Selling

Econ 302 Fall Don t forget to download a copy of the Homework Cover Sheet. Mark the location where you handed in your work.

Econ 302 Fall 2005 Don t forget to download a copy of the Homework Cover Sheet. Mark the location where you handed in your work. Homework #3; Chapter 9. This homework has three parts (A, B, C). Each part

Econ 302 Fall 2005 Don t forget to download a copy of the Homework Cover Sheet. Mark the location where you handed in your work. Homework #3; Chapter 9. This homework has three parts (A, B, C). Each part

D This process could be written backwards and still be a true equation. = A D + B D C D

Section 4 2: Dividing Polynomials Dividing Polynomials if the denominator is a monomial. We add and subtract fractions with a common denominator using the following rule. If there is a common denominator

Section 4 2: Dividing Polynomials Dividing Polynomials if the denominator is a monomial. We add and subtract fractions with a common denominator using the following rule. If there is a common denominator

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47

Time: 60 min Marks: 47") MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

MGT402 Short Notes Lecture 23 to 45 By

MGT402 Short Notes Lecture 23 to 45 By http://vustudents.ning.com Lec # 23 PROCESS COSTING SYSTEM (Opening balance of work in process) Two methods of cost allocation (1) The weighted average (or averaging)

MGT402 Short Notes Lecture 23 to 45 By http://vustudents.ning.com Lec # 23 PROCESS COSTING SYSTEM (Opening balance of work in process) Two methods of cost allocation (1) The weighted average (or averaging)

MGT402 - COST & MANAGEMENT ACCOUNTING

MGT402 - COST & MANAGEMENT ACCOUNTING Lesson No. TOPICS Page No. 1 Cost Classification and Cost Behavior 1 2 Important Terminologies 11 3 Financial Statements 15 4 Financial Statements (Continued)....

MGT402 - COST & MANAGEMENT ACCOUNTING Lesson No. TOPICS Page No. 1 Cost Classification and Cost Behavior 1 2 Important Terminologies 11 3 Financial Statements 15 4 Financial Statements (Continued)....

5_MGT402_Spring_2010_Final_Term_Solved_paper

5_MGT402_Spring_2010_Final_Term_Solved_paper http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one BDH produced 30,500 units of Kisty (a product). Each unit of Kisty takes two units

5_MGT402_Spring_2010_Final_Term_Solved_paper http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one BDH produced 30,500 units of Kisty (a product). Each unit of Kisty takes two units

Principles of Macroeconomics Fall Answer Key - Problem Set 1

EC132.01(02) Serge Kasyanenko Principles of Macroeconomics Fall 2005 Answer Key - Problem Set 1 1. Gross Domestic Product, 2004 (millions of current dollars) I. Personal consumption expenditures 8214.3

EC132.01(02) Serge Kasyanenko Principles of Macroeconomics Fall 2005 Answer Key - Problem Set 1 1. Gross Domestic Product, 2004 (millions of current dollars) I. Personal consumption expenditures 8214.3

MGT101- Financial Accounting

MIDTERM EXAMINATION MGT101- Financial Accounting Question No: 1 ( Marks: 1 ) - Please choose one Depreciation arises because of: Fall in the market value of an asset Fall in the value of money Physical

MIDTERM EXAMINATION MGT101- Financial Accounting Question No: 1 ( Marks: 1 ) - Please choose one Depreciation arises because of: Fall in the market value of an asset Fall in the value of money Physical

Warm Up Lesson Presentation Lesson Quiz. Holt Algebra McDougal 1 Algebra 1

1-4 Warm Up Lesson Presentation Lesson Quiz Holt Algebra McDougal 1 Algebra 1 Warm Up Evaluate each expression. 1. 9 3( 2) 15 2. 3( 5 + 7) 6 3. 4 4. 26 4(7 5) 18 Simplify each expression. 5. 10c + c 11c

1-4 Warm Up Lesson Presentation Lesson Quiz Holt Algebra McDougal 1 Algebra 1 Warm Up Evaluate each expression. 1. 9 3( 2) 15 2. 3( 5 + 7) 6 3. 4 4. 26 4(7 5) 18 Simplify each expression. 5. 10c + c 11c

Managerial Accounting Prof. Dr. Varadraj Bapat Department School of Management Indian Institute of Technology, Bombay

Managerial Accounting Prof. Dr. Varadraj Bapat Department School of Management Indian Institute of Technology, Bombay Lecture - 30 Budgeting and Standard Costing In our last session, we had discussed about

Managerial Accounting Prof. Dr. Varadraj Bapat Department School of Management Indian Institute of Technology, Bombay Lecture - 30 Budgeting and Standard Costing In our last session, we had discussed about

FOR MORE PAPERS LOGON TO

MGT402 - Cost & Management Accounting Question No: 1 ( Marks: 1 ) - Please choose one Opportunity cost is the best example of: Sunk Cost Standard Cost Relevant Cost Irrelevant Cost Question No: 2 ( Marks:

MGT402 - Cost & Management Accounting Question No: 1 ( Marks: 1 ) - Please choose one Opportunity cost is the best example of: Sunk Cost Standard Cost Relevant Cost Irrelevant Cost Question No: 2 ( Marks:

MGT101 All Solved Past Papers of Mid Term Exam in one file By

MGT101 All Solved Past Papers of Mid Term Exam in one file By http://vustudents.ning.com MIDTERM EXAMINATION 7 th Dec 2009 MGT101- Financial Accounting Question No: 1 Income of the business includes: Cash

MGT101 All Solved Past Papers of Mid Term Exam in one file By http://vustudents.ning.com MIDTERM EXAMINATION 7 th Dec 2009 MGT101- Financial Accounting Question No: 1 Income of the business includes: Cash

CMA. Financial Reporting, Planning, Performance, and Control

2019 Edition CMA Preparatory Program Part 1 Financial Reporting, Planning, Performance, and Control Manufacturing Input Variances Sample Brian Hock, CMA, CIA and Lynn Roden, CMA HOCK international, LLC

2019 Edition CMA Preparatory Program Part 1 Financial Reporting, Planning, Performance, and Control Manufacturing Input Variances Sample Brian Hock, CMA, CIA and Lynn Roden, CMA HOCK international, LLC

Chapter 17 Appendix A

Chapter 17 Appendix A The Interest Parity Condition We can derive all the results in the text with a concept that is widely used in international finance. The interest parity condition shows the relationship

Chapter 17 Appendix A The Interest Parity Condition We can derive all the results in the text with a concept that is widely used in international finance. The interest parity condition shows the relationship

ACC 202 Final Project Part I Guidelines and Rubric

ACC 202 Final Project Part I Guidelines and Rubric Overview To be successful, all businesses must perform periodic assessments to determine the efficiency of operations. Whether you are an owner, a manager,

ACC 202 Final Project Part I Guidelines and Rubric Overview To be successful, all businesses must perform periodic assessments to determine the efficiency of operations. Whether you are an owner, a manager,

2.01 Products of Polynomials

2.01 Products of Polynomials Recall from previous lessons that when algebraic expressions are added (or subtracted) they are called terms, while expressions that are multiplied are called factors. An algebraic

2.01 Products of Polynomials Recall from previous lessons that when algebraic expressions are added (or subtracted) they are called terms, while expressions that are multiplied are called factors. An algebraic

Adding and Subtracting Rational Expressions

Adding and Subtracting Rational Expressions To add or subtract rational expressions, follow procedures similar to those used in adding and subtracting rational numbers. 4 () 4(3) 10 1 3 3() (3) 1 1 1 All

Adding and Subtracting Rational Expressions To add or subtract rational expressions, follow procedures similar to those used in adding and subtracting rational numbers. 4 () 4(3) 10 1 3 3() (3) 1 1 1 All

The Core of Macroeconomic Theory

PART III The Core of Macroeconomic Theory 1 of 33 The level of GDP, the overall price level, and the level of employment three chief concerns of macroeconomists are influenced by events in three broadly

PART III The Core of Macroeconomic Theory 1 of 33 The level of GDP, the overall price level, and the level of employment three chief concerns of macroeconomists are influenced by events in three broadly

COMPOSED AND SOLVED BY (SADIA ALI) MBA

MBA") MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 3) Time: 60 min Question No: 1 ( Marks: 1 ) - Please choose one Mr. A sold goods to Mr. B for Rs. 3,000 on October 8, 2008 and Mr.

MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 3) Time: 60 min Question No: 1 ( Marks: 1 ) - Please choose one Mr. A sold goods to Mr. B for Rs. 3,000 on October 8, 2008 and Mr.

Unit 1 Theoretical Framework.

Unit 1 Theoretical Framework. A. Answer the Following (1 Mark) 1. What is Accounting equation? 2. Find out the value of assets if: Liabilities=Rs. 5000 and Capital=Rs.1000. 3. Give the classification of

Unit 1 Theoretical Framework. A. Answer the Following (1 Mark) 1. What is Accounting equation? 2. Find out the value of assets if: Liabilities=Rs. 5000 and Capital=Rs.1000. 3. Give the classification of

ACC406 Tip Sheet. 1) Planning: It is the process of creating a set of plans that a company intends to achieve a particular goal.

Planning: It is the process of creating a set of plans that a company intends to achieve a particular goal.") ACC406 Tip Sheet Chapter 1 Managerial Accounting: It is simply the process of reporting accounting information for a company s internal users such as managers, sales staff and etc. for decision making.

ACC406 Tip Sheet Chapter 1 Managerial Accounting: It is simply the process of reporting accounting information for a company s internal users such as managers, sales staff and etc. for decision making.

Job Ready Assessment Blueprint

Blueprint Test Code: 2120 / Version: 01 Financial and Managerial Accounting (Written Only) Specific Competencies and Skills Tested in this Assessment: Journalizing Understand the theory of double entry

Blueprint Test Code: 2120 / Version: 01 Financial and Managerial Accounting (Written Only) Specific Competencies and Skills Tested in this Assessment: Journalizing Understand the theory of double entry

Arithmetic Review: Equivalent Fractions *

OpenStax-CNX module: m2 Arithmetic Review: Equivalent Fractions * Wade Ellis Denny Burzynski This work is produced by OpenStax-CNX and licensed under the Creative Commons Attribution License.0 Abstract

OpenStax-CNX module: m2 Arithmetic Review: Equivalent Fractions * Wade Ellis Denny Burzynski This work is produced by OpenStax-CNX and licensed under the Creative Commons Attribution License.0 Abstract

STATE OF ALABAMA DEPARTMENT OF EDUCATION LEA

LEA Budget System Combined Budget for,, and Changes in Fund Balances Governmental and Expendable Trust Funds Fiscal Year 2018, Fiscal Period 00 047 - Marion County Schools GOVERNMENTAL FIDUCIARY General

LEA Budget System Combined Budget for,, and Changes in Fund Balances Governmental and Expendable Trust Funds Fiscal Year 2018, Fiscal Period 00 047 - Marion County Schools GOVERNMENTAL FIDUCIARY General

Principles of Managerial Accounting

GALILEO, University System of Georgia GALILEO Open Learning Materials Business Administration, Management, and Economics Open Textbooks Business Administration, Management, and Economics Spring 2019 Principles

GALILEO, University System of Georgia GALILEO Open Learning Materials Business Administration, Management, and Economics Open Textbooks Business Administration, Management, and Economics Spring 2019 Principles

Nature of a Budget. Budgets are an important tool for effective short-term planning and control in organizations.

Budget Preparation Nature of a Budget Budgets are an important tool for effective short-term planning and control in organizations. An operating budget usually covers one year and states the revenues and

Budget Preparation Nature of a Budget Budgets are an important tool for effective short-term planning and control in organizations. An operating budget usually covers one year and states the revenues and

Learning Objectives. 1. Describe how the government budget surplus is related to national income.

Learning Objectives 1of 28 1. Describe how the government budget surplus is related to national income. 2. Explain how net exports are related to national income. 3. Distinguish between the marginal propensity

Learning Objectives 1of 28 1. Describe how the government budget surplus is related to national income. 2. Explain how net exports are related to national income. 3. Distinguish between the marginal propensity

2. The budget or schedule that provides necessary input data for the direct-labor budget is the

Student ID: 22099108 Exam: 061683RR - Planning, Performance, Evaluation, and Control When you have completed your exam and reviewed your answers, click Submit Exam. Answers will not be recorded until you

Student ID: 22099108 Exam: 061683RR - Planning, Performance, Evaluation, and Control When you have completed your exam and reviewed your answers, click Submit Exam. Answers will not be recorded until you

REVIEW FOR FINAL EXAM, ACCT-2302 (SAC)

") 1. Types of Cost Classification REVIEW FOR FINAL EXAM, ACCT-2302 (SAC) CHAPTER 16 a. By Behavior: (1) Variable Cost - constant per unit, changes proportionally with volume. (2) Fixed Cost - fixed in total

1. Types of Cost Classification REVIEW FOR FINAL EXAM, ACCT-2302 (SAC) CHAPTER 16 a. By Behavior: (1) Variable Cost - constant per unit, changes proportionally with volume. (2) Fixed Cost - fixed in total

LU4: Accounting for Overhead

LU4: Accounting for Overhead Contents Introduction Applied manufacturing overheads Allocation of manufacturing overheads Learning objectives Define overhead costs Distinguish between manufacturing and

LU4: Accounting for Overhead Contents Introduction Applied manufacturing overheads Allocation of manufacturing overheads Learning objectives Define overhead costs Distinguish between manufacturing and

BUSINESS FINANCIAL BASICS

BUSINESS FINANCIAL BASICS HERE ARE THREE BASIC FINANCIAL STATEMENTS THAT ARE IMPORTANT FOR YOUR SMALL BUSINESS: BALANCE SHEET. P&L. CASHFLOW STATEMENT 1 BALANCE SHEET A financial statement captures a person

BUSINESS FINANCIAL BASICS HERE ARE THREE BASIC FINANCIAL STATEMENTS THAT ARE IMPORTANT FOR YOUR SMALL BUSINESS: BALANCE SHEET. P&L. CASHFLOW STATEMENT 1 BALANCE SHEET A financial statement captures a person

Standard Costs and Variances

10-1 Standard Costs and Variances Chapter 10 10-2 Standard Costs Standards are benchmarks or norms for measuring performance. In managerial accounting, two types of standards are commonly used. Quantity

10-1 Standard Costs and Variances Chapter 10 10-2 Standard Costs Standards are benchmarks or norms for measuring performance. In managerial accounting, two types of standards are commonly used. Quantity

Prentice Hall Connected Mathematics 2, 7th Grade Units 2009 Correlated to: Minnesota K-12 Academic Standards in Mathematics, 9/2008 (Grade 7)

") 7.1.1.1 Know that every rational number can be written as the ratio of two integers or as a terminating or repeating decimal. Recognize that π is not rational, but that it can be approximated by rational

7.1.1.1 Know that every rational number can be written as the ratio of two integers or as a terminating or repeating decimal. Recognize that π is not rational, but that it can be approximated by rational

ACCY 121 Chapter 16 Practice Quiz Fundamentals of Variance Analysis (1)

") ACCY 121 Chapter 16 Practice Quiz Fundamentals of Variance Analysis (1) 101. The Hageness Company has had great difficulty in controlling overhead costs. At a recent convention, the president heard about

ACCY 121 Chapter 16 Practice Quiz Fundamentals of Variance Analysis (1) 101. The Hageness Company has had great difficulty in controlling overhead costs. At a recent convention, the president heard about

IMPORTANT UNITED STATES FEDERAL INCOME TAX INFORMATION CONCERNING THE NOW INC. STOCK DISTRIBUTION

IMPORTANT UNITED STATES FEDERAL INCOME TAX INFORMATION CONCERNING THE NOW INC. STOCK DISTRIBUTION THE INFORMATION AND EXAMPLES SET FORTH HEREIN ARE FOR GENERAL INFORMATION PURPOSES ONLY AND FOR SHAREHOLDERS

IMPORTANT UNITED STATES FEDERAL INCOME TAX INFORMATION CONCERNING THE NOW INC. STOCK DISTRIBUTION THE INFORMATION AND EXAMPLES SET FORTH HEREIN ARE FOR GENERAL INFORMATION PURPOSES ONLY AND FOR SHAREHOLDERS

Aggregate Expenditure and Equilibrium Output. The Core of Macroeconomic Theory. Aggregate Output and Aggregate Income (Y)

") C H A P T E R 8 Aggregate Expenditure and Equilibrium Output Prepared by: Fernando Quijano and Yvonn Quijano The Core of Macroeconomic Theory 2of 31 Aggregate Output and Aggregate Income (Y) Aggregate

C H A P T E R 8 Aggregate Expenditure and Equilibrium Output Prepared by: Fernando Quijano and Yvonn Quijano The Core of Macroeconomic Theory 2of 31 Aggregate Output and Aggregate Income (Y) Aggregate

STATE OF ALABAMA DEPARTMENT OF EDUCATION LEA

LEA Budget System Combined Budget for,, and Changes in Fund Balances Governmental and Expendable Trust Funds Fiscal Year 2018, Fiscal Period 07 047 - Marion County Schools GOVERNMENTAL FIDUCIARY General

LEA Budget System Combined Budget for,, and Changes in Fund Balances Governmental and Expendable Trust Funds Fiscal Year 2018, Fiscal Period 07 047 - Marion County Schools GOVERNMENTAL FIDUCIARY General

Overhead Cost Controlling

Overhead Cost Controlling Objectives To gain understanding of key business processes of SAP Overhead Cost Management (OCM) Understand the Organizational unit in Controlling Determine the origin of posting

Overhead Cost Controlling Objectives To gain understanding of key business processes of SAP Overhead Cost Management (OCM) Understand the Organizational unit in Controlling Determine the origin of posting

Accounting Glossary 1. an equation showing the relationship among assets, liabilities, and

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

Accounting Glossary 1 GLOSSARY A Account a record summarizing all the information pertaining to a single item in the accounting equation. (p. 10) Account balance the amount in an account. (p. 10) Account

2-4 Completing the Square

2-4 Completing the Square Warm Up Lesson Presentation Lesson Quiz Algebra 2 Warm Up Write each expression as a trinomial. 1. (x 5) 2 x 2 10x + 25 2. (3x + 5) 2 9x 2 + 30x + 25 Factor each expression. 3.

2-4 Completing the Square Warm Up Lesson Presentation Lesson Quiz Algebra 2 Warm Up Write each expression as a trinomial. 1. (x 5) 2 x 2 10x + 25 2. (3x + 5) 2 9x 2 + 30x + 25 Factor each expression. 3.

STANDARD COSTS AND VARIANCE ANALYSIS

STANDARD COSTS AND VARIANCE ANALYSIS Key Terms and Concepts to Know Static or Planning Budgets Used for planning purposes Prepared at the beginning of the period Based on one projected level of activity

STANDARD COSTS AND VARIANCE ANALYSIS Key Terms and Concepts to Know Static or Planning Budgets Used for planning purposes Prepared at the beginning of the period Based on one projected level of activity

Accounting Principles: A Business Perspective, 8e Chapter 1: Accounting and Its Use in Business Decisions

Accounting Principles: A Business Perspective, 8e Chapter 1: Accounting and Its Use in Business Decisions Forms of Business Organizations A business entity is any business organization that exists as an

Accounting Principles: A Business Perspective, 8e Chapter 1: Accounting and Its Use in Business Decisions Forms of Business Organizations A business entity is any business organization that exists as an

1.4. Arithmetic of Algebraic Fractions. Introduction. Prerequisites. Learning Outcomes

Arithmetic of Algebraic Fractions 1.4 Introduction Just as one whole number divided by another is called a numerical fraction, so one algebraic expression divided by another is known as an algebraic fraction.

Arithmetic of Algebraic Fractions 1.4 Introduction Just as one whole number divided by another is called a numerical fraction, so one algebraic expression divided by another is known as an algebraic fraction.

Spring Manufacturing Company Sales Budget 2007

8-56 Comprehensive Profit Plan (90 minutes) 1. Sales Budget Sales Budget Sales (in units) 12,000 9,000 21,000 x Selling Price Per Unit $150 $220 Total Sales Revenue $1,800,000 $1,980,000 $3,780,000 2.

8-56 Comprehensive Profit Plan (90 minutes) 1. Sales Budget Sales Budget Sales (in units) 12,000 9,000 21,000 x Selling Price Per Unit $150 $220 Total Sales Revenue $1,800,000 $1,980,000 $3,780,000 2.

Chapter 8 Aggregate Expenditure and Equilibrium Output. Kazu Matsuda IBEC 203 Macroeconomics

Chapter 8 Aggregate Expenditure and Equilibrium Output Kazu Matsuda IBEC 203 Macroeconomics AGGREGATE OUTPUT AND AGGREGATE INCOME (Y)( = The total quantity of goods and services produced (or supplied)

Chapter 8 Aggregate Expenditure and Equilibrium Output Kazu Matsuda IBEC 203 Macroeconomics AGGREGATE OUTPUT AND AGGREGATE INCOME (Y)( = The total quantity of goods and services produced (or supplied)

COPYRIGHT PAGE. Published by: Flat World Knowledge, Inc th St NW Washington, DC 20036

COPYRIGHT PAGE Published by: Flat World Knowledge, Inc. 1111 19 th St NW Washington, DC 20036 2016 by Flat World Knowledge, Inc. All rights reserved. Your use of this work is subject to the License Agreement

COPYRIGHT PAGE Published by: Flat World Knowledge, Inc. 1111 19 th St NW Washington, DC 20036 2016 by Flat World Knowledge, Inc. All rights reserved. Your use of this work is subject to the License Agreement

CHAPTER 8 FLEXIBLE BUDGETS, OVERHEAD COST VARIANCES, AND MANAGEMENT CONTROL

CHAPTER 8 FLEXIBLE BUDGETS, OVERHEAD COST VARIANCES, AND MANAGEMENT CONTROL 8-1 Effective planning of variable overhead costs involves: 1. Planning to undertake only those variable overhead activities

CHAPTER 8 FLEXIBLE BUDGETS, OVERHEAD COST VARIANCES, AND MANAGEMENT CONTROL 8-1 Effective planning of variable overhead costs involves: 1. Planning to undertake only those variable overhead activities

11-3. IWBAT solve equations with variables on both sides of the equal sign.

IWBAT solve equations with variables on both sides of the equal sign. WRITE: Some problems produce equations that have variables on both sides of the equal sign. Solving an equation with variables on both

IWBAT solve equations with variables on both sides of the equal sign. WRITE: Some problems produce equations that have variables on both sides of the equal sign. Solving an equation with variables on both

SOLVING EQUATIONS ENGAGE NY PINK PACKET PAGE 18

SOLVING EQUATIONS ENGAGE NY PINK PACKET PAGE 18 INEQUALITIES SPRINT #2 You will have 3 minutes to complete as many problems as possible. As soon as the bomb goes off, submit!!! Winner= Person with the

SOLVING EQUATIONS ENGAGE NY PINK PACKET PAGE 18 INEQUALITIES SPRINT #2 You will have 3 minutes to complete as many problems as possible. As soon as the bomb goes off, submit!!! Winner= Person with the

MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2)

") MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Particulars Rs. Opening written down value of machine 1,00,000 Cost of new machine

MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Particulars Rs. Opening written down value of machine 1,00,000 Cost of new machine

Gehrke: Macroeconomics Winter term 2012/13. Exercises

Gehrke: 320.120 Macroeconomics Winter term 2012/13 Questions #1 (National accounts) Exercises 1.1 What are the differences between the nominal gross domestic product and the real net national income? 1.2

Gehrke: 320.120 Macroeconomics Winter term 2012/13 Questions #1 (National accounts) Exercises 1.1 What are the differences between the nominal gross domestic product and the real net national income? 1.2

Measuring the Production, Income, and Spending of Nations

6 Measuring the Production, Income, and Spending of Nations A Precise Definition of GDP GDP: a measure of the value of all newly produced 1 goods and services in a country 2 during some period of time

6 Measuring the Production, Income, and Spending of Nations A Precise Definition of GDP GDP: a measure of the value of all newly produced 1 goods and services in a country 2 during some period of time

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Prentice Hall Connected Mathematics, Grade 7 Unit 2004 Correlated to: Maine Learning Results for Mathematics (Grades 5-8)

") : Maine Learning Results for Mathematics (Grades 5-8) A. NUMBERS AND NUMBER SENSE Students will understand and demonstrate a sense of what numbers mean and how they are used. Students will be able to:

: Maine Learning Results for Mathematics (Grades 5-8) A. NUMBERS AND NUMBER SENSE Students will understand and demonstrate a sense of what numbers mean and how they are used. Students will be able to:

Livelihood Development via Agro-Processing SFA2006 (GCP/RLA/167/EC) Location: Grenada

Location: Grenada") Business Skills Workshop #9 Wednesday, July 14, 2010 & July 21, 2010 Business Skills Training Handbook Livelihood Development via Agro-Processing SFA2006 (GCP/RLA/167/EC) Location: Grenada Dr. Reccia Charles

Business Skills Workshop #9 Wednesday, July 14, 2010 & July 21, 2010 Business Skills Training Handbook Livelihood Development via Agro-Processing SFA2006 (GCP/RLA/167/EC) Location: Grenada Dr. Reccia Charles

ECON 120 -ESSENTIALS OF ECONOMICS

Name ECON 120 -ESSENTIALS OF ECONOMICS CH 24 THE GOVERNMENT AND FISCAL POLICY MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Fiscal policy refers

Name ECON 120 -ESSENTIALS OF ECONOMICS CH 24 THE GOVERNMENT AND FISCAL POLICY MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Fiscal policy refers

Performance Analyzer Formulas. Assumptions. Current Month Adjustments

User's Guide for PA for Windows Error! No text of specified style in document. 1 Performance Analyzer Formulas Assumptions Current Month Adjustments Current Period values (BCWS, BCWP, ACWP) are derived

User's Guide for PA for Windows Error! No text of specified style in document. 1 Performance Analyzer Formulas Assumptions Current Month Adjustments Current Period values (BCWS, BCWP, ACWP) are derived

Reducing Maintenance Costs Using Beyond Economic Repair Analysis

Reducing Maintenance Costs Using Beyond Economic Repair Analysis Jerry Le May Multi-Discipline Engineer June 2011 Copyright 2010 Raytheon Company. All rights reserved. Customer Success Is Our Mission is

Reducing Maintenance Costs Using Beyond Economic Repair Analysis Jerry Le May Multi-Discipline Engineer June 2011 Copyright 2010 Raytheon Company. All rights reserved. Customer Success Is Our Mission is

Chapter 6 Overheads & Absorption Costing. Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing)

") Chapter 6 Overheads & Absorption Costing Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Overheads Overheads is the cost incurred in the course of making a product,

Chapter 6 Overheads & Absorption Costing Ibrahim Sameer (MBA - Specialized in Finance, B.Com Specialized in Accounting & Marketing) Overheads Overheads is the cost incurred in the course of making a product,

FI3300: CORPORATE FINANCE. Problem Set 1 Chapters 1-5

FI3300: CORPORATE FINANCE Problem Set 1 Chapters 1-5 1. The goal of the firm is to. a. maximize profit b. minimize risk c. promote social good d. maximize shareholder wealth 2. Which of the following would

FI3300: CORPORATE FINANCE Problem Set 1 Chapters 1-5 1. The goal of the firm is to. a. maximize profit b. minimize risk c. promote social good d. maximize shareholder wealth 2. Which of the following would

Polynomial and Rational Expressions. College Algebra

Polynomial and Rational Expressions College Algebra Polynomials A polynomial is an expression that can be written in the form a " x " + + a & x & + a ' x + a ( Each real number a i is called a coefficient.

Polynomial and Rational Expressions College Algebra Polynomials A polynomial is an expression that can be written in the form a " x " + + a & x & + a ' x + a ( Each real number a i is called a coefficient.

RECHARGE Frequently Asked Questions

RECHARGE Frequently Asked Questions This is a living document and is continually edited and updated. We welcome your feedback and contributions. General Information: Q: What is a 21 account? A: A 21 account,

RECHARGE Frequently Asked Questions This is a living document and is continually edited and updated. We welcome your feedback and contributions. General Information: Q: What is a 21 account? A: A 21 account,

Slide Contents. Chapter 12. Analyzing Project Cash Flows. Learning Objectives Principles Used in This Chapter. Key Terms

Chapter 12 Analyzing Project Cash Flows Slide Contents Learning Objectives Principles Used in This Chapter 1.Identifying Incremental Cash Flows 2.Forecasting Project Cash Flows 3.Inflation and Capital

Chapter 12 Analyzing Project Cash Flows Slide Contents Learning Objectives Principles Used in This Chapter 1.Identifying Incremental Cash Flows 2.Forecasting Project Cash Flows 3.Inflation and Capital

Here are the steps required for Adding and Subtracting Rational Expressions:

Here are the steps required for Adding and Subtracting Rational Expressions: Step 1: Factor the denominator of each fraction to help find the LCD. Step 3: Find the new numerator for each fraction. To find

Here are the steps required for Adding and Subtracting Rational Expressions: Step 1: Factor the denominator of each fraction to help find the LCD. Step 3: Find the new numerator for each fraction. To find

Fall 2017 COT 3100 Final Exam Part A. Last Name:, First Name:

Fall 2017 COT 3100 Final Exam Part A Last Name:, First Name: 1) (8 pts) It takes Bob six days to paint their townhouse, and it takes Carol ten days to paint their townhouse. For the purposes of this problem,

Fall 2017 COT 3100 Final Exam Part A Last Name:, First Name: 1) (8 pts) It takes Bob six days to paint their townhouse, and it takes Carol ten days to paint their townhouse. For the purposes of this problem,

45 Line -The height of this measures disposable income

Fixed Prices and Expenditure Plans -In the Keynesian model, all firms are like the grocery store: They set their prices and sell the quantities their customers are willing to buy -If they persistently

Fixed Prices and Expenditure Plans -In the Keynesian model, all firms are like the grocery store: They set their prices and sell the quantities their customers are willing to buy -If they persistently

Let s trace the budgets through for a company called the Hayes Company. Sales Budget The first budget prepared, comes from the Sales Forecast

Let s trace the budgets through for a company called the Hayes Company. Sales Budget The first budget prepared, comes from the Sales Forecast Expected sales volume: 3,000 units in the first quarter with

Let s trace the budgets through for a company called the Hayes Company. Sales Budget The first budget prepared, comes from the Sales Forecast Expected sales volume: 3,000 units in the first quarter with

In understanding the behavior of aggregate demand we must take a close look at its individual components: Figure 1, Aggregate Demand

The Digital Economist Lecture 4 -- The Real Economy and Aggregate Demand The concept of aggregate demand is used to understand and measure the ability, and willingness, of individuals and institutions

The Digital Economist Lecture 4 -- The Real Economy and Aggregate Demand The concept of aggregate demand is used to understand and measure the ability, and willingness, of individuals and institutions

Standard 4 pounds Quantity $ 7.50/pound Standard Cost $30.00

Part 1 Study Unit 7 Fausto Company employs a standard cost system in which direct materials inventory is carried at standard cost. The company has established the following standard for the materials costs

Part 1 Study Unit 7 Fausto Company employs a standard cost system in which direct materials inventory is carried at standard cost. The company has established the following standard for the materials costs