Environmental Regulation through Voluntary Agreements

|

|

|

- Tracy Robertson

- 6 years ago

- Views:

Transcription

1 MPRA Munich Personal RePEc Archive Environmental Regulation through Voluntary Agreements Lars Gårn Hansen 1997 Online at MPRA Paper No , posted 11. June :29 UTC

2 Environmental Regulation through Voluntary Agreements (Paper prepared or the workshop on The Economics and Law o Voluntary Approaches in Environmental Policy November 1996, Fondazione Levi, Venezia) Lars Gårn Hansen AKF (Institute o Local Government Studies - Denmark) November 1996 The research leading to this paper is a joint product o the SØM-project 'Complex Regulation Problems' and the AKF-project 'Voluntary Agreements' and has been unded by The Danish Environmental Research Programme and The Danish Energy Research Programme. I thank Peter Munk Christiansen, Signe Krarup, Anders Larsen and Birgitte Sloth or many helpul comments and suggestions. Please address all correspondence to Lars Gårn Hansen, AKF, Nyropsgade 37, DK Copenhagen V, Denmark (pho: , ax: , LGH@AKF.DK). 1

3 Abstract Voluntary agreements with polluting industries are becoming a popular alternative to traditional environmental regulation. One reason may be that voluntary agreements can reduce compliance costs o polluting industries. In this paper we develop a amily o simple policy ormulation and implementation models enabling us to ormally characterize the policy environments that make voluntary agreements possible. The main message o this paper is one o caution. Voluntary agreements that increase compliance costs and reduce social welare can not be ruled out. The analyses also suggests that giving the legislative branch o government an eective power o veto reduces (but does not eliminate) the possibility o welare reducing voluntary agreements. 2

4 1. Introduction The purpose o this paper is to propose and analyse simple economic models describing the regulatory policy approach known as voluntary agreements. The term voluntary agreements attempts to capture the idea that environmental goals and/or instruments o implementation are negotiated with the irms to be regulated prior to implementation or at least that there is some reedom o choice (or the regulated irms) with respect to which regulatory scheme a irm is to be submitted. Beore deining the concept more precisely we will discuss the related concept voluntary regulatory instruments. The term voluntary regulatory instruments (or voluntary approaches) is used to characterize a wide range o inormational and motivational policy instruments which can be divided into three main groups: voluntary instruments that do not involve the public directly, so-called voluntary instruments involving the public and so-called voluntary instruments allowing irms some spectrum o choice as to which regulatory scheme they are to be submitted (see IEA (1995) or an international review o existing schemes or energy eiciency). Voluntary regulatory instruments that do not involve the public directly include energy auditing schemes, promotion o energy savings, promotion o technologies, golden carrot programmes (e.g. subsidizing development and implementation o energy saving products and technologies) and other 'sot' policy instruments. These programmes can be understood as subsidizing development or supply o preerred technologies and subsidies or provision o certain types o costly inormation to irms. The industry s reactions caused by such schemes are no more voluntary than those caused by taxes or other incentive-based regulatory instruments. However, subsidy based instruments have non-negative net income eects or polluting irms, implying that the regulator de acto accepts that irms have the right to pollute. Since polluting irms then have no reason to oppose implementation o such policies they may be said to be more voluntary or irms in this respect. Another class o voluntary regulatory instruments ocuses on channeling credible inormation on irms environmental perormance to the general public (e.g. US EPA's 33/50 program, UK and New Zealand 'corporate commitment' schemes). Economically these schemes are subsidies or provision o credible inormation bringing environmental perormance o irms into the competitive ringe. An environmental dimension is added to irm products which, depending on the weight potential buyers attach to it, may induce better environmental perormance by irms. These schemes are ormally voluntary, but the ensuing competition among irms may well reduce the average proitability in the sector in question (see Arora and Cason (1995) and Arora and Gangopadhyay (1994) or theoretical and empirical analysis o such schemes). Finally, the term 'voluntary instruments' is also used or advanced versions o 'hard' regulatory instruments that e.g. speciy that a irm may be exempt rom standard regulation i it agrees to undertake alternative measures to achieve the same goals. 3

5 These are sophisticated regulatory instruments where irms implicitly reveal private inormation to the regulator by choosing rom a menu o regulatory contracts. I designed correctly regulatory schemes oering irms a choice o dierent regulatory contracts rather than just imposing one uniorm contract on all irms may increase regulatory eiciency (see e.g. Laont and Tirole (1993) or an exposition o applications o contract theory to regulatory economics). In this paper we will not consider the voluntary regulatory instruments. Instead we will understand the term voluntary agreements as characterizing another way o structuring the process, through which environmental goals are ormulated and instruments o implementation are decided on. In other words the voluntary agreement process is one way to organize the game o policy ormulation, while the 'traditional policy ormulation process' is another. The outcome o a voluntary agreement process can in principle be the same environmental goals implemented through the same regulatory instruments as would have been the outcome o a traditional policy ormulation process. However, i the voluntary agreement process is substantially dierent one would expect a dierent policy outcome and thus dierent distributional and social welare eects. In the next section I discuss the voluntary agreement process and the traditional policy ormulation process and propose three central dierences. In the ollowing sections I propose and analyse ormal models incorporating these dierences. The analysis indicates under which conditions voluntary agreements may occur and which changes in distributional and social welare eects the resulting environmental regulation may cause. The approach used in this paper is traditional neoclassic economic analysis. We assume ixed preerences or all agents and that utility is derived rom end states only. It is worth noting that when considering alternative negotiation and decision-making processes these assumptions may be critical. It can be argued that preerence learning and utility derived rom a participatory process are central aspects o voluntary agreements. Through the process irms may learn that they have greater preerence or environmental improvement than they were aware o beore and irms may be willing to pay or the opportunity o a participatory process by accepting end states that are considered less desirable in themselves. 4

6 2. Characteristics Distinguishing Policy Formulation through Voluntary Agreement rom the Traditional Policy Formulation Process Describing the interaction between political players during the policy ormulation and implementation process is the subject o much o the political science literature and a growing body o economic literature on public choice and agency capture. In the ollowing I propose a simplistic description o the traditional policy process and the voluntary agreement process based on empirical surveys (e.g. IEA (1995), Glachant (1994)) which point to the key dierences to be modelled in the ollowing sections. The traditional process consists o legislation on regulatory instruments where implementation and administration o these instruments are delegated to a regulatory agency. While environmental policy goals may be contested and subject to negotiation the real battle is over legislation on regulatory instruments. These usually require a legislative process with direct participation o the executive branch o Government (hereater just called Government) and the legislative bodies o Government (hereater called Congress). Aected industrial organizations and other interest groups are normally consulted by Government as well as Congress and may indirectly inluence the process. Voluntary agreements generally only have Government agencies and individual irms or industrial organizations (hereater also denoted IOs) as direct participants. Normally, agreements do not result in legislation. Firms or IOs commit to targets and monitoring procedures, but not necessarily to speciic instruments or methods o implementation. Normally, no ormal sanctions or non-attention o targets are speciied. One apparent dierence between the two policy ormulation processes is that Congress participates directly in the traditional process, but is excluded rom direct participation in the voluntary process. Instead IOs are elevated to a role as direct participants. Clearly, other (e.g. environmental) interest groups (hereater also denoted IGs) and Congress may still indirectly inluence the voluntary policy process. When considering voluntary agreements with industrial organizations (on which we will ocus in the ollowing) another novelty is that implementation o environmental goals or agreed on instruments is let to the industrial organizations rather than to public agencies. This can be seen as a necessary consequence o not involving Congress directly since implementation by traditional regulatory instruments through Government agencies normally would require passing o legislation. Though regulatory agencies may still have a role as monitors o the agreed targets Governments must contract with industrial organizations or implementation. Thus the responsibility or and practical implementation o regulatory instruments are shited to industrial organizations - oten the choice o instruments o implementation is let to the Ios, too. The reward to IOs or implementing environmental targets is usually implicit in the agreement. One possibility is that Government promises not to push or legislation implementing some kind o traditional regulation i targets are met. Though 5

7 IOs may be able to implement eective regulatory instruments vis-à-vis member irms the issue o credibility o Government threats/promises and IO compliance with the negotiated targets is relevant. Just as implementation through IOs is a logical consequence o excluding Congress rom direct participation so is the voluntary agreement process what makes implementation through IOs possible. I IOs are to take responsibility or implementation Government must o course negotiate an agreement with them. Thus the aim o Governments engaging in a voluntary agreement process need not be the exclusion o Congress, but may instead be to shit the responsibility o implementation to IOs (possibly with the ull support o Congress). In conclusion voluntary agreements can be seen as a policy process with three central characteristics: 1) Congress is no longer a direct participant in the policy ormulation process - instead irms or IOs become direct participants. 2) Responsibility or implementation o regulation is shited to industrial organizations 3) Statutory sanctions ensuring IO participation and compliance are not possible under voluntary agreements. Instead IOs must be induced to comply through e.g. threats o new regulation in the area covered by the agreement. The question o what government credibly can threaten to do arises. The presumption in the ollowing is that Government or opposition parties are able to initiate the traditional policy ormulation process (involving Congress) in any area o regulation, but that once the process is started it can only to some extent inluence the end result. Government is also able to block initiation o the traditional policy ormulation process by opposition parties by entering into a voluntary agreement. In other words Government may choose between entering into a voluntary agreement or initiating a legislative process. To resolve the credibility-compliance issue we will assume that Government threats o imposing punishment (i.e. pushing or legislation or harsher administration o existing legislation) which also reduces the utility o Government are not credible. In other words the only credible Government threat is that o utility maximizing behaviour given that no agreement is made (i.e. Government cannot expropriate utility rom irms by threatening death and destruction). To induce irms to comply with the conditions o a voluntary agreement Government must allot irms at least the same utility that they would have had i Government maximized its utility without a voluntary agreement. We thus assume that there must be mutual gains to trade or an agreement to be made which then also insures irm and Government compliance. In the next three sections we consider voluntary agreements with industrial organizations. In section 3 we develop a model without interest group signalling power ocusing on dierences in policy goals between Congress and Government. In sections 4 and 5 models with interest group signalling power ocusing on the shit o 6

8 responsibility or goal ormulation and or implementation are developed and in section 6 conclusions are drawn. 3. Voluntary Agreements when Interest Groups do not have Signalling Power In this section we speciy a model without interest group inluence through public criticism and ind necessary conditions or use o voluntary agreements. These conditions allow us to characterize the possible environmental and welare eects o voluntary agreements. The model has three active agents: the IO representing polluting irms (hereater also just called the irm), the Government and the Congress. Government may initiate the traditional policy ormulation process through Congress or enter a voluntary agreement process with the IO. Both policy ormulation processes result in the setting o an environmental goal denoted R (indicating amount by which environmental damage is to be reduced) and a tax revenue goal indicating the amount o revenue to be collected through regulatory instruments). Implementation o these goals through the available regulation technology results in irm compliance costs denoted C in addition to the tax revenue payment. Let U denote the utility eect on the irm o regulation and deine: U ' &T & C Government and Congress are both assumed to take into account the utility eects o regulation on the irm, the environmentally concerned part o the public and the part o the public that might beneit rom increased tax revenues. However, they may dier in the relative weights attached to these groups in their respective utility unction. Let U c and U g denote the utility eects o regulation on Congress and Government respectively and deine: U c ' U % 8 c T % * c R U g ' U % 8 g T % * g R where 8c and 8 g are the utility weights attached to tax revenue by Congress and Government respectively, * c and * g are the utility weights attached to environmental damage reduction. We make the natural assumptions 8 c > 0, 8 g > 0, * c > 0, * g > 0. 7

9 The negotiation process between Government and Congress under the traditional policy ormulation process is not modelled explicitly. Instead the utility unction o Congress should be interpreted as representing the result o this process incorporating the relative power o Government and opposition parties in Congress. I Government s utility unction parameters are equal to the parameters o Congress utility unction this implies agreement between Government and opposition parties or a large relative Governmental negotiation power while unequal parameters indicate disagreement and low Government party negotiation power in Congress. The traditional policy process sets goals that are implemented through traditional Government policy instruments. Let C(R, T) describe the irm compliance costs that result when goals are implemented through the available regulation technology. We assume C R > 0, C RR > 0 (i.e. positive and rising marginal compliance cost o damage reduction) and C T $ 0, C TT $0 (i.e. non-negative and non-alling dead-weight loss o tax revenue collection). Underlying the dead-weight loss assumptions is an assumption that tax revenue (e.g. rom environmental tax) can be redistributed to polluting irms through a cost less lump sum scheme. Thus we assume that increasing revenue is possible without dead-weight loss up to the level o revenue implemented by a perect emission tax and that i revenue increases above this level it results in dead-weight loss. Correspondingly, we assume that C RT # 0 (i.e. that marginal compliance costs are non-increasing in collected revenue). Note that the compliance cost unction allows or the possibility that irms as a group derive beneit rom environmental damage reduction (e.g. cost reducing eects o reduced environmental damage). Thus the traditional policy ormulation process is assumed to be described by the ollowing maximization problem: Max R,T U c under C ' C(R,T) the solution to which is denoted R and T. * * Agent utilities with the traditional regulation process become: U ( ' & & C(R (, ) (1) 8

10 The irst order conditions rom step 1 imply U ( c ' U ( % 8 c % * c R ( (2) U ( g ' U( % 8 g % * g R ( (3) C R ' * c (4) and C T ' 8 c & 1 (5) In the voluntary agreement process goals R, T are set through negotiations between Government and the IO and then implemented by the IO. Thus the industrial organization representing irms is assumed to have a regulatory technology vis-à-vis its members with which it can ensure attainment o the environmental goals. Clearly, public tax revenues are not generated (i.e. T ' 0 ). We urther assume that the regulatory technology is described by the unctions C (cr, T) where T = 0. Thus by assumptions the two regulatory technologies are identical save or the cost parameter c and the constraint that T = 0 under IO implementation. This simpliies the ollowing derivations while capturing the essential dierence in relative implementation eiciency through a single parameter c, indicating the relative cost o IOimplementation. Agent utilities under the voluntary agreement process become: Ũ ' &C(c R, 0) (6) Ũ c ' Ũ % * c R (7) Ũ g ' Ũ % * g R (8) 9

11 I the agents utility unctions, the C unction, the c parameter are public inormation * * the result o the traditional policy process R,T can be predicted by Government as well as the irm. Given this, a necessary condition or a voluntary agreement is that both parties to the agreement experience a non-negative utility gain vis-à-vis the traditional policy process which both parties know is the alternative. In other words a non-empty set o goals ( R ) must exist or which both the ollowing individual rationality constraints are satisied: IR-irm: Ũ ' &C(c R, 0) $ & & C(R (, ) ' U ( (9) IR-Government: Ũ g ' Ũ % * g R $ U ( % 8 g % * g R ( ' U ( g (10) In the ollowing we wish to ind the set o parameter tuples (* g, 8 g) that or a given tuple o parameter (* c, 8 c, c) allows a non-empty set o ( R ) satisying both IR constraints. In other words we wish to characterize the set o parameter tuples (* g, 8 g) that makes voluntary agreements possible (hereater called the VA-set). On the border o the VA-set one or both IR constraints are satisied with equality. For suiciently small * g the R that maximizes Government utility Ũ g will be small enough so that irm utility is not exhausted (i.e. the irm IR constraint is not binding). In this area the relationship between 8 g and * g at the set border must satisy (10) with equality and R is set to maximize Ũ g. The equation characterizing the relationship between 8 g, and * g on the part o the set border where the irm constraint is not binding becomes: 8 g ' R & R ( * g % (Ũ ( & U ) (11) where R is set to maximize Ũ g so that the ollowing 1. order condition (derived rom (8)) holds: * g ' C R c (12) 10

12 As * g increases the Ũ g -maximizing R rises and at some point irm utility is exhausted and both constraints must be satisied. Using (9) on (11) we ind the equation characterizing the relationship between 8 g, and * g on the part o the set border where both Government and irm constraints are binding to be: 8 g ' R & R ( * g (13) with (rearranging (9)): R ' C &1 ([ % C(R (, )], 0)/c (14) The VA-set Border As noted, when * g is suiciently small the irm constraint does not bind and the R exhausting irm utility is deemed too high by Government so that reducing R increases utility o both agents. In this area only the IR Government constraint (11) binds. Total dierentiation o (11) with respect to * g and 8 g gives d8 g % R ( d* g ' &C R c d R d* g d* g % Rd* g % * g d R d* g d* g (15) Since R is set to maximize Ũ g we have C R c ' * g so that (15) reduces to: d8 g d* g ' R & R ( (16) Since R is set to maximize Ũ g we know that d R/d* g > 0 so that (11) is a convex curve initially (or small * g ) downward sloping in the * g -8g-plane. It then attains a minimum when R ' R ( and slopes up again. It is apparent that (* c, 8 c) is not in the VA-set when c>1. From (4) we know that C R (R (, ) ' * c and rom (12) we know that C R (c R,0)c ' * g so that or * g=c* we have: c 11

13 C R (R (, ) ' C R (c R,0) (17) and by C <0 and C RT RR >0 we have: * g ' c* c Y c R < R ( (18) This implies that when c is close to 1 (11) has its minimum at a * g value below * c and that or * g ' * c we have R > R (. However, i c is large enough (11) has its minimum at a * g value above * c and then R < R ( or * g ' * c. Now consider the part o the set border where both IR constraints bind satisying (13) and (14). Note that equation (14) implies that there is a unique R or which compliance costs under the voluntary agreement technology just exhaust the gain rom * * not having to pay taxes T and abating to R under the traditional regulatory technology. Thus R only depends on the irm s alternative income and is thus independent o Government utility unction parameter * g and 8 g.we see rom (13) that the set border here is a line through origo with slope: ( R & R ( )/. From (13) and (16) we see that or all border tuples where the associated border slope is negative the corresponding voluntary agreement is characterised by R < R ( and or tuples with a positive associated slope the corresponding voluntary agreement is characterised by R > R (. The above observations allow us to illustrate the set border. In igure 1 three possible set borders are illustrated or c>1 (i.e. no compliance cost advantage).the part o the parameter space in which voluntary agreements are possible is the part o the * g - 8 g plane below the set border. We know that when c>1 the set deined by the border does not include (* c,8 c ) and that the boarder or small * g (where the irm constraint does not bind) is negatively sloped and convex. When c is close to one the boarder may attain its minimum (marked by a square) beore the irm constraint binds and at a * g below * c (as in the highest placed o the three illustrated border lines).when c is large the boarder equation has no minimum (as in the lowest o the three illustrated border lines) or attains its minimum or a * g above * c (as in the middle border line). 12

14 Fig. 1

15 The VA-set Interior: Nash Bargaining Solutions In this subsection we apply the Nash bargaining solution to the negotiation problem presented above thus allowing us to characterize the result o the voluntary agreement process in the interior o the VA-set where the set o easible agreements is not a singleton (see e.g. Osborne and Rubinstein (1990) or a presentation o and reerences to the literature on bargaining models and their applications). The asymmetric Nash bargaining solution is the agreement that maximizes the Nash product: (Ũ &U 0 )" (Ũ g &U 0 g )(1&") (19) where U 0,U 0 g are appropriate alternative beneits to the parties and " is a parameter that can be loosely interpreted as expressing relative bargaining power o the two agents. Initially we briely review two speciications o the underlying dynamic negotiation game that implement the Nash bargaining solution and important implications or speciication and interpretation o the Nash bargaining solution that were pointed out by Binmore, Rubinstein and Wolinsky (1986). 13

16 The underlying bargaining process is in both cases assumed to be a game o alternating oers. For such a game to have a unique solution agents must experience costs in connection with continuation o the bargaining process. Binmore et al. point out that such a game may be driven by impatience or by risk and in both cases result in implementation o the Nash bargaining solution when the cost per negotiation step goes to zero. In the irst case the dominant cost o bargaining is the delay o payo that continued negotiation causes. I agents are impatient to reap the rewards o a bargain each new bargaining step entails a cost in that it postpones the payo entailed by an agreement. In this case agent utility unctions relect time preerences, and the relevant alternative beneits are the beneits accruing to agents during the bargaining process. In the second case the dominant cost associated with bargaining is not the delay o payo caused, but that continued negotiation encompasses an external risk o losing the bargain opportunity altogether (the preposition <external indicates that the risk is uncontrolled by the negotiating parties). Each new bargaining step entails a cost in prolonging the period that the agents are subject to the external risk o losing the opportunity o payo though an agreement - a risk that can only be eliminated by entering into an agreement. In this case the agent utility unctions relect risk aversion and the relevant alternative beneits are the beneits that agents would attain i the opportunity o an agreement were to be lost (and not the beneits actually accruing during negotiation). Here the exogenous risk model seems an obvious choice or the underlying negotiation game or two reasons: 1) there is a risk that the traditional legislative process may be initiated by opposition parties thus eliminating the opportunity o a voluntary agreement, and 2) irms (that are net losers vis-à-vis the unregulated state in either case) cannot as such be impatient or an agreement. This implies that the relevant alternative beneit is the beneit expected to result rom initiation o the traditional legislative process (and not the beneits resulting rom the current unregulated situation as would be the case i the negotiation process were driven by impatience). The thus speciied Nash product is: (Ũ )" (Ũ g g )(1&") (20) Speciying "=1/2 (the symmetric solution) is tempting since dierences in risk aversion are embedded in the utility unctions and thereore cannot motivate use o an asymmetric bargaining solution (in our case both agents have linear (i.e. risk neutral) 1 utility unctions. The asymmetric bargaining solution can, however, be motivated by dierences in the perception o the exogenous risk o break down o negotiations (i.e. 1) Introducing dierences in risk aversion into the model can be done by letting irm utility be a convex unction o monetary costs. This complicates derivation somewhat, but does not essentially change the model. 14

17 dierences in the perception o the risk o opposition parties initiating the traditional policy process) or by asymmetries in the bargaining process itsel (e.g. the time allotted or responding to oers etc.) both o which seem plausible in our case. In the ollowing we thereore uphold the general asymmetric speciication. The irst order condition or maximising (20) with respect to R is: "(Ũ )("&1) dũ (Ũ g g d R )(1&") % (Ũ )" (" & 1)(Ũ g g )&" dũ g d R ' 0 which reduces to: (Ũ g g ) ' (Ũ ) (1&") " (dũ g /d R) &(dũ /d R) Inserting the deinitions o Ũ g, U ( g, Ũ, U ( we have: 8 g ' R & R ( % (Ũ ) * g & (Ũ ( & U ) (1&") " % 1 (1&") "cc R * g (21) The equation deines R as a unction o model parameters and or ixed R it deines the equation or isoquants (iso- R curves) in the (* R < R ( Ũ $ U ( g 8 g ) plane o igure 1. For (where ) isoquants are straight lines with a negative slope. As R grows isoquant slopes grow and become positive i R > R ( when Ũ ' U (. Note also that i " increases isoquants move to the right in the gra and their slope increases (i.e. or any given (* g 8 g ) parameter set increased irm bargaining power reduces R in the resulting voluntary agreement which is in accordance with intuition). In igure 2 one o the VA-sets rom igure 1 is reproduced with its associated interior isoquants indicating the resulting R or the entire VA-set. FIGURE 2 Illustration characterising the VA-set or a model without interest group signalling power 15

18

19 Realisation o Voluntary Agreements and their Distributional and Welare Eects We now speciy the social welare unction with which to evaluate the result o the voluntary agreement process. Clearly at any given time dierent political parties and the dierent branches o government may be biased towards special interest groups (be this because o lobbyism or because o undamental bias). Though by no means perect the division o power between executive and legislative braches o government and the possibility o public scrutiny and debate under the traditional legislative process in a democracy is oten cited as important or balancing o special interest groups and thus securing some adherence to the interests o the general public during the policy ormulation process. I these elements are important it seems likely that the policy priorities implied by the congressional utility unction (embedding compromises between dierent parties and branches o government through such a legislative process) in general will deviate less rom those implied by the <true social welare unction than will the policy priorities implied by the government utility unction. Taking this outset we will assume that the congressional utility unction under the traditional policy ormulation process is the best estimator o the social welare changes caused by changes in goal attainment, i.e. we speciy the ollowing social welare unction: SW(R,T) ' U (R,T) % 8 c T % * c R giving the ollowing social welare eect o allowing a policy ormulation through voluntary agreements: SW( R,0) & SW(R (, ) 'Ũ & 8 c T % * c ( R & R ( ) (22) 16

20 Subtracting equation (2) rom equation (7) we get the utility eect o voluntary agreements or Congress: Ũ c c ' Ũ & 8 c T % * c ( R & R ( ) (23) and or Government (equation (8) minus equation (3)): Ũ g g ' Ũ & 8 g T % * g ( R & R ( ) (24) We see that in this model the social welare eect o a voluntary agreement is equal to the eect on congressional utility. Figure 2 illustrates that i Government and Congress disagree on policy priorities (i.e. i * g * c or i 8 g 8 c ) voluntary agreements become possible even though they imply a all in implementation eiciency (i.e. c>1). I Government is suiciently more pro-irm than Congress then irms as well as Government gain rom reducing environmental goals and tax revenue below the level that would result rom the traditional policy ormulation process involving Congress even though implementation eiciency alls. I Government is suiciently more pro-environment (relative to revenue) than Congress then it becomes possible or Government to oer a mutually advantageous reduction in tax revenue in return or an increase in environmental perormance even though implementation eiciency alls. In both cases irms and Government gain utility (a necessary condition or a voluntary agreement) while the utility o Congress is necessarily reduced (since deviating rom congressional policy priorities is the only possible generator o utility gains or irms and Government when implementation eiciency alls). The utility o the environmental interest group may be reduced or increased as indicated in igure 2. I on the other hand implementation eiciency increases suiciently (i.e. c<1) the VA-set boundary shits up and voluntary agreements become possible when Government and Congress agree on policy priorities. In this case Congress and the environmental interest group as well as irms and Government gain utility. However, i Government and Congress disagree on policy priorities, the resulting voluntary agreement may reduce congressional utility (and social welare) and/or environmental perormance even though it increases implementation eiciency. The distributional and welare consequences o voluntary agreements can be summarised as ollows: 17

21 Falling implementation eiciency Rising implementation eiciency Eect o voluntary agreements on: Government Government Government Government and Congress and Congress and Congress and Congress have same have dierent have same have dierent policy priorities* policy priorities policy priorities policy priorities Firm utility Government Congress - +? Environment? +? Tax Revenue Social welare - +? * Voluntary Agreements are not possible Voluntary agreements become possible when they encompass implementation eiciency gains or when Congress and Government disagree on policy priorities. I Congress and Government agree on policy priorities only agreements that imply increased implementation eiciency and a social welare gain will be realised. I agreement on policy priorities can be insured then allowing policy ormulation through voluntary agreements entails a clear cut welare gain. However, i Congress and Government disagree on policy priorities this may reduce or eliminate the welare gains associated with lower compliance costs. Further, i policy disagreement is large enough, voluntary agreements become possible even though implementation eiciency is reduced. The potential welare problem or voluntary agreements in this model arises because Government is allowed to enter voluntary agreements that reduce congressional utility. Within the model set up the obvious solution is to give Congress the right to veto voluntary agreements. This would restrict the VA-set to agreements that also satisy the congressional utility constraint (i.e. to agreements that are welare improving). 4. Voluntary Agreements when the Firm s Interest Group has Signalling Power The ollowing is an augmentation o the model in the previous section incorporating direct inluence o interest groups in a very simple way. We assume that interest groups may reward/punish those responsible or a decision or a policy result by publicly applauding or criticizing the decision or result. Utility o political actors is aected directly because the general public s perception o them is inluenced by 18

22 interest group criticism. In the ollowing we assume that this process takes on a very simple structure. We assume that an IG can only credibly criticize observed decisions or results as such and that the criticism then will be perceived by the public as applying to all agents responsible or the decision or result. Thus the IG may vary the intensity o criticism, but is not able to inluence the relative utility eect on the dierent actors responsible or the decision or result being criticized. In eect then IG-criticism is a public good/bad or the group o actors responsible or a decision. Further activities o IGs are assumed to be embedded in a larger environment o repeated policy ormulation and criticism. We assume that to be eective IGs must have a predictable and consistent pattern o response to policy across dierent policy settings and that this pattern is a strategy set by each IG outside the model. We urther assume that the costs o deviating rom the pre-set pattern are so large as to make this a non-viable option in the given case (i.e. that deviation i discovered by the public would result in a general and very costly loss o credibility). Basically we assume that IG criticism in order to be credible must be a trustworthy signal that the public can translate into an indicator o damage done to the interest group by policy. The public s punishment decision problem is also assumed to be embedded in a larger environment o repeated decisions and criticism with periodic public punishment o decision makers (through, e.g. voting at elections or product buying decisions). Punishment must be based on an accumulated measure o decision maker perormance. The punishment eectuated by the public may be a non-linear unction o the aggregate perormance measure which again may be a non-linear unction o the damage signals rom interest groups. However, i we assume that the decision problem at hand is small it may be reasonable to model the marginal eects o an interest group s signal on public punishment as linear unctions o the damage caused to the interest group. With this rationale we will model the eect o an IG's criticism on a decision maker s utility as a linear unction o damage done to the interest group. The coeicient being the marginal weight the public attaches to interest group damage in the perormance indicator times the marginal disposition to punish times the marginal utility eect o punishment on the decision makers utility - all o which are assumed to be constant over the spectrum covered by the 'small' regulation problem at hand. Augmenting the previous model we have the ollowing agent utilities under the traditional policy process: U ( ' & & C(R (, ) (25) U ( c ' U ( % 8 c % * c R ( % s e c (R( & R e ) % s c (U( & Ū ) (26) 19

23 U ( g ' U( % 8 g % * g R ( % s e g (R( & R e ) % s g (U( & Ū ) (27) and under the voluntary agreement process: Ũ ' & C(c R, 0) % s e ( R & R e ) (28) Ũ c ' Ũ % * c R (29) Ũ g ' Ũ % * g R % s e g ( R & R e ) (30) where s e, s e c and s e g are the marginal utility eects o environmental interest group criticism on the irm, Congress and Government respectively and s g and s c are the marginal utility eects o irm interest group criticism. R e and Ū are the levels o environmental damage reduction and irm utility where interest group criticism switches rom having a negative to having a positive net utility eect. In the traditional process Government and Congress are responsible and thus aected by criticism/applause rom the environmental and irm interest group. In the voluntary agreement process Congress is not responsible and thereore unaected while the irm now is aected by environmental IG criticism. Taking responsibility or the decision the irm IG can no longer criticize the decision so this element is eliminated rom Government utility. Deriving the voluntary agreement set border as in the previous section the equation describing the irm unconstrained part o the border (corresponding to equation (11)) is 8 g ' R & R ( ) (* g % s e g ) % (Ũ & s g (U( & Ū ) (31) while the irm constrained part is described by the ollowing equations (corresponding to (13) and 17)) 8 g ' R & R ( (* g % s e g ) & s g (U( & Ū ) (32) 20

24 and R ' C &1 ([ % C(R (, ) % s e ( R & R e )], 0)/c (33) The equation or the isoquant curves that characterize the VA-set interior corresponding to equation (21) becomes: 8 g ' R & R ( % (Ũ ) ) (* g % s e g ) & (Ũ (1&") " (1&") "cc R % 1 & s g (U( & Ū ) (* g % s e g ) (34) In the special case where only the irm IG has signalling power (i.e. s e ' s e g ' s e c ' 0 ) we see that the set border here is equal to the set border in the previous section except or the presumably positive constant &s g (U( & Ū )/. Thus the eect o irm IG signalling power corresponds to an upward shit o the set border and iso-quant equation rom the previous section. This is illustrated in igure 3. FIGURE 3 Illustration characterising the VA-set or a model with irm interest group signalling power 21

25

26 We now speciy a social welare unction with wich to evaluate the result o the voluntary agreement process. The two characteristics o the traditional policy ormulation process that we have cited as central or balancing o special interest groups are the division o power and the possibility o public scrutiny. As in the previous section interest groups may subtly aect policy priorities through lobbyism or political agents may be undamentally biased. Thus we will assume that the importance o division o power justiies using the congressional utility unction as a starting point or speciying a social welare unction. In this model, however, the irm interest group also sends a credible signal to the public that allows direct public disciplining o decision makers. This accentuates the potential importance o public scrutiny. Based on this we will assume that public disciplining resulting rom irm IG signalling in general brings the resulting policy decisions closer to the socially optimal. This in turn allows us to assume that the congressional utility unction under the traditional policy ormulation process is the best estimator o the social welare changes caused by changes in goal attainment giving the ollowing social welare unction: SW(R,T) ' (1 % s c )U (R,T) % 8 c T % * c R and the ollowing social welare eect o voluntary agreements: SW( R,0) & SW(R (, ) ' (1 % s c )(Ũ ) & 8 c T % * c ( R & R ( ) (35) The eect o voluntary agreements on congressional utility (equation (29) minus equation (26)) now becomes: Ũ c c ' (1 % s c )(Ũ ) & 8 c T % * c ( R & R ( ) % s c (Ū & Ũ ) (36) and the eect on Government utility (equation (30) minus equation (27)): Ũ g g ' (1 % s g )(Ũ ) & 8 T % * ( R & R ( ) % s g g g (Ū & Ũ ) (37) When comparing with the model in the previous section we see that voluntary agreements give Congress an extra utility gain as a result o avoiding public criticism. Thus the eect on congressional utility may dier rom the eect on social welare (intuitively the utility gained by Congress when avoiding public criticism is as such irrelevant or the general public). I Government and Congress agree on policy 22

27 priorities and have the same susceptibility to irm criticism the utility eects on Government and Congress are the same. The distributional and welare eects o voluntary agreements are summarised below: Falling implementation eiciency Rising implementation eiciency Eect o voluntary agreements on: Government Government Government Government and Congress and Congress and Congress and Congress have same have dierent have same have dierent policy priorities policy priorities policy priorities policy priorities Firm utility Government Congress +? +? Environment???? Tax Revenue Social welare - -?? The main story here is concerned with welare eects. When the irm IG has signalling power Government may ind it advantageous to enter agreements with irms even when implementation eiciency alls and Government has the same policy priorities and susceptibility to irm criticism as Congress. Driving such agreements is the opportunity o avoiding irm IG criticism that otherwise would be initiated i policy was ormulated in the normal way. In exchange or this irms gain a reduction in taxes and possibly a reduction in the severity o environmental goals relative to what would be the result o the normal policy process. When Government and Congress share policy priorities and susceptibility to irm criticism congressional utility will also increase - however, social welare is reduced. Assuming as we have or Government that the net utility eect or Congress o irm criticism is negative (i.e. s c (Ū & Ũ )>0 ) any welare increasing voluntary agreement will also increase congressional utility (as easily seen by comparing (35) and (36)). Thus the VA-set restriction that results when Congress is given the power to veto voluntary agreements is still welare increasing. However, a congressional right to veto no longer assures that voluntary agreements will be welare increasing. 23

28 5. Voluntary Agreements when the Environmental Interest Group has Signalling Power In this section we ocus on environmental interest group signalling power, but in a model allowing separation in time o goal ormulation and implementation. This in turn allows responsibility or goal setting to be decoupled rom responsibility or policy implementation. The idea is that it takes time or policy to work and more important that the results o policy instruments cannot be predicted with certainty at the time o implementation. This means that time elapses between goal setting and observation o the result o policy instruments implemented at the time o goal setting. The environmental interest group may then criticize goal setting as well as goal attainment. Let R g denote the goal set at the time o policy implementation and R the damage reduction attained ater time has elapsed. Let the utility eect o environmental IG criticism have the ollowing structure: 1) at the time o goal setting the utility eect o criticism is: s(r g & R e ) 2) at the time o goal attainment the utility eect o criticism is: s(r & R g ) & ŝ(max[r g & R, 0]) 2 so that goal attainment criticism neutralizes applause o previous criticism o the ormulated goal and punishes the agent or non-attainment o the goal while not rewarding or over-attainment. Deining DR g = R g - R agent utilities under the traditional policy process become: U ( ' & & C(R (, ) (38) U ( c ' U ( % 8 c % * c R ( % s e c (R( & R e ) & ŝ e c (Max(DR( g, 0))2 (39) U ( g ' U( % 8 g % * g R ( % s e g (R( & R e ) & ŝ e g (Max(DR( g, 0))2 (40) 24

29 Trivially DR ( g ' 0 (i.e. R( g ' R( ). Under the voluntary agreement process the Congress has no responsibility. Government shares responsibility or goal ormulation with the irm while implementation is the sole responsibility o the irm. We then have Ũ ' &C(c R, 0) % s e ( R & R e ) & ŝ e (Max(D R g, 0)) 2 (41) Ũ c ' Ũ % * c R (42) Ũ g ' Ũ % * g R % s e g ( R % D R g & R e ) (43) The equation characterizing the irm unconstrained part o the voluntary agreement set border (corresponding to equation (11)) becomes: 8 g ' R & R ( ) (* g % s e g ) % (Ũ e % s g T D R ( g (44) while the irm constrained part o the set border (corresponding to equation (13)) is characterized by: 8 g ' R & R ( (* g % s e g ) % s e g T D R ( g (45) with (corresponding to equation (14)): R ' C &1 ([ % C(R (, ) % s e ( R & R e ) & ŝ e (Max(D R g, 0)) 2 ], 0)/c (46) The equation or the isoquant curves that characterize the VA-set interior corresponding to equation (21) becomes: 25

30 8 g ' R & R ( ) (* g % s e g ) & (Ũ % (Ũ ) (1&") " (1&") "cc R % 1 % s e g D R g (* g % s e g ) (47) Assume that s e = 0. We see that i D R g ' 0 all equations are equal to the equations in model I where * * g % s e g is redeined as g. The possibility o decoupling goal setting and implementation responsibility (positive D R g ) shits the boarder and isoquant curves upwards in the graph vis-à-vis the corresponding curves in section 3. As ŝ e is reduced D R g rises in both parts o the curve and eventually we have: ŝ e D R 2 g ' T( % C(R (, ) ' Û with R ' 0 (48) Ater this point we have D R g ' Û ŝ e (49) so when inserting (48) and (49) into (45) we have: 8 g ' R( * % s e ( g g ) % s e g Û ŝ e This means that any (* g, 8 g) can be included in the set with a suiciently small (i.e. the upward shit o the curve is not bound). This situation is illustrated in igure 4. ŝ e 26

31

32 FIGURE 4 Illustration characterising the VA-set or a model with environmental interest group signalling power Based on the assumption that IG signalling generally brings the resulting policy decisions closer to social optimum, we uphold the assumption that the congressional utility unction under the traditional policy ormulation process is the best estimator o the social welare changes caused by changes in goal attainment. This gives the ollowing social welare unction: SW(R,T) ' U (R,T) % 8 c T % (* c % s e c )R and the ollowing social welare eect o voluntary agreements: SW( R,0) & SW(R (, ) ' Ũ & 8 c T % (* c % s e c )( R & R ( ) (50) The eect o voluntary agreements on congressional utility is (equation (42) minus equation (39)): Ũ c c ' (Ũ ) & 8 T % (* % s e c c c )( R & R ( ) % s e c ( R e & R) (51) and the eect on Government utility is (equation (43) minus equation (40)): 27

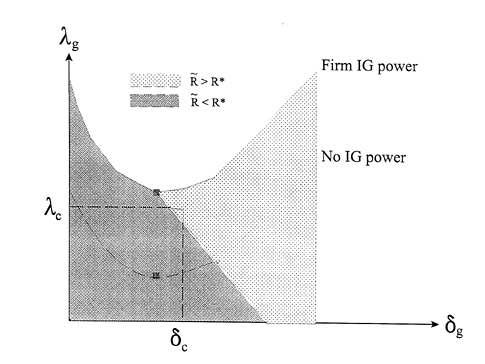

33 Ũ g g ' (Ũ ) & 8 T % (* % s e g g g )( R & R ( ) % s e c (D R g ) (52) As in the previous section we see that voluntary agreements aect Congress by eliminating public criticism rom the environmental IG so that the eect on congressional utility may dier rom the eect on social welare. In contrast to what was the case in the previous section i Government and Congress agree on policy priorities and have the same susceptibility to environmental IG criticism the utility eects on Government and Congress are not the same. The distributional and welare eects o voluntary agreements are summarised below: Falling implementation eiciency Rising implementation eiciency Eect o voluntary agreements on: Government Government Government Government and Congress and Congress and Congress and Congress have same have dierent have same have dierent policy priorities policy priorities policy priorities policy priorities Firm utility Government Congress???? Environment???? Tax Revenue Social welare - -?? Further as environmental interest group signalling power increases (corresponding to an upward shit o the VA-set in igure 4) we see that environmental perormance relative to the traditional policy process is reduced. Thus it is possible that an increase in environmental interest group signalling power will harm the environment by inducing a shit to policy ormulation through voluntary agreements with a lower 2 absolute environmental perormance. 2)The counter intuitive observation that increasing its power may hurt the environmental interest group is also seen in other models o regulation with interest groups, e.g. Laont and Tirole (1993). 28

34 The eect o agreements on congressional utility is unclear even i Government and Congress share the same utility unction. Congressional utility may increase as Congress like Government avoids the eect o environmental interest group criticism o goal achievement. However, unlike Government, Congress is excluded rom the (possibly positive) utility eect o applause o high goal setting so the net utility eect or Congress may be negative. Turning to social welare eects we again ind that when the environmental IG has signalling power Government may ind it advantageous to enter agreements even though implementation eiciency is reduced and Government has the same policy priorities and susceptibility to environmental IG criticism as Congress. By shiting responsibility or implementation Governments avoid criticism or non-attainment o goals - a criticism which irms may be less vulnerable to. Firms take responsibility and endure the criticism o non-attainment while instead gaining the deacto acceptance by Government o a reduction in the attained environmental goals. Giving Congress the power to veto agreements is a somewhat more complicated model change than in the previous models. Since giving Congress the right to veto also moves Congress into the set o actors responsible or goal ormulation Congress will be aected by environmental IG signalling and the eect o a voluntary agreement on congressional utility becomes: Ũ c c ' (Ũ ) & 8 c T % (* c % s e c )( R & R ( ) % s e c (D R g ) (53) As in the previous section any welare increasing voluntary agreement will also increase congressional utility. Thus giving Congress the power to veto voluntary agreements is welare increasing. However, we again see that giving Congress such a power does not assure that voluntary agreements will increase social welare. 6. Conclusion This paper concerns the conditions under which voluntary agreements become possible and their distributional and social welare eects. The simple models developed here ocus on two aspects o voluntary agreements: the exclusion o legislative bodies rom the policy ormulation process and the shit o responsibility or meeting environmental goals and or policy implementation to industrial organisations. To speciy a social welare unction we assume that the balance o power between legislative branches and the possibility o public scrutiny through a legislative process are important or securing the interests o the general public during the policy ormulation process. This enables us to base speciication o the social welare unction on the congressional utility unction. The models developed in the paper ocus on the dierence between political 29

Nontariff Barriers and Domestic Regulation. Alan V. Deardorff University of Michigan

I. Taris A. Market or Imports B. Domestic Market II. Nontari Barriers III. IV. Nontari Barriers and Domestic Regulation Alan V. Deardor University o Michigan Regulation and Related Government Policies

I. Taris A. Market or Imports B. Domestic Market II. Nontari Barriers III. IV. Nontari Barriers and Domestic Regulation Alan V. Deardor University o Michigan Regulation and Related Government Policies

1. Expected utility, risk aversion and stochastic dominance

. Epected utility, risk aversion and stochastic dominance. Epected utility.. Description o risky alternatives.. Preerences over lotteries..3 The epected utility theorem. Monetary lotteries and risk aversion..

. Epected utility, risk aversion and stochastic dominance. Epected utility.. Description o risky alternatives.. Preerences over lotteries..3 The epected utility theorem. Monetary lotteries and risk aversion..

Competition, Deposit Insurance and Bank Risk-taking

Competition, eposit Insurance and Bank Risk-taking Roung-Jen Wu * Chien-Ping Chi ** Abstract This paper presents a inancial intermediation model integrating both loan and deposit markets to study the impacts

Competition, eposit Insurance and Bank Risk-taking Roung-Jen Wu * Chien-Ping Chi ** Abstract This paper presents a inancial intermediation model integrating both loan and deposit markets to study the impacts

The Relationship Between Franking Credits and the Market Risk Premium

The Relationship Between Franking Credits and the Market Risk Premium Stephen Gray * Jason Hall UQ Business School University o Queensland ABSTRACT In a dividend imputation tax system, equity investors

The Relationship Between Franking Credits and the Market Risk Premium Stephen Gray * Jason Hall UQ Business School University o Queensland ABSTRACT In a dividend imputation tax system, equity investors

Misreporting Corporate Performance

ast revision: January 23 Misreporting Corporate Perormance ucian Arye Bebchuk arvard aw School and NBER (bebchuk@law.harvard.edu Oren Bar-Gill arvard Society o Fellows (bargill@law.harvard.edu We are grateul

ast revision: January 23 Misreporting Corporate Perormance ucian Arye Bebchuk arvard aw School and NBER (bebchuk@law.harvard.edu Oren Bar-Gill arvard Society o Fellows (bargill@law.harvard.edu We are grateul

On the Role of Authority in Just-In-Time Purchasing Agreements

Discussion Paper No. A-55 On the Role o Authority in Just-In-Time Purchasing Agreements CHRISTIAN EWERHART and MICHAEL LORTH May 1997 On the Role o Authority in Just-In-Time Purchasing Agreements Christian

Discussion Paper No. A-55 On the Role o Authority in Just-In-Time Purchasing Agreements CHRISTIAN EWERHART and MICHAEL LORTH May 1997 On the Role o Authority in Just-In-Time Purchasing Agreements Christian

Stochastic Dominance Notes AGEC 662

McCarl July 1996 Stochastic Dominance Notes AGEC 66 A undamental concern, when looking at risky situations is choosing among risky alternatives. Stochastic dominance has been developed to identiy conditions

McCarl July 1996 Stochastic Dominance Notes AGEC 66 A undamental concern, when looking at risky situations is choosing among risky alternatives. Stochastic dominance has been developed to identiy conditions

An Empirical Analysis of the Role of Risk Aversion. in Executive Compensation Contracts. Frank Moers. and. Erik Peek

An Empirical Analysis o the Role o Risk Aversion in Executive Compensation Contracts Frank Moers and Erik Peek Maastricht University Faculty o Economics and Business Administration MARC / Department o

An Empirical Analysis o the Role o Risk Aversion in Executive Compensation Contracts Frank Moers and Erik Peek Maastricht University Faculty o Economics and Business Administration MARC / Department o

The Wider Impacts Sub-Objective TAG Unit

TAG Unit 3.5.14 DRAFT FOR CONSULTATION September 2009 Department or Transport Transport Analysis Guidance (TAG) This Unit is part o a amily which can be accessed at www.dt.gov.uk/webtag/ Contents 1 The

TAG Unit 3.5.14 DRAFT FOR CONSULTATION September 2009 Department or Transport Transport Analysis Guidance (TAG) This Unit is part o a amily which can be accessed at www.dt.gov.uk/webtag/ Contents 1 The

Optimal Internal Control Regulation

Optimal Internal ontrol Regulation Stean F. Schantl University o Melbourne and lred Wagenhoer University o Graz bstract: Regulators increasingly rely on regulation o irms internal controls (I) to prevent

Optimal Internal ontrol Regulation Stean F. Schantl University o Melbourne and lred Wagenhoer University o Graz bstract: Regulators increasingly rely on regulation o irms internal controls (I) to prevent

Notes on the Cost of Capital

Notes on the Cost o Capital. Introduction We have seen that evaluating an investment project by using either the Net Present Value (NPV) method or the Internal Rate o Return (IRR) method requires a determination

Notes on the Cost o Capital. Introduction We have seen that evaluating an investment project by using either the Net Present Value (NPV) method or the Internal Rate o Return (IRR) method requires a determination

CHAPTER 13. Investor Behavior and Capital Market Efficiency. Chapter Synopsis

CHAPTER 13 Investor Behavior and Capital Market Eiciency Chapter Synopsis 13.1 Competition and Capital Markets When the market portolio is eicient, all stocks are on the security market line and have an

CHAPTER 13 Investor Behavior and Capital Market Eiciency Chapter Synopsis 13.1 Competition and Capital Markets When the market portolio is eicient, all stocks are on the security market line and have an

Chapter 8. Inflation, Interest Rates, and Exchange Rates. Lecture Outline

Chapter 8 Inlation, Interest Rates, and Exchange Rates Lecture Outline Purchasing Power Parity (PPP) Interpretations o PPP Rationale Behind PPP Theory Derivation o PPP Using PPP to Estimate Exchange Rate

Chapter 8 Inlation, Interest Rates, and Exchange Rates Lecture Outline Purchasing Power Parity (PPP) Interpretations o PPP Rationale Behind PPP Theory Derivation o PPP Using PPP to Estimate Exchange Rate

Quantitative Results for a Qualitative Investor Model A Hybrid Multi-Agent Model with Social Investors

Quantitative Results or a Qualitative Investor Model A Hybrid Multi-Agent Model with Social Investors Stephen Chen, Brenda Spotton Visano, and Michael Lui Abstract A standard means o testing an economic/inancial

Quantitative Results or a Qualitative Investor Model A Hybrid Multi-Agent Model with Social Investors Stephen Chen, Brenda Spotton Visano, and Michael Lui Abstract A standard means o testing an economic/inancial

Entry Mode, Technology Transfer and Management Delegation of FDI. Ho-Chyuan Chen

ntry Mode, Technology Transer and Management Delegation o FDI Ho-Chyuan Chen Department o conomics, National Chung Cheng University, Taiwan bstract This paper employs a our-stage game to analyze decisions

ntry Mode, Technology Transer and Management Delegation o FDI Ho-Chyuan Chen Department o conomics, National Chung Cheng University, Taiwan bstract This paper employs a our-stage game to analyze decisions

THE SLOWDOWN IN GROWTH IN 2008 AND ITS

FISCAL RULES: THE STABILITY AND GROWTH PACT IN THE EUROPEAN MONETARY UNION Domenico Moro, Università Cattolica del Sacro Cuore, Piacenza, Italy INTRODUCTION THE SLOWDOWN IN GROWTH IN 008 AND ITS possible

FISCAL RULES: THE STABILITY AND GROWTH PACT IN THE EUROPEAN MONETARY UNION Domenico Moro, Università Cattolica del Sacro Cuore, Piacenza, Italy INTRODUCTION THE SLOWDOWN IN GROWTH IN 008 AND ITS possible

Chapter 9 The Case for International Diversification

Chapter 9 The Case or International Diversiication 1. The domestic and oreign assets have annualized standard deviations o return o σ d = 15% and σ = 18%, respectively, with a correlation o ρ = 0.5. The

Chapter 9 The Case or International Diversiication 1. The domestic and oreign assets have annualized standard deviations o return o σ d = 15% and σ = 18%, respectively, with a correlation o ρ = 0.5. The

The fundamentals of the derivation of the CAPM can be outlined as follows:

Summary & Review o the Capital Asset Pricing Model The undamentals o the derivation o the CAPM can be outlined as ollows: (1) Risky investment opportunities create a Bullet o portolio alternatives. That

Summary & Review o the Capital Asset Pricing Model The undamentals o the derivation o the CAPM can be outlined as ollows: (1) Risky investment opportunities create a Bullet o portolio alternatives. That

Published in French in: Revue d Economie du Développement, Vol.3, (1995), pp HOUSEHOLD MODELING FOR THE DESIGN OF POVERTY ALLEVIATION

, pp HOUSEHOLD MODELING FOR THE DESIGN OF POVERTY ALLEVIATION") Published in French in: Revue d Economie du Développement, Vol.3, (1995), pp. 3-23. HOUSEHOLD MODELING FOR THE DESIGN OF POVERTY ALLEVIATION STRATEGIES 1 by Alain de Janvry and Elisabeth Sadoulet University

Published in French in: Revue d Economie du Développement, Vol.3, (1995), pp. 3-23. HOUSEHOLD MODELING FOR THE DESIGN OF POVERTY ALLEVIATION STRATEGIES 1 by Alain de Janvry and Elisabeth Sadoulet University

Horizontal Coordinating Contracts in the Semiconductor Industry

Horizontal Coordinating Contracts in the Semiconductor Industry Xiaole Wu* School o Management, Fudan University, Shanghai 2433, China wuxiaole@udaneducn Panos Kouvelis Olin Business School, Washington

Horizontal Coordinating Contracts in the Semiconductor Industry Xiaole Wu* School o Management, Fudan University, Shanghai 2433, China wuxiaole@udaneducn Panos Kouvelis Olin Business School, Washington

Can Social Programs Reduce Producitivity and Growth? A Hypothesis for Mexico

INTERNATIONAL POLICY CENTER Gerald R. Ford School o Public Policy University o Michigan IPC Working Paper Series Number 37 Can Social Programs Reduce Producitivity and Growth? A Hypothesis or Mexico Santiago

INTERNATIONAL POLICY CENTER Gerald R. Ford School o Public Policy University o Michigan IPC Working Paper Series Number 37 Can Social Programs Reduce Producitivity and Growth? A Hypothesis or Mexico Santiago

Money, the Stock Market and the Macroeconomy: A Theoretical Analysis

The Pakistan Development Review 5:3 (Autumn 013) pp. 35 46 Money, the Stock Market and the Macroeconomy: A Theoretical Analysis RILINA BASU and RANJANENDRA NARAYAN NAG * The inance-growth nexus has become

The Pakistan Development Review 5:3 (Autumn 013) pp. 35 46 Money, the Stock Market and the Macroeconomy: A Theoretical Analysis RILINA BASU and RANJANENDRA NARAYAN NAG * The inance-growth nexus has become

The Impact of Labour Market Partial Reforms on Workers Productivity: The Italian Case

Beccarini, International Journal o Applied Economics, 6(2), September 2009, -9 The Impact o Labour Market Partial Reorms on Workers Productivity: The Italian Case Andrea Beccarini * Whilems Universität

Beccarini, International Journal o Applied Economics, 6(2), September 2009, -9 The Impact o Labour Market Partial Reorms on Workers Productivity: The Italian Case Andrea Beccarini * Whilems Universität

WORKING PAPER SERIES

ollege o Business Administration University o hode Island William A. Orme WOKING PE SEIES encouraging creative research Growth Opportunities, Stockholders' laim/liability on Pension Plans and oporate Pension

ollege o Business Administration University o hode Island William A. Orme WOKING PE SEIES encouraging creative research Growth Opportunities, Stockholders' laim/liability on Pension Plans and oporate Pension

Econ 815 Dominant Firm Analysis and Limit Pricing

Econ 815 Dominant Firm Analysis and imit Pricing I. Dominant Firm Model A. Conceptual Issues 1. Pure monopoly is relatively rare. There are, however, many industries supplied by a large irm and a ringe

Econ 815 Dominant Firm Analysis and imit Pricing I. Dominant Firm Model A. Conceptual Issues 1. Pure monopoly is relatively rare. There are, however, many industries supplied by a large irm and a ringe

Alain de Janvry and Elisabeth Sadoulet

DEPARTMENT OF AGRICULTURAL AND RESOURCE ECONOMICS DIVISION OF AGRICULTURE AND NATURAL RESOURCES UNIVERSITY OF CALIFORNIA AT BERKELEY W ORKING PAPER NO. 787 HOUSEHOLD MODELING FOR THE DESIGN OF POVERTY

DEPARTMENT OF AGRICULTURAL AND RESOURCE ECONOMICS DIVISION OF AGRICULTURE AND NATURAL RESOURCES UNIVERSITY OF CALIFORNIA AT BERKELEY W ORKING PAPER NO. 787 HOUSEHOLD MODELING FOR THE DESIGN OF POVERTY

UK Evidence on the Profitability and the Risk-Return Characteristics of Merger Arbitrage

UK Evidence on the Proitability and the isk-eturn Characteristics o Merger Arbitrage Sudi Sudarsanam* Proessor o Finance & Corporate Control Director, MSc in Finance & Management & Director (Finance),

UK Evidence on the Proitability and the isk-eturn Characteristics o Merger Arbitrage Sudi Sudarsanam* Proessor o Finance & Corporate Control Director, MSc in Finance & Management & Director (Finance),

Measuring Alpha-Based Performance: Implications for Alpha-Focused Structured Products

Measuring Alpha-Based Perormance: Implications or Alpha-Focused Structured Products AUTHORS ARTICLE INFO JOURNAL FOUNDER Larry R. Gorman Robert A. Weigand Larry R. Gorman and Robert A. Weigand (2008).

Measuring Alpha-Based Perormance: Implications or Alpha-Focused Structured Products AUTHORS ARTICLE INFO JOURNAL FOUNDER Larry R. Gorman Robert A. Weigand Larry R. Gorman and Robert A. Weigand (2008).

How to Set Minimum Acceptable Bids, with an Application to Real Estate Auctions

November, 2001 How to Set Minimum Acceptable Bids, with an Application to Real Estate Auctions by R. Preston McAee, Daniel C. Quan, and Daniel R. Vincent * Abstract: In a general auction model with ailiated

November, 2001 How to Set Minimum Acceptable Bids, with an Application to Real Estate Auctions by R. Preston McAee, Daniel C. Quan, and Daniel R. Vincent * Abstract: In a general auction model with ailiated

Characterization of the Optimum

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 5. Portfolio Allocation with One Riskless, One Risky Asset Characterization of the Optimum Consider a risk-averse, expected-utility-maximizing

Being Locked Up Hurts

Being Locked Up Hurts Frans A. de Roon, Jinqiang Guo, and Jenke R. ter Horst * This version: January 12, 2009 ABSTRACT This paper examines multi-period asset allocation when portolio adjustment is diicult

Being Locked Up Hurts Frans A. de Roon, Jinqiang Guo, and Jenke R. ter Horst * This version: January 12, 2009 ABSTRACT This paper examines multi-period asset allocation when portolio adjustment is diicult

Edinburgh Research Explorer

Edinburgh Research Explorer Predictability o the simple technical trading rules Citation or published version: Fang, J, Jacobsen, B & Qin, Y 2014, 'Predictability o the simple technical trading rules:

Edinburgh Research Explorer Predictability o the simple technical trading rules Citation or published version: Fang, J, Jacobsen, B & Qin, Y 2014, 'Predictability o the simple technical trading rules:

Perspective of Individuals on Personal Financial Planning

Perspective o Individuals on Personal Financial Planning Ms. Tulsi Raval Assistant Proessor, Sunshine Group o Institutions, Rajkot Email - tulsiraval_84@yahoo.com Abstract: Planning or a secure inancial

Perspective o Individuals on Personal Financial Planning Ms. Tulsi Raval Assistant Proessor, Sunshine Group o Institutions, Rajkot Email - tulsiraval_84@yahoo.com Abstract: Planning or a secure inancial

Risk Aversion, Prudence, and the Three-Moment Decision Model for Hedging

Risk Aversion, Prudence, and the Three-Moment Decision Model or Hedging Xiaomei Chen Graduate Research Assistant School o Economic Sciences Washington State University P.O. Box 64610 Pullman, WA 99164-610

Risk Aversion, Prudence, and the Three-Moment Decision Model or Hedging Xiaomei Chen Graduate Research Assistant School o Economic Sciences Washington State University P.O. Box 64610 Pullman, WA 99164-610

Securitized Markets and International Capital Flows

Securitized Markets and International Capital Flows Gregory Phelan Alexis Akira Toda This version: October 29, 215 Abstract We study the eect o collateralized lending and securitization on international

Securitized Markets and International Capital Flows Gregory Phelan Alexis Akira Toda This version: October 29, 215 Abstract We study the eect o collateralized lending and securitization on international

Multiplicative Risk Prudence *

Multiplicative Risk Prudence * Xin Chang a ; Bruce Grundy a ; George Wong b,# a Department o Finance, Faculty o Economics and Commerce, University o Melbourne, Australia. b Department o Accounting and

Multiplicative Risk Prudence * Xin Chang a ; Bruce Grundy a ; George Wong b,# a Department o Finance, Faculty o Economics and Commerce, University o Melbourne, Australia. b Department o Accounting and

Chapter 1 Microeconomics of Consumer Theory

Chapter Microeconomics of Consumer Theory The two broad categories of decision-makers in an economy are consumers and firms. Each individual in each of these groups makes its decisions in order to achieve

Chapter Microeconomics of Consumer Theory The two broad categories of decision-makers in an economy are consumers and firms. Each individual in each of these groups makes its decisions in order to achieve

Comments on Michael Woodford, Globalization and Monetary Control

David Romer University of California, Berkeley June 2007 Revised, August 2007 Comments on Michael Woodford, Globalization and Monetary Control General Comments This is an excellent paper. The issue it

David Romer University of California, Berkeley June 2007 Revised, August 2007 Comments on Michael Woodford, Globalization and Monetary Control General Comments This is an excellent paper. The issue it

Uncertainty Traps. Edouard Schaal NYU. July 8, 2013 [ PRELIMINARY AND INCOMPLETE ] Abstract

![Uncertainty Traps. Edouard Schaal NYU. July 8, 2013 [ PRELIMINARY AND INCOMPLETE ] Abstract](/thumbs/79/80153408.jpg "Uncertainty Traps. Edouard Schaal NYU. July 8, 2013 [ PRELIMINARY AND INCOMPLETE ] Abstract") Uncertainty Traps Pablo Fajgelbaum UCLA Edouard Schaal NYU July 8, 03 Mathieu Taschereau-Dumouchel Wharton PRELIMINARY AND INCOMPLETE ] Abstract We develop a quantitative theory o endogenous uncertainty

Uncertainty Traps Pablo Fajgelbaum UCLA Edouard Schaal NYU July 8, 03 Mathieu Taschereau-Dumouchel Wharton PRELIMINARY AND INCOMPLETE ] Abstract We develop a quantitative theory o endogenous uncertainty

Monetary credibility problems. 1. In ation and discretionary monetary policy. 2. Reputational solution to credibility problems

Monetary Economics: Macro Aspects, 2/4 2013 Henrik Jensen Department of Economics University of Copenhagen Monetary credibility problems 1. In ation and discretionary monetary policy 2. Reputational solution

Monetary Economics: Macro Aspects, 2/4 2013 Henrik Jensen Department of Economics University of Copenhagen Monetary credibility problems 1. In ation and discretionary monetary policy 2. Reputational solution

Chapter 6: Supply and Demand with Income in the Form of Endowments

Chapter 6: Supply and Demand with Income in the Form of Endowments 6.1: Introduction This chapter and the next contain almost identical analyses concerning the supply and demand implied by different kinds

Chapter 6: Supply and Demand with Income in the Form of Endowments 6.1: Introduction This chapter and the next contain almost identical analyses concerning the supply and demand implied by different kinds

Soft Budget Constraints in Public Hospitals. Donald J. Wright

Soft Budget Constraints in Public Hospitals Donald J. Wright January 2014 VERY PRELIMINARY DRAFT School of Economics, Faculty of Arts and Social Sciences, University of Sydney, NSW, 2006, Australia, Ph:

Soft Budget Constraints in Public Hospitals Donald J. Wright January 2014 VERY PRELIMINARY DRAFT School of Economics, Faculty of Arts and Social Sciences, University of Sydney, NSW, 2006, Australia, Ph:

*** THE APPENDICES ARE NOT FOR PUBLICATION ***

*** THE APPENDICES ARE NOT FOR PUBLICATION *** Appendix A: The Tax Reaction Function: An Explicit Derivation This appendix contains a detailed development o our model o strategic competition and extracts

*** THE APPENDICES ARE NOT FOR PUBLICATION *** Appendix A: The Tax Reaction Function: An Explicit Derivation This appendix contains a detailed development o our model o strategic competition and extracts

WORKING PAPERS. International Outsourcing and Labour with Sector-specific Human Capital. Kurt Kratena

ÖSTERREICHISCHES INSTITT FÜR WIRTSCHAFTSFORSCHNG WORKING PAPERS International Outsourcing and Labour with Sector-speciic Human Capital Kurt Kratena 7/006 International Outsourcing and Labour with Sector-speciic

ÖSTERREICHISCHES INSTITT FÜR WIRTSCHAFTSFORSCHNG WORKING PAPERS International Outsourcing and Labour with Sector-speciic Human Capital Kurt Kratena 7/006 International Outsourcing and Labour with Sector-speciic

Synthetic options. Synthetic options consists in trading a varying position in underlying asset (or

Synthetic options Synthetic options consists in trading a varying position in underlying asset (or utures on the underlying asset 1 ) to replicate the payo proile o a desired option. In practice, traders

Synthetic options Synthetic options consists in trading a varying position in underlying asset (or utures on the underlying asset 1 ) to replicate the payo proile o a desired option. In practice, traders

Cross-Sectional Variation of Intraday Liquidity, Cross-Impact, and their Effect on Portfolio Execution

Cross-Sectional Variation o Intraday Liquity, Cross-Impact, and their Eect on Portolio Execution Seungki Min Costis Maglaras Ciamac C. Moallemi Initial Version: July 2017; December 2017 Current Revision:

Cross-Sectional Variation o Intraday Liquity, Cross-Impact, and their Eect on Portolio Execution Seungki Min Costis Maglaras Ciamac C. Moallemi Initial Version: July 2017; December 2017 Current Revision:

13.1 Infinitely Repeated Cournot Oligopoly

Chapter 13 Application: Implicit Cartels This chapter discusses many important subgame-perfect equilibrium strategies in optimal cartel, using the linear Cournot oligopoly as the stage game. For game theory

Chapter 13 Application: Implicit Cartels This chapter discusses many important subgame-perfect equilibrium strategies in optimal cartel, using the linear Cournot oligopoly as the stage game. For game theory

Unemployment, tax evasion and the slippery slope framework

MPRA Munich Personal RePEc Archive Unemployment, tax evasion and the slippery slope framework Gaetano Lisi CreaM Economic Centre (University of Cassino) 18. March 2012 Online at https://mpra.ub.uni-muenchen.de/37433/

MPRA Munich Personal RePEc Archive Unemployment, tax evasion and the slippery slope framework Gaetano Lisi CreaM Economic Centre (University of Cassino) 18. March 2012 Online at https://mpra.ub.uni-muenchen.de/37433/

Available online at ScienceDirect. Procedia Engineering 129 (2015 ) International Conference on Industrial Engineering

International Conference on Industrial Engineering") Available online at www.sciencedirect.com ScienceDirect Procedia Engineering 129 (215 ) 681 689 International Conerence on Industrial Engineering Analysing the economic stability o an enterprise with the

Available online at www.sciencedirect.com ScienceDirect Procedia Engineering 129 (215 ) 681 689 International Conerence on Industrial Engineering Analysing the economic stability o an enterprise with the

CALCULATION OF COMPANY COSTS THROUGH THE DIRECT-COSTING CALCULATION METHOD

Florin-Constantin DIMA Constantin Brâncoveanu University o Piteşti Piteşti, Romania lorin.dima@univcb.ro LCULATION OF COMPANY COSTS THROUGH THE DIRECT-COSTING LCULATION METHOD Case study Keywords Production

Florin-Constantin DIMA Constantin Brâncoveanu University o Piteşti Piteşti, Romania lorin.dima@univcb.ro LCULATION OF COMPANY COSTS THROUGH THE DIRECT-COSTING LCULATION METHOD Case study Keywords Production

Investment Decisions in Granted Monopolies Under the Threat of a Random Demonopolization

Investment Decisions in Granted Monopolies Under the Threat o a Random Demonopolization Artur Rodrigues and Paulo J. Pereira NEGE, School o Economics and Management, University o Minho. CEF.UP and Faculty

Investment Decisions in Granted Monopolies Under the Threat o a Random Demonopolization Artur Rodrigues and Paulo J. Pereira NEGE, School o Economics and Management, University o Minho. CEF.UP and Faculty

Aysmmetry in central bank inflation control

Aysmmetry in central bank inflation control D. Andolfatto April 2015 The model Consider a two-period-lived OLG model. The young born at date have preferences = The young also have an endowment and a storage

Aysmmetry in central bank inflation control D. Andolfatto April 2015 The model Consider a two-period-lived OLG model. The young born at date have preferences = The young also have an endowment and a storage

Basic Income - With or Without Bismarckian Social Insurance?

Basic Income - With or Without Bismarckian Social Insurance? Andreas Bergh September 16, 2004 Abstract We model a welfare state with only basic income, a welfare state with basic income and Bismarckian

Basic Income - With or Without Bismarckian Social Insurance? Andreas Bergh September 16, 2004 Abstract We model a welfare state with only basic income, a welfare state with basic income and Bismarckian

Fakultät III Univ.-Prof. Dr. Jan Franke-Viebach

Univ.-Pro. Dr. J. Franke-Viebach 1 Universität Siegen Fakultät III Univ.-Pro. Dr. Jan Franke-Viebach Exam International Macroeconomics Winter Semester 2013-14 (1 st Exam Period) Available time: 60 minutes

Univ.-Pro. Dr. J. Franke-Viebach 1 Universität Siegen Fakultät III Univ.-Pro. Dr. Jan Franke-Viebach Exam International Macroeconomics Winter Semester 2013-14 (1 st Exam Period) Available time: 60 minutes

Two-Dimensional Bayesian Persuasion