Mortgage Bankers Association of Puerto Rico. June 8, 2017

|

|

|

- Olivia Stewart

- 5 years ago

- Views:

Transcription

1 Mortgage Bankers Association of Puerto Rico June 8, 2017

2 The information presented in this presentation is for general information only, and is based on guidelines and practices generally accepted within the mortgage finance industry and is not intended to be all-inclusive. MGIC makes no representations or warranties of any kind with respect to the accuracy, completeness or suitability for any purpose of the information contained in this presentation. MGIC expressly disclaims any and all warranties, express or implied, including without limitation warranties of merchantability and fitness for a particular purpose regarding these materials and this presentation. In no event will MGIC be liable for any direct, indirect, incidental, punitive or consequential damages of any kind with respect to the presentation or materials provided. All examples are hypothetical and are for illustrative purposes only. This presentation is not intended and should not be interpreted or relied upon as legal advice. We encourage you to seek advice from a qualified professional.

3 Affordable Lending presented by: Ivonne E. Rodríguez-Colón, PR MGIC Operations Manager

4 MGIC Go! Is the Fastest, Easiest Way to Get MI With DU or Loan Product Advisor DU is a registered Fannie Mae service mark; Loan Product Advisor is a registered Freddie Mac service mark.

5 Overlays are subject to MGIC underwriter discretion. *97% LTV is acceptable for a financed single premium or split up front. **The lowest of all Borrower Indicator Scores the lower of 2 or the middle of 3 credit scores for each borrower. If any borrower has no credit score, see UWG

6 Condominiums Old Process Project compliance was verified with the following: Short form vs. Full form FNMA In-house Lender Form New Process MGIC condominium questionnaire is the only required document for mortgage insurance submission effective June 1, 2017.

7 New Condominium Questionnaire

8 Condominium Project Review Some differences between Conforming and Non-Conforming : Delinquency ratios vary from more than 31 days for Non-Go! vs. 60 days for MGIC Go! Percentage for the reserves account of deferred maintenance which can make the loan MGIC Go! (10%) or non-go! (5%). Both are insurable for MGIC if all other requirements are met The commercial area for conforming loans is 25% but for MGIC is 20%

9 Additional Requirements for MGIC non-go! Condominium Projects Projects with > 10 units Construction of the project or phase is greater than 90% complete At least 51% of the units are sold and conveyed to owner-occupants for use as primary residence or second home Max investor ownership up to 30% of the units No single entity owns more than 10% of the units No more than 15% of the units are more than 30 or more days delinquent on HOA fees

10 Additional Requirements for MGIC non-go! Condominium Projects No more than 20% of the total building square footage is used for commercial purposes Max MGIC-insured units up to 33% of the units sold in the project Changes in Projects with 4-10 units No more than 25% of the units are more than 30 or more days delinquent on HOA fees No space within the development is used for commercial purposes

11 Business Opportunities presented by: Todd Pittman, Managing Director, Southeast Region

12 The information presented in this presentation is for general information only, and is based on guidelines and practices generally accepted within the mortgage finance industry and is not intended to be all-inclusive. MGIC makes no representations or warranties of any kind with respect to the accuracy, completeness or suitability for any purpose of the information contained in this presentation. MGIC expressly disclaims any and all warranties, express or implied, including without limitation warranties of merchantability and fitness for a particular purpose regarding these materials and this presentation. In no event will MGIC be liable for any direct, indirect, incidental, punitive or consequential damages of any kind with respect to the presentation or materials provided. All examples are hypothetical and are for illustrative purposes only. This presentation is not intended and should not be interpreted or relied upon as legal advice. We encourage you to seek advice from a qualified professional.

13 Who we are The nation s oldest private mortgage insurer, with insurance in force of $183.5 billion $4.6 billion cash and investment portfolio as of 3/31/2017, which generates investment income (excludes $451 million at holding company) Preliminary risk-to-capital was 9.9:1 as of 3/31/2017 $1.3 billion reserved for future claim payments as of 3/31/2017

14 Who we are In 1957 Max Karl founded the modern MI industry and MGIC in Milwaukee, WI ~800 employees, including an experienced sales and underwriting team covering the United States, Puerto Rico and Guam

15 What we do Take first-loss credit position on low down payment residential mortgages Reduce cost for borrowers and promote risk-sharing compared to FHA Enable private investments in mortgage credit risk Provide long-term credit enhancement options to investors

16 What we focus on Expanding opportunities for responsible borrowers to achieve and sustain homeownership Maximizing the amount of new business written Maintaining rational underwriting guidelines and pricing

17 What we focus on Mitigating losses in a professional and responsible manner Maintaining industry leading cost advantage

18 Business Opportunities MGIC in Puerto Rico: Currently the only mortgage insurance company on the island Insuring since 1967 Committed to making homeownership affordable

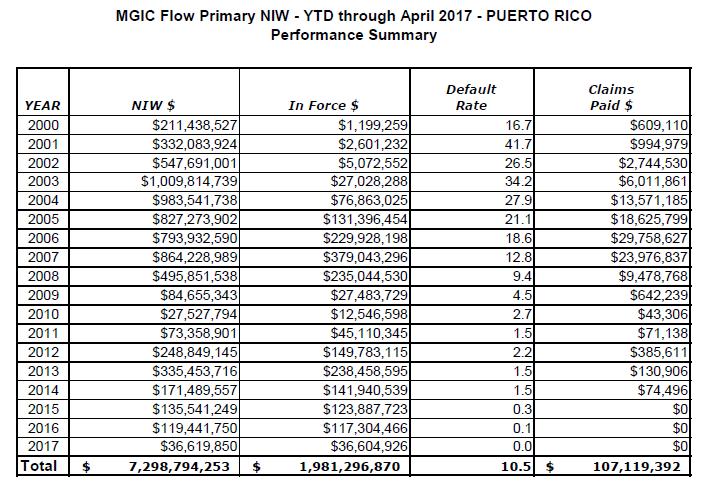

19 Performance

20 Follow Linkedin.com/company/mgic mgic.com/mgicconnects MGICvideos

21 Thank you for choosing MGIC for your mortgage insurance needs

Working with MGIC. Simple, Fair, Transparent

Working with MGIC Simple, Fair, Transparent The information presented in this presentation is for general information only, and is based on guidelines and practices generally accepted within the mortgage

Working with MGIC Simple, Fair, Transparent The information presented in this presentation is for general information only, and is based on guidelines and practices generally accepted within the mortgage

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director Agenda What makes up a credit score (and what doesn t) What causes that score to move

Fact, Fiction & FICOs: Presented by: Vance Edwards, CMB Certified FICO Professional MGIC Marketing Program Director Agenda What makes up a credit score (and what doesn t) What causes that score to move

the Mortgage Process Designs for Learning

The Fundamentals of the Mortgage Process Designs for Learning 1 Legal Disclaimer The information presented in these training materials is based on guidelines and practices accepted within the mortgage

The Fundamentals of the Mortgage Process Designs for Learning 1 Legal Disclaimer The information presented in these training materials is based on guidelines and practices accepted within the mortgage

Self-Employed Borrower Schedule Analysis Method or SAM. Review of the S Corporation Tax Returns Including K-1 April 2017

Self-Employed Borrower Schedule Analysis Method or SAM Review of the S Corporation Tax Returns Including K-1 April 2017 Genworth Mortgage Insurance Corporation 2017 Genworth Financial, Inc. All rights

Self-Employed Borrower Schedule Analysis Method or SAM Review of the S Corporation Tax Returns Including K-1 April 2017 Genworth Mortgage Insurance Corporation 2017 Genworth Financial, Inc. All rights

Self-Employed Borrower Schedule Analysis Method or SAM. Review of the Partnership Tax Returns Including K-1 February 2017

Self-Employed Borrower Schedule Analysis Method or SAM Review of the Partnership Tax Returns Including K-1 February 2017 Genworth Mortgage Insurance Corporation 2017 Genworth Financial, Inc. All rights

Self-Employed Borrower Schedule Analysis Method or SAM Review of the Partnership Tax Returns Including K-1 February 2017 Genworth Mortgage Insurance Corporation 2017 Genworth Financial, Inc. All rights

Avoiding Common Underwriting Errors

September 2015 2012 Genworth Financial, Inc. All rights reserved. Agenda General Underwriting Tips Resources and tools Capacity Credit History Capital Common Sense Compliance 1 Resources Job Aides, Tools

September 2015 2012 Genworth Financial, Inc. All rights reserved. Agenda General Underwriting Tips Resources and tools Capacity Credit History Capital Common Sense Compliance 1 Resources Job Aides, Tools

SECTION 9 HFA PREFERRED TM PROGRAM

SECTION 9 HFA PREFERRED TM PROGRAM 9.1 Eligible Loan Purpose 9.2 Principal Residence Requirement; Owner-Occupancy 9.3 Eligible Property Types 9.4 Sales Price Limits 9.5 Closing Costs 9.6 Interest Rate

SECTION 9 HFA PREFERRED TM PROGRAM 9.1 Eligible Loan Purpose 9.2 Principal Residence Requirement; Owner-Occupancy 9.3 Eligible Property Types 9.4 Sales Price Limits 9.5 Closing Costs 9.6 Interest Rate

Millennials: Obstacles, Opinions & Opportunities

Millennials: Obstacles, Opinions & Opportunities Presented by: Jack Long MGIC Sales Manager Legal Disclaimer The information presented in this presentation is for general information only, and is based

Millennials: Obstacles, Opinions & Opportunities Presented by: Jack Long MGIC Sales Manager Legal Disclaimer The information presented in this presentation is for general information only, and is based

Marketing to Different Generations Opportunities in Today s Market

Marketing to Different Generations Opportunities in Today s Market Presented by: Danielle Swerczek Account Manager Nebraska, North Dakota, South Dakota Before we get started The information presented in

Marketing to Different Generations Opportunities in Today s Market Presented by: Danielle Swerczek Account Manager Nebraska, North Dakota, South Dakota Before we get started The information presented in

Avoiding Common Underwriting Errors

November 2016 2012 Genworth Financial, Inc. All rights reserved. Agenda Introduction General Underwriting Tips Resources Examining and Documenting Files Specific Errors and Recommendations Capacity, Credit

November 2016 2012 Genworth Financial, Inc. All rights reserved. Agenda Introduction General Underwriting Tips Resources Examining and Documenting Files Specific Errors and Recommendations Capacity, Credit

AIG Investments Underwriting Guidelines

AIG Investments Underwriting Guidelines September 5, 2018 MC-2-A987H-1016 2018 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated September 5, 2018.

AIG Investments Underwriting Guidelines September 5, 2018 MC-2-A987H-1016 2018 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated September 5, 2018.

Conventional 97% LTV Options updated 12/5/2018 Freddie Mac HomeOne Mortgage 97% LTV

Max Mortgage Credit Score Max 620, but due to MI requirements borrowers under 680 may benefit from FHA Financing due to MI amounts price comparison is strongly suggested 97% 1 unit 95% for 2 4 unit owner

Max Mortgage Credit Score Max 620, but due to MI requirements borrowers under 680 may benefit from FHA Financing due to MI amounts price comparison is strongly suggested 97% 1 unit 95% for 2 4 unit owner

2016 Wisconsin Real Estate and Economic Outlook Conference. October 13, 2016

2016 Wisconsin Real Estate and Economic Outlook Conference October 13, 2016 Legal Disclaimer The information presented in this presentation is for general information only, and is based on guidelines and

2016 Wisconsin Real Estate and Economic Outlook Conference October 13, 2016 Legal Disclaimer The information presented in this presentation is for general information only, and is based on guidelines and

HomeReady vs. Home Possible Comparison

Occupancy At least one of the borrowers must occupy as their Principal residence All borrowers must occupy as their Principal residence Primary Residence only Non-occupant Non-occupant borrowers permitted

Occupancy At least one of the borrowers must occupy as their Principal residence All borrowers must occupy as their Principal residence Primary Residence only Non-occupant Non-occupant borrowers permitted

Home Possible and Home Possible Advantage

Home Possible and Home Possible Advantage 1 Freddie Mac Home Possible and Home Possible Advantage mortgages (collectively referred to as Home Possible mortgages) are Freddie Mac s Affordable Mortgage products.

Home Possible and Home Possible Advantage 1 Freddie Mac Home Possible and Home Possible Advantage mortgages (collectively referred to as Home Possible mortgages) are Freddie Mac s Affordable Mortgage products.

AIG Investments Underwriting Guidelines

AIG Investments Underwriting Guidelines September 18, 2017 MC-2-A987H-1016 2017 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated. The Underwriting

AIG Investments Underwriting Guidelines September 18, 2017 MC-2-A987H-1016 2017 AIG Investments. All Rights Reserved. These AIG Investments Underwriting Guidelines (Exhibit A-1) are dated. The Underwriting

Announcement 09-08R June 8, Temporary High-Cost Area Loan Limits and Revised Eligibility Requirements for High-Balance Mortgage Loans

Announcement 09-08R June 8, 2009 Amends these Guides: Selling Temporary High-Cost Area Loan Limits and Revised Eligibility Requirements for High-Balance Mortgage Loans Introduction This Announcement (09-08R)

Announcement 09-08R June 8, 2009 Amends these Guides: Selling Temporary High-Cost Area Loan Limits and Revised Eligibility Requirements for High-Balance Mortgage Loans Introduction This Announcement (09-08R)

Attention All Correspondent Lending Sellers: April 20, 2018 CA Announcing Freddie Mac Home Possible and Home Possible Advantage

Attention All Correspondent Lending Sellers: April 20, 2018 CA 18-037 Announcing Freddie Mac Home Possible and Home Possible Advantage Subject Summary Effective Date Home Possible Advantage Mortgage Maximum

Attention All Correspondent Lending Sellers: April 20, 2018 CA 18-037 Announcing Freddie Mac Home Possible and Home Possible Advantage Subject Summary Effective Date Home Possible Advantage Mortgage Maximum

Know Your Products. Marc Kaplan, Sr. VP Retail Sales

Know Your Products Marc Kaplan, Sr. VP Retail Sales 1 Product Overview Agenda 1. Fannie Mae Federal National Mortgage Association (FNMA) 2. Freddie Mac Federal Home Loan Mortgage Corp. (FHLMC) 3. FHA Federal

Know Your Products Marc Kaplan, Sr. VP Retail Sales 1 Product Overview Agenda 1. Fannie Mae Federal National Mortgage Association (FNMA) 2. Freddie Mac Federal Home Loan Mortgage Corp. (FHLMC) 3. FHA Federal

7.1 Genworth-Insured Refinance Program (04/03/09)

") Genworth Mortgage Insurance 7.1 Genworth-Insured Refinance Program (04/03/09) The Genworth-Insured Refinance Program provides expanded underwriting guidelines for rate/term refinances of Genworth-insured

Genworth Mortgage Insurance 7.1 Genworth-Insured Refinance Program (04/03/09) The Genworth-Insured Refinance Program provides expanded underwriting guidelines for rate/term refinances of Genworth-insured

FNMA vs FHLMC Guideline Comparisons

FNMA vs FHLMC Guideline Comparisons Table A: Guidelines for Maximum LTV and Loan Amounts Max LTV/ Loan Amount FANNIE MAE FREDDIE MAC Primary Residence 1 Unit Max LTV Max ARM LTV Max Loan Amount* Max LTV

FNMA vs FHLMC Guideline Comparisons Table A: Guidelines for Maximum LTV and Loan Amounts Max LTV/ Loan Amount FANNIE MAE FREDDIE MAC Primary Residence 1 Unit Max LTV Max ARM LTV Max Loan Amount* Max LTV

Guidelines Correspondent. Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits:

LTV Limits:") Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Property Type w/o Sec Fin. PURCHASE MORTGAGES w/sec Fin. Max TLTV Max HTLTV Loan Limits 1 Unit

Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Property Type w/o Sec Fin. PURCHASE MORTGAGES w/sec Fin. Max TLTV Max HTLTV Loan Limits 1 Unit

COMMERCIAL / MULTIFAMILY MORTGAGE DELINQUENCY RATES FOR MAJOR INVESTOR GROUPS Q3 2017

COMMERCIAL / MULTIFAMILY MORTGAGE DELINQUENCY RATES FOR MAJOR INVESTOR GROUPS Q3 2017 This data is provided by MBA solely for use as a reference. No part of the survey or data may be reproduced, stored

COMMERCIAL / MULTIFAMILY MORTGAGE DELINQUENCY RATES FOR MAJOR INVESTOR GROUPS Q3 2017 This data is provided by MBA solely for use as a reference. No part of the survey or data may be reproduced, stored

Assistance Program: City of Tampa Mortgage Assistance Program Code: DFLTAMPA

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

Investor Participation and Risks

Investor Participation and Risks How investors can participate P A R T I C I P A T E : The trio Obelisk Program trio is the platform that finances the purchase of a property when a lease-to-own agreement

Investor Participation and Risks How investors can participate P A R T I C I P A T E : The trio Obelisk Program trio is the platform that finances the purchase of a property when a lease-to-own agreement

Fannie Mae DU Refi Plus ; Conforming High Balance Changes and New Appraisal Pricing

MSI Mortgage Services III, LLC Wholesale Partner Announcement At MSI Your Interest Is Our Priority! A Subsidiary of First State Bank Member FDIC Issue Date 5/07/09 Effective Date As Noted WPA 2009-020

MSI Mortgage Services III, LLC Wholesale Partner Announcement At MSI Your Interest Is Our Priority! A Subsidiary of First State Bank Member FDIC Issue Date 5/07/09 Effective Date As Noted WPA 2009-020

WHOLESALE BORROWER PAID COMPENSATION RATE SHEET. Liberty Savings Bank Contact Information

Rate Sheet Date: Rate Sheet Price Code: 3/8/2019 3453 *Effective at 11:00 am EST WHOLESALE BORROWER PAID COMPENSATION RATE SHEET FOR LENDER PAID, BROKER MUST DEDUCT COMPENSATION Liberty Savings Bank Contact

Rate Sheet Date: Rate Sheet Price Code: 3/8/2019 3453 *Effective at 11:00 am EST WHOLESALE BORROWER PAID COMPENSATION RATE SHEET FOR LENDER PAID, BROKER MUST DEDUCT COMPENSATION Liberty Savings Bank Contact

<logo> Offered through 21 st Century Home Loans WHOLESALE DIVISION

CHF ACCESS Training Offered through 21 st Century Home Loans WHOLESALE DIVISION Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie

CHF ACCESS Training Offered through 21 st Century Home Loans WHOLESALE DIVISION Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie

PUERTO RICO UNDERWRITING SUMMARY

Questions? Contact the MGIC-Puerto Rico Underwriting Service Center, (787) 765-6545. This summary highlights our most common loan programs. It does not replace our Underwriting Guide, which contains definitions

Questions? Contact the MGIC-Puerto Rico Underwriting Service Center, (787) 765-6545. This summary highlights our most common loan programs. It does not replace our Underwriting Guide, which contains definitions

MODIFICATION REQUEST FORM HARP / Distressed Modifications / Traditional Modifications

MODIFICATION REQUEST FORM HARP / Distressed Modifications / Traditional Modifications United Guaranty Residential Insurance Company P. O. Box 21367 Greensboro, NC 27420-1367 Phone: 888.822.5584 (select

MODIFICATION REQUEST FORM HARP / Distressed Modifications / Traditional Modifications United Guaranty Residential Insurance Company P. O. Box 21367 Greensboro, NC 27420-1367 Phone: 888.822.5584 (select

loan purchase operations training chfa conventional loan programs for closers, funders, and shippers

loan purchase operations training chfa conventional loan programs for closers, funders, and shippers Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training events.

loan purchase operations training chfa conventional loan programs for closers, funders, and shippers Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training events.

FNMA HomeReady & Loan Programs 97%

HomeReady FNMA Standard 97% Description Program DU Eligibility Huron Valley Financial product offering for Fannie Mae 97% is three products offered: 97% Fannie Mae Home Ready Fannie Mae Standard 97% Fannie

HomeReady FNMA Standard 97% Description Program DU Eligibility Huron Valley Financial product offering for Fannie Mae 97% is three products offered: 97% Fannie Mae Home Ready Fannie Mae Standard 97% Fannie

FINANCING OPTIONS FOR CONDOMINIUMS WITH PENDING HOA LITIGATION

FINANCING OPTIONS FOR CONDOMINIUMS WITH PENDING HOA LITIGATION Donald M. Maher Non-Warrantable Condominium Loan Expert www.hoalitigationcondoloans.com (800) 736-0565 Overview This white paper offers information

FINANCING OPTIONS FOR CONDOMINIUMS WITH PENDING HOA LITIGATION Donald M. Maher Non-Warrantable Condominium Loan Expert www.hoalitigationcondoloans.com (800) 736-0565 Overview This white paper offers information

Assistance Program: City of North Lauderdale Purchase Assistance Program Code: DFLLAUDER

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

Assistance Program: City of Tuscaloosa Home Purchase Assistance Program Code: DALTUSHPP

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

Guideline Summary for Housing Finance Agencies

Guideline Summary for Housing Finance Agencies underwriters include: Corporation Genworth Residential Mortgage Insurance Corporation of North Carolina Genworth Residential Mortgage Assurance Corporation

Guideline Summary for Housing Finance Agencies underwriters include: Corporation Genworth Residential Mortgage Insurance Corporation of North Carolina Genworth Residential Mortgage Assurance Corporation

30 YEAR CONFORMING MORTGAGE RATES 30 YEAR CONFORMING MORTGAGE PDF FREDDIE MAC CONFORMING MORTGAGE PROGRAM GUIDE

30 YEAR CONFORMING MORTGAGE PDF FREDDIE MAC CONFORMING MORTGAGE PROGRAM GUIDE FANNIE MAE AND FREDDIE MAC MAXIMUM LOAN LIMITS FOR 1 / 5 2 / 5 3 / 5 30 year conforming mortgage pdf FHLMC 25 YEAR FIXED 300

30 YEAR CONFORMING MORTGAGE PDF FREDDIE MAC CONFORMING MORTGAGE PROGRAM GUIDE FANNIE MAE AND FREDDIE MAC MAXIMUM LOAN LIMITS FOR 1 / 5 2 / 5 3 / 5 30 year conforming mortgage pdf FHLMC 25 YEAR FIXED 300

Arch Rate Quote and Standard MI Order. Loan Fulfillment Center Feature Enhancement

Arch Rate Quote and Standard MI Order Loan Fulfillment Center Feature Enhancement Confidentiality Copyright 2017 Mortgage Cadence, ALL RIGHTS RESERVED. This documentation and the information, data, software

Arch Rate Quote and Standard MI Order Loan Fulfillment Center Feature Enhancement Confidentiality Copyright 2017 Mortgage Cadence, ALL RIGHTS RESERVED. This documentation and the information, data, software

Assistance Program: City of Los Angeles Low Income Purchase Assistance Program (LIPA) Zero Interest Code: DCALIPADP

Zero Interest Code: DCALIPADP") HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

UHM Production Bulletin

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-07 (Reminder) On 1/20/17,

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-07 (Reminder) On 1/20/17,

Bulletin NUMBER: TO: Freddie Mac Sellers November 15, 2011

Bulletin NUMBER: 2011-22 TO: Freddie Mac Sellers November 15, 2011 INTRODUCTION On October 24, 2011 the Federal Housing Finance Agency (FHFA), together with Freddie Mac and Fannie Mae, issued a press release

Bulletin NUMBER: 2011-22 TO: Freddie Mac Sellers November 15, 2011 INTRODUCTION On October 24, 2011 the Federal Housing Finance Agency (FHFA), together with Freddie Mac and Fannie Mae, issued a press release

1-Unit properties, including condominiums and units in Planned Unit Developments o No Manufactured Homes

OVERVIEW HomeOne mortgage, a new conventional (non-fha) 3% down payment option for qualified first-time homebuyers. HomeOne mortgage broadly serves borrowers without geographic or income restrictions.

OVERVIEW HomeOne mortgage, a new conventional (non-fha) 3% down payment option for qualified first-time homebuyers. HomeOne mortgage broadly serves borrowers without geographic or income restrictions.

RBC Capital Markets Financial Institutions Conference. March MGIC Investment Corporation (NYSE: MTG) 1

1") RBC Capital Markets Financial Institutions Conference March 2018 MGIC Investment Corporation (NYSE: MTG) 1 Forward Looking Statements As used below, we, our and us refer to MGIC Investment Corporation

RBC Capital Markets Financial Institutions Conference March 2018 MGIC Investment Corporation (NYSE: MTG) 1 Forward Looking Statements As used below, we, our and us refer to MGIC Investment Corporation

Investor Presentation May MGIC Investment Corporation (NYSE: MTG)

") Investor Presentation May 2018 MGIC Investment Corporation (NYSE: MTG) Forward Looking Statements As used below, we, our and us refer to MGIC Investment Corporation s consolidated operations or to MGIC

Investor Presentation May 2018 MGIC Investment Corporation (NYSE: MTG) Forward Looking Statements As used below, we, our and us refer to MGIC Investment Corporation s consolidated operations or to MGIC

MDR COMMERCIAL / MULTIFAMILY MORTGAGE DELINQUENCY RATES FOR MAJOR INVESTOR GROUPS Q mba.org/research

Q2 Q 2 MD R MDR COMMERCIAL / MULTIFAMILY MORTGAGE DELINQUENCY RATES FOR MAJOR INVESTOR GROUPS Q2 2015 This data is provided by MBA solely for use as a reference. No part of the survey or data may be reproduced,

Q2 Q 2 MD R MDR COMMERCIAL / MULTIFAMILY MORTGAGE DELINQUENCY RATES FOR MAJOR INVESTOR GROUPS Q2 2015 This data is provided by MBA solely for use as a reference. No part of the survey or data may be reproduced,

Assistance Program: County of San Diego Homebuyer Downpayment & Closing Cost Assistance (DCCA)/CalHome Code: DCASDDCCA

/CalHome Code: DCASDDCCA") HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

program compliance loan operations training chfa conventional loan programs for processors and underwriters

program compliance loan operations training chfa conventional loan programs for processors and underwriters Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training

program compliance loan operations training chfa conventional loan programs for processors and underwriters Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training

HomePath Program Guidelines

The following guidelines apply to all DIRECTORS MORTGAGE s HomePath loan programs. All loans must adhere to the criteria of these guidelines. This guide addresses the specific areas needed to facilitate

The following guidelines apply to all DIRECTORS MORTGAGE s HomePath loan programs. All loans must adhere to the criteria of these guidelines. This guide addresses the specific areas needed to facilitate

ditech BUSINESS LENDING CONFORMING FIXED RATE PRODUCT (FANNIE MAE ELIGIBLE)

") 1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage DU Version 10.2 Servicing retained 10 to 30 year term in annual increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans

1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage DU Version 10.2 Servicing retained 10 to 30 year term in annual increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans

ONE TIME CLOSE RENOVATION TO PERM OPTION III

ONE TIME CLOSE RENOVATION TO PERM OPTION III REVISION DATE: 5/4/2018 PRODUCT CODES: RP 1x 15 YR Renovation, RP 1x 30 YR Renovation, RP 1x 5/1 LIBOR ARM 275 2/2/5, RP 1x 5/1 TBill ARM 275 2/2/5, RP 1x 7/1

ONE TIME CLOSE RENOVATION TO PERM OPTION III REVISION DATE: 5/4/2018 PRODUCT CODES: RP 1x 15 YR Renovation, RP 1x 30 YR Renovation, RP 1x 5/1 LIBOR ARM 275 2/2/5, RP 1x 5/1 TBill ARM 275 2/2/5, RP 1x 7/1

WHOLESALE BORROWER PAID COMPENSATION RATE SHEET. Liberty Savings Bank Contact Information

Rate Sheet Date: Rate Sheet Price Code: *Effective at 11:00 am EST 09/14/2018 3319 WHOLESALE BORROWER PAID COMPENSATION RATE SHEET FOR LENDER PAID, BROKER MUST DEDUCT COMPENSATION Liberty Savings Bank

Rate Sheet Date: Rate Sheet Price Code: *Effective at 11:00 am EST 09/14/2018 3319 WHOLESALE BORROWER PAID COMPENSATION RATE SHEET FOR LENDER PAID, BROKER MUST DEDUCT COMPENSATION Liberty Savings Bank

PMI (4764) pmi-us.com

pmi-us.com") 800.966.4PMI (4764) AnswerCenter@pmigroup.com pmi-us.com NON-DISTRESSED PMI MARKETS ELIGIBILITY MATRIX FULL DOC STANDARD JUMBO LOANS* Owner-Occupied Purchase Only Owner-Occupied Purchase or Rate/ Term

800.966.4PMI (4764) AnswerCenter@pmigroup.com pmi-us.com NON-DISTRESSED PMI MARKETS ELIGIBILITY MATRIX FULL DOC STANDARD JUMBO LOANS* Owner-Occupied Purchase Only Owner-Occupied Purchase or Rate/ Term

Hosted by: Learning and Development Presented by: Cathy Bell & Deb Baider Date: Jan 4 th, 2017

Hosted by: Learning and Development Presented by: Cathy Bell & Deb Baider Date: Jan 4 th, 2017 Freedom from reps & warrants plus greater speed and simplicity for Fannie Mae s lender partners DU Validation

Hosted by: Learning and Development Presented by: Cathy Bell & Deb Baider Date: Jan 4 th, 2017 Freedom from reps & warrants plus greater speed and simplicity for Fannie Mae s lender partners DU Validation

WELCOME. Introductions. Housekeeping items. Breaks. Getting Started

Training on CHFA WELCOME Introductions Getting Started Housekeeping items Breaks AGENDA Website www.chfa.org About CHFA-Mission/History Homebuyer Programs Reserving CHFA Funds Homebuyer Program Guidelines

Training on CHFA WELCOME Introductions Getting Started Housekeeping items Breaks AGENDA Website www.chfa.org About CHFA-Mission/History Homebuyer Programs Reserving CHFA Funds Homebuyer Program Guidelines

Ohio Housing & U.S. Bank Home Mortgage- MRBP Division. Product and Underwriting Guidelines

Ohio Housing & U.S. Bank Home Mortgage- MRBP Division Product and Underwriting Guidelines Lou Caresani 2013 Disclaimer This presentation is for basic informational purposes only. It does not modify or

Ohio Housing & U.S. Bank Home Mortgage- MRBP Division Product and Underwriting Guidelines Lou Caresani 2013 Disclaimer This presentation is for basic informational purposes only. It does not modify or

Assistance Program: City of Austin Shared Equity Down Payment Assistance Code: DTXSHARED

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

PURCHASE. Max LTV w/o Sec. Fin. Max LTV w/ Sec. Fin. Max TLTV w/ Sec. Fin.

Agency Revised 3/26/2014 Correspondent Lending Freddie Mac Standard Fixed Rate and ARM Product Profile excludes: Relief Refinance and Super Conforming ELIGIBILITY MATRIX Overlays to Freddie guidelines

Agency Revised 3/26/2014 Correspondent Lending Freddie Mac Standard Fixed Rate and ARM Product Profile excludes: Relief Refinance and Super Conforming ELIGIBILITY MATRIX Overlays to Freddie guidelines

ditech BUSINESS LENDING CONFORMING HIGH-BALANCE PRODUCT (FANNIE MAE ELIGIBLE)

") 1. PRODUCT DESCRIPTION ditech BUSINESS LENDING CONFORMING HIGH-BALANCE PRODUCT Conventional Conforming fixed rate mortgage with High- Balance loan limits DU Version 10.2 Servicing retained 10 to 30 year

1. PRODUCT DESCRIPTION ditech BUSINESS LENDING CONFORMING HIGH-BALANCE PRODUCT Conventional Conforming fixed rate mortgage with High- Balance loan limits DU Version 10.2 Servicing retained 10 to 30 year

(TC) TRADITIONAL PROGRAM MATRIX CONFORMING & HIGH BALANCE

TRADITIONAL PROGRAM MATRIX CONFORMING & HIGH BALANCE") AGENCY CONFORMING DU Multiple Financed Properties CONFORMING DU Multiple Financed Properties FINANCE TYPE PURCHASE & RATE/TERM REFINANCE DELAYED FINANCING CASH OUT REFINANCE OCCUPANCY SECOND HOME INVESTMENT

AGENCY CONFORMING DU Multiple Financed Properties CONFORMING DU Multiple Financed Properties FINANCE TYPE PURCHASE & RATE/TERM REFINANCE DELAYED FINANCING CASH OUT REFINANCE OCCUPANCY SECOND HOME INVESTMENT

Assistance Program: Pima County HOME Down Payment Assistance Loan Code: DAZFHRDPA

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

HLA Rate Sheet FOR INTERNAL USE ONLY. Conventional Fixed Products. 15 Year Fixed 10 Year Fixed 15 Year Fixed Seconds

Lock desk is open from 9:30am to 4:30am (ET). Rates and prices are considered expired outside that window. PROMOTION 0.25% Yield credit on Conventional Loans $200,000 or greater with credit score of 720+

Lock desk is open from 9:30am to 4:30am (ET). Rates and prices are considered expired outside that window. PROMOTION 0.25% Yield credit on Conventional Loans $200,000 or greater with credit score of 720+

VERY IMPORTANT THE LOAN WILL BE RUN THROUGH DU PRIOR TO START OF CONSTRUCTION AND MUST REFLECT APPROVE ELIGIBLE.

REVISION DATE: PRODUCT CODES: One Time CP 15YR, One Time CP 30 YR. PURPOSE: To construct Borrower s primary or second residence with credit approval prior to start of construction. Correspondent will monitor

REVISION DATE: PRODUCT CODES: One Time CP 15YR, One Time CP 30 YR. PURPOSE: To construct Borrower s primary or second residence with credit approval prior to start of construction. Correspondent will monitor

Mortgage Market Statistical Annual 2017 Yearbook. Table of Contents

Mortgage Originations Mortgage Origination Activity Mortgage Market Statistical Annual 2017 Yearbook Table of Contents Mortgage Origination Indicators: 1995-2016... 3 Mortgage Originations by Product:

Mortgage Originations Mortgage Origination Activity Mortgage Market Statistical Annual 2017 Yearbook Table of Contents Mortgage Origination Indicators: 1995-2016... 3 Mortgage Originations by Product:

Issue Date 12/10/18 Effective Date As Noted GA

updates and Conforming Product Suite Purpose This announcement includes the following topic: Federal Housing Finance Agency (FHFA) new loan limits Pricing and Funding FHLMC Rental Income Amendments FHLMC

updates and Conforming Product Suite Purpose This announcement includes the following topic: Federal Housing Finance Agency (FHFA) new loan limits Pricing and Funding FHLMC Rental Income Amendments FHLMC

Request for Additional Clarity and Guidance Related to the FHA Single Family Housing Policy Handbook

Brian Montgomery FHA Commissioner and Assistant Secretary for Housing U.S. Department of Housing and Urban Development 451 7 th Street, SW Washington, DC 20410 Request for Additional Clarity and Guidance

Brian Montgomery FHA Commissioner and Assistant Secretary for Housing U.S. Department of Housing and Urban Development 451 7 th Street, SW Washington, DC 20410 Request for Additional Clarity and Guidance

Guidelines Correspondent. Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits:

LTV Limits:") Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Second Home Investment & Non- Owner Property Type Condominiums are ineligible for this product.

Loan Program: 5/1 LIBOR ARM 2/2/5 85 LTV No PMI Dollar Bank (1585) LTV Limits: Occupancy Primary Residence Second Home Investment & Non- Owner Property Type Condominiums are ineligible for this product.

ditech BUSINESS LENDING CONFORMING FIXED RATE PRODUCT (FANNIE MAE ELIGIBLE)

") 1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10 to 30 year term in annual increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans

1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage DU Version 10.1 Servicing retained 10 to 30 year term in annual increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans

LPA HOME POSSIBLE. Home Possible

LPA HOME POSSIBLE Description: Product Term HPML Loan Purpose Acceptable Property Types Home Possible Home Possible (HP) is a Freddie Mac Community Lending program is designed to meet the needs of low-

LPA HOME POSSIBLE Description: Product Term HPML Loan Purpose Acceptable Property Types Home Possible Home Possible (HP) is a Freddie Mac Community Lending program is designed to meet the needs of low-

THC Asset-Liability Management (ALM) Insight Issue 6. Where Asset Liability Management and Transactions Meet. Overview

Insight Issue 6. Where Asset Liability Management and Transactions Meet. Overview") , THC Asset-Liability Management (ALM) Insight Issue 6 Community banks serve their communities by focusing on customers needs based on each banks core competencies. But customers needs can be diverse.

, THC Asset-Liability Management (ALM) Insight Issue 6 Community banks serve their communities by focusing on customers needs based on each banks core competencies. But customers needs can be diverse.

Cook County Bureau of Economic Development Department of Planning and Development. Cook County Program Guidelines by Loan Type At-a-Glance

Cook County Bureau of Economic Development Department of Planning and Development Cook County Program Guidelines by Loan Type At-a-Glance Government Loans Freddie Mac (FRE) Eligible Loans Eligible Loans

Cook County Bureau of Economic Development Department of Planning and Development Cook County Program Guidelines by Loan Type At-a-Glance Government Loans Freddie Mac (FRE) Eligible Loans Eligible Loans

Guidelines Correspondent

Loan Program: 30-Year Fixed Fannie Mae (630) 20-Year Fixed Fannie Mae (620) 15-Year Fixed Fannie Mae (615) LTV Limits: ❶ ❷ ❸ Occupancy Investment & Non-Owner Type❷ 1 Unit PURCHASE MORTGAGES Max LTV Max

Loan Program: 30-Year Fixed Fannie Mae (630) 20-Year Fixed Fannie Mae (620) 15-Year Fixed Fannie Mae (615) LTV Limits: ❶ ❷ ❸ Occupancy Investment & Non-Owner Type❷ 1 Unit PURCHASE MORTGAGES Max LTV Max

Wholesale Rate Sheet

a new lock may be requested at the current market price without incurring the relock fee. 5 Days 0.150% Conventional Fixed Products 30 Year Fixed 20 Year Fixed Rate 30 Day Price 45 Day Price 60 Day Price

a new lock may be requested at the current market price without incurring the relock fee. 5 Days 0.150% Conventional Fixed Products 30 Year Fixed 20 Year Fixed Rate 30 Day Price 45 Day Price 60 Day Price

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile Overlays to Fannie Mae are underlined

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile 06.15.18 Overlays to Fannie Mae are underlined Fannie Mae - DU Approval Owner-Occupied Only, Purchase and Rate & Term Refinance, Fixed

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile 06.15.18 Overlays to Fannie Mae are underlined Fannie Mae - DU Approval Owner-Occupied Only, Purchase and Rate & Term Refinance, Fixed

Best Practices for Wholesale Lending

July 15, 2010 Best Practices for Wholesale Lending by Anna DeSimone On May 20, HUD stopped accepting applications from brokers for FHA approval but began allowing them to originate loans if they are sponsored

July 15, 2010 Best Practices for Wholesale Lending by Anna DeSimone On May 20, HUD stopped accepting applications from brokers for FHA approval but began allowing them to originate loans if they are sponsored

THC Asset-Liability Management (ALM) Insight Issue 5

Insight Issue 5") , WHOLE LOAN SALE TO AGENCIES: A Strategy key words: risk capacity, G-spread, LLPA, yield attribution, fixed rate 1-4 family mortgage, whole loan pricing THC Asset-Liability Management (ALM) Insight Issue

, WHOLE LOAN SALE TO AGENCIES: A Strategy key words: risk capacity, G-spread, LLPA, yield attribution, fixed rate 1-4 family mortgage, whole loan pricing THC Asset-Liability Management (ALM) Insight Issue

Conventional and Government Program Overlays

Financed Properties OVERLAYS All Programs Limited to maximum 2 loans to one borrower, one must be primary residence Minimum Loan Amount $60,000 Allowed for active duty military personnel, military contractors,

Financed Properties OVERLAYS All Programs Limited to maximum 2 loans to one borrower, one must be primary residence Minimum Loan Amount $60,000 Allowed for active duty military personnel, military contractors,

Chapter 9 Product Matrix

Table of Contents Chapter 9 Product Matrix... 1 CONVENTIONAL CONFORMING LOANS... 2 Secondary Market ARM (Adjustable Rate Mortgage) Loans... 4 HARP (Fannie DU Refi Plus and Freddie Open Access)... 5 FHA/VA

Table of Contents Chapter 9 Product Matrix... 1 CONVENTIONAL CONFORMING LOANS... 2 Secondary Market ARM (Adjustable Rate Mortgage) Loans... 4 HARP (Fannie DU Refi Plus and Freddie Open Access)... 5 FHA/VA

CREDIT UNIONS: REAL ESTATE LENDING AND MORTGAGE BANKINGACTIVITIES

CREDIT UNIONS: REAL ESTATE LENDING AND MORTGAGE BANKINGACTIVITIES ACUIA Region 3 Meeting Presented by: Bob Parks, CPA Director, Financial Institutions Group Overview Mortgage market and credit union trends

CREDIT UNIONS: REAL ESTATE LENDING AND MORTGAGE BANKINGACTIVITIES ACUIA Region 3 Meeting Presented by: Bob Parks, CPA Director, Financial Institutions Group Overview Mortgage market and credit union trends

Participating Lender Training

Participating Lender Training 1 CHFA S MISSION To provide housing opportunities for low and moderate - income people in Connecticut and to aid economic development. 2 www.chfa.org 3 CHFA AND BOND COMPLIANCE

Participating Lender Training 1 CHFA S MISSION To provide housing opportunities for low and moderate - income people in Connecticut and to aid economic development. 2 www.chfa.org 3 CHFA AND BOND COMPLIANCE

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY

Product Description Allowable Origination Channel HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year Conforming

Product Description Allowable Origination Channel HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year Conforming

More on Mortgages. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

More on Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Oldest form Any standard home mortgage loan not insured by FHA or guaranteed by Department of

More on Mortgages McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Oldest form Any standard home mortgage loan not insured by FHA or guaranteed by Department of

Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training events. The training content provided is intended

chfa products Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training events. The training content provided is intended to help explain CHFA s programs, but should

chfa products Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training events. The training content provided is intended to help explain CHFA s programs, but should

Automated Property Service: Frequently Asked Questions

Automated Property Service: Frequently Asked Questions December 2014 APS Overview Q1: What is Fannie Mae s Automated Property Service (APS) Fannie Mae s Automated Property Service (APS) is an automated

Automated Property Service: Frequently Asked Questions December 2014 APS Overview Q1: What is Fannie Mae s Automated Property Service (APS) Fannie Mae s Automated Property Service (APS) is an automated

solid, established, reliable - since 1959 All appraisals must be ordered through Nationwide Property & Appraisal Services

Conforming Overlays solid, established, reliable - since 1959 1/5/17 All appraisals must be ordered through Nationwide Property & Appraisal Services All loans must be DU underwritten and receive an Approve

Conforming Overlays solid, established, reliable - since 1959 1/5/17 All appraisals must be ordered through Nationwide Property & Appraisal Services All loans must be DU underwritten and receive an Approve

Correspondent Overlay Matrix

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

UHM Production Bulletin

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-01 HUD: FHA has announced

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-01 HUD: FHA has announced

GUILD MORTGAGE COMPANY Loan program cheat sheet. 100% Financing REHAB PROGRAM 97% FINANCING PROGRAMS CONFORMING ARMS NON CONFORMING ARMS

GUILD MORTGAGE COMPANY Loan program cheat sheet Mar-09 100% Financing REHAB PROGRAM USDA - Rural Housing FHA 203K Streamline VA 97% FINANCING PROGRAMS CONFORMING ARMS FNMA FLEX Win World FNMA My Community

GUILD MORTGAGE COMPANY Loan program cheat sheet Mar-09 100% Financing REHAB PROGRAM USDA - Rural Housing FHA 203K Streamline VA 97% FINANCING PROGRAMS CONFORMING ARMS FNMA FLEX Win World FNMA My Community

Assistance Program: Pasco County Homebuyer Assistance Program Code: DFLPCYHAP

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30 year

Table of Contents. Sample

TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 CHAPTER 2 ACCOUNTABILITY AND MONITORING... 5 2.1 INTERNAL CONTROLS... 5

TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 CHAPTER 2 ACCOUNTABILITY AND MONITORING... 5 2.1 INTERNAL CONTROLS... 5

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC Two common first time homebuyer programs are MyCommunityMortgage from FNMA and Home Possible from FHLMC. This reference will help you understand

Hit the Books: First Time Homebuyer Programs from FNMA and FHLMC Two common first time homebuyer programs are MyCommunityMortgage from FNMA and Home Possible from FHLMC. This reference will help you understand

HLA Rate Sheet FOR INTERNAL USE ONLY. 95% LTV. Extensions 5 Days 0.150% 10 Days 0.200% 15 Days 0.250% 20 Days 0.300% 25 Days 0.350% 30 Days 0.

Lock desk is open from 9:30am to 4:30am (ET). Rates and prices are considered expired outside that window. PROMOTION 0.25% Yield credit on Conventional Fixed Products $200,000 or greater with credit score

Lock desk is open from 9:30am to 4:30am (ET). Rates and prices are considered expired outside that window. PROMOTION 0.25% Yield credit on Conventional Fixed Products $200,000 or greater with credit score

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Program Approval Expiration Housing Authority Second mortgage loan program to be used in conjunction

Announcement May 20, 2005

Announcement 05-03 May 20, 2005 Amends these Guides: Selling Condominium Project Acceptance Fannie Mae is committed to expanding opportunities for homeownership. Condominium ownership typically offers

Announcement 05-03 May 20, 2005 Amends these Guides: Selling Condominium Project Acceptance Fannie Mae is committed to expanding opportunities for homeownership. Condominium ownership typically offers

Radian Guaranty: Ensuring the American Dream with MI MJ Watkins September 2015

Radian Guaranty: Ensuring the American Dream with MI MJ Watkins September 2015 Objective Position Mortgage Insurance (MI) as a resource by helping you understand how to leverage MI to: Expand homeownership

Radian Guaranty: Ensuring the American Dream with MI MJ Watkins September 2015 Objective Position Mortgage Insurance (MI) as a resource by helping you understand how to leverage MI to: Expand homeownership

Section DU Refi Plus Loan Program

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Product Summary... 2 Features and Benefits... 4 Related Bulletins...

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Product Summary... 2 Features and Benefits... 4 Related Bulletins...

MGIC UNDERWRITING GUIDE

MGIC UNDERWRITING GUIDE EFFECTIVE OCT. 20, 2017 Summary of changes Summary of Changes Changes throughout the guide are indicated with green type. Effective OCT. 20,, 2017, as announced in our national

MGIC UNDERWRITING GUIDE EFFECTIVE OCT. 20, 2017 Summary of changes Summary of Changes Changes throughout the guide are indicated with green type. Effective OCT. 20,, 2017, as announced in our national

AUTOMATED UNDERWRITING, CONVENTIONAL

Automated Underwriting rev. 04 Revised 7/2/2013 Plaza s Underwriting Guidelines are designed to provide guidance as a standard to underwriting loans. There are cases where specific loan programs have more

Automated Underwriting rev. 04 Revised 7/2/2013 Plaza s Underwriting Guidelines are designed to provide guidance as a standard to underwriting loans. There are cases where specific loan programs have more

Assistance Program: Palm Beach County SHIP Purchase Assistance Program Code: DFLPBCSMS

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

HOMEOWNERSHIP ASSISTANCE PROGRAM SUMMARY Product Description Allowable Origination Channel Program Name Second mortgage loan program to be used in conjunction with: FHA Fixed Rate Fannie Mae Fixed 30-year

6/18/2015. Residential Mortgage Types and Borrower Decisions. Role of the secondary market Mortgage types:

Residential Mortgage Types and Borrower Decisions Role of the secondary market Mortgage types: Conventional mortgages FHA mortgages VA mortgages Home equity Loans Other Role of mortgage insurance Mortgage

Residential Mortgage Types and Borrower Decisions Role of the secondary market Mortgage types: Conventional mortgages FHA mortgages VA mortgages Home equity Loans Other Role of mortgage insurance Mortgage

Correspondent Overlay Matrix

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published

Correspondent Overlay Matrix The Overlay Matrix is a summary of Pacific Union Financial, LLC (Pacific Union) guideline overlays. This document should be used in conjunction with Pacific Union published