Avoiding Common Underwriting Errors

|

|

|

- Arron Hampton

- 6 years ago

- Views:

Transcription

1 September Genworth Financial, Inc. All rights reserved.

2 Agenda General Underwriting Tips Resources and tools Capacity Credit History Capital Common Sense Compliance 1

3 Resources Job Aides, Tools and Websites 2

4 Generic Fannie Mae Guidelines For Information: 3

5 Generic Freddie Mac Guidelines For Information: 4

6 Freddie Mac Documentation Matrix Documentation Matrix Assists in properly underwriting and documenting the loan file Note: Many changes for rentals are effective for settlements on or after October 25,

7 For Information: 6

8 7

9 Genworth Tools And Webinar Schedule 8

10 Genworth Tools And Webinar Schedule 9

11 General Underwriting Reminders Using Guidelines and AUS Reports, Documenting Files 10

12 Quality Origination Reminders Verify documentation prior to submission to an AUS Always follow prudent underwriting standards Information must be consistent. All applicable guidelines should be followed. Guidelines show minimum requirements. 11

13 Common Underwriting Errors Capacity, Credit History, Capital, Compliance, Common Sense 12

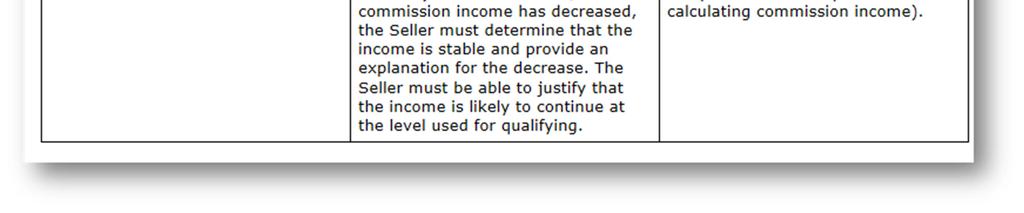

14 Five Cs Capacity Credit History Collateral Capital Compliance Common Sense 13

15 Capacity Errors Income Calculation and Documentation, Self Employed Borrowers 14

16 Capacity Incorrect Documentation Document income per Desktop Underwriter Findings Report or Loan Prospector Feedback Certificate Different products many have different requirements; Always double check product profiles If necessary, obtain additional documentation, explanations or support to clarify the income/employment 15

17 Capacity Steady, Stable, Likely to Continue and History of Receipt Two Year History typically required Guideline exceptions for some income types Examples: Alimony, Survivor Benefits, Retirement, New to Work Force Three Year Continuance Note income, Alimony and child support Supported by Documentation AUS offers minimum requirements Seek additional documentation if necessary to clarify inconsistencies 16

18 Fannie Mae Seller Guide Continuance of Income requirements for Fannie Mae 17

19 Capacity Evaluating Income Types Always Break Income out by Type Overtime/Bonus/Commission History Two Years on the same job Continuance Likely to continue? Declining overtime/bonus Can it be used? Has it Stabilized? Properly explained? Use most conservative amounts when in doubt 18

20 Capacity Show Your Work Agencies/Investors Require Calculations Self Employed Borrowers Complete One or Two Years Tax Returns, signed with all pages and schedules Written Analysis Genworth Income tool available at Rentals Self-employed borrowers Trend Form 1088 Solvency and Liquidity Calculator Notepad your files or letters of income calculations for underwriter to review 19

21 Fannie Mae Seller Guide See B , Commission Income Requirements (06/30/2015) 20

22 Capacity Unreimbursed Employee Business Expenses (UEBE) Fannie Mae Selling Guide Announcement (June 30, 2015) UEBE policy Borrowers qualified using base pay, bonus, overtime or commission <25% The following do not have to be analyzed or deducted or included as a liability. UEBE or 2106 expenses Union Dues Voluntary Deductions Even if identified on tax return or transcript. Still required for commission >25% and other borrowers for whom you must analyze tax returns. Freddie Mac Products UEBE expenses must be subtracted when detected for all borrowers If W-2 transcripts available for LP approvals no further investigation is required. 21

23 Capacity Fannie Mae Rental Income Guidelines Fannie Mae Forms 1037, 1038 and Located at Leases can be used only for purchases and recently acquired rental properties 22

24 Freddie Mac Seller/Servicer Guide Chapter Stable monthly Income and asset qualification sources 23

25 Freddie Mac Seller/Servicer Guide Chapter Stable monthly Income and asset qualification sources 24

26 Bulletin Provides Guidance to stable monthly Income qualification sources 25

27 Bulletin Updates to documentation for Retirement, long-term disability, survivor and dependent benefit income, social security supplemental income and public assistance income. 26

28 Bulletin Updates for Income Continuance Requirements 27

29 Freddie Mac Bonus & Commission Income 28

30 Freddie Mac Bonus & Commission Income 29

31 Capacity Freddie Mac Rental Income Guidelines Updated New Rental Income Matrix (Oct 2015) Increased the maximum number of financed properties from 4-6 *Removing the requirement for Rent Loss Insurance *Removing the requirement of the borrower having a 2-year history of Managing Investment Properties Effective for loan settlements on or after October 26, 2015 Always Check With Your Specific Investor For Overlays Or Variance To This Policy 30

32 Bulletin Effective Dates Staggered Removal of 5% contribution from borrower personal funds Seasoning requirements for Refinances Removal of manual overlay for LP loans with a short sale Removal of Primary Residence Conversion Requirements Updates requirements when credit cards, cash advances or unsecured lines of credit used as source of funds Updates to condominium project review LP Documentation Matrix Updated September 2015 and Rental Income Matrix Updated October

33 Capacity Examine Paystubs Carefully Clear Explanations for Withholding Items Possible Undisclosed Debt Consistent Information Address Social Security Number Last Four Digits Year to Date Consistent With Annual Annual Consistent with Prior Year Verification of Employment Written and Verbal Additional Support Clarify Information 32

34 Fannie Mae Seller Guide Other Income 33

35 Fannie Mae FAQs Answers Common Lender Income Questions dunderwriting 34

36 Credit History Errors Credit Scores, Credit Reports, Liabilities 35

37 Credit History Credit Scores What is the Minimum for the specific product AUS Approve/Accept Eligible, is there an Overlay? Is it a Usable Score: Some examples of overlays might be. Is it based on three or four trade lines? Does it require a 12 month history Does each borrower have to have one? Information Requested from Three One Reported Acceptable to GSEs utilizing AUS with Approve/Accept but as always. 36

38 Credit History Credit Concerns Not Recognized by AUS Documentation Missing such as Missing HUD-1/CD from sale of current property Missing support that current residence is owned free and clear Missing information about cosigned/endorsed credit obligation Examine documents carefully for undisclosed debt Original Loan Application Bank statements Pay stubs Credit Report 37

39 Credit History Minimum Payments Usually on Credit Report If Not on Credit Report or Unreliable Creditor Supplied Documentation Revolving 5% of Outstanding Balance Open Ended Accounts Sufficient Funds for Repayment Yes Inclusion Not Required No Inclusion of 5% Outstanding Balance for Freddie Mac Only Cannot Close Loan until funds to cover the amount for Fannie Mae Third Party Responsibility Example: Employer Reimbursement Document with Letter from Employer/Responsible Party 38

40 Credit History Deferred Installment Debts Must Include regardless of deferment period Monthly Payment from Payment Letter Forbearance Agreement Creditor Supplied Information Student Loans Standard Fannie Mae and Freddie Mac Guidelines: Use the greater of the verified proposed monthly payment amount, or use a minimum of 1% of the outstanding balance for qualifying purposes Review Product Profiles as Overlays May Apply 39

41 Credit History Co-Signed Loans Contingent Liability Examples Co-signed note Business debt guaranty Include if Borrower Qualifies Anyway Most Conservative Approach Situations Allowing Exclusion in Debt Ratio Primary Obligor Pays as Agreed Upon Twelve Months History Situations Requiring Inclusion in Debt Ratio Obligator s Payment Not Documented Sufficient History Not Established Delinquency 40

42 Credit History Recent Credit Inquiries Within 120 Days Freddie Mac requires all inquires to be investigated Fannie Mae no specific policy Confirm New Credit Obtained Inclusion in Credit Report Disclosed on Application Freddie Mac Documentation Examples Creditor Letter Signed Borrower Letter. Obtain Verification Include in Ratios Evaluate Risk Represents Higher Risk Highest Risk in Combination With: Recently Opened Accounts Delinquent Credit Report Reason Codes 41

43 Credit History Derogatory Information AUS Loans Considered in Risk Evaluation Verify the AUS saw the derogatory info Manual review of credit report and codes Is a manual underwrite required when AUS did not see the event? Consult Guidelines Waiting Periods Re-establishing Credit Proper documentation and explanations Extenuating Circumstances vs Financial Mismanagement Investors often apply the Financial Mismanagement waiting periods apply in all cases Review all trade lines on credit report, narratives and public record sections for possible significant derogatory information the AUS does not see 42

44 Capital Errors Seller Concessions, Assets to Close, Borrower s Own Funds, Gift Funds, Reserves and Large Deposits 43

45 Capital Excessive Seller Contributions Follow GSE Standard Guidelines, subject to these maximum contribution amounts: Loans with payment abatements are ineligible. Check for additional AUS or Product Program guideline overlays. 44

46 Capital Large Deposits Fannie Mae/Freddie Mac When Bank statements are used, the lender must evaluate large deposits, which are defined as a single deposit that exceeds 50% of the total monthly qualifying income for the loan if the deposit is needed to meet borrower funds and/or required reserves. When a deposit is not documented and is not needed for borrower funds/reserves, reduce the funds used for qualifying purposes by the amount of the unverified deposit. The reduced asset amount is what is used for LP/DU purposes Fannie Mae If funds verified are 20% or greater of the amount needed for down payment and closing costs, NO proof of liquidation is needed.but review product profiles as this policy may not apply to every product type Newly Opened Accounts Verify accounts opened within 90 days Lender Guidelines May be More Conservative 45

47 Capital Reserves Follow Applicable Guidelines Enter Reserve Funds into AUS System Document Reserves Approve or Accept/Eligible Agency Loans Typically follow AUS report Most investors want only verified assets/reserves entered into AUS Manual Overlays for Investment Properties & 2 nd Homes 46

48 Capital Reserves -Continued Reduction of Certain Types of Assets when used for reserves Retirement Accounts with Documentation of Access Fannie Mae 60% (unless applicant is 59 ½ or older) then 70% use Freddie Mac 70% 47

49 Capital Assets to Close Check Amount Needed Cash to Close Did it change from when loan was approved? Resubmit back to underwriter for review if yes Reserves LP DU *Follow LP Feedback *Follow DU Findings Report Best Practice: Only enter needed funds Other Funds Necessary for Transaction Debts Paid at Close 30-Day Accounts, if applicable *A manual overlay for reserve funds applies to DU & LP files when a borrower owns multiple rental properties and/or second homes and the subject transaction is a second home or investment 48

50 Capital Borrower s Own Funds Determine Required Amount Fannie Mae and Freddie Mac Vary LP Does Not Calculate May be Required if LTV > 80%. Second Homes Investment 2-4 unit Manufactured Home All funds must be the borrower s on an Investment Transaction Gift funds from an acceptable source may be allowed. Acceptable donor gift Agency/Charity grant Proper gift letter, proof of transfer and receipt 49

51 Common Sense Use proper judgment 50

52 Common Sense Occupancy Must Make Sense Review File Documentation for Consistency Types Primary Residence Second Home Investment Property Number of Days to Take Occupancy For Primary residences occupancy within 60 days of closing 51

53 Common Sense Primary Residence Conversion Follow specific program requirements Fannie Mae removed Primary Residence Conversion Overlays Freddie Mac removed Primary Residence Conversion Overlay No more 30% equity requirement No more two or six months reserves for both properties No more evidence of receipt of security deposit Genworth MI Aligns with Agency Updates 52

54 Compliance Completeness 53

55 Compliance Ensure Completeness Two Year History Employment Residence Proofread All Information Provided All Documents in File Program eligibility verified All inconsistencies addressed Complete Explanation to Investor 54

56 Legal Disclaimer Genworth Mortgage Insurance is happy to provide you with these training materials. While we strive for accuracy, we also know that any discussion of laws and their application to particular facts is subject to individual interpretation, change, and other uncertainties. Our training is not intended as legal advice, and is not a substitute for advice of counsel. You should always check with your own legal advisors for interpretations of legal and compliance principles applicable to your business. GENWORTH EXPRESSLY DISCLAIMS ANY AND ALL WARRANTIES, EXPRESS OR IMPLIED, INCLUDING WITHOUT LIMITATION WARRANTIES OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE, WITH RESPECT TO THESE MATERIALS AND THE RELATED TRAINING. IN NO EVENT SHALL GENWORTH BE LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, PUNITIVE, OR CONSEQUENTIAL DAMAGES OF ANY KIND WHATSOEVER WITH RESPECT TO THE TRAINING AND THE MATERIALS. 55

57 Thank you! Genworth Financial is the NAFCU Services Preferred Partner for Private Mortgage Insurance. More educational resources are available at Save the date! October 27 th, 2:00 pm 3:00 pm ET.Analyzing Appraisals: Focus on Sales Comparison That MI Guy! Genworth Financial, Inc. All rights reserved. 56

Avoiding Common Underwriting Errors

November 2016 2012 Genworth Financial, Inc. All rights reserved. Agenda Introduction General Underwriting Tips Resources Examining and Documenting Files Specific Errors and Recommendations Capacity, Credit

November 2016 2012 Genworth Financial, Inc. All rights reserved. Agenda Introduction General Underwriting Tips Resources Examining and Documenting Files Specific Errors and Recommendations Capacity, Credit

Loan Prospector Documentation Matrix

Use the following information as a reference for documenting your Loan Prospector loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie Mac Single-

Use the following information as a reference for documenting your Loan Prospector loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie Mac Single-

Loan Prospector Documentation Matrix

Use the following information as a reference for documenting your Loan Prospector loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie Mac Single-

Use the following information as a reference for documenting your Loan Prospector loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie Mac Single-

Self-Employed Borrower Schedule Analysis Method or SAM. Review of the S Corporation Tax Returns Including K-1 April 2017

Self-Employed Borrower Schedule Analysis Method or SAM Review of the S Corporation Tax Returns Including K-1 April 2017 Genworth Mortgage Insurance Corporation 2017 Genworth Financial, Inc. All rights

Self-Employed Borrower Schedule Analysis Method or SAM Review of the S Corporation Tax Returns Including K-1 April 2017 Genworth Mortgage Insurance Corporation 2017 Genworth Financial, Inc. All rights

UHM Production Bulletin

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-07 (Reminder) On 1/20/17,

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: FHA Annual Premium Reduction, Mortgagee Letter 2017-07 (Reminder) On 1/20/17,

Loan Product Advisor SM Documentation Matrix

Use the following information as a reference for documenting your Loan Product Advisor loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie

Use the following information as a reference for documenting your Loan Product Advisor loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie

Selling Guide Announcement SEL

Selling Guide Announcement SEL-2012-09 Updates to Refi Plus and DU Refi Plus September 14, 2012 The positive impact of Refi Plus and DU Refi Plus continues, enabling borrowers who have demonstrated an

Selling Guide Announcement SEL-2012-09 Updates to Refi Plus and DU Refi Plus September 14, 2012 The positive impact of Refi Plus and DU Refi Plus continues, enabling borrowers who have demonstrated an

Self-Employed Borrower Schedule Analysis Method or SAM. Review of the Partnership Tax Returns Including K-1 February 2017

Self-Employed Borrower Schedule Analysis Method or SAM Review of the Partnership Tax Returns Including K-1 February 2017 Genworth Mortgage Insurance Corporation 2017 Genworth Financial, Inc. All rights

Self-Employed Borrower Schedule Analysis Method or SAM Review of the Partnership Tax Returns Including K-1 February 2017 Genworth Mortgage Insurance Corporation 2017 Genworth Financial, Inc. All rights

Loan Product Advisor SM FHA TOTAL Mortgage Scorecard Documentation Matrix

Loan Product Advisor SM FHA TOTAL Mortgage Scorecard Documentation Matrix The information in this matrix is provided as a tool to help you document Federal Housing Administration (FHA) mortgages. The matrix

Loan Product Advisor SM FHA TOTAL Mortgage Scorecard Documentation Matrix The information in this matrix is provided as a tool to help you document Federal Housing Administration (FHA) mortgages. The matrix

Hosted by: Learning and Development Presented by: Cathy Bell & Deb Baider Date: Jan 4 th, 2017

Hosted by: Learning and Development Presented by: Cathy Bell & Deb Baider Date: Jan 4 th, 2017 Freedom from reps & warrants plus greater speed and simplicity for Fannie Mae s lender partners DU Validation

Hosted by: Learning and Development Presented by: Cathy Bell & Deb Baider Date: Jan 4 th, 2017 Freedom from reps & warrants plus greater speed and simplicity for Fannie Mae s lender partners DU Validation

FNMA HomePath Product Guidelines

April 15, 2013 FNMA HomePath Product Guidelines Standard Conforming Occupancy Primary Residence Max LTV Max TLTV Max CLTV 1 Unit 97 97 97 2 Unit 80 80 80 3-4 Unit 75 75 75 Second Home 1 Unit 90 90 90 Investment

April 15, 2013 FNMA HomePath Product Guidelines Standard Conforming Occupancy Primary Residence Max LTV Max TLTV Max CLTV 1 Unit 97 97 97 2 Unit 80 80 80 3-4 Unit 75 75 75 Second Home 1 Unit 90 90 90 Investment

(TC) TRADITIONAL PROGRAM MATRIX CONFORMING & HIGH BALANCE

TRADITIONAL PROGRAM MATRIX CONFORMING & HIGH BALANCE") AGENCY CONFORMING DU Multiple Financed Properties CONFORMING DU Multiple Financed Properties FINANCE TYPE PURCHASE & RATE/TERM REFINANCE DELAYED FINANCING CASH OUT REFINANCE OCCUPANCY SECOND HOME INVESTMENT

AGENCY CONFORMING DU Multiple Financed Properties CONFORMING DU Multiple Financed Properties FINANCE TYPE PURCHASE & RATE/TERM REFINANCE DELAYED FINANCING CASH OUT REFINANCE OCCUPANCY SECOND HOME INVESTMENT

Max LTV/CLTV FICO 1 Unit 95/95% /90% 620 Purchase 85/85% 620 Refi 75/75% 2 Units Purchase & Refi- 85/85% 620 N/A N/A 75/75% 620

Revision: October 25, 2016 (Product Information Center, 949-390-2670, www.jmaclending.com) Fixed Rate (Purchase & Rate/Term Refinances) Fannie Mae DU Products: CF30, CF20, CF15, CF10 Occupancy Owner Occupied

Revision: October 25, 2016 (Product Information Center, 949-390-2670, www.jmaclending.com) Fixed Rate (Purchase & Rate/Term Refinances) Fannie Mae DU Products: CF30, CF20, CF15, CF10 Occupancy Owner Occupied

Agency Guideline Revisions Note: Underlined items indicate an overlay.

Alimony, Child Support, and Maintenance Payments Products Texas Cash-Out Refi Income Income may be used if received for a minimum of six months and must continue for at least three years after the date

Alimony, Child Support, and Maintenance Payments Products Texas Cash-Out Refi Income Income may be used if received for a minimum of six months and must continue for at least three years after the date

DU 9.1 Revisions and Other Agency Enhancements

Bankruptcies Products (non AUS & DU) If a public record does not indicate a bankruptcy, but an individual tradeline does, the borrower must meet these bankruptcy guidelines. Generally, bankruptcies (except

Bankruptcies Products (non AUS & DU) If a public record does not indicate a bankruptcy, but an individual tradeline does, the borrower must meet these bankruptcy guidelines. Generally, bankruptcies (except

Topic Current FHA Guideline New FHA Guideline

FHA Underwriting Guideline Changes Effective for Case Numbers Assigned On or After September 14, 2015 Assets Gift Funds Documenting Transfer Earnest Money Guidance was unclear about requiring donor s bank

FHA Underwriting Guideline Changes Effective for Case Numbers Assigned On or After September 14, 2015 Assets Gift Funds Documenting Transfer Earnest Money Guidance was unclear about requiring donor s bank

Documentation Guide June 15, 2015

Documentation Guide June 15, 2015 This document is intended to be a reference guide and is not a supplement to Radian s published guidelines. Note: The following guide reflects Radian Standard/Manual underwriting

Documentation Guide June 15, 2015 This document is intended to be a reference guide and is not a supplement to Radian s published guidelines. Note: The following guide reflects Radian Standard/Manual underwriting

FHA Underwriting Changes. Effective for case numbers issued on and after September 14, 2015

FHA Underwriting Changes Effective for case numbers issued on and after September 14, 2015 Today s Presentation Overview of the most substantial changes to the FHA single family handbook. Not realistic

FHA Underwriting Changes Effective for case numbers issued on and after September 14, 2015 Today s Presentation Overview of the most substantial changes to the FHA single family handbook. Not realistic

Summary of Agency Income Guideline Revisions

Summary of Agency Guideline Revisions General Update Comments: All LP (i.e., Loan Prospector) references were changed to LPA (i.e., Loan Product Advisor) For purposes of the revised LP income requirements:

Summary of Agency Guideline Revisions General Update Comments: All LP (i.e., Loan Prospector) references were changed to LPA (i.e., Loan Product Advisor) For purposes of the revised LP income requirements:

FHA Guideline Changes Effective for Case Numbers Assigned On or After September 14, 2015 April 30, 2015

Assets Gift Funds Documenting Transfer Not clear about requiring donor s bank statement in all instances. Requires donor s bank statement showing withdrawal of funds. Earnest Money Document source of funds

Assets Gift Funds Documenting Transfer Not clear about requiring donor s bank statement in all instances. Requires donor s bank statement showing withdrawal of funds. Earnest Money Document source of funds

Loan Product Advisor SM Documentation Matrix

Effective for Mortgages with Freddie Mac Settlement Dates on or after July 6, 2017; but Sellers may implement for Mortgages with Settlement Dates on or after March 6, 2017 Use the following information

Effective for Mortgages with Freddie Mac Settlement Dates on or after July 6, 2017; but Sellers may implement for Mortgages with Settlement Dates on or after March 6, 2017 Use the following information

FHA Changes Effective for Case Numbers on or after 9/14/15

FHA Changes Effective for Case Numbers on or after 9/14/15 Topic Current FHA Guideline New FHA Guideline Gift Funds Documenting Transfer Earnest Money Assets Not clear about requiring donor s bank statement

FHA Changes Effective for Case Numbers on or after 9/14/15 Topic Current FHA Guideline New FHA Guideline Gift Funds Documenting Transfer Earnest Money Assets Not clear about requiring donor s bank statement

ACHIEVE YOUR AMERICAN DREAM WITH AMERICAN LENDING!

Green - Doctors Program Guidelines Property Type 1-Unit Warrantable Condo PUD PRIMARY RESIDENCE - PURCHASE & RATE.TERM REFINANCE Minimum LTV 80.01% 80.01% 80.01% Maximum LTV/CLTV/HCLTV 97% 95% 90% Minimum

Green - Doctors Program Guidelines Property Type 1-Unit Warrantable Condo PUD PRIMARY RESIDENCE - PURCHASE & RATE.TERM REFINANCE Minimum LTV 80.01% 80.01% 80.01% Maximum LTV/CLTV/HCLTV 97% 95% 90% Minimum

HUD Underwriting Changes

HUD Underwriting Changes For all Case # issued on/after 9/14/15 www.impacmortgage.com 9/8/15 MD 1 Goodbye to the 4155 Handbook Approximately 450 handbooks, mortgagee letters and policy statements were

HUD Underwriting Changes For all Case # issued on/after 9/14/15 www.impacmortgage.com 9/8/15 MD 1 Goodbye to the 4155 Handbook Approximately 450 handbooks, mortgagee letters and policy statements were

Desktop Underwriter/Desktop Originator Release Notes

Desktop Underwriter/Desktop Originator Release Notes DU Version 10.2 September Update July 24, 2018 During the weekend of Sept. 22, 2018, Fannie Mae will implement an update to Desktop Underwriter (DU

Desktop Underwriter/Desktop Originator Release Notes DU Version 10.2 September Update July 24, 2018 During the weekend of Sept. 22, 2018, Fannie Mae will implement an update to Desktop Underwriter (DU

Processing VA Mortgages

Introduction The Department of Veterans Affairs (VA) Freddie Mac allows Loan Product Advisor automated underwriting service to assess VA loan applications. The Department of Veterans Affairs then guarantees

Introduction The Department of Veterans Affairs (VA) Freddie Mac allows Loan Product Advisor automated underwriting service to assess VA loan applications. The Department of Veterans Affairs then guarantees

Loan Prospector December 13 Release New and Updated Feedback Messages

Loan Prospector December 13 Release New and Updated Feedback Messages On December 13, we re updating Loan Prospector to align with previously announced underwriting and credit requirement changes. To help

Loan Prospector December 13 Release New and Updated Feedback Messages On December 13, we re updating Loan Prospector to align with previously announced underwriting and credit requirement changes. To help

FNMA VS. FHLMC 09/04/2017

FNMA VS. FHLMC 09/04/2017 Disputed Accounts FNMA When the credit report contains tradelines disputed by the borrower, DU will first assess the risk of the loan casefile using all tradelines, including

FNMA VS. FHLMC 09/04/2017 Disputed Accounts FNMA When the credit report contains tradelines disputed by the borrower, DU will first assess the risk of the loan casefile using all tradelines, including

PRODUCT GUIDELINES LENDER PAID MORTGAGE INSURANCE PROGRAM (LPMI) PROGRAM CODES: C30FLPMI, H30FLPMI

PROGRAM CODES: C30FLPMI, H30FLPMI") Occupancy Purpose Max Loan Amount Maximum LTV/ CLTV LOAN AMOUNTS

Occupancy Purpose Max Loan Amount Maximum LTV/ CLTV LOAN AMOUNTS

Underwriting Guideline Matrix

NewLeaf 1: DU-LP & Program / Product Codes: : NewLeaf 1 30 Year Fixed (W101) NewLeaf 1 20 Year Fixed (W102) NewLeaf 1 15 Year Fixed (W113) NewLeaf 1 10 Year Fixed (W114) NewLeaf 1 30 Year Fixed LPMI (W143)

NewLeaf 1: DU-LP & Program / Product Codes: : NewLeaf 1 30 Year Fixed (W101) NewLeaf 1 20 Year Fixed (W102) NewLeaf 1 15 Year Fixed (W113) NewLeaf 1 10 Year Fixed (W114) NewLeaf 1 30 Year Fixed LPMI (W143)

Bulletin NUMBER: TO: Freddie Mac Sellers November 15, 2011

Bulletin NUMBER: 2011-22 TO: Freddie Mac Sellers November 15, 2011 INTRODUCTION On October 24, 2011 the Federal Housing Finance Agency (FHFA), together with Freddie Mac and Fannie Mae, issued a press release

Bulletin NUMBER: 2011-22 TO: Freddie Mac Sellers November 15, 2011 INTRODUCTION On October 24, 2011 the Federal Housing Finance Agency (FHFA), together with Freddie Mac and Fannie Mae, issued a press release

HUD/FHA POLICY CHANGES EFFECTIVE 09/14/2015

UNDERWRITING TOTAL Scorecard Manual Downgrade Requirements (Topic continued on next page) Manual downgrades are required when: Delinquent federal debt is present. CAIVRS claim is present unless erroneous

UNDERWRITING TOTAL Scorecard Manual Downgrade Requirements (Topic continued on next page) Manual downgrades are required when: Delinquent federal debt is present. CAIVRS claim is present unless erroneous

High-Cost Area (High Balance) Loan Amounts

Loan Amounts") Program Qualifications Eligible loans are conforming and high balance loans receiving a DU Version 10.0 or later Approve/Eligible. Maximum Loan Amounts Conforming Maximum Loan Amounts Units Continental

Program Qualifications Eligible loans are conforming and high balance loans receiving a DU Version 10.0 or later Approve/Eligible. Maximum Loan Amounts Conforming Maximum Loan Amounts Units Continental

Mortgage Bankers Association of Puerto Rico. June 8, 2017

Mortgage Bankers Association of Puerto Rico June 8, 2017 The information presented in this presentation is for general information only, and is based on guidelines and practices generally accepted within

Mortgage Bankers Association of Puerto Rico June 8, 2017 The information presented in this presentation is for general information only, and is based on guidelines and practices generally accepted within

Guideline Reference Applies to ALL Products

Guideline Reference Applies to ALL Products 4506-T CG Ch 5E Loan Documents & Notes CG Ch 6F Employment & Documentation CG Ch 7G FHA Employment & Evaluation & Documentation Product summaries IRS Form 4506T

Guideline Reference Applies to ALL Products 4506-T CG Ch 5E Loan Documents & Notes CG Ch 6F Employment & Documentation CG Ch 7G FHA Employment & Evaluation & Documentation Product summaries IRS Form 4506T

PURCHASE. Max LTV w/o Sec. Fin. Max LTV w/ Sec. Fin. Max TLTV w/ Sec. Fin.

Agency Revised 3/26/2014 Correspondent Lending Freddie Mac Standard Fixed Rate and ARM Product Profile excludes: Relief Refinance and Super Conforming ELIGIBILITY MATRIX Overlays to Freddie guidelines

Agency Revised 3/26/2014 Correspondent Lending Freddie Mac Standard Fixed Rate and ARM Product Profile excludes: Relief Refinance and Super Conforming ELIGIBILITY MATRIX Overlays to Freddie guidelines

Communicate standard industry expectations for the content of documentation provided.

Documentation Guide This document is intended to be a reference guide and is not a supplement to Radian s published guidelines. The purpose of this document is to: Identify the type of documentation that

Documentation Guide This document is intended to be a reference guide and is not a supplement to Radian s published guidelines. The purpose of this document is to: Identify the type of documentation that

Underwriting Procedures

Underwriting Section 4 Underwriting Procedures ----------------------------------------------------------------- 4.2 Underwriting Turn-Around --------------------------------------------------------------

Underwriting Section 4 Underwriting Procedures ----------------------------------------------------------------- 4.2 Underwriting Turn-Around --------------------------------------------------------------

10, 15, 20, 25 & 30 YR Fixed Rates

Agency Correspondent Lending Fannie Mae Standard Fixed Rate and ARM Product Profile excludes: DU Refi Plus, High-Balance, HomeStyle Renovation and MyCommunity Mortgage ELIGIBILITY MATRIX & SUMMARY GUIDELINES

Agency Correspondent Lending Fannie Mae Standard Fixed Rate and ARM Product Profile excludes: DU Refi Plus, High-Balance, HomeStyle Renovation and MyCommunity Mortgage ELIGIBILITY MATRIX & SUMMARY GUIDELINES

Crescent Mortgage Underwriting Guidelines

Crescent Mortgage Underwriting Guidelines 8/10/2018 Underwriting guidelines are subject to change without notice. While every attempt has been made to make this document as complete as possible all loans

Crescent Mortgage Underwriting Guidelines 8/10/2018 Underwriting guidelines are subject to change without notice. While every attempt has been made to make this document as complete as possible all loans

") ; LOAN AMOUNTS

; LOAN AMOUNTS 5/1 ARM 1 ; 7/1 or 10/1 ARM 2 Must exceed Conforming Standard and High Balance Limit for State/County %/40% 80%* 80%* $2,000,000 1

Conventional Jumbo Loan Program The Conventional Jumbo Loan program can be used to provide financing options for Primary Residences with jumbo loan amounts in excess of Conventional High-Balance limits.

Conventional Jumbo Loan Program The Conventional Jumbo Loan program can be used to provide financing options for Primary Residences with jumbo loan amounts in excess of Conventional High-Balance limits.

Loan Product Advisor Documentation Matrix

Effective for Mortgages with Settlement Dates on and after November 30, 2018, but Sellers may implement the changes in their entirety immediately Use the following information as a reference for documenting

Effective for Mortgages with Settlement Dates on and after November 30, 2018, but Sellers may implement the changes in their entirety immediately Use the following information as a reference for documenting

Fannie Mae Conventional Standard Purchase, Rate and Term Refinance and Cash Out Refinance

Product Guideline Summary Fannie Mae Conventional Standard Purchase, Rate and Term Refinance and Cash Out Refinance Fannie Mae Conventional Standard Purchase, Rate and Term Refinance and Cash Out Refinance

Product Guideline Summary Fannie Mae Conventional Standard Purchase, Rate and Term Refinance and Cash Out Refinance Fannie Mae Conventional Standard Purchase, Rate and Term Refinance and Cash Out Refinance

DU Conforming Fixed & ARM and High- Balance Fixed & ARM

DU Conforming Fixed & ARM and High- Balance Fixed & ARM PURCHASE & RATE/TERM REFINANCE PRIMARY RESIDENCE Property Type FRM LTV/CLTV/HCLTV ARM LTV/CLTV/HCLTV 1 Unit 97% (1) 95% (2) 2 Units 85% 85% 3-4 Units

DU Conforming Fixed & ARM and High- Balance Fixed & ARM PURCHASE & RATE/TERM REFINANCE PRIMARY RESIDENCE Property Type FRM LTV/CLTV/HCLTV ARM LTV/CLTV/HCLTV 1 Unit 97% (1) 95% (2) 2 Units 85% 85% 3-4 Units

Gold Jumbo Program Eligibility Guide. Effective 1/1/18

Gold Jumbo Effective 1/1/18 Jumbo Table of Contents Jumbo Loans (QM) Eligibility Matrix...4 Primary Residence Purchase, Rate & Term Refinance...4 Primary Residence Cash-Out Refinance...4 Second Home...4

Gold Jumbo Effective 1/1/18 Jumbo Table of Contents Jumbo Loans (QM) Eligibility Matrix...4 Primary Residence Purchase, Rate & Term Refinance...4 Primary Residence Cash-Out Refinance...4 Second Home...4

FHA Underwriting Updates Before-and-After Matrix Effective for FHA Case Numbers Assigned on and after April 1, 2012

Self Employed Borrowers Generally, standard FHA guidelines apply with some exceptions on documentation requirements. If Approve/Eligible, the borrower must provide two (2) years of individual federal tax

Self Employed Borrowers Generally, standard FHA guidelines apply with some exceptions on documentation requirements. If Approve/Eligible, the borrower must provide two (2) years of individual federal tax

Conventional Loan Program - Quick Reference Guide

Loan Program - Quick Reference Guide Eligible Products LTV/(H)CLTV Matrices and Freddie Only Products 5/1 and 7/1 ARMS, 15 and 30 year Fully Amortizing Fixed Rate Fannie Only Products 5/1 and 7/1 ARMS,

Loan Program - Quick Reference Guide Eligible Products LTV/(H)CLTV Matrices and Freddie Only Products 5/1 and 7/1 ARMS, 15 and 30 year Fully Amortizing Fixed Rate Fannie Only Products 5/1 and 7/1 ARMS,

Desktop Underwriter/Desktop Originator Release Notes

Desktop Underwriter/Desktop Originator Release Notes DU Version 10.3 Oct. 23, 2018 Updated Oct. 31, 2018 During the weekend of Dec. 8, 2018, Fannie Mae will implement Desktop Underwriter (DU ) Version

Desktop Underwriter/Desktop Originator Release Notes DU Version 10.3 Oct. 23, 2018 Updated Oct. 31, 2018 During the weekend of Dec. 8, 2018, Fannie Mae will implement Desktop Underwriter (DU ) Version

AMX / Land Home Financial Services Wholesale Lending Division

1 of 10 Fixed Program Codes: CRR 30-006, CRR25-006, CRR20-006, CRR15-006, SCRR30-006, SCRR15-006 Adjustable Program Codes: Not Available Automated Underwriting: LP Accept/Eligible Conforming Loan Continental

1 of 10 Fixed Program Codes: CRR 30-006, CRR25-006, CRR20-006, CRR15-006, SCRR30-006, SCRR15-006 Adjustable Program Codes: Not Available Automated Underwriting: LP Accept/Eligible Conforming Loan Continental

FHLMC Relief Refinance Open Access

The Federal Housing Finance Agency (FHFA) Home Affordable Refinance Program ( HARP ) is designed to assist borrowers who have demonstrated an acceptable payment history on their existing Freddie Mac mortgage

The Federal Housing Finance Agency (FHFA) Home Affordable Refinance Program ( HARP ) is designed to assist borrowers who have demonstrated an acceptable payment history on their existing Freddie Mac mortgage

Lender Letter LL

Lender Letter LL-2017-05 To: All Fannie Mae Single-Family Sellers High Loan-to-Value Refinance Option September 08, 2017 At the direction of the Federal Housing Finance Agency (FHFA), Fannie Mae will offer

Lender Letter LL-2017-05 To: All Fannie Mae Single-Family Sellers High Loan-to-Value Refinance Option September 08, 2017 At the direction of the Federal Housing Finance Agency (FHFA), Fannie Mae will offer

FHA Underwriting Changes Effective for Case Numbers Assigned on or After September 14, 2015

Assets Topic Gift Funds - Documenting Transfer Earnest Money Large Deposit Definition Joint Funds Access Retirement Accounts Interested Party Credits/Costs Paid Outside Closing/Minimum Required Investment

Assets Topic Gift Funds - Documenting Transfer Earnest Money Large Deposit Definition Joint Funds Access Retirement Accounts Interested Party Credits/Costs Paid Outside Closing/Minimum Required Investment

program compliance loan operations training chfa conventional loan programs for processors and underwriters

program compliance loan operations training chfa conventional loan programs for processors and underwriters Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training

program compliance loan operations training chfa conventional loan programs for processors and underwriters Disclaimer This Disclaimer applies to all content provided through CHFA webinars or other training

AUTOMATED UNDERWRITING, CONVENTIONAL

Automated Underwriting rev. 04 Revised 7/2/2013 Plaza s Underwriting Guidelines are designed to provide guidance as a standard to underwriting loans. There are cases where specific loan programs have more

Automated Underwriting rev. 04 Revised 7/2/2013 Plaza s Underwriting Guidelines are designed to provide guidance as a standard to underwriting loans. There are cases where specific loan programs have more

Fannie Mae (DU) Conventional Loan Matrix

Conventional Loan Matrix") PURCHASE/ LIMITED CASH OUT REFINANCES STANDARD and HIGH BALANCE LOAN AMOUNTS Occupancy Maximum* LTV Maximum* CLTV Min FICO* Max Ratios Minimum Cash Investments Mortgage/ Rental History Reserves 1 Unit

PURCHASE/ LIMITED CASH OUT REFINANCES STANDARD and HIGH BALANCE LOAN AMOUNTS Occupancy Maximum* LTV Maximum* CLTV Min FICO* Max Ratios Minimum Cash Investments Mortgage/ Rental History Reserves 1 Unit

FHA Underwriting Guideline Changes Effective for Case Numbers Assigned On or After September 14, 2015 September 14, 2015

September 14, 2015 Assets Gift Funds Documenting Transfer Earnest Money Not clear about requiring donor s bank statement in all instances. Document source of funds if amount exceeds 2% of sales price or

September 14, 2015 Assets Gift Funds Documenting Transfer Earnest Money Not clear about requiring donor s bank statement in all instances. Document source of funds if amount exceeds 2% of sales price or

FIXED RATE (30 & 15)

") Page 1 of 19 FIXED RATE (30 & 15) PRIMARY RESIDENCE Purchase & Rate/Term Refinance PROPERTY TYPE LTVCLTV/HCLTV LOAN AMOUNT 1 FICO 2 MAX DTI UNDW OPTIONS 3 1 unit (SFR,Condos,PUDs) Cash/Out Refinance 4

Page 1 of 19 FIXED RATE (30 & 15) PRIMARY RESIDENCE Purchase & Rate/Term Refinance PROPERTY TYPE LTVCLTV/HCLTV LOAN AMOUNT 1 FICO 2 MAX DTI UNDW OPTIONS 3 1 unit (SFR,Condos,PUDs) Cash/Out Refinance 4

FHA Underwriting Guideline Changes Effective for Case Numbers Assigned On or After September 14, 2015

Topic Assets Interested Party Credits / Costs Paid Outside Closing / Minimum Required Investment (MRI) Current FHA Guideline New FHA Guideline Gift Funds Documenting Transfer Not clear about requiring

Topic Assets Interested Party Credits / Costs Paid Outside Closing / Minimum Required Investment (MRI) Current FHA Guideline New FHA Guideline Gift Funds Documenting Transfer Not clear about requiring

Understanding Credit Reports & Credit Scoring

Understanding Credit Reports & Credit Scoring April 2017 2012 Genworth Financial, Inc. All rights reserved. Overview & Course Objectives Credit Reports & Scoring Credit Reports & Scoring are designed to

Understanding Credit Reports & Credit Scoring April 2017 2012 Genworth Financial, Inc. All rights reserved. Overview & Course Objectives Credit Reports & Scoring Credit Reports & Scoring are designed to

Processing FHA TOTAL Mortgages

Introduction This reference contains information to help you process Federal Housing Administration (FHA) mortgages using Freddie Mac Loan Product Advisor SM, including information on data entry requirements,

Introduction This reference contains information to help you process Federal Housing Administration (FHA) mortgages using Freddie Mac Loan Product Advisor SM, including information on data entry requirements,

Conventional Conforming Fixed Matrix PURCHASE AND RATE TERM REFINANCE CASH-OUT REFINANCE. Program Matrix Notes

Conventional Conforming Fixed Program Summary Conventional Conforming Fixed Matrix PURCHASE AND RATE TERM REFINANCE Occupancy Units FICO DU LTV/CLTV/HCLTV¹ LP LTV/CLTV/HCLTV¹ Primary Residence Second Home

Conventional Conforming Fixed Program Summary Conventional Conforming Fixed Matrix PURCHASE AND RATE TERM REFINANCE Occupancy Units FICO DU LTV/CLTV/HCLTV¹ LP LTV/CLTV/HCLTV¹ Primary Residence Second Home

Listing of Various HUD Handbook Changes

Listing of Various HUD Handbook 4000.1 Changes Please note this list is not all-inclusive, all FHA loans with cases assigned on or after 9/14/15 must meet all new handbook requirements.. http://portal.hud.gov/hudportal/hud?src=/program_offices/administration/hudclips/handbooks/hsgh

Listing of Various HUD Handbook 4000.1 Changes Please note this list is not all-inclusive, all FHA loans with cases assigned on or after 9/14/15 must meet all new handbook requirements.. http://portal.hud.gov/hudportal/hud?src=/program_offices/administration/hudclips/handbooks/hsgh

ELIGIBILITY MATRIX & SUMMARY GUIDELINES 15 & 30 YR Fixed Rates

Revised 6/2/2014 Changes from prior versions are in red font Overlays to Fannie guidelines are underlined Correspondent Lending Jumbo "Premier" Fixed Rate and ARM Product Profile Based on a Fannie Mae

Revised 6/2/2014 Changes from prior versions are in red font Overlays to Fannie guidelines are underlined Correspondent Lending Jumbo "Premier" Fixed Rate and ARM Product Profile Based on a Fannie Mae

DU Refi Plus. Eligibility Matrix Loan Amount & LTV Limitations

This matrix is intended as an aid to assist in determining if a property/loan qualifies for the DU Refi Plus program. It is not intended as a replacement for the full DU Refi Plus guidelines. Users are

This matrix is intended as an aid to assist in determining if a property/loan qualifies for the DU Refi Plus program. It is not intended as a replacement for the full DU Refi Plus guidelines. Users are

Participating Lender Training

Participating Lender Training 1 CHFA S MISSION To provide housing opportunities for low and moderate - income people in Connecticut and to aid economic development. 2 www.chfa.org 3 CHFA AND BOND COMPLIANCE

Participating Lender Training 1 CHFA S MISSION To provide housing opportunities for low and moderate - income people in Connecticut and to aid economic development. 2 www.chfa.org 3 CHFA AND BOND COMPLIANCE

1-Unit properties, including condominiums and units in Planned Unit Developments o No Manufactured Homes

OVERVIEW HomeOne mortgage, a new conventional (non-fha) 3% down payment option for qualified first-time homebuyers. HomeOne mortgage broadly serves borrowers without geographic or income restrictions.

OVERVIEW HomeOne mortgage, a new conventional (non-fha) 3% down payment option for qualified first-time homebuyers. HomeOne mortgage broadly serves borrowers without geographic or income restrictions.

FHLMC PROGRAM LINEUP`

FHLMC PROGRAM LINEUP` Table of Contents Conventional Conforming (fixed & ARM)... 2 Super Conforming Fixed Rate... 5 Super Conforming ARM... 7 Home Possible... 11 Open Access... 16 HomeOne... 18 www.mcfunding.com

FHLMC PROGRAM LINEUP` Table of Contents Conventional Conforming (fixed & ARM)... 2 Super Conforming Fixed Rate... 5 Super Conforming ARM... 7 Home Possible... 11 Open Access... 16 HomeOne... 18 www.mcfunding.com

FREDDIE MAC PRODUCT PROFILE

This product may only be used when one of the following exists: A Non-occupying co-borrower is on the loan and blended ratios are being used. The occupying borrower must have the ability to at least make

This product may only be used when one of the following exists: A Non-occupying co-borrower is on the loan and blended ratios are being used. The occupying borrower must have the ability to at least make

PRIMARY RESIDENCE PURCHASE & RATE/TERM REFINANCE PRIMARY RESIDENCE CASH-OUT REFINANCE SECOND HOME PURCHASE AND RATE/TERM REFINANCE

PRIMARY RESIDENCE PURCHASE & RATE/TERM REFINANCE Property Type Max. Loan mount Max. LTV Max. CLTV/HCLTV Min. FICO 1-Unit, PUD $679,650 85% N/A 760 Warrantable Condo $679,650 80% 90% 680 PRIMARY RESIDENCE

PRIMARY RESIDENCE PURCHASE & RATE/TERM REFINANCE Property Type Max. Loan mount Max. LTV Max. CLTV/HCLTV Min. FICO 1-Unit, PUD $679,650 85% N/A 760 Warrantable Condo $679,650 80% 90% 680 PRIMARY RESIDENCE

Gold Jumbo 90 QM Program Eligibility Guide

Version 1.8 Effective 06.27.2018 Eligibility Matrix Table of Contents Eligibility Matrix... 3 Primary Residence Purchase, Rate and Term Refinance... 3 Underwriting Guidelines... 4 Eligible Products...

Version 1.8 Effective 06.27.2018 Eligibility Matrix Table of Contents Eligibility Matrix... 3 Primary Residence Purchase, Rate and Term Refinance... 3 Underwriting Guidelines... 4 Eligible Products...

Gold Jumbo 90 (QM) Program Guidelines

Program Guidelines") Gold Jumbo 90 (QM) Program Guidelines Version 2.0 Effective 1.2.19 Eligibility Matrix Table of Contents Eligibility Matrix...2 Primary Residence Purchase, Rate and Term Refinance... 2 Underwriting Guidelines...3

Gold Jumbo 90 (QM) Program Guidelines Version 2.0 Effective 1.2.19 Eligibility Matrix Table of Contents Eligibility Matrix...2 Primary Residence Purchase, Rate and Term Refinance... 2 Underwriting Guidelines...3

National MI TrueGuide SM : Underwriting Guidelines

1 Table of Contents 1.0. Introduction... 7 1.1 National MI TrueGuide SM Underwriting Philosophy... 7 1.2 Fair Lending... 8 1.3 Insured Originator Approval... 8 1.4 Delegation of Underwriting Authority...

1 Table of Contents 1.0. Introduction... 7 1.1 National MI TrueGuide SM Underwriting Philosophy... 7 1.2 Fair Lending... 8 1.3 Insured Originator Approval... 8 1.4 Delegation of Underwriting Authority...

Correspondent Lending Chase DU/LP Overlay Matrix

Agency Collateral Overlays 2070 & 2075 Appraisals CB12-18 The Fannie Mae Desktop Underwriter Property Inspection Report 2075 and Freddie Mac Loan Prospector Property Inspection Report 2070 do not contain

Agency Collateral Overlays 2070 & 2075 Appraisals CB12-18 The Fannie Mae Desktop Underwriter Property Inspection Report 2075 and Freddie Mac Loan Prospector Property Inspection Report 2070 do not contain

FAQs June 20, Product. Submission. Financed MI (Single Premium) SplitEdge. ExpressTrack SM. Refer with Caution, Caution

SplitEdge. ExpressTrack SM. Refer with Caution, Caution") s June 20, 2016 The answers contained within are specific to loan files reviewed for eligibility under Radian s standard published guidelines. A separate is available for loan files which qualify under

s June 20, 2016 The answers contained within are specific to loan files reviewed for eligibility under Radian s standard published guidelines. A separate is available for loan files which qualify under

DU Refi Plus. Table of Contents

Table of Contents 1. Eligible Existing Mortgage Loan Types... 2 2. Ineligible Existing Mortgage Loan Types... 2 3. Ineligible New Mortgage Loan Types... 2 4. Program Expiration... 2 5. Incentives for Borrowers...

Table of Contents 1. Eligible Existing Mortgage Loan Types... 2 2. Ineligible Existing Mortgage Loan Types... 2 3. Ineligible New Mortgage Loan Types... 2 4. Program Expiration... 2 5. Incentives for Borrowers...

Home Possible and Home Possible Advantage

Home Possible and Home Possible Advantage 1 Freddie Mac Home Possible and Home Possible Advantage mortgages (collectively referred to as Home Possible mortgages) are Freddie Mac s Affordable Mortgage products.

Home Possible and Home Possible Advantage 1 Freddie Mac Home Possible and Home Possible Advantage mortgages (collectively referred to as Home Possible mortgages) are Freddie Mac s Affordable Mortgage products.

USDA / GUS Basics for Success

USDA / GUS Basics for Success INDEX BENEFITS OF MSF USDA HOUSEHOLD ELIGIBILITY ASSETS AND LIABILITIES INTRODUCTION INCOME ELIGIBILITY TRANSACTION DETAILS OVERVIEW LOAN TERMS ADDITIONAL DATA GUS DECISION

USDA / GUS Basics for Success INDEX BENEFITS OF MSF USDA HOUSEHOLD ELIGIBILITY ASSETS AND LIABILITIES INTRODUCTION INCOME ELIGIBILITY TRANSACTION DETAILS OVERVIEW LOAN TERMS ADDITIONAL DATA GUS DECISION

Gold Jumbo Plus (Non-QM) Guidelines

Guidelines") (Non-QM) Guidelines Version 2.2 Effective 12.4.18 Table of Contents Eligibility Matrix...2 Primary Residence Purchase, Rate and Term Refinance... 2 Primary Residence Cash-Out Refinance... 2 Second Home

(Non-QM) Guidelines Version 2.2 Effective 12.4.18 Table of Contents Eligibility Matrix...2 Primary Residence Purchase, Rate and Term Refinance... 2 Primary Residence Cash-Out Refinance... 2 Second Home

AFR JUMBO OVERVIEW COPYRIGHT 2017 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED

12/20/2017 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do not reproduce, display, or distribute without

12/20/2017 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do not reproduce, display, or distribute without

Financing Residential Real Estate. Qualifying the Buyer

Financing Residential Real Estate Lesson 8: Qualifying the Buyer Introduction In this lesson we will cover: the underwriting process, qualifying the buyer, and factors taken into account when a buyer s

Financing Residential Real Estate Lesson 8: Qualifying the Buyer Introduction In this lesson we will cover: the underwriting process, qualifying the buyer, and factors taken into account when a buyer s

The Chase Guaranteed Rural Housing Purchase Program Features

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

VA FULLY AMORTIZING FIXED, HIGH BALANCE & JUMBO PROGRAM

VA FULLY AMORTIZING FIXED, HIGH BALANCE & JUMBO PROGRAM PROGRAM SPECIFICATIONS Description A mortgage loan program established by the United States Department of Veterans Affairs to help veterans and their

VA FULLY AMORTIZING FIXED, HIGH BALANCE & JUMBO PROGRAM PROGRAM SPECIFICATIONS Description A mortgage loan program established by the United States Department of Veterans Affairs to help veterans and their

UHM Production Bulletin

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: HUD 92900-A As announced in Mortgagee Letter 2016-06, the updated 92900-A (HUD/VA

TOPICS IMPACTED IN THIS BULLETIN FNMA and FHLMC Products FHA/VA Mortgage Insurance USDA Other Underwriting Guidelines FHA: HUD 92900-A As announced in Mortgagee Letter 2016-06, the updated 92900-A (HUD/VA

Fannie & High BalanceGuidelines

Fannie & High BalanceGuidelines Agency Finance Type Occupancy Term High balance and transactions with non-occupant coborrowers are limited to 95% LTV/CLTV. High Balance Cash Out Transactions are limited

Fannie & High BalanceGuidelines Agency Finance Type Occupancy Term High balance and transactions with non-occupant coborrowers are limited to 95% LTV/CLTV. High Balance Cash Out Transactions are limited

Underwriting Guideline Manual

Underwriting Guideline Manual VERSION 3.5 DECEMBER 14, 2015 Mortgage insurance provided by Essent Guaranty, Inc. Two Radnor Corporate Center, 100 Matsonford Road, Radnor, PA 19087 essent.us EGI-6801.015

Underwriting Guideline Manual VERSION 3.5 DECEMBER 14, 2015 Mortgage insurance provided by Essent Guaranty, Inc. Two Radnor Corporate Center, 100 Matsonford Road, Radnor, PA 19087 essent.us EGI-6801.015

CONFORMING FIXED FNMA HOMESTYLE RENOVATION GUIDELINES

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

PRODUCT DESCRIPTION 15 and 30 year Fixed Rate PRODUCT CODE CF15-HS (15 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HS (30 year Fixed Rate Conforming HomeStyle Renovation Loan ) CF30-HSHP

Loan Product Advisor Documentation Matrix

Use the following information as a reference for documenting your Loan Product Advisor loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie

Use the following information as a reference for documenting your Loan Product Advisor loans. For complete documentation information and specific program eligibility requirements, refer to the Freddie

PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE. Reserves

Click Here For PDF Version Full/Alternative Documentation 1-2 Unit 1 Unit 3-4 Unit PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE Maximum Qualifying Ratios Required MI Minimum LTV CLTV Loan Amount

Click Here For PDF Version Full/Alternative Documentation 1-2 Unit 1 Unit 3-4 Unit PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE Maximum Qualifying Ratios Required MI Minimum LTV CLTV Loan Amount

Fannie Mae High Balance Matrix

Revision: July 16, 2016 (Product Information Center, 949-390-2684, www.jmaclending.com Finance Type Purchas and Rate/Term Refinances Cash Out Refinances Occupancy Owner Occupied Owner Occupied Term Property

Revision: July 16, 2016 (Product Information Center, 949-390-2684, www.jmaclending.com Finance Type Purchas and Rate/Term Refinances Cash Out Refinances Occupancy Owner Occupied Owner Occupied Term Property

PennyMac Correspondent Group Freddie Mac Home Possible Overlays to Freddie Mac are underlined

PennyMac Correspondent Group Freddie Mac Home Possible 01.18.18 Overlays to Freddie Mac are underlined Home Possible Freddie Mac - LPA Accept Owner-Occupied Only, Purchase and Rate & Term Refinance, Fixed

PennyMac Correspondent Group Freddie Mac Home Possible 01.18.18 Overlays to Freddie Mac are underlined Home Possible Freddie Mac - LPA Accept Owner-Occupied Only, Purchase and Rate & Term Refinance, Fixed

Section DU Refi Plus Loan Program

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Product Summary... 2 Features and Benefits... 4 Related Bulletins...

Section 2.04 - DU Refi Plus Loan Program In This Product Description This product description contains the following topics: Overview... 2 Product Summary... 2 Features and Benefits... 4 Related Bulletins...

CHFA-Approved Lenders Mortgage Program Training. Rev 5/10/18

CHFA-Approved Lenders Mortgage Program Training Rev 5/10/18 Our Mission To alleviate the shortage of housing for low-to-moderate income families and persons in this State and, when appropriate, to promote

CHFA-Approved Lenders Mortgage Program Training Rev 5/10/18 Our Mission To alleviate the shortage of housing for low-to-moderate income families and persons in this State and, when appropriate, to promote

Working with MGIC. Simple, Fair, Transparent

Working with MGIC Simple, Fair, Transparent The information presented in this presentation is for general information only, and is based on guidelines and practices generally accepted within the mortgage

Working with MGIC Simple, Fair, Transparent The information presented in this presentation is for general information only, and is based on guidelines and practices generally accepted within the mortgage

Diamond Jumbo QM and Jumbo 90 QM Program Eligibility Guide

Diamond Jumbo QM and Jumbo 90 QM Effective 01.28.2019 Table of Contents Diamond Jumbo QM and Jumbo 90 Table of Contents Diamond Jumbo QM and Jumbo 90 Eligibility Matrix...3 Primary Residence Purchase,

Diamond Jumbo QM and Jumbo 90 QM Effective 01.28.2019 Table of Contents Diamond Jumbo QM and Jumbo 90 Table of Contents Diamond Jumbo QM and Jumbo 90 Eligibility Matrix...3 Primary Residence Purchase,

Program Qualifications

This matrix is intended as an aid to assist in determining if a property/loan qualifies for certain USDA offered programs. It is not intended as a replacement for USDA guidelines. Users are expected to

This matrix is intended as an aid to assist in determining if a property/loan qualifies for certain USDA offered programs. It is not intended as a replacement for USDA guidelines. Users are expected to

FHA Advantage Underwriting Guide

FHA Advantage Underwriting Guide Page left blank intentionally. WHEDA Introduction 1 Last Revised Date: October 20, 2017 Table of Contents 1.00 Introduction... 6 2.00 Underwriting Philosophy... 7 3.00

FHA Advantage Underwriting Guide Page left blank intentionally. WHEDA Introduction 1 Last Revised Date: October 20, 2017 Table of Contents 1.00 Introduction... 6 2.00 Underwriting Philosophy... 7 3.00

APPENDIX Q SUMMARY Employment Related Income 3 Stability of Income 3 Effective Income 3 Verifying Employment History 3 Analyzing a Consumer's

APPENDIX Q SUMMARY Employment Related Income 3 Stability of Income 3 Effective Income 3 Verifying Employment History 3 Analyzing a Consumer's Employment Record 3 Extended Absence 3 Salary, Wage and Other

APPENDIX Q SUMMARY Employment Related Income 3 Stability of Income 3 Effective Income 3 Verifying Employment History 3 Analyzing a Consumer's Employment Record 3 Extended Absence 3 Salary, Wage and Other

Full/Alternative Documentation PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE Property Type Max. LTV Max. CLTV

Click here for PDF version Full/Alternative Documentation PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE Maximum Loan Credit Score 3 Program 1- to 2-unit 95% 1 n/a $300,000 28/36 2 months 660 Standard

Click here for PDF version Full/Alternative Documentation PRIMARY RESIDENCE - PURCHASE & RATE/TERM REFINANCE Maximum Loan Credit Score 3 Program 1- to 2-unit 95% 1 n/a $300,000 28/36 2 months 660 Standard

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile Overlays to Fannie Mae are underlined

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile 06.15.18 Overlays to Fannie Mae are underlined Fannie Mae - DU Approval Owner-Occupied Only, Purchase and Rate & Term Refinance, Fixed

PennyMac Correspondent Group Fannie Mae HomeReady Product Profile 06.15.18 Overlays to Fannie Mae are underlined Fannie Mae - DU Approval Owner-Occupied Only, Purchase and Rate & Term Refinance, Fixed