BUS210. Accounting for Financing Decisions: Long-Term Liabilities

|

|

|

- Mark Rafe Jenkins

- 5 years ago

- Views:

Transcription

1 BUS210 Accounting for Financing Decisions: Long-Term Liabilities

2 Liabilities Current or Short-term Liabilities Long-term Debt (borrowed funds) Lease Liabilities Deferred Taxes Contingencies and Commitments Accounting for liabilities is a subject that can be very technical. There is a tendency for some institutions to create exotic instruments for marketing of funds in recent years. Despite this, there are some basic principles that govern the accounting for liabilities.

3

4 Basis for Valuing Liabilities Because money has time value, the amount of money needed today to pay a future debt is less than the future obligation. Historically, the best basis for valuing a liability was its economic present value (the present value of the future cash flows, i.e., the amount of money that would have to be set aside today to accumulate to the future cash flows required to pay the interest and the principal of the debt). Most current liabilities are reported on the BS at their face (or nominal value) the amount that will be paid. Most Long-term liabilities are reported on the BS at their present value (the time-discounted value of the future cash flows).

5 Basic Definitions and Different Contractual Forms Some contracts, called interest-bearing obligations, require periodic (annual or semiannual) cash payments (called interest) that are determined as a percentage of the face, principal, or maturity value, which must be paid at the end of the contract period. Non-interest-bearing obligations, on the other hand, require no periodic payments, but only a single cash payment at the end of the contract period. These contractual forms may contain additional terms that specify assets pledged as security or collateral in case the required cash payments are not met (default), as well as additional provisions (restrictive covenants).

6 Short-term Liabilities Report at Face value: Accounts payable, Accrued expenses, Unearned revenue, Taxes payable, Warranties payable Non-interest bearing ST Notes Payable generally are reported at maturity value less any unamortized interest discount. i.e., BS shows either: Note payable $950 or Note payable $1,000 less Unamortized discount $50. Interest-bearing ST Notes Payable generally are reported at the maturity (face) value plus any accrued interest. i.e., Note Payable $1,000 and Interest payable $50 on BS. Short-term debt which company has no intentions of liquidating, but plans to continually refinance, should be classified as long-term. Also, the current portion (the amount that will be paid within one year) of any longterm debt should be classified on the BS as a current liability.

7 Long-term Debts Since interest accounts for the difference between the amount received and the amount paid back, the interest rate is the basis for computing interest. On all long-term debt contracts there are two interest rates: The stated rate and the effective rate, they may not be the same The stated rate is the interest rate on interest-bearing debt that is used to calculate the amount of cash interest payments that will be made to the lender. The effective rate is the compounded interest rate that mathematically accounts for the total difference between the amount borrowed and the amount repaid.

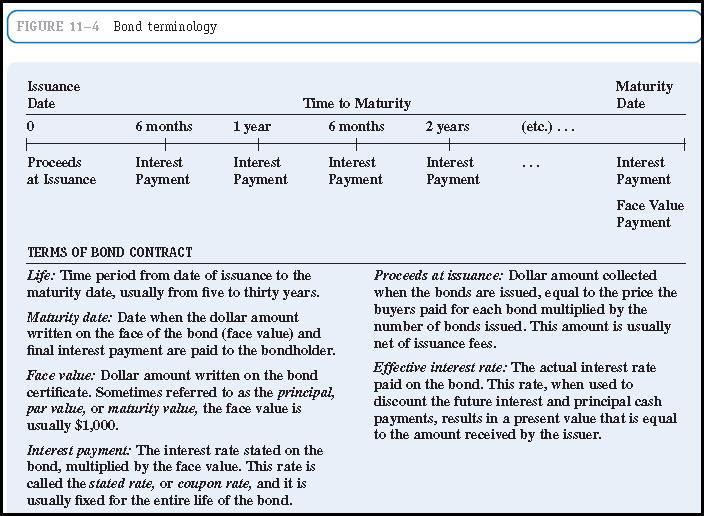

8 Bond Terminology

? -Interest bearing or Noninterest bearing? What is the interest payment? How often?")

9 Key Questions: -Present Value? Issue value or Proceeds -Future Value? Maturity value or Face value -n= number of periods? -r=effective or market interest rate? -Bond or Note stated rate or face rate? -Single payment or Ordinary annuity (multiple payments)? -Interest bearing or Noninterest bearing? What is the interest payment? How often? Draw a Timeline and fill in: -Issue date -When pay interest and amortize discount or premium -Maturity date

10 BE11-2 Bond Terms In October 1997 HP issued zero-coupon bonds with a face of 1.8 billion, due in 2017, for proceeds of $968 million. a. What is the life of these bonds? b. What is the stated rate on these bonds? c. Estimate the effective interest rate of these bonds. (hint: $PV/$FV = approximate Table value) d. How many bonds did HP issue? e. What entry did HP make when the bonds were issued?

11 E11-8 Present Value of a Non-interest-bearing Note Purchased a building in exchange for a 3 year non-interest-bearing note with a face of $693,000. Building appraisal is $550,125. a. What amount should this building be capitalized?

12 E11-8 Present Value of a Non-interest-bearing Note Purchased a building in exchange for a 3 year non-interestbearing note with a face of $693,000. Building appraisal is $550,125. b. Compute the present value of the note s future cash flows, using the following discount rates: 1. 6 percent 2. 8 percent percent c. What is the effective rate of this note?

13 E11-5 Discounted Non-interest-bearing Notes Purchase equipment with a FMV of $11,348 in exchange for a 5 year non-interest-bearing note with a face of $20,000. d. Explain how one could more quickly compute the effective interest rate on the note. e. Compute the effective interest rate on the note payable. f. Prepare entry to record the purchase.

14 E11-5 Discounted Non-interest-bearing Notes Purchase equipment with a FMV of $11,348 in exchange for a 5 year non-interest-bearing note with a face of $20,000. g. How much interest expense should be recognized in the first year? h. What is the BS value of the note at the end of the first year? i. Will the interest expense recognized in the second year be greater, equal, or less than the interest expense recognized in the first year? Why?

15 E11-4 Non-interest-bearing Note Payable Proceeds Compute the proceeds from the following notes payable. Interest payments are made annually. PV Principal PV Interest Payments = Proceeds Stated Rate Effective Rate Face Value Life 0% 8% $1,000 4 years 0% 6% $5,000 6 years

16

17 Recap: Non-Interest Bearing Notes and Bonds >Issue date >Amortize discount >Maturity date

18 Accounting for Non-Interest Bearing Notes Payable Recap

19 Sample Non-interest bearing Long-term Notes Payable Problem 1: On January 2, 2008, Pearson Company purchases a section of land for its new plant site. Pearson issues a 5 year noninterest bearing note, and promises to pay $50,000 at the end of the 5 year period. What is the cash equivalent price of the land, if a 6 percent discount rate is assumed? PV1 = 50,000 x ( ) = $37,363 [ i=6%, n=5] Journal entry Jan. 2, 2008: Dr. Land 37,363 Dr. Discount on N/P 12,637 Cr. Notes Payable 50,000

20 Sample Problem 1 Solution, continued The Effective Interest Method: Interest Expense = Carrying value x Effective interest rate x Time period (CV) (Per year) (Portion of year) Where carrying value = face - discount. For Example 1, CV= 50,000-12,637 = 37,363 Interest expense = 37,363 x 6% per year x 1year = $2,242

21 Sample Problem 1 Solution, continued Journal entry, December 31, 2008: Interest expense 2,242 Discount on N/P 2,242 Carrying value on B/S at 12/31/2008: Notes Payable $50,000 Discount on N/P (10,395) $39,605 (Discount = $12,637-2,242 = $10,395)

22 Sample Problem 1 Solution, continued Interest expense at Dec. 31, 2009: 39,605 x 6% x 1 = $2,376 Journal entry, December 31, 2009: Interest expense 2,376 Discount on N/P 2,376 Carrying value on B/S at 12/31/2009: Notes Payable $50,000 Discount on N/P (8,019) $41,981 (Discount = 10,395-2,376) Carrying value on 12/31/2012 (before retirement)? $50,000

23 Time Value of Money and Interest bearing Long- Term Liabilities: Notes, Bonds, and Leases Long-term liabilities are recorded at the present value of the future cash flows. Two components determine the time value of money: interest (discount) rate number of periods of discounting Types of activities that require PV calculations: notes payable bonds payable and bond investments capital leases

24 Interest bearing: Bond Prices

25 E 11-3 Bond Terms The stated and effective interest rates for several notes and bonds follow: Is Note or Bond issued a Par, Premium, or Discount? Bond Stated Interest Rate Effective or Market Interest Rate 1. 10% 10% 2. 7% 8% 3. 9% 8% % 9%

26

27 E11-4 Interest-bearing and Non-interest-bearing Note Payable Proceeds Compute the proceeds from the following notes payable. Interest payments are made annually. PV Principal PV Interest Payments = Proceeds Stated Rate Effective Rate Face Value Life 4% 12% $8,000 6 years 8% 8% $3,000 7 years 10% 6% $10, years

28

29 Bonds Payable Issued at a Discount If bonds are issued at a discount, the carrying value will be below face value at the date of issue. The Discount on B/P account has a normal debit balance and is a contra to B/P (similar to the Discount on N/P). The Discount account is amortized with a credit. Note that the difference between Cash Paid and Interest Expense is still the amount of amortization. Interest expense for bonds issued at a discount will be greater than cash paid. The amortization table will show the bonds amortized up to face value.

30 E11-13 Bonds issued at a Discount Issued 500 five-year bonds on Interest payments are due semiannually at 1.1 and 7.1 at an interest rate of 6%. The effective rate is 8%. The face value of each bond is $1,000. a entry when bonds are issued? b entry at yearend?

31 E11-13 Bonds issued at a Discount Issued 500 five-year bonds on Interest payments are due semiannually at 1.1 and 7.1 at an interest rate of 6%. The effective rate is 8%. The face value of each bond is $1,000. c Balance sheet value? d. PV of bonds remaining cash flows as of ?

32 Your Turn

33 E11-14 Bonds issued at a Premium Issued 100 ten-year bonds on Interest payments are due semiannually (1.1 and 7.1) at an annual rate of 8%. The effective rate is 6%. The face of each bond is $1,000. a entry to issue bonds? b entry?

34 E11-14 Bonds issued at a Premium Issued 100 ten-year bonds on Interest payments are due semiannually (1.1 and 7.1) at an annual rate of 8%. The effective rate is 6%. The face of each bond is $1,000. c balance sheet value? d. PV of remaining cash flows as of ?

35 Your Turn

36 Sample Problem 2: Bonds Payable issued at Premium, semiannual interest payments On July 1, 2007, Mustang Corporation issues $100,000 of its 5-year bonds which have an annual stated rate of 7%, and pay interest semiannually each June 30 and December 31, starting December 31, The bonds were issued to yield 6% annually. Calculate the issue price of the bond: (1) What are the cash flows and factors? Face value at maturity = $100,000 Stated Interest = Face value x stated rate x time period 100,000 x 7% x (1/2) = $3,500 Number of periods = n = 5 years x 2 = 10 Discount rate = 6% / 2 = 3% per period

37 Sample Problem 2 - calculations PV of interest annuity: PVOA Table PVOA = 3,500 ( ) = $29,856 i = 3%, n = 10 PV of face value: PV1 Table PV = 100,000 ( )=$74,409 i=3%, n=10 Total issue price = $104,265 Issued at a premium of $4,265 because the company was offering an interest rate greater than the market rate, and investors were willing to pay more for the higher interest rate.

38 Sample Problem 2 - Amortization Schedule To recognize interest expense using the effective interest method, an amortization schedule must be constructed. (This expands the text discussion.) To calculate the columns (see next slide): Cash interest paid = Face x Stated Rate x Time = 100,000 x 7% x 1/2 year = $3,500 (this is the same amount every period) Int. Expense = CV x Market Rate x Time at 12/31/07 = 104,265 x 6% x 1/2 year = 3,128 at 6/30/08 = 103,893 x 6% x 1/2 year = 3,117 The difference between cash paid and interest expense is the periodic amortization of premium. Note that the carrying value is amortized down to face value by maturity.

39 Sample Problem 2 - Amortization Schedule Cash Interest Carrying Date Paid Expense Premium Value 7/01/07 104,265 12/31/07 3,500 3, ,893 6/30/08 3,500 3, ,510 12/31/08 3,500 3, ,115 6/30/09 3,500 3, ,708 12/31/09 3,500 3, ,289 6/30/10 3,500 3, ,858 12/31/10 3,500 3, ,414 6/30/11 3,500 3, ,956 12/31/11 3,500 3, ,485 6/30/12 3,500 3, ,000

40 Sample Problem 2 - Journal Entries JE at 7/1/07 to issue the bonds: Cash 104,265 Premium on B/P 4,265 Bonds Payable 100,000 JE at 12/31/07 to pay interest: Interest Expense 3,128 Premium on B/P 372 Cash 3,500 Note that the numbers for each interest payment come from the lines on the amortization schedule.

41 Sample Bonds Issued at Face Value

42 Sample Bonds Issued at a Discount

43 Sample Bond Amortization Table

44 Recap: Interest Bearing Notes and Bonds >Issue date >Pay interest and amortize discount or premium >Maturity date

45 Investor s Bond Yield= annual cash received/note price The yield on a 10 year note, which was hovering at about 2.2% before the release of the non-farm report [on Friday] plummeted to about 2.07% in a matter of minutes. Yields, which move in the opposite direction to prices, continued to move lower, ending the day at 2.056%, compared with 2.173% late Thursday. Page B2, The Wall Street Journal,

46 Bond Redemptions When bonds are redeemed at the maturity date, the issuing company simply pays cash to the bondholders in the amount of the face value and removes the bond payable from the balance sheet. To illustrate the redemption of a bond issuance prior to maturity at a loss, assume that bonds with a $100,000 face value and a $5,000 unamortized discount are redeemed for $102,000. The $7,000 loss on redemption would decrease net income

47 P11-10 Callable Bond Redemptions account balances are: Bond payable $500,000 Premium on bond payable $ 12,600 The bonds have an annual stated rate of 8% and an effective rate of 6%. Interest is paid 6.30 and a. Compute the gain or loss if the bonds are called for 104 on ?

48 P11-10 Callable Bond Redemptions account balances are: Bond payable $500,000 Premium on bond payable $ 12,600 The bonds have an annual stated rate of 8% and an effective rate of 6%. Interest is paid 6.30 and b. Compute the gain or loss if the bonds are called for 108 on ? c. Compute the gain or loss if the bonds are called for 110 on ?

49 Bond Conversions The Jolly Corporation has $400,000 of 6 percent bonds outstanding. There is $20,000 of unamortized discount remaining on these bonds after the July 1, 2011, semiannual interest payment. The bonds are convertible at the rate of 20 shares of $5 par value common stock for each $1,000 bond. On July 1, 2011, bondholders presented $300,000 of the bonds for conversion. 1. Is there a gain or loss on conversion, and if so, how much is it? 2. How many shares of common stock are issued in exchange for the bonds? 3. In dollar amounts, how does this transaction affect the total liabilities and the total stockholders' equity of the company? In your answer, show the effects on four accounts.

50 International Perspective The accounting disclosure requirements in non-u.s. countries and IFRS are not as comprehensive as those in the United States, partially because the information needs of the major capital providers (i.e., banks) are satisfied in a relatively straightforward way through personal contact and direct visits. A second way in which the heavy reliance on debt affects non- U.S. accounting systems is that the required disclosures and regulations tend to be designed either to protect the creditor or to help in the assessment of solvency.

51 Economic Consequences of Reporting Long-Term Liabilities Improved credit ratings can lead to lower borrowing costs Management has strong incentive to manage the balance sheet by using off-balance-sheet financing i.e., operating leases

52 Leases: operating or capital FASB issued SFAS No. 13, which requires certain leases to be recorded as capital leases. Capital leases record the leased asset as a capital asset, and reflect the present value of the related payment contract as a liability. Requirements of SFAS No record as capital lease for the lessee if any one of the following is present in the lease: Title transfers at the end of the lease period, The lease contains a bargain purchase option, The lease life is at least 75% of the useful life of the asset, or The lessee pays for at least 90% of the fair market value of the lease.

53 Capital Lease

54 P11-14 Capital and Operating Leases Company leased equipment on for an annual lease payment of $30,000. Assume the lease term is 5 years and the life of the equipment is also 5 years. If the lease is treated as a capital lease, the FMV of the equipment is $119,781. The straight line depreciation method is used to depreciate fixed assets. The effective interest rate on the lease is 8%. a. Compute rent expense for if lease is treated as an operating lease. b. Compute the amounts that would complete the table: Date BS Value Leasehold Obligation Interest Expense Depreciation Expense Total Expense c. Compare total expense over 5 years for the two methods and comment.

55

BUS512M Session 9. Accounting for Financing Decisions: Long-Term Liabilities and Stockholders Equity

BUS512M Session 9 Accounting for Financing Decisions: Long-Term Liabilities and Stockholders Equity Liabilities Current or Short-term Liabilities Long-term Debt (borrowed funds) Lease Liabilities Deferred

BUS512M Session 9 Accounting for Financing Decisions: Long-Term Liabilities and Stockholders Equity Liabilities Current or Short-term Liabilities Long-term Debt (borrowed funds) Lease Liabilities Deferred

Chapter 11. Notes, Bonds, and Leases

1 Chapter 11 Long- Term Liabilities Notes, Bonds, and Leases 2 Long- Term Liabilities Many companies finance their operations and growth opportunities through the use of long term debt instruments: Notes

1 Chapter 11 Long- Term Liabilities Notes, Bonds, and Leases 2 Long- Term Liabilities Many companies finance their operations and growth opportunities through the use of long term debt instruments: Notes

Before Class starts.(make sure your name is on all submissions)

") Before Class starts.(make sure your name is on all submissions) Last Homework due Thursday 4/17 before class. Final Exam is Saturday May 3 9:00-Noon; Conflicts? Contact me ASAP! What questions do you have

Before Class starts.(make sure your name is on all submissions) Last Homework due Thursday 4/17 before class. Final Exam is Saturday May 3 9:00-Noon; Conflicts? Contact me ASAP! What questions do you have

ACCOUNTING FOR BONDS

ACCOUNTING FOR BONDS Key Terms and Concepts to Know Bonds are a medium to long-term financing alternative to issuing stock. Bonds are issued or sold face amount or par, at a discount if they pay less than

ACCOUNTING FOR BONDS Key Terms and Concepts to Know Bonds are a medium to long-term financing alternative to issuing stock. Bonds are issued or sold face amount or par, at a discount if they pay less than

ACCT 101 Bonds LECTURE NOTES CH. 10 Prof. Johnson

ACCT 101 Bonds LECTURE NOTES CH. 10 Prof. Johnson BASICS OF BONDS How corporations are financed Corporations raise cash from outside parties by: 1. Equity Financing. This involves issuing common or preferred

ACCT 101 Bonds LECTURE NOTES CH. 10 Prof. Johnson BASICS OF BONDS How corporations are financed Corporations raise cash from outside parties by: 1. Equity Financing. This involves issuing common or preferred

Chapter 10 - REPORTING AND ANALYZING LIABILITIES

Revised Summer 2018 Chapter 10 Review 1 Chapter 10 - REPORTING AND ANALYZING LIABILITIES LO 1: Explain how to account for current liabilities. Current Liability: a debt that a company expects to pay 1.

Revised Summer 2018 Chapter 10 Review 1 Chapter 10 - REPORTING AND ANALYZING LIABILITIES LO 1: Explain how to account for current liabilities. Current Liability: a debt that a company expects to pay 1.

Reporting and Interpreting Bonds

Reporting and Interpreting Bonds CHAPTER 10 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Not Barry and not James Slide 2 Understanding the Business The mixture of debt and equity used to finance

Reporting and Interpreting Bonds CHAPTER 10 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Not Barry and not James Slide 2 Understanding the Business The mixture of debt and equity used to finance

Bonds and Long-term Notes

Section 11 Bonds & PV Tables (Noncurrent Liabilities) 14-1 Bonds and Long-term Notes The Nature of Long-Term Debt Liabilities signify creditors interest in a company s assets. note payable and note receivable:

Section 11 Bonds & PV Tables (Noncurrent Liabilities) 14-1 Bonds and Long-term Notes The Nature of Long-Term Debt Liabilities signify creditors interest in a company s assets. note payable and note receivable:

ACCOUNTING - CLUTCH CH LONG TERM LIABILITIES.

!! www.clutchprep.com CONCEPT: INTRODUCTION TO BONDS AND BOND CHARACTERISTICS Bonds Payable are groups of debt securities issued to lenders Example: Company wants to raise $1,000,000. The company can sell

!! www.clutchprep.com CONCEPT: INTRODUCTION TO BONDS AND BOND CHARACTERISTICS Bonds Payable are groups of debt securities issued to lenders Example: Company wants to raise $1,000,000. The company can sell

4/10/2012. Liabilities and Interest. Learning Objectives (LO) LO 1 Current Liabilities. LO 1 Current Liabilities. LO 1 Current Liabilities

LO 1 Current Liabilities. LO 1 Current Liabilities. LO 1 Current Liabilities") Learning Objectives (LO) Liabilities and Interest CHAPTER 9 After studying this chapter, you should be able to 1. Account for current liabilities 2. Measure and account for long-term liabilities 3. Account

Learning Objectives (LO) Liabilities and Interest CHAPTER 9 After studying this chapter, you should be able to 1. Account for current liabilities 2. Measure and account for long-term liabilities 3. Account

Click to edit Master title style

1 Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 1 2 15 Bonds Payable and Investments

1 Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 1 2 15 Bonds Payable and Investments

Liabilities. Chapter 10. Learning Objectives. After studying this chapter, you should be able to:

10-1 Chapter 10 Liabilities 10-2 Learning Objectives After studying this chapter, you should be able to: 1. Explain a current liability, and identify the major types of current liabilities. 2. Describe

10-1 Chapter 10 Liabilities 10-2 Learning Objectives After studying this chapter, you should be able to: 1. Explain a current liability, and identify the major types of current liabilities. 2. Describe

1. Classification of Debt and Measurement Issues

Chapter 12 Debt Financing 1. Classification and measurement issues associated with debt 2. Accounting for short-term debt 3. Accounting for long-term debt (mortgages) 4. Understand the various types of

Chapter 12 Debt Financing 1. Classification and measurement issues associated with debt 2. Accounting for short-term debt 3. Accounting for long-term debt (mortgages) 4. Understand the various types of

PREVIEW OF CHAPTER 14-2

14-1 PREVIEW OF CHAPTER 14 14-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 14 Non-Current Liabilities LEARNING OBJECTIVES After studying this chapter, you should be able to:

14-1 PREVIEW OF CHAPTER 14 14-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 14 Non-Current Liabilities LEARNING OBJECTIVES After studying this chapter, you should be able to:

Long-Term Liabilities C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

Long-Term Liabilities E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to the

Long-Term Liabilities E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition to the

Chapter 15 Long-Term Liabilities

Chapter 15 Long-Term Liabilities CHAPTER OVERVIEW In Chapters 13 and 14 you learned about topics related to shareholders equity. Contributed capital is a major source of funds for corporations. However,

Chapter 15 Long-Term Liabilities CHAPTER OVERVIEW In Chapters 13 and 14 you learned about topics related to shareholders equity. Contributed capital is a major source of funds for corporations. However,

FAR. Financial Accounting & Reporting. Roger Philipp, CPA

FAR Financial Accounting & Reporting Roger Philipp, CPA FAR Financial Accounting and Reporting Written By: Roger Philipp, CPA Roger CPA Review 1288 Columbus Ave #278 San Francisco, CA 94133 www.rogercpareview.com

FAR Financial Accounting & Reporting Roger Philipp, CPA FAR Financial Accounting and Reporting Written By: Roger Philipp, CPA Roger CPA Review 1288 Columbus Ave #278 San Francisco, CA 94133 www.rogercpareview.com

NON-CURRENT (LONG-TERM) LIABILITIES

LIABILITIES") NON-CURRENT (LONG-TERM) LIABILITIES 1 MRI = Market Rate of Interest CR = Coupon Rate IE = Interest Expense FV = Fair Value PV = Present Value A&L = Assets & Liabilities CV = Carrying Value BS = Balance

NON-CURRENT (LONG-TERM) LIABILITIES 1 MRI = Market Rate of Interest CR = Coupon Rate IE = Interest Expense FV = Fair Value PV = Present Value A&L = Assets & Liabilities CV = Carrying Value BS = Balance

Long-Term Liabilities and Investments

Ch 21 Long-Term Liabilities and Investments Understanding bonds Accounting for issuance of bond Retirement of a bond Bond sinking funds Accounting for investments in stocks and bonds Presentation of bonds

Ch 21 Long-Term Liabilities and Investments Understanding bonds Accounting for issuance of bond Retirement of a bond Bond sinking funds Accounting for investments in stocks and bonds Presentation of bonds

Chapter Ten, Debt Financing: Bonds of Introduction to Financial Accounting online text, by Henry Dauderis and David Annand is available under

Chapter Ten, Debt Financing: Bonds of Introduction to Financial Accounting online text, by Henry Dauderis and David Annand is available under Creative Commons Attribution-NonCommercial- ShareAlike 4.0

Chapter Ten, Debt Financing: Bonds of Introduction to Financial Accounting online text, by Henry Dauderis and David Annand is available under Creative Commons Attribution-NonCommercial- ShareAlike 4.0

Accounting for Long. Different Ways to Finance a Company. u Borrowing from a Bank (Ch 9): Notes Payable More expensive and restrictive than bonds.

: Notes Payable More expensive and restrictive than bonds.") Accounting for Long Term Liabilities Ch 10 Acc 1a Different Ways to Finance a Company u Borrowing from a Bank (Ch 9): Notes Payable More expensive and restrictive than bonds. u Selling Stock (Ch 11): Gives

Accounting for Long Term Liabilities Ch 10 Acc 1a Different Ways to Finance a Company u Borrowing from a Bank (Ch 9): Notes Payable More expensive and restrictive than bonds. u Selling Stock (Ch 11): Gives

> DO IT! Chapter 15 Long-Term Liabilities. Bond Terminology. Bond Issuance D-69. Solution. Solution

Chapter 15 Long-Term Liabilities Bond Terminology Review the types of bonds and the basic terms associated with bonds. State whether each of the following statements is true or false. 1. Mortgage bonds

Chapter 15 Long-Term Liabilities Bond Terminology Review the types of bonds and the basic terms associated with bonds. State whether each of the following statements is true or false. 1. Mortgage bonds

LONG-TERM LIABILITIES

Chapter 14 LONG-TERM LIABILITIES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin Copyright

Chapter 14 LONG-TERM LIABILITIES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA McGraw-Hill/Irwin Copyright

Exercises. The bond is being issued at a premium, and the selling price would be higher than the face amount.

Chapter 11 Liabilities: Bonds Payable Study Guide Solutions Fill-in-the-Blank Equations 1. A discount 2. The face amount 3. A premium 4. Interest expense Exercises 1. Roses Corporation issued a bond with

Chapter 11 Liabilities: Bonds Payable Study Guide Solutions Fill-in-the-Blank Equations 1. A discount 2. The face amount 3. A premium 4. Interest expense Exercises 1. Roses Corporation issued a bond with

Accounting for Long-Term Debt

Accounting for Long-Term Debt 15.511 Corporate Accounting Summer 2004 Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology July 2, 2004 1 Agenda Long-Term Debt Extend

Accounting for Long-Term Debt 15.511 Corporate Accounting Summer 2004 Professor S. P. Kothari Sloan School of Management Massachusetts Institute of Technology July 2, 2004 1 Agenda Long-Term Debt Extend

Adjustments, Financial Statements and the Quality of Earnings

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

Before Class starts.(make sure your name is on all submissions)

") Before Class starts.(make sure your name is on all submissions) Last Homework due TODAY before class. LAST class review Final Exam is Saturday December 13 9:00-Noon; Conflicts? Contact me ASAP! What questions

Before Class starts.(make sure your name is on all submissions) Last Homework due TODAY before class. LAST class review Final Exam is Saturday December 13 9:00-Noon; Conflicts? Contact me ASAP! What questions

Prof Albrecht s Notes Accounting for Bonds Intermediate Accounting 2

Prof Albrecht s Notes Accounting for Bonds Intermediate Accounting 2 Companies need capital to fund the acquisition of various resources for use in business operations. They get this capital from owners

Prof Albrecht s Notes Accounting for Bonds Intermediate Accounting 2 Companies need capital to fund the acquisition of various resources for use in business operations. They get this capital from owners

Exam 1 Acct 414 Corporate Accounting & Reporting II Spring 2011

Exam # Name: Exam 1 Acct 414 Corporate Accounting & Reporting II Spring 2011 Show any necessary computations if you want to be eligible for partial credit. Present your work in a neat, well-organized manner.

Exam # Name: Exam 1 Acct 414 Corporate Accounting & Reporting II Spring 2011 Show any necessary computations if you want to be eligible for partial credit. Present your work in a neat, well-organized manner.

Chapter 11: Liabilities, on and off balance sheet. General issues Long-term debt, contingent liabilities

Chapter 11: Liabilities, on and off balance sheet General issues Long-term debt, contingent liabilities 1 Liabilities, definition and classification present obligations based on past transactions or events

Chapter 11: Liabilities, on and off balance sheet General issues Long-term debt, contingent liabilities 1 Liabilities, definition and classification present obligations based on past transactions or events

Exercise Maturity Interest paid Stated rate Effective (market) rate 10 years annually 10% 12%

rate 10 years annually 10% 12%") Exercise 14-2 1. Maturity Interest paid Stated rate Effective (market) rate 10 years annually 10% 12% Interest $100,000 x 5.65022 * = $565,022 Principal $1,000,000 x 0.32197 ** = 321,970 Present value

Exercise 14-2 1. Maturity Interest paid Stated rate Effective (market) rate 10 years annually 10% 12% Interest $100,000 x 5.65022 * = $565,022 Principal $1,000,000 x 0.32197 ** = 321,970 Present value

REPORTING AND INTERPRETING LIABILITIES

REPORTING AND INTERPRETING LIABILITIES Chapter 9 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Slide Inc. 1 UNDERSTANDING THE BUSINESS The acquisition of assets is financed from two sources: Debt -

REPORTING AND INTERPRETING LIABILITIES Chapter 9 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Slide Inc. 1 UNDERSTANDING THE BUSINESS The acquisition of assets is financed from two sources: Debt -

November 7, 2005 Anderson ECON 136B Midterm #2 Name

November 7, 2005 Anderson ECON 136B Midterm #2 Name Complete the multiple choice questions (#1-25) on a green scantron, and the problems in your blue-book. 1. The term used for bonds that are unsecured

November 7, 2005 Anderson ECON 136B Midterm #2 Name Complete the multiple choice questions (#1-25) on a green scantron, and the problems in your blue-book. 1. The term used for bonds that are unsecured

Copyright 2009 The Learning House, Inc. Income Taxes and Investments Page 1 of 17

Copyright 2009 The Learning House, Inc. Income Taxes and Investments Page 1 of 17 Introduction Taxes are a significant expense for most companies and must be considered when analyzing a company. Differences

Copyright 2009 The Learning House, Inc. Income Taxes and Investments Page 1 of 17 Introduction Taxes are a significant expense for most companies and must be considered when analyzing a company. Differences

ACCT 101 GROUP PROJECT INSTRUCTIONS

ACCT 101 GROUP PROJECT INSTRUCTIONS This project is to be completed as a group. All group members should actively participate in the project and it is up to the group to decide who will be responsible

ACCT 101 GROUP PROJECT INSTRUCTIONS This project is to be completed as a group. All group members should actively participate in the project and it is up to the group to decide who will be responsible

ACCT 652 Accounting. Payroll accounting. Payroll accounting Week 8 Liabilities and Present value

11-1 ACCT 652 Accounting Week 8 Liabilities and Present value Some slides Times Mirror Higher Education Division, Inc. Used by permission 2016, Michael D. Kinsman, Ph.D. 1 1 Payroll accounting I am sure

11-1 ACCT 652 Accounting Week 8 Liabilities and Present value Some slides Times Mirror Higher Education Division, Inc. Used by permission 2016, Michael D. Kinsman, Ph.D. 1 1 Payroll accounting I am sure

LONG-TERM LIABILITIES

Chapter 14 LONG-TERM LIABILITIES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

Chapter 14 LONG-TERM LIABILITIES PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

Long-Term Liabilities. Record and Report Long-Term Liabilities

SECTION Long-Term Liabilities VII OVERVIEW What this section does This section explains transactions, calculations, and financial statement presentation of long-term liabilities, primarily bonds and notes

SECTION Long-Term Liabilities VII OVERVIEW What this section does This section explains transactions, calculations, and financial statement presentation of long-term liabilities, primarily bonds and notes

LONG-TERM LIABILITIES: NOTES, BONDS, AND LEASES

FINANCIAL ACCOUNTING Week 10 LONG-TERM LIABILITIES: NOTES, BONDS, AND LEASES I. Learning Objectives - Long-term Liabilities A. Understand what are long-term liabilities, e.g., longterm notes payable, bonds

FINANCIAL ACCOUNTING Week 10 LONG-TERM LIABILITIES: NOTES, BONDS, AND LEASES I. Learning Objectives - Long-term Liabilities A. Understand what are long-term liabilities, e.g., longterm notes payable, bonds

John J. Wild Sixth Edition

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 10 Reporting and Analyzing Long-Term Liabilities Conceptual

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 10 Reporting and Analyzing Long-Term Liabilities Conceptual

2010 To accrue the expense and liability for vacations: Vacation Wages Payable 7,740. To record vacation time paid:

FA 2.3 EXERCISE 13-10 (25-30 minutes) (a) 2010 To accrue the expense and liability for vacations: Wages Expense 7,740 (1) Vacation Wages Payable 7,740 To record vacation time paid: No entry. 2011 To accrue

FA 2.3 EXERCISE 13-10 (25-30 minutes) (a) 2010 To accrue the expense and liability for vacations: Wages Expense 7,740 (1) Vacation Wages Payable 7,740 To record vacation time paid: No entry. 2011 To accrue

Acct Fall D: 2015 Spring B Smartbook 5 - B18

1. value: 2.00 points Exercise 13-2 Accounting for par, stated, and no-par stock issuances LO P1 Rodriguez Corporation issues 18,000 shares of its common stock for $405,000 cash on February 20. 1. Assume

1. value: 2.00 points Exercise 13-2 Accounting for par, stated, and no-par stock issuances LO P1 Rodriguez Corporation issues 18,000 shares of its common stock for $405,000 cash on February 20. 1. Assume

Gleim CPA Test Prep: Financial (137 questions)

") [1] Gleim #: 12.1.1 -- Source: CPA 1189 T-18 Bonds payable issued with scheduled maturities at various dates are called Serial Bonds Term Bonds No Yes No No Yes No Yes Yes [2] Gleim #: 12.1.2 -- Source:

[1] Gleim #: 12.1.1 -- Source: CPA 1189 T-18 Bonds payable issued with scheduled maturities at various dates are called Serial Bonds Term Bonds No Yes No No Yes No Yes Yes [2] Gleim #: 12.1.2 -- Source:

SOLUTIONS TO EXERCISES

EXERCISE 13-1 (10 15 minutes) SOLUTIONS TO EXERCISES (a) (b) (c) (d) (e) (f) (g) (h) (i) (j) (k) (l) (m) (n) (o) (p) Current liability or long-term liability depending on term of warranty. Current or noncurrent

EXERCISE 13-1 (10 15 minutes) SOLUTIONS TO EXERCISES (a) (b) (c) (d) (e) (f) (g) (h) (i) (j) (k) (l) (m) (n) (o) (p) Current liability or long-term liability depending on term of warranty. Current or noncurrent

Adjustments, Financial Statements, and the Quality of Earnings

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Singer Financial Corporation Financial Statements December 31, 2013 and 2012

Singer Financial Corporation Financial Statements December 31, 2013 and 2012 Contents December 31, 2013 and 2012 Page(s) Independent Accountants Compilation Report... 1 Financial Statements Balance Sheets...

Singer Financial Corporation Financial Statements December 31, 2013 and 2012 Contents December 31, 2013 and 2012 Page(s) Independent Accountants Compilation Report... 1 Financial Statements Balance Sheets...

CHAPTER 6 ACCOUNTING AND THE TIME VALUE OF MONEY. MULTIPLE CHOICE Conceptual

CHAPTER 6 ACCOUNTING AND THE TIME VALUE OF MONEY MULTIPLE CHOICE Conceptual 21. Which of the following transactions would require the use of the present value of an annuity due concept in order to calculate

CHAPTER 6 ACCOUNTING AND THE TIME VALUE OF MONEY MULTIPLE CHOICE Conceptual 21. Which of the following transactions would require the use of the present value of an annuity due concept in order to calculate

Student Learning Outcomes

Chapter 14: Bonds and Long-Term Notes Part 1 - Bonds Intermediate Accounting II Dr. Chula King Student Learning Outcomes Account for bonds at face value, at a discount, or at a premium using the effective

Chapter 14: Bonds and Long-Term Notes Part 1 - Bonds Intermediate Accounting II Dr. Chula King Student Learning Outcomes Account for bonds at face value, at a discount, or at a premium using the effective

Section 13 Liabilities

15-1 Section 13 Liabilities Probable future sacrifices of economic benefits. Arise from present obligations to other entities. Result from past transactions or events. What is a Current Liability? 15-2

15-1 Section 13 Liabilities Probable future sacrifices of economic benefits. Arise from present obligations to other entities. Result from past transactions or events. What is a Current Liability? 15-2

STATEMENT OF FINANCIAL CONDITION JUNE 30, 2018

STATEMENT OF FINANCIAL CONDITION JUNE 30, 2018 Member SIPC FINRA Filed in accordance with Rule 17a-5(e)(3) as a PUBLIC DOCUMENT Page 1 of 10 STATEMENT OF FINANCIAL CONDITION As of JUNE 30, 2018 ASSETS

STATEMENT OF FINANCIAL CONDITION JUNE 30, 2018 Member SIPC FINRA Filed in accordance with Rule 17a-5(e)(3) as a PUBLIC DOCUMENT Page 1 of 10 STATEMENT OF FINANCIAL CONDITION As of JUNE 30, 2018 ASSETS

Accounting for Financial Institutions Course code: ACT305 Bank Accounting

Accounting for Financial Institutions Course code: ACT305 Bank Accounting Lectures 3 and 4 1 Accounting for Investment Securities 2 1 There are three types of investment, which are: 1. Government treasury

Accounting for Financial Institutions Course code: ACT305 Bank Accounting Lectures 3 and 4 1 Accounting for Investment Securities 2 1 There are three types of investment, which are: 1. Government treasury

PRINCIPLES OF FINANCIAL AND MANAGERIAL ACCOUNTING II. Long-Term Liabilities. 1. Determine and record the selling price of bonds payable.

Objectives: PRINCIPLES OF FINANCIAL AND MANAGERIAL ACCOUNTING II Long-Term Liabilities 1. Determine and record the selling price of bonds payable. 2. Determine and record amortization of premium and discount

Objectives: PRINCIPLES OF FINANCIAL AND MANAGERIAL ACCOUNTING II Long-Term Liabilities 1. Determine and record the selling price of bonds payable. 2. Determine and record amortization of premium and discount

Financial Instruments: Presentation INTRODUCTION

IAS 32 Financial Instruments: Presentation INTRODUCTION Objective Scope Application The stated objective of IAS 32 is to establish principles for presenting financial instruments as liabilities or equity

IAS 32 Financial Instruments: Presentation INTRODUCTION Objective Scope Application The stated objective of IAS 32 is to establish principles for presenting financial instruments as liabilities or equity

Investments and Fair Value Accounting

C H A P T E R 15 Investments and Fair Value Accounting QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 15. 1. This chapter

C H A P T E R 15 Investments and Fair Value Accounting QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 15. 1. This chapter

Math 34: Section 7.2 (Bonds)

") Math 34: 2016 Section 7.2 (Bonds) Bond is a type of promissory note. A bond written agreement between borrower and a lender specifying the terms of the loan. We usually use the word bond when the borrower

Math 34: 2016 Section 7.2 (Bonds) Bond is a type of promissory note. A bond written agreement between borrower and a lender specifying the terms of the loan. We usually use the word bond when the borrower

Original SSAP and Current Authoritative Guidance: SSAP No. 15

Statutory Issue Paper No. 80 Debt STATUS Finalized March 16, 1998 Original SSAP and Current Authoritative Guidance: SSAP No. 15 Type of Issue: Common Area SUMMARY OF ISSUE 1. Current statutory accounting

Statutory Issue Paper No. 80 Debt STATUS Finalized March 16, 1998 Original SSAP and Current Authoritative Guidance: SSAP No. 15 Type of Issue: Common Area SUMMARY OF ISSUE 1. Current statutory accounting

CHAPTER 12. Statement of Cash Flows. Study Objectives

CHAPTER 12 Statement of Cash Flows Study Objectives Indicate the primary purpose of the statement of cash flows. Distinguish among operating, investing, and financing activities. Explain the impact of

CHAPTER 12 Statement of Cash Flows Study Objectives Indicate the primary purpose of the statement of cash flows. Distinguish among operating, investing, and financing activities. Explain the impact of

Profit or loss recorded to Retained Earnings

Cash basis Recognizes transactions when cash or equivalents DIAGRAM OF T-ACCOUNTS METHODS & ORGS Balance Sheet as of 12/31/2100 Accrual basis Follows the matching principle and recognizes Assets = Liabilities

Cash basis Recognizes transactions when cash or equivalents DIAGRAM OF T-ACCOUNTS METHODS & ORGS Balance Sheet as of 12/31/2100 Accrual basis Follows the matching principle and recognizes Assets = Liabilities

AN ALTERNATIVE APPROACH FOR TEACHING THE INTEREST METHOD AMORTIZATION OF BOND PREMIUMS AND DISCOUNTS

AN ALTERNATIVE APPROACH FOR TEACHING THE INTEREST METHOD AMORTIZATION OF BOND PREMIUMS AND DISCOUNTS Stephen T. Scott Associate Professor School of Commerce Northwestern Business College Chicago, IL 5733

AN ALTERNATIVE APPROACH FOR TEACHING THE INTEREST METHOD AMORTIZATION OF BOND PREMIUMS AND DISCOUNTS Stephen T. Scott Associate Professor School of Commerce Northwestern Business College Chicago, IL 5733

REINFORCEMENT ACTIVITY 3, Part B, p. 715

REINFORCEMENT ACTIVITY 3, Part B, p. 715 10. Unadjusted Trial Balance December 31, 20X4 ACCOUNT TITLE DEBIT CREDIT Cash 25 0 0 1 40 Petty Cash 4 0 0 00 Accounts Receivable 15 7 8 9 20 Allowance for Uncollectible

REINFORCEMENT ACTIVITY 3, Part B, p. 715 10. Unadjusted Trial Balance December 31, 20X4 ACCOUNT TITLE DEBIT CREDIT Cash 25 0 0 1 40 Petty Cash 4 0 0 00 Accounts Receivable 15 7 8 9 20 Allowance for Uncollectible

XTEND, INC. FINANCIAL STATEMENTS September 30, 2017 and 2016

FINANCIAL STATEMENTS Grand Rapids, Michigan FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 FINANCIAL STATEMENTS BALANCE SHEETS... 3 STATEMENTS OF INCOME... 4 STATEMENTS OF STOCKHOLDERS'

FINANCIAL STATEMENTS Grand Rapids, Michigan FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 FINANCIAL STATEMENTS BALANCE SHEETS... 3 STATEMENTS OF INCOME... 4 STATEMENTS OF STOCKHOLDERS'

Accounting & Reporting of Financial Instruments 2016

Illustration 1 (Exchange of Financial Liability at Unfavorable terms) A company borrowed 50 lacs @ 12% p.a. Tenure of the loan is 10 years. Interest is payable every year and the principal is repayable

Illustration 1 (Exchange of Financial Liability at Unfavorable terms) A company borrowed 50 lacs @ 12% p.a. Tenure of the loan is 10 years. Interest is payable every year and the principal is repayable

COPYRIGHTED MATERIAL INDEX 1087

INDEX 1087 A Accelerated depreciation, 233 Accounting basis of, 49, 140 Cash to accrual conversion, 51 Accounting changes, 106 Interim reporting, 789 Accounting information Qualitative characteristics

INDEX 1087 A Accelerated depreciation, 233 Accounting basis of, 49, 140 Cash to accrual conversion, 51 Accounting changes, 106 Interim reporting, 789 Accounting information Qualitative characteristics

CEBU CPAR CENTER. M a n d a u e C I t y

Page 1 of 11 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF LIABILITIES PROBLEM NO. 1 In the audit of the Heats Corporation s financial statements at December 31, 2005, the chief accountant

Page 1 of 11 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF LIABILITIES PROBLEM NO. 1 In the audit of the Heats Corporation s financial statements at December 31, 2005, the chief accountant

Accounting Cheat Sheet

DIAGRAM OF TACCOUNTS Assets = Balance Sheet as of 12/31/20 Liabilit ies + = + Equity METHODS & ORGS Accrual basis Follows the matching principle and recognizes transactions as they occur (GAAP Method)

DIAGRAM OF TACCOUNTS Assets = Balance Sheet as of 12/31/20 Liabilit ies + = + Equity METHODS & ORGS Accrual basis Follows the matching principle and recognizes transactions as they occur (GAAP Method)

Financial Statement Analysis. L3: Analyzing Financing Activities - Liabilities

1 Financial Statement Analysis L3: Analyzing Financing Activities - Liabilities 2 Content 1. Leases 2. Post retirement benefits 3. Contingencies 4. Off-balance Sheet finance 5. Shareholder s equity 3 Liabilities

1 Financial Statement Analysis L3: Analyzing Financing Activities - Liabilities 2 Content 1. Leases 2. Post retirement benefits 3. Contingencies 4. Off-balance Sheet finance 5. Shareholder s equity 3 Liabilities

STATEMENT OF FINANCIAL CONDITION JUNE 30, Member SIPC FINRA Est. 1971

STATEMENT OF FINANCIAL CONDITION JUNE 30, 2015 Member SIPC FINRA Est. 1971 Filed in accordance with Rule 17a-5(e)(3) as a PUBLIC DOCUMENT STOCKCROSS FINANCIAL SERVICES, INC. STATEMENT OF FINANCIAL CONDITION

STATEMENT OF FINANCIAL CONDITION JUNE 30, 2015 Member SIPC FINRA Est. 1971 Filed in accordance with Rule 17a-5(e)(3) as a PUBLIC DOCUMENT STOCKCROSS FINANCIAL SERVICES, INC. STATEMENT OF FINANCIAL CONDITION

Accounting for Liabilities

CHAPTER 7 Accounting for Liabilities LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Show how notes payable and related interest expense affect financial

CHAPTER 7 Accounting for Liabilities LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Show how notes payable and related interest expense affect financial

Definition: present obligations based on past transactions or events that require either future payment or future performance of services

Liabilities Definition: present obligations based on past transactions or events that require either future payment or future performance of services A liability is a present obligation of the enterprise

Liabilities Definition: present obligations based on past transactions or events that require either future payment or future performance of services A liability is a present obligation of the enterprise

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

2 Glossary. report diluted EPS if the securities in their capital structure are antidilutive; they will report only the basic EPS number.

Glossary accelerated depreciation methods Depreciation methods that allow for higher depreciation charges in the early years and lower charges in later periods. Termed accelerated because these methods

Glossary accelerated depreciation methods Depreciation methods that allow for higher depreciation charges in the early years and lower charges in later periods. Termed accelerated because these methods

Chapter. Investing in Bonds. 3.1 Evaluating Bonds 3.2 Buying and Selling Bonds South-Western, Cengage Learning

Chapter 3 Investing in Bonds 3.1 Evaluating Bonds 3.2 Buying and Selling Bonds Lesson 3.1 Evaluating Bonds Learning Objectives LO 1-1 Describe the characteristics and different types of corporate bonds.

Chapter 3 Investing in Bonds 3.1 Evaluating Bonds 3.2 Buying and Selling Bonds Lesson 3.1 Evaluating Bonds Learning Objectives LO 1-1 Describe the characteristics and different types of corporate bonds.

Chapter 10. Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? FASB - Probable future sacrifice of economic benefits arising from

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? FASB - Probable future sacrifice of economic benefits arising from

Analyzing Financing Activities

Analyzing Financing Activities 3 CHAPTER McGraw-Hill/Irwin 2007, The McGraw-Hill Companies, All Rights Reserved Current (Shortterm) Liabilities Liabilities Classification Noncurrent (Long- Term) Liabilities

Analyzing Financing Activities 3 CHAPTER McGraw-Hill/Irwin 2007, The McGraw-Hill Companies, All Rights Reserved Current (Shortterm) Liabilities Liabilities Classification Noncurrent (Long- Term) Liabilities

practices or behaviour may constitute a constructive obligation in certain instances. A) True

True") MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Conceptually, liabilities constitute a present obligation as a result of a past event and entail

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Conceptually, liabilities constitute a present obligation as a result of a past event and entail

Handbook Volume II: Manuals. Fair Value Accounting Policy

Handbook Volume II: Manuals Fair Value Accounting Policy This NCREIF PREA Reporting Standards Manual has been developed with participation from NCREIF s Accounting Committee. The Manual has been endorsed

Handbook Volume II: Manuals Fair Value Accounting Policy This NCREIF PREA Reporting Standards Manual has been developed with participation from NCREIF s Accounting Committee. The Manual has been endorsed

1. The usual impetus for transactions that create a long-term debtor-creditor relationship between members of a consolidated group is due to the:

ultiple Choice 1. The usual impetus for transactions that create a long-term debtor-creditor relationship between members of a consolidated group is due to the: a. subsidiary's ability to borrow larger

ultiple Choice 1. The usual impetus for transactions that create a long-term debtor-creditor relationship between members of a consolidated group is due to the: a. subsidiary's ability to borrow larger

Shafter Joint Powers Financing Authority Basic Financial Statements For the year ended June 30, 2007

Basic Financial Statements Table of Contents Page Independent Auditors Report...1 Basic Financial Statements: Statement of Net Assets...3 Statement of Activities and Changes in Net Assets...4 Statement

Basic Financial Statements Table of Contents Page Independent Auditors Report...1 Basic Financial Statements: Statement of Net Assets...3 Statement of Activities and Changes in Net Assets...4 Statement

Lecture. Business Environment & Strategy Analysis. Industry. Strategy. Analysis. Analysis. Financial. Analysis. Analysis. of Sources &Uses of Funds

2 Lecture Industry Analysis Business Environment & Strategy Analysis Strategy Analysis Financial Statement Analysis Accounting Analysis Profitability Analysis Financial Analysis Analysis of Sources &Uses

2 Lecture Industry Analysis Business Environment & Strategy Analysis Strategy Analysis Financial Statement Analysis Accounting Analysis Profitability Analysis Financial Analysis Analysis of Sources &Uses

Chapter 12 - Reporting and Analyzing Cash Flows. Chapter Outline

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

Financial Statement Analysis

Financial Statement Analysis Introduction to Financial Reporting 1. Financial Accounting Standard Board (FASB) conceptual framework is applicable to general purpose financial statements. 2. Financial statements

Financial Statement Analysis Introduction to Financial Reporting 1. Financial Accounting Standard Board (FASB) conceptual framework is applicable to general purpose financial statements. 2. Financial statements

Stat 274 Theory of Interest. Chapter 6: Bonds. Brian Hartman Brigham Young University

Stat 274 Theory of Interest Chapter 6: Bonds Brian Hartman Brigham Young University Bonds A bond is a security issued by a government or a corporation which promises payments at future dates. Maturity

Stat 274 Theory of Interest Chapter 6: Bonds Brian Hartman Brigham Young University Bonds A bond is a security issued by a government or a corporation which promises payments at future dates. Maturity

The Adjustment Process and Financial Statements Irwin/McGraw-Hill

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

COMPREHENSIVE EXAMINATION A PART 1 (Chapters 1-6)

") COMPREHENSIVE EXAMINATION A PART 1 (Chapters 1-6) Problem A-I Multiple Choice. Choose the best answer for each of the following questions and enter the identifying letter in the space provided. 1. How

COMPREHENSIVE EXAMINATION A PART 1 (Chapters 1-6) Problem A-I Multiple Choice. Choose the best answer for each of the following questions and enter the identifying letter in the space provided. 1. How

COMPREHENSIVE EXAMINATION A PART 1 (Chapters 1-6)

") COMPREHENSIVE EXAMINATION A PART 1 (Chapters 1-6) Problem A-I Multiple Choice. Choose the best answer for each of the following questions and enter the identifying letter in the space provided. 1. 2. 3.

COMPREHENSIVE EXAMINATION A PART 1 (Chapters 1-6) Problem A-I Multiple Choice. Choose the best answer for each of the following questions and enter the identifying letter in the space provided. 1. 2. 3.

SU 3.1 Property, Plant, and Equipment

Part 1 Study Unit 3 SU 3.1 Property, Plant, and Equipment Overview Property, plant and equipment are also referred to as fixed assets, or capital assets. Last more than 1 year. Are for production or benefit

Part 1 Study Unit 3 SU 3.1 Property, Plant, and Equipment Overview Property, plant and equipment are also referred to as fixed assets, or capital assets. Last more than 1 year. Are for production or benefit

Lesson 9: Breaking Down the Balance Sheet

Lesson 9: Breaking Down the Balance Sheet As we touched upon in previous lessons, a balance sheet is divided into three categories: Assets, Liabilities, and Owner s Equity. This lesson will go over each

Lesson 9: Breaking Down the Balance Sheet As we touched upon in previous lessons, a balance sheet is divided into three categories: Assets, Liabilities, and Owner s Equity. This lesson will go over each

IFRS for SMEs IFRS Foundation-World Bank

International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 23 24 May 2011 Minsk, Belarus Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic 1.6 Section

International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 23 24 May 2011 Minsk, Belarus Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic 1.6 Section

INTERMEDIATE ACCOUNTING

Chapter 13 Investments and Long-Term Receivables INTERMEDIATE ACCOUNTING whole or in part. Objectives 1. Explain the classification and valuation of investments. 2. Account for investments in debt securities

Chapter 13 Investments and Long-Term Receivables INTERMEDIATE ACCOUNTING whole or in part. Objectives 1. Explain the classification and valuation of investments. 2. Account for investments in debt securities

CHAPTER 15 12e Update

CHAPTER 15 12e Update Stockholders Equity ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis *1. Stockholders rights; corporate form. 1,

CHAPTER 15 12e Update Stockholders Equity ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis *1. Stockholders rights; corporate form. 1,

RIGOS CMA REVIEW PART 1 CHAPTER 1 EXTERNAL FINANCIAL REPORTING DECISIONS

RIGOS CMA REVIEW PART 1 CHAPTER 1 EXTERNAL FINANCIAL REPORTING DECISIONS Course 5342 copyright 2019. The Rigos programs have educated over 100,000 professionals since 1980. 1-19 RIGOS CMA REVIEW PART

RIGOS CMA REVIEW PART 1 CHAPTER 1 EXTERNAL FINANCIAL REPORTING DECISIONS Course 5342 copyright 2019. The Rigos programs have educated over 100,000 professionals since 1980. 1-19 RIGOS CMA REVIEW PART

Chapter 11 Current Liabilities and Contingencies

Chapter 11 Current Liabilities and Contingencies Chapter 11 Current Liabilities and Contingencies M. Problems P11-1. Suggested solution: Item Liability Financial or non-financial obligation? Explanation

Chapter 11 Current Liabilities and Contingencies Chapter 11 Current Liabilities and Contingencies M. Problems P11-1. Suggested solution: Item Liability Financial or non-financial obligation? Explanation

Standard Financial Corp. Consolidated Statements of Financial Condition (Dollars in thousands except share and per share data)

") Consolidated Statements of Financial Condition (Dollars in thousands except share and per share data) March 31, September 30, 2015 2014 Cash on hand and due from banks $ 2,074 $ 2,166 Interest-earning

Consolidated Statements of Financial Condition (Dollars in thousands except share and per share data) March 31, September 30, 2015 2014 Cash on hand and due from banks $ 2,074 $ 2,166 Interest-earning

Chapter 21. Financial Instruments

Reference: IAS 32; IAS 39 and IFRS 7 Financial Instruments Contents: Page 1. Introduction 648 2. Definitions Example 1: financial assets Example 2: financial liabilities 3. Financial Risks 3.1 Overview

Reference: IAS 32; IAS 39 and IFRS 7 Financial Instruments Contents: Page 1. Introduction 648 2. Definitions Example 1: financial assets Example 2: financial liabilities 3. Financial Risks 3.1 Overview

Handbook Volume II: Manuals. Fair Value Accounting Policy

Handbook Volume II: Manuals Fair Value Accounting Policy This NCREIF PREA Reporting Standards Manual has been developed with participation from NCREIF s Accounting Committee. The Manual has been endorsed

Handbook Volume II: Manuals Fair Value Accounting Policy This NCREIF PREA Reporting Standards Manual has been developed with participation from NCREIF s Accounting Committee. The Manual has been endorsed

Time Value of Money. Appendix E. Learning Objectives. After studying this chapter, you should be able to:

E- 1 Appendix E Time Value of Money E- 2 Learning Objectives After studying this chapter, you should be able to: 1. Distinguish between simple and compound interest. 2. Solve for future value of a single

E- 1 Appendix E Time Value of Money E- 2 Learning Objectives After studying this chapter, you should be able to: 1. Distinguish between simple and compound interest. 2. Solve for future value of a single

INTRODUCTION TO FINANCIAL AND ACTUARIAL MATHEMATICS. Marek Šulista, Václav Nýdl, Gregory Moore

INTRODUCTION TO FINANCIAL AND ACTUARIAL MATHEMATICS Marek Šulista, Václav Nýdl, Gregory Moore 2 Text vznikl v rámci grantu FRVŠ 1632/2005. Chapter 1 BONDS Bond or debenture is a debt instrument that obligates

INTRODUCTION TO FINANCIAL AND ACTUARIAL MATHEMATICS Marek Šulista, Václav Nýdl, Gregory Moore 2 Text vznikl v rámci grantu FRVŠ 1632/2005. Chapter 1 BONDS Bond or debenture is a debt instrument that obligates

EDUCATIONAL MEDIA FOUNDATION

EDUCATIONAL MEDIA FOUNDATION Rocklin, California CONSOLIDATED WITH INDEPENDENT AUDITORS REPORT TABLE OF CONTENTS Page Number Independent Auditors Report 1 Consolidated Statement of Financial Position 2

EDUCATIONAL MEDIA FOUNDATION Rocklin, California CONSOLIDATED WITH INDEPENDENT AUDITORS REPORT TABLE OF CONTENTS Page Number Independent Auditors Report 1 Consolidated Statement of Financial Position 2

SELECTED FINANCIAL DATA (dollars in thousands, except share and per share data) Years Ended December 31 2014 2013 2012 2011 2010 SUMMARY OF OPERATIONS: Total interest income.. $ 36,355 $ 35,958 $ 39,001

SELECTED FINANCIAL DATA (dollars in thousands, except share and per share data) Years Ended December 31 2014 2013 2012 2011 2010 SUMMARY OF OPERATIONS: Total interest income.. $ 36,355 $ 35,958 $ 39,001

Chapter 11 Current Liabilities and Contingencies

Intermediate Accounting Vol 2 Canadian 3rd Edition Lo SOLUTIONS MANUAL Full download at: https://testbankreal.com/download/intermediate-accounting-vol-2-canadian- 3rd-edition-lo-solutions-manual/ Intermediate

Intermediate Accounting Vol 2 Canadian 3rd Edition Lo SOLUTIONS MANUAL Full download at: https://testbankreal.com/download/intermediate-accounting-vol-2-canadian- 3rd-edition-lo-solutions-manual/ Intermediate