Section 13 Liabilities

|

|

|

- Domenic King

- 6 years ago

- Views:

Transcription

1 15-1 Section 13 Liabilities Probable future sacrifices of economic benefits. Arise from present obligations to other entities. Result from past transactions or events.

2 What is a Current Liability? 15-2 LIABILITIES Current Liabilities Obligations payable within one year or one operating cycle, whichever is longer. Expected to be satisfied with: current assets or the creation of other current liabilities. Long-term Liabilities Note: Operating cycle The time span from when cash is used to acquire goods and services until cash is received from the sale of goods and services. Operating: refers to company operations Cycle: refers to the circle flow of cash used for co. inputs and then cash received from its outputs. Length of a cycle: Service co: the time span between (1) paying employees who perform the services & (2) receiving cash from customers. Merchandiser: the time span between (1) paying suppliers for merchandise and (2) receiving cash from customers.

3 15-3 Current Liabilities Accounts payable Taxes payable (Fed, State, Local) Unearned revenues Current Liabilities Cash dividends payable Accrued expenses Short-term notes payable

4 15-4 Accrued Expenses: Compensation expenses: such as salaries, commissions, and bonuses are liabilities at the balance sheet date if earned but unpaid. Accrued expenses/accrued liabilities: are recorded with an adjusting entry at period end, prior to preparing financial statements.

5 CASH-BASIS ACCOUNTING vs. ACCRUAL-BASIS ACCOUNTING 15-5 Most companies use accrual-basis accounting recognize revenue when it is earned and expenses in the period incurred, without regard to the time of receipt or payment of cash. Under the strict cash-basis, companies record revenue only when they receive cash, and record expenses only when they disperse cash. Cash basis financial statements are not in conformity with GAAP.

6 CASH-BASIS ACCOUNTING vs. ACCRUAL-BASIS ACCOUNTING Conversion From Cash Basis To Accrual Basis Example: Dr. Diane Windsor, like many small business owners, keeps her accounting records on a cash basis. In the year 2012, Dr. Windsor received $300,000 from her patients and paid $170,000 for operating expenses, resulting in an excess of cash receipts over disbursements of $130,000 ($300,000 - $170,000). At January 1 and December 31, 2012, she has accounts receivable, unearned service revenue, accrued liabilities, and prepaid expenses as shown in following Illustration. 15-6

7 CASH-BASIS ACCOUNTING vs. ACCRUAL-BASIS ACCOUNTING 15-7 Cash Accounts Receivalbe All Collections in 2012 (plug #) 293,000 1/1/ ,000 A/R Collection in ,000 Unearned Revenue 4,000 All Payments in 2012 (plug) 169,100 Prepaid in Collection in ,000 12/31/ ,000 12/31/2012 9,000 Accrual Basis: 120,400=130,000-3,000-4, , ,100 = 170, Unearned Revenue 1/1/ ,000= Unprovided service in , ,000-3,000-4,000 12/31/2012 4,000 Prepaid Expense 1/1/2012 1,800 New prepaid incurred in /31/2012 2,700 Accrued Salary Payable 1/1/2012 2,000 Unpaid expense in ,500 12/31/2012 5,500

8 CASH-BASIS ACCOUNTING vs. ACCRUAL-BASIS ACCOUNTING 15-8 Conversion From Cash Basis To Accrual Basis 120,400 = 130,000-3,000-4, ,500 Converting back from Accrual to Cash basis: 120, , , ,500 = 130,000 (Cash) Or, 130,000 = NI + 3,000+4, ,500 NI = 120,400 (Accrual basis)

9 15-9 REVERSING ENTRIES (Not Required) With or Without Reversing Entries for Accruals Example: Notes: assuming 10/31 is period end for closing books.

10 USING REVERSING ENTRIES Summary of Reversing Entries, If Used 1. Accrued expenses and revenue: may be reversed; revenue earned but cash not collected or expenses incurred but not paid. 2. Deferred (Unearned or future) revenue: for which a company debited cash and credited Unearned Revenue. No reversing entries, but adjusting entries are needed when services are rendered. (Note: Deferred charges (see slide 23) bond issue costs, amortized, not reversed. Deferred income taxes - When book income > taxable income: Dr. Income tax Cr. Income tax payable (current, due) Deferred (future) tax liability (no reversing; see slide 22-37) Note: Adjusting entries - depreciation and amortization; never reverse.

11 15-11 Troubled Debt Restructuring When changing the original terms of a debt agreement is motivated by financial difficulties experienced by the debtor (borrower), the new arrangement is referred to as a troubled debt restructuring. A troubled debt restructuring may be achieved in either of two ways: 1.The debt may be settled at the time of the restructuring. 2.The debt may be continued, but with modified terms.

12 Debt Settled at Time of Restructuring - Example First Prudent Bank is holding a $30,000,000 note from the developer of some property. The developer is in financial trouble and cannot pay the bank the amount owed. The bank agrees to accept land with a fair value of $20,000,000 in full settlement of the note. The property is carried on the books of the developer at $17,000,000. The entries on the books of the developer to record the settlement: Land... 3,000,000 Gain on disposal of land... 3,000,000 ($20,000,000 less carrying value of $17,000,000) Note payable... 30,000,000 Gain on troubled debt restructuring. 10,000,000 Land. 20,000,000

13 Debt is Continued with Modified Terms - Example Example: the total cash payments are less than the carrying amount of the debt. First Prudent Bank holds a $30,000,000 note from a property developer. The note bears interest at 10%, and matures in 2 years. The developer is in financial difficulty and the bank agrees to modify the terms of the agreement as follows: 1. Forgive or reverse the interest accrued last year of $3,000,000, un-accrued interest is irrelevant as loan terms will be modified. 2. Adjust or reduce the interest payments to $2,000,000 each year. 3. Reduce the principal amount to $25,000,000. Principal Interest Total Carrying amount $ 30,000,000 $ 3,000,000 $ 33,000,000 Future payments 25,000,000 4,000,000 29,000,000 Gain to developer $ 4,000,000

14 15-14 Debt is Continued with Modified Terms At the date of the new agreement, the following journal entry is required: Accrued interest payable... 3,000,000 Note payable - old... 30,000,000 Gain on debt restructuring. 4,000,000 Note payable new. 29,000,000 Net Notes Payable $29,000,000 (total future cash payments including new principal and new interests) At each of the next two interest payments, make the following entry: Note payable... 2,000,000 Cash 2,000,000

15 Debt is Continued with Modified Terms - Summary Amount Face amount of old note $ 30,000,000 Entry at date of restructuring (1,000,000) First interest payment (2,000,000) Second interest payment (2,000,000) Maturity value of note $ 25,000,000 At maturity, the developer will make the following entry: Note payable... 25,000,000 Cash 25,000,000

16 Current Maturities of Long-Term Debt Long-term obligations (bonds, notes, lease liabilities, deferred tax liabilities) usually are reclassified and reported as current liab. when they become payable within the operating year (or operating cycle, if longer than a year). Exclude long-term debts maturing currently as current liabilities if they are to be: 1. Retired by assets accumulated that have not been shown as current assets, 2. Refinanced, or retired from the proceeds of a new debt issue, or 3. Converted into capital stock.

17 Short-Term Obligations Expected to be Refinanced May reclassify a short-term liability as long-term if two conditions are met: It has the intent to refinance on a long-term basis. and It has demonstrated the ability to refinance. The ability to refinance on a long-term basis can be demonstrated by an existing refinancing agreement, or actual financing prior to issuance of the financial statements.

18 15-18 Short-Term Obligations Expected to be Refinanced - Cont d Mgmt. Intends of Refinance YES Demonstrates Ability to Refinance Actual Refinancing after balance sheet date but before issue date YES or NO NO Classify as Current Liability Financing Agreement Noncancellable with Capable Lender Exclude Short-Term Obligations from Current Liabilities and Reclassify as LT Debt Note: treated differently from subsequent event

19 Subsequent Events 1. Conditions existed on the Balance Sheet Date (year end date), e.g., the bankruptcy of a customer 10 days after the balance sheet date usually reflects the poor financial health that existed on the balance sheet date, and the estimate of bad debts may therefore need to be revised to reflect the new info. (i.e., if estimated losses incurred prior to balance sheet date but settled subsequently (before issuance date); should be accrued as of balance sheet date] Cause of Loss Contingency Clarification Year End Date (Balance Sheet Date) Financial Statements issue Date Financial Statement Period Subsequent Events Period

20 Subsequent Events 2. Evidence of conditions (events) occurring after the year-end date (balance sheet date) but before the financial statements issued, if the possible loss would cause the fin. Statements to be misleading, it should be disclosed on the financial statements. E.g., the loss of inventories or plant assets due to a casualty, a sale of bond or capital stock issue Cause of Loss Contingency Clarification Fiscal Year Ends Financial Statements issued

21 Refinancing of Short-Term Debt - Example On December 31, 2010, Alexander Company had $1,200,000 of short-term debt in the form of notes payable due February 2, On January 21, 2011, the company issued 25,000 shares of its common stock for $36 per share, receiving $900,000 proceeds after brokerage fees and other costs of issuance. On February 2, 2011, the proceeds from the stock sale, supplemented by an additional $300,000 cash, are used to liquidate the $1,200,000 debt. The December 31, 2010, balance sheet is issued on February 23, Instructions: Show how the $1,200,000 of short-term debt should be presented on the December 31, 2010, balance sheet, including note disclosure

22 Refinancing of Short-Term Debt - Example Cont d Partial Balance Sheet Current liabilities: Notes payable (not refin ed by NP) Long-term debt: Notes payable refinanced (via CS) Total liabilities $ 300, ,000 $1,200,000

23 Asset Retirement Obligations Environmental Liabilities (e.g., mines, nuclear power plants) A company must recognize an asset retirement obligation (ARO) when it has an existing legal obligation associated with the retirement of a long-lived asset and when it can reasonably estimate the amount of the liability. NOTE: The SEC argues that if the liability is within a range, and no amount within the range is the best estimate, then management should recognize the minimum amount of the range.

24 15-24 Environmental Liabilities Cont d Obligating Events. Examples of existing legal obligations, which require recognition of a liability include, but are not limited to: decommissioning nuclear facilities, dismantling, restoring, and reclamation of oil and gas properties, certain closure, reclamation, and removal costs of mining facilities, closure and post-closure costs of landfills.

25 15-25 Environmental Liabilities Example On January 1, 2010, Wildcat Oil Company erected an oil platform in the Gulf of Mexico. Wildcat is legally required to dismantle and remove the platform at the end of its useful life, estimated to be five years. Wildcat estimates that dismantling and removal will cost $1,000,000. Based on a 10 percent discount rate, the fair value of the asset retirement obligation is estimated to be $620,920 ($1,000,000 x PV of $1). Wildcat records this ARO as follows. Drilling platform 620,920 Asset retirement obligation 620,920

26 Environmental Liabilities Example Cont d During the life of the asset, Wildcat allocates the asset retirement cost to expense. Using the straight-line method, Wildcat makes the following entries to record this expense. December 31, 2010, 2011, 2012, 2013, 2014 Depreciation expense ($620,920 / 5) 124,184 Accumulated depreciation 124,184

27 Environmental Liabilities Example Cont d Illustration: On January 10, 2015, Wildcat contracts with Rig Reclaimers, Inc. to dismantle the platform at a contract price of $995,000. Wildcat makes the following journal entry to record settlement of the ARO. January 10, 2015 Asset retirement obligation 1,000,000 Gain on settlement of ARO 5,000 Cash 995,000

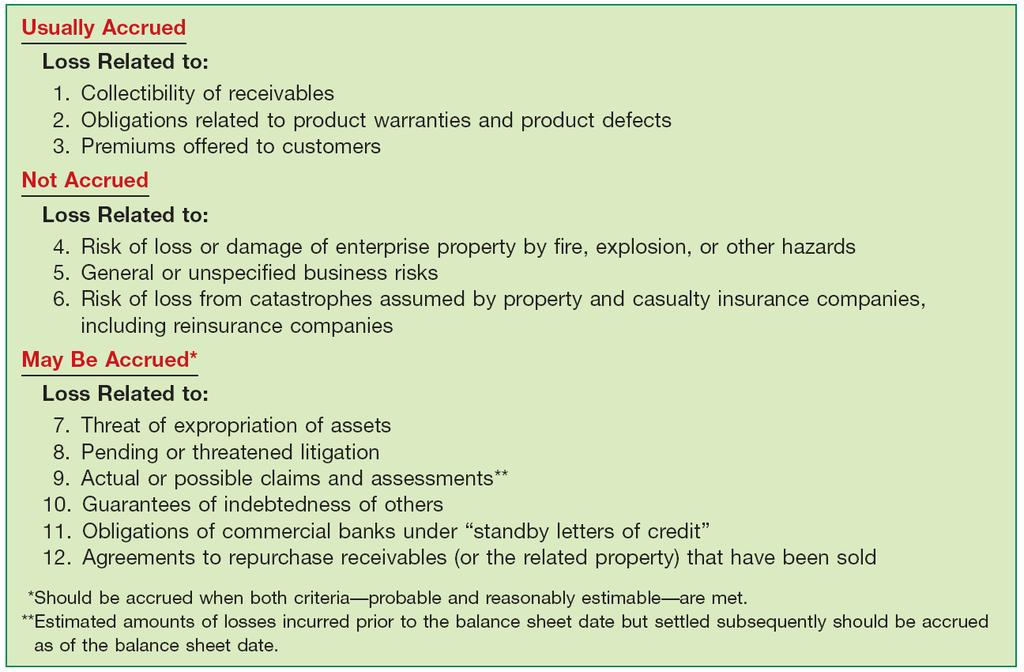

28 15-28 Contingencies An existing condition, situation, or set of circumstances involving uncertainty as to possible gain (gain contingency) or loss (loss contingency) to an enterprise that will ultimately be resolved when one or more future events occur or fail to occur. * * Accounting for Contingencies, Statement of Financial Accounting Standards No. 5 (Stamford, Conn.: FASB, 1975), par. 1

29 15-29 Gain Contingencies Typical Gain Contingencies are: 1. Possible receipts of monies from gifts, donations, and bonuses. 2. Possible refunds from the government in tax disputes. 3. Pending court cases with a probable favorable outcome. 4. Tax loss carryforwards. Gain contingencies are not recorded. Disclosed only if probability of receipt is high.

30 15-30 Contingent Liability Loss Contingencies The likelihood that the future event will confirm the incurrence of a liability can range from probable to remote. FASB uses three areas of probability: Probable. Reasonably possible. Remote.

31 15-31 Loss Contingencies Probability Probable Reasonably Possible Remote Accounting Accrue Footnote Ignore

Prepare the December 31 entry assuming it is probable that Scorcese will be liable for $900,000 as a result of this suit.")

32 15-32 Loss Contingencies - Example Scorcese Inc. is involved in a lawsuit at December 31, (a) Prepare the December 31 entry assuming it is probable that Scorcese will be liable for $900,000 as a result of this suit. (b) Prepare the December 31 entry, if any, assuming it is not probable that Scorcese will be liable for any payment as a result of this suit. (a) Lawsuit loss 900,000 Lawsuit liability 900,000 (b) No entry is necessary. The loss is not accrued because it is not probable that a liability has been incurred at 12/31/10.

33 Loss Contingencies 15-33

34 15-34 Loss Contingencies Common loss contingencies: 1. Litigation, claims, and assessments. 2. Guarantee and warranty costs. 3. Premiums and coupons. 4. Environmental liabilities.

35 15-35 Loss Contingencies Guarantee and Warranty Costs Promise made by a seller to a buyer to make good on a deficiency of quantity, quality, or performance in a product. If it is probable that customers will make warranty claims and a company can reasonably estimate the costs involved, the company must record an expense.

36 15-36 Extended Warranty Contracts Extended warranties are sold separately from the product. The related revenue is unearned until: Claims are made against the extended warranty, or The extended warranty period expires.

37 15-37 Guarantee and Warranty Costs Two basic methods of accounting for warranty costs: 1. Cash-Basis method Expense warranty costs as incurred, because 1. it is not probable that a liability has been incurred, or 2. it cannot reasonably estimate the amount of the liability.

38 15-38 Guarantee and Warranty Costs Two basic methods of accounting for warranty costs: 2. Accrual-Basis method Charge warranty costs to operating expense in the year of sale of the related products. Method is the generally accepted method. Referred to as the expense warranty approach.

39 15-39 Warranty Expense - Example Streep Factory provides a 2-year warranty with one of its products which was first sold in In that year, Streep spent $70,000 servicing warranty claims. At year-end, Streep estimates that an additional $400,000 will be spent in the future to service warranty claims related to 2010 sales. Prepare Streep s journal entry to record the $70,000 expenditure, and the December 31 adjusting entry Warranty expense 70,000 Cash, Inventory, Payroll 70,000 12/31/10 Warranty expense 400,000 Warranty liability 400,000

40 15-40 Premiums and Coupons Companies should charge the costs of premiums and coupons to expense in the period of the product sale that benefits from the plan. Accounting: Company estimates the number of outstanding premium offers that customers will present for redemption. Company charges the cost of premium offers to Premium Expense and credits Estimated Liability for Premiums.

41 15-41 Premiums - Example Fluffy Cakemix Company offered its customers a large nonbreakable mixing bowl in exchange for 25 cents and 10 boxtops. The mixing bowl costs Fluffy Cakemix Company 75 cents, and the company estimates that customers will redeem 60 % of the boxtops. The premium offer began in June 2010 and resulted in the transactions journalized below. Fluffy Cakemix Company records purchase of 20,000 mixing bowls as follows. Inventory of Premium Mixing Bowls 15,000 Cash 15,000 $20,000 x.75 = $15,000

42 15-42 Premiums Example (cont d) The entry to record sales of 300,000 boxes of cake mix would be: 300,000 x.80 (given) = $240,000 Cash 240,000 Sales 240,000 Fluffy records the actual redemption of 60,000 boxtops (given), the receipt of 25 cents per 10 boxtops, and the delivery of the mixing bowls as follows. Cash [(60,000 / 10) x $0.25] 1,500 Premium Expense (( ) x 6,000) 3,000 Inventory of Premium Mixing Bowls 4,500 Cost Computation: (60,000 / 10) x $0.75 = $4,500

43 15-43 Premiums Example (cont d) Finally, Fluffy makes an end-of-period adjusting entry for estimated liability for outstanding premium offers (boxtops) as follows. Premium expense 6,000 Liability for premiums 6,000 Or, 120,000 = (300,000 x 60%) 60,000 redeemed

Current Liabilities and Contingencies

Irsan Lubis - Dosen Perbanas Institute PREVIEW OF CHAPTER 13 13-1 Intermediate Accounting 15th Edition Kieso Weygandt Warfield 13 and Contingencies LEARNING OBJECTIVES After studying this chapter, you

Irsan Lubis - Dosen Perbanas Institute PREVIEW OF CHAPTER 13 13-1 Intermediate Accounting 15th Edition Kieso Weygandt Warfield 13 and Contingencies LEARNING OBJECTIVES After studying this chapter, you

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 13-1 13-2 PREVIEW OF CHAPTER 13 13-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 13-1 13-2 PREVIEW OF CHAPTER 13 13-3

Chapter 11: Liabilities, on and off balance sheet. General issues Long-term debt, contingent liabilities

Chapter 11: Liabilities, on and off balance sheet General issues Long-term debt, contingent liabilities 1 Liabilities, definition and classification present obligations based on past transactions or events

Chapter 11: Liabilities, on and off balance sheet General issues Long-term debt, contingent liabilities 1 Liabilities, definition and classification present obligations based on past transactions or events

Chapter 10. Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? FASB - Probable future sacrifice of economic benefits arising from

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? FASB - Probable future sacrifice of economic benefits arising from

YORK UNIVERSITY SCHOOL OF ADMINISTRATIVE STUDIES (Last) (First) Professor Sung Kwon (Course Director) and Ms. Trish Farrell

(First) Professor Sung Kwon (Course Director) and Ms. Trish Farrell") YORK UNIVERSITY Name, SCHOOL OF ADMINISTRATIVE STUDIES (Last) (First) Professor Sung Kwon (Course Director) and Ms. Trish Farrell ADMS 3595 Intermediate Financial Accounting II EXAM I, Winter 2012 (White

YORK UNIVERSITY Name, SCHOOL OF ADMINISTRATIVE STUDIES (Last) (First) Professor Sung Kwon (Course Director) and Ms. Trish Farrell ADMS 3595 Intermediate Financial Accounting II EXAM I, Winter 2012 (White

US Financial Reporting - Primary Terms (Definition Report)

") 1 String usfr-gc General Concepts (usfr-gc:generalconcepts) This is a category for storing general concepts. General concepts are high-level business reporting concepts such as "assets" and "liabilities"

1 String usfr-gc General Concepts (usfr-gc:generalconcepts) This is a category for storing general concepts. General concepts are high-level business reporting concepts such as "assets" and "liabilities"

practices or behaviour may constitute a constructive obligation in certain instances. A) True

True") MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Conceptually, liabilities constitute a present obligation as a result of a past event and entail

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Conceptually, liabilities constitute a present obligation as a result of a past event and entail

CHAPTER 13. Current Liabilities and Contingencies 1, 2, 3, 4, 6, Collections for third parties. 16 7, 8 8, 9, 10, 21 17, 18, 19, 20, 21, 23

CHAPTER 13 Current Liabilities and Contingencies ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Concept of liabilities; definition

CHAPTER 13 Current Liabilities and Contingencies ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Concept of liabilities; definition

Chapter 10. Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? Probable future sacrifice of economic benefits arising from present

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? Probable future sacrifice of economic benefits arising from present

Balance Sheet: Reporting Liabilities

Balance Sheet: Reporting Liabilities Publication Date: August 2015 Balance Sheet: Reporting Liabilities Copyright 2015 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any

Balance Sheet: Reporting Liabilities Publication Date: August 2015 Balance Sheet: Reporting Liabilities Copyright 2015 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any

IFRS questions are available at the end of this chapter. TRUE-FALSE Conceptual

ACC 304 Week 9 Quiz Strayer NEW Click On The Link Below to Purchase A+ Graded Material Instant Download http://www.hwgala.com/acc-304-week-9-quiz-strayer-new-acc304w9q.htm Week 9 Quiz 5: Chapter 13, Quiz

ACC 304 Week 9 Quiz Strayer NEW Click On The Link Below to Purchase A+ Graded Material Instant Download http://www.hwgala.com/acc-304-week-9-quiz-strayer-new-acc304w9q.htm Week 9 Quiz 5: Chapter 13, Quiz

Before Class starts.(make sure your name is on all submissions)

") Before Class starts.(make sure your name is on all submissions) Last Homework due Thursday 4/17 before class. Final Exam is Saturday May 3 9:00-Noon; Conflicts? Contact me ASAP! What questions do you have

Before Class starts.(make sure your name is on all submissions) Last Homework due Thursday 4/17 before class. Final Exam is Saturday May 3 9:00-Noon; Conflicts? Contact me ASAP! What questions do you have

SU 3.1 Property, Plant, and Equipment

Part 1 Study Unit 3 SU 3.1 Property, Plant, and Equipment Overview Property, plant and equipment are also referred to as fixed assets, or capital assets. Last more than 1 year. Are for production or benefit

Part 1 Study Unit 3 SU 3.1 Property, Plant, and Equipment Overview Property, plant and equipment are also referred to as fixed assets, or capital assets. Last more than 1 year. Are for production or benefit

4/10/2012. Liabilities and Interest. Learning Objectives (LO) LO 1 Current Liabilities. LO 1 Current Liabilities. LO 1 Current Liabilities

LO 1 Current Liabilities. LO 1 Current Liabilities. LO 1 Current Liabilities") Learning Objectives (LO) Liabilities and Interest CHAPTER 9 After studying this chapter, you should be able to 1. Account for current liabilities 2. Measure and account for long-term liabilities 3. Account

Learning Objectives (LO) Liabilities and Interest CHAPTER 9 After studying this chapter, you should be able to 1. Account for current liabilities 2. Measure and account for long-term liabilities 3. Account

CHAPTER 6 ACCOUNTING AND THE TIME VALUE OF MONEY. MULTIPLE CHOICE Conceptual

CHAPTER 6 ACCOUNTING AND THE TIME VALUE OF MONEY MULTIPLE CHOICE Conceptual 21. Which of the following transactions would require the use of the present value of an annuity due concept in order to calculate

CHAPTER 6 ACCOUNTING AND THE TIME VALUE OF MONEY MULTIPLE CHOICE Conceptual 21. Which of the following transactions would require the use of the present value of an annuity due concept in order to calculate

Before Class starts.(make sure your name is on all submissions)

") Before Class starts.(make sure your name is on all submissions) Last Homework due TODAY before class. LAST class review Final Exam is Saturday December 13 9:00-Noon; Conflicts? Contact me ASAP! What questions

Before Class starts.(make sure your name is on all submissions) Last Homework due TODAY before class. LAST class review Final Exam is Saturday December 13 9:00-Noon; Conflicts? Contact me ASAP! What questions

Accounting for Income Taxes

Accounting for Income Taxes Publication Date: November 2016 Accounting for Income Taxes Copyright 2016 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form or by any

Accounting for Income Taxes Publication Date: November 2016 Accounting for Income Taxes Copyright 2016 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form or by any

YORK UNIVERSITY SCHOOL OF ADMINISTRATIVE STUDIES (Last) (First) Professor Sung Kwon (Section B) Ms. Shaweta Roopra (Section A)

(First) Professor Sung Kwon (Section B) Ms. Shaweta Roopra (Section A)") YORK UNIVERSITY Name, SCHOOL OF ADMINISTRATIVE STUDIES (Last) (First) Professor Sung Kwon (Section B) Ms. Shaweta Roopra (Section A) ADMS 3595 Intermediate Financial Accounting II EXAM I, Fall 2013 (White

YORK UNIVERSITY Name, SCHOOL OF ADMINISTRATIVE STUDIES (Last) (First) Professor Sung Kwon (Section B) Ms. Shaweta Roopra (Section A) ADMS 3595 Intermediate Financial Accounting II EXAM I, Fall 2013 (White

HappyBottoms Independent Auditor s Report and Financial Statements December 31, 2017

HappyBottoms Independent Auditor s Report and Financial Statements December 31, 2017 CONTENTS Page Independent Auditor s Report 1 Financial Statements Statement of Financial Position 2 Statement of Activities

HappyBottoms Independent Auditor s Report and Financial Statements December 31, 2017 CONTENTS Page Independent Auditor s Report 1 Financial Statements Statement of Financial Position 2 Statement of Activities

ACCOUNTING FOR UNCERTAINTY IN INCOME TAXES UNDER FASB ASC 740 (FIN 48)

") ACCOUNTING FOR UNCERTAINTY IN INCOME TAXES UNDER FASB ASC 740 (FIN 48) FIN 48 Prior to FIN 48, FASB ASC 450 (SFAS No. 5), Accounting for Contingencies, provided the guidance for tax contingencies. Under

ACCOUNTING FOR UNCERTAINTY IN INCOME TAXES UNDER FASB ASC 740 (FIN 48) FIN 48 Prior to FIN 48, FASB ASC 450 (SFAS No. 5), Accounting for Contingencies, provided the guidance for tax contingencies. Under

Definition: present obligations based on past transactions or events that require either future payment or future performance of services

Liabilities Definition: present obligations based on past transactions or events that require either future payment or future performance of services A liability is a present obligation of the enterprise

Liabilities Definition: present obligations based on past transactions or events that require either future payment or future performance of services A liability is a present obligation of the enterprise

1. Classification of Debt and Measurement Issues

Chapter 12 Debt Financing 1. Classification and measurement issues associated with debt 2. Accounting for short-term debt 3. Accounting for long-term debt (mortgages) 4. Understand the various types of

Chapter 12 Debt Financing 1. Classification and measurement issues associated with debt 2. Accounting for short-term debt 3. Accounting for long-term debt (mortgages) 4. Understand the various types of

JOURNAL ENTRIES APPENDIX

The Ultimate Accountants Reference: Including GAAP, IRS and SEC Regulations, Leases, and More, 3rd Edition Steven M. Bragg Copyright 2010 by John Wiley & Sons, Inc. APPENDIX B JOURNAL ENTRIES B.1 ACQUISITIONS

The Ultimate Accountants Reference: Including GAAP, IRS and SEC Regulations, Leases, and More, 3rd Edition Steven M. Bragg Copyright 2010 by John Wiley & Sons, Inc. APPENDIX B JOURNAL ENTRIES B.1 ACQUISITIONS

CEBU CPAR CENTER. M a n d a u e C I t y

Page 1 of 11 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF LIABILITIES PROBLEM NO. 1 In the audit of the Heats Corporation s financial statements at December 31, 2005, the chief accountant

Page 1 of 11 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF LIABILITIES PROBLEM NO. 1 In the audit of the Heats Corporation s financial statements at December 31, 2005, the chief accountant

ACC 356 Financial Reporting II Spring 2012 Exam 1 (CH 13, 14) I. Multiple Choice: 15 2 points each 30. II.

I. Multiple Choice: 15 2 points each 30. II.") Name Section ACC 356 Financial Reporting II Spring 2012 Exam 1 (CH 13, 14) I. Multiple Choice: 15 questions @ 2 points each 30 II. Contingencies 18 III. Current Liabilities 14 IV. Bonds 27 V. Troubled-Debt

Name Section ACC 356 Financial Reporting II Spring 2012 Exam 1 (CH 13, 14) I. Multiple Choice: 15 questions @ 2 points each 30 II. Contingencies 18 III. Current Liabilities 14 IV. Bonds 27 V. Troubled-Debt

SOLUTIONS TO EXERCISES

EXERCISE 13-1 (10 15 minutes) SOLUTIONS TO EXERCISES (a) (b) (c) (d) (e) (f) (g) (h) (i) (j) (k) (l) (m) (n) (o) (p) Current liability or long-term liability depending on term of warranty. Current or noncurrent

EXERCISE 13-1 (10 15 minutes) SOLUTIONS TO EXERCISES (a) (b) (c) (d) (e) (f) (g) (h) (i) (j) (k) (l) (m) (n) (o) (p) Current liability or long-term liability depending on term of warranty. Current or noncurrent

Provisions, Contingent Liabilities and Contingent Assets

Indian Accounting Standard (Ind AS) 37 Provisions, Contingent Liabilities and Contingent Assets (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority.

Indian Accounting Standard (Ind AS) 37 Provisions, Contingent Liabilities and Contingent Assets (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority.

Chapter 10 - REPORTING AND ANALYZING LIABILITIES

Revised Summer 2018 Chapter 10 Review 1 Chapter 10 - REPORTING AND ANALYZING LIABILITIES LO 1: Explain how to account for current liabilities. Current Liability: a debt that a company expects to pay 1.

Revised Summer 2018 Chapter 10 Review 1 Chapter 10 - REPORTING AND ANALYZING LIABILITIES LO 1: Explain how to account for current liabilities. Current Liability: a debt that a company expects to pay 1.

Indian Accounting Standard (Ind AS) 37. Provisions, Contingent Liabilities and Contingent Assets

37. Provisions, Contingent Liabilities and Contingent Assets") Indian Accounting Standard (Ind AS) 37 Provisions, Contingent Liabilities and Contingent Assets Indian Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets CONTENTS Paragraphs

Indian Accounting Standard (Ind AS) 37 Provisions, Contingent Liabilities and Contingent Assets Indian Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets CONTENTS Paragraphs

BUS210. Accounting for Financing Decisions: Long-Term Liabilities

BUS210 Accounting for Financing Decisions: Long-Term Liabilities Liabilities Current or Short-term Liabilities Long-term Debt (borrowed funds) Lease Liabilities Deferred Taxes Contingencies and Commitments

BUS210 Accounting for Financing Decisions: Long-Term Liabilities Liabilities Current or Short-term Liabilities Long-term Debt (borrowed funds) Lease Liabilities Deferred Taxes Contingencies and Commitments

Intermediate Financial Reporting 2 Primer

Intermediate Financial Reporting 2 Chartered Professional Accountants of Canada, CPA Canada, CPA are trademarks and/or certification marks of the Chartered Professional Accountants of Canada. 2018, Chartered

Intermediate Financial Reporting 2 Chartered Professional Accountants of Canada, CPA Canada, CPA are trademarks and/or certification marks of the Chartered Professional Accountants of Canada. 2018, Chartered

PG&E Corporation. Table 1: Earnings Summary First Quarter 2005 vs. First Quarter 2004 (in millions except per share amounts)

") Table 1: Earnings Summary First Quarter 2005 vs. First Quarter 2004 (in millions except per share amounts) Earnings (Loss) Three months ended Earnings (Loss) per Common Share (Diluted) Three months ended

Table 1: Earnings Summary First Quarter 2005 vs. First Quarter 2004 (in millions except per share amounts) Earnings (Loss) Three months ended Earnings (Loss) per Common Share (Diluted) Three months ended

Auditing Contingencies and Going Concern

Auditing Contingencies and Going Concern READING MATERIAL 1 I. Contingencies 1 A. Overview 1 B. Measurement principles 1 1. Definition of a contingency 1 2. Loss contingencies 1 3. Probability classification

Auditing Contingencies and Going Concern READING MATERIAL 1 I. Contingencies 1 A. Overview 1 B. Measurement principles 1 1. Definition of a contingency 1 2. Loss contingencies 1 3. Probability classification

Three months ended June 30, Six months ended June 30,

Table 1: Earnings Summary Second Quarter and Year-to-Date, 2005 vs. 2004 (in millions, except per share amounts) Three months ended June 30, Six months ended June 30, Earnings (Loss) Earnings (Loss) per

Table 1: Earnings Summary Second Quarter and Year-to-Date, 2005 vs. 2004 (in millions, except per share amounts) Three months ended June 30, Six months ended June 30, Earnings (Loss) Earnings (Loss) per

FAC PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS IAS 37

FAC 3701 2012 PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS IAS 37 PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS STUDY OBJECTIVES: 1. PROVISIONS VS OTHER LIABILITIES 2. RECOGNITION

FAC 3701 2012 PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS IAS 37 PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS STUDY OBJECTIVES: 1. PROVISIONS VS OTHER LIABILITIES 2. RECOGNITION

HappyBottoms Independent Auditor s Report and Financial Statements December 31, 2015

HappyBottoms Independent Auditor s Report and Financial Statements December 31, 2015 CONTENTS Page Independent Auditor s Report 1 Financial Statements Statement of Financial Position 2 Statement of Activities

HappyBottoms Independent Auditor s Report and Financial Statements December 31, 2015 CONTENTS Page Independent Auditor s Report 1 Financial Statements Statement of Financial Position 2 Statement of Activities

Bikes for the World, Inc. Audited Financial Statements. For the six months ended June 30, 2016 with Report of Independent Auditors

Audited Financial Statements For the six months ended June 30, 2016 with Report of Independent Auditors Audited Financial Statements For the six months ended June 30, 2016 Contents Report of Independent

Audited Financial Statements For the six months ended June 30, 2016 with Report of Independent Auditors Audited Financial Statements For the six months ended June 30, 2016 Contents Report of Independent

BROADRIDGE BUSINESS PROCESS OUTSOURCING, LLC (An indirect wholly-owned subsidiary of Broadridge Financial Solutions, Inc.)

") BROADRIDGE BUSINESS PROCESS OUTSOURCING, LLC (An indirect wholly-owned subsidiary of Broadridge Financial Solutions, Inc.) STATEMENT OF FINANCIAL CONDITION (UNAUDITED) AS OF DECEMBER 31, 2016 ****** Broadridge

BROADRIDGE BUSINESS PROCESS OUTSOURCING, LLC (An indirect wholly-owned subsidiary of Broadridge Financial Solutions, Inc.) STATEMENT OF FINANCIAL CONDITION (UNAUDITED) AS OF DECEMBER 31, 2016 ****** Broadridge

Name: ACC 4020 DW Take-Home Test #2

ACC 4020 DW Take-Home Test #2 Name: 1. Of the following items, the one that should be classified as a current asset is a. Trade installment receivables normally collectible in 18 months b. Cash designated

ACC 4020 DW Take-Home Test #2 Name: 1. Of the following items, the one that should be classified as a current asset is a. Trade installment receivables normally collectible in 18 months b. Cash designated

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

ROCHER DEBOULE MINERALS CORP. (formerly Ameridex Minerals Corp.) For the Three and Nine Months Ended. April 30, 2007

For the Three and Nine Months Ended. April 30, 2007") FINANCIAL STATEMENTS For the Three and Nine Months Ended April 30, 2007 Balance Sheets April 30, July 31, 2007 2006 Unaudited Audited Assets Current Assets Cash $ 537,538 $ 314,330 Amounts receivable 1,710

FINANCIAL STATEMENTS For the Three and Nine Months Ended April 30, 2007 Balance Sheets April 30, July 31, 2007 2006 Unaudited Audited Assets Current Assets Cash $ 537,538 $ 314,330 Amounts receivable 1,710

CAPE FEAR HABITAT FOR HUMANITY, INC.

CAPE FEAR HABITAT FOR HUMANITY, INC. Audited Financial Statements for the fiscal year ended (with comparative totals for 2014) Table of Contents Independent Auditor s Report... 3 Financial Statements Statement

CAPE FEAR HABITAT FOR HUMANITY, INC. Audited Financial Statements for the fiscal year ended (with comparative totals for 2014) Table of Contents Independent Auditor s Report... 3 Financial Statements Statement

Lifewater International, Inc. Financial Statements. Year Ended March 31, 2012

Financial Statements Year Ended March 31, 2012 Financial Statements Year Ended March 31, 2012 Table of Contents Page Independent Auditors' Report 3 Statement of Financial Position 4 Statement of Activities

Financial Statements Year Ended March 31, 2012 Financial Statements Year Ended March 31, 2012 Table of Contents Page Independent Auditors' Report 3 Statement of Financial Position 4 Statement of Activities

PG&E Corporation. Table 1: Earnings Summary Third Quarter and Year-to-Date, 2005 vs (in millions, except per share amounts)

") Table 1: Earnings Summary Third Quarter and Year-to-Date, 2005 vs. 2004 (in millions, except per share amounts) Three months ended September 30, Nine months ended September 30, Earnings (Loss) Earnings

Table 1: Earnings Summary Third Quarter and Year-to-Date, 2005 vs. 2004 (in millions, except per share amounts) Three months ended September 30, Nine months ended September 30, Earnings (Loss) Earnings

HILL PHYSICIANS MEDICAL GROUP, INC. AND SUBSIDIARIES. Consolidated Financial Statements. December 31, 2017 and 2016

Consolidated Financial Statements (With Independent Auditors Report Thereon) KPMG LLP Suite 1400 55 Second Street San Francisco, CA 94105 Independent Auditors Report To the Board of Directors Hill Physicians

Consolidated Financial Statements (With Independent Auditors Report Thereon) KPMG LLP Suite 1400 55 Second Street San Francisco, CA 94105 Independent Auditors Report To the Board of Directors Hill Physicians

Introduction to Health Care Accounting. Matthew J. Claeys, CPA

Introduction to Health Care Accounting Matthew J. Claeys, CPA 1 Agenda Basics of a health care financial statement Common and important ratios you should understand Revenue recognition and allowances Transactions

Introduction to Health Care Accounting Matthew J. Claeys, CPA 1 Agenda Basics of a health care financial statement Common and important ratios you should understand Revenue recognition and allowances Transactions

Catholic Diocese of Columbus Parish Accrual Accounting Implementation Guide

The purpose of this document is to guide you through implementation of accrual accounting for your Parish. Moving to accrual accounting will involve establishing accurate accrual accounting balances in

The purpose of this document is to guide you through implementation of accrual accounting for your Parish. Moving to accrual accounting will involve establishing accurate accrual accounting balances in

FORT VALLEY STATE UNIVERSITY FOUNDATION, INC. FORT VALLEY, GEORGIA

FORT VALLEY STATE UNIVERSITY FOUNDATION, INC. FORT VALLEY, GEORGIA CONSOLIDATED FINANCIAL STATEMENTS AS OF JUNE 30, 2017 AND 2016 AND INDEPENDENT AUDITOR S REPORT FORT VALLEY STATE UNIVERSITY FOUNDATION,

FORT VALLEY STATE UNIVERSITY FOUNDATION, INC. FORT VALLEY, GEORGIA CONSOLIDATED FINANCIAL STATEMENTS AS OF JUNE 30, 2017 AND 2016 AND INDEPENDENT AUDITOR S REPORT FORT VALLEY STATE UNIVERSITY FOUNDATION,

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

HALO COMPANIES, INC. (Exact name of registrant as specified in Charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q [X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q [X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

BRATTLEBORO MEMORIAL HOSPITAL FINANCIAL STATEMENTS. With Independent Auditors' Report

FINANCIAL STATEMENTS With Independent Auditors' Report TABLE OF CONTENTS Page(s) Independent Auditors' Report 1 Balance Sheets 2 Statements of Operations 3 Statements of Changes in Net Assets 4 Statements

FINANCIAL STATEMENTS With Independent Auditors' Report TABLE OF CONTENTS Page(s) Independent Auditors' Report 1 Balance Sheets 2 Statements of Operations 3 Statements of Changes in Net Assets 4 Statements

U.S. SECURITIES AND EXCHANGE COMMISSION Washington, D.C FORM 10-Q. For the quarterly period ended September 30, 2014

U.S. SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended September

U.S. SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended September

Exhibit Table 1: PG&E Corporation Business Priorities

Exhibit 99.2 Table 1: PG&E Corporation Business Priorities 2006-2010 1. Advance business transformation 2. Provide attractive shareholder returns 3. Increase investment in utility infrastructure 4. Implement

Exhibit 99.2 Table 1: PG&E Corporation Business Priorities 2006-2010 1. Advance business transformation 2. Provide attractive shareholder returns 3. Increase investment in utility infrastructure 4. Implement

Boss Holdings, Inc. and Subsidiaries. Consolidated Financial Statements December 31, 2016

Consolidated Financial Statements December 31, 2016 Contents Independent Auditor s Report 1-2 Financial statements Consolidated balance sheets 3 Consolidated statements of comprehensive income 4 Consolidated

Consolidated Financial Statements December 31, 2016 Contents Independent Auditor s Report 1-2 Financial statements Consolidated balance sheets 3 Consolidated statements of comprehensive income 4 Consolidated

La Familia Medical Center

Accountants Reports and Financial Statements June 30, 2009 and 2008 June 30, 2009 and 2008 Contents Independent Accountants Report... 1 Financial Statements Balance Sheets... 3 Statements of Operations...

Accountants Reports and Financial Statements June 30, 2009 and 2008 June 30, 2009 and 2008 Contents Independent Accountants Report... 1 Financial Statements Balance Sheets... 3 Statements of Operations...

- A resource - Controlled by the entity - As a result of a past event - From economic benefits are expected to flow to the entity.

Elements and recognition criteria 1. Identify the definition for each of these elements: a. Assets b. Liabilities c. Equity d. Income e. Expenses - A resource - Controlled by the entity - As a result of

Elements and recognition criteria 1. Identify the definition for each of these elements: a. Assets b. Liabilities c. Equity d. Income e. Expenses - A resource - Controlled by the entity - As a result of

PERSHING RESOURCES COMPANY, INC. AND SUBSIDIARY CONSOLIDATED FINANCIAL STATEMENTS FOR THE NINE MONTHS ENDED SEPTEMBER 30, 2017 AND 2016

CONSOLIDATED FINANCIAL STATEMENTS FOR THE NINE MONTHS ENDED SEPTEMBER 30, 2017 AND 2016 TABLE OF CONTENTS Consolidated Financial Statements: Consolidated Balance Sheets 1-2 Consolidated Statements of Operations

CONSOLIDATED FINANCIAL STATEMENTS FOR THE NINE MONTHS ENDED SEPTEMBER 30, 2017 AND 2016 TABLE OF CONTENTS Consolidated Financial Statements: Consolidated Balance Sheets 1-2 Consolidated Statements of Operations

Profit or loss recorded to Retained Earnings

Cash basis Recognizes transactions when cash or equivalents DIAGRAM OF T-ACCOUNTS METHODS & ORGS Balance Sheet as of 12/31/2100 Accrual basis Follows the matching principle and recognizes Assets = Liabilities

Cash basis Recognizes transactions when cash or equivalents DIAGRAM OF T-ACCOUNTS METHODS & ORGS Balance Sheet as of 12/31/2100 Accrual basis Follows the matching principle and recognizes Assets = Liabilities

ACCT 100 Intro to Acct. Chapter 12: Accruals, Deferrals, and the Worksheet Johnson

ACCT 100 Intro to Acct. Chapter 12: Accruals, Deferrals, and the Worksheet Johnson Where we have been: We have learned a lot about the selling and buying functions of merchandiser. You have learned many

ACCT 100 Intro to Acct. Chapter 12: Accruals, Deferrals, and the Worksheet Johnson Where we have been: We have learned a lot about the selling and buying functions of merchandiser. You have learned many

FORT VALLEY STATE UNIVERSITY FOUNDATION, INC. FORT VALLEY, GEORGIA

FORT VALLEY STATE UNIVERSITY FOUNDATION, INC. FORT VALLEY, GEORGIA CONSOLIDATED FINANCIAL STATEMENTS AS OF JUNE 30, 2016 AND 2015 AND INDEPENDENT AUDITOR S REPORT FORT VALLEY STATE UNIVERSITY FOUNDATION,

FORT VALLEY STATE UNIVERSITY FOUNDATION, INC. FORT VALLEY, GEORGIA CONSOLIDATED FINANCIAL STATEMENTS AS OF JUNE 30, 2016 AND 2015 AND INDEPENDENT AUDITOR S REPORT FORT VALLEY STATE UNIVERSITY FOUNDATION,

Paper-12 : COMPANY ACCOUNTS & AUDIT

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

Feltl and Company, Inc.

Minnetonka, Minnesota Balance Sheets December 31, 2017 and 2016 WIPFLi... Report of Independent Registered Public Accounting Firm Board of Directors Feltl and Company, Inc. Minnetonka, Minnesota Opinion

Minnetonka, Minnesota Balance Sheets December 31, 2017 and 2016 WIPFLi... Report of Independent Registered Public Accounting Firm Board of Directors Feltl and Company, Inc. Minnetonka, Minnesota Opinion

PERSHING RESOURCES COMPANY, INC. AND SUBSIDIARY CONSOLIDATED FINANCIAL STATEMENTS FOR THE THREE MONTHS ENDED MARCH 31, 2017 AND 2016

CONSOLIDATED FINANCIAL STATEMENTS FOR THE THREE MONTHS ENDED MARCH 31, 2017 AND 2016 TABLE OF CONTENTS Consolidated Financial Statements: Consolidated Balance Sheets 1-2 Consolidated Statements of Operations

CONSOLIDATED FINANCIAL STATEMENTS FOR THE THREE MONTHS ENDED MARCH 31, 2017 AND 2016 TABLE OF CONTENTS Consolidated Financial Statements: Consolidated Balance Sheets 1-2 Consolidated Statements of Operations

XTEND, INC. FINANCIAL STATEMENTS September 30, 2017 and 2016

FINANCIAL STATEMENTS Grand Rapids, Michigan FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 FINANCIAL STATEMENTS BALANCE SHEETS... 3 STATEMENTS OF INCOME... 4 STATEMENTS OF STOCKHOLDERS'

FINANCIAL STATEMENTS Grand Rapids, Michigan FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 FINANCIAL STATEMENTS BALANCE SHEETS... 3 STATEMENTS OF INCOME... 4 STATEMENTS OF STOCKHOLDERS'

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield. Slide 3-2

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

Feltl and Company, Inc.

Minneapolis, Minnesota Balance Sheets December 31, 2016 and 2015 Balance Sheets December 31, 2016 and 2015 Table of Contents Independent Auditor s Report...1 Balance Sheets Balance Sheets... 2... 3 Balance

Minneapolis, Minnesota Balance Sheets December 31, 2016 and 2015 Balance Sheets December 31, 2016 and 2015 Table of Contents Independent Auditor s Report...1 Balance Sheets Balance Sheets... 2... 3 Balance

APPENDIX 4H. Disclosure Checklist for Income Tax Basis Financial Statements. Financial Statement Date:

4 51 APPENDIX 4H Disclosure Checklist for Income Tax Basis Financial Statements Entity: Prepared by: Financial Statement Date: Date: Explanatory Comments This checklist includes the more common disclosure

4 51 APPENDIX 4H Disclosure Checklist for Income Tax Basis Financial Statements Entity: Prepared by: Financial Statement Date: Date: Explanatory Comments This checklist includes the more common disclosure

UNION PACIFIC RAILROAD COMPANY and CONSOLIDATED SUBSIDIARY COMPANIES

UNION PACIFIC RAILROAD COMPANY and CONSOLIDATED SUBSIDIARY COMPANIES Condensed Consolidated Financial Statements For the Quarterly Period Ended March 31, 2013 UNION PACIFIC RAILROAD COMPANY and CONSOLIDATED

UNION PACIFIC RAILROAD COMPANY and CONSOLIDATED SUBSIDIARY COMPANIES Condensed Consolidated Financial Statements For the Quarterly Period Ended March 31, 2013 UNION PACIFIC RAILROAD COMPANY and CONSOLIDATED

BUS210. Chapter 4 Sessions 4, 5, 6, & 7 Mechanics of Financial Information

BUS210 Chapter 4 Sessions 4, 5, 6, & 7 Mechanics of Financial Information Connecting the Accounting Equation with Transactions: Journal Entries, T Accounts E4-9 Prepare journal entries for each cash transaction

BUS210 Chapter 4 Sessions 4, 5, 6, & 7 Mechanics of Financial Information Connecting the Accounting Equation with Transactions: Journal Entries, T Accounts E4-9 Prepare journal entries for each cash transaction

XTEND, INC. FINANCIAL STATEMENTS September 30, 2018 and 2017

FINANCIAL STATEMENTS Grand Rapids, Michigan FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 FINANCIAL STATEMENTS BALANCE SHEETS... 3 STATEMENTS OF INCOME... 4 STATEMENTS OF STOCKHOLDERS'

FINANCIAL STATEMENTS Grand Rapids, Michigan FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 FINANCIAL STATEMENTS BALANCE SHEETS... 3 STATEMENTS OF INCOME... 4 STATEMENTS OF STOCKHOLDERS'

CHAPTER 1 UNDERSTANDING THE ISSUES

CHAPTER 1 UNDERSTANDING THE ISSUES 1. (a) Product extension manufacturer expands product lines in boating industry. (b) Vertical forward manufacturer buys distribution outlets (c) Conglomerate unrelated

CHAPTER 1 UNDERSTANDING THE ISSUES 1. (a) Product extension manufacturer expands product lines in boating industry. (b) Vertical forward manufacturer buys distribution outlets (c) Conglomerate unrelated

Smith Equipment Corporation Part II Suggested Journal Entries

Smith Equipment Corporation Part II Suggested Journal Entries 1 To summarize purchases on account for $800,000 Merchandise inventory (a) 800,000 Accounts payable (l) 800,000 2 To summarize payments to

Smith Equipment Corporation Part II Suggested Journal Entries 1 To summarize purchases on account for $800,000 Merchandise inventory (a) 800,000 Accounts payable (l) 800,000 2 To summarize payments to

QUARTERLY REPORT TO INVESTORS QUARTERLY REPORT TO INVESTORS SIX MONTHS ENDED AS OF AND FOR THE

QUARTERLY REPORT TO INVESTORS AS OF QUARTERLY AND FOR THE QUARTERLY REPORT TO INVESTORS REPORT SIX MONTHS ENDED TO INVESTORS AS JUNE OF QUARTERLY AND 30, FOR 2010 THE AS OF AND FOR THE THREE REPORT AND

QUARTERLY REPORT TO INVESTORS AS OF QUARTERLY AND FOR THE QUARTERLY REPORT TO INVESTORS REPORT SIX MONTHS ENDED TO INVESTORS AS JUNE OF QUARTERLY AND 30, FOR 2010 THE AS OF AND FOR THE THREE REPORT AND

Chapter 11 Current Liabilities and Contingencies

Intermediate Accounting Vol 2 Canadian 3rd Edition Lo SOLUTIONS MANUAL Full download at: https://testbankreal.com/download/intermediate-accounting-vol-2-canadian- 3rd-edition-lo-solutions-manual/ Intermediate

Intermediate Accounting Vol 2 Canadian 3rd Edition Lo SOLUTIONS MANUAL Full download at: https://testbankreal.com/download/intermediate-accounting-vol-2-canadian- 3rd-edition-lo-solutions-manual/ Intermediate

THE NEW YORK STATE SOCIETY OF CERTIFIED PUBLIC ACCOUNTANTS AND RELATED ENTITIES COMBINED FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION

THE NEW YORK STATE SOCIETY OF CERTIFIED PUBLIC ACCOUNTANTS COMBINED FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION YEARS ENDED MAY 31, 2014 AND 2013 AND INDEPENDENT AUDITORS REPORT TABLE OF CONTENTS

THE NEW YORK STATE SOCIETY OF CERTIFIED PUBLIC ACCOUNTANTS COMBINED FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION YEARS ENDED MAY 31, 2014 AND 2013 AND INDEPENDENT AUDITORS REPORT TABLE OF CONTENTS

CPA Summary Notes. Statement of Cash Flow. Objective of IAS 7

CPA Summary Notes Statement of Cash Flow Objective of IAS 7 The objective of IAS 7 is to require the presentation of information about the historical changes in cash and cash equivalents of an entity by

CPA Summary Notes Statement of Cash Flow Objective of IAS 7 The objective of IAS 7 is to require the presentation of information about the historical changes in cash and cash equivalents of an entity by

MYRTLE BEACH AREA CHAMBER OF COMMERCE AND SUBSIDIARY CONSOLIDATED FINANCIAL STATEMENTS AND ADDITIONAL INFORMATION. Year Ended December 31, 2014

CONSOLIDATED FINANCIAL STATEMENTS AND ADDITIONAL INFORMATION Year Ended December 31, 2014 TABLE OF CONTENTS December 31, 2014 Independent Auditors Report 1 Consolidated Financial Statements Consolidated

CONSOLIDATED FINANCIAL STATEMENTS AND ADDITIONAL INFORMATION Year Ended December 31, 2014 TABLE OF CONTENTS December 31, 2014 Independent Auditors Report 1 Consolidated Financial Statements Consolidated

Chapter 17. Provisions, Contingencies & Events after the Reporting Period

Provisions, Contingencies and Events after the Reporting Period Reference: Contents: IAS 37 Provisions, Contingent Liabilities and Contingent Assets IAS 10 Events After the Reporting Period IFRIC 1 Changes

Provisions, Contingencies and Events after the Reporting Period Reference: Contents: IAS 37 Provisions, Contingent Liabilities and Contingent Assets IAS 10 Events After the Reporting Period IFRIC 1 Changes

Balance Sheet - Form of Statement

Annex K ( SRC Rule 68 ) Balance Sheet - Form of Statement If applicable, and except as otherwise permitted by the Commission, the following line items and certain additional disclosures should appear on

Annex K ( SRC Rule 68 ) Balance Sheet - Form of Statement If applicable, and except as otherwise permitted by the Commission, the following line items and certain additional disclosures should appear on

Caterpillar Corporation

Caterpillar Corporation Caterpillar, Inc was founded in 1925. Headquartered in Peoria, Illinois, the company manufactures construction and mining equipment, diesel and natural gas engines, and industrial

Caterpillar Corporation Caterpillar, Inc was founded in 1925. Headquartered in Peoria, Illinois, the company manufactures construction and mining equipment, diesel and natural gas engines, and industrial

SELECTED FINANCIAL DATA (dollars in thousands, except share and per share data) Years Ended December 31 2014 2013 2012 2011 2010 SUMMARY OF OPERATIONS: Total interest income.. $ 36,355 $ 35,958 $ 39,001

SELECTED FINANCIAL DATA (dollars in thousands, except share and per share data) Years Ended December 31 2014 2013 2012 2011 2010 SUMMARY OF OPERATIONS: Total interest income.. $ 36,355 $ 35,958 $ 39,001

Chapter 011 Current Liabilities and Payroll Accounting

Summary of Questions by Difficulty Level (DL) and Learning Objective (LO) True/False Item DL LO Item DL LO Item DL LO 1. Easy C1 20. Hard C3 39. Med P3 2. Easy C1 21. Easy A1 40. Med P3 3. Med C1 22. Med

Summary of Questions by Difficulty Level (DL) and Learning Objective (LO) True/False Item DL LO Item DL LO Item DL LO 1. Easy C1 20. Hard C3 39. Med P3 2. Easy C1 21. Easy A1 40. Med P3 3. Med C1 22. Med

SOUTHERN CALIFORNIA PUBLIC POWER AUTHORITY INDEPENDENT AUDITOR S REPORT AND COMBINED FINANCIAL STATEMENTS JUNE 30, 2006 AND 2005

SOUTHERN CALIFORNIA PUBLIC POWER AUTHORITY INDEPENDENT AUDITOR S REPORT AND COMBINED FINANCIAL STATEMENTS JUNE 30, 2006 AND 2005 CONTENTS MANAGEMENT S DISCUSSION AND ANALYSIS 1-22 INDEPENDENT AUDITOR S

SOUTHERN CALIFORNIA PUBLIC POWER AUTHORITY INDEPENDENT AUDITOR S REPORT AND COMBINED FINANCIAL STATEMENTS JUNE 30, 2006 AND 2005 CONTENTS MANAGEMENT S DISCUSSION AND ANALYSIS 1-22 INDEPENDENT AUDITOR S

Sri Lanka Accounting Standard LKAS 37. Provisions, Contingent Liabilities and Contingent Assets

Sri Lanka Accounting Standard LKAS 37 Provisions, Contingent Liabilities and Contingent Assets CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 37 PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS paragraphs

Sri Lanka Accounting Standard LKAS 37 Provisions, Contingent Liabilities and Contingent Assets CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 37 PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS paragraphs

INTERNATIONAL ISOTOPES INC. (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q (Mark One) QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q (Mark One) QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period

Chapter 11 Current Liabilities and Contingencies

Chapter 11 Current Liabilities and Contingencies Chapter 11 Current Liabilities and Contingencies M. Problems P11-1. Suggested solution: Item Liability Financial or non-financial obligation? Explanation

Chapter 11 Current Liabilities and Contingencies Chapter 11 Current Liabilities and Contingencies M. Problems P11-1. Suggested solution: Item Liability Financial or non-financial obligation? Explanation

POLK-BURNETT ELECTRIC COOPERATIVE AND SUBSIDIARIES CENTURIA, WI CONSOLIDATED FINANCIAL STATEMENTS December 31, 2017 and 2016

AND SUBSIDIARIES CENTURIA, WI CONSOLIDATED FINANCIAL STATEMENTS and REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS AND SUBSIDIARIES CENTURIA,WISCONSIN CONTENTS Report of Independent Certified Public

AND SUBSIDIARIES CENTURIA, WI CONSOLIDATED FINANCIAL STATEMENTS and REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS AND SUBSIDIARIES CENTURIA,WISCONSIN CONTENTS Report of Independent Certified Public

1 st FRANKLIN FINANCIAL CORPORATION QUARTERLY REPORT TO INVESTORS AS OF AND FOR THE THREE MONTHS ENDED MARCH 31, 2018

1 st FRANKLIN FINANCIAL CORPORATION QUARTERLY REPORT TO INVESTORS AS OF AND FOR THE THREE MONTHS ENDED MARCH 31, 2018 MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

1 st FRANKLIN FINANCIAL CORPORATION QUARTERLY REPORT TO INVESTORS AS OF AND FOR THE THREE MONTHS ENDED MARCH 31, 2018 MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

HABITAT FOR HUMANITY OF BROWARD, INC.

HABITAT FOR HUMANITY OF BROWARD, INC. Financial Statements and Independent Auditor s Report For the Year Ended June 30, 2018 (With Summarized Comparative Financial Information for the Year Ended June 30,

HABITAT FOR HUMANITY OF BROWARD, INC. Financial Statements and Independent Auditor s Report For the Year Ended June 30, 2018 (With Summarized Comparative Financial Information for the Year Ended June 30,

DRONE USA, INC. AND SUBSIDIARIES Consolidated Financial Statements December 31, (Unaudited)

") Consolidated Financial Statements December 31, 2016 (Unaudited) Table of Contents Page Consolidated Financial Statements Consolidated Balance Sheets F 1 Consolidated Statements of Operations (Unaudited)

Consolidated Financial Statements December 31, 2016 (Unaudited) Table of Contents Page Consolidated Financial Statements Consolidated Balance Sheets F 1 Consolidated Statements of Operations (Unaudited)

MYRTLE BEACH AREA CHAMBER OF COMMERCE AND SUBSIDIARY CONSOLIDATED FINANCIAL STATEMENTS AND ADDITIONAL INFORMATION. Year Ended December 31, 2015

CONSOLIDATED FINANCIAL STATEMENTS AND ADDITIONAL INFORMATION Year Ended December 31, 2015 TABLE OF CONTENTS December 31, 2015 Independent Auditors Report 1 Consolidated Financial Statements Consolidated

CONSOLIDATED FINANCIAL STATEMENTS AND ADDITIONAL INFORMATION Year Ended December 31, 2015 TABLE OF CONTENTS December 31, 2015 Independent Auditors Report 1 Consolidated Financial Statements Consolidated

Cara Operations Limited. Consolidated Financial Statements For the 52 weeks ended December 27, 2015 and December 30, 2014

Consolidated Financial Statements KPMG LLP Chartered Accountants Telephone (416) 777-8500 Bay Adelaide Centre Fax (416) 777-8818 333 Bay Street Suite 4600 Internet www.kpmg.ca Toronto ON M5H 2S5 Canada

Consolidated Financial Statements KPMG LLP Chartered Accountants Telephone (416) 777-8500 Bay Adelaide Centre Fax (416) 777-8818 333 Bay Street Suite 4600 Internet www.kpmg.ca Toronto ON M5H 2S5 Canada

Chapter 11 Current Liabilities and Contingencies

Intermediate Accounting Vol 2 Canadian 3rd Edition Lo Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-vol-2-canadian-3rd-edition-lo-solutions-manual/ Chapter 11

Intermediate Accounting Vol 2 Canadian 3rd Edition Lo Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-vol-2-canadian-3rd-edition-lo-solutions-manual/ Chapter 11

ACCT 652 Accounting. Payroll accounting. Payroll accounting Week 8 Liabilities and Present value

11-1 ACCT 652 Accounting Week 8 Liabilities and Present value Some slides Times Mirror Higher Education Division, Inc. Used by permission 2016, Michael D. Kinsman, Ph.D. 1 1 Payroll accounting I am sure

11-1 ACCT 652 Accounting Week 8 Liabilities and Present value Some slides Times Mirror Higher Education Division, Inc. Used by permission 2016, Michael D. Kinsman, Ph.D. 1 1 Payroll accounting I am sure

AMERICAN INSTITUTE FOR ECONOMIC RESEARCH AND SUBSIDIARY. CONSOLIDATED FINANCIAL STATEMENTS and INDEPENDENT AUDITOR S REPORT

CONSOLIDATED FINANCIAL STATEMENTS and INDEPENDENT AUDITOR S REPORT December 31, 2010 and 2009 CONSOLIDATED FINANCIAL STATEMENTS and INDEPENDENT AUDITOR S REPORT December 31, 2010 and 2009 C O N T E N T

CONSOLIDATED FINANCIAL STATEMENTS and INDEPENDENT AUDITOR S REPORT December 31, 2010 and 2009 CONSOLIDATED FINANCIAL STATEMENTS and INDEPENDENT AUDITOR S REPORT December 31, 2010 and 2009 C O N T E N T

PREVIEW OF CHAPTER 14-2

14-1 PREVIEW OF CHAPTER 14 14-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 14 Non-Current Liabilities LEARNING OBJECTIVES After studying this chapter, you should be able to:

14-1 PREVIEW OF CHAPTER 14 14-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 14 Non-Current Liabilities LEARNING OBJECTIVES After studying this chapter, you should be able to:

HALO COMPANIES, INC. (Exact name of registrant as specified in Charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q [X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q [X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

Combining Financial Statements

Combining Financial Statements Years Ended September 30, 2003 and 2002 Community Power. Statewide Strength. This page intentionally left blank. Combining Financial Statements Years Ended September 30,

Combining Financial Statements Years Ended September 30, 2003 and 2002 Community Power. Statewide Strength. This page intentionally left blank. Combining Financial Statements Years Ended September 30,

1. Advance business transformation. 2. Provide attractive shareholder returns. 3. Increase investment in utility infrastructure

Table 1: PG&E Corporation Business Priorities 2006-2010 1. Advance business transformation 2. Provide attractive shareholder returns 3. Increase investment in utility infrastructure 4. Implement an effective

Table 1: PG&E Corporation Business Priorities 2006-2010 1. Advance business transformation 2. Provide attractive shareholder returns 3. Increase investment in utility infrastructure 4. Implement an effective

DISTRICT 7 FIRE AND RESCUE (A NONPROFIT FIRE DEPARTMENT) FINANCIAL STATEMENTS FOR THE YEAR ENDED SEPTEMBER 30, 2014

FINANCIAL STATEMENTS FOR THE YEAR ENDED SEPTEMBER 30, 2014") (A NONPROFIT FIRE DEPARTMENT) FINANCIAL STATEMENTS FOR THE YEAR ENDED SEPTEMBER 30, 2014 TABLE OF CONTENTS INDEPENDENT AUDITOR S REPORT... 1 STATEMENT OF FINANCIAL POSITION... 3 STATEMENT OF ACTIVITIES...

(A NONPROFIT FIRE DEPARTMENT) FINANCIAL STATEMENTS FOR THE YEAR ENDED SEPTEMBER 30, 2014 TABLE OF CONTENTS INDEPENDENT AUDITOR S REPORT... 1 STATEMENT OF FINANCIAL POSITION... 3 STATEMENT OF ACTIVITIES...