|

|

|

- Ariel Poole

- 5 years ago

- Views:

Transcription

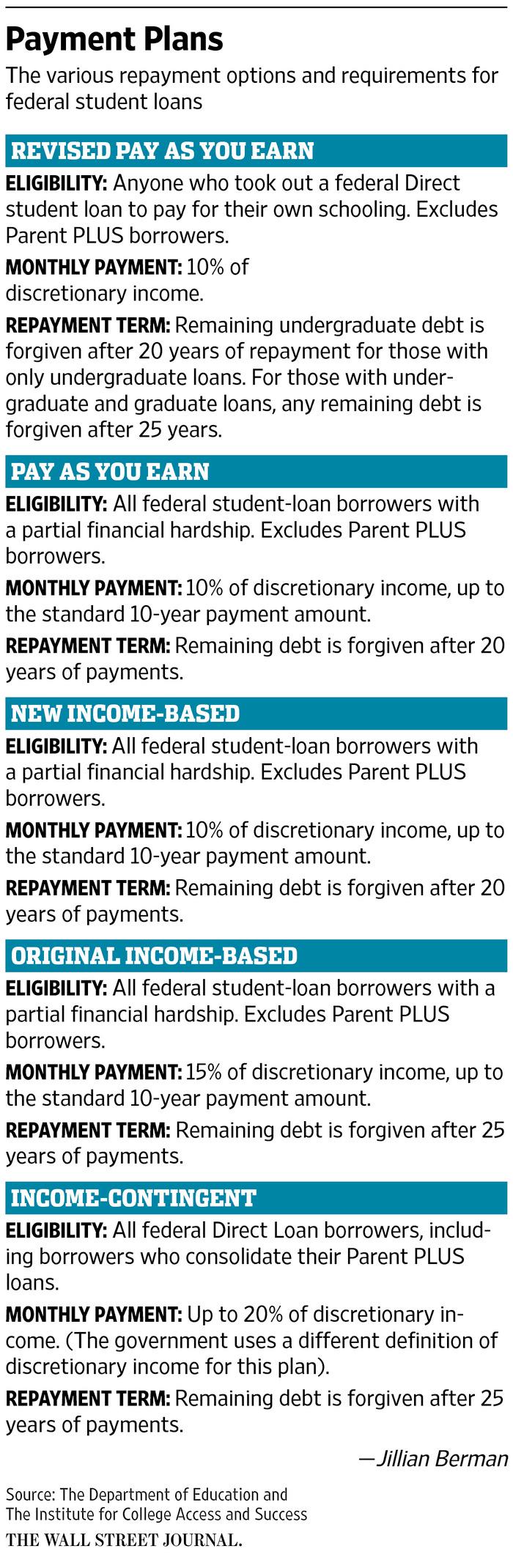

1 Six Common Mistakes People Make With Their Student Loans By Anne Tergesen WSJ print Sept 12, 2016 As millennials struggle to repay record levels of student-loan debt, many are making costly mistakes that threaten to undermine their long-term financial security. For instance, roughly one in four is behind on repayments or in default, which can result in a host of negative consequences, from damaged credit to garnished wages. Meanwhile, many others are struggling to find enough money, after making their loan payments, to save for retirement. Among 401(k) participants with student debt in plans administered by Fidelity Investments, two-thirds say they have reduced or stopped their 401(k) contributions or have taken out a 401(k) loan or hardship withdrawal. With total college-loan debt in the U.S. more than five times what it was just 20 years ago, the consequences of managing that debt have never been greater, says Heather Jarvis, an attorney who teaches financial professionals about student loans. What follows are six student-loan mistakes people commonly make and how you can avoid them. MISTAKE NO. 1: Failing to consider income-driven repayment plans When it comes to government-backed student loans, many people stick with a standard repayment plan. This default option requires the borrower to make fixed monthly payments for up to 10 years an approach that often minimizes the interest the borrower will pay over the life of the loan, in comparison to other payment plans, but maximizes monthly payments. Some borrowers particularly those who are cash-strapped may benefit from an income-driven repayment plan. These plans, the newest of which became available last year, cap student-loan repayments at 10% to 15% of a borrower s annual discretionary income an amount that is determined by a formula that includes the borrower s income and family size, among other factors. Using one, a borrower can free up cash for other long-term financial goals, such as saving for retirement.

2

3 They also offer the possibility of loan forgiveness after a set number of years of on-time repayments from 10 to 25 years, depending on the plan and the borrower s profession. More on that in Mistake No. 3. For those looking to reduce their monthly payments, these options generally are more attractive than older alternatives, including graduated and extended plans, says Ms. Jarvis. Graduated plans start with lower payments that increase every two years and eventually surpass the standard fixed payment. Extended plans lower monthly payments by allowing up to 25 years for repayment. Borrowers whose debt is two-thirds of their income or more are likely to qualify for at least some of the various income-driven repayment plans, says Mark Kantrowitz, a financial-aid expert and the publisher of Cappex.com, a college scholarship and search site. But those who can benefit the most from these plans generally have debt in excess of their income a threshold at which borrowers are likely to eventually see some of their loan balances forgiven, says Ms. Jarvis. MISTAKE NO. 2: Failing to understand the loans There are two basic types of student loans: federal and private. Interest rates on federal loans are set annually by a formula based on the yield of the 10-year Treasury note. With private loans, banks set interest rates using a borrower s credit history. To understand their repayment options, it s important for borrowers to compile a list of their loans, including the loan type, principal amount and interest rate. Lenders should have the details or, for federal loans, borrowers can go to the National Student Loan Data System at nslds.ed.gov. Why bother? For one thing, borrowers need to know the interest rates on their loans to figure out whether it makes sense to refinance or consolidate what they owe. (With refinancing, a borrower takes out a new private loan to pay off some or all of his or her existing loans, typically at a lower interest rate. With consolidation, the borrower combines some or all existing federal loans at the weighted average interest rate on the old loans. See more on these options in Mistake No. 5.) In addition, to understand which income-driven repayment options borrowers are eligible for, they ll need to know the dates when they borrowed. For example, to use the popular Pay As You Earn (PAYE) method an income-driven plan that frequently generates the lowest monthly payments and the highest projected loan

4 forgiveness a borrower can t have borrowed before Oct. 1, 2007 and must have taken out at least one federal loan on or after Oct. 1, To see what monthly and total payments would be under the various repayment options, borrowers can plug their loan information into the U.S. Education Department s online Repayment Estimator. Among other things, this tool assumes income will rise 5% a year. If borrowers want to control that and other inputs such as the number of children they plan to have and information about their spouse they can use the Student Loan Repayment Simulator sponsored by the nonprofit VIN Foundation for veterinarians. For advice, a borrower might consider hiring a financial planner. The XY Planning Network consists of some 290 financial advisers who cater to younger clients. Some have expertise in student loans and charge hourly or project-based fees. Beware of companies that charge an upfront fee to help student-loan borrowers obtain debt relief, says Ms. Jarvis, adding that some are scams. MISTAKE NO. 3: Failing to research student-loan forgiveness programs Some employers including the U.S. military, PricewaterhouseCoopers and Fidelity Investments contribute to employees student-loan payments. Borrowers with federal loans who use income-driven repayment plans may also receive partial loan forgiveness. Under the Federal government s Public Service Loan Forgiveness program, teachers, law-enforcement employees, doctors, lawyers and others who work full-time for 10 years for certain types of nonprofits or government are eligible to have their remaining balances forgiven tax-free after 10 years of payments. To ensure they will receive loan forgiveness, they should use an income-driven repayment plan. For those not in public-service jobs, loan forgiveness is less generous. To qualify, these borrowers must repay their loans for 20 to 25 years the exact term depends on which income-driven repayment plan they select. In addition, they must pay income tax on any debt that is canceled a payment that can amount to as much as one-third or more of the forgiven amount. MISTAKE NO. 4: Prioritizing student loans at the expense of retirement savings In a push to become debt-free, many borrowers prioritize paying off their student loans over saving for retirement.

5 That s a mistake. A recent report from Morningstar Inc. subsidiary HelloWallet found that someone with a starting salary of $50,000 who pays off a $20,000 student loan ahead of schedule but skimps on retirement savings by contributing only enough to an employer-sponsored 401(k) plan to receive half the employer s 3% matching contribution will wind up with a net worth at age 65 that s $150,000 below where it would have been had he or she contributed enough to receive the full match and repaid the loan over a longer period, by making the minimum required payment. The match is free money, says Marcio Silveira, a financial adviser in Arlington, Va. If a company offers a 50-cent match for every dollar an employee contributes to a 401(k) plan up to 6% of pay, it s a 50% return on your money, he says. That s far higher than the return on paying off a student loan, which is equivalent to the loan s interest rate. If payments under a 10-year standard repayment plan leave a borrower too cashstrapped to get an employer s full matching contribution and the employee doesn t have room to cut spending, he or she might consider an income-driven repayment plan, says Jake Spiegel, a senior research analyst at HelloWallet. His advice: Borrowers should use the cash they free up to set aside at least three months of expenses in an emergency fund. Then, they can save enough in their 401(k) plan to receive their employer s full matching contribution. Their next priority should be to pay down any high-interest credit-card debt they owe. And if choosing an income-driven plan means they re likely to incur a tax on debt forgiveness, they should save a little each month to cover the projected tab. Anything left over should go into a retirement plan, says Mr. Spiegel. Why? People are likely to earn a higher return in stocks and bonds that will compound for decades than they would by extinguishing student-loan debt at today s low interest rates, he says. In addition, the more a person contributes to a traditional 401(k) plan, the lower his or her adjusted gross income will be. This will help reduce income-driven student-loan payments the next year, says Daniel Wrenne, a financial adviser in Lexington, Ky. MISTAKE NO. 5: Automatically refinancing or consolidating If people with student loans have private loans with high interest rates, they should look into refinancing. Online lenders including Social Finance Inc., CommonBond Inc., and First Republic Bank frequently offer attractive deals to those with healthy credit scores and good prospects for future earnings, among other factors, says Mr. Wrenne.

6 Borrowers can refinance their federal loans, too, but they should be careful, weighing any interest-rate reduction they receive against the benefits they ll lose by swapping their federal loans for private loans. These include the flexibility to suspend their payments if they become unemployed or to use an income-driven repayment plan. The decision to consolidate also requires analysis. Consolidation makes it easier to keep track of and repay student debt. It also allows borrowers to swap loans issued under the discontinued Federal Family Education Loan program for a new Federal Direct loan a prerequisite to using certain income-driven repayment plans. But borrowers who consolidate all their loans lose the flexibility to pay off the ones with the highest interest rates first. Borrowers who want to maintain that flexibility don t have to consolidate all of their loans, says Ms. Jarvis. MISTAKE NO. 6: Failing to automate payments To ensure they won t be late with their loan payments a misstep that can wreak havoc with credit scores and push back the date at which one becomes eligible for debt forgiveness borrowers should automate all of their loan payments. Many lenders offer those who do so a reduction of a quarter to half a percentage point in their interest rates, says Mr. Kantrowitz. Advisers suggest that people automate their savings, too, including contributions to 401(k) plans and emergency savings. If they are in an income-driven repayment plan that will generate a tax bill on forgiven debt, they should start saving for that, as well. To keep tax savings on track, Alan Moore, a financial planner in Nashville, Tenn., suggests segregating this money in a separate investment account. If you don t save enough money for the tax bill, all you are accomplishing is swapping your student-loan debt for a debt to the IRS, he says, adding that savings earmarked for the tax payment shouldn t be invested too heavily in stocks due to the risk of a bear market. Ms. Tergesen is a Wall Street Journal reporter in New York.

PLAIN LANGUAGE DISCLOSURE FOR DIRECT SUBSIDIZED LOANS AND DIRECT UNSUBSIDIZED LOANS WILLIAM D. FORD FEDERAL DIRECT LOAN PROGRAM

1. GENERAL INFORMATION You are receiving a Direct Subsidized Loan and/or Direct Unsubsidized Loan under a Master Promissory Note (MPN) that you signed previously (see Item 2). This Plain Language Disclosure

1. GENERAL INFORMATION You are receiving a Direct Subsidized Loan and/or Direct Unsubsidized Loan under a Master Promissory Note (MPN) that you signed previously (see Item 2). This Plain Language Disclosure

Repaying your federal student loans

Repaying your federal student loans Many borrowers don t worry about their student loans until they graduate or leave school. But you should immediately notify your loan servicer and school in writing

Repaying your federal student loans Many borrowers don t worry about their student loans until they graduate or leave school. But you should immediately notify your loan servicer and school in writing

Student Loan Ombudsman Caucus

Student Loan Ombudsman Caucus Repayment Plans Selecting the right repayment plan is important in the successful management of your student loan. You can change repayment plans contact your lender/servicer

Student Loan Ombudsman Caucus Repayment Plans Selecting the right repayment plan is important in the successful management of your student loan. You can change repayment plans contact your lender/servicer

Student Loan Repayment Workshop. Amanda Seitz Direct Loan Coordinator - Student Financial Services

Student Loan Repayment Workshop Amanda Seitz Direct Loan Coordinator - Student Financial Services Amanda.seitz@purchase.edu (914) 251-6080 Types of Student Loans Subsidized Direct Loan fixed interest loan

Student Loan Repayment Workshop Amanda Seitz Direct Loan Coordinator - Student Financial Services Amanda.seitz@purchase.edu (914) 251-6080 Types of Student Loans Subsidized Direct Loan fixed interest loan

THE ROAD TO ZERO. A Strategic Approach to Student Loan Repayment. Financial education resources from a nonprofit you can trust. AccessLex.

THE ROAD TO ZERO A Strategic Approach to Student Loan Repayment Financial education resources from a nonprofit you can trust. AccessLex.org 1 GET STARTED. 3 KNOW WHAT YOU OWE. 4 KNOW YOUR OPTIONS. 6 Debt-Driven

THE ROAD TO ZERO A Strategic Approach to Student Loan Repayment Financial education resources from a nonprofit you can trust. AccessLex.org 1 GET STARTED. 3 KNOW WHAT YOU OWE. 4 KNOW YOUR OPTIONS. 6 Debt-Driven

Student loans: there s more than one way to repay

Student loans: there s more than one way to repay Repayment options 1 Consolidation If you have multiple federal student loans, you may be interested in a Direct Consolidation Loan to simplify loan repayment.

Student loans: there s more than one way to repay Repayment options 1 Consolidation If you have multiple federal student loans, you may be interested in a Direct Consolidation Loan to simplify loan repayment.

Federal Student Loan Repayment Do s & Don ts

Federal Student Loan Repayment Do s & Don ts College graduates with Federal student loans have a number of repayment options at their disposal. This guide will walk you through your options so you can

Federal Student Loan Repayment Do s & Don ts College graduates with Federal student loans have a number of repayment options at their disposal. This guide will walk you through your options so you can

1040 Form: The standard Internal Revenue Service (IRS) form that individuals use. to file their annual income tax returns.

form that individuals use. to file their annual income tax returns.") 1040 Form: The standard Internal Revenue Service (IRS) form that individuals use to file their annual income tax returns. 1040A Form: A simplified version of the 1040 form for individual income tax. To

1040 Form: The standard Internal Revenue Service (IRS) form that individuals use to file their annual income tax returns. 1040A Form: A simplified version of the 1040 form for individual income tax. To

STUDENT LOAN REPAYMENT. Leslie Tobakos Registrar, Financial Aid & Admissions Manager Cranbrook Academy of Art

STUDENT LOAN REPAYMENT Leslie Tobakos Registrar, Financial Aid & Admissions Manager Cranbrook Academy of Art In this world nothing can be said to be certain, except death and taxes. Benjamin Franklin,

STUDENT LOAN REPAYMENT Leslie Tobakos Registrar, Financial Aid & Admissions Manager Cranbrook Academy of Art In this world nothing can be said to be certain, except death and taxes. Benjamin Franklin,

Conquering student loan debt

Conquering student loan debt Financial wellness education series FINANCIAL LITERACY EDUCATION PROGRAMS [Name of presenter] [Title of presenter] Agenda 1 The student loan crisis 2 Managing student loan

Conquering student loan debt Financial wellness education series FINANCIAL LITERACY EDUCATION PROGRAMS [Name of presenter] [Title of presenter] Agenda 1 The student loan crisis 2 Managing student loan

Private Loan Guide. Apply for free, federal and state financial aid programs:

Private loan basics Private student loans are non-federal loans. Private Loan Guide You should only borrow private loans to fund your education as a last resort. Do all of the following before you consider

Private loan basics Private student loans are non-federal loans. Private Loan Guide You should only borrow private loans to fund your education as a last resort. Do all of the following before you consider

Exit Counseling M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES

Exit Counseling FALL 2017 M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES Agenda Loan types and interest rates Grace periods Repaying

Exit Counseling FALL 2017 M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES Agenda Loan types and interest rates Grace periods Repaying

Federal Student Aid. Direct Loan. Entrance Counseling Guide

2018 Federal Student Aid Direct Loan Entrance Counseling Guide U.S. Department of Education Betsy DeVos Secretary Federal Student Aid James Manning Acting Chief Operating Officer Federal Student Aid, an

2018 Federal Student Aid Direct Loan Entrance Counseling Guide U.S. Department of Education Betsy DeVos Secretary Federal Student Aid James Manning Acting Chief Operating Officer Federal Student Aid, an

Exit Counseling M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES

Exit Counseling SPRING 2018 M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES Agenda Loan types and interest rates Grace periods

Exit Counseling SPRING 2018 M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES Agenda Loan types and interest rates Grace periods

Should Physicians REPAYE?

Should Physicians REPAYE? [Editor s Note: This is a guest post from blog advertiser and student loan expert Jan Miller, President of Student Loan Consultant. He offers fee-only advice about your student

Should Physicians REPAYE? [Editor s Note: This is a guest post from blog advertiser and student loan expert Jan Miller, President of Student Loan Consultant. He offers fee-only advice about your student

William D. Ford Federal Direct Loan Program Direct Subsidized Loan and Direct Unsubsidized Loan Borrower s Rights and Responsibilities Statement

Important Notice: This Borrower s Rights and Responsibilities Statement provides additional information about the terms and conditions of the loans you receive under the accompanying Master Promissory

Important Notice: This Borrower s Rights and Responsibilities Statement provides additional information about the terms and conditions of the loans you receive under the accompanying Master Promissory

Please Check In and Pick Up Your Folder. Exit Counseling Folder

Exit Counseling Please Check In and Pick Up Your Folder Exit Counseling Folder Personalized federal student loan balances Letter from our office and bookmark Loan Servicer information Loan Tips and Resources

Exit Counseling Please Check In and Pick Up Your Folder Exit Counseling Folder Personalized federal student loan balances Letter from our office and bookmark Loan Servicer information Loan Tips and Resources

Direct Loan Exit Counseling Guide

2018 Federal Student Aid Direct Loan Exit Counseling Guide For Borrowers of Direct Loans and Federal Family Education Program Loans U.S. Department of Education Betsy DeVos Secretary Federal Student Aid

2018 Federal Student Aid Direct Loan Exit Counseling Guide For Borrowers of Direct Loans and Federal Family Education Program Loans U.S. Department of Education Betsy DeVos Secretary Federal Student Aid

Federal Student Loan Repayment

Federal Student Loan Repayment The Road to Zero Know your financial goals. Know what you owe. Know what time it is. Know your options. Select your plan. Manage your payments. AccessGroup.org Financial

Federal Student Loan Repayment The Road to Zero Know your financial goals. Know what you owe. Know what time it is. Know your options. Select your plan. Manage your payments. AccessGroup.org Financial

623 POLICY Federal Direct Loans/Plus Statement of Policy

623 POLICY Federal Direct /Plus 623.1 Statement of Policy The Redlands Community College Financial Aid Office participates in Loan Programs to assist students with financial loans during their enrollment

623 POLICY Federal Direct /Plus 623.1 Statement of Policy The Redlands Community College Financial Aid Office participates in Loan Programs to assist students with financial loans during their enrollment

Warm-Up 2/12/16. If you make $8.25/hour, work an average of 25 hours per week, and lose 20% to taxes, what is your annual NET pay?

Warm-Up 2/12/16 If you make $8.25/hour, work an average of 25 hours per week, and lose 20% to taxes, what is your annual NET pay? If you are paid a salary of $40,900 and lose 20% to taxes, what is your

Warm-Up 2/12/16 If you make $8.25/hour, work an average of 25 hours per week, and lose 20% to taxes, what is your annual NET pay? If you are paid a salary of $40,900 and lose 20% to taxes, what is your

About Salt Money Management Student Loan Repayment

About Salt Money Management Student Loan Repayment Michele Almeida Senior Associate Director of SFS Jane Aube Loan Programs & Compliance Specialist Kim Downs-Burns AVP Student Financial Services American

About Salt Money Management Student Loan Repayment Michele Almeida Senior Associate Director of SFS Jane Aube Loan Programs & Compliance Specialist Kim Downs-Burns AVP Student Financial Services American

TICAS Proposal to Create One Improved Income-Driven Repayment Plan

TICAS Proposal to Create One Improved Income-Driven Repayment Plan All federal student loan borrowers should be able to choose the assurance of manageable payments and forgiveness after 20 years of payments.

TICAS Proposal to Create One Improved Income-Driven Repayment Plan All federal student loan borrowers should be able to choose the assurance of manageable payments and forgiveness after 20 years of payments.

That means the average cost for just one four-year degree will be $132,000

With the cost of tuition constantly going up these days, it is a rarity that I speak to a recent graduate who is not in student loan debt of some kind. In fact, the most recent statistics show that over

With the cost of tuition constantly going up these days, it is a rarity that I speak to a recent graduate who is not in student loan debt of some kind. In fact, the most recent statistics show that over

Maximizing The Benefits Of Loan Repayment Assistance And Forgiveness Programs

Maximizing The Benefits Of Loan Repayment Assistance And Forgiveness Programs Kelly Carmody, Carmody and Associates, Phoenix, AZ Heather Wells Jarvis, Equal Justice Works, Washington, DC Don Saunders,

Maximizing The Benefits Of Loan Repayment Assistance And Forgiveness Programs Kelly Carmody, Carmody and Associates, Phoenix, AZ Heather Wells Jarvis, Equal Justice Works, Washington, DC Don Saunders,

Student Loan Repayment. Health Sciences Financial Aid Office May 17 th, 2018

Student Loan Repayment Health Sciences Financial Aid Office May 17 th, 2018 TOPICS KNOW YOUR LOAN PORTFOLIO HOW TO POSTPONE PAYMENTS REPAYMENT PLANS OTHER CONSIDERATIONS CREDIT QUESTIONS KNOW YOUR LOAN

Student Loan Repayment Health Sciences Financial Aid Office May 17 th, 2018 TOPICS KNOW YOUR LOAN PORTFOLIO HOW TO POSTPONE PAYMENTS REPAYMENT PLANS OTHER CONSIDERATIONS CREDIT QUESTIONS KNOW YOUR LOAN

Partial Financial Hardship 8/11/2014. Disadvantages of income-driven plans. Interest and capitalization benefits accompany the income-driven plans

Income-Driven Plan Payment Amount Comprehensive Student Loan Training Series Income-Contingent The lesser of: 20 percent of discretionary income, or what borrower would pay on a fixed payment over the

Income-Driven Plan Payment Amount Comprehensive Student Loan Training Series Income-Contingent The lesser of: 20 percent of discretionary income, or what borrower would pay on a fixed payment over the

4/4/2018 MANAGING STUDENT LOAN REPAYMENT FOR GRADUATING SENIORS

MANAGING STUDENT LOAN REPAYMENT FOR GRADUATING SENIORS MASSACHUSETTS EDUCATIONAL FINANCING AUTHORITY About MEFA Not-for-profit state authority created in 1982 Helping families plan, save, and pay for college

MANAGING STUDENT LOAN REPAYMENT FOR GRADUATING SENIORS MASSACHUSETTS EDUCATIONAL FINANCING AUTHORITY About MEFA Not-for-profit state authority created in 1982 Helping families plan, save, and pay for college

January-June 2019 Loan Application and Information

January-June 2019 Loan Application and Information Introduction The Loan Repayment Assistance Program of Minnesota ( LRAP or LRAP MN ) exists to support recent law graduates in choosing employment in the

January-June 2019 Loan Application and Information Introduction The Loan Repayment Assistance Program of Minnesota ( LRAP or LRAP MN ) exists to support recent law graduates in choosing employment in the

College Numbers Planning

College Numbers Planning Today s Plan What s new in financial aid and student borrowing What s the deal with student loan interest rates How to use consolidation (and how not to) Comparing repayment options

College Numbers Planning Today s Plan What s new in financial aid and student borrowing What s the deal with student loan interest rates How to use consolidation (and how not to) Comparing repayment options

c» BALANCE C:» Financially Empowering You Repaying Student Loans Podcast [Music plays] Nikki:

![c» BALANCE C:» Financially Empowering You Repaying Student Loans Podcast [Music plays] Nikki:](/thumbs/77/76062165.jpg "c» BALANCE C:» Financially Empowering You Repaying Student Loans Podcast [Music plays] Nikki:") Repaying Student Loans Podcast [Music plays] Nikki: You re listening to Repaying student loans. Hi. I m Nicky, your host for today s podcast. If you re intimidated by the prospect of paying back a student

Repaying Student Loans Podcast [Music plays] Nikki: You re listening to Repaying student loans. Hi. I m Nicky, your host for today s podcast. If you re intimidated by the prospect of paying back a student

STATE OF NEW JERSEY STUDENT LOAN GUIDE

STATE OF NEW JERSEY STUDENT LOAN GUIDE New Jersey Higher Education Student Assistance Authority The Student Loan Guide provides general student loan information to assist students and their families in

STATE OF NEW JERSEY STUDENT LOAN GUIDE New Jersey Higher Education Student Assistance Authority The Student Loan Guide provides general student loan information to assist students and their families in

SUNY Downstate. Medical Students guide to student loans. The Financial Aid Office 2017

SUNY Downstate Medical Students guide to student loans The Financial Aid Office 2017 Quick thoughts about repayment 1) Be organized and pay attention to the details of your loans. 2) Set a monthly budget

SUNY Downstate Medical Students guide to student loans The Financial Aid Office 2017 Quick thoughts about repayment 1) Be organized and pay attention to the details of your loans. 2) Set a monthly budget

Navigating Student Loan Repayment

Navigating Student Loan Repayment Objectives The goal of this presentation is to prepare you for student loan repayment, to encourage healthy financial habits, and to connect you with resources to help

Navigating Student Loan Repayment Objectives The goal of this presentation is to prepare you for student loan repayment, to encourage healthy financial habits, and to connect you with resources to help

Sign in & click on Complete Counseling Select Exit Counseling

www.studentloans.gov Sign in & click on Complete Counseling Select Exit Counseling Required Withdraw Graduate Enrollment drops below half-time Transfer to another school This counseling session covers

www.studentloans.gov Sign in & click on Complete Counseling Select Exit Counseling Required Withdraw Graduate Enrollment drops below half-time Transfer to another school This counseling session covers

NORTHERN CALIFORNIA CARPENTERS 401(K) PLAN

PLAN") NORTHERN CALIFORNIA CARPENTERS 401(k) PLAN ANNOUNCING THE NEWLY ESTABLISHED NORTHERN CALIFORNIA CARPENTERS 401(K) PLAN IMPORTANT INFORMATION IRS SAFE HARBOR PLAN NOTICE NORTHERN CALIFORNIA CARPENTERS 401(K)

NORTHERN CALIFORNIA CARPENTERS 401(k) PLAN ANNOUNCING THE NEWLY ESTABLISHED NORTHERN CALIFORNIA CARPENTERS 401(K) PLAN IMPORTANT INFORMATION IRS SAFE HARBOR PLAN NOTICE NORTHERN CALIFORNIA CARPENTERS 401(K)

Between 2004 and 2014, the total student debt in the US tripled from $364 billion in 2004 to $1.16 trillion in 2014.

1 Statistic s from the Federal Reserve Bank of New York February 2015 Between 2004 and 2014, the total student debt in the US tripled from $364 billion in 2004 to $1.16 trillion in 2014. Our research indicates

1 Statistic s from the Federal Reserve Bank of New York February 2015 Between 2004 and 2014, the total student debt in the US tripled from $364 billion in 2004 to $1.16 trillion in 2014. Our research indicates

Student Loans & Service Members

PF SMS icons PF SMS icons Student Loans & Service Members https://learn.extension.org/events/3014 This material is based upon work supported by the National Institute of Food and Agriculture, U.S. Department

PF SMS icons PF SMS icons Student Loans & Service Members https://learn.extension.org/events/3014 This material is based upon work supported by the National Institute of Food and Agriculture, U.S. Department

Welcome to Student Loan Repayment Strategies

Welcome to Student Loan Repayment Strategies Kathy Sweedler Consumer Economics Educator University of Illinois Extension sweedler@illinois.edu 1 Make Plan: Take Action Where are you now? Evaluate repayment

Welcome to Student Loan Repayment Strategies Kathy Sweedler Consumer Economics Educator University of Illinois Extension sweedler@illinois.edu 1 Make Plan: Take Action Where are you now? Evaluate repayment

Student Loan Repayment

Student Loan Repayment LIKE US ON FACEBOOK: FAME Education for weekly scholarship and financial aid information Copyright 2017 Finance Authority of Maine Welcome Nikki Vachon College Access Counselor Agenda

Student Loan Repayment LIKE US ON FACEBOOK: FAME Education for weekly scholarship and financial aid information Copyright 2017 Finance Authority of Maine Welcome Nikki Vachon College Access Counselor Agenda

REPAYING STUDENT LOANS

REPAYING STUDENT LOANS 1 It is not unusual for college tuition to cost $30,000 or more a year. Some students are able to pay for it with savings or get grants or scholarships. However, many have to turn

REPAYING STUDENT LOANS 1 It is not unusual for college tuition to cost $30,000 or more a year. Some students are able to pay for it with savings or get grants or scholarships. However, many have to turn

Meet The Speakers. Sasha Grabenstetter, AFC Consumer Economics Educator University of Illinois Extension

Welcome to 1 Meet The Speakers Sasha Grabenstetter, AFC Consumer Economics Educator University of Illinois Extension Andrea Pellegrini Assistant Director Student Money Management Center 2 Where are you

Welcome to 1 Meet The Speakers Sasha Grabenstetter, AFC Consumer Economics Educator University of Illinois Extension Andrea Pellegrini Assistant Director Student Money Management Center 2 Where are you

c» BALANCE c» Financially Empowering You Credit Matters Podcast

Credit Matters Podcast [Music plays] Nikki: You re listening to Credit Matters. Hi. I m Nikki, your host for today s podcast. In today s world credit does matter. In fact, getting and using credit is part

Credit Matters Podcast [Music plays] Nikki: You re listening to Credit Matters. Hi. I m Nikki, your host for today s podcast. In today s world credit does matter. In fact, getting and using credit is part

Student Loan Terms to Know

Definitions of terms related to federal student loans and the Nelnet repayment process Accrue The act of interest accumulating on the borrower s principal balance Adjusted Gross Income (AGI) The adjusted

Definitions of terms related to federal student loans and the Nelnet repayment process Accrue The act of interest accumulating on the borrower s principal balance Adjusted Gross Income (AGI) The adjusted

Student Loan - Know Before You Owe Questions & Answers Prepared by: The Counselor s Corner, Inc. April 25, 2018

Question: I'm interested on Student Loans, but for a Master s degree. Will this series of webinars provide information about this? Answer: Yes, we will provide a limited amount of information on Federal

Question: I'm interested on Student Loans, but for a Master s degree. Will this series of webinars provide information about this? Answer: Yes, we will provide a limited amount of information on Federal

What is an income-driven repayment plan?

Income-Driven Plans for Federal Student Loans What is an income-driven repayment plan? An income-driven repayment plan is a repayment plan that sets your monthly student loan payment at an amount that

Income-Driven Plans for Federal Student Loans What is an income-driven repayment plan? An income-driven repayment plan is a repayment plan that sets your monthly student loan payment at an amount that

THE DISTRICT OF COLUMBIA BAR FOUNDATION

THE DISTRICT OF COLUMBIA BAR FOUNDATION FUNDING LEGAL SERVICES FOR THOSE IN NEED DC BAR FOUNDATION LOAN REPAYMENT ASSISTANCE PROGRAMS Do I have to work in DC? FREQUENTLY ASKED QUESTIONS Yes. You must be

THE DISTRICT OF COLUMBIA BAR FOUNDATION FUNDING LEGAL SERVICES FOR THOSE IN NEED DC BAR FOUNDATION LOAN REPAYMENT ASSISTANCE PROGRAMS Do I have to work in DC? FREQUENTLY ASKED QUESTIONS Yes. You must be

Ten Things You Should Know About Student Loans

Ten Things You Should Know About Student Loans 1: BORROW ONLY WHAT YOU NEED 4: UNDERSTAND YOUR LOANS There are several different kinds of loans. Here are some key factors to be aware of: 7: MAKE PAYMENTS

Ten Things You Should Know About Student Loans 1: BORROW ONLY WHAT YOU NEED 4: UNDERSTAND YOUR LOANS There are several different kinds of loans. Here are some key factors to be aware of: 7: MAKE PAYMENTS

Sign in using your FSA ID & click on Complete Counseling Select Exit Counseling

Please Check In www.studentloans.gov Sign in using your FSA ID & click on Complete Counseling Select Exit Counseling Required Withdraw Graduate Enrollment drops below half-time Transfer to another school

Please Check In www.studentloans.gov Sign in using your FSA ID & click on Complete Counseling Select Exit Counseling Required Withdraw Graduate Enrollment drops below half-time Transfer to another school

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS U.S. Department of Education Arne Duncan Secretary Federal Student Aid James W. Runcie Chief Operating Officer

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS U.S. Department of Education Arne Duncan Secretary Federal Student Aid James W. Runcie Chief Operating Officer

How to Get Ahead of Your Student Debt

Client Conversations How to Get Ahead of Your Student Debt WHEN COLLEGE ENDS, YOU RE LEFT WITH A DIPLOMA AND A SENSE OF ACCOMPLISHMENT but you re also probably left with some pretty hefty debt and subsequent

Client Conversations How to Get Ahead of Your Student Debt WHEN COLLEGE ENDS, YOU RE LEFT WITH A DIPLOMA AND A SENSE OF ACCOMPLISHMENT but you re also probably left with some pretty hefty debt and subsequent

Public Service Loan Forgiveness & Beyond: The Changing Landscape of Educational Debt Relief

Public Service Loan Forgiveness & Beyond: The Changing Landscape of Educational Debt Relief Heather Jarvis, AskHeatherJarvis.com, Wilmington, NC. Radhika Singh Miller, Equal Justice Works, Washington,

Public Service Loan Forgiveness & Beyond: The Changing Landscape of Educational Debt Relief Heather Jarvis, AskHeatherJarvis.com, Wilmington, NC. Radhika Singh Miller, Equal Justice Works, Washington,

Understanding and Managing your Student Loans and Repayment

Understanding and Managing your Student Loans and Financial Literacy Programs University of Colorado Denver Presenter: M. Lesa Briggs Financial Literacy & Wellness After this presentation, you will be

Understanding and Managing your Student Loans and Financial Literacy Programs University of Colorado Denver Presenter: M. Lesa Briggs Financial Literacy & Wellness After this presentation, you will be

Documeent title on one or two. during the 2013 IRA season

Documeent title on one or two Tax lines savings Gustan opportunities Book 24pt during the 2013 IRA season The IRA season, from January 1 through April 15, may offer you opportunities to cut taxes and enhance

Documeent title on one or two Tax lines savings Gustan opportunities Book 24pt during the 2013 IRA season The IRA season, from January 1 through April 15, may offer you opportunities to cut taxes and enhance

How U.S. Universities Spend Money Paying for college

Student Loans (UXL) Student loan debt has risen alarmingly in the last several years. (Student loans are loans that help students pay for college tuition, books, and living expenses.) Going to college

Student Loans (UXL) Student loan debt has risen alarmingly in the last several years. (Student loans are loans that help students pay for college tuition, books, and living expenses.) Going to college

July 1, 2019 June 30, 2020 Loan Application Information and Instructions

P July 1, 2019 June 30, 2020 Loan Application Information and Instructions Introduction LRAP Minnesota helps reduce the education debt burden experienced by dedicated public interest lawyers who represent

P July 1, 2019 June 30, 2020 Loan Application Information and Instructions Introduction LRAP Minnesota helps reduce the education debt burden experienced by dedicated public interest lawyers who represent

SEVEN LIFE-DEFINING FINANCIAL DECISIONS

SEVEN LIFE-DEFINING FINANCIAL DECISIONS A Joint Project of The Actuarial Foundation and WISER, the Women's Institute for a Secure Retirement 4 HOME OWNERSHIP, DEBT, AND CREDIT Buying a home is one of the

SEVEN LIFE-DEFINING FINANCIAL DECISIONS A Joint Project of The Actuarial Foundation and WISER, the Women's Institute for a Secure Retirement 4 HOME OWNERSHIP, DEBT, AND CREDIT Buying a home is one of the

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS U.S. Department of Education Betsy DeVos Secretary Federal Student Aid A. Wayne Johnson Chief Operating Officer

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS U.S. Department of Education Betsy DeVos Secretary Federal Student Aid A. Wayne Johnson Chief Operating Officer

Money 101 Presenter s Guide

For College Students Money 101 Presenter s Guide A Crash Course in Better Money Management For College Students Getting Started The What s My Score Money 101 presentation features six topics that should

For College Students Money 101 Presenter s Guide A Crash Course in Better Money Management For College Students Getting Started The What s My Score Money 101 presentation features six topics that should

Direct Loan: Post-Graduation

Direct Loan: Post-Graduation Direct Loan Repayment Glossary: Before we begin Principal: The actual dollar figure of the amount borrowed Interest: Periodic fee charged to borrower; usually a percentage

Direct Loan: Post-Graduation Direct Loan Repayment Glossary: Before we begin Principal: The actual dollar figure of the amount borrowed Interest: Periodic fee charged to borrower; usually a percentage

A Guide to Student Loan Refinancing. Practical repayment information for everyone (with special tips for medical professionals)

") A Guide to Student Loan Refinancing Practical repayment information for everyone (with special tips for medical professionals) For years student loan borrowers have felt stuck, with limited options to

A Guide to Student Loan Refinancing Practical repayment information for everyone (with special tips for medical professionals) For years student loan borrowers have felt stuck, with limited options to

Student Loans. Paying for college without taking out loans is ideal, but sometimes you need a loan to cover all the costs.

student loans 1 Student Loans Paying for college without taking out loans is ideal, but sometimes you need a loan to cover all the costs. At CAPlus, we recommend the following student loan resources (in

student loans 1 Student Loans Paying for college without taking out loans is ideal, but sometimes you need a loan to cover all the costs. At CAPlus, we recommend the following student loan resources (in

Two s a Crowd: Are Retirement Savings Being Crowded Out by Student Loans?

Two s a Crowd: Are Retirement Savings Being Crowded Out by Student Loans? Scott Cooley Director of Policy Research, Morningstar Jake Spiegel Senior Research Analyst, HelloWallet March 2016 Two s a Crowd:

Two s a Crowd: Are Retirement Savings Being Crowded Out by Student Loans? Scott Cooley Director of Policy Research, Morningstar Jake Spiegel Senior Research Analyst, HelloWallet March 2016 Two s a Crowd:

Federal Loan Borrowers REPAYMENT INFORMATION & STRATEGIES

Federal Loan Borrowers REPAYMENT INFORMATION & STRATEGIES Types of federal loans Direct Unsubsidized Loan (Direct Stafford Unsubsidized, William D. Ford Federal Direct Loan) Direct GradPLUS Loan (Direct

Federal Loan Borrowers REPAYMENT INFORMATION & STRATEGIES Types of federal loans Direct Unsubsidized Loan (Direct Stafford Unsubsidized, William D. Ford Federal Direct Loan) Direct GradPLUS Loan (Direct

Student loan payment and forgiveness opportunities

Americans have a total of $1.5 trillion in student debt. THERE ARE WAYS TO REDUCE YOUR DEBT CONQUER YOUR STUDENT LOAN DEBT Student loan payment and forgiveness opportunities Student loan debt is a burden

Americans have a total of $1.5 trillion in student debt. THERE ARE WAYS TO REDUCE YOUR DEBT CONQUER YOUR STUDENT LOAN DEBT Student loan payment and forgiveness opportunities Student loan debt is a burden

Syllabus. Smart Money Certification. SMC S M Desi g n a t i o n. LFE Institute LLC

Smart Money Certification SMC S M Desi g n a t i o n Syllabus LFE Institute LLC 877.533.5557 www.lfeinstitute.com smc@lfeinstitute.com Smart Money Certification Syllabus: SMC SM Designation Helping Americans

Smart Money Certification SMC S M Desi g n a t i o n Syllabus LFE Institute LLC 877.533.5557 www.lfeinstitute.com smc@lfeinstitute.com Smart Money Certification Syllabus: SMC SM Designation Helping Americans

Reverse mortgages. A discussion guide. Consumer Financial Protection Bureau

Reverse mortgages A discussion guide Consumer Financial Protection Bureau About this discussion guide This guide gives an overview of many key concepts of reverse mortgages. A qualified reverse mortgage

Reverse mortgages A discussion guide Consumer Financial Protection Bureau About this discussion guide This guide gives an overview of many key concepts of reverse mortgages. A qualified reverse mortgage

14 Reasons Why You Shouldn t Retire Early

14 Reasons Why You Shouldn t Retire Early Early retirement is a goal for many, including physicians. An extra decade or two to travel, pursue hobbies, and volunteer becomes more and more attractive, especially

14 Reasons Why You Shouldn t Retire Early Early retirement is a goal for many, including physicians. An extra decade or two to travel, pursue hobbies, and volunteer becomes more and more attractive, especially

What You Need to Know About Public Service Loan Forgiveness (PSLF) Chicago Office of Financial Aid

Chicago Office of Financial Aid") What You Need to Know About Public Service Loan Forgiveness (PSLF) Chicago Office of Financial Aid What will we go over? What is Public Service Loan Forgiveness (PSLF)? How do I qualify for PSLF? Eligible

What You Need to Know About Public Service Loan Forgiveness (PSLF) Chicago Office of Financial Aid What will we go over? What is Public Service Loan Forgiveness (PSLF)? How do I qualify for PSLF? Eligible

How to Pick the Best the Policy for Your Needs and What to Avoid

1 of 6 6/4/2014 3:01 PM JOURNAL REPORTS How to Pick the Best the Policy for Your Needs and What to Avoid By ANNE TERGESEN April 13, 2014 4:50 p.m. ET Brian Stauffer It's a decision many baby boomers are

1 of 6 6/4/2014 3:01 PM JOURNAL REPORTS How to Pick the Best the Policy for Your Needs and What to Avoid By ANNE TERGESEN April 13, 2014 4:50 p.m. ET Brian Stauffer It's a decision many baby boomers are

Student Loan Exit Counseling Graduate/Professional

Student Loan Exit Counseling Graduate/Professional To successfully manage loan repayment... Understand the basic terms and conditions of your loans. Know how much you have to repay, when and to whom. Define

Student Loan Exit Counseling Graduate/Professional To successfully manage loan repayment... Understand the basic terms and conditions of your loans. Know how much you have to repay, when and to whom. Define

Frequently Asked Questions

Short Sale 101 Frequently Asked Questions What is a Short Sale? In the world of Real Estate, a short sale refers to the sale of real property for an amount less than the amount owed on the property. In

Short Sale 101 Frequently Asked Questions What is a Short Sale? In the world of Real Estate, a short sale refers to the sale of real property for an amount less than the amount owed on the property. In

FREQUENTLY ASKED QUESTIONS

FREQUENTLY ASKED QUESTIONS Hardest Hit Funding Round 2 opened Monday August 1 st, 2016 Please click on one of the following links below to go to the section you are most interested in. Introduction to

FREQUENTLY ASKED QUESTIONS Hardest Hit Funding Round 2 opened Monday August 1 st, 2016 Please click on one of the following links below to go to the section you are most interested in. Introduction to

Marketplace Grace Periods Working as Intended

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Revised October 14, 2016 Marketplace Grace Periods Working as Intended Restrictions

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Revised October 14, 2016 Marketplace Grace Periods Working as Intended Restrictions

Borrower s Rights and Responsibilities Statement Important Notice: 5. Use of Loan Money 1. Governing Law

Borrower s Rights and Responsibilities Statement Important Notice: The Borrower s Rights and Responsibilities Statement provides additional information about the terms and conditions of loans you receive

Borrower s Rights and Responsibilities Statement Important Notice: The Borrower s Rights and Responsibilities Statement provides additional information about the terms and conditions of loans you receive

Post-Loan (Exit) Counseling Supplement:

Counseling Supplement:") Post-Loan (Exit) Counseling Supplement: Prepared by: Dr. Deb Figart Director, Stockton Center for Economic & Financial Literacy Deb.Figart@stockton.edu Why this Presentation? The federal online, required

Post-Loan (Exit) Counseling Supplement: Prepared by: Dr. Deb Figart Director, Stockton Center for Economic & Financial Literacy Deb.Figart@stockton.edu Why this Presentation? The federal online, required

Invest now to help make your retirement dreams a reality

Invest now to help make your retirement dreams a reality What s inside The sooner you start, the better off you ll be... 1 Chart your path to a comfortable retirement.... 2 Why Vanguard?... 5 Choose the

Invest now to help make your retirement dreams a reality What s inside The sooner you start, the better off you ll be... 1 Chart your path to a comfortable retirement.... 2 Why Vanguard?... 5 Choose the

Your guide to Releasing cash from your home. Lifetime mortgages that do more from

Your guide to Releasing cash from your home Lifetime mortgages that do more from Shouldn t there be more to life than worrying about money in retirement? That s what we believe and that s why more 2 life

Your guide to Releasing cash from your home Lifetime mortgages that do more from Shouldn t there be more to life than worrying about money in retirement? That s what we believe and that s why more 2 life

Entrance Counseling Guide for Direct Loan Borrowers

You are borrowing Direct Subsidized Loans and/or Direct Unsubsidized Loans to help you finance your education. Repaying these loans is a serious responsibility. This guide explains some of the most important

You are borrowing Direct Subsidized Loans and/or Direct Unsubsidized Loans to help you finance your education. Repaying these loans is a serious responsibility. This guide explains some of the most important

How Financial Advisors Get Paid and

How Financial Advisors Get Paid and Why it Matters to You January 2012 Helping you take care of your money so you can do more of what you love! How Financial Advisors Get Paid and Why It Matters to You

How Financial Advisors Get Paid and Why it Matters to You January 2012 Helping you take care of your money so you can do more of what you love! How Financial Advisors Get Paid and Why It Matters to You

Class of 2014 Loan Repayment Information Session

Class of 2014 Loan Repayment Information Session Presented by: Gina Soliz, Director of Financial Aid Emily Zipprich, Financial Aid Coordinator Spring 2014 What we ll cover today Summarize the types of

Class of 2014 Loan Repayment Information Session Presented by: Gina Soliz, Director of Financial Aid Emily Zipprich, Financial Aid Coordinator Spring 2014 What we ll cover today Summarize the types of

Retirement Savings Plan 401(k)

") Retirement Savings Plan 401(k) Retirement Savings Plan 401(k) Advocate Health Care Network offers the Advocate Health Care Network Retirement Savings Plan 401(k) ( 401(k) Plan or Plan ) as part of its

Retirement Savings Plan 401(k) Retirement Savings Plan 401(k) Advocate Health Care Network offers the Advocate Health Care Network Retirement Savings Plan 401(k) ( 401(k) Plan or Plan ) as part of its

Student Loan Debt Management

Student Loan Debt Management Jointly presented by 360 Degrees of Financial Literacy, AICPA Personal Financial Planning Division 360 Degrees of Financial Literacy AICPA Personal Financial Planning Division

Student Loan Debt Management Jointly presented by 360 Degrees of Financial Literacy, AICPA Personal Financial Planning Division 360 Degrees of Financial Literacy AICPA Personal Financial Planning Division

THE COLUMBIA LAW SCHOOL LOAN REPAYMENT ASSISTANCE PROGRAM

THE COLUMBIA LAW SCHOOL LOAN REPAYMENT ASSISTANCE PROGRAM COLUMBIA LAW SCHOOL Financial Aid Office 435 West 116 th Street, MB A-4 New York, NY 27 Page 2 of 1 THE COLUMBIA LAW SCHOOL LOAN REPAYMENT ASSISTANCE

THE COLUMBIA LAW SCHOOL LOAN REPAYMENT ASSISTANCE PROGRAM COLUMBIA LAW SCHOOL Financial Aid Office 435 West 116 th Street, MB A-4 New York, NY 27 Page 2 of 1 THE COLUMBIA LAW SCHOOL LOAN REPAYMENT ASSISTANCE

9/19/2013 BORROWERS HAVE MORE OPTIONS OBJECTIVES COUNSELING BORROWERS ON PAY AS YOU EARN AND INCOME-DRIVEN PLANS

COUNSELING BORROWERS ON PAY AS YOU EARN AND INCOME-DRIVEN PLANS BORROWERS HAVE MORE OPTIONS We know many recent graduates are worried about repaying their student loans as our economy continues to recover,

COUNSELING BORROWERS ON PAY AS YOU EARN AND INCOME-DRIVEN PLANS BORROWERS HAVE MORE OPTIONS We know many recent graduates are worried about repaying their student loans as our economy continues to recover,

Student Loan Exit Counseling Graduate/Professional

Student Loan Exit Counseling Graduate/Professional School of Education & Social Policy McCormick School of Engineering Kellogg School of Management Bienen School of Music School of Professional Studies

Student Loan Exit Counseling Graduate/Professional School of Education & Social Policy McCormick School of Engineering Kellogg School of Management Bienen School of Music School of Professional Studies

SOCIAL SECURITY DISABILITY (SSD)

") SOCIAL SECURITY DISABILITY (SSD) Social Security is a federal program that pays monthly benefits to aged, blind and disabled people. In some cases, other family members may also be eligible to get benefits

SOCIAL SECURITY DISABILITY (SSD) Social Security is a federal program that pays monthly benefits to aged, blind and disabled people. In some cases, other family members may also be eligible to get benefits

What is a SHORT SALE?

Frequently Asked Questions What is a SHORT SALE? What is a Short Sale? In the world of Real Estate, a short sale refers to the sale of real property for an amount less than the amount owed on the property.

Frequently Asked Questions What is a SHORT SALE? What is a Short Sale? In the world of Real Estate, a short sale refers to the sale of real property for an amount less than the amount owed on the property.

REPAYING YOUR FEDERAL FAMILY EDUCATION LOAN

What s Inside: Getting Started REPAYING YOUR FEDERAL FAMILY EDUCATION LOAN Understanding My Statement Repayment Plans Standard Income Sensitive Graduated Extended Income-Based Repayment (IBR) PLUS Interest

What s Inside: Getting Started REPAYING YOUR FEDERAL FAMILY EDUCATION LOAN Understanding My Statement Repayment Plans Standard Income Sensitive Graduated Extended Income-Based Repayment (IBR) PLUS Interest

Starting a business venture

Business Formations Starting a business venture Business Formations When starting a business venture, you ll need to decide how to structure your operation. There are many types of business formations,

Business Formations Starting a business venture Business Formations When starting a business venture, you ll need to decide how to structure your operation. There are many types of business formations,

Minnesota Office of Higher Education TUDENT OANS & CONSUMER PROTECTION

4 Minnesota Office of Higher Education TUDENT OANS & CONSUMER PROTECTION Postseconary Student Loans : These are important words to know as you are going through the process of applying for a loan! Co-Signer:

4 Minnesota Office of Higher Education TUDENT OANS & CONSUMER PROTECTION Postseconary Student Loans : These are important words to know as you are going through the process of applying for a loan! Co-Signer:

THE FINANCIAL PLANNER S GUIDE TO STUDENT LOAN REFINANCING

THE FINANCIAL PLANNER S GUIDE TO STUDENT LOAN REFINANCING ADVISING CLIENTS WITH STUDENT LOANS Financial planners today have more clients dealing with student loans than ever before. Outstanding student

THE FINANCIAL PLANNER S GUIDE TO STUDENT LOAN REFINANCING ADVISING CLIENTS WITH STUDENT LOANS Financial planners today have more clients dealing with student loans than ever before. Outstanding student

LOAN REPAYMENT STRATEGIES

LOAN REPAYMENT STRATEGIES Be Ready! Develop a Plan! Fall 2017 Jeffrey Hanson Education Services Boston University School of Law You have CHOICES Decisions to be made 2 Should you pay the interest on your

LOAN REPAYMENT STRATEGIES Be Ready! Develop a Plan! Fall 2017 Jeffrey Hanson Education Services Boston University School of Law You have CHOICES Decisions to be made 2 Should you pay the interest on your

How to Strategically Manage Your Debt

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

Debt. Funny how four little letters can feel so dirty. Most of us have it in one shape or another, but none of us like to talk about it. Debt can get us into trouble, especially if it is unplanned and

CHAPTER TEN FREQUENTLY ASKED LOAN QUESTIONS

1. What is a Grace Period? CHAPTER TEN FREQUENTLY ASKED LOAN QUESTIONS A Grace Period is a block time frame (defined in your promissory note) where you are not required to make any loan payments. A student

1. What is a Grace Period? CHAPTER TEN FREQUENTLY ASKED LOAN QUESTIONS A Grace Period is a block time frame (defined in your promissory note) where you are not required to make any loan payments. A student

Bear Down on Student Loan Debt Options and Strategies for Repayment

Bear Down on Student Loan Debt Options and Strategies for Repayment Think About It Agenda Who We Are Student Loan Crisis Get Started Repayment Options Case Studies How We Can Help Q & A Who We Are Mission

Bear Down on Student Loan Debt Options and Strategies for Repayment Think About It Agenda Who We Are Student Loan Crisis Get Started Repayment Options Case Studies How We Can Help Q & A Who We Are Mission

Preparing for Your Loan Repayment. Full-Time MBA, Spring 2017

Preparing for Your Loan Repayment Full-Time MBA, Spring 2017 Agenda Federal Loans Terms & Conditions Repayment Options Private Loans Terms & Conditions Lender Information Next Steps Register ACH Prepay

Preparing for Your Loan Repayment Full-Time MBA, Spring 2017 Agenda Federal Loans Terms & Conditions Repayment Options Private Loans Terms & Conditions Lender Information Next Steps Register ACH Prepay

Earning for Today and Saving for Tomorrow. Retirement Savings Plan 401(k) inspiring possibilities

inspiring possibilities") Earning for Today and Saving for Tomorrow Retirement Savings Plan 401(k) inspiring possibilities Retirement Savings Plan 401(k) Advocate Health Care Network offers the Advocate Health Care Network Retirement

Earning for Today and Saving for Tomorrow Retirement Savings Plan 401(k) inspiring possibilities Retirement Savings Plan 401(k) Advocate Health Care Network offers the Advocate Health Care Network Retirement

Student Loan Repayment 101 Know Before You Owe. Holly Wright Program Manager

Student Loan Repayment 101 Know Before You Owe Holly Wright Program Manager Federal Student Aid Personal Finance Budgets Credit Reports Savings Account Reaching Financial Goals FRE E Private Student Loans

Student Loan Repayment 101 Know Before You Owe Holly Wright Program Manager Federal Student Aid Personal Finance Budgets Credit Reports Savings Account Reaching Financial Goals FRE E Private Student Loans

Title IV Loans: Understanding The Basics

Title IV Loans: Understanding The Basics Objectives Review Title IV loans and their basic terms Review some changes to Title IV loans RMASFAA Conference 2012, Omaha, NE Just the Basics: entrance/exit counseling,

Title IV Loans: Understanding The Basics Objectives Review Title IV loans and their basic terms Review some changes to Title IV loans RMASFAA Conference 2012, Omaha, NE Just the Basics: entrance/exit counseling,