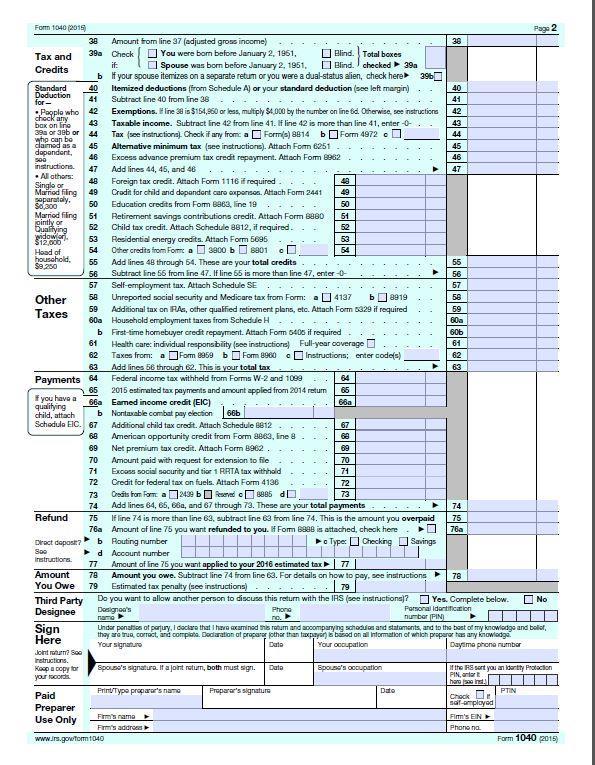

1040 Form: The standard Internal Revenue Service (IRS) form that individuals use. to file their annual income tax returns.

|

|

|

- Geraldine Harmon

- 5 years ago

- Views:

Transcription

1 1040 Form: The standard Internal Revenue Service (IRS) form that individuals use to file their annual income tax returns.

2

3 1040A Form: A simplified version of the 1040 form for individual income tax. To be eligible to use a 1040A form, an individual must fulfill certain requirements: 1. not itemizing deductions, 2. not owning a business and 3. Having a taxable income of less than $100,000.

4 1040EZ Form unofficially known as the easy form for single and joint filers with no dependents shortest version of the Internal Revenue Service's (IRS) Form 1040, and it offers a faster and easier way to file income taxes for taxpayers with basic tax situations. 1. must have taxable income of less than $100,000, 2. Interest income of $1,500 or less and 3. no dependents.

5 Need-based federal student aid 1. Federal Pell Grant programs: 2. Federal Supplemental Educational Opportunity Grant (FSEOG) 3. Federal Perkins Loan 4. Federal Work Study 5. Subsidized Stafford Loan

6 Federal Pell Grant For the award year (July 1, 2016, to June 30, 2017), the maximum award is $5,815. Amounts can change yearly. Does not need to be repaid

7 Federal Supplemental Educational Opportunity Grant (FSEOG) A grant for undergraduate students with exceptional financial need. Does not need to be repaid. Administered directly by the financial aid office at each participating school and is therefore called campus-based aid. Check with school's financial aid office to find out if the school offers the FSEOG.

8 Federal Perkins Loan Fixed interest rate loan of 5% for undergraduate and graduate students with exceptional financial need. No origination charges Interest is paid (subsidized) by the federal government until nine months after the student leaves college. Maximum Loan Amounts: Undergraduate - up to $5,500 a year (maximum of $27,500 as an undergraduate)

9 Federal Work-Study Part-time jobs for undergraduate and graduate students with financial need Allows them to earn money to help pay education expenses. Administered by schools participating in the Federal Work-Study Program. Check with your school's financial aid office to find out if your school participates.

10 Subsidized Stafford Loan Fixed interest Rate of 3.76% The Federal Government pays the interest while the student is in college or while the loan is in deferment. Meaning that any interest that accrues during your college career and six months afterward is completely paid for. Paid over 10 years The loan origination fee for all Direct Stafford loans (subsidized and unsubsidized) is 1.068%. These loan fees are deducted proportionately from each loan disbursement. You have a six-month grace period after graduation

11 Non-need-based federal student aid: 1. Unsubsidized Stafford Loan 2. Federal PLUS Loan 3. Teacher Education Access for College and Higher Education (TEACH) Grant

12 Unsubsidized Stafford Loan: Interest rate is 3.76% The loan origination fee for all Direct Stafford loans (subsidized and unsubsidized) is 1.068%. The loan fees are deducted proportionately from each loan disbursement. Paid over 10 years Interest begins from the date of your first loan disbursement, though you are not required to pay that interest until you finish school. When you graduate, the amount of money that accrued during the period is added to the principal loan amount and you begin paying off that new amount.

13 PLUS Loans (Parents Loans for Undergraduate Students) Loans for parents of undergraduate students and for graduate/professional students. Interest Rate of 6.31% Loan origination fee is 4.276% and deducted proportionately from each disbursement. Interest is charged, and you pay, from the first disbursement. The maximum PLUS loan amount you can borrow is the total cost of attendance (COA determined by the school) minus any other financial assistance received. Example: If the COA at a college was $25,000 and the amount of financial aid offered was $12,000, the parents would be eligible for a $13,000 PLUS loan. However, if the student was offered no financial aid the parents would be eligible for a $25,000 PLUS loan. A credit check will be performed.

14 PLUS Loans letter:

15 Teacher Education Access for College and Higher Education (TEACH) Grant: Requires you to take certain kinds of classes and Perform a certain type of job to keep the grant from turning into a loan.

16 Private Education Loans: Variable interest rates of 3% to 12%, and include higher origination fees and other charges. Federal education loans also offer better repayment and forgiveness options, therfore students should exhaust their eligibility for federal education loans before resorting to private student loans.

17 State grants: This is a website to view SC state sponsored grants and scholarships yingforcollege/financialassistanceavailable/scholars hipsgrantsforscresidents.aspx Nonprofits or Private organizations

18

19 Other Loans:

20 Award letters and comparisons:

21

22

23

24

25

26 There are various types of repayment plans for federal loans: Standard Repayment Plan Extended Repayment Plan Graduated Repayment Plan Income Contingent Repayment Plan Income Sensitive Repayment Plan

27 Standard Repayment Plan: Fixed payment amount each month--at least $50--for up to 10 years.

28 Extended Repayment Plan: Extended loan repayment over a period that is generally 12 to 30 years Minimum monthly payment is $50. Monthly payment may be lower than it would be if the same total loan amount were repaid under the Standard Repayment Plan. However, the total amount of interest, over the life of the loan, may be higher because the repayment period may be longer.

29 Graduated Repayment Plan: Payments are lower at first and then increase generally every two years. length of the repayment period generally ranges from 12 to 30 years Monthly payment may range from 50% to 150% of what it would be if the same total loan amount were repaid under the Standard Repayment Plan. However, a higher total amount of interest is paid because the repayment period is longer than it is under the Standard Repayment Plan.

30 Income Contingent Repayment Plan: Bases the monthly payments on yearly income, family size, and loan amount. As income rises or falls, so do the monthly payments. After 25 years, any remaining balance on the loan can be forgiven, but taxes may have to be paid on the amount forgiven.

31 Income-Sensitive Repayment Plan: Bases monthly repayment on yearly income and loan amount. As income rises or falls, so do the monthly payments. Each of the payments must at least equal to the interest accrued on the loan between scheduled payments

32 Automated Payments (Electronic Debit): Have your bank automatically make your monthly loan payments for you from your checking or savings account. There is a 0.25% reduction in the interest rate on your loans during any period when your payments are made through EDA.

33 Should I Consolidate My loans?

34 Fixed interest rate for the life of the loan. Based on the weighted average of the interest rates on the loans being consolidated. Simplify loan repayment by centralizing your loans to one bill, and can lower monthly payments by giving you up to 30 years to repay your loans. However, if you increase the length of your repayment period, you will also make more payments and pay more interest. Be sure to compare your current monthly payments to what monthly payments would be if you consolidated your loans. Once your loans are combined into a Direct Consolidation Loan, they cannot be removed. You apply through StudentLoans.gov.

35 Loan Deferment: You do not need to make payments Depending on the type of the loan (Subsidized) the federal government may pay the interest during the deferment period On loans the government does not pay (Unsubsidized), interest will still accrue and will be added to the loan amount when you start to repay. The student qualifies when the student meets one of the following six criteria: 1. enrolled, at least half time, at an institution that meets the eligibility requirements 2. enrolled in a graduate program 3. unemployed (for up to three years) 4. economic hardship (for up to three years). 5. During a period of active duty military service during a war, military operation, or national emergency. 6. During the 13 months following the conclusion of qualifying active duty military service, or until you return to enrollment on at least a half-time basis, whichever is earlier. Request should be submitted to the organization to which you make your loan payments.

36 Loan Forbearance: If you cannot make your scheduled loan payments, but do not qualify for a deferment, your loan servicer may be able to grant you a forbearance. You may be able to stop making payments or reduce your monthly payment for up to 12 months. Interest will continue to accrue on your subsidized and unsubsidized loans (including all PLUS loans). Must apply by making a request to your loan servicer. You can pay the interest during forbearance or allow the interest to accrue (accumulate) and added to your balance when forbearance is over.

37 Public Service Loan Forgiveness (PSLF) Program? Forgives the remaining balance on your Direct Loans after you have made 120 qualifying monthly payments under a qualifying repayment plan while working full-time for a qualifying employer. 1. Government organizations at any level (federal, state, local, or tribal) 2. Not-for-profit organizations that are tax-exempt under Section 501(c)(3) of the Internal Revenue Code 3. Other types of not-for-profit organizations that provide certain types of qualifying public services

38 Loan Bankruptcy: A borrower may be able to bankrupt out of a federal education loan ONLY if the court allows it, because of excessive hardship of repayment. This is very tough to show and most courts will not let the borrower bankrupt out of an education loan.

39 Tax strategies: 1. Student Loan Interest Deduction 2. American Opportunity Credit 3. Lifetime Learning Credit

40 Student Loan Interest Deduction: A deduction to adjusted gross income for interest paid on qualified student loans. The loans do not have to be federal interest subsidized loans. The maximum interest deduction allowed is $2,500. Parents are able to deduct education interest expense on PLUS loans during college years.

41 American Opportunity Credit: A credit against an individual's federal income tax liability. Calculated by taking 100% of the first $2,000 of "qualified tuition and related expenses" plus 25% of the excess of these expenses up to a maximum credit of $2,500. Example: If the qualified expenses of an individual student were $2,500, the AOC would be $2,125 (100% x $2,000 plus 25% x $500). If the expenses were only $1,600, the American Opportunity Credit would be $1,600 (100% x $1,600). Can be claimed for each student claimed on tax return for four years For example, if there are two "eligible students" who have qualified expenses, a maximum American Opportunity Credit of $5,000 (2 students x $2,500) can be claimed. Phased out when the taxpayer reaches certain levels of "Modified Adjusted Gross Income. After $90,000 for single or head of household and $180,000 for married taxpayers.

42 Lifetime Learning Credit: Calculated by taking 20% of up to a maximum of $10,000 in "qualified tuition and related expenses." Limit is $2,000 per taxpayer tax return not per eligible student. The qualified expenses for all eligible students can be combined to reach the maximum credit of $2,000. Example: If there are two eligible students that each have qualified expenses of $10,000, the maximum Lifetime Learning Credit that could be claimed is $2,000 per that taxpayer return. If the same family only had combined expenses of $8,000, the Lifetime Learning Credit would be $1,600, 20% x $8,000. The Lifetime Learning Credit is phased out when the taxpayer reaches certain levels of Modified AGI.$62,000 for Single or Head-of-Household and $124,000 for Married filing jointly).

43 College Savings Plans

Student Loan Terms to Know

Definitions of terms related to federal student loans and the Nelnet repayment process Accrue The act of interest accumulating on the borrower s principal balance Adjusted Gross Income (AGI) The adjusted

Definitions of terms related to federal student loans and the Nelnet repayment process Accrue The act of interest accumulating on the borrower s principal balance Adjusted Gross Income (AGI) The adjusted

623 POLICY Federal Direct Loans/Plus Statement of Policy

623 POLICY Federal Direct /Plus 623.1 Statement of Policy The Redlands Community College Financial Aid Office participates in Loan Programs to assist students with financial loans during their enrollment

623 POLICY Federal Direct /Plus 623.1 Statement of Policy The Redlands Community College Financial Aid Office participates in Loan Programs to assist students with financial loans during their enrollment

THE ROAD TO ZERO. A Strategic Approach to Student Loan Repayment. Financial education resources from a nonprofit you can trust. AccessLex.

THE ROAD TO ZERO A Strategic Approach to Student Loan Repayment Financial education resources from a nonprofit you can trust. AccessLex.org 1 GET STARTED. 3 KNOW WHAT YOU OWE. 4 KNOW YOUR OPTIONS. 6 Debt-Driven

THE ROAD TO ZERO A Strategic Approach to Student Loan Repayment Financial education resources from a nonprofit you can trust. AccessLex.org 1 GET STARTED. 3 KNOW WHAT YOU OWE. 4 KNOW YOUR OPTIONS. 6 Debt-Driven

Direct Loan Exit Counseling Guide

2018 Federal Student Aid Direct Loan Exit Counseling Guide For Borrowers of Direct Loans and Federal Family Education Program Loans U.S. Department of Education Betsy DeVos Secretary Federal Student Aid

2018 Federal Student Aid Direct Loan Exit Counseling Guide For Borrowers of Direct Loans and Federal Family Education Program Loans U.S. Department of Education Betsy DeVos Secretary Federal Student Aid

William D. Ford Federal Direct Loan Program Direct Subsidized Loan and Direct Unsubsidized Loan Borrower s Rights and Responsibilities Statement

Important Notice: This Borrower s Rights and Responsibilities Statement provides additional information about the terms and conditions of the loans you receive under the accompanying Master Promissory

Important Notice: This Borrower s Rights and Responsibilities Statement provides additional information about the terms and conditions of the loans you receive under the accompanying Master Promissory

Meet The Speakers. Sasha Grabenstetter, AFC Consumer Economics Educator University of Illinois Extension

Welcome to 1 Meet The Speakers Sasha Grabenstetter, AFC Consumer Economics Educator University of Illinois Extension Andrea Pellegrini Assistant Director Student Money Management Center 2 Where are you

Welcome to 1 Meet The Speakers Sasha Grabenstetter, AFC Consumer Economics Educator University of Illinois Extension Andrea Pellegrini Assistant Director Student Money Management Center 2 Where are you

Student Loan Repayment. Health Sciences Financial Aid Office May 17 th, 2018

Student Loan Repayment Health Sciences Financial Aid Office May 17 th, 2018 TOPICS KNOW YOUR LOAN PORTFOLIO HOW TO POSTPONE PAYMENTS REPAYMENT PLANS OTHER CONSIDERATIONS CREDIT QUESTIONS KNOW YOUR LOAN

Student Loan Repayment Health Sciences Financial Aid Office May 17 th, 2018 TOPICS KNOW YOUR LOAN PORTFOLIO HOW TO POSTPONE PAYMENTS REPAYMENT PLANS OTHER CONSIDERATIONS CREDIT QUESTIONS KNOW YOUR LOAN

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS U.S. Department of Education Betsy DeVos Secretary Federal Student Aid A. Wayne Johnson Chief Operating Officer

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS U.S. Department of Education Betsy DeVos Secretary Federal Student Aid A. Wayne Johnson Chief Operating Officer

Borrower s Rights and Responsibilities Statement Important Notice: 5. Use of Loan Money 1. Governing Law

Borrower s Rights and Responsibilities Statement Important Notice: The Borrower s Rights and Responsibilities Statement provides additional information about the terms and conditions of loans you receive

Borrower s Rights and Responsibilities Statement Important Notice: The Borrower s Rights and Responsibilities Statement provides additional information about the terms and conditions of loans you receive

Private Education Loan Application and Solicitation Disclosure Page 1 of 3

Private Education Loan Application and Solicitation Disclosure Page 1 of 3 Loan Interest Rate & Fees Your starting interest rate will be between 4.725% and 11.865% After the starting rate is set, your

Private Education Loan Application and Solicitation Disclosure Page 1 of 3 Loan Interest Rate & Fees Your starting interest rate will be between 4.725% and 11.865% After the starting rate is set, your

Welcome to Student Loan Repayment Strategies

Welcome to Student Loan Repayment Strategies Kathy Sweedler Consumer Economics Educator University of Illinois Extension sweedler@illinois.edu 1 Make Plan: Take Action Where are you now? Evaluate repayment

Welcome to Student Loan Repayment Strategies Kathy Sweedler Consumer Economics Educator University of Illinois Extension sweedler@illinois.edu 1 Make Plan: Take Action Where are you now? Evaluate repayment

What is an income-driven repayment plan?

Income-Driven Plans for Federal Student Loans What is an income-driven repayment plan? An income-driven repayment plan is a repayment plan that sets your monthly student loan payment at an amount that

Income-Driven Plans for Federal Student Loans What is an income-driven repayment plan? An income-driven repayment plan is a repayment plan that sets your monthly student loan payment at an amount that

Federal Student Aid. Direct Loan. Entrance Counseling Guide

2018 Federal Student Aid Direct Loan Entrance Counseling Guide U.S. Department of Education Betsy DeVos Secretary Federal Student Aid James Manning Acting Chief Operating Officer Federal Student Aid, an

2018 Federal Student Aid Direct Loan Entrance Counseling Guide U.S. Department of Education Betsy DeVos Secretary Federal Student Aid James Manning Acting Chief Operating Officer Federal Student Aid, an

Objectives. Objectives. Loans 101. Purpose and types of Federal loans. Life cycle of a Federal loan. Repayment options. Delinquency and default

Loans 101 Becky Davis and Debbie Murphy Ascendium Education Solutions Objectives 1 2 3 Purpose and types of Federal loans Life cycle of a Federal loan Repayment options 2019 ILASFAA Annual Conference 2

Loans 101 Becky Davis and Debbie Murphy Ascendium Education Solutions Objectives 1 2 3 Purpose and types of Federal loans Life cycle of a Federal loan Repayment options 2019 ILASFAA Annual Conference 2

Student Loans 101 Loan Repayment, Consolidation and Forgiveness. Holly Wright UM Financial Education Program Manager

Student Loans 101 Loan Repayment, Consolidation and Forgiveness Holly Wright UM Financial Education Program Manager Federal Student Aid Process Financial Aid Package Student Loans Personal Finance Budgeting

Student Loans 101 Loan Repayment, Consolidation and Forgiveness Holly Wright UM Financial Education Program Manager Federal Student Aid Process Financial Aid Package Student Loans Personal Finance Budgeting

Financial Aid and Financial Literacy Glossary

Financial Aid and Financial Literacy Glossary Accrued Interest Interest that accumulates and is paid in installments at a later time (usually when the principal becomes due) rather than paid on a regular

Financial Aid and Financial Literacy Glossary Accrued Interest Interest that accumulates and is paid in installments at a later time (usually when the principal becomes due) rather than paid on a regular

PLAIN LANGUAGE DISCLOSURE FOR DIRECT SUBSIDIZED LOANS AND DIRECT UNSUBSIDIZED LOANS WILLIAM D. FORD FEDERAL DIRECT LOAN PROGRAM

1. GENERAL INFORMATION You are receiving a Direct Subsidized Loan and/or Direct Unsubsidized Loan under a Master Promissory Note (MPN) that you signed previously (see Item 2). This Plain Language Disclosure

1. GENERAL INFORMATION You are receiving a Direct Subsidized Loan and/or Direct Unsubsidized Loan under a Master Promissory Note (MPN) that you signed previously (see Item 2). This Plain Language Disclosure

Federal Student Loan Repayment

Federal Student Loan Repayment The Road to Zero Know your financial goals. Know what you owe. Know what time it is. Know your options. Select your plan. Manage your payments. AccessGroup.org Financial

Federal Student Loan Repayment The Road to Zero Know your financial goals. Know what you owe. Know what time it is. Know your options. Select your plan. Manage your payments. AccessGroup.org Financial

About Salt Money Management Student Loan Repayment

About Salt Money Management Student Loan Repayment Michele Almeida Senior Associate Director of SFS Jane Aube Loan Programs & Compliance Specialist Kim Downs-Burns AVP Student Financial Services American

About Salt Money Management Student Loan Repayment Michele Almeida Senior Associate Director of SFS Jane Aube Loan Programs & Compliance Specialist Kim Downs-Burns AVP Student Financial Services American

Student Loan Ombudsman Caucus

Student Loan Ombudsman Caucus Repayment Plans Selecting the right repayment plan is important in the successful management of your student loan. You can change repayment plans contact your lender/servicer

Student Loan Ombudsman Caucus Repayment Plans Selecting the right repayment plan is important in the successful management of your student loan. You can change repayment plans contact your lender/servicer

Income-Driven Repayment Plans

Income-Driven Repayment Plans Agenda Income-Driven Repayment Plans Overview Income-Based Repayment Plan (IBR) Income-Contingent Repayment Plan (ICR) Pay As You Earn Plan (PAYE) Revised Pay As You Earn

Income-Driven Repayment Plans Agenda Income-Driven Repayment Plans Overview Income-Based Repayment Plan (IBR) Income-Contingent Repayment Plan (ICR) Pay As You Earn Plan (PAYE) Revised Pay As You Earn

9/19/2013 BORROWERS HAVE MORE OPTIONS OBJECTIVES COUNSELING BORROWERS ON PAY AS YOU EARN AND INCOME-DRIVEN PLANS

COUNSELING BORROWERS ON PAY AS YOU EARN AND INCOME-DRIVEN PLANS BORROWERS HAVE MORE OPTIONS We know many recent graduates are worried about repaying their student loans as our economy continues to recover,

COUNSELING BORROWERS ON PAY AS YOU EARN AND INCOME-DRIVEN PLANS BORROWERS HAVE MORE OPTIONS We know many recent graduates are worried about repaying their student loans as our economy continues to recover,

LOAN REPAYMENT AND DEFAULT PREVENTION. Financial Aid and Scholarship Office

LOAN REPAYMENT AND DEFAULT PREVENTION Financial Aid and Scholarship Office 1 TOPICS TO BE COVERED Exit Counseling Loan Consolidation Repayment Options Deferment and Forbearance Discharge and Forgiveness

LOAN REPAYMENT AND DEFAULT PREVENTION Financial Aid and Scholarship Office 1 TOPICS TO BE COVERED Exit Counseling Loan Consolidation Repayment Options Deferment and Forbearance Discharge and Forgiveness

Should I Refinance My Student Loans? Presented by: Tricia Poplicean College Access Counselor

Should I Refinance My Student Loans? Presented by: Tricia Poplicean College Access Counselor Presentation Highlights Understand your student loans Federal vs. Private Student loan consolidation Student

Should I Refinance My Student Loans? Presented by: Tricia Poplicean College Access Counselor Presentation Highlights Understand your student loans Federal vs. Private Student loan consolidation Student

Federal Loan Borrowers REPAYMENT INFORMATION & STRATEGIES

Federal Loan Borrowers REPAYMENT INFORMATION & STRATEGIES Types of federal loans Direct Unsubsidized Loan (Direct Stafford Unsubsidized, William D. Ford Federal Direct Loan) Direct GradPLUS Loan (Direct

Federal Loan Borrowers REPAYMENT INFORMATION & STRATEGIES Types of federal loans Direct Unsubsidized Loan (Direct Stafford Unsubsidized, William D. Ford Federal Direct Loan) Direct GradPLUS Loan (Direct

What Is Direct Loan Exit Counseling?

What Is Direct Loan Exit Counseling? Before you graduate, or if you drop below less-than-half-time enrollment, you must complete a Direct Loan (Stafford) Exit Counseling session. You can complete the entire

What Is Direct Loan Exit Counseling? Before you graduate, or if you drop below less-than-half-time enrollment, you must complete a Direct Loan (Stafford) Exit Counseling session. You can complete the entire

5 Steps to Request a Student Loan

5 Steps to Request a Student Loan Complete FAFSA www.fafsa.ed.gov Spring 2013 Deadlines FAFSA Submission Deadline November 2, 2012 Financial Aid Student Loan Application/ Certification Request and Completion

5 Steps to Request a Student Loan Complete FAFSA www.fafsa.ed.gov Spring 2013 Deadlines FAFSA Submission Deadline November 2, 2012 Financial Aid Student Loan Application/ Certification Request and Completion

This presentation is for discussion purposes only.

This presentation is for discussion purposes only. Robyn Hughes School Ombudsman Navient 2 Agenda Student loan cycle What to communicate to borrowers For your students: 10 things to do before you make

This presentation is for discussion purposes only. Robyn Hughes School Ombudsman Navient 2 Agenda Student loan cycle What to communicate to borrowers For your students: 10 things to do before you make

PUBLIC SERVICE LOAN FORGIVENESS

PUBLIC SERVICE LOAN FORGIVENESS Presented by: Scott Harrison, Assistant Director Student Financial Services (SFS) PSLF Program Basics The remaining balance on your qualified Direct Loans is forgiven and

PUBLIC SERVICE LOAN FORGIVENESS Presented by: Scott Harrison, Assistant Director Student Financial Services (SFS) PSLF Program Basics The remaining balance on your qualified Direct Loans is forgiven and

Between 2004 and 2014, the total student debt in the US tripled from $364 billion in 2004 to $1.16 trillion in 2014.

1 Statistic s from the Federal Reserve Bank of New York February 2015 Between 2004 and 2014, the total student debt in the US tripled from $364 billion in 2004 to $1.16 trillion in 2014. Our research indicates

1 Statistic s from the Federal Reserve Bank of New York February 2015 Between 2004 and 2014, the total student debt in the US tripled from $364 billion in 2004 to $1.16 trillion in 2014. Our research indicates

STATE OF NEW JERSEY STUDENT LOAN GUIDE

STATE OF NEW JERSEY STUDENT LOAN GUIDE New Jersey Higher Education Student Assistance Authority The Student Loan Guide provides general student loan information to assist students and their families in

STATE OF NEW JERSEY STUDENT LOAN GUIDE New Jersey Higher Education Student Assistance Authority The Student Loan Guide provides general student loan information to assist students and their families in

Entrance Counseling Guide for Direct Loan Borrowers

You are borrowing Direct Subsidized Loans and/or Direct Unsubsidized Loans to help you finance your education. Repaying these loans is a serious responsibility. This guide explains some of the most important

You are borrowing Direct Subsidized Loans and/or Direct Unsubsidized Loans to help you finance your education. Repaying these loans is a serious responsibility. This guide explains some of the most important

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS U.S. Department of Education Arne Duncan Secretary Federal Student Aid James W. Runcie Chief Operating Officer

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS U.S. Department of Education Arne Duncan Secretary Federal Student Aid James W. Runcie Chief Operating Officer

Direct Loan: Post-Graduation

Direct Loan: Post-Graduation Direct Loan Repayment Glossary: Before we begin Principal: The actual dollar figure of the amount borrowed Interest: Periodic fee charged to borrower; usually a percentage

Direct Loan: Post-Graduation Direct Loan Repayment Glossary: Before we begin Principal: The actual dollar figure of the amount borrowed Interest: Periodic fee charged to borrower; usually a percentage

4/4/2018 MANAGING STUDENT LOAN REPAYMENT FOR GRADUATING SENIORS

MANAGING STUDENT LOAN REPAYMENT FOR GRADUATING SENIORS MASSACHUSETTS EDUCATIONAL FINANCING AUTHORITY About MEFA Not-for-profit state authority created in 1982 Helping families plan, save, and pay for college

MANAGING STUDENT LOAN REPAYMENT FOR GRADUATING SENIORS MASSACHUSETTS EDUCATIONAL FINANCING AUTHORITY About MEFA Not-for-profit state authority created in 1982 Helping families plan, save, and pay for college

For additional information, contact your financial aid office or the U. S. Department of Education at:

Pennsylvania Private Loan Marketplace http://pennsylvania.privateloanmarketplace.com/ Once you and your family have considered institutional and federal loan options, you can use the Pennsylvania Private

Pennsylvania Private Loan Marketplace http://pennsylvania.privateloanmarketplace.com/ Once you and your family have considered institutional and federal loan options, you can use the Pennsylvania Private

Understanding Student Loans

Understanding Student Loans 2018 Student Loan Headlines Has Student Loan Debt Reached A Crisis Point? Beyond the Headlines: Is Student Debt Strangling Millennials' Chances for Success? Student Loan Debt

Understanding Student Loans 2018 Student Loan Headlines Has Student Loan Debt Reached A Crisis Point? Beyond the Headlines: Is Student Debt Strangling Millennials' Chances for Success? Student Loan Debt

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS U.S. Department of Education Arne Duncan Secretary Federal Student Aid James W. Runcie Chief Operating Officer

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS U.S. Department of Education Arne Duncan Secretary Federal Student Aid James W. Runcie Chief Operating Officer

PUBLIC SERVICE LOAN FORGIVENESS

PUBLIC SERVICE LOAN FORGIVENESS Presented by: Scott Harrison, Assistant Director Student Financial Services (SFS) PSLF Program Basics The remaining balance on your qualified Direct Loans is forgiven and

PUBLIC SERVICE LOAN FORGIVENESS Presented by: Scott Harrison, Assistant Director Student Financial Services (SFS) PSLF Program Basics The remaining balance on your qualified Direct Loans is forgiven and

Student Loan Exit Counseling Graduate/Professional

Student Loan Exit Counseling Graduate/Professional To successfully manage loan repayment... Understand the basic terms and conditions of your loans. Know how much you have to repay, when and to whom. Define

Student Loan Exit Counseling Graduate/Professional To successfully manage loan repayment... Understand the basic terms and conditions of your loans. Know how much you have to repay, when and to whom. Define

PERKINS LOAN ENTRANCE INTERVIEW CONFIRMATION

PERKINS LOAN ENTRANCE INTERVIEW CONFIRMATION Last Name First Name Student ID # Permanent Home Address City/State Zip Home Telephone Number Cell Telephone Number First and Last Name of nearest relative,

PERKINS LOAN ENTRANCE INTERVIEW CONFIRMATION Last Name First Name Student ID # Permanent Home Address City/State Zip Home Telephone Number Cell Telephone Number First and Last Name of nearest relative,

Award Letter Analyzer

Award Letter Analyzer Name: High School: College name On/Off Campus Tuition & Fees Room & Board Total Direct Costs Direct Cost Year Gift Aid Pell Grant State Grant SEOG Grant Institutional Grants/Scholarships

Award Letter Analyzer Name: High School: College name On/Off Campus Tuition & Fees Room & Board Total Direct Costs Direct Cost Year Gift Aid Pell Grant State Grant SEOG Grant Institutional Grants/Scholarships

Minnesota Office of Higher Education TUDENT OANS & CONSUMER PROTECTION

4 Minnesota Office of Higher Education TUDENT OANS & CONSUMER PROTECTION Postseconary Student Loans : These are important words to know as you are going through the process of applying for a loan! Co-Signer:

4 Minnesota Office of Higher Education TUDENT OANS & CONSUMER PROTECTION Postseconary Student Loans : These are important words to know as you are going through the process of applying for a loan! Co-Signer:

Student Loan Repayment 101 Know Before You Owe. Holly Wright Program Manager

Student Loan Repayment 101 Know Before You Owe Holly Wright Program Manager Federal Student Aid Personal Finance Budgets Credit Reports Savings Account Reaching Financial Goals FRE E Private Student Loans

Student Loan Repayment 101 Know Before You Owe Holly Wright Program Manager Federal Student Aid Personal Finance Budgets Credit Reports Savings Account Reaching Financial Goals FRE E Private Student Loans

Partial Financial Hardship 8/11/2014. Disadvantages of income-driven plans. Interest and capitalization benefits accompany the income-driven plans

Income-Driven Plan Payment Amount Comprehensive Student Loan Training Series Income-Contingent The lesser of: 20 percent of discretionary income, or what borrower would pay on a fixed payment over the

Income-Driven Plan Payment Amount Comprehensive Student Loan Training Series Income-Contingent The lesser of: 20 percent of discretionary income, or what borrower would pay on a fixed payment over the

10/17/2016. Haverford HS College Financial Aid Programs. Paying for College 10/10 Loans & Repayment 10/17 Saving For College 10/24

Presented By Fred Amrein Haverford HS College Financial Aid Programs Paying for College 10/10 Loans & Repayment 10/17 Saving For College 10/24 Amrein Financial is an independent, fee only Registered Investment

Presented By Fred Amrein Haverford HS College Financial Aid Programs Paying for College 10/10 Loans & Repayment 10/17 Saving For College 10/24 Amrein Financial is an independent, fee only Registered Investment

GLOSSARY OF LOAN TERMS

GLOSSARY OF LOAN TERMS Accrued Interest Interest that accumulates on the unpaid principal balance of a loan. Accrual Date The date on which interest charges on an educational loan begin to accrue. Amortization

GLOSSARY OF LOAN TERMS Accrued Interest Interest that accumulates on the unpaid principal balance of a loan. Accrual Date The date on which interest charges on an educational loan begin to accrue. Amortization

Drowning in Debt? How government and nonprofit employees can earn public service loan forgiveness

Drowning in Debt? How government and nonprofit employees can earn public service loan forgiveness Isaac Bowers ibowers@equaljusticeworks.org www.equaljusticeworks.org Today s Agenda Resources for Managing

Drowning in Debt? How government and nonprofit employees can earn public service loan forgiveness Isaac Bowers ibowers@equaljusticeworks.org www.equaljusticeworks.org Today s Agenda Resources for Managing

aascu policy statements

Federal Role in College Affordability aascu policy statements Federal Grants Pell Grants u Advocate for sufficient funding to sustain the value of Pell Grant awards by ensuring an appropriations base of

Federal Role in College Affordability aascu policy statements Federal Grants Pell Grants u Advocate for sufficient funding to sustain the value of Pell Grant awards by ensuring an appropriations base of

LRAP & FINANCIAL PLANNING

LRAP & FINANCIAL PLANNING Berkeley Law: Financial Aid Office March 11, 2014 COLLEGE COST REDUCTION & ACCESS ACT AND PSLF OVERVIEW Public Service Loan Forgiveness (PSLF) Income Based Repayment (IBR) Pay

LRAP & FINANCIAL PLANNING Berkeley Law: Financial Aid Office March 11, 2014 COLLEGE COST REDUCTION & ACCESS ACT AND PSLF OVERVIEW Public Service Loan Forgiveness (PSLF) Income Based Repayment (IBR) Pay

TAKE CHARGE OF LOAN REPAYMENT!

1 TAKE CHARGE OF LOAN REPAYMENT! Strategies for Managing Your Debt Successfully Spring 2013 Jeffrey Hanson Education Services University of San Diego School of Law Your Action Plan 4 Steps 2 1. Take stock

1 TAKE CHARGE OF LOAN REPAYMENT! Strategies for Managing Your Debt Successfully Spring 2013 Jeffrey Hanson Education Services University of San Diego School of Law Your Action Plan 4 Steps 2 1. Take stock

Bear Down on Student Loan Debt Options and Strategies for Repayment

Bear Down on Student Loan Debt Options and Strategies for Repayment Think About It Agenda Who We Are Student Loan Crisis Get Started Repayment Options Case Studies How We Can Help Q & A Who We Are Mission

Bear Down on Student Loan Debt Options and Strategies for Repayment Think About It Agenda Who We Are Student Loan Crisis Get Started Repayment Options Case Studies How We Can Help Q & A Who We Are Mission

Understanding and Managing your Student Loans and Repayment

Understanding and Managing your Student Loans and Financial Literacy Programs University of Colorado Denver Presenter: M. Lesa Briggs Financial Literacy & Wellness After this presentation, you will be

Understanding and Managing your Student Loans and Financial Literacy Programs University of Colorado Denver Presenter: M. Lesa Briggs Financial Literacy & Wellness After this presentation, you will be

Financial Aid Basics 2.0: The College Years

Financial Aid Basics 2.0: The College Years Objectives o Discuss some recent updates made to the FSA ID and changes to the IRS Data Retrieval Tool for the 2018-19 FAFSA. o Review financial aid available

Financial Aid Basics 2.0: The College Years Objectives o Discuss some recent updates made to the FSA ID and changes to the IRS Data Retrieval Tool for the 2018-19 FAFSA. o Review financial aid available

Class of 2014 Loan Repayment Information Session

Class of 2014 Loan Repayment Information Session Presented by: Gina Soliz, Director of Financial Aid Emily Zipprich, Financial Aid Coordinator Spring 2014 What we ll cover today Summarize the types of

Class of 2014 Loan Repayment Information Session Presented by: Gina Soliz, Director of Financial Aid Emily Zipprich, Financial Aid Coordinator Spring 2014 What we ll cover today Summarize the types of

Private Loan Guide. Apply for free, federal and state financial aid programs:

Private loan basics Private student loans are non-federal loans. Private Loan Guide You should only borrow private loans to fund your education as a last resort. Do all of the following before you consider

Private loan basics Private student loans are non-federal loans. Private Loan Guide You should only borrow private loans to fund your education as a last resort. Do all of the following before you consider

Entrance COUNSELING GUIDE

Entrance COUNSELING GUIDE For direct Loan Borrowers U.S. Department of Education John King Secretary Federal Student Aid James W. Runcie Chief Operating Officer September 2016 If you are a borrower with

Entrance COUNSELING GUIDE For direct Loan Borrowers U.S. Department of Education John King Secretary Federal Student Aid James W. Runcie Chief Operating Officer September 2016 If you are a borrower with

Student Loan Exit Counseling Graduate/Professional

Student Loan Exit Counseling Graduate/Professional School of Education & Social Policy McCormick School of Engineering Kellogg School of Management Bienen School of Music School of Professional Studies

Student Loan Exit Counseling Graduate/Professional School of Education & Social Policy McCormick School of Engineering Kellogg School of Management Bienen School of Music School of Professional Studies

CRS Report for Congress

Order Code RL30655 CRS Report for Congress Received through the CRS Web Federal Student Loans: Terms and Conditions for Borrowers Updated June 1, 2004 Adam Stoll Specialist in Social Legislation Domestic

Order Code RL30655 CRS Report for Congress Received through the CRS Web Federal Student Loans: Terms and Conditions for Borrowers Updated June 1, 2004 Adam Stoll Specialist in Social Legislation Domestic

Exit Counseling M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES

Exit Counseling FALL 2017 M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES Agenda Loan types and interest rates Grace periods Repaying

Exit Counseling FALL 2017 M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES Agenda Loan types and interest rates Grace periods Repaying

Office of Student Financial Management. Kasia Palm, Director of Student Financial Management

Office of Student Financial Management Kasia Palm, Director of Student Financial Management We advise prospective, current, and former Denver Law students on: General financial aid questions We do not

Office of Student Financial Management Kasia Palm, Director of Student Financial Management We advise prospective, current, and former Denver Law students on: General financial aid questions We do not

REPAYING STUDENT LOANS

REPAYING STUDENT LOANS 1 It is not unusual for college tuition to cost $30,000 or more a year. Some students are able to pay for it with savings or get grants or scholarships. However, many have to turn

REPAYING STUDENT LOANS 1 It is not unusual for college tuition to cost $30,000 or more a year. Some students are able to pay for it with savings or get grants or scholarships. However, many have to turn

Federal Student Loan Repayment Do s & Don ts

Federal Student Loan Repayment Do s & Don ts College graduates with Federal student loans have a number of repayment options at their disposal. This guide will walk you through your options so you can

Federal Student Loan Repayment Do s & Don ts College graduates with Federal student loans have a number of repayment options at their disposal. This guide will walk you through your options so you can

Exit Counseling M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES

Exit Counseling SPRING 2018 M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES Agenda Loan types and interest rates Grace periods

Exit Counseling SPRING 2018 M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES Agenda Loan types and interest rates Grace periods

Undergraduate subsidized & unsubsidized. % fixed Graduate

Private Education Loan Variable Rate Application and Solicitation Disclosure Firstrust Savings Bank c/o College Ave Student Loans 1105 N. Market St. Wilmington, DE 1801 LOAN & FEES YOUR STARTING (UPON

Private Education Loan Variable Rate Application and Solicitation Disclosure Firstrust Savings Bank c/o College Ave Student Loans 1105 N. Market St. Wilmington, DE 1801 LOAN & FEES YOUR STARTING (UPON

For additional information, contact your financial aid office or the U. S. Department of Education at:

Private Student Loan Marketplace Revised 7/1/11 http://www.privateloanmarketplace.com/ Once you and your family have considered institutional and federal loan options, you can use the Private Student Loan

Private Student Loan Marketplace Revised 7/1/11 http://www.privateloanmarketplace.com/ Once you and your family have considered institutional and federal loan options, you can use the Private Student Loan

Navigating Student Loan Repayment

Navigating Student Loan Repayment Objectives The goal of this presentation is to prepare you for student loan repayment, to encourage healthy financial habits, and to connect you with resources to help

Navigating Student Loan Repayment Objectives The goal of this presentation is to prepare you for student loan repayment, to encourage healthy financial habits, and to connect you with resources to help

Repaying your federal student loans

Repaying your federal student loans Many borrowers don t worry about their student loans until they graduate or leave school. But you should immediately notify your loan servicer and school in writing

Repaying your federal student loans Many borrowers don t worry about their student loans until they graduate or leave school. But you should immediately notify your loan servicer and school in writing

Post-Loan (Exit) Counseling Supplement:

Counseling Supplement:") Post-Loan (Exit) Counseling Supplement: Prepared by: Dr. Deb Figart Director, Stockton Center for Economic & Financial Literacy Deb.Figart@stockton.edu Why this Presentation? The federal online, required

Post-Loan (Exit) Counseling Supplement: Prepared by: Dr. Deb Figart Director, Stockton Center for Economic & Financial Literacy Deb.Figart@stockton.edu Why this Presentation? The federal online, required

2/26/2015 SENIOR LOAN EXIT INTERVIEW DENTAL HYGIENE CLASS OF Repayment Strategies for Managing Your Student Loans

SENIOR LOAN EXIT INTERVIEW DENTAL HYGIENE CLASS OF 2015 Repayment Strategies for Managing Your Student Loans 1 Considerations Multiple ways to effectively handle your student loan debt Constantly evaluate

SENIOR LOAN EXIT INTERVIEW DENTAL HYGIENE CLASS OF 2015 Repayment Strategies for Managing Your Student Loans 1 Considerations Multiple ways to effectively handle your student loan debt Constantly evaluate

Class of 2018! Congratulations! University of Louisville School of Medicine. From the SOM Financial Aid Office. aamc.org/first

From the SOM Financial Aid Office Congratulations! University of Louisville School of Medicine Class of 2018! 1 Student Loans and Repayment Strategies Prepared for the Graduating Class of 2018 Leslie R.

From the SOM Financial Aid Office Congratulations! University of Louisville School of Medicine Class of 2018! 1 Student Loans and Repayment Strategies Prepared for the Graduating Class of 2018 Leslie R.

c» BALANCE C:» Financially Empowering You Repaying Student Loans Podcast [Music plays] Nikki:

![c» BALANCE C:» Financially Empowering You Repaying Student Loans Podcast [Music plays] Nikki:](/thumbs/77/76062165.jpg "c» BALANCE C:» Financially Empowering You Repaying Student Loans Podcast [Music plays] Nikki:") Repaying Student Loans Podcast [Music plays] Nikki: You re listening to Repaying student loans. Hi. I m Nicky, your host for today s podcast. If you re intimidated by the prospect of paying back a student

Repaying Student Loans Podcast [Music plays] Nikki: You re listening to Repaying student loans. Hi. I m Nicky, your host for today s podcast. If you re intimidated by the prospect of paying back a student

Student Loan Repayment Workshop. Amanda Seitz Direct Loan Coordinator - Student Financial Services

Student Loan Repayment Workshop Amanda Seitz Direct Loan Coordinator - Student Financial Services Amanda.seitz@purchase.edu (914) 251-6080 Types of Student Loans Subsidized Direct Loan fixed interest loan

Student Loan Repayment Workshop Amanda Seitz Direct Loan Coordinator - Student Financial Services Amanda.seitz@purchase.edu (914) 251-6080 Types of Student Loans Subsidized Direct Loan fixed interest loan

Introduction. Entrance Counseling Guide for Borrowers

Entrance Counseling Guide for Borrowers Introduction Your William D. Ford Federal Direct Loans are made directly to you by the U.S. Department of Education (ED) through the school(s) you attend. ED is

Entrance Counseling Guide for Borrowers Introduction Your William D. Ford Federal Direct Loans are made directly to you by the U.S. Department of Education (ED) through the school(s) you attend. ED is

1. Career goals and repayment objectives 2. What you borrowed and when your loans come due 3. Repayment options, including consolidation and service

1. Career goals and repayment objectives 2. What you borrowed and when your loans come due 3. Repayment options, including consolidation and service programs 4. Rights and Responsibilities, resources,

1. Career goals and repayment objectives 2. What you borrowed and when your loans come due 3. Repayment options, including consolidation and service programs 4. Rights and Responsibilities, resources,

Student Loan Debt Management

Student Loan Debt Management OVERVIEW Recent Market and Regulatory Changes Identify your Loans Evaluating Federal Consolidation Federal Loan Payment Relief Programs Public Service Loan Forgiveness LRAP

Student Loan Debt Management OVERVIEW Recent Market and Regulatory Changes Identify your Loans Evaluating Federal Consolidation Federal Loan Payment Relief Programs Public Service Loan Forgiveness LRAP

How are you feeling about your student loan debt? 2017 Association of American Medical Colleges. All rights reserved. aamc.org/first/graduating-edm

How are you feeling about your student loan debt? 2017 Association of American Medical Colleges. All rights reserved. aamc.org/first/graduating-edm Student Loan Repayment Strategies Julie Gilbert Sr. Education

How are you feeling about your student loan debt? 2017 Association of American Medical Colleges. All rights reserved. aamc.org/first/graduating-edm Student Loan Repayment Strategies Julie Gilbert Sr. Education

How U.S. Universities Spend Money Paying for college

Student Loans (UXL) Student loan debt has risen alarmingly in the last several years. (Student loans are loans that help students pay for college tuition, books, and living expenses.) Going to college

Student Loans (UXL) Student loan debt has risen alarmingly in the last several years. (Student loans are loans that help students pay for college tuition, books, and living expenses.) Going to college

DEBT MANAGEMENT FOR JUILLIARD GRADUATES. Presented by the Office of Financial Aid

DEBT MANAGEMENT FOR JUILLIARD GRADUATES Presented by the Office of Financial Aid Broad Strokes Terms and Legislation Explained TERMS TO KNOW Servicer An organization that monitors loans while borrowers

DEBT MANAGEMENT FOR JUILLIARD GRADUATES Presented by the Office of Financial Aid Broad Strokes Terms and Legislation Explained TERMS TO KNOW Servicer An organization that monitors loans while borrowers

Avoiding Student Loan Default

Avoiding Student Loan Default - 321 Loans https://www.321financial.com/avoiding-student-loan-default/ About Us Reviews Blog Contact Us File a complaint Review us SEARCH Recent Posts Credit Card Debt and

Avoiding Student Loan Default - 321 Loans https://www.321financial.com/avoiding-student-loan-default/ About Us Reviews Blog Contact Us File a complaint Review us SEARCH Recent Posts Credit Card Debt and

Loan Repayment Strategy Session

Loan Repayment Strategy Session California College of the Arts Spring 2012 Scott Cline Associate Director of Financial Aid Overview of Loans Subsidized (FFEL or Direct) Loans Year Interest Rate (Undergraduate)

Loan Repayment Strategy Session California College of the Arts Spring 2012 Scott Cline Associate Director of Financial Aid Overview of Loans Subsidized (FFEL or Direct) Loans Year Interest Rate (Undergraduate)

CHAPTER TEN FREQUENTLY ASKED LOAN QUESTIONS

1. What is a Grace Period? CHAPTER TEN FREQUENTLY ASKED LOAN QUESTIONS A Grace Period is a block time frame (defined in your promissory note) where you are not required to make any loan payments. A student

1. What is a Grace Period? CHAPTER TEN FREQUENTLY ASKED LOAN QUESTIONS A Grace Period is a block time frame (defined in your promissory note) where you are not required to make any loan payments. A student

Financial Aid Package

2014 2015 Academic Year Financial Aid Package Understanding Your Financial Aid TABLE OF CONTENTS. Making Villanova University Affordable. Next Steps You Should Take Page 1. Sources of Aid That May be Listed

2014 2015 Academic Year Financial Aid Package Understanding Your Financial Aid TABLE OF CONTENTS. Making Villanova University Affordable. Next Steps You Should Take Page 1. Sources of Aid That May be Listed

PUBLIC SERVICE LOAN REPAYMENT STRATEGIES

1 PUBLIC SERVICE LOAN REPAYMENT STRATEGIES Spring 2014 Jeffrey Hanson Education Services University of California Hastings College of the Law Good News! 2 Borrowers now have: Loan forgiveness options Income-defined

1 PUBLIC SERVICE LOAN REPAYMENT STRATEGIES Spring 2014 Jeffrey Hanson Education Services University of California Hastings College of the Law Good News! 2 Borrowers now have: Loan forgiveness options Income-defined

PUBLIC SERVICE LOAN REPAYMENT STRATEGIES

1 PUBLIC SERVICE LOAN REPAYMENT STRATEGIES Spring 2014 Jeffrey Hanson Education Services University of California Hastings College of the Law Good News! 2 Borrowers now have: Loan forgiveness options Income-defined

1 PUBLIC SERVICE LOAN REPAYMENT STRATEGIES Spring 2014 Jeffrey Hanson Education Services University of California Hastings College of the Law Good News! 2 Borrowers now have: Loan forgiveness options Income-defined

Managing Debt, Delinquency, And Default

Managing Debt, Delinquency, And Default Speaker: Christie Smith Date: October 18, 2018 Agenda 2 Understanding Student Loan Debt Preventing Delinquency and Default Keys to Successful Loan Repayment Tools

Managing Debt, Delinquency, And Default Speaker: Christie Smith Date: October 18, 2018 Agenda 2 Understanding Student Loan Debt Preventing Delinquency and Default Keys to Successful Loan Repayment Tools

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed OASFAA - April 2016

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed OASFAA - April 2016 Latest Report Class of 2014 average student loan debt $28,950 2014 unemployment rate for college graduates 7.2%

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed OASFAA - April 2016 Latest Report Class of 2014 average student loan debt $28,950 2014 unemployment rate for college graduates 7.2%

Repayment Strategies Title Lorem Ipsum. Quillen College of Medicine

Repayment Strategies Title Lorem Ipsum Subhead duis tincidunt lectus Quillen College of Medicine Authors Julie Gilbert Sr. Education Debt Management Specialist April 10, 2018 Agenda aamc.org/nextsteps

Repayment Strategies Title Lorem Ipsum Subhead duis tincidunt lectus Quillen College of Medicine Authors Julie Gilbert Sr. Education Debt Management Specialist April 10, 2018 Agenda aamc.org/nextsteps

Call: Frequently Asked Questions about Student Loans

Frequently Asked Questions about Student Loans What are private student loans? Private student loans are meant to help students fill the funding gaps that federal aid can leave behind. Private loans should

Frequently Asked Questions about Student Loans What are private student loans? Private student loans are meant to help students fill the funding gaps that federal aid can leave behind. Private loans should

New Directions. New Directions. A Guide to Repaying Your Federal Student Loans

New Directions New Directions A Guide to Repaying Your Federal Student Loans This booklet is a resource to help you learn more about: Your rights and responsibilities as a student loan borrower of a Federal

New Directions New Directions A Guide to Repaying Your Federal Student Loans This booklet is a resource to help you learn more about: Your rights and responsibilities as a student loan borrower of a Federal

Repayment Plans. October Kim Wells U.S. Department of Education 1. Agenda. Standard Plan. Default repayment plan Loans eligible for inclusion

Repayment Plans U.S. Department of Education Agenda Standard Plan Extended Plan Graduated Plan Income-Driven Plans Resources 2 Standard Plan Default repayment plan Loans eligible for inclusion Direct Subsidized

Repayment Plans U.S. Department of Education Agenda Standard Plan Extended Plan Graduated Plan Income-Driven Plans Resources 2 Standard Plan Default repayment plan Loans eligible for inclusion Direct Subsidized

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed Latest Report Class of 2015 average student loan debt $30,100 44% of college grads in their 20s are employed in low-wage jobs Many

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed Latest Report Class of 2015 average student loan debt $30,100 44% of college grads in their 20s are employed in low-wage jobs Many

MISSOURI WESTERN FINANCIAL AID AND BUSINESS OFFICE. Helping you Achieve your Goals

MISSOURI WESTERN FINANCIAL AID AND BUSINESS OFFICE Helping you Achieve your Goals Not having your Financial Aid in place WELL BEFORE the first day of class causes high levels of Want to start school stress-free?

MISSOURI WESTERN FINANCIAL AID AND BUSINESS OFFICE Helping you Achieve your Goals Not having your Financial Aid in place WELL BEFORE the first day of class causes high levels of Want to start school stress-free?

COUNSELING GUIDE FOR DIRECT LOAN BORROWERS

Entrance COUNSELING GUIDE FOR DIRECT LOAN BORROWERS U.S. Department of Education Arne Duncan Secretary Federal Student Aid James W. Runcie Chief Operating Officer December 2013 Revised: July 2014 Online

Entrance COUNSELING GUIDE FOR DIRECT LOAN BORROWERS U.S. Department of Education Arne Duncan Secretary Federal Student Aid James W. Runcie Chief Operating Officer December 2013 Revised: July 2014 Online

Sam Houston State University

Sam Houston State University Division of Student Services - SMMC Services Personal Financial Counseling/Coaching Classroom Presentations Workshops Personnel 2 Full-time Staff members 5 Student Employees

Sam Houston State University Division of Student Services - SMMC Services Personal Financial Counseling/Coaching Classroom Presentations Workshops Personnel 2 Full-time Staff members 5 Student Employees

Financial Aid Basics 2.0: The College Years

Financial Aid Basics 2.0: The College Years 2 Objectives o Students will understand recent and upcoming changes to the FAFSA, including FSA IDs and Prior-Prior-Year. o Students will review financial aid

Financial Aid Basics 2.0: The College Years 2 Objectives o Students will understand recent and upcoming changes to the FAFSA, including FSA IDs and Prior-Prior-Year. o Students will review financial aid

How are you feeling about your student loan debt? 2017 Association of American Medical Colleges. All rights reserved. aamc.org/first/graduating-edm

How are you feeling about your student loan debt? 2017 Association of American Medical Colleges. All rights reserved. aamc.org/first/graduating-edm Student Loan Repayment Strategies Julie Gilbert Sr. Education

How are you feeling about your student loan debt? 2017 Association of American Medical Colleges. All rights reserved. aamc.org/first/graduating-edm Student Loan Repayment Strategies Julie Gilbert Sr. Education

REPAYING YOUR FEDERAL FAMILY EDUCATION LOAN

What s Inside: Getting Started REPAYING YOUR FEDERAL FAMILY EDUCATION LOAN Understanding My Statement Repayment Plans Standard Income Sensitive Graduated Extended Income-Based Repayment (IBR) PLUS Interest

What s Inside: Getting Started REPAYING YOUR FEDERAL FAMILY EDUCATION LOAN Understanding My Statement Repayment Plans Standard Income Sensitive Graduated Extended Income-Based Repayment (IBR) PLUS Interest

2/22/2015 SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF Repayment Strategies for Managing Your Student Loans

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2015 Repayment Strategies for Managing Your Student Loans 1 Considerations Dental school graduates have great track record for repayment Multiple ways

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2015 Repayment Strategies for Managing Your Student Loans 1 Considerations Dental school graduates have great track record for repayment Multiple ways

Financing Options for Students and Parents

Financing Options for Students and Parents 2011-12 It is a fundamental principle of Princeton s aid program that no student is required to borrow to meet their determined financial need. Since 2001, grants

Financing Options for Students and Parents 2011-12 It is a fundamental principle of Princeton s aid program that no student is required to borrow to meet their determined financial need. Since 2001, grants