Between 2004 and 2014, the total student debt in the US tripled from $364 billion in 2004 to $1.16 trillion in 2014.

|

|

|

- Amelia Gray

- 5 years ago

- Views:

Transcription

1 1

2 Statistic s from the Federal Reserve Bank of New York February 2015 Between 2004 and 2014, the total student debt in the US tripled from $364 billion in 2004 to $1.16 trillion in Our research indicates that this increase in aggregate debt was due to increases in both the number of borrowers as well as increases in the average balance per borrower. Between 2004 and 2014, the number of borrowers increased by 92 percent from 23 million borrowers to 43 million. In the same period, average debt per borrower increased by 74 percent, from about $15,000 to $27,000. With respect to the rise in the number of borrowers, we find that a steadily increasing share of young people are taking out student loans: in 2004, only about 27 percent of 25 year olds had student debt while 9 years later, in 2013, the proportion of 25 years olds with student debt had increased to about 45 percent. 2

3 3

4 Free Tax Prep: this is where it all starts! The tax return is more and more integrated into financial aid. Returns must be done with accuracy and early in the year C4C: with FAFSA prep we get the chance to discuss financial aid process, learn financial aid terms, understand options / students can always come back with award letters if they need help understanding it / with scholarship mentoring students get one on one support seeking out free funding for school. Financial Education: Students have the option of taking a Money Management class before heading off to college so they can begin to understand how to manage their finances / Individuals who have already gotten into trouble or are worried about their budget and ability to pay their loan can meet one on one with a financial coach to discuss options 4

5 5

6 6

7 7

8 8

9 9

10 10

11 11

12 12

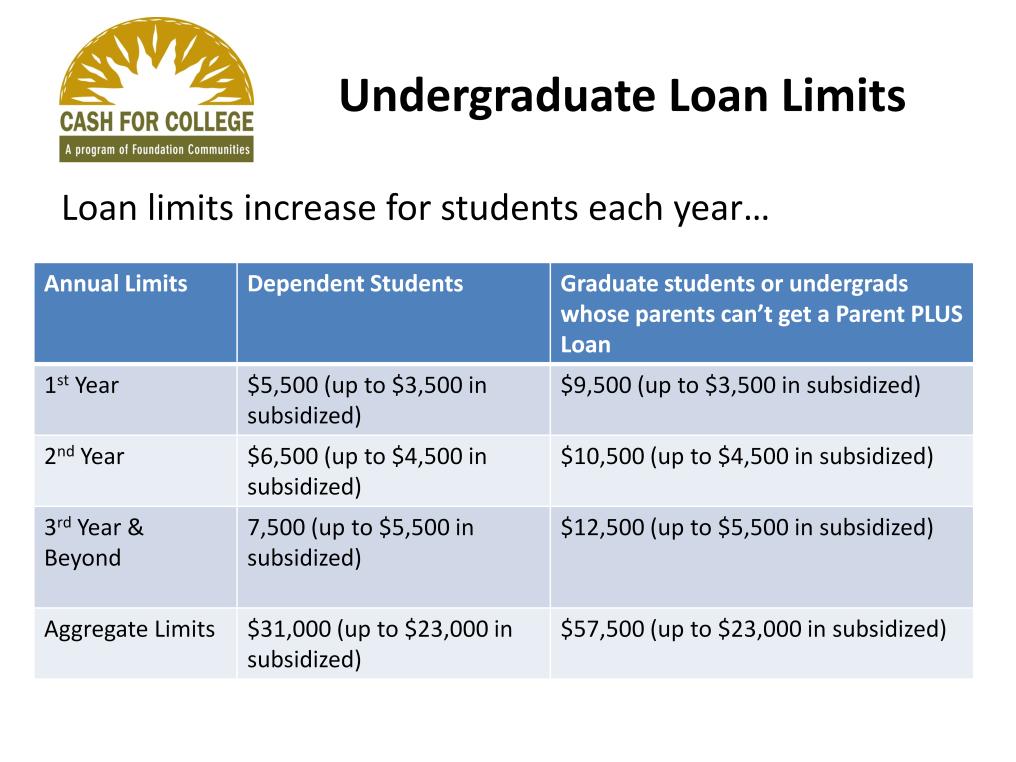

13 The Master Promissory Note (MPN) is a legal document in which you promise to repay your loan(s) and any accrued interest and fees to the U.S. Department of Education. It also explains the terms and conditions of your loan(s). Unless your school does not allow more than one loan to be made under the same MPN, you can borrow additional Direct Loans on a single MPN for up to 10 years. 13

14 14

15 15

16 16

17 17

18 18

19 19

20 20

21 Now we re going to focus on repayment issues. Although you may read lots of articles and news reports that the national default rates on student loans are currently on the rise, the majority of borrowers do pay off their loan obligation in full. 21

22 Once the borrower drops below half-time enrollment, a 6-month grace period begins. This 6-month period allows the borrower time to look for employment, and get ready for repayment. During the grace period, the loan servicer, and possibly the school and the guaranty agency, contact the borrower multiple times to remind him of the end date of the grace period, the importance of keeping accurate contact information of file, and who to ask for help with repayment, if necessary. Stafford loans enter repayment when the grace period ends. Technically, PLUS loans enter repayment when the loan is fully disbursed, but as we talked about previously, many borrowers are taking advantage of the new in-school and 6-month deferments that are available after the borrower and/or dependent student drops below half-time enrollment. 22

23 Without the right information student loan repayment can be pretty scary for borrowers! 23

24 The Institute for College Access & Success (TICAS) published state by state data for The national average is $28,400. Texas borrowers has a slightly lover average student loan debt of $25,244 with about 59% of students needing to borrow. 24

25 Unfortunately, many borrowers don t know where to find information that will provide them with all the options available for them to successfully manage their repayment. In Texas, the default rate is higher at 15.9%. The good news is that most borrowers do manage to pay off their student loans. However, that doesn t mean they don t have periods of delinquency and frustration and even default along the way! That s where our financial coaching and credit counseling programs can help! 25

26 So what repayment options are available to borrowers? There are a variety of payment plans to choose from, and borrowers can change repayment plans at least once per year. Borrowers will automatically be placed in a standard 10-year repayment period unless they request a different plan. Standard repayment means 120 monthly payments in equal amounts. Under this standard plan, though, the total time to repay the loan can exceed 10 years if the borrower uses a deferment or forbearance. Under the graduated plan, or what we sometimes call the optimistic plan, the monthly payment is scheduled to change increase at regular intervals. For example, every two years, over the repayment period. This is helpful for borrowers who expect a low entry level wage with regular wage increases. The extended plan is available to new borrowers as of October 7, 1998, who have outstanding interest and principal over $30,000. Extended repayment allows for a 25- year repayment term. Income-driven plans are also an option and one many of our clients should be able to take advantage of. 26

27 For many of our clients, the income-driven plans will be the best repayment option. Under the IBR, PAYE and ICR plans. And beginning in December 2015, a new REPAYE plan will be available, but only for Direct Loan borrowers. 27

28 This slide lists some of the main benefits of an income-driven repayment plan: Borrower must have a partial financial hardship. For IBR, the maximum monthly payment will be 10% (PAYE) or 15% (ICR, IBR) of discretionary income, the difference between your adjusted gross income and 150 percent of the poverty guideline for your family size and state of residence (other conditions apply). Monthly payments will be lower than payments under the 10-year standard plan. Payments change as the borrower s income changes; annual reapplication process. Borrower will pay more for your loan over time than under the 10-year standard plan. If borrower has not repaid loan in full after making the equivalent of 20 years (PAYE) or 25 years (ICR, IBR) of qualifying monthly payments, any outstanding balance on the loan will be forgiven. Under current IRS rules, amount forgiven is considered taxable income. The new REPAYE plan that will be available in December 2015, does not require a borrower to qualify. It s based solely on 10% of discretionary income and has a 20 or 25 year term depending on whether the borrower received loans for undergraduate or graduate study. 28

29 Before we look at each repayment plan, I want to share a helpful tool that borrowers can use as they re trying to decide which plan is best for them. Probably the questions going through most borrowers minds and causing the most stress are: What will my payment amount be? and Will I be able to afford it? An easy way for a borrower to estimate what the payment amount will look like under the various plans is to use the Department s Repayment Estimator calculator. This estimator lets the borrower compare what the monthly repayment amounts would likely be across repayment options available for Direct Loans. The income-sensitive plan which is only available to FFELP borrowers--is not included in the calculator. 29

30 Here s an example of the Department s Repayment Estimator calculator. In this example, you can see that the borrower qualifies for 5 different plans shown here in different colors. The tool also shows the estimated payment amount the borrower will pay under each plan. Borrowers can access by signing into their accounts online (with their PIN soon to be replaced with an FSA ID). 30

31 Regardless of which repayment plan a borrower chooses, sometimes a borrower has difficulty making his or her monthly payments. When that happens, the lender or the ED servicer can provide some temporary options for the borrower to postpone or reduce the monthly payments. The most advantageous of those options is a deferment. Every loan has some deferment options, but not all loan types have all deferments available to them. Deferments are benefits to which the borrower is entitled so if he qualifies, the lender must grant it. During deferment, payments are postponed. The most common reasons for deferment are a return to at least half-time enrollment (70%) and economic hardship (15%). Other reasons a deferment may be granted include a borrower who is employed in a public service position, military active duty, family leave/working mother, temporary disability, rehabilitation training, PEACE Corps service, and many others. 31

32 With certain exceptions ED pays the interest on behalf of the borrower for a subsidized Stafford loan and any underlying subsidized Stafford loan that is included in a consolidation loan. Interest is capitalized during deferment on unsubsidized Stafford loans, both Grad and Parent PLUS loans, and any underlying unsubsidized Stafford or PLUS that is included in a consolidation loan. But just like during the in-school status for these loan types, the borrower CAN pay interest if he or she wishes, rather than allowing it to capitalize. 32

33 If a borrower has exhausted her deferment eligibility, and still needs to postpone repayment, she can request a forbearance from her loan holder or ED servicer. In many cases, the granting of a forbearance is at the lender s or servicer s discretion, although there are some limited circumstances that require the lender or servicer to grant a forbearance; those are called a mandatory forbearance. A forbearance allows the borrower to cease, reduce, or extend repayment when she s willing to repay but is temporarily unable to do so. A forbearance may be granted for as little as a few months, or up to 12 months at a time, and it may or may not be extended after it expires. During forbearance, the borrower is responsible for all interest that accrues even for subsidized Stafford loans. So as you can see, a forbearance truly should be a last resort, since a borrower can quickly accrue large amounts of interest in a relatively short period of time, then re-enter repayment with even larger monthly payment that she may still be unable to manage. 33

34 Finally, let s talk about the federal consolidation loan. A variety of loan types Stafford and PLUS in the FFELP and FDLP, Perkins, and loans through the now-discontinued HEAL program, or Health Education Assistance Loan may be included in a consolidation loan, but doing so may not necessarily be in the best interest of the borrower. If a borrower considering consolidation, it s important to think about the interest rates on the loans that are being included in the consolidation loan, and in the case of Perkins loans, the cancellation benefits and longer grace period that will be lost upon consolidation. In order to consolidate, the borrower must be in his or her grace period or have entered repayment on each loan being consolidated. That means a borrower who is still in school is not eligible for consolidation. The interest rate on a consolidation loan is fixed, and depends on the interest rates of the loans that are included in the consolidation loan what we call underlying loans. The final rate is the weighted average of those underlying loans, rounded up to the nearest 1/8 th of one percent, and is capped at 8.25% 34

35 This slide shows the primary reasons why a borrower may choose consolidation as his repayment option. 35

36 Some borrowers with older FFELP loans may choose to consolidate into the Direct Loan Program to take advantage of the Public Service Loan Forgiveness Program which is only available for Direct loans. A borrower may also use consolidation to resolve a defaulted loan. I ll talk a little more about that in just a minute. 36

37 How many of you have worked with clients who have defaulted student loans? Do they ask how their loan balance got so high? Let s look at a simple example of a student in Texas who only borrowed the average $25,400 in loans, graduated in 4 years, and then defaulted. To keep it simple, I m also showing all unsubsidized loans so the borrower is responsible for all interest that accrues. Default means that the borrower has not made any payments within 270 days or about 9 months. So, about 5 years after beginning school, the borrower defaults with an outstanding loan balance of about $30,000. If the borrower does not establish repayment arrangements for the defaulted loan, collection costs are added, and the loan balance continues to balloon with most of the increase due to collection costs. As financial coaches, it s important to keep our clients out of default; and for those who have already defaulted, help them resolve that default as soon as possible! 37

38 How does a borrower resolve a defaulted loan? Again, if a borrower does not make any payment on a student loan for 270 days, the loan is considered to be in default. Once a loan defaults, the lender transfers ownership of the loan to a guaranty agency or ED who is now responsible for collecting the loan debt. Before turning to involuntary repayment strategies (which I ll talk about on the next slide), all efforts are made to encourage the borrower to make voluntary payments. Of course, a borrower can always pay his loan in full, but that doesn t often happen. One program used to enable a borrower to repair his or her credit rating and establish good repayment habits is rehabilitation. Through the rehabilitation program, the borrower agrees to make 9 voluntary, on-time, consecutive, monthly payments on his defaulted loans. Once the borrower fulfills the agreement, the loan is sold to a lender and taken out of the default status. And most importantly, the default is removed from the borrower s credit report. But it s important for the borrower to continue to make payments because if he slips and defaults, again, he will not have the option to rehabilitate a second time. Consolidation is also a tool to help borrowers resolve a defaulted loan. After making three voluntary, on-time, payments, he can consolidate and immediately reinstate eligibility for federal student aid. In this process the default is not removed from the borrower s credit record. 38

39 Unfortunately, if a borrower does not begin to repay his or her defaulted loan, the guaranty agency or ED may use a variety of tools to collect the debt. AWG means that up to 15% of the borrower s disposable pay is taken out of his paycheck (by his employer) and applied to his loan. Treasury offset means that the IRS income tax refunds are intercepted and applied to the outstanding loan balance. In addition, the GA may seize lottery winnings and withhold of professional licenses. It s important to make sure a borrower understands that except for very limited situations a Federal loan debt never goes away! ED will continue to collect on the loan, and actually has collection tools above and beyond those of the lender and guaranty agency. For example, ED can and will seize Social Security benefits. ED will garnish your retirement check if necessary. 39

40 40

41 41

Objectives. Objectives. Loans 101. Purpose and types of Federal loans. Life cycle of a Federal loan. Repayment options. Delinquency and default

Loans 101 Becky Davis and Debbie Murphy Ascendium Education Solutions Objectives 1 2 3 Purpose and types of Federal loans Life cycle of a Federal loan Repayment options 2019 ILASFAA Annual Conference 2

Loans 101 Becky Davis and Debbie Murphy Ascendium Education Solutions Objectives 1 2 3 Purpose and types of Federal loans Life cycle of a Federal loan Repayment options 2019 ILASFAA Annual Conference 2

Repayment Overview. A guide to repaying your federal student loans

Repayment Overview A guide to repaying your federal student loans Table of Contents A guide to repaying your federal student loans...2 Learning about available repayment plans...4 Standard Repayment Plan...4

Repayment Overview A guide to repaying your federal student loans Table of Contents A guide to repaying your federal student loans...2 Learning about available repayment plans...4 Standard Repayment Plan...4

REPAYING YOUR FEDERAL FAMILY EDUCATION LOAN

What s Inside: Getting Started REPAYING YOUR FEDERAL FAMILY EDUCATION LOAN Understanding My Statement Repayment Plans Standard Income Sensitive Graduated Extended Income-Based Repayment (IBR) PLUS Interest

What s Inside: Getting Started REPAYING YOUR FEDERAL FAMILY EDUCATION LOAN Understanding My Statement Repayment Plans Standard Income Sensitive Graduated Extended Income-Based Repayment (IBR) PLUS Interest

What Is Direct Loan Exit Counseling?

What Is Direct Loan Exit Counseling? Before you graduate, or if you drop below less-than-half-time enrollment, you must complete a Direct Loan (Stafford) Exit Counseling session. You can complete the entire

What Is Direct Loan Exit Counseling? Before you graduate, or if you drop below less-than-half-time enrollment, you must complete a Direct Loan (Stafford) Exit Counseling session. You can complete the entire

Direct Loan Exit Counseling Guide

2018 Federal Student Aid Direct Loan Exit Counseling Guide For Borrowers of Direct Loans and Federal Family Education Program Loans U.S. Department of Education Betsy DeVos Secretary Federal Student Aid

2018 Federal Student Aid Direct Loan Exit Counseling Guide For Borrowers of Direct Loans and Federal Family Education Program Loans U.S. Department of Education Betsy DeVos Secretary Federal Student Aid

Understanding and Managing your Student Loans and Repayment

Understanding and Managing your Student Loans and Financial Literacy Programs University of Colorado Denver Presenter: M. Lesa Briggs Financial Literacy & Wellness After this presentation, you will be

Understanding and Managing your Student Loans and Financial Literacy Programs University of Colorado Denver Presenter: M. Lesa Briggs Financial Literacy & Wellness After this presentation, you will be

Private Loan Guide. Apply for free, federal and state financial aid programs:

Private loan basics Private student loans are non-federal loans. Private Loan Guide You should only borrow private loans to fund your education as a last resort. Do all of the following before you consider

Private loan basics Private student loans are non-federal loans. Private Loan Guide You should only borrow private loans to fund your education as a last resort. Do all of the following before you consider

Repaying your federal student loans

Repaying your federal student loans Many borrowers don t worry about their student loans until they graduate or leave school. But you should immediately notify your loan servicer and school in writing

Repaying your federal student loans Many borrowers don t worry about their student loans until they graduate or leave school. But you should immediately notify your loan servicer and school in writing

New Directions. New Directions. A Guide to Repaying Your Federal Student Loans

New Directions New Directions A Guide to Repaying Your Federal Student Loans This booklet is a resource to help you learn more about: Your rights and responsibilities as a student loan borrower of a Federal

New Directions New Directions A Guide to Repaying Your Federal Student Loans This booklet is a resource to help you learn more about: Your rights and responsibilities as a student loan borrower of a Federal

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed Latest Report Class of 2015 average student loan debt $30,100 44% of college grads in their 20s are employed in low-wage jobs Many

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed Latest Report Class of 2015 average student loan debt $30,100 44% of college grads in their 20s are employed in low-wage jobs Many

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed OASFAA - April 2016

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed OASFAA - April 2016 Latest Report Class of 2014 average student loan debt $28,950 2014 unemployment rate for college graduates 7.2%

Repayment Plans 2.0: Strategies and Insights to Help Borrowers Succeed OASFAA - April 2016 Latest Report Class of 2014 average student loan debt $28,950 2014 unemployment rate for college graduates 7.2%

Student Loan Terms to Know

Definitions of terms related to federal student loans and the Nelnet repayment process Accrue The act of interest accumulating on the borrower s principal balance Adjusted Gross Income (AGI) The adjusted

Definitions of terms related to federal student loans and the Nelnet repayment process Accrue The act of interest accumulating on the borrower s principal balance Adjusted Gross Income (AGI) The adjusted

623 POLICY Federal Direct Loans/Plus Statement of Policy

623 POLICY Federal Direct /Plus 623.1 Statement of Policy The Redlands Community College Financial Aid Office participates in Loan Programs to assist students with financial loans during their enrollment

623 POLICY Federal Direct /Plus 623.1 Statement of Policy The Redlands Community College Financial Aid Office participates in Loan Programs to assist students with financial loans during their enrollment

Exit Counseling M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES

Exit Counseling FALL 2017 M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES Agenda Loan types and interest rates Grace periods Repaying

Exit Counseling FALL 2017 M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES Agenda Loan types and interest rates Grace periods Repaying

About Salt Money Management Student Loan Repayment

About Salt Money Management Student Loan Repayment Michele Almeida Senior Associate Director of SFS Jane Aube Loan Programs & Compliance Specialist Kim Downs-Burns AVP Student Financial Services American

About Salt Money Management Student Loan Repayment Michele Almeida Senior Associate Director of SFS Jane Aube Loan Programs & Compliance Specialist Kim Downs-Burns AVP Student Financial Services American

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS U.S. Department of Education Arne Duncan Secretary Federal Student Aid James W. Runcie Chief Operating Officer

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS U.S. Department of Education Arne Duncan Secretary Federal Student Aid James W. Runcie Chief Operating Officer

Federal Student Loan Repayment

Federal Student Loan Repayment The Road to Zero Know your financial goals. Know what you owe. Know what time it is. Know your options. Select your plan. Manage your payments. AccessGroup.org Financial

Federal Student Loan Repayment The Road to Zero Know your financial goals. Know what you owe. Know what time it is. Know your options. Select your plan. Manage your payments. AccessGroup.org Financial

What is an income-driven repayment plan?

Income-Driven Plans for Federal Student Loans What is an income-driven repayment plan? An income-driven repayment plan is a repayment plan that sets your monthly student loan payment at an amount that

Income-Driven Plans for Federal Student Loans What is an income-driven repayment plan? An income-driven repayment plan is a repayment plan that sets your monthly student loan payment at an amount that

Student Loan Repayment. Health Sciences Financial Aid Office May 17 th, 2018

Student Loan Repayment Health Sciences Financial Aid Office May 17 th, 2018 TOPICS KNOW YOUR LOAN PORTFOLIO HOW TO POSTPONE PAYMENTS REPAYMENT PLANS OTHER CONSIDERATIONS CREDIT QUESTIONS KNOW YOUR LOAN

Student Loan Repayment Health Sciences Financial Aid Office May 17 th, 2018 TOPICS KNOW YOUR LOAN PORTFOLIO HOW TO POSTPONE PAYMENTS REPAYMENT PLANS OTHER CONSIDERATIONS CREDIT QUESTIONS KNOW YOUR LOAN

THE ROAD TO ZERO. A Strategic Approach to Student Loan Repayment. Financial education resources from a nonprofit you can trust. AccessLex.

THE ROAD TO ZERO A Strategic Approach to Student Loan Repayment Financial education resources from a nonprofit you can trust. AccessLex.org 1 GET STARTED. 3 KNOW WHAT YOU OWE. 4 KNOW YOUR OPTIONS. 6 Debt-Driven

THE ROAD TO ZERO A Strategic Approach to Student Loan Repayment Financial education resources from a nonprofit you can trust. AccessLex.org 1 GET STARTED. 3 KNOW WHAT YOU OWE. 4 KNOW YOUR OPTIONS. 6 Debt-Driven

Financial Literacy South Florida State College

Financial Literacy South Florida State College Financial Literacy This Financial Literacy workshop provides tips on managing money, keeping track of your finances and planning ahead. You will also learn

Financial Literacy South Florida State College Financial Literacy This Financial Literacy workshop provides tips on managing money, keeping track of your finances and planning ahead. You will also learn

Borrower s Rights and Responsibilities Statement Important Notice: 5. Use of Loan Money 1. Governing Law

Borrower s Rights and Responsibilities Statement Important Notice: The Borrower s Rights and Responsibilities Statement provides additional information about the terms and conditions of loans you receive

Borrower s Rights and Responsibilities Statement Important Notice: The Borrower s Rights and Responsibilities Statement provides additional information about the terms and conditions of loans you receive

Please Check In and Pick Up Your Folder. Exit Counseling Folder

Exit Counseling Please Check In and Pick Up Your Folder Exit Counseling Folder Personalized federal student loan balances Letter from our office and bookmark Loan Servicer information Loan Tips and Resources

Exit Counseling Please Check In and Pick Up Your Folder Exit Counseling Folder Personalized federal student loan balances Letter from our office and bookmark Loan Servicer information Loan Tips and Resources

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS U.S. Department of Education Betsy DeVos Secretary Federal Student Aid A. Wayne Johnson Chief Operating Officer

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS U.S. Department of Education Betsy DeVos Secretary Federal Student Aid A. Wayne Johnson Chief Operating Officer

Student Loan Exit Counseling Graduate/Professional

Student Loan Exit Counseling Graduate/Professional To successfully manage loan repayment... Understand the basic terms and conditions of your loans. Know how much you have to repay, when and to whom. Define

Student Loan Exit Counseling Graduate/Professional To successfully manage loan repayment... Understand the basic terms and conditions of your loans. Know how much you have to repay, when and to whom. Define

Direct Loan: Post-Graduation

Direct Loan: Post-Graduation Direct Loan Repayment Glossary: Before we begin Principal: The actual dollar figure of the amount borrowed Interest: Periodic fee charged to borrower; usually a percentage

Direct Loan: Post-Graduation Direct Loan Repayment Glossary: Before we begin Principal: The actual dollar figure of the amount borrowed Interest: Periodic fee charged to borrower; usually a percentage

Exit Counseling M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES

Exit Counseling SPRING 2018 M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES Agenda Loan types and interest rates Grace periods

Exit Counseling SPRING 2018 M I D D L E B U R Y I N S T I T U T E O F I N T E R N A T I O N A L S T U D I E S S T U D E N T F I N A N C I A L SERVICES Agenda Loan types and interest rates Grace periods

William D. Ford Federal Direct Loan Program Direct Subsidized Loan and Direct Unsubsidized Loan Borrower s Rights and Responsibilities Statement

Important Notice: This Borrower s Rights and Responsibilities Statement provides additional information about the terms and conditions of the loans you receive under the accompanying Master Promissory

Important Notice: This Borrower s Rights and Responsibilities Statement provides additional information about the terms and conditions of the loans you receive under the accompanying Master Promissory

Ten Things You Should Know About Student Loans

Ten Things You Should Know About Student Loans 1: BORROW ONLY WHAT YOU NEED 4: UNDERSTAND YOUR LOANS There are several different kinds of loans. Here are some key factors to be aware of: 7: MAKE PAYMENTS

Ten Things You Should Know About Student Loans 1: BORROW ONLY WHAT YOU NEED 4: UNDERSTAND YOUR LOANS There are several different kinds of loans. Here are some key factors to be aware of: 7: MAKE PAYMENTS

STUDENT LOAN REPAYMENT. Leslie Tobakos Registrar, Financial Aid & Admissions Manager Cranbrook Academy of Art

STUDENT LOAN REPAYMENT Leslie Tobakos Registrar, Financial Aid & Admissions Manager Cranbrook Academy of Art In this world nothing can be said to be certain, except death and taxes. Benjamin Franklin,

STUDENT LOAN REPAYMENT Leslie Tobakos Registrar, Financial Aid & Admissions Manager Cranbrook Academy of Art In this world nothing can be said to be certain, except death and taxes. Benjamin Franklin,

The Truth About Student Loans JumpStart Conference May Copyright 2016 Finance Authority of Maine

The Truth About Student Loans JumpStart Conference May 2016 Copyright 2016 Finance Authority of Maine Loans TYPES William D Ford Federal Direct Loan Program (Direct) o Direct Subsidized and Direct Unsubsidized

The Truth About Student Loans JumpStart Conference May 2016 Copyright 2016 Finance Authority of Maine Loans TYPES William D Ford Federal Direct Loan Program (Direct) o Direct Subsidized and Direct Unsubsidized

Federal Student Aid. Direct Loan. Entrance Counseling Guide

2018 Federal Student Aid Direct Loan Entrance Counseling Guide U.S. Department of Education Betsy DeVos Secretary Federal Student Aid James Manning Acting Chief Operating Officer Federal Student Aid, an

2018 Federal Student Aid Direct Loan Entrance Counseling Guide U.S. Department of Education Betsy DeVos Secretary Federal Student Aid James Manning Acting Chief Operating Officer Federal Student Aid, an

Repayment of Your Student Loan Debt. your dream, your plan, your future

Repayment of Your Student Loan Debt your dream, your plan, your future Repayment of Your Student Loan Debt Table of Contents Introduction................................. 1 Basic Student Loan Terminology..................

Repayment of Your Student Loan Debt your dream, your plan, your future Repayment of Your Student Loan Debt Table of Contents Introduction................................. 1 Basic Student Loan Terminology..................

9/19/2013 BORROWERS HAVE MORE OPTIONS OBJECTIVES COUNSELING BORROWERS ON PAY AS YOU EARN AND INCOME-DRIVEN PLANS

COUNSELING BORROWERS ON PAY AS YOU EARN AND INCOME-DRIVEN PLANS BORROWERS HAVE MORE OPTIONS We know many recent graduates are worried about repaying their student loans as our economy continues to recover,

COUNSELING BORROWERS ON PAY AS YOU EARN AND INCOME-DRIVEN PLANS BORROWERS HAVE MORE OPTIONS We know many recent graduates are worried about repaying their student loans as our economy continues to recover,

Student Loan Repayment Workshop. Amanda Seitz Direct Loan Coordinator - Student Financial Services

Student Loan Repayment Workshop Amanda Seitz Direct Loan Coordinator - Student Financial Services Amanda.seitz@purchase.edu (914) 251-6080 Types of Student Loans Subsidized Direct Loan fixed interest loan

Student Loan Repayment Workshop Amanda Seitz Direct Loan Coordinator - Student Financial Services Amanda.seitz@purchase.edu (914) 251-6080 Types of Student Loans Subsidized Direct Loan fixed interest loan

STATE OF NEW JERSEY STUDENT LOAN GUIDE

STATE OF NEW JERSEY STUDENT LOAN GUIDE New Jersey Higher Education Student Assistance Authority The Student Loan Guide provides general student loan information to assist students and their families in

STATE OF NEW JERSEY STUDENT LOAN GUIDE New Jersey Higher Education Student Assistance Authority The Student Loan Guide provides general student loan information to assist students and their families in

Student Loan Exit Counseling Graduate/Professional

Student Loan Exit Counseling Graduate/Professional School of Education & Social Policy McCormick School of Engineering Kellogg School of Management Bienen School of Music School of Professional Studies

Student Loan Exit Counseling Graduate/Professional School of Education & Social Policy McCormick School of Engineering Kellogg School of Management Bienen School of Music School of Professional Studies

Class of 2014 Loan Repayment Information Session

Class of 2014 Loan Repayment Information Session Presented by: Gina Soliz, Director of Financial Aid Emily Zipprich, Financial Aid Coordinator Spring 2014 What we ll cover today Summarize the types of

Class of 2014 Loan Repayment Information Session Presented by: Gina Soliz, Director of Financial Aid Emily Zipprich, Financial Aid Coordinator Spring 2014 What we ll cover today Summarize the types of

Federal Loan Borrowers REPAYMENT INFORMATION & STRATEGIES

Federal Loan Borrowers REPAYMENT INFORMATION & STRATEGIES Types of federal loans Direct Unsubsidized Loan (Direct Stafford Unsubsidized, William D. Ford Federal Direct Loan) Direct GradPLUS Loan (Direct

Federal Loan Borrowers REPAYMENT INFORMATION & STRATEGIES Types of federal loans Direct Unsubsidized Loan (Direct Stafford Unsubsidized, William D. Ford Federal Direct Loan) Direct GradPLUS Loan (Direct

Student Loan Repayment 101 Know Before You Owe. Holly Wright Program Manager

Student Loan Repayment 101 Know Before You Owe Holly Wright Program Manager Federal Student Aid Personal Finance Budgets Credit Reports Savings Account Reaching Financial Goals FRE E Private Student Loans

Student Loan Repayment 101 Know Before You Owe Holly Wright Program Manager Federal Student Aid Personal Finance Budgets Credit Reports Savings Account Reaching Financial Goals FRE E Private Student Loans

Repayment of Your Student Loan Debt. Office of Student Financial Assistance

Repayment of Your Student Loan Debt 1 Office of Student Financial Assistance 2 Agenda What are my rights and responsibilities? How do I choose a repayment plan? What are consequences of default? Where

Repayment of Your Student Loan Debt 1 Office of Student Financial Assistance 2 Agenda What are my rights and responsibilities? How do I choose a repayment plan? What are consequences of default? Where

PLAIN LANGUAGE DISCLOSURE FOR DIRECT SUBSIDIZED LOANS AND DIRECT UNSUBSIDIZED LOANS WILLIAM D. FORD FEDERAL DIRECT LOAN PROGRAM

1. GENERAL INFORMATION You are receiving a Direct Subsidized Loan and/or Direct Unsubsidized Loan under a Master Promissory Note (MPN) that you signed previously (see Item 2). This Plain Language Disclosure

1. GENERAL INFORMATION You are receiving a Direct Subsidized Loan and/or Direct Unsubsidized Loan under a Master Promissory Note (MPN) that you signed previously (see Item 2). This Plain Language Disclosure

1040 Form: The standard Internal Revenue Service (IRS) form that individuals use. to file their annual income tax returns.

form that individuals use. to file their annual income tax returns.") 1040 Form: The standard Internal Revenue Service (IRS) form that individuals use to file their annual income tax returns. 1040A Form: A simplified version of the 1040 form for individual income tax. To

1040 Form: The standard Internal Revenue Service (IRS) form that individuals use to file their annual income tax returns. 1040A Form: A simplified version of the 1040 form for individual income tax. To

Student Loan Ombudsman Caucus

Student Loan Ombudsman Caucus Repayment Plans Selecting the right repayment plan is important in the successful management of your student loan. You can change repayment plans contact your lender/servicer

Student Loan Ombudsman Caucus Repayment Plans Selecting the right repayment plan is important in the successful management of your student loan. You can change repayment plans contact your lender/servicer

Navigating Your Student Loan Repayment. Spring, 2016

Navigating Your Student Loan Repayment Spring, 2016 Overview Determining Your Loan Portfolio Understanding Loan Types Debt Management Considerations Repayment Plans Strategies for Repayment Other Resources

Navigating Your Student Loan Repayment Spring, 2016 Overview Determining Your Loan Portfolio Understanding Loan Types Debt Management Considerations Repayment Plans Strategies for Repayment Other Resources

Navigating Student Loan Repayment

Navigating Student Loan Repayment Objectives The goal of this presentation is to prepare you for student loan repayment, to encourage healthy financial habits, and to connect you with resources to help

Navigating Student Loan Repayment Objectives The goal of this presentation is to prepare you for student loan repayment, to encourage healthy financial habits, and to connect you with resources to help

c» BALANCE C:» Financially Empowering You Repaying Student Loans Podcast [Music plays] Nikki:

![c» BALANCE C:» Financially Empowering You Repaying Student Loans Podcast [Music plays] Nikki:](/thumbs/77/76062165.jpg "c» BALANCE C:» Financially Empowering You Repaying Student Loans Podcast [Music plays] Nikki:") Repaying Student Loans Podcast [Music plays] Nikki: You re listening to Repaying student loans. Hi. I m Nicky, your host for today s podcast. If you re intimidated by the prospect of paying back a student

Repaying Student Loans Podcast [Music plays] Nikki: You re listening to Repaying student loans. Hi. I m Nicky, your host for today s podcast. If you re intimidated by the prospect of paying back a student

Student Loan Repayment Strategy Session. Fernando Gomez Financial Aid

Student Loan Repayment Strategy Session Fernando Gomez Financial Aid AGENDA Your Federal Loan Portfolio Repayment Plans After Graduation Other Considerations Questions & Answers Your Federal/Private Student

Student Loan Repayment Strategy Session Fernando Gomez Financial Aid AGENDA Your Federal Loan Portfolio Repayment Plans After Graduation Other Considerations Questions & Answers Your Federal/Private Student

1. Career goals and repayment objectives 2. What you borrowed and when your loans come due 3. Repayment options, including consolidation and service

1. Career goals and repayment objectives 2. What you borrowed and when your loans come due 3. Repayment options, including consolidation and service programs 4. Rights and Responsibilities, resources,

1. Career goals and repayment objectives 2. What you borrowed and when your loans come due 3. Repayment options, including consolidation and service programs 4. Rights and Responsibilities, resources,

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS U.S. Department of Education Arne Duncan Secretary Federal Student Aid James W. Runcie Chief Operating Officer

EXIT COUNSELING GUIDE FOR BORROWERS OF DIRECT LOANS AND FEDERAL FAMILY EDUCATION PROGRAM LOANS U.S. Department of Education Arne Duncan Secretary Federal Student Aid James W. Runcie Chief Operating Officer

TAKE CHARGE OF LOAN REPAYMENT!

1 TAKE CHARGE OF LOAN REPAYMENT! Strategies for Managing Your Debt Successfully Spring 2013 Jeffrey Hanson Education Services University of San Diego School of Law Your Action Plan 4 Steps 2 1. Take stock

1 TAKE CHARGE OF LOAN REPAYMENT! Strategies for Managing Your Debt Successfully Spring 2013 Jeffrey Hanson Education Services University of San Diego School of Law Your Action Plan 4 Steps 2 1. Take stock

Managing Debt, Delinquency, And Default

Managing Debt, Delinquency, And Default Speaker: Christie Smith Date: October 18, 2018 Agenda 2 Understanding Student Loan Debt Preventing Delinquency and Default Keys to Successful Loan Repayment Tools

Managing Debt, Delinquency, And Default Speaker: Christie Smith Date: October 18, 2018 Agenda 2 Understanding Student Loan Debt Preventing Delinquency and Default Keys to Successful Loan Repayment Tools

2/26/2015 SENIOR LOAN EXIT INTERVIEW DENTAL HYGIENE CLASS OF Repayment Strategies for Managing Your Student Loans

SENIOR LOAN EXIT INTERVIEW DENTAL HYGIENE CLASS OF 2015 Repayment Strategies for Managing Your Student Loans 1 Considerations Multiple ways to effectively handle your student loan debt Constantly evaluate

SENIOR LOAN EXIT INTERVIEW DENTAL HYGIENE CLASS OF 2015 Repayment Strategies for Managing Your Student Loans 1 Considerations Multiple ways to effectively handle your student loan debt Constantly evaluate

Income-Driven Repayment Plans

Income-Driven Repayment Plans Agenda Income-Driven Repayment Plans Overview Income-Based Repayment Plan (IBR) Income-Contingent Repayment Plan (ICR) Pay As You Earn Plan (PAYE) Revised Pay As You Earn

Income-Driven Repayment Plans Agenda Income-Driven Repayment Plans Overview Income-Based Repayment Plan (IBR) Income-Contingent Repayment Plan (ICR) Pay As You Earn Plan (PAYE) Revised Pay As You Earn

Understanding Student Loans

Understanding Student Loans 2018 Student Loan Headlines Has Student Loan Debt Reached A Crisis Point? Beyond the Headlines: Is Student Debt Strangling Millennials' Chances for Success? Student Loan Debt

Understanding Student Loans 2018 Student Loan Headlines Has Student Loan Debt Reached A Crisis Point? Beyond the Headlines: Is Student Debt Strangling Millennials' Chances for Success? Student Loan Debt

Student Loans 101 Loan Repayment, Consolidation and Forgiveness. Holly Wright UM Financial Education Program Manager

Student Loans 101 Loan Repayment, Consolidation and Forgiveness Holly Wright UM Financial Education Program Manager Federal Student Aid Process Financial Aid Package Student Loans Personal Finance Budgeting

Student Loans 101 Loan Repayment, Consolidation and Forgiveness Holly Wright UM Financial Education Program Manager Federal Student Aid Process Financial Aid Package Student Loans Personal Finance Budgeting

Loan Repayment Strategy Session

Loan Repayment Strategy Session California College of the Arts Spring 2012 Scott Cline Associate Director of Financial Aid Overview of Loans Subsidized (FFEL or Direct) Loans Year Interest Rate (Undergraduate)

Loan Repayment Strategy Session California College of the Arts Spring 2012 Scott Cline Associate Director of Financial Aid Overview of Loans Subsidized (FFEL or Direct) Loans Year Interest Rate (Undergraduate)

Title IV Loans: Understanding The Basics

Title IV Loans: Understanding The Basics Objectives Review Title IV loans and their basic terms Review some changes to Title IV loans RMASFAA Conference 2012, Omaha, NE Just the Basics: entrance/exit counseling,

Title IV Loans: Understanding The Basics Objectives Review Title IV loans and their basic terms Review some changes to Title IV loans RMASFAA Conference 2012, Omaha, NE Just the Basics: entrance/exit counseling,

This presentation is for discussion purposes only.

This presentation is for discussion purposes only. Robyn Hughes School Ombudsman Navient 2 Agenda Student loan cycle What to communicate to borrowers For your students: 10 things to do before you make

This presentation is for discussion purposes only. Robyn Hughes School Ombudsman Navient 2 Agenda Student loan cycle What to communicate to borrowers For your students: 10 things to do before you make

CONTRA COSTA COLLEGE OFFICE OF FINANCIAL ASSISTANCE

CONTRA COSTA COLLEGE OFFICE OF FINANCIAL ASSISTANCE Default Management: A Plan for Student Success Written by: Default Management Team Monica Rodriguez, Financial Aid Supervisor Barbara Rance, Financial

CONTRA COSTA COLLEGE OFFICE OF FINANCIAL ASSISTANCE Default Management: A Plan for Student Success Written by: Default Management Team Monica Rodriguez, Financial Aid Supervisor Barbara Rance, Financial

DEBT MANAGEMENT FOR JUILLIARD GRADUATES. Presented by the Office of Financial Aid

DEBT MANAGEMENT FOR JUILLIARD GRADUATES Presented by the Office of Financial Aid Broad Strokes Terms and Legislation Explained TERMS TO KNOW Servicer An organization that monitors loans while borrowers

DEBT MANAGEMENT FOR JUILLIARD GRADUATES Presented by the Office of Financial Aid Broad Strokes Terms and Legislation Explained TERMS TO KNOW Servicer An organization that monitors loans while borrowers

LOAN REPAYMENT AND DEFAULT PREVENTION. Financial Aid and Scholarship Office

LOAN REPAYMENT AND DEFAULT PREVENTION Financial Aid and Scholarship Office 1 TOPICS TO BE COVERED Exit Counseling Loan Consolidation Repayment Options Deferment and Forbearance Discharge and Forgiveness

LOAN REPAYMENT AND DEFAULT PREVENTION Financial Aid and Scholarship Office 1 TOPICS TO BE COVERED Exit Counseling Loan Consolidation Repayment Options Deferment and Forbearance Discharge and Forgiveness

PERKINS LOAN ENTRANCE INTERVIEW CONFIRMATION

PERKINS LOAN ENTRANCE INTERVIEW CONFIRMATION Last Name First Name Student ID # Permanent Home Address City/State Zip Home Telephone Number Cell Telephone Number First and Last Name of nearest relative,

PERKINS LOAN ENTRANCE INTERVIEW CONFIRMATION Last Name First Name Student ID # Permanent Home Address City/State Zip Home Telephone Number Cell Telephone Number First and Last Name of nearest relative,

Student Loan - Know Before You Owe Questions & Answers Prepared by: The Counselor s Corner, Inc. April 25, 2018

Question: I'm interested on Student Loans, but for a Master s degree. Will this series of webinars provide information about this? Answer: Yes, we will provide a limited amount of information on Federal

Question: I'm interested on Student Loans, but for a Master s degree. Will this series of webinars provide information about this? Answer: Yes, we will provide a limited amount of information on Federal

2/22/2015 SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF Repayment Strategies for Managing Your Student Loans

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2015 Repayment Strategies for Managing Your Student Loans 1 Considerations Dental school graduates have great track record for repayment Multiple ways

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2015 Repayment Strategies for Managing Your Student Loans 1 Considerations Dental school graduates have great track record for repayment Multiple ways

TOPICS: Overview of the Office of Student Finance. Financial Aid Process Student Loans Repayment Options Budgeting Q & A

TOPICS: Overview of the Office of Student Finance Financial Aid Student Accounts Financial Aid Process Student Loans Repayment Options Budgeting Q & A Contact Information Located on the 10 th floor: Suite

TOPICS: Overview of the Office of Student Finance Financial Aid Student Accounts Financial Aid Process Student Loans Repayment Options Budgeting Q & A Contact Information Located on the 10 th floor: Suite

EXIT COUNSELING GUIDE

EXIT COUNSELING GUIDE For Federal Student Loan Borrowers Contents Intro 1 Exit Counseling Federal Student Loan Programs Getting Started 1 Types of Federal Student Loans Loan Terminology Repaying Your

EXIT COUNSELING GUIDE For Federal Student Loan Borrowers Contents Intro 1 Exit Counseling Federal Student Loan Programs Getting Started 1 Types of Federal Student Loans Loan Terminology Repaying Your

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF Repayment Strategies for Managing Your Student Loans

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2014 Repayment Strategies for Managing Your Student Loans Considerations Dental school graduates have great track record for repayment Multiple ways to

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2014 Repayment Strategies for Managing Your Student Loans Considerations Dental school graduates have great track record for repayment Multiple ways to

This form is for use by Vermont Student Assistance Corporation customers only. If your loans are not serviced by VSAC please contact your servicer

This form is for use by Vermont Student Assistance Corporation customers only. If your loans are not serviced by VSAC please contact your servicer directly for the appropriate application. This page intentionally

This form is for use by Vermont Student Assistance Corporation customers only. If your loans are not serviced by VSAC please contact your servicer directly for the appropriate application. This page intentionally

GLOSSARY OF LOAN TERMS

GLOSSARY OF LOAN TERMS Accrued Interest Interest that accumulates on the unpaid principal balance of a loan. Accrual Date The date on which interest charges on an educational loan begin to accrue. Amortization

GLOSSARY OF LOAN TERMS Accrued Interest Interest that accumulates on the unpaid principal balance of a loan. Accrual Date The date on which interest charges on an educational loan begin to accrue. Amortization

Bear Down on Student Loan Debt Options and Strategies for Repayment

Bear Down on Student Loan Debt Options and Strategies for Repayment Think About It Agenda Who We Are Student Loan Crisis Get Started Repayment Options Case Studies How We Can Help Q & A Who We Are Mission

Bear Down on Student Loan Debt Options and Strategies for Repayment Think About It Agenda Who We Are Student Loan Crisis Get Started Repayment Options Case Studies How We Can Help Q & A Who We Are Mission

FEDERAL PERKINS LOAN PROGRAM

FEDERAL PERKINS LOAN PROGRAM Bursar s Office UNIVERSITY OF DENVER 2197 S. UNIVERSITY BLVD. Suite 223 DENVER, COLORADO 80208 (303) 871-4944 www.du.edu/bursar GENERAL INFORMATION BORROWER RIGHTS & RESPONSIBILITIES

FEDERAL PERKINS LOAN PROGRAM Bursar s Office UNIVERSITY OF DENVER 2197 S. UNIVERSITY BLVD. Suite 223 DENVER, COLORADO 80208 (303) 871-4944 www.du.edu/bursar GENERAL INFORMATION BORROWER RIGHTS & RESPONSIBILITIES

Meet The Speakers. Sasha Grabenstetter, AFC Consumer Economics Educator University of Illinois Extension

Welcome to 1 Meet The Speakers Sasha Grabenstetter, AFC Consumer Economics Educator University of Illinois Extension Andrea Pellegrini Assistant Director Student Money Management Center 2 Where are you

Welcome to 1 Meet The Speakers Sasha Grabenstetter, AFC Consumer Economics Educator University of Illinois Extension Andrea Pellegrini Assistant Director Student Money Management Center 2 Where are you

Understanding Loan Repayment Plans and Alternative Repayment

Understanding Loan Repayment Plans and Alternative Repayment Session Outline Grace Periods Direct Loan and FFEL Repayment Plans Emphasis on Income Driven Plans Other Repayment Strategies Default Management

Understanding Loan Repayment Plans and Alternative Repayment Session Outline Grace Periods Direct Loan and FFEL Repayment Plans Emphasis on Income Driven Plans Other Repayment Strategies Default Management

What You Need to Know About Student Loans

Chapter 9 What You Need to Know About Student Loans Why should you find out about student loans? Unless you re one of the lucky few who manage to get full scholarships or you can afford to pay for your

Chapter 9 What You Need to Know About Student Loans Why should you find out about student loans? Unless you re one of the lucky few who manage to get full scholarships or you can afford to pay for your

Student Loan Debt Management

Student Loan Debt Management Jointly presented by 360 Degrees of Financial Literacy, AICPA Personal Financial Planning Division 360 Degrees of Financial Literacy AICPA Personal Financial Planning Division

Student Loan Debt Management Jointly presented by 360 Degrees of Financial Literacy, AICPA Personal Financial Planning Division 360 Degrees of Financial Literacy AICPA Personal Financial Planning Division

US Financing Information at

US Financing Information at Contents Introduction... 3 Available US Loans... 4 Eligibility and Assessment... 5 Repayment: Options and Obligations... 6 Refund and Return to Title IV Policy... 11 Satisfactory

US Financing Information at Contents Introduction... 3 Available US Loans... 4 Eligibility and Assessment... 5 Repayment: Options and Obligations... 6 Refund and Return to Title IV Policy... 11 Satisfactory

Managing Student Loans During Residency

FIRST for Medical Education Financial Information, Resources, Services, and Tools Managing Student Loans During Residency Nicole Knight Spring 2010 NOTE: All information and estimates are based on AAMC

FIRST for Medical Education Financial Information, Resources, Services, and Tools Managing Student Loans During Residency Nicole Knight Spring 2010 NOTE: All information and estimates are based on AAMC

Loan Repayment Strategies 1: Help Your Students Choose the Right Plan for Success

Loan Repayment Strategies 1: Help Your Students Choose the Right Plan for Success Loan Repayment Struggles Millions of students are senselessly defaulting on their debt while failing to take advantage

Loan Repayment Strategies 1: Help Your Students Choose the Right Plan for Success Loan Repayment Struggles Millions of students are senselessly defaulting on their debt while failing to take advantage

IBR and ICR Options to help borrowers manage repayment

IBR and ICR Options to help borrowers manage repayment Course outline Similarities of IBR and ICR plans Overview of IBR plan Overview of ICR plan Summary Upcoming changes Resources 1 Staggering growth

IBR and ICR Options to help borrowers manage repayment Course outline Similarities of IBR and ICR plans Overview of IBR plan Overview of ICR plan Summary Upcoming changes Resources 1 Staggering growth

Loan Information and Request Form

2018-2019 Loan Information and Request Form Understanding the Student Loan Process 3 Your financial aid file must be complete. 3 Complete the Loan Request Form (LRF). Your loan eligibility is calculated

2018-2019 Loan Information and Request Form Understanding the Student Loan Process 3 Your financial aid file must be complete. 3 Complete the Loan Request Form (LRF). Your loan eligibility is calculated

Loan Repayment Strategies: Help Your Students Choose the Right Plan for Success

Loan Repayment Strategies: Help Your Students Choose the Right Plan for Success Loan Repayment Struggles Millions of students are senselessly defaulting on their debt while failing to take advantage of

Loan Repayment Strategies: Help Your Students Choose the Right Plan for Success Loan Repayment Struggles Millions of students are senselessly defaulting on their debt while failing to take advantage of

Follow the below directions to print and mail your application and income documentation:

IDR Request Servicer Mailing Information Follow the below directions to print and mail your application and income documentation: 1. View your completed application (below). Note: Responses to all applicable

IDR Request Servicer Mailing Information Follow the below directions to print and mail your application and income documentation: 1. View your completed application (below). Note: Responses to all applicable

Issue Paper #6 Loans Group Final Consensus Language: Contextual Format 03/30/2012

Issue: Statutory Cite: Forbearance for Post-270 day Defaulted Loan Borrowers Prior to Lender Claim Payment or Transfer to ED Default Collections 428(c)(3) Regulatory Cites: 682.211(d) and 685.205 Summary

Issue: Statutory Cite: Forbearance for Post-270 day Defaulted Loan Borrowers Prior to Lender Claim Payment or Transfer to ED Default Collections 428(c)(3) Regulatory Cites: 682.211(d) and 685.205 Summary

Student Loans. Paying for college without taking out loans is ideal, but sometimes you need a loan to cover all the costs.

student loans 1 Student Loans Paying for college without taking out loans is ideal, but sometimes you need a loan to cover all the costs. At CAPlus, we recommend the following student loan resources (in

student loans 1 Student Loans Paying for college without taking out loans is ideal, but sometimes you need a loan to cover all the costs. At CAPlus, we recommend the following student loan resources (in

REPAYING STUDENT LOANS

REPAYING STUDENT LOANS 1 It is not unusual for college tuition to cost $30,000 or more a year. Some students are able to pay for it with savings or get grants or scholarships. However, many have to turn

REPAYING STUDENT LOANS 1 It is not unusual for college tuition to cost $30,000 or more a year. Some students are able to pay for it with savings or get grants or scholarships. However, many have to turn

Repayment Strategies for Dental School Graduates

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2018 Repayment Strategies for Dental School Graduates Considerations Dental school graduates have a great track record for repayment Use free resources

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2018 Repayment Strategies for Dental School Graduates Considerations Dental school graduates have a great track record for repayment Use free resources

MONEY? Your Guide to Federal Stafford and PLUS Loans. Oklahoma Guaranteed Student Loan Program

ARE YOU LOOKING FOR MONEY? Your Guide to Federal Stafford and PLUS Loans Oklahoma Guaranteed Student Loan Program A division of the Oklahoma State Regents for Higher Education A college education is a

ARE YOU LOOKING FOR MONEY? Your Guide to Federal Stafford and PLUS Loans Oklahoma Guaranteed Student Loan Program A division of the Oklahoma State Regents for Higher Education A college education is a

PUBLIC SERVICE LOAN FORGIVENESS

PUBLIC SERVICE LOAN FORGIVENESS Presented by: Scott Harrison, Assistant Director Student Financial Services (SFS) PSLF Program Basics The remaining balance on your qualified Direct Loans is forgiven and

PUBLIC SERVICE LOAN FORGIVENESS Presented by: Scott Harrison, Assistant Director Student Financial Services (SFS) PSLF Program Basics The remaining balance on your qualified Direct Loans is forgiven and

FEDERAL STUDENT LOANS. Basics for Students

FEDERAL STUDENT LOANS Basics for Students 2 U.S. Department of Education Arne Duncan Secretary Federal Student Aid James W. Runcie Chief Operating Officer Customer Experience Office Brenda F. Wensil Chief

FEDERAL STUDENT LOANS Basics for Students 2 U.S. Department of Education Arne Duncan Secretary Federal Student Aid James W. Runcie Chief Operating Officer Customer Experience Office Brenda F. Wensil Chief

HIGHERD EDUCATION RECONCILIATION ACT (HERA)

") FREQUENTLY ASKED QUESTIONS LEGISLATIVE When was the Higher Education Reconciliation Act (HERA) legislation signed by the President? HERA is Title VIII of the Deficit Reduction Act of 2005 (DRA), which

FREQUENTLY ASKED QUESTIONS LEGISLATIVE When was the Higher Education Reconciliation Act (HERA) legislation signed by the President? HERA is Title VIII of the Deficit Reduction Act of 2005 (DRA), which

TICAS Proposal to Create One Improved Income-Driven Repayment Plan

TICAS Proposal to Create One Improved Income-Driven Repayment Plan All federal student loan borrowers should be able to choose the assurance of manageable payments and forgiveness after 20 years of payments.

TICAS Proposal to Create One Improved Income-Driven Repayment Plan All federal student loan borrowers should be able to choose the assurance of manageable payments and forgiveness after 20 years of payments.

Sign in & click on Complete Counseling Select Exit Counseling

www.studentloans.gov Sign in & click on Complete Counseling Select Exit Counseling Required Withdraw Graduate Enrollment drops below half-time Transfer to another school This counseling session covers

www.studentloans.gov Sign in & click on Complete Counseling Select Exit Counseling Required Withdraw Graduate Enrollment drops below half-time Transfer to another school This counseling session covers

Sam Houston State University

Sam Houston State University Division of Student Services - SMMC Services Personal Financial Counseling/Coaching Classroom Presentations Workshops Personnel 2 Full-time Staff members 5 Student Employees

Sam Houston State University Division of Student Services - SMMC Services Personal Financial Counseling/Coaching Classroom Presentations Workshops Personnel 2 Full-time Staff members 5 Student Employees

Repayment Strategies for Managing Your Student Loans

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2016 Repayment Strategies for Managing Your Student Loans Considerations Dental school graduates have a great track record for repayment Multiple ways

SENIOR LOAN EXIT INTERVIEW DENTAL SCHOOL CLASS OF 2016 Repayment Strategies for Managing Your Student Loans Considerations Dental school graduates have a great track record for repayment Multiple ways

Loan Repayment- The Buck Starts Where? Dana Kelly Nelnet Loan Servicing

Loan Repayment- The Buck Starts Where? Dana Kelly Nelnet Loan Servicing Agenda Exit Counseling What s New? Repayment Plans not Based on Income Income-Driven Repayment Plans Highlights and Examples Public

Loan Repayment- The Buck Starts Where? Dana Kelly Nelnet Loan Servicing Agenda Exit Counseling What s New? Repayment Plans not Based on Income Income-Driven Repayment Plans Highlights and Examples Public

Repayment Plans. October Kim Wells U.S. Department of Education 1. Agenda. Standard Plan. Default repayment plan Loans eligible for inclusion

Repayment Plans U.S. Department of Education Agenda Standard Plan Extended Plan Graduated Plan Income-Driven Plans Resources 2 Standard Plan Default repayment plan Loans eligible for inclusion Direct Subsidized

Repayment Plans U.S. Department of Education Agenda Standard Plan Extended Plan Graduated Plan Income-Driven Plans Resources 2 Standard Plan Default repayment plan Loans eligible for inclusion Direct Subsidized

Federal Student Loan Repayment Do s & Don ts

Federal Student Loan Repayment Do s & Don ts College graduates with Federal student loans have a number of repayment options at their disposal. This guide will walk you through your options so you can

Federal Student Loan Repayment Do s & Don ts College graduates with Federal student loans have a number of repayment options at their disposal. This guide will walk you through your options so you can

Private Loans. Private Loans Get the big picture

Private Loans Private Loans Get the big picture How do I compare private loans? Let s say that you have exercised all other available options and decided that you must borrow a private loan to meet your

Private Loans Private Loans Get the big picture How do I compare private loans? Let s say that you have exercised all other available options and decided that you must borrow a private loan to meet your

PUBLIC SERVICE LOAN FORGIVENESS

PUBLIC SERVICE LOAN FORGIVENESS Presented by: Scott Harrison, Assistant Director Student Financial Services (SFS) PSLF Program Basics The remaining balance on your qualified Direct Loans is forgiven and

PUBLIC SERVICE LOAN FORGIVENESS Presented by: Scott Harrison, Assistant Director Student Financial Services (SFS) PSLF Program Basics The remaining balance on your qualified Direct Loans is forgiven and