ACCREDITED FINANCIAL COUNSELOR REVIEW COURSE

|

|

|

- Dwain Chapman

- 5 years ago

- Views:

Transcription

1 ACCREDITED FINANCIAL COUNSELOR REVIEW COURSE Designed for Cities for Financial Empowerment Counselors Course Taught by: Dr. Mary Bell Carlson, Ph.D., AFC, CFP

2 Unit 7 Study Guide Unit 7 Surviving Debt Chapter 3 Personal Finance review Chapter 6 Unit 8 Study Guide Unit 8 Surviving Debt Chapters 1, 7, 8, 9, 14, 15, 16, 17, 19, 21 Personal Finance review Chapter 6

3 UNIT 7 Credit Reports and Scores

4 Counselor Competencies List the information that is included in a credit report. Describe how to build, maintain, or rebuild a strong credit report. Explain how to address a credit report error. Summarize how to obtain and monitor a credit report. List the factors that affect credit scores. Summarize how to obtain and monitor a credit score.

5 Overview Credit Reports Credit Scores

6 Credit Reports What is a credit report? A record of a person s dealings with debt Credit Bureaus Only collect information Sell information to lenders Regulated by the Fair Credit Reporting Act Experian, Equifax, TransUnion

7 Credit Reports What is included Personal Information Account Information Public Record Information Inquiries

8 Credit Reports What to Look For Negative Items Mistakes Fraud

9

10 Credit Reports Free Report Denied Credit

11 Credit Reports Who Has Access Creditors Employers Government Agencies Insurance Companies Landlords

12 Credit Score Definition a statistical measure used to rate applicants based on various factors of creditworthiness Importance How to get one

13 Credit Score Factors Payment History (35%) Amount of Used Available Credit (30%) Length of Credit History (15%) New Credit (10%) Types of Credit (10%)

14 Favorite Counselor Skills Effectively help clients understand credit reports Teach clients how to build or maintain a good credit report

15 UNIT 8 Over Indebtedness

16 Counselor Competencies Describe signs of overindebtedness. Describe how to set a reasonable debt limit. Summarize strategies to reduce debt. Discuss consequences of default. Explain methods of restructuring debt.

17 Overview Overindebtedness Consequences Reducing Debt

18 Overindebtedness Signs 1. Exceeding limits 2. Not knowing how much you owe 3. Running out of money 4. Paying only minimum amount 5. Requesting new credit and higher limits 6. Paying late or skipping payments 7. Taking add-on loans (aka flipping) 8. Using debt-consolidation loans 9. Experiencing garnishments 10. Experiencing repossessions or foreclosures

19 Overindebtedness How to Set Debt Limits? Mary s Tip: Set limits within the budget: - Housing < 26% - Utilities between 5 10% - Savings > 10% - Transportation <10% - Debt Expenses < 10% - Food between 9 14% - Everything else <20% - Total = 100%

20 Overindebtedness Terms Statute of Limitations - a rule that sets a time limit within which a creditor may sue you for payment of a debt. The length of time that a creditor has to sue you on an unpaid debt varies from state to state. In some states, it's four years. In other states, it might be longer. Cooling-off Period - an interval after a sales contract is agreed upon during which the purchaser can decide to cancel without loss. Seller must tell you your rights to cancelling a contract. Cease Letter first step to asking a creditor or collector to stop an illegal activity or harassment. Examples of cease letters can be found at Consumerfinance.gov

21 Consequences Prioritizing High Priority Low Priority

22 Consequences Consequences of Default Repossession Self-help - Self-help repossession is simply repossession of collateral based on terms of a contract rather than a court order Reinstatement you get the loan current by making up all of the past due payments, including applicable fees and late charges, in one lump sum. Redeem - if you pay the entire outstanding balance due on the car loan, you can get the car back. The balance you would need to pay to redeem the vehicle may include extra fees and charges (including repo and storage fees and even attorney fees). Deficiency balance - the remaining amount that is due and owing a lender after the collateral (real estate or personal property) securing a loan is sold for less than the outstanding balance of the loan.

23 Consequences Consequences of Default, con t. Garnishment - a court order directing that money or property of a third party (usually wages paid by an employer) be seized to satisfy a debt owed by a debtor to a plaintiff creditor. Bank Setoff where the bank can removes money from the debtor s bank account to cover a missed payment on a loan owed to that institution. Assignment Order - court order that requires a debtor to assign certain rights to the creditor.

24 Consequences Judgments Basic - an official result of a lawsuit in court. In debt collection lawsuits, the judge may award the creditor or debt collector a judgment against you. Summary - a means by which the creditor can obtain a judgment against you without having to go to trial. Default - If you do not file an answer to the complaint within the response period, you lose the right to challenge the creditor's lawsuit. With a judgement, creditors can: garnish or attach your wages attach your bank account Execute against personal property, or file a lien against your real estate.

25 Consequences Liens Judgment Property Tax - property that has a lien attached to it cannot be sold or refinanced until the taxes are paid and the lien is removed. IRS - the government's legal claim against your property when you neglect or fail to pay a tax debt. The lien protects the government's interest in all your property, including real estate, personal property and financial assets. Mechanic s - a security interest in the title to property for the benefit of those who have supplied labor or materials that improve the property. The lien exists for both real property and personal property.

26 Reducing Debt Steps to Reduce Excessive Debt 1. Determine who and what is owed 2. Focus budget on debt reduction 3. Contact creditors 4. Take on no new debt 5. Refinance when appropriate 6. Avoid bad help 7. Find good help 8. Make power payments

27 Reducing Debt Restructuring Debt Consolidate Refinance Negotiate Better Terms File for Bankruptcy

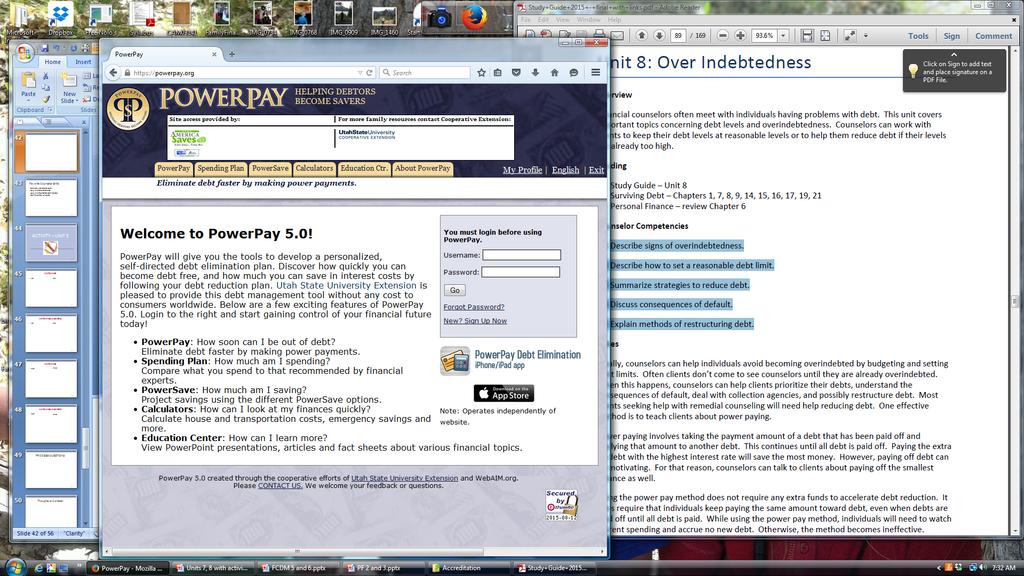

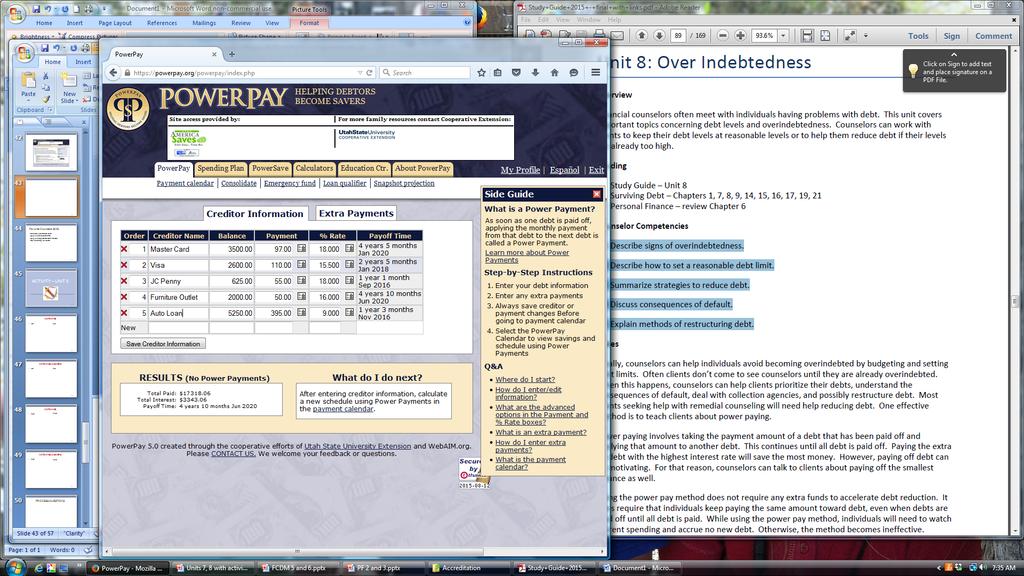

28 Reducing Debt Power Payments Uses the same amount of total monthly debt payments Greatly reduces the interest paid Reduces amount of time to pay off debt Take on no new debt Use program at Can be very motivating

29

30

31

32

33 Favorite Counselor Skills Evaluate clients debt levels Help clients set debt limits Help clients prioritize debt if needed Run PowerPay for clients

34 FOR NEXT WEEK Personal Finance: Ch. 7 Surviving Debt: Ch. 5, 18, 20

Chapter 26 11/9/2017 1

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Chapter 26 11/9/2017 1 Average college students has 3 credit cards Also between $1500 & $2000 in debt Things to know if you re getting a credit card Who accepts it? What amount can you charge to meet your

Federal Reserve Bank of Philadelphia

Federal Reserve Bank of Philadelphia 1 When you apply for credit, whether it s a credit card, car loan, or a mortgage, lenders want to know whether you are likely to repay your loan and make the payments

Federal Reserve Bank of Philadelphia 1 When you apply for credit, whether it s a credit card, car loan, or a mortgage, lenders want to know whether you are likely to repay your loan and make the payments

Solving Money Problems

Solving Money Problems 14 th Edition Robin Leonard, J.D. Attorney Margaret Reiter Chapter 1 How Much Do You Owe?... 1 Learning Objectives... 1 Introduction... 1 How Much Do You Earn?... 2 How Much Do You

Solving Money Problems 14 th Edition Robin Leonard, J.D. Attorney Margaret Reiter Chapter 1 How Much Do You Owe?... 1 Learning Objectives... 1 Introduction... 1 How Much Do You Earn?... 2 How Much Do You

Volume 2 Your Credit Report and Your Rights

Volume 2 Your Credit Report and Your Rights Your Credit Report and Your Rights Take the first step in changing your financial future. Call InCharge Debt Solutions today at 1.877.544.7772 or visit www.incharge.org

Volume 2 Your Credit Report and Your Rights Your Credit Report and Your Rights Take the first step in changing your financial future. Call InCharge Debt Solutions today at 1.877.544.7772 or visit www.incharge.org

Credit Cards. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage.

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

Credit Cards Annual Fee - Amount you pay each year to have a credit card. Annual Percentage Rate - What you are paying each month -- unpaid balances calculated as a percentage. Balance - The total charges

A Credit Smart Start. Michael Trecek Sr. Risk Analyst Commerce Bank - Retail Lending

A Credit Smart Start Michael Trecek Sr. Risk Analyst Commerce Bank - Retail Lending Agenda Credit Score vs. Credit Report Credit Score Components How Credit Scoring Helps You 10 Things that Hurt Your Credit

A Credit Smart Start Michael Trecek Sr. Risk Analyst Commerce Bank - Retail Lending Agenda Credit Score vs. Credit Report Credit Score Components How Credit Scoring Helps You 10 Things that Hurt Your Credit

TABLE OF CONTENTS. Healthier Black Elders Center

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

TABLE OF CONTENTS What is credit............................................1 The five C s of credit...................................... 2 Types of credit...........................................3

Managing in Tough Times

Managing in Tough Times Deciding Which Bills to Pay First When you do not have enough money to cover your family s basic living expenses and pay all your creditors, you face some difficult financial decisions.

Managing in Tough Times Deciding Which Bills to Pay First When you do not have enough money to cover your family s basic living expenses and pay all your creditors, you face some difficult financial decisions.

Welcome. 1. Agenda. 2. Ground Rules. 3. Introductions. Charge It Right 2

Charge It Right Welcome 1. Agenda 2. Ground Rules 3. Introductions Charge It Right 2 Objectives Define credit Explain why credit is important Identify the factors creditors look for when making credit

Charge It Right Welcome 1. Agenda 2. Ground Rules 3. Introductions Charge It Right 2 Objectives Define credit Explain why credit is important Identify the factors creditors look for when making credit

UNDERSTANDING YOUR CREDIT REPORT & YOUR CREDIT SCORE

UNDERSTANDING YOUR CREDIT REPORT & YOUR CREDIT SCORE Presented By: Tom Painter Chief Lending Officer WHAT IS A CREDIT SCORE? A credit score is a number that summarizes your credit risk, based on a snapshot

UNDERSTANDING YOUR CREDIT REPORT & YOUR CREDIT SCORE Presented By: Tom Painter Chief Lending Officer WHAT IS A CREDIT SCORE? A credit score is a number that summarizes your credit risk, based on a snapshot

Debt Collection & the Fair Debt Collection Practice Act (FDCPA)

") Debt Collection & the Fair Debt Collection Practice Act (FDCPA) Please note that this Information Paper only provides basic information and is not intended to serve as a substitute for personal consultations

Debt Collection & the Fair Debt Collection Practice Act (FDCPA) Please note that this Information Paper only provides basic information and is not intended to serve as a substitute for personal consultations

Beyond the Classroom. Blaise P. Johnson Gate City Bank

Beyond the Classroom Blaise P. Johnson Gate City Bank 1 Topics To Be Discussed 1. Credit Reports & Credit Scores 2. Repayment/Consolidation of Student Loans 3. Obtaining A Personal or Home Loan 4. Open

Beyond the Classroom Blaise P. Johnson Gate City Bank 1 Topics To Be Discussed 1. Credit Reports & Credit Scores 2. Repayment/Consolidation of Student Loans 3. Obtaining A Personal or Home Loan 4. Open

Office of Student Financial Management

September 2015 Office of Student Financial Management Kasia Palm: Director of Student Financial Management What is Credit? - The ability to obtain goods/services before payment based on the trust that

September 2015 Office of Student Financial Management Kasia Palm: Director of Student Financial Management What is Credit? - The ability to obtain goods/services before payment based on the trust that

c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:

![c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:](/thumbs/76/73531259.jpg "c» BALANCE C:» Financially Empowering You The World of Credit Reports Podcast [Music plays] Nikki:") The World of Credit Reports Podcast [Music plays] Nikki: You re listening to world of credit. Hi, I m Nikki, your host for today s podcast. Credit reports and credit scores influence our lives in many

The World of Credit Reports Podcast [Music plays] Nikki: You re listening to world of credit. Hi, I m Nikki, your host for today s podcast. Credit reports and credit scores influence our lives in many

Find us online Facebook:

Find us online Facebook: http://www.facebook.com/#!/personalfinance4pfms Blog: http://blogs.extension.org/militaryfamilies/category/ personal-finance/ Website: http://www.extension.org/militaryfamilies

Find us online Facebook: http://www.facebook.com/#!/personalfinance4pfms Blog: http://blogs.extension.org/militaryfamilies/category/ personal-finance/ Website: http://www.extension.org/militaryfamilies

Understanding Credit Reports and Scores and How to Improve It!

Understanding Credit Reports and Scores and How to Improve It! Ryan Chatterton, CCCC What Will We Cover? When we are finished, you will understand: Credit Reports and Credit Scores - What they are and

Understanding Credit Reports and Scores and How to Improve It! Ryan Chatterton, CCCC What Will We Cover? When we are finished, you will understand: Credit Reports and Credit Scores - What they are and

Financial Fitness: MONEY Matters

Financial Fitness: MONEY Matters Financial Literacy and Education University of Colorado Denver Spring 2015 Presenter: M. Lesa Briggs After this presentation, you will be able to: Evaluate your student

Financial Fitness: MONEY Matters Financial Literacy and Education University of Colorado Denver Spring 2015 Presenter: M. Lesa Briggs After this presentation, you will be able to: Evaluate your student

HOW TO USE CREDIT. Latino Community Credit Union & the Latino Community Development Center.

HOW TO USE CREDIT Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright 2016 Latino Community Credit Union Made possible by a generous contribution from the

HOW TO USE CREDIT Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright 2016 Latino Community Credit Union Made possible by a generous contribution from the

ECONOMIC EDUCATION FOR CONSUMERS Chapter 10

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

WHAT S AHEAD 10.1 What Is Credit? 10.2 How to Qualify for Credit 10.3 Sources of Consumer Credit 10.4 Credit Rights and Responsibilities 10.5 Maintain a Good Credit Rating LESSON 10.1 What Is Credit? GOALS

Your Money, Your Goals Spotlight Series. Understanding credit reports and scores: An in-depth look

Your Money, Your Goals Spotlight Series Understanding credit reports and scores: An in-depth look DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on

Your Money, Your Goals Spotlight Series Understanding credit reports and scores: An in-depth look DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on

Stopping Debt Collection Harassment and Responding to Debt Collection Suits

Stopping Debt Collection Harassment and Responding to Debt Collection Suits Robert J. Hobbs National Consumer Law Center Michelle A. Weinberg Legal Assistance Foundation of Metropolitan Chicago Jessica

Stopping Debt Collection Harassment and Responding to Debt Collection Suits Robert J. Hobbs National Consumer Law Center Michelle A. Weinberg Legal Assistance Foundation of Metropolitan Chicago Jessica

Money Management Curriculum

Money Management Module 4: Credit Reports & Credit Scores Money Management Curriculum Module 4: Credit Reports & Credit Scores Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom,

Money Management Module 4: Credit Reports & Credit Scores Money Management Curriculum Module 4: Credit Reports & Credit Scores Project Team: Ruby Ward, Professor, Utah State University Trent Teegerstrom,

February 2015 Wednesday Webinar ~ Credit Matters - Resources to Educate Students About Credit and Debt

February 2015 Wednesday Webinar ~ Credit Matters - Resources to Educate Students About Credit and Debt 1 Mike Fagone Jennifer Pincus Jessica Whittier Bernstein Shur US Dept. of Justice FAME 2 About CARE

February 2015 Wednesday Webinar ~ Credit Matters - Resources to Educate Students About Credit and Debt 1 Mike Fagone Jennifer Pincus Jessica Whittier Bernstein Shur US Dept. of Justice FAME 2 About CARE

Credit Education Program

Credit Education Program Course Objectives Identify ways to decrease spending and increase income Read and understand the purpose of your credit report Discuss common debt traps to avoid How lenders evaluate

Credit Education Program Course Objectives Identify ways to decrease spending and increase income Read and understand the purpose of your credit report Discuss common debt traps to avoid How lenders evaluate

Credit Building & Budgeting

Credit Building & Budgeting Tips, tools and information on credit and budgeting Presented by Mercy Credit Union Credit Building & Budgeting Learn what affects your credit and how to build and/or improve

Credit Building & Budgeting Tips, tools and information on credit and budgeting Presented by Mercy Credit Union Credit Building & Budgeting Learn what affects your credit and how to build and/or improve

DEALING WITH DEBT. Your Rights and Responsibilities in Minnesota

DEALING WITH DEBT Your Rights and Responsibilities in Minnesota Fifth Edition Revised June 2012 The laws explained in this booklet change frequently, so be sure to check for changes. This booklet can only

DEALING WITH DEBT Your Rights and Responsibilities in Minnesota Fifth Edition Revised June 2012 The laws explained in this booklet change frequently, so be sure to check for changes. This booklet can only

FINANCIAL FITNESS EDUCATION

(Agency s Name & Logo) FINANCIAL FITNESS EDUCATION Sponsored by BETTER FORTUNES Control Your Money Control Your Life Knowing the difference can make all the difference Chapter One ECONOMIC WAY OF THINKING

(Agency s Name & Logo) FINANCIAL FITNESS EDUCATION Sponsored by BETTER FORTUNES Control Your Money Control Your Life Knowing the difference can make all the difference Chapter One ECONOMIC WAY OF THINKING

Secrets to Success: Personal Finance Management

Secrets to Success: Personal Finance Management Harvard University Employees Credit Union (HUECU) A financial institution exclusively serving the Harvard University students, alumni, faculty, staff, and

Secrets to Success: Personal Finance Management Harvard University Employees Credit Union (HUECU) A financial institution exclusively serving the Harvard University students, alumni, faculty, staff, and

Credit Reports 101. Bill Bufkins, November 3, 2011

Credit Reports 101 Bill Bufkins, November 3, 2011 What is a credit report? A credit report is a record of your past borrowing and repayment activity. The information in your credit report helps determine

Credit Reports 101 Bill Bufkins, November 3, 2011 What is a credit report? A credit report is a record of your past borrowing and repayment activity. The information in your credit report helps determine

Debt getting in your way? Get a handle on it.

Debt getting in your way? Get a handle on it. Bureau of Consumer Financial Protection Your Money, Your Goals About the Bureau The Bureau of Consumer Financial Protection regulates the offering and provision

Debt getting in your way? Get a handle on it. Bureau of Consumer Financial Protection Your Money, Your Goals About the Bureau The Bureau of Consumer Financial Protection regulates the offering and provision

Module 4: Debt Lesson Part 2

Module 4: Debt Lesson Part 2 Module 4: Debt Lesson Part 2 Getting Rid of Your Debt Forever The Lesson Blueprint Where do I Start First? What Tools Can I Use? Rookie Mistakes Where Do I Start? Debt Snowball

Module 4: Debt Lesson Part 2 Module 4: Debt Lesson Part 2 Getting Rid of Your Debt Forever The Lesson Blueprint Where do I Start First? What Tools Can I Use? Rookie Mistakes Where Do I Start? Debt Snowball

CreditReport.LifeTips.com

CreditReport.LifeTips.com Category: About Credit Reports Subcategory: About Credit Reports Tip: About Credit Reports A credit report is a compilation of information that gives potential creditors a snapshot

CreditReport.LifeTips.com Category: About Credit Reports Subcategory: About Credit Reports Tip: About Credit Reports A credit report is a compilation of information that gives potential creditors a snapshot

Understanding Your FICO Score. Understanding FICO Scores

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

EasterSeal/Freddie Mac CreditSmart Training Credit Questions & Answers

Bankruptcy What Is Bankruptcy? Bankruptcy is a legal proceeding in which a person who cannot pay his or her bills can get a fresh financial start. The right to file for bankruptcy is provided by federal

Bankruptcy What Is Bankruptcy? Bankruptcy is a legal proceeding in which a person who cannot pay his or her bills can get a fresh financial start. The right to file for bankruptcy is provided by federal

Understanding Credit. What it is, why it s important, and how you can maintain it. Brought to you by Sallie Mae and FICO

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

Understanding Credit What it is, why it s important, and how you can maintain it Brought to you by Sallie Mae and FICO Introduction A student loan may be your first major credit experience. This is a good

CHAPTER 13 BANKRUPTCY IN THE EASTERN DISTRICT OF KENTUCKY

CHAPTER 13 BANKRUPTCY IN THE EASTERN DISTRICT OF KENTUCKY [PHOTO] THE DEBTOR S CHAPTER 13 HANDBOOK A Publication of the Chapter 13 Trustee for the Eastern District of Kentucky 2018 Beverly M. Burden, Trustee

CHAPTER 13 BANKRUPTCY IN THE EASTERN DISTRICT OF KENTUCKY [PHOTO] THE DEBTOR S CHAPTER 13 HANDBOOK A Publication of the Chapter 13 Trustee for the Eastern District of Kentucky 2018 Beverly M. Burden, Trustee

Your Credit. Objectives. An Introduction to Personal Credit. By the end of this presentation you will have a understanding of: 1/19/2016.

Your Credit An Introduction to Personal Credit Objectives By the end of this presentation you will have a understanding of: Credit Score Where can I find it? What is it? How do I get it? Advantages of

Your Credit An Introduction to Personal Credit Objectives By the end of this presentation you will have a understanding of: Credit Score Where can I find it? What is it? How do I get it? Advantages of

Chapter 6 - Credit. Section 6.1

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

Chapter 6 - Credit Section 6.1 Credit is a medium of exchange which allows individuals to buy goods or services now and pay for them later The creditor supplies money, goods, or services in a credit agreement

Credit Reports & Credit Scores 101. Mary C. Hurlburt Certified Consumer Credit Counselor and Score Volunteer

Credit Reports & Credit Scores 101 Mary C. Hurlburt Certified Consumer Credit Counselor and Score Volunteer mary.hurlburt@scorevolunteer.org Mary Hurlburt Mary Hurlburt is the Financial Counseling and

Credit Reports & Credit Scores 101 Mary C. Hurlburt Certified Consumer Credit Counselor and Score Volunteer mary.hurlburt@scorevolunteer.org Mary Hurlburt Mary Hurlburt is the Financial Counseling and

Chapter 9 Credit Problems and Laws. Copyright 2007 Thomson South-Western

Chapter 9 Credit Problems and Laws Copyright 2007 Thomson South-Western Errors and Fraud Recourse is a remedy for unfair treatment Credit to your account Replacement for damaged goods Disputing charges

Chapter 9 Credit Problems and Laws Copyright 2007 Thomson South-Western Errors and Fraud Recourse is a remedy for unfair treatment Credit to your account Replacement for damaged goods Disputing charges

Credit and Debt.notebook August 28, 2014

Credit and Debt What does it mean to have credit? Credit means someone is willing to loan you money in exchange for your promise to repay it, usually with interest. Interest the amount of money you pay

Credit and Debt What does it mean to have credit? Credit means someone is willing to loan you money in exchange for your promise to repay it, usually with interest. Interest the amount of money you pay

20 STEPS TO IMPROVE YOUR CREDIT SCORE APPROVED CREDIT SCORE SUPER FAST CREDIT RANKINGS

20 STEPS TO IMPROVE YOUR CREDIT SCORE APPROVED CREDIT SCORE SUPER FAST CREDIT RANKINGS 2 Approved Credit Score info@approvedcreditscore.com www.approvedcreditscore.com APPROVED CREDIT SCORE CONGRATULATIONS!

20 STEPS TO IMPROVE YOUR CREDIT SCORE APPROVED CREDIT SCORE SUPER FAST CREDIT RANKINGS 2 Approved Credit Score info@approvedcreditscore.com www.approvedcreditscore.com APPROVED CREDIT SCORE CONGRATULATIONS!

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Empowering people to lead financially healthy lives. TABLE OF CONTENTS Understanding credit reports...2 What s in a credit

TIP: Make sure this information is correct. A wrong address or phone number could be a mistake or a sign of identity theft.

Reading a Sample Credit Report This sample report shows what kind of information might appear on your own credit report, also called a consumer disclosure statement, from the 3 major Credit Reporting Agencies

Reading a Sample Credit Report This sample report shows what kind of information might appear on your own credit report, also called a consumer disclosure statement, from the 3 major Credit Reporting Agencies

A CONSUMER S GUIDE TO INSURANCE COMPANIES' USE OF CREDIT INFORMATION

A CONSUMER S GUIDE TO INSURANCE COMPANIES' USE OF CREDIT INFORMATION INSURANCE CREDIT SCORING IN NORTH CAROLINA Insurance companies licensed to sell private passenger automobile and residential property

A CONSUMER S GUIDE TO INSURANCE COMPANIES' USE OF CREDIT INFORMATION INSURANCE CREDIT SCORING IN NORTH CAROLINA Insurance companies licensed to sell private passenger automobile and residential property

FTC Facts. For Consumers Federal Trade Commission. Credit Scoring Ever wonder how a creditor decides

FTC Facts For Consumers Federal Trade Commission For The Consumer May 2006 Credit Scoring www.ftc.gov 1-877-ftc-help Ever wonder how a creditor decides whether to grant you credit? For years, creditors

FTC Facts For Consumers Federal Trade Commission For The Consumer May 2006 Credit Scoring www.ftc.gov 1-877-ftc-help Ever wonder how a creditor decides whether to grant you credit? For years, creditors

LAUREN ROSS Attorney at Law 2550 N. Hollywood Way Suite 404 Burbank, CA Tel.(818) Facsimile (818)

Facsimile (818)") LAUREN ROSS Attorney at Law 2550 N. Hollywood Way Suite 404 Burbank, CA 91505-5046 Tel.(818) 847-0211 Facsimile (818) 847-0214 INITIAL CONSULTATION AGREEMENT AND REQUIRED NOTICES Please Note: These documents

LAUREN ROSS Attorney at Law 2550 N. Hollywood Way Suite 404 Burbank, CA 91505-5046 Tel.(818) 847-0211 Facsimile (818) 847-0214 INITIAL CONSULTATION AGREEMENT AND REQUIRED NOTICES Please Note: These documents

FORECLOSURE. I don t think I can make my mortgage payments but I don t want to go through a foreclosure. What are some of my options?

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy This means that if you don t pay, the creditor can foreclose upon (or take

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy This means that if you don t pay, the creditor can foreclose upon (or take

Table of Contents. Money Smart for Small Business Page 2 of 19

Table of Contents Welcome... 4 What Do You Know? Credit Reporting for a Small Business... 5 Pre-Test... 6 Credit Reporting... 7 Credit Report Impact... 7 Business Credit Reports... 7 Discussion Point #1:

Table of Contents Welcome... 4 What Do You Know? Credit Reporting for a Small Business... 5 Pre-Test... 6 Credit Reporting... 7 Credit Report Impact... 7 Business Credit Reports... 7 Discussion Point #1:

Borrowing Basics. FDIC Money Smart for Young Adults. Building: Knowledge, Security, Confidence

Borrowing Basics FDIC Money Smart for Young Adults Building: Knowledge, Security, Confidence Objectives Define credit Explain why credit is important Identify three types of loans Identify the costs associated

Borrowing Basics FDIC Money Smart for Young Adults Building: Knowledge, Security, Confidence Objectives Define credit Explain why credit is important Identify three types of loans Identify the costs associated

In Debt? Presented by: Together, we do the community justice.

In Debt? Presented by: Together, we do the community justice. HOW CAN SOMEONE COLLECT A DEBT FROM YOU? People can collect money from you only if they follow the law. The law permits people to collect a

In Debt? Presented by: Together, we do the community justice. HOW CAN SOMEONE COLLECT A DEBT FROM YOU? People can collect money from you only if they follow the law. The law permits people to collect a

Introduction. Purpose. Student Introductions. Objectives (Continued) Objectives

Objectives") Introduction Instructor and student introductions. Module overview. 1 2 Your name. Student Introductions Your expectations, questions and concerns about credit cards. Purpose will teach you about credit

Introduction Instructor and student introductions. Module overview. 1 2 Your name. Student Introductions Your expectations, questions and concerns about credit cards. Purpose will teach you about credit

MINNESOTA REAL ESTATE FORECLOSURES: 21 COMMON QUESTIONS & ANSWERS

MINNESOTA REAL ESTATE FORECLOSURES: 21 COMMON QUESTIONS & ANSWERS Our Creditors Remedies attorneys answer the most asked questions from their clients. Practice Area: CREDITORS REMEDIES, BANKRUPTCY & WORK-OUT

MINNESOTA REAL ESTATE FORECLOSURES: 21 COMMON QUESTIONS & ANSWERS Our Creditors Remedies attorneys answer the most asked questions from their clients. Practice Area: CREDITORS REMEDIES, BANKRUPTCY & WORK-OUT

FINANCIAL LITERACY WHAT YOU NEED TO KNOW TO SURVIVE IN TODAY S ECONOMY

FINANCIAL LITERACY WHAT YOU NEED TO KNOW TO SURVIVE IN TODAY S ECONOMY Presented by: Terry Lawson Lawson Law Center 700 E. 8 th St. Kansas City, MO 64106 www.llckc.com LAWSON LAW CENTER LLC WWW. LLCKC.COM

FINANCIAL LITERACY WHAT YOU NEED TO KNOW TO SURVIVE IN TODAY S ECONOMY Presented by: Terry Lawson Lawson Law Center 700 E. 8 th St. Kansas City, MO 64106 www.llckc.com LAWSON LAW CENTER LLC WWW. LLCKC.COM

GETTING RID OF DEBT: WHAT IS THE BEST OPTION FOR YOU?

GETTING RID OF DEBT: WHAT IS THE BEST OPTION FOR YOU? What debt are we talking about? What are the methods to get rid of debt? What are the benefits of each method? What are the downsides? How do I determine

GETTING RID OF DEBT: WHAT IS THE BEST OPTION FOR YOU? What debt are we talking about? What are the methods to get rid of debt? What are the benefits of each method? What are the downsides? How do I determine

Project Pro$per. Credit Reports and Credit Scores

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

Project Pro$per Presents Credit Reports and Credit Scores Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo s Hands on Banking The Hands on Banking program is

VISA Gold 12.84% Not applicable. There is no minimum. None. None None None. $20.00 None $15.00 (from self) / $5.00 (from other)

/ $5.00 (from other)") Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases 12.84% APR for Balance Transfers 12.84% APR for Cash Advances 12.84% VISA Gold This APR is effective January 1, 2016 through

Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases 12.84% APR for Balance Transfers 12.84% APR for Cash Advances 12.84% VISA Gold This APR is effective January 1, 2016 through

Credit and Credit Cards

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

Credit and Credit Cards What s Next Project Credit Cards They are all around you. Most people have at least one. Some have many. They are credit cards. A credit card allows you to pay for merchandise or

CREDIT SCORE USER GUIDE

Page 1 of 11 ABOUT EQUIFAX Equifax empowers businesses and consumers with information they can trust. A global leader in information solutions, we leverage one of the largest sources of consumer and commercial

Page 1 of 11 ABOUT EQUIFAX Equifax empowers businesses and consumers with information they can trust. A global leader in information solutions, we leverage one of the largest sources of consumer and commercial

THE CONSUMER LAW GROUP, P. C.

THE CONSUMER LAW GROUP, P. C. 1801 Libbie Avenue, Suite 202 Richmond, Virginia 23226 (804) 282-7900 Protecting and Fighting for Consumer Rights www.theconsumerlawgroup.com FAX (804) 673-0316 email: pcampbell@theconsumerlawgroup.com

THE CONSUMER LAW GROUP, P. C. 1801 Libbie Avenue, Suite 202 Richmond, Virginia 23226 (804) 282-7900 Protecting and Fighting for Consumer Rights www.theconsumerlawgroup.com FAX (804) 673-0316 email: pcampbell@theconsumerlawgroup.com

MANAGING YOUR DEBT. An Informational and Educational Guide for Residents of New York State

MANAGING YOUR DEBT An Informational and Educational Guide for Residents of New York State Designed and Provided by the Rural Law Center of New York, Inc. Rural Law Center of New York, Inc. WHAT TO DO WHEN

MANAGING YOUR DEBT An Informational and Educational Guide for Residents of New York State Designed and Provided by the Rural Law Center of New York, Inc. Rural Law Center of New York, Inc. WHAT TO DO WHEN

UNDERSTANDING CREDIT. KASFAA Conference Manhattan, KS April 21, Robb Cummings Director of Business Development

UNDERSTANDING CREDIT KASFAA Conference Manhattan, KS April 21, 2016 Robb Cummings Director of Business Development FICO Score 2 A FICO Score is a three-digit number calculated from the credit information

UNDERSTANDING CREDIT KASFAA Conference Manhattan, KS April 21, 2016 Robb Cummings Director of Business Development FICO Score 2 A FICO Score is a three-digit number calculated from the credit information

Building Credit. Inside this issue:

CCCS of Rochester/RethinkingDebt Headquarters: 1000 University Ave, Rochester, NY 14607 **Fall 2018** Inside this issue: Building Credit Building Credit 1 Retail Credit Cards 2 By: CCCS of Rochester Student

CCCS of Rochester/RethinkingDebt Headquarters: 1000 University Ave, Rochester, NY 14607 **Fall 2018** Inside this issue: Building Credit Building Credit 1 Retail Credit Cards 2 By: CCCS of Rochester Student

Creditworthiness (UXL)

") Creditworthiness (UXL) Since so much debt is unsecured, it is important for companies to have information on how well their potential borrowers handle money in order to assess their creditworthiness, or

Creditworthiness (UXL) Since so much debt is unsecured, it is important for companies to have information on how well their potential borrowers handle money in order to assess their creditworthiness, or

Your Money, Your Goals Spotlight Series. Dealing with debt: A closer look

Your Money, Your Goals Spotlight Series Dealing with debt: A closer look DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on behalf of the Bureau. It

Your Money, Your Goals Spotlight Series Dealing with debt: A closer look DISCLAIMER This presentation is being made by a Consumer Financial Protection Bureau representative on behalf of the Bureau. It

Credit Building Apps

Credit Building Apps Apps that Can Help Build and Repair Credit Webinar of September 27, 2018 Sponsored by Community Development and the Payments, Standards, and Outreach Group of the Federal Reserve Bank

Credit Building Apps Apps that Can Help Build and Repair Credit Webinar of September 27, 2018 Sponsored by Community Development and the Payments, Standards, and Outreach Group of the Federal Reserve Bank

Module 7 - Credit Reporting HANDOUT 7-1

ParticipantHandbook 1 Module 7 - Credit Reporting HANDOUT 7-1 Credit bureaus Credit bureaus are agencies that collect information about how we use credit. They produce personal credit reports. Credit bureaus

ParticipantHandbook 1 Module 7 - Credit Reporting HANDOUT 7-1 Credit bureaus Credit bureaus are agencies that collect information about how we use credit. They produce personal credit reports. Credit bureaus

Understanding Vehicle Financing

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

Understanding credit reports and scores

MODULE 7: Understanding credit reports and scores If you have a 10 -minute session... If you have a 30 -minute session... If you have multiple sessions... Tool 1: Getting your credit reports and scores

MODULE 7: Understanding credit reports and scores If you have a 10 -minute session... If you have a 30 -minute session... If you have multiple sessions... Tool 1: Getting your credit reports and scores

June, The Self Help Legal Center. Southern Illinois University School Of Law Carbondale, IL (618)

") June, 2008 The Self Help Legal Center Southern Illinois University School Of Law Carbondale, IL 62901 (618) 453-3217 2 TABLE OF CONTENTS Table of Contents 2 Disclaimer 3 Warning to all readers 4 Who should

June, 2008 The Self Help Legal Center Southern Illinois University School Of Law Carbondale, IL 62901 (618) 453-3217 2 TABLE OF CONTENTS Table of Contents 2 Disclaimer 3 Warning to all readers 4 Who should

in Head Start Credit and Debt: Make it work for you!

in Head Start Credit and Debt: Make it work for you! Annual Credit Report Request Form You have the right to get a free copy of your credit file disclosure, commonly called a credit report, once every

in Head Start Credit and Debt: Make it work for you! Annual Credit Report Request Form You have the right to get a free copy of your credit file disclosure, commonly called a credit report, once every

Reviewing C YouR CRedit RepoRt

ChapteR 2 Reviewing C YouR CRedit RepoRt What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

ChapteR 2 Reviewing C YouR CRedit RepoRt What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

Wisconsin Consumer Act II 1

WISCONSIN CONSUMER ACT II: DELINQUENCY & COLLECTIONS PRESENTED BY: PAUL GUTTORMSSON LATE FEES Consumer Act does not restrict late fees on open-end plans, but your agreement must provide for them. Consumer

WISCONSIN CONSUMER ACT II: DELINQUENCY & COLLECTIONS PRESENTED BY: PAUL GUTTORMSSON LATE FEES Consumer Act does not restrict late fees on open-end plans, but your agreement must provide for them. Consumer

Home Mortgage Foreclosures in Maine

Home Mortgage Foreclosures in Maine Find more easy-to-read legal information at www.ptla.org Important Note: This is very general information about home mortgage and foreclosure rules in Maine. It is not

Home Mortgage Foreclosures in Maine Find more easy-to-read legal information at www.ptla.org Important Note: This is very general information about home mortgage and foreclosure rules in Maine. It is not

money management managing credit and debt

money management managing credit and debt our mission The mission of The USAA Educational Foundation is to help consumers make informed decisions by providing information on financial management, safety

money management managing credit and debt our mission The mission of The USAA Educational Foundation is to help consumers make informed decisions by providing information on financial management, safety

Table of Contents. Money Smart for Small Business Page 2 of 29

Table of Contents Getting Started... 4 Training Overview... 6 Welcome... 7 What Do You Know?... 9 Credit Reporting... 12 Business Credit Reports... 13 Discussion Point #1: Business Credit Reports... 14

Table of Contents Getting Started... 4 Training Overview... 6 Welcome... 7 What Do You Know?... 9 Credit Reporting... 12 Business Credit Reports... 13 Discussion Point #1: Business Credit Reports... 14

Equifax Credit Report Personal Information Since xx/xx/xx FAD xx/xx/xx SSN Information Employment Beacon

PO Box 1386, Columbia, SC 29202 www.icscredit.com This document is provided only to assist new users in reading an Equifax Credit Report. It is not intended to be authoritative, and may not reflect the

PO Box 1386, Columbia, SC 29202 www.icscredit.com This document is provided only to assist new users in reading an Equifax Credit Report. It is not intended to be authoritative, and may not reflect the

WHOLESALE LENDING AT-A-GLANCE CREDIT

DESCRIPTION STANDARD A borrower s creditworthiness is based on past and present credit history. The credit history must demonstrate the borrower s ability and willingness to handle financial obligations.

DESCRIPTION STANDARD A borrower s creditworthiness is based on past and present credit history. The credit history must demonstrate the borrower s ability and willingness to handle financial obligations.

Frequently Asked Questions

Frequently Asked Questions 1. What is the difference between a professional collection service and a creditor collecting on its own behalf? Sometimes consumers confuse third-party collectors with the in-house

Frequently Asked Questions 1. What is the difference between a professional collection service and a creditor collecting on its own behalf? Sometimes consumers confuse third-party collectors with the in-house

PERSONAL FINANCIAL LITERACY EVENT PARTICIPANT INSTRUCTIONS

CAREER CLUSTER Financial Literacy INSTRUCTIONAL AREA Credit and Debt PERSONAL FINANCIAL LITERACY EVENT PARTICIPANT INSTRUCTIONS PROCEDURES 1. The event will be presented to you through your reading of

CAREER CLUSTER Financial Literacy INSTRUCTIONAL AREA Credit and Debt PERSONAL FINANCIAL LITERACY EVENT PARTICIPANT INSTRUCTIONS PROCEDURES 1. The event will be presented to you through your reading of

Now, let me turn the program over to Jacqueline Cooke, Women s Bureau Regional Administrator in Boston, to introduce our first speaker. Jackie?

Wi$e Up Teleconference Call February 28, 2006 Becoming Credit Smart Speaker 1 Amy Perry Jane Walstedt: Now, let me turn the program over to Jacqueline Cooke, Women s Bureau Regional Administrator in Boston,

Wi$e Up Teleconference Call February 28, 2006 Becoming Credit Smart Speaker 1 Amy Perry Jane Walstedt: Now, let me turn the program over to Jacqueline Cooke, Women s Bureau Regional Administrator in Boston,

Florida Foreclosure Law E-Book

Florida Foreclosure Law E-Book Simple Guide to Florida Foreclosure Law by: florida Law Advisers, P.A. 1 Table Of Contents INTRODUCTION.... 3 FIGHTING THE FORECLOSURE OF YOUR HOME.... 3 PREDATORY LENDING.....

Florida Foreclosure Law E-Book Simple Guide to Florida Foreclosure Law by: florida Law Advisers, P.A. 1 Table Of Contents INTRODUCTION.... 3 FIGHTING THE FORECLOSURE OF YOUR HOME.... 3 PREDATORY LENDING.....

On the path to a great financial life, it s

05_0789735083_CH03.qxd 10/17/06 3:10 PM Page 33 3 Zeroing In on Your Debt On the path to a great financial life, it s easy to get sidetracked by debt. This chapter gives you strategies to improve your

05_0789735083_CH03.qxd 10/17/06 3:10 PM Page 33 3 Zeroing In on Your Debt On the path to a great financial life, it s easy to get sidetracked by debt. This chapter gives you strategies to improve your

Understanding Credit. Lisa Mitchell, Sallie Mae April 6, Champions of Financial Aid ILASFAA Conference

Understanding Credit Lisa Mitchell, Sallie Mae April 6, 2017 Credit Management Agenda Understanding Your Credit Report Summary: Financial Health Tips Credit Management Credit Basics Credit health plays

Understanding Credit Lisa Mitchell, Sallie Mae April 6, 2017 Credit Management Agenda Understanding Your Credit Report Summary: Financial Health Tips Credit Management Credit Basics Credit health plays

Date: Petitioner. Date Petitioner. Lorraine Thomas

Date: agrees to prepare all necessary forms and paperwork surrounding the Chapter 7 Bankruptcy Petition. Lorraine (Thomas) is not an attorney and did not provide legal advice concerning the Chapter 7 Bankruptcy

Date: agrees to prepare all necessary forms and paperwork surrounding the Chapter 7 Bankruptcy Petition. Lorraine (Thomas) is not an attorney and did not provide legal advice concerning the Chapter 7 Bankruptcy

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

13.1. Reading a Credit Report EXERCISE. THEME 4 Lesson 13: Applying for Credit NAME: CLASS PERIOD:

13.1 NAME: CLASS PERIOD: Reading a Credit Report Your ability to qualify for a loan depends on a credit report. A credit report is a record of an individual s personal credit history. It is probably a

13.1 NAME: CLASS PERIOD: Reading a Credit Report Your ability to qualify for a loan depends on a credit report. A credit report is a record of an individual s personal credit history. It is probably a

Rebuilding YOUR CREDIT. Leader s Guide

Rebuilding YOUR CREDIT Leader s Guide C CONTENTS Table of contents Page Topic 1 Introduction 2 Damaged credit 2 Credit reports 5 Mistakes on your credit report 6 Credit scoring 8 Credit repair offers 8

Rebuilding YOUR CREDIT Leader s Guide C CONTENTS Table of contents Page Topic 1 Introduction 2 Damaged credit 2 Credit reports 5 Mistakes on your credit report 6 Credit scoring 8 Credit repair offers 8

Understanding Credit

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

Understanding Credit LAURA STEINBECK DIRECTOR OF BUSINESS DEVELOPMENT, SALLIE MAE 2018 MASFAP CONFERENCE Agenda 2 Credit Management Protect Yourself Understanding Credit Reports Summary: Financial Health

Foreclosure Process in Minnesota

Foreclosure Process in Minnesota Foreclosure by Advertisement Missed payments 6 weeks before sale 4 weeks before sale Sheriff s Sale Missed payment notices Default / intent to foreclose notice Pre foreclosure

Foreclosure Process in Minnesota Foreclosure by Advertisement Missed payments 6 weeks before sale 4 weeks before sale Sheriff s Sale Missed payment notices Default / intent to foreclose notice Pre foreclosure

You re listening to rebuilding after a financial crisis. Hi, I m Niki, your host for today s Podcast.

Rebuilding After a Financial Crisis Podcast [Music plays] Nikki: You re listening to rebuilding after a financial crisis. Hi, I m Niki, your host for today s Podcast. There are many things in life that

Rebuilding After a Financial Crisis Podcast [Music plays] Nikki: You re listening to rebuilding after a financial crisis. Hi, I m Niki, your host for today s Podcast. There are many things in life that

For Further Information Money Smart for Young Adults Page 2 of 38

Table of Contents Money Smart for Young Adults Modules... 3 Your Guides... 3 Checking In... 5 Welcome... 5 Purpose... 5 Objectives... 5 Student Materials... 5 Pre-Assessment... 6 Borrowing Basics... 9

Table of Contents Money Smart for Young Adults Modules... 3 Your Guides... 3 Checking In... 5 Welcome... 5 Purpose... 5 Objectives... 5 Student Materials... 5 Pre-Assessment... 6 Borrowing Basics... 9

CHAPTER TEN. Something Borrowed. Consumer Credit. over time, homes, cars, appliances, clothing, vacations, and other goods and services.

CHAPTER TEN Something Borrowed Consumer Credit THE USE OF CREDIT is as American as apple pie. Americans routinely borrow money to buy, over time, homes, cars, appliances, clothing, vacations, and other

CHAPTER TEN Something Borrowed Consumer Credit THE USE OF CREDIT is as American as apple pie. Americans routinely borrow money to buy, over time, homes, cars, appliances, clothing, vacations, and other

DEFINITION OF COMMON TERMS

DEFINITION OF COMMON TERMS Actual Cash Value: An amount equal to the replacement value of damaged property minus depreciation. Adjustable-Rate Mortgage (ARM): Also known as a variable-rate loan, an ARM

DEFINITION OF COMMON TERMS Actual Cash Value: An amount equal to the replacement value of damaged property minus depreciation. Adjustable-Rate Mortgage (ARM): Also known as a variable-rate loan, an ARM

Table of Contents. Introduction. The History of Credit Scoring. What Is a Good Credit Score? The 5 Factors of Credit Scoring

Table of Contents Introduction The History of Credit Scoring What Is a Good Credit Score? The 5 Factors of Credit Scoring 3 Ways to Get Your Credit Score Get Your FREE Credit Report What If There Are Errors

Table of Contents Introduction The History of Credit Scoring What Is a Good Credit Score? The 5 Factors of Credit Scoring 3 Ways to Get Your Credit Score Get Your FREE Credit Report What If There Are Errors

RETAIL INSTALMENT CREDIT AGREEMENT ( RETAIL CHARGE)

") RETAIL INSTALMENT CREDIT AGREEMENT ( RETAIL CHARGE) Luther Credit Terms & Conditions 1. PROMISE TO PAY: You (meaning each applicant and co-applicant for credit identified on the application which is incorporated

RETAIL INSTALMENT CREDIT AGREEMENT ( RETAIL CHARGE) Luther Credit Terms & Conditions 1. PROMISE TO PAY: You (meaning each applicant and co-applicant for credit identified on the application which is incorporated

Today s Business Environment

6/21/2013 SECURING FINANCING IN TODAY S BUSINESS ENVIRONMENT Presented by Ken Paton Today s Business Environment In recovery from worst recession since the Great Depression Hundreds of bank failures More

6/21/2013 SECURING FINANCING IN TODAY S BUSINESS ENVIRONMENT Presented by Ken Paton Today s Business Environment In recovery from worst recession since the Great Depression Hundreds of bank failures More

Part 2 Understanding Credit. And Your Credit Report

Part 2 Understanding Credit And Your Credit Report What Is Credit? (Developed by Z. Omarali, Toronto District School Board) 50% of Canadians do not know what factors contribute to a credit rating. The

Part 2 Understanding Credit And Your Credit Report What Is Credit? (Developed by Z. Omarali, Toronto District School Board) 50% of Canadians do not know what factors contribute to a credit rating. The

JANUARY SUCCESSFUL Ways to Reduce Your Debt In 2018

JANUARY 2018 5 SUCCESSFUL Ways to Reduce Your Debt In 2018 Date/time to schedule: Monday, January 1 @ 7:00 p.m. Preheader Text: Finally a resolution with long-term benefits. Facebook Share Text: Ready

JANUARY 2018 5 SUCCESSFUL Ways to Reduce Your Debt In 2018 Date/time to schedule: Monday, January 1 @ 7:00 p.m. Preheader Text: Finally a resolution with long-term benefits. Facebook Share Text: Ready

WORRIED. about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA)

") WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) About HAFA Keeping families in their homes is a top priority for REALTORS. While there are loan

WORRIED about Foreclosure? HAFA MAY BE ABLE TO HELP HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM (HAFA) About HAFA Keeping families in their homes is a top priority for REALTORS. While there are loan