Economics 721. International Finance

|

|

|

- Marshall Snow

- 5 years ago

- Views:

Transcription

1 Economics 721 International Finance

2 Week I

3 Lecture 1: Introduction

4 What is financial globalization? The increasing importance and even dominance of international financial transactions in the global economy. This affects economic growth, stability and equality.

5 What has been the Impact of Financial Globalization? Economic growth Inequality Instability Distribution of power classes, nations Trajectory of national economics and world economy

6 What are the contradictions and trajectories of this phase of global capitalist development?

7 What has been the impact on the ability of national institutions the state to chart their own courses?

8 Fred Block: Distinction between open and closed economies

9 Distinction between open and closed NOT whether there are international flows of goods or finance, but whether these are dominated by international capitalist markets and institutions, as opposed to national capitalists states or other noncapitalist institutions

10 Block: Goals of US in post wwii reconstruction To get other countries to adopt open economies Not just fighting communism but also national capitalist economies in europe and elsewhere

11 US Capitalists, and economy benefit But finance dominated by industry

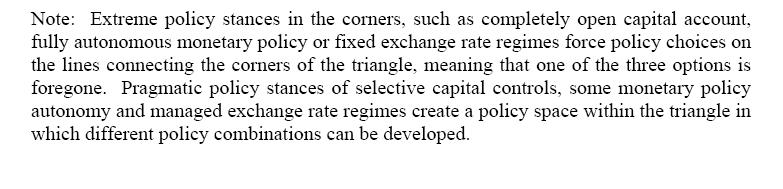

12 Eric Helleiner Over post-war period, finance makes a come back. Increase financial power over the period. Now, many argue that the power of finance supreme (Dumenil and Levy, Crotty)

13 Obstfeld and Taylor Organize their history by idea of trilemma in international economy.

14 Bradford

15

16 Questions about Trilemma How do governments choose where on triangle to be? What are the role of class forces and coalitions? What is the role of underlying productive structre?

17 Questions about Trilemma What are the impacts of different choices in terms of income distribution, economic growth, class power? Where do IMF/World Bank push countries to be and why? Domestic capitalists? What are their interests?

18 Capital Mobility and Financialization Finance push for financial liberalization and capital mobility What are impacts?

19 Summary of Two Related Framework: Trilemma and policy Choice Trilemma Stable Exchange Rate Free capital mobility Autonomous macroeconomic policy Conflicts Capital labor Finance industry Center periphery (country s location in the international economy and structure of corporate governance and financial markets)

20 Two other big frameworks of great relevance to understanding dynamics of international finance I. International Monetary Regime Organization of the International Monetary System 2. International Credit Regime - organization of the supply, demand and enforcement of credit relations

21 International Trade Regime This is a third framework of key importance But we will not directly address this much in this class except where it clearly and significantly interacts with the other two

22 International Monetary Regime - It Involves: Exchange Rate Mechanism (fixed; floating; managed) Currency (ies) Used in various roles Reserve currency International medium (a) of exchange International means of payment N-1 Country Mechanisms of coordination and monitoring

23 Which Countries can issue hard currencies Key divide in global economy (medium of exchange, and means of payment dollars; pesos?)

24 Key Currencies Store of value (reserves) Medium of exchange (vehicle currency) Intervention currency (intervene in foreign exchange markets) Means of payment (service debts)

25 International Monetary Systems See next slide

26

27 International Credit Regime: Has Two Components Operating in Tandem Enforcement Regime: The institutions and policies implemented by creditors to punish non-payment and reward payment Repayment Regime: the institutions and policies implemented by debtors to credibly signal that they will repay

28 International Credit Regime has a Third Component Working in Tension with the Other Two The Keynesian/Mynskian Imperative: Competition, behavioral aspects, and fundamental uncertainty: Excessive lending and bubbles

29 Enforcement Regime in Tension and Contradiction Enforcement Regime Repayment Regime Keynsian/Minskian Imperatives

30 Current Aspects of International Credit Regime

31

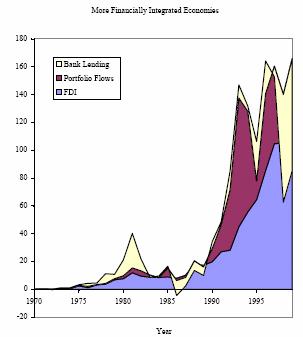

32 International Credit Regime (continued)

33 Implicit in These are Different Theories/Models of International Capital Markets

34 Different Theories Walrasian: interest rates clear markets; exogenous enforcement of contracts; rationality and perfect information New Keynesian/Asymmetric Information: non-market clearing; non exogenous enforcement; principal-agent problems Power Laden: non exogenous enforcement (marxian, neo-marxian)

35 Different Theories: continued Keynesian/Minskyian: fundamental uncertainty; endogenous cycles Behavioral Finance: psychological departures from rationality

36 Survey of Some Current Financial Markets/Institutions

37 Current value of Daily Forex trading 1.9 trillion dollars daily

38 Source: Bank for International Settlements

39 Types of financial flows: Debt -portfolio -banks Equity -portfolio -FDI Derivatives and other exotic transactions

40 4 Figure 1: Increasing Capital Account Openness High Income Countries 3.5 Capital Account Openness Lower Middle Income Countries Upper Middle Income Countries Low Income Countries All Countries Source: Jayadev and Lee, 2005

41 This Surge in Trading and Flows Relatively new During 1930 s, WWII, and early post-war period, tight regulations over forex trading and capital flows.

42 Capital Controls Quantity based: prohibitions on trading of assets denominated in foreign exchange (forex). Examples: exchange controls, restrictions on buying or selling foreign assets Price Based: taxes on inflows or outflows of capital

43 Distinction Between De-jure and De-facto financial liberalization De-jure: legal restrictions (or the absence there-of) De-facto: quantity of flows

44

45

46

47

48

49

50

51 Financial Integration and Economic Growth

52 Uses of international financial system Transfer capital to those who have too much to those who have too little Help diversify risks Help smooth consumption Help generate jobs (FDI)

53 Critiques of International financial flows Problem: most capital is flowing from the poorer countries to the richer countries (primarily the US) When capital does flow to poorer countries, it can (and often does) lead to financial instability and crisis.

54 Source: Obstfeld /Taylor

55 Bretton Woods Institutions (BWI s) IMF World Bank Formed in 1944, Bretton Woods Conference

56 Original Functions IMF, to help stabilize the international financial system and to help avoid the deflationary bias of the world Economy in the 1930 s

57 World Bank Medium to longer term lending for reconstruction after war and for developing countries

58 IMF Became more and more involved in longer term lending structural adjustment Interfering in operations of domestic economies

59 Pushed International financial Liberalization Internal: free up domestic financial markets External: reduce capital controls

60 Washington Consensus Financial Liberalization Privatization Trade Liberalization Cut Budget Deficits

61 Washington Consensus Export led growth and free markets Making countries attractive for international investment These are the keys to economic growth

62 Prabhat Patnaik Illusionism of Finance

63 3 defining moments Third World Debt Crisis, 1982 Asian Financial Crisis, /11 Iraq and the Election of progressive leaders in Latin America, opposed to Washington consensus

64 4 Figure 1: Increasing Capital Account Openness High Income Countries 3.5 Capital Account Openness Lower Middle Income Countries Upper Middle Income Countries Low Income Countries All Countries Source: Jayadev and Lee, 2005

65 International Financial Crises Third World Debt Crisis of 1982; defining moment in world economy

66 Third World Debt Crisis Background Impacts Led to neo-liberal globalization Increasing role of IMF and structural adjustment Neo-liberalism and Washington Consensus

67 Asian Financial Crisis 2 nd defining moment What went wrong with neo-liberalism?

68 International Financial Crises Third World Debt Crisis of 1982; defining moment in world economy Asian Financial Crisis of the 1990 s

69 Third World Debt Crisis Background Impacts Led to neo-liberal globalization Increasing role of IMF and structural adjustment Neo-liberalism and Washington Consensus

70 Are capital flows volatile Pro-cyclical Sudden stops

71 What happens when capital flows and then sudden stops Individuals, companies and governments build up debts Debts denominated in foreign currencies Rely on future flows to service past flows

72 Debt Service Debt Service =interest payments plus amortization (repaying debt)

73 If debts in foreign currency When forex stops flowing in, creates problem If raise interest rates, problem worse If exchange rate falls, problem becomes worse debts denominated in foreign currency becomes greater in domestic currency

74 Effect of depreciation on value of debt Exchange rate: 1 peso = 1dollar 100 dollars debt = 100 pesos debt Exchange rate devalues (depreciates): 2 pesos = 1 dollar Now the country has 200 pesos worth of debt!!

75 Such depreciations can lead to bankruptcies

76 Volatility of Different Capital Flows FDI, Investment of Choice?

77

78

79 Does more capital flows increase economic growth?

80 No Clear Relationship between financial openess And Economic Growth

81 Conditioning on other factors

82 Volatility and Financial Integration Look here Source: IMF

83 Source: IMF

84

85 Differences between trade in Goods and in Financial Assets Financial Assets are bets on the future; trade is production in the present Trade is based on newly produced goods generates jobs. Finance ---already produced assets. Creation of a financial asset necessarily creates a debt.

86 A trade-off between Finance and Trade?

87 Scepticism about Washington Consensus Post-Washington Consensus More Policy space Not all one size fits all Capital controls?

88 Scepticism about Washington Consensus Post-Washington Consensus More Policy space Not all one size fits all Capital controls?

89 Increasing Concern Even Among Neo-liberal institutions like IMF

90 Raghuram G. Rajan Economic Counselor and Director of Research Has Financial Development Made the World Riskier?

91 Financial Landscape Altered Technical Change De-regulation Institutional Change

92 Risk: Spreading and Concentration: role of banks Securitization: selling assets ( plain vanilla assets: financial commodities) Banks holding onto less liquid assets.

93 Implications for Systemic Risk? Incentives facing bank managers and investors increasing systemic risk? Banks and other investment institutions have more incentive to take on risk:

94 Incentives to take on Risk Compensation: asymmetric: upside is compensated more than downside is penalized Performance judged relative to peers -incentive to take hidden risk -incentive to herd (ass covering) Reinforce each other in boom -willing to bear low probablity TAIL RISK

95 Tail Risk Non-normal probability distributions

96 Biggest Concern Will Banks be able to provide liquidity in the case of tail risk materializes In the past banks played that role Based on their sound balance sheets allowing them to attract liquidity in a crisis that they could on-lend

97 Illiquidity Risk? Banks today require liquid markets to hedge their bets, making them less able to provide the liquidity assurance they have provided in the past

98 Conclusion Even though there are far more participants today able to absorb risk, the financial risks that are being created by the system are greater. More pro-cyclicality Increased probablility of catastrophic meltdown.

To Fix or Not to Fix?

To Fix or Not to Fix? Linda Tesar, Department of Economics Notes at: http://www.econ.lsa.umich.edu/~ltesar April 5, 2000 Fixed vs. Flexible Exchange rates The Theory: Money demand: M/P = L(Y,I) Interest

To Fix or Not to Fix? Linda Tesar, Department of Economics Notes at: http://www.econ.lsa.umich.edu/~ltesar April 5, 2000 Fixed vs. Flexible Exchange rates The Theory: Money demand: M/P = L(Y,I) Interest

19.2 Exchange Rates in the Long Run Introduction 1/24/2013. Exchange Rates and International Finance. The Nominal Exchange Rate

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Prepared by Iordanis Petsas To Accompany. by Paul R. Krugman and Maurice Obstfeld

Chapter 22 Developing Countries: Growth, Crisis, and Reform Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld Chapter

Chapter 22 Developing Countries: Growth, Crisis, and Reform Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice Obstfeld Chapter

Objective; Introduction; Maximizing shareholder value and the corporate dynamics; Macroeconomic instability in emerging economies; Concluding remarks.

Objective; Introduction; Maximizing shareholder value and the corporate dynamics; Macroeconomic instability in emerging economies; Concluding remarks. The aim of this paper is to address the behavior of

Objective; Introduction; Maximizing shareholder value and the corporate dynamics; Macroeconomic instability in emerging economies; Concluding remarks. The aim of this paper is to address the behavior of

Index. exchange rates, 104 5, net inflows, 100, 115, Bretton Woods system, 96 7 business cycles, 57

Index additional monetary tightening (AMT), 43 4 advanced economies, central banks in, 35 6 agency problems, 153, 163n47 aggregate demand, 18, 138 9, 141 2 Asian financial crisis, 8, 10, 13 15, 57, 65,

Index additional monetary tightening (AMT), 43 4 advanced economies, central banks in, 35 6 agency problems, 153, 163n47 aggregate demand, 18, 138 9, 141 2 Asian financial crisis, 8, 10, 13 15, 57, 65,

ECO 403 L0301 Developmental Macroeconomics. Lecture 8 Balance-of-Payment Crises

ECO 403 L0301 Developmental Macroeconomics Lecture 8 Balance-of-Payment Crises Gustavo Indart Slide 1 The Capitalist Economic System Capitalism is basically an unstable economic system Disequilibrium is

ECO 403 L0301 Developmental Macroeconomics Lecture 8 Balance-of-Payment Crises Gustavo Indart Slide 1 The Capitalist Economic System Capitalism is basically an unstable economic system Disequilibrium is

483 Subject Index. Global Depositiory Receipts, 250 Grassman s law, 148, 160

Subject Index Adjustabonos, 401-3 Agency for International Development, 100 American depository receipts (ADRs): considered as foreign securities, 250; traded on over-the-counter market, 245 Arbitrage:

Subject Index Adjustabonos, 401-3 Agency for International Development, 100 American depository receipts (ADRs): considered as foreign securities, 250; traded on over-the-counter market, 245 Arbitrage:

Developing Countries Chapter 22

Developing Countries Chapter 22 1. Growth 2. Borrowing and Debt 3. Money-financed deficits and crises 4. Other crises 5. Currency board 6. International financial architecture for the future 1 Growth 1.1

Developing Countries Chapter 22 1. Growth 2. Borrowing and Debt 3. Money-financed deficits and crises 4. Other crises 5. Currency board 6. International financial architecture for the future 1 Growth 1.1

4/14/2011. Exchange Rate Policy and Devaluation. The Central Bank Balance Sheet. Central Bank Policy Options in a Crisis

Exchange Rate Policy and Devaluation BOP Surpluses: excess supply of Forex CB buys BOP Deficits: excess demand for Forex CB sells OSB must offset BOP ISLM-FX with an unexpected devaluation ISLM-FX with

Exchange Rate Policy and Devaluation BOP Surpluses: excess supply of Forex CB buys BOP Deficits: excess demand for Forex CB sells OSB must offset BOP ISLM-FX with an unexpected devaluation ISLM-FX with

Globalization and crises

Globalization and crises Luis Servén The World Bank Kuala Lumpur, November 2016 1 Plan Stylized facts 1. Financial globalization 2. Currency crises 3. Bubbles 4. Sovereign debt and default 5. Financial

Globalization and crises Luis Servén The World Bank Kuala Lumpur, November 2016 1 Plan Stylized facts 1. Financial globalization 2. Currency crises 3. Bubbles 4. Sovereign debt and default 5. Financial

Economic Policy in PNG:

Economic Policy in PNG: 2010-2020 Institute of National Affairs 30 June 2016 Martin Davies Washington and Lee University and Development Policy Center, Crawford School of Public Policy, Australian National

Economic Policy in PNG: 2010-2020 Institute of National Affairs 30 June 2016 Martin Davies Washington and Lee University and Development Policy Center, Crawford School of Public Policy, Australian National

Chapter 18. The International Financial System

Chapter 18 The International Financial System Unsterilized Foreign Exchange Intervention Federal Reserve System Assets Liabilities Federal Reserve System Assets Liabilities Foreign Assets -$1B Currency

Chapter 18 The International Financial System Unsterilized Foreign Exchange Intervention Federal Reserve System Assets Liabilities Federal Reserve System Assets Liabilities Foreign Assets -$1B Currency

The Economics of the European Union

Fletcher School of Law and Diplomacy, Tufts University The Economics of the European Union Professor George Alogoskoufis Lecture 10: Introduction to International Macroeconomics Scope of International

Fletcher School of Law and Diplomacy, Tufts University The Economics of the European Union Professor George Alogoskoufis Lecture 10: Introduction to International Macroeconomics Scope of International

9 Right Prices for Interest and Exchange Rates

9 Right Prices for Interest and Exchange Rates Roberto Frenkel R icardo Ffrench-Davis presents a critical appraisal of the reforms of the Washington Consensus. He criticises the reforms from two perspectives.

9 Right Prices for Interest and Exchange Rates Roberto Frenkel R icardo Ffrench-Davis presents a critical appraisal of the reforms of the Washington Consensus. He criticises the reforms from two perspectives.

The Economics of International Financial Crises 3. An Introduction to International Macroeconomics and Finance

Fletcher School of Law and Diplomacy, Tufts University The Economics of International Financial Crises 3. An Introduction to International Macroeconomics and Finance Prof. George Alogoskoufis Scope of

Fletcher School of Law and Diplomacy, Tufts University The Economics of International Financial Crises 3. An Introduction to International Macroeconomics and Finance Prof. George Alogoskoufis Scope of

Open Economy AS/AD: Applications

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Open Economy AS/AD: Applications Econ 309 Martin Ellison UBC Agenda and References Trilemma Jones, chapter 20, section 7 Euro crisis Jones, chapter 20, section 8 Global imbalances Jones, chapter 29, section

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System

Chapter 18 The International Financial System") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

Design Failures in the Eurozone. Can they be fixed? Paul De Grauwe London School of Economics Eurozone s design failures: in a nutshell 1. Endogenous dynamics of booms and busts endemic in capitalism continued

ECO 406 Developmental Macroeconomics. Lecture 2 The Role of Aggregate Demand in the Process of Growth

ECO 406 Developmental Macroeconomics Lecture 2 The Role of Aggregate Demand in the Process of Growth Gustavo Indart Slide 1 Insufficient Aggregate Demand and Recessions How to increase Aggregate Demand

ECO 406 Developmental Macroeconomics Lecture 2 The Role of Aggregate Demand in the Process of Growth Gustavo Indart Slide 1 Insufficient Aggregate Demand and Recessions How to increase Aggregate Demand

( ) 1945) Successes and Failures in Japanese Economic Development. Phase II (1970s 80s) Failure to reform & bubble economy

1945) Successes and Failures in Japanese Economic Development. Phase II (1970s 80s) Failure to reform & bubble economy") Post-war Development of the Japanese Economy Development, Japanese/Asian Style April, 8 Shigeru T. Otsubo* GSID, Nagoya University Devastation during WWII (1941-1945) 1945) Human loss 1.85 million (.8

Post-war Development of the Japanese Economy Development, Japanese/Asian Style April, 8 Shigeru T. Otsubo* GSID, Nagoya University Devastation during WWII (1941-1945) 1945) Human loss 1.85 million (.8

Chapter 7 Fixed Exchange Rate Regimes and Short Run Macroeconomic Policy

George Alogoskoufis, International Macroeconomics and Finance Chapter 7 Fixed Exchange Rate Regimes and Short Run Macroeconomic Policy Up to now we have been assuming that the exchange rate is determined

George Alogoskoufis, International Macroeconomics and Finance Chapter 7 Fixed Exchange Rate Regimes and Short Run Macroeconomic Policy Up to now we have been assuming that the exchange rate is determined

Chapter 18. The International Financial System Intervention in the Foreign Exchange Market

Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding of foreign assets in the foreign exchange market

Chapter 18 The International Financial System 18.1 Intervention in the Foreign Exchange Market 1) A central bank of domestic currency and corresponding of foreign assets in the foreign exchange market

Chapter Eleven. The International Monetary System

Chapter Eleven The International Monetary System Introduction 11-3 The international monetary system refers to the institutional arrangements that govern exchange rates. Floating exchange rates occur when

Chapter Eleven The International Monetary System Introduction 11-3 The international monetary system refers to the institutional arrangements that govern exchange rates. Floating exchange rates occur when

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, Barry Bosworth

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

Financing the U.S. Trade Deficit

Order Code RL33274 Financing the U.S. Trade Deficit Updated January 31, 2008 James K. Jackson Specialist in International Trade and Finance Foreign Affairs, Defense, and Trade Division Financing the U.S.

Order Code RL33274 Financing the U.S. Trade Deficit Updated January 31, 2008 James K. Jackson Specialist in International Trade and Finance Foreign Affairs, Defense, and Trade Division Financing the U.S.

Asian Financial Crisis. Jianing Li/Wei Ye/Jingyan Zhang 2018/11/29

Asian Financial Crisis Jianing Li/Wei Ye/Jingyan Zhang 2018/11/29 Causes--Current account deficit 1. Liberalization of capital markets. 2. Large capital inflow due to the interest rates fall in developed

Asian Financial Crisis Jianing Li/Wei Ye/Jingyan Zhang 2018/11/29 Causes--Current account deficit 1. Liberalization of capital markets. 2. Large capital inflow due to the interest rates fall in developed

The Great Depression, golden age, and global financial crisis

The Great Depression, golden age, and global financial crisis ECONOMICS Dr. Kumar Aniket Bartlett School of Construction & Project Management Lecture 17 CONTEXT Good policies and institutions can promote

The Great Depression, golden age, and global financial crisis ECONOMICS Dr. Kumar Aniket Bartlett School of Construction & Project Management Lecture 17 CONTEXT Good policies and institutions can promote

ECO 406 Developmental Macroeconomics. Lecture 1 The Theoretical and Methodological Framework

ECO 406 Developmental Macroeconomics Lecture 1 The Theoretical and Methodological Framework Gustavo Indart Slide 1 Economic Models and the Great Recession We failed to prevent and forecast the downturn

ECO 406 Developmental Macroeconomics Lecture 1 The Theoretical and Methodological Framework Gustavo Indart Slide 1 Economic Models and the Great Recession We failed to prevent and forecast the downturn

POLI 12D: International Relations Sections 1, 6

POLI 12D: International Relations Sections 1, 6 Spring 2017 TA: Clara Suong Chapter 9 International Monetary Relations 9 INTERNATIONAL MONETARY RELATIONS Core of the Analysis National Monetary Order Fixed

POLI 12D: International Relations Sections 1, 6 Spring 2017 TA: Clara Suong Chapter 9 International Monetary Relations 9 INTERNATIONAL MONETARY RELATIONS Core of the Analysis National Monetary Order Fixed

Macro-Modelling. with a focus on the role of financial markets. University of Pennsylvania ECON 244, Spring January 7, 2013.

with a focus on the role of financial markets University of Pennsylvania ECON 244, Spring 2013 Guillermo Ordoñez January 7, 2013 Course Information Instructor: Guillermo Ordonez (ordonez@econ.upenn.edu)

with a focus on the role of financial markets University of Pennsylvania ECON 244, Spring 2013 Guillermo Ordoñez January 7, 2013 Course Information Instructor: Guillermo Ordonez (ordonez@econ.upenn.edu)

Keynes, Minsky and International Financial Fragility Jan Kregel, Levy Economics Institute

Keynes, Minsky and International Financial Fragility Jan Kregel, Levy Economics Institute Draft Presentation prepared for 11th International Keynes Conference (IKC) On Globalized Capitalism Hitotsubashi

Keynes, Minsky and International Financial Fragility Jan Kregel, Levy Economics Institute Draft Presentation prepared for 11th International Keynes Conference (IKC) On Globalized Capitalism Hitotsubashi

Suggested Solutions to Problem Set 4

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 4 Problem 1 : True, False, Uncertain (a) False or Uncertain. In first generation

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 4 Problem 1 : True, False, Uncertain (a) False or Uncertain. In first generation

Chapter 6. The Balance of Payments

Chapter 6 The Balance of Payments 1 Learning Objectives To understand the fundamental principles of how countries measure international business activity, the balance of payments To examine the similarities

Chapter 6 The Balance of Payments 1 Learning Objectives To understand the fundamental principles of how countries measure international business activity, the balance of payments To examine the similarities

Chapter 19 International Monetary Systems: An Historical Overview

Chapter 19 International Monetary Systems: An Historical Overview Copyright 2012 Pearson Addison-Wesley. All rights reserved. Preview Goals of macroeconomic policies internal and external balance Gold

Chapter 19 International Monetary Systems: An Historical Overview Copyright 2012 Pearson Addison-Wesley. All rights reserved. Preview Goals of macroeconomic policies internal and external balance Gold

A post-keynesian Perspective on Capital Mobility, Exchange rate Dynamics and BoP crises in Developing Countries

A post-keynesian Perspective on Capital Mobility, Exchange rate Dynamics and BoP crises in Developing Countries Alberto Botta Co-organised by Foundation for European Progressive Studies (FEPS) Greenwich

A post-keynesian Perspective on Capital Mobility, Exchange rate Dynamics and BoP crises in Developing Countries Alberto Botta Co-organised by Foundation for European Progressive Studies (FEPS) Greenwich

Global Business Economics. Mark Crosby SEMBA International Economics

Global Business Economics Mark Crosby SEMBA International Economics The balance of payments and exchange rates Understand the structure of a country s balance of payments. Understand the difference between

Global Business Economics Mark Crosby SEMBA International Economics The balance of payments and exchange rates Understand the structure of a country s balance of payments. Understand the difference between

ECN 160B SSI Final Exam August 1 st, 2012 VERSION B

ECN 160B SSI Final Exam August 1 st, 2012 VERSION B Name: ID#: Instruction: Write your name and student ID number on this exam and your blue book and your scantron. Be sure to answer all multiple choice

ECN 160B SSI Final Exam August 1 st, 2012 VERSION B Name: ID#: Instruction: Write your name and student ID number on this exam and your blue book and your scantron. Be sure to answer all multiple choice

4. INTERNATIONAL MONETARY SYSTEMS AND BALANCE OF PAYMENTS

4. INTERNATIONAL MONETARY SYSTEMS AND BALANCE OF PAYMENTS CHAPTER OVERVIEW INTERNATIONAL MONETARY SYSTEM HISTORY PERFORMANCE OF INTERNATIONAL MONETARY SYSTEMS EUROPEAN MONETARY SYSTEMS INTERNATIONAL DEBT

4. INTERNATIONAL MONETARY SYSTEMS AND BALANCE OF PAYMENTS CHAPTER OVERVIEW INTERNATIONAL MONETARY SYSTEM HISTORY PERFORMANCE OF INTERNATIONAL MONETARY SYSTEMS EUROPEAN MONETARY SYSTEMS INTERNATIONAL DEBT

Exchange Rate Regimes

Exchange Rate Regimes Lecture 2 LIUC 2011 1 How many exchange rate regimes do we have? Hard pegs or no legal tender (23 countries or %12): No separate legal tender (10 countries) The country adopts a foreign

Exchange Rate Regimes Lecture 2 LIUC 2011 1 How many exchange rate regimes do we have? Hard pegs or no legal tender (23 countries or %12): No separate legal tender (10 countries) The country adopts a foreign

Financial Instability and Overvaluation of the Exchange Rate in Latin America: Analysis and Policy Recommendations

Brazilian Journal of Political Economy, vol. 31, nº 5 (125), pp. 833-837, Special edition 2011 the project: Financial Instability and Overvaluation of the Exchange Rate in Latin America: Analysis and Policy

Brazilian Journal of Political Economy, vol. 31, nº 5 (125), pp. 833-837, Special edition 2011 the project: Financial Instability and Overvaluation of the Exchange Rate in Latin America: Analysis and Policy

Are BRIC countries currencies to play. a dominant role in the system? A Brazilian perception

Are BRIC countries currencies to play The Policy of International Reserves a dominant role in the system? Accumulation: Lessons from the A Brazilian perception Crisis (Brazil s Perspective) Carlos Hamilton

Are BRIC countries currencies to play The Policy of International Reserves a dominant role in the system? Accumulation: Lessons from the A Brazilian perception Crisis (Brazil s Perspective) Carlos Hamilton

FINANCE, STABILITY AND GROWTH

FINANCE, STABILITY AND GROWTH 2 ND ORGANISATION OF ISLAMIC COOPERATION (OIC) EXPERTS GROUP WORKSHOP Central Banking and Financial sector Development Bank Negara Malaysia, Kuala Lumpur, Malaysia, 13-14

FINANCE, STABILITY AND GROWTH 2 ND ORGANISATION OF ISLAMIC COOPERATION (OIC) EXPERTS GROUP WORKSHOP Central Banking and Financial sector Development Bank Negara Malaysia, Kuala Lumpur, Malaysia, 13-14

Exchange Rates and International Finance

Exchange Rates and International Finance Week 12 Vivaldo Mendes Dep. of Economics Instituto Universitário de Lisboa 8 December 2017 (Vivaldo Mendes ISCTE-IUL ) Macroeconomics I (L0271) 8 December 2014

Exchange Rates and International Finance Week 12 Vivaldo Mendes Dep. of Economics Instituto Universitário de Lisboa 8 December 2017 (Vivaldo Mendes ISCTE-IUL ) Macroeconomics I (L0271) 8 December 2014

International Finance Prof. A. K. Misra Department of Management Indian Institute of Technology, Kharagpur

International Finance Prof. A. K. Misra Department of Management Indian Institute of Technology, Kharagpur Lecture - 1 International Financial Environment Good morning, today we will discuss about international

International Finance Prof. A. K. Misra Department of Management Indian Institute of Technology, Kharagpur Lecture - 1 International Financial Environment Good morning, today we will discuss about international

Presentation. The Boom in Capital Flows and Financial Vulnerability in Asia

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 2011, Manila,

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 2011, Manila,

Designing Financial Safety Net A.Prasetyantoko ATMA JAYA School of Economics and Business

Designing Financial Safety Net A.Prasetyantoko ATMA JAYA School of Economics and Business International Seminar Befriending with the "Boom-Bust" Cycle, Jakarta, 23 September 2914, Indonesia Deposit Insurance

Designing Financial Safety Net A.Prasetyantoko ATMA JAYA School of Economics and Business International Seminar Befriending with the "Boom-Bust" Cycle, Jakarta, 23 September 2914, Indonesia Deposit Insurance

Financing the U.S. Trade Deficit

Order Code RL33274 Financing the U.S. Trade Deficit Updated September 4, 2007 James K. Jackson Specialist in International Trade and Finance Foreign Affairs, Defense, and Trade Division Financing the U.S.

Order Code RL33274 Financing the U.S. Trade Deficit Updated September 4, 2007 James K. Jackson Specialist in International Trade and Finance Foreign Affairs, Defense, and Trade Division Financing the U.S.

Bretton Woods II: The Reemergence of the Bretton Woods System

Bretton Woods II: The Reemergence of the Bretton Woods System by Teresa M. Foy January 28, 2005 Department of Economics, Queen s University, Kingston, Ontario, Canada, K7L 3N6. foyt@qed.econ.queensu.ca,

Bretton Woods II: The Reemergence of the Bretton Woods System by Teresa M. Foy January 28, 2005 Department of Economics, Queen s University, Kingston, Ontario, Canada, K7L 3N6. foyt@qed.econ.queensu.ca,

Policy Options for Dealing with the Impact of the Financial Crisis on the External Debt of Developing Countries

U.N. Department of Economic and Social Affairs Financing for Development Office Policy Options for Dealing with the Impact of the Financial Crisis on the External Debt of Developing Countries Implementation

U.N. Department of Economic and Social Affairs Financing for Development Office Policy Options for Dealing with the Impact of the Financial Crisis on the External Debt of Developing Countries Implementation

Review of. Financial Crises, Liquidity, and the International Monetary System by Jean Tirole. Published by Princeton University Press in 2002

Review of Financial Crises, Liquidity, and the International Monetary System by Jean Tirole Published by Princeton University Press in 2002 Reviewer: Franklin Allen, Finance Department, Wharton School,

Review of Financial Crises, Liquidity, and the International Monetary System by Jean Tirole Published by Princeton University Press in 2002 Reviewer: Franklin Allen, Finance Department, Wharton School,

International Finance

International Finance 19 1 Balance of Payments International economic transactions Flow of transactions period of time May not involve cash payments Double-entry bookkeeping Credits Inflow of receipts

International Finance 19 1 Balance of Payments International economic transactions Flow of transactions period of time May not involve cash payments Double-entry bookkeeping Credits Inflow of receipts

Notes on Hyman Minsky s Financial Instability Hypothesis

FINANCIAL INSTABILITY Prof. Pavlina R. Tcherneva Econ 331/WS 2006 Notes on Hyman Minsky s Financial Instability Hypothesis Summary Prior to WWII, economies were described by frequent and severe depressions

FINANCIAL INSTABILITY Prof. Pavlina R. Tcherneva Econ 331/WS 2006 Notes on Hyman Minsky s Financial Instability Hypothesis Summary Prior to WWII, economies were described by frequent and severe depressions

CRS Report for Congress

Order Code RL33274 CRS Report for Congress Received through the CRS Web Financing the U.S. Trade Deficit February 14, 2006 James K. Jackson Specialist in International Trade and Finance Foreign Affairs,

Order Code RL33274 CRS Report for Congress Received through the CRS Web Financing the U.S. Trade Deficit February 14, 2006 James K. Jackson Specialist in International Trade and Finance Foreign Affairs,

News STABILIZING CAPITAL FLOWS TO EMERGING MARKETS. Contact: John Williamson, July 19, 2005

News 1 7 5 0 M A SS A C H U S E T T S A V E N U E, N W W A S H I N G T O N, D C 2 0 0 3 6-1 9 0 3 T E L : ( 2 0 2 ) 3 2 8-9 0 0 0 F A X : ( 2 0 2 ) 6 5 9-3 2 2 5 W W W. I I E. C O M Contact: John Williamson,

News 1 7 5 0 M A SS A C H U S E T T S A V E N U E, N W W A S H I N G T O N, D C 2 0 0 3 6-1 9 0 3 T E L : ( 2 0 2 ) 3 2 8-9 0 0 0 F A X : ( 2 0 2 ) 6 5 9-3 2 2 5 W W W. I I E. C O M Contact: John Williamson,

Slides for International Finance Macroeconomic Policy (KOM Chapter 19)

") Macroeconomic Policy (KOM Chapter 19) American University 2010-09-17 Preview Macroeconomic Policy Goals of macroeconomic policies Monetary standards Gold standard International monetary system during 1918-1939

Macroeconomic Policy (KOM Chapter 19) American University 2010-09-17 Preview Macroeconomic Policy Goals of macroeconomic policies Monetary standards Gold standard International monetary system during 1918-1939

Development Policy Macro Management and Development Macro Stability and Growth: Case Study of Vietnam

Development Policy Macro Management and Development Macro Stability and Growth: Case Study of Vietnam James Riedel Outline: 1. How macro stability/instability is measured? 2. Inflation rate in Vietnam

Development Policy Macro Management and Development Macro Stability and Growth: Case Study of Vietnam James Riedel Outline: 1. How macro stability/instability is measured? 2. Inflation rate in Vietnam

Singapore Economic Review Conference (SERC) 2007

2007") Singapore Economic Review Conference (SERC) 2007 2-4 th August 2007 Meritus Mandarin Hotel, Singapore Keynote Address by Professor Joseph Stiglitz, 2001 Nobel Laureate in Economics Global Financial Integration,

Singapore Economic Review Conference (SERC) 2007 2-4 th August 2007 Meritus Mandarin Hotel, Singapore Keynote Address by Professor Joseph Stiglitz, 2001 Nobel Laureate in Economics Global Financial Integration,

UNIT FIVE (5) The International Monetary Environment and Financial Management in the Global Firm

The International Monetary Environment and Financial Management in the Global Firm") UNIT FIVE (5) The International Monetary Environment and Financial Management in the Global Firm Objectives Exchange rates and currencies How exchange rates are determined The monetary and financial systems

UNIT FIVE (5) The International Monetary Environment and Financial Management in the Global Firm Objectives Exchange rates and currencies How exchange rates are determined The monetary and financial systems

Chapter 29 The Global Economy and Policy Principles of Economics in Context (Goodwin et al)

") Chapter 29 The Global Economy and Policy Principles of Economics in Context (Goodwin et al) Chapter Overview This chapter will take you through the basics of international trade and finance. The chapter

Chapter 29 The Global Economy and Policy Principles of Economics in Context (Goodwin et al) Chapter Overview This chapter will take you through the basics of international trade and finance. The chapter

Impact of Rupee- Dollar Fluctuations on Indian Economy

Impact of Rupee- Dollar Fluctuations on Indian Economy Ayush Singh 1, Vinaytosh Mishra 2, Akhilendra.B.Singh 3 Department of Mechanical Engineering, Indian Institute of Technology (BHU) Varanasi 221005

Impact of Rupee- Dollar Fluctuations on Indian Economy Ayush Singh 1, Vinaytosh Mishra 2, Akhilendra.B.Singh 3 Department of Mechanical Engineering, Indian Institute of Technology (BHU) Varanasi 221005

Quantitative Easing and the implications for Actuaries & Economics Discussion

Quantitative Easing and the implications for Actuaries & Economics Discussion Colm Fitzgerald Dublin City University / Paragon Research Ltd Society of Actuaries in Ireland May 17 th 2011 Introduction Context

Quantitative Easing and the implications for Actuaries & Economics Discussion Colm Fitzgerald Dublin City University / Paragon Research Ltd Society of Actuaries in Ireland May 17 th 2011 Introduction Context

Suggested Solutions to Problem Set 6

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

Department of Economics University of California, Berkeley Spring 2006 Economics 182 Suggested Solutions to Problem Set 6 Problem 1: International diversification Because raspberries are nontradable, asset

Chapter# The Level and Structure of Interest Rates

Chapter# The Level and Structure of Interest Rates Outline The Theory of Interest Rates o Fisher s Classical Approach o The Loanable Funds Theory o The Liquidity Preference Theory o Changes in the Money

Chapter# The Level and Structure of Interest Rates Outline The Theory of Interest Rates o Fisher s Classical Approach o The Loanable Funds Theory o The Liquidity Preference Theory o Changes in the Money

Introduction to Economics. MACROECONOMICS Chapter 6 International Economics

Introduction to Economics MACROECONOMICS Chapter 6 International Economics contents 6.1 6.2 6.3 6.4 6.5 6.6 Theory of Comparative Advantage Gains from International Trade Trade Barriers Balance of Payments

Introduction to Economics MACROECONOMICS Chapter 6 International Economics contents 6.1 6.2 6.3 6.4 6.5 6.6 Theory of Comparative Advantage Gains from International Trade Trade Barriers Balance of Payments

3. TFU: A zero rate of increase in the Consumer Price Index is an appropriate target for monetary policy.

Econ 304 Fall 2014 Final Exam Review Questions 1. TFU: Many Americans derive great utility from driving Japanese cars, yet imports are excluded from GDP. Thus GDP should not be used as a measure of economic

Econ 304 Fall 2014 Final Exam Review Questions 1. TFU: Many Americans derive great utility from driving Japanese cars, yet imports are excluded from GDP. Thus GDP should not be used as a measure of economic

POLICY PRESCRIPTIONS FOR EAST ASIA

POLICY PRESCRIPTIONS FOR EAST ASIA Masaru Yoshitomi* At the Asian Development Bank Institute in Tokyo, we recently produced policy recommendations about how to avoid another financial crisis and, if we

POLICY PRESCRIPTIONS FOR EAST ASIA Masaru Yoshitomi* At the Asian Development Bank Institute in Tokyo, we recently produced policy recommendations about how to avoid another financial crisis and, if we

Alternatives to Inflation Targeting for Equitable, Stable and Sustainable Development

Alternatives to Inflation Targeting for Equitable, Stable and Sustainable Development Gerald Epstein Professor of Economics and Co-Director Political Economy Research Institute (PERI) University of Massachusetts,

Alternatives to Inflation Targeting for Equitable, Stable and Sustainable Development Gerald Epstein Professor of Economics and Co-Director Political Economy Research Institute (PERI) University of Massachusetts,

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 55

The Financial System 1 / 55") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

Dunbar s Big Review Sheet AP Macroeconomics Exam Content Area [Hubbard Textbook pages] (percentage coverage on AP Macroeconomics Exam) I.

![Dunbar s Big Review Sheet AP Macroeconomics Exam Content Area [Hubbard Textbook pages] (percentage coverage on AP Macroeconomics Exam) I.](/thumbs/77/76534172.jpg "Dunbar s Big Review Sheet AP Macroeconomics Exam Content Area [Hubbard Textbook pages] (percentage coverage on AP Macroeconomics Exam) I.") Dunbar s Big Review Sheet AP Macroeconomics Exam Content Area [Hubbard Textbook pages] (percentage coverage on AP Macroeconomics Exam) I. Basic Economic Concepts (8-12%) Three Fundamental Questions [8]:

Dunbar s Big Review Sheet AP Macroeconomics Exam Content Area [Hubbard Textbook pages] (percentage coverage on AP Macroeconomics Exam) I. Basic Economic Concepts (8-12%) Three Fundamental Questions [8]:

MANAGING CAPITAL FLOWS

MANAGING CAPITAL FLOWS Yılmaz Akyüz South Centre, Geneva Capital Account Regulations and Global Economic Governance Workshop Organized by UNCTAD and GEGI, Geneva, Palais des Nations, 3-4 October 2013 www.southcentre.int

MANAGING CAPITAL FLOWS Yılmaz Akyüz South Centre, Geneva Capital Account Regulations and Global Economic Governance Workshop Organized by UNCTAD and GEGI, Geneva, Palais des Nations, 3-4 October 2013 www.southcentre.int

The IMF. Benjamin Graham

The IMF Benjamin Graham The IMF Benjamin Graham Housekeeping Brief Note: Why I assigned readings that are generally pro-imf Reading Quiz (1) Which of the following are true? a. The IMF stands for the International

The IMF Benjamin Graham The IMF Benjamin Graham Housekeeping Brief Note: Why I assigned readings that are generally pro-imf Reading Quiz (1) Which of the following are true? a. The IMF stands for the International

Discussion of: On the Desirability of Capital Controls. Markus K. Brunnermeier. IMF Jacques Polak conference. Princeton University

Discussion of: On the Desirability of Capital Controls Markus K. Brunnermeier Princeton University International Credit Flows, IMF Jacques Polak conference Washington, DC, Nov. 13 th, 2014 Capital Flows:

Discussion of: On the Desirability of Capital Controls Markus K. Brunnermeier Princeton University International Credit Flows, IMF Jacques Polak conference Washington, DC, Nov. 13 th, 2014 Capital Flows:

Financial Bubbles: What is next?

Financial Bubbles: What is next? Professor El Thalassinos University of Piraeus, Greece www.unipi.gr Chair Jean Monnet General Editor ERSJ www.ersj.eu 1 Abstract The main aim of this paper is: to analyse

Financial Bubbles: What is next? Professor El Thalassinos University of Piraeus, Greece www.unipi.gr Chair Jean Monnet General Editor ERSJ www.ersj.eu 1 Abstract The main aim of this paper is: to analyse

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 52

The Financial System 1 / 52") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

THE GLOBAL ECONOMY AND POLICY Macroeconomics in Context (Goodwin, et al.)

") Chapter 14 THE GLOBAL ECONOMY AND POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter will take you through the basics of international trade and finance. The chapter introduces

Chapter 14 THE GLOBAL ECONOMY AND POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter will take you through the basics of international trade and finance. The chapter introduces

From Cardinal Sin to Policy Agenda? The Role of Capital Controls in Emerging Market Economies: A Study of the Korean Case,

From Cardinal Sin to Policy Agenda? The Role of Capital Controls in Emerging Market Economies: A Study of the Korean Case, 1997-2011, PhD Candidate Department of Political Science, Boston University /

From Cardinal Sin to Policy Agenda? The Role of Capital Controls in Emerging Market Economies: A Study of the Korean Case, 1997-2011, PhD Candidate Department of Political Science, Boston University /

East Asia s Foreign Exchange Rate Policies

Order Code RS22860 April 10, 2008 East Asia s Foreign Exchange Rate Policies Summary Michael F. Martin Analyst in Asian Trade and Finance Foreign Affairs, Defense, and Trade Division The economies of East

Order Code RS22860 April 10, 2008 East Asia s Foreign Exchange Rate Policies Summary Michael F. Martin Analyst in Asian Trade and Finance Foreign Affairs, Defense, and Trade Division The economies of East

Business cycle fluctuations Part II

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

Understanding the World Economy Master in Economics and Business Business cycle fluctuations Part II Lecture 7 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 7: Business cycle fluctuations

TOWARDS A REFORM OF THE GLOBAL RESERVE SYSTEM 1. Joseph E. Stiglitz Columbia University

TOWARDS A REFORM OF THE GLOBAL RESERVE SYSTEM 1 Joseph E. Stiglitz Columbia University It is a pleasure to be here and to have an opportunity to discuss what I consider to be one of the most important

TOWARDS A REFORM OF THE GLOBAL RESERVE SYSTEM 1 Joseph E. Stiglitz Columbia University It is a pleasure to be here and to have an opportunity to discuss what I consider to be one of the most important

Lecture 20: Exchange Rate Regimes. Prof.J.Frankel

Lecture 20: Exchange Rate Regimes What exchange rate regimes do countries choose? 1. Classification of exchange rate regimes What regimes should countries choose? 2. Advantages of fixed rates 3. Advantages

Lecture 20: Exchange Rate Regimes What exchange rate regimes do countries choose? 1. Classification of exchange rate regimes What regimes should countries choose? 2. Advantages of fixed rates 3. Advantages

Fragility of Incomplete Monetary Unions

Fragility of Incomplete Monetary Unions Incomplete monetary unions Fixed exchange-rate regimes that fall short of a full monetary union but they substantially constrain the ability of the national government

Fragility of Incomplete Monetary Unions Incomplete monetary unions Fixed exchange-rate regimes that fall short of a full monetary union but they substantially constrain the ability of the national government

LECTURE XIV. 31 July Tuesday, July 31, 12

LECTURE XIV 31 July 2012 TOPIC 16 Exchange Rates and Policy BIG PICTURE What are different common exchange rate systems? How can exchange rates be manipulated to affect a country s real variables? What

LECTURE XIV 31 July 2012 TOPIC 16 Exchange Rates and Policy BIG PICTURE What are different common exchange rate systems? How can exchange rates be manipulated to affect a country s real variables? What

THE IMF: INSTRUMENTS AND STRATEGIES. Lecture 4 LIUC 2008

THE IMF: INSTRUMENTS AND STRATEGIES Lecture 4 LIUC 2008 WHAT IS THE INTERNATIONAL MONETARY FUND? The IMF is an international cooperative financial institution. Each member deposits a sum of money into

THE IMF: INSTRUMENTS AND STRATEGIES Lecture 4 LIUC 2008 WHAT IS THE INTERNATIONAL MONETARY FUND? The IMF is an international cooperative financial institution. Each member deposits a sum of money into

POLICY BRIEF. Resurgent Capital Flows to Developing Countries: Policies to Improve Their Impact

J u n e 2 0 1 3 n u m b e r 1 0 Resurgent Capital Flows to Developing Countries: Policies to Improve Their Impact James A. Hanson* Overview Some developing countries have reinstated controls on capital

J u n e 2 0 1 3 n u m b e r 1 0 Resurgent Capital Flows to Developing Countries: Policies to Improve Their Impact James A. Hanson* Overview Some developing countries have reinstated controls on capital

THE 5th ANNUAL CUSCO CONFERENCE ORGANIZED BY THE CENTRAL RESERVE BANK OF PERU AND THE REINVENTING BRETTON WOODS COMMITTEE SESSION DISCUSSION POINTS

THE 5th ANNUAL CUSCO CONFERENCE ORGANIZED BY THE CENTRAL RESERVE BANK OF PERU AND THE REINVENTING BRETTON WOODS COMMITTEE SESSION DISCUSSION POINTS 70 YEARS AFTER BRETTON WOODS: MANAGING THE INTERCONNECTEDNESS

THE 5th ANNUAL CUSCO CONFERENCE ORGANIZED BY THE CENTRAL RESERVE BANK OF PERU AND THE REINVENTING BRETTON WOODS COMMITTEE SESSION DISCUSSION POINTS 70 YEARS AFTER BRETTON WOODS: MANAGING THE INTERCONNECTEDNESS

Mexico s relationship with its real exchange rate has been tumultuous since its first

Policy Brief Stanford Institute for Economic Policy Research Mexico s Macroeconomic Policy Dilemma: How to deal with the super-peso? José Antonio González Mexico s relationship with its real exchange rate

Policy Brief Stanford Institute for Economic Policy Research Mexico s Macroeconomic Policy Dilemma: How to deal with the super-peso? José Antonio González Mexico s relationship with its real exchange rate

G20 Working Group on the Reform of the International Monetary System

UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENT G2 Working Group on the Reform of the International Monetary System Contribution by the UNCTAD Secretariat to Subgroup I: Capital Flow Management March

UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENT G2 Working Group on the Reform of the International Monetary System Contribution by the UNCTAD Secretariat to Subgroup I: Capital Flow Management March

Volume Author/Editor: Takatoshi Ito and Anne O. Krueger, Editors. Volume URL:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Financial Deregulation and Integration in East Asia, NBER-EASE Volume 5 Volume Author/Editor:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Financial Deregulation and Integration in East Asia, NBER-EASE Volume 5 Volume Author/Editor:

The International Monetary System

The International Monetary System Eiteman et al., Chapter 2 Winter 2004 Outline of the Chapter Currency Terminology History of the International Monetary System Contemporary Currency Regimes Emerging Markets

The International Monetary System Eiteman et al., Chapter 2 Winter 2004 Outline of the Chapter Currency Terminology History of the International Monetary System Contemporary Currency Regimes Emerging Markets

Globalization of Korea s Foreign Exchange System. Seoul Asian Financial Forum. June 4, Michael Hellbeck

Globalization of Korea s Foreign Exchange System Seoul Asian Financial Forum June 4, 2012 Michael Hellbeck COO & Head of Regulatory Affairs Standard Chartered Bank Korea 2 Agenda Introduction to Standard

Globalization of Korea s Foreign Exchange System Seoul Asian Financial Forum June 4, 2012 Michael Hellbeck COO & Head of Regulatory Affairs Standard Chartered Bank Korea 2 Agenda Introduction to Standard

The International Financial System

The International Financial System Notes on Mishkin, Chapter 21 Leigh Tesfatsion Economics Department Iowa State University, Ames IA Last Revised: 27 April 2011 Key In-Class Discussion Questions Mishkin,

The International Financial System Notes on Mishkin, Chapter 21 Leigh Tesfatsion Economics Department Iowa State University, Ames IA Last Revised: 27 April 2011 Key In-Class Discussion Questions Mishkin,

Chapter 24 CRISES IN EMERGING MARKETS

Chapter 24 CRISES IN EMERGING MARKETS The previous chapter extended the IS-LM-BP model to accommodate high capital mobility. Chapter 24 applies that model to the crises that beset some middle-income countries

Chapter 24 CRISES IN EMERGING MARKETS The previous chapter extended the IS-LM-BP model to accommodate high capital mobility. Chapter 24 applies that model to the crises that beset some middle-income countries

The politics of Brazilian debt dynamics in the light of Argentina s default 1. By Domingo F. Cavallo

The politics of Brazilian debt dynamics in the light of Argentina s default 1 The political and economic decisions of Brazilian President Luis Inacio Lula da Silva in connection with the country s public

The politics of Brazilian debt dynamics in the light of Argentina s default 1 The political and economic decisions of Brazilian President Luis Inacio Lula da Silva in connection with the country s public

Banks can also borrow reserves from the Fed at the (Click to select) at the. References

at the. References") 1. Award: 10.00 points If a bank is unable to borrow reserves from the Fed funds market to meet its reserve requirement, where else might it borrow reserves? What is the name of the rate it pays to borrow

1. Award: 10.00 points If a bank is unable to borrow reserves from the Fed funds market to meet its reserve requirement, where else might it borrow reserves? What is the name of the rate it pays to borrow

Canada s Pioneering Experience with a Flexible Exchange Rate in the 1950s: (Hard) Lessons Learned for Monetary Policy in a Small Open Economy.

Lessons Learned for Monetary Policy in a Small Open Economy.") Canada s Pioneering Experience with a Flexible Exchange Rate in the 1950s: (Hard) Lessons Learned for Monetary Policy in a Small Open Economy. Lawrence Schembri International Department Bank of Canada

Canada s Pioneering Experience with a Flexible Exchange Rate in the 1950s: (Hard) Lessons Learned for Monetary Policy in a Small Open Economy. Lawrence Schembri International Department Bank of Canada

Chapter 19 (8) International Monetary Systems: An Historical Overview

International Monetary Systems: An Historical Overview") Chapter 19 (8) International Monetary Systems: An Historical Overview Preview Goals of macroeconomic policies internal and external balance Gold standard era 1870 1914 International monetary system during

Chapter 19 (8) International Monetary Systems: An Historical Overview Preview Goals of macroeconomic policies internal and external balance Gold standard era 1870 1914 International monetary system during

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

internationa macroeconomics

internationa macroeconomics ROBERT C. FEENSTRA ALAN M.TAYLOR University WORTH PUBLISHERS Contents Preface XVII CHAPTER 1 The Globai Macroeconomy 1 PART 1 1 Foreign Exchange: Of Currencies and Crises 2,.

internationa macroeconomics ROBERT C. FEENSTRA ALAN M.TAYLOR University WORTH PUBLISHERS Contents Preface XVII CHAPTER 1 The Globai Macroeconomy 1 PART 1 1 Foreign Exchange: Of Currencies and Crises 2,.

Making Securitization Work for Financial Stability and Economic Growth

Shadow Financial Regulatory Committees of Asia, Australia-New Zealand, Europe, Japan, Latin America, and the United States Making Securitization Work for Financial Stability and Economic Growth Joint Statement

Shadow Financial Regulatory Committees of Asia, Australia-New Zealand, Europe, Japan, Latin America, and the United States Making Securitization Work for Financial Stability and Economic Growth Joint Statement

Future strategies for regional financial development

Future strategies for regional financial development March 2, 2009 Tokyo, Japan Noritaka Akamatsu The World Bank Issues Implications of the global financial crisis for the Asian markets and the main policy

Future strategies for regional financial development March 2, 2009 Tokyo, Japan Noritaka Akamatsu The World Bank Issues Implications of the global financial crisis for the Asian markets and the main policy