COLLECTION POLICY - SAMPLE -

|

|

|

- Jonah Toby Hill

- 5 years ago

- Views:

Transcription

1 COLLECTION POLICY - SAMPLE - Auteur: VVCM Contents 1 Scope 1.1 Objective Organisation Responsibility 3 2. Collections Introduction Collections Practices Customer Segmentation for Collections Collection strategy Reminder stop Debt Recovery Payment plans Legal Proceedings Doubtful & Uncollectible accounts buckets Specific provision aligned with accounting instructions A/R write-off align with accounting instructions Income from cash collections on written off receivables 7 3 Credit Stop Customer Credit Stop Process Aged Debt Report Reviewed Stop Process Release 9 4 Dispute Management Overview Objectives of Dispute Management Organization, Authorities, Escalation Organization Resolution and Authorization Escalations Reminder Stop Sales Teams 10 5 Reporting 10 1

2 1.Scope This Credit Policy is part of the documentation of the Credit and Collections management covering all aspects Credit Management activities. The Collections Policy specifies guidelines, standard practices, and authorization limits. 1.1 Objective This Credit and Collections Policy is designed to maximise earnings and profit from sales revenue and minimise exposure to slow paying customers and trade losses ensuring a healthy cash and working capital position. This is accomplished by applying consistent practices being cognizant of country, and regional differences in operations, customs, and resources. Policy compliance will be evaluated through independent audit reviews based upon this Credit and Collections Policy. This template Collections Policy describes the procedures which will be followed by the Credit and Collections Staff. This Policy will be reviewed periodically and adjusted as required dependent upon: Market conditions Economic conditions Working Capital requirements. 1.2 Organisation The Credit and Collection activities will be structured as per the following Organisation chart: 2

3 1.3 Responsibility The O2C [Credit manager] has the overall responsibility for the Credit Policy. This includes any policy modifications. The policy will always be in compliance with the Group Policies and Procedures. The O2C [Credit manager] acts as the administrator of the Policy. Overview of the Credit and Collection responsibilities The Credit and Collections Strategy aims at optimizing the effectiveness and the efficiency of the Credit and Collections Department whilst adhering to the Credit and Collections Strategic Objectives of the group. The O2C [Credit manager] remains responsible overall for the O2C processes of Customer Master Data, Credit Management, Collections and Cash Application, even though the individual tasks are performed by the organization. 2. Collections 2.1 Introduction Customers are expected to pay all invoices on or before the designated due date. Proactively, the Collections department should identify and correct process defects that would prevent a customer from paying on time. Best Practice methods will advise displaying process standards, scorecards and other forms of guidance prominently in the workplace, improving Collection productivity and Communication and include KPIs together with goals and metrics. (DSO, Cash collected, overdues, ageing of receivables, bad debts). This will lead to following the practice of establishing and conducting routine interactions for reviewing collections performance, managing work and assigning actions, for managing daily operations and driving collection improvement. When a customer is past due, the intent of this process is to determine the reason for non-payment and take appropriate steps to collect from customers unable to pay or correct the defect that renders the customer unwilling to pay. Actions are taken to obtain payment as quickly as possible, in a cost-effective manner, consistent with local laws and business practices. Effective collection practices serve to identify and minimize risk of loss and improve cash flow and serve to identify and minimize risk of loss. 2.2 Collections Practices Customer accounts receivables are aged. The collection call prioritization for collectors will be based on a treatment schedule determined for each customer segment. It is the responsibility of Credit Department to ensure that the treatment schedules are maintained in accordance with the agreements with. O2C [Credit manager] will assess each treatment schedule on an ongoing basis and adjust where required in line with market and economic conditions along with customer behaviours. 3

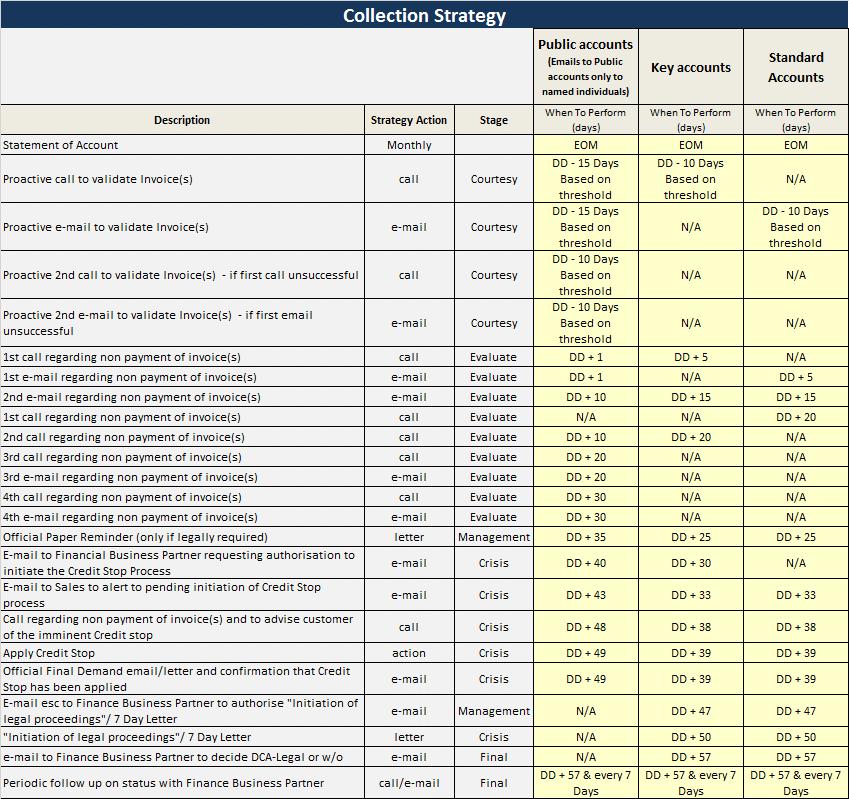

4 Collection priorities are established based upon customer segment, exposure and aging. Collection responsibility is defined with appropriate performance measurements tied to department and geographic goals. Effective collection practices include the following: 2.3 Customer Segmentation for Collections In order to ensure the Collections process is efficient and effective, the customers will be broken down in different customer segments. For each customer segment, a separate Reminder strategy will be defined. Customer segments allow the collectors to focus on high value accounts, whilst the reminder process of lower value accounts is more automated. These accounts will be contacted by collectors when these accounts move to later past due stages. For Collection purposes, the same customer segments as in Credit are recognized: (Table below is a sample. Amend to reflect the needs of the organization) Public Accounts Key accounts Standard accounts The customer segments are based on their value along with risk category. The customer segments should be reviewed on a quarterly basis. and adjusted according to the market, economic and customer behaviour. It is the responsibility of O2C [Credit manager] to ensure that Collection treatment strategies are kept up to date and, those customers are assigned to the right customer segment All customer contacts will always have to be conducted in a professional manner in accordance with local customs and practices. However, the guidelines included in this policy document are not intended to stop the collectors from agreeing specific steps with the customer with regard to the payment of overdue invoices. 2.4 Collection strategy For each customer segment, a specific collection strategy has been developed. It is important that all parts of the organization adhere to the agreed steps and timelines in the strategies to ensure that the way approaches its customers is uniform across countries. The strategies and timing of the steps are detailed in the table below. The timing of steps can be adjusted to accommodate the requirements and standard practices in different countries. Any country specific amendment to the standard strategy needs to be approved by the country Finance Manager. 4

5 5

6 The steps in the strategy are complemented by the actions the collectors deem necessary to respond to the specific circumstances of a customer. These actions can include ad hoc s, additional telephone calls or responding to specific customer requests. If a customer cannot be reached, the collector is expected to call back two times before leaving leave a message. If no response is received, follow up e mails should be sent two days after the initial attempt to make a phone call and the collector should verify the correctness of the customer contact data. If all attempts to contact the customer fail, the account should be escalated to the Customer Service organization with recommendations with regards to the desired follow up actions. 2.5 Reminder stop A Reminder stop i.e. the initiation of a stop to prevent the customers receiving automatic chase letters, needs to be in accordance with agreed collection procedures or approved by O2C [Credit manager] A disputed invoice will be blocked for dunning. Upon resolution of the dispute, the dunning process will be resumed. 2.6 Debt Recovery If amounts remain overdue due to the debtor s financial inability (insolvency, receivership, voluntary wind up) to pay or his unwillingness to pay (refusal to resolve queries) the account should be placed into Collection Agency, internal or. Collection Agency will take all steps to recover monies due. This will include the involvement of court action if necessary. Co-operation with external collection agencies requires a documented contract, a treatment plan and adequate processes to ensure appropriate information. If Recovery is successful without legal action the account will be passed back to the normal ledger but the credit limit will be set to -0- (zero). If legal action is taken the account will usually be closed, except in special cases when controls or guarantees will be put in place. If all steps are unsuccessful the amount due may need to be written off to Bad Debts. 2.7 Payment plans In exceptional cases where a customer is unable to pay his obligations within the agreed timeframe, a payment plan may be agreed. The Collector will discuss with the customers the options. The collector will present to the O2C [Credit manager] a payment plan proposal. O2C [Credit manager] will review the proposal and, if he agrees, forward the proposal to the Finance Manager for approval. Upon receipt of the approval, the collector will send the confirmation of the agreed payment plan to the Customer. If the customer fails to adhere to the payment conditions of the payment plan, the collection strategy will immediately accelerate to the Credit Stop stage. 6

7 2.8 Legal Proceedings In case of insolvency, the Customer case must be referred to the Finance Manager. In case of fraud, the Finance Manager, the Legal department and the Sales Department have to be informed immediately by telephone call, with an follow up. Bad debt provisions and bad debt write-offs are to be made in full alignment with the corporate standards 2.9 Doubtful & Uncollectible accounts buckets In the case of tangible external information indicating a probable risk of nonrecovery, the balance of such accounts should be reclassified to a separate doubtful bucket). Examples for such cases are: Financial difficulties Following negotiation Court rulings and receivership or administration Specific provision aligned with accounting instructions Consequently the doubtful accounts receivables must be provided for on a case by case basis, depending on the estimated risk of non-recovery being supported by external documentation. After initial reclassification and provisioning, these receivables must be reassessed periodically for any additional impairment, in order to reflect their current recovery value and adjust subsequently the related bad debt provision. When at any point of time, it is recognized that any cash recovery is more than unlikely (triggering event for impairment, i.e. in the case of legal proceedings or liquidation), these doubtful accounts must be fully provided for(100%) and disclosed as uncollectible A/R write-off align with accounting instructions Accounts receivables, for which external assessment or information is confirming any final non recovery of an outstanding balance due, must be written off and expensed to the income statement. This implies that the write-off expense is reflected in the income statement and not offset against the bad debt provision account in the balance sheet. However, in case of a specific bad debt provision already provided for, whether in full or partial, this provision should be reversed entirely to the income statement Income from cash collections on written off receivables Cash collection and recoveries of receivables written off in prior periods will be booked directly to the P&L as income specifically to the account Income from cash collection on written off receivables. 7

8 3.Credit Stop 3.1 Customer Credit Stop Process Customers who do not pay their outstanding receivables can be put on Credit Stop. Credit Stop means that that no new orders will be accepted Aged Debt Report Reviewed All customers who have undisputed invoices which remain unpaid 30 days or more after due date will be put on Credit Stop. Credit Stop is a process that has the potential to interrupt the business of the customer. As a consequence, the credit stop procedure needs to be strictly followed to avoid any potential liabilities. On a daily basis, the system or the collector creates a reports listing all customers for whom the Credit Stop Process needs to be initiated. For each customer segment, the Collection strategy sets the number of days after Due date when the Credit Stop needs to be applied Key accounts and partners As soon as the open invoices on the account of a customer in the customer segments Public and Key accounts reaches the Credit Stop stage, the system or the collections department will send an e mail to the Finance Manager to request authorization to initiate the Credit Stop process. The Finance Manager will return the decision to authorize or deny the Credit Stop Process within 2 business days. In case the Credit Stop has been approved, the collector will then attempt contact with the customer to advise them of the imminent Stop action. The telephone call will be followed up by an confirming the imminent credit stop. If the customer cannot be reached by telephone, a letter will be sent to advice the customer about the imminent Credit Stop. Should payment not be secured or a query identified this will be reflected in the comments as to why the debt has not been collected along with the Stop recommendation Other Accounts As soon as the open invoices on the account of a customer in the customer segments Other Commercial Account reaches the Credit Stop stage, the collections department will send an e mail to the customer advising the customer about the imminent credit stop. The collections department will then attempt contact with the customer to advise them of the imminent Stop action. Should payment not be secured or a query 8

9 identified this will be reflected in the comments as to why the debt has not been collected along with the Stop recommendation. 3.2 Stop Process After following the process described above, the Collections department will enter the Credit Stop into the system. Any new orders will be temporarily held whilst the Stop activity is ongoing- the account would show as delinquent. If the customer calls in whilst they are on STOP, all calls or enquiries should be referred to the O2C [Credit manager]. 3.3 Release The account would only be released if payment is made (cleared funds into our bank) or a valid query raised. If a customer can be release from Credit Stop, the Collections team send a request for release to the Finance Manager. The request will specify the details of the payment received or the details of the dispute and the name of the proposed dispute resolution owner. Only the Finance Manager can authorise the release of the account from Credit Stop. When an account is taken off Stop, an e mail advice will be sent to the same stakeholders who were sent an e mail advising the imminent credit stop. 4.Dispute Management 4.1Overview Customer disputes are an element of the business relationship. Typically, disputes can be categorized into claims and queries. Claims are directly related to the quality of services or related to Commercial agreements between us and the customer. Queries relate to commercial aspects. e.g.: billing issues (incorrect rate) other documentary issues. 4.2 Objectives of Dispute Management The objectives of dispute management are to resolve a customer dispute in the fastest and most efficient cycle time possible in order to sustain customer satisfaction, to remove barriers to payment and to improve quality standards. 4.3 Organization, Authorities, Escalation Organization Disputes are handled by the collections team. The manager [...] is responsible for the resolution decisions. If Collection Department Staff during the collection process identify that the customer wants to record a dispute, the dispute is registered into the finance system by the collector and, depending on the content of the query, forwarded 9

10 electronically to the relevant unit responsible for resolving the dispute. (Resolution owner) Disputed invoices will be put on reminder block. The collector will monitor the progress through the dispute lifecycle of each transaction in dispute. The table below documents the touch points in the process and the turnaround times for each action: Resolution and Authorization The resolution owner will investigate the query and, if needed, contact the customer for additional information, Once all information is available, the resolution owner will communicate to the Collections team the resolution decision. If the dispute is finalized with issuing a correction-invoice or credit note, approval for the issuance of a credit note will be given by the Finance Manager Escalations The collection team will send reminders to the resolution owners if disputes remain open beyond the agreed time frame. If following a reminder, a reply is not received, the collections team will escalate the dispute to the Finance Manager The person within organization responsible for the dispute resolution will respond within 7 working days. To check whether feedback concerning the dispute has been received from the relevant area, the collectors need to have the correct contacts and escalation from Sales and the different operational units Reminder Stop During the time that an invoice is disputed, the invoice will be excluded from the collection process. Upon resolution of the dispute, either by rejection of the dispute or by issuing a Credit Note to correct the original invoice, the status of the dispute will change to closed within Dispute Management. By changing the status of the dispute, the corrected invoice shall be unblocked for debt collection and the collections path restarted. 4.4 Sales Teams Collections will hold regular dialogue with Sales to co-ordinate actions and share responses on the > 90 days overdue debt. The BPO Manager will also flag the current top 5 Sales Issues on the fortnightly Sales Managers call and agree deadlines. 5. Reporting Reporting involves provision for timely and accurate information that meets the needs of management team within organization, with respect to the amount, age and content of receivables, while maintaining compliance with local and corporate accounting requirements. 10

11 Accounts receivable reporting consists of standard reports from several sources. These include: Credit management system ERP system External sources In order to ensure consistency and comparability of data, it is important that the same set of reports and calculation methodologies are applied across Regions or Countries. 11

CREDIT POLICY - SAMPLE -

CREDIT POLICY - SAMPLE - Contents 1 Scope 3 1.1 Objective 2 1.2 Organisation 2 1.3 Responsibility 3 1.4 Overview of the Credit and Collection responsibilities 3 2 Customer Master Data 3 2.1 Customer Setup

CREDIT POLICY - SAMPLE - Contents 1 Scope 3 1.1 Objective 2 1.2 Organisation 2 1.3 Responsibility 3 1.4 Overview of the Credit and Collection responsibilities 3 2 Customer Master Data 3 2.1 Customer Setup

SAP Receivables Management SAP Collections Management Webinar - Improve Receivables Performance with Advanced Collection Strategies

SAP Receivables Management SAP Collections Management Webinar - Improve Receivables Performance with Advanced Collection Strategies Webcast March 27, 2012 presented by SAP and HighRadius SAP Receivables

SAP Receivables Management SAP Collections Management Webinar - Improve Receivables Performance with Advanced Collection Strategies Webcast March 27, 2012 presented by SAP and HighRadius SAP Receivables

Efficient Credit & Collections Management: The Way to Optimize Your Working Capital. SAP Lounge, Brussels October 3-4, 2007

Efficient Credit & Collections Management: The Way to Optimize Your Working Capital Nathalie Nolf Consultant Crion Stefaan Ovaere Partner Intensum SAP Lounge, Brussels October 3-4, 2007 Optimizing Order-to-Cash

Efficient Credit & Collections Management: The Way to Optimize Your Working Capital Nathalie Nolf Consultant Crion Stefaan Ovaere Partner Intensum SAP Lounge, Brussels October 3-4, 2007 Optimizing Order-to-Cash

General Insurance Agency Management Framework THE BEST PRACTICES GUIDE

General Insurance Agency Management Framework THE BEST PRACTICES GUIDE 11 JULY 2005 BEST PRACTICES GUIDELINES FOR AGENCY MANAGEMENT 1. The Best Practices Guidelines for Agency Management ( the Best Practices

General Insurance Agency Management Framework THE BEST PRACTICES GUIDE 11 JULY 2005 BEST PRACTICES GUIDELINES FOR AGENCY MANAGEMENT 1. The Best Practices Guidelines for Agency Management ( the Best Practices

Group Credit Policy. Copyright Sandvik AB. Effective date: Date of last review:

Group Credit Policy Copyright Sandvik AB Title: Group Credit Policy Effective date: 24.09.2009 Date of last review: 27.11.2014 Document responsible: Per-Olof Duvhammar, Group Credit Controller Approved

Group Credit Policy Copyright Sandvik AB Title: Group Credit Policy Effective date: 24.09.2009 Date of last review: 27.11.2014 Document responsible: Per-Olof Duvhammar, Group Credit Controller Approved

ISEB Certificate in Modelling Business Processes

ISEB Certificate in Modelling Business Processes Sample Paper A You are allowed fifteen (15) minutes reading time before the examination starts. You are not allowed to write anything during that reading

ISEB Certificate in Modelling Business Processes Sample Paper A You are allowed fifteen (15) minutes reading time before the examination starts. You are not allowed to write anything during that reading

Office of Sponsored Programs Procedure Accounts Receivable Associated with Sponsored Awards Revision Date: 09/01/ Introduction. 2.

Office of Sponsored Programs Procedure 30002 Accounts Receivable Associated with Sponsored Awards Revision Date: 09/01/2016 TABLE OF CONTENTS 1. INTRODUCTION... 1 2. SCOPE... 1 3. PROCEDURE STATEMENT...

Office of Sponsored Programs Procedure 30002 Accounts Receivable Associated with Sponsored Awards Revision Date: 09/01/2016 TABLE OF CONTENTS 1. INTRODUCTION... 1 2. SCOPE... 1 3. PROCEDURE STATEMENT...

ISEB Certificate in Modelling Business Processes

ISEB Certificate in Modelling Business Processes Sample Paper A 1 Hour Examination You are allowed fifteen (15) minutes reading time before the examination starts. You are not allowed to write anything

ISEB Certificate in Modelling Business Processes Sample Paper A 1 Hour Examination You are allowed fifteen (15) minutes reading time before the examination starts. You are not allowed to write anything

The role requires working in accordance with the Company s Credit Policy and within existing procedures, in order to:

Position Description: GLOBAL ROLE PROFILE template Global Job Title: Credit Controller Job Reference Number: Job Family: Location: Reporting to: Credit Manager Grade: 3 Purpose of the role The Credit Controller

Position Description: GLOBAL ROLE PROFILE template Global Job Title: Credit Controller Job Reference Number: Job Family: Location: Reporting to: Credit Manager Grade: 3 Purpose of the role The Credit Controller

TERMS FOR THE APPOINTMENT OF CORRESPONDENTS OF FOREIGN INSURANCE UNDERTAKINGS FOR THE HANDLING OF MOTOR ACCIDENTS CLAIMS

TERMS FOR THE APPOINTMENT OF CORRESPONDENTS OF FOREIGN INSURANCE UNDERTAKINGS FOR THE HANDLING OF MOTOR ACCIDENTS CLAIMS In Article 4 of the Internal Regulations it is provided that each Bureau shall set

TERMS FOR THE APPOINTMENT OF CORRESPONDENTS OF FOREIGN INSURANCE UNDERTAKINGS FOR THE HANDLING OF MOTOR ACCIDENTS CLAIMS In Article 4 of the Internal Regulations it is provided that each Bureau shall set

2015 STAR Best Practices

2015 STAR Best Practices 2015 STAR Best Practices General Servicing Best Practices... 3 Investor Reporting and Accounting... 3 Optimizing personnel... 3 Quality and management oversight... 3 Reporting,

2015 STAR Best Practices 2015 STAR Best Practices General Servicing Best Practices... 3 Investor Reporting and Accounting... 3 Optimizing personnel... 3 Quality and management oversight... 3 Reporting,

Suffolk County Council. Debt Recovery Policy

Suffolk County Council Debt Recovery Policy 1. Framework 1.1 This policy document sets out the Debt Recovery Policy for Suffolk County Council to ensure that all sundry debts and income of the Authority

Suffolk County Council Debt Recovery Policy 1. Framework 1.1 This policy document sets out the Debt Recovery Policy for Suffolk County Council to ensure that all sundry debts and income of the Authority

Credit Control Policy. Document Control Authorised by: Distributed to: Version No. 1 Secretary General Head Office Staff & Head of Finance

Credit Control Policy Document Control Authorised by: Distributed to: Version No. 1 Secretary General Head Office Staff & Head of Finance January 2014 Contents Page No. 1. Purpose and Scope 1 1.1. 1.2.

Credit Control Policy Document Control Authorised by: Distributed to: Version No. 1 Secretary General Head Office Staff & Head of Finance January 2014 Contents Page No. 1. Purpose and Scope 1 1.1. 1.2.

Protect your Balance Sheet with Collections Scoring

Protect your Balance Sheet with Collections Scoring Maximizing Collections Results Credit & Collections Professionals are continually faced with the challenges of a changing business landscape, economic

Protect your Balance Sheet with Collections Scoring Maximizing Collections Results Credit & Collections Professionals are continually faced with the challenges of a changing business landscape, economic

Effective Credit Control Management

Effective Credit Control Management Do you have control of your cash flow? Take a look at these 10 effective steps to gain control of your cash flow, improve your credit control and management of bad debtors

Effective Credit Control Management Do you have control of your cash flow? Take a look at these 10 effective steps to gain control of your cash flow, improve your credit control and management of bad debtors

Debt Management Receivables Policy

Debt Management Receivables Policy Policy Code: FN1855 Table of Contents Purpose... 1 Scope... 1 Legislative Context... 1 Definitions... 1 Policy Statement... 2 Supporting Documents... 3 Implementation

Debt Management Receivables Policy Policy Code: FN1855 Table of Contents Purpose... 1 Scope... 1 Legislative Context... 1 Definitions... 1 Policy Statement... 2 Supporting Documents... 3 Implementation

The key objectives from the Corporate Debt Policy should be considered and the following key messages highlighted:

Write off Policy This write off policy is linked to Corporate Debt Policy The key objectives from the Corporate Debt Policy should be considered and the following key messages highlighted: 1. The preference

Write off Policy This write off policy is linked to Corporate Debt Policy The key objectives from the Corporate Debt Policy should be considered and the following key messages highlighted: 1. The preference

Office of the Ombudsman

Office of the Ombudsman 2013 Annual Report! A Message from the Ombudsman 2 - Ombudsman Mandate - 407 ETR s 3- step Dispute ResoluDon Process " The Ombudsman in AcDon..6-4 Types of Contact - Method and

Office of the Ombudsman 2013 Annual Report! A Message from the Ombudsman 2 - Ombudsman Mandate - 407 ETR s 3- step Dispute ResoluDon Process " The Ombudsman in AcDon..6-4 Types of Contact - Method and

Credit Reporting Policy

Credit Reporting Policy Tango Energy Pty Ltd Version 1.0 October 2017 Tango Energy Pty Ltd ABN 43 155 908 839 tangoenergy.com Table of Contents Credit Reporting Policy... 3 1. What credit information we

Credit Reporting Policy Tango Energy Pty Ltd Version 1.0 October 2017 Tango Energy Pty Ltd ABN 43 155 908 839 tangoenergy.com Table of Contents Credit Reporting Policy... 3 1. What credit information we

B2B DEBT COLLECTION BEST PRACTICES INTRODUCTION COLLECTION BEST PRACTICES. Presented by Michael C. Dennis, MBA, CBF, CCP, CPC

B2B DEBT COLLECTION BEST PRACTICES Presented by Michael C. Dennis, MBA, CBF, CCP, CPC 2019. Michael C. Dennis. All Rights Reserved 1 INTRODUCTION About 80% of people learn about B2B collection on the job

B2B DEBT COLLECTION BEST PRACTICES Presented by Michael C. Dennis, MBA, CBF, CCP, CPC 2019. Michael C. Dennis. All Rights Reserved 1 INTRODUCTION About 80% of people learn about B2B collection on the job

Factoring with Credit Protection Guide

Factoring with Credit Protection Guide Invoice Finance Why are we providing this guide? As part of our commitment to treating clients fairly we want to provide you with information which is clear and gives

Factoring with Credit Protection Guide Invoice Finance Why are we providing this guide? As part of our commitment to treating clients fairly we want to provide you with information which is clear and gives

STUDENT DEBT POLICY Contents

STUDENT DEBT POLICY Contents 1. INTRODUCTION AND CONTACT DETAILS... 2 2. INVOICES PAYMENT TERMS... 3 3. DEFINITION OF ACADEMIC AND NON-ACADEMIC DEBT TYPES... 3 4. TUITION FEES... 3 4.1. Tuition Fees collection

STUDENT DEBT POLICY Contents 1. INTRODUCTION AND CONTACT DETAILS... 2 2. INVOICES PAYMENT TERMS... 3 3. DEFINITION OF ACADEMIC AND NON-ACADEMIC DEBT TYPES... 3 4. TUITION FEES... 3 4.1. Tuition Fees collection

ROI Avenue Advertising Services General Terms and Conditions

ROI Avenue Advertising Services General Terms and Conditions 1. Parties The Company and the Agency as specified in Campaign Order. The above named shall hereinafter individually be referred to as a Party

ROI Avenue Advertising Services General Terms and Conditions 1. Parties The Company and the Agency as specified in Campaign Order. The above named shall hereinafter individually be referred to as a Party

Six Scenarios that Lead to Under Performing Receivables

Six Scenarios that Lead to Under Performing Receivables Practices, processes, and problems that are commonly seen in the credit and collection area that lead to high DSO, weak cash flow, and low resource

Six Scenarios that Lead to Under Performing Receivables Practices, processes, and problems that are commonly seen in the credit and collection area that lead to high DSO, weak cash flow, and low resource

PRE-IMPLEMENTATION GUIDE VERSION 1.0

PRE-IMPLEMENTATION GUIDE VERSION 1.0 FOR IMPLEMENTATION OF CREDIT MANAGEMENT Advanced Professional Solutions PAGE 1 OF 22 Created and Published by Advanced Professional Solutions Pty Ltd Level 7, 65 Berry

PRE-IMPLEMENTATION GUIDE VERSION 1.0 FOR IMPLEMENTATION OF CREDIT MANAGEMENT Advanced Professional Solutions PAGE 1 OF 22 Created and Published by Advanced Professional Solutions Pty Ltd Level 7, 65 Berry

Terms And Conditions Governing UK Property Loans

Oversea-Chinese Banking Corporation Limited 65 Chulia Street OCBC Centre Singapore 049513 Tel: +65 6363 3333 FAX: +65 6533 7955 www.ocbc.com Terms And Conditions Governing UK Property Loans 1. Definitions

Oversea-Chinese Banking Corporation Limited 65 Chulia Street OCBC Centre Singapore 049513 Tel: +65 6363 3333 FAX: +65 6533 7955 www.ocbc.com Terms And Conditions Governing UK Property Loans 1. Definitions

Collectors Work Queue

Collectors Work Queue Credit control is a vital process that establishes controls both pre and post sales to ensure a timely recovery of income owed to the University. Many factors need to be taken into

Collectors Work Queue Credit control is a vital process that establishes controls both pre and post sales to ensure a timely recovery of income owed to the University. Many factors need to be taken into

Credit Control Policy

Credit Control Policy This policy was adopted by the Board of Directors of Armagh Credit Union Limited. Signed:- ------------------------------------------ Position ------------------------------------------

Credit Control Policy This policy was adopted by the Board of Directors of Armagh Credit Union Limited. Signed:- ------------------------------------------ Position ------------------------------------------

Atradius Media Policy - Sample

Atradius Media Policy - Sample Domestic: Dedicated Protection for a Dynamic Sector This is a sample of our Media Policy wording only and is not a legally valid insurance policy. Agreement 00100.00 Agreement

Atradius Media Policy - Sample Domestic: Dedicated Protection for a Dynamic Sector This is a sample of our Media Policy wording only and is not a legally valid insurance policy. Agreement 00100.00 Agreement

OPERATIONAL PROCEDURES FOR APPROVED LISTING MARKET OPERATORS USING ASX SETTLEMENT SERVICES

OPERATIONAL PROCEDURES FOR APPROVED LISTING MARKET OPERATORS USING ASX SETTLEMENT SERVICES V5.0 11 July 2014 Table of Contents 1. Introduction... 5 2. Event Notification... 6 3. Contact and Assistance...

OPERATIONAL PROCEDURES FOR APPROVED LISTING MARKET OPERATORS USING ASX SETTLEMENT SERVICES V5.0 11 July 2014 Table of Contents 1. Introduction... 5 2. Event Notification... 6 3. Contact and Assistance...

This Page Intentionally Left Blank

This Page Intentionally Left Blank SedonaOffice Page 2 of 21 Table of Contents Accounts Receivable Overview... 4 Aging Categories (Buckets) and Aging... 5 Aging Categories (Buckets)... 5 Aging Method...

This Page Intentionally Left Blank SedonaOffice Page 2 of 21 Table of Contents Accounts Receivable Overview... 4 Aging Categories (Buckets) and Aging... 5 Aging Categories (Buckets)... 5 Aging Method...

SECTION: VI Revenues EFFECTIVE DATE: July 1, SUB-SECTION: 3 - Accounts Receivable REVISION DATE: September 1, 2007

SUBJECT: Policy and Procedures PAGE: 1 of 6 ACCOUNTS RECEIVABLE RECORDING, BILLING AND COLLECTION, WRITE-OFF, AND REPORTING It is the responsibility of each State department, agency or institution of higher

SUBJECT: Policy and Procedures PAGE: 1 of 6 ACCOUNTS RECEIVABLE RECORDING, BILLING AND COLLECTION, WRITE-OFF, AND REPORTING It is the responsibility of each State department, agency or institution of higher

Terms and Conditions for Simple Business Overdrafts

Terms and Conditions for Simple Business Overdrafts Dated 19 April 2017 Terms and conditions These products are issued by the Commonwealth Bank of Australia ABN 48 123 123 124 AFSL 234945 Overdraft terms

Terms and Conditions for Simple Business Overdrafts Dated 19 April 2017 Terms and conditions These products are issued by the Commonwealth Bank of Australia ABN 48 123 123 124 AFSL 234945 Overdraft terms

UNIVERSITY OF WORCESTER

UNIVERSITY OF WORCESTER POLICY DEBT MANAGEMENT POLICY: STUDENTS Contact Officer Account Receivable Manager Purpose A detailed guide of the debt management process for the University in relation to student

UNIVERSITY OF WORCESTER POLICY DEBT MANAGEMENT POLICY: STUDENTS Contact Officer Account Receivable Manager Purpose A detailed guide of the debt management process for the University in relation to student

Appendix L1. London Borough of Barnet. Debt Management Policy

Appendix L1 London Borough of Barnet Debt Management Policy 10 February 2017 1 Introduction and objectives The Council has a statutory and fiduciary responsibility to protect public funds for the benefit

Appendix L1 London Borough of Barnet Debt Management Policy 10 February 2017 1 Introduction and objectives The Council has a statutory and fiduciary responsibility to protect public funds for the benefit

COMING INTO EFFECT SEPTEMBER 17, 2018

COMING INTO EFFECT SEPTEMBER 17, 2018 Payments Canada is in the process of implementing a multi-year roadmap to modernize Canada s national payments clearing and settlement infrastructure, to better support

COMING INTO EFFECT SEPTEMBER 17, 2018 Payments Canada is in the process of implementing a multi-year roadmap to modernize Canada s national payments clearing and settlement infrastructure, to better support

REGULATIONS FOR THE PAYMENT OF UNIVERSITY FEES

REGULATIONS FOR THE PAYMENT OF UNIVERSITY FEES Document Title: Document Author: Responsible Person and Department: Approving Body: Regulations for the Payment of University Fees Carole Trantham Simon Day,

REGULATIONS FOR THE PAYMENT OF UNIVERSITY FEES Document Title: Document Author: Responsible Person and Department: Approving Body: Regulations for the Payment of University Fees Carole Trantham Simon Day,

AR324: Maintaining and Updating Receivables. Instructor Led Training

AR324: Maintaining and Updating Receivables Instructor Led Training Lesson 1: Understanding Receivables Maintenance Introduction Welcome Welcome to Cardinal Training! This training provides employees with

AR324: Maintaining and Updating Receivables Instructor Led Training Lesson 1: Understanding Receivables Maintenance Introduction Welcome Welcome to Cardinal Training! This training provides employees with

UPHL DEBTORS MANAGEMENT POLICY

2 nd Dec 2013 UPHL DEBTORS MANAGEMENT POLICY User UPHL DEBTORS MANAGEMENT POLICY TABLE OF CONTENTS PREAMBLE... 3 Review... 5 1.0 BACKGROUND.5 2.0 DEFINITIONS OF TERMS... 5 3.0 POLICIES AND PROCEDURES...

2 nd Dec 2013 UPHL DEBTORS MANAGEMENT POLICY User UPHL DEBTORS MANAGEMENT POLICY TABLE OF CONTENTS PREAMBLE... 3 Review... 5 1.0 BACKGROUND.5 2.0 DEFINITIONS OF TERMS... 5 3.0 POLICIES AND PROCEDURES...

CODES OF PRACTICE FOR THE TRINIDAD AND TOBAGO ELECTRICITY COMMISSION

CODES OF PRACTICE FOR THE TRINIDAD AND TOBAGO ELECTRICITY COMMISSION TABLE OF CONTENTS Page No. 1. INTRODUCTION 1 2. PROVISION OF PRIORITY SERVICES FOR THE ELDERLY, DISABLED AND CHRONICALLY SICK 4 2.1

CODES OF PRACTICE FOR THE TRINIDAD AND TOBAGO ELECTRICITY COMMISSION TABLE OF CONTENTS Page No. 1. INTRODUCTION 1 2. PROVISION OF PRIORITY SERVICES FOR THE ELDERLY, DISABLED AND CHRONICALLY SICK 4 2.1

Getting Delinquent Accounts to Pay Up. Presented by Larry Holmes

Getting Delinquent Accounts to Pay Up Presented by Larry Holmes Overview 1. Writing a good collection policy 2. Elements of a collection call 3. Handling the no money excuse 4. 5 techniques for collection

Getting Delinquent Accounts to Pay Up Presented by Larry Holmes Overview 1. Writing a good collection policy 2. Elements of a collection call 3. Handling the no money excuse 4. 5 techniques for collection

Research Councils Pension Scheme Administration Standards

Purpose of this document This document details the administration standards that JSS and employers adhere to. The document is owned and approved by the RCPS Management Board who; act as managers of the

Purpose of this document This document details the administration standards that JSS and employers adhere to. The document is owned and approved by the RCPS Management Board who; act as managers of the

National Hardship Policy

National Hardship Policy 1 BACKGROUND... 2 2 THE PRINCIPLES THAT UNDERLINE THIS POLICY... 3 3 DEFINITIONS... 3 4 INDICATORS OF FINANCIAL HARDSHIP... 3 5 OUR CUSTOMER VALUES... 4 6 OUR CUSTOMER CHARTER...

National Hardship Policy 1 BACKGROUND... 2 2 THE PRINCIPLES THAT UNDERLINE THIS POLICY... 3 3 DEFINITIONS... 3 4 INDICATORS OF FINANCIAL HARDSHIP... 3 5 OUR CUSTOMER VALUES... 4 6 OUR CUSTOMER CHARTER...

1706 OFFICIAL NOTICES 17 April 2009 WORKCOVER GUIDELINES FOR CLAIMING COMPENSATION BENEFITS

1706 OFFICIAL NOTICES 17 April 2009 WORKCOVER GUIDELINES FOR CLAIMING COMPENSATION BENEFITS Workers Compensation Act 1987 Workplace Injury Management and Workers Compensation Act 1998 Explanatory Note

1706 OFFICIAL NOTICES 17 April 2009 WORKCOVER GUIDELINES FOR CLAIMING COMPENSATION BENEFITS Workers Compensation Act 1987 Workplace Injury Management and Workers Compensation Act 1998 Explanatory Note

TO: ALL COUNTY PERSONNEL FROM: ROBERT WEISMAN COUNTY ADMINISTRATOR PREPARED BY: OFFICE OF FINANCIAL MANAGEMENT AND BUDGET (OFMB)

") TO: ALL COUNTY PERSONNEL FROM: ROBERT WEISMAN COUNTY ADMINISTRATOR PREPARED BY: OFFICE OF FINANCIAL MANAGEMENT AND BUDGET (OFMB) SUBJECT: RECEIVABLES COLLECTIONS AND WRITE-OFFS PPM#: CW-F-048 ISSUE DATE

TO: ALL COUNTY PERSONNEL FROM: ROBERT WEISMAN COUNTY ADMINISTRATOR PREPARED BY: OFFICE OF FINANCIAL MANAGEMENT AND BUDGET (OFMB) SUBJECT: RECEIVABLES COLLECTIONS AND WRITE-OFFS PPM#: CW-F-048 ISSUE DATE

Why is Credit Management important?

Why is Credit Management important? Cash flow is crucial for the survival and success of any business. It is generally accepted that cash flow is the single most pressing concern of most small and medium-sized

Why is Credit Management important? Cash flow is crucial for the survival and success of any business. It is generally accepted that cash flow is the single most pressing concern of most small and medium-sized

AMERICAN EXPRESS CHARGE CARDS TERMS & CONDITIONS

AMERICAN EXPRESS CHARGE CARDS TERMS & CONDITIONS American Express Charge Cards THE PARTIES TO THE AGREEMENT The parties to this Cardmember Agreement (the "Agreement") are AMEX (Middle East) B.S.C. (c)

AMERICAN EXPRESS CHARGE CARDS TERMS & CONDITIONS American Express Charge Cards THE PARTIES TO THE AGREEMENT The parties to this Cardmember Agreement (the "Agreement") are AMEX (Middle East) B.S.C. (c)

General Conditions of Lending Prevailing for contracts falling under the scope of Act No. V. of 2013

Commerzbank Zrt. General Conditions of Lending Prevailing for contracts falling under the scope of Act No. V. of 2013 PREAMBLE When granting a credit, Commerzbank Zrt s Business Regulations shall be amended

Commerzbank Zrt. General Conditions of Lending Prevailing for contracts falling under the scope of Act No. V. of 2013 PREAMBLE When granting a credit, Commerzbank Zrt s Business Regulations shall be amended

Working Capital Management Policy

Working Capital Management Policy Reference No: P_F_03 Version 1 Ratified by: LCHS Trust Board Date ratified: 11 September 2018 Name of originator / author: Kelvin Mucheke, Operational Finance Manager

Working Capital Management Policy Reference No: P_F_03 Version 1 Ratified by: LCHS Trust Board Date ratified: 11 September 2018 Name of originator / author: Kelvin Mucheke, Operational Finance Manager

Trade Credit Insurance Proposal form

Trade Credit Insurance Proposal form QBE Insurance (Australia) Limited ABN 78 003 191 035 AFSL 239 545 Please return the completed form to your broker or to qbetc.newbiz@qbe.com For assistance or information

Trade Credit Insurance Proposal form QBE Insurance (Australia) Limited ABN 78 003 191 035 AFSL 239 545 Please return the completed form to your broker or to qbetc.newbiz@qbe.com For assistance or information

INFORMATION ACT 1982

01 Nov REPORT - Debt Collection Report for Minister Responsible for Novopay The data in this report is provided by Talent2 and the Ministry of Education. It is extracted from the workflow tools on 1 November

01 Nov REPORT - Debt Collection Report for Minister Responsible for Novopay The data in this report is provided by Talent2 and the Ministry of Education. It is extracted from the workflow tools on 1 November

CUSTOMER RELATIONS POLICIES

CUSTOMER RELATIONS POLICIES Approved 11/25/15 CUSTOMER SERVICE GENERAL POLICIES TABLE OF CONTENTS 1. GENERAL POLICIES 3 1.1 Customer Defined 3 1.2 Deposits 4 1.3 Issuance of Bills 4 1.4 Estimated Bills

CUSTOMER RELATIONS POLICIES Approved 11/25/15 CUSTOMER SERVICE GENERAL POLICIES TABLE OF CONTENTS 1. GENERAL POLICIES 3 1.1 Customer Defined 3 1.2 Deposits 4 1.3 Issuance of Bills 4 1.4 Estimated Bills

Finance & Business Services Kindergarten Fee Collection Policy

Early Childhood Management Services 1.0 Finance & Business Services Kindergarten Fee Collection Policy Policy statement This policy will provide clear guidelines for: the collection of 3-year-old and 4-year-old

Early Childhood Management Services 1.0 Finance & Business Services Kindergarten Fee Collection Policy Policy statement This policy will provide clear guidelines for: the collection of 3-year-old and 4-year-old

University Hospitals Bristol NHS Foundation Trust

University Hospitals Bristol NHS Foundation Trust TREASURY MANAGEMENT POLICY [Approved by Trust Board July 2008] Original Policy: July 2008 Reviewed: July 2009 To Finance Committee: July 2009 To Trust

University Hospitals Bristol NHS Foundation Trust TREASURY MANAGEMENT POLICY [Approved by Trust Board July 2008] Original Policy: July 2008 Reviewed: July 2009 To Finance Committee: July 2009 To Trust

Water Supply Customer Contract Terms & Conditions. Table of Contents

Water Supply Customer Contract Terms & Conditions Table of Contents 1. What is a customer contract and who is covered by it? 1.1 What is a customer contract? 1.2 Customer categories covered by the contract?

Water Supply Customer Contract Terms & Conditions Table of Contents 1. What is a customer contract and who is covered by it? 1.1 What is a customer contract? 1.2 Customer categories covered by the contract?

Consumer Credit sourcebook. Chapter 8. Debt advice

Consumer Credit sourcebook Chapter Debt advice CONC : Debt advice Section.1 : Application.1 Application.1.1 This chapter applies, unless otherwise stated in or in relation to a rule to every firm with

Consumer Credit sourcebook Chapter Debt advice CONC : Debt advice Section.1 : Application.1 Application.1.1 This chapter applies, unless otherwise stated in or in relation to a rule to every firm with

Intelligent Debt Collection Techniques PROFESSIONAL DEBT COLLECTORS

Intelligent Debt Collection Techniques 2016 South African debt statistics 23.8 million South Africans are credit active consumers Outstanding consumer credit balances increased by 2.3% since last year

Intelligent Debt Collection Techniques 2016 South African debt statistics 23.8 million South Africans are credit active consumers Outstanding consumer credit balances increased by 2.3% since last year

Privacy. In this section: Privacy Notice. Important information relating to credit reporting

Privacy Your Coles Mastercard is issued by Wesfarmers Finance Pty Ltd and we are committed to ensuring the privacy and security of your personal information and your transactions. In this section: Privacy

Privacy Your Coles Mastercard is issued by Wesfarmers Finance Pty Ltd and we are committed to ensuring the privacy and security of your personal information and your transactions. In this section: Privacy

Collection of Student Debt Policy

Collection of Student Debt Policy AUGUST 2017 Contents 1. Introduction... 2 2. Policy... 2 3. Process... 3 4. Policy Review... 4 1 P a g e 1. Introduction The following debt collection policy will apply

Collection of Student Debt Policy AUGUST 2017 Contents 1. Introduction... 2 2. Policy... 2 3. Process... 3 4. Policy Review... 4 1 P a g e 1. Introduction The following debt collection policy will apply

ACG 2003 Annual Report Computer Systems in the Physician s Office Electronic Medical Records Return on Investment

The Business Case for the EMR ACG 2003 Annual Report Making the transition to an electronic medical record (EMR) is a major undertaking for any physician office. It not only involves an expenditure of

The Business Case for the EMR ACG 2003 Annual Report Making the transition to an electronic medical record (EMR) is a major undertaking for any physician office. It not only involves an expenditure of

6 HACKS FOR WHOLESALERS TO GET PAID FASTER. (Plus a bonus ROI calculator)

") 1 6 HACKS FOR WHOLESALERS TO GET PAID FASTER (Plus a bonus ROI calculator) 2 Contents 1. Late payments and the wholesale industry 3 2. Calculating the cost of unpaid invoices on your cash cycle 5 3. ezycollect

1 6 HACKS FOR WHOLESALERS TO GET PAID FASTER (Plus a bonus ROI calculator) 2 Contents 1. Late payments and the wholesale industry 3 2. Calculating the cost of unpaid invoices on your cash cycle 5 3. ezycollect

Atradius Modula Policy - Sample

Atradius Modula Policy - Sample A flexible and tailored approach to Credit Insurance This is a sample of our Modula Policy wording only and is not a legally valid insurance policy. Agreement 00100.00 Agreement

Atradius Modula Policy - Sample A flexible and tailored approach to Credit Insurance This is a sample of our Modula Policy wording only and is not a legally valid insurance policy. Agreement 00100.00 Agreement

INCOME MAXIMISATION & RENT ARREARS RECOVERY POLICY Document control Policy approval GDT November 2017 Updating

INCOME MAXIMISATION & RENT ARREARS RECOVERY POLICY 2017-2020 Document control Policy approval GDT November 2017 Updating Income Maximisation & Rent Arrears Recovery Policy 2016-2017 Next review date June

INCOME MAXIMISATION & RENT ARREARS RECOVERY POLICY 2017-2020 Document control Policy approval GDT November 2017 Updating Income Maximisation & Rent Arrears Recovery Policy 2016-2017 Next review date June

PAYROLL OVERPAYMENT RECOVERY POLICY

FOR DECISION PAYROLL OVERPAYMENT RECOVERY POLICY AGENDA ITEM 4.1 13 JULY 2010 Report of Paper prepared by Purpose of Paper Action/Decision required Link to Health Care Standards: Link to Health Board s

FOR DECISION PAYROLL OVERPAYMENT RECOVERY POLICY AGENDA ITEM 4.1 13 JULY 2010 Report of Paper prepared by Purpose of Paper Action/Decision required Link to Health Care Standards: Link to Health Board s

TERMS OF BUSINESS AGREEMENT INSURANCE MADE TO MEASURE

TERMS OF BUSINESS AGREEMENT INSURANCE MADE TO MEASURE This Agreement is between You the client or potential client You, Your and Lark (Group) Limited We, Us, Our, and applies to all work that We carry

TERMS OF BUSINESS AGREEMENT INSURANCE MADE TO MEASURE This Agreement is between You the client or potential client You, Your and Lark (Group) Limited We, Us, Our, and applies to all work that We carry

AUTHORIZATION AND PAYMENT

In this Choice Rewards World MasterCard Card ( Agreement and Disclosure Statement ) the words: I, me, my and mine mean any and all of those who apply for or use the First Technology Federal Credit Union

In this Choice Rewards World MasterCard Card ( Agreement and Disclosure Statement ) the words: I, me, my and mine mean any and all of those who apply for or use the First Technology Federal Credit Union

Conditions for supplying energy to small and medium enterprises (November 2016)

") Conditions for supplying energy to small and medium enterprises (November 2016) 1 Introduction 1.1 These conditions apply if we supply your business with energy and: you have entered into a verbal or written

Conditions for supplying energy to small and medium enterprises (November 2016) 1 Introduction 1.1 These conditions apply if we supply your business with energy and: you have entered into a verbal or written

TERMS OF BUSINESS 1. INTRODUCTION AND DEFINITIONS

TERMS OF BUSINESS Please read the following paragraphs carefully. These are our terms of business and explain the scope of our service to you. When you instruct us to act you are confirming that you agree

TERMS OF BUSINESS Please read the following paragraphs carefully. These are our terms of business and explain the scope of our service to you. When you instruct us to act you are confirming that you agree

Working Capital Management: An Enterprise Endeavor. Deborah McSheffrey, CTP

Working Capital Management: An Enterprise Endeavor Deborah McSheffrey, CTP Common working capital metrics Some common metrics include: Days Sales Outstanding (DSO) Days Payables Outstanding (DPO) Days

Working Capital Management: An Enterprise Endeavor Deborah McSheffrey, CTP Common working capital metrics Some common metrics include: Days Sales Outstanding (DSO) Days Payables Outstanding (DPO) Days

Terms and Conditions 1. Definition

Terms and Conditions 1. Definition 1.1 We, The Company, Our and Us means Guardian Recovery Limited whose registered office is 4 Tustin Court, Port Way, Preston, PR2 2YQ. Guardian Recovery Limited is registered

Terms and Conditions 1. Definition 1.1 We, The Company, Our and Us means Guardian Recovery Limited whose registered office is 4 Tustin Court, Port Way, Preston, PR2 2YQ. Guardian Recovery Limited is registered

Using SAP Collection Strategies & Correspondence Automation to Increase Collections Performance and Reduce DSO

SAP Receivables Management Seminar Using SAP Collection Strategies & Correspondence Automation to Increase Collections Performance and Reduce DSO Sashi Narahari CEO, HighRadius Feb 6, 2013 Dallas, Texas

SAP Receivables Management Seminar Using SAP Collection Strategies & Correspondence Automation to Increase Collections Performance and Reduce DSO Sashi Narahari CEO, HighRadius Feb 6, 2013 Dallas, Texas

Working Capital Management

Leitfaden für die nachhaltige Optimierung von Vorräten, Forderungen und Verbindlichkeitn Bearbeitet von Dr. Hendrik Vater, Elena Bail, Prof. Dr. Heinz-Jürgen Klepz, Internationaler Controller Verein 1.

Leitfaden für die nachhaltige Optimierung von Vorräten, Forderungen und Verbindlichkeitn Bearbeitet von Dr. Hendrik Vater, Elena Bail, Prof. Dr. Heinz-Jürgen Klepz, Internationaler Controller Verein 1.

HC 486 SesSIon October HM Revenue & Customs. Engaging with tax agents

Report by the Comptroller and Auditor General HC 486 SesSIon 2010 2011 13 October 2010 HM Revenue & Customs Engaging with tax agents Our vision is to help the nation spend wisely. We apply the unique perspective

Report by the Comptroller and Auditor General HC 486 SesSIon 2010 2011 13 October 2010 HM Revenue & Customs Engaging with tax agents Our vision is to help the nation spend wisely. We apply the unique perspective

Operational Procedures for Approved Market Operators

Operational Procedures for Approved Market Operators V12.0 JULY 2017 Table of Contents 1. Introduction... 6 1.1 Notification of changes to these procedures... 8 2. Event Notification... 8 3. Contact and

Operational Procedures for Approved Market Operators V12.0 JULY 2017 Table of Contents 1. Introduction... 6 1.1 Notification of changes to these procedures... 8 2. Event Notification... 8 3. Contact and

Terms and Conditions. Indian Rupee Travel Card

Terms and Conditions Indian Rupee Travel Card TERMS AND CONDITIONS FOR ICICI BANK INDIAN RUPEE TRAVEL CARD The following terms and conditions ( Terms and Conditions ) apply to the ICICI Bank Travel Card

Terms and Conditions Indian Rupee Travel Card TERMS AND CONDITIONS FOR ICICI BANK INDIAN RUPEE TRAVEL CARD The following terms and conditions ( Terms and Conditions ) apply to the ICICI Bank Travel Card

DNE PLUMBING & HEATING TERMS AND CONDITIONS

BACKGROUND: DNE PLUMBING & HEATING TERMS AND CONDITIONS These Terms and Conditions are the standard terms which apply to the provision of plumbing or Heating services by DNE Plumbing & Heating ( the Trader

BACKGROUND: DNE PLUMBING & HEATING TERMS AND CONDITIONS These Terms and Conditions are the standard terms which apply to the provision of plumbing or Heating services by DNE Plumbing & Heating ( the Trader

5:30-9 LOCAL FINANCE BOARD - GOVERNMENT ELECTRONIC RECEIPT ACCEPTANCE

5:30-9 LOCAL FINANCE BOARD - GOVERNMENT ELECTRONIC RECEIPT ACCEPTANCE 5:30-9.1 Purpose and authority (a) This subchapter includes rules and guidance for local government units to utilize credit cards,

5:30-9 LOCAL FINANCE BOARD - GOVERNMENT ELECTRONIC RECEIPT ACCEPTANCE 5:30-9.1 Purpose and authority (a) This subchapter includes rules and guidance for local government units to utilize credit cards,

THE CITY OF GREATER SUDBURY POLICIES AND PROCEDURES

THE CITY OF GREATER SUDBURY POLICIES AND PROCEDURES DEPARTMENT: Finance SECTION: All Sections TITLE: Accounts Receivable and Collections APPROVED BY: DATE: CFO/Treasurer July 8, 2009; Revised April 29,

THE CITY OF GREATER SUDBURY POLICIES AND PROCEDURES DEPARTMENT: Finance SECTION: All Sections TITLE: Accounts Receivable and Collections APPROVED BY: DATE: CFO/Treasurer July 8, 2009; Revised April 29,

Disputing an assessment

IR776 June 2018 Disputing an assessment What to do if you dispute an assessment 2 DISPUTING AN ASSESSMENT Introduction While we make every effort to apply the tax laws fairly and correctly, there may be

IR776 June 2018 Disputing an assessment What to do if you dispute an assessment 2 DISPUTING AN ASSESSMENT Introduction While we make every effort to apply the tax laws fairly and correctly, there may be

Investor Key Information Understanding your investment

Key Information and Investor Terms Investor Key Information Understanding your investment You should read the following information and the Investor Terms (below) carefully before making your investment.

Key Information and Investor Terms Investor Key Information Understanding your investment You should read the following information and the Investor Terms (below) carefully before making your investment.

North American Support Policy Client Technical Support

North American Support Policy Client Technical Support This policy provides current guidance for Client interaction with Experian Data Quality ( EDQ ) North America Client Technical Support. This document

North American Support Policy Client Technical Support This policy provides current guidance for Client interaction with Experian Data Quality ( EDQ ) North America Client Technical Support. This document

Terms And Conditions Governing Mortgage Loans

Oversea-Chinese Banking Corporation Limited 65 Chulia Street OCBC Centre Singapore 049513 Tel: +65 6363 3333 FAX: +65 6533 7955 www.ocbc.com Terms And Conditions Governing Mortgage Loans 1. Definitions

Oversea-Chinese Banking Corporation Limited 65 Chulia Street OCBC Centre Singapore 049513 Tel: +65 6363 3333 FAX: +65 6533 7955 www.ocbc.com Terms And Conditions Governing Mortgage Loans 1. Definitions

Port Louis Automated Clearing House

Bank of Mauritius Port Louis Automated Clearing House Direct Debit Scheme Rules Bank of Mauritius 9 May 2017 Reviewed on 10 January 2019 Direct Debit Scheme Rules Table of Contents Table of Contents...

Bank of Mauritius Port Louis Automated Clearing House Direct Debit Scheme Rules Bank of Mauritius 9 May 2017 Reviewed on 10 January 2019 Direct Debit Scheme Rules Table of Contents Table of Contents...

Discussion Paper: Claims Handling. April 2017 The Insurance in Superannuation Working Group

Discussion Paper: Claims Handling April 2017 The Insurance in Superannuation Working Group CONTENTS ISWG Foreword... 1 Executive Summary... 2 Section A: Discussion... 3 A.1 The member experience at claim

Discussion Paper: Claims Handling April 2017 The Insurance in Superannuation Working Group CONTENTS ISWG Foreword... 1 Executive Summary... 2 Section A: Discussion... 3 A.1 The member experience at claim

Berger Primary School Charging Policy

Berger Primary School Charging Policy This policy has been compiled recognising the difficulties placed on school in balancing the social welfare of pupils with the responsibility of managing the School

Berger Primary School Charging Policy This policy has been compiled recognising the difficulties placed on school in balancing the social welfare of pupils with the responsibility of managing the School

MASTER AGREEMENT FOR FOREIGN EXCHANGE AND DERIVATIVE TRANSACTIONS

MASTER AGREEMENT FOR FOREIGN EXCHANGE AND DERIVATIVE TRANSACTIONS Legal & Compliance Level 12, 530 Collins Street Melbourne Victoria 3000 Telephone: (613) 9273 1780 Facsimile: (613) 9629 2536 Copyright

MASTER AGREEMENT FOR FOREIGN EXCHANGE AND DERIVATIVE TRANSACTIONS Legal & Compliance Level 12, 530 Collins Street Melbourne Victoria 3000 Telephone: (613) 9273 1780 Facsimile: (613) 9629 2536 Copyright

INSURANCE IN SUPERANNUATION VOLUNTARY CODE OF PRACTICE

INSURANCE IN SUPERANNUATION VOLUNTARY CODE OF PRACTICE What is the Insurance in Superannuation Voluntary Code of Practice? The Code is the superannuation industry s commitment to high standards when providing

INSURANCE IN SUPERANNUATION VOLUNTARY CODE OF PRACTICE What is the Insurance in Superannuation Voluntary Code of Practice? The Code is the superannuation industry s commitment to high standards when providing

Financial procedures manual

Contents Introduction... 2 Finance authorisation procedure... 2 Bank account procedure... 3 Petty cash procedure... 4 Use of business credit card procedure... 5 New supplier procedure... 6 New customer

Contents Introduction... 2 Finance authorisation procedure... 2 Bank account procedure... 3 Petty cash procedure... 4 Use of business credit card procedure... 5 New supplier procedure... 6 New customer

The Beyontec Suite. Everything you need. Right where you need it.

R The Beyontec Suite Everything you need. Right where you need it. www.beyontec.com Fully Developed The Beyontec Suite is a fully developed, highly configurable, real-time, multi-line administration system

R The Beyontec Suite Everything you need. Right where you need it. www.beyontec.com Fully Developed The Beyontec Suite is a fully developed, highly configurable, real-time, multi-line administration system

Corporate debt recovery. The ideal partner for your credit management needs

Corporate debt recovery The ideal partner for your credit management needs Established in 2001, Hilton-Baird Collection Services provides award-winning commercial debt recovery services to the UK s corporate

Corporate debt recovery The ideal partner for your credit management needs Established in 2001, Hilton-Baird Collection Services provides award-winning commercial debt recovery services to the UK s corporate

CUA Credit Cards. Conditions of Use and Credit Guide

CUA Credit Cards Conditions of Use and Credit Guide Effective 8 August 2016 Note: This document does not contain all of the required precontractual information for your Agreement. You should also refer

CUA Credit Cards Conditions of Use and Credit Guide Effective 8 August 2016 Note: This document does not contain all of the required precontractual information for your Agreement. You should also refer

UNFCU Digital Banking Agreement

UNFCU Digital Banking Agreement Please read this Digital Banking Agreement (the Agreement ) carefully. This Agreement sets forth the terms and conditions that govern your use of UNFCU s Digital Banking

UNFCU Digital Banking Agreement Please read this Digital Banking Agreement (the Agreement ) carefully. This Agreement sets forth the terms and conditions that govern your use of UNFCU s Digital Banking

EQUAL ACCESS FUNDING PTY LTD PRIVACY POLICY

1. INTRODUCTION EQUAL ACCESS FUNDING PTY LTD PRIVACY POLICY This Policy applies to Equal Access Funding Pty Ltd ABN 23 156 554 255 (referred to as EAF, we, our, us ) and covers all of its operations and

1. INTRODUCTION EQUAL ACCESS FUNDING PTY LTD PRIVACY POLICY This Policy applies to Equal Access Funding Pty Ltd ABN 23 156 554 255 (referred to as EAF, we, our, us ) and covers all of its operations and

HC 486 SesSIon October HM Revenue & Customs. Engaging with tax agents

Report by the Comptroller and Auditor General HC 486 SesSIon 2010 2011 13 October 2010 HM Revenue & Customs Engaging with tax agents 4 Summary Engaging with tax agents Summary 1 Eight million taxpayers

Report by the Comptroller and Auditor General HC 486 SesSIon 2010 2011 13 October 2010 HM Revenue & Customs Engaging with tax agents 4 Summary Engaging with tax agents Summary 1 Eight million taxpayers

Next Business Energy Customer terms and conditions. Small customer market contract November 2017

Next Business Energy Customer terms and conditions Small customer market contract November 2017 0 1. Introduction 1.1 This is a market contract for small business customers and residential customers. 1.2

Next Business Energy Customer terms and conditions Small customer market contract November 2017 0 1. Introduction 1.1 This is a market contract for small business customers and residential customers. 1.2

Eurocard Corporate. Eurocard Purchasing Account. Terms and Conditions (Corporate) 1 General. 3 Payment instruments. 2 Definitions

1 General. 3 Payment instruments. 2 Definitions") Eurocard Corporate Eurocard Purchasing Account Terms and Conditions (Corporate) (1/2018) 1 General These terms and conditions apply to the account issued by SEB Kort to an account holder, to the card issued

Eurocard Corporate Eurocard Purchasing Account Terms and Conditions (Corporate) (1/2018) 1 General These terms and conditions apply to the account issued by SEB Kort to an account holder, to the card issued

NAB Personal Project Loan Terms and Conditions Including: Information Statement

NAB Personal Project Loan Terms and Conditions Including: Information Statement Effective 01 August 2008 Lost/stolen card reporting In Australia Call toll free, 24 hours per day 1800 033 103 Overseas Call

NAB Personal Project Loan Terms and Conditions Including: Information Statement Effective 01 August 2008 Lost/stolen card reporting In Australia Call toll free, 24 hours per day 1800 033 103 Overseas Call

Written Statement of Services (Revised 2017 Edition)

") Written Statement of Services (Revised 2017 Edition) In accordance with the Property Factors (Scotland) Act 2011, this statement sets the Terms and Service Delivery Standards of the arrangement between

Written Statement of Services (Revised 2017 Edition) In accordance with the Property Factors (Scotland) Act 2011, this statement sets the Terms and Service Delivery Standards of the arrangement between

Upgrading to Receivables R12?

Upgrading to Receivables R12? Angela Chin Senior Functional Consultant, HP Consulting 2006 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice

Upgrading to Receivables R12? Angela Chin Senior Functional Consultant, HP Consulting 2006 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice

CUA Credit Cards Conditions of Use and Credit Guide

CUA Credit Cards Conditions of Use and Credit Guide Effective 1 January 2019 Note: This document does not contain all of the required precontractual information for your Agreement. You should also refer

CUA Credit Cards Conditions of Use and Credit Guide Effective 1 January 2019 Note: This document does not contain all of the required precontractual information for your Agreement. You should also refer